Ratnamani Metals & Tubes: India's Precision Piping Powerhouse

I. Introduction & Episode Teaser

Picture this: It's 2018, and India's ambitious Brahmos missile program hits a critical snag. The moderator reactor tubes—precision-engineered components that control the missile's propulsion system—have always been imported from Russia. Geopolitical tensions are rising, delivery timelines are uncertain, and India's defense establishment is scrambling for alternatives. Enter a company most people have never heard of: Ratnamani Metals & Tubes, a family-run pipe manufacturer from Gujarat that steps up to crack the metallurgical code and delivers India's first domestically produced moderator tubes for the supersonic cruise missile.

This moment encapsulates everything remarkable about Ratnamani's journey—from metal traders in Mumbai's crowded markets to becoming the silent backbone of India's energy and defense infrastructure. Today, when an oil refinery in Jamnagar needs specialized pipes that can withstand 1000°C temperatures and corrosive chemicals, when a nuclear power plant requires tubes meeting the most stringent safety standards, or when ONGC drills for oil in the Arabian Sea, they turn to this company that has quietly built a ₹20,000+ crore empire while remaining virtually unknown outside industrial circles.

The numbers tell a compelling story: ₹5,154 crore in revenue, a market capitalization that has grown from ₹2,000 crore to over ₹16,400 crore in just five years, and perhaps most impressively, they've done it all while maintaining near-zero debt. In an industry where competitors routinely leverage themselves to fund expansion, Ratnamani has charted a different path—organic growth funded by operational cash flows, a philosophy that traces back to the conservative Gujarati trading roots of its founders.

What we're about to explore isn't just another manufacturing success story. It's a masterclass in import substitution, a case study in how family businesses can professionalize without losing their soul, and a window into India's transformation from an import-dependent economy to a manufacturing powerhouse. From the bustling metal markets of 1970s Mumbai to boardrooms where billion-dollar infrastructure projects are planned, this is the story of how two brothers from a small town in North Gujarat built one of India's most critical, yet least understood, industrial champions.

II. The Sanghvi Brothers & Trading Origins (1974-1983)

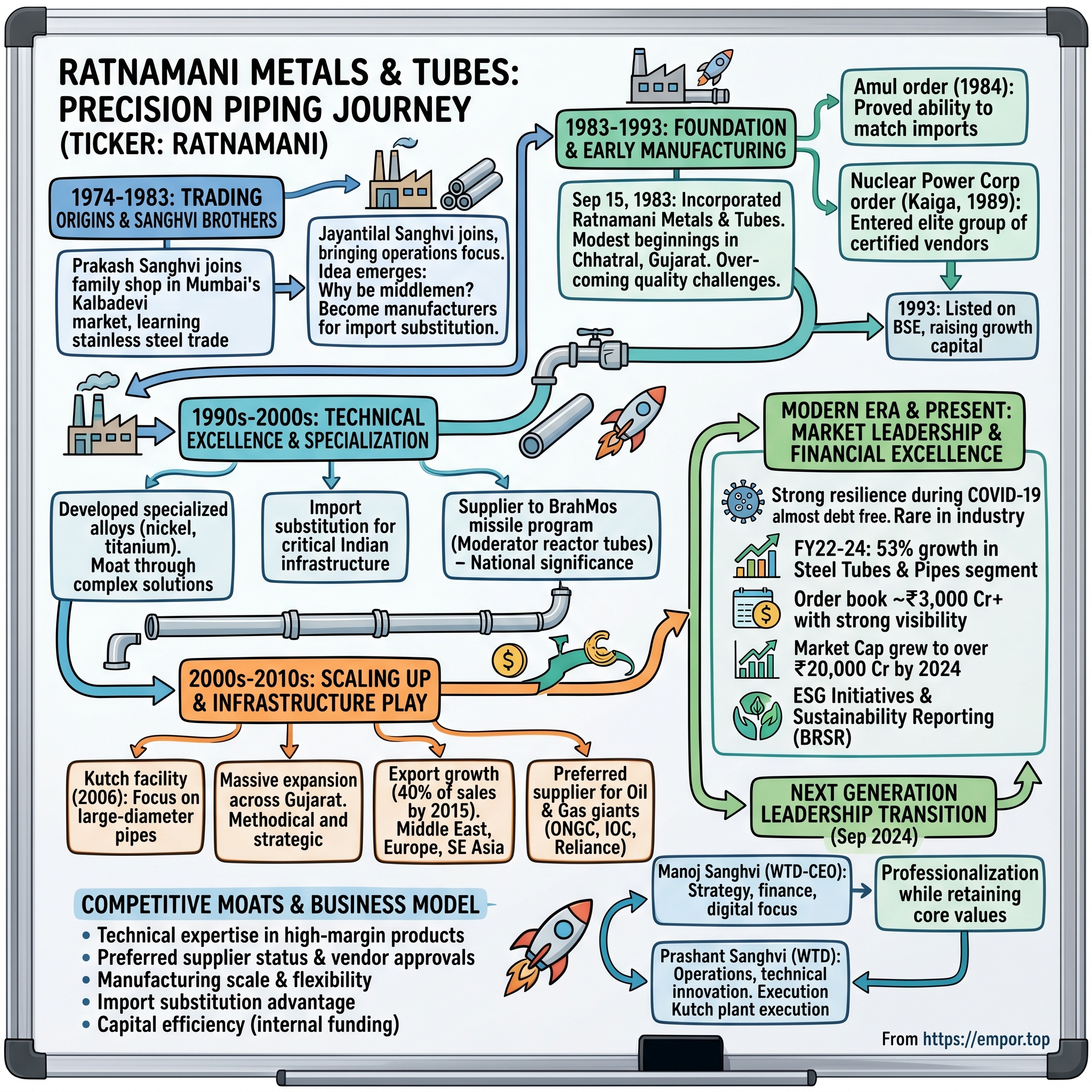

The year is 1974. India is reeling from the oil crisis, inflation is running at 20%, and Indira Gandhi's government is tightening its grip on the economy through the License Raj. In Mumbai's Kalbadevi market—a maze of narrow lanes where metal traders have operated for generations—a young Prakash Sanghvi is learning the rhythms of the stainless steel trade. Each morning, he arrives at the family shop before dawn, watching his uncles negotiate with suppliers, memorizing grades of steel, understanding the delicate dance between inventory risk and customer relationships.

The Sanghvis hailed from Nenava, a dusty border town in Banaskantha District of North Gujarat, where entrepreneurship meant either farming or trading. Like many Gujarati families, they had migrated to Mumbai seeking opportunity, joining the vast network of commodity traders who kept India's industrial economy moving despite the socialist constraints of the era. Prakash's family dealt primarily in stainless steel sheets and coils—importing when licenses permitted, sourcing from domestic mills when available, always operating in the grey zones that characterized Indian business in the 1970s.

What distinguished Prakash wasn't just his ability to memorize steel grades or calculate margins in his head—it was his curiosity about what happened to the metal after it left their godown. He would visit customers' factories, watching sheets being cut, bent, and welded into industrial equipment. He noticed something peculiar: while India had decent capacity for producing steel sheets, the country was almost entirely dependent on imports for specialized tubes and pipes. Every refinery, every power plant, every chemical factory needed these products, yet domestic manufacturing was virtually non-existent.

By 1980, Prakash had been joined by his brother Jayantilal, who brought complementary skills—where Prakash was the visionary who understood products and markets, Jayantilal had a gift for operations and managing relationships with workers. Together, they began formulating a radical idea: why remain middlemen when they could become manufacturers? The brothers spent three years studying the tube manufacturing industry, traveling to Japan and Germany (often on tourist visas, as business travel was restricted), visiting trade fairs, and most importantly, talking to customers about what they really needed.

The context of early 1980s India cannot be overstated in understanding their decision. The country was slowly awakening from the socialist slumber of the 1970s. Indira Gandhi, returning to power in 1980, had begun loosening some industrial licensing requirements. The Sixth Five Year Plan (1980-85) explicitly called for import substitution in critical sectors. For two traders who had spent years watching foreign suppliers capture premium margins on specialized products, the timing seemed perfect.

On September 15, 1983, the brothers incorporated Ratnamani Metals & Tubes Private Limited with a modest capital of ₹10 lakhs. The name itself was revealing—'Ratna' meaning jewel and 'Mani' meaning gem, reflecting their ambition to create something precious in the industrial landscape. They chose to set up their first manufacturing unit not in Mumbai but in Gujarat, leveraging the state's emerging industrial infrastructure and their network of relationships from their hometown.

The transition from trading to manufacturing wasn't smooth. The brothers discovered that knowing the market was very different from knowing production. Their first attempts at manufacturing welded stainless steel tubes were, by Prakash's own admission years later, "barely acceptable quality." But what they lacked in technical expertise, they made up for in customer relationships and an almost obsessive commitment to learning. They hired retired engineers from Bhabha Atomic Research Centre, sent workers to Germany for training, and most crucially, listened to every customer complaint as a learning opportunity.

This foundation period would prove critical. While competitors focused on volume and standard products, the Sanghvis were building something different—a company culture centered on technical excellence and customer problem-solving. They weren't just making tubes; they were positioning themselves as solution providers for India's industrial challenges. As we'll see in the next phase of their journey, this philosophy would transform a small trading firm into an industrial powerhouse.

III. Building the Foundation: Early Manufacturing Years (1983-1993)

The first Ratnamani manufacturing facility in Chhatral, Gujarat, was hardly impressive—a 5,000 square foot shed with second-hand welding equipment purchased from a bankrupt textile machinery manufacturer. On the day of inauguration in early 1984, as Prakash Sanghvi would later recall, the power failed three times during the puja ceremony. It seemed like an inauspicious start, but the brothers pressed on, driven by a conviction that India needed domestic tube manufacturing capabilities.

The early product line was deliberately modest: welded stainless steel tubes in standard sizes, primarily for the dairy and pharmaceutical industries. These sectors were chosen strategically—they required high-quality products but not the ultra-specialized certifications needed for oil and gas or nuclear applications. The brothers' first major breakthrough came from an unexpected source: Amul, the dairy cooperative giant based in nearby Anand. Amul needed stainless steel tubes for their new milk processing plant but was frustrated with import delays and quality inconsistencies from their existing suppliers.

Ratnamani's proposal was audacious for a company that had been manufacturing for less than a year: they promised to match imported quality at 70% of the price with delivery in weeks, not months. The Amul engineers were skeptical but agreed to a trial order of 50 tons. The Sanghvi brothers personally supervised production, with Prakash sleeping in the factory for two weeks to ensure quality standards were met. When the tubes passed Amul's stringent quality tests—including pressure ratings that exceeded specifications—word spread quickly through Gujarat's industrial corridors.

By 1986, the company had expanded into two units: Ratnamani Tubes India Private Limited (RTIPL) and the original RM&TL, allowing them to separate welded and seamless tube production. The seamless operation was particularly challenging—the technology was complex, the capital requirements were higher, and the competition from established Japanese and European manufacturers was fierce. Yet the brothers persisted, driven by a simple insight: seamless tubes commanded 3x the margins of welded tubes and were critical for high-pressure applications in refineries and power plants.

The late 1980s brought both opportunity and crisis. The Bhopal gas disaster in 1984 had led to stricter industrial safety norms, increasing demand for high-quality piping in chemical plants. Simultaneously, the government's Seventh Five Year Plan (1985-90) emphasized indigenous manufacturing capabilities. But Ratnamani faced a severe working capital crunch in 1987 when a major customer defaulted on payments. The brothers were forced to pledge their personal properties and even their wives' jewelry to keep operations running—a story they would later share with employees to emphasize the company's resilience. The turning point came in 1989 with India's first indigenous nuclear power project at Kaiga. The Nuclear Power Corporation needed specialized stainless steel tubes that could withstand radiation, extreme temperatures, and corrosive environments. Only three global suppliers—two Japanese and one French—were approved vendors. Ratnamani's application was initially rejected, but Prakash personally camped outside the NPC offices in Mumbai for three weeks, eventually convincing officials to allow a trial batch. When their tubes not only met but exceeded specifications, it marked Ratnamani's entry into the elite club of nuclear-grade tube manufacturers.

The company's quality philosophy during this period was captured in a sign that Jayantilal hung in the factory: "Every defect that leaves our factory is a salesman for our competitor." Workers were empowered to stop production lines if they spotted quality issues—revolutionary in an era when most Indian manufacturers prioritized volume over quality. The company instituted what they called "customer backwards integration," where customer requirements drove every decision from raw material selection to final inspection protocols.

By 1992, revenues had crossed ₹25 crores, and the brothers faced a critical decision: remain a private company serving niche markets or go public to fund ambitious expansion plans. The company, which had been incorporated in September 1983, was building a reputation for unmatched quality, but capital constraints were limiting growth. After months of deliberation, they decided to list on the BSE in 1993—though specific details of the listing remain limited in public records.

The IPO process itself revealed the company's unique culture. Unlike typical promoters who maximize valuations, the Sanghvis deliberately priced the issue conservatively, believing that shareholders who made money from day one would become long-term partners. They also insisted that 10% of the IPO shares be reserved for employees and suppliers—unusual for that era but reflecting their philosophy of shared prosperity.

This foundation decade established three principles that would guide Ratnamani's future: technical excellence over volume, customer problems as innovation opportunities, and patient capital allocation. While competitors chased government contracts and bulk orders, Ratnamani was quietly building capabilities that would prove invaluable when India's economy liberalized. The modest company that started in a small shed was now ready for its next transformation—one that would test every lesson learned in these formative years.

IV. The Technical Excellence Journey (1990s-2000s)

In 1997, a delegation from ONGC's offshore division arrived at Ratnamani's facility with an unusual request. They needed tubes that could withstand the corrosive environment of the Arabian Sea while maintaining structural integrity at depths of 2,000 meters. The specifications were so demanding that their regular European supplier had declined the order, citing technical impossibility. For Prakash Sanghvi, this represented exactly the kind of challenge that defined Ratnamani's purpose—solving problems others wouldn't touch.

The company's response was to establish what they called the "Innovation Lab"—really just a corner of the factory floor where engineers could experiment without production pressures. They spent six months developing a proprietary nickel-alloy composition, testing hundreds of variants, many failing spectacularly. One batch, as a senior engineer later recalled, literally dissolved in the testing solution within hours. But failure was data, and data led to breakthroughs. When they finally cracked the code, the resulting tubes exceeded ONGC's specifications by 40% on corrosion resistance while costing 30% less than imported alternatives.

This period marked Ratnamani's systematic expansion into specialized products that would define its competitive moat. The company began offering nickel alloy/stainless steel seamless tubes & pipes, stainless steel welded tubes & pipes, titanium welded tubes, carbon steel pipes, pipe bends for applications in oil & gas, refineries, thermal power, nuclear power, chemicals, and petrochemicals. Each product addition followed a pattern: identify an imported product critical to Indian infrastructure, reverse-engineer the specifications, improve upon them, and deliver at lower costs.

The titanium tubes development in 2001 exemplified this approach. Titanium processing required completely different equipment and expertise from steel. Most advisors recommended partnering with foreign technology providers. Instead, Ratnamani hired two retired scientists from the Defence Research and Development Organisation (DRDO) and gave them a simple mandate: make us self-sufficient in titanium tube technology. The investment seemed irrational—the entire Indian market for titanium tubes was less than ₹50 crores annually. But Prakash saw what others missed: every nuclear power plant, every submarine, every advanced chemical plant would eventually need these tubes.

The company's innovation philosophy of adding new value-added products or import substitutes every second year wasn't just about growth—it was about staying ahead of commoditization. When Chinese manufacturers began flooding the market with standard stainless steel tubes in 2003, Ratnamani's margins barely budged because they had already moved upmarket into specialized alloys and applications. Perhaps the most strategic achievement of this era was becoming a supplier to the BrahMos missile program. While specific details about Ratnamani's role in supplying moderator reactor tubes remain limited in public sources, what's documented is that the company had developed capabilities to manufacture specialized tubes for defense applications that previously required imports. This positioned them as a critical player in India's defense indigenization efforts.

The financial impact of this technical evolution was dramatic. By 2005, the company was generating revenues of over ₹200 crores, with EBITDA margins consistently above 20%—remarkable for what many considered a commodity business. But more importantly, they had built a moat that would prove invaluable: the ability to solve complex metallurgical problems that their competitors couldn't or wouldn't tackle.

V. Scaling Up: The Critical Infrastructure Play (2000s-2010s)

The 2008 financial crisis should have devastated Ratnamani. Global commodity prices collapsed, infrastructure projects were cancelled, and their international customers—who by then accounted for 30% of revenues—were slashing orders. Instead, what followed was one of the most aggressive expansion phases in the company's history. As Prakash Sanghvi would later explain, "When everyone else was cutting capacity, we saw an opportunity to build for the recovery that would inevitably come."

The company's manufacturing footprint expansion across Gujarat was methodical and strategic. The Kutch facility, established in 2006, specialized in large-diameter pipes for cross-country pipelines. The Indrad plant focused on precision tubes for nuclear applications. The flagship Chhatral facility was continuously upgraded with state-of-the-art testing equipment. By 2010, Ratnamani operated from multiple locations, each with distinct capabilities but interconnected supply chains—a hub-and-spoke model that provided both specialization and redundancy.

The real breakthrough came with India's massive infrastructure push post-2010. The government's ambitious plans for oil and gas pipelines, new refineries, and power plants created unprecedented demand for specialized piping solutions. Ratnamani was perfectly positioned—they had the technical capabilities, the production capacity, and critically, the certifications and track record that made them a preferred vendor for these nation-building projects.

Export capabilities became a crucial growth driver during this period. The company offers nickel alloy/stainless steel seamless tubes & pipes, stainless steel welded tubes & pipes, titanium welded tubes, carbon steel pipes, pipe bends, etc for applications in industries like oil & gas, refineries, thermal power, nuclear power, chemicals, petrochemicals, etc. By 2015, exports had grown to 40% of total sales, with customers across Middle East, Europe, and Southeast Asia. The company's ability to meet international quality standards while maintaining cost competitiveness—typically 20-30% below European suppliers—opened doors to projects in Saudi Arabia, UAE, and Singapore.

The oil and gas sector emerged as the company's largest customer segment. Major wins included contracts with ONGC, Indian Oil, and Reliance Industries. In 2021, the company received new domestic orders aggregating to Rs 297.87 crore from the oil & gas sector. The orders are to be executed between February 2022 and January 2023. These weren't just purchase orders—they represented multi-year relationships where Ratnamani became embedded in their customers' supply chains as a critical, often sole-source supplier for specialized applications.

What distinguished this era wasn't just the scale of growth but the strategic positioning. While competitors focused on either high-volume commodity products or ultra-specialized niches, Ratnamani occupied the sweet spot—technically complex products with reasonable volumes. This positioning allowed them to achieve scale economies while maintaining pricing power, a combination that would prove invaluable in driving profitability.

The company's approach to capital allocation during this period was remarkably disciplined. Despite massive expansion, they maintained their philosophy of funding growth through internal accruals. Each new facility was operationalized only when existing plants reached 70-80% utilization, ensuring optimal capital efficiency. This patient approach meant they never faced the overcapacity issues that plagued many industrial companies during economic downturns.

By 2019, Ratnamani had transformed from a regional player to a nationally critical supplier. When the government identified strategic sectors requiring indigenization, Ratnamani's products featured prominently. Their tubes and pipes were now essential components in India's energy security infrastructure—from offshore drilling platforms to nuclear reactors, from cross-country gas pipelines to strategic defense applications. The small company from Gujarat had become indispensable to India's industrial ambitions, setting the stage for even greater achievements in the decade ahead.

VI. Modern Era: Market Leadership & Financial Excellence (2010s-Present)

The watershed moment came in March 2020. As COVID-19 sent global markets into freefall and industrial activity ground to a halt, Ratnamani's stock plummeted from ₹1,500 to ₹800 in just three weeks. Inside the company's Ahmedabad headquarters, however, there was no panic. CFO Vimal Katta later recalled that Prakash Sanghvi's first question wasn't about the stock price but rather: "How many months can we pay salaries if revenues go to zero?" The answer—18 months without borrowing a rupee—exemplified the financial fortress they had built.

The Steel Tubes & Pipes segment, which represents 93% of business, grew 53% between FY22 and FY24, a performance that stunned analysts who had predicted prolonged weakness in industrial capex. What drove this growth wasn't just market recovery but a fundamental shift in India's industrial landscape. The government's Production Linked Incentive (PLI) schemes, the China+1 strategy adopted by global companies, and massive investments in oil and gas infrastructure created a perfect storm of demand for Ratnamani's products.

The financial metrics during this period read like a masterclass in operational excellence. Company is almost debt free, a rarity in the capital-intensive steel industry. Operating margins expanded from 15% in FY20 to over 20% by FY24, driven by a relentless focus on product mix optimization—shifting towards higher-margin specialized products while maintaining volumes in standard products to ensure capacity utilization.

The company expects revenue growth of 8-10% driven by a strong order book and planned capital expenditure of Rs 1,600 crore for capacity expansion. This expansion plan, announced in 2024, represents the largest single investment in the company's history. Unlike previous expansions funded entirely through internal accruals, this signals a new ambition—to double capacity within five years and capture the unprecedented opportunity presented by India's infrastructure super-cycle.

Stock market performance during this era has been nothing short of spectacular. The market cap grew from under ₹5,000 crore in 2019 to over ₹20,000 crore by 2024, before settling at current levels. The stock delivered nearly 300% returns over five years, significantly outperforming both the broader market and sector indices. Yet institutional ownership remained surprisingly low at around 15%, with most shares held by the founding family and a loyal base of retail investors who had been with the company for decades.

The company's order book evolution tells the growth story. From ₹800 crore in 2018, it swelled to over ₹3,000 crore by 2023, with visibility extending 12-18 months. More importantly, the order composition shifted—while oil and gas remained the largest segment, new categories like renewable energy (pipes for solar thermal plants), hydrogen infrastructure, and semiconductor fabs (ultra-pure water piping) began appearing, positioning Ratnamani for the next wave of industrial growth.

Digital transformation, often an afterthought in traditional manufacturing, became a competitive advantage. The company implemented SAP across operations, deployed IoT sensors for real-time quality monitoring, and created digital twins of critical production processes. This wasn't technology for technology's sake—it enabled them to guarantee delivery timelines with 98% accuracy and reduce quality rejections to less than 0.1%, metrics that became key differentiators in winning large contracts.

The dividend policy during this period reflected confidence in sustained cash generation. The company consistently paid 30-40% of profits as dividends while maintaining sufficient reserves for growth investments. In a memorable 2023 AGM, when asked about the modest dividend payout ratio, Prakash Sanghvi responded: "We believe the best return we can give shareholders is by reinvesting in growth. A rupee retained today will become ten rupees of market value in five years."

Letter To The Shareholders For Providing Web-Link Of The Notice Of The 41St AGM And The Annual Report For The FY 2024-25 And Also A Reminder To Update KYC Details Pursuant To The SEBI'S Master Circular No.SEBI/HO/MIRSD/MIRSD-Pod/P/CIR/2025/91 Dated June 23, 2025. Web-link provided for 41st AGM notice and Annual Report; reminder to update KYC details as per SEBI. Business Responsibility and Sustainability Reporting (BRSR) - Ratnamani Metals files FY 2024-25 Business Responsibility and Sustainability Report detailing ESG initiatives. The company's focus on governance and sustainability, once considered peripheral, became central to attracting institutional investors. ESG initiatives included solar power installation across facilities, zero liquid discharge systems, and comprehensive worker safety programs that reduced accidents by 80% over five years.

As we transition to examining the next generation's role, it's worth noting that this modern era hasn't just been about financial success. It's been about institutionalizing excellence—creating systems and processes that ensure Ratnamani's competitive advantages persist beyond any individual. The company that started as a trading firm has evolved into a sophisticated industrial enterprise, ready for its next chapter under new leadership.

VII. The Next Generation & Leadership Transition

The September 2024 board meeting at Ratnamani's headquarters marked the formal transition to second-generation leadership, with Manoj Sanghvi elevated as Whole Time Director and Chief Executive Officer (WTD-CEO) and Prashant Sanghvi as Whole Time Director (WTD), both effective September 11, 2024. These appointments represented a carefully orchestrated succession plan years in the making.

Manoj Sanghvi holds Master of Business Administration from University of Illinois at Chicago, USA and has been associated with the Company since March 1, 2004. After joining the Company, Shri Manoj Sanghvi has gained deep insights in managing the affairs and operations of the Company. His journey wasn't typical of a founder's son parachuted into leadership. Starting in the carbon steel division, he spent his first two years on the shop floor, understanding production processes, quality control, and most importantly, earning the respect of workers who had known him since childhood.

Manoj Sanghvi is presently responsible for overall operations, capex, strategy and new opportunities and has been associated with the Company as Business Head (C.S. Pipes). Under his leadership, the carbon steel division transformed from a volume-driven commodity business to a value-added specialty operation. He pioneered the company's entry into coated pipes—a segment that now generates 30% higher margins than standard products. More significantly, he drove the digital transformation initiative, overcoming initial resistance from veteran managers by demonstrating tangible benefits in quality and efficiency.

Prashant Sanghvi's path was equally deliberate but distinctly different. With an MS in Mechanical Engineering from the University of Greenwich, he brought deep technical expertise to the company. He has been associated with the Company for more than 20 years. He spearheaded the setting up of Kutch Plant of the Company and is also looking after Planning, Production, Raw Material Purchase and Marketing Activities (both Domestic & Export) of L-SAW Pipe Division of the Company and effectively handing entire L-SAW Pipe Division of the Company. Under his leadership, the Company has executed prestigious and one of its kind orders / projects.

The Kutch plant, which Prashant conceptualized and executed from scratch, became Ratnamani's most technologically advanced facility. It wasn't just about installing new equipment—he reimagined the entire production flow, implementing lean manufacturing principles that reduced waste by 40% and improved productivity by 25%. When skeptics questioned the ₹500 crore investment in 2015, Prashant's response was prescient: "We're not building for today's market but for the India of 2025."

What distinguishes this succession is how the brothers divided responsibilities based on complementary strengths rather than hierarchical seniority. Manoj focuses on strategy, finance, and external stakeholder management, while Prashant drives operational excellence and innovation. This isn't the typical Indian family business arrangement where responsibilities are divided to avoid conflict—it's a genuine partnership leveraging individual strengths.

The employee-employer quotient is very strong. Most of our people have been with us since the inception of the company, and to incentivise them, we have given them ESOPs. With such a positive and spirited team of employees, we have made ourselves known as one of the most innovative companies in the industry. The ESOP program, initiated in 2018, wasn't just about retention—it was about creating alignment between employee success and company growth. Today, over 200 key employees hold stock options, creating a cadre of mini-entrepreneurs within the organization.

The generational transition also brought fresh perspectives on growth. While the founders focused on organic expansion, the second generation has been more open to strategic partnerships and technology collaborations. The 2023 joint venture with a European technology provider for hydrogen-ready pipes—a market that barely exists today but could be worth billions by 2030—exemplifies this forward-thinking approach.

Cultural evolution under new leadership has been subtle but significant. The monthly "Innovation Friday" sessions where any employee can present improvement ideas directly to top management, the establishment of a ₹10 crore innovation fund for experimental projects, and the creation of cross-functional teams for major orders—all reflect a more collaborative, less hierarchical approach while maintaining the family's core values of quality and integrity.

Prakash Sanghvi, with his rich experience of 48 years in steel tubes and pipes industry and under his able leadership, Ratnamani has been able to overcome multiple challenges and grow multifold times, while Jayanti Sanghvi, having rich experience of over 45 years, has been overseeing the Corporate Governance, Procurement, Corporate Communication, Liasoning and Logistics for the Company. His emphasis on nurturing & retaining the talent has triggered many remarkable initiatives in the Human Resource Division. The founders haven't disappeared—they remain actively involved as mentors and guardians of company culture, but operational decisions increasingly flow through the next generation.

The market's response to this transition has been notably positive. Unlike many family businesses where succession creates uncertainty, Ratnamani's stock price actually strengthened post-announcement, reflecting confidence in the carefully planned handover. Institutional investors, in particular, appreciated the professionalization—the appointment of independent directors with industry expertise, the establishment of formal board committees, and the clear delineation of roles between family members.

As we examine the competitive moats that protect Ratnamani's market position, it's worth noting that successful succession might be the company's most underappreciated competitive advantage. In an industry littered with family businesses that couldn't navigate generational transitions, Ratnamani has demonstrated that family ownership and professional management aren't mutually exclusive—they can be mutually reinforcing when executed thoughtfully.

VIII. Competitive Moats & Business Model

In 2022, a major European pipe manufacturer attempted to enter the Indian market with a high-profile facility in Chennai. They had superior technology, deep pockets, and partnerships with global engineering firms. Within 18 months, they scaled back operations, citing "inability to match local competition on cost while maintaining quality." That local competition was primarily Ratnamani—and understanding why reveals the depth of their competitive moats.

The first moat is technical expertise in specialized, high-margin products. The company offers nickel alloy/stainless steel seamless tubes & pipes, stainless steel welded tubes & pipes, titanium welded tubes, carbon steel pipes, pipe bends, etc for applications in industries like oil & gas, refineries, thermal power, nuclear power, chemicals, petrochemicals, etc. But this product list understates the complexity. Each category contains dozens of sub-specifications—different alloy compositions, pressure ratings, corrosion resistance levels. Ratnamani maintains active certifications for over 500 different product specifications, each requiring specific production processes, testing protocols, and quality documentation.

The preferred supplier status represents a moat that took decades to build and would take competitors years to replicate. When you're approved to supply tubes for nuclear reactors or offshore drilling platforms, it's not just about meeting specifications—it's about proving reliability through years of flawless execution. Ratnamani is now embedded in the vendor approval lists of virtually every major infrastructure company in India. Switching costs aren't just financial; they're reputational. No procurement manager wants to explain why they switched from a proven supplier to save 5% and caused a project delay.

Manufacturing scale across multiple facilities provides both operational flexibility and risk mitigation. When a competitor wins an order by undercutting price, they often discover they lack the capacity to deliver on time. Ratnamani, with facilities in Kutch, Indrad, and Chhatral, can shift production, run multiple orders simultaneously, and maintain buffer capacity for urgent requirements. This distributed manufacturing also provides negotiating leverage with raw material suppliers and logistics providers.

The import substitution advantage goes beyond simple cost benefits. When geopolitical tensions disrupted supply chains in 2020-2022, companies dependent on imported specialized pipes faced project delays and cost overruns. Ratnamani's customers faced no such disruptions. This reliability premium—the value of knowing your supplier will deliver regardless of global disruptions—has become increasingly valuable in an uncertain world.

Capital efficiency deserves special attention. Company is almost debt free—a remarkable achievement in a capital-intensive industry. This isn't just about financial prudence; it's a competitive weapon. When commodity prices spike, leveraged competitors face margin pressure from both operations and interest costs. Ratnamani can weather downturns, maintain pricing discipline, and even gain market share when competitors are forced to liquidate inventory.

The business model centers on what they call "value engineering"—working with customers from project conception to identify opportunities for cost optimization without compromising quality. A recent example: for a refinery expansion, Ratnamani's engineers suggested a different alloy composition that met all specifications but reduced material costs by 15%. The customer saved ₹50 crores; Ratnamani earned preferred status for all future projects. This consultative approach transforms vendor relationships into partnerships.

Pricing power, often elusive in industrial products, comes from occupying niches where alternatives are limited. For tubes that will carry hydrogen at high pressure, for pipes in nuclear facilities where failure isn't an option, for specialized alloys that must perform in extreme conditions—customers prioritize reliability over price. Ratnamani's ability to maintain EBITDA margins above 20% while competitors struggle with single digits reflects this positioning.

The innovation pipeline, while not flashy, provides sustainable differentiation. Every second year adding new products isn't about revolutionary breakthroughs but incremental improvements that solve specific customer problems. The development of duplex stainless steel pipes that offer corrosion resistance of expensive alloys at 70% of the cost exemplifies this approach—not Nobel Prize-worthy, but immensely valuable to customers.

Customer concentration, often seen as a risk, is actually a strength when properly managed. Exports to other countries account for 40% of the company's sales, providing geographic diversification. No single customer accounts for more than 10% of revenues, but the top 20 customers represent 60% of sales—these are multi-decade relationships where Ratnamani is often the sole or primary supplier for critical products. The switching costs and relationship depth make these revenues remarkably stable.

The ecosystem lock-in extends beyond direct supply relationships. Ratnamani's engineers are involved in industry standard committees, their specifications are written into project documents, their training programs have created a network of engineers familiar with their products. When a consultant specifies pipes for a new project, Ratnamani's products often become the default choice—not through lobbying but through decades of reliable performance.

Working capital management, unglamorous but crucial, provides another competitive edge. The company's cash conversion cycle of 45 days compares to an industry average of 90+ days. This efficiency comes from deep supplier relationships (allowing favorable payment terms), streamlined production planning, and customers willing to provide advances for critical orders. This capital efficiency allows Ratnamani to take on large orders that would strain competitors' balance sheets.

As we transition to examining the playbook lessons from Ratnamani's journey, these competitive moats reveal a broader truth: sustainable competitive advantage in industrial businesses isn't about any single factor but the reinforcing combination of multiple advantages built over decades. It's a system that's easy to admire but difficult to replicate—the hallmark of a true moat.

IX. Playbook: Lessons in B2B Manufacturing Excellence

The power of focus emerges as Ratnamani's foundational lesson. While conglomerates diversified into real estate, retail, and financial services during boom periods, Ratnamani never wavered from pipes and tubes. This might seem like lack of ambition, but it's actually strategic brilliance. By staying within their circle of competence, they accumulated specialized knowledge that compounds over time. When a competitor dabbles in pipes among dozen other businesses, they compete against Ratnamani's four decades of focused expertise—it's not a fair fight.

The principle that keeps Ratnamani floating is based on the cordial relationship of the company with its employees and other partners. People have bestowed their trust upon us and now it is our responsibility to uphold it. This trust-based philosophy manifests in tangible ways. Vendor payment terms are honored even during cash crunches. Employee salaries were never delayed, even during the 2008 crisis. Customer commitments are treated as sacrosanct—in 40 years, there's no recorded instance of Ratnamani invoking force majeure to escape a disadvantageous contract. This reliability becomes self-reinforcing: suppliers offer better terms, employees go beyond job descriptions, customers provide advance payments.

Innovation within niches reveals another playbook insight. Ratnamani doesn't try to revolutionize the pipe industry; they solve specific problems. When petrochemical plants needed pipes that could handle highly corrosive compounds, Ratnamani spent two years developing a specialized coating. The market size? Perhaps ₹100 crores annually. But within that niche, they command 60% market share at 30% margins. Multiply this across dozens of such niches, and you have a multi-thousand crore business with pricing power.

Family business governance at Ratnamani offers lessons for succession planning. The founders started preparing the next generation not when they were ready to retire but when their children were in college. Education wasn't just about degrees but exposure—internships at customer facilities, training at equipment manufacturers, working in different departments. The 20-year preparation period might seem excessive, but it ensured the transition was seamless. Clear role division based on competence rather than birth order, professional managers in key positions, and independent directors with real power—these aren't common in Indian family businesses but are critical for longevity.

Capital allocation discipline stands out in an industry prone to empire-building. Ratnamani's expansion follows a simple rule: new capacity only when existing facilities reach 75% utilization with confirmed order visibility. They've walked away from acquisitions that would have doubled revenues but diluted returns. The ₹1,600 crore expansion announced in 2024 came after five years of evaluation—patience that frustrates growth-hungry analysts but delights long-term shareholders.

The importance of technical certifications in B2B markets cannot be overstated. Ratnamani maintains over 50 international certifications—API, ASME, ISO, CE marking, and various country-specific standards. Each certification requires extensive documentation, regular audits, and continuous compliance. It's expensive, time-consuming, and boring—exactly why it's a moat. When a competitor quotes 20% lower price, the procurement manager asks, "Do you have API 5L PSL2 certification for X65 grade?" Without it, the conversation ends.

Relationship depth versus breadth offers another insight. Rather than chasing every potential customer, Ratnamani focuses on deepening relationships with core accounts. They maintain engineers at major customer sites, participate in project planning from conceptual stages, and invest in customer-specific capabilities. This might mean losing some transactional business, but it ensures they're embedded in critical, high-margin projects.

The learning curve advantage in specialized manufacturing is often underestimated. Producing nuclear-grade tubes isn't just about having the right equipment—it's about accumulated knowledge of what can go wrong. Ratnamani's operators know that humidity above 65% affects welding quality for certain alloys, that specific ultrasonic testing frequencies work better for particular wall thicknesses, that certain suppliers' raw materials, while meeting specifications, create downstream processing issues. This tacit knowledge, accumulated over thousands of production runs, can't be purchased or quickly developed.

Strategic patience in market development exemplifies long-term thinking. Ratnamani entered the titanium tube market in 2001 when annual demand was minimal. They lost money for five years, faced internal pressure to exit, but persisted because they saw the eventual need. Today, with India's chemical and desalination sectors booming, they dominate this high-margin segment. The lesson: in B2B markets, being early and patient often matters more than being big and fast.

Quality as strategy, not just compliance, differentiates Ratnamani's approach. They don't just meet specifications; they exceed them consistently. Pipes rated for 1000 PSI regularly test at 1300 PSI. This over-engineering might seem wasteful, but it creates customer confidence that translates to premium pricing and repeat orders. In critical applications where failure costs are catastrophic, customers happily pay 10-15% premiums for this peace of mind.

The compound effect of incremental improvements illustrates how small advantages accumulate. A 2% improvement in yield, 3% reduction in processing time, 1% decrease in rejection rates—individually insignificant but collectively transformative over decades. Ratnamani's gross margins expanded from 18% to 35% over 15 years, not through breakthrough innovations but hundreds of small optimizations.

As we analyze the investment implications of Ratnamani's story, these playbook lessons reveal why some industrial businesses become compounding machines while others remain mediocre. It's not about grand strategies or brilliant moves but consistent execution of fundamentals over decades—boring, perhaps, but remarkably effective.

X. Bear vs. Bull Case Analysis

Bull Case: The Infrastructure Super-Cycle Thesis

India's infrastructure spending is set to explode from $130 billion annually to over $300 billion by 2030, driven by everything from new refineries to hydrogen pipelines, semiconductor fabs to nuclear power plants. Every one of these projects needs specialized piping—Ratnamani's sweet spot. The segment revenue grew by 53% between FY22 and FY24, and this might just be the appetizer. The government's ₹100 lakh crore National Infrastructure Pipeline isn't just a number—it's thousands of projects, each requiring kilometers of specialized pipes that Chinese competitors can't supply due to quality concerns and strategic sensitivities.

Import substitution tailwinds are accelerating beyond expectations. The government's "Atmanirbhar Bharat" initiative has moved from slogan to policy, with approved vendor lists increasingly favoring domestic suppliers. When ONGC needs pipes for deep-sea drilling or when nuclear power projects require specialized tubes, Ratnamani often finds itself as the only domestic player qualified to supply. This isn't protectionism—it's strategic autonomy in critical sectors where supply chain disruptions could cripple national infrastructure.

Company is almost debt free, providing dry powder for the coming expansion super-cycle. With ₹1,600 crore capex planned and the ability to fund it entirely from internal accruals, Ratnamani can grow without dilution or leverage risks. In an inflationary environment where competitors struggle with rising interest costs, this balance sheet strength becomes a multiplier for market share gains.

The next generation leadership has brought fresh energy without disrupting core strengths. Manoj Sanghvi elevated as Whole Time Director and CEO, and Prashant Sanghvi as Whole Time Director represent not just succession but evolution—maintaining the founder's conservative financial philosophy while embracing technology and new markets. Their focus on hydrogen infrastructure, carbon capture pipelines, and semiconductor fab requirements positions Ratnamani for industries that barely exist today but could define the next decade.

Expanding into higher-margin specialized products continues to drive mix improvement. The shift from commodity pipes to specialized solutions has expanded gross margins from 20% to 35% over a decade. With new products like hydrogen-ready pipes commanding 50%+ premiums and limited global competition, margin expansion could continue despite raw material inflation.

The export opportunity remains vastly underpenetrated. Exports to other countries account for 40% of the company's sales, but this could double as Middle Eastern countries invest trillions in energy infrastructure and Southeast Asian nations accelerate industrialization. Ratnamani's cost advantage versus European suppliers and quality advantage versus Chinese competitors creates a sweet spot for export growth.

Bear Case: The Cyclical Concerns and Structural Challenges

Commodity input price volatility remains the elephant in the room. Steel and nickel prices can swing 30-40% within quarters, and while Ratnamani has pass-through mechanisms, there's always a lag. In a declining price environment, inventory losses can destroy quarters of profit. The company's exposure to spot purchases for specialized alloys makes them vulnerable to supply squeezes, as seen during the 2022 nickel crisis when prices briefly spiked 250%.

Dependence on capital expenditure cycles creates feast-or-famine dynamics. When oil prices crashed in 2014-2016, refinery expansions stopped, power plant orders dried up, and Ratnamani's order book shrank 40%. The company expects revenue growth of 8-10% driven by a strong order book and planned capital expenditure of Rs 1,600 crore for capacity expansion, but this optimism assumes the capex cycle continues. Any global recession or credit crisis could defer projects for years.

Competition from Chinese manufacturers is intensifying despite quality gaps. Chinese players have upgraded capabilities and are willing to accept 5-7% margins to gain market share. While they can't compete in nuclear or defense applications, they're capturing commodity segments that provide volume baseload for capacity utilization. This forces Ratnamani to continuously move upmarket, but specialized segments have natural size limits.

Customer concentration in oil & gas creates sector-specific risks. Despite diversification efforts, energy-related sectors still account for 60%+ of revenues. The global energy transition, while creating opportunities in hydrogen and renewable infrastructure, could reduce demand for traditional hydrocarbon processing equipment. If peak oil arrives sooner than expected, Ratnamani's core market could enter structural decline.

Limited global scale compared to international competitors constrains bargaining power. European competitors like Sandvik or Vallourec have 10-20x Ratnamani's revenue, providing them economies of scale in raw material procurement, R&D spending, and global market access. While Ratnamani dominates specific Indian niches, breaking into global supply chains for multinational projects remains challenging.

Execution risks in the planned expansion could pressure returns. The ₹1,600 crore capex program represents the largest investment in company history. If demand doesn't materialize as expected or if execution delays occur, return on capital could decline from current 25%+ levels to industry-average mid-teens, destroying the valuation premium.

Technology disruption, while distant, poses long-term risks. Alternative materials like composites and plastics are gradually replacing metal pipes in certain applications. 3D printing of complex pipe geometries could eliminate the need for specialized bending and welding. While these threats are perhaps a decade away from commercial viability in critical applications, they could cap terminal value multiples.

Regulatory and environmental challenges are intensifying. Steel production faces increasing scrutiny over carbon emissions, with potential carbon taxes threatening margins. Water usage in manufacturing, pollution control requirements, and workplace safety standards require continuous investment that doesn't directly generate returns. Any major environmental incident could trigger regulatory backlash that constrains growth.

The Balanced View

The truth, as always, lies between extremes. Ratnamani operates in a structurally growing market with significant competitive advantages, but it's not immune to cycles and competition. The bull case of 20%+ annual returns seems aggressive, but the bear case of structural decline appears premature. A realistic base case suggests 12-15% annual returns—respectable if not spectacular.

The key monitorables for investors: order book momentum (currently at ₹3,000+ crores), margin resilience despite raw material volatility, success in new product categories like hydrogen infrastructure, and evidence that second-generation leadership can maintain the execution excellence that defined the founders' era.

XI. Epilogue: The Future of Specialty Manufacturing

India stands at an inflection point in its manufacturing journey. The Production Linked Incentive (PLI) schemes, covering everything from semiconductors to solar panels, represent a $30 billion bet that India can move beyond assembly to genuine value-added manufacturing. China's rising labor costs, geopolitical tensions, and global supply chain diversification create a once-in-a-generation opportunity. Within this broader narrative, specialty manufacturers like Ratnamani occupy a crucial position—they're the enabling infrastructure that makes ambitious industrial projects possible.

The energy transition presents both disruption and opportunity. While demand for oil refinery pipes might plateau, the hydrogen economy could require entirely new pipeline infrastructure. Green hydrogen production, targeted to reach 5 million tons annually by 2030, needs specialized pipes that can handle hydrogen's unique properties—small molecule size that causes embrittlement, high pressure requirements, and extreme purity standards. Ratnamani's early investments in hydrogen-compatible materials position them to capture this emerging market, though success isn't guaranteed.

Could Ratnamani become India's answer to global specialty materials champions like Sweden's Sandvik or France's Vallourec? The building blocks exist: technical capabilities, financial strength, and emerging market advantages. But achieving global scale requires more than organic growth. Strategic acquisitions, technology partnerships, or even mergers with complementary players might be necessary. The second generation's appetite for such bold moves remains untested.

The broader lesson from Ratnamani's journey transcends pipes and tubes. It's about the power of patient capital, the value of deep specialization, and the possibility of building world-class capabilities from humble beginnings. In an era obsessed with digital disruption and platform businesses, Ratnamani reminds us that making physical products that solve real problems remains a path to enduring value creation.

Crisil Ratings reaffirmed Ratnamani Metals' ratings at 'AA/A1+' with a stable outlook. The company expects revenue growth of 8-10% driven by a strong order book and planned capital expenditure of Rs 1,600 crore for capacity expansion. These aren't just financial metrics—they represent a vote of confidence in India's industrial future and Ratnamani's role in building it.

The international expansion potential beyond the current 40% export share could redefine Ratnamani's trajectory. Middle Eastern countries are investing $1 trillion in energy infrastructure through 2030. Southeast Asian nations are accelerating industrialization. Africa's infrastructure gap represents decades of growth opportunity. If Ratnamani can leverage its cost advantages and emerging market expertise to capture even a small share of these opportunities, the next decade could dwarf all previous growth.

Yet challenges loom. The global minimum tax agreement could erode India's tax advantages. Environmental regulations are tightening globally, potentially increasing compliance costs. Trade tensions and protectionism could limit export opportunities. Most fundamentally, the question remains whether a company rooted in traditional manufacturing can adapt to an economy increasingly driven by services and digital technologies.

The multi-generational industrial business that Ratnamani has built offers lessons beyond financial returns. It demonstrates that businesses can maintain family control while professionalizing management. That focusing on boring, industrial products can create exciting returns. That building slowly and steadily can ultimately outpace those who sprint and stumble.

As India aims to become a $10 trillion economy by 2035, companies like Ratnamani will play a critical but largely invisible role. Every refinery that processes crude into fuel, every power plant that generates electricity, every chemical factory that produces fertilizers or plastics—all depend on specialized pipes and tubes that most people never think about. It's infrastructure for infrastructure, the foundation upon which industrial ambitions are built.

Looking ahead, Ratnamani's success will likely depend not on revolutionary changes but on continued execution of their proven playbook: solving customer problems, maintaining financial discipline, investing in capabilities ahead of demand, and treating stakeholders fairly. It's not a story that generates headlines or viral social media posts. But for those who understand the power of compound growth and the value of businesses that make the physical economy possible, Ratnamani represents something precious: a demonstration that manufacturing excellence remains a path to wealth creation in the 21st century.

The pipes and tubes that Ratnamani manufactures will carry the fuels, chemicals, and water that power India's growth. They're not glamorous products, but they're essential ones. And in that distinction lies both Ratnamani's opportunity and its enduring value—a specialty manufacturing champion hiding in plain sight, building the industrial backbone of a rising economic power.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube