RELAXO: Building India's Footwear Empire from ₹10,000

I. Introduction & Opening Hook

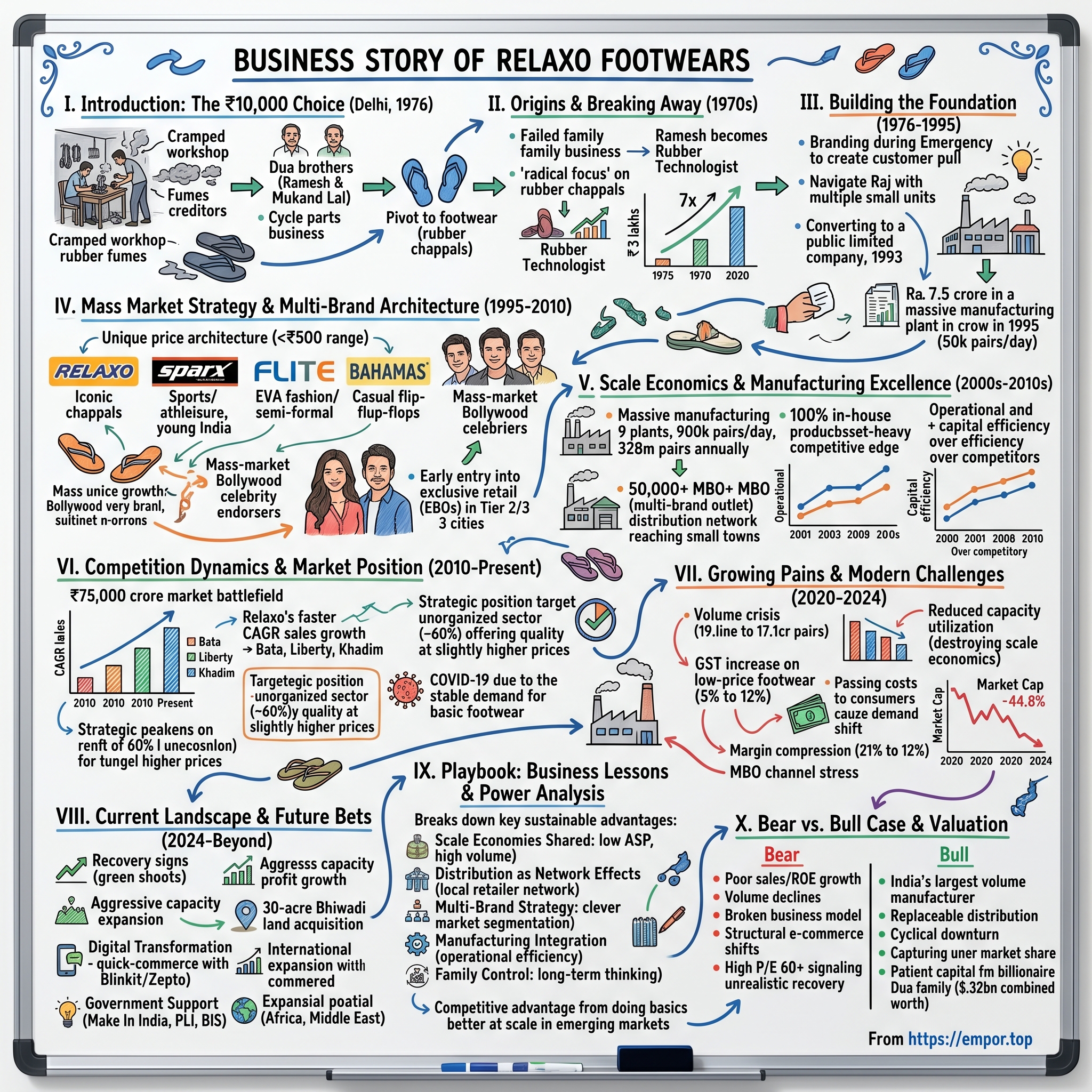

Picture this: Delhi, 1976. Two brothers stand in a cramped workshop, rubber fumes thick in the air, creditors at the door, and a failing cycle parts business bleeding cash. They have exactly ₹10,000—a deposit from a property deal—and a choice: continue the slow death of their inherited business or pivot to something radically different. Ramesh Kumar Dua and Mukand Lal Dua chose footwear. Not leather boots or fancy shoes, but the humblest product imaginable: rubber chappals that would sell for less than a cup of tea.

Fast forward to 2024. That ₹10,000 investment has transformed into a ₹10,860 crore market cap empire. Relaxo Footwears manufactures 725,000 pairs of footwear every single day—enough to shoe the entire population of Bhutan in a week. With Forbes pegging the Dua brothers' combined net worth at $2.32 billion, they've built India's largest footwear manufacturer by volume and second-largest by revenue, commanding a distribution network of 50,500 stores that reaches into every corner of the subcontinent.

But here's the puzzle that should fascinate every student of business: How do you build a moat in rubber slippers? How does a company selling products at an average price of ₹146—less than $2—create sustainable competitive advantages against both multinational giants like Bata and the vast unorganized sector that controls 60% of India's footwear market? The story of Relaxo isn't about premium positioning or technological disruption. It's about understanding that in a country where millions still earn less than ₹500 per day, the ability to produce a functional slipper for under ₹100 isn't just business—it's a form of economic democracy. This episode explores how the Dua brothers built one of India's most remarkable manufacturing stories, why they stubbornly refused to follow competitors upmarket, and what happens when a company optimized for volume suddenly faces a world that wants value.

II. Origins: The Dua Brothers & Breaking Away (1970s)

The story begins not with triumph, but with failure. In 1971, Mukand Lal Dua and Ramesh Kumar Dua watched their father's business crumble. The family enterprise—a hodgepodge of cycle parts manufacturing and small-scale trading—was hemorrhaging money. Creditors circled like vultures. The brothers faced a stark choice: declare bankruptcy and start fresh, or somehow salvage what remained.

They chose a third option: radical focus.

"We were producing quality products, but what the staff in the store said resonated with me," Ramesh would later recall about a pivotal conversation with a retailer who bluntly told him their products were good but their business model was garbage. The message was clear: stop trying to be everything to everyone. By 1976, the decision was made. The company would stop manufacturing cycle parts entirely and focus solely on footwear. But not just any footwear—they would start with hawai chappals, the ubiquitous rubber slippers that every Indian household owned but no one thought to brand. The brothers discarded the cycle parts segment in 1976 and decided to concentrate solely on footwear.

What happened next would define Relaxo's entire trajectory. Ramesh Kumar Dua became a qualified Rubber Technologist (licentiate of LPRI, London), understanding that to compete in commodities, you needed technical excellence. He contacted rubber technologists who helped improve product quality, working on formulations that would make their chappals last longer in Indian conditions—monsoon floods, scorching summers, rough village roads.

The initial results were dismal. From an initial turnover of just ₹3 lakhs, the business was barely surviving. But by 1978, something clicked. The improved quality, combined with aggressive pricing and early advertising efforts, pushed revenues to over ₹20 lakhs—a nearly 7x growth in two years. The brothers had found their formula: make it better than the unbranded competition, price it just slightly higher to signal quality, but keep it affordable enough for the masses.

As a result of the 1971 separation, Dua's father had to take on the creditors of the family business, who owed the family Rs 1 lakh. But when he went to collect the money he realised they were unwilling to pay up, and he eventually had to write the money off. "So we started with a deficit of Rs 1 lakh," Dua explains. The family rented out a property at Rs 350 a month for which they took a deposit of Rs 10,000. It was this money that became the initial capital with which they started Relaxo.

Think about the audacity of this moment: starting with negative net worth, using a property deposit as seed capital, and choosing to compete in the most commoditized segment of footwear. It shouldn't have worked. But the Duas understood something profound about Indian consumption that Western MBAs often miss: in a country where the per capita income was less than $200 annually, the ability to deliver value at scale wasn't just a business model—it was a form of social infrastructure.

III. Building the Foundation: From Hawai Chappals to Brand Building (1976-1995)

The Emergency of 1975-1977 should have killed Relaxo. Indira Gandhi's authoritarian experiment meant midnight raids, arbitrary business shutdowns, and economic paralysis. But Ramesh Dua saw opportunity in crisis. The decision to set up a brand was taken during the Emergency as he believed that if he had a brand, retailers would not remove his products from stores overnight as they did with unbranded footwear. If customers asked for shoes by name, shopowners would have to keep stocks.

This insight—that branding creates switching costs even in commodities—would become Relaxo's first major strategic innovation. The name "Relaxo" itself was carefully chosen: easy to pronounce across India's linguistic diversity, suggesting comfort, and crucially, trademarkable.

But building a brand in footwear faced a unique Indian challenge: the License Raj. They set up several units under different names as the footwear sector was reserved, by the government, for small scale manufacturers. The government's small-scale reservation policy meant you couldn't build large factories. So the Duas did what countless Indian entrepreneurs did in that era: they hacked the system. Multiple units, different names, same management—a corporate structure designed not for tax optimization but for regulatory arbitrage.

Incorporated in 1984, Relaxo is the largest footwear manufacturer in India. The formal incorporation came eight years after they started operations—a testament to how informal India's business environment was. By 1993, they converted to a public limited company, signaling ambitions beyond the neighborhood chappal market.

The real transformation came in 1995. With liberalization finally opening up the Indian economy, Relaxo made its biggest bet yet: investing Rs 7.5 crore in a manufacturing plant that could produce 50,000 pairs per day. To put this in perspective, that's 18 million pairs annually from a single facility—more than the entire footwear consumption of many small countries.

This wasn't just about scale; it was about changing the economics of footwear manufacturing. At 50,000 pairs per day, fixed costs per unit dropped dramatically. Suddenly, Relaxo could offer branded products at prices that unbranded players couldn't match even with zero marketing costs. They had discovered what would become their core competitive advantage: scale economics shared with consumers.

IV. The Mass Market Strategy & Multi-Brand Architecture (1995-2010)

Every business school teaches segmentation, but Relaxo's approach was distinctly Indian. Rather than segmenting by income (which would have pushed them upmarket), they segmented by occasion and aspiration while keeping prices accessible to the masses.

Its most popular brands – Relaxo, Sparx, Flite & Bahamas – are each a leader in their space. Relaxo, an iconic brand synonymous with rubber slippers, is the most versatile footwear for all segments of society, while Flite is a popular range of fashionable and semi-formal slippers. Sparx reflects the attitude, style, dynamism, and spirit of young India, offering sports shoes, sandals & slippers. The colorful range of Bahamas casual flip-flops exudes the spirit of freedom, fun, and modernity of youth.

The genius wasn't in having multiple brands—it was in the price architecture. All brands operated in the sub-₹500 range, but each carried different psychological positioning. A construction worker might buy Relaxo for daily wear but Sparx for his son's school sports day. Same wallet, different mental accounts.

In 2004, Relaxo set up India's largest EVA (Ethylene Vinyl Acetate) slipper plant. EVA was lighter than rubber, more colorful, and critically, allowed for injection molding that could produce complex designs at high speed. The Flite brand, launched from this facility, would become their fashion play—still priced for masses but designed for aspiration.

Relaxo entered the sports and athleisure segment with its Sparx brand in FY05, and it now contributes about 38 per cent of revenue. The timing was perfect. India's youth population was exploding, cable TV was bringing global fashion to small towns, and suddenly every teenager wanted "sports shoes" even if they never played sports.

The celebrity endorsement strategy reflected this mass-premium positioning. Bollywood actors signed up to endorse the company's brands are Salman Khan, Akshay Kumar, Katrina Kaif and Sonakshi Sinha. These weren't arthouse cinema stars; they were mass-market heroes whose posters adorned truck stops and tea stalls across India.

By 2005, Relaxo ventured into exclusive retail, opening their own stores. But unlike Bata's high-street locations, Relaxo stores appeared in tier-2 and tier-3 cities where real estate was cheap and brand experience mattered more than address prestige.

V. Scale Economics & Manufacturing Excellence (2000s-2010s)

Here's where Relaxo's strategy becomes genuinely fascinating for students of competitive advantage. With eight manufacturing units, Relaxo has the capacity to produce over 7.25 lakh pairs of footwear every day! By the 2010s, they had expanded to nine state-of-the-art plants with a total capacity of 900,000 pairs daily.

Let's pause on that number: 900,000 pairs per day. That's 328 million pairs annually. To put this in perspective, that's roughly one pair for every American, or enough to shoe the entire population of Indonesia twice over.

But capacity alone doesn't create competitive advantage—utilization does. And here's where Relaxo's model shines. Relaxo Footwear is the only company among its peers to manufacture 100 per cent of its products in-house. While competitors like Bata increasingly moved to an asset-light model, outsourcing production, Relaxo doubled down on manufacturing.

Why? Because in the sub-₹500 price range, every rupee of margin matters. Outsourcing might reduce capital requirements, but it also means paying someone else's margin. When your average selling price is ₹146, you can't afford middlemen.

It has a pan-India distribution footprint and a network of more than 50,500 stores. The company operates 50,000 multi-brand outlets (MBOs), and 402 exclusive brand outlets (EBOs). This distribution network became Relaxo's second major moat. But unlike FMCG companies that built distribution through distributors, Relaxo went direct to retailers whenever possible.

The economics are compelling: A typical MBO (multi-brand outlet) in small-town India might stock 5-10 footwear brands. But Relaxo products, with their combination of brand recognition, quality, and price points, might account for 30-40% of sales. This gives Relaxo significant leverage in negotiations—they're not just another supplier; they're often the retailer's largest source of footwear revenue.

The operational metrics from this period are staggering. The firm has outperformed its competitors in terms of operational and capital efficiency as a result of strong internal manufacturing facilities, successful addition of higher value-added categories, and a solid distribution network. While competitors struggled with 15-20% capacity utilization during downturns, Relaxo maintained 70-80% utilization by flexing across product lines and price points.

VI. Competition Dynamics & Market Position (2010-Present)

The Indian footwear market is a ₹75,000 crore battlefield, and Relaxo's position in it tells us everything about competitive dynamics in emerging markets. Despite selling ~18 crore pairs, Relaxo's current market share is <10%. This seems paradoxical—how can India's largest footwear manufacturer by volume have less than 10% market share?

The answer lies in market structure. The consumer is highly price conscious, which is visible due to the presence of >60% share of unorganized players. The unorganized sector—small workshops, local manufacturers, roadside cobblers—still dominates. But this apparent weakness is actually Relaxo's opportunity.

Relaxo's sales have expanded remarkably faster than those of its competitors in terms of CAGR. The 3-year and 5-year sales CAGR growth of Relaxo Footwears was 6.7% and 6.6%, respectively. Meanwhile, CAGR sales growth was in the range of 1-3% for competitors Mirza International and Khadim India. Even in the past three years, Bata India, Liberty Shoes, and Sreeleather's sales growth had fallen to negative double digits.

The competitive dynamics reveal a fascinating pattern. Bata, with its premium positioning and high-street retail, operates in a different universe—higher margins but limited volume growth. Liberty and Khadim, regional players, lack the scale to compete on price. Metro Brands, the new entrant post-IPO, focuses on premium segments that Relaxo consciously avoids.

But the real competition isn't other brands—it's the unorganized sector. And here, Relaxo's strategy is surgical. They don't try to compete with the absolute bottom of the market (the ₹30-50 chappal segment). Instead, they position just above it, offering branded products at ₹80-150 that provide dramatically better quality and durability.

Relaxo Footwear, a leading Fortune 500 company in India, dominates the open footwear segment, holding over 50 per cent of the market share in organized retail. This dominance in "open footwear" (sandals, slippers, flip-flops) is strategic. Closed footwear requires fitting, reducing online sales potential and increasing return rates. Open footwear is more forgiving—a size 9 chappal fits anyone from size 8.5 to 9.5.

During COVID-19, this strategy paid off spectacularly. Even though Covid-19 restrictions severely impacted the sales of most footwear companies, Relaxo's sales declined by just 2.13%. While premium footwear collapsed as offices closed and social events disappeared, demand for basic footwear remained stable. People still needed chappals for home and essential outings.

VII. Growing Pains & Modern Challenges (2020-2024)

Success in business is often a prelude to crisis, and Relaxo's recent challenges prove this axiom. After riding high through COVID, the company hit multiple headwinds simultaneously.

The volume crisis hit first. In FY2021, Relaxo sold 19.1 crore pairs. By FY2023, this had declined to 17.1 crore pairs—a 10% volume decline even as the market was supposedly recovering. Capacity utilization crashed from 70-80% to 50-55%, destroying the scale economics that underpinned the entire business model.

What went wrong? The answer lies in a critical strategic miscalculation. In FY2022, the govt. increased the GST on footwear priced below ₹1,000 from 5% to 12%, which impacted demand. EBITDA margin decreased mainly due to steep increase in raw material prices and extra support provided to trade towards GST rate differential on inventory.

Faced with a 7% tax increase and raw material inflation (crude oil derivatives like EVA and PU), Relaxo made the classic mistake: they passed on the full cost to consumers. When the company raised its prices in FY2022 and FY2023, then its customers immediately shifted to other cheaper products and Relaxo Footwears Ltd was forced to cut prices.

The margin story is even more troubling. Operating profit margins, which had touched 21% in FY2021, crashed to 12% in FY2023. The company found itself in a vicious cycle: raise prices and lose volume to unorganized players, or maintain prices and watch margins evaporate.

Relaxo Footwears is highly dependent on its 50,000 MBOs or retailers. This MBO dependency became a critical weakness. Small retailers, already stressed by COVID and e-commerce competition, couldn't finance inventory. The traditional Indian retail credit system—where brands give 60-90 day credit to retailers—started breaking down.

The stock market's reaction was brutal. Market Cap: 10,779 Crore (down -44.8% in 1 year). From peaks above ₹1,400, the stock crashed to under ₹500, destroying nearly half of shareholder value. The market was pricing in a fundamental break in the business model.

VIII. The Current Landscape & Future Bets (2024-Beyond)

But reports of Relaxo's demise appear premature. FY2024 brought green shoots of recovery. Operating income rose 4.7% year-on-year, operating profit jumped 20.9%, and net profit grew 29.8%. The company seems to have found its footing again, but the path forward requires fundamental strategic shifts.

In December 2023, Relaxo Footwears acquired a 30-acre land parcel in Bhiwadi, Rajasthan, for ₹135 crore. This aggressive capacity expansion seems counterintuitive given current utilization rates, but it signals management's confidence in long-term demand recovery.

The digital transformation is accelerating. Beyond traditional e-commerce, Relaxo is experimenting with quick-commerce platforms like Blinkit and Zepto. The economics are challenging—delivering a ₹150 chappal for a ₹30 delivery fee doesn't compute—but the company is betting on basket size expansion and platform subsidies.

The footwear industry is recognized by the Indian government as a priority sector under the Make In India mission. The Indian footwear industry expects to reach $27.84 billion by 2027, with the potential to grow 10-fold! Government support through PLI schemes and BIS standard implementation (which Relaxo already complies with) could accelerate organized sector growth.

The international expansion represents another vector. Targeting Africa and the Middle East makes strategic sense—similar price-conscious markets with large populations and underdeveloped organized retail. But success here requires more than just exporting products; it needs localized distribution and brand building.

IX. Playbook: Business Lessons & Power Analysis

After nearly five decades, what sustainable competitive advantages has Relaxo actually built? Let's apply the Seven Powers framework:

Scale Economies Shared: This is Relaxo's primary power. The average selling price (ASP) of its products is ₹146/-. At this price point, only massive scale makes the economics work. But unlike traditional scale economies that create producer surplus, Relaxo shares these benefits with consumers through lower prices, creating a virtuous cycle.

Distribution as Network Effects: With 50,000+ MBOs, Relaxo has achieved something remarkable—local network effects in physical retail. Each retailer that stocks Relaxo makes it easier for the next retailer to stock it (consumer demand is proven), and makes it harder for competitors to gain shelf space.

Multi-Brand Strategy: This isn't true counter-positioning, but it's clever market segmentation. By maintaining multiple brands at similar price points but different psychological positioning, Relaxo captures more wallet share without premium pricing.

Manufacturing Integration: The firm has outperformed its competitors in terms of operational and capital efficiency as a result of strong internal manufacturing facilities. Vertical integration usually doesn't create lasting advantage, but in commodity manufacturing at razor-thin margins, it can be the difference between profit and loss.

Family Control as Alignment: Promoter Holding: 71.3%. High promoter holding ensures long-term thinking but raises governance concerns. The Dua family's billion-dollar wealth is tied entirely to Relaxo, creating powerful alignment but also potential for minority shareholder exploitation.

The fundamental lesson from Relaxo is that in emerging markets, competitive advantage often comes not from differentiation but from doing the basics better at scale. It's not sexy, but it's effective.

X. Bear vs. Bull Case & Valuation

The Bear Case is compelling and grounded in current reality:

The company has delivered a poor sales growth of 2.96% over past five years. Company has a low return on equity of 9.11% over last 3 years. Volume declines, margin compression, and capacity under-utilization suggest a broken business model. The MBO channel stress could be structural, not cyclical, as e-commerce permanently changes retail dynamics.

The valuation metrics support the bears. At current prices, Relaxo trades at a P/E of 60+ despite single-digit growth and ROE. This suggests the market is pricing in a recovery that may never materialize.

The Bull Case rests on mean reversion and structural advantages:

Relaxo remains India's largest footwear manufacturer by volume with irreplaceable distribution. The current downturn is cyclical, driven by one-time GST changes and temporary inflation. As the unorganized sector struggles with BIS compliance and GST formalization, Relaxo stands to capture massive market share.

Forbes India listed Ramesh Kumar Dua as having a net worth of $1 billion as of 2023. The combined Dua family wealth of $2.32 billion represents patient capital that can weather short-term storms for long-term gains.

The truth, as always, likely lies between extremes. Relaxo faces real structural challenges—the rise of e-commerce, changing consumer preferences, and the limits of the low-price model. But it also possesses real structural advantages—scale, distribution, and brand recognition in a market where 60% remains unorganized.

XI. Epilogue: The Dua Legacy & What's Next

The journey from ₹10,000 to ₹10,000+ crore market cap represents more than financial success—it's a testament to the power of focus, frugality, and understanding your customer deeply. The Dua brothers didn't try to sell shoes to India's elite; they sold chappals to India's masses.

But every business model has its season, and Relaxo's fundamental question for the next decade is whether mass-market footwear can create durable competitive advantages in an increasingly digital, brand-conscious world.

The second-generation transition looms large. Unlike software or services businesses that can be professionally managed, manufacturing businesses often struggle with succession. Will the next generation maintain the cost discipline and operational focus that built Relaxo? Or will they chase premium segments and destroy what makes Relaxo special?

For investors and founders, Relaxo offers profound lessons: In emerging markets, serving the masses isn't just morally admirable—it can be enormously profitable. But it requires patient capital, operational excellence, and the humility to make unglamorous products that solve real problems.

The company that started with hawai chappals in a Delhi workshop now employs 18,000 people and touches millions of lives daily. That's the real legacy of Relaxo—proof that in business, as in life, you can build empires by keeping people's feet on the ground.

The fundamental question remains: In a world increasingly divided between premium and value, between digital and physical, between global and local, can a company built on ₹146 chappals continue to thrive? The next chapter of Relaxo's story will answer whether the Dua brothers built a business for their generation or for generations to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube