Rain Industries: The Alchemists of Carbon

I. Introduction & Opening Context

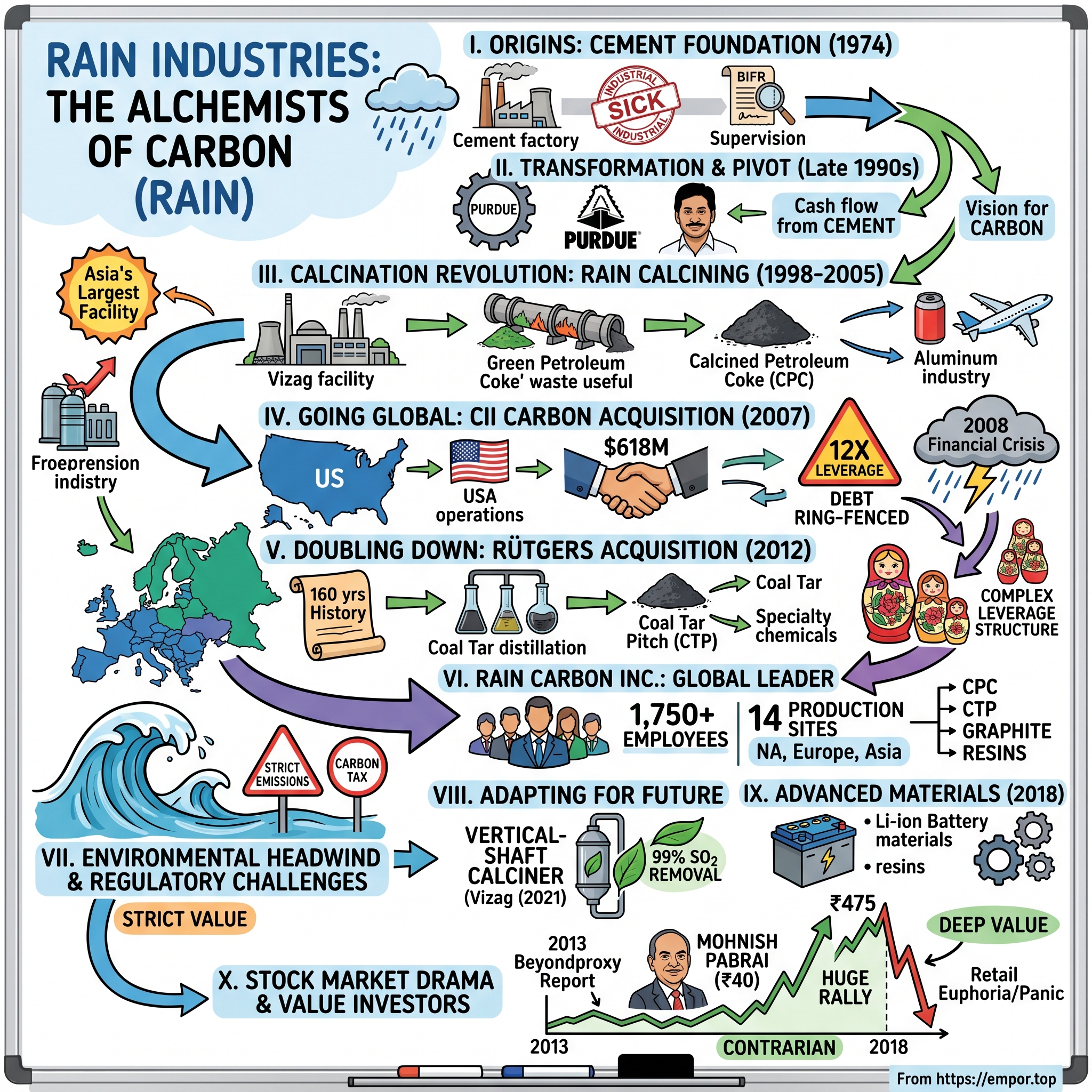

Picture this paradox: A struggling Indian cement company from the dusty plains of Andhra Pradesh transforms itself into one of the world's largest carbon product suppliers, essential to the aluminum industry from Pittsburgh to Shanghai. Rain Industries Limited, erstwhile known as Priyadarshini Cement Limited was established on March 15, 1974 under the name of Tadpatri Cements Limited. Today, standing as one of the world's leading producers of calcinated petroleum coke, coal tar pitch and other high quality basic and specialty chemicals, Rain Industries defies conventional business logic—a phoenix rising not from ashes, but from petroleum coke and coal tar.

The transformation story of Rain Industries reads like industrial alchemy. What began as a regional cement manufacturer during India's infrastructure boom evolved into a global industrial powerhouse through audacious acquisitions, extreme leverage, and an uncanny ability to spot value in the unglamorous corners of the carbon products industry. RCI is the Stamford, Connecticut, USA holding company that integrates the Rain CII and RÜTGERS brands under a unified, global management team. RCI, is a wholly owned subsidiary of India-based Rain Industries Ltd., The company has 14 production sites and 1,750 employees across North America, Asia and Europe with more than 220 combined years of continuously evolving experience in the production of carbon-based materials.

This is a story of transformation through extreme financial engineering—where in 2007, Rain Calcining became the second-largest calciner in the world with the acquisition of the Texas-based CII for a consideration of $618 million; the company's debt-to-equity ratio shot up to 12X for the year ending December 2007, and where a second-generation entrepreneur with a Purdue education saw opportunity where others saw only industrial waste. It's a tale that captivated value investors like Mohnish Pabrai, triggered euphoric stock rallies, and demonstrated how emerging market entrepreneurs can build global empires through sheer audacity.

The journey from a sick industrial company under BIFR supervision to becoming a global leader and innovator in the production of crucial raw materials for the production of primary aluminum (including calcined petroleum coke (CPC) and coal tar pitch (CTP)), graphite, carbon black, refractory, titanium dioxide, lithium-ion batteries and a host of other products. RCI has a production capacity of 2.4 million tons per year of calcined petroleum coke and a total distillation capacity of 1.5 million tons per year.

II. Origins & The Cement Foundation

The sweltering heat of Tadpatri in 1974 seemed an unlikely birthplace for a global industrial empire. In post-independence India, where the government's five-year plans drove massive infrastructure development, cement was liquid gold. Into this environment, The Company was Incorporated on 15th March, under the name Tadpatri Cements, Ltd. and the Certificate of Commencement of Business was obtained on 10th April. The Company was promoted by D.G.K. Murthy, a technocrat, S. Veera Reddy, N. Radhakrishna Reddy, P. Pratap Reddy and others who saw opportunity in India's building boom.

But the path was far from smooth. The cement industry's brutal economics—capital intensive, cyclical, and plagued by overcapacity—soon caught up with the fledgling company. By 1990, the weight of debt and operational challenges pushed the company into dire straits. The Company came under the provision of the Sick Industrial Companies (Sp. Provisions) during the year 1990 and in April of the year 1992, Board for Industrial and Finance Reconstruction (BIFR) had accepted the sick industrial companies (Sp.Provisions) scheme, also passed an order.

The BIFR period represented the company's darkest hour—a time when creditors circled, operations stuttered, and survival seemed uncertain. Yet this crucible would forge the resilience and opportunistic mindset that would later define Rain's trajectory. The company limped through the 1990s, restructuring debt, optimizing operations, and searching for a path forward.

N. Radhakrishna Reddy, one of the original promoters, watched his cement company struggle against larger, better-capitalized competitors. But his son had different ideas. Jagan Mohan Reddy, fresh from his industrial engineering degree at Purdue University, saw beyond the cement silos and limestone quarries. Mr. Jagan Mohan Reddy Nellore brings to the Company 31 years of experience in the finance, commercial and operations areas. Mr. Nellore is currently the Managing Director of Rain Industries Limited and CEO of Rain Carbon, Inc., USA. Mr. Nellore was the founder of Rain CII Carbon (Vizag) Limited, which had originally been incorporated as Rain Calcining Limited and which had commenced production of calcined petroleum coke (CPC) and electricity in 1998 in India. Mr. Nellore holds a bachelor of science degree in industrial engineering from Purdue University, USA.

The transformation wouldn't happen overnight. Through the 1990s, the company slowly stabilized, changed names multiple times—from Tadpatri Cements to Priyadarshini Cement Limited in 1984, and eventually to Rain Commodities Limited in 2004—each rebrand marking a step in its evolution. RCL commissioned its first ready mix concrete plant in December of the year 1999 at Hyderabad. The second ready mix concrete plant of the company had set up at Miyapur, also in Hyderabad. It had set up two manufacturing plants with a rated capacity of 7200 cubic meters per month.

The cement business provided the cash flow, but it was clear that remaining a regional cement player in an increasingly consolidated industry was a recipe for mediocrity. The stage was set for a radical pivot that would transform this struggling cement company into something entirely different.

III. The Calcination Revolution: Birth of Rain Calcining

The port city of Visakhapatnam in 1998 hummed with industrial activity. Ships loaded with raw petroleum coke—a black, carbon-rich byproduct of oil refining that most saw as waste—arrived at the docks. But where others saw industrial refuse, Jagan Mohan Reddy saw gold. Meanwhile, in 1998, Rain Calcining Limited (RCL), an independent start-up based in India, constructed Asia's largest calcination facility in the port city of Visakhapatnam (Vizag), India.

Understanding calcination requires appreciating industrial alchemy. Green petroleum coke, the raw material, is essentially the bottom of the barrel in oil refining—a carbon-rich residue that needs transformation to become useful. Through calcination—heating to temperatures exceeding 1,200°C in massive rotary kilns—this waste product transforms into calcined petroleum coke (CPC), an essential ingredient for aluminum production. Without CPC, there would be no aluminum cans, no aircraft fuselages, no smartphone casings.

The aluminum industry's dirty secret was its absolute dependence on this transformed waste product. Aluminum smelters use carbon anodes made primarily from CPC in the electrolytic process that transforms bauxite into aluminum. For every ton of aluminum produced, approximately 0.4 tons of CPC is consumed. And here lay the opportunity: while thousands of companies produced aluminum, only a handful mastered the art of calcination at scale.

The oligopolistic nature of the calcination market created extraordinary economics. High capital requirements—a single calcination plant could cost hundreds of millions—deterred new entrants. Environmental regulations added another barrier. The need for proximity to both petroleum coke suppliers and aluminum smelters created logistical moats. And the technical expertise required to consistently produce specification-grade CPC while managing environmental compliance wasn't easily replicated.

Starting out with a 0.3 million-tonne capacity in the port city of Visakhapatnam, the group's calcining arm has travelled places over the years. The Vizag facility wasn't just ambitious in scale—it represented a bet that an Indian company could compete globally in a market dominated by American and European giants. The location was strategic: close to ports for importing raw materials and exporting finished products, with access to India's growing aluminum industry.

By 2005, success bred expansion. In 2005, RCL doubled its capacity through the expansion of the Vizag facility. The company had proven it could operate efficiently, meet international quality standards, and compete on cost. But Jagan Mohan Reddy's ambitions extended far beyond being Asia's largest calciner. The global market beckoned, and with it, the opportunity to roll up a fragmented industry through aggressive acquisition.

IV. The CII Carbon Acquisition: Going Global

The boardroom in Hyderabad crackled with tension in early 2007. Jagan Mohan Reddy was proposing something that seemed insane: acquiring CII Carbon LLC, an American company with revenues multiple times larger than Rain's entire market value. The price tag: $618 million. Rain's market cap: less than $200 million.

RCI's calcination roots date back to 1959, when Kaiser Aluminum and Chemical Corporation (KACC) constructed a calciner in the state of Mississippi, USA, to convert petroleum coke -- a solid carbon by-product of the oil refining industry -- into an essential raw material for the production of aluminum anodes. KACC built three more U.S. Gulf Coast calciners, and in 1988, these operations became the independently owned CII Carbon LLC (CII). CII subsequently grew through the acquisition of three additional U.S. calcining plants, including two from a Conoco joint-venture company.

CII Carbon wasn't just any acquisition target—it was American industrial royalty with a pedigree stretching back to Kaiser Aluminum. With calcination plants in Illinois, Louisiana, Mississippi, and West Virginia, CII controlled nearly 20% of American CPC production. The Company had acquired CII Carbon of USA In July of the same year 2007, manufacturing 1.9Million TPA of CPC with manufacturing facilities in Illinois, Louisiana, Missisipi and West Virginia.

The financing structure was audacious beyond belief. Rain would borrow more than three times its entire enterprise value, pushing debt-to-equity ratios into territory that made bankers nervous and competitors incredulous. In 2007, Rain Calcining became the second-largest calciner in the world with the acquisition of the Texas-based CII for a consideration of $618 million; the company's debt-to-equity ratio shot up to 12X for the year ending December 2007.

But Jagan had structured the deal with the cunning of a chess grandmaster. The debt was non-recourse—secured only against CII's assets, not Rain's Indian operations. If the acquisition failed, the Indian parent would survive. It was heads-I-win, tails-I-don't-lose-everything financial engineering at its finest. The acquisition closed in mid-2007, and overnight, Rain CII Carbon (Vizag) Limited (RCCVL) in India and Rain CII Carbon LLC (RCC) in the United States emerged as the world's second-largest CPC producer.

The integration challenged everything about Rain's DNA. A company that had never operated outside India suddenly managed plants across America's industrial heartland. Cultural differences, regulatory complexities, and operational challenges tested the organization. Yet Jagan's hands-on approach—he personally spent months at U.S. facilities, understanding operations, building relationships, optimizing processes—turned potential disaster into triumph.

The timing seemed perfect. Aluminum demand was soaring, driven by China's infrastructure boom and global economic growth. CPC prices were firm, margins healthy. The newly christened Rain CII became the preferred supplier to aluminum giants like Alcoa, Rio Tinto, and Century Aluminum. The debt, while massive, seemed manageable given the cash flows.

Then 2008 happened.

The financial crisis struck like a tsunami. Aluminum demand collapsed. CPC prices plummeted. Suddenly, Rain CII's debt mountain looked less like aggressive expansion and more like a death warrant. Credit markets froze. Refinancing seemed impossible. Competitors whispered about bankruptcy, waiting to pick up assets at distressed prices.

But Rain survived through a combination of operational excellence, cost cutting, and sheer determination. While competitors mothballed capacity, Rain kept plants running, maintaining customer relationships even at lower margins. By 2010, as markets recovered, Rain CII emerged stronger, battle-tested, and ready for its next transformation.

V. The RÜTGERS Acquisition: Doubling Down on Carbon

If the CII acquisition was audacious, what came next bordered on lunacy. In October 2012, with debt from the CII deal still weighing heavily, Jagan Mohan Reddy announced Rain's next target: RÜTGERS N.V., a Belgian company with 160 years of history and operations spanning Europe.

Rain CII acquired 100% of the shares of RUETGERS pursuant to an agreement with Triton for a gross enterprise value of €702.0 million plus certain contingent payments not exceeding €27.0 million during the next three years. Once again, Rain was attempting to acquire a company larger than itself, using predominantly debt financing, in the midst of a global economic slowdown.

RCI's distillation roots date back to the German industrial pioneer, Julius Rütgers, who founded a company that was later to become the RÜTGERS Group. In 1849, the 18-year-old entrepreneur took over his father's troubled wood impregnation business for the production of railway sleeper ties. The young entrepreneur soon discovered that coal tar had the potential to be more than an impregnation agent. Rütgers set up his first distillation plant near Berlin to extract the many valuable compounds and transform them into a range of useful products. Distillation allowed RÜTGERS to greatly diversify its product line and risk profile, propelling the company's business in new directions and launching aromatic chemistry in Germany.

RÜTGERS brought something different to the table: coal tar distillation expertise. While Rain CII transformed petroleum coke from oil refineries, RÜTGERS processed coal tar from steel mills. Europe and the second largest coal tar distiller in the world. It has three coal tar distillation sites, along with six downstream (refining) facilities. The strategic logic was compelling—vertical integration into coal tar pitch (CTP), another essential ingredient for aluminum production, while diversifying into specialty chemicals with higher margins and more stable demand.

The financing structure demonstrated Jagan's evolution as a dealmaker. This time, the debt was secured against CII's assets, not Rain's Indian operations. If RÜTGERS failed, it would take down CII, but the Indian parent would survive. It was financial engineering layered upon financial engineering—a Russian doll of corporate structures designed to capture upside while limiting downside.

The acquisition for a gross enterprise-value of €702 mln (₨59.6 bln) was the company's second overseas leveraged buyout (LBO), and with it Rain became the largest 'carbon' supplier to the aluminum industry globally. The acquisition was completed on Jan-04-2013 and yet for nine months ending Sep-30-2013 Rain has earned ₨10.03/sh versus ₨13.22/sh for the same period in 2012. At the time of the announcement, Rain had a market capitalization of ₨14.9 bln (US$280 mln) and based on 2012 earnings, was trading at a P/E of 3.2x. Currently Rain trades 2.7x 2013E earnings with a market capitalization of ₨12.0 bln (US$195 mln).

The integration of RÜTGERS proved even more complex than CII. European labor laws, environmental regulations, and cultural differences created friction. The aluminum industry downturn post-2013 added pressure. However, the volume of calcined pet coke (CPC) fell 5% yoy in 2013 and realisations dipped 13% on continued weakness in aluminium markets. However, the price of the key raw material – green pet coke (GPC) has fallen moderately (less than 5%), resulting in a decline in EBITDA per tonne.

Yet gradually, the strategic vision crystallized. Rain Carbon Inc. emerged as the unified holding company, integrating CII's calcination expertise with RÜTGERS' distillation capabilities. The company could now offer aluminum producers a complete carbon solution—both CPC and CTP from a single supplier. Operational synergies emerged: coordinated purchasing, optimized logistics, shared technical expertise.

By 2015, the transformation was complete. What had been three separate companies—Rain Calcining, CII Carbon, and RÜTGERS—now operated as one integrated entity. Rain had become the only global player with leadership positions in both calcination and distillation, serving customers across aluminum, steel, titanium dioxide, and specialty chemical industries.

VI. Environmental Headwinds & Regulatory Challenges

The irony wasn't lost on anyone: Rain Industries, built on transforming carbon-rich waste products, faced its greatest existential threat from the global push toward decarbonization. By 2015, environmental regulations were tightening worldwide. China, historically Rain's largest market, began implementing stringent pollution controls. European carbon taxes loomed. Even India started enforcing stricter emissions standards.

The aluminum industry, Rain's primary customer, faced its own environmental reckoning. Aluminum production is energy-intensive and carbon-heavy. As sustainability became a boardroom priority, aluminum producers faced pressure to reduce their carbon footprint. Some questioned the long-term viability of carbon anodes altogether, exploring inert anode technologies that could eliminate the need for CPC entirely.

Rain's response demonstrated the adaptability that had carried it through previous crises. In 2018, the company created a new Advanced Materials reporting segment. In 2013, RCI acquired RÜTGERS, and five years later the company created a new Advanced Materials reporting segment to reflect RCI's increasing focus on transforming by-products of its coal tar and petrochemical feedstock distillation activities to produce raw materials that support high-growth products of the future. This wasn't just rebranding—it represented a fundamental shift in strategy.

The Advanced Materials segment focused on products for emerging technologies: specialty carbon materials for lithium-ion batteries, resins for electric vehicle components, and high-performance materials for renewable energy applications. The company that had built its fortune on the old economy was positioning itself for the new.

The pivot accelerated with concrete investments in environmental technology. In 2021, Rain achieved what many thought impossible: In 2021, RCI began commercial operation of its newest calcination facility in the Andhra Pradesh Special Economic Zone in India, increasing the company's annual CPC production to approximately 2.4 metric tons. The company's first vertical-shaft calciner is also equipped with a state-of-the-art flue-gas desulfurization system that removes more than 99% of the plant's sulfur dioxide emissions, making it the most environmentally friendly calcination plant in the world.

This wasn't greenwashing—it was a USD 75 million bet that environmental leadership could become a competitive advantage. The vertical-shaft design improved energy efficiency by 15% compared to traditional rotary kilns. The flue-gas desulfurization system didn't just meet environmental standards; it exceeded them by orders of magnitude.

The facility became Rain's showcase, demonstrating to regulators, customers, and investors that carbon processing and environmental responsibility weren't mutually exclusive. Delegations from China, Europe, and the Middle East visited to understand how Rain had squared this circle. Some competitors dismissed it as expensive virtue signaling. Time would tell who was right.

Meanwhile, other challenges emerged. In 2018, India's Supreme Court temporarily banned petroleum coke imports, threatening Rain's Vizag operations. The company navigated the crisis through legal challenges, operational adjustments, and government relations. The ban was eventually modified, but it highlighted the regulatory risks inherent in the business.

China's evolving policies created both threats and opportunities. Environmental crackdowns shuttered competing calcination capacity, tightening global supply. But Chinese aluminum production curbs reduced demand. Rain walked a tightrope, adjusting production and managing inventory to navigate the volatility.

VII. The Value Investor Discovery & Stock Market Drama

The 2013 Beyondproxy report landed on investment desks with little fanfare. This was the prevailing mantra in the Indian Investment community until in 2013, a report from an American research company (Beyondproxy) claimed that it had chanced upon a value stock and an opportunity that came once in a lifetime all bundled inside a little-known company from Hyderabad called Rain Industries. In an era of momentum investing and growth stocks, who cared about an overleveraged Indian company in the unglamorous business of processing petroleum coke?

The depressed valuation of this leveraged, underfollowed, niche market, stable margin, and oligopolistic natured business provides an opportunity for a serial capital compounder. Investment Thesis The investment idea presented in this report is a little known industrial business based out of India with global operations called Rain Industries Limited ("Rain"). What started as an Indian cement producer in the early-70's, is now a global conglomerate with over US$2 bln in annual revenues. Rain can be split into three primary businesses: petroleum coke calcining (36% of revenues), RÜTGERS' primary coal tar distillation and chemicals production (58%), and the cement business (7%).

The report's analysis was meticulous, highlighting factors that traditional investors overlooked: the oligopolistic market structure, the essential nature of Rain's products, the impossibility of substitution, and most importantly, the massive disconnect between the company's debt-adjusted enterprise value and its earnings power. Rain was trading at less than 3x earnings, with a price-to-book ratio of 0.5x.

For two years, the report circulated among value investing circles with little impact. Rain's stock price languished around ₹40, ignored by institutional investors and retail alike. The debt scared everyone. The complexity of the business model confused analysts. The lack of comparable companies made valuation difficult.

Then, in 2015, the report reached Mohnish Pabrai's desk. About 2½ years ago a benevolent human (whom I have yet to meet or speak to) sent me an elegant write-up on a Hyderabad, India-based company I had never heard of called Rain Industries. When Pabrai Funds first invested in Rain in mid2015, the market cap was $175 million. This was a business that had revenues of $1.9 billion in 2013 and 2014.

Pabrai's interest transformed Rain from an obscure industrial company into a value investing cause célèbre. Pabrai has so far picked up 10 million shares of the company at about ₹40. As is well known, Pabrai only invests in stocks that he thinks have deep value and the potential to give multi-fold return. His investment thesis evolved beyond simple cheapness to focus on management quality and capital allocation.

In the last 3+ years that we have owned Rain, I have seen Jagan Reddy (Rain's Managing Director and 40+% shareholder) make one smart decision after another. In fact, I have never seen Jagan make even one dumb decision. He has made very large capital allocation calls over the last 12+ years and they have been flawless. It is a remarkable record. He is a dream manager.

For nearly two years after Pabrai's investment, nothing happened. The stock bounced between ₹40 and ₹80, frustrating believers and emboldening skeptics. The debt deleveraging proceeded slowly. Aluminum markets remained weak. The market's verdict seemed clear: Rain was a value trap, not a value investment.

Then, in late 2017, everything changed. China's environmental crackdowns shuttered illegal aluminum capacity and restricted calcination operations. Global aluminum prices spiked. CPC prices followed. Suddenly, Rain's earnings exploded. The stock price responded with violence—surging from ₹120 in August 2017 to an all-time high of ₹475 in January 2018. RAIN reached its all-time high on Jan 9, 2018 with the price of 475.00 INR, and its all-time low was 25.50 INR and was reached on Feb 12, 2016.

The euphoria was intoxicating. Investors who had bought at ₹40 sat on 12x returns. Message boards erupted with celebration. Pabrai's investment thesis seemed vindicated. Rain Industries became the poster child for deep value investing in India.

But markets, as always, overdid it. The stock's parabolic rise attracted momentum traders with no understanding of the underlying business. Retail investors piled in at ₹400+, expecting the rally to continue indefinitely. The smart money began quietly exiting.

The reversal was as swift as the rise. Environmental concerns in India, fears about electric vehicles reducing aluminum demand, and general market weakness triggered selling. By June 2018, the stock had crashed to ₹220—a 53% decline from its peak. The momentum traders fled. Message boards turned from euphoria to acrimony. MMB has turned into a virtual battlefield amongst Rain Industries' supporters and detractors. The detractors have been emboldened by the savage crash in the stock price to take potshots at the supporters.

Pabrai, characteristically, used the crash to buy more. His conviction remained unshaken. But for many retail investors who had bought at the peak, Rain Industries became a cautionary tale about the dangers of following guru investors blindly. The stock entered a long, grinding bear market, eventually bottoming around ₹120 in 2020—almost exactly where the rally had begun three years earlier.

VIII. Modern Operations & Business Segments

Today's Rain Industries operates as three distinct yet interconnected businesses, each serving different end markets while sharing common infrastructure and expertise. The company operates through three segments: Carbon, Advanced Materials and Cement.

The Carbon segment remains the crown jewel, contributing approximately 74% of consolidated revenue. RCI is a global leader and innovator in the production of crucial raw materials for the production of primary aluminum (including calcined petroleum coke (CPC) and coal tar pitch (CTP)), graphite, carbon black, refractory, titanium dioxide, lithium-ion batteries and a host of other products. RCI has a production capacity of 2.4 million tons per year of calcined petroleum coke and a total distillation capacity of 1.5 million tons per year. The segment operates 13 production facilities across the United States, India, and China, with deep-water shipping terminals providing global reach.

The operational complexity is staggering. Each calcination plant must manage multiple variables: raw material quality that varies by source and season, customer specifications that differ by application, environmental regulations that change by jurisdiction, and energy costs that fluctuate daily. Rain's competitive advantage lies in its ability to optimize across this complexity, using proprietary blending techniques to produce consistent quality from variable inputs.

The Advanced Materials segment, contributing 19% of revenue, represents Rain's future. The Advanced Materials segment includes the downstream operations of coal tar distillation and consists of engineered products, petrochemical intermediaries, naphthalene derivatives and resins. Products include PETRORES for lithium-ion battery anodes, LIONCOAT thermal barrier coatings, and specialized resins for emerging applications. The segment's margins exceed those of traditional carbon products, and demand growth outpaces the overall market.

The transformation of this segment accelerated with the 2019 commissioning of a hydrogenated hydrocarbon resins facility in Germany. In 2019, the company began commercial operation of an advanced hydrogenated hydrocarbon resins production facility at its Castrop-Rauxel site in Germany. These water-white resins serve hygiene and adhesive applications where purity is paramount—a far cry from the black carbon products that built the company.

The Cement segment, contributing 7% of revenue, might seem like an anachronism—a vestige of the company's origins. Yet it provides stable cash flow and serves as a natural hedge against the cyclicality of carbon markets. Rain Industries operates two integrated cement plants in South India—one in Telangana and the other in Andhra Pradesh. These plants have an aggregate installed capacity of four million tonnes per annum, producing two grades of cement: Ordinary Portland Cement (OPC) and Portland Pozzolana Cement (PPC).

The geographic diversification mirrors the operational variety. Europe generates 36% of revenues, North America 35%, Asia 19%, with the balance from other regions. This global footprint provides natural hedging against regional economic cycles and regulatory changes. When Chinese environmental crackdowns constrain supply, U.S. operations benefit from higher prices. When European demand weakens, Asian growth compensates.

Energy recovery has become a critical differentiator. Rain operates waste-heat recovery systems that capture energy from the calcination process, generating electricity for internal use or sale to the grid. These systems reduce operating costs while improving environmental credentials—a win-win that exemplifies Rain's operational philosophy.

The logistics network rivals that of major shipping companies. Rain moves millions of tons of materials annually via ship, rail, truck, and pipeline. The company operates its own terminals, maintains dedicated rail cars, and has long-term shipping contracts. This infrastructure, built over decades, would be nearly impossible for new entrants to replicate.

IX. Playbook: Lessons from Rain's Journey

The Oligopoly Play: Rain's success stems from identifying and dominating niche markets with oligopolistic characteristics. Calcination and coal tar distillation aren't sexy businesses, but they're essential, hard to replicate, and dominated by a handful of global players. The lesson: sometimes the best opportunities lie in the ignored corners of the industrial economy.

Debt as a Tool: Rain's hyper-aggressive use of leverage—reaching 12x debt-to-equity at one point—would terrify most investors. Yet Jagan Mohan Reddy structured each acquisition to limit downside through non-recourse debt and ring-fenced subsidiaries. The lesson: debt is a tool that, wielded skillfully, can create extraordinary returns. Wielded poorly, it destroys companies.

Vertical Integration: By combining calcination (CII) with distillation (RÜTGERS), Rain created unique competitive advantages. Customers could source complete carbon solutions from one supplier. Operations could be optimized across the value chain. The lesson: vertical integration works when it creates genuine synergies, not just corporate complexity.

Timing the Cycle: Rain's major acquisitions—CII in 2007, RÜTGERS in 2013—occurred during industry downturns when valuations were depressed. The company then rode the subsequent upturns, generating returns that justified the risk. The lesson: in cyclical industries, timing is everything. Buy when others are selling; sell when others are buying.

Geographic Arbitrage: Rain leveraged Indian cost structures to compete globally. Engineers paid Indian salaries optimized American plants. Indian capital costs funded European acquisitions. The lesson: emerging market companies can build global empires by arbitraging cost differences while meeting international quality standards.

Environmental Adaptation: Rather than fighting environmental regulations, Rain embraced them, building the world's cleanest calcination plant and pivoting toward green technologies. The lesson: regulatory changes create opportunities for companies willing to adapt and invest.

The Conglomerate Discount: Markets consistently undervalued Rain due to its complexity—multiple business segments, global operations, opaque industry dynamics. This created opportunity for investors willing to do the work to understand the business. The lesson: complexity creates opportunity for those willing to embrace it.

X. Bear vs. Bull Case Analysis

Bear Case: The bears see structural headwinds everywhere. Aluminum demand faces long-term pressure as electric vehicles use less aluminum than traditional cars (no engine blocks). Carbon-free aluminum production technologies, while still experimental, threaten to eliminate the need for carbon anodes entirely. Environmental regulations continue tightening globally, potentially making carbon processing uneconomical in developed markets.

The debt burden, while reduced from peak levels, remains substantial. Rising interest rates increase financing costs. Any significant downturn in aluminum markets could stress cash flows, potentially triggering covenant breaches. The company's history of aggressive leverage suggests management might take excessive risks again.

China's dominance in both aluminum production and carbon processing creates constant uncertainty. Policy changes in Beijing reverberate globally, creating volatility Rain cannot control. Chinese competitors, often state-supported, could undercut pricing to gain market share.

The Advanced Materials pivot, while promising, remains unproven at scale. Competition from established chemical companies with deeper pockets and stronger customer relationships could limit growth. The segment's contribution to overall profitability remains modest despite years of investment.

Bull Case: The bulls see Rain as essential infrastructure for the modern economy. Aluminum demand might shift from automobiles to other applications—renewable energy infrastructure, electric grid expansion, consumer electronics—but absolute demand continues growing. Carbon anodes remain the only commercially viable technology for aluminum production, with alternatives decades away from large-scale adoption.

The company's environmental investments position it to benefit from, rather than suffer from, tightening regulations. As dirty capacity shutters, Rain's clean operations gain market share and pricing power. The vertical-shaft calciner demonstrates technological leadership that competitors will struggle to match.

500339's debt to equity ratio has reduced from 147.8% to 108.8% over the past 5 years. The deleveraging story remains intact, with debt ratios improving yearly. Management learned from past excesses, now maintaining conservative financial policies. The company generates substantial free cash flow even in downcycles, providing cushion against market volatility.

The Advanced Materials segment's growth accelerates as electric vehicle adoption drives demand for specialized carbon materials in batteries. Rain's unique position—straddling traditional carbon markets and emerging technologies—cannot be easily replicated. Early investments in these markets will pay off as volumes scale.

Valuation remains compelling despite the stock's volatility. Trading at single-digit P/E ratios with a price-to-book below 1x, the market prices Rain as if it's going out of business. Any positive catalyst—aluminum price recovery, successful Advanced Materials launch, further deleveraging—could trigger significant rerating.

XI. If We Were CEOs: Strategic Options

Standing in Jagan Mohan Reddy's shoes today, several strategic pathways beckon, each with its own risks and rewards.

The first option: double down on Advanced Materials through targeted acquisitions. The segment shows promise but lacks scale. Acquiring complementary technologies—silicon carbon for next-generation batteries, specialized resins for 5G applications, or graphene production capabilities—could accelerate growth. The balance sheet has deleveraged enough to support modest acquisitions without returning to dangerous leverage levels.

Strategic partnerships with battery manufacturers represent another avenue. Rather than competing with established chemical giants, Rain could position itself as the carbon specialist within broader consortiums. Joint ventures with Chinese battery manufacturers, European automotive companies, or American energy storage firms could provide market access and technical expertise while sharing risk.

The cement business presents a strategic dilemma. It generates steady cash flow but offers limited growth and dilutes the carbon-focused equity story. A spin-off could unlock value—the cement business might trade at higher multiples as a standalone regional player, while RemainCo would become a pure-play carbon company. Alternatively, selling the cement business could fund Advanced Materials investments without additional debt.

Geographic expansion into Africa and the Middle East deserves consideration. These regions are building aluminum smelting capacity to monetize energy resources and create industrial bases. Rain's expertise in building and operating calcination plants in challenging environments positions it well to capture this growth. Local partnerships could mitigate political risk while providing market access.

Technology investments could create new competitive advantages. Artificial intelligence for optimizing calcination parameters, blockchain for supply chain transparency, or carbon capture technologies for net-zero operations represent areas where early investment could yield long-term benefits. The company's engineering expertise and operational data provide a foundation for such initiatives.

The most radical option: pivot entirely toward the circular economy. Position Rain not as a carbon processor but as a waste-to-value company. Expand beyond petroleum coke and coal tar to process other industrial waste streams—plastic pyrolysis residues, biomass chars, electronic waste. This would require significant investment and risk but could transform Rain from a cyclical commodity processor into a sustainable materials company commanding ESG premiums.

XII. Epilogue & Reflections

The rain had finally stopped in Hyderabad as 2025 drew to a close. From his office overlooking the city where it all began, perhaps Jagan Mohan Reddy reflected on the extraordinary journey—from a sick cement company under BIFR supervision to a global industrial conglomerate essential to the world economy.

The transformation defied conventional wisdom at every turn. An Indian company acquiring American industrial assets. A regional player becoming a global leader through extreme leverage. A carbon processor becoming an environmental leader. Each paradox resolved through a combination of vision, execution, and sheer audacity.

The stock market's verdict remained mixed. From the January 2018 peak of ₹475, the stock had given back most of its gains, trading around ₹130 as investors grappled with the company's complexity and cyclical exposure. Yet the business itself had never been stronger—debt reduced, operations optimized, new growth avenues emerging.

The lessons from Rain's journey extend beyond industrial strategy or financial engineering. They speak to the possibility of transformation—how companies from emerging markets can reshape global industries through ambition and execution. They demonstrate that value creation often occurs in the unloved, misunderstood corners of the economy where few dare to venture.

The future remains unwritten. Will Advanced Materials fulfill its promise, transforming Rain into a specialty chemical company? Will environmental regulations destroy or enhance the carbon processing business? Will the next generation of leadership maintain the entrepreneurial edge while avoiding the excessive risk-taking that nearly destroyed the company?

Perhaps the most profound insight from Rain's story is that industrial alchemy—transforming waste into value—mirrors corporate alchemy—transforming struggling companies into global leaders. Both require the right conditions, the right catalyst, and perhaps a touch of magic.

As night fell over Hyderabad, the lights from Rain's offices reflected off the wet streets, creating patterns that seemed to dance and shift—much like the company itself, constantly transforming, always adapting, forever seeking the next metamorphosis. The alchemists of carbon had proven that with enough vision, courage, and perhaps a little rain, even the humblest beginnings could yield golden outcomes.

The story of Rain Industries stands as testament to the power of contrarian thinking, the importance of timing, and the reality that sometimes the greatest opportunities lie not in Silicon Valley's gleaming startups or Wall Street's financial engineering, but in the grimy, essential work of processing the world's industrial byproducts. It's a reminder that value—real, enduring value—often hides in plain sight, waiting for those brave enough to see it and bold enough to capture it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube