PTC Industries: From Small-Town Foundry to Aerospace Titan

I. Introduction & Cold Open

The titanium ingot glows cherry-red in the vacuum chamber, 2,400 degrees Celsius of molten metal that will eventually find its way into a Safran LEAP engine, perhaps powering a Boeing 737 MAX or an Airbus A320neo somewhere over the Atlantic. This scene unfolds not in Seattle or Toulouse, but in Lucknow—a city better known for its Mughal architecture and kebabs than aerospace-grade metallurgy.

In May 2025, when Defence Minister Rajnath Singh cut the ribbon at what would become the world's largest single-site titanium and superalloy materials plant, he wasn't just inaugurating another factory. He was validating a 62-year journey that began with a modest foundry casting water pumps and valve bodies for India's nascent industrial sector. Today, PTC Industries Limited manufactures metal components so critical that when they fail, planes fall from the sky, nuclear reactors melt down, and oil rigs explode.

The numbers tell part of the story: a market capitalization that has exploded to ₹21,370 crore, stock returns of 2,517% over five years, and a customer roster that reads like a who's who of global aerospace—Rolls-Royce, Safran, BAE Systems, Israel Aerospace Industries. But numbers alone don't explain how a company from the heart of Uttar Pradesh convinced the world's most demanding customers to trust them with components where failure isn't an option.

This is a story about patient capital deployed over decades, about building capabilities when no one would teach you, about earning trust one titanium casting at a time. It's about timing—how PTC positioned itself perfectly for the confluence of India's defense modernization, global supply chain diversification, and the aerospace industry's post-COVID recovery. And perhaps most importantly, it's about solving a ₹35,000 crore problem: India's crippling dependence on imported defense-grade materials.

The central question isn't just how PTC made this transformation—it's what their journey reveals about manufacturing excellence in emerging markets, about competing globally from unexpected geographies, and about the intersection of geopolitics and industrial strategy. Because when you're casting titanium for fighter jets and submarine components, you're not just running a business—you're building sovereign capability.

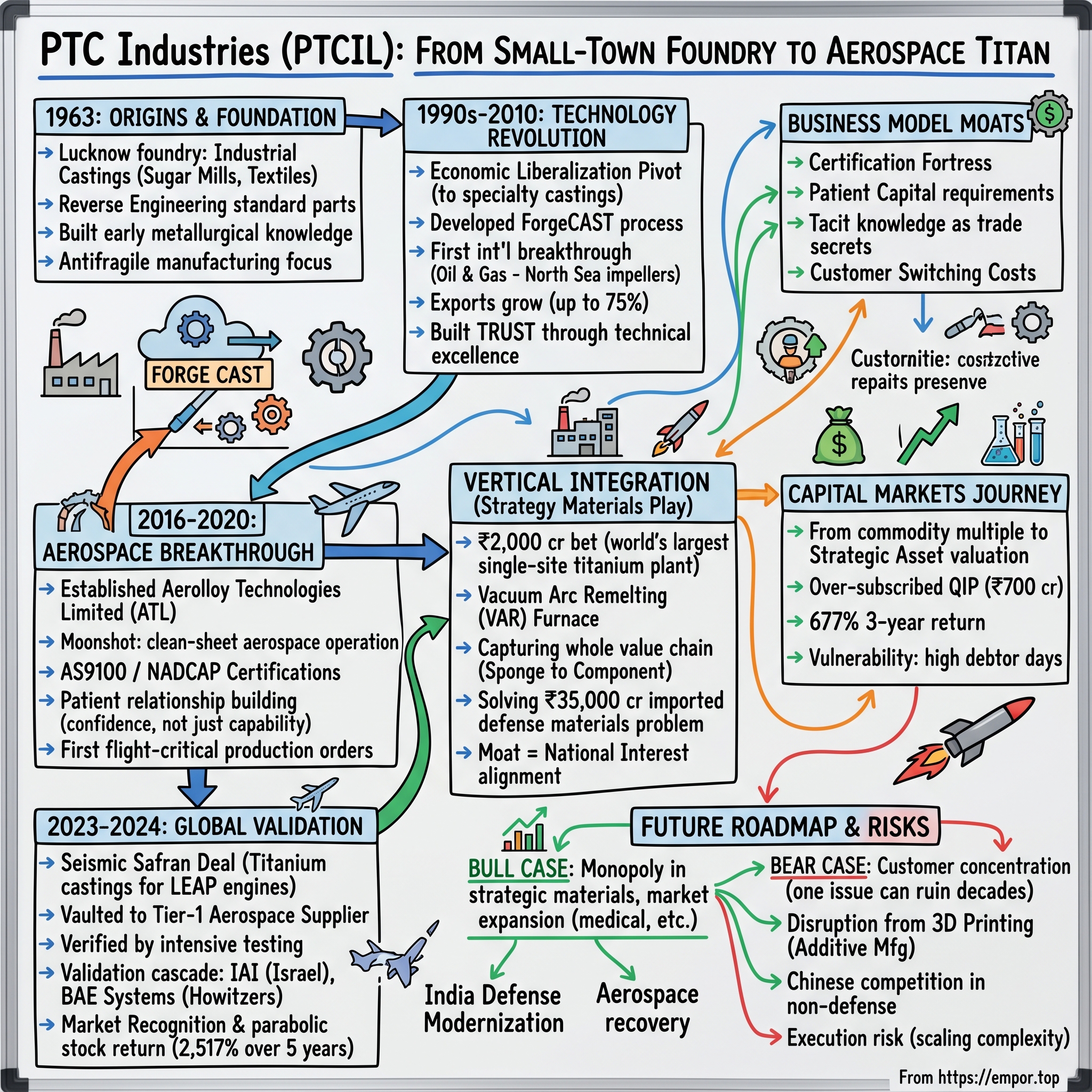

II. Origins & The Foundation Years (1963-1990s)

Picture Lucknow in 1963: sixteen years after independence, Nehru's temples of modern India rising from agricultural plains, the city still carrying the faded grandeur of its Nawabi past. This was where PTC Industries began—not with grand ambitions of aerospace glory, but with the prosaic goal of making industrial castings for sugar mills and textile factories sprouting across newly independent India.

The founders understood something fundamental about post-colonial industrialization: you couldn't import your way to self-reliance. Every valve, every pump impeller, every gear housing that broke down in a factory meant production stoppage, foreign exchange bleeding out for replacements, and delays that could stretch for months. PTC positioned itself as the solution—a foundry that could reverse-engineer, adapt, and manufacture what India's industries needed.

The technological foundation came from an unlikely source: the Replicast process, a ceramic shell investment casting technology installed in the 1960s when such precision casting was virtually unknown in India. While competitors poured metal into sand molds producing rough castings requiring extensive machining, PTC could achieve near-net shapes with surface finishes that seemed impossible by Indian standards of the era. Think of it as the difference between carving a statue with a chainsaw versus a scalpel—both get you there, but only one gives you Michelangelo's David.

Operating in what economists would later call the "License Raj"—India's Byzantine system of industrial permits and production quotas—PTC learned to be technically excellent because mediocrity meant waiting years for import licenses. When a textile mill's critical component failed, PTC's engineers would study the broken part, often German or British-made, decipher the metallurgy, and produce a replacement that sometimes outlasted the original. This wasn't just import substitution; it was capability building through reverse engineering elevated to an art form.

By the 1980s, PTC had quietly built something remarkable: a library of metallurgical knowledge covering hundreds of alloys, a workforce that could read the grain structure of metal like others read newspapers, and relationships with industrial customers who had learned to trust this foundry in Lucknow over suppliers in Birmingham or Stuttgart. The company was manufacturing components for critical applications—if a PTC-made valve failed in a chemical plant, it could mean catastrophe. This early focus on consequence management, on understanding that their products stood between normal operation and disaster, would prove foundational.

The global context matters here. While Japan was perfecting just-in-time manufacturing and Silicon Valley was birthing the personal computer revolution, PTC was solving a different class of problems: how to make things that absolutely, positively could not fail, using equipment that was often decades old, with raw materials of questionable providence, for customers who couldn't afford downtime. They were building what we might now call "antifragile manufacturing"—getting stronger through adversity rather than despite it.

III. The Technology Revolution: Indigenous Innovation (1990s-2010)

The liberalization of India's economy in 1991 should have killed PTC Industries. Suddenly, Indian companies could import whatever they wanted. German precision castings, Japanese valve bodies, American pump impellers—all available with a purchase order. The protective walls that had sheltered domestic manufacturers for decades came crashing down. Most Indian foundries either closed or retreated to the lowest end of the market. PTC did something different: they went upmarket, fast.

The strategic pivot began with a simple observation. While anyone could now import a standard casting, nobody wanted to wait 16 weeks for a custom titanium component for an offshore oil rig, or pay European prices for exotic alloy castings needed in small quantities. PTC's new thesis: become the specialist for impossible castings, the ones where material cost was irrelevant compared to performance, where failure meant headlines, where certification requirements kept out casual competitors.

This meant developing capabilities that didn't exist in India. Take ForgeCAST, a hybrid process PTC developed that combined forging and casting to achieve mechanical properties previously thought impossible in cast components. Imagine trying to get the strength of a forged part with the complex geometry only possible through casting—like having your cake and eating it too, except your cake needs to withstand 1,000 atmospheres of pressure in a deep-sea drilling application.

The international breakthrough came almost by accident. A Dutch company needed replacement impellers for pumps used in North Sea oil extraction. The original supplier quoted 20 weeks; PTC promised eight. The Dutch were skeptical—how could a foundry in Lucknow deliver what established European suppliers couldn't? PTC not only delivered on time but the impellers lasted 40% longer than the originals. Word spread through the insular world of oil and gas equipment manufacturers. By 2000, PTC was exporting three-quarters of its production to Europe and North America.

Building these relationships required more than technical excellence. PTC's engineers learned to speak the language of their customers—not just English, but the subtle dialects of different industries. Nuclear power components required different documentation than marine applications. Aerospace had its own mythology of quality. Each sector had unwritten rules, inherited fears, legendary failures that shaped specifications. PTC became fluent in all of them.

The numbers from this period tell a story of patient building: exports growing from virtually zero to 75% of revenue, customer count expanding from dozens to hundreds, alloy capabilities expanding from basic steels to exotic nickel-based superalloys that could maintain strength at temperatures where normal steel would be puddles. But the real asset being built was trust—the knowledge in boardrooms from Houston to Hamburg that when you needed something difficult, something that pushed the boundaries of what was possible in metal, you called Lucknow.

Consider the audacity of this position. PTC was asking global companies to trust them with components where failure could mean environmental disaster, loss of life, or hundreds of millions in downtime. From a city most Western executives couldn't find on a map, in a country not exactly synonymous with precision manufacturing. That they succeeded reveals something profound about how technical excellence can transcend geography—but only if you're willing to be better, not just cheaper.

IV. The Aerospace Breakthrough (2016-2020)

The email from Rolls-Royce arrived on an unremarkable Tuesday in 2016. They needed a supplier for titanium castings—not for their legendary jet engines, not yet, but for a smaller project, almost a test. Could PTC deliver aerospace-grade components? The inquiry might as well have asked if PTC could put a man on Mars. Aerospace wasn't just another vertical; it was a different universe with its own physics of quality, traceability, and zero-defect manufacturing.

To understand the leap, consider this: PTC had been making critical castings for decades, components where failure meant disaster. But aerospace operates on another plane entirely. When a valve fails in a chemical plant, you shut down the line. When a turbine blade fails at 40,000 feet, 300 people die. The documentation requirements alone—every heat of metal traced to its mine, every process step recorded, every deviation analyzed—would break most manufacturers. PTC saw it as the ultimate validation of everything they'd built.

The transformation began with Aerolloy Technologies Limited (ATL), PTC's wholly-owned subsidiary created specifically for aerospace and defense. Think of ATL as PTC's moonshot project—a clean-sheet operation designed from the ground up for aerospace standards. While PTC's main foundry had evolved organically over decades, ATL was engineered for perfection: controlled environments, segregated alloy processing, digital twins of every component before physical production began.

Getting AS9100 certification—aerospace's gold standard—took 18 months of preparation. Every process had to be documented, every possible failure mode analyzed, every employee trained not just in what to do, but why it mattered. The NADCAP certification for special processes came next, requiring PTC to prove their heat treatment, non-destructive testing, and welding processes met the exacting standards of the global aerospace industry. These weren't just certificates to hang on the wall; they were passports to a $400 billion global aerospace supply chain.

The real breakthrough came through patient relationship building. PTC's engineers spent months at customer facilities, understanding not just specifications but fears. What kept chief engineers awake at night? What failures haunted their industry? They learned that aerospace purchasing wasn't just about capability—it was about confidence. Could you sleep soundly knowing a PTC casting was spinning at 10,000 RPM in a jet engine?

By 2019, PTC had secured its first production orders for aerospace components. Not prototypes, not samples—actual flight-critical parts. The volumes were small, almost insignificant compared to their industrial business. But symbolically, they were enormous. An Indian company, from Lucknow no less, was making parts that would fly in Western aircraft. The psychological barrier had been broken.

The timing was fortuitous. The global aerospace industry was hitting unprecedented production rates—Airbus and Boeing had backlogs stretching nearly a decade. Tier-1 suppliers like Safran and Rolls-Royce were desperately seeking additional capacity, particularly in Asia where the growth was happening. The Trump administration's trade war with China had made Chinese suppliers radioactive for defense applications. India, democratic and English-speaking, emerged as the obvious alternative. PTC had spent three years getting ready for a moment that arrived exactly when they were prepared to seize it.

V. The Safran Partnership & Global Validation (2023-2024)

The Safran deal announcement in November 2023 read like corporate boilerplate: "multi-year contract," "industrial cooperation," "LEAP engine casting parts." But for those who understood the aerospace industry's hierarchies and handshakes, this was seismic. Safran doesn't just make engines; they power half of all single-aisle aircraft flying today. The LEAP engine—a joint venture with General Electric—represents the pinnacle of commercial aviation technology. And they were trusting PTC with titanium castings for these engines.

To grasp the significance, understand that aerospace suppliers exist in rigid tiers. At the top sit the OEMs—Boeing, Airbus. Below them, Tier-1 suppliers like Safran, Rolls-Royce, and Pratt & Whitney who make engines and major systems. Tier-2 suppliers provide subsystems and components to Tier-1s. Most emerging market suppliers spend decades trying to break into Tier-3, making simple parts to drawings provided by others. PTC had vaulted directly to supplying Tier-1, and not just any components—titanium castings that go directly into the hot section of engines where material science meets its limits.

The negotiation had taken two years. Safran's engineers visited PTC's facilities seven times, each visit more intensive than the last. They tested PTC's titanium castings to destruction—literally. Thermal cycling that simulated decades of takeoffs and landings. Stress testing that pushed materials past their theoretical limits. Microscopic analysis that could detect impurities measured in parts per billion. PTC didn't just pass; they exceeded specifications by margins that surprised even Safran's veterans.

What sealed the deal wasn't just technical capability—it was PTC's vertical integration story. While other suppliers bought titanium ingots from global traders, PTC was building India's first private-sector titanium melting capability. They could control quality from raw material to finished component, a level of integration that even established Western suppliers rarely achieved. For Safran, worried about supply chain resilience post-COVID, this was compelling.

The first deliveries began in early 2024, ahead of schedule. Each casting was a testament to six decades of capability building, but also a bet on the future. These weren't commodity parts that could be easily re-sourced; they were complex geometries that pushed the boundaries of what was possible in titanium casting. Every successful delivery built trust, and trust in aerospace is the ultimate currency.

Then came the validation cascade. Israel Aerospace Industries, one of the world's most sophisticated defense contractors, placed their first-ever order with an Indian company for titanium aerospace components. IAI doesn't make decisions lightly—their products protect a nation surrounded by existential threats. That they chose PTC signaled to the global industry that this wasn't a fluke or a cost play. This was genuine technical capability.

BAE Systems followed with a massive contract for titanium castings for the M777 Ultra-Lightweight Howitzer, the same artillery system that had proved decisive in conflicts from Afghanistan to Ukraine. The M777's performance depends on titanium's strength-to-weight ratio—steel would make it too heavy for helicopter transport, aluminum too weak for the violence of artillery fire. PTC's castings would enable these weapons to rain precision fire then relocate before counter-battery radar could respond.

The financial markets responded with their own validation. PTC's stock price trajectory went parabolic, but this wasn't speculation—it was recognition that PTC had crossed the aerospace Rubicon. They were no longer trying to break in; they were in, with multi-year contracts and relationships that would take competitors decades to replicate.

VI. The Strategic Materials Play: Vertical Integration

January 2025, inside PTC's new facility: the Vacuum Arc Remelting (VAR) furnace hums with barely contained energy, turning titanium sponge—ugly, grey chunks that look like metallic popcorn—into aerospace-grade ingots with crystalline structures so perfect they could be museum pieces. This furnace, the first of its kind in India's private sector, represents more than capital equipment. It's industrial sovereignty materialized in refractory-lined steel.

To understand why PTC spent hundreds of crores on melting capability, follow the titanium value chain. It starts in mines in Australia or South Africa, where ilmenite ore is extracted. This gets processed into titanium sponge in China, Russia, Japan, or Kazakhstan—only seven countries have this capability. The sponge gets melted into ingots in even fewer locations, then rolled into plates, forged into billets, or cast into components. At each step, value multiplies and suppliers dwindle. By the time titanium reaches aerospace specifications, you're dealing with a oligopoly that can name its price.

India imports ₹14,000 crore worth of defense-grade materials annually, projected to hit ₹35,000 crore by 2026 as military modernization accelerates. Every Tejas fighter, every Arjun tank, every nuclear submarine depends on materials India doesn't produce. This isn't just expensive—it's a strategic vulnerability. Sanctions, supply disruptions, or simple commercial disputes could cripple defense production. PTC's vertical integration directly attacks this weakness.

The Lucknow facility inaugurated in May 2025 sprawls across acres like a small city dedicated to metallurgy. The world's largest single-site titanium and superalloy plant isn't hyperbole—it's a ₹2,000 crore bet that India's demand for aerospace materials will explode and that global customers will trust Indian-made materials. Defence Minister Rajnath Singh's presence at the inauguration wasn't ceremonial; it was strategic messaging to both domestic forces and foreign suppliers.

The technology inside reads like science fiction. Electron beam melting furnaces that operate in near-perfect vacuum, where a focused beam of electrons generates temperatures that would vaporize normal furnaces. Plasma arc melting that creates alloys impossible through conventional methods. Hot rolling mills acquired from the United States that can turn rough ingots into aerospace-grade sheets with tolerances measured in microns. Each piece of equipment represents not just capital investment but knowledge transfer—PTC's engineers spent months at equipment manufacturers, learning not just operation but the science behind the systems.

Vertical integration changes PTC's entire business model. Instead of buying titanium ingots at $30-40 per kilogram and adding value through casting, they can buy sponge at $8-10 per kilogram and capture the entire value chain. Margins expand from 15-20% to potentially 35-40%. But more importantly, they control quality from the atomic level up. When Safran needs assurance about material properties, PTC can provide documentation from sponge to finished component—a level of traceability that commands premium pricing.

The capacity numbers tell their own story: 1,500 metric tons of titanium alloy annually, expanding to 5,000 tons by 2027. For context, India's entire current consumption of aerospace-grade titanium is around 2,000 tons. PTC isn't just meeting current demand—they're betting on a future where India manufactures aircraft, not just components. Where the Tejas Mark-2 and the Advanced Medium Combat Aircraft programs drive thousands of tons of domestic demand. Where global OEMs establish final assembly lines in India, requiring local material sources.

But the real strategic play is even bigger. By establishing material capability, PTC becomes indispensable to India's defense industrial base. They're not just a supplier; they're critical infrastructure. This creates a moat that transcends normal competitive dynamics. Even if Chinese suppliers offered titanium at half the price, would India's defense establishment accept that dependency? PTC has positioned itself where national interest and business interest align—the ultimate durable competitive advantage.

VII. Financial Engineering & Capital Markets Journey

The spreadsheet told a story of transformation: revenue multiplying from ₹200 crore to over ₹1,000 crore, EBITDA margins expanding despite massive capital investments, return on capital employed that would make software companies envious. But PTC's capital markets journey wasn't just about numbers improving—it was about convincing investors that a foundry could have the multiples of a technology company.

When PTC went public, the market didn't know what to make of them. Manufacturing companies in India traded at single-digit PE ratios, treated as cyclical, capital-intensive businesses with limited growth potential. PTC was lumped in with commodity steel producers and auto ancillary suppliers. The stock languished for years, trading at ₹30-40, valued like a company making manhole covers, not aerospace components.

The perception shift began slowly. Quarterly earnings calls became education sessions, with management patiently explaining the difference between commodity castings and aerospace-grade titanium components. They shared metrics the market hadn't seen before from Indian manufacturers: customer stickiness measured in decades, order books stretching years, price escalation clauses that made them inflation-proof. Slowly, analysts began to understand: this wasn't manufacturing as they knew it.

The ₹700 crore Qualified Institutional Placement (QIP) in 2024-25 marked the inflection point. The book was oversubscribed within hours, with marquee funds fighting for allocation. These weren't momentum traders chasing a hot stock; they were long-term investors who had done the work, visited facilities, spoken to customers, understood the strategic position PTC had built. The pricing—at minimal discount to market despite the size—signaled institutional confidence.

Stock performance followed understanding. The 677% three-year return and staggering 2,517% five-year appreciation wasn't just multiple expansion—it was category creation. PTC wasn't being valued as a manufacturer anymore; they were being priced as a strategic asset play, a derivative on India's aerospace ambitions, a scarce pure-play on critical materials. The ₹21,370 crore market capitalization made them worth more than steel companies producing thousand times their volume.

But the balance sheet revealed vulnerabilities too. Debtor days stretching to 170—nearly six months of revenue tied up in receivables. In any other industry, this would signal distress, customers delaying payment, potential bad debts. In aerospace, it's different. Boeing pays on Boeing's schedule. Safran's payment terms are non-negotiable. This is the price of admission to the aerospace club—you finance your customers' working capital, and you smile while doing it.

The capital allocation strategy showed sophisticated thinking. While expanding capacity aggressively—capex running at 30-40% of revenue—PTC maintained disciplined debt levels. They understood that aerospace customers evaluate supplier financial stability as rigorously as technical capability. Too much leverage would spook customers worried about supply continuity. The balance was delicate: grow fast enough to capture opportunity, but not so fast that balance sheet stress threatened customer confidence.

Institutional ownership patterns revealed the smart money's positioning. Mutual funds that typically avoided manufacturing were taking 2-3% positions. Foreign institutional investors, usually allergic to Indian capital goods companies, were accumulating steadily. The register read like a who's who of quality-focused investing. These weren't traders; they were partners for the long journey ahead.

The valuation metrics sparked debate. At 50-60 times earnings, PTC traded at multiples typically reserved for software or pharmaceutical companies. Bears argued this was unsustainable—how could a foundry justify such valuations? Bulls countered that traditional metrics missed the point. This wasn't just current earnings; it was an option on India's aerospace future, on supply chain reorganization, on technological sovereignty. The market was pricing not what PTC was, but what it could become.

VIII. Business Model & Competitive Moats

Walk through PTC's facility and you encounter a paradox: machines that look like industrial archaeology—some dating to the 1960s—operating alongside equipment so advanced it requires clean room protocols. This isn't poor capital allocation; it's the physical manifestation of PTC's competitive moat. Those old machines, modified and refined over decades, can do things no modern equipment can replicate. They're like Stradivarius violins—irreplaceable, mysterious, and devastatingly effective.

The product portfolio reads like a periodic table of exotic alloys: duplex and super duplex stainless steels that resist corrosion in the most aggressive environments, nickel-based superalloys that maintain strength at temperatures where normal metals become putty, titanium alloys that combine the strength of steel with the weight of aluminum. Each material requires different melting techniques, heat treatment protocols, and quality control methods. Mastering one might take years; PTC has mastered dozens.

The real moat isn't the range—it's the institutional knowledge of when to use what. A customer comes with a problem: a valve that fails after six months in a sulfurous environment. PTC's engineers don't just recommend a material; they understand the failure mode, suggest design modifications, predict service life, and often guarantee performance. This consultative approach transforms PTC from vendor to partner, embedding them so deeply in customer operations that switching becomes unthinkable.

Consider the certification fortress PTC has built. AS9100 for aerospace quality management, NADCAP for special processes, ISO 14001 for environmental management, OHSAS 18001 for occupational health and safety—each certificate took years to obtain and requires continuous compliance. But the real barrier isn't getting certified; it's maintaining certification while actually producing. Many companies can pass an audit; few can deliver aerospace-grade components daily while maintaining perfect documentation. PTC has been doing it for years, building a track record that new entrants can't quickly replicate.

The customer approval process in aerospace adds another layer to the moat. It takes 2-3 years typically from first contact to production order. Engineers visit multiple times, samples undergo extensive testing, quality systems are audited, financial stability is verified. Once approved, switching suppliers requires repeating this entire process with someone else. PTC's customers aren't just sticky; they're superglued. The cost and risk of switching suppliers for flight-critical components means relationships are measured in decades, not quarters.

Technology like Replicast® and RapidCast™ sounds prosaic—just different ways of making castings. But these processes, refined over decades, achieve things that shouldn't be possible. RapidCast can go from 3D model to finished casting in days, not weeks, enabling rapid prototyping for aerospace customers accustomed to year-long development cycles. Replicast achieves surface finishes that eliminate machining operations, saving costs that dwarf the casting price. These aren't just manufacturing techniques; they're competitive weapons that took decades to forge.

The capital intensity that scares away competitors becomes a moat once you're established. A new entrant would need ₹500-1,000 crore just for equipment, then years of losses while building capabilities and certifications. And that assumes they could find and train the specialized workforce—metallurgists who understand aerospace specifications, quality engineers who speak NADCAP, production managers who can maintain aerospace discipline while hitting cost targets. PTC has been building this human capital for decades; it can't be bought, only built.

Working capital requirements add another barrier. Those 170-day debtor periods mean financing roughly half a year of operations. For PTC at current scale, that's ₹500+ crore tied up in receivables. A new entrant would need not just capital for equipment and operations, but patient capital willing to finance customer working capital for years before achieving positive cash flow. In a world of quarterly earnings pressure, finding such patient capital is nearly impossible.

The vertical integration into materials transforms the moat into something more like a castle with multiple walls. Competitors must now match not just casting capability but melting, rolling, and forging. The capital requirement doubles or triples. The technical complexity exponentiates. The customer value proposition—single-source responsibility from raw material to finished component—becomes unmatchable by focused players.

IX. Strategic Playbook & Lessons

The PTC story offers a masterclass in patient capital deployment in deep tech manufacturing—a game where winners are decided over decades, not quarters. While Silicon Valley celebrates blitzscaling and winner-take-all dynamics, PTC played a different game entirely: capability accumulation where each year's investment built on the last, creating compound advantages that accelerated over time.

Consider the sequencing of their strategic moves. They didn't start by targeting aerospace; they began with industrial castings, building fundamental capabilities in metallurgy and process control. Only after mastering the basics did they move to critical applications in oil and gas. Aerospace came only after decades of proving they could deliver zero-defect quality. Each phase built capabilities required for the next—a strategic staircase where skipping steps meant falling.

The timing of their aerospace entry reveals sophisticated market reading. They began investing in aerospace capabilities in 2016, when global aviation was booming and suppliers couldn't keep pace with demand. By the time they were certified and ready in 2019-2020, they had relationships and credibility. When COVID crashed aviation demand, lesser suppliers retreated. PTC doubled down, using the downturn to accelerate capability building. When demand roared back in 2023, they were one of the few suppliers ready with capacity and certification.

Their approach to indigenous technology development challenges conventional wisdom about emerging market manufacturers. Rather than licensing technology from developed markets—the standard playbook—PTC developed proprietary processes. This took longer, cost more, and risked failure. But it created genuine differentiation. When customers asked about their process capabilities, PTC could offer something unique, not just a cheaper version of Western technology.

Building trust in global supply chains from an emerging market requires playing a different game than established suppliers. PTC couldn't rely on reputation or relationships built over generations. Instead, they over-delivered systematically. If specifications called for 99.5% purity, they delivered 99.8%. If lead time was 12 weeks, they delivered in 10. This wasn't just good service; it was strategic trust-building, accumulating credibility deposits that would pay dividends when they asked customers to take bigger leaps of faith.

The management of customer concentration reveals sophisticated risk thinking. While 75% export concentration seems risky, dig deeper and you find hundreds of customers across multiple industries and geographies. No single customer exceeds 15% of revenue. This diversification within concentration—broad enough to mitigate single-customer risk but focused enough to build domain expertise—is harder to achieve than it appears.

The transition from industrial to aerospace customers required almost organizational schizophrenia. Industrial customers value cost, delivery, and "good enough" quality. Aerospace customers are willing to pay premium prices but demand perfection, documentation, and zero-defect delivery. Running both businesses simultaneously requires different systems, cultures, even languages. PTC managed this through organizational separation—ATL for aerospace, PTC for industrial—while sharing underlying technical capabilities.

Their capital raising strategy showed unusual sophistication for an Indian manufacturing company. Rather than diluting early when capital was expensive, they bootstrapped growth through customer advances and internal accruals. Only after achieving strategic position—aerospace certification, Tier-1 relationships—did they raise significant capital. The ₹700 crore QIP wasn't desperation financing; it was growth capital raised from a position of strength at attractive valuations.

The intellectual property strategy was counterintuitive. Rather than filing patents that would reveal process details, PTC kept innovations as trade secrets. Their competitive advantage wasn't in any single innovation but in the accumulation of thousands of small improvements over decades—what Japanese manufacturers call "kaizen" but applied to aerospace-grade casting. This tacit knowledge, embedded in people and processes rather than patents, proved harder to copy than documented innovations.

X. Future Roadmap & Risks

The numbers are staggering: India's defense budget climbing toward $100 billion, indigenous content requirements increasing to 70%, aerospace manufacturing predicted to reach $70 billion by 2030. For PTC, positioned at the intersection of these trends, the opportunity seems limitless. But the path from ₹1,000 crore to ₹10,000 crore in revenue isn't just about scaling what works—it's about navigating risks that multiply with success.

The immediate opportunity is almost overwhelming. India's defense modernization isn't incremental; it's a generational upgrade. The Light Combat Aircraft Tejas Mark-2, the fifth-generation Advanced Medium Combat Aircraft, nuclear submarine programs, indigenous jet engines—each requires thousands of tons of specialty materials PTC is uniquely positioned to supply. The mathematics are compelling: if India achieves even 50% of its stated defense production goals, PTC's domestic opportunity alone exceeds its current global revenue by multiples.

The global aerospace recovery adds another growth vector. Boeing and Airbus have backlogs approaching 15,000 aircraft—nearly a decade of production at maximum rates. Each aircraft contains tons of titanium and specialty alloys. As production ramps from COVID lows to meet this demand, supplier capacity becomes the bottleneck. PTC's timing—adding capacity just as demand explodes—could prove either prescient or lucky, but either way, profitable.

Yet customer concentration remains the sword of Damocles. Safran, IAI, BAE—losing any major customer would crater not just revenue but credibility. In aerospace, losing a customer signals quality problems, creating a cascade where other customers reconsider relationships. PTC's quality record is pristine so far, but aerospace is unforgiving. One failed component in service, one quality escape that causes an incident, and decades of reputation evaporates.

The technology disruption from additive manufacturing (3D printing) looms as an existential question. Why cast complex titanium components when you can print them? The technology promises reduced waste, unlimited complexity, and distributed production. Major aerospace companies are investing billions in additive capabilities. For PTC, this isn't just competition—it's potential obsolescence of their core capability.

But PTC's response shows strategic thinking. They're not fighting additive manufacturing; they're embracing it as complementary. Many 3D-printed components require cast substrates or traditionally manufactured critical sections. The powder metallurgy capabilities PTC is building for titanium production position them to supply raw materials for additive manufacturing. It's a hedge that could transform threat into opportunity.

Chinese competition presents a different challenge. Chinese titanium producers, backed by state capital and serving a massive domestic aerospace industry, are achieving scale PTC can't match. They're also moving upmarket, from simple components to complex assemblies. For non-defense applications, Chinese suppliers offer comparable quality at 30-40% lower prices. PTC's defense focus provides some insulation—Western defense contractors can't use Chinese suppliers—but commercial aerospace is fair game.

The working capital challenge intensifies with growth. Those 170-day receivables mean every ₹100 crore of additional revenue requires ₹50 crore of working capital financing. At projected growth rates, PTC needs ₹200-300 crore of additional working capital annually. This creates a vicious cycle: grow faster, need more capital, dilute more, pressure stock price. Breaking this requires either customer payment term improvements (unlikely given aerospace dynamics) or innovative financing structures.

Execution risks multiply with vertical integration. Running a foundry is complex enough; adding melting, rolling, and forging operations exponentially increases operational complexity. Each process has different chemistry, physics, and failure modes. A problem in melting affects casting affects delivery. The integrated model that creates competitive advantage also creates systemic risk where problems cascade rather than isolate.

The next phase—moving from components to assemblies—requires different capabilities entirely. Assembly means managing hundreds of suppliers, systems integration, software, electronics. It's a different business with different economics, skills, and risks. Many component suppliers have failed trying to move up the value chain. PTC's ambitions here are logical but fraught with execution challenges.

The regulatory environment adds uncertainty. India's defense procurement policies change with political winds. Offset requirements, indigenous content definitions, procurement preferences—all can shift, affecting demand patterns. Global trade policies add another variable. What if India-US relations deteriorate? What if Europe implements carbon border taxes that affect titanium imports? PTC operates at the intersection of industrial policy and geopolitics, exposed to risks beyond their control.

XI. Bear vs. Bull Case Analysis

The Bull Case: A Trajectory to ₹100,000 Crore Market Cap

The bulls see PTC as India's answer to Precision Castparts—Warren Buffett's $37 billion aerospace acquisition that proved specialty manufacturers can achieve technology valuations. Start with the structural tailwinds: India's defense spending must increase from 2% to 3% of GDP to meet strategic challenges, creating a ₹35,000 crore annual materials opportunity. PTC isn't just participating; they're the only Indian company with integrated titanium capabilities, making them essentially a monopoly in strategic materials.

The aerospace validation cascade has just begun. Safran was the first domino; expect Rolls-Royce, Pratt & Whitney, and GE to follow. Each relationship takes years to build but, once established, generates decades of revenue. At full capacity, the new titanium facility could generate ₹5,000 crore in revenue at 40% EBITDA margins—that alone justifies current valuations. Add the existing casting business, growing at 30% annually, and you're looking at ₹10,000 crore revenue potential by 2030.

Vertical integration creates margin expansion that's just beginning. Moving from casting (20% margins) to integrated materials-to-components (40% margins) doubles profitability on every rupee of revenue. As the product mix shifts toward proprietary materials and processes, PTC transforms from a manufacturing company to a materials science company—and markets pay very different multiples for those categories.

The optionality in the business model is underappreciated. PTC's capabilities—vacuum melting, precision casting, exotic alloy expertise—have applications beyond aerospace. Medical implants, semiconductor equipment, nuclear power, space technology—each represents billion-dollar adjacent markets PTC could enter with minimal additional investment. They're not just building an aerospace supplier; they're creating a platform for advanced materials applications.

Geopolitical dynamics create a sustainable moat. The US-China decoupling means Western aerospace companies must find non-Chinese suppliers for critical materials. India, as a democratic ally, becomes the default choice. This isn't just cost arbitrage that can be competed away; it's strategic alignment that creates decades-long partnerships. PTC benefits from being in the right country at the right time with the right capabilities.

The Bear Case: Priced for Perfection in an Imperfect World

The bears see a company priced at 60 times earnings in an industry where 15 times is considered expensive. Start with customer concentration: despite hundreds of customers, the top 10 likely drive 50%+ of revenue. Losing Safran alone would crater the stock. In aerospace, customer relationships can end overnight—one quality issue, one failed audit, one incident traced to your component, and you're radioactive for years.

The working capital dynamics are unsustainable. At 170 days receivables and projected growth rates, PTC needs ₹500 crore of additional working capital annually. That's either massive dilution or dangerous leverage—neither supports current valuations. And those payment terms won't improve; if anything, aerospace customers are extending payments as they manage their own cash flows post-COVID.

Execution risk is multiplying faster than revenue. PTC is simultaneously ramping aerospace production, building materials capability, entering defense markets, and expanding internationally. Each requires different skills, systems, and capital. History is littered with manufacturers who failed trying to do everything at once. The management team, while technically excellent, hasn't proven they can manage this complexity at scale.

Competition is coming from every direction. Chinese titanium producers have 10x PTC's scale and government backing. Western suppliers are establishing Indian operations to capture the same opportunity. New technologies like additive manufacturing could obsolete traditional casting. PTC is fighting multi-front war with limited resources against better-funded competitors.

The margin expansion story requires perfect execution. Moving from 20% to 40% margins sounds simple but requires flawless operations across complex, capital-intensive processes. One furnace failure, one contaminated heat, one process deviation can destroy millions in inventory and shut down production for weeks. The operational leverage that creates upside in good times becomes devastating in disruptions.

Global aerospace is cyclical, and we're near the peak. Order backlogs look impressive but remember 2001, 2008, 2020—aerospace demand can evaporate overnight. When airlines cancel orders, OEMs cut production, suppliers slash inventory. PTC's operating leverage means a 20% revenue decline could cause 50% profit collapse. The stock is priced as if aerospace only goes up; history suggests otherwise.

The technology disruption risk is existential. Additive manufacturing isn't complementary; it's replacement technology. Why would anyone cast complex shapes when 3D printing offers unlimited complexity with less waste? PTC's powder metallurgy investments are reactive, not proactive. They're playing catch-up in a technology race where established players have multi-year head starts and billion-dollar R&D budgets.

XII. Epilogue & Reflections

Standing in PTC's Lucknow facility, watching molten titanium flow into ceramic molds that will become jet engine components, you're witnessing more than manufacturing—you're seeing the physical manifestation of industrial policy, technological ambition, and patient capital allocation. The story that began with a modest foundry in 1963 has become something altogether different: a testament to what's possible when emerging market companies refuse to accept their assigned role in global value chains.

The PTC journey challenges several orthodoxies about manufacturing in emerging markets. First, that technical excellence can emerge anywhere, not just in traditional industrial centers. Lucknow had no aerospace cluster, no ecosystem of suppliers, no university cranking out aerospace engineers. PTC built capability through internal development, customer partnerships, and sheer persistence. Geography is destiny in many industries; PTC proved it doesn't have to be.

Second, that competing on quality rather than cost from an emerging market is not just possible but profitable. PTC's components aren't cheaper than Western alternatives; they're often more expensive. Customers pay premium prices for the combination of technical capability, supply chain flexibility, and strategic partnership PTC offers. This inverts the traditional emerging market playbook of competing on cost while accepting quality discounts.

The role of patient, technical entrepreneurship emerges as perhaps the most important lesson. PTC's founders and management didn't chase quick returns or fashionable sectors. They committed to deep technical capability building over decades, accepting lower returns initially for the possibility of exceptional returns eventually. In an era of quarterly capitalism, PTC played a game measured in decades—and won.

India's evolving position in global aerospace supply chains reflects broader shifts in global manufacturing. The pandemic exposed the fragility of concentrated supply chains; the US-China tensions revealed the strategic vulnerability of depending on geopolitical rivals for critical materials. India, democratic but non-aligned, English-speaking but independent, emerges as the natural hedge. PTC didn't create these dynamics, but they positioned perfectly to benefit from them.

The surprises in the PTC story are what make it compelling. Who would have predicted that a Lucknow foundry would supply Safran? That India would build titanium melting capability before semiconductor fabs? That aerospace manufacturers would trust emerging market suppliers with flight-critical components? These outcomes seemed impossible until they happened, reminding us that industrial development follows no predetermined path.

The non-obvious insight is that manufacturing moats in the 21st century aren't built on scale or capital but on trust and capability accumulation. PTC's competitive advantage isn't their furnaces or certifications—competitors can buy those. It's the decades of accumulated knowledge, relationships, and credibility that create customer confidence. In industries where failure means catastrophe, trust is the ultimate currency, and trust can't be bought, only earned over time.

Looking forward, PTC represents a broader template for industrial development in emerging markets. Don't accept your position in existing value chains; create new ones. Don't just transfer technology; develop indigenous capabilities. Don't compete on cost; compete on unique value. Don't think quarters; think decades. It's a playbook that requires patience, capital, and courage—but as PTC proves, the payoff can be extraordinary.

The final reflection is about what PTC means for India's industrial ambitions. For decades, India's manufacturing champions were in low-value sectors—textiles, generic pharmaceuticals, automotive components. PTC represents something different: a globally competitive player in the most demanding manufacturing sector that exists. If a Lucknow foundry can become a trusted supplier to Safran and BAE Systems, what else is possible?

The titanium ingot that began this story—glowing in vacuum, destined for aerospace glory—is more than metal. It's materialized ambition, decades of capability building made tangible, proof that emerging market manufacturers can compete at the highest levels of global industry. PTC's story isn't complete; in many ways, it's just beginning. But what they've achieved already rewrites the rules about what's possible in global manufacturing from unexpected places.

The question isn't whether PTC will succeed in their ambitious plans—scaling to ₹10,000 crore revenue, becoming India's aerospace materials champion, enabling indigenous defense production. The question is what their success means for the hundreds of other specialized manufacturers across India, watching and learning, preparing their own assaults on global value chains. PTC didn't just build a company; they built a proof point that Indian manufacturing can compete on quality, not just cost, in the most demanding industries on earth.

That might be their greatest contribution: not the titanium castings or aerospace components, but the demonstration effect, the proof that it's possible, the path illuminated for others to follow. In the end, industrial development isn't just about individual companies succeeding; it's about ecosystems emerging, capabilities spreading, ambitions rising. PTC's story, still being written in molten metal and certified quality, is really India's story—a nation refusing to accept its assigned place in global value chains, insisting instead on writing its own industrial future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube