Raj Rayon Industries: The Textile Phoenix of Silvassa

I. Introduction & The "Zombie" Resurrection

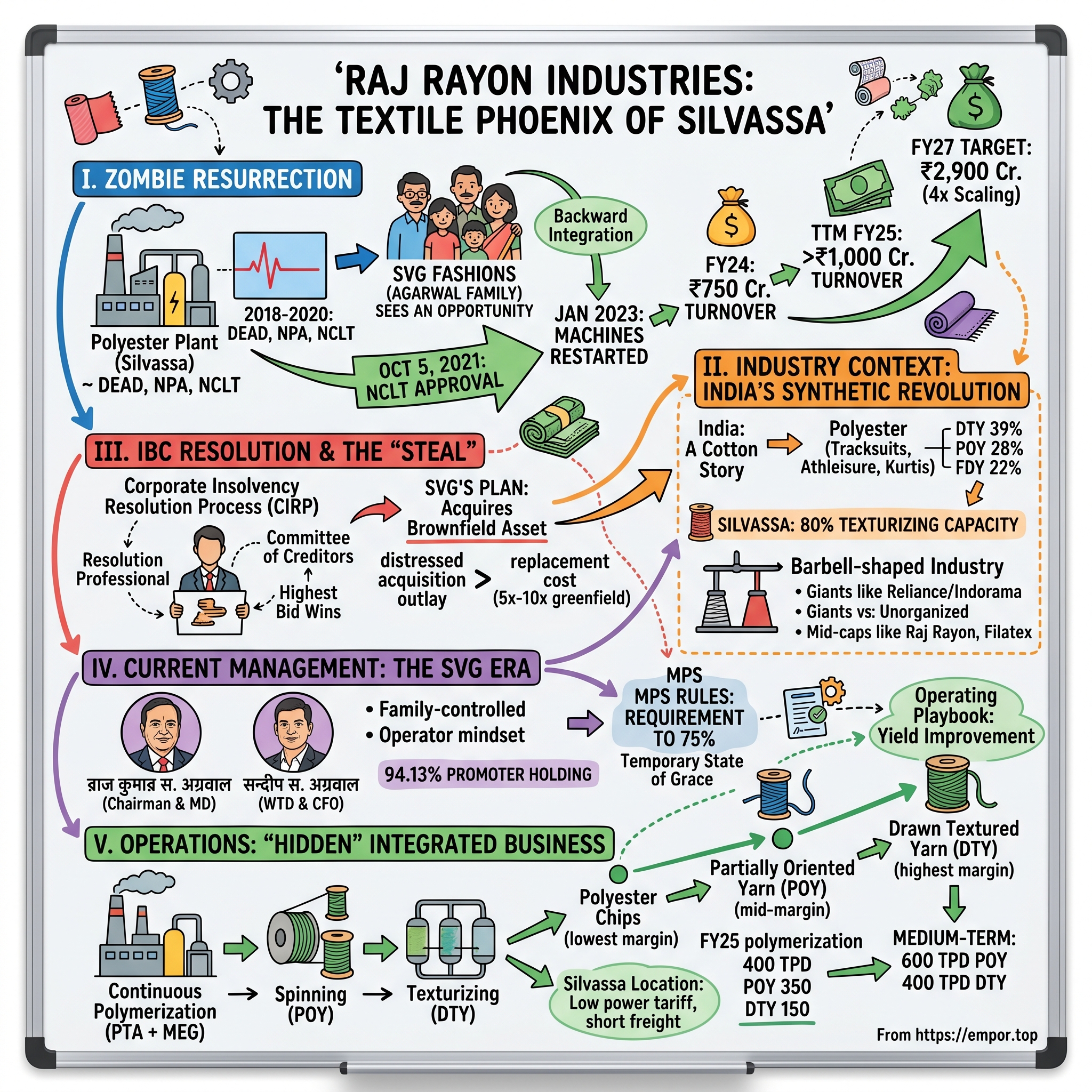

There is a particular kind of silence that settles over an industrial estate when the machines stop. Not the silence of a holiday, when the gates are locked and lights are off, but the deeper hush of capital that has been written down. Walk past the chain-link in places like सिलवासा Silvassa in 2020 and you would have heard it in a 25-acre compound off the Mumbai–Ahmedabad highway: a 600,000-square-foot polyester plant that had not spun a single ton of yarn since 2018, its boilers cold, its paychecks unpaid, its name dragged before the National Company Law Tribunal in Ahmedabad.12

That plant was Raj Rayon Industries Limited. By every conventional measure, it was dead. The lenders had marked it as a non-performing asset. Production had ceased. Promoters had walked. The एनएसई NSE ticker still flickered on screens, but only in the way a flatlining EKG flickers — a procedural twitch on the way to delisting. In the cold prose of insolvency law, the company had become what bankers privately call a "zombie" — technically alive, economically buried.2

And then, exactly as the IBC framers had hoped, something unexpected happened. A Mumbai-based polyester fabric weaver — a private family firm called SVG Fashions, run by the Agarwal family — looked at this corpse and saw, rather than a graveyard, the missing piece of a vertically integrated textile machine. They submitted a resolution plan. The committee of creditors voted. The NCLT Ahmedabad bench signed off on October 5, 2021.2 The machines were turned back on in January 2023.3

Within the first full year of restarted production, Raj Rayon recorded a turnover of roughly ₹750 crore — an all-time high in the company's three-decade history.3 By the financial year ended March 2025, that number had climbed past ₹1,000 crore on a trailing twelve-month basis, and the new owners had publicly set their sights on ₹2,900 crore by FY27.14 That is a roughly 4x scaling target, anchored against a brownfield asset most of the market had already given up on.

This is, in other words, a story about the messiest and most under-appreciated piece of plumbing in modern Indian capitalism: the भारतीय दिवाला और शोधन अक्षमता संहिता Insolvency and Bankruptcy Code (IBC) of 2016 and the way it is quietly recycling distressed industrial assets back into the productive economy. Raj Rayon is not a unicorn. It is not a moat-rich consumer brand. It is, depending on how you squint, either a polyester yarn manufacturer or a real options bet on what happens when you take a half-built thermal-power-and-polymer complex, hand it to operators who actually know how to run it, and then let them sweat it without legacy debt.

The episode runs in three acts. First, the collapse — how a 1993-vintage Silvassa textile player got itself into bankruptcy. Second, the resolution — how the Agarwal family's SVG Fashions cleared the NCLT process, and why the price they paid is the entire investment thesis. And third, the operating playbook — what the new management has actually done with the plant, the segment mix between polyester chips, POY and DTY, and where the ₹2,900 crore target either becomes a base rate or a cautionary tale.

This is not a story about a glamorous franchise. It is a story about the cost of replacement, the value of a clean balance sheet, and what happens when a textile commodity asset gets a second life under operators with skin in the game. Let's get into it.

II. The Industry Context: India's Synthetic Revolution

To understand why a 350-tons-per-day polyester yarn plant in a Union Territory most foreign analysts cannot find on a map can credibly target a 4x revenue scale-up, you have to first understand what Indian textiles actually look like in 2026 — and what they used to look like in 1993, when Raj Rayon was incorporated.

India was, for most of its post-independence economic history, a cotton story. Hindi cinema costume designers, the Bombay mills, the cooperative spinners of Tamil Nadu, the खादी khadi political symbolism — all of it ran on cotton. Synthetic fibers were treated as the cheap, slightly disreputable cousin: the stuff of bus seat covers and uniform shirts. Then the middle class expanded, urbanized, and started buying tracksuits, branded innerwear, athleisure, and the printed ladies' kurtis that fill every high-street rack in Delhi or Surat. The fiber that quietly took over that wardrobe was polyester.

By the mid-2020s, polyester filament yarn was the workhorse of the Indian apparel value chain. It was cheap, it dyed brilliantly, it traveled well across humidity and temperature, and — critically for a country that imports most of its energy — its raw material chain was anchored in petrochemicals already being produced at scale by रिलायंस इंडस्ट्रीज Reliance Industries. Polyester filament yarn, in segment terms, broke down roughly into Drawn Textured Yarn (DTY) at around 39% of demand, Partially Oriented Yarn (POY) at 28%, and Fully Drawn Yarn (FDY) at about 22% globally — a mix that India broadly tracked.5

The peculiar thing about Indian polyester production is its geographic concentration. Drive about three hours north of Mumbai into the Union Territory of दादरा और नगर हवेली Dadra and Nagar Haveli, and you arrive in Silvassa: a small, low-tax, low-friction industrial enclave where, according to local industry estimates, roughly 80% of India's polyester texturizing capacity is housed.6 रिलायंस Reliance runs one of its larger PFY plants there. So does Alok Industries. The town is, in functional terms, the polyester yarn capital of the country. If you want to be in this business, you either build in Silvassa or you accept a permanent freight and tax penalty against players who did.

The structure of the Indian polyester yarn industry is barbell-shaped. At one end, you have the giants — रिलायंस Reliance, इंडोरामा वेंचर्स Indorama Ventures, integrated through the entire petrochemical chain from purified terephthalic acid (PTA) and monoethylene glycol (MEG) all the way through to fabric. At the other end, you have hundreds of small unorganized texturizers — single-line operators with one or two machines, no balance sheet, surviving on conversion margins of a few rupees per kilogram. In the middle sits a thin band of mid-cap integrated players: companies like फिलाटेक्स इंडिया Filatex India, संगम इंडिया Sangam India, गार्डन सिल्क मिल्स Garden Silk Mills (in its various afterlives), अलोक इंडस्ट्रीज Alok Industries, and Raj Rayon. Filatex alone runs a 600-tons-per-day plant at Dahej, and as recently as January 2025, its board cleared a further ₹155 crore expansion.7 These are the mid-cap operators that Raj Rayon is benchmarking against.

The brutal truth of polyester yarn as a business is that it is, fundamentally, a spread game. The chip-maker buys PTA and MEG, polymerizes them into chips, spins them into POY, and texturizes that POY into DTY. At every step the value addition is real but modest, and competition is fierce. The two structural variables that decide whether you make money are (a) the cost of power, because polymerization is brutally electricity-intensive, and (b) capacity utilization, because fixed costs per kilogram fall sharply once you push your reactors past the 70% utilization line. Almost every textile bankruptcy in India in the last twenty years can be traced to one of two failures: building too much capacity at too high a debt load, or running too low on utilization to amortize fixed costs. Often both.

That, in essence, is what happened to the original Raj Rayon. The 1990s and 2000s saw Indian textiles attract aggressive bank lending against capacity expansion, much of it in foreign currency. When the rupee weakened, when global polyester prices wobbled, when Chinese over-capacity bled into export markets — the players who had borrowed most aggressively, with the least sophisticated treasury operations, found themselves unable to service their interest costs. The original Raj Rayon, by 2018, was one of those players. Production halted. Lenders filed.13 The IBC clock started ticking.

The lesson the next operator would have to absorb was the obvious one, but it is the obvious lessons that bankruptcy proceedings exist to enforce. In a commodity business, your balance sheet is your strategy. And the company that emerged from the NCLT process would be defined, more than anything else, by what it no longer carried.

III. Inflection Point: The IBC Resolution & The "Steal"

The NCLT Ahmedabad bench, on a Tuesday in January 2020, admitted application C.P. (IB) No. 350/NCLT/AHM/2019 against Raj Rayon Industries Limited.2 The corporate insolvency resolution process — what Indian bankers shorthand as CIRP — was now formally underway. A resolution professional was appointed. Operations were already at a standstill. Creditors were invited to submit claims. And, most importantly for our story, prospective resolution applicants were invited to submit plans to acquire the company.

The IBC was at this point a young statute — passed in 2016, refined through a flurry of Supreme Court cases and amendments, and only just beginning to deliver its first wave of large-asset resolutions. The framework's core promise was elegantly simple: take a defaulting company, freeze its operations under a moratorium, hand control to a court-appointed professional, run a competitive bidding process, and let the highest credible bid wash through the capital structure. Equity holders typically got wiped out. Operational creditors took deep haircuts. Financial creditors recovered what the bid mechanics allowed. The new owner walked away with the assets — clean of legacy litigation, clean of legacy debt, and clean of the operational baggage that had killed the previous regime.

Into this process walked SVG Fashions Private Limited. SVG was not a financial sponsor. It was not a private equity fund. It was a Mumbai-based weaving and processing house, founded in 1984, run by the Agarwal family, that had spent four decades building a vertically integrated textile business with facilities in सिलवासा Silvassa, दमन Daman, and अंकलेश्वर Ankleshwar.3 They wove polyester fabric. They processed it. They made garments and home furnishings. What they did not do — what they bought from third parties at margins they did not control — was make their own polyester yarn.

You can already see the strategic logic. For a fabric weaver, the input cost line that hurts most is yarn, because yarn pricing tracks petrochemical volatility and the merchant yarn market is dominated by giants who set the spread. The dream of every integrated weaver is backward integration into spinning, and beyond that into polymerization, and ultimately into chips. SVG had spent decades looking at this problem, and now an entire 350 TPD POY plant — sitting in Silvassa, where they already operated — was being put up for auction at distressed prices.

The Committee of Creditors voted on the SVG plan in their tenth meeting. The NCLT Ahmedabad bench gave its approval order on October 5, 2021.2 Public reporting and subsequent industry interviews indicate that SVG's headline acquisition outlay through the resolution plan was a relatively modest sum — in the range of a few tens of crores — followed by a much larger ₹300 crore programme of post-acquisition capital expenditure to actually restart and re-tool the plant.3

This is the part of the story that deserves to be slowed down, because the entire investment thesis hinges on it. Forget the headline acquisition number for a moment and think about replacement cost. A greenfield 350-TPD POY plant with continuous polymerization in India, built today, would require land acquisition, environmental clearances, two to three years of construction, civil works, imported spinning lines, captive power tie-ups, and working capital. Industry rules of thumb suggest the all-in greenfield capex for that profile would run into many hundreds of crores — comfortably 5x to 10x what SVG paid in the resolution and the subsequent restart together. They were not buying earnings. They were buying a brownfield with assets that would have cost the rest of the industry several years and several thousands of crores to replicate.

The other thing they were buying, almost as an afterthought, was a public listing. Raj Rayon's shares continued to trade on the एनएसई NSE under the ticker RAJRILTD even as the company moved through CIRP. For SVG — a private family business — a listed vehicle was a free option on future capital raises, employee stock plans, and an eventual liquidity event for the founding family. Resolution applicants in distressed Indian situations often inherit this listed-vehicle optionality at no incremental cost, and it is one of the under-appreciated drivers of why family business groups have become some of the most active bidders in the IBC ecosystem.

The accounting around the resolution is worth pausing on. As is typical in IBC cases, the resolution plan extinguished the existing equity, allotted new shares to the resolution applicant, and converted residual creditor balances — operational and statutory — into preference shares with long-dated terms.8 The company that emerged blinking into 2022 was, on paper, a different animal: same plant, same workforce shell, same ticker, but a fundamentally restructured capital stack. It is hard to overstate how rare and valuable this is. In a sector defined by legacy debt servicing, Raj Rayon was now operating from a near-clean slate.

Did SVG overpay? In hindsight, the answer is plainly no. They paid distressed-asset prices for a brownfield with optionality, in a sector where the marginal cost of new capacity is dominated by long lead times and clearance frictions they did not have to face. The operating question — the one that still hangs over the story today — is whether they can run it.

IV. Current Management: The SVG Era

The man most associated with the Raj Rayon turnaround — and the one whose name appears on the regulatory filings as Whole Time Director and Chief Financial Officer — is संदीप सत्यनारायण अग्रवाल Sandiip Satyanarayan Agarwwal.3 His older relative, राजकुमार सत्यनारायण अग्रवाल Rajkumar Satyanarayan Agarwal, holds the chairman and managing director title.9 Together, the two run a family-controlled operating shop with little of the polish or PR machinery of a Mumbai-listed mid-cap and a great deal of operational hands-on time on the shop floor.

Sandiip Agarwal's background tells you most of what you need to know about the operating philosophy. He holds an MBA from नरसी मुनजी इंस्टीट्यूट NMIMS University in Mumbai. By his own count, he has spent more than three decades in textiles — first inside the family business, then as the architect of SVG's expansion into home furnishings, and most recently as the executive who personally led the Raj Rayon acquisition and turnaround.3 He is, in the parlance of operations, a yarn guy. He can talk about denier counts and titanium dioxide ratios and the way a polymerization reactor's residence time changes the IV (intrinsic viscosity) of the chip. This is not a financier who acquired a textile asset. This is a textile operator who happened to use the IBC as an acquisition channel.

That distinction matters, because the IBC has produced two different species of resolution applicant. The first is the financial sponsor — usually a stressed-asset fund, sometimes a global private equity name — that buys the asset for spread and either turns it around through a parachuted-in CEO or sells it on. The second is the strategic operator — typically an existing player in the same value chain — who buys for backward or forward integration. The first type tends to optimize for sale multiples. The second type tends to optimize for through-life cash flows. Sandiip Agarwal, and SVG more broadly, are unambiguously in the second camp. The Raj Rayon plant is not a holding to be flipped. It is the spinning-and-polymerization head of a fabric-and-garment business that already exists.

The shareholding pattern reflects this. As of the most recent filings, SVG Fashions Private Limited alone held 84.88% of Raj Rayon's equity, with the wider promoter group holding roughly 94.13%, and public shareholders rounding out the rest.94 This is, by any sensible standard, an extraordinary level of skin-in-the-game. There is no pretense of professional managerial separation. The family that owns the parent runs the listed subsidiary, and the wealth of the family is concentrated almost entirely in the same plant the listed company runs.

The flip side of that concentration is the regulatory clock that is now ticking on it. SEBI's minimum public shareholding (MPS) rules require listed Indian companies to maintain at least 25% public float, which means promoters cannot hold more than 75%.10 Companies that emerge from IBC with promoter holdings well above that ceiling — and Raj Rayon, at 94%, is one of the more extreme examples — are typically given a multi-year window to comply. The mechanics of compliance can be brutal on near-term share prices: it usually involves a qualified institutional placement, an offer-for-sale, or a long-dated employee stock plan, all of which create supply pressure on the float. We will return to this in the bear case. For now, simply note that 94% promoter holding is not a destination — it is a temporary state of grace, and the path to 75% is one of the most important capital markets events in the company's near future.

The cultural shift inside the company, by all available accounts, has been pronounced. Pre-IBC Raj Rayon was a debt-laden industrial firm with the classic stressed-asset pathologies: deferred maintenance, overdue working capital, demoralized middle management, and a strategic plan dictated by interest coverage rather than market opportunity. Post-IBC Raj Rayon is, fundamentally, a department of SVG run as a separately listed entity. Management discipline is family-style: capital allocation decisions sit with the Agarwals, capacity utilization is treated as a sacred metric, and the entire operating cadence is oriented around what bankers euphemistically call "sweating the assets" — pushing the plant toward maximum throughput as quickly as the market allows.

There is something culturally familiar about this style if you have spent any time around mid-cap Indian manufacturing. The promoter-operator model — where the family is on the shop floor, on the supplier calls, and on the export shipping documents — is deeply unfashionable in modern corporate governance circles, but it has historically been the dominant generator of industrial alpha in India. It comes with real risks (key-person concentration, related-party-transaction grey zones, succession opacity) and real benefits (decision speed, alignment, frugality). For Raj Rayon, the bet is that the benefits compound faster than the risks accumulate.

The strategic chess move now is execution. SVG bought a sleeping plant. They restarted it. The question that defines the next three years is whether they can take it from a 250-tons-per-day commissioned-but-ramping facility to the 700-TPD fully-utilized integrated complex that the public targets imply.13 That, in turn, depends on what is actually happening inside the gates of the Silvassa plant.

V. Operations: The "Hidden" Integrated Business

Step inside the Silvassa complex and the first thing you notice — once your eyes adjust to the contrast between the bright outdoor sun and the cavernous, mostly grey interior — is how vertical the layout is. Continuous polymerization reactors at one end, where PTA and MEG enter as white powder and ethylene glycol liquid and emerge minutes later as molten polymer. Spinning bays in the middle, where the polymer is extruded through showerhead-like spinneret plates into thousands of fine filaments, then quenched, drawn, and wound onto bobbins as POY. And texturizing lines further down, where those POY bobbins are unspooled, false-twisted, heat-set, and rewound as the bulkier, springier DTY that the fabric trade actually buys. Each step is a different segment in the company's published P&L. Each is a different margin.1

The product taxonomy is worth slowing down on, because it is the entire commercial story. At the bottom of the value chain sit polyester chips — small, lentil-sized white pellets of polyethylene terephthalate produced by polymerizing PTA and MEG. Chips are the most commoditized output: the spread between the input mix and the chip price is thin and tightly correlated to PTA-MEG futures. Selling chips on the merchant market is essentially a way of monetizing surplus polymer capacity when downstream spinning is at its limit.

One step up is POY. Partially Oriented Yarn is what you get when the molten polymer is spun through spinnerets and partially drawn — meaning the polymer chains are aligned but not fully oriented along the fiber axis. POY is the standard merchant yarn that small texturizers buy. It is reasonably commoditized but commands a higher margin per kilogram than chips, simply because it has captured one more value-addition step. POY is Raj Rayon's bread and butter — the volume product that fills the trucks leaving Silvassa.

The interesting product, and the one that most clearly shapes the equity story, is DTY. Drawn Textured Yarn takes POY and runs it through a texturizing machine, where it is simultaneously twisted, heat-set, and untwisted to produce a curly, voluminous filament that mimics the bulk and softness of natural fibers. DTY is what most fabric weavers actually want. It is the input for athleisure, sarees, kurtis, suiting, and home furnishings. Margins on DTY run materially higher than on POY — Raj Rayon's own published targets imply DTY margins in the 10–12% range against POY margins of 5–7%.1 DTY is also more technically differentiated: titer, denier, luster, dye uptake, and texturizing recipe all matter for end-use specs, which means a competent DTY producer has a small but real moat against the unorganized texturizing fringe.

What SVG has been quietly doing — and what the public market took some time to register — is shifting Raj Rayon's product mix up the value chain. In the first phase of the restart, the plant ran primarily on bought-in chips, spun POY, and sold to merchant texturizers. That generates revenue but not margin. The next phase, executed across a series of capital expansions, was to bring polymerization in-house, so that the plant could feed itself from PTA-MEG rather than buying chips at a markup. By the end of FY25, polymerization capacity had reached 400 tons per day, with POY capacity at 350 TPD and DTY at 150 TPD.14 That is a fully integrated mid-cap configuration, and crucially, it pushes more of the eventual product into the higher-margin DTY bucket.

The company's published roadmap is to keep going. The medium-term target is 600 TPD of POY capacity and 400 TPD of DTY, financed by a ₹500–600 crore capex programme spread over the next two to three years.1 The math here is the real interesting part. Once polymerization is sized to feed the full POY line, and POY in turn is sized to feed an expanded DTY line, the marginal kilogram coming off the plant is heavily weighted toward higher-margin DTY rather than lower-margin merchant POY. That mix shift, more than the topline number, is what creates the operating leverage the FY27 ₹2,900 crore target is built on. The published segment-revenue mix at that target — POY ₹780 crore, DTY ₹1,760 crore, chips ₹360 crore — implicitly bets that DTY becomes the dominant revenue contributor.1

There are three specific things the market seemed to miss as this scaling was happening. First, the speed: the company executed three consecutive capacity expansions in roughly 24 months, which for an asset this size is operationally aggressive.1 Second, the sequencing: each expansion was financed primarily out of internal accruals and modestly increased borrowings, with total borrowings only at ₹262 crore as of March 2025 against assets of around ₹500 crore — a leverage ratio that is comfortable for the sector.4 Third, the product mix: most analysts modeled Raj Rayon as a POY merchant; in practice, the operating focus has been on DTY, the segment with structurally higher margins and more defensible end-customer relationships.

Sitting behind all of this is the Silvassa location itself. Power tariffs in दादरा और नगर हवेली Dadra and Nagar Haveli have historically been favorable for textile players, the freight to the Mumbai port and to the Surat fabric markets is short, and the local industrial ecosystem — chemical suppliers, packaging, transporters, machine engineers — is dense enough that capacity restarts and expansions face fewer logistical bottlenecks than they would in a less established hub.6 None of these are individually unique advantages, but stacked together they are non-trivial. They are why 80% of India's polyester texturizing sits in this strip of UT real estate, and why Raj Rayon is competing on cost with the largest integrated players rather than the unorganized fringe.6

The deeper question, then, is not whether Raj Rayon can execute another 100 TPD of capacity addition. It is whether the structural advantages of a debt-light brownfield in the Silvassa hub translate into a durable cost edge as the cycle turns. Which brings us to the strategy frameworks.

VI. Strategy Framework: Hamilton's 7 Powers

It is tempting, when looking at a turnaround story like Raj Rayon, to mistake balance-sheet repair for competitive advantage. They are not the same thing. A clean balance sheet wins you the right to compete at industry margins. A power, in the Hamilton Helmer sense, wins you the right to earn above-industry margins on a sustained basis. So the analytically interesting question is: which of the seven powers, if any, does Raj Rayon actually have access to?

Start with Scale Economies. Polyester polymerization, like most petrochemical-derivative processes, is a textbook scale game. The fixed costs — reactor capital, captive utilities, manpower at minimum staffing — are largely independent of throughput, while the variable costs of PTA, MEG, and electricity scale linearly with output. Above a certain utilization line, every additional ton of yarn carries fixed-cost absorption that small unorganized texturizers — running single-digit-TPD operations on bought-in chips — simply cannot match. At 400 TPD of polymerization, Raj Rayon is comfortably inside the scale economy zone for an integrated mid-cap.1 It is not at Reliance's scale, and it never will be, but it is decisively above the fragmented bottom of the market. As the plant moves toward 600 TPD POY and 400 TPD DTY, that scale advantage strengthens. This is a real, if moderate, power.

Then there is Process Power — the slow accumulation of operating know-how that compounds inside an organization and is hard for new entrants to replicate. Helmer's classic example is トヨタ Toyota's production system, which took decades for competitors to even partially understand. Raj Rayon's analogue is more humble but, in its sector, real: the discipline of restarting a dormant polymerization line, of tuning the power-to-yarn ratio (electricity is the single largest variable cost in polyester yarn manufacturing, often more than 25% of conversion cost), of optimizing changeovers between yarn deniers without sacrificing yield. SVG's three-decade textile heritage shows up here.3 The "turnaround secret" is not a secret — it is the unglamorous, daily discipline of yield improvement, and it is one of the few places where an operating-house acquirer can outperform a financial-sponsor acquirer in the same asset.

Cornered Resource is perhaps the most straightforward power to identify. Silvassa is, in the most literal sense, a cornered resource for Indian polyester. The Union Territory has historically offered favorable tax treatment, lower land costs, predictable industrial power, and proximity to both ports and downstream fabric markets.6 Raj Rayon's 25-acre footprint inside this hub is not replicable in a meaningful way for new entrants — there is only so much industrial land in the UT, and the existing players are not selling. This is not a power that produces extreme economic profit on its own, but it is a structural cost advantage versus textile players in less optimal geographies.

The remaining four powers — Counter-Positioning, Switching Costs, Branding, and Network Economies — are essentially absent. Raj Rayon does not have a counter-positioned business model relative to Reliance; its model is structurally similar, just smaller and more focused. There are no meaningful switching costs in merchant yarn sales — fabric weavers buy on price and quality, not on relationships. Branding is non-existent at the yarn layer; even at the fabric layer, polyester is overwhelmingly white-label. And there are no network economies in this commodity chain.

The honest assessment, then, is that Raj Rayon has access to about two and a half of the seven powers — Scale Economies, Process Power, and a partial Cornered Resource via Silvassa. That is more than most small textile players can credibly claim, but it is meaningfully less than what consumer-facing textile brands enjoy. The implication is important: Raj Rayon's economic profitability over the cycle will likely sit somewhere between the unorganized fringe (low and volatile) and the integrated giants (moderate and stable), with the absolute level driven primarily by capacity utilization and the PTA-MEG-yarn spread.

The clean balance sheet, while not itself a Helmer power, functions as a strategic enabler. With borrowings of around ₹262 crore against revenues now exceeding ₹1,000 crore, interest coverage is comfortable.4 That gives management the option to pursue capex through a mix of internal accruals and incremental debt without the existential pressure that defined the pre-IBC company. In a cyclical commodity business, the players that survive the troughs are the ones with optionality at the bottom of the cycle, and Raj Rayon has more optionality than most of its peers.

The strategy frameworks tell you, in summary, that Raj Rayon is a structurally stronger version of a structurally average business. It is what you would get if you took a generic polyester yarn plant, gave it an integrated owner, located it in the right place, and stripped its balance sheet to the studs. That is not a wide-moat compounder. It is, more honestly, a well-positioned cyclical operator with embedded operating leverage as it scales toward full utilization. Whether that is enough depends on the broader competitive forces playing out around it.

VII. Porter's Five Forces Analysis

The more orthodox lens on competition — Michael Porter's five forces, drawn up at Harvard Business School in the late 1970s — is in some ways better suited to commodity industrial businesses than the Helmer powers framework. Porter is fundamentally about the structural attractiveness of an industry. Polyester yarn manufacturing in India is not a structurally attractive industry. But it is one with internal segmentation, and Raj Rayon sits in a segment that is more attractive than the average.

Rivalry, in the Porter sense, is intense. The Indian polyester yarn market has at least half a dozen credible mid-cap operators, an integrated giant in रिलायंस Reliance whose marginal economics on PFY are essentially unbeatable, and a fragmented texturizing fringe that competes on price for spot orders. Margins across the sector compress and expand with the PTA-MEG spread, and any individual producer's pricing power on POY or even DTY is limited to the brief windows when the cycle leans favorable. What differentiates Raj Rayon inside this rivalry, structurally, is the clean balance sheet — peers like अलोक इंडस्ट्रीज Alok Industries are still working through the operational consequences of past distress, while integrated peers like फिलाटेक्स इंडिया Filatex India and संगम इंडिया Sangam India carry varying levels of conventional debt service.7 Being one of the lowest-leverage integrated players in a high-rivalry sector is not a power, but it is a real cost advantage at the trough of the cycle.

Buyer Power is genuinely high in this industry, and that is the unromantic reality the bull case has to swallow. Fabric weavers, garment makers, and merchant yarn traders are organized, price-aware, and switch suppliers easily. Most yarn purchases are spot, with no contractual lock-in. Volume buyers — large garment manufacturers, branded apparel players, exporters — can and do play producers off against each other on quality-equivalent specs. The mitigating factor for Raj Rayon is the move into DTY, where end-customer specifications are tighter and the pool of qualified suppliers is smaller. DTY also lends itself to specialty variants — moisture-wicking yarns, antimicrobial yarns, recycled-content yarns — where the buyer power, while still meaningful, is reduced by technical fit. Raj Rayon's published portfolio explicitly includes cationic and anti-microbial yarn variants, hinting at this premiumization push.4

Supplier Power is moderately high, primarily because the upstream petrochemical chain is concentrated in a small number of large producers — रिलायंस Reliance, इंडियन ऑयल Indian Oil, मित्सुबिशी Mitsubishi, इंडोरामा Indorama — and PTA and MEG prices are essentially set by global supply-demand and crude oil dynamics, neither of which the yarn producer can influence. The mitigation here is structural: every other yarn producer in India faces the same supplier power, so it is not a relative disadvantage so much as an industry-wide friction. The producer who can pass through input cost movements fastest, on the back of the most flexible product mix, wins.

Threat of New Entrants is, against all instinct, low for the integrated mid-cap segment. The capital cost of a greenfield 350-TPD POY plant with continuous polymerization is large enough — and the construction lead time and clearance friction onerous enough — to deter new entrants without an existing strategic motive. The IBC has, paradoxically, been one of the few channels through which new strategic players have actually entered the segment, and Raj Rayon itself is an example of that. But once the wave of distressed-asset acquisitions clears, new capacity will overwhelmingly come from existing integrated players expanding their own brownfields, not from new participants. That favors incumbents.

Threat of Substitutes is, for polyester at large, low. Cotton remains polyester's main substitute, but cotton has structural disadvantages — water-intensive, subject to monsoon dependence, more expensive per kilogram of fabric, and prone to shrinkage and color fade. Within synthetics, viscose, nylon, and acrylic occupy specific niches but do not compete head-on with polyester for the bulk apparel and home-furnishing market. Recycled polyester is the most credible long-term competitive threat, and Raj Rayon's parent group has flagged investment in this area, which is the industry-standard hedge.3 Globally, polyester remains the cheapest synthetic fiber by a significant margin, and that price advantage is largely structural.

Putting the five forces together, the picture is one of an unattractive industry with pockets of relative attractiveness. The integrated mid-cap segment, with brownfield assets, low leverage, and a DTY-weighted mix in the Silvassa cluster, is the most attractive pocket. That is exactly the segment Raj Rayon now occupies. The Porter analysis does not tell you the company will earn extraordinary returns. It tells you the company is positioned where the structural drag from the industry's worst features — rivalry, buyer power, supplier power — is least severe, and where the structural protection from new entrants and substitutes is most pronounced.

The investing implication is uncomplicated. This is not an industry where you ride structural alpha. It is one where you bet on operational execution, balance sheet discipline, and capacity utilization at favorable points in the input cost cycle. Which is, conveniently, the only kind of bet a turnaround playbook can credibly support.

VIII. The Playbook: Business & Investing Lessons

There is a particular class of investing case study that the post-2016 IBC era has produced, and Raj Rayon is one of its cleanest examples. Call it the distressed-asset playbook — the strategic acquisition, by an existing operator, of a brownfield manufacturing asset through bankruptcy court, at a price meaningfully below replacement cost, financed by the buyer's own cash flow, executed without the legacy debt service that killed the previous regime. It is a playbook that has been run, with varying degrees of success, on भूषण स्टील Bhushan Steel (acquired by टाटा Tata in 2018), मॉनेट इस्पात Monnet Ispat (acquired by जे.एस.डब्ल्यू. JSW), एस्सार स्टील Essar Steel (acquired by आर्सेलर मित्तल ArcelorMittal-निप्पॉन Nippon JV in 2019), and several smaller cases. In every successful version, the same elements appear.

First, the buyer is a strategic operator, not a financial sponsor. The asset is acquired for use, not for sale. This matters because the day-one operational decisions — workforce retention, supplier renegotiation, restart sequencing, working-capital deployment — are made by people who plan to live with the consequences for a decade, not exit on a five-year fund clock. SVG's behavior since 2021 — the ₹300 crore of post-acquisition capex, the three consecutive expansions, the commitment to integrate vertically into PTA-MEG sourcing — is the textbook strategic-operator behavior.13

Second, the asset is bought at distressed prices but operated at industry-standard capability. The mistake distressed-asset buyers make is to assume that if the price is low enough, mediocre operations will still produce a good return. They will not. Polyester yarn margins are too thin and the cycle is too punishing. The good distressed-asset buyers recognize that the discount on the asset is a one-time gain; the actual return on the investment depends on bringing the asset to industry-standard operational capability. The scale-up to 400 TPD of polymerization is precisely that move.

Third, the buyer benefits from a "Day 1" mindset that pre-IBC operators cannot replicate. The legacy creditors are paid out (or not) through the resolution plan; the new owner inherits the assets and the listing but not the obligations. There is no overhang of preference shareholders demanding redemptions, no senior debt with restrictive covenants, no operational creditors threatening winding-up petitions. Every rupee of operating cash flow is available for either reinvestment or distribution. In a sector where peers are still routing meaningful portions of EBITDA to interest service, this is a structural cost-of-capital advantage that compounds over years.

Fourth — and this is the part most retail investors miss — the IBC playbook works best when the listed vehicle survives the resolution. Raj Rayon's NSE listing made it through CIRP, which means the new owners inherited not just the operating asset but the public company structure. That structure is the channel through which the asset's value will eventually be re-rated by the public markets, monetized through the eventual MPS dilution to 75%, and used as currency for any future acquisitions. The listed vehicle is the back door through which family-business value gets onto the public ledger.

The benchmarking against peers is informative. फिलाटेक्स Filatex operates at much higher absolute capacity — 600 TPD at Dahej alone — but trades at lower asset-turnover ratios and carries a more complex capital structure.7 संगम इंडिया Sangam India is more diversified across cotton, denim, and yarn, with lower polyester exposure. अलोक इंडस्ट्रीज Alok Industries, post its own IBC resolution, is in a structurally similar situation but at much larger scale. Against these peers, Raj Rayon's investment characteristics are smaller-scale, higher-growth-runway, and more concentrated on the polyester-yarn vertical. The investing thesis is essentially that a smaller integrated player, with a clean balance sheet and a runway from 400 to 700 TPD, can compound revenue at sector-beating rates for the next three to four years simply by completing the announced capex programme.

The risk of that thesis is, of course, that revenue scaling does not equal profit scaling. Polyester yarn margins move with the spread, and a cyclical downturn in the global polyester market — whether driven by a slowdown in the Chinese export apparel chain, by a spike in PTA-MEG prices, or by a glut of new capacity in Southeast Asia — could compress unit margins faster than capacity additions can compensate. The FY27 ₹2,900 crore target, plotted against the FY24 ₹750 crore base, is plausible at industry-standard margins; it is not bulletproof at trough margins.13

The lesson for founders, transposed onto the case, is more general: the value of operational continuity, in a manufacturing business, is enormous, and the IBC has created a structured channel for transferring that continuity from failing owners to capable ones. For investors, the lesson is harder. Distressed-asset plays look like value investing on the surface, but they are actually operating bets dressed in value clothes. The asset price is rarely the variable that determines the outcome; the operator's competence is.

The specific competence to track here is capacity utilization. That is the single number most worth watching as the next two years unfold.

IX. Analysis: The Bear vs. Bull Case

The bull case for Raj Rayon is, in its fullest articulation, an operating-leverage thesis stacked on top of a balance-sheet repair thesis. The operating leverage thesis is that a polyester yarn plant in the Silvassa cluster, configured to integrated polymerization-to-DTY, hitting 70%-plus utilization at 400 TPD polymerization and progressively scaling toward 600 TPD POY and 400 TPD DTY, will generate operating cash flows that meaningfully exceed the maintenance capex of the existing plant.14 Those cash flows can fund the announced ₹500–600 crore expansion programme primarily through internal accruals plus modest incremental debt, without distressing the balance sheet.14 If management hits the published FY27 ₹2,900 crore topline, even at conservative blended margins of 7–9%, the implied EBITDA is materially higher than the FY25 base — and the equity value compounds with it.4

The balance-sheet repair thesis is more straightforward. Total borrowings of around ₹262 crore against assets of around ₹500 crore as of March 2025 represent moderate leverage for the sector, and the IBC-clean structure means no legacy preference shareholder overhangs threatening dividend or equity dilution beyond the MPS requirement.4 In a sector where competitors are still working through the consequences of pre-2016 leverage, Raj Rayon's debt-light position is a real structural cost advantage at the trough of the cycle. The bull case argues that this advantage compounds over multiple cycles.

Layer onto that the optionality embedded in the listed vehicle: the eventual MPS dilution from 94% to 75% will, once it happens, bring the float into a tradable range, attract index inclusion possibilities, and create a marginal liquidity premium that the current 26,000-shareholder shareholder base does not enjoy.94 The DTY mix shift, the move toward specialty yarns including कैटायोनिक cationic and antimicrobial variants, and the nascent recycled-polyester plans all add discrete optionality on top of the volume base case.34

The bear case, in turn, is less about any single failure point and more about the ways an apparently clean thesis can degrade. Start with the most fundamental: this is a commodity business, and PTA-MEG prices are set by global crude oil dynamics, the Chinese petrochemical cycle, and capacity addition decisions made by integrated giants whose strategic horizon includes Raj Rayon as competitive collateral damage. A sustained period of weak yarn spreads, of the kind the industry experienced in 2014–2016, can compress margins below the level at which capacity additions pay back their capex. The FY27 target depends on margins not collapsing.

Second is the global textile demand picture. The Chinese export apparel chain has been the dominant marginal demand setter for global polyester for two decades. Any sustained slowdown there — driven by tariffs, by the shift of garment manufacturing to Southeast Asia and Bangladesh, or by a structural slowdown in Western consumer apparel demand — flows back into upstream yarn pricing within months. India is, increasingly, a beneficiary of "China plus one" sourcing strategies, but that thesis has been more often invoked than realized, and any retreat in that narrative would hit Raj Rayon's exporter customers and, indirectly, the company itself.

Third is the MPS overhang. Promoter holding at roughly 94% must come down to 75% within a regulatorily defined window, and the mechanics of that dilution — almost certainly some combination of qualified institutional placement and offer-for-sale — will create real supply pressure on the float at whatever price level the market clears at the time of execution.910 In the worst case, the dilution coincides with a margin compression cycle, and the share price has to absorb both the supply of the dilution and the operational softness simultaneously. This is a risk that is not avoidable, only timeable, and the timing decision sits with the promoter group.

Fourth is the related-party-transaction risk inherent in the SVG-Raj Rayon structure. SVG Fashions, the privately held parent, is also the largest customer of Raj Rayon's yarn — buying yarn from the listed entity to feed its own fabric and garment production. This is by no means improper, but it does mean that the pricing of those internal transactions, the credit terms, and the volume allocations are a matter of governance discipline rather than arms-length market dynamics. Investors in the listed vehicle have to take on faith that the Agarwal family will price its own purchases from itself fairly. The 94% promoter holding makes that easier rather than harder — at this level of ownership, value transfer between vehicles is more or less neutral to the family — but the dilution to 75% will progressively shift the calculus.

Fifth, and most under-discussed, is execution risk on the capex programme itself. The published targets imply capacity additions totaling 250 TPD on POY and 250 TPD on DTY, financed by ₹500–600 crore of capex over 24–36 months.1 That is operationally aggressive for an asset of this size. Equipment delivery delays, environmental clearances in दादरा एवं नगर हवेली Dadra and Nagar Haveli, civil works, captive power tie-ups, working capital scaling — any of these can slip. Slippage compresses the period over which the new capacity earns at full margin, and pushes the FY27 target into FY28 or beyond.

The Hamilton Helmer overlay says: this is a business with two and a half powers, sitting in an industry with high rivalry and high buyer power. The Porter overlay says: the segment is structurally less unattractive than the sector average, but it is not structurally attractive in absolute terms. The IBC overlay says: the asset was bought well, the operator is competent, and the balance sheet is genuinely clean. None of these frameworks individually decides the case. Together, they say the same thing: this is a cyclical operating bet with positive structural setup, and the dominant variable is execution against the published capacity and margin targets.

The single most important KPI to track over the next eight quarters, accordingly, is capacity utilization — specifically, what percentage of the installed 400 TPD polymerization, 350 TPD POY, and 150 TPD DTY capacity is being run at any given quarter, and how that ratchets up as the announced expansions come online.14 The second is the segment mix between chips, POY, and DTY, because the gross margin walk depends almost entirely on whether the marginal output is being sold as merchant chips (low margin) or texturized DTY (higher margin).1 A distant third is the company's working capital cycle, because for a manufacturer of this scale, days-of-receivables and days-of-inventory are the variables most likely to mask or amplify any underlying margin movement.

The myth-vs-reality gap on Raj Rayon is sharper than on most listed mid-caps. The popular narrative — and the source of much retail interest — is the "phoenix" framing: zombie company brought back from the dead, multi-bagger turnaround, India's IBC working as designed. The reality is more sober. The company has executed a credible operational restart, the parent has injected genuine capital, the segment positioning is sensible, and the balance sheet is healthier than peers'. But it is still a polyester yarn manufacturer, in a commodity industry, with margins that move with global petrochemical spreads, and an aggressive capacity target that depends on perfect execution. Both the myth and the reality can be true simultaneously; the investing question is which of them is already priced in.

X. Epilogue & Final Reflections

There is a particular kind of company that you only get in countries that have just started enforcing modern bankruptcy law. Pre-2016 India did not have these companies; the legal architecture for cleanly transferring control of a failing manufacturer from defaulting promoters to capable acquirers simply did not exist. The Sick Industrial Companies Act, the BIFR process, the multi-decade litigation that surrounded earlier failed attempts at corporate revival — all of these conspired to keep zombie companies zombified, lenders writing down assets without recovery, and capital frozen in place. The IBC, for all its early teething problems, broke that pattern.

Raj Rayon is a small data point in that larger statute-level transformation, but it is a clean one. A 1993-vintage textile asset that ceased production in 2018 was, through the formal CIRP process, transferred to a capable strategic acquirer in 2021, restarted in 2023, scaled across three consecutive expansions, and is now publicly targeting a roughly 4x revenue scale-up by FY27.123 Whatever eventually happens to the share price — and that is properly the territory of the reader and not the writer — the underlying transfer of an industrial asset from a non-productive state to a productive one is a positive externality of the legal framework that produced it.

The lesson for India's mid-cap investors, if there is one, is that the universe of distressed-resolution-emerged listed companies is now large enough to be a legitimate sub-sector. Bhushan Steel under Tata, Essar Steel under ArcelorMittal-Nippon, Alok Industries under Reliance, Ruchi Soya under Patanjali, Jet Airways under Jalan-Kalrock — each has a different operating profile, but each shares the structural characteristic of having been bought at distressed prices, restarted with strategic-operator capital, and listed publicly with a multi-year MPS clock attached. As a category, these companies are neither growth stories nor value stories in the conventional sense; they are operating-execution stories with embedded balance-sheet optionality. Raj Rayon belongs squarely inside that category, at the smaller end of the size spectrum, in a sector that is structurally underowned by domestic institutional capital relative to its share of GDP.

The lesson for founders is more pointed. The IBC, in practice, has rewarded operators who acquire troubled assets within their own value chain at distressed prices, deploy genuine post-acquisition capital, and operate the assets through the cycle rather than flipping them. SVG Fashions did not have to do anything innovative to capture this opportunity. They had to know polyester yarn, identify a stranded asset in their own backyard, submit a credible resolution plan, and then put real capex behind the restart. The competitive advantage was patience and operating familiarity, not financial wizardry. The same template is replicable in any sub-sector where stranded brownfields exist — chemicals, paper, packaging, intermediate manufacturing — and where domestic operators have the capital and the appetite to acquire through the IBC channel.

The lesson for the company itself, looking forward, is the eternal one of mid-cap commodity manufacturing: the cycle will turn. PTA-MEG spreads will compress at some point in the next three to five years. Global polyester demand will hit a soft patch. The Chinese export apparel chain will continue its slow, lurching reconfiguration. None of these events are knowable in their timing, but all of them are knowable in their nature. The Raj Rayon that survives the next downturn well will be the one whose capacity additions are paid for through the upcycle, whose working capital is disciplined, whose product mix is weighted toward higher-value DTY, and whose related-party transactions remain clean as the promoter holding gradually compresses toward 75%. The Raj Rayon that struggles through the next downturn will be the one that pushed too hard on debt-financed expansion and got caught with new capacity coming online into a margin trough.

The phoenix metaphor is overworked, and it does not really fit. Raj Rayon was not reborn in any mythological sense; it was acquired through a court process and operated by a competent family. What is more interesting than the phoenix framing is the institutional one: the IBC framework, the NCLT bench at Ahmedabad, the resolution professional, the committee of creditors, and the strategic operator with the right industrial logic — all of them did the boring, procedural work that converts a stranded industrial asset back into a producing one. That is not romance. It is plumbing. And, as anyone who has ever lived in a building with bad plumbing can attest, plumbing is what holds modern life together.

The art of the turnaround, in its most honest form, is not about the dramatic restart or the visionary CEO. It is about the day-after-day, ton-by-ton, basis-point-by-basis-point work of running an industrial asset at industry-standard discipline. The Agarwals, in सिलवासा Silvassa, are doing that work. The market will, over the cycle, adjudicate how well.

References

-

SVG Group's Strategic Acquisition: Raj Rayon Aims for INR 2900 Cr. Turnover with Major Investments — The Indian Textile Magazine ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

NCLT approves resolution plan of Raj Rayon Industries Limited — EquityBulls, 2021-10-05 ↩↩↩↩↩↩

-

SVG Fashions: A Vertically Integrated Textile Powerhouse — Textile Value Chain ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Raj Rayon Industries Ltd — Screener.in financial summary ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Polyester Filament Yarn Market Growth & Forecast 2025 — Business Research Insights ↩

-

Silvassa industrial hub overview — Wikipedia / IBEF Reliance Silvassa commissioning ↩↩↩↩

-

Filatex India Limited — Company website (capacity, Dahej plant, expansion announcements) ↩↩↩

-

Board of Raj Rayon Industries allots preference shares to creditors — Business Standard, 2022-12-23 ↩

-

Manner of achieving minimum public shareholding — SEBI Circular SEBI/HO/CFD/PoD2/P/CIR/2023/18, 2023-02-03 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube