Quality Power: The Quiet Architect of the Global Energy Transition

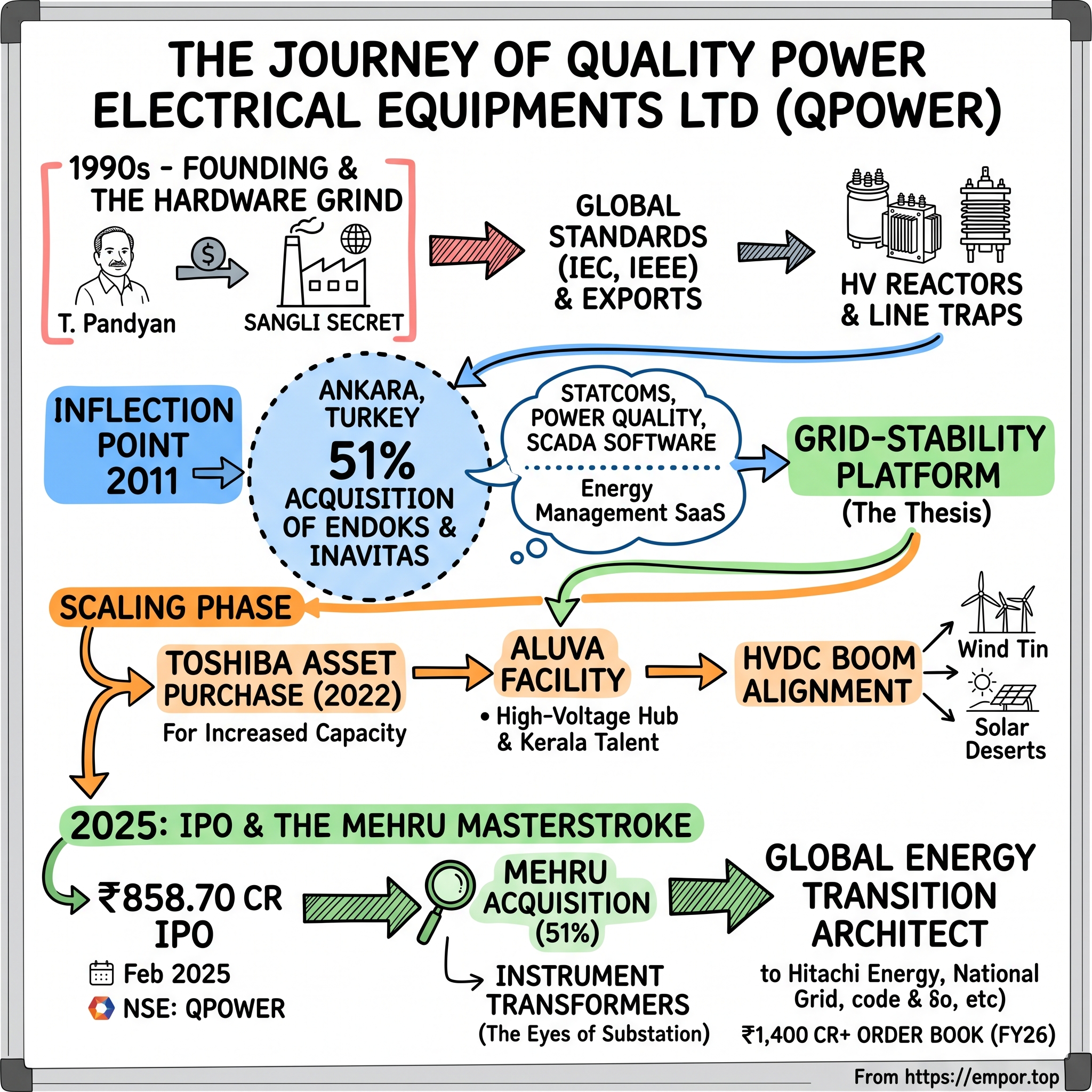

I. Introduction: The Sangli Secret

Drive four hours south-east from Mumbai, past the sugarcane fields and the dusty service stations of महाराष्ट्र Maharashtra's Krishna river belt, and you arrive in सांगली Sangli — a town the rest of India mostly forgets exists. Sangli is famous, locally, for turmeric auctions and a centuries-old wrestling tradition. It is not famous for anything resembling power electronics. There is no IIT here. There are no venture capitalists. The nearest international airport requires a four-hour drive. And yet, tucked inside the कुपवाड MIDC Kupwad MIDC industrial estate on the outskirts of the town, is a factory whose copper-wound reactors and air-core coils end up inside some of the most complex high-voltage power projects on earth — the multi-billion-dollar HVDC interconnectors that stitch together the wind farms of the North Sea, the solar deserts of Texas, and the data-centre clusters of Frankfurt.1

The hook here is not just geographic improbability. It is that क्वालिटी पावर इलेक्ट्रिकल इक्विपमेंट्स लिमिटेड Quality Power Electrical Equipments Ltd (NSE: QPOWER) — a family-run business that most Indian retail investors had never heard of before February 2025 — exports the majority of what it builds, ships into more than 100 countries, and sits on the supplier panels of utilities like नेशनल ग्रिड National Grid, Hitachi Energy, and the Tier-1 HVDC integrators that European and American grid operators outsource to.1[^2]

This is not a story about a transformer company. That is the first cognitive trap. Walk into the Sangli plant and yes, you will see hot oil tanks, copper winding lathes, and the unmistakable smell of impregnated cellulose paper that anyone who has been inside a power-transformer plant knows. But walk through to the back, into the test bay, and you find something almost no Indian peer of comparable size has: a 24/7 SCADA wall, real-time telemetry streaming back from STATCOM स्टैटकॉम units installed in Australia, the Philippines, and Turkey, and software engineers from Endoks in Ankara watching grid-stability metrics on the other side of the world. The thesis of this episode is that Quality Power — QPEEL, as it is known on its own letterhead — is not a "dumb iron" hardware vendor. It is a software-enabled grid-stability platform that happens to have spent thirty years mastering the very specific, very unforgiving hard-tech of high-voltage reactors.

That bifurcation — hardware in Maharashtra and Kerala, software and power electronics in Turkey — is what makes QPEEL one of the more interesting industrial bets to come out of India this decade. The world is moving, fast, from steady spinning-mass generation (coal, gas, hydro) to volatile inverter-based generation (solar, wind, batteries). Every gigawatt of renewables that gets plugged into a grid creates a corresponding need for grid-conditioning equipment to keep voltage stable and frequency synchronised. Reactors smooth out current. STATCOMs absorb or inject reactive power on millisecond timescales. HVDC links move bulk power between asynchronous regions. These are not glamorous products. They do not sit on Apple keynote slides. But without them, the भारत Bharat-to-Germany-to-Texas energy transition simply does not work.

QPEEL has positioned itself, deliberately and patiently across nearly two decades, at the chokepoint where these three product lines converge. And in February 2025, after years of quiet compounding inside private ownership, the Pandyan family finally took the company public.[^2] The remainder of this episode is the story of how a Sangli-based workshop became a critical-path supplier to the global grid — and why the most interesting parts of its business are the ones most investors are currently mispricing.

II. Founding & The Hardware Grind (1990s–2010)

To understand QPEEL, you have to understand थलवैदुराई पांडियन Thalavaidurai Pandyan — and to understand him, you have to understand the very specific universe of mid-2000s Indian electrical manufacturing, which was a dispiriting business to be in if you wanted to build anything globally competitive. The state electricity boards — the SEBs — were the only meaningful buyers. Their tenders were L1-driven, meaning the lowest bidder won regardless of quality. Margins were single-digit. Payment terms were ruinous. And the political economy of it all encouraged exactly the wrong kind of competition: aggressive under-bidding, weak product specifications, frequent failures in the field, and an entire ecosystem of mid-tier manufacturers content to recycle the same 1970s designs as long as the SEB cheques eventually cleared.

Pandyan, a Tamil engineer who had spent years in the trenches of Indian transformer manufacturing, decided very early that this was not the business he wanted to build. The company that would eventually be incorporated in 2001 as Quality Power Electrical Equipments Private Limited was founded on a principle that, in retrospect, sounds obvious but at the time was almost heretical inside the Indian electrical sector: build to global IEC and IEEE standards from Day One, even if your immediate Indian customers do not require it; chase exports even if the rupee margin per kilogram of copper looks worse on a one-year view; and refuse, categorically, to enter the commodity distribution-transformer market where everyone else was bleeding.1

The first product moat was reactors. Reactors are the unsung workhorses of any modern grid — coils of copper that "choke" or absorb current to control fault levels, smooth out harmonics, and stabilise voltage. They are not interesting to look at. They are not, on the surface, hard to make. But the design tolerances at high voltages (220kV, 400kV, and above) are brutal. A miscalculation of a millimetre in the magnetic flux path can cause a coil to overheat catastrophically in service, taking down a substation and triggering cascading regional blackouts. Most Indian manufacturers stayed away from high-voltage reactors because the risk-reward was unforgiving: one warranty failure could wipe out a year of margin. QPEEL went the other way and made it the core competency. By the late 2000s, the company was credibly being described inside the industry as one of the four largest medium-voltage air-core reactor manufacturers in the world.2

Alongside reactors came Line Traps — wave-trap coils that block carrier-frequency communication signals from leaking out of high-voltage transmission lines. Line traps are deeply, almost comically niche. They are also indispensable: every modern HV transmission substation needs them, and there are perhaps five or six companies on earth qualified to make them at scale. By picking products like reactors and line traps — high-voltage, low-volume, high-engineering-content, high-switching-cost once installed — Pandyan was effectively running the same playbook that hidden-champion German Mittelstand companies had run for decades: dominate a niche too small for Siemens or ABB to bother with but too technical for low-cost commodity competitors to enter.

The decision to chase exports from a town with no port, no airport, and a four-hour road to either was itself a tell. Most Indian electrical companies of this era were addicted to the comfortable, slow-paying domestic SEB pipeline. QPEEL spent the 2000s grinding out CPRI test certifications, KEMA approvals from the Netherlands, and IEEE qualifications in the United States — the bureaucratic prerequisites without which no Tier-1 utility on earth will let you bid on their tenders.1 This took years, and the financial returns during the period were, by all accounts, modest. But by the end of the decade, Quality Power had something almost no Indian peer had: a credible export channel into Europe, Southeast Asia, and the Gulf, and a customer file that included the major Western OEM-integrators who themselves sold into utilities like Electricité de France EDF and Tennet.

By 2010, the company had a defensible hardware niche and a respectable export book. What it did not have — and what every conversation with the leadership team at the time apparently kept circling back to — was software. The grid was about to change, fundamentally, and selling iron alone was not going to be enough.

III. The 2011 Inflection Point: The Endoks Acquisition

The deal that changed everything was not announced with a press conference. There was no investment banker pitch deck floating around Mumbai. There was no Bloomberg headline. Sometime in 2011, a relatively obscure private Indian company from Sangli quietly bought 51% of a relatively obscure private Turkish company in Ankara called Endoks Enerji Dağıtım Sistemleri.13 To anyone watching from the outside, this looked bizarre. Why would an Indian reactor manufacturer with no obvious international M&A track record buy into a Turkish power-electronics firm? Why Turkey? And — for a company whose revenues at the time were modest — what was the strategic logic?

The strategic logic, with the benefit of fifteen years of hindsight, is one of the cleanest pieces of cross-border M&A any Indian mid-cap has executed. Endoks was, and still is, a STATCOM and power-quality specialist. A STATCOM — a Static Synchronous Compensator — is essentially a fast-switching power-electronics module that injects or absorbs reactive power on millisecond timescales to keep grid voltage stable. The technical analogy that works is that of a shock absorber on a car: as the road (the grid) gets bumpier and bumpier with the volatility of solar and wind, you need a faster, smarter, more adaptive shock absorber. Traditional capacitor banks and mechanically switched reactors — the equipment QPEEL had spent the 2000s making — are like 1960s leaf-spring suspensions. STATCOMs are active, software-controlled, microsecond-response suspensions. The grid of the next thirty years cannot run on leaf springs.

By buying Endoks, QPEEL did three things at once. First, it acquired an IP base in power electronics and control software that would have taken a decade and tens of millions of dollars to build organically in India. Second, it acquired engineering talent that simply did not exist at scale in mid-2010s India — Turkish electrical engineers trained in the European tradition, with deep experience integrating renewable plants into the heavily interconnected European grid. And third, it acquired a foothold in the technology stack — SVC (Static Var Compensator), STATCOM, harmonic filter design — that bolted directly on top of QPEEL's existing reactor and capacitor-bank product line. A reactor without a STATCOM is just iron. A STATCOM without reactors is incomplete. Together, they form a grid-conditioning solution that a utility can buy as a package.

There is a contrast worth drawing here. Through the 2010s, plenty of Indian companies bought foreign assets — Tata Motors bought Jaguar Land Rover, Bharti Airtel bought Zain Africa, Hindalco bought Novelis. Some of these deals worked, several did not, and the common pattern was that the Indian buyer was buying scale, brand, or geographic footprint. QPEEL bought something different. It bought R&D and IP. There was no "vanity asset" calculation. The Pandyan family did not put up a billboard in अंकारा Ankara saying that an Indian firm had taken control. They quietly integrated the Endoks engineering team, kept the Turkish brand, kept the Turkish management mostly in place, and started cross-pollinating product roadmaps.

The sleeper inside the sleeper was a software arm. In 2012, the Endoks group spun up Inavitas, a smart-energy management platform that today supplies all 21 Distribution System Operators in Turkey with SCADA, outage management, and power-quality monitoring software.4 Inavitas operates on a SaaS-like Energy Management as a Service (EMaaS) model — recurring software revenue, sticky relationships with utilities, and gross margins that look nothing like the gross margins of stamping out copper-wound reactors. This is the segment most Indian sell-side analysts entirely miss when they model QPEEL, and it is the segment that may, over the next decade, change the multiple the market is willing to assign the consolidated entity.

By the mid-2010s, the strategic geometry was set. QPEEL had a hardware base in India, a power-electronics and software arm in Turkey, and a sales footprint that was now genuinely global. What it needed next was capacity — and the world, conveniently, was about to hand it some at a discount.

IV. The Scaling Phase: Distressed Assets & Market Share

Some of the best industrial businesses are built not by greenfielding fancy new plants but by buying high-quality equipment at distressed prices from sellers who, for one reason or another, want out. The Pandyan family, by all available indication, understood this in their bones. Through the late 2010s and into the early 2020s, while the rest of the Indian electrical sector was either consolidating around a few large players (Siemens India, ABB India, CG Power) or quietly going bankrupt under the weight of post-2014 SEB receivables, QPEEL was doing something different: picking through distressed industrial estates and buying machinery, lines, and occasionally entire companies at cents on the dollar.

The Toshiba transaction is the canonical example. In late 2022, QPEEL acquired manufacturing assets from Toshiba Transmission & Distribution Systems (India) — the Indian arm of Japan's 東芝 Toshiba, which had been struggling for years with its own global restructuring saga.[^6] The transaction was not a full company acquisition. It was a clinical, surgical asset purchase: specific machinery, specific tooling, specific lines that fitted directly into QPEEL's reactor and transformer manufacturing roadmap. The value of this kind of deal is enormous and almost always understated in public reporting, because the alternative — buying brand-new equivalent equipment at list prices from European or Japanese OEMs — would have taken several multiples of capital and roughly two years of delivery lead time. Instead, QPEEL was able to bolt the capacity onto its सांगली Sangli and अलुवा Aluva plants and start cranking out additional units in months, not years.

The Aluva facility itself is worth pausing on. Tucked into Kerala's industrial belt outside कोच्चि Kochi, Aluva became QPEEL's high-voltage reactor and special-application transformer hub. The choice was deliberate: Kerala offers a steady supply of vocational and engineering talent, predictable power infrastructure, port access via Kochi, and — critically — a workforce that has been used to dealing with European and Middle Eastern export documentation for decades. Indian manufacturing strategy is often discussed in macro terms (मेक इन इंडिया Make in India, PLI schemes, etc.). The reality on the ground is far more granular: each plant location is a decision about labour pools, port logistics, and customs-clearance friction, and QPEEL's location strategy reflects a company that has been quietly thinking about export logistics for two decades.

The other side of the scaling story was alignment with the HVDC boom. High Voltage Direct Current — moving electricity not as AC at 50 or 60 hertz but as straight DC at hundreds of kilovolts — is the technology of choice when you need to move bulk power over very long distances, integrate offshore wind, or stitch together asynchronous grids. The HVDC market globally is estimated by BloombergNEF to be heading toward dramatic expansion through the end of the decade, driven by exactly the renewables and data-centre buildouts that are eating the headlines.5 Almost every HVDC project on earth needs reactors — smoothing reactors, filter reactors, harmonic-trap reactors — at voltages and current ratings that perhaps a dozen manufacturers globally are qualified to supply. QPEEL had spent twenty years getting itself onto that list. The Toshiba asset buyout, and parallel capacity expansions at Sangli and Aluva, were the moves that translated that qualification into shipping volume.

By 2024, QPEEL's order book began reflecting this. The company was credibly competing for — and winning — packages on inter-regional HVDC links in India, multi-terminal Voltage Source Converter (VSC) projects in Australia, and FACTS (Flexible AC Transmission Systems) deployments across the Americas, Europe, the Middle East, and Asia-Pacific.6 This is not a small-utility customer base. These are the big leagues, won one painful qualification at a time. And by the time the company was ready to go public in early 2025, it had something most newly listed Indian small-caps do not: a multi-hundred-crore order book of contracts that had already been won, derisked, and were sitting in execution backlog.

The next move would not be a quiet asset purchase. It would be a full-bore capital-markets debut.

V. The 2025 IPO & The Mehru Masterstroke

Indian IPO windows are weird. They open and close on a rhythm that has more to do with foreign-portfolio-investor risk appetite and सेबी SEBI paperwork timelines than with the underlying readiness of the businesses going public. By late 2024, the window for industrial mid-caps was, after years of speculative tech-adjacent listings, finally swinging open. QPEEL filed its Draft Red Herring Prospectus with SEBI on 16 September 2024, walked through the regulatory review in roughly four months, and on 14 February 2025 opened its book for what would become a ₹858.70 crore mainboard IPO — comprising a fresh issue of ₹225 crore and an offer-for-sale tranche of ₹633.70 crore by the promoter family at a price band of ₹401 to ₹425 per share.[^2]7

The structural logic of this issue is more interesting than the headline number. The fresh-issue component, at roughly 26% of the total, was earmarked largely for funding the Mehru acquisition (more on that in a moment) and for working capital. The remaining ₹633.70 crore — the majority — was an OFS by promoters. This is a configuration that some investors instinctively flinch at — "the founders are cashing out!" — but in QPEEL's case it bears closer inspection. Even after the OFS, the Pandyan family retained roughly 74% of the company, and the family's personal financial outcomes remained almost entirely yoked to the stock price.8 The OFS was not an exit. It was a partial monetisation of three decades of illiquid wealth, accompanied by a deliberate decision to bring in public-market investors as a permanent capital base for the next round of consolidation.

The IPO closed on 18 February 2025 with the book subscribed roughly 1.29 times overall — modest by Indian IPO standards but reflecting institutional discipline rather than retail euphoria.7 The stock listed on 24 February 2025 at ₹430, a tepid 1.18% premium to the upper band.7 In a year when several Indian IPOs had popped 40-60% on listing day before grinding lower, QPEEL's quiet listing was, in retrospect, the right kind of debut for an industrial compounder: priced for the cash flows, not for the headlines.

Then came the Mehru deal — and this is where the IPO's strategic intent became transparent. Within weeks of listing, QPEEL announced and closed its acquisition of a 51% stake in Mehru Electrical and Mechanical Engineers Pvt Ltd for ₹120 crore cash consideration, with the Share Purchase Agreement signed back in April 2024 and completion on 6 March 2025.910 Mehru, headquartered in भिवाड़ी Bhiwadi, Rajasthan, is a specialist in high-voltage instrument transformers — current transformers (CTs), potential transformers (PTs), and capacitor voltage transformers (CVTs). These are the sensing elements that sit on every high-voltage substation bay, measuring current and voltage so that protection relays and metering systems can do their work. They are, in technology terms, the eyes of a substation.

The strategic logic was almost embarrassingly clean. QPEEL already built reactors, capacitor banks, line traps, and STATCOMs — the active grid-conditioning hardware. Mehru built the instrument transformers — the sensing layer. Put them together, and QPEEL can now go to a utility or an EPC integrator and bid not just for individual components but for the entire substation electrical package: a complete grid-interconnection solution from one supplier. That is the kind of bundling that wins HVDC and FACTS tenders against the global majors, because it reduces interface risk, simplifies the warranty perimeter, and gives the buyer a single throat to choke when something fails. At ₹120 crore for 51%, the deal implied an enterprise value for Mehru that, on the cursory benchmarks against listed peers like GE T&D India and CG Power, looked reasonable rather than aggressive. Whether it proves a bargain depends on execution — but the strategic positioning of the deal is largely unambiguous.

The signal here, for investors, is what the Pandyan family is using public capital for. They are not declaring special dividends. They are not paying down a non-existent debt pile. They are using the public market as a consolidation vehicle for a fragmented Indian electrical-component sector. That is a very different playbook from the typical Indian mid-cap IPO of the last five years, and it deserves attention.

VI. The "Hidden" Business: Grid-AI & Software

If you were to construct a clean mental model of QPEEL by reading sell-side reports, you would conclude that this is a high-voltage hardware company with a global export footprint and some growing exposure to HVDC. That model is not wrong. It is just incomplete in a way that may matter enormously over the next decade. Because tucked inside the Endoks subsidiary in Ankara is a software business that, by orders of magnitude, has higher gross margins, higher growth rates, and a recurring-revenue profile that looks much more like a B2B SaaS company than like a manufacturing concern.

That business is Inavitas. Established in 2012 as a sister entity to Endoks and now operationally embedded within the QPEEL group, Inavitas builds and operates a smart-energy management platform with deployments spanning all 21 Distribution System Operators (DSOs) in Turkey for power-quality monitoring, SCADA, distribution management, and outage management.4 Its portfolio, per company disclosures, includes monitoring software running on over 2 GW of renewable energy installations.4 R&D and sales offices have been added in India and Australia, riding the QPEEL group's existing customer relationships.

The analogy that makes this segment intuitive is this: if QPEEL's hardware is the body of a Formula One car — the engine block, the chassis, the suspension — then Inavitas is the telemetry system. The telemetry system is what makes the car raceable. It is what tells the pit crew, in real time, what is happening at every corner. In modern grids, that telemetry layer is no longer optional. As inverter-based renewables proliferate, as electric vehicle charging loads spike and crater on minute-by-minute timescales, and as data-centre loads stack hundreds of megawatts behind a single feeder, the ability to monitor and orchestrate the grid in real time becomes a basic operational necessity. The hardware vendor that ships you the iron plus the telemetry stack is, structurally, far more entrenched in the customer's operations than the one that ships you iron alone.

This matters for two reasons. The first is unit economics. Hardware sales for high-voltage reactors are large but lumpy: a multi-crore order books, ships, and is recognised. The relationship pulses in and out depending on the customer's capex cycle. Software-as-a-service relationships, by contrast, are smoother, stickier, and — once a customer's operational workflows have been built around the software — almost impossible to unwind without significant pain. The second reason is multiple. Public markets value SaaS revenue at 8-15x sales depending on growth and retention; they value high-voltage transformer revenue at 2-4x sales. If even a meaningful single-digit-percentage slice of consolidated QPEEL revenue is genuine recurring SaaS, the sum-of-the-parts maths starts to look interesting in a way that flat-multiple analyses miss.

QPEEL has been notably quiet about disclosing Inavitas revenue and margins as a standalone segment. From the company's filings, the software/monitoring business is folded into the broader grid-interconnection solutions category. This is, depending on how cynical one wants to be, either a regrettable lack of disclosure or a deliberate strategic ambiguity to keep competitors from understanding how much of the value sits in the software layer. Either way, it is the segment that long-term investors should watch most carefully over the next two to three reporting cycles. As Inavitas extends from Turkey into India and Australia on the back of QPEEL's existing customer relationships, the segment economics — if they are disclosed cleanly — could materially reframe how this company is valued.

The deeper point is conceptual. QPEEL is not really competing in the "Indian electrical equipment" peer group anymore. It is competing in the global "grid-stability platform" peer group, where the competitors are not other Indian transformer companies but the grid-modernisation arms of Hitachi Energy, Siemens Energy, and Schneider Electric. None of those peers can manufacture air-core reactors as cheaply out of Sangli. None of them have a Turkish software arm that already runs 21 DSO contracts. The shape of QPEEL's competitive perimeter is, slowly, becoming visible.

VII. Management & The Pandyan Dynasty

Spend an hour listening to थलवैदुराई पांडियन Thalavaidurai Pandyan Perumal describe a 400kV reactor design, and a few things become immediately apparent. The first is that he is, in temperament, a working engineer rather than a salesman or a financier. He talks about magnetic flux density and dielectric stress with the easy precision of someone who has spent decades on a factory floor. The second is that his vocabulary about the business is almost entirely operational. Capital allocation, M&A, and equity-market positioning are described in plain, unembellished terms — there is no startup-flavoured marketing language about "transforming the future of energy." There is, instead, a quiet conviction that the company is doing serious work for serious customers and that the customers will keep paying so long as the work remains serious.

His son and co-promoter, भरणीधरन पांडियन Bharanidharan Perumal Pandyan, who serves as Joint Managing Director, brings a different but complementary energy. The technical visionary of the next generation, Bharanidharan is the family member most closely identified with the international acquisitions — Endoks, Inavitas, and the broader software pivot. He is the one who, by all available indications, drove the conviction that QPEEL had to become a power-electronics and software company rather than a pure hardware manufacturer. Together with Chitra Pandyan, the family operates as a tight management unit that, post-IPO, still controls approximately 74% of the issued capital — with Bharanidharan personally holding around 37% as the single largest individual shareholder.8

The incentive structure that this creates is worth dwelling on. The Pandyan family's wealth is, almost in its entirety, locked into QPEEL equity. They draw managerial salaries that, by listed-company standards, are modest. There are no related-party management fees flowing into a sister entity. There are no parallel real-estate or hospitality businesses absorbing promoter attention. The cash flows that the company generates either get reinvested into the business, deployed into acquisitions like Mehru, or — eventually — paid out as dividends to all shareholders pro rata. This is the kind of skin-in-the-game arrangement that most public-market investors will pay a multiple premium for, and it is conspicuously absent in many of QPEEL's Indian listed peers, where related-party transactions, sprawling diversification, and management self-dealing are unfortunate norms.

The cultural choice that shows up most clearly in the company's filings and disclosures is the bias toward engineering talent over commercial talent. QPEEL's R&D and engineering headcount as a proportion of total employees is unusually high for an Indian electrical manufacturer. The Sangli test and research laboratory holds ISO 17025:2017 accreditation, meaning its test data is mutually recognised internationally — a credential that takes years and significant capital to acquire.1 Customer-acquisition is driven, in practice, less by traditional B2B sales than by demonstrable engineering credibility: pass the prequalification, deliver the first unit on spec, deliver the second one early, and the customer's procurement team starts requesting QPEEL by name on subsequent tenders.

Succession is the question every family business eventually has to answer, and QPEEL has answered it about as well as any Indian mid-cap could. The transition from a founder-led workshop to a professionalised, internationally integrated corporation has, by all accounts, been gradual and orderly. The Endoks team in Ankara is run by Turkish managers with operational autonomy. The Aluva and Sangli plants run with deep technical management teams. The Mehru integration is being handled with the same patience that characterised the Endoks acquisition fifteen years earlier. This is a company that has, repeatedly, demonstrated that it can absorb businesses across geographies and cultures without breaking them — a meta-capability that may, over time, be the single most valuable asset on the balance sheet.

VIII. Playbook: Porter's Five Forces & Hamilton's Seven Powers

If you run QPEEL through Hamilton Helmer's 7 Powers framework, the picture that emerges is not of a company with one giant moat but of a company with multiple smaller, mutually reinforcing moats — which, arguably, is the more durable configuration. Take Counter-Positioning first. The global incumbents in grid-conditioning hardware — Hitachi Energy (formerly the ABB Power Grids unit), Siemens Energy, Mitsubishi Electric — operate with European or Japanese cost structures, multi-layered global sales organisations, and gross margins that reflect their incumbent rents. QPEEL counter-positions against them by selling functionally equivalent hardware at lower fully-loaded cost, with software integration thrown in, to mid-tier utilities and EPC integrators who cannot or do not want to pay for the brand-premium kit. The incumbents cannot easily respond without cannibalising their own pricing — the classic counter-positioning trap.

Cornered Resource shows up in two places. The first is the specialised reactor and STATCOM design talent that QPEEL has accumulated across Sangli, Aluva, and Ankara — a workforce that is genuinely difficult to assemble at scale and that competes effectively against far better-funded global peers because the specialism is narrow enough that the global talent pool is small. The second is the regulatory and qualification credentials — the CPRI, KEMA, IEEE, and ISO 17025 accreditations — that take years to acquire and that effectively wall off the market against new entrants. A startup with venture capital cannot conjure a CPRI-certified high-voltage test facility into existence in 18 months.

Switching Costs is the most underappreciated power in QPEEL's profile. Once a utility has commissioned a STATCOM or a set of reactors from QPEEL, integrated the Inavitas monitoring stack into its control room, trained its operators on the interfaces, and validated the equipment through the multi-year warranty and reliability period, the cost of switching to a competitor on the next package is enormous. Not because the hardware itself is proprietary, but because the operational learning, the spare-parts inventory, the relay-protection calibration files, and the operator workflows are all built around the installed base. This is the same dynamic that makes enterprise software so sticky, mapped onto industrial hardware.

Run the same exercise through Porter's Five Forces and the picture is broadly favourable. Barriers to Entry are high — start a high-voltage reactor company from scratch and you will spend several years and tens of millions of dollars before you can credibly bid on a Tier-1 utility tender. Supplier Power is low — copper, electrical steel, insulation materials, and power-electronics components are commodities with multiple sources globally, and QPEEL is vertically integrated in several key sub-assemblies. Buyer Power is moderate — large utilities and Tier-1 OEM integrators have negotiating leverage, but the project-specific qualification dynamics and the multi-year commissioning cycles limit how aggressively they can squeeze. Threat of Substitutes is low in the near term — there is no plausible substitute for reactors or STATCOMs in modern grid architecture, and indeed the substitutes are growing the market (more renewables means more STATCOMs).

The only force that is genuinely tense is Industry Rivalry. In the global grid-conditioning hardware space, the rivalry is rational rather than destructive — incumbents like Hitachi Energy compete on technology and reliability rather than on slash-and-burn pricing — but in QPEEL's adjacent Indian segments (where it bumps up against भारत हेवी इलेक्ट्रिकल्स लिमिटेड BHEL, CG Power and Industrial Solutions, GE T&D India, and the resurgent Siemens India), the competitive intensity is real and the discipline of margin protection becomes important. Mehru's CT/PT segment, in particular, is a competitive space domestically and the integration must produce genuine cross-sell synergies rather than mere headline consolidation if it is to justify the ₹120 crore price tag.

The strategy professor's verdict on QPEEL, by the end of this exercise, is that this is a company sitting in a comparatively well-protected competitive position with multiple reinforcing moats — but one that depends critically on continued execution discipline. The moats are real. They are also defendable only as long as the engineering and operational excellence that built them continues.

IX. Bull vs. Bear: The Investor's Lens

The bull case for QPEEL is straightforward and, at this point in the narrative, almost too easy to articulate. The world is electrifying. Every credible scenario from the IEA, BNEF, and the major grid operators converges on the same conclusion: global investment in transmission and distribution infrastructure will need to roughly double over the next decade to absorb renewable generation, electrify transport and heating, and supply the rapidly growing data-centre load that AI compute is driving.5 The grid-conditioning equipment market — reactors, STATCOMs, FACTS devices, HVDC converters — sits squarely in the path of that capex. QPEEL has demonstrated technical credibility, global qualification, and a manufacturing cost base in India that is structurally cheaper than the European and Japanese incumbents. The Mehru acquisition adds the instrument-transformer layer that converts QPEEL from a component supplier into a substation-package supplier. The Inavitas software arm — currently underappreciated — provides recurring revenue and an entry point into a higher-multiple business segment. The Pandyan family is aligned with minority shareholders, the balance sheet is conservatively managed, and the order book at the close of FY26 exceeded ₹1,400 crore, equivalent to roughly 1.4 times annual revenue, providing meaningful execution visibility.6 If you believe the electrification thesis, QPEEL is exposed to it in a way that few other Indian listed equities can match.

The bear case requires more care. Start with concentration risk. Exports account for the dominant share of QPEEL's revenue — the company has long disclosed an export-heavy profile, with a "One Star Export House" status under India's foreign trade policy and a customer base spanning more than 100 countries.1 That international diversification is a strength when world trade is open. It becomes a vulnerability when it is not. The Trump-era and post-Trump-era tariff regimes, the EU's Carbon Border Adjustment Mechanism, and rising "Buy American" or "Buy European" preferences in utility procurement could, over time, erode QPEEL's cost-advantage entry points into Western markets. A 10-15% tariff applied to Indian-origin electrical equipment landing in the US or EU does not theoretically kill QPEEL, but it absolutely compresses its bidding margin against domestic incumbents.

Second, customer concentration within the export base is opaque. The company does not publicly disclose the share of revenue from its top five or top ten customers, and the project-driven nature of HVDC and FACTS contracts means that the timing of major contract awards can move quarterly revenue by double-digit percentages. This is a classic small-cap industrial volatility profile, and investors who are uncomfortable with lumpy quarterly numbers will struggle to hold the stock through a soft quarter.

Third, execution risk on the Mehru integration is real. Indian mid-cap acquisitions of family-owned electrical manufacturers have, historically, produced wildly mixed outcomes. The cultural integration of a Rajasthan-based instrument-transformer business into a Sangli-and-Ankara-based global hardware-and-software platform is not trivial. The first year of consolidated numbers will need to be watched carefully for signs of margin dilution, integration writedowns, or working-capital absorption.

Fourth, valuation. Following the IPO and the subsequent operational outperformance in FY26 — with revenue crossing ₹1,000 crore for the first time and EBITDA nearly doubling — the stock has been priced by the market with significant assumptions about continued growth and margin durability baked in.6 Whether the current multiple reflects "hidden gem" or "priced for perfection" depends almost entirely on whether the next two to three years deliver the operational execution that the bull thesis requires. The market is rarely patient with industrial mid-caps that miss two consecutive quarters.

The honest synthesis is that QPEEL is a high-quality business sitting in a structurally favourable end-market, with a credible management team and a defensible competitive moat — and that, after the multi-year operational outperformance, the margin for execution error has narrowed. The KPIs that long-term holders should watch with the most discipline are three: (1) the order book and the book-to-bill ratio, which together provide forward visibility on revenue and serve as the leading indicator of competitive positioning in HVDC and FACTS tenders; (2) the consolidated EBITDA margin trajectory, which will tell investors whether the Endoks/Inavitas software mix is materially shifting the blended profitability profile; and (3) the proportion of revenue derived from recurring or service-based contracts (the Inavitas EMaaS segment), which is the single best leading indicator of whether QPEEL is genuinely transitioning into a platform business or remains a hardware company with a software bolt-on.

Myth versus reality is worth one final look. The market narrative around QPEEL has, at times, been that this is a "transformer company." That is a category error. QPEEL is a grid-conditioning and grid-monitoring platform with a hardware backbone, and the meaningful comparable peer group sits in Frankfurt, Zurich, and Tokyo rather than in मुंबई Mumbai. Investors who internalise that framing will think about the company very differently from those who do not.

X. Conclusion & Lessons for Founders

There is something almost old-fashioned about the QPEEL story. In an era of venture-funded, marketing-saturated, narrative-first technology companies, here is a business that spent twenty-five years quietly mastering one of the most unforgiving corners of industrial engineering — and built an export-driven, software-augmented, family-controlled compounder out of a town that almost nobody outside Maharashtra has heard of. The lessons for founders, both in India and elsewhere, are worth stating plainly.

First, geography is a constraint, not a destiny. The conventional wisdom in Indian manufacturing has been that you need to be close to a major port, close to a major airport, close to a major customer cluster, and close to a major talent pool. QPEEL had access to none of these from सांगली Sangli. The company succeeded because it made the constraints of its location irrelevant through deliberate investment in international logistics, internationally recognised certifications, and a willingness to send engineers around the world to install and commission equipment on-site. The geography problem was solved not by relocating but by upgrading the channels through which the geography mattered.

Second, hardware and software are not opposites — they are complements, and the businesses that integrate both win. The Endoks and Inavitas acquisitions were not, in the way that some Indian conglomerates have done, vanity diversifications. They were deliberate, surgical extensions of the hardware franchise into the software layer that the hardware itself was about to require. The lesson for founders is to read the technology trajectory of your end-market early, and to position your company at the intersection of the categories that will converge — not in the comfortable middle of the category you started in.

Third, capital markets are a tool, not a destination. The Pandyan family took QPEEL public at a moment when the company had a multi-year operational track record, an executable acquisition pipeline, and a clear use of proceeds. They did not IPO at the first opportunity, did not chase the highest possible valuation, and did not use the listing as a personal exit. They used it as a consolidation platform. That is the right way to use the public markets for a multi-decade compounder, and it is the playbook that founders who think in decades rather than quarters should study.

Fourth, the unglamorous problems are often the most defensible ones. Reactors are not interesting. Line traps are not interesting. Capacitor voltage transformers are not interesting. But every credible energy-transition scenario needs them in enormous quantities, and the supplier base that can deliver them at global quality is small. The best long-term competitive positions are often built in the corners of the industry where nobody is paying attention, until suddenly everybody is.

The final reflection, then, is that QPEEL is a counterexample to the prevailing belief that "Old Economy" manufacturing cannot generate new-economy growth profiles. It can. The grid is the most important piece of physical infrastructure being rebuilt over the next two decades, and the companies that supply its connective tissue — the iron, the silicon, and the software — will, almost regardless of macro cycle, find themselves on the right side of the most consequential capex wave of our lifetimes. From a small industrial estate on the outskirts of Sangli, the Pandyan family has built a company that sits squarely on that wave. Whether the next decade rewards them as fully as the last has remains to be written. But the foundations, by any honest reading of the corporate evidence, look unusually well-laid.

References

References

-

About Us — Quality Power Electrical Equipments Limited ↩↩↩↩↩↩↩

-

Endoks Enerji — Power Quality and Energy Management Solutions ↩

-

High Voltage Direct Current (HVDC) Market Outlook — BloombergNEF ↩↩

-

Quality Power Equipments closes FY26 with Rs.1,400 crore-plus order book — T&D India ↩↩↩

-

Quality Power acquires 51% stake in Mehru Electrical — Business Standard, 2025-03-07 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube