Radico Khaitan: The Alchemist of Indian Spirits

I. Introduction & Episode Roadmap

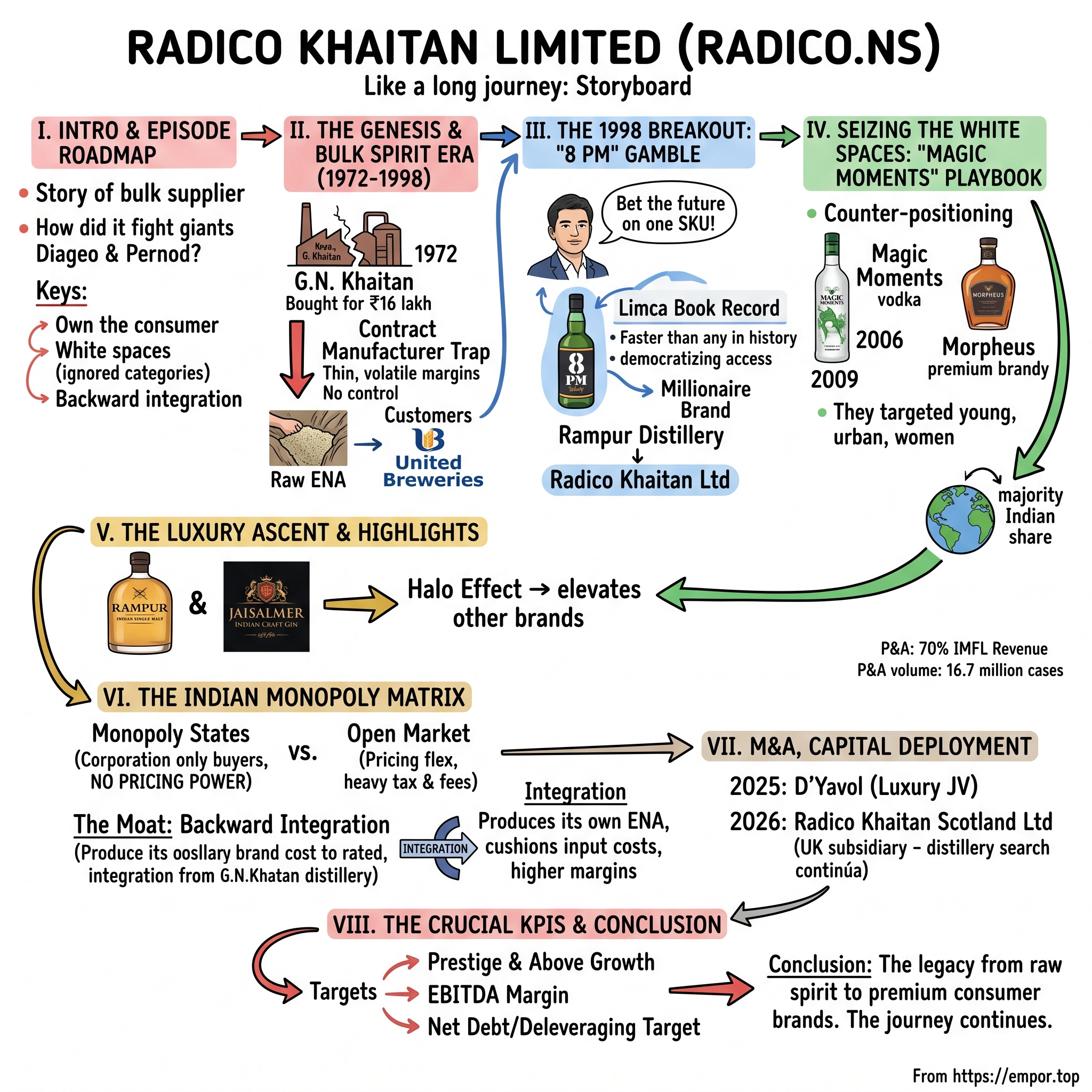

In 1972, in the princely town of Rampur in Uttar Pradesh, a Marwari industrialist named G.N. Khaitan signed papers to take over a tired, money-losing distillery that most people in the liquor trade would not have touched. The plant did not make brands. It made raw spirit — industrial alcohol and Extra Neutral Alcohol — that other, more famous companies bought, bottled, and sold under their own labels. It was, in the language of modern business, a contract manufacturer: the invisible factory behind someone else's logo. The price for this defunct asset was roughly ₹16 lakh, a sum that today would barely buy a mid-range apartment in a tier-two Indian city.1

Fast-forward to 2026. That same distillery sits at the center of a company called Radico Khaitan Limited, which crossed ₹6,050 crore in net revenue and posted more than ₹1,000 crore in EBITDA for the fiscal year ending March 2026.2 Its vodka is the sixth-largest by volume on Earth. Its single malt sells in duty-free shops in London and Singapore. Its founders are billionaires. And in January 2026, the company that began life bottling spirit for other people announced it was setting up a subsidiary in Scotland to one day own a Scotch distillery of its own.3

So here is the question this story turns on. How did a back-end, low-margin commodity producer — a business with no brands, no marketing muscle, and no consumer relationships — claw its way into the front of the bottle and end up competing, profitably, against the two largest spirits companies on the planet, Diageo and Pernod Ricard, on their most important growth market?

The thesis of this episode is that Radico Khaitan is the textbook case of the "commodity-to-brand" transition in a brutally regulated industry. It is a story about three things stacked on top of each other: first, an obsessive bet on owning the consumer rather than renting capacity to whoever owns the consumer; second, a disciplined, repeated playbook of finding "white spaces" — categories the giants ignored — and planting a flag there before anyone noticed; and third, deep backward integration into raw material that turned India's vicious input-cost cycles from an existential threat into a competitive weapon. None of this is a foregone conclusion, and a neutral investor should be skeptical of the tidy narrative. We will test each claim against the numbers, the earnings calls, and the parts of the story management would rather you skip.

Here is the road we will travel. We start with the genesis — twenty-five years as an anonymous bulk supplier, and why that quarter-century of being squeezed shaped everything that came after. Then the 1998 inflection, the all-or-nothing launch of 8 PM Whisky. Then the counter-positioning era of Magic Moments vodka and Morpheus brandy, where Radico learned to win categories the incumbents thought beneath them. Then the luxury ascent into single malt and craft gin. We will dissect the actual economics of selling liquor in India — a country that is not one market but twenty-eight, many of them state-run monopolies where the distiller has, quite literally, no pricing power. We will benchmark the M&A and the audacious Scotland venture. We will run a skeptical stress test on the balance sheet, the related-party transactions, and the promoter pay. And we will close with the frameworks, the bull and bear cases, and the handful of numbers that actually matter from here.

Let us begin where it began: with a broken factory and a family that decided being a supplier was a trap.

II. Part I: The Genesis & The Bulk Spirit Era

Picture the production floor of a distillery in 1943. The British Raj is at war. In the princely state of Rampur, a sleepy region of northern Uttar Pradesh better known for its nawabs and its knife-makers than for industry, a plant called the Rampur Distillery & Chemical Company comes online. Its job is unglamorous and essential: ferment molasses, distill it into alcohol, and supply that alcohol in bulk — for the military, for industrial use, and as the base spirit for other companies' liquor.4

For its first three decades, that is exactly what it does. It is a cog. The brands of the era — names like Shaw Wallace, Mohan Meakin (the maker of Old Monk rum), and the United Breweries group — buy spirit and bottling services from plants like Rampur and sell the finished product under labels the public actually recognizes.4 The distillery makes the wine, so to speak, and someone else gets the toast.

By 1972 the unit is distressed and loss-making, and it changes hands. G.N. Khaitan acquires it for a figure remembered in company lore as about ₹16 lakh.1 The Khaitans are a traditional industrial family, comfortable in the world of factories and commodities. And for the next twenty-five years, they run Rampur the way it has always been run — as a contract bottler and a supplier of Extra Neutral Alcohol, the clean, near-flavorless 96% spirit that is the raw material of practically every whisky, vodka, gin, and rum sold in India.

Here is the strategic trap, and it is worth sitting with because it explains the entire later story. A contract manufacturer's economics are governed by its customers, not by itself. If the company you bottle for decides to move that volume to a rival plant closer to its markets, you lose the business overnight. If your customer wants a lower price, you have almost no leverage to refuse, because the spirit you sell is a commodity — chemically identical to what the plant down the road produces. You are a price-taker in the most literal sense. Margins are thin, they are volatile, and they are entirely outside your control. A bumper sugarcane harvest or a drought can swing your input costs by double digits, and you absorb the shock because you have no brand premium to cushion it.

It is worth pausing on just how thankless the bulk-spirit business is, because the pain of it is the engine of the whole later story. A contract bottler lives in the gap between two prices it does not set: the price of molasses going in, which the sugar cycle dictates, and the price its customers will pay for finished spirit going out, which those customers dictate. In a good year, that gap is thin. In a bad year — a drought, a glut, a customer playing two suppliers against each other — the gap can vanish entirely, and the bottler discovers it has spent a year of effort to break even or worse. There is no brand to retreat to, no loyal consumer who will pay a premium for your alcohol over the identical alcohol next door, because at the molecular level there is no difference. You are selling a commodity, and the iron law of commodities is that the producer captures almost none of the value. That is the trap, and the Khaitans lived inside it for a quarter of a century.

This is the world the next generation of Khaitans inherited, and at least one of them found it intolerable. In 1995, Dr. Lalit Khaitan — G.N. Khaitan's son — took charge of the liquor division.4 A year later, in 1996, his own son, Abhishek Khaitan, joined the business. Abhishek was young, restless, and trained on a different intuition than the family had operated by. The conventional family wisdom said: make spirit efficiently, keep the customers happy, survive the cycles. Abhishek's instinct said the opposite. A supplier, no matter how efficient, is always one negotiation away from irrelevance. The only durable position in consumer goods is to own the consumer's loyalty directly — to be the name on the bottle, not the chemistry inside it.

That conviction — own the customer or be squeezed out of existence — is the founding mental model of modern Radico. It is easy, three decades and several billion dollars later, to call it visionary. At the time it was closer to reckless. The company had no consumer marketing capability, no national distribution to retailers, no advertising budget worth the name, and it was proposing to compete head-on with entrenched players who had all three. A skeptic on that 1990s board would have been right to ask: what makes a molasses distiller think it can build a brand? The answer would take a single product, launched in 1998, to settle. And that gamble is where the real story starts.

III. Part II: The 1998 Breakout — The "8 PM" Gamble

Every founding myth has its leap-of-faith moment, and for Radico it arrived in a boardroom where a young Abhishek Khaitan had to convince a deeply skeptical group of directors to do something the company had never done: spend its own money to put its own name in front of consumers, and hope they bought it.

The skepticism was rational. Building a liquor brand in India in the late 1990s meant going up against companies with decades of consumer relationships and far deeper pockets. The cost of failure was not just the marketing spend; it was the credibility of the entire strategic pivot. If the brand flopped, the lesson the board would draw was clear — stick to making spirit, leave branding to the branders. Abhishek was, in effect, betting the family's strategic future on a single SKU.

The product was a whisky, and the genius of it was in two unglamorous decisions that had nothing to do with the liquid and everything to do with understanding the Indian consumer.

The first was the name. They called it 8 PM. Abhishek's own explanation was almost disarmingly simple — the company felt that "8 was the simplest thing to depict," and that "people usually start drinking at 8 pm."4 In a country with dozens of languages and enormous variation in literacy, a number is universal. Eight o'clock is the hour the working day ends and the evening begins — the moment of transition from labor to leisure that the brand quietly claimed as its own. It was not aspirational in the way premium Scotch is aspirational. It was relatable. It embedded itself in the rhythm of an ordinary day.

The second decision was about packaging, and it reveals how a manufacturer's mindset can become a marketing advantage. Conventional liquor came in glass bottles, which were expensive and, crucially, fragile — a serious problem when your distribution has to reach deep into rural India over rough roads, where breakage in transit was a real and recurring cost. Radico leaned into formats that solved the logistics problem: smaller, more durable packs that lowered the cost of getting the product into the hands of price-sensitive consumers and reduced the breakage that ate into everyone's margins. It was a back-end insight — the company knew supply chains and unit economics cold — applied to a front-end problem. Democratizing access was not a slogan; it was an operational decision.

The result was the kind of outcome that does not happen twice in a career. Within a year of its 1998 launch, 8 PM became a "millionaire brand," selling a million cases — and it did so faster than any brand in the history of the Indian liquor industry. It was the first liquor brand ever to be recognized in the Limca Book of Records for the feat.4 To translate the achievement: a company with no brand-building track record had, on its first serious attempt, produced one of the fastest-scaling launches the industry had seen.

What did that prove, in evidence terms? It proved that the distribution reach and manufacturing cost base Radico had built up over decades as a supplier could be turned outward — that the same machinery that made it a good vendor could make it a formidable brand owner, if the product was priced and positioned for the mass consumer it already knew how to reach. The "own the customer" thesis was no longer a theory on a whiteboard. It had a million cases behind it.

There is a subtler lesson buried in the 8 PM launch that explains why so many incumbents failed to see it coming. The conventional view in branded liquor was that brand-building was a marketing competency — a function of advertising spend, glossy positioning, and consumer research budgets, all of which favored the deep-pocketed giants. Radico's win suggested something heretical: that in a market as vast, fragmented, and logistically punishing as India, distribution and cost could matter as much as advertising. A brand that could physically reach a village shop in eastern Uttar Pradesh, survive the journey without breaking, and sell at a price the local consumer could afford had an advantage that no amount of metropolitan ad spend could replicate. Radico did not out-market the incumbents in 1998. It out-operated them, and dressed the operational edge in a brand the consumer could love. That insight — that the back-end and the front-end are not separate disciplines but two ends of the same lever — became the company's enduring signature.

In 1999, riding the cash flow and the validation, the company formally shed the old identity. Rampur Distillery & Chemical Company became Radico Khaitan Limited.4 The name change was more than cosmetic. It was the public declaration that the business had crossed from the back of the bottle to the front — from chemistry vendor to consumer-brands company. The factory in Rampur was still there, still making spirit. But the company that owned it now understood that the real value was not in the molecules. It was in the name.

One million cases of a value whisky, however, is a volume game, and volume games in India are perpetually exposed to the price of grain, the price of glass, and the whims of state excise departments. The next act of the story is about a far more interesting question: could Radico do it again, but this time in a category with better economics and less competition? That is the Magic Moments chapter.

IV. Part III: Seizing the White Spaces — The "Magic Moments" Playbook

To understand the cleverness of what Radico did next, you have to picture the Indian liquor market of the early 2000s as a battlefield where everyone was fighting over the same hill. The hill was brown spirits — whisky and, to a lesser extent, brandy and rum. Whisky alone accounted for the overwhelming majority of all spirits volume, and it was where the giants concentrated their firepower. Diageo, through its control of United Spirits, and the French house Pernod Ricard were locked in an expensive, grinding war over the mid-premium whisky consumer, slugging it out with brands like Royal Stag, Blenders Pride, and McDowell's. It was a war of advertising surrogates, distributor incentives, and shelf dominance, and it was enormously capital-intensive.

Abhishek Khaitan's read of that battlefield was contrarian. Why charge up the same hill that two of the richest companies in the world were defending? The smarter move was to find the ground they were not defending at all. And the undefended ground, he concluded, was white spirits — vodka and gin.

White spirits were dismissed by the incumbents as a niche. India drank whisky; vodka was a rounding error. But Abhishek was looking at a different India than the one in the rear-view mirror: young, rapidly urbanizing, with a fast-growing cohort of women and first-time drinkers for whom a clear, mixable, less "heavy" spirit was far more appealing than a peaty whisky. The incumbents saw a small category. Radico saw a small category that was about to become a demographic wave — and, critically, one in which it would not have to outspend Diageo to win, because Diageo was not really there.

This is the strategic move that the 7 Powers framework calls counter-positioning: adopting a position the incumbent cannot copy without damaging its existing business. The giants could not pour their energy into vodka without admitting that the future might not be all whisky, and their entire organizations — their distributor relationships, their marketing playbooks, their factory mixes — were built around brown spirits. Radico, with nothing to protect, could move freely.

In 2006 it launched Magic Moments vodka. The positioning was deliberate and disciplined: not a cheap local vodka, and not a costly import like Smirnoff or Absolut, but the affordable-premium sweet spot in between — trendy, accessible, and aspirational without being out of reach. The aesthetic broke entirely from the macho, leather-and-horses iconography of whisky advertising. Frosted glass, youthful and lifestyle-driven imagery, a brand built for parties and nightlife rather than for the contemplative evening dram. Radico was not just selling a different liquid; it was selling to a different person, one the incumbents had not bothered to court.

The payoff compounded over two decades. By the FY2026 reporting period, Magic Moments had become the dominant force in Indian vodka — commanding a majority share of the domestic category — and had crossed into the upper ranks of global vodka brands by volume, a remarkable position for a product conceived for the Indian market.5 The analytical point is not the trophy ranking; it is what the ranking implies. A leading share in a category you essentially created and then defended for twenty years is the closest thing the alcohol business offers to a moat. Consumers form habits with white spirits the way they do with brown ones, and shelf space and distributor mindshare in a category you dominate are genuinely hard for a latecomer to dislodge.

Then Radico ran the same play a second time, in an even more overlooked corner of the market. In 2009 it turned to brandy — a category most of urban India regarded as a downmarket, almost medicinal "winter" drink, especially in the south. Radico launched Morpheus as a super-premium brandy, sold in a distinctive, stylized teardrop-shaped bottle at a price point that signaled indulgence rather than remedy. By premiumizing a category nobody else had thought worth premiumizing, Morpheus came to dominate the premium brandy segment, building a commanding share concentrated in the high-consumption southern states of Tamil Nadu, Andhra Pradesh, and Karnataka. Morpheus eventually crossed the million-case mark in its own right.[^6]

The Magic Moments and Morpheus chapters together teach the deeper lesson of Radico's middle period. The first act, 8 PM, proved Radico could build a brand. This second act proved something more valuable: that Radico had a repeatable method — find a category the giants are ignoring, enter it with a premium-but-accessible positioning and distinctive design, and own it before anyone decides to fight back. A one-off hit is luck. A repeatable playbook is a capability. And a capability is what eventually justifies reaching for the very top of the market — which is where the story goes next.

V. Part IV: The Luxury Ascent & "Hidden" High-Margin Gems

There is a moment in the maturation of every consumer company when management has to decide what kind of company it wants to be. For Radico, that moment crystallized in the mid-2010s, and the decision was deceptively consequential: stop chasing volume for its own sake, and start chasing value.

The logic was rooted in a vulnerability we have already met. Mass-market brands — the original 8 PM, the value rums like Contessa — generate volume and keep the distribution machine humming, but their economics are exposed. They sell at low price points, which means a spike in the cost of grain or glass eats directly into a thin margin, and in many states the distiller cannot simply raise the shelf price to recover the cost because the state controls pricing. The structural answer was to tilt the portfolio toward the Prestige & Above segment — the premium and luxury tiers where the consumer pays for the brand, not just the buzz, and where a far larger margin cushion absorbs input-cost shocks.

The first luxury statement came in 2016, and it drew on the oldest asset in the building. Radico reached back to the heritage of that original 1943 Rampur facility and launched Rampur Indian Single Malt — a 100% malt whisky, matured in the foothills of the Himalayas, with no industrial spirit blended in.4 This was a categorically different proposition from everything Radico had done before. It was not affordable-premium; it was genuinely premium, and the company aimed it first at export and duty-free markets — the US, the UK, Europe — where it could earn luxury credentials in front of discerning global drinkers before being released selectively into premium Indian retail. The sequencing mattered. A single malt's value is its story and its scarcity, and establishing the brand abroad first lent it an authenticity that a domestic-first launch could not have manufactured.

Two years later, in 2018, Radico caught the global gin revival — the so-called "gin-naissance" — with Jaisalmer Indian Craft Gin, a triple-distilled gin infused with hand-picked Indian botanicals and wrapped in luxury packaging. Jaisalmer moved quickly to a leading position in India's small but fast-growing luxury craft gin niche. Like Rampur, it was a brand designed to signal that Radico belonged in the same conversation as the world's craft distillers, not merely India's mass blenders.

Now, a skeptical investor will look at these two brands and shrug. Single malt and craft gin are a rounding error in Radico's total case volume — a few hundred thousand cases against tens of millions. Why should they matter to the investment case?

The answer is in the per-case economics, and it is the most important "hidden" fact in the Radico story. These super-premium brands command multiples of the net realization per case of regular IMFL — on the order of several times, and at the very top end closer to eight or ten times the revenue per case of a value whisky. That means a tiny slice of volume can throw off a disproportionate slice of profit. A single case of Rampur sold in a London duty-free shop contributes more gross margin than a stack of value-whisky cases sold through a state monopoly. The luxury brands are not a vanity project; they are a high-margin cash engine bolted onto a high-volume distribution machine.

They do a second job, too, which is harder to measure but real: the halo effect. A company known as a maker of award-winning single malts and craft gins is no longer perceived as merely a mass distiller. That elevation lifts the perceived quality — and the pricing latitude — of everything beneath it in the portfolio, from premium whiskies down to the workhorse brands. The luxury tier reshapes the brand equity of the whole house.

Between the affordable-premium middle and the rarefied luxury peak sits a third tier that has quietly become one of Radico's most important growth stories: premium whisky. This is the contested, high-volume battleground where Pernod Ricard's Royal Stag and Blenders Pride have long ruled, and where Radico, historically a white-spirits and brandy specialist, was a relative newcomer. The company has been pushing into it with deliberate force. The flagship is 8PM Premium Black, launched in 2018 as a refined extension of the original 8 PM franchise; by mid-2025 it had crossed 12 million cases sold cumulatively and become one of Radico's "millionaire" brands.10 Above it sits Royal Ranthambore, a crafted whisky inspired by the tigers of Rajasthan that Radico has positioned at the premium-to-luxury seam, rolling it into the lucrative Canteen Stores Department channel that serves India's military and into export markets including the United States.11 The strategic point is that Radico is no longer content to win only the categories the giants ignore — it is now contesting the category the giants most care about, and doing so with brands designed from the start for the premium consumer rather than dragged upmarket from the value tier.

The right way to hold these facts together is this: the mass brands give Radico reach and scale; the premium whiskies give it volume in the industry's biggest pool; and the luxury brands give it margin and prestige. The luxury portfolio alone reached roughly ₹475 crore in FY2026, and management has guided for it to keep compounding at around 25% a year.9 None of these tiers alone is the business. The combination — a broad base of volume, a fast-growing premium-whisky middle, and a narrow spike of very-high-margin cash flow that is largely insulated from Indian state price controls because so much of it is exported and earned in hard currency — is the architecture management has spent a decade building. Whether that architecture actually delivers superior, durable economics is a question we can only answer by getting under the hood of how Radico makes money. So let us go there next, into the genuinely strange machinery of selling alcohol in India.

VI. Part V: Core Business, Economics & The Indian Monopoly Matrix

If you want to understand why the Indian spirits business is one of the hardest consumer industries on Earth — and why a company that masters it earns a real moat — you have to abandon almost everything you assume about how a product reaches a shelf. In most of the world, a company makes a thing, ships it to retailers, and sets a price. In India, the state sits in the middle of every one of those steps, and it sits differently in each of twenty-eight states. Before we get there, though, the money.

Where the money actually is

Radico's reported business splits into two segments, and the split is where the strategy becomes visible in the numbers. In FY2026, the Prestige & Above segment — the premium engine — contributed roughly 70% of IMFL revenue while accounting for under half of physical volume; the segment's volume grew about 28.5% year-on-year to 16.7 million cases, and P&A made up 45.6% of IMFL volume and 70.3% of IMFL revenue.2 Read that again, because it is the whole thesis in two numbers: less than half the cases, more than two-thirds of the revenue. The premium tier is doing the heavy lifting.

The Regular & Popular segment is the mirror image: the majority of physical cases, but a shrinking minority of revenue. And it is shrinking on purpose — Radico has been deliberately de-prioritizing the lowest-margin, most price-sensitive volumes, accepting flat or falling case counts at the bottom in exchange for richer mix at the top. The fingerprint of that strategy is all over the consolidated results for FY2026: net revenue of ₹6,050 crore, up 24.7%; EBITDA of ₹1,018.5 crore, up 52.4%; and an EBITDA margin that expanded by roughly 305 basis points to 16.8%.2 When margin expands that much faster than revenue, it tells you the growth is coming from mix and price, not just from selling more cheap cases. That is the premiumization thesis showing up where it counts — in the spread between top-line and profit growth.

Profit followed. In the fourth quarter of FY2026 alone, net profit jumped about 93% to roughly ₹175 crore, on quarterly revenue of around ₹1,503.7 crore.6 A near-doubling of quarterly profit on mid-teens revenue growth is, again, the signature of operating leverage and mix — not of a company simply riding a volume wave.

The competitor matrix

Radico does not play this game alone, and a sense of scale matters. The undisputed titan is Diageo's Indian arm, United Spirits, with net sales well north of ₹11,000 crore and a portfolio built around prestige whisky brands like McDowell's No. 1, Royal Challenge, and Signature. Pernod Ricard India, though it reports differently, is widely regarded as the profitability king of Indian whisky, dominating the lucrative mid-premium tier with Royal Stag and Blenders Pride and commanding deep, durable brand equity. Against these two, Radico — at roughly ₹6,050 crore in net revenue — is the credible challenger rather than the incumbent: smaller than United Spirits, but growing faster and owning categories the giants conceded, namely white spirits and premium brandy, while pushing aggressively into premium whisky with brands like 8PM Premium Black and Royal Ranthambore. At the other end sits Tilaknagar Industries, a far smaller player concentrated in brandy through its Mansion House franchise, which collides directly with Morpheus in the south.

The analytical takeaway from the matrix is that Radico is not trying to beat Diageo at Diageo's game. It is trying to grow faster than the market in the niches it owns, and to use premium whisky to chip at the giants' core without betting the company on a frontal assault. Whether that flanking strategy keeps working depends heavily on the thing that makes India unique: route to market.

Myth versus reality

Before we get there, it is worth puncturing a stubborn piece of the consensus narrative, because it shapes how the market values the company. The myth is that Radico is, at heart, a cheap-liquor company — a maker of value whisky and mass rum that has dressed up a couple of premium brands for show. The reality, visible in the segment economics, is the inverse. The mass tier is the part of the business Radico is deliberately shrinking, and the premium and luxury tiers are where the revenue, the growth, and nearly all of the incremental profit now live. A company whose Prestige & Above segment already supplies the clear majority of revenue, whose luxury portfolio is approaching ₹500 crore, and whose single malt sits on duty-free shelves is not, by any honest reading, a cheap-liquor company that happens to dabble in premium. It is a premium company still carrying a mass-market tail it is steadily de-emphasizing.29 The distinction matters for investors because the two framings imply very different earnings trajectories and very different multiples. The legitimate skeptical counter is that the mass tail still accounts for the majority of physical volume, so a sharp downturn in those low-end states would still sting — but the direction of travel is unambiguous, and it points up-market.

The route-to-market maze

In India, alcohol is a state subject — meaning each state writes its own rules for how liquor is made, distributed, taxed, and sold. The practical result is not one Indian market but twenty-eight micro-markets, each with its own excise regime, its own licensing, and its own model of who gets to sell to whom. Broadly, they fall into two camps, and the difference between them is the difference between having pricing power and having none.

In the monopoly (or "corporation") states — Tamil Nadu, Kerala, Karnataka, Andhra Pradesh, and others — a state-run beverage corporation (TASMAC in Tamil Nadu, BEVCO in Kerala) is the only legal buyer. The corporation purchases directly from distillers, fixes the retail price, and controls the entire distribution and retail network. For a company like Radico, this is a monopsony: a single buyer on the other side of the table. The distiller has, functionally, zero direct pricing power. If grain or glass costs spike, Radico cannot raise its price; it must petition the state government for a price revision and wait — sometimes for many months — for an answer that may never come. This is the single most important risk in the entire business, and we will return to it.

In the open (private) market states — Maharashtra, Haryana, and others — private distributors and retailers operate, and pricing is more flexible. But the trade-off is steep: these states extract enormous licensing fees and excise duties, so the freedom to price comes bundled with a heavy tax load. There is no easy state in India. There are only different kinds of hard.

The moat: backward integration

So how does a company survive — and expand margins — inside a system where it often cannot set its own prices and is perpetually exposed to agricultural inflation? Radico's answer, and the heart of its cost moat, is backward integration into its own raw material.

The base of every spirit is Extra Neutral Alcohol. A non-integrated blender has to buy ENA on the open market, where the price swings violently with the cost of molasses and grain. When ENA prices spike, the non-integrated player's margin collapses, because in a monopoly state it cannot pass the cost on. Radico, by contrast, produces a large share of its own ENA from grain at its own distillation plants in Rampur and Aurangabad. By controlling the production of its core input, it insulates its gross margin from the open-market ENA cycle — it is, in effect, both the farmer's-market and the kitchen.

The evidence that this works showed up vividly in the FY2026 numbers. By the fourth quarter, Radico's gross margin reached 48% — an expansion of roughly 453 basis points year-on-year, of which management attributed about 225 basis points specifically to raw material, the direct payoff of softening grain prices flowing through an integrated cost base.9 A non-integrated rival captures far less of that benefit because it is buying finished ENA at whatever the market dictates. When the cycle turns the other way, the same integration cushions the blow. That is the asymmetry backward integration buys: more of the upside when input costs fall, and a softer landing when they rise.

But — and this is the neutral investor's caveat — backward integration is a shock absorber, not a force field. Radico still has to buy the grain (broken rice and maize) that feeds its own distilleries, and it still has to buy glass for its bottles, and both of those are exposed to weather, harvests, and commodity markets. Owning the ENA step protects you from the ENA traders' margin and from one layer of volatility; it does not exempt you from the underlying agricultural cycle. When management talks about margins, the honest framing is that integration narrows the range of outcomes — it does not guarantee the good one.

That tension — a genuine cost advantage that is real but not absolute — is exactly the kind of thing that gets tested when a company starts spending serious money. And Radico has been spending. Which brings us to capital allocation.

VII. Part VI: M&A, Capital Deployment, & The Scotland Venture

The cleanest way to judge a management team is not to read its strategy slides but to follow its money. Where does the cash go when there is cash to deploy? For Radico, the answer across two decades reveals a company that has generally been disciplined about acquisitions — and is now placing its most ambitious and most questionable bet yet.

The 2005 Brihan Maharashtra deal — disciplined brand-building

Rewind to 2005. Radico, flush from the success of 8 PM and still a few years from launching Magic Moments, made a quiet acquisition that would prove strategically outsized relative to its modest price. It bought a portfolio of eight brands from the Brihan Maharashtra Sugar Syndicate for roughly ₹35 crore.

What makes this deal interesting is not the brands themselves but the price and the geography. Global spirits M&A routinely changes hands at three to five times sales or more, because established brands with loyal consumers are rare and defensible assets. Radico paid a small fraction of that. More importantly, the deal handed Radico an immediate manufacturing and distribution footprint in western and southern India — precisely the regions where brandy consumption is highest. When Radico launched Morpheus four years later and needed a southern beachhead, the Brihan Maharashtra infrastructure was already in place. This is the model of a good tuck-in acquisition: cheap, strategically enabling, and digested without drama. It bought capability, not vanity.

It is worth contrasting Radico's M&A temperament with the path its larger rivals took, because the contrast is instructive about capital discipline. The Indian spirits industry of the 2000s and 2010s was littered with expensive, debt-fueled empire-building — most spectacularly at the company that became United Spirits, whose previous owner pursued growth through aggressive acquisition and leverage until the balance sheet buckled and control passed to Diageo. Radico, by comparison, grew its brand portfolio mostly organically, launching its own products rather than buying other people's at inflated prices, and reserving acquisitions for small, strategically targeted tuck-ins. That conservatism is not glamorous, and it arguably left Radico smaller than it might otherwise have become. But it also meant the company never bet its survival on a single overpriced deal — a discipline that looks wise in hindsight and that frames the more recent, splashier moves into D'Yavol and Scotland as departures from a long-standing pattern of restraint, departures a neutral investor should watch precisely because they break the historical mold.

The 2025 D'Yavol luxury joint venture

Fast-forward two decades and Radico's M&A instincts had shifted toward the luxury end and toward optionality. In 2025, the company took a 47.5% stake in D'Yavol Spirits BV, a Netherlands-registered luxury venture associated with Aryan Khan — son of Bollywood superstar Shah Rukh Khan — targeting ultra-premium spirits and lifestyle.[^8] Structurally, this is a low-capital, high-optionality bet: a minority stake in a brand whose entire value proposition is celebrity-driven cultural cachet, aimed at the very peak of India's emerging luxury pyramid. If it works, Radico gets a foothold in a segment where margins are extraordinary and brand-building is half the battle. If it fails, the downside is contained to a minority investment. It is the kind of asymmetric bet a company can afford once its core is generating real cash. The neutral read: sensible in size, unproven in outcome, and worth watching rather than celebrating.

The 2026 Scotland venture — necessity or distraction?

And then there is the bet that has analysts arguing. In January 2026, Radico's board approved the creation of Radico Khaitan Scotland Ltd, a wholly owned UK subsidiary, in a filing with the National Stock Exchange dated January 22, 2026. The stated purpose was to handle the distillation, maturation, storage, and trading of Scotch whisky — and, eventually, to acquire, own, and operate a distillery in Scotland itself.3

The strategic logic is coherent on its face. As Radico's premium whisky and single malt portfolio grows, so does its need for mature malt spirit — including imported Scotch malt used in blending. A company spokesperson framed it precisely in those terms: as the whisky portfolio grows, "our import requirement will also increase in the coming years," and the move was "towards securing access to mature supply chains for distillation and maturation in a cost-effective manner."7 Owning a Scottish distillery would lock in a long-term, captive source of aged malt and build direct European distribution — vertical integration of the same kind that made the ENA strategy work at home, now extended to the luxury whisky supply chain. The India-UK Free Trade Agreement signed in July 2025, which lowers trade barriers, sweetens the rationale.7

But a neutral investor should hold two skeptical facts in view. First, management itself has been conspicuously cautious about how real this is. The same spokesperson admitted the acquisition idea was "at a very initial stage, particularly the acquisition bit, where we are not actively pursuing or evaluating any assets."7 By mid-2026, the search reportedly continued with the company "keeping all options open."3 A subsidiary has been incorporated; a distillery has not been bought. Second, and more substantively, this is exactly the moment to ask whether capital allocated to a Scottish distillery is capital well spent. Radico has spent years telling the market it is on a path to becoming net-debt-free, and a Scotch distillery is an expensive, foreign, operationally unfamiliar asset. The bull sees vertical integration securing a premium supply chain. The bear sees a domestically focused company reaching across continents for an asset it does not yet need, at a time when its own balance sheet deleveraging is already running behind schedule. Both readings are legitimate, and which one proves right depends on execution Radico has not yet had to demonstrate.

That unfinished deleveraging story is the natural hinge into the harder questions — the ones a short-seller would ask. So let us put management itself on the stand.

VIII. Part VII: Management, Alignment, & The Skeptical Investor Stress Test

Two men have run Radico for the entire modern arc of this story, and any assessment of the company is, at bottom, an assessment of them.

Dr. Lalit Khaitan, the chairman, is the patriarch who took over the liquor division in 1995 and oversaw the build-out of the physical infrastructure — the distilleries, the integration, the manufacturing backbone that everything else rests on. Abhishek Khaitan, the managing director who joined in 1996, is the brand-builder — the architect of 8 PM, Magic Moments, Morpheus, Rampur, and Jaisalmer. The division of labor between them, factory and brand, father and son, maps almost perfectly onto the two halves of the Radico story. The relevant point for an investor is consistency: this is the same leadership that articulated the "own the customer" thesis three decades ago and has executed against it, through several input-cost cycles and competitive waves, with a coherence that is genuinely rare in family-run businesses. Strategic consistency over twenty-five years is itself a form of evidence — it is the opposite of the serial-pivot, blame-shifting pattern that should worry investors in other companies.

There is also a tell in how management communicates with the market. Across recent earnings calls, the language has been notably consistent and quantified — specific volume-growth targets for each segment, explicit margin-expansion goals in basis points, a stated minimum dividend payout, and a named deadline for going debt-free.9 Quantified, falsifiable guidance is itself a credibility signal: it is far easier to hide behind vague aspiration than to commit to a number an analyst can check against you next quarter. The flip side, which a skeptic should hold onto, is that committing to numbers only builds credibility if you hit them — and the one major target Radico has missed, the original debt-free deadline, is precisely the one that matters most to the balance-sheet bulls. So the management scorecard is mixed in an interesting way: highly credible and consistent on the operating line, where the premium mix and margin guidance have largely come through, but with one conspicuous slip on the financial line that it is now asking the market to trust it will close in FY2027.

On alignment, the structure is reassuring. Promoters hold roughly 40% of the company, with the stake concentrated in a family holding entity, Sapphire Intrex Limited, which owns close to 34%.8 The Khaitans' direct personal shareholdings are tiny — fractions of a percent each — which at first glance looks like low skin in the game. It is the opposite: nearly all of the family's enormous wealth sits inside that holding company, which means their private fortune rises and falls with the same listed share price that public shareholders own. Their interests and minority shareholders' interests point in the same direction. That is the kind of alignment you want.

On pay, the picture is more debatable. In FY2025, the two Khaitans drew compensation in the neighborhood of ₹13–14 crore each. For a mid-cap Indian company, that is on the rich side, and a governance-minded investor is entitled to flag it. The mitigant is the ownership structure: when management's pay is dwarfed by the value of its equity stake, the incentive to milk the company through salary rather than build it through share value is weak. The pay is high; the alignment blunts the concern without erasing it.

Now the stress test — the three things a skeptical long-short investor or an activist would press on.

First, the moving deleveraging target. Management had guided that Radico would reach a net-debt-free balance sheet by FY2026. That target slipped to the first half of FY2027, with the explanation being ongoing capital expenditure on the Rampur and Aurangabad distillery expansions — the very backward integration that underpins the cost moat. A charitable reading is that the company is investing in capacity that will pay off for years, and that a one-period slip on deleveraging in service of high-return capex is a reasonable trade. A skeptical reading is that a missed balance-sheet promise is a missed promise, full stop, and that the new Scotland ambition raises the question of whether capital is being recycled with the discipline management claims. The honest verdict is that this is a yellow flag, not a red one — but it is the kind of yellow flag that turns red if the timeline slips a second time.

Second, related-party transactions. Radico, like many promoter-controlled Indian companies, has leased commercial properties and warehousing from promoter-linked entities. There is nothing inherently wrong with this — it is common — but it is precisely the kind of arrangement an activist demands transparency on, because related-party leasing is a classic channel through which value can quietly leak from public shareholders to the controlling family. The diligence question is not "does this exist" but "is it priced at arm's length," and the burden of proof sits with the company to demonstrate that it is.

Third, the input-cost squeeze that integration does not fully solve. We have established that backward integration cushions the ENA cycle. But Radico remains genuinely exposed to things it must buy on the open market — and the FY2026 environment showed how sharp those swings can be. Industry bodies flagged glass bottle costs up around 20%, paper carton costs up by nearly 100%, and logistics costs up roughly 10% over the period, pressures severe enough that liquor associations were petitioning state governments for retail price increases of 15–20% just to keep current pricing sustainable.9 That is the crux of the structural problem laid bare: the costs are non-negotiable and rise on the market's schedule, while the prices are negotiable only with a state bureaucracy that moves on its own. When packaging and freight inflate and a key monopoly state drags its feet on a price revision, the margin compression is real and there is little management can do in the short run. Backward integration into ENA does nothing to solve a doubling of carton costs. This is not a hypothetical risk; it is the recurring reality of operating inside state-controlled pricing, and it caps how much credit a neutral investor should give to the "margins only go up" version of the story.

None of these three issues is disqualifying. Together they are the realistic texture of a well-run but promoter-controlled company operating in a hostile regulatory environment. The job of the frameworks we turn to next is to weigh these frictions against the genuine sources of advantage — and to be honest about which of those advantages are durable and which are merely management's preferred narrative.

IX. Part VIII: Strategic Frameworks — Hamilton's Powers & Porter's Forces

Strategy frameworks are only useful if you let them argue against the company as well as for it. Run honestly, they separate the parts of Radico's moat that are real and durable from the parts that are softer than the bull case admits.

Hamilton Helmer's 7 Powers, applied to Radico

Counter-positioning — strong, and proven. This is Radico's signature power, and it is the most genuinely earned. Twice — first with Magic Moments vodka in 2006, then with luxury craft spirits like Jaisalmer and Rampur — Radico occupied ground the incumbents could not contest without disrupting their own whisky-centric businesses. The evidence is in the resulting market positions, which the giants conceded by inaction. This power is real because it is structural: Diageo and Pernod Ricard's reluctance to cannibalize their own franchises was not a one-time mistake but an ongoing constraint.

Cornered resource — strong, and underrated. In India, a new greenfield distillery license is extraordinarily hard to obtain, gated by political, environmental, and excise hurdles that can take years to clear, if they clear at all. Radico's existing, high-capacity, licensed manufacturing footprint in Uttar Pradesh and Maharashtra is therefore not easily replicable by a new entrant — it is a scarce asset protected by the very regulatory thicket that makes the industry so painful. This is arguably Radico's most defensible and least appreciated power.

Brand — strong in its niches. Deep, hard-to-replicate consumer equity in Magic Moments, Morpheus, and 8 PM gives Radico pricing latitude and shelf priority within the categories it owns. The caveat: brand power in spirits is category-specific. Radico's brand is formidable in vodka and premium brandy and respectable in value whisky; it is still a challenger in premium whisky, where Pernod's equity runs deeper. The power is real but unevenly distributed across the portfolio.

Scale economies — moderate to high. Backward integration and high-volume grain-ENA production let Radico amortize fixed costs in a way non-integrated blenders cannot. This is a genuine cost edge, but it is bounded — Radico is meaningfully smaller than United Spirits, so on pure procurement and distribution scale, it is not the cost leader of the industry.

Switching costs — low. Here the framework cuts against the company. End consumers face essentially zero cost to switch liquor brands; loyalty is habit and brand affinity, not lock-in. There are modest B2B switching frictions — shelf space, distributor and state-corporation relationships — but at the consumer level this power is largely absent. Any bull case that leans on consumer stickiness is leaning on sand.

Network effects — none. Alcohol simply does not have them. No analyst should pretend otherwise.

Process power — low to moderate. Proprietary blending recipes and wood-maturation know-how for Rampur single malt confer some advantage, but it is incremental, not a category-defining edge.

The honest scorecard: Radico's real powers are counter-positioning, its licensed manufacturing footprint, and brand within specific categories. The softer claims — switching costs, network effects, broad process power — should be discounted. A moat built on three solid pillars is a real moat; it is just narrower than a promotional telling would suggest.

Porter's Five Forces, for the Indian alcobev industry

Bargaining power of buyers — extremely high. This is the dominant force in the whole analysis. In the monopoly states, the government corporation is the sole buyer and the price-setter, and the distiller has almost no leverage. No amount of brand strength fully escapes a monopsonist who controls your price.

Threat of new entrants — very low. Draconian, state-by-state licensing; the near-impossibility of new greenfield licenses; high capital intensity for integration; and a complete ban on direct alcohol advertising (which forces incumbents into expensive surrogate marketing that newcomers cannot easily match) together make entry at scale almost impossible. This force strongly favors all incumbents, Radico included.

Competitive rivalry — high. Radico shares the field with two of the largest, best-capitalized spirits companies on Earth. Rivalry is intense, and Radico wins by avoiding head-on collisions, not by overpowering its rivals.

Bargaining power of suppliers — moderate. Backward integration into ENA mutes supplier power on the most important input, but glass makers and grain suppliers retain real leverage, as discussed.

Threat of substitutes — low. Beer and country liquor exist as alternatives, but spirits occupy a distinct and culturally entrenched place in Indian consumption that is not easily substituted away.

Put the two frameworks together and a clear picture emerges. The Indian spirits industry is a fortress: brutally hard to enter, dominated by a few players, and protected by regulation. But it is a fortress whose front gate is held by the state, which can dictate prices and even, in places like Bihar and Gujarat, ban the product entirely. Radico has built genuine, defensible advantages inside that fortress. The open question — the one no framework can settle — is whether those advantages compound faster than the regulatory and input-cost frictions erode them. That is the bull-versus-bear debate.

X. Part IX: Bull vs. Bear Case & Key KPIs

The bull case

The bull case rests on three pillars, each grounded in something already visible in the numbers rather than in pure projection.

The first is the premiumization runway. The Prestige & Above segment has been compounding at a high-twenties percentage rate, and because premium cases carry far more margin than mass cases, every point of mix shift toward P&A pulls the company's EBITDA margin upward.2 The FY2026 result — 305 basis points of margin expansion in a single year — is concrete evidence that the mechanism works, not just a slide. And management has put specific numbers on the next leg: on the Q4 FY2026 earnings call it guided to roughly 20% Prestige & Above volume growth, 25% luxury portfolio growth, a further 125 basis points of EBITDA margin expansion, debt-free status, and a minimum dividend payout of 20% of profit after tax for FY2027.9 What is notable for a neutral observer is that this is not vague ambition; it is a quantified, falsifiable target set against the company's own prior record of expanding margins. If India's premiumization wave has years left to run — and the demographic and income trends suggest it does — Radico is positioned at the front of it in the categories it owns. The bull case is that management has, so far, tended to deliver on the operating targets even as the balance-sheet timeline slipped.

The second is the balance-sheet turnaround. If Radico hits the revised target and reaches net-debt-free status in the first half of FY2027, it frees up substantial free cash flow currently servicing debt — cash that can fund dividends, the luxury bets, and further integration without diluting shareholders. A debt-free Radico is a structurally higher-quality company than the leveraged one.

The third is the global craft playbook. Rampur single malt and Jaisalmer gin earn hard-currency revenue in export and duty-free markets that is entirely outside the reach of Indian state price controls. As those brands scale, they add a stream of high-margin, regulation-insulated profit — exactly the kind of earnings that deserve a premium multiple because they are both fast-growing and structurally protected from the domestic monopsony problem.

The bear case

The bear case is equally grounded, and it maps onto the risks we have already surfaced.

The first is regulatory and monopsony shock. A single large consuming state can rewrite its route-to-market policy, hike excise, refuse a needed price increase, or — as Bihar and Gujarat have shown — impose outright prohibition, instantly erasing a chunk of localized revenue with no recourse. Concentration of volume in a few big states makes this a live, not theoretical, danger.

The second is the input-cost squeeze. A bad monsoon or an adverse shift in agricultural policy can spike grain prices, and glass remains volatile; when those costs rise and the monopoly states drag their feet on price revisions, margins compress regardless of how good the brands are. Backward integration softens this but does not remove it.

The third is capex and Scotland execution risk. The deleveraging timeline has already slipped once. Layering on an ambitious, capital-intensive, operationally unfamiliar Scottish distillery — an asset the company itself admits it is not yet actively pursuing — raises the risk of capital being deployed for ambition rather than return, with integration and regulatory friction in a foreign jurisdiction and the potential to distract from the domestic engine that actually generates the cash.

The neutral synthesis is that Radico is a genuinely good business in a genuinely hard industry, with real moats and real, structural vulnerabilities that no amount of execution can fully eliminate. The bull and bear cases are not mutually exclusive; they are two true descriptions of the same company, and which one dominates in any given year is decided largely by forces — monsoons, excise departments, state politics — that sit outside management's control.

The three KPIs that actually matter

For an investor tracking Radico from here, most metrics are noise. Three are signal.

First, Prestige & Above volume and revenue growth, tracked quarterly. This is the single clearest read on whether the premiumization engine is still running. As long as P&A is growing in the mid-twenties or faster and taking share of the revenue mix, the core thesis is intact. A deceleration here would be the first and most important warning.

Second, gross and EBITDA margin, in basis points. This is the scoreboard for the contest between premiumization plus integration on one side and grain-and-glass inflation plus monopsony pricing on the other. Expanding margins mean Radico is winning that contest; compressing margins mean the input-cost and regulatory pressures are overwhelming the mix benefit.

Third, net debt, in absolute crores. This is the discipline gauge. Watch whether the company actually reaches net-debt-free in the first half of FY2027 as promised. Hitting it validates management's capital discipline; a second slip — particularly if Scotland-related spending is the reason — would be a meaningful mark against the team's credibility.

XI. Epilogue & Outro

Step back from the quarterly numbers and the framework scorecards, and the Radico Khaitan story resolves into a few durable lessons that outlast any single fiscal year.

The first is that the brand is the ultimate moat — but only certain brands, in certain categories. Physical plants can be rebuilt and recipes reverse-engineered, but cultural real estate in a consumer's mind — the reflex that makes "8 PM" mean the end of the workday or "Magic Moments" mean a night out — generates cash flow that compounds for decades. The qualifier the neutral investor must keep is that this power is category-specific and consumer switching is cheap; the moat is real where Radico is dominant and thin where it is merely a challenger.

The second is that backward integration in a regulated, inflationary economy is not a cost-saving footnote; it is a survival mechanism. Controlling its own ENA is what lets Radico hold its margins inside a system where it frequently cannot set its own prices. It is the corporate equivalent of growing your own food when you cannot control the price of bread. But control of one input is not control of all inputs, and the company remains hostage to harvests and to the glass market in ways no slide deck fully escapes.

The third is that premiumization is a marathon measured in decades, not quarters. Turning a molasses distiller into a house that sells award-winning single malt took Radico the better part of fifty years of consistent, patient, sometimes contrarian execution — and the work is not finished. The Scotland venture, the D'Yavol bet, the relentless mix shift toward Prestige & Above: these are the latest moves in a very long game, and their outcomes are not yet written.

The legacy of that 1972 acquisition of a broken Rampur distillery is a company that learned, against the odds and against the entrenched logic of its own industry, to climb from the back of the bottle to the front. Whether Radico can keep climbing — into super-premium whisky, into global markets, into a debt-free future — is the open question that makes it one of the more compelling consumer stories in the emerging markets today. The history is settled. The next chapter is not.

References

-

Radico Khaitan posts FY26 net revenue of ₹6,050 crore — ScanX / Stock Market News, 2026 ↩↩↩↩↩

-

Radico Khaitan 'keeping all options open' as scotch distillery search continues — Global Drinks Intel, 2026 ↩↩↩

-

Radico Khaitan Limited | History, Brands and Company Profile — Radico Khaitan official website ↩↩↩↩↩↩↩

-

How Magic Moments vodka captured India — Fortune India, 2025 ↩

-

Radico Khaitan Q4 profit jumps 93% on premium liquor boom — Storyboard18, 2026 ↩

-

Radico Khaitan to establish Scotch whisky arm — The Spirits Business, 2026-01 ↩↩↩

-

Radico Khaitan Ltd. shareholding pattern: Promoter, FII, DII — Tijori Finance ↩

-

Radico Khaitan Q4FY26 Concall Transcript: FY27 Guidance, Brand Growth & Margin Targets — ScanX, 2026 ↩↩↩↩↩↩

-

Radico Khaitan Unveils the New 8PM Premium Black Pack — PR Newswire, 2025-06 ↩

-

Radico Khaitan introduces Royal Ranthambore Whisky at Canteen Stores Department — Business Today, 2025-02-20 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube