The Ramco Cements: Building South India's Cement Empire

I. Introduction & Episode Roadmap

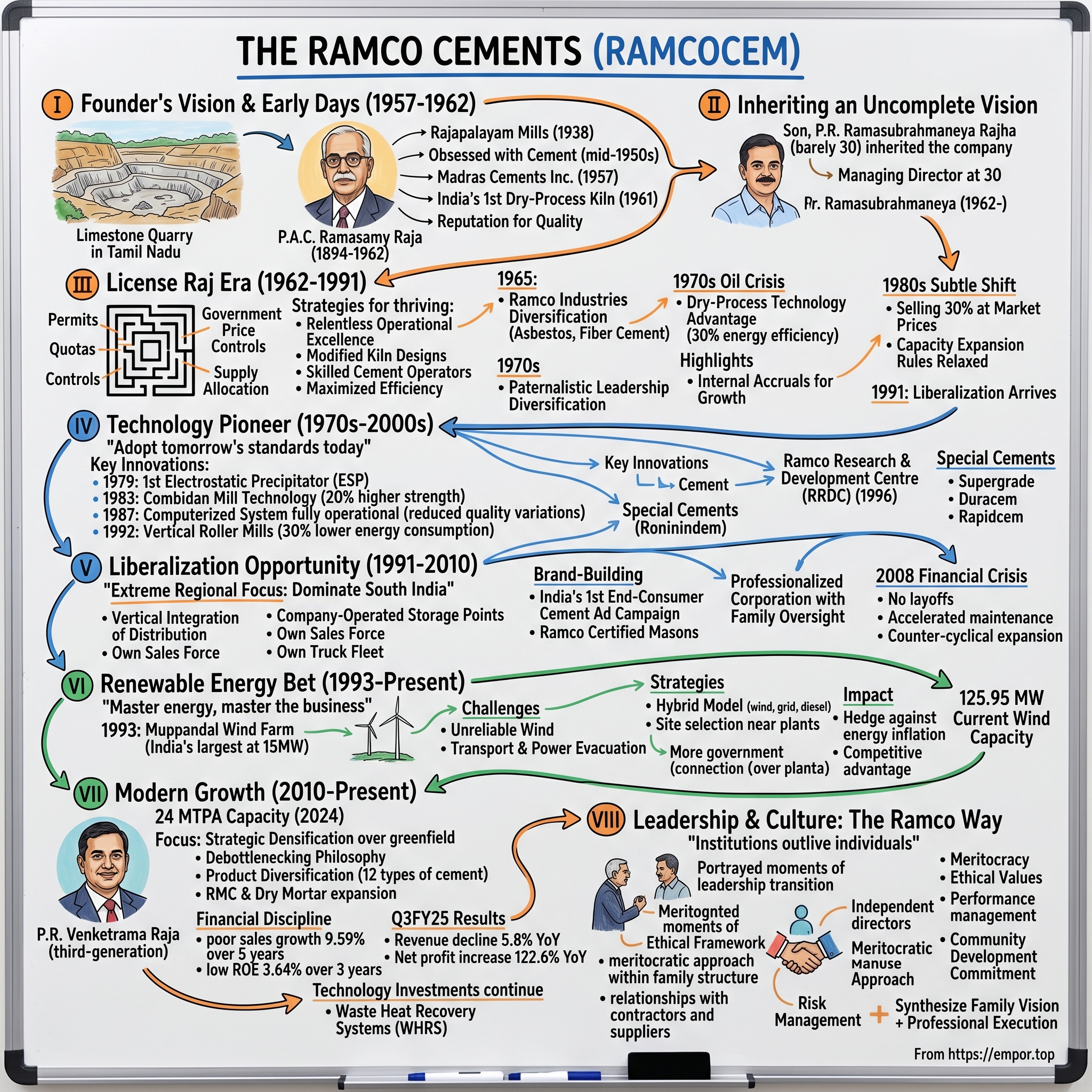

Picture this: A dusty quarry in Virudhunagar, Tamil Nadu, 1961. The limestone cliffs shimmer in the brutal afternoon heat. A group of engineers, their white shirts already yellowed with dust, stand around a newly imported kiln—India's first dry-process cement technology. Their leader, P.A.C. Ramasamy Raja, a 67-year-old industrialist who'd already built a textile empire, points to the barren landscape and declares, "Here, we will build something that outlasts us all."

Today, that single plant has morphed into The Ramco Cements Limited—a ₹27,436 crore market cap behemoth, the fifth-largest cement producer in India, with 24 million tonnes per annum capacity spread across multiple states. The company doesn't just make cement; it manufactures Ready Mix Concrete (RMC) and dry mortar products, operates wind farms generating 125.95 MW of power, and has become synonymous with quality construction materials across South India.

But here's the fascinating question: How did a company that started in the most capital-intensive, commodity-driven, government-controlled industry of post-independence India not just survive but thrive through six decades of economic upheaval? How did it pioneer technologies that multinational giants hadn't dared to implement? And why, in an era of pan-India consolidation, does this regional powerhouse continue to command premium valuations?

This is a story of three generations of leadership, of betting on technology when competitors relied on labor, of building wind farms when oil was cheap, and of choosing regional dominance over reckless expansion. It's about navigating the treacherous License Raj, capitalizing on liberalization, and somehow maintaining family control while building institutional excellence.

We'll journey through the founder's textile-to-cement pivot, the son who inherited a company days after his father's death and ran it for 55 years, and the current generation balancing tradition with transformation. We'll examine how Ramco became India's cement technology pioneer—first with dry-process kilns, first with electrostatic precipitators, first with vertical roller mills. We'll decode their contrarian renewable energy bet that now powers their competitive advantage.

Along the way, we'll unpack critical strategic decisions: Why stay regional when everyone went national? How do you build a premium brand in a commodity business? What happens when your biggest competitive advantage—cheap power—becomes table stakes? And ultimately, we'll wrestle with the investor's dilemma: Is this a value trap in a cyclical industry, or an underappreciated compounder with decades of growth ahead?

II. The Founder's Vision & Early Days (1957-1962)

The story begins not with cement, but with cotton. P.A.C. Ramasamy Raja, born in 1894 in the village of Rajapalayam to Shri Pusapati Chinniah Raja and Smt. Chittammal, belonged to that rare breed of first-generation Indian industrialists who saw business as nation-building. His father was a zamindar—a landowner—but young Ramasamy Raja had different dreams. While his peers pursued civil service or managed ancestral lands, he envisioned smokestacks and spinning mills transforming South India's agrarian landscape.

September 1938 marked his first major victory. Rajapalayam Mills Limited roared to life with 6,800 spindles imported from England—a massive investment for that era. The timing was audacious: World War II loomed, the independence movement intensified, and British firms dominated Indian industry. Yet Ramasamy Raja's textile venture flourished, earning him both wealth and reputation as a visionary industrialist who could execute complex projects.

But textiles were just the beginning. By the mid-1950s, Ramasamy Raja, now in his sixties, became obsessed with cement. Post-independence India desperately needed infrastructure—roads, dams, buildings—and cement was the bottleneck. The industry was nascent, capital-intensive, and technologically complex. Most Indian businessmen avoided it. Foreign technology was expensive, skilled operators were scarce, and the government's price controls made profitability questionable.

Yet Ramasamy Raja saw opportunity where others saw obstacles. In 1957, he incorporated Madras Cements Limited (the company wouldn't become "The Ramco Cements Limited" until July 2013). The headquarters was established in Chennai, but the real action happened 500 kilometers south, in his native Virudhunagar district. Here, amid limestone deposits and close to his textile operations, he would build his cement empire.

The early years were brutal. Cement manufacturing in the late 1950s meant wrestling with massive capital requirements—a single kiln cost more than entire textile mills. The technology was jealously guarded by European companies. The Indian government's stringent price controls and supply allocation policies made the business model precarious. Industry veterans warned Ramasamy Raja: "Cement will drain your textile profits. It's a government-controlled commodity with no pricing power."

But Ramasamy Raja had a different thesis. He believed India's infrastructure boom was inevitable, that technology would democratize over time, and that disciplined execution could overcome regulatory hurdles. More importantly, he understood something his critics missed: in a supply-constrained market with government-allocated quotas, the scarce resource wasn't capital—it was the license to produce.

The Ramasamy Raja Nagar plant in Virudhunagar represented a technological leap. While competitors used wet-process kilns—energy-intensive and inefficient—Ramasamy Raja imported India's first dry-process kiln technology with a capacity of 1,200 tonnes per day. The technology cost a fortune, required foreign technicians for installation, and demanded operators be trained abroad. But it offered 30% better fuel efficiency—a massive advantage in an industry where energy costs determined survival.

By 1961, the plant was operational. The early production runs were erratic—equipment breakdowns were frequent, quality varied wildly, and the monsoons played havoc with logistics. But gradually, the operation stabilized. Madras Cements began supplying to Tamil Nadu's irrigation projects and housing developments. The company earned a reputation for quality—its cement set faster and lasted longer than competitors'.

Then, on September 3, 1962, everything changed. P.A.C. Ramasamy Raja, now 68 and seriously ill, summoned his son P.R. Ramasubrahmaneya Rajha to his bedside. The conversation, according to family lore, was brief but profound. The father spoke not of the business's past but its future—of expansion plans, of new technologies he'd been studying, of his dream to make Madras Cements the pride of South India. Hours later, he passed away.

Ramasubrahmaneya Rajha, barely 30 years old, inherited not just a company but an incomplete vision. The cement plant was operational but not yet profitable. The technology was advanced but temperamental. The market was growing but government-controlled. Most critically, the company culture was still forming—would it remain a family fief dom or evolve into a professional organization?

The young heir faced immediate skepticism. Board members questioned whether someone so young could navigate the complex world of industrial licensing, government relations, and technological innovation. Competitors circled, hoping to acquire the advanced plant at a distressed price. Even family members wondered if selling to established players like ACC or Dalmia Cements might be prudent.

But Ramasubrahmaneya Rajha had spent years shadowing his father, absorbing not just business acumen but philosophy. He understood that Madras Cements represented more than profits—it was about industrial self-reliance, about proving Indian companies could match global standards. Within days of his father's death, he assumed the role of Managing Director, beginning a remarkable 55-year tenure that would transform a single plant into South India's cement colossus.

III. The License Raj Era & Building Against Odds (1962-1991)

The India that Ramasubrahmaneya Rajha inherited in 1962 was a byzantine maze of permits, quotas, and controls. The cement industry, deemed "essential" by the government, faced particularly suffocating regulations. Every bag's price was fixed by bureaucrats in Delhi. Distribution was controlled through a levy system—companies had to sell 50% of production to the government at below-market rates. Capacity expansion required licenses that took years to obtain and often came with political strings attached.

Consider the absurdity: In 1963, Madras Cements identified an opportunity to double production by adding a second kiln. The technology was available, funding was arranged through internal accruals, and market demand was obvious—Tamil Nadu's cement shortage was acute. Yet it took four years of applications, committee meetings, and "facilitation payments" before the license was granted. By then, equipment costs had risen 40%, and competitors had grabbed market share.

This was the reality of Indian business in the License Raj—an environment where political connections mattered more than efficiency, where production was deliberately constrained to prevent "concentration of economic power," where entrepreneurship was viewed with suspicion. Nehru's socialist vision had created a system that claimed to protect the poor but enriched the corrupt and penalized the efficient.

Yet somehow, Ramasubrahmaneya Rajha thrived in this hostile environment. His strategy was counterintuitive: instead of fighting the system or trying to game it through political patronage, he focused relentlessly on operational excellence within regulatory constraints. If the government controlled prices, he'd control costs. If capacity was restricted, he'd maximize efficiency. If distribution was regulated, he'd dominate the free market portion.

The numbers tell the story. Between 1962 and 1975, while industry capacity grew at 4% annually, Madras Cements' actual production grew at 12%. How? Through countless small innovations—modified kiln designs that increased throughput, local fabrication of spare parts to avoid import delays, training programs that created India's most skilled cement operators. When competitors achieved 70% capacity utilization, Madras Cements consistently hit 95%.

The 1965 founding of Ramco Industries Limited under Ramasubrahmaneya Rajha's leadership marked a crucial diversification. While cement remained the core, the new entity ventured into asbestos sheets, fiber cement products, and eventually surgical cotton—each business chosen for its synergy with existing operations. This wasn't conglomerate empire-building; it was careful risk mitigation in an uncertain regulatory environment.

The 1970s brought new challenges. The oil crisis made energy costs spiral—devastating for an energy-intensive industry like cement. The government's response was typical: price controls remained while input costs soared. Many cement companies hemorrhaged cash; several smaller players shut down. Industry consolidation seemed inevitable.

But Madras Cements had an ace up its sleeve—the dry-process technology invested in by the founder. While competitors' wet-process plants consumed 1,400 kcal per kg of clinker, Madras Cements needed just 950 kcal. This 30% energy advantage, marginal in good times, became existential during the energy crisis. The company not only survived but had cash to acquire distressed assets from struggling competitors.

The human dimension of this era deserves attention. Ramasubrahmaneya Rajha's leadership style was distinctly paternalistic—employees were "family," their children's education was the company's responsibility, and layoffs were unthinkable even during downturns. This created extraordinary loyalty. When union violence paralyzed other cement plants in the 1970s, Madras Cements operated without a single day's disruption. Workers took pride in their plant's technological superiority and their company's reputation for quality.

Family dynamics added another layer of complexity. As the company grew, so did the family. Ramasubrahmaneya Rajha had to balance the aspirations of siblings, cousins, and in-laws—each wanting their piece of the growing pie. His solution was elegant: family members could join the business but had to prove competence. Positions weren't inherited; they were earned. This meritocratic approach within a family structure created a unique culture—professional yet personal, demanding yet supportive.

The 1980s marked a subtle shift in government policy. Rajiv Gandhi's early liberalization initiatives loosened some controls. Cement companies could now sell 30% of production at market prices. Capacity expansion rules were relaxed slightly. For most companies, these were marginal improvements. For Madras Cements, they were transformative opportunities.

The company had spent two decades perfecting operations within constraints. Now, with even modest freedom, it could flex its muscles. New plants were planned with mathematical precision—located near limestone deposits, connected to rail networks, powered by captive power plants. While competitors celebrated deregulation with aggressive expansion, Madras Cements expanded methodically, ensuring each new tonne of capacity was the lowest-cost tonne in the region.

By 1991, when India finally embraced economic liberalization, Madras Cements had evolved from a single plant operation into a multi-location cement major. Revenue had grown from ₹5 crores in 1962 to over ₹200 crores. Employment had risen from a few hundred to more than 3,000. Most remarkably, this growth occurred entirely through internal accruals—not a single rupee of debt was raised until the late 1980s.

The License Raj era, which destroyed so many Indian businesses, had paradoxically strengthened Madras Cements. The constraints forced innovation, the price controls demanded efficiency, and the artificial scarcity created a culture of quality over quantity. When liberalization finally arrived, the company wasn't just ready to compete—it was ready to dominate.

IV. Technology Pioneer: The Innovation Story (1970s-2000s)

Inside the Ramco Research & Development Centre in Chennai, 1978. Dr. K. Krishnamoorthy, a chemical engineer recently returned from Germany, stands before a room of skeptical plant managers. On the board behind him: blueprints for India's first Electrostatic Precipitator (ESP) for cement kilns. "Gentlemen," he says, "we're going to capture 99.9% of particulate emissions. Not because the government requires it—they don't yet—but because it's the right thing to do." The room erupts. "That will cost crores!" "Our competitors aren't doing this!" "The government will never mandate it!"

Ramasubrahmaneya Rajha, sitting quietly in the corner, finally speaks: "Dr. Krishnamoorthy is right. We implement it next quarter."

This scene captures the essence of Ramco's technology philosophy: adopt tomorrow's standards today, even if—especially if—competitors think you're crazy. The ESP installation in 1979 cost ₹3 crores, nearly 10% of annual revenue. Competitors mocked it as "Rajha's folly." But when pollution norms tightened in 1987, Ramco was already compliant while rivals scrambled to retrofit plants, facing shutdowns and penalties.

The ESP was just the beginning. Throughout the 1980s and 1990s, Ramco pioneered technologies that redefined Indian cement manufacturing. Each innovation followed a pattern: identify global best practices, adapt them to Indian conditions, implement despite short-term costs, then reap long-term advantages when the industry eventually followed.

Take the Combidan Mill Technology, introduced in 1983. Cement fineness determines strength—the finer the particles, the stronger the concrete. Traditional ball mills could achieve 300-350 m²/kg fineness. The Combidan technology, licensed from Denmark at enormous cost, achieved 450 m²/kg. The result? Ramco's cement offered 20% higher strength at the same price. Construction companies began specifying "Ramco or equivalent"—except there was no equivalent.

The technology bets weren't always smooth. In 1985, Ramco attempted to implement a computer-controlled kiln operation system—radical for an era when most Indian factories still used manual log books. The initial implementation was disastrous. The software, designed for European conditions, couldn't handle Indian power fluctuations. Sensors failed in Tamil Nadu's humidity. The plant efficiency actually dropped for six months.

Lesser companies might have abandoned the experiment. Ramco doubled down. Engineers were sent to Japan to study adaptation techniques. The software was rewritten with Indian conditions in mind. Backup systems were installed for power stability. By 1987, the computerized system was fully operational, improving fuel efficiency by 8% and reducing quality variations by 60%. When competitors finally computerized in the mid-1990s, Ramco had a decade's lead in operational data and optimization algorithms.

The vertical roller mill installation in 1992 represents perhaps Ramco's boldest technological gambit. Ball mills had been the industry standard for a century—reliable, simple, well-understood. Vertical roller mills promised 30% lower energy consumption but were complex, temperamental, and had failed at several European plants. No Indian company had attempted them.

Ramco didn't just install one vertical roller mill—they replaced entire grinding lines across multiple plants simultaneously. The capital expenditure was staggering: ₹50 crores when annual profit was ₹30 crores. The board was divided. Financial advisors warned of bankruptcy if the technology failed. Even supportive executives suggested a gradual, plant-by-plant approach.

But Ramasubrahmaneya Rajha understood something crucial: in commodity businesses, temporary advantages evaporate quickly. If vertical roller mills worked, competitors would copy within years. The window for competitive advantage was narrow. Going all-in was risky, but going slow was pointless. The mills were installed in a massive 18-month transformation.

The initial months were nightmarish. The mills required different raw material preparation, new maintenance protocols, and retraining of entire workforces. Production dropped 20%. Quality became erratic. One mill suffered a catastrophic failure, shutting down an entire plant for three weeks. The financial press speculated about Ramco's impending collapse.

Then, gradually, the mills were tamed. Engineers developed India-specific modifications—better sealing for monsoon moisture, modified grinding pressures for local limestone. By 1994, all mills were operational at design capacity. Energy costs dropped 35%. Maintenance costs, after the initial learning curve, were 40% lower than ball mills. The payback period, projected at seven years, was achieved in four.

The Ramco Research & Development Centre (RRDC), established formally in 1996 but operational since the early 1980s, became the intellectual heart of these innovations. Unlike typical corporate R&D centers focused on incremental improvements, RRDC pursued fundamental research. They studied concrete chemistry at the molecular level, experimented with alternative fuels before sustainability was fashionable, and developed proprietary cement formulations that competed with international grades.

RRDC's crown jewel was the development of special cements for specific applications. Ramco Supergrade for high-rise construction, offering 53-grade strength when the industry standard was 43-grade. Ramco Duracem for marine structures, with enhanced chloride resistance. Ramco Rapidcem for infrastructure projects, achieving 70% strength in 3 days versus the standard 7 days. Each product commanded premium pricing in a supposedly commoditized market.

The innovation culture permeated beyond technology to processes. Ramco pioneered vendor development programs, teaching limestone quarry owners modern mining techniques to ensure consistent raw material quality. They created India's first cement customer education centers, training masons and contractors on optimal cement usage. They even developed proprietary logistics software in the 1990s, optimizing truck routing when competitors still used paper manifests.

What drove this relentless innovation in an industry notorious for conservatism? Part was competitive paranoia—Ramasubrahmaneya Rajha often said, "In commodities, you innovate or you die slowly." Part was the founder's DNA—P.A.C. Ramasamy Raja's early technology bet had saved the company during the oil crisis, a lesson never forgotten. But mostly, it was the recognition that in a price-controlled, capacity-constrained industry, the only true freedom was technical superiority.

By 2000, Ramco's technology leadership was undisputed. They had filed 47 patents, more than the next three competitors combined. Their plants consistently achieved the lowest energy consumption per tonne in India. International cement majors studying Indian acquisitions invariably benchmarked against Ramco's operational metrics. The boy who inherited a single plant in 1962 had built India's most technically advanced cement company.

V. The Liberalization Opportunity & Regional Dominance (1991-2010)

July 24, 1991. Finance Minister Manmohan Singh rises in Parliament to present the Union Budget. His words would reshape Indian industry: "No power on earth can stop an idea whose time has come." License Raj was dead. Price controls were abolished. Foreign investment was welcomed. For Indian cement, it was Year Zero of a new era.

In Ramco's Chennai headquarters, the mood was electric yet anxious. Executives who'd spent careers navigating government controls suddenly faced free markets. The opportunity was obvious—no more artificial constraints on growth. The threat was equally clear—global giants like Holcim and Lafarge were eyeing India, and domestic rivals like Birla and ACC would expand aggressively.

Ramasubrahmaneya Rajha, now 60 and with three decades of leadership experience, called a strategy session that would define Ramco's next phase. The conventional wisdom was unanimous: go national immediately. Build plants across India. Match the pan-India footprint of emerging leaders. Regional players would be roadkill in the consolidation wars ahead.

Ramco chose the opposite path: extreme regional focus. Instead of spreading resources across India, they would dominate South India completely. While competitors rushed to establish token presence in multiple states, Ramco would build dense capacity in Tamil Nadu, Andhra Pradesh, and Karnataka. The strategy had a simple premise: in commodity businesses, the lowest-cost producer in a region wins, and transportation costs make true national competition impossible.

The Gokul Cements acquisition in 2000 exemplified this approach. Gokul's 290,000 tonnes per annum plant in Mathodu wasn't attractive for its size—it was tiny by industry standards. But its location was perfect: close to Ramco's existing plants, allowing shared logistics and management, yet serving a distinct micro-market. The acquisition price of ₹45 crores seemed high for such small capacity. But Ramco understood something others missed: in cement, market share in a 50-kilometer radius matters more than national capacity rankings.

Post-liberalization, Ramco's distribution strategy was revolutionary for its simplicity. While competitors built complex multi-tier distribution networks with C&F agents, stockists, and retailers, Ramco went direct. They established company-operated storage points in every major town in South India. They employed their own sales force rather than relying on distributors. They even operated their own truck fleet for last-mile delivery.

This vertical integration of distribution was capital-intensive and operationally complex. Managing 200+ storage points and 1,000+ trucks required sophisticated logistics capabilities. The working capital requirements were enormous—Ramco was essentially funding inventory across the entire supply chain. Financial analysts criticized the asset-heavy approach in an era celebrating asset-light business models.

But the strategy created an unassailable moat. Ramco knew exact demand patterns in every micro-market. They could adjust production and pricing in real-time. Most critically, they owned the customer relationship. When construction companies needed urgent supplies or special grades, Ramco could deliver within hours while competitors took days navigating their distribution layers.

The brand-building in a commodity category was another contrarian bet. Conventional wisdom held that cement was cement—builders bought whatever was cheapest. Ramco disagreed. They launched India's first cement advertising campaign targeted at end consumers, not just builders. The tagline—"Ramco Cement: Bharosa Zindagi Bhar Ka" (Trust for a Lifetime)—positioned cement as a long-term investment in family security, not just a construction input.

The marketing went beyond advertising. Ramco created "Ramco Certified Masons"—training programs that educated construction workers on optimal cement usage. Graduates received certificates, tool kits, and critically, recommendation letters for employment. Within years, asking for a "Ramco Certified Mason" became standard in South Indian construction. The masons, in turn, recommended Ramco cement to their clients.

Competition intensified through the 1990s as liberalization attracted global players. Lafarge entered through acquisitions. Holcim partnered with Indian companies. Italcementi explored greenfield plants. Each brought global best practices, deep pockets, and acquisition appetites. Industry consolidation seemed inevitable—analysts predicted India would follow the global pattern of 4-5 players controlling 70% market share.

Ramco's response was to make acquisition economically irrational. They densified capacity around existing plants rather than building new locations. They locked in limestone reserves for 50+ years through long-term mining leases. They created switching costs through customer education and service levels. By 2000, acquiring Ramco's South Indian market share would require not just buying plants but rebuilding an entire ecosystem—economically unfeasible even for global giants.

The numbers validated the strategy. Between 1991 and 2010, Ramco's capacity grew from 2 million tonnes to 15 million tonnes—a 7.5x increase entirely in South India. Market share in Tamil Nadu reached 35%, in Andhra Pradesh 25%. EBITDA margins consistently exceeded 25%, versus industry averages of 18%. Return on capital employed stayed above 20% even during downturns.

The company's evolution during this period went beyond business metrics. The organization transformed from a traditional family-run enterprise to a professionally managed corporation with family oversight. Independent directors were inducted in 1995, ahead of regulatory requirements. Performance management systems replaced seniority-based promotions. Stock options were granted to senior management—rare for family-controlled Indian companies.

This professionalization was tested during the 2008 financial crisis. Demand collapsed 30% in six months. Prices fell below variable costs. Several competitors shut plants or deferred maintenance. Ramco's response showcased institutional maturity: no layoffs despite the downturn, accelerated maintenance to prepare for recovery, and counter-cyclical capacity expansion when project costs were lowest.

By 2010, Ramco Cements had achieved something remarkable: regional dominance in India's most competitive infrastructure sector. They weren't the largest cement company in India—that was UltraTech. They weren't the most global—that was ACC-Holcim. But in South India, they were the undisputed leader, with brand recognition exceeding national players and operational metrics matching global benchmarks.

VI. The Renewable Energy Bet: Wind Power Pioneer (1993-Present)

The Muppandal Pass, 1992. Wind velocity: 25 kilometers per hour, gusting to 40. Ramasubrahmaneya Rajha stands on a barren hillside in Tamil Nadu's Kanyakumari district, holding German wind survey maps. His engineers think he's lost his mind. "Sir, we make cement, not electricity," one ventures. Rajha's response would prove prophetic: "We don't make cement. We convert energy into building materials. Master energy, master the business."

The early 1990s were a peculiar time to bet on wind power. Oil was cheap at $20 per barrel. Coal was abundant. India's power deficit meant any electricity generation was welcome, but wind was considered unreliable, expensive, and technically unsuitable for industrial use. The global wind industry was nascent—Denmark and Germany had small installations, but no one had proven wind viable for heavy industry.

Yet Rajha saw what others missed. Cement manufacturing is essentially energy arbitrage—40% of production costs come from power and fuel. In Tamil Nadu, industrial electricity tariffs were climbing 15% annually. Power cuts disrupted production regularly. The state electricity board prioritized agricultural and residential supply over industry. Energy wasn't just a cost item; it was an existential risk.

The Muppandal Wind Farm, commissioned in 1993, was audacious in scale. While experimental wind projects typically started with 1-2 MW, Ramco installed 15 MW immediately—India's largest wind farm at the time. The 250 KW Vestas turbines from Denmark cost ₹4 crores each. Total project cost exceeded ₹75 crores, nearly equal to Ramco's entire annual profit.

The execution challenges were staggering. The turbines had to be transported through village roads never designed for 20-ton loads. Danish technicians had to be housed in a region with no hotels. The power evacuation infrastructure didn't exist—Ramco had to build their own transmission lines to connect to the grid. Most critically, no one knew if the monsoon winds that made Muppandal attractive would also destroy the turbines.

The first year was brutal. Capacity utilization was 18% versus the projected 30%. Maintenance costs exceeded projections by 200%—salt air corroded components faster than anticipated. The grid refused to accept power during certain hours, forcing turbines to idle. Critics called it "Rajha's white elephants"—magnificent but useless.

But Ramco persisted with engineering modifications. Blade angles were adjusted for Indian wind patterns. Components were tropicalized for humidity and salt resistance. Most innovatively, they developed a hybrid model—wind power for base load, grid power for peak demand, diesel generators for backup. This tri-source strategy ensured uninterrupted production while optimizing energy costs.

The Poolavadi wind farm in 1995 and Uthumalai in 2005 showed Ramco had learned from Muppandal. Sites were selected not just for wind speeds but for proximity to cement plants. Power purchase agreements were structured to ensure grid acceptance. Indigenous maintenance capabilities were developed to reduce dependence on foreign technicians. By 2006, when the Karnataka wind farm was commissioned, Ramco had become India's most sophisticated industrial wind operator.

The financial impact transformed Ramco's economics. By 2000, when grid electricity cost ₹4 per unit, Ramco's wind power cost ₹1.50 per unit after factoring in depreciation benefits. During the 2008 commodity boom when power costs spiked, Ramco's energy costs actually declined as a percentage of revenue. Competitors paying ₹6 per unit watched Ramco's margins expand while theirs compressed.

Beyond direct cost benefits, wind power created strategic advantages. During Tamil Nadu's chronic power cuts in the 2000s, Ramco plants operated at full capacity while competitors faced shutdowns. The renewable energy certificates (RECs) generated after 2010 became a revenue stream. The carbon credits during the CDM (Clean Development Mechanism) era generated millions in additional income.

The 125.95 MW current wind capacity, comprising 127 wind electric generators, represents more than just renewable energy infrastructure. It's a hedge against energy inflation, insurance against grid unreliability, and increasingly, a competitive differentiator as ESG considerations influence industrial purchasing.

The wind bet also transformed Ramco's organizational capabilities. Managing distributed generation assets across multiple states required sophisticated monitoring systems. Predicting wind patterns to optimize production scheduling demanded analytical capabilities. Negotiating with state electricity boards, understanding renewable energy regulations, managing power trading—Ramco developed competencies far beyond traditional cement manufacturing.

What's remarkable is the timing. Ramco built wind capacity when no one cared about climate change, when renewable energy had no subsidies, when ESG was an unknown acronym. They did it purely for economic reasons—controlling energy costs in an energy-intensive business. That this positioned them perfectly for the sustainability era was serendipitous yet inevitable.

Today, when cement companies globally struggle with carbon transition, Ramco's 30-year renewable energy experience provides a massive head start. They understand renewable energy's intermittency challenges and solutions. They have relationships with equipment suppliers, maintenance protocols, and operational expertise. While competitors pilot 5 MW solar projects, Ramco operates utility-scale renewable assets.

The wind power journey also reveals Ramco's decision-making philosophy: make big bets on fundamental business drivers, not incremental improvements. While competitors focused on marginally improving kiln efficiency, Ramco transformed their entire energy equation. It's the difference between optimization and transformation—a distinction that separates survivors from leaders in commodity businesses.

VII. Modern Growth Story: Capacity Expansion & Market Position (2010-Present)

The Kurnool plant construction site, 2019. Bulldozers carve through red earth as Andhra Pradesh's newest integrated cement facility takes shape. A.V. Dharmakrishnan, now CEO, watches the foundation laying with P.R. Venketrama Raja, the third-generation chairman. "Grandfather built one plant in 40 years. Father built ten in 55 years. Our generation needs to build differently—not just more capacity, but smarter capacity," Venketrama Raja tells the assembled team.

This scene encapsulates Ramco's modern growth paradox: how to maintain aggressive expansion while preserving the operational excellence that defined previous generations. The answer has been a carefully orchestrated capacity multiplication strategy that prioritizes efficiency over ego, regional density over national headlines.

The numbers tell a remarkable story. From 15 million tonnes per annum (MTPA) in 2010, Ramco has expanded to 24 MTPA by 2024—a 60% increase that seems modest compared to peers who doubled or tripled capacity. But this comparison misses the point. Ramco increased cement capacity by nearly 1Mta following debottlenecking at its Kalavatala plant in Andhra Pradesh, increasing capacity to 2Mta from 1.5Mta. The company's Valapaadi grinding unit in Tamil Nadu increased capacity from 1.6Mta to 2Mta. The company's total cement grinding capacity increased by 0.9Mta, from 23.14Mta to 24.04Mta with an investment of INR580m—roughly $7 million for nearly 1 million tonnes of additional capacity, a fraction of greenfield costs.

This debottlenecking philosophy—squeezing more output from existing assets before building new ones—reflects deep operational sophistication. While competitors rush to announce new plants, Ramco's engineers obsess over kiln modifications that add 5% capacity, grinding optimizations that improve throughput 10%, or logistics tweaks that reduce turnaround time by hours. Unglamorous work, but devastatingly effective.

The Kolimigundla expansion showcases this evolution. The Ramco Cements Ltd has announced plans to double capacity at its Kalavatala plant in Andhra Pradesh, setting up a second line to increase clinker capacity at the works to 6.3Mta and cement capacity to 3Mta. The expansion is expected to cost INR12,500m (US$150.57m). But this isn't just capacity addition—it's strategic densification. The new line shares infrastructure with the existing plant, uses the same limestone mines, leverages common logistics networks. The result: 30% lower capital cost per tonne than a greenfield project.

Product diversification has been equally strategic. The company produces 12 types of cement for different uses—not random SKU proliferation but carefully targeted grades for specific applications. Ramco Supergrade for high-rises commands 15% premium. Marine Plus for coastal construction fetches 20% extra. Each product required years of R&D, customer education, and market development. But in a commodity business, even 10% price realization improvement transforms economics.

The ready-mix concrete (RMC) and dry mortar expansion represents another strategic layer. These aren't just adjacent products; they're customer lock-in mechanisms. When Ramco supplies both cement and RMC to a project, switching costs multiply. Quality issues become Ramco's responsibility, removing a key customer pain point. The business model shifts from selling bags to providing solutions.

Geographic expansion has been surgical rather than scattershot. While UltraTech planted flags across India, Ramco deepened its South Indian fortress while selectively entering adjacent markets. The Odisha grinding unit, doubling to 1.8 MTPA, targets eastern markets where Ramco has distribution but no production. The logistics arbitrage—shipping clinker from southern plants, grinding locally—provides 15% cost advantage over competitors shipping finished cement.

The financial discipline during this expansion deserves scrutiny. The company has delivered a poor sales growth of 9.59% over past five years. Company has a low return on equity of 3.64% over last 3 years. These metrics would concern growth investors, but they reflect conscious choices. Ramco expanded during industry overcapacity, when cement prices were depressed. They prioritized balance sheet strength over aggressive leverage. They accepted lower near-term returns for sustainable long-term positioning.

The capacity roadmap reveals ambition tempered by pragmatism. Ramco Cements plans to achieve cement capacity of 30Mta by March 2026 with the commissioning of a second line in Kolimigundla along with de-bottlenecking of existing facilities and adding grinding capacities in existing locations with nominal capex. This 25% capacity increase requires modest capital—most growth comes from sweating existing assets harder, not building monuments to management ego.

Recent operational metrics validate the strategy. The Ramco Cements Ltd reported a 2.9% quarter-on-quarter decrease in its consolidated revenues for Q3FY25. On a year-on-year basis, it witnessed a decline of 5.8%. The net profit increased 604.6% QoQ and increased 122.6% YoY. Revenue declined due to cement price weakness, but profits surged through operational efficiency and one-time gains. This demonstrates Ramco's ability to generate returns even in challenging markets.

The technology investments continue paying dividends. The company's Ramasamy Raja Nagar plant in Tamil Nadu is to receive a 10MW WHRS at a cost of INR1530m. The WHRS is expected to be commissioned by March 2025 and will boost The Ramco Cement's waste heat recovery capacity from 43MW to 68MW. Waste heat recovery systems capture kiln exhaust heat to generate power—free electricity from waste energy. When operational, 68MW of WHRS capacity will reduce power costs by ₹200 crores annually.

Market dynamics have shifted dramatically since 2010. The industry added 200 MTPA capacity while demand grew only 150 MTPA. Utilization rates dropped from 85% to 65%. Pricing power evaporated—cement prices in real terms are lower today than in 2010. In this environment, only the most efficient survive profitably.

Ramco's response has been to double down on operational excellence. Power consumption per tonne has decreased 15% through technology upgrades. Logistics costs have dropped 20% through network optimization. Manufacturing costs are 10% below the industry average. These aren't dramatic improvements, but compound over time into insurmountable advantages.

The organizational evolution mirrors business complexity. From 3,000 employees in 2010 to over 5,000 today, but revenue per employee has increased 40%. Digital systems now manage everything from quarry operations to customer delivery. Predictive maintenance prevents breakdowns. AI optimizes production scheduling. The company that started with manual kilns now runs algorithm-driven factories.

Competition has intensified with global consolidation. LafargeHolcim (now Holcim) commands massive resources. UltraTech's national footprint provides economies of scale. Adani's entry brings deep pockets and infrastructure synergies. Regional players are getting squeezed between national giants and local producers. Ramco's middle path—regional dominance with selective expansion—requires perfect execution to remain viable.

VIII. Leadership & Culture: The Ramco Way

The boardroom at Ramco's Chennai headquarters, 2017. After 55 years at the helm, P.R. Ramasubrahmaneya Rajha, now 86, stands to address the board one final time as Managing Director. His voice, weathered by decades of shareholder meetings and factory inaugurations, carries surprising strength: "I inherited a company from my father. I leave behind an institution. The difference is that institutions outlive individuals."

This transition moment—a founder's son stepping down after more than half a century of leadership—could have been traumatic. Family businesses often implode during succession. Yet Ramco's handover to P.R. Venketrama Raja as Chairman was remarkably smooth, predetermined by years of careful preparation and cultural architecture that prioritized institutional strength over individual dominance.

The Ramco leadership philosophy emerged from necessity. When Ramasubrahmaneya Rajha took charge in 1962, he was surrounded by managers older and more experienced. He couldn't command through authority; he had to lead through competence and vision. This early constraint shaped a culture of meritocracy unusual in family-controlled Indian businesses.

Consider A.V. Dharmakrishnan's journey. Joining as a chartered accountant in 1982, "AVD" (as he's universally known) could have remained a capable CFO in a typical family company. Instead, his unique combination of financial expertise and technological curiosity propelled him through operations, strategy, and eventually to CEO. Under the Rajha family's leadership, professional managers weren't threats to be contained but assets to be developed.

The numbers reflect this professional management. During Ramasubrahmaneya Rajha's 55-year tenure (1962-2017), revenue grew from ₹5 crores to over ₹7,000 crores—a 1,400x increase. But more impressively, this growth came with institutional strengthening. Independent directors joined boards before regulations mandated it. Performance metrics replaced seniority for promotions. Stock options were granted to senior management when most family companies guarded equity jealously.

The cultural DNA traces back to founder P.A.C. Ramasamy Raja's original vision: "We follow our founder's strong belief in ethical values, leadership qualities and motivation to form a committed team." This wasn't corporate speak but lived reality. When cement price cartels formed in the 1990s, Ramco refused participation despite short-term losses. When competitors delayed supplier payments during downturns, Ramco maintained payment schedules. "When we have good relationships with contractors and suppliers, we'll deal with them forever."

This ethical framework created unexpected competitive advantages. During the 2008 construction boom, when cement was scarce, suppliers prioritized Ramco because of historical fairness. Skilled operators joined Ramco for career stability, not just salaries. Banks offered better terms recognizing management integrity. In commodity businesses where differentiation is minimal, reputation became a moat.

The family's approach to wealth deserves examination. Despite controlling 42.6% of a ₹27,000+ crore company, the Rajhas maintain modest lifestyles. No private jets, no ostentatious displays, no vanity projects. Profits are reinvested or distributed to shareholders, not extracted through complex related-party transactions. This restraint signals long-term thinking to investors and commitment to employees.

Succession planning began decades before actual transition. P.R. Venketrama Raja didn't suddenly appear as chairman; he grew through responsibilities over 20 years. Starting in manufacturing, moving through marketing, understanding finance, eventually leading strategy. By succession time, he knew every plant manager, understood every market nuance, had credibility with every stakeholder. The transition was continuation, not disruption.

The professional management layer provides ballast. CEO Dharmakrishnan represents continuity—four decades with the company, deep technical knowledge, respected by family and institutions alike. The CFO, Company Secretary, and operational heads average 25+ years tenure. This isn't organizational inertia but institutional memory—understanding why certain decisions were made, which experiments failed, what truly drives value.

Cultural transmission mechanisms are deliberately designed. The Ramco Management Development Program recruits from top engineering and business schools but emphasizes cultural fit over credentials. New hires spend their first year rotating through plants, living in factory townships, understanding ground reality. Senior managers mentor juniors formally and informally. Technical expertise is documented obsessively—Ramco's internal knowledge repository rivals academic libraries.

The community development commitment reflects founding values. "His true legacy is the robust value system, commitment to ethics and manifold community development programmes." Every Ramco plant supports local schools, runs health clinics, provides vocational training. This isn't CSR compliance but genuine stakeholder capitalism. Plant managers are evaluated on community relations alongside production metrics.

Decision-making blends family wisdom with professional analysis. Major capital allocations require family consensus but are preceded by rigorous management evaluation. The board includes independent directors with relevant expertise—former cement executives, technology leaders, financial experts. Family members chair boards but CEOs run operations. This balance prevents both autocratic overreach and bureaucratic paralysis.

The innovation culture permeates beyond R&D. Plant operators suggest process improvements rewarded through formal programs. Sales teams identify customer needs that drive product development. Even truck drivers provide logistics optimization ideas. This bottom-up innovation complements top-down strategy, creating continuous improvement momentum.

Risk management reflects institutional maturity. Every capacity expansion includes downside scenarios. Technology investments have fallback plans. Market assumptions are stress-tested. This isn't paranoia but prudence—understanding that in capital-intensive businesses, one major mistake can destroy decades of value creation.

The stakeholder management philosophy extends beyond shareholders. Employee welfare programs include housing, healthcare, education support for children. Vendor development initiatives help small suppliers upgrade capabilities. Customer education programs improve construction quality industry-wide. This ecosystem approach creates mutual dependencies that strengthen Ramco's position.

What's remarkable is how this culture survived transitions that destroy other family businesses. The shift from founder to son, from second to third generation, from family-led to professionally-managed—each potentially fatal to organizational culture. Yet Ramco's values persisted through deliberate cultivation, not happy accident.

The challenges are real. Attracting young talent to traditional manufacturing gets harder as technology companies offer excitement and stock options. Maintaining family harmony as ownership dilutes across generations requires constant communication. Balancing regional identity with growth ambitions creates strategic tension. Preserving entrepreneurial spirit within institutional frameworks demands conscious effort.

Yet the Ramco Way endures because it solves the fundamental paradox of family businesses: how to maintain family control while building professional excellence. The answer isn't choosing one over the other but synthesizing both—family provides vision and values while professionals provide execution and expertise.

IX. Financial Performance & Market Dynamics

The numbers tell a story of resilience in an unforgiving industry. Mkt Cap: 27,436 Crore—a respectable valuation that places Ramco among India's top cement companies. But beneath this headline number lies a complex narrative of cyclical pressures, strategic choices, and the eternal challenge of creating value in commodity businesses.

The company has delivered a poor sales growth of 9.59% over past five years. Company has a low return on equity of 3.64% over last 3 years. These metrics would make growth investors flee. Yet they obscure important context: India's cement industry has been in its worst downcycle in two decades. Capacity exceeded demand by 30%. Prices in real terms hit 15-year lows. In this environment, survival itself is success.

The Q3FY25 results provide a snapshot of current dynamics. Profit before exceptional items and tax for the company's cement business fell to Rs 4.35 crore during the October-to-December period from Rs 135 crore a year earlier—a 97% collapse that seems catastrophic. But exceptional items tell a different story: The company reported a one-time gain of Rs 329 crore from the sale of its surplus land and investments. This asset monetization strategy—selling non-core holdings to strengthen the balance sheet—shows management adapting to market realities.

The volume-price dynamics reveal industry-wide challenges. Revenue from the cement business fell 6 per cent on-year to Rs 1,977 crore despite volumes growing 9%. This implies a 14% price decline—brutal in a business where 40% of costs are fixed. When cement sells below ₹300 per bag (the current reality), most producers lose money on marginal production.

Yet Ramco's operational metrics show relative strength. Capacity utilization at 68% exceeds the industry average of 60%. EBITDA per tonne, while compressed, remains positive when several competitors report negative unit economics. The balance sheet, with net debt at ₹4,616 crores (as of December 2024), provides cushion for further downturns.

The industry structure explains persistent challenges. India has 600+ million tonnes of cement capacity for 400 million tonnes of demand. The top five players control just 55% market share versus 70-80% in developed markets. This fragmentation prevents pricing discipline. When demand weakens, prices collapse as producers chase volumes to cover fixed costs.

Regional variations add complexity. South India, Ramco's stronghold, faces particular oversupply with 40% excess capacity. Andhra Pradesh and Tamil Nadu, core markets, have seen intense competition from UltraTech, Dalmia, and newer entrants. Karnataka offers better pricing but limited growth. Kerala provides premium realization but small volumes. This geographic concentration—strength in good times—becomes vulnerability during downturns.

The cost structure reveals both advantages and challenges. Power and fuel represent 30% of costs—here Ramco's renewable energy provides an edge. Raw materials account for 20%—controlled through captive limestone mines. Freight comprises 15%—optimized through regional focus. But employee costs at 12% exceed industry averages of 8%, reflecting Ramco's no-layoff policy and higher skill levels.

Capital allocation decisions shape returns. Over the past five years, Ramco invested ₹5,000 crores in capacity expansion and modernization. With revenues growing slower than capital employed, return metrics deteriorated. But this analysis misses strategic positioning—investments made during downturns typically generate superior through-cycle returns.

The working capital management shows discipline. Despite industry practice of extended credit terms to boost sales, Ramco maintains strict 45-day collection periods. Inventory turns have improved from 8x to 12x through supply chain optimization. Creditor days are managed carefully to maintain supplier relationships. This working capital efficiency provides ₹500 crores of free cash flow even during downturns.

Debt metrics require nuanced interpretation. Company has low interest coverage ratio—concerning in isolation. But this reflects temporary earnings compression rather than structural leverage. Net debt to EBITDA at 5x seems high, but asset coverage remains comfortable. More importantly, debt is primarily project-specific with extended tenures, providing repayment flexibility.

The shareholder return profile reflects industry cyclicality. Five-year returns of 45% lag broader markets but exceed industry peers. Dividend consistency—maintained even during losses—signals management confidence. The 42.6% promoter holding provides alignment but limits float, affecting liquidity and institutional interest.

Recent strategic initiatives show adaptation. Asset monetization generated ₹500+ crores, reducing leverage. The focus on premium products improved realization by ₹200 per tonne. Cost reduction programs saved ₹300 crores annually. These incremental improvements, while unsexy, are the difference between survival and failure in commodity downturns.

The valuation paradox persists. At 15x P/E, Ramco trades at premium to peers despite inferior recent performance. The market values quality—superior assets, strong brand, clean balance sheet, credible management. But this premium assumes recovery that remains elusive.

Looking ahead, the financial trajectory depends on macro factors beyond company control. If infrastructure spending accelerates and housing demand recovers, Ramco's operational leverage will drive explosive earnings growth. But if oversupply persists and prices remain depressed, even excellent operations can't overcome industry headwinds.

The ultimate financial question isn't whether Ramco can generate returns—they've proven this through cycles. It's whether cement as an industry can escape the value destruction of excessive competition and capital intensity. Ramco's answer has been to focus on what they control—costs, quality, service—while positioning for inevitable consolidation.

X. Playbook: Business & Investing Lessons

What can we extract from six decades of Ramco's journey that applies beyond cement, beyond India, beyond industrial businesses? The playbook emerges not from strategic brilliance but from consistent execution of timeless principles in a challenging industry.

Lesson 1: Technology as Competitive Advantage in Commodities

Ramco's obsession with technology—dry-process kilns, ESPs, vertical roller mills, renewable energy—seems counterintuitive in a commodity business where products are undifferentiated. But that's precisely the point. When you can't differentiate the product, you must differentiate the process. Every 5% efficiency improvement compounds over decades into insurmountable cost advantages.

The key insight: adopt technology before it's mandatory, when it's expensive, when competitors think you're foolish. By the time technology becomes industry standard, you've captured years of superior returns and developed implementation expertise competitors lack. This requires patient capital and conviction that short-term costs generate long-term moats.

Lesson 2: Vertical Integration as Risk Management

Conventional wisdom suggests focus beats diversification. Ramco's journey—backward into limestone mining, forward into RMC, sideways into power generation—seems to violate this principle. But in volatile commodity businesses, vertical integration isn't empire-building; it's risk mitigation.

When power costs spike, captive generation provides hedge. When cement prices crash, RMC maintains margins. When logistics bottleneck, captive transport ensures delivery. Each integration decision responded to specific vulnerability. The cumulative effect: a business resilient to external shocks that regularly destroy focused competitors.

Lesson 3: Regional Dominance Over National Presence

While peers pursued pan-India footprints, Ramco deepened regional roots. This wasn't timidity but strategic clarity. In businesses where transportation costs matter, local density beats geographic spread. Owning 35% of Tamil Nadu generates better returns than owning 5% of India.

Regional focus enables customer intimacy—understanding local construction practices, maintaining contractor relationships, providing technical support. It allows operational excellence—optimizing logistics networks, sharing management resources, achieving maintenance economies. Most importantly, it creates pricing power—when you're the dominant local supplier, customers pay premiums for reliability.

Lesson 4: Family Business Succession Through Institutionalization

Most family businesses fail during succession. Ramco survived three generations by separating ownership from management. Family provides vision and values; professionals execute operations. This isn't abdication but evolution—recognizing that modern business complexity exceeds individual capability.

The blueprint: Start succession planning decades early. Rotate successors through functions to build credibility. Maintain meritocracy even for family members. Create cultural transmission mechanisms beyond individuals. Most critically, prioritize institutional strength over family harmony—better to have competent outsiders than incompetent relatives.

Lesson 5: ESG Before It Was Fashionable

Ramco's environmental investments—renewable energy in 1993, pollution control in 1979, sustainability before the term existed—weren't driven by regulations or PR but by economic logic. Energy efficiency reduces costs. Pollution control avoids shutdowns. Community development ensures social license.

The learning: true ESG isn't compliance or marketing but operational excellence. When environmental and social initiatives generate economic returns, they become sustainable. When they're seen as costs, they're abandoned during downturns. Ramco's 30-year renewable energy journey proves that doing good and doing well aren't mutually exclusive but mutually reinforcing.

Lesson 6: Capital Allocation in Cyclical Industries

Cement is viciously cyclical—boom periods of shortage and pricing power followed by busts of overcapacity and losses. Most companies expand aggressively during booms (when capital is expensive) and retreat during busts (when assets are cheap). Ramco does the opposite—cautious during booms, aggressive during busts.

This contrarian capital allocation requires financial strength to invest during downturns and emotional discipline to resist during upturns. It means accepting criticism for being too conservative during good times and too aggressive during bad times. But through-cycle returns vindicate the strategy—assets acquired during distress generate extraordinary returns during recovery.

Lesson 7: Relationships as Competitive Moat

"When we have good relationships with contractors and suppliers, we'll deal with them forever." This philosophy seems quaint in an era of competitive bidding and supplier squeezing. But in industries requiring complex coordination—limestone suppliers, transport contractors, construction companies—relationships reduce transaction costs and ensure reliability.

During the 2008 shortage, Ramco received limestone when competitors' mines ran dry—suppliers remembered decades of fair treatment. During COVID, truckers prioritized Ramco loads—they knew payments would be honored. These relationship premiums, invisible in financial statements, appear during stress when they matter most.

Lesson 8: The Power of Incremental Innovation

Ramco never invented breakthrough technology. Every innovation—dry-process kilns, vertical mills, waste heat recovery—was pioneered elsewhere. Their genius was relentless incremental improvement—adapting global technologies to Indian conditions, optimizing through thousands of small modifications, accumulating marginal gains into substantial advantages.

This approach suits capital-constrained environments where R&D budgets are limited. Instead of pursuing moonshots, focus on certain improvements. A 2% efficiency gain, 3% cost reduction, 1% quality improvement—insignificant individually but transformative cumulatively. In commodity businesses, margins are won in basis points, not percentage points.

Lesson 9: Culture as Strategy

Ramco's no-layoff policy seems economically irrational—maintaining excess workforce during downturns destroys returns. But this policy creates loyalty that generates unmeasurable value. Workers share improvement ideas because they benefit from efficiency. Operators take ownership because they have career security. Knowledge accumulates because people stay.

In industries where operational excellence determines success, culture becomes strategy. The cost of excess workers during downturns is offset by superior performance during upturns. More importantly, cultural reputation attracts talent that wouldn't otherwise join traditional manufacturing. In human-capital-intensive businesses, being the employer of choice is competitive advantage.

Lesson 10: Playing the Long Game

Every major Ramco decision—technology adoption, capacity expansion, market development—had 10+ year horizons. This long-term orientation enabled investments competitors couldn't justify to quarterly-focused markets. It meant accepting years of subpar returns for decades of superior positioning.

Playing the long game requires patient capital (family ownership helps), stakeholder alignment (consistent communication essential), and conviction (believing in strategies despite market skepticism). Most importantly, it requires scorekeeping over decades, not quarters. In industries with 30-year asset lives, quarterly earnings are noise; competitive position is signal.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Infrastructure Supercycle Meets Operational Excellence

Bulls see Ramco as a coiled spring awaiting catalyst. Ramco Cements plans to achieve cement capacity of 30Mta by March 2026—perfectly timed for India's infrastructure boom. Government spending on highways, railways, airports, and smart cities will drive cement demand growth from current 400 MTPA to 600+ MTPA by 2030. Housing for all, urbanization, and industrial construction add another demand layer.

In this scenario, Ramco's operational leverage explodes. With 70% capacity utilization, the company breaks even. At 85% utilization (achievable during boom), every incremental tonne generates ₹2,000 EBITDA. That's ₹6 billion additional EBITDA on unchanged cost base—a 3x increase that would drive the stock multiples higher.

The regional dominance thesis remains intact. South India's economy grows faster than the national average. Tamil Nadu's industrial focus, Karnataka's technology boom, Andhra Pradesh's capital construction, Telangana's infrastructure push—all drive cement demand in Ramco's core markets. While national players spread resources across India, Ramco deepens its southern fortress.

The technology investments compound advantages. Renewable energy provides ₹200 crores annual cost advantage that widens as power prices rise. Waste heat recovery adds another ₹100 crores. Premium products command ₹500/tonne extra realization. Operational efficiency saves ₹300 crores annually. These structural advantages, invisible during downturns, become decisive during upturns.

Management quality deserves premium valuation. The smooth leadership transition, professional governance, and clean accounting inspire confidence. The ₹500 crores asset monetization shows financial flexibility. The maintained dividend during downturns signals balance sheet strength. In an industry plagued by corporate governance issues, Ramco's reputation commands scarcity value.

The consolidation opportunity beckons. India's fragmented cement industry must consolidate—economics demand it. Ramco could be acquirer (strong balance sheet, operational expertise) or target (attractive assets, clean structure). Either scenario unlocks value. As a consolidator, Ramco applies operational excellence to subscale assets. As a target, strategic buyers pay premiums for quality.

ESG tailwinds strengthen. Global investors increasingly screen for sustainability. Ramco's 30-year renewable energy history, environmental compliance, and community development tick every box. As ESG-focused funds grow, Ramco benefits from inclusion in sustainability indices, attracting patient capital that values long-term positioning over quarterly earnings.

The Bear Case: Structural Oversupply Meets Regional Concentration

Bears see value trap, not opportunity. Company has low interest coverage ratio—concerning when interest rates rise. The cement industry's structural oversupply—600 MTPA capacity for 400 MTPA demand—won't resolve quickly. Every price increase triggers new capacity additions. The industry destroyed value for two decades; why would the next decade differ?

Regional concentration becomes vulnerability. South India has India's worst oversupply—40% excess capacity. Every national player targets the region for growth. New entrants like Adani bring unlimited capital. Regional players like Chettinad compete fiercely. Ramco's dominance erodes as competition intensifies, pricing power evaporates, and margins compress permanently.

The financial metrics flash warnings. Company has a low return on equity of 3.64% over last 3 years—destroying shareholder value. Revenue growth of 9.59% over five years barely exceeds inflation. With ₹5,000 crores invested for minimal return improvement, capital allocation appears value-destructive. Why would future investments generate better returns?

Execution risks multiply with expansion. The expansion is expected to cost INR12,500m for Kalavatala alone. If project costs escalate, timelines delay, or demand disappoints, returns evaporate. Ramco's conservative culture, while admirable, may lack the aggressiveness needed to compete with ambitious rivals who accept losses for market share.

Technology advantages erode over time. Competitors replicate innovations within years. Vertical roller mills, once Ramco's differentiator, are now industry standard. Renewable energy, pioneered by Ramco, is now everyone's strategy. Premium products face competition from UltraTech, ACC, and imports. What seems like moat today becomes table stakes tomorrow.

The commodity trap persists. Despite six decades of excellence, Ramco can't escape cement's fundamental challenge: undifferentiated product, price-taking behavior, capital intensity, cyclical demand. Great operations can't overcome poor industry structure. Even the best-run commodity businesses generate mediocre returns over cycles.

Limited geographic diversification hurts during regional downturns. When South Indian construction slows, Ramco suffers disproportionately. National players offset regional weakness through portfolio effects. Ramco's concentrated bet, while generating superior returns during upturns, amplifies downside during downturns.

The family ownership structure, while providing stability, limits strategic flexibility. The 42.6% promoter holding reduces float, affecting liquidity. Family dynamics might prevent hard decisions like massive layoffs or plant closures. The emotional attachment to legacy assets could delay necessary restructuring.

Technological disruption looms. 3D printing promises construction without cement. Green cement alternatives reduce carbon footprint. Modular construction minimizes cement usage. While distant threats, they question terminal value assumptions. Why invest in 30-year cement assets if technology makes them obsolete?

The Verdict: Patience Required

Both cases have merit. Bulls correctly identify operational excellence, strategic positioning, and sector tailwinds. Bears rightfully highlight structural challenges, financial metrics, and execution risks. The truth, as always, lies between extremes.

Ramco represents a classic value-versus-growth dilemma. The stock appears cheap on asset value but expensive on earnings. The company has competitive advantages but operates in a structurally challenged industry. Management is excellent but constrained by market realities.

For investors, the decision depends on time horizon and risk tolerance. Patient investors believing in India's infrastructure story and cement sector consolidation might find Ramco attractive at current valuations. Momentum investors seeking near-term catalysts should look elsewhere. The stock is for those who measure success in decades, not quarters.

XII. Epilogue & "If We Were CEOs"

The present moment finds Ramco at an inflection point. Ramco Cements disposes non-core assets worth Rs.500.86 crore, progressing Rs.1000 crore target. This asset monetization isn't distress selling but strategic deleveraging—preparing the balance sheet for the next growth phase or potential downturn. It signals management pragmatism: when operations can't generate adequate returns, financial engineering provides a bridge.

The debt trajectory tells the story. Net debt stood at ₹5,100 crores in early 2024. Through asset sales and cash generation, it's now ₹4,616 crores—a ₹500 crore reduction despite capacity investments. The target is ₹3,500 crores by 2026, achieving comfortable leverage for a cyclical business. This deleveraging during industry stress positions Ramco to capitalize when markets recover.

If we were CEOs, what strategic choices would we make?

First, we'd accelerate the premium product mix. Currently, 15% of volumes are specialty grades. This should be 30% within three years. Every percentage point shift from commodity to specialty adds ₹50 crores EBITDA. The R&D capability exists; the market education and distribution need acceleration.

Second, we'd pursue tactical acquisitions in adjacent markets. Small grinding units in Kerala, Karnataka, or Maharashtra—₹200-300 crore investments that provide immediate market access. Not transformational deals but tactical fills that leverage existing capabilities while diversifying geographic risk.

Third, we'd monetize the renewable energy expertise. With 125 MW operating and deep implementation knowledge, why not develop renewable projects for other industries? Create a subsidiary, attract green finance, generate fee income from development and operations. The capability exists; it needs commercialization.

Fourth, we'd digitize the customer experience. Cement buying remains archaic—phone calls, paper orders, uncertain delivery. Create an app for contractors: real-time pricing, guaranteed delivery slots, quality certificates, credit management. In commodities, customer experience is the final frontier for differentiation.

Fifth, we'd explore value-added services. Technical consulting for large projects, construction management for affordable housing, quality auditing for infrastructure—services that leverage cement expertise but generate fee income independent of volumes. Transform from product supplier to solution provider.

The capital allocation framework would be explicit: 40% for maintenance and debottlenecking (generating 20%+ returns), 30% for strategic growth (15% return hurdle), 20% for technology and sustainability (10% return but strategic necessity), 10% for ventures and experiments (option value). This balanced approach maintains operational excellence while enabling innovation.

The communication strategy would shift from defending current performance to articulating long-term vision. Quarterly earnings calls would discuss 10-year strategic progress, not 90-day variations. Investor days would showcase technology leadership, customer relationships, and organizational capability—intangibles that drive long-term value but don't appear in financial statements.

Most importantly, we'd prepare for industry consolidation. Whether as consolidator or target, Ramco must be ready. This means clean corporate structure, transparent accounting, documented processes, and demonstrated synergies. When consolidation accelerates—and it will—prepared companies capture disproportionate value.

The future outlook balances optimism with realism. India needs enormous infrastructure investment—$1.4 trillion over the next decade. Affordable housing requires 20 million units annually. Industrial expansion demands commercial construction. These drivers ensure cement demand growth, even if the pace disappoints expectations.

But supply discipline remains elusive. Every demand uptick triggers capacity announcements. Regional players defend turf irrationally. New entrants bring patient capital. Until the industry consolidates to 4-5 players controlling 70% capacity (from current 10 players with 55%), pricing power remains elusive.

For Ramco, the path forward is clear if not easy. Maintain operational excellence—the foundation of everything. Deepen regional dominance—the source of pricing power. Expand selectively—growth for growth's sake destroys value. Invest in technology—the only sustainable differentiator. Develop people—the ultimate competitive advantage.

The remarkable journey from a single plant in 1961 to South India's cement leader demonstrates what's possible through patient execution of sound strategy. The next chapter—whether independent growth, sector consolidation, or strategic transformation—remains unwritten. But with strong assets, capable management, and clear strategy, Ramco is positioned to prosper regardless of path.

The cement industry will exist as long as humans build. The question isn't whether demand exists but who captures value. Companies with the lowest costs, best service, strongest relationships, and deepest capabilities will thrive. Others will survive. Some will disappear.

Ramco has proven it belongs in the first category. Through License Raj and liberalization, through booms and busts, through family transitions and technological disruptions, it has not just survived but strengthened. The next 60 years will bring different challenges—climate change, technological disruption, demographic shifts. But the principles that built Ramco—operational excellence, technological leadership, stakeholder focus, long-term thinking—remain timeless.

In the dusty quarries of Tamil Nadu where this story began, limestone still feeds kilns that transform rock into civilization's foundation. The process seems unchanged—crush, heat, grind, pack. But everything else has transformed—the technology, the scale, the complexity, the competition. Ramco's ability to preserve what matters while transforming everything else explains its endurance.

That, ultimately, is the lesson: in business, as in cement, strength comes not from rigidity but from the right mix of stability and adaptation, tradition and innovation, patience and urgency. Ramco has found that mix. Whether investors profit from it depends on their ability to match Ramco's timeline—measuring success not in quarters but in decades, not in stock prices but in competitive position, not in promises but in execution.

The story continues, one bag of cement at a time, building India's future on foundations laid 60 years ago by a visionary who saw opportunity where others saw obstacles. That vision, institutionalized and evolved, remains Ramco's greatest asset—worth more than plants, brands, or balance sheets. It's the belief that excellence, sustained over time, creates value that transcends cycles, surprises skeptics, and rewards the patient.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube