REDTAPE: India's Fashion Export Pioneer That Conquered the UK

I. Introduction & Episode Roadmap

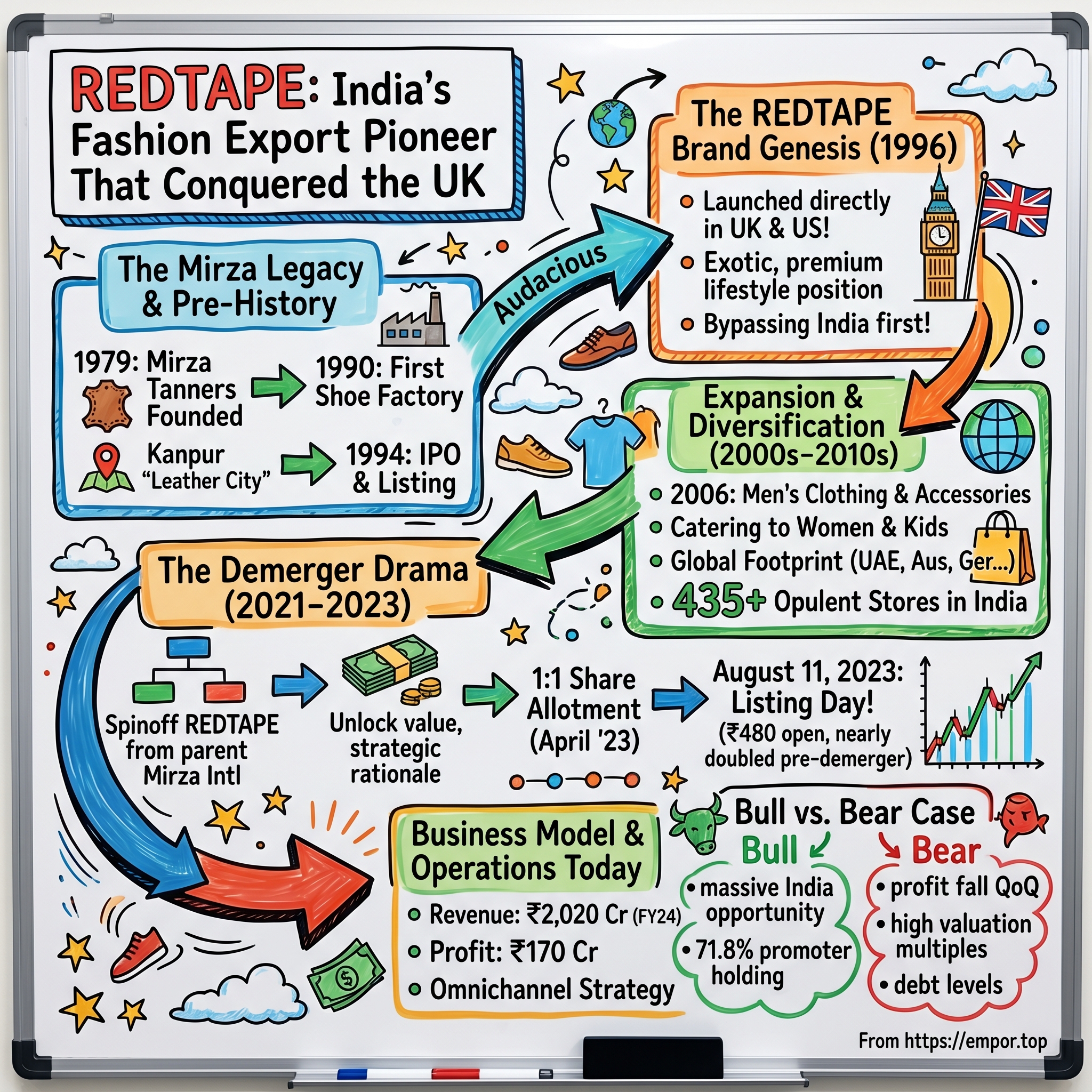

Picture this: It's August 11, 2023, and the Indian stock market witnesses something extraordinary. A fashion company that most domestic investors had never heard of as a standalone entity opens for trading at ₹480—nearly double its implied pre-demerger value. Within hours, REDTAPE Limited has created ₹3,000 crores of market value out of thin air. The kicker? This wasn't some tech unicorn or EV startup. This was a 27-year-old footwear brand that had quietly built an empire by doing something counterintuitive: conquering London's high streets before Mumbai's malls.

Today, REDTAPE commands a market capitalization north of ₹6,700 crores, with revenues touching ₹2,020 crores and profits of ₹170 crores. But the numbers only tell part of the story. This is a tale of how two brothers from Kanpur transformed their father's small tannery into one of India's first truly global fashion brands—a company that dared to launch in Selfridges before Shoppers Stop, that built credibility in Birmingham before Bangalore.

The question that drives this entire narrative: How did an Indian footwear brand, born in the leather clusters of Uttar Pradesh, become one of the first to crack the notoriously difficult UK market in 1996—at a time when "Made in India" meant cheap exports, not aspirational brands?

We'll journey through four distinct acts in REDTAPE's evolution. First, the Mirza family's three-generation transformation from leather traders to fashion moguls. Then, the audacious 1996 decision to launch REDTAPE directly in UK and US markets—bypassing India entirely. Next, the explosive growth phase where REDTAPE expanded from shoes to shirts, from London to Lagos, building a 435-store empire. Finally, the financial engineering masterpiece: the 2023 demerger that unlocked billions in shareholder value and set the stage for REDTAPE's next chapter.

This isn't just a business story—it's a playbook on building fashion brands in emerging markets, the power of backward integration, and why sometimes the best way to win at home is to prove yourself abroad first.

The Mirza Legacy & Pre-History

The monsoon winds of 1979 carried the scent of raw hides through the narrow lanes of Magarwara, on the outskirts of Kanpur. Here, in what was already known as India's "Leather City," two brothers—Irshad Mirza and Rashid Ahmed Mirza—stood before a modest tannery unit, surveying vats of chromium-tanned leather. They had just founded Mirza Tanners Private Limited, but their ambitions stretched far beyond the industrial clusters of Uttar Pradesh. In 1979, Mirza Tanners Private Ltd was founded by Mr. Irshad Mirza and Mr. Rashid Ahmed Mirza as a small tannery unit with a big vision for the leather industry.

This was Kanpur in its golden age of leather—a city that had reinvented itself after the collapse of its textile mills and the decline of the famous Lal Imli blankets following nationalization in the 1970s. It was leather that led the revival of Kanpur's manufacturing sector in the 1980s. The timing was perfect. The establishment of the Indian Leather Development Programme (ILDP) in the 1980s further propelled the industry by encouraging modern production techniques and enhancing export opportunities. The global appetite for leather goods was growing, and India, with 20% of world cattle & buffalo and 11% of world goat & sheep population, sat on an ocean of raw materials waiting to be transformed.

Irshad Mirza wasn't just another leather trader. An alumnus of Aligarh Muslim University, he brought an intellectual rigor to the rough-and-tumble world of tanneries. He was an alumnus of the Aligarh Muslim University and a former member of the University Court. His approach was methodical: understand the science of leather, master the craft, then scale. By the time the 1980s rolled around, Mirza Tanners had grown from processing raw hides into finished leather to dreaming of something bigger—manufacturing the end products themselves.

The watershed moment came in 1990. In 1990, Mirza inaugurated its first shoe manufacturing factory, taking the first step towards establishing a global footprint with premium quality leather. This wasn't just vertical integration; it was a statement of intent. While most Indian leather companies were content being suppliers to Western brands, the Mirza brothers wanted to be brand builders themselves.

Four years later, the company took another leap. In 1994, Mirza Tanners Private Limited was retitled Mirza Tanners Limited, and it became a deemed public company with a public issue of shares and a listing on the stock market. Going public wasn't just about raising capital—it was about institutionalizing ambition. The IPO proceeds funded modernization, expanded production capacity, and most importantly, gave them the war chest needed for what would become their most audacious move yet.

The accolades started rolling in by 1995, with the Council of Leather Exports recognizing their export excellence. By 1997, Irshad Mirza had earned the title "Doyen of Leather Industry"—a recognition that would culminate years later when He was awarded the fourth-highest Indian civilian award of Padma Shri by the Government of India in 2010, for his outstanding contribution in the field of trade and industry.

What set Mirza International apart in this era wasn't just scale—it was sophistication. The company is ISO 9001, 9002 and 14000 certified, and has a fully integrated in-house shoe production facility backed by a state-of-the-art double density direct injection polyurethane plant, a tannery with its own pollution treatment plant, and a dedicated design studio in London. That London design studio would prove prophetic.

The Indian leather industry of the 1990s was at an inflection point. The leather industry has undergone radical structural transformation from merely exporting raw materials in the 1960s to exporting value-added finished products from 1990s onward. In the 1990s, Kanpur's leather industry employed a million workers. The stage was set for ambitious players to make their mark—not as suppliers to global brands, but as brands themselves.

III. The REDTAPE Brand Genesis (1996)

In the leather boardrooms of Kanpur, conventional wisdom held that Indian brands should first dominate domestically, then venture abroad. The Mirza brothers had a different idea—one that would have seemed ludicrous to most Indian manufacturers of that era. They would launch their new brand, REDTAPE, directly in the United Kingdom and United States markets, bypassing India entirely.

It emerged as the first Indian footwear brand in 1996 to have a strong presence in global markets like UK. Think about the audacity of this move. Before the Indian economy opened up in the early 1990s, "imported" goods were a sought-after commodity, their foreignness often being their most desirable attribute. The perception of "Made in India" products internationally was problematic—associated with cheap exports rather than premium brands. Yet here was Mirza International, preparing to compete not in Mumbai's malls but on London's high streets.

The strategy was counterintuitive but brilliant. The in-house designers and the marketing team of Mirza International took upon this challenge and started working on growing the company's success to the new pivots. They introduced Redtape as a premium brand, representing the latest fashion in the UK. All the hard work paid off when the success of the flagship brand Redtape hit in 1996, UK.

Why go international first? The answer lay in a sophisticated understanding of brand perception. In India, any new footwear brand would have to compete with established players like Bata and Liberty, fighting for shelf space and consumer mindshare in a price-conscious market. But in the UK, REDTAPE could position itself differently—as an exotic, premium lifestyle brand with quality leather craftsmanship at competitive prices.

The story dates back to 1996 when it became one of the first Indian Footwear Brands to be available in the leading Global Markets such as the UK & US. It has a strong presence in the UK where it is sold through the Top-Chain Stores and Multi-Brand Outlets. In the US and Europe, where it has a growing presence, the brand is sold through multi-brand outlets.

The early product strategy was crucial. REDTAPE didn't try to undercut Western brands on price alone—that would have reinforced negative stereotypes about Indian manufacturing. Instead, they focused on premium positioning with genuine leather products, sophisticated designs from their London studio, and quality that could match European standards. The pricing was strategic: lower than luxury Italian brands but higher than mass-market offerings, positioning REDTAPE in the sweet spot of accessible premium.

This gave them a foothold in the international market and helped them grow to new levels. Breaking into UK chain stores wasn't easy. Each buyer meeting was a lesson in overcoming prejudice. "Indian leather? Yes, we know you can tan it. But can you design? Can you deliver consistent quality? Can you understand Western fashion trends?" The Mirza team answered each challenge methodically, leveraging their London design studio as proof of their fashion credentials.

The challenges of being an Indian brand in Western markets during the 1990s cannot be overstated. However, I didn't find the 'Made in India' tag as the selling point there. The perception is if an Indian brand is selling the same product, it wouldn't be of good quality. REDTAPE had to navigate this perception carefully. They emphasized their British design connections, their use of European-standard manufacturing processes, and their compliance with international quality certifications.

But the masterstroke was what happened next. After the successful establishment of the brands overseas, Redtape shifted the attention to its origin country, India. At times, the lack of a true-blue fashionable shoe brand gave this company the perfect launchpad. Having proven themselves in the demanding UK market, REDTAPE could now enter India with a powerful story: "The Indian brand that conquered Britain."

This reverse strategy—building brand credibility abroad to win at home—would become a template for other Indian brands to follow. It transformed REDTAPE from just another footwear manufacturer into a global lifestyle brand with an origin story that resonated with aspirational Indian consumers who wanted international quality with Indian pride.

IV. Expansion & Diversification (2000s–2010s)

The year 2006 marked REDTAPE's transformation from a footwear specialist to a complete lifestyle brand. Enthused by popularity of the brand, in 2006, we extended our brand to the Men's Clothing and Accessories category with our product offerings comprising of Casual and Semi-Formal Apparels including Shirts, T-Shirts, Trousers, Denim, Sweaters, Jackets, Ethnic Wear and Accessories such as Belts, Socks, Handkerchiefs and Wallets. This wasn't just product line extension—it was a calculated bet that REDTAPE's brand equity, built over a decade in footwear, could carry an entire wardrobe.

The decision to diversify came from observing customer behavior. Young professionals who bought REDTAPE shoes were looking for complete fashion solutions. Why should they trust an Italian brand for shirts when the Indian brand they loved for footwear could deliver the same quality and style? The move into apparel was particularly bold because it meant competing with established players like Arrow, Van Heusen, and Louis Philippe in the formal segment, while taking on Levi's and Pepe in casuals.

The product expansion strategy was methodical. Start with accessories that naturally complemented footwear—belts and wallets that matched the leather quality customers already trusted. Then move to apparel categories where fit and fabric mattered as much as fashion. Each new category launch was a test: Could REDTAPE maintain its premium positioning while expanding its price points to capture a broader market?

By the late 2000s, REDTAPE had evolved its target market strategy. Today, the brand also caters to the Fashion-Conscious Women and Kids with a wide array of products. This wasn't just about selling smaller shoes or pink shirts. It meant understanding entirely different consumer psychologies, shopping patterns, and fashion cycles. Women's fashion moved faster, kids' products needed durability over style, and both segments demanded different retail experiences.

The geographic expansion during this period was equally ambitious. Internationally, we sell in the markets of US, UK, UAE, Australia, Turkiye, France, Germany, West Asia and South Africa through our Extensive Global Distribution Channel. Each new market presented unique challenges. In the UAE, REDTAPE competed with luxury European brands in glitzy Dubai malls. In South Africa, they navigated complex import regulations and local manufacturing preferences. In Germany, they had to prove their quality standards matched local expectations.

But the real transformation was happening back home in India. India's trusted leading Fashion & Lifestyle brand with over 435+ opulent stores across PAN India. This wasn't organic growth—it was an explosion. From metro cities to tier-2 towns, REDTAPE stores became aspirational destinations. The retail strategy was nuanced: flagship stores in premium malls, smaller format stores in high streets, and shop-in-shops in multi-brand outlets.

The omnichannel approach emerged before the term became fashionable. Our Omni-Channel Retail Strategy, with a Strong Emphasis on Digital Infrastructure, is enabling us to consistently increase our domestic reach and deliver an engaging and seamless brand experience to consumers both in-store and online. While competitors struggled to integrate online and offline experiences, REDTAPE was building systems that let customers browse online, try in store, and buy through whichever channel they preferred.

The numbers told the story of successful diversification. By the end of the 2010s, REDTAPE wasn't just a footwear brand that sold some clothes—it had become a complete lifestyle destination. The brand had successfully navigated the treacherous waters of category expansion where many others had failed, maintaining its premium positioning while dramatically expanding its addressable market.

V. The Demerger Drama: Mirza International's REDTAPE Spinoff (2021-2023)

December 10, 2021: The boardroom at Mirza International's Delhi headquarters buzzed with tension as directors voted to split the crown jewel REDTAPE business from its parent company after 42 years. This wasn't just corporate restructuring—it was financial surgery on a living, breathing business empire.

The numbers made the case compelling. The demerged business has reported Turnover of INR 6.78 billion and net worth of INR 2.48 billion. RedTape had accounted for over 55 per cent of all sales and over half the profits of the entity pre-demerger. In essence, REDTAPE had grown so large within Mirza International that it was suffocating under the parent company structure, unable to access capital markets independently or pursue its own strategic initiatives.

The scheme was complex—a composite arrangement that would simultaneously merge RTS Fashions (a promoter group entity) into Mirza International while spinning off REDTAPE into a separate listed entity. The company on 27 February 2023 received approval from the National Company Law Tribunal (NCLT) for the composite scheme of arrangement between RTS Fashions, Mirza International, and Redtape.

The share exchange ratio was elegantly simple: Under the scheme of the arrangement, the board approved the allotment of 17.9 million (m) equity shares of the company, to RTS Fashions, in the share exchange ratio of 1:1. This means one equity share of Redtape, for every one equity share held in Mirza International to RTS Fashions. Every Mirza International shareholder would receive one REDTAPE share for each share they held—a clean split that preserved ownership proportions.

March 29, 2023, became the pivotal date. Shares of Mirza International traded ex-date for the merger of promoter group-owned entity RTS Fashions into the company and the demerger of its branded business into Redtape for the same on 29 March 2023. The market reaction was dramatic and immediate. A day before (on March 28), shares of Mirza International had settled at Rs 252.45, and on the record day, it opened lower at Rs 33.05 on the BSE and closed at Rs 34.70.

This wasn't a crash—it was the mathematical result of value being split between two entities. Investors who held Mirza International shares at ₹252.45 now held two separate assets: Mirza International shares trading around ₹35 and the promise of REDTAPE shares to be listed soon. The demerger had effectively unlocked value that was hidden within the conglomerate structure.

RedTape has approved the allotment of 13,82,01,900 shares of face value of Rs 2 each as fully paid up to the equity shareholders of Mirza International in a 1:1 exchange ratio. The shares were allotted to investors in April. The bureaucratic machinery moved with unusual speed—NCLT approval in February, effectiveness in March, share allotment in April.

Then came August 11, 2023—listing day. RedTape listed on the NSE at Rs 480 per share on Friday. The stock value nearly doubled at the relisting from pre-demerger price of Mirza International shares of Rs 252.45. For shareholders who had held on through the demerger, this was vindication. The combined value of their Mirza International and REDTAPE holdings now far exceeded what they had owned before the split.

The current market capitalisation of the company stands at Rs 6302 crore. Regarding ownership details, the promoter holds a significant 71.76% stake in the company, while the remaining 28.24% is owned by public investors, as stated by the company. The high promoter stake sent a signal: the Mirza family believed in REDTAPE's independent future.

Why demerge at all? The strategic rationale was multifaceted. First, it allowed each business to pursue its own capital allocation strategy. Mirza International could focus on its core leather manufacturing and export business, while REDTAPE could invest aggressively in brand building and retail expansion. Second, it provided transparency—investors could now value each business on its own merits rather than applying a conglomerate discount. Third, it created currency for acquisitions—REDTAPE shares could now be used for strategic deals in the fashion space.

The demerger also solved a talent problem. According to the scheme of arrangement, all the employees (including Managing Director and Whole-time Director) engaged in the REDTAPE Business of Mirza International Limited got transferred into REDTAPE Limited. This meant REDTAPE could now offer stock options in a pure-play fashion company, attracting retail and brand talent who might have been less interested in a diversified leather conglomerate.

The financial engineering had worked brilliantly. Since announcing the scheme of amalgamation, shares of the company have gained 267 percent till date. Value that was locked within a complex corporate structure had been released, creating billions in market capitalization seemingly out of thin air. The demerger would become a case study in how strategic corporate restructuring can unlock shareholder value—when done right.

VI. Business Model & Operations Today

REDTAPE stands as a formidable player in India's fashion landscape with a business model that seamlessly blends heritage craftsmanship with modern retail dynamics. Revenue: 2,020 Cr · Profit: 170 Cr, positioning the company among India's leading fashion brands with over 435+ opulent stores across PAN India.

The portfolio architecture reflects strategic brand positioning across price points and demographics. The company offers its products under the RedTape, RedTape Athleisure, MODE by RedTape, and BOND STREET by RedTape brands. Each sub-brand targets distinct consumer segments: RedTape for premium lifestyle, RedTape Athleisure for the sports-conscious, MODE for fashion-forward women, and BOND STREET for the value-conscious consumer seeking quality at accessible prices.

The product range has evolved far beyond the original leather shoes. It offers footwear, such as boots, sliders, casual and formal shoes, sandals, slippers, flip flops, classics range, and sports shoes; topwear, including jackets, shirts, sweaters, sweat shirts, hoodies, T-shirts, kurtas, top/tunics, and dress/jumpsuits; bottomwear, such as jeans, trousers, shorts, jeggings, pants, bottoms, trackpants, and joggers; and sports wear comprising active T-shirts, shorts, tights/leggings, and trackpants/joggers; as well as innerwear comprising briefs and trunks. This comprehensive portfolio transforms REDTAPE from a footwear specialist into a complete wardrobe solution.

Geographic diversification remains a cornerstone of the business model. Our Global Footprint spans across 17 Countries over 6 Continents. The brand has gained a strong foothold in the niche markets of India, UK, US, Australia, Turkiye, UAE, France, Germany, West Asia and South Africa and others. This international presence serves dual purposes: reducing dependence on any single market and maintaining the premium positioning that comes from being a global brand.

The omnichannel strategy has become increasingly sophisticated. It operates through retail stores and online channels. The digital infrastructure investments are paying off—REDTAPE Limited has commenced operations at its new Online Warehouse in Ludhiana, enhancing its e-commerce logistics and delivery infrastructure. The facility spans 47,700 square feet and aims to improve order fulfillment and service capabilities for online consumers across India.

Financial performance tells a story of rapid growth post-demerger. The revenues of REDTAPE stood at Rs 18,560 m in FY24, which was up 25.8% compared to Rs 14,750 m reported in FY23. REDTAPE's revenue has grown from Rs 3,035 m in FY22 to Rs 18,560 m in FY24. Over the past 3 years, the revenue of REDTAPE has grown at a CAGR of 147.3%. This explosive growth reflects both organic expansion and the clarity that comes from being a focused fashion business.

Profitability metrics reveal operational efficiency. REDTAPE LTD EBITDA is 3.43 B INR, and current EBITDA margin is 16.60%. While Net profit margins during the year declined from 9.7% in FY23 to 9.6% in FY24, the absolute profit numbers grew significantly: The net profit of REDTAPE stood at Rs 1,762 m in FY24, which was up 24.0% compared to Rs 1,422 m reported in FY23. Over the past 3 years, REDTAPE net profit has grown at a CAGR of 146.4%.

Recent quarterly performance shows some headwinds. Redtape's consolidated net profit fell 43.25% QoQ to Rs 41.47 crore in Q4 FY25, with net sales down 23.57%. Yearly net profit decreased 3.40%, while sales rose 9.28%. This volatility reflects the fashion industry's seasonal nature and the challenges of maintaining growth momentum after years of rapid expansion.

The capital structure remains conservative. Long-term debt down at Rs 249 million as compared to Rs 307 million during FY23, a fall of 18.9%, with Debt to Equity ratio for FY24 stood at 0.0 as compared to 0.1 in FY23. This low leverage provides flexibility for future expansion without diluting equity or taking excessive financial risk.

Manufacturing and supply chain capabilities underpin the retail success. The backward integration from Mirza International's tannery operations provides cost advantages and quality control that pure-play fashion retailers lack. Combined with design studios and a network of contract manufacturers, REDTAPE can respond quickly to fashion trends while maintaining margin discipline.

The competitive positioning is unique: premium enough to command respect, accessible enough to drive volume. In a market where international brands struggle with pricing and local brands struggle with aspiration, REDTAPE has found the sweet spot—international quality at Indian prices, with the brand story to match.

Market Performance & Stock Analysis

The stock market has delivered a harsh verdict on REDTAPE's post-demerger journey. Mkt Cap: 6,681 Crore (down -29.6% in 1 year), telling a story of investor skepticism despite strong operational metrics. The current valuation presents a fascinating paradox: a profitable, growing company trading at levels that suggest the market doesn't quite believe the story.

Let's start with the headline numbers that make investors wince. The P/E ratio of Redtape Ltd is 42.85 times as on 29-Jul-2025, a 165% premium to its peers' median range of 16.17 times. The P/B ratio of Redtape Ltd is 9.25 times as on 29-Jul-2025, a 285% premium to its peers' median range of 2.40 times. These are not valuations for the faint-hearted—they scream either overvaluation or exceptional growth expectations.

The stock's journey since listing has been a rollercoaster. REDTAPE reached its all-time high on Oct 31, 2024 with the price of 245.00 INR, and its all-time low was 102.76 INR and was reached on Sep 7, 2023. That's a peak-to-trough volatility that would make even seasoned traders nervous. The 52-week range tells a similar story of extreme sentiment swings.

Return on equity (ROE) is 23.69% and return on invested capital (ROIC) is 11.93%. These are respectable numbers—the ROE particularly suggests the company is generating strong returns for shareholders. But here's where it gets interesting: The intrinsic value of one REDTAPE stock under the Base Case scenario is 91.31 INR. Compared to the current market price of 127.69 INR, RedTape is Overvalued by 28%.

The dividend story adds another layer. REDTAPE LTD dividend yield was 1.54% in 2024, and payout ratio reached 73.05%. The year before the numbers were 0.00% and 0.00% correspondingly. This dramatic shift from no dividends to a high payout ratio suggests management is trying to reward shareholders and signal confidence, but the high payout ratio limits reinvestment capacity.

Promoter Holding: 71.8% remains a double-edged sword. On one hand, it signals skin in the game and alignment with minority shareholders. On the other, it limits free float and can exacerbate volatility—as we've seen with the stock's wild swings.

Recent trading patterns reveal investor nervousness. REDTAPE stock is 4.29% volatile and has beta coefficient of 0.42. The low beta is surprising given the stock's actual price movements, suggesting it doesn't correlate strongly with broader market moves—REDTAPE marches to its own drum.

The operational metrics tell a more positive story than the stock price. REDTAPE LTD EBITDA is 3.43 B INR, and current EBITDA margin is 16.60%. These are healthy margins for a fashion retailer, particularly one competing in India's value-conscious market. In the last 12 months, REDTAPE had revenue of INR 20.20 billion and earned 1.70 billion in profits. Earnings per share was 12.32.

But cash flow paints a concerning picture. In the last 12 months, operating cash flow was 139.60 million and capital expenditures -1.71 billion, giving a free cash flow of -1.57 billion. Negative free cash flow for a mature retail business raises questions about capital allocation and the sustainability of the dividend policy.

The debt situation has deteriorated post-demerger. The company has 145.70 million in cash and 7.24 billion in debt, giving a net cash position of -7.09 billion or -12.83 per share. This leverage, combined with negative free cash flow, explains some of the market's caution.

Analyst coverage remains sparse—REDTAPE Limited is covered by 0 analysts. 0 of those analysts submitted the estimates of revenue or earnings used as inputs to our report. The lack of institutional research coverage creates an information vacuum that often leads to higher volatility and potentially inefficient pricing.

The stock's recent performance has been particularly weak. Over the past 6 months, the Redtape share price has decreased by 22.94% and in the last one year, it has decreased by 28.24%. This underperformance comes despite reasonable operational performance, suggesting the market is pricing in concerns about future growth or margin sustainability.

What explains this disconnect between operational performance and stock valuation? Several factors are at play. First, the fashion industry's inherent cyclicality makes investors nervous about paying high multiples. Second, the recent quarterly volatility has shaken confidence. Third, the high promoter holding limits liquidity, potentially keeping institutional investors at bay. Finally, the lack of a clear moat in fashion retail—where trends change rapidly and barriers to entry are low—makes sustaining premium valuations challenging.

VIII. Playbook: Fashion Brand Building Lessons

The REDTAPE story offers a masterclass in building fashion brands in emerging markets—a playbook that challenges conventional wisdom at every turn. Here are the key lessons that emerge from their 28-year journey from Kanpur's tanneries to global runways.

Going Global to Build Local Credibility

REDTAPE's most counterintuitive move—launching in the UK before India—proved to be genius. In 1996, when Indian consumers still equated quality with foreign brands, REDTAPE flipped the script. By succeeding in London's competitive retail environment first, they earned the right to command premium prices in India. The lesson: sometimes the best way to win your home market is to prove yourself abroad first.

This strategy worked because it solved a trust deficit. Indian consumers in the 1990s had been conditioned to believe that local meant inferior. REDTAPE's UK success story became their calling card—"If it's good enough for London, it's good enough for Ludhiana." This approach requires patience and capital, but it builds a brand moat that pure domestic players struggle to replicate.

The Power of Backward Integration

Starting from a tannery base gave REDTAPE advantages that pure-play fashion brands could never match. Control over raw material quality, cost advantages from vertical integration, and the ability to respond quickly to market trends—all stemmed from this backward integration. When leather prices spiked or quality issues emerged, REDTAPE had direct control rather than being at the mercy of suppliers.

The integration went beyond just cost savings. It allowed REDTAPE to maintain consistent quality across massive production volumes, experiment with new materials and finishes, and crucially, tell a farm-to-fashion story that resonated with increasingly conscious consumers.

Family Business Governance and Professionalization

The Mirza family's approach to governance offers lessons in balancing family control with professional management. Maintaining 71.8% promoter holding post-demerger signals commitment, but they've also brought in professional managers, independent directors, and modern systems. The demerger itself was a masterstroke in governance—separating businesses to unlock value while maintaining family control.

The key was knowing when to let go and when to hold tight. Operations, technology, and retail were professionalized. But brand vision, capital allocation, and strategic direction remained firmly with the family. This hybrid model preserved entrepreneurial agility while building institutional capability.

Managing Multi-Brand, Multi-Category Complexity

REDTAPE's evolution from single-product (footwear) to multi-category (complete wardrobe) and from single-brand to portfolio (RedTape, Mode, Bond Street) required organizational gymnastics. Each sub-brand needed its own identity while leveraging common infrastructure. Each category demanded different design sensibilities, supply chains, and retail strategies.

The secret was in the sequencing. First, establish the core brand in the core category (REDTAPE footwear). Then extend into adjacent categories (accessories) that leverage existing capabilities. Only then venture into distinct categories (apparel) or segments (women's, kids'). This patient, methodical expansion reduced execution risk and preserved brand equity.

Timing Market Entry: First-Mover Advantages

Being among the first Indian footwear brands in international markets in 1996 gave REDTAPE disproportionate advantages. They faced less competition for shelf space, built relationships with retailers when barriers were lower, and established their brand before the market got crowded. The same principle applied to their domestic retail expansion—entering tier-2 cities before they became battlegrounds.

First-mover advantage in fashion is particularly valuable because it allows you to shape consumer preferences rather than fight for share in established categories. REDTAPE defined what affordable premium meant in many markets they entered.

The Demerger Playbook: When and How to Unlock Value

The 2021-2023 demerger offers a template for value creation through corporate restructuring. The timing was crucial—REDTAPE had reached sufficient scale to stand alone, capital markets were receptive to pure-play stories, and the conglomerate discount had become too large to ignore.

The execution was equally important. Clean share swap ratio (1:1), simultaneous merger of related party entity, clear business separation, and transparent communication. The result: nearly doubling of market value on listing day. The lesson: sometimes the best way to create value is to simplify the story.

Building Fashion Brands in Price-Conscious Markets

REDTAPE cracked the code on premiumization in value-conscious markets. The formula: international quality at local prices, with a story that justifies the premium. They understood that Indian consumers weren't cheap—they were value-conscious. Give them a reason to pay more (international validation, superior quality, aspirational positioning) and they would.

This required discipline in saying no—no to deep discounting, no to compromising quality for volumes, no to diluting the brand for short-term gains. It meant accepting slower growth initially but building a more valuable business long-term.

The Omnichannel Imperative

REDTAPE's early investment in omnichannel capabilities—before COVID made it mandatory—provided competitive advantage. But they understood omnichannel isn't just about being present everywhere; it's about creating seamless experiences across touchpoints. Browse online, try in store, buy on app, return anywhere—this flexibility became their differentiator.

The 47,700 square foot Ludhiana warehouse isn't just infrastructure—it's a statement of intent about serving the omnichannel consumer.

Managing Fashion Risk Through Portfolio Approach

Fashion is inherently risky—trends change, seasons disappoint, inventory becomes obsolete. REDTAPE's portfolio approach—multiple brands, categories, and price points—diversifies this risk. When formal shoes slow, sports shoes compensate. When men's fashion stutters, women's picks up. When domestic demand weakens, exports cushion.

This portfolio approach requires careful balance. Too much diversification dilutes focus and confuses consumers. Too little leaves you vulnerable to fashion cycles. REDTAPE found their sweet spot: focused enough to build expertise, diversified enough to manage risk.

The International Credibility Dividend

Even today, REDTAPE's international presence pays dividends beyond direct sales. It provides design inspiration, quality benchmarks, and brand credibility. It attracts talent who want global exposure. It provides natural hedge against currency fluctuations and market cycles. Most importantly, it keeps the organization hungry and humble—competing globally means you can never rest on your laurels.

IX. Bear vs. Bull Case

Bull Case: The Blueprint for a ₹25,000 Crore Company

The bulls see REDTAPE as India's best shot at creating a global fashion powerhouse. Start with the brand heritage— REDTAPE has a strong brand recall of 26+ yrs. In fashion, heritage matters. It provides authenticity that new-age D2C brands struggle to manufacture. This isn't a startup trying to find product-market fit; it's a proven winner with generations of customer loyalty.

The market opportunity is massive and growing. India's fashion market is expected to reach $200 billion by 2030, growing at 10-12% annually. REDTAPE's current ₹2,020 crore revenue represents less than 0.2% market share—the runway for growth is enormous. Add international expansion potential, and the addressable market multiplies.

Geographic diversification is already a reality. Our Global Footprint spans across 17 Countries over 6 Continents. The brand has gained a strong foothold in the niche markets of India, UK, US, Australia, Turkiye, UAE, France, Germany, West Asia and South Africa and others. This isn't aspiration—it's established presence that can be scaled.

The high promoter stake of 71.8% should be viewed positively. The Mirza family has skin in the game, aligned with minority shareholders. They've shown willingness to make bold moves (like the demerger) to unlock value. Their three-generation commitment to the business ensures long-term thinking over quarterly earnings management.

Category expansion has barely scratched the surface. From footwear to apparel to accessories, each category addition multiplies the wallet share opportunity. The women's and kids' segments are still nascent—imagine the growth when these mature. Plus, new categories like watches, perfumes, or even home furnishings become natural extensions.

Digital transformation provides another growth lever. REDTAPE Limited has commenced operations at its new Online Warehouse in Ludhiana, enhancing its e-commerce logistics and delivery infrastructure. The facility spans 47,700 square feet. This infrastructure investment positions them to capture the e-commerce boom without depending on marketplace aggregators.

The valuation, while optically high, is justified by growth potential. Fashion brands with strong moats trade at premium multiples globally. If REDTAPE can maintain 20%+ growth while expanding margins through operating leverage, today's valuations will look cheap in hindsight.

Bear Case: Fashion's Fickle Nature Meets Execution Challenges

The bears point to concerning recent trends. Redtape's consolidated net profit fell 43.25% QoQ to Rs 41.47 crore in Q4 FY25, with net sales down 23.57%. Yearly net profit decreased 3.40%, while sales rose 9.28%. This isn't just a bad quarter—it's a warning sign that growth is stalling and margins are under pressure.

Valuations have disconnected from fundamentals. Trading at P/E of 39.4x and P/B of 8.5x prices in perfection. Any disappointment—a fashion miss, inventory writedown, or margin compression—could trigger a significant correction. The stock's down nearly 30% from highs suggests the market is already losing faith.

Competition is intensifying from every direction. International brands like Zara and H&M are expanding aggressively in India. D2C brands are attacking from below with lower costs and social media savvy. Traditional players like Bata and Liberty aren't standing still. REDTAPE's moat—if it ever had one—is eroding.

Fashion industry cyclicality is unavoidable. Today's hot brand is tomorrow's clearance rack. REDTAPE has had a good run, but fashion brands rarely sustain premium positioning beyond a generation. Young consumers don't care about heritage—they want what's trending on Instagram.

The recent profit decline is particularly concerning given it occurred during what should be a growth phase post-demerger. Netprofit is down for the last 2 quarters, 73.07 Cr → 41.47 Cr (in ₹), with an average decrease of 43.3% per quarter. If they can't grow profits when they have tailwinds, what happens when headwinds emerge?

Execution risks multiply with expansion. Managing 435+ stores across India while expanding internationally, maintaining inventory across multiple categories, keeping designs fresh across brands—the complexity is staggering. One supply chain hiccup or inventory miscalculation could crater margins.

The high promoter holding that bulls love is actually a liquidity trap. Low free float means higher volatility, limited institutional interest, and potential for sharp moves on small volumes. When sentiment turns—and in fashion, it always does—the exit door will be narrow.

Debt levels post-demerger are concerning. The company has 145.70 million in cash and 7.24 billion in debt. For a fashion retailer facing margin pressure, this leverage limits flexibility. Rising interest rates could further pressure profitability.

The lack of analyst coverage is telling—REDTAPE Limited is covered by 0 analysts. Institutional investors are staying away, suggesting they see better opportunities elsewhere. Retail investors betting on the REDTAPE story might find themselves holding an illiquid, volatile stock with limited institutional support.

The Verdict: A Story Still Being Written

Both bulls and bears have merit. REDTAPE has built something remarkable—a truly Indian fashion brand with global presence and multi-generational appeal. The business fundamentals are solid, the brand is strong, and the market opportunity is vast.

But fashion is unforgiving. Today's leader is tomorrow's laggard. High valuations leave no room for error. Recent performance raises questions about execution capability.

The truth likely lies somewhere in between. REDTAPE will probably neither become India's LVMH nor collapse into irrelevance. It will more likely muddle through—growing steadily but not spectacularly, maintaining position but not dominating, creating value but not windfalls.

For investors, the key question isn't whether REDTAPE is a good company—it clearly is. The question is whether it's a good investment at current valuations. With the stock pricing in aggressive growth while operations show strain, the risk-reward seems tilted toward risk.

X. Future Outlook & Strategic Questions

The next five years will determine whether REDTAPE becomes India's first truly global fashion powerhouse or remains a successful but regional player. The strategic choices made today will echo for decades.

The E-commerce Transformation

The Ludhiana warehouse is just the beginning. REDTAPE must decide whether to build a direct-to-consumer powerhouse or remain dependent on multi-brand platforms. The D2C route offers higher margins and customer data but requires massive technology investment. The marketplace model provides reach but commoditizes the brand.

The smart move might be a hybrid—own the premium experience through D2C while using marketplaces for customer acquisition. But execution will be everything. Can a company rooted in physical retail master digital's different rhythms?

The International Expansion Dilemma

With presence in 17 countries, REDTAPE faces a classic challenge: go deep or go wide? Doubling down on existing markets like the UK and UAE could build meaningful scale. Or expanding into new markets like Southeast Asia could diversify risk.

The answer likely depends on brand strength. In markets where REDTAPE has heritage and recognition, depth makes sense. In new markets, testing with capital-light models (franchising, online-only) might be wiser. The key is avoiding the trap of spreading too thin—being everywhere but dominant nowhere.

The Premiumization Opportunity

India's premium fashion market is exploding as affluent consumers seek differentiation. Should REDTAPE launch an ultra-premium line to capture this opportunity? Or would that dilute the accessible premium positioning that built the brand?

History suggests brands that successfully premiumize create new brands rather than stretch existing ones. Perhaps it's time for REDTAPE to acquire or create a luxury brand, leveraging their infrastructure while protecting the core brand's positioning.

The Sustainability Imperative

Fashion's environmental impact is under scrutiny globally. REDTAPE's leather heritage could become either an asset or liability depending on how sustainability trends evolve. The company must decide whether to lead on sustainability or follow.

Leading requires investment—sustainable materials, transparent supply chains, circular economy initiatives. But it could differentiate REDTAPE in an increasingly conscious market. Following is cheaper but risks being left behind as sustainability becomes table stakes.

The M&A Question

With ₹6,700 crore market cap and established infrastructure, REDTAPE could be an acquirer or acquisition target. Acquiring struggling brands could provide instant scale. Being acquired by a global major could provide resources for international expansion.

The family's 71.8% stake suggests they're not selling soon. But strategic partnerships or minority investments could provide growth capital without diluting control. The question is whether the family's appetite for control will limit strategic options.

Digital-First Sub-Brands

The next generation shops differently. Should REDTAPE launch digital-native sub-brands targeting Gen Z? These could experiment with different models—drops, collaborations, NFTs—without risking the core brand.

The challenge is organizational. Can a company with traditional retail DNA build digital-first brands? The capability gap might be too large to bridge organically, suggesting acquisitions or partnerships might be necessary.

The Manufacturing Modernization

Industry 4.0 is transforming fashion manufacturing—3D printing, automated cutting, AI-driven demand planning. REDTAPE must decide how aggressively to modernize. Early adoption could provide competitive advantage but requires capital. Waiting risks falling behind.

The sweet spot might be selective modernization—automating where it drives clear ROI while maintaining craftsmanship where it differentiates. But identifying these areas requires deep understanding of where value is created.

Store Format Evolution

With 435+ stores, REDTAPE has significant fixed costs. Should they double down on physical retail or rationalize the store base? The answer isn't binary—it's about evolution.

Stores must become experience centers, not just transaction points. Smaller formats in high-traffic areas, flagship experience stores in key cities, pop-ups for testing new markets—the portfolio must become more dynamic. But this requires different capabilities than traditional retail expansion.

The Data Monetization Opportunity

REDTAPE has millions of customers but likely underutilizes their data. Building a data-driven understanding of fashion preferences, purchase patterns, and price sensitivity could transform merchandising, marketing, and design.

But becoming data-driven requires more than technology—it requires cultural change. Can an organization built on intuition and relationships embrace analytics and algorithms?

The Platform Play

Could REDTAPE become a platform for other brands? Their retail footprint, supply chain, and customer base are valuable assets that could be monetized beyond their own brands.

This would require a fundamental shift in mindset—from brand owner to platform operator. Few fashion companies have successfully made this transition. But those that have unlocked tremendous value.

Key Questions for Stakeholders

For investors: Is REDTAPE a growth story worth premium valuations, or a mature business that should return cash to shareholders?

For management: Will you prioritize growth or profitability, expansion or consolidation, control or scale?

For the board: How do you balance family legacy with shareholder value, tradition with transformation?

For employees: Can you build new capabilities while maintaining the culture that brought success?

For customers: Will REDTAPE remain relevant as your needs, values, and shopping behaviors evolve?

The answers to these questions will determine whether REDTAPE's next chapter surpasses its first. The foundation is solid, the brand is strong, and the opportunity is vast. But in fashion, past success guarantees nothing. The only certainty is change, and those who adapt fastest win.

Can REDTAPE become India's first global fashion powerhouse? The potential exists. The heritage provides credibility. The infrastructure enables scale. The market offers opportunity.

But potential must be converted through execution. Heritage must be balanced with innovation. Infrastructure must be modernized for digital. And opportunity must be seized before competitors do.

The next five years will tell whether REDTAPE writes a new chapter in Indian business history or becomes another reminder that in fashion, there are no permanent winners—only those who stay relevant a little longer.

XI. Recent News

The year 2025 has marked a significant transformation for REDTAPE, characterized by strategic corporate governance changes and robust dividend distributions that signal management's confidence despite market volatility.

Leadership Restructuring and Governance Updates

On August 14, 2025, REDTAPE's board announced the re-designation of Mr. Abhinav Jain from Chief Financial Officer to Vice President-Finance, a move that suggests organizational restructuring aimed at bringing in fresh financial leadership while retaining institutional knowledge in a strategic advisory capacity.

The company's commitment to governance transparency is evident in its recent regulatory filings. REDTAPE filed its Business Responsibility & Sustainability Report (BRSR) as part of the Annual Report for FY2024-25 on September 1, 2025, demonstrating increased focus on ESG compliance—a critical factor for institutional investors in the current market environment.

Dividend Policy and Capital Allocation

REDTAPE's dividend strategy has emerged as a key highlight. The company declared and approved an Interim Dividend of INR 2 (100%) per equity share for the financial year 2024-25, with January 3, 2025, fixed as the record date. This aggressive dividend policy, combined with the upcoming AGM on September 26, 2025, proposing a final dividend of Re.0.25 in addition to the interim Rs2, represents a total dividend of Rs 2.25 per share—a substantial payout that reflects management's confidence in cash generation capabilities.

Financial Performance Volatility

Recent quarterly results paint a mixed picture. Revenue for March '25 stood at ₹519.2 crore, declining 22.46% from December '24's ₹669.58 crore. EBITDA fell 28.8% to ₹95.24 crore, while net profit dropped 43.25% to ₹41.47 crore from ₹73.07 crore. This sharp sequential decline raises questions about seasonality impacts and operational challenges in maintaining growth momentum.

Stock Market Response

The market has responded cautiously to these developments. As of July 31, 2025, REDTAPE shares traded at Rs 129.70, down 1.37% from the previous close of Rs 131.50. More concerning is the longer-term trend: over the last 12 months, REDTAPE share price has declined 27.95% on BSE, reflecting investor concerns about growth sustainability and valuation multiples.

Infrastructure Investments Continue

Despite market headwinds, REDTAPE continues investing in growth infrastructure. The previously announced Ludhiana warehouse expansion represents a strategic bet on e-commerce growth, positioning the company to capture the digital commerce opportunity as consumer behavior continues shifting online.

Regulatory Compliance and Transparency

The company has transitioned to integrated filing for financial results from March 2025 onwards, aligning with new regulatory requirements and improving disclosure standards. This move toward greater transparency should help address the current gap in analyst coverage and potentially attract institutional interest.

XII. Links & Resources

Official Company Resources: - REDTAPE Investor Relations: about.redtape.com/investor-relation - Annual Reports & Financial Results: about.redtape.com/financial-results.php - Corporate Announcements: NSE India REDTAPE page - E-commerce Platform: redtape.com - Store Locator: redtape.com/pages/location

Stock Market Resources: - NSE Symbol: REDTAPE - BSE Code: 543957 - Live Price Tracking: NSE India, BSE India - Financial Analysis: Screener.in/company/REDTAPE - Market Data: Trendlyne, Ticker.finology.in

Industry Research: - Council of Leather Exports India - Indian Brand Equity Foundation (IBEF) - Leather Industry Reports - Euromonitor - India Fashion Retail Analysis - McKinsey India Fashion Report

Recommended Reading: - "The Luxury Strategy" by Jean-Noël Kapferer and Vincent Bastien - "Shoe Dog" by Phil Knight (Nike's founding story) - "The Everything Store" by Brad Stone (Amazon's retail revolution) - "Delivering Happiness" by Tony Hsieh (Zappos' customer-centric approach)

Relevant Business Podcasts: - Acquired.fm episodes on fashion brands (LVMH, Nike, Lululemon) - The Business of Fashion Podcast - How I Built This - Fashion brand episodes - Masters of Scale - Reid Hoffman's scaling strategies

Historical Context: - Mirza International's transformation journey (1979-2021) - India's economic liberalization impact on fashion retail (1991-2000) - The rise of Indian brands in international markets - Demerger case studies in Indian markets

Competitor Analysis: - Bata India Limited annual reports - Liberty Shoes investor presentations - Metro Brands Limited (listed 2021) - Campus Activewear IPO prospectus

Fashion Industry Databases: - WGSN for trend forecasting - Edited for retail analytics - Fashion United industry statistics - Statista fashion retail data

Final Analysis: The Verdict on REDTAPE's Journey

As we conclude this deep dive into REDTAPE's remarkable journey, we're left with a company that defies simple categorization. This isn't merely a footwear manufacturer that got lucky, nor is it a fashion unicorn destined for global domination. REDTAPE represents something more nuanced—a testament to the power of patient brand building in emerging markets and the complexities of sustaining that success in public markets.

The fundamental question investors must grapple with isn't whether REDTAPE is a good company—by most metrics, it clearly is. With revenues exceeding ₹2,000 crores, a 28-year heritage, presence in 37 countries, and over 435 stores, REDTAPE has built something substantial. The question is whether it's a good investment at current valuations, and whether its best days are ahead or behind.

The Structural Advantages Remain Intact

REDTAPE's core strengths—backward integration from tanneries, international brand credibility, and omnichannel presence—provide durable competitive advantages. These aren't easily replicable by new entrants or pure-play digital brands. The company's ability to control quality from raw material to retail, while maintaining presence across price points through sub-brands, creates a moat that should endure medium-term fashion cycles.

The Execution Challenges Are Real

However, recent quarterly volatility suggests execution challenges in managing this complex, multi-category, multi-geography business. The 43% sequential profit decline in Q4 FY25 can't be dismissed as mere seasonality. It points to potential issues in inventory management, pricing power, or operational efficiency that need addressing before growth can resume sustainably.

The Valuation Conundrum

Trading at 40x P/E in a fashion retail business is betting on perfection—perfection that recent results suggest isn't forthcoming. The market's 28% haircut over the past year reflects this recalibration of expectations. For new investors, the question becomes whether the correction is sufficient or if further re-rating awaits.

The Path Forward

REDTAPE's future likely lies not in explosive growth but in steady evolution—improving same-store sales, gradual margin expansion through operational efficiency, and selective international expansion. The company needs to prove it can generate consistent free cash flow before markets will reward it with premium valuations again.

The recent dividend policy shift signals management's recognition that REDTAPE may be transitioning from growth to maturity. This isn't necessarily negative—many successful fashion brands have created tremendous shareholder value as mature, cash-generative businesses. But it requires a different playbook than the aggressive expansion that characterized REDTAPE's first 25 years.

The Generational Question

Perhaps the most critical challenge facing REDTAPE is generational relevance. Fashion brands face an existential question every decade: can they remain relevant to new consumers while retaining their core customer base? REDTAPE's heritage is both asset and liability here. The brand that conquered UK high streets in 1996 must now win over Gen Z consumers who shop on Instagram and value sustainability over heritage.

The India Opportunity

Despite challenges, the India opportunity remains massive. Fashion retail penetration is still low, branded products are gaining share from unorganized players, and rising disposable incomes continue expanding the addressable market. REDTAPE is well-positioned to capture this growth—if it can execute.

The Investment Perspective

For potential investors, REDTAPE presents a complex risk-reward proposition. The bear case of fashion cyclicality, execution challenges, and high valuations is valid. But so is the bull case of brand strength, market opportunity, and operational leverage potential.

The pragmatic view: REDTAPE is neither a momentum growth story nor a value trap. It's a business in transition, navigating the challenging shift from entrepreneurial growth to institutional maturity. Success isn't guaranteed, but the foundations—brand, infrastructure, and market position—provide a reasonable probability of creating long-term value.

The Historical Context

In the annals of Indian business history, REDTAPE has already secured its place as a pioneer—one of the first Indian brands to successfully challenge Western dominance in fashion retail. Whether it becomes India's LVMH or remains a successful but regional player will be determined in the next five years.

The Mirza family's journey from Kanpur's tanneries to London's high streets to India's malls is more than a business success story. It's a narrative about ambition, timing, and the courage to challenge conventional wisdom. That same courage will be needed as REDTAPE navigates its next chapter—one where the challenges are different but no less daunting than those faced by two brothers standing before a modest tannery in 1979.

The Closing Thought

REDTAPE's story reminds us that building enduring brands requires more than capital and strategy—it requires patience, vision, and the ability to evolve while staying true to core values. The company has proven it can build; now it must prove it can sustain and transform.

For shareholders, employees, and customers, the next chapter of the REDTAPE story is being written now. The pen is in the hands of a management team that must balance heritage with innovation, growth with profitability, and Indian roots with global ambitions. The outcome isn't predetermined, but the stage is set for either triumph or disappointment.

In fashion, as in investing, timing is everything. Whether this is REDTAPE's moment to buy, hold, or sell depends on one's conviction about Indian consumption, faith in management execution, and tolerance for volatility. What's certain is that REDTAPE's journey—from Kanpur to the world and back—offers lessons in brand building, value creation, and the endless complexity of public market capitalism.

The red tape that once symbolized British bureaucracy has been transformed by an Indian company into a symbol of aspiration and achievement. Whether that symbol retains its luster or fades into fashion history's footnotes will be determined not by past glories but by future execution. The market, as always, will be the final judge.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube