Quess Corp: The Workforce Engine of the Subcontinent

I. Introduction & The "Prem Watsa" Connection

Picture a sprawling Whitefield tech park on the eastern fringe of Bengaluru at six in the morning. Long before the engineers swipe in, a small army has already been at work for hours. Security guards in pressed grey uniforms man the boom barriers. Housekeeping crews in matching aprons polish the marble lobby. Cafeteria contractors haul in tiffin carriers from a central kitchen. A team of receptionists, all on payrolls outside the building's marquee tenants, slide behind their desks. And up on the third floor, in a back office of a Fortune 500 customer, a hundred-odd voice agents log into a call queue that wakes up just as the United States goes to bed.

Almost none of these people technically work for the companies they serve. They work for क्वेस Quess Corp — and on any given day, somewhere around half a million of them are on the move across India, Southeast Asia, North America and the Middle East.1

That number — half a million — is the punchline of an unusually Indian business story. Quess is the largest private-sector employer in the country. It is bigger by headcount than रिलायंस Reliance Industries, bigger than टाटा Tata Consultancy Services, bigger than any of the legacy industrial houses whose names dominate every list of "India's biggest companies."[^16] Yet most retail investors would struggle to describe what Quess actually does, because what it does is not one thing. It does payroll. It does facility management. It runs the country's largest non-government job board. It does customer service for global banks. It repairs your laptop under warranty. It manages physical security at airports. The common thread is that Quess is what you call when you would rather not employ the person yourself.

How did a 19-year-old company end up running so much of the messy middle of the Indian economy? The short answer is two letters and a name: M, A, and प्रेम वत्सा Prem Watsa.

In 2013, फेयरफैक्स Fairfax Financial Holdings — the Canadian insurance and investment conglomerate that the financial press has spent two decades calling "the Berkshire of the North" because of Watsa's value-investing style — bought a controlling interest in a small Indian recruitment firm called इक्या IKYA Human Capital Solutions through its publicly listed travel subsidiary Thomas Cook (India).2 What that capital injection bought wasn't really a staffing company. It bought a founder, Ajit Isaac, and a thesis that the formalisation of Indian labour was going to be one of the great structural trades of the century. Over the next thirteen years, Watsa would back Isaac through more than a dozen acquisitions, an oversubscribed IPO, a sprawl into adjacencies the staffing industry had never colonised, and finally a three-way structural demerger that completed in June 2025.10

This is the story of how a small Bengaluru-based recruiter went from being one of dozens of "people supply" firms to becoming a 14,967-crore-rupee revenue platform — and why its founders and largest shareholder just decided to take the platform apart on purpose.11 It is also a story about something subtler: the slow, grinding shift of hundreds of millions of Indians from the असंगठित क्षेत्र unorganised sector into the formal economy, and how exactly you build a business that monetises that shift without getting crushed by its margins.

II. Founding & The "Formalization" Macro-Theme

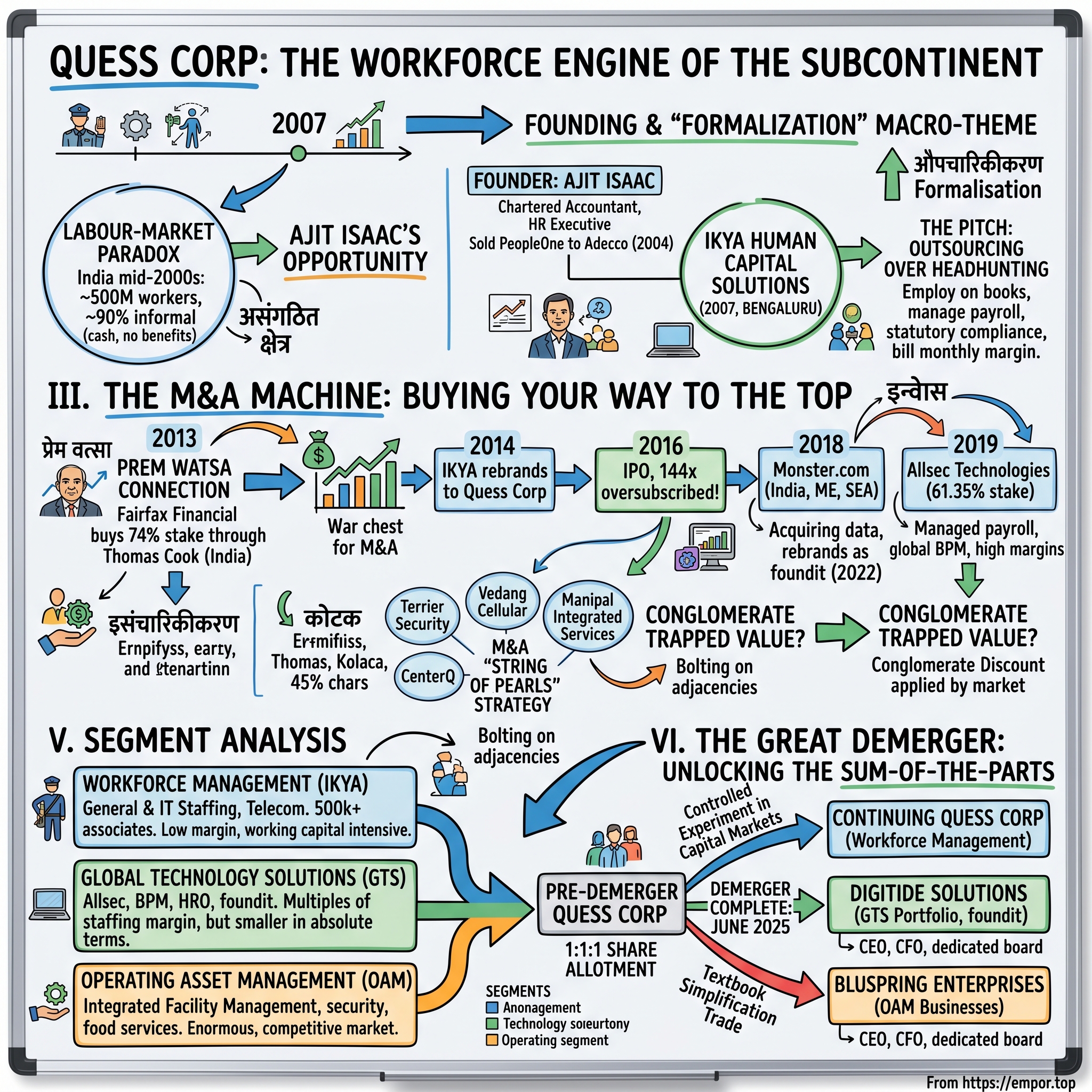

To understand why Quess exists, you have to understand the room Ajit Isaac walked into when he started IKYA in 2007.

India in the mid-2000s was a labour-market paradox. The country had close to half a billion working-age people, a savings rate north of 30%, and a GDP growing in the high single digits. Yet roughly nine out of every ten workers were employed informally — paid in cash, off the books, with no provident fund, no employee state insurance, no appointment letter, no paper trail. The official labour codes were a thicket: 29 distinct central acts, each layered with state amendments, each enforced by a separate inspectorate. Hiring even a hundred people the "right" way required so much compliance overhead that most mid-sized companies simply did not bother. They subcontracted, they used cash, they accepted the risk.

That mess was Ajit Isaac's opportunity.

Isaac was not a typical Indian founder. He was a chartered accountant turned HR executive who had spent the 1990s running employee benefits programmes inside multinationals before deciding, in the early 2000s, that the staffing industry was the play. He launched a firm called PeopleOne Consulting, scaled it for four years, and sold it to the Swiss giant アデコ Adecco in 2004. That sale gave Isaac two things most Indian founders never get on their first try: serious cash, and a graduate-level education in how a global staffing platform actually works.

Three years later, with a non-compete behind him and a Rolodex full of Indian CFOs, he was back. IKYA Human Capital Solutions was founded in 2007 in Bengaluru with what was, at the time, a slightly heretical pitch. Most Indian staffing firms in that era were essentially headhunters — they took a fee for placing a candidate and then disappeared. Isaac's bet was that what corporate India actually needed was not headhunting but outsourcing — not "find me a person" but "find me a person, employ them on your books, run their payroll, file their statutory contributions, deal with their grievances, and bill me a monthly margin per head." If you could get the operations tight enough, the per-head margin was thin but the volumes were enormous. And once a customer plugged you into their HRIS and gave you their statutory compliance to manage, they almost never switched providers.

This is the part the outline calls औपचारिकीकरण formalisation — the slow, multi-decade conversion of informal labour into formal labour. Every time the Indian government tightened a labour law, every time a large customer's auditor flagged a contractor compliance gap, every time a multinational expanded into a new tier-two city and didn't want to set up its own HR team — IKYA's addressable market expanded by another notch.

For five years Isaac and his small team — including a young operations specialist named Guruprasad Srinivasan, who would later become CEO — ground it out.12 They built scale in general staffing, they bolted on early IT staffing capability, they began to win marquee logos in BFSI and telecom. And then in early 2013 came the moment that turned IKYA from a fast-growing private company into something with the capital to think much bigger.

On February 5, 2013, Thomas Cook (India) Limited — the publicly listed Indian travel-services subsidiary that Prem Watsa's Fairfax had bought a controlling stake in just months earlier — announced that it was acquiring a 74% stake in IKYA for approximately ₹256 crore.2 On paper it looked like a strange combination: a travel and forex business buying a staffing firm. In practice, Watsa was using the listed Thomas Cook vehicle as a holding company. Fairfax's thesis was that the Indian non-banking services economy had ten or fifteen years of structural compounding ahead of it, and the cheapest way to play that thesis was to back a founder who already understood one piece of it deeply, then hand him capital to acquire the adjacent pieces.

Isaac got his war chest. The "Big Bang" had landed.

III. The M&A Machine: Buying Your Way to the Top

What followed between 2013 and 2020 was one of the most aggressive M&A campaigns in modern Indian corporate history — and almost nobody outside the staffing industry was paying attention.

The strategy, lifted straight from the playbook that built American consolidators like Aramark and ABM Industries, was what bankers call "string of pearls." Don't pay up for a single transformative acquisition. Instead, buy small, buy adjacent, buy at sensible multiples, and use shared services, shared sales teams and shared compliance infrastructure to extract synergies the seller couldn't. Do that often enough and the conglomerate becomes worth substantially more than the sum of what you paid.

The first big move under the new ownership was less an acquisition than a rebrand. In 2014, IKYA was renamed Quess Corp, signalling the shift from a single-line recruitment firm to a multi-product business services platform. Then came the deals — into IT staffing, into facility management, into engineering services, into telecom infrastructure maintenance. By the time Quess went public in 2016, it was already operating across five distinct verticals and bringing in roughly ₹3,400 crore in annual revenue.

The IPO itself was a coming-out party. The book opened on June 29, 2016 with a price band of ₹310 to ₹317 and a target raise of around ₹400 crore.3[^4] When the subscription window closed, the issue had been oversubscribed 144 times — the highest level of subscription for any Indian IPO in nine years.[^4] On listing day, July 12, 2016, the stock opened on the NSE at ₹500, a 58% premium to issue.3 Quess had arrived in the public markets as the rare Indian company growing 50%+ annually without burning cash, and it had the Fairfax brand stamped on it for credibility. The Watsa fingerprint mattered: foreign institutional investors who would never have looked twice at an Indian staffing firm gave it the benefit of the doubt because of who the anchor was.

Then the M&A machine really opened up.

In February 2018, Quess paid roughly $14 million — about 0.5x trailing revenue — to acquire the India, Middle East and Southeast Asia operations of Monster.com from ランスタッド Randstad, which had picked up the global Monster business a few months earlier and immediately decided the APAC piece wasn't strategic.4 On paper, the deal looked like Quess buying a dying asset cheap. Monster had been losing share for years to LinkedIn at the white-collar end and to Naukri at the Indian mass-market end. The job-board business model — charge employers to post listings, sell candidates a premium profile upgrade — was clearly under attack from social-graph-based recruiting.

What Quess was actually buying was data. Monster's APAC database held tens of millions of resumes, search histories, application patterns and salary benchmarks across markets where there was no real digital incumbent. Layered on top of Quess's existing staffing operation, the database became a sourcing engine for the parent. Whether it could ever recover as a standalone product was a separate question — one the company would not answer until November 2022, when it rebranded the entire international footprint as foundit and re-pitched it as a data-driven talent platform aimed at recruiters rather than a job board aimed at candidates.7

A year after Monster came Allsec Technologies. In April 2019, a Quess subsidiary called Conneqt Business Solutions paid for a 61.35% controlling stake in Allsec — buying 35.35% from the founding promoters and 26% from カーライル Carlyle's Mauritius vehicle.5 Allsec was a different animal entirely from anything else in the portfolio. It was a niche BPM firm with two genuinely high-margin product lines: managed payroll services for global enterprises, and customer lifecycle management for financial-services clients. Where general staffing was a 4–5% EBITDA margin business at scale, Allsec was running margins three to four times higher because it was selling software-enabled services rather than raw labour. In 2022, Quess collapsed Allsec into itself entirely via an all-stock merger, removing the minority discount and consolidating the cash flow.6

Slotted in between these big-name deals were the unglamorous ones that actually built the moat. Terrier Security Services brought a fleet of trained guards and the licences required to deploy them at airports, malls and SEZs. Vedang Cellular Services bolted on telecom tower maintenance. Manipal Integrated Services added integrated facility management. CenterQ pulled in dedicated training infrastructure. Each was small. Together, they meant that by 2020 a customer like an इन्फोसिस Infosys campus or a कोटक Kotak head office could outsource almost every non-core function — security, housekeeping, cafeteria, facility maintenance, IT helpdesk, payroll, hiring — to a single counterparty.

The numbers explain why Watsa kept funding the deals. Quess's revenue compounded from around ₹3,400 crore at IPO to over ₹13,000 crore by FY24.[^16] Most of that growth was inorganic, but the organic compound was running double-digits too, driven by the underlying formalisation tailwind. The criticism — and it was a real one — was that the EBITDA margin barely moved. Quess was building scale that looked impressive on a revenue line but never quite translated into the kind of operating leverage you would see at a Recruit Holdings or a Randstad. The bear thesis on Indian staffing kept reasserting itself: it doesn't matter how big you get if the underlying gross margin is structurally pinned at 5–6%.

That tension — scale versus margin, conglomerate versus focus — would eventually force the company's hand. But before it did, there was a leadership transition to navigate.

IV. Current Management & The Governance Pivot

For most of Quess's history, Ajit Isaac was the face of the company. He set the M&A agenda, he sold the story to investors, he closed the deals over dinner. By the early 2020s, with the platform now sprawling across multiple continents and verticals, the question of what came after the founder began to weigh on the board.

The answer, when it came, was less a succession than an evolution. In 2022, Isaac transitioned from Executive Chairman & Managing Director into a non-executive Founder-Chairman role, while Guruprasad Srinivasan — the longtime operations head who had been with the company essentially from day one — was elevated to Executive Director & Group CEO.12

Guruprasad's biography reads almost like a control variable for the founder myth. He was not a star recruit. He was, by his own telling, the fourth person to join the firm. He had spent the previous decade-plus quietly building out the workforce management platform, integrating each new acquisition into a shared services backbone, and standing up the offshore operations centre that processes the payroll for the company's six-figure associate base.12 If Isaac was the deal-maker, Guruprasad was the integrator — and the board's bet was that the next phase of Quess's life required more of the second skill than the first.

That choice signalled a change in the company's centre of gravity. The Isaac years had been about gross addition: more employees, more verticals, more countries, more revenue lines. The Guruprasad era was framed around what the company called "OCF before EBITDA" — Operating Cash Flow as the central performance metric, with the implication that revenue and even EBITDA growth would no longer be celebrated if they did not convert into cash on a sensible timeline. For a staffing business, where working-capital intensity (employees get paid weekly or monthly, customers pay in 60 to 90 days) is the single biggest determinant of whether the model actually compounds value, this was not a cosmetic change. It was a discipline.

Behind both men sat the most important shareholder in the story. Through Thomas Cook (India) and a related vehicle called Fairbridge Capital, Prem Watsa's Fairfax controlled roughly a third of Quess's equity going into the demerger.[^16] That stake had been built at an average cost so far below the public market price that, on a mark-to-market basis, Quess was already one of the best India bets Fairfax had ever made. But Watsa is not a trader. The Fairfax position had been held for thirteen years through multiple cycles, and the public letters from Fairfax describe Quess less as a stock and more as a permanent pillar of the firm's India platform — sitting alongside बजाज Bajaj Allianz, IIFL Wealth and a clutch of unlisted holdings.

Below Fairfax, the ownership ladder included Isaac himself (still a meaningful holder, with a chunk that came to him originally as part of the 2013 sale and that had since been added to through performance ESOPs), a long tail of Indian mutual funds, and a smaller foreign institutional float. Critically, what the cap table did not include was significant retail froth. Quess had never been a retail story stock, and that mattered for the next chapter — because demergers, particularly in India, can be brutal on companies whose retail base does not understand what they are looking at.

The cultural piece was trickier than the cap table. Running a company with more than half a million associates means that no individual employment decision can be made by headquarters. The "Day 1" mentality that Isaac liked to invoke — entrepreneurial, fast, hands-on — fights with the reality of a business where statutory compliance is the entire competitive moat. You cannot move fast and break things when the thing you would break is provident-fund filings for 500,000 people across 28 Indian states. The new management's job, in effect, was to industrialise without bureaucratising — to put the systems in place that let the company scale to a million people without losing the discipline that had got it to half a million.

That set of constraints — operational efficiency, cash discipline, governance maturation — was the prologue to the bigger structural call that came in early 2024.

V. The "Hidden" Businesses & Segment Analysis

To see why the conglomerate eventually had to be unbundled, it helps to walk through what was actually inside it. By the early 2020s Quess was running three quite different businesses under a single ticker, and they had less in common than the org chart suggested.

The first and largest was Workforce Management — the descendant of the original IKYA business. This was the engine: general staffing, IT staffing, telecom-skilled workforce and a small recruitment placement business, all built around the same underlying capability of payrolling associates on behalf of customers. As of FY25 the segment carried more than 500,000 associates and accounted for the bulk of consolidated revenue.11[^15] The margin profile was exactly what you would expect from labour arbitrage at scale: gross take rates of a few percent on revenue, EBITDA margins compressed by mandatory statutory contributions, and a working-capital cycle that ate cash whenever growth accelerated. What made it defensible was not pricing power — there is no pricing power in supplying a contract IT engineer to a customer who also has bids from टीमलीज TeamLease and सीआईईएल CIEL HR — but data and compliance. Quess knew, better than almost anyone, what every category of skilled and semi-skilled labour cost in every Indian district, and it could deploy a new associate compliantly within days where competitors took weeks.

The second business, which the company called Global Technology Solutions (GTS), was the high-margin secret. This was where Allsec, the BPM acquisitions, the HR outsourcing operations and the technology platforms lived. Within GTS sat three roughly distinct sub-segments: BPM and customer lifecycle management (call-centre operations for global financial institutions and telcos); HR outsourcing (managed payroll, statutory compliance and employee benefits administration for enterprise customers); and Insurtech (back-office processing for general and life insurance companies). The combined gross margin profile of these businesses was multiples of the staffing segment, but the segment was much smaller in absolute terms — meaning that whenever group-level investors looked at Quess they tended to see the workforce numbers and ignore the GTS economics.

The third was Operating Asset Management (OAM) — एकीकृत सुविधा प्रबंधन integrated facility management. This is the physical-world business. Security guards, housekeepers, pantry staff, soft services, integrated facility management contracts for tech parks and corporate campuses, industrial services for manufacturing customers and a growing food-services arm. The Indian IFM market is enormous and structurally underpenetrated — most large facilities still run a Frankenstein of single-trade contractors rather than a single integrated provider — but it is also intensely competitive, with multinational majors like सोडेक्सो Sodexo, ISS and Compass on one side and dozens of regional sub-scale Indian operators on the other.

Sitting alongside these three were two product-led "dark horses" that the company hoped would punch above their weight. DigiCare is Quess's after-sales electronics service network, doing in-warranty and out-of-warranty repairs for global consumer-electronics brands across India. The unit-economics story here is genuinely interesting: every smartphone, laptop or appliance sold in India needs a warranty service backbone, very few brands want to build one themselves, and Quess has the physical footprint and trained technicians to be the white-label partner of choice. The second dark horse is foundit, the rebranded Monster business, which the company is repositioning as an AI-driven talent platform competing in the recruiter-tooling layer rather than the job-board layer.7 If either of these scales as planned, it changes the consolidated margin profile materially. If they don't, they are rounding errors.

The deeper investor problem with this structure was not that any one of the segments was bad. It was that no single equity investor could plausibly want to own all of them at the same price. A staffing specialist looking at the Workforce Management segment was paying a multiple set by the GTS earnings. An IFM specialist looking at OAM was paying a multiple set by the staffing earnings. A tech-services investor looking at GTS was paying for facility-management exposure they didn't want. Every shareholder was, in effect, getting two-thirds of a business they hadn't asked for, and the market was applying a conglomerate discount to express its discomfort.

That is exactly the trapped value the next chapter was designed to unlock.

VI. The Great Demerger: Unlocking the Sum-of-the-Parts

The announcement came on a Friday evening in early 2026 — sorry, early 2024. On February 16 of that year, Quess Corp filed with the exchanges that its board had approved a "composite scheme of arrangement" to demerge the company into three separately listed entities.813 The continuing entity would retain the Quess Corp name and the workforce management business. A second listco, eventually named Digitide Solutions, would absorb the GTS portfolio: BPM, HRO, insurtech and the foundit platform. A third, eventually named Bluspring Enterprises, would consolidate the OAM businesses — facility management, security, food services, industrial and telecom infrastructure.

Existing shareholders would receive, for every share of pre-demerger Quess Corp, one share each in Digitide and Bluspring on top of their continuing Quess share. The structure was designed to be exactly 1:1:1 so that nobody could complain about valuation arbitrage between the new entities.

The why was simple and had been telegraphed for years. The company's own investor materials had been describing each of the three businesses as having "distinct customer journeys, distinct capital intensity profiles and distinct go-to-market motions." That is corporate-speak for: these don't really belong together, and we know it. The conglomerate discount was real and visible — peers in pure-play IFM were trading at one multiple, peers in pure-play BPM at another, peers in pure-play staffing at a third, and the blended Quess multiple sat below the weighted average of the three.

Watsa, the anchor shareholder, blessed it. In effect, the demerger was a controlled experiment in Indian capital markets. If the three baby companies, sized appropriately and pitched to specialist investors, traded collectively at a meaningful premium to where the conglomerate had been, the trade vindicated thirteen years of M&A: the parts were always more valuable than the sum, and you needed the holding-co structure to assemble them and then needed to dissolve it to harvest the value. If they didn't, the conglomerate discount argument was a myth and Quess had spent fifteen months of management attention and tens of crores in transaction costs to prove nothing.

The execution took fourteen months, which is fast by Indian regulatory standards. The National Company Law Tribunal's Bengaluru bench approved the composite scheme on March 4, 2025.9 The record date for share allotment in the new entities was set for May 15, 2025.10 And on June 11, 2025, Digitide Solutions and Bluspring Enterprises began trading on the NSE and BSE — Digitide opening at ₹245 and Bluspring at roughly ₹87 per share.10

The leadership stack was reshuffled accordingly. Guruprasad continued to lead the continuing Quess Corp entity. Each of the new listcos got its own CEO, its own CFO and its own dedicated board, with cross-directorships kept light so each company could develop a distinct investor identity. Fairfax, through Thomas Cook, ended up as a major anchor in all three.

In the language of the Acquired Playbook this was a textbook simplification trade — taking a complex, lumpy multi-business structure and giving each component a clean equity story, a clean cap table and a clean P&L. Whether it pays off in shareholder return depends on what each of the three baby companies does next. But the strategic logic — that an Indian conglomerate trading at a discount can sometimes be worth more dead than alive — is one that more Indian holding structures will probably copy in the years ahead.

That brings us to the harder question. Now that the structure is clean, what are the actual sources of competitive advantage that Quess (and its two siblings) carry into their independent lives?

VII. Playbook: 7 Powers and Porter's 5 Forces

The temptation with a sprawling, post-demerger holding structure is to use a different framework for each entity. But the moats — the actual durable sources of advantage — are remarkably consistent across the three. Walk through Hamilton Helmer's 7 Powers and Michael Porter's classic Five Forces, and the same handful of themes keep showing up.

Scale economies. This is the headline power, and the only Indian staffing competitor that comes close to matching it on volume is टीमलीज TeamLease Services. When you employ 500,000 people in a country with 28 state-level labour regimes, your per-employee cost of statutory compliance is dramatically lower than a competitor employing 50,000 people. The same shared services centre that files provident-fund returns for one customer files them for two thousand. The same vendor management software that tracks one client's contract workers tracks every client's. None of this matters at small scale, but at Quess's scale it translates into a structural unit-cost advantage of several hundred basis points over sub-scale competitors. Crucially, the scale economy compounds: every new customer adds compliance volume without adding much compliance cost.

Switching costs. This is the quieter, more important power. Once Quess is running your payroll, your security, your housekeeping and your IT helpdesk under integrated SLAs, "ripping and replacing" the relationship is not a procurement decision — it is an operational nightmare that requires re-onboarding several hundred contract workers, re-mapping statutory filings, re-issuing identity cards and access credentials, and absorbing weeks of operational risk. Customers who have integrated Quess across multiple service lines (and the company has been steadily moving customers up the integration curve) almost never churn the bundle, even when they renegotiate the price. The numbers bear this out: in segments where Quess has multi-service penetration, customer tenure stretches well past a decade.

Counter-positioning. A subtler power, but real. Multinational staffing majors like Randstad, Adecco and Manpower could in theory build out the same India platform Quess has built, but they would have to accept Indian-style margins on top of their global cost base. They don't, which is why Randstad sold the Monster APAC assets to Quess in the first place. The Indian-listed conglomerate is structurally cheaper to operate than the Indian subsidiary of a global multinational, and that asymmetry shows up in win rates on large RFPs.

The other 7 Powers — cornered resource, branding, network economies, process power — are present in varying degrees but not load-bearing. Quess doesn't own a unique resource; the company doesn't really have brand pricing power (staffing customers are coldly transactional); network economies are visible only in the foundit data layer, and even there only marginally. Process power — institutional knowledge of how to onboard 5,000 associates a week across India — is real but imitable over time by anyone willing to invest a decade of operational learning.

Now flip to Porter:

Bargaining power of buyers is the perennial overhang in core general staffing. Large enterprise customers know exactly what the cost-to-company of a contract worker is, and they will compress the staffing margin as hard as they can. In specialised IT staffing, in BPM and in HRO, buyer power is materially weaker because the switching cost is higher and the supplier is selling expertise rather than bodies.

Bargaining power of suppliers — which in this industry means the workers themselves — is rising. India is gradually formalising not just employment but worker representation, and labour-market tightness in skilled categories (IT, engineering, healthcare) is increasing. That is a margin pressure that did not exist a decade ago.

Threat of new entrants is structurally low at scale. You cannot wake up tomorrow and decide to compete for a 500,000-associate national contract; the compliance machinery alone takes years to build. But at the small-customer, single-city, single-service end of the market, entry is trivially easy, which is why Indian staffing has thousands of sub-scale competitors.

Threat of substitutes is the most interesting force. Automation, robotic process automation, AI-driven customer service and self-service HR platforms all chip away at parts of the addressable market. Quess's response has been to lean into the substitute — the foundit AI repositioning, Allsec's automated payroll product, DigiCare's diagnostic tooling — rather than to defend the labour-arbitrage moat to the death.

Industry rivalry is intense in every segment. The good news for Quess is that scale and integration make it the rational acquirer or partner whenever a smaller competitor decides to consolidate.

The one or two or three KPIs that actually matter for tracking Quess's ongoing performance, in this writer's view, are the headcount in the Workforce Management segment, the operating cash flow conversion (OCF as a percentage of EBITDA), and the segment-level revenue split between general staffing and the higher-margin specialised verticals. Headcount tells you whether the formalisation tailwind is still at the company's back. OCF conversion tells you whether growth is value-accretive or working-capital-financed. The revenue mix tells you whether the company is climbing the value chain or stuck at the bottom.

With the framework in hand, we can stress-test the future.

VIII. Myth vs Reality, and the Bear vs Bull Case

Before the cases, three pieces of consensus narrative are worth fact-checking, because they shape how the market values this entire complex.

Myth: Quess is "just a staffing company." Reality: even before the demerger, less than half of operating profit came from pure-play general staffing. The high-margin GTS segment — now spun out as Digitide — was already contributing a disproportionate share of EBITDA. Investors who valued Quess as a staffing pure-play were systematically underestimating the BPM and HRO businesses sitting inside it.

Myth: The Fairfax stake means Quess is "controlled" by Watsa. Reality: Fairfax's stake is roughly a third on a look-through basis and is held primarily through Thomas Cook (India), itself a listed entity with its own minority shareholders. Watsa has been a patient, non-interfering anchor for thirteen years and has explicitly favoured giving the operating team running room. There is no evidence in the company's filings or in Fairfax's annual letters that Quess has ever been managed for the convenience of its largest shareholder.

Myth: The demerger is a value-unlocking magic trick. Reality: demergers move accounting boxes around; they do not change underlying cash flow. Whether the three baby companies trade at a sum-of-the-parts premium depends entirely on whether specialist investors actually emerge for each of them. India does not have the deep ecosystem of staffing-only or facility-management-only institutional investors that exists in North America, and that ecosystem will need to develop in parallel for the demerger thesis to fully play out.

With that out of the way, the cases:

The bear case starts with margin. The structural EBITDA margin in Indian general staffing has been pinned in mid-single digits for a decade, and there is no obvious reason it will expand. Every percentage point of statutory cost (provident fund, employee state insurance, gratuity, bonus, leave encashment) that the central government adds to the formal-sector cost stack lands on Quess's gross margin first. The November 2025 rollout of India's four new labour codes — consolidating 29 central labour laws into a single framework — adds compliance burden, expands worker coverage to include gig and platform workers, and mandates that platform aggregators contribute 1–2% of annual turnover to a social-security fund.1415 In the short run that is unambiguously cost-additive for the staffing industry, even if the formalisation trend it accelerates is long-run positive for Quess.

Add to that the execution risk of running three newly independent companies, each with its own CEO who has to learn to be a public-company chief. Add the working-capital intensity of a business model that pays employees weekly and collects from customers in 60–90 days. Add the possibility that the foundit turnaround simply doesn't work, leaving the platform as a slowly bleeding cost centre inside Digitide. Add the risk of customer concentration in the BFSI and IT-services verticals that buy most of the staffing spend. Each of these is survivable in isolation. Stacked, they describe a business that is much more fragile than its headcount might suggest.

There is also a softer governance overlay. Indian listed companies that grow through serial M&A almost always accumulate goodwill on the balance sheet faster than they generate operating cash flow, and Quess is no exception. The auditor signals over the last several years have been clean, but the magnitude of intangibles relative to tangible book value is the kind of thing that turns into a discussion topic in any market drawdown.

The bull case is the structural one. India has roughly 500 million workers and the formalisation rate is still under 25%. Every additional ten percentage points of formalisation is, in effect, the creation of an entirely new addressable market for someone like Quess. There is no obvious second player at the same scale, and there is no obvious foreign player with the appetite or India-specific operating capability to build to that scale from scratch. The labour codes that look like a near-term cost burden are simultaneously a long-term moat: every regulatory change that raises the cost of doing things informally pushes more customers into the formal-staffing pool. The largest competitor in pure-play labour, TeamLease, is roughly half the size by headcount and lacks the integrated GTS and OAM adjacencies.

The bull case also rests on the GTS / Digitide story doing what the parent company always promised it would. If Allsec's managed-payroll platform scales into the global mid-market, if the BPM business converts its enterprise wins into multi-year annuity contracts, and if foundit even partially recovers a meaningful share of the recruiter-tooling market in Southeast Asia, the standalone Digitide multiple could expand significantly. Bluspring, the IFM entity, has a quieter but similar setup — JLL and सीबीआरई CBRE research has long suggested the Indian integrated facility management market is several times larger than the current spend, with most growth coming from bundled multi-service contracts.

Compared with global peers, Quess sits in an unusual valuation zone. The global staffing majors — Randstad, Adecco, ManpowerGroup — trade on relatively muted multiples reflecting their mature, low-growth Western markets. リクルート Recruit Holdings, the Japanese parent of Indeed and Glassdoor, trades at a richer multiple reflecting its tech-platform mix. Indian peers like TeamLease and SIS sit somewhere in between. Quess, post-demerger, is in effect three different bets that have historically been priced as one — which is exactly why the structural simplification mattered.

The Acquired-style verdict on the 2013 Fairfax investment writes itself: it has been one of the most patient, highest-conviction India platform bets any foreign investor has made in the past two decades. Whether that history extends another decade depends on how cleanly the three resulting entities execute on their separate strategies, and on whether the underlying Indian formalisation tailwind continues to do for them what it has done for the previous thirteen years.

IX. Outro & Further Reading

The story of Quess Corp is, in the end, a story about a particular kind of complexity that doesn't get nearly enough airtime in business journalism: the complexity of moving very large numbers of people through formal-economy plumbing in a country that is still inventing that plumbing. It is not a glamorous business. There is no consumer brand at the end of it. There is no product on a shelf. There is just a half-million-strong workforce showing up every morning at someone else's office, doing the work, and getting paid through Quess's payroll engine and statutory filings.

What Ajit Isaac and Prem Watsa built over the last thirteen years, and what Guruprasad Srinivasan now inherits, is essentially a piece of India's economic infrastructure — one that is large enough, integrated enough and compliant enough that the country's largest enterprises have effectively outsourced a meaningful slice of their workforce administration to it. The 2025 demerger has unbundled that infrastructure into three cleaner equity stories, and for the first time investors can look at the Indian staffing thesis, the Indian BPM thesis and the Indian facility-management thesis as discrete bets rather than as a single tangled holding.

The interesting parts of the next chapter are not really about the parent ticker anymore. They are about whether Digitide can convince the market to value it as an HRO and BPM platform rather than as a staffing spin-off. They are about whether Bluspring can consolidate the fragmented Indian IFM market the way Aramark and ABM did in North America. They are about whether the continuing Quess Corp entity can keep adding hundreds of thousands of associates to its workforce platform without seeing its already-thin EBITDA margin compress further under the weight of the new labour codes.

And in the very background, behind all three, sits the same compounding question that has driven the story from the beginning. How much of India's labour force will end up on a formal payroll in the next decade — and how much of that flow will end up running through pipes that say "Quess" on them.

References

References

-

Thomas Cook India to buy majority stake in IKYA Human Capital for Rs 256 cr — Business Standard, 2013-02-05 ↩↩

-

Quess Corp lists at 58% premium to issue price — Business Standard, 2016-07-12 ↩↩

-

Quess acquires job listing portal Monster's business units for $14 million — Business Standard, 2018-02-01 ↩

-

Quess Corp acquires Allsec Technologies — Crunchbase, 2019-04-18 ↩

-

Allsec Technologies to merge with Quess Corp in an all stock deal — Business Standard, 2022-06-22 ↩

-

Monster.com rebrands to foundit — Deccan Herald, 2022-11-23 ↩↩

-

Quess to demerge into 3 entities — Quess, Digitide, Bluspring — HRKatha ↩

-

Quess Corp gains 6% on NCLT approval for three-way demerger — Business Standard, 2025-03-07 ↩

-

Digitide Solutions, Bluspring Enterprises debut after Quess Corp demerger — Business Standard, 2025-06-11 ↩↩↩

-

Exclusive: Ajit Isaac on Quess Corp's three-way split and future strategy — Moneycontrol, 2024-02-19 ↩

-

India's Labour Codes — Ministry of Labour and Employment, Government of India ↩

-

Labour Reforms Driving Structural Shift In India's Gig Hiring, Says Quess Corp CEO — ScanX ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube