Rallis India: From Greek Trading House to Agri-Tech Powerhouse

I. Introduction & Episode Teaser

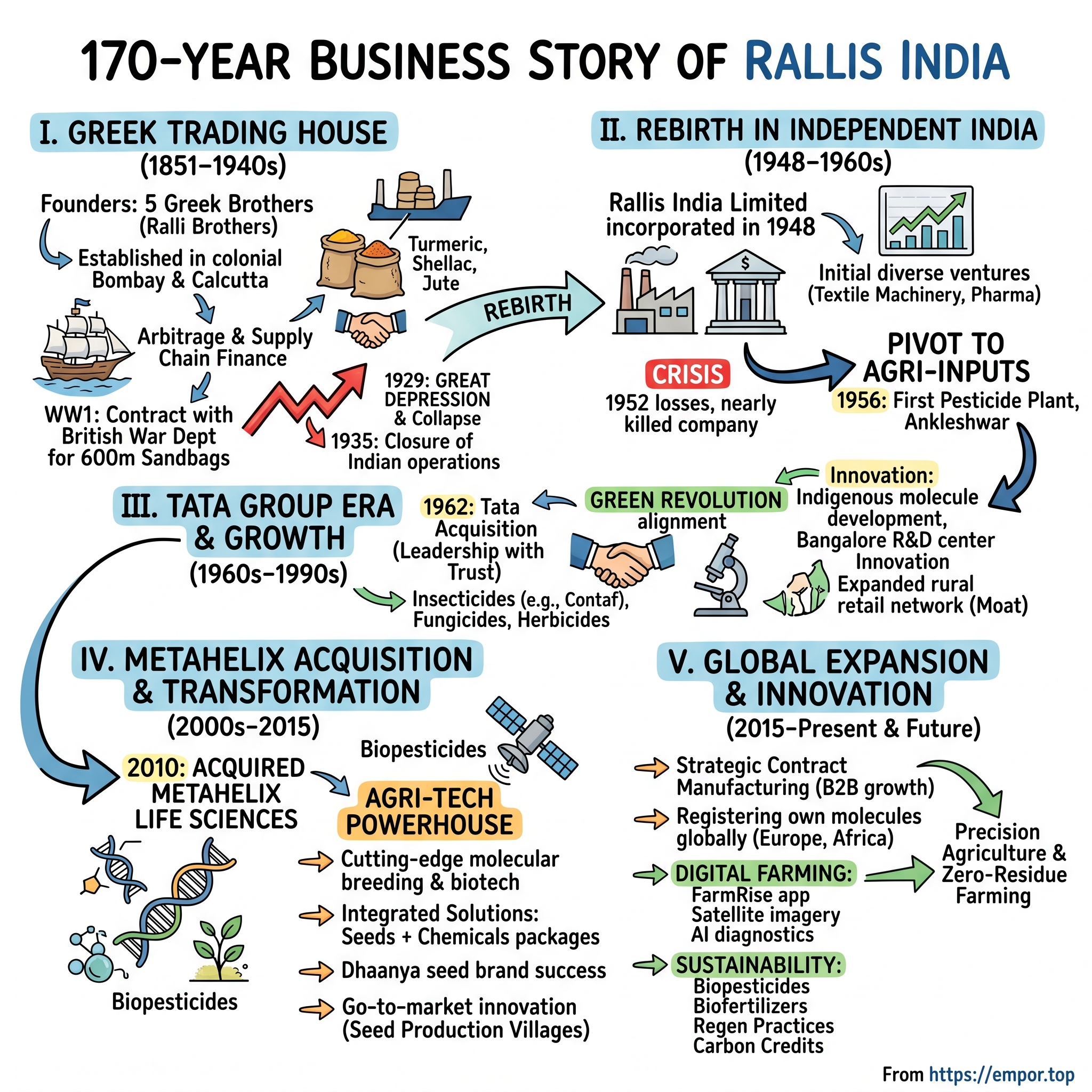

Picture this: Five Greek brothers from the island of Chios, their merchant empire stretching from Marseille to Manchester, from Constantinople to Calcutta. The year is 1851, and the Ralli Brothers have just opened their doors in colonial Bombay, trading in exotic goods—turmeric, shellac, and jute—that would soon clothe the British Empire's wars in sandbags. Fast forward 170 years, and that same company, now Rallis India, touches the lives of five million Indian farmers, its products protecting crops across 80% of India's districts.

This is the improbable story of how a 19th-century Greek trading house became India's agrochemical giant—a journey through colonial commerce, partition, corporate transformation, and ultimately, agricultural revolution. Today, Rallis India stands as a ₹7,251 crore market cap company, the Tata Group's sole representative in the agrochemical space, commanding a strategic importance that belies its relatively modest size within the conglomerate.

The question that drives our story isn't just how this transformation happened, but why it matters. In a nation where agriculture employs 43% of the workforce but contributes only 18% to GDP, Rallis represents something larger: the modernization of Indian farming itself. From importing goods on sailing ships to developing molecular compounds in research labs, from serving British war departments to empowering smallholder farmers with biotechnology—this is a company that has reinvented itself more times than most firms exist.

What we'll uncover is not just a corporate history, but a masterclass in adaptation. We'll explore how patient capital from the Tata Group allowed Rallis to survive decades of losses while building capabilities. We'll see how a pivot from trading to manufacturing to innovation created defensive moats in rural India. And we'll understand why, in an era of climate change and food security concerns, this 170-year-old company might be more relevant than ever.

II. The Ralli Brothers Era: Greek Merchants in Colonial India (1850s–1948)

The story begins not in India, but on the Greek island of Chios, where five brothers—Pandely, Eustratio, Toumazis, Augustus, and Zannis Ralli—were born into a wealthy merchant family. Their father, Stephen Ralli, had witnessed the shifting tides of global commerce in the aftermath of the Napoleonic Wars. The old Mediterranean trading routes were giving way to new imperial networks, and Stephen saw opportunity in the expanding British Empire. He relocated to Marseille, establishing a base that would serve as the launching pad for what would become perhaps the most successful expatriate Greek merchant business of the Victorian era.

In 1851, when the Great Exhibition in London was showcasing the industrial might of the British Empire, the Ralli Brothers made their decisive move eastward. They established operations in Calcutta and Bombay—the twin commercial hearts of British India. The timing was no accident. The American Civil War was about to create massive disruptions in global cotton supplies, the Suez Canal would soon reshape Asian trade routes, and India was emerging as the crown jewel of the British Empire's commercial network.

The brothers didn't just trade; they built an infrastructure empire. By the 1870s, Ralli Brothers employed 4,000 clerks and 15,000 warehousemen and dockers across their Indian operations. Their warehouses in Calcutta stretched along the Hooghly River, storing jute that would become burlap sacks for the world's grain harvests. In Bombay, their godowns held shellac for the gramophone records that would soundtrack the Jazz Age, sesame for Mediterranean kitchens, and spices that would flavor European tables.

What set the Rallis apart was their understanding of information arbitrage. In an era before telegraphs were common, they maintained their own communication networks—fast ships carrying market intelligence between ports, trusted agents in remote districts reporting on harvest conditions. They pioneered what we'd now call supply chain finance, extending credit to Indian farmers against future crops, essentially becoming rural India's first organized lenders.

When World War I erupted in 1914, Rallis India found itself holding the exclusive contract with the British War Department for jute sandbags. Consider the scale: millions of sandbags were needed monthly for the Western Front's trenches. The company's Calcutta mills ran 24 hours, their ships given military escort priority. Between 1914 and 1918, Rallis supplied an estimated 600 million sandbags to the Allied forces—a number that staggers even by today's standards.

But empires built on commodities are vulnerable to commodity cycles. The Great Depression of 1929 hit Rallis like a tsunami. Jute prices collapsed by 70%, global trade volumes plummeted, and the company found itself with warehouses full of unsellable inventory and mounting debts. By 1935, cash flow problems forced the Indian operations to close—a stunning reversal for a firm that had seemed invincible just years earlier.

The Argenti family, another Greek trading dynasty with whom the Rallis had both competed and collaborated, stepped in as agents to wind down operations. Through the late 1930s and World War II, the Rallis name in India existed more as a memory than a business—their grand offices on Bombay's Ballard Estate standing empty, their Calcutta warehouses repurposed for the war effort.

Yet even as the original Ralli Brothers empire crumbled, seeds of resurrection were being planted. Indian merchants who had worked with the company, British colonial administrators who remembered their reliability, and a new generation of Indian industrialists who had studied their methods—all carried forward lessons from the Rallis playbook. When India gained independence in 1947, the stage was set for an unlikely rebirth.

III. Rebirth in Independent India (1948–1962)

August 15, 1947: India gains independence. August 23, 1948: Rallis India Limited is incorporated in Bombay. Just 373 days separated colonial subjugation from corporate rebirth—a timeline that speaks to both urgency and opportunity in newly independent India.

The company that emerged was fundamentally different from its Greek predecessor. Where the Ralli Brothers had been traders and middlemen, the new Rallis India would be manufacturers and innovators. The founders—a consortium of Indian businessmen who had acquired rights to the Rallis name—understood that independent India needed not just to trade agricultural products but to transform agriculture itself.

The early vision was ambitious, perhaps overly so. Between 1948 and 1951, Rallis India launched into multiple ventures simultaneously: textile machinery, pharmaceuticals, and most presciently, fertilizers and pesticides. The logic seemed sound—a newly independent nation would need everything, and Rallis would provide it. The company's prospectus from this era reads like a manifesto for industrial self-reliance, echoing Nehru's vision of a modern, industrialized India.

In 1951, Rallis India went public on the Bombay Stock Exchange. The IPO was oversubscribed 3.2 times—remarkable for a company with more ambition than assets. Middle-class Indians, many investing in stocks for the first time, saw Rallis as a bet on India's agricultural future. The offering raised ₹2.5 crores, substantial capital for that era.

Then came 1952—the annus horribilis that nearly killed the company in its infancy. Everything that could go wrong did. The textile machinery division, having imported expensive European equipment, found no buyers as Indian mills struggled with post-partition disruptions. The pharmaceutical venture, lacking both technical expertise and distribution, hemorrhaged money. Even the fertilizer business, seemingly straightforward, stumbled on logistics—how do you transport bulk chemicals to farmers who can barely afford bullock carts?

By year-end 1952, Rallis India posted losses of ₹1.8 crores—nearly 75% of its IPO proceeds evaporated. The stock price collapsed from ₹100 to ₹22. Board meetings turned acrimonious, with investors demanding explanations and resignations. The company's first annual general meeting in 1953 lasted seven hours, with shareholders openly questioning whether Rallis should simply be liquidated.

It was in this crisis that the company's true pivot began. A young executive named K.K. Mistry, recruited from ICI (Imperial Chemical Industries), proposed a radical simplification: abandon everything except agricultural inputs. His logic was elegant—India had 350 million people to feed, farming employed 70% of the workforce, yet crop yields were among the world's lowest. The Green Revolution was still a decade away, but Mistry saw its necessity.

Between 1953 and 1958, Rallis methodically shut down its non-agricultural ventures, taking massive write-offs but freeing up capital and management focus. The company established its first pesticide formulation plant in Ankleshwar, Gujarat, in 1956—a modest facility that could produce 500 tons annually of DDT and BHC (both later banned but then considered miraculous).

The transformation showed in the numbers. From losses of ₹1.8 crores in 1952, Rallis returned to profitability by 1957, posting modest profits of ₹32 lakhs. By 1960, profits had grown to ₹78 lakhs. The stock, which had bottomed at ₹22, recovered to ₹85. More importantly, the company had found its calling.

But Rallis needed more than focus—it needed capital, technology, and management expertise to compete with multinational giants like Bayer and BASF entering India. The board began discrete discussions with potential partners. Two suitors emerged: Fisons, a British chemical company with phosphate expertise, and the Tata Group, India's most prestigious business house. The negotiations would culminate in a deal that would define Rallis for the next six decades.

IV. The Tata Acquisition & Transformation (1962–1978)

June 1962: In a wood-paneled boardroom at Bombay House, three men signed documents that would reshape Indian agriculture. Representing Fisons was Lord Hanworth, representing Tata was Naval Tata, and for Rallis India, chairman S.K. Krishnan. The deal structure was unusual—Fisons and Tata would become joint majority shareholders, with Fisons managing operations while Tata nominated the chairman. It was a marriage of British technical expertise, Indian capital, and local market knowledge.

The Tata connection ran deeper than mere investment. J.R.D. Tata, the group patriarch, saw agriculture as crucial to India's development. "You cannot industrialize a nation where farmers are poor," he once told his board. The Tatas brought not just capital but an ethos—the famous promise that "a Tata product is a guarantee of quality." For farmers accustomed to adulterated fertilizers and spurious pesticides, this reputation mattered immensely.

Under the joint arrangement, Fisons transferred technology for phosphatic fertilizers, crucial for Indian soils deficient in phosphorus. The first major investment was a ₹5 crore expansion of the Ankleshwar plant, adding capacity for 10,000 tons of technical-grade pesticides annually. But the real transformation was cultural. Fisons introduced systematic research protocols, quality control standards that exceeded Indian regulations, and crucially, the concept of "extension services"—teams of agronomists who would educate farmers on proper chemical usage.

By 1964, tensions emerged in the partnership. Fisons, facing financial pressures in Britain, wanted quicker returns. Tata, playing a longer game, prioritized market share over margins. The resolution came through a gradual buyout—Tata steadily increased its stake while Fisons retreated. By 1965, Rallis had become a Tata enterprise in practice if not yet in complete ownership.

The transformation under full Tata control was dramatic. Between 1965 and 1970, Rallis underwent a massive expansion through acquisitions. The company absorbed Ruby Chemicals (gaining insecticide capacity), Hindustan Insecticides (adding distribution networks), and most significantly, Fertilisers and Chemicals Travancore (FCT's) agrochemical division. Each acquisition wasn't just about assets—it was about capabilities. Ruby brought formulation expertise, Hindustan brought rural reach, FCT brought process technologies.

The 1971 Bangladesh Liberation War created unexpected opportunity. As refugees flooded into India and food security became paramount, the government launched "Grow More Food" campaigns. Rallis, with its expanded capacity, became a key supplier. Sales jumped from ₹12 crores in 1970 to ₹31 crores in 1972. But rapid growth brought problems—quality complaints increased, working capital stretched, and management systems creaked.

Enter Darbari Seth, appointed Managing Director in 1974. A chemical engineer from MIT and a Tata veteran, Seth brought American management methods to a company still run on colonial-era practices. He introduced cost centers, management information systems, and most radically, performance-linked bonuses. "We must think like farmers, not chemists," became his motto, pushing the company to develop products suited to Indian conditions rather than simply copying Western formulations.

The period saw Rallis develop its first indigenous pesticide molecule—a pyrethroid variant effective against bollworms in cotton. The R&D effort took four years and cost ₹3 crores—massive for that era—but proved Rallis could innovate, not just manufacture. The company also pioneered "combination products," pre-mixing pesticides to reduce farmer application costs, a practice later adopted globally.

By 1978, Rallis had transformed from a troubled trading firm reborn as a chemical company into India's largest agrochemical manufacturer. Revenues reached ₹89 crores, the company operated four manufacturing plants, and its products reached 100,000 villages. The Tata acquisition, initially seen as a rescue, had become a transformation story. But the real growth was yet to come.

V. Building the Agrochemical Empire (1980s–2000s)

The 1980s opened with Rallis making a decision that would define its next three decades: absolute focus. Under chairman Nani Palkhivala's directive, the company shut down its engineering division (manufacturing spray equipment) and its pharmaceutical business (generic antibiotics), both marginally profitable but massive distractions. The board meeting minutes from 1981 record heated debate—several directors argued diversification reduced risk. Palkhivala's response was prescient: "In agrochemicals, we can be number one in India. In everything else, we'll be also-rans."

The focus enabled radical restructuring. The Ankleshwar plant, once a collection of sheds, was rebuilt as an integrated complex capable of producing 25,000 tons annually. New plants came up in Pune (for specialty pesticides) and Akola (strategically located in Maharashtra's cotton belt). But the real innovation was in the research center established in Bangalore in 1983—India's first private-sector agrochemical R&D facility.

The Bangalore center, headed by Dr. V.S. Rao (poached from Union Carbide), became Rallis's innovation engine. The mandate was ambitious: develop six new compounds annually, with at least two reaching commercialization within five years. The early years were disappointing—of 30 compounds synthesized between 1983-1986, none reached market. But persistence paid off. By 1990, Rallis had launched three proprietary molecules, including an innovative fungicide for grape downy mildew that captured 60% market share within two years.

The seeds business, started almost accidentally in 1987 when Rallis acquired a struggling hybrid corn company, became a surprise success. The insight was integration—selling seeds along with crop protection chemicals created a "solutions" approach that farmers valued. By the early 1990s, Rallis had become India's fourth-largest seed company, with particular strength in cotton and vegetable seeds.

The 1991 liberalization changed everything. Suddenly, multinational giants—Monsanto, DuPont, Syngenta—could enter India directly. Many predicted Rallis would be crushed. Instead, the company thrived through what management called "the Goldilocks strategy"—not competing with multinationals on cutting-edge technology, nor with local players on price, but finding the "just right" middle ground of appropriate technology at affordable prices.

A defining moment came in 1994 when Rallis launched "Contaf," an insecticide specifically formulated for Indian cotton varieties and pest patterns. Monsanto's competing product, technically superior, cost three times more. Contaf captured 40% market share within 18 months. The lesson was clear: in Indian agriculture, "good enough" at the right price beat perfection.

The late 1990s saw Rallis building distribution muscle. The company pioneered the "Rallis Krishi Samadhan" centers—one-stop shops where farmers could buy inputs, get soil tested, and receive agronomic advice. By 2000, 500 such centers operated across six states. This retail presence, expensive to build but impossible for competitors to quickly replicate, became a crucial moat.

Financial performance reflected the strategy's success. Revenues grew from ₹89 crores in 1980 to ₹650 crores by 2000—a 10.5% CAGR sustained over two decades. More impressively, EBITDA margins expanded from 8% to 15% as the company moved up the value chain from commoditized chemicals to specialty products and services.

The 2000s brought new challenges. The government, under pressure from environmental groups, banned several older pesticides that were Rallis staples. Chinese generic manufacturers began dumping products at prices below Rallis's raw material costs. Bt cotton, genetically modified to resist pests, reduced insecticide demand by 30% in key markets. By 2008, despite revenues crossing ₹1,000 crores, profits stagnated.

The financial crisis of 2008-09 nearly broke the company. Commodity chemical prices crashed, farmers defaulted on credit, and Rallis posted its first loss in decades—₹42 crores in FY09. The stock price halved. Analysts questioned whether the focused agrochemical strategy had run its course.

But by year-end 2009, in a dramatic turnaround, Rallis posted profits of ₹100 crores. The recovery came from an unexpected source: contract manufacturing for global giants looking to reduce costs. Rallis's plants, upgraded over decades and now meeting international standards, became preferred suppliers for companies like FMC Corporation and Nippon Soda. This B2B business, invisible to farmers but highly profitable, would become a crucial second engine of growth.

In 2010, another transformation began. Tata Chemicals, consolidating its holdings, made Rallis a direct subsidiary (previously, ownership was scattered across multiple Tata companies). This simplified structure enabled the next big move: the acquisition that would redefine Rallis's future.

VI. The Metahelix Acquisition & Seeds Revolution (2010–2015)

Dr. K.K. Narayanan, managing director of Rallis, stood before the board in October 2010 with a proposal that divided the room: acquire Metahelix Life Sciences for ₹410 crores—nearly half Rallis's market cap. Metahelix was burning cash, had never turned a profit, and operated in the controversial realm of agricultural biotechnology. Half the board saw disaster; Narayanan saw destiny.

Metahelix wasn't just another seed company. Founded in 2000 by scientists from Monsanto and Mahyco, it possessed something Rallis desperately needed: cutting-edge research capabilities in molecular breeding and biotechnology. The Bangalore-based company had spent a decade building a library of germplasm (genetic material) covering rice, cotton, corn, and vegetables—essentially, the source code for crop improvement.

The strategic rationale went beyond technology. Global agriculture was consolidating—the "Big Six" (Monsanto, DuPont, Syngenta, Dow, Bayer, BASF) controlled 75% of private sector agricultural R&D. For Rallis to remain relevant, it needed to move beyond being a chemicals company that also sold seeds to become an integrated agricultural solutions provider. Metahelix was the bridge to that future.

Integration proved challenging. Metahelix's 200 scientists, accustomed to academic freedom and long research horizons, clashed with Rallis's quarterly earnings focus. Several key researchers left within six months. The companies operated on different timescales—Rallis measured success in seasons, Metahelix in plant generations. Early integration meetings devolved into mutual incomprehension.

The breakthrough came through an unlikely source: farmer feedback sessions. When Rallis brought Metahelix scientists to field demonstrations in Punjab, the researchers saw their laboratory creations wilting under real-world conditions—heat stress, water scarcity, pest pressure their controlled environments hadn't replicated. Conversely, Rallis field staff saw how genetic improvements could reduce chemical dependency. Both sides realized they needed each other.

By 2012, the first integrated products emerged. A drought-tolerant corn hybrid, developed using Metahelix's marker-assisted breeding but refined through Rallis's field trials, became a category leader. More innovative was the "package approach"—selling seeds with tailored chemical regimens, essentially prescribing treatment plans for crops. Farmers paid 20% premiums for these integrated solutions.

The seeds division, rebranded as "Dhaanya" (Sanskrit for grain), became Rallis's growth engine. Between 2010 and 2015, seed revenues grew from ₹78 crores to ₹340 crores—a 34% CAGR. The portfolio expanded to 35 hybrids across seven crops. Particularly successful were vegetable seeds, where Rallis captured 15% market share in hybrid tomatoes and peppers, categories dominated by multinational players.

The real innovation was in go-to-market strategy. Rallis created "Seed Production Villages"—partnering with entire communities to produce certified seeds, guaranteeing buyback at premium prices. This solved two problems: ensuring seed quality (farmer-produced seeds met specifications 95% of the time versus 70% from contractors) and creating rural prosperity that built brand loyalty.

Technology transfer accelerated. Metahelix's tissue culture capabilities enabled Rallis to mass-produce disease-free potato and banana plantlets—high-value products that commanded 50% gross margins. The company also ventured into biofertilizers and biopesticides, leveraging Metahelix's microbiology expertise to develop products aligned with growing environmental consciousness.

But the acquisition's greatest value was defensive. In 2013, when DuPont attempted to acquire Rallis (offering a 40% premium), the board could credibly argue that Metahelix's pipeline justified higher valuations. The takeover was rejected. Two years later, when Chinese companies dumped generic seeds at predatory prices, Rallis's proprietary varieties maintained pricing power because farmers trusted their performance.

By 2015, the Metahelix acquisition was vindicated. The combined entity generated ₹180 crores in EBITDA from seeds alone—meaning the acquisition paid for itself in under four years. More importantly, Rallis had transformed from a chemicals company that happened to sell seeds into an agricultural technology company that happened to manufacture chemicals. The distinction would prove crucial as the industry evolved.

VII. Modern Era: Contract Manufacturing & Global Expansion

The letter arrived on a humid Mumbai morning in July 2016: FMC Corporation, the American agricultural giant, wanted Rallis to manufacture three complex molecules exclusively for global markets. The five-year contract was worth $200 million. For Rallis, manufacturing for others might have seemed like retreat—from brand owner to contract manufacturer. CEO V. Shankar saw it differently: "We're not going backward; we're going global."

Contract manufacturing wasn't new to Rallis—the company had quietly made products for Japanese firms since 2005. But post-2015, it became strategic. The logic was compelling: global agrochemical companies, facing investor pressure to improve returns, wanted to close high-cost European and American plants. India offered 60% cost advantages, but most local manufacturers couldn't meet quality standards. Rallis, with its Tata pedigree and decades of operational excellence, became the partner of choice.

The numbers told the story. Contract manufacturing revenues grew from ₹200 crores in 2015 to ₹680 crores by 2020—a 28% CAGR. Margins were attractive: while domestic formulations earned 12-15% EBITDA margins, contract manufacturing delivered 20-25%. The business was also counter-cyclical—when Indian monsoons failed and domestic demand dropped, global contracts provided stability.

Rallis didn't just manufacture; it became a development partner. The company's Turbhe facility near Mumbai was upgraded to handle multi-step synthesis, allowing production of complex molecules that few Indian companies could attempt. When Nippon Soda needed a facility for a new fungicide requiring cryogenic reactions (below -50°C), Rallis invested ₹45 crores in specialized equipment, securing a 10-year exclusive contract.

The international business expanded beyond contract manufacturing. Rallis began registering its own molecules in international markets—a expensive, lengthy process (registration in the EU took average 4 years and cost ₹8 crores) but crucial for margins. By 2020, Rallis products were registered in 58 countries, from Vietnam to Venezuela.

Africa became a surprise success. Rallis's products, designed for small Indian farmers, translated perfectly to African conditions—similar plot sizes, comparable pest pressures, price sensitivity. The company's cotton insecticides captured 25% market share in Tanzania. In Kenya, Rallis's potato fungicides became category leaders. African revenues grew from ₹50 crores in 2015 to ₹300 crores by 2022.

Distribution innovation drove domestic growth. Rallis couldn't match the advertising budgets of multinationals, so it went direct. The company deployed 1,000 "Rallis Sampark" vans—mobile stores that brought products to villages too small for permanent shops. Each van was equipped with soil testing kits, weather stations, and tablets loaded with crop advisory apps. Farmers could see weather forecasts, check market prices, and receive customized spray schedules.

Digital transformation went deeper. In 2018, Rallis launched "FarmRise," a mobile app that used satellite imagery to assess crop health and recommend interventions. Within two years, 500,000 farmers had downloaded it. The app was free, but users bought 30% more Rallis products than non-users—proof that information was the ultimate loyalty program.

The retailer network, now 70,000 strong covering 80% of India's districts, became a data goldmine. Rallis knew which villages were planting what crops, which pests were emerging where, and how weather patterns affected demand. This information enabled precision inventory management—the company reduced working capital requirements by 20% while improving product availability.

Sustainability became central to strategy. Rallis introduced biodegradable packaging, reduced water consumption in manufacturing by 30%, and launched "Green Guards"—biological pesticides that complemented chemical products. When the government announced restrictions on certain chemicals, Rallis was ready with alternatives. Environmental compliance, once seen as cost, became competitive advantage.

In July 2023, Tata Chemicals increased its stake in Rallis from 50.06% to 55.05%, investing ₹300 crores. The message was clear: despite being among the smaller Tata companies, Rallis was strategic. As Tata Chemicals' CEO explained: "Agriculture is where chemistry meets biology meets data science. Rallis is our platform for that convergence."

The modern Rallis bore little resemblance to its trading house origins. The company operated six manufacturing facilities, employed 3,000 people, and generated ₹3,200 crores in revenue. Yet challenges remained—Chinese competition, regulatory pressures, climate change impacts. But with contract manufacturing providing stability, international markets offering growth, and digital tools enabling efficiency, Rallis had more levers to pull than ever before.

VIII. Product Portfolio & Innovation Strategy

Inside Rallis's Bangalore Innovation Center, Dr. Padma Krishnan holds a vial containing what might be the future of Indian agriculture: a novel fungicide molecule that targets plant pathogens while leaving beneficial soil microbes untouched. It took her team seven years and ₹50 crores to develop. In the hypercompetitive world of agrochemicals, where Chinese companies can copy and produce generic versions within months, why does Rallis still invest in innovation?

The answer lies in the portfolio strategy that Rallis has methodically built. The company operates across five distinct business verticals, each serving different customer needs and risk profiles. Domestic crop protection remains the core, contributing 45% of revenues through 60+ formulations covering insecticides (40% of sales), fungicides (35%), and herbicides (25%). But it's the interplay between divisions that creates value.

Take "Nagata," Rallis's blockbuster insecticide for cotton and vegetables. While competitors offer similar active ingredients, Rallis combines it with proprietary adjuvants that improve leaf absorption by 30%. This formulation technology, protected by process patents rather than molecule patents, provides a 3-4 year competitive advantage—crucial time to establish market presence before generics arrive.

The innovation strategy, crystallized in the motto "Serving Farmers through Science," operates on three horizons. Horizon 1 (current year) focuses on formulation improvements and line extensions. Horizon 2 (2-5 years) develops new combinations and delivery systems. Horizon 3 (5+ years) pursues novel molecules and biological products. This staged approach ensures steady launches while maintaining long-term pipeline.

Plant growth nutrients, contributing 15% of revenues, exemplify value-addition. "Geolife," Rallis's specialty fertilizer brand, combines traditional nutrients with biostimulants—seaweed extracts, amino acids, humic substances. These products command 40% price premiums over commodity fertilizers. The secret is customization: 15 different formulations target specific soil deficiencies across India's diverse agricultural zones.

The seeds division showcases integration benefits. When Rallis develops a new hybrid, the crop protection team simultaneously develops optimal chemical protocols. "Akshay," a cotton hybrid, comes with a season-long protection package—specific pesticides timed to growth stages. Farmers buying this integrated solution report 20% higher yields than those buying seeds and chemicals separately.

Biological products represent the future. Rallis's "Bio-Genesis" range includes Trichoderma (a beneficial fungus), Pseudomonas (bacteria that fight root diseases), and neem-based pesticides. Currently just 5% of revenues, biologicals grow at 35% annually. The challenge is education—convincing farmers that invisible microbes can protect crops requires extensive demonstration and trust-building.

Research capabilities underpin everything. The Innovation Center employs 200 scientists across chemistry, biology, and data science. The facility includes controlled environment chambers simulating different climatic conditions, molecular biology labs for marker-assisted breeding, and India's largest private repository of soil samples—50,000 specimens mapping the country's agricultural diversity.

Recent breakthroughs demonstrate capability evolution. In 2022, Rallis launched "Yokozuna," a patented fungicide for sheath blight in rice. What's remarkable isn't just the molecule but the development process: AI algorithms screened 100,000 potential compounds, identifying 50 for synthesis, of which three reached field trials, and one commercialized. This compressed development time from 10 years to 6.

The company holds 45 patents, with 20 more pending. But intellectual property strategy goes beyond patents. Rallis maintains trade secrets around manufacturing processes—specific reaction conditions, purification techniques, formulation methods—that provide sustainable advantages even after patents expire.

Sustainability initiatives, once peripheral, now drive innovation. "Sustainable Crop Solutions" certification, covering 30 products, guarantees reduced environmental impact. "Clean & Green" herbicides biodegrade 50% faster than conventional products. Water-soluble packaging eliminates plastic waste. These products command 10-15% premiums from environmentally conscious farmers and export markets.

The Responsible Care recognition from Indian Chemical Council—awarded to only 12 companies—validates operational excellence. Rallis's Ankleshwar plant achieved zero liquid discharge in 2020, recycling 100% of process water. Energy intensity reduced 25% through cogeneration and solar installations. Safety metrics match global standards: 0.3 lost-time injuries per million man-hours versus industry average of 2.1.

Digital integration augments traditional R&D. Satellite imagery identifies pest outbreaks before visible symptoms appear. Weather stations predict disease pressure. Soil sensors optimize fertilizer application. This data feeds back into product development—understanding exactly when, where, and why products succeed or fail accelerates innovation cycles.

The innovation strategy faces challenges. Developing a new molecule costs ₹200-300 crores with 10% success probability. Regulatory approval takes 3-4 years. Generic competition emerges within 18 months of launch. Yet Rallis persists because innovation creates defensibility. As CEO Sanjiv Lal explains: "Anybody can manufacture chemicals. Not everybody can solve farmers' problems. That's where science becomes competitive advantage."

IX. Playbook: Business & Investing Lessons

The Rallis story offers a masterclass in corporate longevity and transformation. What lessons emerge from 170 years of evolution—from Greek traders to Tata subsidiary to agri-tech innovator?

The Power of Patient Capital and Conglomerate Backing

When Rallis posted losses for three consecutive years in the early 1950s, when it struggled through the 2008 financial crisis, when the Metahelix acquisition took four years to pay off—the company survived because Tata provided patient capital. This isn't just about deep pockets. Conglomerate backing provided credibility with farmers ("Tata doesn't make bad products"), access to talent (rotation programs brought expertise from Tata Steel and TCS), and strategic flexibility (the ability to sacrifice short-term profits for long-term position).

The contrast with standalone competitors is stark. Pesticides India, a similar-sized peer, couldn't invest counter-cyclically during downturns and lost market share. Excel Crop Care, lacking patient capital, sold to Sumitomo when Chinese competition intensified. Rallis's ability to think in decades rather than quarters—a luxury provided by stable ownership—enabled transformation rather than mere survival.

Pivoting from Trading to Manufacturing to Innovation

Rallis's three pivots—from trading (1850s-1940s) to manufacturing (1950s-1990s) to innovation (2000s-present)—each required abandoning successful models for uncertain futures. The pattern is instructive: pivots succeeded when driven by external disruption (independence, liberalization, biotechnology) rather than internal strategy. Companies that pivot proactively often pivot too early; those that wait for market signals pivot with validation.

The execution pattern matters too. Rallis didn't abandon previous capabilities—it layered new ones. Manufacturing capability enabled innovation. Trading relationships became distribution networks. This accumulation of capabilities created compound advantages that pure-play competitors couldn't match.

Building Distribution Moats in Rural India

Rallis's 70,000 retailer network, reaching 80% of India's districts, took 50 years to build. It's a classic example of a slow-burn competitive advantage. Unlike technology or products that can be copied, distribution networks exhibit increasing returns—each additional retailer makes the network more valuable to farmers (convenience) and suppliers (reach).

The moat isn't just physical presence but embedded relationships. Rallis retailers often extend credit to farmers, provide agronomic advice, and serve as information nodes. These social connections, built over generations, can't be disrupted by e-commerce or direct-to-farmer models. When Bayer tried entering India through digital channels in 2019, they ultimately partnered with established networks like Rallis's.

Managing Cyclicality in Agriculture

Agriculture is inherently cyclical—monsoons, commodity prices, pest outbreaks. Rallis developed multiple hedges: geographic diversification (different regions have different seasons), product diversification (seeds do well when pesticides struggle), and business model diversification (contract manufacturing provides stability when domestic markets fluctuate).

The company also learned to read cycles. Management tracks 30+ indicators—reservoir levels, commodity futures, government procurement prices—to predict demand 6-12 months ahead. This enables pre-positioning inventory, adjusting production, and managing working capital. During the 2019 drought, Rallis reduced inventory by 30% before the season, avoiding write-offs that hurt competitors.

The Tata Ethos: Leadership with Trust

"Leadership with Trust"—the Tata motto—manifests tangibly at Rallis. When spurious pesticides killed crops in Andhra Pradesh in 2018, Rallis replaced competitor products for affected farmers, earning loyalty that marketing couldn't buy. During COVID-19, Rallis kept factories running (agriculture was essential service) while providing workers full pay plus hazard compensation.

This trust translates to pricing power. Rallis products command 5-10% premiums over identical generics because farmers believe in quality consistency. Retailers stock Rallis products because return rates are 60% lower than industry average. Banks lend to Rallis at 50 basis points below comparable companies because governance standards reduce risk.

Contract Manufacturing as Strategic Hedge

The decision to embrace contract manufacturing—seemingly a step backward from branded products—proved strategically brilliant. It provided four benefits: stable revenues during agricultural downturns, access to global technology through partner relationships, capacity utilization that improved manufacturing economics, and competitive intelligence about international markets.

The key insight: contract manufacturing isn't commoditized if you move up the complexity curve. Rallis focused on difficult chemistries—multi-step synthesis, hazardous reactions, precise specifications—that few Indian companies could handle. This created switching costs for clients and 20%+ EBITDA margins versus 8-10% for simple toll manufacturing.

The playbook reveals a broader truth: sustainable competitive advantages in commodity industries come not from any single factor but from the accumulation of small advantages—trust, distribution, capabilities, relationships—that compound over time. Rallis succeeded not through disruption but through patient accumulation of hard-to-replicate assets. For investors, the lesson is clear: in evaluating industrial companies, look beyond products and technology to the organizational capabilities that enable adaptation across cycles and generations.

X. Analysis & Bear vs. Bull Case

Bull Case: The Agricultural Transformation Play

The optimist's view of Rallis starts with a simple observation: India feeds 1.4 billion people using farming methods that are decades behind global standards. Average yields for rice, wheat, and cotton are 50-60% below China's and 30-40% below global averages. This yield gap represents enormous opportunity for agricultural input companies.

Consider the structural tailwinds. India's agricultural solutions market, currently $8 billion, grows at 8-10% annually—faster than GDP. Within this, the shift from commoditized chemicals to specialty products and integrated solutions accelerates margins. Rallis, with its established distribution and farmer trust, is positioned to capture disproportionate value from this premiumization.

The contract manufacturing business provides a second growth engine with different dynamics. Global agrochemical companies face pressure to reduce manufacturing footprints and environmental liabilities. India offers not just cost advantages but regulatory stability and technical capability. Rallis's contract manufacturing revenues could double by 2027 as more molecules go off-patent and production shifts to India.

Having Tata Chemicals as a 55% shareholder provides strategic advantages beyond capital. Tata Chemicals' basic chemistry expertise enables backward integration, reducing raw material costs by 10-15%. Group synergies—shared R&D, cross-selling opportunities, management expertise—create value not reflected in standalone analysis.

The distribution network represents an underappreciated asset. With rural smartphone penetration crossing 50%, Rallis's 70,000 touch-points become nodes for digital services—credit, insurance, advisory. This platform could be monetized through partnerships with fintech and agri-tech companies, creating revenue streams beyond traditional products.

Climate change, paradoxically, benefits Rallis. Erratic weather increases pest and disease pressure, driving demand for crop protection. Farmers facing yield uncertainty invest more in quality inputs. Rallis's stress-tolerance seeds and protective chemicals become essential rather than optional, supporting pricing power.

The international opportunity remains underpenetrated. Rallis generates just 20% of revenues from exports versus 40-50% for peers like UPL and PI Industries. As product registrations accumulate and manufacturing capabilities expand, international revenues could reach ₹1,500 crores by 2027, improving margins through geographic diversification.

Recent initiatives show management execution. The bio-pesticides portfolio, though small, grows at 35% annually. Digital tools improve farmer engagement and reduce customer acquisition costs. Sustainability initiatives, beyond compliance, attract premium customers and international partners. These aren't transformative individually but collectively indicate a company adapting successfully to changing markets.

Bear Case: The Commodity Trap

The skeptic's case begins with a harsh reality: Rallis has delivered just 3.4% revenue CAGR over the past five years, underperforming both inflation and agricultural sector growth. This isn't cyclical weakness but structural challenge—the company operates in commoditizing segments where pricing power erodes continuously.

Chinese competition represents an existential threat. Chinese manufacturers, with 40-50% cost advantages from scale and subsidies, have destroyed margins in generic pesticides. They're moving up-market into formulations and even seeds. Rallis's response—focusing on specialty products—works only until Chinese companies target those segments too.

Regulatory risks loom large. The government, under environmental pressure, regularly bans pesticides that constitute significant revenues. When Monocrotophos was banned in 2018, Rallis lost ₹80 crores in annual sales overnight. Europe's Green Deal could eliminate 50% of chemical pesticides by 2030—a precedent India might follow. Rallis's chemical-heavy portfolio faces obsolescence risk that markets underappreciate.

The seeds business, despite Metahelix acquisition, remains subscale. Rallis has 2% market share versus Nuziveedu's 15% or Kaveri's 10%. Biotechnology development requires massive investment—Monsanto spent $1.5 billion developing Bt cotton. Rallis lacks resources to compete meaningfully in next-generation traits like gene editing or RNA interference.

Digital disruption threatens distribution advantages. Companies like DeHaat and AgroStar offer direct-to-farmer models that eliminate intermediaries. While Rallis's retailer network provides current advantage, it could become a liability—70,000 relationships to manage, credit to extend, margins to share. Digital natives without legacy infrastructure might leapfrog traditional players.

Financial metrics raise concerns. Return on capital employed (ROCE) has declined from 18% in 2018 to 12% in 2023. Working capital days increased from 95 to 120 as channel inventory builds. The company generates ₹200-250 crores in operating cash flow—insufficient for major capacity expansion or acquisition without dilution.

The parent relationship cuts both ways. While Tata provides stability, it also imposes constraints. Conservative financial policies prevent aggressive expansion. ESG commitments limit product choices. Management bandwidth gets consumed by group initiatives. Rallis might be better off as an independent company or part of a global agrochemical major.

Competition intensifies from all directions. Multinationals like Bayer and Corteva bring superior technology. Local players like Dhanuka and Insecticides India compete on price and relationships. New entrants like Adama and Crystal Crop Protection combine Chinese supply chains with Indian distribution. Rallis, caught in the middle, lacks clear differentiation.

The macro environment deteriorates. Input cost inflation (energy, chemicals, logistics) squeezes margins. Farmer incomes, despite government support, remain stressed—limiting ability to pay premiums. Climate change, while driving some demand, also increases business volatility and working capital requirements.

The Verdict

The truth, as often, lies between extremes. Rallis is neither the transformation story bulls envision nor the commodity trap bears fear. It's a steady, defensive business with modest growth prospects and limited downside. For investors seeking excitement, Rallis disappoints. For those valuing stability, predictability, and gradual improvement, it merits consideration.

The key variables to watch: contract manufacturing growth (indicating global competitiveness), biologicals adoption (showing innovation capability), and ROCE improvement (demonstrating execution). If two of three trend positive, the bull case gains credibility. If not, the bear case prevails. At current valuations—trading at 18x P/E versus historical average of 22x—markets seem to be pricing in modest expectations, creating asymmetric risk-reward for patient investors.

XI. Epilogue & Looking Forward

As monsoon clouds gather over Mumbai in June 2024, Rallis India stands at another inflection point. The company that began with Greek merchants trading jute in colonial Calcutta now deploys artificial intelligence to predict pest outbreaks across millions of farms. The transformation seems complete, yet the story is far from over.

India's agricultural transformation—the backdrop against which Rallis operates—accelerates. The country must feed 1.6 billion people by 2050 while facing water scarcity, soil degradation, and climate volatility. Traditional solutions—more fertilizer, more pesticides—reach diminishing returns. The future demands precision agriculture: exactly the right input, at the right time, in the right place. This transition from broadcast to precision, from chemistry to biology, from products to solutions, defines Rallis's next chapter.

Climate change reshapes everything. Erratic monsoons, rising temperatures, and new pest pressures make traditional farming calendars obsolete. Rallis responds by developing climate-resilient solutions—drought-tolerant seeds, heat-stable pesticides, stress-mitigation biologicals. The company's weather stations and satellite monitoring systems, collecting data from 10,000 locations, feed machine learning models that predict agricultural risks 30 days ahead. This predictive capability, still nascent, could become core competitive advantage.

Digital agriculture promises revolution but delivers evolution. Rallis's experiments—drone spraying, IoT sensors, blockchain traceability—show mixed results. Farmers adopt technology that provides immediate, visible benefits but resist complexity. The winning formula emerges: simple interfaces delivering sophisticated analytics. Rallis's "FarmRise" app, redesigned with WhatsApp-like simplicity, now guides 800,000 farmers through personalized crop calendars.

Sustainable agriculture transitions from niche to necessity. European buyers demand residue-free produce. Domestic consumers, increasingly health-conscious, pay premiums for organic food. Government policy shifts toward natural farming. Rallis adapts by expanding biological products, developing biodegradable formulations, and creating "residue management" protocols that ensure chemical-free harvests. The company's "Project Shoonya" (zero residue) covers 50,000 hectares today but targets 500,000 by 2027.

The next frontier is carbon. Agriculture contributes 14% of India's greenhouse gas emissions but could become carbon negative through regenerative practices. Rallis pilots carbon credit programs where farmers earn income by sequestering carbon through cover crops and reduced tillage. Early results show farmers earning ₹3,000-5,000 per hectare from carbon credits—meaningful supplementary income. If scaled, this could transform Rallis from input supplier to sustainability partner.

Organizational evolution continues. Rallis hires data scientists alongside chemists, agronomists alongside software engineers. The average employee age dropped from 45 to 35 over five years as digital natives join traditional agricultural experts. This cultural transformation—from manufacturing mindset to service orientation—challenges but energizes the organization.

For investors and entrepreneurs, Rallis offers timeless lessons. First, longevity requires continuous reinvention—the company that survives 170 years is not the same company throughout but multiple companies within continuous corporate identity. Second, in commodity industries, competitive advantage comes from accumulation rather than disruption—thousands of small improvements compound into insurmountable leads. Third, patient capital enables transformation—the ability to invest through cycles, to accept short-term pain for long-term gain, remains rare and valuable.

The strategic questions facing Rallis mirror those confronting Indian agriculture: How to balance productivity with sustainability? How to serve smallholder farmers profitably? How to compete globally while remaining locally relevant? The answers remain uncertain, but the company's history suggests adaptive capacity to find them.

As we conclude this journey through Rallis's past and present, the future beckons with both promise and peril. Climate change, technological disruption, and geopolitical shifts create unprecedented uncertainty. Yet agriculture remains humanity's foundational activity—people must eat, crops must grow, farmers must farm. Companies that help them do so better, more sustainably, more profitably, will endure and thrive.

Rallis India—from Greek trading house to Tata subsidiary to agri-tech innovator—embodies this endurance. The company that survived colonial extraction, partition violence, industrial transformation, and market liberalization now faces digital disruption and climate crisis. History suggests it will adapt, evolve, and emerge transformed once again. For in the end, Rallis's story is not about chemicals or seeds or technology. It's about feeding India—a mission that began with trading rice in 1851 and continues with gene editing in 2024.

The monsoon clouds burst, sending traders scurrying for cover on Dalal Street. But in Rallis's boardroom, executives plan for seasons yet to come. Some companies measure success in quarters, others in years. Rallis, approaching its second century, measures success in generations. In Indian agriculture, where patience is prerequisite and change is constant, that perspective remains its greatest asset.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube