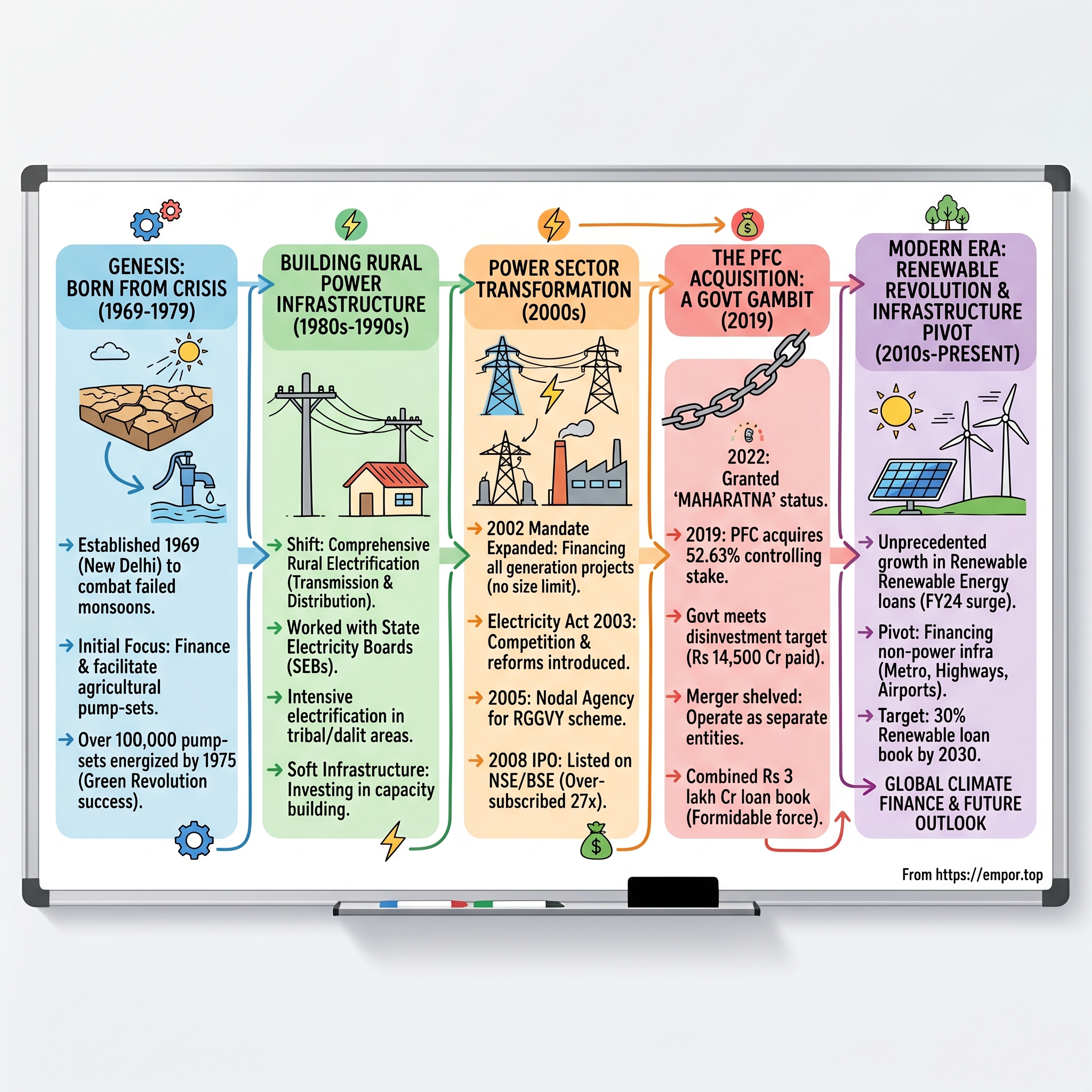

Genesis: Born from Crisis (1969-1979)

The late 1960s were India's years of reckoning. The euphoria of independence had given way to the harsh realities of nation-building, and nowhere was this more apparent than in agriculture. The Green Revolution was still finding its feet when nature delivered a cruel blow—three successive years of failed monsoons between 1965 and 1967 had pushed the country to the brink of famine. In villages across the heartland, farmers watched helplessly as their fields cracked under the relentless sun, knowing that salvation lay just meters below their feet—if only they had the means to reach it.

Rec Limited, a active public limited union government company, was established on 25 July 1969 in New Delhi, Delhi, India. The timing was no accident. Prime Minister Indira Gandhi's government, facing mounting criticism over food shortages and rural distress, needed a bold response. The answer came in the form of an audacious plan: energize agricultural pump-sets across the country to tap groundwater resources, thereby breaking agriculture's fatal dependence on erratic monsoons.

But creating REC was easier said than done in the License Raj era, where every government initiative required navigating a labyrinth of approvals, permits, and bureaucratic protocols. The initial mandate was deceptively simple yet enormously complex in execution: finance and facilitate the installation of electric pump-sets in rural areas. This meant not just providing money, but building an entire ecosystem—from convincing skeptical State Electricity Boards to cooperate, to training local technicians who could maintain equipment in remote villages where the nearest town might be a day's journey away.

The early team at REC, operating from a modest office in Delhi's government quarters, faced challenges that would seem almost quaint by today's standards. There were no computers to track loan disbursements, no satellite imagery to identify areas most in need of intervention, and certainly no sophisticated risk assessment models. What they had was a map of India, colored pins to mark electrified villages, and an unwavering belief that access to electricity could transform rural India.

By 1975, REC had financed the energization of over 100,000 pump-sets, but the real achievement lay in what these numbers represented. In village after village, the arrival of electricity meant farmers could irrigate their fields regardless of rainfall patterns. Productivity soared. In parts of Punjab and Haryana, wheat yields doubled within three years of pump-set installation. The Green Revolution, which might have withered without irrigation, instead flourished, turning India from a food-deficit nation to one approaching self-sufficiency.

The institutional capabilities REC built during these formative years would prove invaluable. They developed a unique model of working with State Electricity Boards—part financier, part technical advisor, part mediator between state and central governments. This wasn't just about writing checks; REC officials would spend weeks in the field, understanding local conditions, negotiating with village councils, and sometimes even mediating disputes over pump-set allocations.

One particularly telling episode from 1977 illustrates REC's evolving role. In a cluster of villages in Maharashtra's Vidarbha region, a REC team discovered that newly installed pump-sets were lying idle. The reason? Local farmers didn't know how to operate them and were afraid of electrical equipment. REC's response was characteristic of its approach—they didn't just send instruction manuals. Instead, they organized training camps, bringing in agricultural extension workers and successful farmers from neighboring districts to demonstrate the equipment. Within months, the same villages were showcasing productivity gains that attracted delegations from across the state.

For Efficient implementation of projects, REC emphasizes on man power development so a training institute named RECIPMT is established at Hyderabad. This focus on capacity building would become a hallmark of REC's operations, distinguishing it from conventional financial institutions that saw their role ending with loan disbursement.

As the 1970s drew to a close, REC had established itself as more than just another government corporation. It had become an essential piece of India's agricultural transformation puzzle, proving that targeted infrastructure investment could deliver both economic returns and social impact. The organization's loan book had grown from virtually nothing to over ₹500 crore, but more importantly, it had created a template for development finance that combined commercial viability with public purpose. Little did anyone know that the next decade would test this model in ways no one had anticipated, as India's power sector stood on the brink of fundamental transformation.

Building India's Rural Power Infrastructure (1980s-1990s)

The summer of 1982 brought an unusual visitor to the villages of eastern Uttar Pradesh. R. V. Shahi, then a senior official at REC, had eschewed the comfort of his Delhi office to spend three weeks traveling through some of India's most impoverished districts. What he witnessed would fundamentally reshape REC's mission. In village after village, he saw the same pattern: pump-sets humming during the day to irrigate fields, while families huddled around kerosene lamps after sunset. The infrastructure for power was tantalizingly close, yet household electrification remained a distant dream.

This disconnect between agricultural and domestic electrification revealed a critical gap in India's development strategy. Till 2000, REC focused on the Transmission and Distribution aspect of power, with projects for household electrification in rural and semi-urban areas, area electrification in tribal/ dalit areas, intensive el[ectrification]. The organization began to reimagine itself not just as a financier of pump-sets, but as the architect of comprehensive rural electrification.

Working with State Electricity Boards (SEBs) during this period was like navigating a minefield blindfolded. Each state had its own political dynamics, technical standards, and financial constraints. Tamil Nadu's electricity board operated differently from Bihar's, and what worked in Kerala would fail spectacularly in Rajasthan. REC had to become a chameleon, adapting its approach to each state's unique circumstances while maintaining uniform lending standards—a balancing act that required equal parts diplomacy and determination.

The politics of power in 1980s India were as complex as they were contentious. Electricity was—and remains—a concurrent subject under the Indian Constitution, meaning both state and central governments had jurisdiction. This created a web of competing interests. State politicians wanted free or subsidized power for farmers (a powerful vote bank), while SEBs needed cost-recovery to remain viable. The central government pushed for efficiency and reform, while state governments resisted changes that might upset electoral calculations. REC found itself in the middle of this tug-of-war, trying to finance projects that were technically sound, financially viable, and politically acceptable.

One breakthrough came through REC's innovative "soft infrastructure" approach. Rather than just financing hardware—transformers, transmission lines, distribution networks—the organization began investing heavily in capacity building. REC-funded training programs turned village youth into linemen and technicians, creating local employment while ensuring sustainable maintenance of electrical infrastructure. By 1987, REC had trained over 15,000 technical personnel across 15 states, creating a decentralized workforce that could respond to local needs without waiting for experts from state capitals.

The technical assistance REC provided went beyond training. The organization pioneered the concept of "shadow pricing" for rural electricity projects, developing methodologies to capture benefits that didn't show up in conventional financial analysis—improved health outcomes from refrigerated vaccines, educational gains from children studying under electric lights, productivity increases from small-scale industries. These frameworks would later influence how international development banks evaluated infrastructure projects in developing countries.

Then came 1991, and with it, India's economic liberalization. Liberalisation by the Government of India (GoI) in 1991 saw introduction of amendments to existing laws and reform measures enabling the private sector to participate in large-scale in manufacturing industry, services industry and infrastructure. For REC, this meant a fundamental shift in its operating environment. Suddenly, private players could enter the power sector—a domain that had been exclusively government territory since independence.

The organization's response to liberalization showcased its adaptability. Instead of viewing private sector participation as a threat, REC repositioned itself as a bridge between public and private interests. It began developing new financial products tailored for private developers while maintaining its commitment to rural electrification. This dual approach allowed REC to expand its portfolio while staying true to its social mandate.

A pivotal moment came in 1994 when REC financed its first private sector rural electrification project in Karnataka. The project was modest—electrifying 50 villages through a private contractor—but it proved that private participation could work in rural areas if properly structured and monitored. The success of this pilot led to a wave of similar initiatives, with REC acting as both financier and quality controller.

The monitoring systems REC developed during this period were revolutionary for their time. Long before "big data" became a buzzword, REC was collecting and analyzing vast amounts of information on rural electrification patterns. Every project was tracked through multiple parameters—not just financial metrics, but social indicators like the number of schools electrified, health centers powered, and cottage industries enabled. This data-driven approach helped REC make a compelling case for continued investment in rural infrastructure, even as India's economic priorities shifted toward urban and industrial development.

By the mid-1990s, REC's portfolio had evolved dramatically from its pump-set origins. The organization was financing everything from high-voltage transmission lines connecting remote areas to mini-hydel projects providing localized power generation. REC also started extending loans to manufacturers of T&D equipment. Till 2000, REC focused on the Transmission and Distribution aspect of power, with projects for household electrification in rural and semi-urban areas.

The human stories behind these statistics were compelling. In a tribal hamlet in Odisha, REC-financed electrification enabled a small cooperative of women to start a food processing unit, turning seasonal surplus into year-round income. In Rajasthan's desert districts, electric power allowed farmers to experiment with drip irrigation, growing water-intensive crops in areas that had never seen anything but millet and pulses. These success stories weren't just about electricity; they were about transformation—economic, social, and psychological.

As the millennium approached, REC had established itself as India's premier rural power finance institution, with a loan portfolio exceeding ₹10,000 crore and a presence in every state. But the biggest transformation was yet to come, as India prepared to restructure its entire power sector through landmark legislation that would redefine REC's role in the 21st century.

The Power Sector Transformation (2000s)

The millennium opened with rolling blackouts in Bangalore, India's IT capital, threatening to derail the country's software boom before it could properly begin. Tech companies were installing diesel generators by the dozen, a Band-Aid solution that symbolized everything wrong with India's power sector. It was against this crisis that REC would undergo its most dramatic transformation yet, evolving from a rural electrification agency into a comprehensive power sector financier.

In June 2002, the REC's mandate was expanded to financing all generation projects without limit on size or location. This wasn't just a policy tweak—it was a fundamental reimagining of REC's role in India's energy landscape. Suddenly, the organization that had spent three decades focusing on rural pump-sets and village electrification could finance massive thermal power plants, hydroelectric projects, and emerging renewable energy installations.

The expansion coincided with the Electricity Act of 2003, arguably the most significant reform in India's power sector since independence. The Act unbundled the monolithic State Electricity Boards into separate generation, transmission, and distribution companies, introduced competition, and opened doors for private investment. For REC, this meant navigating an entirely new landscape where the old certainties no longer applied.

The challenges were immense. REC's traditional expertise lay in rural distribution projects—relatively small-ticket items with predictable risks. Now, they were being asked to evaluate 1,000 MW thermal power plants costing thousands of crores, with complex fuel supply agreements, environmental clearances, and power purchase contracts. The learning curve was steep, but REC approached it with characteristic thoroughness, bringing in external experts, partnering with international financial institutions, and building in-house capabilities that would rival any commercial bank.

A defining moment came in 2005 when REC has been appointed nodal agency by Ministry of Power for Government of India scheme Rajiv Gandhi Grameen Vidyutikaran Yojana. The scheme was ambitious beyond anything attempted before—complete rural electrification, not just of revenue villages but of hamlets, daanis, and tolas that didn't even appear on official maps. Under the scheme, a 90% capital subsidy is provided by Government of India for overall project cost. Cumulatively till FY10, works in 190,858 villages were completed with free connections to over 10 million impoverished households.

Managing RGGVY required REC to become more than a financial institution—it had to be a project manager, quality controller, and social mediator rolled into one. The organization developed an elaborate monitoring system, tracking everything from transformer installations to household connections in real-time. Field officers would upload progress reports from remote locations using early mobile data technology, creating one of India's first large-scale digital governance initiatives.

But it was the 2008 IPO that truly marked REC's coming of age. The company was listed on the National Stock Exchange and the Bombay Stock Exchange on 12 March 2008. REC went for Initial Public Offer of 156,120,000 equity shares in February 2008 which was oversubscribed by about 27 times, raising a total amount of ₹819 crore. The overwhelming response—from institutional investors and retail participants alike—validated REC's transformation from a government agency to a commercially viable financial institution.

The IPO roadshow itself was a study in contrasts. REC executives found themselves explaining to fund managers in Mumbai's gleaming towers how financing a distribution transformer in rural Bihar could generate returns comparable to any infrastructure investment. They spoke about India's power deficit not as a problem but as an opportunity—every megawatt of capacity added, every village electrified, represented potential revenue for decades to come.

The listing also brought new disciplines. As a public company, REC now had to balance its developmental mandate with shareholder expectations. Quarterly earnings calls became platforms to showcase how commercial success and social impact weren't mutually exclusive but mutually reinforcing. The market responded positively—REC's stock price doubled within 18 months of listing, even as the global financial crisis ravaged other sectors.

During this period, REC also began its quiet revolution in renewable energy financing. While the sector was still nascent in India, REC was already funding small hydro projects in Himachal Pradesh, wind farms in Tamil Nadu, and biomass plants in Punjab. These early investments, considered risky at the time, would position REC perfectly for the renewable energy boom that would follow.

The human dimension of REC's transformation during the 2000s often gets lost in financial metrics. Consider the story of Shyam Sunder, a REC project officer who spent 2007 documenting electrification in Chhattisgarh's Naxal-affected areas. His reports, written sometimes by candlelight in villages where development workers were viewed with suspicion, captured not just technical specifications but the social dynamics of bringing power to India's most marginalized communities. His observation that "electricity is not just about lighting bulbs, it's about lighting aspirations" became an informal motto within REC.

The organization's work in these challenging areas demonstrated that infrastructure development couldn't be separated from social development. REC began incorporating security costs into project estimates, working with local communities to ensure buy-in, and sometimes even facilitating dialogue between different stakeholders. This approach—patient, inclusive, and sensitive to local contexts—helped REC succeed where purely commercial entities might have failed.

Technology adoption during this decade transformed REC's operations. The organization implemented one of India's first enterprise resource planning systems for a financial institution, digitized its loan processing, and created online platforms for borrowers to track their applications. This digital infrastructure would prove invaluable during the next phase of REC's evolution, as India's power sector faced its biggest disruption yet—the aggressive entry of a sister organization that would attempt to swallow REC whole.

The PFC Acquisition: A Government Gambit (2019)

March 28, 2019, dawned like any other day at REC's headquarters in Gurugram, but by noon, the organization's five-decade journey as an independent entity had effectively ended. State-owned Power Finance Corporation (PFC) on Thursday completed the acquisition of majority stake in REC Ltd by transferring Rs 14,500 crore to the government, an official said. The transaction has helped the government meet its disinvestment target of Rs 80,000 crore for the current financial year. "The entire consideration of Rs 14,500 crore for acquiring 52.63 per cent equity of the Government of India in REC is paid by PFC through RTGS (real-time gross settlement) mode this morning," the official told PTI.

The acquisition was a masterclass in financial engineering—or financial jugglery, depending on whom you asked. The government, desperate to meet its disinvestment targets as the fiscal year drew to a close, had orchestrated a transaction where one state-owned company bought another using borrowed money that would ultimately be guaranteed by the same government. It was like moving money from your left pocket to your right and calling it income.

Behind the scenes, the deal had been months in the making. Finance Ministry officials had been burning the midnight oil since December 2018, when the Cabinet Committee on Economic Affairs gave its in-principle approval. The challenge was structuring a transaction that would satisfy multiple stakeholders: the government needed its disinvestment proceeds, PFC needed to ensure the acquisition made commercial sense, and REC's minority shareholders needed protection of their interests.

PFC bought REC shares at Rs 139.50 per piece with total acquisition cost of about Rs 14,500 crore. The price—a discount to REC's then-market value—raised eyebrows among institutional investors. Some saw it as the government prioritizing fiscal targets over fair value; others viewed it as a reasonable premium considering PFC was acquiring control.

The financing of the deal was equally controversial. PFC has raised money from Bank of Baroda, Life Insurance Corporation and State Bank of India, among others, to make the payment, the source added. Essentially, state-owned banks were lending to a state-owned company to buy another state-owned company, with the proceeds going to the government that owned all of them. Critics called it financial incest; supporters argued it was efficient capital allocation within the public sector.

For REC employees, the acquisition triggered a mix of anxiety and anger. Two organizations with similar mandates but different cultures were being forced together. PFC, established in 1986, had always been seen as the urbane cousin—focusing on large generation projects and transmission infrastructure. REC, with its rural roots and grassroots orientation, feared its unique identity would be subsumed. Water cooler conversations revolved around who would retain their positions, whose policies would prevail, and whether REC's development mandate would survive the merger.

The market's reaction was swift and negative. Both stocks tumbled on the announcement, with investors worried about integration challenges, overlapping portfolios, and the debt burden PFC was taking on. Analysts questioned the strategic rationale—what synergies could be achieved by combining two organizations that essentially did the same thing? The government's response, that consolidation would create a larger, more efficient entity, rang hollow to many.

On 20 March 2019, PFC agreed to acquire a 52.63% controlling stake in REC for ₹14,500 crore (US$1.7 billion). On 28 March, PFC announced it had paid for the acquisition and intended to merge with REC in 2020. However, REC has maintained that merging PFC-REC is no longer an option. The planned merger hit regulatory roadblocks almost immediately. The Reserve Bank of India's regulations on lending exposure meant a combined entity would breach single-borrower limits for several state power utilities. Moreover, combining two systemically important financial institutions raised concerns about concentration risk in power sector lending.

The human drama played out in parallel to the financial maneuvering. At REC's Hyderabad training institute, instructors wondered whether their meticulously developed rural electrification curricula would survive. In field offices across India, REC officers who had spent decades building relationships with state utilities suddenly found themselves reporting to new bosses who didn't understand local dynamics.

One particularly poignant moment came during the first joint management meeting post-acquisition. A veteran REC officer, presenting on rural electrification challenges in the Northeast, was interrupted by a PFC executive questioning the commercial viability of such projects. The REC officer's response—"We measure success not just in IRR but in homes illuminated"—captured the cultural chasm between the organizations.

Despite the challenges, some positive signs emerged. The combined entity's lending capacity increased dramatically, allowing them to take on larger infrastructure projects. The Rs 3 lakh crore combined loan book made them a formidable force in power sector financing. International rating agencies maintained their ratings, suggesting confidence in the combined entity's creditworthiness.

The political dimensions of the acquisition were hard to ignore. This was the second major transaction where the government used one PSU to buy another—after ONGC's acquisition of HPCL—to meet disinvestment targets. Critics argued this defeated the purpose of disinvestment, which was supposed to reduce government ownership and bring in private efficiency. The government countered that consolidation within the public sector was a precursor to eventual privatization, though few believed this narrative.

For minority shareholders in both companies, the acquisition created a complex situation. They now owned stakes in entities where the principal shareholder (PFC in REC's case) had its own minority shareholders, creating nested ownership structures that complicated governance. Proxy advisory firms raised concerns about related-party transactions and potential conflicts of interest.

As 2019 drew to a close, the planned merger was quietly shelved. The organizations would remain separate entities, with PFC as REC's majority owner—a structure that persists to this day. This outcome, while suboptimal from an efficiency standpoint, perhaps preserved something valuable: REC's unique identity and its special focus on rural and renewable energy, which would prove prescient as India embarked on its ambitious energy transition in the following years.

Modern Era: Renewable Revolution & Infrastructure Pivot (2010s-Present)

The morning of September 22, 2022, marked a watershed moment in REC's corporate evolution. The Department of Department of Public Enterprises, under the Ministry of Finance has issued an order on 22 September 2022, granting the status of a 'Maharatna' Central Public Sector Enterprise (CPSE) to the Rural Electrification Corporation (REC). REC is the 12th CPSE to be granted Maharatna status. The elevation wasn't just ceremonial—it represented a fundamental shift in REC's autonomy and ambition, granting it powers to make equity investments up to ₹5,000 crore without government approval.

The Maharatna status arrived at an inflection point in India's energy transition. For the fiscal year 2023-24, REC Limited sanctioned loans amounting to ₹3.588 lakh crore, marking a significant increase of 33.66% from the previous year's ₹2.688 lakh crore. A notable part of this growth is the remarkable surge in sanctions for renewable energy projects, which saw an unprecedented rise of 538.79%, from ₹21,371 crore in FY 2022-23 to ₹1,36,516 crore in FY 2023-24. This wasn't just growth—it was a metamorphosis.

The transformation was driven by a new generation of leadership that understood renewable energy not as an obligation but as an opportunity. In boardrooms across Gurugram, REC executives were rewriting lending playbooks developed over decades for thermal power. Solar projects had different risk profiles than coal plants—lower operating costs but higher weather dependence, minimal fuel risk but technology obsolescence concerns. Wind farms required understanding capacity utilization factors and power curves. Battery storage projects demanded evaluation frameworks that didn't yet exist in India.

REC has expanded its mandate to include financing power generation, transmission, and distribution projects, as well as renewable energy projects – with an aim to grow its renewable loan book portfolio of 9% to 30% by the end of 2030. This ambitious target meant REC needed to finance nearly ₹3 lakh crore in renewable projects over the decade—more than its entire loan book just a few years earlier.

The organization's green bond issuances became a barometer of India's renewable ambitions. In April 2024, REC Limited secures a pioneering SACE-covered green loan for JPY 60.536 billion, marking a milestone in sustainable finance for India's power sector and bolstering Indo-Italian green energy collaboration. The facility also marks SACE's first JPY-denominated loan transaction and first green loan transaction in India. The transaction's complexity—involving banks from Asia, USA, and Europe—demonstrated REC's evolution into a sophisticated global borrower.

But the real revolution was happening in the field. In Rajasthan's Bhadla Solar Park, one of the world's largest solar installations, REC's financing enabled a project that would have seemed like science fiction just a decade earlier—2,245 MW of solar capacity spread across 14,000 acres of desert, generating electricity at rates cheaper than coal. The park became a pilgrimage site for energy professionals worldwide, showcasing what was possible when financial innovation met technological advancement.

The infrastructure pivot added another dimension to REC's evolution. In 2022–23, REC expanded the business portfolio with lending to the non-power infrastructure and logistics sector, including roads/highways, airports, metro rail networks, healthcare infrastructure and ports. This wasn't mission creep—it was strategic expansion into sectors where REC's project finance expertise could create value while diversifying risk.

Consider REC's financing of the Mumbai Metro Line 3, its first major urban transport project. The ₹2,500 crore commitment required REC to develop entirely new competencies—understanding ridership projections, evaluating real estate development rights, assessing integration with existing transport networks. The learning curve was steep, but REC approached it with the same methodical intensity that had characterized its rural electrification efforts decades earlier.

The digital transformation of India's power sector created new opportunities and challenges. REC found itself financing smart meter deployments, grid modernization projects, and SCADA systems—technologies that promised to revolutionize power distribution but required new frameworks for evaluation and monitoring. The organization's lending for electric vehicle charging infrastructure opened another frontier, positioning REC at the intersection of transportation and energy transitions.

REC Limited, a maharatna CPSE under the Ministry of Power and a leading NBFC, has disbursed loans worth ₹90,955 crore, up 20.10% year-on-year for the half year ended September 30, 2024. The quantum of renewable energy loans grew 92.68% year-on-year to ₹11,297 crore. These numbers reflected not just growth but transformation—from a thermal-heavy portfolio to one increasingly dominated by clean energy.

The international dimension of REC's operations expanded dramatically. Beyond traditional foreign currency borrowings, REC began participating in global climate finance initiatives. The organization's involvement in financing green hydrogen projects in Oman signaled ambitions beyond India's borders, positioning REC as a potential player in the global energy transition.

Technology adoption accelerated through the decade. REC implemented artificial intelligence models for credit risk assessment, blockchain pilots for renewable energy certificate trading, and satellite imagery analysis for project monitoring. The organization that once tracked projects with colored pins on physical maps now used machine learning algorithms to predict loan defaults and optimize portfolio allocation.

The human element remained central to REC's evolution. A new generation of employees, many with international education and private sector experience, brought fresh perspectives while respecting institutional wisdom. The cultural synthesis wasn't always smooth—veterans who had spent careers financing coal plants sometimes struggled to embrace solar projects with enthusiastic conviction—but gradually, a new organizational identity emerged that honored the past while embracing the future.

The renewable revolution also brought unexpected challenges. Unlike thermal plants with predictable generation patterns, renewable projects introduced intermittency risks. REC had to develop new products—like financing for battery storage systems and hybrid renewable projects—to address grid stability concerns. The organization's loan book, now exceeding ₹5.66 lakh crore, had become a complex portfolio requiring sophisticated risk management tools that would have been unimaginable in its early days.

As India accelerated toward its ambitious target of 500 GW of renewable capacity by 2030, REC positioned itself as the financial backbone of this transition. REC Ltd, in a release, said that it has undertaken a non-binding financial commitment of increasing its renewable energy (RE) loan book to over Rs.3 lakh crore (Rs.3 trillion), by 2030. This commitment—equivalent to financing roughly 100 GW of renewable capacity—would make REC one of the world's largest clean energy financiers, a remarkable evolution for an organization born to finance diesel pump-sets during a drought.

Government Schemes & Nation Building

The scorching summer of 2017 found Power Minister Piyush Goyal making an audacious promise from the ramparts of the Red Fort: every Indian household would have electricity by December 2018. In a country where 40 million households still lived in darkness, it seemed like political hyperbole. Yet behind this ambitious declaration lay meticulous planning, and at its heart was REC, appointed as the nodal agency for what would become one of the world's largest electrification drives—the Pradhan Mantri Sahaj Bijli Har Ghar Yojana, or Saubhagya.

The REC is the nodal agency under the SAUBHAGYA Yojana. The scheme's scale was staggering: electrify 40 million households in 18 months, roughly equivalent to providing power to the entire population of Spain. REC's role went far beyond cutting checks. The organization had to create an entire ecosystem—from developing a mobile app for real-time progress tracking to training thousands of field workers who would install connections in remote hamlets.

The Saubhagya war room at REC's headquarters became the nerve center of India's electrification push. Giant screens displayed real-time data from 29 states—households electrified, transformers installed, cable laid. Every evening at 6 PM, a video conference connected field officers from Arunachal Pradesh to Gujarat, troubleshooting problems that ranged from militant insurgency in the Northeast to leopard attacks on line workers in Madhya Pradesh.

The human stories behind Saubhagya's statistics were profound. In a tribal village in Odisha's Kandhamal district, the arrival of electricity meant children could study after sunset for the first time. The village's first engineering graduate, who emerged three years later, credited that light bulb with changing her life's trajectory. In Bihar's Musahari community—traditionally rat catchers living on society's margins—electricity became a symbol of inclusion, of finally being counted as citizens worthy of development.

But REC's role as a nodal agency involved navigating complex political dynamics. State governments, regardless of party affiliation, wanted to claim credit for electrification. Opposition-ruled states suspected the central scheme of having political motives. REC had to maintain strict neutrality while ensuring implementation speed, often mediating between warring political factions to keep projects on track. The organization's officers became skilled diplomats, speaking the language of development while carefully avoiding political landmines.

In the past, REC has been associated as nodal agency for Pradhan Mantri Sahaj Bijli Har Ghar Yojana (SAUBHAGAYA), Deen Dayal Upadhaya Gram Jyoti Yojana (DDUGJY) and National Electricity Fund (NEF) Scheme. These schemes resulted in strengthening of last mile distribution system, 100% village electrification and household electrification in the country.

The DDUGJY scheme, which preceded Saubhagya, had focused on strengthening rural distribution infrastructure. REC's implementation revealed the gap between electrification on paper and in reality. Many villages deemed "electrified" had power in name only—a single bulb at the panchayat office qualifying entire settlements as covered. REC's field surveys, often conducted at considerable personal risk in Naxal-affected areas, provided the ground truth that shaped subsequent policy.

The financial architecture of these schemes showcased REC's evolution from mere lender to development partner. The organization created innovative financing structures that aligned incentives—states received funds based on verified household connections, not just infrastructure creation. This outcome-based approach, revolutionary in India's subsidy-driven power sector, ensured that transformers didn't rust in warehouses while villages remained dark.

In addition, REC has been appointed as the National Program Implementing Agency for the 'PM Surya Ghar Muft Bijli Yojana', which aims to install rooftop solar systems on 10 million residential households by March 2027, targeting a total renewable energy capacity of 30GW. This latest responsibility represents REC's transition from rural electrification to distributed renewable energy, requiring entirely new capabilities in consumer financing and rooftop solar assessment.

The PM Surya Ghar scheme's implementation challenges differ markedly from grid electrification. REC must now evaluate individual household creditworthiness, assess rooftop structural integrity, and manage thousands of small installations rather than few large projects. The organization is developing artificial intelligence models to automate application processing, partnering with fintechs for digital lending, and creating virtual training programs for installation contractors.

The dual role—commercial lender and policy implementation arm—creates unique tensions. Market analysts question whether REC can maintain commercial discipline while executing government schemes that may not meet conventional lending criteria. The organization's response has been to segregate these roles organizationally while maintaining unified oversight. Scheme implementation follows government guidelines and receives budgetary support, while commercial lending adheres to market principles.

This balancing act plays out daily in REC's operations. A loan officer evaluating a private solar project in the morning might spend the afternoon reviewing Saubhagya implementation in the same district. The skills required—financial analysis for one, social mobilization for the other—are vastly different, yet REC's workforce has learned to switch between these modes seamlessly.

The impact of REC's scheme implementation extends beyond mere statistics. India's achievement of near-universal household electrification—from 67% in 2000 to 99.9% by 2021—represents one of the fastest expansions of electricity access in history. Currently, as a nodal agency for the Revamped Distribution Sector Scheme (RDSS), REC is contributing to improve health of DISCOMS by ensuring quality, accountability & reliability in power supply nationwide.

The RDSS, with its focus on distribution company viability, represents the next frontier. REC is financing smart meter deployments that will eliminate power theft, reduce commercial losses, and enable time-of-day pricing. The organization's role has evolved from building infrastructure to optimizing its operation—a transition that requires new competencies in data analytics, consumer behavior, and digital systems.

The smart meter rollout illustrates this evolution. REC isn't just financing hardware installation; it's helping utilities develop capabilities to analyze consumption patterns, predict demand, and optimize power procurement. In Uttar Pradesh, REC-financed smart meters have reduced commercial losses by 15% in pilot areas, generating savings that exceed the investment cost within two years.

The organization's work in implementing government schemes has created a vast repository of development experience. REC's databases contain granular information on every village's electrification status, household consumption patterns, and infrastructure quality. This data goldmine, properly analyzed, could revolutionize energy planning in India, moving from political promises to data-driven policy.

As India pivots toward renewable energy and electric mobility, REC's role in government schemes continues evolving. The organization is now preparing to implement schemes for electric bus deployment, green hydrogen production, and grid-scale battery storage. Each new responsibility adds layers of complexity but also opportunity—to shape India's energy transition while maintaining commercial viability. The challenge ahead isn't just financing infrastructure but reimagining what infrastructure means in a rapidly changing energy landscape.

Playbook: The Infrastructure Finance Model

Understanding REC's business model requires peeling back layers of financial engineering that would make Wall Street quantitative analysts pause. At its core, REC operates as a government-backed non-banking financial company (NBFC), but that description barely scratches the surface of an organization that has mastered the art of turning sovereign credibility into infrastructure reality.

Domestic debt instruments of REC have been assigned "AAA" by credit rating agencies CRISIL, Fitch and ICRA. Moody's and Fitch rated its international credit at par with India's sovereign rating. This sovereign-equivalent rating is REC's superpower—it can borrow at rates just marginally above government securities, then lend to infrastructure projects at spreads that generate healthy returns while remaining competitive.

The arithmetic seems simple: borrow at 7%, lend at 9%, pocket the 2% spread. But infrastructure finance is anything but simple. Power projects have gestation periods measured in years, not quarters. A thermal power plant might take five years to build and thirty years to repay its loan. REC must match these long-term assets with appropriate liabilities, a challenge that has humbled many financial institutions globally.

Consider REC's asset-liability management in practice. In 2023, the organization had outstanding borrowings of ₹4.2 lakh crore funding a loan book of ₹5.6 lakh crore. The maturity profile is carefully orchestrated—short-term commercial papers for working capital needs, medium-term bonds for under-construction projects, and long-term loans for operational assets. This temporal matching requires constant vigilance, as any mismatch could trigger a liquidity crisis.

The government backing provides a crucial safety net but comes with strings attached. REC must balance commercial objectives with developmental mandates, fund projects in backward areas that private lenders wouldn't touch, and implement government schemes that may not meet conventional risk-return parameters. This dual personality—part commercial bank, part development institution—defines REC's unique positioning in India's financial landscape.

Risk management at REC has evolved from simple credit evaluation to sophisticated portfolio optimization. The organization uses Monte Carlo simulations to stress-test its portfolio against various scenarios—what if monsoons fail and hydropower generation drops? What if coal prices spike and thermal plants become unviable? What if solar panel prices crash and existing projects face competition from newer, cheaper installations? Each scenario requires different hedging strategies, from interest rate swaps to partial credit guarantees.

The competitive dynamics with Power Finance Corporation, REC's parent company, create an unusual situation. Both organizations essentially compete for the same borrowers, yet they're part of the same corporate family. This has led to an informal division of territory—PFC focusing more on generation and transmission, REC on distribution and renewables—though boundaries remain fluid. State utilities play one against the other for better terms, a dynamic that would be problematic in pure commercial banking but serves a purpose in development finance by ensuring competitive pricing.

Commercial banks pose a different challenge. With their lower cost of funds (thanks to deposit access) and regulatory advantages, banks can cherry-pick the best projects, leaving REC with riskier propositions. REC's response has been to leverage its sector expertise—while banks might offer lower rates, REC provides technical assistance, helps navigate regulatory approvals, and continues support during distress periods when banks might withdraw.

The international dimension adds another layer of complexity. Foreign currency borrowings contribute 29% of the company's overall borrowings, 99% of which are hedged until maturity. This hedging is expensive but essential—a rupee depreciation without protection could wipe out years of profits. REC uses a combination of forward contracts, currency swaps, and natural hedges (lending in foreign currency to exporters) to manage this risk.

Capital allocation at REC follows a sophisticated framework that would be familiar to any private equity firm. Each project undergoes multiple levels of evaluation—technical feasibility, financial viability, environmental compliance, and social impact. The organization has developed proprietary models for different asset classes. A solar project in Rajasthan requires different metrics than a hydropower plant in Himachal Pradesh or a transmission line in Assam.

The balancing act between commercial returns and developmental goals plays out in every lending decision. A purely commercial approach might suggest focusing on large urban projects with strong counterparties. But REC's mandate requires funding rural distribution networks with uncertain revenue streams, renewable projects in remote locations, and infrastructure in states with weak financial positions. The organization has developed creative structures—viability gap funding, interest subvention during construction, partial risk guarantees—to make these projects bankable while protecting its balance sheet.

REC's treasury operations resemble those of a small central bank. On any given day, the treasury team might be issuing bonds in Tokyo, negotiating credit lines in Frankfurt, or managing liquidity in Mumbai. The organization maintains relationships with over 100 financial institutions globally, providing funding diversity that proved crucial during crises like the 2008 financial meltdown or the 2020 pandemic.

The digital transformation of REC's operations has introduced new efficiencies. Loan applications that once took months now clear in weeks through automated workflows. Machine learning algorithms flag potential defaults before they materialize. Blockchain pilots track renewable energy certificates. These technological investments, while expensive upfront, have reduced operating costs and improved risk management.

The human capital strategy is equally sophisticated. REC recruits from India's top engineering and business schools, competing with private banks and consultancies for talent. The organization offers something money can't buy—the opportunity to finance projects that transform millions of lives. This purpose-driven positioning helps REC attract professionals who might earn more elsewhere but find meaning in development finance.

Regulatory navigation requires constant attention. REC must comply with Reserve Bank of India regulations for NBFCs, Securities and Exchange Board of India rules for listed companies, and Power Ministry guidelines for sector-specific lending. Recent regulations on infrastructure investment trusts and renewable energy certificates have created new business opportunities while adding compliance complexity.

The organization's approach to distressed assets showcases its institutional maturity. When borrowers face difficulties—as many did during the coal shortage crisis or pandemic lockdowns—REC doesn't immediately invoke recovery proceedings. Instead, it works with borrowers on restructuring, provides bridge financing, and sometimes takes equity stakes to preserve value. This patient capital approach, possible only because of government backing, has helped REC maintain relatively low non-performing asset ratios despite operating in a stressed sector.

Looking ahead, REC's playbook must evolve for emerging challenges. The energy transition means thermal assets might become stranded. Distributed renewable generation could bypass traditional utilities. Electric vehicles might reshape power demand patterns. Each shift requires REC to reimagine its role—from financing large centralized infrastructure to enabling distributed, digital, and democratized energy systems. The organization that mastered the art of infrastructure finance in the 20th century must now reinvent itself for the realities of the 21st.

Analysis & Investment Case

The investment thesis for REC Limited reads like a paradox wrapped in a sovereign guarantee. Here's a company trading at a price-to-book ratio of just 1.2x, delivering return on equity of 18%, and paying dividend yields approaching 5%—metrics that would make value investors salivate. Yet the stock perpetually trades at a discount to private sector peers, a puzzle that reveals deeper truths about how markets value government-owned enterprises in emerging economies.

In Q2 FY24-25, REC disbursed loans amounting to Rs 47,303 crore, which is higher by 13.71% compared to Rs 41,598 crore disbursed in Q2 FY23-24. The growth trajectory appears robust, but raw numbers tell only part of the story. The composition of this growth—increasingly tilted toward renewable energy and infrastructure—represents a fundamental shift in risk profile that markets are still digesting.

The bull case for REC rests on three pillars, each compelling in isolation but powerful in combination. First, India's energy transition represents a $500 billion opportunity over the next decade. With 500 GW of renewable capacity targeted by 2030, the financing requirement exceeds ₹30 lakh crore. REC, with its established relationships, sector expertise, and government backing, is positioned to capture a significant share of this opportunity.

Second, the infrastructure boom extends beyond power. India plans to spend $1.4 trillion on infrastructure by 2025, encompassing everything from highways to hospitals. REC's expansion into these sectors, leveraging its project finance expertise, opens addressable markets that dwarf its current loan book. The organization's recent financing of metro projects, airports, and port facilities demonstrates this isn't just strategic intent but operational reality.

Third, the government backing provides a moat that private competitors cannot replicate. In 2021-22, REC made its highest-ever net profit of Rs 10,046 crore and reached a net worth of Rs 50,986 crore. In FY22, REC made its highest-ever net profit of Rs 10,046 crore and reached a net worth of Rs 50,986 crore. This profitability, achieved while maintaining developmental mandates, suggests the government backing enhances rather than constrains commercial performance.

But the bear case deserves equal attention. Asset quality remains the sword of Damocles hanging over REC's valuation. The power sector's stressed assets, while improving, haven't fully recovered. Distribution companies owe over ₹1 lakh crore to generators, creating cascade effects throughout the value chain. REC's gross NPA ratio of 4.5%, while manageable, could deteriorate if sector stress resurfaces.

Regulatory risks loom large. The Reserve Bank of India's tightening of NBFC regulations, while aimed at systemic stability, increases compliance costs and constrains lending flexibility. Recent proposals for infrastructure investment trusts could disintermediate traditional lenders like REC. The push for direct benefit transfer in subsidies might reduce REC's role in government scheme implementation.

Competition from private capital intensifies daily. International pension funds and sovereign wealth funds increasingly eye Indian infrastructure, willing to accept lower returns for long-term stable assets. Green bonds issued directly by renewable developers bypass intermediaries like REC. The emergence of specialized infrastructure funds creates alternatives for borrowers who previously had limited options.

The valuation puzzle reflects these contradictions. REC trades at roughly 8x price-to-earnings, compared to 15-20x for private sector banks with similar growth rates. The discount partially reflects government ownership—markets assume political interference, lending directed by policy rather than profit, and potential burden from unviable mandates. Yet this same government ownership provides stability that private entities lack.

Examining financial metrics reveals operational excellence obscured by ownership structure. Net interest margins have expanded from 3.2% to 3.8% over three years, impressive for an infrastructure lender. Operating costs remain below 0.3% of assets, among the lowest globally for development finance institutions. Credit costs have declined despite portfolio expansion, suggesting improved risk management.

As on 31.12.2024, REC had a Loan Book of ₹5,65,621 Cr with 88% loans to state sector. The Net Worth of the company stood at ₹76,502 Cr. This state sector concentration is both strength and weakness—providing stable asset quality but limiting growth potential as states face fiscal constraints.

The ESG angle adds complexity to the investment case. REC finances both coal plants and solar farms, supporting India's baseload power needs while enabling energy transition. International investors increasingly screen out fossil fuel exposure, potentially limiting foreign institutional investment. Yet India's energy reality requires both renewable growth and thermal stability, at least for the next decade, making REC's dual approach pragmatic if not pure.

Peer comparison illuminates REC's relative positioning. Against Power Finance Corporation, its parent, REC offers similar fundamentals at a slight discount. Compared to private infrastructure lenders like L&T Finance, REC provides lower growth but higher stability. International comparisons with Brazil's BNDES or South Africa's DBSA suggest REC trades at reasonable valuations for a sovereign-backed infrastructure lender.

The dividend story appeals to yield-seekers. REC has maintained dividend payout ratios above 30%, providing steady income in a volatile market. The government's dependence on dividend income from PSUs ensures continuation of generous payouts, barring severe stress. For investors seeking bond-like returns with equity upside, REC offers an attractive proposition.

Recent developments strengthen the investment narrative. The Maharatna status provides operational autonomy that could accelerate growth. The renewable energy pivot aligns with global capital flows toward sustainable investments. Smart meter financing and electric vehicle infrastructure open new revenue streams with attractive economics.

Yet questions persist. Can REC maintain asset quality as it expands into unfamiliar sectors? Will political pressure force uneconomic lending ahead of elections? How will the organization navigate the energy transition's creative destruction of traditional power assets? These uncertainties explain why REC trades at valuations that would trigger takeover bids in developed markets.

The investment decision ultimately depends on one's view of India's development trajectory. Believers in India's infrastructure buildout and energy transition might see REC as undervalued. Skeptics worried about government interference and sector stress might consider current valuations appropriate. The truth, as often in emerging markets, lies somewhere between these extremes—REC offers both opportunity and risk, with the balance shifting based on political cycles, policy changes, and sector dynamics.

For institutional investors, REC provides exposure to India's infrastructure story with sovereign comfort. For retail investors, it offers dividend income with growth potential. For the philosophically inclined, it poses a question: Can an organization simultaneously serve public purpose and private profit? REC's next decade will provide the answer, and investors betting either way are essentially taking a position on whether India can achieve development without sacrificing commercial discipline.

Epilogue & Future Outlook

As dawn breaks over the Pavagada Solar Park in Karnataka—one of the world's largest solar installations that REC helped finance—the 2,000 MW facility begins its daily conversion of sunlight into electricity, a sight that would have seemed fantastical to REC's founders who began their journey financing diesel pump-sets in drought-stricken villages. The transformation from those desperate origins to becoming India's renewable energy financing powerhouse encapsulates not just REC's evolution but India's entire development arc.

The $500 billion opportunity in renewable energy that lies ahead makes REC's journey so far seem like a prelude. India's commitment to achieving net-zero emissions by 2070 requires installing 40-50 GW of renewable capacity annually—equivalent to adding Switzerland's entire power system every year. This unprecedented scale demands not just capital but expertise in evaluating technologies that are evolving in real-time. Floating solar, offshore wind, green hydrogen—each presents unique challenges that REC must master while maintaining the financial discipline that has brought it this far.

The digital infrastructure revolution adds another dimension to REC's future. As India builds its stack of digital public goods—from UPI payments to Aadhaar authentication—the power infrastructure must evolve to support a digitized economy. Data centers, consuming enormous amounts of electricity, are sprouting across India. 5G towers need reliable power in remote locations. Electric vehicle charging networks require grid upgrades. REC finds itself financing not just electrons but the digital economy they enable.

New energy technologies present both opportunity and threat. Small modular nuclear reactors, still experimental but promising, could revolutionize baseload power. Grid-scale batteries might make traditional peaking plants obsolete. Blockchain-based peer-to-peer energy trading could bypass utilities entirely. REC must evaluate and potentially finance technologies that could disrupt its traditional borrowers—a delicate balance between enabling innovation and protecting existing investments.

What would different leadership do with REC? A private equity owner might strip out the developmental mandate, focus on profitable urban infrastructure, and maximize returns. A visionary entrepreneur might transform REC into a green investment bank, leveraging its sovereign backing to attract global climate finance. A technocrat might digitize operations entirely, using artificial intelligence to automate lending decisions and blockchain to track energy assets. Each path offers possibilities, but REC's reality requires balancing all these visions while serving its fundamental purpose—ensuring every Indian has access to reliable, affordable power.

The international dimension of REC's future cannot be ignored. As India emerges as a global power, its infrastructure finance model attracts attention from developing nations facing similar challenges. REC's expertise in rural electrification, renewable energy financing, and managing political economy complexities could be exported. Imagine REC advisors helping electrify villages in Africa, finance solar projects in Southeast Asia, or structure green bonds for Latin American utilities. The organization that learned by doing could teach by sharing.

Climate change adds urgency to every decision. The infrastructure REC finances today must withstand the weather of tomorrow—more intense cyclones, unprecedented floods, extended droughts. This requires incorporating climate resilience into project evaluation, financing adaptation alongside mitigation, and sometimes accepting that certain investments might become stranded as climate impacts accelerate. The organization's risk models, developed for a stable climate, need fundamental recalibration.

The human dimension of REC's future deserves attention. The organization must attract talent that combines financial acumen with engineering expertise and social consciousness. The next generation of REC leaders must be equally comfortable discussing collateralized loan obligations and kilowatt-hours, equally fluent in Sanskrit scriptures and Python programming. Building this workforce requires reimagining recruitment, training, and retention in an era when the best minds have unlimited options.

Key lessons from REC's journey resonate beyond India's borders. First, development finance can be commercially viable if structured properly—patient capital, government backing, and clear mandates create sustainable institutions. Second, infrastructure transformation requires more than money—it needs institutional capacity, technical expertise, and social legitimacy. Third, the supposed contradiction between public purpose and private profit often exists more in theory than practice—well-run development finance institutions can serve both masters.

For emerging markets worldwide, REC offers a template worth studying if not replicating. Countries struggling to finance infrastructure while maintaining fiscal discipline might find REC's model—leveraging sovereign credibility without burdening government budgets—particularly relevant. The organization's evolution from single-sector lender to comprehensive infrastructure financier provides lessons in institutional adaptation. Its balance between developmental mandates and commercial discipline offers insights into managing political economy challenges.

The measurement of success must evolve with REC's mission. Traditional metrics—loan book growth, net interest margins, return on equity—remain important but insufficient. How many tons of carbon emissions were avoided through renewable energy financing? How many hours of productive time were created through reliable electricity? How many enterprises were enabled through infrastructure investment? These impact metrics, harder to quantify but essential to capture, must complement financial indicators.

REC's next chapter will be written against the backdrop of global energy transition, technological disruption, and climate urgency. The organization must finance infrastructure for a future that's uncertain—will hydrogen replace natural gas? Will nuclear fusion become commercially viable? Will quantum computing revolutionize grid management? Each possibility requires different preparations, yet REC must act today based on incomplete information about tomorrow.

The philosophical question that has defined REC since 1969 remains relevant: What is the purpose of development finance? Is it to maximize economic returns, deliver social benefits, or enable national development? REC's answer—that these objectives are complementary rather than contradictory—will be tested as never before. The easy infrastructure has been built; what remains requires navigating complex tradeoffs between efficiency and equity, growth and sustainability, centralization and distribution.

As India stands on the cusp of becoming a developed nation, REC's role must evolve accordingly. The organization that brought light to villages must now illuminate pathways to sustainable prosperity. The institution that financed yesterday's infrastructure must enable tomorrow's innovations. The entity born from crisis must help prevent future catastrophes through resilient, sustainable development.

The story of REC Limited, from drought relief agency to infrastructure finance colossus, mirrors India's own transformation. Both journeys—marked by ambition, adaptation, and occasional adversity—remain unfinished. The next chapters, yet to be written, will determine whether the promise of sustainable prosperity becomes reality or remains perpetually just beyond reach. For REC, as for India, the future demands not just financial resources but imagination, courage, and unwavering commitment to the belief that infrastructure finance can be a force for transformative good.

The morning sun now fully illuminates Pavagada Solar Park, its panels converting photons into electrons that will power homes, hospitals, and hopes across Karnataka. Somewhere in corporate boardrooms and village panchayats, REC officers are evaluating the next project, the next technology, the next transformation. The journey from financing pump-sets to funding the future continues, one loan, one project, one transformed life at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube