Redington: The Story of India's Distribution Powerhouse

I. Introduction & Episode Roadmap

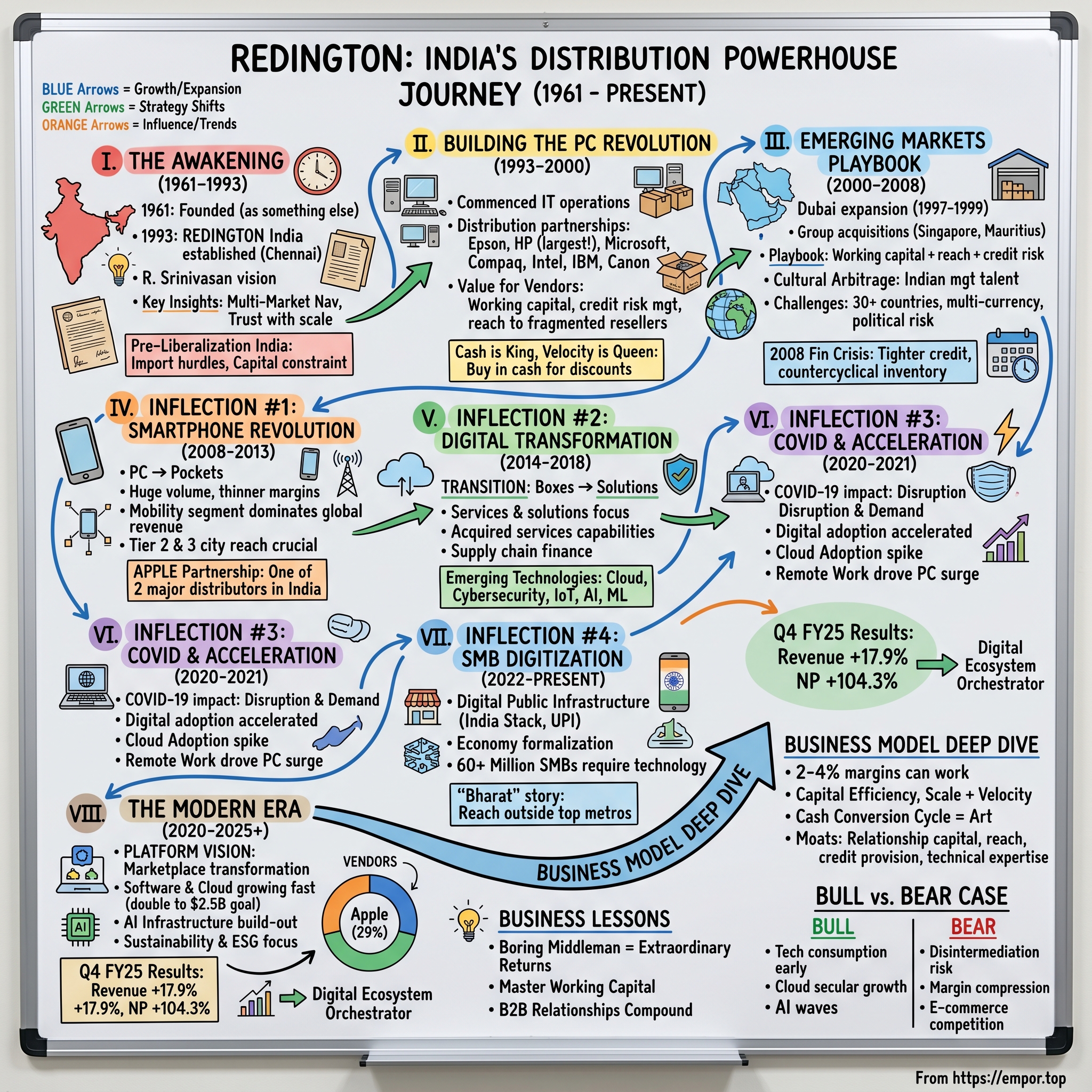

Chennai, 1993. The Berlin Wall had fallen four years earlier. India had just opened its economy to the world. And in a small office in Tamil Nadu, a vision was taking shape that would eventually touch billions of dollars in technology flowing through emerging markets.

R. Srinivasan co-founded Redington in 1993, though the company was incorporated on May 2, 1961. Today, Redington is valued at over $10 billion, with a network of 450+ international brands across 40 markets. The company has become something most people will never hear about yet touch every day—with revenues of ₹99,333.65 crore (approximately $12 billion) in fiscal 2025, Redington represents the invisible infrastructure that makes the technology revolution possible.

The central mystery of Redington's story isn't just how a Chennai startup became one of the world's seventh-largest technology distributors. It's a deeper question: How does a company operating on razor-thin margins—typically 2-4%—create sustainable value and competitive advantage in an age when everyone talks about "cutting out the middleman"?

This is the acquired.fm treatment: we'll trace Redington's evolution from a traditional trading house selling HP printers to a sophisticated supply chain orchestrator managing cloud subscriptions and AI infrastructure. Along the way, we'll unpack four major inflection points that redefined the company, explore why distribution in emerging markets creates different economic dynamics than in developed ones, and understand how "boring" businesses in growth industries can generate extraordinary returns.

The themes we'll explore: Network effects in B2B markets. The power of being "picks and shovels" during tech booms. Working capital as competitive moat. And the transition from moving boxes to orchestrating digital ecosystems.

II. Founding Context & India's Tech Awakening (1961–1993)

Before Redington became Redington, there was a different India—one locked behind the "License Raj," where importing a computer required government permission and forex allocations were measured in drops.

R. Srinivasan, an alumnus of IIM Ahmedabad, moved to Indonesia and then Singapore in the early 1980s, where he founded Redington focusing on the market in India and the Middle East. Prior to starting Redington in Singapore, he spent three years in Indonesia with a leading textile company from 1978 to 1981, and his experience also included years with Readers Digest and The Coca-Cola Corporation in India.

The business model was simple but required deep expertise: import technology products—starting with printers—and navigate the labyrinthine regulations of multiple emerging markets. But this wasn't just about buying low and selling high. Distribution in pre-liberalization India meant understanding working capital cycles in an environment where letters of credit took weeks, vendor relationships required personal trust built over years, and logistics meant physical presence in dozens of cities connected by questionable infrastructure.

Why did tech companies need distributors like the early Redington? Three reasons stood out: Working capital provision (vendors wanted cash, resellers needed credit), geographic reach (HP couldn't afford sales offices in 200 Indian cities), and credit risk management (someone needed to evaluate thousands of small resellers' creditworthiness).

The inflection point arrived with economic liberalization in 1991. India's doors opened to foreign investment. Tech multinationals saw a billion-person market awakening. And suddenly, in 1993, Srinivasan decided to set up Redington in Chennai to distribute IT products, just as liberalization had begun in India.

The seeds were planted. What came next would be two decades of riding multiple technology waves while building something harder than it looked: a distribution network with trust at scale.

III. The Foundation Years: Riding India's PC Revolution (1993–2000)

During 1994, Redington commenced service operations for IT products, distribution of Epson and Tripplite IT products, and distribution of Samsung monitors, also commencing its operations in Northern India. The company was positioning itself at a critical moment: India's PC revolution was just beginning.

The value proposition Redington offered to multinational vendors like HP and Microsoft was deceptively simple but operationally complex: We'll provide working capital, last-mile reach to thousands of resellers, manage credit risk, offer technical support, and do it all at scale. For vendors, this meant avoiding the capital intensity of building their own distribution while accessing a fragmented market of thousands of small retailers and system integrators.

In 1995, Redington started operations in Eastern India and commenced distribution of Compaq and Philips products. In 1996, the company started distributing Intel products. The company made tie-ups with Microsoft for distribution of software products in 1997 and also with IBM, APC and Canon for distribution of their products in 1998.

The business model at this stage operated on what might be called "the aggregation of marginal resellers" model. India's tech market wasn't dominated by Best Buy-style superstores. Instead, thousands of small shops in cities and towns served as the interface between technology and consumers. These resellers needed someone to provide inventory, credit terms, technical training, and warranty support. Redington became that someone.

The financial model was already taking shape: The company mostly makes purchases in cash to avail cash discounts instead of buying goods on credit to stay in the competition, with cash discounts helping improve profit margins, which are generally very thin in distribution. Volume business includes high-volume, fast-moving products like Samsung monitors and HP peripherals, where brands are well established and distributors act as liaisons.

Redington went public with an IPO in 2004, raising approximately INR 1.5 billion to fund its expanding distribution network. By the end of the decade, Hewlett Packard honored the company as an excellent service provider in 2000. The foundation was solid: pan-India presence, blue-chip vendor relationships, and a growing understanding that in distribution, cash is king and velocity is queen.

The competitive landscape featured established players. Ingram Micro is Redington's biggest competition in the Indian market, with Redington and Ingram addressing the majority of the market (around 70%) in India, while other regional players include Savex Technologies and Rashi Peripherals.

Yet Redington was building something harder to replicate than it appeared: not just warehouses and trucks, but relationships compounded over thousands of transactions. Every month, every quarter, the trust ledger grew. Resellers learned Redington delivered on time. Vendors learned Redington managed credit risk well. And Redington learned the intricate dance of working capital management that would become its core competency.

The Y2K boom at the decade's end provided rocket fuel. Companies rushed to upgrade systems. Redington works with 300+ brands including Apple, Microsoft, Dell, HP, Lenovo, Samsung, Adobe, Cisco, AWS, though many of these partnerships would develop in subsequent years. By 2000, Redington had become HP's largest distributor in India—a position that spoke to both scale and execution capability.

IV. Geographic Expansion: Building the Emerging Markets Playbook (2000–2008)

The key insight that would define Redington's next phase was elegantly simple: If distribution in India is hard because of fragmentation, poor infrastructure, credit risk, and complex logistics, then these same challenges exist across dozens of other emerging markets. And we've already learned how to solve them.

Redington started business in Dubai in 1997, distributing computing devices and networking products. Redington Gulf FZE started operation in 1999 as a subsidiary of Redington Mauritius Limited, and in April 2004, the Redington group acquired Redington Gulf FZE from Redington Mauritius.

The Middle East strategy was shrewd: Dubai became a hub for serving not just the UAE but the broader Gulf region and eventually Africa. During this time, the Redington group also invested significantly in Redington Distribution Pte Ltd and Cadensworth, and in 2006, acquired 100% stake in both Redington Distribution Pte Ltd and Cadensworth.

The expansion wasn't just opportunistic—it was a deliberate playbook. Take the distribution challenges from India, adapt them to local regulations and cultural contexts, and deploy the same fundamental model: aggregate vendor relationships, provide working capital, manage credit risk, build last-mile reach. Redington operates in over 30+ emerging markets including India, Middle East, Africa, and South Asia.

There was what one might call "cultural arbitrage" at work: Indian management talent, experienced in navigating complexity, understanding hierarchical business structures, and operating with capital efficiency, proved adept at managing emerging market challenges that stumped many Western companies. When HP or Microsoft wanted to enter markets in Africa or South Asia, partnering with Redington meant working with executives who understood emerging market realities viscerally.

The challenges were formidable. The ratings factor in modest operating margin and large working capital requirement in the distribution business. Multiply that across 20+ countries, each with different currencies, political risks, import/export regulations, and payment terms, and the complexity becomes exponential.

Yet Redington's vendor relationships deepened during this period. In 2007, Redington India started to distribute Apple products. In 2008, Redington India became the distributor of Adobe products and forged partnership with Adobe in February 2008. The portfolio was becoming a who's who of tech: HP, Microsoft, Apple, Cisco, Lenovo, Dell, Samsung.

The 2008 financial crisis tested the model. Global demand collapsed. Credit markets froze. But Redington's countercyclical inventory management—reducing stock as demand fell, negotiating extended vendor payment terms, tightening reseller credit—demonstrated operational sophistication that would serve it well in future downturns.

In 2008, Investcorp bought 26% stake of Redington International, which they later sold in 2012. Synnex Corp, one of the largest IT distributors in the world, invested $24 million in 2005 for a 36.31 percent stake in the Redington Group in a strategic alliance, with Synnex enhancing their reach in India in exchange for improving Redington's logistics management and operational efficiency.

By the end of this period, Redington had established something powerful: a multi-country distribution network that vendors couldn't easily replicate and competitors couldn't easily match. The moat was being dug, transaction by transaction, market by market.

V. Inflection Point #1: The Smartphone & Mobility Revolution (2008–2013)

Then the ground shifted. The iPhone launched in 2007. Android followed. And within a few years, the center of gravity in consumer technology moved from PCs to pockets.

Redington commenced distribution and servicing of Motorola mobile phones during 2003, but the real smartphone wave hit later. The mobility segment would eventually transform Redington's business mix. India's market was particularly explosive: hundreds of millions of consumers were skipping PCs entirely and going straight to smartphones.

Redington faced a strategic challenge: pure-play mobile distributors were emerging, brands were experimenting with direct models, and margins on mobility products were even thinner than PCs. The competitive intensity was fierce. Chinese brands—Xiaomi, OnePlus, Vivo, Oppo—flooded the Indian market, each needing distribution partners to reach tier-two and tier-three cities.

The strategic response involved building mobility-specific supply chains and credit lines. Redington and Ingram Micro are the only major distributors of Apple products in India—a privileged position as Apple's brand cachet grew among India's aspirational middle class.

Margins came under severe pressure, but volumes exploded. Distribution of smartphones and featurephones is Redington's largest contributor to global revenues at ₹8,713 crore in recent quarters. The India smartphone story was mesmerizing: feature phone users upgrading to smartphones by the tens of millions annually. Redington's pan-India reach—covering not just metros but towns with populations of 100,000—became invaluable as brands raced for market share.

The geography-as-moat thesis proved valid. Brands could theoretically go direct online, but offline retail still dominated in India, especially outside major cities. Building and managing relationships with 40,000+ retail touchpoints across India's impossible geography—that couldn't be replicated overnight.

During this period, revenue crossed significant milestones. The company was approaching $10 billion in annual revenue, driven substantially by the mobility boom. But a deeper question was emerging: What happens when technology shifts from atoms to bits? When software eats distribution?

VI. Inflection Point #2: The Digital Transformation & Services Pivot (2014–2018)

The existential question crystallized around 2014: In a world moving to cloud computing, SaaS, and direct digital downloads, what role exists for a physical goods distributor?

Cloud computing was the obvious threat. Why would companies need distributors for software they could download directly from AWS, Microsoft Azure, or Google Cloud? Amazon Web Services was growing explosively, offering infrastructure with a credit card—no distributor required. The "boxes and wires" business model faced potential obsolescence.

Redington's strategic response would define the next chapter: repositioning from product distribution to services and solutions. During FY 2019-20, the company took decisive steps in its pivot towards transitioning itself into a Solution Oriented Distributor and augmented its skills and capabilities in critical, future-oriented and emerging technologies in areas of Cloud, Cybersecurity, Internet of Things (IoT), Artificial Intelligence (AI) & Machine Learning (ML).

The pivot involved several dimensions. First, acquiring services capabilities. Redington setup Citrus Consulting in 2018 to provide niche services like cloud transformation, advanced analytics, big data management, data centre modernisation, recording revenues of Rs 205 mn in FY20.

Second, expanding into cybersecurity distribution. In October 2015, Redington Value forged partnership with CyberArk through which Redington Value became enabled to distribute CyberArk's Privileged Account Security Platform throughout the middle east region. In September 2020, Redington Value signed partnership with CrowdStrike to distribute its falcon endpoint protection suite in the MENA region.

Third, building managed services offerings. In 2012, Redington started carrying out supply chain management business independently through a wholly owned subsidiary, ProConnect Supply Chain Solutions Limited. The goal was creating recurring revenue streams less dependent on hardware sales volatility.

Fourth, innovating in supply chain finance. The insight: Redington's core competency wasn't just moving boxes—it was managing working capital and credit risk at scale. Why not offer invoice discounting, channel financing platforms, and payment solutions to the ecosystem? This built on existing strengths while creating new revenue streams.

The enterprise and cloud solutions segment is fast-growing, high-margin business, including SaaS, cloud infrastructure, cybersecurity, and licensing. The services mix was beginning to shift the overall margin profile.

The company also rationalized its portfolio. During 2021, the company sold its entire shareholding in Ensure Support Services (India) Limited, a wholly owned subsidiary, to Accel Limited, as this business vertical was not strategic to the company.

Leadership transitions marked this period as well. In August 2023, Rajiv Srivastava resigned as Managing Director of Redington citing personal reasons. Redington became a professionally run company since 2015, with the founder divesting all his stake in 2018.

The strategic bet: Distribution wouldn't disappear—it would transform. Cloud software still needed to be sold, configured, integrated, and supported. Someone needed to aggregate demand from 40,000 resellers and match it to offerings from Microsoft, AWS, Google, and hundreds of ISVs. That someone could be Redington.

By the end of this period, services and software had grown to represent a meaningful portion of revenue, though hardware distribution remained dominant. The transformation was underway, but incomplete.

VII. Inflection Point #3: COVID-19 and Accelerated Digital Adoption (2020–2021)

Then came March 2020. The pandemic shut down offices, retail stores, schools. And paradoxically, demand for technology exploded.

The COVID-19 impact on Redington manifested in multiple ways. Remote work drove a PC and laptop surge—enterprises rushed to equip employees for work-from-home. Digital transformation spending, which had been a multi-year journey for many companies, suddenly became a multi-month emergency. Cloud adoption accelerated by several years in several months.

As a major milestone, Redington surpassed Rs. 62,000 crores in revenues for the full year FY'22, with PAT growth at 69% for the year. The pandemic revealed Redington's value: when supply chains got disrupted globally, having a local distributor with inventory, logistics capabilities, and vendor relationships became crucial.

The stock market recognized this value creation. Share prices surged from around ₹80 pre-pandemic to over ₹200 during 2020-2021 as investors appreciated both the immediate revenue boost and the long-term digital transformation tailwind.

Redington's cloud resell and managed services business is the fastest growing at 53% year-on-year, though contributing only ₹972 crore to overall revenue in recent quarters. The services transformation was gaining momentum, accelerated by pandemic-driven digital adoption.

Leadership changes continued. Ramesh Natarajan, currently CEO of Redington India with over 28 years at Redington, was elevated to CEO – IME (India and Middle East) effective July 1, 2025, instrumental in scaling both consumer and enterprise verticals. Rajat Vohra, the current Chief Sales Officer for Redington India, was appointed CEO – India effective July 1, 2025.

VIII. The Modern Era: Multi-Cloud, AI, and Platform Play (2020–2025)

Today, Redington operates at a different scale and in a different mode than its founding vision. With presence across 38 markets through 60 subsidiary offices, over 300 brand associations, and 43,000 channel partners, Redington enables seamless end-to-end distribution.

In Q4 FY25 announced on May 19, 2025, Redington's revenue from operations increased 17.9% to ₹26,439.68 crore compared to ₹22,433.41 crore year-over-year, with consolidated net profit growing 104.3% to ₹665.62 crore from ₹325.59 crore. The financial performance demonstrated sustained momentum.

The services mix has reached critical mass. Software business, currently part of the technology solutions unit, currently makes up 10% of the Redington Group's overall business, with plans for expansion. Redington expects its software business to double to $2.5 billion in the next three to five years, growing at 30-40% annually.

Cloud distribution evolution represents a major focus. CloudQuarks, Redington's online cloud platform ensures a seamless cloud journey for partners and customers, with capabilities emboldened by partnerships with leading players like Amazon, Microsoft and Google. The newly minted Software Solutions Group (SSG) consolidates the distributor's cloud, software, and security businesses into a single, digitally driven powerhouse.

Cybersecurity has become a major growth engine. In September 2025, Redington announced a strategic distribution agreement with CrowdStrike to bring the AI-native CrowdStrike Falcon platform to Redington's customers and partners across India. The post-COVID awareness of cyber threats, combined with regulatory requirements, has driven enterprise investment in security solutions.

Apple ecosystem distribution remains significant. Redington's single largest vendor is Apple, with a revenue contribution of 29% in the first half of FY25, followed by HP at 10%, Lenovo at 8%, and Samsung and Dell each contributing 7%. India's premiumization trend—rising affluence driving demand for premium devices—plays into Redington's Apple relationship.

The AI hardware wave is just beginning. Companies are investing in GPUs, servers, and edge computing infrastructure to support AI workloads. The market is expected to see faster tech refresh cycles in the next three years on personal computers, mobile phones and servers, besides cloud solutions and new AI solutions. Redington is positioning to capture this demand.

The platform vision is taking shape. Redington is looking to transform itself into a marketplace platform from a pure-play distribution company, with the change stemming from sharp growth in software and cloud segments, with the marketplace platform beginning to take shape from 2025. Redington is investing a few million dollars on the platform called Cloud Quarks to make it more analytically oriented, building a marketplace around it with multiple vendors and software.

Sustainability and ESG focus has grown. The company is solving environmental problems by renovating four village ponds which increased water storage of 12,000 cubic meters, constructing 3 model biogas plants, 16 community wells, and six rainwater harvesting structures, increasing water inflow and groundwater enabling year-round water access.

Leadership for the modern era combines seasoned Redington veterans with external expertise. V.S. Hariharan, Group CEO of Redington Limited, is an accomplished leader with three decades of experience in sales, marketing, and general management, with career defined by commitment to innovation and driving growth, including global and Asia pacific leadership roles at Hewlett-Packard.

IX. Inflection Point #4: India's Digital Public Infrastructure & SMB Digitization (2022–Present)

The fourth inflection point isn't a product cycle—it's infrastructure. India has built a remarkable stack of digital public goods: the India Stack (Aadhaar for identity, UPI for payments), GST for tax administration, and a broader push toward formalizing the economy.

The implications for Redington are profound. Small and medium-sized businesses account for around 31% of India's GDP and 43% of exports, contributing to economic growth with substantial labor force. As these 60+ million SMBs digitize—adopting cloud accounting, digital payments, e-commerce, online marketing—they need technology infrastructure.

Government initiatives provide tailwinds. The Digital India initiative has been extended with a total budget of ~INR 14,903 Cr from 2021-22 to 2025-26. Production-linked incentive schemes for electronics manufacturing are bringing more manufacturing to India, creating demand for enterprise IT infrastructure.

The "Bharat" story—India beyond the top metros—is where Redington's geographic reach shines. While Amazon Business, Flipkart B2B, and other e-commerce platforms compete in major cities, reaching small towns requires the kind of physical presence and relationship capital that Redington has built over decades.

Competition from e-commerce is real but not existential. Redington's domestic business has seen increased competition from e-commerce players in PC, laptops, and mobility markets, with many brands having direct partnerships with e-commerce players or large format retailers, and competitors expanding reach throughout the country. But B2B purchasing, especially for enterprises, still values the services layer that distributors provide: credit terms, technical support, installation, warranty management.

The fintech integration opportunity is intriguing. Redington sits on valuable transaction data across tens of thousands of resellers. Understanding payment patterns, inventory turns, and credit risk could enable embedded financial services—offering working capital loans, payment processing, trade finance to channel partners. This leverages existing relationships while creating new revenue streams.

According to Zinnov, SMB digitalization in India will be a USD 80Bn opportunity by 2024, getting significant global attention. In 2019, SMBs offered a massive USD 30 BN digital opportunity, with only 53% tapped, set to grow to USD 80-85 Bn over five years. Redington is positioning itself to capture a meaningful share of this wave.

X. The Business Model Deep Dive

Understanding Redington requires understanding why a 2-4% margin business can be attractive and sustainable. The unit economics work through scale and velocity.

Gross margins on product distribution are thin—ratings reflect strong business risk profile backed by established market position in IT and mobility products distribution, improving product and geographical diversification, offset by modest operating margin and large working capital requirement. But at ₹100,000 crore revenue, even 2% margin generates ₹2,000 crore in gross profit.

The real art is working capital mastery. Redington purchases products in bulk from vendors and sells them to resellers/sub-distributors/system integrators and retailers on a principal-to-principal basis. The company mostly makes purchases in cash to avail cash discounts instead of buying on credit to stay competitive, with cash discounts helping improve profit margins which are generally very thin in distribution.

The cash conversion cycle is critical: How many days between paying vendors and collecting from resellers? Compress that cycle, and the same capital can be turned over more times per year, multiplying returns. Extend vendor payment terms from 30 to 45 days while collecting from resellers in 60 instead of 90 days, and suddenly you've freed up significant working capital.

The flywheel operates like this: Scale with vendors leads to better commercial terms and priority allocation during shortages. Better terms enable competitive pricing to resellers. Larger reseller network creates more demand, which vendors value. Vendor appreciation leads to more product allocation and better terms. The cycle reinforces itself.

Why is this a "good" low-margin business? Three reasons:

First, capital efficiency improves with scale. Higher operational profits due to effective global working capital management resulted in greater ROCE, with EBIT improving in FY22 pushing ROCE to greater heights, while ROE rose to 24.1% in FY22 compared to 16.4% in FY21. When you can turn capital over 8-10 times per year, 2-3% margins on each turn compound to attractive returns on equity.

Second, the business generates cash. Unlike capital-intensive manufacturing or R&D-heavy software, distribution—done well—converts earnings to cash relatively quickly. This enables dividends and reinvestment without requiring external capital.

Third, the services overlay improves the blended margin profile. As software, cloud, and services grow to 25-30% of revenue with better margins, overall profitability improves while maintaining the volume base from hardware.

Moats and defensibility come from several sources:

Relationship capital compounds over decades. Redington has relationships with over 30 vendors for more than 10 years. Trust isn't built overnight—it's built transaction by transaction, quarter by quarter, through market cycles.

Geographic reach and logistics infrastructure can't be replicated quickly. Currently, the company has three automated distribution centres (ADCs)—in Chennai and Kolkata in India, and Dubai. Building this physical presence requires years and capital.

Working capital and credit provision represent a genuine barrier. Small resellers can't get bank loans easily. Redington's ability to provide 60-90 day payment terms, backed by its own credit lines and vendor relationships, creates dependency.

Technical expertise and certification programs matter in enterprise sales. Redington invests in training its sales force and channel partners on new technologies. Redington invests in capability building through Redington Academy and training, and specialized practices in areas like security, analytics, and AI, ensuring teams and partners are equipped to deliver value.

Scale advantages and data are emerging as the platform strategy develops. Transaction data across thousands of partners and millions of end customers provides insights into demand patterns, helping with inventory optimization and forecasting.

Risks and vulnerabilities are real:

Disintermediation remains the existential threat. If major vendors go completely direct or if e-commerce fully replaces offline retail, distribution's role shrinks. Cloud software in particular reduces the need for physical distribution.

Margin compression from competition is constant. The company operates on thin margins influenced by declining IT product prices, short product life cycles, and pricing pressures from OEMs and resellers, with revenue concentration on select products or customers amplifying pressure.

Inventory obsolescence and forex exposure create risk. Risks include low gross margins characteristic of the business, high vendor concentration with HP accounting for ~35% of overall sales, receivable risk from selling goods on credit to fragmented resellers, high working capital intensity, and inventory risk. Technology products depreciate quickly—last quarter's models lose value fast.

Concentration risk exists with top vendors. Apple contributes 29% of revenue in H1 FY25. Losing a major vendor relationship would materially impact the business.

Working capital management during downturns tests the model. When demand falls, inventory must be reduced quickly, reseller credit tightened, and vendor payment terms renegotiated—all while maintaining relationships.

XI. Competitive Landscape & Market Position

Redington operates in a moderately consolidated industry with a few large players and many smaller regional distributors.

Ingram Micro is Redington's biggest competition in the Indian market, with Redington and Ingram addressing the majority of the market (around 70%) in India, while other regional players include Savex Technologies and Rashi Peripherals. Redington is currently the 2nd largest technology product distributor in India behind Ingram Micro and the largest IT distributor in Middle East, Turkey and Africa.

Globally, the competitive set includes massive distributors. Ingram name-checked Pax8 as one of 15 competitors alongside TD Synnex, Arrow, Scanscource, Westcon-Comstor, Synnex Technology, Anixter, ALSO, Esprinet, Redington, Exclusive Networks, Intcomex, D&H, Carahsoft and AppDirect. Redington Ltd is headquartered in India with 5,037 employees and $11.9B revenue, smaller than global giants but significant in its markets.

Why is India distribution uniquely fragmented? The country's geography, diversity of local markets, language barriers, payment systems, and credit dynamics create complexity that favors local expertise. A global distributor can't easily parachute in and win—local presence, relationships, and understanding matter enormously.

The "long tail" of resellers creates stickiness. Unlike the US where a handful of large retailers (Best Buy, Amazon, big system integrators) might cover most volume, India has thousands of small retailers and system integrators. Reaching and serving them profitably requires the scale and infrastructure Redington has built.

Vertical specialists versus horizontal generalists represents a strategic choice. Some competitors focus on specific product categories (networking, security) or verticals (healthcare, government). Redington's horizontal approach—serving multiple product categories across verticals—provides diversification but potentially less depth in any single category.

Direct-to-consumer threats and hybrid models are evolving. Being one of two only distributors of Apple in India is a big advantage for Redington, supplying Apple products to both offline and online players, with Redington believing Apple's online store will increase demand overall, maintaining market share as in UAE despite Apple stores and direct partnerships.

What does Redington do better than anyone else? Three capabilities stand out:

Multi-market orchestration: Operating successfully across 38+ countries with different regulations, currencies, and business cultures requires organizational capability that few possess.

Working capital at scale: Managing billions of dollars in inventory, receivables, and payables across fragmented markets is genuinely hard. Redington's track record here is its calling card.

Vendor-agnostic breadth: Rather than betting on single platforms, Redington maintains relationships across the technology ecosystem—Apple, Microsoft, Google, AWS, HP, Dell, Lenovo, Cisco, and hundreds more. This diversification reduces risk and provides optionality as technology waves shift.

XII. Playbook: Business & Investing Lessons

Redington's story teaches lessons applicable beyond distribution:

Lesson 1: Being a "boring" middleman in a growth industry can generate extraordinary returns. Distribution lacks the glamour of SaaS unicorns or AI breakthroughs. But positioning between multinational vendors and billions of emerging market consumers during a multi-decade technology adoption wave created immense value. Sometimes the picks and shovels in a gold rush outperform the prospectors.

Lesson 2: Master working capital in low-margin, high-velocity businesses. The art isn't charging high margins—it's turning capital over efficiently. Effective global working capital management resulted in higher operational profits and greater ROCE. Each percentage point improvement in inventory turns or payment terms compounds to meaningful returns.

Lesson 3: Geographic expansion as diversification and learning. Redington's expansion across emerging markets provided revenue diversification, but also learning: Each market taught lessons about credit risk, vendor negotiations, and operational efficiency that improved the overall business.

Lesson 4: Platform businesses start as service businesses. Redington is looking to transform into a marketplace platform from pure-play distribution, with the marketplace platform beginning to take shape from 2025. The transition from "pipes" (moving products) to "platforms" (connecting ecosystem participants digitally) builds on existing relationships and trust rather than starting from scratch.

Lesson 5: In B2B, relationships and trust compound over decades. Consumer businesses can scale virally through products. B2B requires relationship building at scale—harder but more defensible. Redington has relationships with over 30 vendors for more than 10 years. That trust represents a genuine moat.

Lesson 6: Anticipate industry shifts 3-5 years early. During FY 2019-20, the company took decisive steps in its pivot towards Solution Oriented Distributor, augmenting capabilities in Cloud, Cybersecurity, IoT, AI & ML. The pivot to services began before cloud completely dominated, allowing Redington to build capabilities before existential pressure arrived.

Lesson 7: Services and software margins subsidize product distribution. The enterprise and cloud solutions segment is fast-growing, high-margin business including SaaS, cloud infrastructure, cybersecurity, and licensing. The blended margin profile improves while maintaining volume relationships.

Lesson 8: In emerging markets, execution capability is the ultimate moat. Strategy documents look similar across competitors. Execution—actually delivering products on time, managing credit risk, training thousands of salespeople, navigating regulatory complexity—separates winners from aspirants.

Capital allocation philosophy has been measured. Redington's Board recommended a final dividend of ₹3.5 per equity share for FY 2024-25. The company has pursued selective acquisitions to build capabilities rather than buying revenue, maintained balance sheet discipline, and returned cash to shareholders when appropriate.

XIII. Bull vs. Bear Case

Bull Case:

India's tech consumption remains early innings. Despite growth, India still has relatively low per-capita ownership of PCs, smartphones, and enterprise IT infrastructure compared to developed markets. Hundreds of millions of consumers will upgrade devices over the next decade. Tens of thousands of enterprises will modernize IT infrastructure.

Services mix inflecting toward 40-50% of revenue with better margins. Software currently makes up 10% of overall business, with expectations to double to $2.5 billion in 3-5 years growing at 30-40% annually. As this mix shifts, overall profitability improves meaningfully.

Cloud and cybersecurity secular growth trends favor Redington's positioning. The Global AI in Cybersecurity market was valued at USD 29.04 billion in 2024, projected to reach USD 288.28 billion by 2034, exhibiting a CAGR of 25.8% during 2025–2034. Redington's partnerships and capabilities position it to capture this wave.

AI infrastructure build-out drives demand for GPUs, servers, and edge computing hardware. The market expects faster tech refresh cycles in the next three years on PCs, mobile phones and servers, besides cloud solutions and new AI solutions. Redington can ride this hardware upgrade cycle.

Emerging markets digitization tailwind extends beyond India. Redington's presence across 38 markets through 60 subsidiary offices positions it across multiple growth markets. Africa, Middle East, and South Asia are earlier in digital transformation journeys than developed markets.

Platform ecosystem creating network effects. Redington is investing millions in Cloud Quarks platform to make it analytically oriented, building a marketplace with multiple vendors and software. Successfully transitioning to a platform model could unlock new revenue streams and defensibility.

Strong cash generation and improving ROE. ROE rose to 24.1% in FY22 compared to 16.4% in FY21. The business model, operating efficiently, generates attractive returns on equity without requiring continuous capital infusions.

Undervalued relative to growth prospects if services transformation succeeds. With improving margins, faster-growing services revenue, and platform optionality, current valuation may not reflect future earning power.

Bear Case:

Structural margin compression from direct models and e-commerce threatens the business model. Redington has seen increased competition from e-commerce players in PC, laptops, and mobility markets, with many brands having direct partnerships with e-commerce players. As online penetration grows, distribution's role shrinks.

Vendor consolidation reduces negotiating power. If HP and Dell merge, or if major vendors rationalize distributor relationships to just one per market, Redington loses leverage and potentially revenue.

Large customers bringing distribution in-house is a constant risk. Major enterprises might decide they're big enough to negotiate directly with vendors, cutting out distributors entirely for high-volume purchases.

Cloud software reducing physical distribution need remains a long-term threat. While Redington is pivoting to cloud services, the core economic shift—from selling physical products to provisioning digital services—fundamentally changes the role and margins of distribution.

Working capital risks during economic downturn could be severe. In a liquidity crisis, vendors might demand faster payment while resellers slow collections. Managing working capital through a severe downturn tests the model.

Currency exposure across 35+ countries creates earnings volatility. Risks include high working capital intensity, inventory risk, receivable risk from fragmented resellers, and high vendor concentration. Exchange rate swings can materially impact consolidated results.

Execution risk in services transformation is substantial. Building services capabilities, acquiring technical talent, and shifting organizational culture from product distribution to solution selling is genuinely hard. Many have tried; fewer have succeeded.

Limited pricing power in commoditized products constrains margins. PCs, smartphones, and standard IT hardware have become increasingly commodity-like. Distributors can't command premium prices without differentiated services.

Competition from well-capitalized e-commerce giants in B2B represents a formidable threat. Amazon Business, Flipkart's B2B operations, and potential new entrants have deeper pockets and technology platforms that could disrupt traditional distribution.

XIV. Recent Developments & Future Outlook

Latest results from Q4 FY25 announced May 19, 2025 showed revenue increasing 17.9% to ₹26,439.68 crore with net profit growing 104.3% to ₹665.62 crore. EBITDA for the quarter stood at ₹576.91 crore, marking 25.7% increase with EBITDA margin improving to 2.2% from 2.0% year-over-year, reflecting enhanced operational efficiency.

Management commentary emphasizes strategic priorities around services expansion and platform development. Group CEO V.S. Hariharan said the marketplace platform will begin taking shape from 2025 and later become a larger play, with investment of few million dollars on Cloud Quarks platform to make it analytically oriented.

Emerging opportunities span multiple domains:

AI hardware distribution: As enterprises adopt AI, they need infrastructure. GPUs from NVIDIA, specialized AI chips, edge computing devices—Redington's distribution network positions it to supply this emerging category.

IoT and edge computing: The proliferation of connected devices creates demand for gateways, sensors, and edge processing equipment. Distribution expertise applies to these emerging product categories.

Green tech and sustainability: India's push toward renewable energy and electric vehicles creates demand for solar equipment, EV charging infrastructure, and energy management systems—adjacent markets where Redington could expand.

Potential adjacencies include:

Fintech and embedded finance: Leveraging B2B transaction data and credit relationships to offer working capital, payment processing, and financial services to channel partners.

SaaS marketplace: Building a true platform where ISVs can list offerings, resellers can discover and purchase, and Redington facilitates transactions and billing—analogous to AWS Marketplace or Microsoft AppSource but for emerging markets.

Data analytics: The transaction data across thousands of partners has value. Offering insights back to vendors about demand patterns, pricing elasticity, and channel performance could create new revenue streams.

M&A pipeline activity has been selective rather than aggressive. The strategy appears focused on building capabilities organically while making targeted acquisitions to fill specific gaps (cybersecurity partnerships, cloud expertise) rather than buying revenue.

Succession planning saw Ramesh Natarajan elevated to CEO – IME (India and Middle East) effective July 1, 2025, with Rajat Vohra appointed CEO – India. Professor J. Ramachandran is Chairman of Redington Limited, guiding transformation from founder-managed to board-led institution since 2006, with tenure seeing ten-fold revenue growth to USD 10 billion and twentyfold market cap growth, making Redington the world's seventh-largest technology distribution company.

The next chapter: From distributor to digital ecosystem orchestrator. The vision involves Redington not just moving products but operating the platform where brands, channel partners, and customers connect—facilitating transactions, providing financing, offering analytics, and capturing value from orchestrating the ecosystem rather than just participating in it.

XV. "If We Were CEOs": Strategic Options

If handed the keys to Redington today, five strategic paths warrant serious consideration:

Option 1: Double down on services—acquire more capabilities, build proprietary platforms. This means aggressively shifting the revenue mix toward higher-margin services. Acquire specialized cybersecurity, cloud consulting, or managed services companies in target markets. Build proprietary IP in areas like cloud cost optimization, security automation, or AI infrastructure management. Target 40-50% services mix within five years. The risk: execution complexity and integration challenges. The opportunity: meaningfully improved margins and defensibility.

Option 2: Vertical integration—move into manufacturing or retail. Consider acquiring electronics manufacturing capacity (contract manufacturing for phones or PCs in India taking advantage of PLI schemes) or retail chains (Apple Premium Reseller stores, for example). This captures more value chain but also more capital intensity and changes the business model fundamentally. Probably not the right path—it dilutes focus from core competencies.

Option 3: Geographic consolidation—exit lower-margin countries, focus on India + select markets. Rather than maintaining presence across 38 markets, concentrate capital and management attention on the 5-10 highest-potential markets. This simplifies operations, reduces currency exposure, and allows deeper investment in fewer markets. The risk: forgoing diversification and growth optionality. The benefit: operational focus and potentially higher returns on concentrated investment.

Option 4: Become a fintech play—leverage B2B transaction data and credit relationships. Build a full-stack financial services offering for SMB channel partners: working capital loans, payment processing, trade finance, insurance. The data from transactions provides underwriting advantage. The existing relationships provide distribution. This could transform Redington from distributor with fintech features to fintech company with distribution heritage. High risk but potentially transformational value creation if executed well.

Option 5: Platform aggregation—build the "Alibaba for enterprise tech" in emerging markets. Go all-in on the marketplace vision. Invest $100M+ in building a true two-sided platform that connects not just Redington's vendor relationships but becomes THE destination where any technology buyer in emerging markets discovers and purchases solutions, and any technology seller lists offerings. Capture transaction fees, data insights, advertising revenue. This is the highest-risk, highest-reward path—it requires betting against established players (AWS Marketplace, Microsoft AppSource) and achieving network effects before burning through capital.

What would we prioritize?

A hybrid of Options 1 and 4 seems most promising: Services-first transformation with embedded fintech. Aggressively grow services to 35-40% of revenue within 5 years through organic investment and selective M&A. Simultaneously, build a fintech vertical offering working capital and payment solutions leveraging Redington's credit risk expertise and transaction data. This plays to existing strengths while building new moats.

The platform vision (Option 5) is compelling long-term but requires careful sequencing. Build the platform initially to serve existing channel partners and vendors, creating utility before pursuing broader marketplace ambitions. Think of it as evolving Cloud Quarks from internal tool to ecosystem platform gradually rather than betting the company on a greenfield marketplace.

The 3-5 year bets: Cloud and cybersecurity services scaling to $3B annually. Fintech offerings reaching $500M in revenue. Platform GMV hitting $5B (transactions flowing through Redington's digital marketplace). Hardware distribution remaining stable but growing slower than overall company.

The "boring but brilliant" path: Methodically migrate toward higher-margin, more defensible services and platform revenues while maintaining discipline in core distribution. No hero bets. No transformational M&A. Just consistent execution on strategic priorities with financial discipline. Sometimes boring brilliance beats transformational gambles.

XVI. Epilogue & Reflection

Why does Redington's story matter? Because behind every iPhone sold in Lagos, every HP laptop deployed in a Mumbai enterprise, every cloud subscription provisioned in Dubai, sits invisible infrastructure that makes modern technology accessible.

Redington is the Indiana Jones of distribution—operating in frontier markets, managing complexity most companies avoid, turning obstacles into advantages. While Silicon Valley startups fantasize about eliminating intermediaries, Redington demonstrates that in messy, fragmented, capital-constrained emerging markets, the right intermediary creates enormous value.

What surprised us researching this story was the sheer operational sophistication required to make low-margin distribution work. It looks simple from outside: buy from vendors, sell to resellers, pocket the spread. But managing working capital across 38 countries, maintaining relationships with 300+ vendors and 43,000+ channel partners, forecasting demand for thousands of SKUs, navigating currency fluctuations and credit risk—this operational excellence, compounded over 30+ years, builds something formidable.

The broader lesson: Value creation doesn't require invention. Orchestration done brilliantly—matching buyers and sellers, providing capital, managing risk, offering expertise—creates value without inventing new products. In some ways, this is more sustainable than pure innovation. Products get commoditized. Relationships and operational excellence compound.

The founder-led to professional management transition deserves reflection. Redington became professionally run since 2015, with the founder divesting all stake in 2018. This is relatively rare in India's business landscape, where family control persists. Redington's transition suggests that well-governed, professionally-managed companies can sustain growth and culture beyond founders. The governance philosophy—shaping governance philosophy and strategic direction, successfully navigating technology shifts, regulatory changes, and market dynamics while staying true to founding principles—provides a template.

Where will Redington be in 10 years?

The optimistic scenario: A $20B revenue company with 35% coming from high-margin services and platform businesses, operating the leading B2B technology marketplace in emerging markets, capturing value from orchestrating a digital ecosystem rather than just moving boxes. Think TD SYNNEX meets AWS Marketplace with embedded fintech.

The realistic scenario: A $15B revenue company that successfully managed the transition to hybrid distribution-services-platform model, growing mid-single-digits with improving margins, generating healthy cash flows, and maintaining relevance through continued adaptation to technology waves.

The pessimistic scenario: A $10B revenue company struggling with margin pressure as e-commerce and direct models erode traditional distribution, services pivot incomplete, platform ambitions unrealized, relegated to commodity distribution of shrinking hardware categories.

Our bet: Closer to realistic with upside toward optimistic. Redington has demonstrated adaptability through multiple technology shifts. The organization understands its core competency—orchestrating complex B2B transactions in emerging markets—and is methodically building adjacent capabilities. That combination of self-awareness and execution suggests a company that will find its way forward, even if the path isn't perfectly straight.

XVII. Further Reading & Resources

For those wanting to dive deeper into Redington's story and the dynamics of technology distribution:

Primary Sources: 1. Redington Annual Reports (2010-2025) - Available at redingtongroup.com/financial-reports/. The MD&A sections track strategic evolution beautifully, especially the articulation of services pivot in 2018-2020 reports.

-

Investor Presentations and Analyst Calls - Quarterly earnings presentations at redingtongroup.com/investors provide management commentary on strategic priorities and segment performance.

-

CRISIL and ICRA Credit Ratings Reports - These assessments provide third-party evaluation of business risk profile, working capital management, and competitive positioning.

Industry Context: 4. "Distribution Revolution" by V. Kasturi Rangan (Harvard Business Review) - Academic framework for understanding channel dynamics and distribution economics.

-

IT Industry Analyses from NASSCOM and Gartner - For market sizing, growth projections, and technology trend analysis relevant to distribution.

-

"Digital India: Technology to Transform a Connected Nation" - McKinsey Global Institute report providing macro context on India's digital transformation.

Comparative Analysis: 7. TD SYNNEX and Ingram Micro Annual Reports - For benchmarking against global distribution peers. Ingram's 2024 annual report particularly useful for understanding industry-wide platform transformation.

- "Supply Chain Management in Emerging Markets" - Research by Hau Lee (Stanford) on unique challenges of distribution in developing economies.

Financial Deep Dives: 9. Equity Research from Motilal Oswal, ICICI Securities, Kotak - Sell-side research provides detailed financial modeling, competitive positioning analysis, and valuation frameworks.

- Working Capital Management Case Studies - Harvard Business School and Darden cases on distribution companies illustrate cash conversion cycle dynamics.

Bonus Materials: - R. Srinivasan Interviews - Founder's reflections on building distribution networks across emerging markets (various business publications 2010-2018). - Case Studies on Emerging Market Expansion - Academic papers analyzing how companies successfully scale across developing markets with infrastructure constraints. - "Platform Revolution" by Parker, Van Alstyne, Choudary - Framework for understanding transition from linear to platform business models, relevant to Redington's transformation ambitions. - Industry Reports on Cloud Distribution - Gartner and Forrester research on evolution of software and cloud distribution models.

Final Word:

Redington doesn't make headlines. The company doesn't disrupt industries with breakthrough products or viral consumer apps. It does something harder and more valuable: It makes complex things work at scale across impossible geography, turning operational excellence into sustainable competitive advantage.

In an age celebrating software eating the world, Redington reminds us that someone still needs to orchestrate the physical and financial logistics making that software accessible to billions. Sometimes the most important companies are the ones you never hear about—the infrastructure enabling everything else.

That's the Redington story: Thirty-plus years of boring brilliance, turning distribution into an art form, building relationships that compound, and adapting to technology waves before they crash. Not glamorous. Just essential. And in its own way, extraordinary.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube