PVR INOX: The Emperors of the Indian Big Screen

I. Introduction and The Thesis

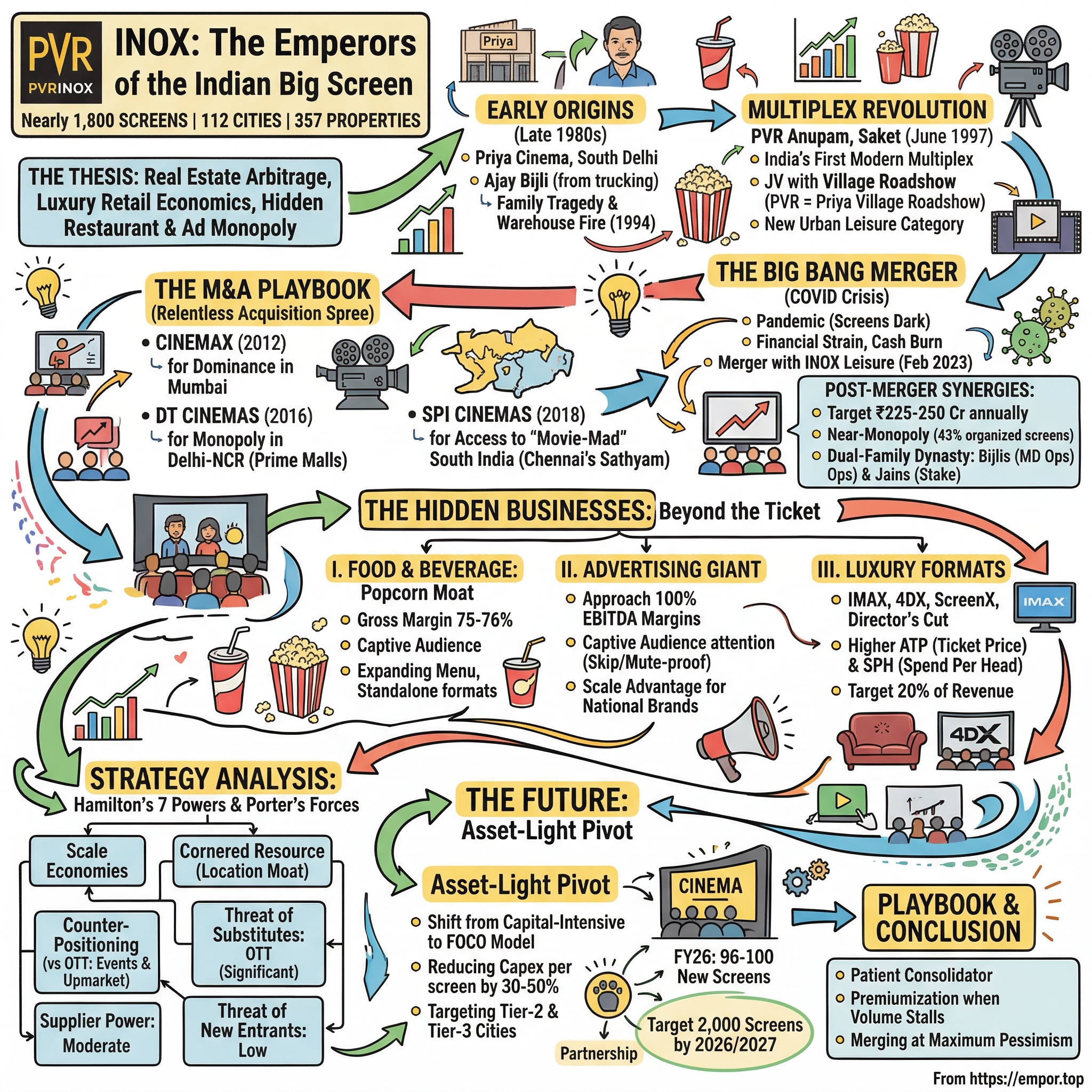

How does a single-screen theater in South Delhi become the fifth-largest cinema chain in the world? That is the question at the heart of this story, and the answer has almost nothing to do with movies.

PVR INOX Limited, listed on the NSE and BSE under the symbol PVRINOX, operates nearly 1,800 screens across 357 properties in 112 cities spanning India and Sri Lanka. It is a company that most people associate with popcorn and Bollywood blockbusters. But peel back the curtain and something far more interesting emerges. This is a story about real estate arbitrage, luxury retail economics, and what happens when you hide a restaurant business and an advertising monopoly inside a movie theater.

The Indian cinema exhibition industry is unlike any other in the world. India sells more movie tickets annually than any country on Earth, roughly four billion admissions in a good year, yet revenue per screen is a fraction of what American or European exhibitors generate. The country has approximately 10,000 screens for a population of 1.4 billion, compared to roughly 45,000 screens in the United States serving 330 million people. That gap, the vast gulf between ticket volume and monetization per patron, is the canvas on which PVR INOX painted its empire.

The narrative breaks into three acts. First, the multiplex revolution of the late 1990s and early 2000s, when a trucking family's son bet everything on changing how India watched movies. Second, the relentless acquisition spree that killed regional competition and created a national champion. And third, the "Big Bang" merger with INOX Leisure during the existential crisis of COVID-19, a deal that was part survival pact and part strategic masterstroke that created a near-monopoly in organized Indian cinema exhibition.

But before all of that, there was a cinema called Priya, a family tragedy, a warehouse fire, and a young man who had no idea he was about to reshape an industry.

II. Founding and The Priya Origins

Picture South Delhi in the late 1980s. Vasant Vihar, one of the capital's leafy, upscale neighborhoods, is home to a modest single-screen cinema called Priya. The Bijli family acquired it back in 1978. It is a perfectly serviceable theater of its era: one screen, one auditorium, the standard Indian movie-going experience of ceiling fans, hard seats, and intermission samosas.

Ajay Bijli, the man who would eventually build India's largest cinema chain, was not born into the entertainment business. He was born into trucks. His father, Krishan Mohan Bijli, ran Amritsar Transport Company, a road freight operation. Ajay attended Modern School in Delhi, one of the city's elite institutions, then completed his B.Com from Hindu College at the University of Delhi. After college in 1988, he joined the family trucking business and, by his own candid admission, "made a disaster of it."

Then, in 1992, his father passed away. Two years later, a devastating warehouse fire essentially destroyed what remained of the transport business. At twenty-something, Ajay Bijli found himself with a struggling logistics company, mounting debts, and one underperforming cinema. Most people in that position would have sold the theater and tried to rescue the core business. Bijli did the opposite. He decided to bet on Priya.

He renovated the cinema in 1990, turning it into one of Delhi's better single-screen venues. But the real inflection point came in 1995, when Bijli traveled to Australia and walked into a Village Roadshow multiplex for the first time. The concept was a revelation: multiple screens under one roof, each playing a different film, with clean lobbies, comfortable seating, concession stands selling overpriced snacks, and an atmosphere that felt more like a premium retail experience than a dingy movie hall. Bijli immediately understood that this model could transform Indian cinema-going.

In 1995, Priya Exhibitors Private Limited entered a 60:40 joint venture with Village Roadshow Limited, the Australian cinema and entertainment giant. The entity was christened PVR, standing for Priya Village Roadshow. The venture's first project was PVR Anupam, a multiplex in the Saket neighborhood of New Delhi. When it opened for commercial operations in June 1997, it became widely recognized as India's first modern multiplex cinema.

The cultural shift was seismic. For decades, the Indian movie-going experience had been defined by single-screen theaters, many of them crumbling relics of a different era. The audience was overwhelmingly male, the facilities were often uncomfortable, and middle-class families, particularly women, frequently avoided the experience altogether. PVR Anupam changed the equation. Air conditioning, cushioned seats, clean restrooms, and a concession stand that sold popcorn and cold drinks at prices that would make a restaurant blush. Suddenly, watching a movie became an aspirational outing rather than a guilty pleasure. Bijli had not just opened a theater; he had created a new category of urban leisure.

By 2000, PVR had expanded to 12 screens across Delhi. But the partnership with Village Roadshow was fraying. The Australian company, dealing with its own strategic challenges globally, decided to exit India. In November 2002, Village Roadshow sold its entire stake back to Priya Exhibitors and departed. This was a critical moment. Without Village Roadshow's capital and operational expertise, PVR needed a new financial partner.

Enter ICICI Ventures. In 2003, the venture capital arm of India's largest private bank invested approximately 40 crore rupees into PVR. This was not just money; it was a stamp of institutional credibility. With ICICI's backing, Bijli now had the firepower and the confidence to think beyond Delhi. The trucking family's son was ready to build a national champion.

The IPO came in January 2006, when PVR listed on the NSE and BSE at 225 rupees per share. In a coincidence that would prove prophetic, INOX Leisure, the company PVR would eventually merge with two decades later, also went public that same year, listing at 120 rupees per share. Two rival cinema chains, born in the same era, listing in the same year, destined to become one.

But first, PVR had a continent to conquer.

III. The M&A Playbook: Consolidating a Continent

The Indian multiplex industry in the late 2000s looked like the American railroad industry in the 1870s: dozens of regional operators, fragmented markets, thin margins, and massive capital requirements. Someone was going to consolidate it. The question was who, and at what price.

Ajay Bijli's answer was a decade-long acquisition spree that methodically absorbed regional chains, eliminated competition, and built the largest cinema network India had ever seen. Three deals, in particular, defined the strategy.

The first was Cinemax in 2012. The Kanakia Group's CineMAX chain operated 138 screens across 39 properties, concentrated heavily in Mumbai, Pune, Bengaluru, Hyderabad, and several other cities. PVR, through its subsidiary Cine Hospitality Private Limited, acquired the entire chain for 395 crore rupees, which worked out to roughly 2.8 crore per screen. At the time, critics called it expensive. But the deal gave PVR something it desperately needed: dominance in Mumbai, India's financial capital and its most important movie market. Before Cinemax, PVR was essentially a North Indian chain with strength in Delhi-NCR and a scattering of properties elsewhere. After Cinemax, it was a genuinely national player.

The strategic logic was straightforward. In cinema exhibition, screen count is destiny. More screens mean better negotiating leverage with film distributors, who are desperate for wide release coverage. More screens mean you are the "only game in town" for national advertisers who want to reach a pan-India audience through in-cinema advertising. And more screens mean you can spread fixed costs across a larger base, improving unit economics on everything from technology procurement to popcorn supplies. The Cinemax acquisition was PVR's declaration that it intended to be the consolidator, not the consolidated.

The second pivotal deal came in 2016: DT Cinemas. The DLF Group, India's largest real estate developer, had operated a cinema chain called DT Cinemas within its premium mall properties, primarily in Delhi-NCR. Bijli had been pursuing this acquisition for nearly seven years, a testament to both his persistence and DLF's reluctance to part with a trophy asset. When the deal finally closed at 500 crore rupees, it gave PVR near-monopoly status in the Delhi-NCR market, which happens to be one of India's highest-spending catchments for entertainment. The DT screens were situated inside DLF malls in locations like Vasant Kunj, Saket, and Noida, areas where affluent North Indian families spent their weekends. Owning these screens was not just about ticket sales; it was about controlling prime real estate in the country's most premium retail environments.

The third and arguably most strategic acquisition landed in 2018: SPI Cinemas, the parent company of Chennai's legendary Sathyam Cinemas brand. This was the crown jewel. SPI Cinemas had been founded around the Royal Theatre, a venue built in 1974 and acquired by the Kiran Reddy family in the 1980s, which evolved into Sathyam, one of the most beloved cinema brands in South India. PVR paid approximately 850 crore rupees in a cash-and-stock deal, a significant premium that raised eyebrows.

But Bijli understood something that many analysts initially missed. South India is the beating heart of Indian cinema. The four southern states, Tamil Nadu, Andhra Pradesh, Telangana, and Kerala, consistently deliver the highest occupancy rates in the country. The culture of movie-going in the South is deeper, more passionate, and more resilient than anywhere else in India. Tamil and Telugu audiences do not merely watch movies; they celebrate them. First-day-first-show is a cultural event. Fan clubs for stars like Rajinikanth and Thalapathy Vijay operate with the fervor of religious organizations. By acquiring SPI Cinemas, PVR was not just buying screens; it was buying access to the most "movie-mad" audience on the subcontinent.

The capital deployment strategy across all three deals revealed a sophisticated playbook. PVR consistently used its relatively high stock market valuation as currency, supplementing cash payments with equity swaps. The company was essentially trading its own highly valued paper for cash-flow-generating regional assets, a classic consolidator's move. Whether PVR "overpaid" for any individual acquisition is debatable. What is not debatable is that the combined portfolio gave PVR a geographic reach and a scale advantage that no competitor could match, setting the stage for the ultimate deal: the merger with INOX.

IV. The Current Management and The Power Balance

The boardroom of PVR INOX Limited is a study in delicate diplomacy. When the merger with INOX Leisure closed in February 2023, it brought together two families with very different cultures, very different geographies, and very different ideas about how to run a cinema chain. Making that marriage work is the central management challenge of the company today.

On the PVR side sits Ajay Bijli, the Managing Director. Now in his late fifties, Bijli is the quintessential founder-operator: charismatic, brand-obsessed, and deeply involved in the customer-facing aspects of the business. He is the man who personally approves the design of new luxury auditoriums, who insists on tasting new menu items at concession stands, and who has been known to walk into PVR theaters unannounced to check on cleanliness and service standards. He completed the Owner/President Management program at Harvard Business School, and that combination of entrepreneurial instinct and professional polish defines his leadership style. His younger brother, Sanjeev Kumar Bijli, serves as Executive Director and has traditionally been the operations and expansion engine, the person who negotiates lease terms with mall developers and oversees the logistical machinery of opening new screens.

On the INOX side, the key figure is Siddharth Jain, who serves as Non-Executive Director. The Jain family's roots run deep in Indian industry. The INOX Group traces its origins to 1923 as a paper and newsprint trading business, later diversifying into industrial gases in 1963, chemicals through Gujarat Fluorochemicals Limited in 1987, and renewable energy through Inox Wind in 2009. INOX Leisure was promoted by the GFL group and emerged in 1999 with a vision to bring world-class cinema technology to India, opening its first four-screen multiplex at Inorbit Mall in Mumbai's Malad suburb. The family split amicably in November 2021, with Pavan Jain retaining INOX Leisure and INOX Air Products while his brother Vivek Jain took Gujarat Fluorochemicals and the wind energy businesses.

The post-merger shareholding structure tells an interesting story about power dynamics. The Jain family, as the INOX promoters, held roughly 16.66 percent of the combined entity immediately after the merger, with GFL Limited alone accounting for 16.13 percent. The Bijli family held approximately 10.62 percent. Combined promoter holding stands at about 27.5 percent. This means the INOX side actually holds a larger stake than the PVR side, yet operational control rests firmly with the Bijlis, with Ajay serving as MD. It is a governance arrangement that works only as long as both families remain aligned on strategy.

The institutional investor base is formidable. Mutual funds hold nearly 32 percent, foreign institutional investors hold close to 20 percent, and the Indian public accounts for about 14 percent. This means the company is effectively institutionally controlled, with the promoter families serving more as stewards than as majority owners.

The incentive structure underwent a significant revision in 2023, shifting toward a "pay-for-performance" model that reflects the company's post-merger priorities. Variable compensation, which can reach up to 100 percent of fixed pay for senior management, is now explicitly tied to achieving merger synergies, targeted in the range of 225 to 250 crore rupees, and to executing the transition toward an asset-light operating model. This is a meaningful signal. It tells you that the board recognizes the company is transitioning from a "founder-led growth" phase to a "professionalized integration" phase, and that management's financial rewards are calibrated accordingly.

In August 2024, PVR INOX promoters, including Ajay Bijli, divested a small 0.33 percent stake through the open market. Such sales always attract scrutiny, but in context, the amount was modest and consistent with personal liquidity management rather than any loss of conviction.

The real test of this governance structure will come when the easy synergies have been captured and the harder questions about capital allocation, format strategy, and geographic priorities demand genuine disagreement and resolution. For now, the dual-family dynasty holds.

V. The Hidden Businesses: Beyond the Ticket

Walk into any PVR INOX theater and the first thing you encounter is not a movie screen. It is a concession counter. A gleaming, brightly lit expanse of popcorn machines, soda fountains, nachos warmers, and gourmet snack displays that looks more like a fast-casual restaurant than a cinema lobby. This is not an accident. It is the entire business model.

The conventional wisdom about cinema chains is that they are in the movie business. They are not. They are in the captive-audience business, and the three pillars that generate outsized profitability have almost nothing to do with the films being screened.

The Popcorn Moat: Food and Beverage

The F&B segment is the engine room of PVR INOX's economics. In the most recent quarter, Q3 FY26, Spend Per Head on food and beverage reached 146 rupees, up 4 percent year-over-year. The full-year F&B revenue for FY26 was on track to surpass 2,000 crore rupees, having already crossed 1,800 crore earlier in the fiscal year. But the truly extraordinary figure is the gross margin: somewhere in the range of 75 to 76 percent.

Think about that for a moment. A bag of popcorn that costs PVR INOX roughly 25 to 30 rupees to produce sells for 200 to 350 rupees. A fountain drink that costs perhaps 10 rupees in syrup and carbonated water sells for 150 rupees. These are not food service margins; these are luxury goods margins, comparable to what you might see at an LVMH brand or an Apple accessory. And they come with a structural advantage that no restaurant can replicate: a captive audience that cannot leave to get cheaper food elsewhere. Once you are inside the theater, PVR INOX has a near-monopoly on your stomach.

The company has been actively expanding the F&B offering beyond traditional popcorn and cola. Regional food options, healthier snack alternatives, and branded collaborations have been introduced to increase attach rates and average transaction sizes. More interestingly, PVR INOX has explored partnerships, including a joint venture with Devyani International, to extend F&B sales beyond the cinema lobby and into standalone retail formats. The thesis is simple: if you have already built a food supply chain and a brand that consumers associate with indulgent snacking, why limit it to people who are already watching a movie?

The Advertising Giant

The second hidden business is advertising, and its economics are even more remarkable than F&B. In-cinema advertising revenue reached approximately 1,486 million rupees in a recent quarter, the highest level since the pandemic. Q1 FY26 advertising income alone was 1,096 million rupees, reflecting 17 percent year-over-year growth.

The beauty of in-cinema advertising is its cost structure. The screens are already there. The projectors are already running. The audience is already seated and, crucially, cannot skip, fast-forward, or mute the ads. The incremental cost of running an additional thirty-second commercial before a movie is essentially zero, which means advertising revenue drops almost entirely to the bottom line. EBITDA margins on this segment approach 100 percent in practical terms.

For national advertisers, PVR INOX's nearly 1,800 screens represent an irresistible proposition: guaranteed attention from an urban, middle-to-upper-class demographic that is notoriously difficult to reach through digital channels where ad-blocking and skip buttons reign supreme. The company's scale advantage is decisive here. No other cinema chain in India can offer advertisers comparable pan-India reach, which gives PVR INOX meaningful pricing power.

There is an interesting strategic tension, however, between advertising revenue and the premium experience. PVR INOX has experimented with reducing pre-show advertising in its luxury formats to create a more premium, ad-free experience. The logic is that wealthy patrons paying a premium for Director's Cut or Insignia screens expect not to sit through fifteen minutes of advertisements. This trade-off, sacrificing some of the highest-margin revenue to protect brand positioning, reveals a company thinking carefully about long-term value rather than short-term extraction.

Luxury Formats: Where the Real Money Lives

PVR INOX operates a staggering array of premium cinema formats: IMAX, 4DX, ScreenX, MX4D, Onyx (Samsung LED screens), ICE, P[XL], Director's Cut, Insignia, and Luxe. Each format commands a significant premium over standard tickets and attracts a wealthier demographic that spends more on food and beverages.

Premium formats currently account for approximately 14 percent of total revenue, and the company has set an ambitious target of expanding this to 20 percent. The math on premium screens is compelling. A Director's Cut auditorium might have only 30 to 50 recliner seats compared to 250 or more in a standard auditorium, but each ticket sells for three to five times the standard price. When you layer in the higher F&B spend from this affluent audience and the premium positioning that attracts luxury advertisers, the revenue per seat in a premium format dramatically outperforms a standard screen.

In February 2024, PVR INOX made a statement by reopening the 86-year-old heritage Eros Cinema in Mumbai's Churchgate neighborhood as India's first standalone IMAX theater with 4K projection. The restoration of this Art Deco landmark into a cutting-edge IMAX venue was part branding exercise, part love letter to cinema history, and entirely on-strategy: demonstrating that PVR INOX owns not just the future of Indian moviegoing but its past as well.

PVR INOX Pictures: Controlling the Supply Chain

The fourth leg of the stool is PVR INOX Pictures, the company's distribution arm and the largest independent distributor of foreign-language films in India. The division has distributed over 500 Hollywood films and more than 200 Bollywood titles. Post-merger, it was rebranded as PVR INOX Pictures and expanded its focus to include regional Indian cinema, particularly Malayalam and Bengali films, alongside English-language releases. Across a recent period, the team distributed 124 films, split fairly evenly between international, regional, and Hindi titles.

The distribution segment contributes between 5 and 10 percent of total revenues, but its strategic value far exceeds its financial contribution. By controlling distribution rights, PVR INOX ensures a steady supply of content for its screens while also earning margins on films that play in competitor theaters. It is a vertical integration play that strengthens the company's negotiating position with Hollywood studios and independent producers alike.

The 4700BC Story: A Masterclass in Non-Core Monetization

One of the most elegant transactions in PVR INOX's recent history is the 4700BC story. In 2015, PVR acquired a 70 percent stake in Zea Maize Private Limited, the parent company of 4700BC, a gourmet popcorn brand founded in 2013 by Chirag Gupta as one of India's first premium popcorn startups. The acquisition price was a mere 5 crore rupees.

Over the following decade, PVR INOX invested approximately 94.6 crore rupees in total equity into the business, helping scale 4700BC from a niche brand into a nationally recognized snacking company offering popped chips, makhana, crunchy corn, and nachos alongside its signature gourmet popcorn. In January 2026, PVR INOX sold its 93.27 percent stake to Marico Limited, the FMCG giant, for 226.8 crore rupees in an all-cash transaction, representing a roughly 40-fold jump in valuation from the original investment and an internal rate of return of approximately 24.5 percent.

The deal was instructive on multiple levels. PVR INOX exited a non-core, loss-making retail snacking business while retaining its far more profitable in-theater F&B operations. The proceeds were earmarked for debt reduction, directly supporting the company's stated goal of reaching a net-debt-free balance sheet. And it demonstrated management's willingness to harvest value from non-core assets rather than clinging to them for strategic optionality. In a conglomerate-happy country like India, that discipline is rare and worth noting.

VI. Strategy Analysis: Hamilton's 7 Powers and Porter's Competitive Forces

The most important question for any long-term investor is not whether PVR INOX had a good quarter. It is whether the company possesses durable competitive advantages that will still matter in five, ten, or twenty years. The frameworks of Hamilton Helmer's 7 Powers and Michael Porter's Five Forces provide a useful lens.

Scale Economies

PVR INOX's nearly 1,800 screens give it scale advantages that compound across multiple dimensions. Procurement costs for everything from projection equipment to popcorn kernels decline on a per-unit basis as volume increases. Negotiating leverage with film studios improves because distributors need wide release access. Corporate advertising contracts gravitate toward the chain that can deliver national reach. Technology investments in apps, loyalty programs, and data analytics can be amortized across a vastly larger base. When a national advertiser wants to buy cinema advertising in India, PVR INOX is effectively the only call they need to make.

The nearest competitor, Cinepolis India, operates roughly 485 screens, less than a third of PVR INOX's count. Miraj Cinemas has about 244. The gap is so wide that PVR INOX functions as a near-monopoly in the organized multiplex segment, commanding an estimated 43 percent share of multiplex screens nationally.

Cornered Resource: The Location Moat

Perhaps the most underappreciated power PVR INOX possesses is its portfolio of long-term leases in virtually every Tier-1 shopping mall in India. Cinema screens in malls are not interchangeable commodities. A mall developer allocates a specific, purpose-built space for a cinema operator, typically on a 15 to 30 year lease, and it is economically prohibitive to have two competing multiplex operators in the same mall. Once PVR INOX locks in a lease at a premium mall, that location is effectively cornered for decades.

This is the "location moat" in its purest form. A competitor cannot simply "build across the street." Cinema development requires specific real estate, zoning approvals, acoustic engineering, and massive upfront capital. In Tier-1 cities, where the highest-spending audiences live, the best locations have already been claimed. New entrants would need to wait for leases to expire, a process measured in decades rather than years.

Switching Costs: The Passport Program

The PVR INOX Passport, priced at 349 rupees per month, offers subscribers up to four movies per month on weekdays for tickets priced at 350 rupees or less. The three-month plan at 1,047 rupees includes free F&B vouchers worth 350 rupees. The program has been expanded to become pan-India, though it is sold on a first-come-first-served basis with a cap of 50,000 passes per tranche.

Subscription programs create switching costs by converting occasional moviegoers into habitual ones. Once a consumer has pre-paid for four movies a month, they are not browsing Cinepolis or Miraj for showtimes. They are locked into the PVR INOX ecosystem, and every visit generates incremental F&B and advertising revenue that would not exist without the subscription pull. The model mirrors what AMC's A-List and Regal's Unlimited achieved in the United States: using subscriptions to increase visit frequency and lifetime customer value.

Counter-Positioning: Fighting the OTT Threat

The existential narrative around cinema exhibition since 2020 has been the rise of OTT platforms. Netflix, Amazon Prime Video, Disney+ Hotstar, Sony LIV, and Zee5 have collectively invested billions of dollars in Indian content, and the pandemic accelerated streaming adoption dramatically. Hindi cinema had one of its worst box-office years in FY25, amplifying concerns that theatrical exhibition is in structural decline.

PVR INOX's counter-positioning strategy rests on a simple insight: there are certain experiences that cannot be replicated on a couch. An IMAX screen with 4K laser projection and Dolby Atmos surround sound is not competing with a 55-inch television. A Director's Cut auditorium with recliner seats, gourmet food, and butler service is not competing with someone watching Netflix in their pajamas. The investment in premium formats is fundamentally a bet that cinema can survive the OTT era by moving upmarket, by becoming an "event" rather than a convenience.

Porter's Five Forces Assessment

The threat of new entrants is low. The capital requirements are enormous, the best locations are locked up, and the scale disadvantages facing a new entrant are prohibitive. The bargaining power of suppliers (film studios and distributors) is moderate; a blockbuster film has nowhere to go except into theaters, but studios can negotiate on revenue-share terms and theatrical window lengths. The bargaining power of buyers (moviegoers) is limited inside the theater but real in the decision of whether to go to the theater at all versus staying home with an OTT subscription. The threat of substitutes, primarily OTT and home entertainment, is the most significant force and the one that keeps cinema bulls up at night. Rivalry among existing competitors is muted by PVR INOX's dominant market share, though Cinepolis continues to expand aggressively in select markets.

Brand Power and Process Power

Two additional Helmer powers deserve mention. PVR INOX has built genuine brand equity, particularly in premium formats. The PVR name in North India and the INOX name in West and Central India carry associations of quality, comfort, and aspiration that regional chains cannot easily replicate. Process power, the accumulated operational know-how of managing complex cinema operations at scale including everything from F&B supply chains to dynamic ticket pricing algorithms, creates efficiencies that new entrants would need years to develop.

The synthesis across both frameworks is consistent. PVR INOX occupies a structurally advantaged position in Indian cinema exhibition, protected by scale, location lock-in, and brand equity. The primary vulnerability is not competition from other exhibitors but the secular shift in consumer entertainment habits toward at-home streaming. The company's strategic response, premiumization and experience differentiation, is sound but untested over a full economic cycle in the post-OTT era.

VII. COVID-19: The Existential Crisis That Forged the Merger

The pandemic did not merely hurt the Indian cinema industry. It nearly destroyed it.

When India entered its first nationwide lockdown in March 2020, every screen in the country went dark simultaneously. For an industry with massive fixed costs, primarily long-term real estate leases, the impact was catastrophic. Monthly expenditures for PVR and INOX individually ran at approximately 850 million rupees even with theaters shuttered. Through brutal cost-cutting, both companies slashed their monthly burn rates to roughly 120 million rupees, but the bleeding continued for months.

The broader industry lost an estimated 9,000 crore rupees in revenue during the lockdown period. When theaters were finally allowed to reopen, they were restricted to 50 percent capacity. The 2021 box office recovered to only 37 percent of 2019 levels. Approximately 1,000 screens across India may have permanently closed, many of them independent single-screen theaters that lacked the balance sheet strength to survive an extended shutdown.

Both PVR and INOX publicly opposed the trend of direct-to-OTT releases during the lockdowns, arguing vociferously that theatrical windows needed to be preserved. But behind the public stance, the financial reality was dire. Both companies were burning cash, carrying significant lease liabilities, and facing an uncertain recovery timeline.

It was in this crucible that the merger was conceived. On March 27, 2022, PVR and INOX Leisure announced an all-stock amalgamation deal. The merger ratio was set at 3 shares of PVR for every 10 shares of INOX Leisure. The combined entity at announcement encompassed 1,546 screens across 341 properties in 109 cities. The Mumbai bench of the National Company Law Tribunal approved the scheme on January 12, 2023, and the deal closed in February 2023, with PVR renamed as PVR INOX Limited.

The strategic rationale was multi-layered. Scale was the obvious driver: the merged entity would command approximately 50 percent of India's multiplex screens and 16 percent of overall screens including single screens. But scale was only part of the story. The real prize was cost synergies. Two separate head offices, two technology platforms, two procurement teams, two advertising sales forces, all could be rationalized. The synergy target of 225 to 250 crore rupees annually represented a meaningful improvement in profitability without needing a single additional customer to walk through the door.

There was also a defensive dimension. Reports from early 2022 suggested that PVR had explored merger discussions with Cinepolis India, valued at roughly 13,600 crore rupees. Those talks did not materialize, but they signaled that consolidation was inevitable. The INOX merger ensured that PVR would be the consolidator, not the target. The resulting duopoly between PVR INOX and Cinepolis, with a massive gap to the third player, reshaped the competitive landscape of Indian cinema exhibition fundamentally.

The merger's financial trajectory has been encouraging. Net debt, which stood at approximately 14,304 million rupees at the time of the merger in March 2023, was reduced to just 365 crore rupees by December 2025, a decline of over 75 percent. Management expects the company to be net-debt-free by the end of FY26 or early FY27. That deleveraging speed speaks to both the synergies being realized and the cash-generative nature of the combined business when content supply normalizes.

VIII. The Future: The Asset-Light Pivot

For the first twenty-five years of its existence, PVR's growth model was simple and capital-intensive: sign a long-term lease with a mall developer, spend 4 to 6 crore rupees per screen on fit-out and equipment, and operate the resulting cinema. This model worked brilliantly when the company was expanding into Tier-1 cities where affluent audiences could support premium ticket prices and high F&B spend. But it also meant that every new screen required significant upfront capital, creating a perpetual hunger for cash that constrained the pace of expansion.

The asset-light pivot, centered on the FOCO model, represents a fundamental rethinking of this approach. Under FOCO, a franchise partner or real estate investor owns the cinema assets, including the real estate and the interior fit-out. PVR INOX provides its expertise in design, development, execution, and day-to-day operations, earning a management fee and a share of revenue without deploying significant capital. The model reduces PVR INOX's per-screen capital expenditure by 30 to 50 percent.

Progress has been meaningful. By Q3 FY26, 100 screens had been signed under asset-light structures across 22 cinemas, with 31 screens under the pure FOCO model and 69 under related asset-light arrangements. The first PVR INOX Luxe format under the FOCO model opened in Raipur, Chhattisgarh, a Tier-2 city that exemplifies the target geography. For FY26, approximately 15 percent of new screens followed the FOCO model, 35 to 50 percent used broader asset-light structures, and the remainder were traditional structured lease agreements.

The FOCO model is particularly well-suited for Tier-2 and Tier-3 city expansion, where real estate costs are lower but local developers may lack cinema operating expertise. By partnering with local investors who understand their markets and can secure favorable real estate, PVR INOX can extend its brand and operational platform into cities that would not have justified the full capital commitment under the old model.

The screen addition targets reflect this new approach. FY26 is expected to see approximately 96 to 100 new screen additions, with a ramp to 150 new screens in FY27. The company's stated ambition is to reach 2,000 total screens by calendar year 2026 or early 2027, up from the current count of 1,783.

The Bear Case

The bear case for PVR INOX centers on three risks. First, content volatility: cinema exhibition is inherently dependent on the quality of the film slate. FY25 was a painfully weak year for Hindi cinema, and the company reported a revenue decline of 5 percent to 5,780 crore rupees and a net loss of 280 crore rupees, significantly worse than the 32 crore loss in FY24. When hit movies do not arrive, no amount of operational excellence can fill empty seats.

Second, the OTT window continues to shrink. Studios are under pressure from streaming platforms to reduce the gap between theatrical release and digital availability. If that window compresses from the current 6 to 8 weeks to 3 to 4 weeks, the urgency for audiences to see films in theaters diminishes materially. The "I will just wait for it on streaming" behavior is already widespread among casual moviegoers.

Third, while the balance sheet has improved dramatically, lease liabilities remain substantial as an off-balance-sheet consideration under Ind AS 116 accounting standards. Investors should scrutinize the total lease obligation alongside reported net debt for a complete picture of the company's financial commitments.

The Bull Case

The bull case rests on equally compelling arguments. First, consolidation is complete. PVR INOX operates in what is effectively a duopoly with Cinepolis, with a commanding lead. This market structure supports pricing power, advertising revenue growth, and favorable terms with studios and mall developers.

Second, the premiumization of the Indian middle class is a secular trend. As disposable incomes rise across India's urban population, the willingness to pay for premium experiences, whether a Director's Cut screening or a gourmet concession meal, increases. PVR INOX is positioned as the primary beneficiary of this trend.

Third, F&B is becoming a standalone growth driver. The segment's combination of massive gross margins and increasing attach rates means that even flat footfall growth can deliver meaningful revenue and profit expansion if SPH continues to rise.

Fourth, the FOCO model, if executed successfully, transforms PVR INOX from a capital-intensive operator into a capital-light platform company, fundamentally improving return on equity and free cash flow generation.

The Q3 FY26 results demonstrated the earnings power of the model when content supply cooperates. Revenue of 1,908 crore rupees was up 9.7 percent year-over-year, net profit reached 96 to 115 crore rupees, EBITDA of 345 crore rupees was up 33.7 percent, and occupancy improved to 28.5 percent from 25.7 percent in the prior-year quarter. Average Ticket Price reached 293 rupees, up 4 percent, while F&B SPH hit 146 rupees, also up 4 percent. Footfalls of 40.5 million guests were up 9 percent.

IX. The Key Performance Indicators That Matter

For investors tracking PVR INOX's ongoing performance, the avalanche of reported metrics can be overwhelming. But if you strip away the noise, two KPIs capture the essential health of this business better than any others.

Average Ticket Price (ATP)

ATP, currently at 293 rupees, measures the company's ability to monetize each admission. It is a function of pricing power, premium format mix, and audience willingness to pay. In an industry where footfall growth is constrained by content quality and the secular competition from streaming, ATP growth is the primary lever for revenue expansion on a per-screen basis. A rising ATP signals successful premiumization; a declining ATP signals that the company is being forced to discount to fill seats. The trend matters more than the absolute number.

F&B Spend Per Head (SPH)

SPH, currently at 146 rupees, measures the company's ability to extract ancillary revenue from each visitor. Given the extraordinary gross margins on F&B, every rupee of SPH growth drops disproportionately to the bottom line. SPH growth is driven by menu innovation, upselling, attach rate improvements, and the shift toward premium formats where wealthier audiences spend more freely. If ATP tells you how much the customer paid to enter, SPH tells you how much you extracted from them once they were inside. Together, these two metrics, total Revenue Per Patron (ATP plus SPH), provide the single clearest signal of whether PVR INOX's premiumization strategy is working.

X. The Playbook and Conclusion

The PVR INOX story offers a playbook that extends well beyond cinema exhibition. It is the playbook of the patient consolidator in a fragmented, high-capex industry.

The first lesson is that in industries with high fixed costs and fragmented competition, being the last one standing is a viable and often lucrative strategy. Ajay Bijli did not invent a better way to show movies. He assembled the most screens, locked up the best locations, and forced the industry to consolidate around him. The value was not in innovation; it was in aggregation.

The second lesson is the power of premiumization when volume growth stalls. India's total cinema footfalls have been essentially flat for years, bouncing around with content cycles but showing no sustained upward trend. PVR INOX's response has been to win on value rather than volume, raising ATP through premium formats, growing SPH through expanded F&B offerings, and monetizing the captive audience through high-margin advertising. When the units are not growing, you must grow the unit economics. PVR INOX has executed this pivot more successfully than almost any comparable exhibitor globally.

The third lesson concerns timing and courage in mergers. The PVR-INOX deal was announced in March 2022, during one of the darkest periods in the history of theatrical exhibition. COVID had shattered industry confidence, OTT was being widely proclaimed as the death of cinema, and both companies were financially strained. Merging at the point of maximum pessimism, rather than at the top of a cycle when prices would have been higher, may prove to have been the defining strategic decision of both families' business legacies.

Whether the INOX merger was the "trade of the century" for the Bijlis remains to be seen. The synergies are being realized. The debt is being paid down. The asset-light model is gaining traction. But the ultimate verdict depends on a question that no amount of financial engineering can answer: will Indian audiences continue to leave their homes, put down their phones, and sit in a dark room with strangers to watch stories told on a big screen?

The Bijli family, the Jain family, and 1,783 screens across India are betting the answer is yes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube