RateGain: The SaaS Plumbing of Global Travel

I. Introduction & The "Invisible" Giant

Picture the last time you opened a browser and typed "hotel in Lisbon for next weekend." You probably bounced between three or four tabs — Booking.com, Expedia, maybe 携程集团 Trip.com, perhaps the hotel's own website to check if the direct rate was cheaper. In the span of about ninety seconds, you compared maybe fifty different price points across maybe ten different surfaces. Then, because the rates kept moving by a euro or two, because the photos were not quite what you wanted, because someone shouted from the next room — you closed the tabs. You did not book. You went to make tea.

In that ninety seconds, somewhere in a data centre in Noida or northern Virginia, a server belonging to a company most travellers have never heard of likely processed your activity multiple times. It scraped competitor rates for the hotels you looked at. It pushed inventory changes from the hotel's central system out to the OTAs you were browsing. It logged your travel-intent signal into a digital identity that, the next morning, would help that same hotel chain re-target you on Instagram. The hotel paid for all of it. So did the OTA. So, in a sense, did you. The transaction was invisible. The pipe through which it flowed was very much not.

There is a peculiar geometry to industries like global hospitality. From the outside, what you see is the consumer brand — Marriott, Hilton, Booking, Expedia. From the inside, what holds the whole thing together is a layer of middleware that is older than the iPhone, older than the public internet, in some cases older than the founders of the largest OTAs. It is in that middleware that businesses like RateGain make their living, and it is in that middleware that the most durable economics in travel software hide in plain sight.

To make the scale concrete: the global hospitality industry processed roughly 1.5 billion international tourist arrivals in the most recent full year of data, with several multiples of that number in domestic travel. Each of those arrivals corresponds to anywhere from one to ten distinct online price-checks before booking, and each booking corresponds to dozens of downstream data exchanges between hotels, OTAs, GDSs, payment processors, loyalty programmes, and marketing platforms. The total number of inter-system data exchanges in global hospitality, on any given day, runs into the tens of billions. RateGain processes a meaningful slice of that volume. The plumbing metaphor is, if anything, an understatement.

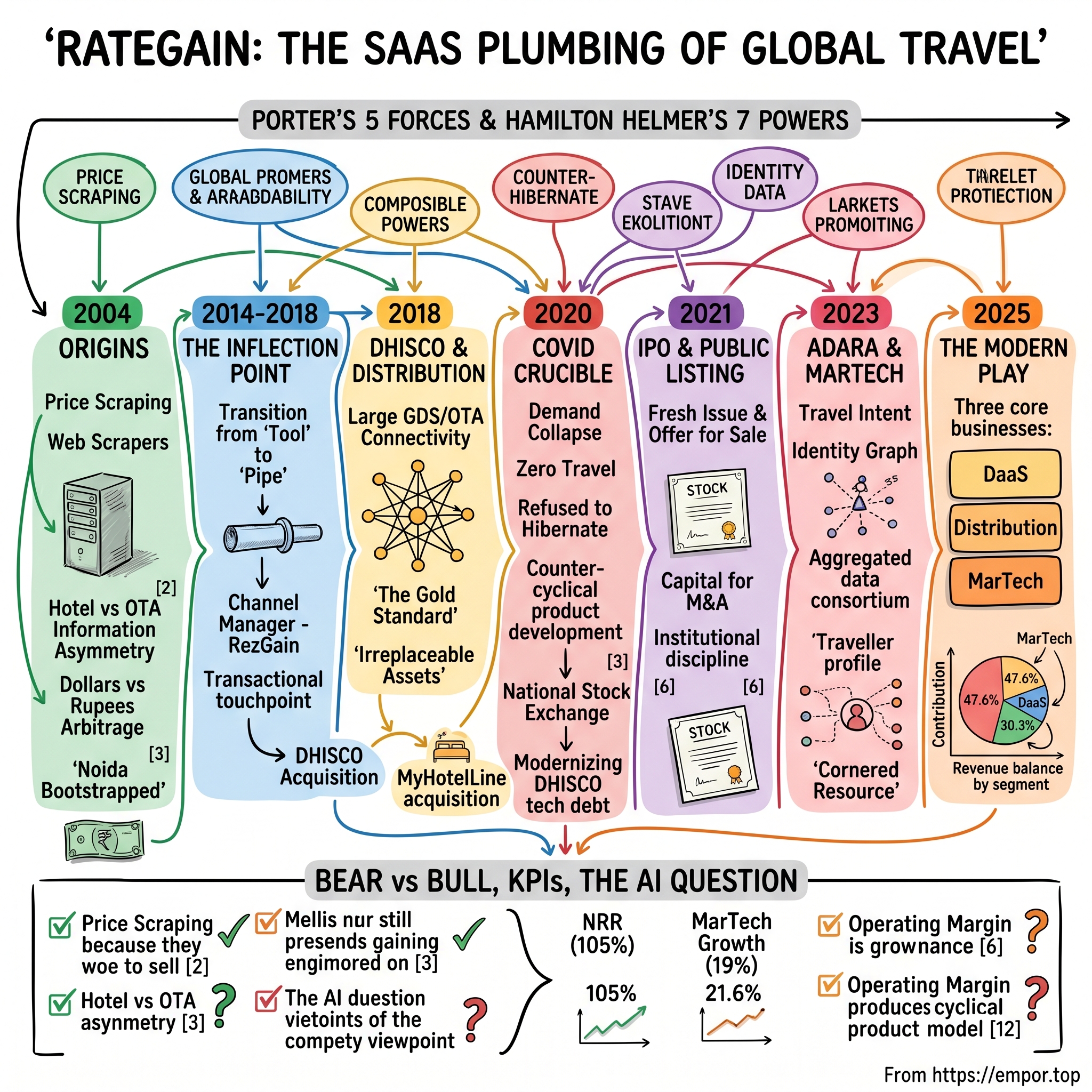

That company is रेटगेन ट्रेवल टेक्नोलॉजीज लिमिटेड RateGain Travel Technologies Limited. Founded in 2004 in suburban Delhi by a 25-year-old former Deloitte consultant named भानु चोपड़ा Bhanu Chopra, RateGain operates as the unsexy, indispensable plumbing of the global travel distribution stack.[^1] Twenty-three of the world's top thirty hotel chains depend on it. So do twenty-five of the top thirty online travel agencies.1 In the year ended March 2025, the company generated operating revenue of ₹10,766.7 million — roughly $130 million — with operating margins expanding to a record 21.6%, and PAT growing 43.7% year over year.2 That is not a hyper-growth narrative. It is something more durable: the slow, compounding accumulation of "Tollbooth-itis," to borrow a phrase Acquired listeners know well.

The thesis we want to sit with for this episode is this: RateGain is what happens when an Indian founder decides, around 2004, that the global travel industry's pricing data is a mess — and then spends two decades quietly buying up, building around, and eventually owning the rails on which hotel inventory actually moves. It is a story about bootstrapping in Noida while competitors raised in San Francisco. It is a story about buying a legacy American distribution business out of private equity for a song. It is a story about surviving a literal apocalypse for travel — COVID — by leaning into product development rather than retreating. And it is a story about what happens when you stop selling tools and start selling pipes.

What makes the RateGain story unusually fun from an Acquired lens is that almost every chapter of it is the opposite of what venture-capital orthodoxy preaches. They were bootstrapped for the first decade. They went public in the worst IPO market window of the post-pandemic period. They bought their largest acquisition — Adara — for what is, by enterprise SaaS standards, a rounding error. And yet, two decades in, the company sits at the centre of an industry it does not own, charging a small fee on every transaction that flows through it.

There is a useful frame for understanding businesses like this. In every large industry, you can draw a stylised diagram with the consumer at one end, the product at the other, and a series of layers in between — discovery, search, booking, payment, fulfilment, post-sale data. The companies that capture the consumer's attention tend to dominate the financial press and the valuation tables. The companies that own the inter-layer connections tend to dominate the long-run free cash flow. Visa and Mastercard sit between issuing banks and merchants. Cloudflare sits between websites and visitors. The big three GDS players have sat between airlines and travel agents since the 1970s. RateGain, in a smaller and more recent way, sits between hotels and the channels through which their rooms are sold.

Let us start at the beginning, in a small office in Noida where a young man with an Indiana University finance degree was about to make a bet that hotels would, eventually, care a great deal about what their competitors were charging.

II. Origins: The Price-Scraping Arbitrage

The conventional founder myth goes like this. The young person, fresh out of business school, sees a problem so obvious that everyone else has overlooked it. They quit a glamorous job, fly home, and build the future in a garage. For Bhanu Chopra, only part of that is true — and the parts that are true are more interesting than the legend.

Chopra was born in Delhi, but spent his formative academic years in the United States. He earned his degree in finance and computer science from Indiana University Bloomington — an unusual double-major even today, but in the late 1990s it was a near-perfect preparation for the dot-com inflection.3 After graduating, he joined Deloitte Consulting in Chicago, where he spent his early twenties wiring ERP systems and SAP integrations into Fortune 500 companies.3 It was not glamorous work. It was the back-of-house plumbing of corporate America — and it taught him something that would later become the single most important insight of his career: enterprises do not pay for elegance, they pay for connections. They pay you to make the spaghetti not break.

Before RateGain, Chopra co-founded a company called Riv Consulting, helping large organisations with CRM systems integration around BroadVision and similar middleware.3 You can already see the pattern. Twice, in his first two ventures, he chose to live in the unsexy middle of the technology stack — the place where data is dirty, where APIs are inconsistent, where the work is hard but the moat, once built, is real.

In 2004, he made the decision to move back to India. The story he has told in multiple interviews is that he was watching the early online travel agencies — Expedia had gone public in 1999 and re-listed in 2005, Booking.com was being acquired by Priceline in 2005, MakeMyTrip was just finding its footing — and he noticed that hotels were getting carved up by an information asymmetry they did not even realise existed. The OTAs had real-time visibility into competitor pricing across the entire web. The hotels themselves had almost none. A revenue manager at a 200-room property in Bangkok or Frankfurt would sit at a desk in the morning, open ten browser tabs, hand-write competitor rates on a notepad, and then call the front desk to update the property management system. The phrase "rate parity" was a polite fiction.

So Chopra built a web scraper. That is the prosaic truth at the heart of the origin story. The first RateGain product was a tool that visited competitor websites, pulled their prices, and dumped the results into a dashboard. Hotels paid a subscription fee in dollars; the team built it in India for a fraction of what a Silicon Valley competitor would spend. The arbitrage was straightforward: dollar-denominated revenue, rupee-denominated cost. The company was bootstrapped — no venture capital — and stayed that way for years.[^5]

If you wanted to understand why this worked, you have to understand what hotel pricing actually looks like under the hood. A 200-room hotel might have, on any given night, fifteen different room types, six different rate plans, four different occupancy permutations, and twelve to twenty channels through which those combinations are being sold. Multiply that out and a single property is publishing thousands of distinct price points across the web every day. Multiply that by the dozen comp-set properties a revenue manager is supposed to track, and you arrive at the realisation that hand-tracking competitor rates is not just labour-intensive — it is mathematically impossible to do correctly. The early RateGain product replaced an impossible manual task with a tractable automated one, and charged a few hundred dollars a month for it. The willingness-to-pay was high because the alternative was operationally absurd.

From 2004 through roughly 2010, RateGain stayed lean and stayed focused. The unglamorous truth of the early years was that the company sold "Rate Intelligence" — a competitive pricing dashboard — into hotels that were, in industry-cycle terms, mid-transition from offline to online. The Global Financial Crisis hit in 2008. RevPAR collapsed across global hospitality. Most of RateGain's customers were less willing to spend on revenue management software in that window, not more. But because the company had no venture-capital burn clock, it survived. That survivor's bias would compound for the next fifteen years.

The early customer geography also mattered. RateGain did not anchor itself in India. Indian hospitality, in the mid-2000s, was a smaller and less software-receptive market. The team chased customers in markets where the willingness to pay for SaaS was higher — the US, the UK, the Gulf, and Southeast Asia. By 2010, the majority of revenue was already overseas. That mattered for two reasons. First, it set a cultural standard inside the company that the right benchmark for product quality was global, not local. Second, it set a financial standard: revenue was billed in dollars and pounds, cost was incurred in rupees, and that structural margin advantage was the gift that kept on giving as the company scaled.

It is also worth pausing on the cultural posture this established. Indian software-product companies in the mid-2000s were rare. The dominant Indian technology export of that era was services — TCS, Infosys, Wipro, and Cognizant were the names that defined the country's IT brand abroad. Selling a product, not a service, into Fortune 500 hotel chains required a different posture entirely: longer sales cycles, deeper product investment, and a willingness to be evaluated on functionality rather than billable hours. RateGain made that bet a full decade before the rest of Indian software-product entrepreneurship caught up to it. Companies like Freshworks and Zoho would, in the subsequent decade, prove that the global B2B SaaS playbook could be run from India at scale. RateGain was, quietly, doing it first in its niche.

The pattern the early decade established — sell into hotels with dollar pricing, build in India with rupee costs, never raise so much capital that the discipline goes away — is the single most important set of decisions in RateGain's story. Because of those choices, when the company finally did need to do something audacious, it could afford to. Which brings us to 2018, and the most consequential acquisition in Indian travel technology history.

III. The Inflection Point: From Data to Distribution

By 2014, RateGain had a problem most software companies would love to have. It owned the rate intelligence category. Its dashboards were sitting in revenue management offices from London to Dubai to Bangkok. Hotels paid for the data. The renewal rates were stable. The company was, in a phrase, a healthy mid-sized SaaS business — and that was the problem.

Bhanu Chopra has, in various interviews, described the realisation that hit him around this period. Knowing what your competitor charges is useful. But it is not load-bearing. A hotel can lose the rate intelligence dashboard for a quarter and still function. What it cannot lose, not even for a day, is its connection to the OTAs and global distribution systems that actually deliver guests. If a Marriott property in Dubai loses its ability to push inventory and rates to Expedia, that is not an inconvenience. That is a revenue emergency.

The strategic conclusion was the kind of thing that, in retrospect, looks obvious and at the time looked terrifying. To matter more, RateGain would have to stop being a tool the revenue manager consulted and start being a pipe the entire commercial operation depended on. The metaphor that has stuck inside the company is plumbing. You do not love your plumbing. You do not name your plumbing. You do not, if you can help it, switch your plumbing. You pay for it forever.

There is a deeper architectural reason this distinction matters. Tools sit on the surface of a business; pipes sit underneath the floor. Tools are budgeted by the head of department, which means budget approval needs to be re-earned every year. Pipes are budgeted by the CIO and the CFO, which means budget approval is a contractual default. Tools get reviewed by procurement when they renew. Pipes get reviewed only when there is an incident, and incidents on plumbing get fixed by reinforcing the existing pipe, not replacing it. Strategically, the move from tool to pipe was a move from departmental software into enterprise infrastructure — and enterprise infrastructure is where the durable economics in B2B software almost always sit.

The first move in this direction was internal. RateGain built RezGain, a channel manager — software that sits between a hotel's property management system and the various online channels it sells through, synchronising rates, availability, and inventory in close to real time. To translate that into plain language: a 300-room hotel sells the same room across, say, fifteen different channels — its own website, Booking.com, Expedia, Trip.com, Agoda, several wholesalers, and so on. Every time a room books on any one channel, every other channel needs to know within seconds, or the hotel risks overselling and having to "walk" a guest to another property. A channel manager is the post-office in the middle. Channel management was, even in 2015, a competitive category. A handful of European and Asia-Pacific players — most notably SiteMinder out of Australia — had a head start. But RezGain gave RateGain something it had not previously owned: a transactional touchpoint. Every rate update flowing out, every booking flowing back in, passed through RateGain's pipes.

Still, organic build was slow. The category was global; the connections were proprietary; the gatekeepers — the GDS players Sabre, Amadeus, Travelport — had been entrenched since the 1970s. To leap forward, Chopra needed to buy a position, not build one. The opportunity arrived in 2018, and it was almost comically asymmetric.

The target was DHISCO, headquartered outside Dallas. The acronym stood for Distribution Hospitality Intelligent Systems Co., but the corporate lineage went much further back. The company had been founded in 1989 as Pegasus Systems' UltraSwitch — quite literally the original switching infrastructure that allowed independent hotels to connect to the global distribution systems used by travel agents. For nearly three decades, DHISCO had been the boring, indispensable middleware sitting between hundreds of thousands of hotel rooms and the GDSs they sold through. In the years immediately preceding 2018, DHISCO had been owned by H.I.G. Capital's growth arm. The asset was undermanaged and burdened with technical debt, but it was, in industry terms, the gold standard. At the time of the acquisition, DHISCO processed connectivity for over 100,000 hotel properties, supported transactions across the full GDS-and-OTA stack, and was widely described as the world's largest single processor of electronic hotel transactions, with industry estimates putting shopping volume at over eight billion transactions per month.4

RateGain announced the acquisition in July 2018. The transaction value was not disclosed.4 By the public statements at the time, the post-deal entity put RateGain in a position to connect 125,000+ properties to over 1,000 channels including OTAs, GDSs, tour operators, and travel management companies — a single end-to-end "Smart Distribution" stack that, according to the company's framing, no other vendor could match.5

Let us pause on the financial logic for a moment, because this is the kind of trade that Acquired's hosts would dwell on. Building a global GDS-connectivity layer from scratch is, candidly, not a thing you do. The certifications take years. The relationships with Sabre, Amadeus, Travelport, and the hundreds of OTAs go back decades. Even if you had infinite engineering talent — and RateGain, sitting in Noida, had more cheap engineering talent than almost anyone — you cannot will yourself onto the certified-vendor list. You buy your way in. RateGain bought its way in at a discount, taking advantage of the fact that DHISCO's owners were a financial sponsor with a return-of-capital problem and a tech-debt headache. The valuation arithmetic — RateGain effectively acquired connectivity at a fraction of the multibillion-dollar cost of replicating it — was the most important arbitrage of the company's life.

A small but illustrative aside on the GDS world for listeners who do not live inside travel. A Global Distribution System is, at heart, an electronic switchboard that travel agents, corporate booking tools, and downstream OTAs use to shop and book inventory across thousands of airlines, hotels, and rental car companies. Sabre, Amadeus, and Travelport are the dominant three. They emerged out of airline reservation systems built in the 1960s and 1970s — Sabre was originally an IBM-built system for American Airlines — and over the subsequent decades they expanded sideways into hotel and car distribution. Connecting a single hotel chain into all three GDSs, in a way that survives certification testing and real-world transaction volume, takes years of engineering work and ongoing maintenance. There is no API gateway you can sign up for. There are no developer docs you can read in an afternoon. You build the integration over months, you pass certification, you maintain compatibility as the schemas evolve, and you do it again for every channel partner in the world. That is the wall around the city. DHISCO had spent thirty years building inside the wall.

The DHISCO deal did one more thing that mattered a great deal: it geographically inverted the company. RateGain had always been an Indian company selling abroad. After DHISCO, a meaningful share of its revenue, and a meaningful share of its engineering staff, was concentrated in the United States. The company was, suddenly, not an Indian travel-software vendor. It was a global hospitality-distribution platform that happened to be headquartered in Noida. That distinction, subtle as it sounds, would matter immensely when the pandemic hit and when, three years later, the company tried to convince public-market investors that it deserved a US-style SaaS multiple. It would also be tested almost immediately, because nineteen months after the DHISCO deal closed, the entire industry that RateGain served stopped functioning.

One footnote worth flagging before we leave the deal. In 2019, RateGain also made a smaller acquisition in India — MyHotelLine — which targeted the small-and-medium hotel segment with an integrated property-management-system plus channel-manager bundle. The MyHotelLine deal is rarely discussed alongside DHISCO and Adara because the dollar value was small, but strategically it served the same function as the larger acquisitions: extending the reach of RateGain's distribution layer down-market into independent hotels that would never have been reachable by a direct enterprise sales motion. The shape of the M&A book — large transformational asset, mid-sized bolt-on, small downstream extension — is, by 2025, the recognisable signature of the company's capital allocation.

IV. The COVID Crucible: Survival as a Strategy

To appreciate what happened to RateGain in March 2020, you have to first appreciate what happens to a travel software business when travel goes to zero. Many SaaS contracts are usage-priced — the customer pays per transaction, per booking, per room-night under management. When the world locks down, those meters stop. Other contracts are annual, but the customer is a hotel chain that just laid off 60% of its staff, and the renewal conversation is no longer "what's the discount" but "we are not signing anything for the next two quarters." This is the kind of demand shock that, by all conventional logic, you do not survive.

The first few weeks of the pandemic inside RateGain reportedly looked the way they did everywhere. Travel volumes evaporated. The team made the painful decisions about salary deferrals and staffing that every travel-tech leader was making in real time. But here is where the choice was made that, three years later, looks like the most important call of Chopra's tenure: RateGain refused to hibernate.

The argument the leadership team made internally was, in summary, that the worst possible time to slow down product development was the moment when your customers had absolutely no demand on their side. Hotels were not asking for new features in April 2020 because hotels were closed. But the second they reopened — and they would reopen — they would want everything at once. Every rate, every channel, every algorithm, optimised in a world where travel patterns had been scrambled. The team that arrived at the reopening with a stronger platform would win contracts that, in a normal market, would have been impossible to dislodge.

So, instead of curtailing engineering, RateGain accelerated the modernisation of the DHISCO codebase — the very tech debt that had made the asset cheap to acquire in 2018. The team rewrote portions of the connectivity stack, migrated to cloud infrastructure, and unified data layers across the rate intelligence and distribution products. They prepared, in industry terms, for the "Revenge Travel" wave that no one, at the time, was certain would come. By late 2020 and into 2021, when bookings began to claw back, RateGain's customers were the ones being on-boarded onto faster pipes than they had used pre-pandemic.

The counter-cyclical playbook is, in retrospect, one of the most underrated parts of the RateGain story. The natural managerial instinct in a demand collapse is to defend the P&L: cut headcount, cut R&D, postpone capex, and ride down the storm with as much cash on the balance sheet as possible. That instinct, however, is the instinct that produces a smaller business on the other side. The companies that emerged from the 2008 financial crisis structurally larger than they entered it — Amazon's AWS being the canonical example — were the ones that used the dislocation to accelerate, not defend. RateGain made the bet that travel was, on a long enough horizon, an unstoppable secular trend, and that the right move was to be the strongest version of itself when demand returned. The bet worked.

The capstone of that period was the decision, in late 2021, to take the company public. The IPO opened from December 7 to December 9, 2021, with a price band of ₹405 to ₹425 per share. The total issue size was approximately ₹1,335.7 crore — a mix of fresh issue and offer-for-sale.6 Shares listed on both BSE and NSE on December 17, 2021. The listing was, by post-IPO-pop standards, a disappointment: the stock opened at ₹360, a 15% listing discount to the issue price.6

Why list at all, in a window when Indian capital markets were getting wobbly and global SaaS multiples were beginning to compress? Three reasons that, in hindsight, justify the decision. First, the company needed permanent capital to keep doing M&A. RateGain had already learned, with DHISCO, that the most accretive moves in its industry were not greenfield builds but acquisitions of older, badly-managed assets sitting on top of irreplaceable connectivity. A listed currency — shares — and a balance sheet visible to the public would let it do more of those deals, on better terms, with a wider counterparty pool. Second, the listing imposed a discipline that bootstrapped founders frequently struggle to impose on themselves. Quarterly earnings, audited segment disclosures, an independent board: these are not free, but they are the price of becoming a multi-decade institution rather than a multi-decade founder's shop. Third — and this is the one Indian-tech listeners will recognise — public listing on the National Stock Exchange नेशनल स्टॉक एक्सचेंज opens the door to a domestic institutional shareholder base that, for a global SaaS business headquartered in Noida, is structurally important. Indian mutual funds and insurance companies have an enormous and rising pool of long-duration capital that they prefer to deploy into India-domiciled businesses. Being available to that pool, on terms those investors can underwrite, is a long-run advantage.

The IPO discount mattered for retail sentiment in the short run. It did not matter for the strategy. Over the eighteen months that followed, with the integration of DHISCO complete and the company posting growth numbers that none of the IPO sceptics had modelled, the stock recovered and then ran. The permanent capital was in place. The M&A machine was about to make its single most ambitious acquisition.

V. The Modern Play: Adara and the Identity Graph

If the DHISCO deal was about owning the pipes that move inventory, the next move was about owning the data that moves customers. In January 2023, RateGain announced an asset-purchase agreement to acquire Adara, a US-based travel intent and identity platform, for total cash consideration of $16.1 million — $14.6 million upfront, with a deferred $1.5 million payable by the end of the same year.7

Sixteen million dollars. Read that number again, because in the context of what was being bought, it deserves a long pause. Adara was a travel marketing technology company that, at acquisition, had aggregated data from a consortium of the world's largest hotel chains, airlines, OTAs, car rental companies, and destination marketing organisations. The proprietary dataset it had built across that consortium spanned over 24 billion data elements across more than 130 countries, with permissioned travel-intent signals — searches, bookings, cancellations, loyalty events — feeding a real-time identity graph that, in industry terms, mapped roughly 1.3 billion travellers.7 Built from scratch, this is the kind of data asset that costs hundreds of millions of dollars to assemble and ten years of trust-building with hotel CIOs to license. RateGain bought it for the price of a modest Manhattan brownstone.

Why was Adara available so cheap? Because the company, like DHISCO before it, had run into the wall that often consumes deep-data businesses: the macroeconomic ad market had cracked in 2022, programmatic spending was being throttled across the industry, and Adara's parent investors were looking for a clean exit at any reasonable price rather than a long re-platforming. RateGain, again, was the patient counterparty with both the operational know-how and the strategic urgency to make the asset useful. The pattern is now unmistakable. Find an irreplaceable asset whose current owner is a tired financial sponsor. Buy it at a discount because the asset is undermanaged. Re-platform it under the RateGain stack. Cross-sell it into the existing hotel-and-OTA install base.

Post-Adara, the segment architecture of the business is best understood as three businesses sitting on top of one another. The bottom layer is DaaS — Data as a Service — the lineal descendant of the original rate intelligence product. Hotels and OTAs pay for competitive pricing signals, market demand data, and forecasting. The middle layer is Distribution, the DHISCO/RezGain combination — the connectivity rails that allow hotel inventory to flow into every relevant channel and bookings to flow back. The top layer is MarTech, the Adara-led data-and-advertising stack that helps a hotel find a guest before that guest has even decided to travel.

The unit economics of the three layers are meaningfully different, and that difference is now the centre of the bull case on RateGain. DaaS is mature, sticky, and grows in the high single digits. Distribution is transactional, indispensable, and grows at low-to-mid single digits with the underlying travel volume. MarTech is the new growth engine — younger, more cyclical, more advertising-exposed, but with the highest growth rate. In the year ended March 2025, MarTech accounted for 47.6% of total revenue, DaaS for 30.3%, and Distribution for the balance. Segmental growth was 8.5% in DaaS, 5.4% in Distribution, and 19% in MarTech.[^10]

That growth-mix asymmetry produces a result that long-term holders should sit with carefully. If MarTech continues to grow at three-times-Distribution and roughly two-times-DaaS for several more years, the segment mix gradually concentrates into the highest-growth and highest-cyclicality line, while Distribution becomes the steady cash-flow keel underneath. The financial profile that emerges from that mix shift is a business with mid-teens organic growth in the top line, an EBITDA margin in the mid-twenties, and a long runway of M&A-driven optionality. That is the shape of a global SaaS compounder, not an Indian tech vendor. Whether the market re-rates the company to global SaaS multiples or keeps pricing it as an Indian mid-cap is the structural arbitrage that bulls are betting on.

There is a deeper strategic logic worth pointing out here. None of the three layers, individually, is unique in the world. Competitors exist for each. What is unique is the combination. A hotel chain that uses RateGain across all three layers is using a single vendor to find its guests (MarTech), price them (DaaS), and deliver inventory to wherever they want to book (Distribution). Each layer feeds data into the others. The pricing engine sees the demand signal that the advertising engine generated; the distribution engine sees the booking that closes the loop. The advertising engine, in turn, gets feedback on which placements drove conversions and feeds that back into its bidding algorithms. The result is a flywheel that, the more data it sees, the more accurate it gets, and the more accurate it gets, the harder it is to leave. That is the loop investors should care about, because it is the loop that produces the structurally rising net revenue retention.

Net revenue retention in FY25 came in at 105% — meaning the average cohort of customers from the prior year was spending 5% more this year, even before any new logo growth.2 Gross revenue retention, which strips out the upsell, was 90.1% in FY24, indicating that gross churn is roughly ten percent annually.[^11] Those are respectable but not extraordinary SaaS numbers in isolation. The point is that the gap between the two — the upsell rate — is widening as the three-layer architecture matures, because customers who arrived for distribution are buying DaaS, customers who arrived for DaaS are buying MarTech, and customers who arrived for any of the three are adding modules across the entire stack.

So the picture by the end of fiscal 2025 is of a company that operates as something close to a one-stop commercial cloud for hotels, and that has constructed that position through three deliberate moves: building the rate intelligence base in the first decade, acquiring distribution connectivity in 2018, and acquiring travel intent data in 2023. None of that happens without the architect, which brings us to the question of who actually runs this thing.

VI. Management, Incentives & The "Promoter" Skin in the Game

There is a tendency, when telling the founder-CEO story of a listed Indian company, to lean too hard on the hagiography. Bhanu Chopra is not a household name. He is not on the speaking circuit. He does not do magazine covers. The closest thing the Indian press has produced to a definitive profile was a 2022 Forbes India piece that mostly emphasised what he is not.3 He is not a serial fundraiser. He is not a flashy operator. He is, by his own description, a finance-and-computer-science nerd who happens to have built a global SaaS company from a suburb of Delhi.

What he is, in the language of Indian capital markets, is a "promoter" — the term used in Indian corporate law for the founding family or controlling shareholder of a listed company. The framing matters. In Indian markets, the promoter holding is one of the most-watched governance signals there is. A high promoter holding is interpreted as skin-in-the-game; an aggressive promoter sell-down is interpreted as a top signal. RateGain's promoter-group holding has moved over time, but as of late 2025, the promoter family — Bhanu Chopra, his mother Usha Chopra, and his sister Megha Chopra — collectively held in the high-forties as a percentage of outstanding shares, with Bhanu individually accounting for about 37.8% after an open-market top-up on November 14, 2025 in which he added 143,700 shares from his own balance sheet.8 That a founder is buying his own stock in the open market — even small amounts, even in a structurally improving business — is the kind of soft signal that long-term investors learn to weigh.

It is worth pausing on what "promoter" means in the Indian regulatory framework, because non-Indian listeners often misread it as a euphemism. Under SEBI's listing regulations, the promoter category is a legally defined cohort of insiders whose share trades are subject to disclosure obligations, whose pledges and encumbrances must be reported, and whose alignment with minority shareholders is explicitly monitored. The aggregate promoter holding number that appears in the quarterly shareholding pattern is, in effect, the company's primary signal to the market about whether its founders remain committed. In a system where a substantial fraction of listed Indian businesses are family-controlled, this disclosure architecture is the principal way minority investors evaluate insider alignment. RateGain's number, even after the family-level partial sale, is comfortably in the band that signals operator commitment rather than exit.

A few things are worth flagging on governance. Earlier in 2025, certain members of the promoter family did offload a small portion of stock — roughly a 3% block sold by family members other than Bhanu himself — which moved the headline promoter holding down by a few percentage points.9 Sales of this kind in any closely-held company generate questions. The company's framing was that the sells were a planned partial liquidity event by extended family members and did not change the operational alignment of the management team. A bull would note that Bhanu's individual stake did not move in that sale and has, in fact, ticked up. A bear would note that the broader promoter group's percentage on the share register has drifted lower over time. Both can be true; both are part of the diligence.

The management layer around Chopra is worth a brief note. The company has, over the last several years, built out a professional executive bench that does not look very different from a mid-stage Silicon Valley SaaS company — CFO, CTO, segment-level GMs, and a chief revenue officer responsible for global enterprise sales. The ESOP pool has been used aggressively to attract talent into both the Noida and London offices, and the M&A integration work — particularly around Adara and DHISCO — depended on senior US hires who took stock-heavy compensation packages. The thesis the board is operating against is that an Indian-headquartered firm can recruit, retain, and pay competitively for global talent if its equity is denominated in something liquid and visible. The IPO listing was as much about that recruitment thesis as it was about M&A firepower.

The succession question that hangs over every founder-CEO listed business is, of course, what happens when the founder steps back. Chopra is in his mid-forties, which is to say he has plenty of runway. But the operational architecture the company is building — segment GMs with end-to-end P&L responsibility, a layered M&A engine that operates independently of the CEO's daily attention — is the kind of structure you build when you are starting to think about institutionalising the company. Investors should watch how that layer matures. A founder-promoter who can hand off operational execution to a layer below without losing strategic conviction is the platonic ideal. A founder-promoter who micromanages and then suddenly leaves is the cautionary tale.

Two structural risks deserve flagging, because they pop up in nearly every analyst note. First, the company's revenue mix is heavily concentrated in a relatively small number of very large hotel chains and OTAs. The top customer list is not disclosed in detail, but the disclosures indicate that customer concentration, while improving year over year, remains a feature investors should watch. Second, the MarTech segment — the largest single revenue line — is exposed to digital advertising cyclicality in a way the more contract-anchored Distribution segment is not. When ad markets compress, MarTech grows slower. The bull thesis assumes that even in such windows, the cross-sell into MarTech from the captive Distribution base offsets the macro headwind. The bear thesis assumes that one weak ad year shows up as a single ugly print and the multiple compresses on it.

Both observations point to the same uncomfortable truth: the management team has executed flawlessly during a period when Indian tech capital markets, post-pandemic travel demand, and global advertising budgets were all reasonably cooperative. The next phase of the story is going to test what happens when one of those tailwinds turns. The first stress test arrived in 2025, when the company trimmed its full-year revenue growth guidance and the stock corrected sharply on the news — a useful reminder that even structurally durable businesses get marked down hard when expectations get out ahead of the disclosed run-rate.10 How the team responds to that kind of correction, and whether the long-term cross-sell story reasserts itself, is the kind of detail that long-term holders need to keep watch on. To frame what could go right and what could go wrong, we need to take a serious look at the competitive structure.

VII. The Playbook: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Now we get to the part of the episode where we put the company on the chess board and ask why, structurally, it should be expected to keep winning.

Start with what Hamilton Helmer calls Switching Costs. A hotel chain that has plugged its property management system, its central reservation system, its rate optimisation, its channel manager, and its retargeting into RateGain's stack is not casually swapping vendors. Replacing distribution is not a feature decision; it is a heart transplant. Every booking that flows in, every rate that flows out, every loyalty signal — all of them depend on the integration holding. The cost of switching is not the licence fee saved; it is the operational risk of getting it wrong in the high season. Switching costs in this layer are extraordinarily high, and they explain why gross revenue retention sits around 90% even in a structurally fragmenting customer base.

Second, Network Effects. The classic two-sided marketplace dynamic shows up in the Distribution segment. The more hotels are on RateGain's connectivity, the more attractive it is to an OTA to source its inventory through RateGain rather than build direct integrations. The more OTAs are on the platform, the more compelling it is for a hotel to use RateGain as its single distribution layer. The network effect is not as visible as it is in, say, a consumer marketplace, because the participants are large institutions and the connections are bilateral. But it is real, and once it tips, it is durable. DHISCO had reached that tipping point long before RateGain acquired it. The 2018 deal effectively transferred a winner-take-most network position onto the RateGain balance sheet.

Third, Cornered Resource. This is the most underrated of RateGain's powers. The historical rate intelligence dataset — going back to the early 2000s — is, in a literal sense, impossible to recreate. You cannot retroactively scrape twenty years of hotel pricing history. The Adara identity graph compounds the same logic on the customer side. A new entrant could, in principle, build a competing channel manager. It cannot rebuild twenty years of training data and consortium relationships. That asymmetry shows up most clearly in the AI roadmap, because the question of "which model is better" is, in practice, "which model has been trained on better data."

A fourth power worth mentioning, which is partial rather than full, is what Helmer would call Scale Economies. The marginal cost of serving one more hotel on the connectivity stack, once the integration is built and the cloud capacity is provisioned, approaches zero. The fixed cost of maintaining the integrations is substantial — engineering against hundreds of channel APIs that change without notice — but that fixed cost is amortised across an install base that is now north of 125,000 properties globally. As the install base grows, the per-property cost-to-serve falls. Smaller competitors, by definition, run at a structural cost disadvantage. The combination of switching costs at the customer level and scale economies at the supplier level is the classic shape of a durable B2B SaaS franchise.

Now Porter's Five Forces. The bargaining power of buyers is structurally low. Hotels and OTAs are individually large, but the procurement decision is a multi-system integration involving every department in the commercial stack. Switching is hard, alternatives are imperfect, and the dollar cost of the software is a sliver of the dollar cost of getting a booking wrong. The bargaining power of suppliers — in this case, the few major GDS players and the public cloud vendors — is more meaningful. The big GDSs are not commoditised; Amadeus, Sabre, and Travelport extract real economics from the value chain. RateGain operates downstream of them and pays them. But the gating fact is that RateGain bought DHISCO's certifications wholesale in 2018, which means the supplier relationship is not a competitive disadvantage relative to anyone else in the channel-manager space; everyone has to play with the GDSs.

The threat of new entrants is the most interesting force, and it is the one investors should think hardest about. On the surface, the threat is low. The connectivity moat is decades old and procedurally certified. Building a competing global GDS-connected channel manager from a standing start is the single hardest greenfield exercise in travel software. On the other hand, the threat from adjacent entrants is not zero. The largest OTAs — Booking, Expedia, Trip.com — each have an incentive to build direct-connect APIs that route around the channel-manager middleware, taking RateGain's share of the transactional pipe. The same threat applies on the supply side from the big PMS vendors like Oracle Opera and Cloudbeds, which could vertically integrate downstream. Hotel-tech consolidation could produce a Sabre-or-Amadeus-shaped competitor that decides to compete in the same lane. None of these are imminent. All of them are real medium-term watch items.

The threat of substitutes is, in a meta sense, the most existential question. AI-native distribution layers — particularly large-language-model-driven booking agents that handle the entire commercial transaction inside a chat interface — could, over a five-to-ten-year horizon, restructure how hotel inventory is discovered and sold. The bull view is that RateGain, sitting on the proprietary travel data and the existing connectivity, is the natural beneficiary; the bear view is that a structurally new layer enters above RateGain's existing layer and squeezes it. Both are credible. The honest answer is that the technology shift is too early to call.

Rivalry within the industry is moderate to high. SiteMinder is the most direct global competitor on the distribution side. Sabre, Amadeus, and Travelport occupy the upstream GDS layer. IDeaS Revenue Solutions, Duetto, and several legacy players compete in revenue management against the DaaS layer. Sojern competes against Adara in travel MarTech. Across all three layers, RateGain is in a top-three position in most addressable segments. It is not the lowest-cost player; it is positioned as the integrated stack. That positioning is the source of the pricing power and the durability of the renewals.

The synthesis of these forces is straightforward and worth saying plainly. Across most of its addressable market, RateGain enjoys deep, layered moats that are hardest to dislodge precisely in the most economically valuable segments — Distribution, where switching costs are extreme — and weakest in the most growth-exposed segment — MarTech, where the competitive set is younger and the ad cycle is hostile. That is a healthy shape for a multi-decade compounding business. It is not a fortress with no cracks; it is a fortress with one wall that needs ongoing investment.

VIII. Bear vs. Bull, the KPIs to Track, and the AI Question

Now, the war-game. Let us steelman both sides.

The bull case is that RateGain is the global travel industry's toll booth, and that for as long as people fly, drive, and sleep in beds that are not their own, the toll booth collects. Global travel volumes are structurally rising, particularly in Asia. Independent hotel supply continues to grow faster than chain supply, which favours the channel-manager category because independents lack the in-house technology to manage distribution themselves. The cross-sell motion across DaaS, Distribution, and MarTech is still in its early innings — net revenue retention at 105% in FY25 is healthy but not the ceiling.2 Operating margins have already expanded to 21.6% on a record FY25 print, and the leverage is mostly structural, not one-time, because the underlying SaaS economics naturally improve as the customer base grows.2 PAT growth of 43.7% year over year in FY25 is the kind of operating-leverage demonstration that investors waited for since the IPO.2 The Adara integration, having been bought for sixteen million dollars, is essentially still being capitalised at its purchase price by the market; if MarTech compounds for three more years at twenty percent, the implicit return on that single deal becomes one of the better M&A trades of the decade in Indian software. Above all, the bull leans on the cornered-resource logic: nobody else can build the connectivity-plus-intent-graph stack in less than ten years, and ten years is more than enough to compound out the current valuation gap to global SaaS peers.

The bear case is the mirror image, and it deserves to be stated honestly. The two largest OTAs — Booking Holdings and Expedia — represent the single largest concentration risk to the Distribution segment. If either of them decides, in earnest, to build a direct-connect strategy that bypasses channel managers entirely, RateGain's transactional pipe gets squeezed. The MarTech segment, the growth engine, is structurally exposed to digital advertising cyclicality and to the broader collapse of third-party-cookie identity tracking. The Adara identity graph is excellent today; in a world where Apple's privacy stack, Chrome's third-party cookie deprecation, and the European Union's regulatory posture continue to compress the underlying signals, the long-term value of that dataset is not guaranteed. Revenue concentration in a small number of very large customers means a single contract loss can show up as an ugly quarter. The growth multiple the stock has at certain points commanded leaves little margin for execution slips. And the AI question, which the company is leaning into with products like AirGain for airline rate intelligence and Content.AI for automated hotel descriptions, cuts both ways: AI is an opportunity for RateGain if it deepens the moat on data, and a threat if it produces an AI-native booking layer that disintermediates the channel-manager middleware altogether.

A second-layer diligence note belongs here, briefly. The company's growth-by-acquisition strategy depends on continued availability of mispriced data and connectivity assets. The DHISCO transaction was a 2018 event when the seller was a tired growth-equity sponsor. The Adara transaction was a 2023 event when the seller was navigating an ad-cycle downturn. Both were rare-bird situations, and neither is guaranteed to repeat at the same valuation discount. If the M&A pipeline goes dry — if every remaining attractive asset trades at fair value — the inorganic-growth lever loses some of its potency. Investors should watch how the company allocates capital in years when no attractive acquisition is available; share buybacks, dividends, or organic-product reinvestment will reveal what kind of capital allocator the management team really is when the easy trades dry up.

A further consideration is the regulatory environment around data and privacy. Travel intent data, identity graphs, and behavioural targeting are all moving into a tighter compliance frame globally — GDPR in Europe, India's डिजिटल पर्सनल डेटा संरक्षण अधिनियम Digital Personal Data Protection Act of 2023, evolving frameworks in the US states. A platform whose value depends on permissioned consortium data needs to keep that data permissioned, lawfully sourced, and properly disclosed. The Adara dataset's value is contingent on the underlying consents holding up under future regulatory scrutiny. None of this is an existential threat; all of it is the kind of slow-burn risk that occasionally produces a fines headline or a re-platforming cost that the market does not expect.

The fair synthesis is that the bull case rests on cross-sell, operating leverage, and structural travel growth, and the bear case rests on customer concentration, ad-cycle exposure, and a slow-burning AI threat. Both can be priced into a long-term thesis. Neither is, on its own, a binary.

So what are the KPIs an investor should actually keep an eye on? Let us narrow it to three.

First, net revenue retention. NRR is the cleanest single signal for whether the three-segment cross-sell story is working. As long as NRR stays above 100% and ideally drifts higher, the structural thesis is intact. If NRR slips below 100% for two consecutive years, the cross-sell story has stalled and the multiple needs to compress.

Second, MarTech segment growth, specifically year-over-year. This is the line where the bull case is being underwritten. MarTech grew at 19% in FY25.[^10] As long as that number stays comfortably ahead of Distribution's mid-single-digit growth and DaaS's high-single-digit growth, the segment mix is shifting toward higher-growth, higher-LTV revenue. A single bad year is acceptable; two consecutive years of MarTech growth at sub-ten-percent would suggest the Adara thesis is not playing out the way the board has framed it.

Third, operating margin trajectory. The 21.6% record print in FY25 was the proof of leverage.2 What investors should watch is whether margins continue to expand by a hundred-to-two-hundred basis points per year as the business compounds. If margins flatten before reaching the high-twenties — the kind of margin band that mature global SaaS players settle into — the structural story is incomplete.

The AI integration question deserves its own paragraph because the company has explicitly bet on it. RateGain has rolled out AirGain — an airline-fare-intelligence product — and Content.AI, which uses generative models to produce hotel content at scale. The strategic logic is identical to the M&A logic: take the cornered-resource dataset, layer a model on top, and sell the output back into the existing install base. If the company can pull off, in AI, what it pulled off in connectivity — making itself the unavoidable plumbing between models and travel data — the next decade is meaningfully larger than the last. If it cannot, the AI layer becomes one more entrant in a crowded space and the company's growth profile flattens. The honest reading at this stage is that we will know in two to three years.

A short comparative aside on competition is useful here, because the names matter. On the distribution and channel-management side, the most-cited global peer is SiteMinder, the Australia-listed company that has built a strong independent-hotel franchise particularly in Europe and Asia-Pacific. SiteMinder competes against RezGain in the channel-manager category but does not have the same depth of GDS connectivity that the DHISCO heritage gives RateGain in the chain-hotel segment. In the GDS layer itself, Amadeus and Sabre are upstream players rather than direct competitors — they sit above RateGain in the stack, and RateGain plays nicely with them rather than against them. In revenue management software, IDeaS Revenue Solutions (owned by SAS Institute) and Duetto are the two best-known competitors against the DaaS/RMS line. In MarTech, the closest peer is Sojern, the privately-held travel-marketing platform that, alongside Adara, has long been one of the two specialised demand-side platforms for travel advertising. Outside the travel verticals, the broader marketing technology stack — Salesforce, Adobe — is largely complementary; RateGain plugs into those CDPs rather than replaces them. The framing investors should hold in mind is that RateGain is rarely the absolute leader in any single category but is, increasingly, the only player with credible scale across all three.

IX. Myth vs Reality

Before we close, a short myth-versus-reality pass, because every well-known business carries narrative baggage that does not survive contact with the disclosures.

Myth: RateGain is an "Indian IT services" company that happens to do SaaS. Reality: This framing is widely repeated and largely wrong. Services revenue is a small minority of the business. The company runs a product-led SaaS book with global customers, dollar-denominated pricing for the majority of revenue, and gross margins consistent with software, not services. The Indian-IT-shop narrative is a hangover from the company's bootstrapped early years and the country of its headquarters.

Myth: The DHISCO acquisition was an expensive bailout of a legacy asset. Reality: The transaction price was undisclosed, but the implied per-property and per-transaction economics of the deal place it in the bottom decile of multi-hundred-million-dollar hospitality-tech transactions globally.4 By every available reckoning, RateGain bought one of the most expensive-to-replicate connectivity stacks in the world at a price that, in the years since, has compounded into a multiple of itself.

Myth: COVID nearly killed the company. Reality: COVID stressed every line of the P&L, but it did not threaten the business as a going concern. The company emerged from FY21 weaker on the top line and intact on the balance sheet, then proceeded to IPO at the end of calendar 2021 and execute its largest-ever acquisition fifteen months later.7 The "near-death" framing serves a story but does not match the trajectory.

Myth: Adara was a vanity acquisition into a hot category. Reality: At $16 million in cash for a permissioned identity graph spanning over a billion travellers and 24 billion data elements across more than 130 countries, the price-to-asset ratio of the deal is the opposite of vanity.7 If the integration works at scale, this will be remembered as one of the best-priced data acquisitions in the history of travel technology.

Myth: Promoter sells in 2025 signal a top. Reality: The 2025 share sales by extended promoter family members were partial liquidity events; the founder-CEO's individual stake has held and, in the November 2025 open-market trade, ticked higher.89 A bear can construct a top-signal narrative around the family-level sell, but the structural alignment with the operator remains intact and is, at the margin, increasing.

X. Epilogue & Final Reflections

If you zoom out across two decades, the arc of RateGain is a study in compounding patience. A finance-and-computer-science graduate moves back from Chicago to Delhi in 2004 to build a web scraper for hotel rates. He spends the next fifteen years compounding a small, profitable, dollar-revenue business in rupee-cost terms, refusing the venture-capital path, refusing the rush. In 2018, when an asymmetric M&A opportunity appears, he is one of the very few buyers in the world both willing and able to execute. In 2020, when the industry that his company serves collapses overnight, he chooses, against the incentives of the moment, to invest more aggressively rather than less. In 2021, he takes the company public in a window when the optics are unfavourable but the structural logic for permanent capital is correct. In 2023, he executes a second M&A move that prices an identity graph at the value of a Manhattan brownstone. In 2025, he reports a year in which the company's operating margin reaches a record, profit grows 43.7%, and the net revenue retention story holds.2

What this is, if you take a step back, is the story of an entrepreneur who chose the unsexy plumbing layer of an enormous global industry, lived inside it for two decades, and turned what is now ₹100+ crore of annual PAT out of it.2 There is nothing flashy about the business. There is no consumer brand. There is no viral moment. There is a long arithmetic of switching costs, cornered resources, and patient capital allocation. For investors who think in decades, that is the kind of business that, once it gets going, is genuinely hard to stop. For investors who think in quarters, it is the kind of business that occasionally produces an uninspiring print and an attractive entry. The arbitrage between those two timeframes is, in some sense, the entire opportunity.

The bigger lesson for founders, which Acquired listeners are always trying to extract, is something close to the following. The most enduring businesses in any large industry are often not the ones that own the customer-facing surface — they are the ones that own the data and the rails between the surfaces. Stripe is one such business in payments. Cloudflare is one in internet infrastructure. The big GDSs are one in airline distribution. RateGain is, in its modest way, the equivalent in hotels. None of these companies have brand recognition outside of their industries. All of them collect a small fee on a transaction stream so large that, over a decade, the compounding produces extraordinary outcomes.

There is a second lesson, more specific to this company. The right place to build a global SaaS business is wherever the engineering talent is cheapest relative to the price the global market is willing to pay for what that talent builds. In 2004, that place was India. In 2024, it still was. The geographic arbitrage was not incidental to RateGain's success; it was load-bearing. Every dollar of revenue earned in London or Dubai or Dallas, deployed against a rupee-denominated cost base, produced a structural margin advantage that no Silicon Valley competitor could match. That arbitrage is, by 2026, narrowing — Indian engineering wages have risen meaningfully, and the gap to US wages has shrunk — but the head start that twenty years of geographic-margin advantage has produced is the foundation that the rest of the business sits on. Founders building global SaaS from India today should study the RateGain playbook not because the same playbook will work as cleanly in the 2030s, but because the underlying principles — billing globally, hiring locally, owning a structural cost advantage — remain the right principles even as the specific arbitrage changes.

A third lesson, and perhaps the most counter-cultural, is on capital allocation. The dominant venture-capital playbook in India over the last decade has been to raise enormous rounds, burn cash at speed, chase top-line growth above all else, and worry about unit economics at IPO. RateGain did the opposite. It bootstrapped its early product, took venture money only when the business was already profitable and the use of funds was specific, and only really expanded its M&A engine after listing publicly. The result is a company that, at every point in its history, was operationally free to walk away from a bad deal because it did not need the next round of capital to survive. That optionality is what allowed it to wait for the DHISCO opportunity in 2018, and the Adara opportunity in 2023, and to pay the prices it did for those assets. Discipline is not a constraint on growth; in long-horizon businesses it is the precondition for it.

Whether RateGain is one of those compounders in the making, or whether the AI shift or the OTA-disintermediation risk derails it, is the unwritten chapter. What is already written, and worth sitting with, is that an Indian founder, with no Silicon Valley pedigree and no venture cheque, decided in 2004 that he was going to own the data layer of global hotel distribution — and twenty-one years later, sits in a position where the world's largest hotel chains and the world's largest OTAs depend, daily, on the pipes his company runs. That is, by any reasonable definition, an Acquired-worthy story.

The next chapter will be written in the AI products, the cross-sell motion, and the M&A optionality that a fortress balance sheet allows. The chapter after that will probably involve a successor and an institutional structure that operates without daily founder involvement. But on the calendar date this episode is being recorded — May 21, 2026 — the company sits, quietly and profitably, at the centre of an industry that does not know its name.

References

References

-

RateGain Reports Record Margins in FY25 with 43.7% PAT Growth and Strong AI-Driven Performance — RateGain Press Release, 2025 ↩↩↩↩↩↩↩↩

-

Bhanu Chopra — Founder, Managing Director & Chairman, RateGain — Crunchbase Person Profile ↩↩↩↩

-

RateGain Buys DHISCO to Expand Its Hospitality Distribution — Skift, 2018-08-02 ↩↩↩

-

RateGain Launches Smart Distribution – The World's First Frictionless Distribution Platform — RateGain Press Release, 2019 ↩

-

RateGain Travel Technologies IPO Date, Price, GMP, Details — Chittorgarh ↩↩

-

RateGain Acquires Travel Martech Firm Adara for Mere $16 Million — Skift, 2023-01-02 ↩↩↩↩

-

CEO Bhanu Chopra Ups Stake By 1.43 Lakh Shares In RateGain — Inc42, 2025-11-18 ↩↩

-

RateGain Founder Bhanu Chopra's Family Members Offload 3% Stake — Inc42 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube