Raymond Limited: The Complete Transformation of India's Suit King

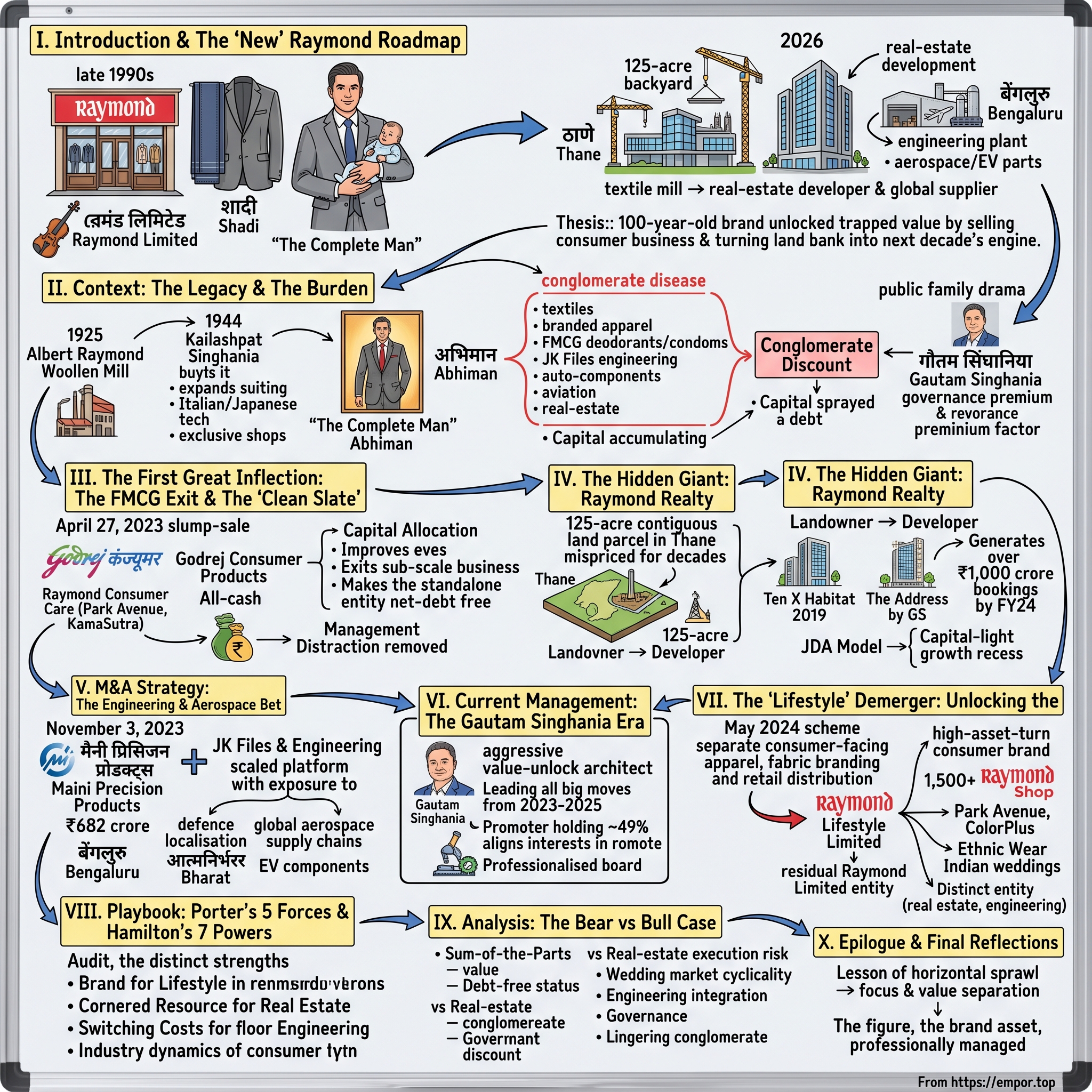

I. Introduction & The "New" Raymond Roadmap

Walk through almost any Indian neighbourhood market in the late 1990s and you would have found a familiar sight. A wood-and-glass storefront, lit a little too brightly, with mannequins standing at a polite, almost regimental, attention. A roll of bottle-green worsted fabric draped over a wooden display block. And, somewhere on the wall or in a small black television in the corner, a man in a sharp grey suit cradling his infant child, set to the soft hum of a violin. The man did not speak. The voiceover did the work: "The Complete Man."

For nearly two generations, that man, and that store, were रेमंड लिमिटेड Raymond Limited. A suit length from Raymond was the unspoken price of entering Indian adulthood, the gift fathers handed their sons before the first job interview, the bolt of fabric a future mother-in-law inspected before signing off on a शादी Shadi (wedding) trousseau. The brand was less a company and more a domestic ritual.

Fast-forward to 2026, and the company that owns "The Complete Man" looks almost nothing like the textile mill that built him. The flagship apparel business has been carved out into its own listed entity. The famous FMCG portfolio, with पार्क एवेन्यू Park Avenue deodorants and कामसूत्र KamaSutra condoms, has been sold. The remaining Raymond Limited entity is, of all things, a real-estate developer pouring concrete onto its own 125-acre backyard in ठाणे Thane, on the northern edge of Mumbai, while quietly assembling a global aerospace and electric-vehicle components supplier in बेंगलुरु Bengaluru.

The thesis of this episode is simple and a little jarring. A 100-year-old textile brand unlocked a previously trapped pool of value by, in effect, selling its public-facing soul, the consumer business that ran on television sets every evening, and by turning its dusty industrial land bank into the engine of its next decade. In the process, Raymond went from being the textbook "Indian conglomerate discount" stock to a three-pillar, debt-free holding structure where each pillar wants to be valued on its own terms.

The structure of this deep dive mirrors that pivot. We will start at the looms in Thane in 1925 and the long, slow accumulation of brand equity that made Raymond a household word. We will sit through the painful chapter where the market quietly stopped believing in the conglomerate. Then we will track, year by year, the three big bets that re-priced the company between 2023 and 2026: the गोदरेज Godrej FMCG sale, the Thane real-estate build-out, and the engineering acquisition that nobody on the street saw coming. We will end with a Hamilton Helmer-style power audit and the bull and bear cases that long-term investors have to actually choose between today.

This is the story of how India's most recognisable suit-maker quietly turned itself into something else entirely.

II. Context: The Legacy & The Burden

The Raymond story does not begin with a Singhania. It begins with a textile mill on the swampy industrial edge of Mumbai, set up in 1925 by a businessman named Albert Raymond and a group of local partners. For its first two decades, the Raymond Woollen Mill was an unremarkable operation, churning out coarse fabric for the British Indian Army and for a domestic market that, frankly, did not yet know it wanted worsted suiting.

The pivot came in 1944, when कैलाशपत सिंघानिया Kailashpat Singhania, the patriarch of a Kanpur-based industrial family with interests across cement, jute and chemicals, bought the mill. The Singhanias were not flashy industrialists. They were the kind of family that owned half a city block without anyone in the city knowing. What they recognised, almost immediately, was that post-Independence India would generate a new middle class that wanted to look like its colonial bosses had looked, but at Indian prices. A premium domestic suiting brand could ride that wave for fifty years.

It rode it for closer to seventy. Through the 1960s and 1970s, Raymond expanded its worsted suiting capacity, brought in Italian and Japanese technology, and built a network of exclusive franchised "The Raymond Shop" outlets that became the company's signature distribution moat. By the 1980s, under विजयपत सिंघानिया Vijaypat Singhania, the company was the dominant Indian player in premium fabric, with a vertically integrated wool and polyester-blend mill in Thane that was, for its time, one of the most modern textile facilities in Asia.

Then in 1990, the brand made the move that fixed it in the Indian cultural imagination. The agency Enterprise Nexus, working with Raymond, launched the now-iconic "The Complete Man" campaign, anchoring the brand not to the fabric itself but to a particular kind of Indian man: educated, professional, emotionally available, faintly Westernised but rooted in family. That was the अभिमान Abhiman (pride) currency of Raymond. You weren't buying cloth; you were buying a self-image that worked equally well at the office and at the family dinner table.

So why did the market quietly stop loving Raymond? Because somewhere between roughly 2005 and 2020, the company became a case study in the classic Indian conglomerate disease. The brand was extraordinary, but the balance sheet was tired. Raymond was simultaneously a textile manufacturer, a branded apparel retailer, an FMCG company selling deodorants and condoms, a tool-and-file maker via its JK Files engineering subsidiary, an auto-component supplier, an aviation business, and a real-estate landowner that wasn't really developing anything. Capital was sprayed across too many ideas. Debt accumulated. The market did what markets do with that profile: it slapped on a conglomerate discount and walked away.

There was also a deeply public family drama. The relationship between Vijaypat Singhania and his son गौतम सिंघानिया Gautam Singhania had broken down by the late 2010s in a way that played out in court and on the pages of every Indian business paper, with disputes over a Malabar Hill bungalow, a stake transfer, and the ownership of the family's most visible asset.[^7] Family-led Indian businesses survive a lot, but they rarely survive that kind of public airing without paying a governance premium to investors who suddenly need more comfort about who is actually steering the ship.

By the end of the 2010s, Raymond carried an iconic brand, an underutilised land bank, a complicated debt stack, a fractious family backdrop, and a market that simply did not know what story to tell about the company anymore. Something had to break. As it turned out, multiple things did, and the breaking was, for shareholders, the best thing that had happened in a generation.

III. The First Great Inflection: The FMCG Exit & The "Clean Slate"

On the morning of April 27, 2023, the press releases hit the wires in a flurry. गोदरेज कंज्यूमर प्रोडक्ट्स Godrej Consumer Products announced it had agreed to acquire Raymond Consumer Care, the subsidiary that housed the entire branded FMCG portfolio, in a slump-sale transaction valued at ₹2,825 crore.2[^8] The deal, structured as an all-cash purchase of the business undertaking, would hand Godrej one of India's most recognisable male grooming brands, Park Avenue, alongside KamaSutra in condoms and a basket of premium personal-care SKUs.2

It is hard to overstate how surprising this was to anyone who had grown up with Raymond. The FMCG business was, in many ways, the most consumer-visible part of the company. Park Avenue deodorant was a tier-one mass-market brand. KamaSutra had cleared a category that was deeply taboo in Indian advertising. These were the businesses you saw on TV. The worsted suiting business, by contrast, was the one that ran quietly through 1,500 storefronts and a B2B fabric channel.

So why sell what looked, from the outside, like the crown jewels? The answer is the answer to almost every Indian conglomerate puzzle: capital allocation. The FMCG business, while glamorous, was a sub-scale player going up against हिंदुस्तान यूनिलीवर Hindustan Unilever, आईटीसी ITC and Godrej itself. To remain competitive, it needed sustained ad-spend and constant innovation outlays, both of which Raymond's broader balance sheet could not generously fund without choking the other businesses. The exit multiple of roughly 3.5 times the unit's trailing sales was, in the context of small-cap Indian FMCG deals, broadly in line with what scale buyers had paid for similar assets, and meaningfully above what the market was implicitly assigning to the business when it sat inside the Raymond holding structure.[^8]

The strategic logic was even sharper than the multiple. Raymond was carrying gross consolidated debt that, going into FY23, had made it one of the more leveraged mid-cap names in Indian textiles.1 The cash from the Godrej transaction, combined with internal accruals, allowed Raymond to do something it had not done in years: declare itself effectively net-debt free at the standalone level.[^8] That single line item, "net cash positive," rewrote the entire equity story. A company that had been valued on EBITDA-minus-interest could now be valued on EBITDA plus optionality.

There is a second-order effect worth dwelling on. By spinning the FMCG business out cleanly, Raymond removed an enormous management distraction. Branded personal care is a brutally operational business: SKU proliferation, distributor margins, retailer slotting fees, monthly promotion calendars. It eats CEO time. Once Park Avenue and KamaSutra were Godrej's problem, Gautam Singhania's senior team could narrow the lens to fabric, apparel, real estate and engineering, four businesses that share much less day-to-day workflow than they look like they do, but which at least allow for cleaner functional leadership.[^7]

The market read it correctly. In the weeks following the Godrej announcement, the equity narrative around Raymond began to shift from "tired old textile holding" to "deleveraging story with embedded land bank optionality."[^10] That re-rating, which a year earlier would have sounded like sell-side wishful thinking, became the operating thesis. It also set the table for the next, even larger move: deciding what to actually do with the 125 acres of dirt sitting under the Thane factory.

IV. The Hidden Giant: Raymond Realty

If you stand at the edge of the old Raymond textile complex in Thane today and look northwest, you can see the past and the future of this company in a single frame. To one side, the still-running fabric mill that has been weaving worsted cloth since the 1940s. To the other, cranes, scaffolding, and the rising glass-and-aluminium skin of high-rise residential towers that did not exist five years ago. Walk a hundred metres in either direction and you cross between two entirely different companies, both stamped with the same lion-and-shield Raymond logo.

This is the asset that Wall Street and Dalal Street alike had been quietly mispricing for two decades: a contiguous 125-acre parcel of industrial land in Thane, an inner suburb of Mumbai whose property market in the 2020s exploded as the city's centre of gravity migrated northeast.4 In a real-estate market where developers in the Mumbai Metropolitan Region spent years and crores assembling fragmented plots of two or three acres at a time, Raymond owned an unbroken parcel large enough to be a small township. It had been carried on the books at heritage industrial valuations and treated, for most of the company's history, as an operational footprint rather than as inventory.

The intellectual leap, championed inside the company by Gautam Singhania and a senior leadership team brought in specifically for the realty push, was to refuse to sell that land to a developer. Instead, Raymond decided to become the developer. The first phase, branded "Ten X Habitat," went live in 2019 and tested the proposition that a Raymond-branded residential project, in a competitive Thane micro-market, could clinch premium pricing and inventory absorption.6 The market answer was yes.

By the launch of the next-generation project, "The Address by GS," the realty story had moved from experiment to engine.6 Raymond Realty stacked further phases at Thane and, importantly, began signing joint-development agreements (JDAs) outside its own land bank, including in Mumbai's western suburbs.4 The JDA model is worth understanding because it is the structural reason this business does not need a fresh land-acquisition cycle to grow. In a JDA, the landowner contributes the plot and the developer brings construction expertise, brand and execution capacity, with the resulting saleable area split between the two. For a brand like Raymond, with no legacy real-estate debt and a recognisable name, that is a near-perfect asymmetry: capital-light growth on someone else's dirt.

The segment financials moved fast. Raymond Realty went from a non-existent line item to a vertical with bookings that, by FY24, had crossed ₹1,000 crore in a single fiscal year, with EBITDA margins materially above what the rest of the Raymond group had historically generated in textiles or apparel.48 Inside the company, real estate quietly became the fastest-growing engine, while remaining structurally protected by the fact that the underlying Thane plot had been on the books for decades at a fraction of its present-day market value.4

What does that mean for an investor sitting in 2026? It means that for the first time in Raymond's history, the largest source of incremental enterprise value is not the brand on the storefront but the asset under the storefront. The realty pipeline, including the in-house Thane phases plus the growing JDA portfolio, gives the company a multi-year visibility of revenue that does not depend on whether Indian grooms continue to buy worsted suit lengths from "The Raymond Shop." It is the cleanest example in this story of how recognising a cornered resource, in Hamilton Helmer's vocabulary, can reset an entire equity narrative. With real estate finally being recognised as a primary engine and not a sleeping balance sheet entry, management's next question became where to deploy the operational and financial firepower freed up by the FMCG exit. The answer arrived, with deliberately strategic timing, seven months later.

V. M&A Strategy: The Engineering & Aerospace Bet

For most of its modern history, Raymond's engineering business lived in the shadow of the textile mill. The unit, organised under JK Files & Engineering and a couple of smaller auto-component subsidiaries, made hand tools, precision steel files, ring gears and starter motor components, the kind of products you find in industrial supply catalogues rather than glossy annual reports. It was profitable, in its own quiet way. It was also, frankly, not the reason anyone owned the stock.

That changed on November 3, 2023, when Raymond announced the acquisition of मैनी प्रिसिजन प्रोडक्ट्स Maini Precision Products for ₹682 crore.[^4]5 On paper, the headline was a mid-sized Indian engineering deal. In strategic terms, it was the moment Raymond declared, without quite saying so out loud, that it intended to build a global engineering platform on the back of its existing JK Files spine.

What does Maini actually do? Founded in बेंगलुरु Bengaluru, Maini Precision Products had spent more than a decade quietly entrenching itself as a tier-2 and tier-3 supplier into the global aerospace, hydraulics and powertrain supply chains.5 Its parts go into commercial aircraft hydraulics, industrial fluid power systems, and increasingly, electric-vehicle drivetrain components. These are not commodity machined parts. Aerospace-grade precision components carry multi-year qualification cycles, customer-specific tooling, and a regulatory paper trail that is, by design, a moat against new entrants.

The strategic logic for Raymond was to bolt Maini onto JK Files & Engineering to create a single, scaled engineering platform with exposure to three secular tailwinds: defence localisation under India's आत्मनिर्भर भारत Atmanirbhar Bharat (self-reliant India) procurement push, the global rebalancing of aerospace supply chains away from over-concentrated Western tier-2 vendors, and the early-cycle EV component opportunity. None of these are guaranteed winners on a five-year view. Collectively, they give the combined engineering business a believable claim to growing meaningfully faster than the underlying Indian industrial economy.

Did Raymond overpay? That is the harder question. At roughly ₹682 crore for a target with the revenue scale Maini disclosed at the time of the deal, the enterprise-value-to-sales and EV/EBITDA entry multiples landed in a range broadly comparable to where Indian precision engineering peers, such as भारत फोर्ज Bharat Forge and सोना बीएलडब्ल्यू Sona BLW, were trading on a forward basis at the time.5 That is not a bargain price. It is also not the kind of frothy multiple that suggests Raymond was forced to bid against itself. The honest reading is that this was a fair price for a high-quality asset in a structurally attractive niche, paid by a buyer with a clear plan to consolidate the operations behind it.

There is a softer, less spreadsheet-friendly part of this story that matters too. Engineering acquisitions, especially in aerospace, only create value if the operational integration is patient. Customer qualifications cannot be rushed. Existing program contracts cannot be re-tendered on a buyer's preferred timeline. The fact that Raymond signalled it would consolidate JK Files and Maini under a single engineering vertical, rather than fold Maini into the legacy textiles holding structure, suggests an awareness that this is a long-cycle operating business that needed its own management bandwidth.[^7]

Step back and the M&A move makes a particular kind of sense. With FMCG sold, real estate compounding on a captive land bank, and core fabric / apparel under cyclical pressure from competing formats, engineering was the one obvious place where the group could deploy fresh capital into a business with global pricing power and an underweighted Indian capital-markets multiple. The Maini acquisition was, in effect, Raymond purchasing optionality on the next decade of Indian export-led industrial growth, using cash freed up by a Mumbai-based personal-care divestment. That is the kind of trade only a chairman with a long enough rope from his board can make.

VI. Current Management: The Gautam Singhania Era

Walk into a Raymond annual general meeting in the 2020s and the man at the head of the table is unmistakable: dark sunglasses on more often than they need to be, race-team t-shirt under a blazer, and a slightly impatient energy that telegraphs that he would rather be on a track in Maharashtra than in a hotel ballroom in south Mumbai. Gautam Hari Singhania, born 1965, has been chairman and managing director of Raymond Limited since 2000, taking over from his father at the start of the new millennium and steering the group through almost every significant inflection described in this article.[^7]

Singhania did not arrive at the chairman's seat as a corporate textbook successor. He arrived as a self-styled industrialist-petrolhead, a motorsport sponsor and an Indian Racing League promoter on the side, with a public persona that has, at various points, been more interesting to lifestyle press than to sell-side analysts. That mattered, because in the Indian context the personal brand of a promoter and the corporate brand of the company are rarely cleanly separated. When the Singhania family disputes spilled into the public domain in the late 2010s and again in 2023, the questions investors asked were not just about the Singhania family bungalow. They were about whether the controlling shareholder's bandwidth was fully committed to the company.[^7]

The honest answer, from the operating record, is that Gautam Singhania has been the architect of the most aggressive value-unlock cycle in Raymond's history. The Godrej Consumer transaction, the Maini Precision acquisition, the standalone scaling of Raymond Realty, the lifestyle demerger, and the simultaneous professionalisation of the senior leadership bench did not happen by accident. They happened in a tightly compressed window between 2023 and 2025, and the through-line is a chairman willing to lop off the most consumer-visible part of the conglomerate (FMCG), separate the most emotionally-loaded part of the legacy (lifestyle apparel) into its own listed entity, and use the proceeds to seed engineering and concrete.2[^4]3

Promoter shareholding, as of recent disclosures, has remained in the 49% range, which is meaningful for two reasons.[^9] First, it gives the family enough alignment to behave as long-term owners rather than rotating professional managers; second, it leaves enough float that institutional investors can meaningfully build positions and exert quiet governance pressure. The pattern of recent board appointments and the formalisation of independent director-led committees has been part of a broader narrative that the Raymond board, post-2023, is closer to a "professional board with a promoter chair" than the "family-led" archetype it had been historically.7

The compensation and incentive question is the standard one for any Indian promoter-led structure, and the answer is straightforward: alignment runs primarily through the equity stake, not through option-heavy executive comp packages of the kind one sees in tech multinationals. For an investor, that is a feature, not a bug, provided the promoter's interests are well-aligned with public shareholders. The Lifestyle demerger is the test case here. By separating the consumer-facing apparel business into its own listed company, Raymond is forcing each vertical, lifestyle, real estate, engineering, to be measured on its own KPIs, with its own management team, and arguably its own dedicated equity story.3 Promoter holding gets mirrored across the demerged entities, which means the family wins or loses on each vertical's performance separately.

The piece of management style that is hardest to find in any annual report, but which a long-term investor needs to underwrite, is whether Gautam Singhania will continue to behave as a portfolio rationaliser rather than as an empire builder. The 2023–2025 cycle says yes. He has been a net seller of complexity and a net acquirer of focused exposure. The bear-case version of the same person says that the racing, the public family disputes, and the entrepreneurial restlessness could yet produce a distraction. Both readings are legitimate. What is no longer legitimate, after this transformation cycle, is to claim that the chairman has been passive.

VII. The "Lifestyle" Demerger: Unlocking the Brand

If the FMCG sale was Raymond pulling out a tooth, the lifestyle demerger was Raymond performing surgery on its own face. In May 2024, the company received regulatory clarification on its scheme of arrangement to demerge the Lifestyle Business, the apparel, fabric branding and retail distribution operations, into a separately listed entity to be known as Raymond Lifestyle Limited.3 In practical terms, the consumer-facing apparel company most Indians actually picture when they hear "Raymond" was being detached from the holding structure that owns the Thane land and the engineering subsidiaries.

The strategic motivation was painfully obvious once you said it out loud. The lifestyle apparel business is a high-asset-turn, low-capital-intensity consumer brand. The realty business is a long-cycle, lumpy revenue, balance-sheet-heavy developer. The engineering business is an export-oriented, long-qualification-cycle precision manufacturer. No reasonable equity investor was ever going to apply the same multiple to all three, and as long as they sat in one listed wrapper, the market was forced to. The demerger said, in effect: stop trying to value the whole thing on a textile multiple.

What does the standalone lifestyle entity actually look like? It is one of the largest worsted suiting fabric brands globally by volume, with a vertically integrated mill, a branded apparel portfolio that includes Raymond Ready-to-Wear, पार्क एवेन्यू Park Avenue apparel, कलरप्लस ColorPlus, and एथनिक वियर Ethnic Wear propositions targeting the Indian wedding occasion-wear category.1 It runs a franchised retail network of more than 1,500 stores, branded as The Raymond Shop, that reaches into tier-2 and tier-3 Indian towns in a way few competitors can match.1

The competitive frame for that business has changed dramatically. The dominant fashion competitors in India today are not other textile mills. They are scaled apparel platforms: आदित्य बिड़ला फैशन Aditya Birla Fashion and Retail with its multi-brand portfolio anchored by Allen Solly, Van Heusen, Louis Philippe and Peter England; रिलायंस ट्रेंड्स Reliance Trends and the broader Reliance Retail apparel footprint with its hypermarket-style scale and aggressive private label strategy; Trent's Westside and Zudio formats; and on the global side, Zara and H&M holding the premium and value-fashion ends of the urban mall format. Raymond Lifestyle, the standalone entity, is competing in a sector where shelf space and brand fatigue are real risks.

What Raymond brings to that fight is twofold. First, "The Complete Man" still works, just not for the same generation. The brand's lock on Indian wedding occasion-wear, both for the groom and increasingly for his extended family, is a structural advantage that mall-based competitors cannot easily replicate because it depends on local franchise relationships in cities that international chains do not deeply penetrate.1 Second, the ColorPlus and casual-wear sub-brands are the company's hedge against the secular shift from formal to casual, which is the single biggest threat to the legacy worsted suiting category. The pivot to ethnic and occasion wear, where the average ticket size is high and the emotional purchase context is captive, is the more interesting growth lever for the standalone lifestyle entity.

For investors, the lifestyle demerger meant something quite specific: the market would, for the first time in the company's history, have to assign an explicit multiple to the brand. No more hiding inside a conglomerate average. Whether that multiple landed closer to a textile manufacturer or to a consumer-brand peer would be one of the more interesting price discovery exercises in Indian mid-cap equities. The cleaner the standalone vertical, the easier it is to overlay tools like Porter's Five Forces and Hamilton Helmer's 7 Powers framework and ask the harder question: which of these three new Raymonds actually has durable competitive power, and which is just a good asset trapped in a difficult industry?

VIII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Apply Hamilton Helmer's 7 Powers framework to the post-transformation Raymond group and the diagnosis is interestingly uneven across the three verticals. That asymmetry is itself the investment story.

Start with Brand. Raymond's legacy worsted-suiting brand is one of the cleanest examples of a Helmer-style brand power in Indian textiles. Decades of "The Complete Man" advertising built a willingness-to-pay premium for cloth that is, in physical terms, broadly substitutable. That brand power is concentrated in the wedding occasion-wear segment, where the buyer (often a parent or relative) anchors on cultural trust rather than on yarn count or GSM. It is weaker in everyday casual wear, where Zara, H&M and Reliance Trends compete on fast-fashion cycles that Raymond's vertically integrated mill cannot economically match.

Move to Cornered Resource. The Thane land bank is the textbook case.4 Raymond owns roughly 125 contiguous acres in one of the fastest-appreciating residential micro-markets in the Mumbai Metropolitan Region. It cannot be replicated by any new entrant because the underlying land is non-fungible. Crucially, the cost basis of that land is decades old, which means the realty business prints gross margins that a developer assembling land at today's prices simply cannot match. This is also why the Joint Development Agreement model layered on top of the captive land is structurally interesting: capital-light growth on top of capital-cheap base.

Scale Economies is present but uneven. The 1,500-plus Raymond Shop franchised distribution network is meaningful scale in a country where retail penetration is fragmented, and it gives the lifestyle business a fixed-cost-to-revenue advantage in tier-2 and tier-3 cities that pure mall-based competitors cannot economically address.1 On the manufacturing side, Raymond's worsted mill in Thane is one of the largest of its kind globally, which gives the company some unit-cost advantage in B2B fabric, but textile manufacturing is a globally competitive industry where scale alone does not produce durable margin leadership.

Switching Costs are surprisingly relevant on the engineering side. Once Maini Precision and JK Files have qualified into a global aerospace OEM's bill of materials, that customer relationship is sticky for years because re-qualification of an alternate vendor is expensive and time-consuming.5 This is not the cheapest source of power, but it is among the most durable, which is why aerospace component businesses tend to trade on premium multiples globally.

The other three powers, Network Economies, Counter-Positioning, and Process Power, are largely absent here, which is honest framing. Raymond does not run a marketplace, it does not have a fundamentally cheaper-to-serve business model that incumbents structurally cannot copy, and while it does have process know-how in fabric and in precision machining, neither rises to the level of a defensible Process Power moat.

Now overlay Porter's Five Forces:

Bargaining power of buyers. In branded apparel and ready-to-wear, buyer power is high and rising, because Indian consumers can shop seamlessly across Raymond, Aditya Birla Fashion, Reliance Trends and global fast-fashion chains, with full price visibility online. In B2B fabric sold to garment manufacturers and corporate uniforms, buyer power is moderated by the limited number of suppliers who can deliver worsted suiting at scale, which is one of the few places Raymond's legacy heft still translates into pricing power.

Threat of substitutes. The single biggest substitute threat in Raymond's core lifestyle business is the cultural shift from formal to casual wear, particularly in the post-pandemic Indian workplace. ColorPlus and the company's broader ethnic-wear pivot are explicit responses to that substitution risk.1

Threat of new entrants. High in apparel retail, where the friction to launch a D2C brand has collapsed; meaningfully lower in vertically integrated worsted suiting manufacturing, where the capital intensity of a modern mill is a real barrier; very low in residential real estate development in Mumbai once you assume an existing land bank, which is exactly the dynamic Raymond Realty is exploiting in reverse.

Bargaining power of suppliers. Wool and synthetic fibre suppliers operate in globally traded commodity markets, which limits supplier leverage but exposes Raymond to input-price volatility. In engineering, supplier power is concentrated around specialty steels and aerospace-grade alloys, which is one of the operating risks of the Maini-integrated platform.

Industry rivalry. High in apparel, moderate in fabric, and intensely local in Thane real estate, where Raymond competes against a small set of large developers per micro-market rather than against a national field.

The clearest takeaway from this audit is that the three Raymonds do not share a single source of durable power. Lifestyle leans on brand, real estate leans on a cornered resource, and engineering leans on switching costs. That heterogeneity is precisely why the demerger and segment-level reporting matter so much: the parts are not just worth more separated than combined, they are also more analyzable separately than combined.

IX. Analysis: The Bear vs Bull Case

Let us start with the bull case, because it is, at this point, the consensus view on the street. The argument runs as follows. Raymond, after the FMCG exit, the Maini acquisition, and the lifestyle demerger, is no longer one company; it is three businesses sitting under a single promoter family with aligned incentives. The standalone realty business alone, fed by 125 acres of own-account Thane land plus a growing JDA pipeline, has a multi-year revenue visibility and gross margins materially above the rest of the group, which means on a Sum-of-the-Parts basis the realty vertical can plausibly justify a meaningful chunk of the entire group's enterprise value by itself.48 Add a debt-free balance sheet at the consolidated level after the Godrej proceeds were applied, layer on the lifestyle business with its 1,500-store franchised network and its grip on the wedding occasion-wear market, and finish with an engineering vertical that has bolted on Maini's aerospace and EV exposure into what was previously a sleepy file-and-tool unit.2[^4]5 The bull case is, fundamentally, that the conglomerate discount has finally been broken and that the new equity story is structurally cleaner than at any point in the company's modern history.

The Hamilton Helmer-style framing supports this. Multiple sources of competitive power, distributed across three distinct verticals, with a promoter who has demonstrated, in real time and with hard cash, that he is willing to sell complexity and buy focus. For long-term fundamental investors looking for an Indian industrial story that has already done the painful balance-sheet repair work, that is the kind of profile that is hard to find.

Now the bear case, which deserves an equal and honest hearing.

First, real-estate execution risk. Raymond Realty's growth thesis depends on continuing to deliver projects on time, at margin, and into a residential market that has been historically cyclical. The Indian residential market in 2026 sits at a relatively benign point in its cycle, but the operating leverage of a developer cuts both ways, and any extended slowdown in MMR residential absorption would hit a business that has only really existed in its current form for about five years.4 Long-term track records in Indian residential development are scarce, and the ones that exist are built over multiple cycles, not within a single bull market.

Second, the cyclical nature of the wedding and occasion-wear market. The Lifestyle business is heavily exposed to a category that, while culturally durable, is sensitive to changes in consumer wallets, formal wear penetration, and competitive pricing from larger apparel platforms. The secular shift from formal to casual, which has accelerated across Indian metros post-pandemic, is the kind of slow-moving substitution risk that does not show up in any one quarter but can compound against the brand over a decade.

Third, engineering integration risk. Maini Precision and JK Files together are now expected to produce an integrated, export-grade engineering platform. Integrations of aerospace-qualified suppliers are slow, and the period between paying the acquisition price in late 2023 and seeing the consolidated platform deliver the kind of margin and growth profile that justifies the entry multiple is, by the nature of the industry, multi-year.5 This is a 2027-and-beyond story, not a 2026 one, and the market is, at points, going to be impatient.

Fourth, and most uncomfortably, governance and key-person risk. Gautam Singhania has been the engineering force behind every strategic move of the last three years, but he is also the singular point of dependency. The professionalisation of the board has gone some distance to reducing that risk, but a long-term investor underwriting Raymond is still, to a meaningful degree, underwriting one chairman's continued focus and judgement.[^7]7

Fifth, the conglomerate discount may not entirely disappear. Even with the lifestyle demerger creating cleaner price discovery, the residual Raymond Limited entity is still a mixed bag of real estate, engineering and corporate functions. Indian markets have historically been willing to apply meaningful discounts to mixed entities, and the new Raymond Limited will need to demonstrate, over several reporting cycles, that the segments inside it deserve to be valued individually rather than as a blended industrial multiple.

If a long-term investor is keeping a watch list of operating KPIs that matter for tracking this transformation, three stand out. First, Raymond Realty's pre-sales (bookings) value per quarter and gross development value (GDV) pipeline, which together capture both immediate cash-generation momentum and the multi-year runway.8 Second, the consolidated net debt to EBITDA ratio, because the entire post-Godrej equity story rests on the company never re-leveraging back into the trap it spent two decades escaping.[^8] Third, lifestyle business same-store-sales growth and average ticket size in the wedding occasion-wear segment, because that is the metric that will tell you whether the brand is genuinely modernising or merely surviving on inertia.1

Beyond those three, second-layer diligence overlays worth keeping in peripheral vision include the credit-rating trajectory of the consolidated entity, which after the FMCG sale moved meaningfully into a more comfortable category and which any future leveraging would test; the concentration of institutional ownership across the demerged entities, where a concentrated long-only investor base typically signals comfort with the SOTP story; and the optionality embedded in any non-core land parcels outside the Thane core, which have historically been quietly meaningful and infrequently disclosed in detail. None of these is a primary driver, but each is the kind of detail that, in an Indian industrial holding structure, can either confirm or quietly puncture the bull case.

X. Epilogue & Final Reflections

Stand in ठाणे Thane in 2026 and look at the Raymond complex one last time. The mill is still running. The towers are rising. The Maini facility in Bengaluru is qualifying parts for the next generation of commercial aviation. The Raymond Shop on the corner of a tier-3 town in Maharashtra is still measuring suit lengths for a groom whose grandfather did exactly the same thing forty years ago. None of these scenes look like they belong to the same company, and yet they do.

The lesson of Raymond, for any observer of Indian पारिवारिक व्यवसाय Family Businesses, is structural. For decades, the Indian conglomerate model was built on horizontal sprawl: a textile family also ran a deodorant brand, also owned an industrial tools business, also held land for a future that never quite arrived. The cost of that sprawl was a permanent discount on the equity, a perpetually distracted senior management, and a balance sheet that could never get fully clean because something else always needed feeding. Raymond's last three years are a case study in the opposite playbook. Sell what doesn't fit, even if it is what everyone associates the brand with. Develop what you already own, even if it means becoming a completely different industry. Acquire what gives you an export-grade growth engine, even if it sits two thousand kilometres from the corporate headquarters. And critically, separate the surviving businesses into legal vehicles that the market can value on their own merits, so that the discount has nowhere to hide.

The Complete Man, the figure who has stared out from television screens and storefronts for thirty-five years, is now a brand asset inside a standalone lifestyle company, professionally managed and explicitly competing on its own multiple. His former roommates, real estate and engineering, have gone on to lead lives of their own. Whether the next decade rewards each of them at the multiple their bulls hope for, or punishes them when one of the cycles turns, is a question for future episodes. What is no longer in question is whether this company knew how to change. It did. The harder part, holding the focus once the cameras have moved on, is the part that begins now.

References

References

-

Godrej Consumer Products to acquire Raymond Consumer Care business — GodrejCP.com, 2023-04-27 ↩↩↩↩

-

Raymond Lifestyle Demerger Update — National Stock Exchange of India, 2024-05-03 ↩↩↩

-

Raymond Realty: Creating Value from Land Bank — Investor Presentation Q4FY24, Raymond.in ↩↩↩↩↩↩↩

-

Raymond to buy Maini Precision Products for ₹682 crore — Reuters, 2023-11-04 ↩↩↩↩↩↩

-

Raymond Realty Project Updates – TenX Habitat and The Address by GS — RaymondRealty.in ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube