PTC India: From Power Trading Pioneer to Energy Market Architect

I. Introduction & Opening Hook

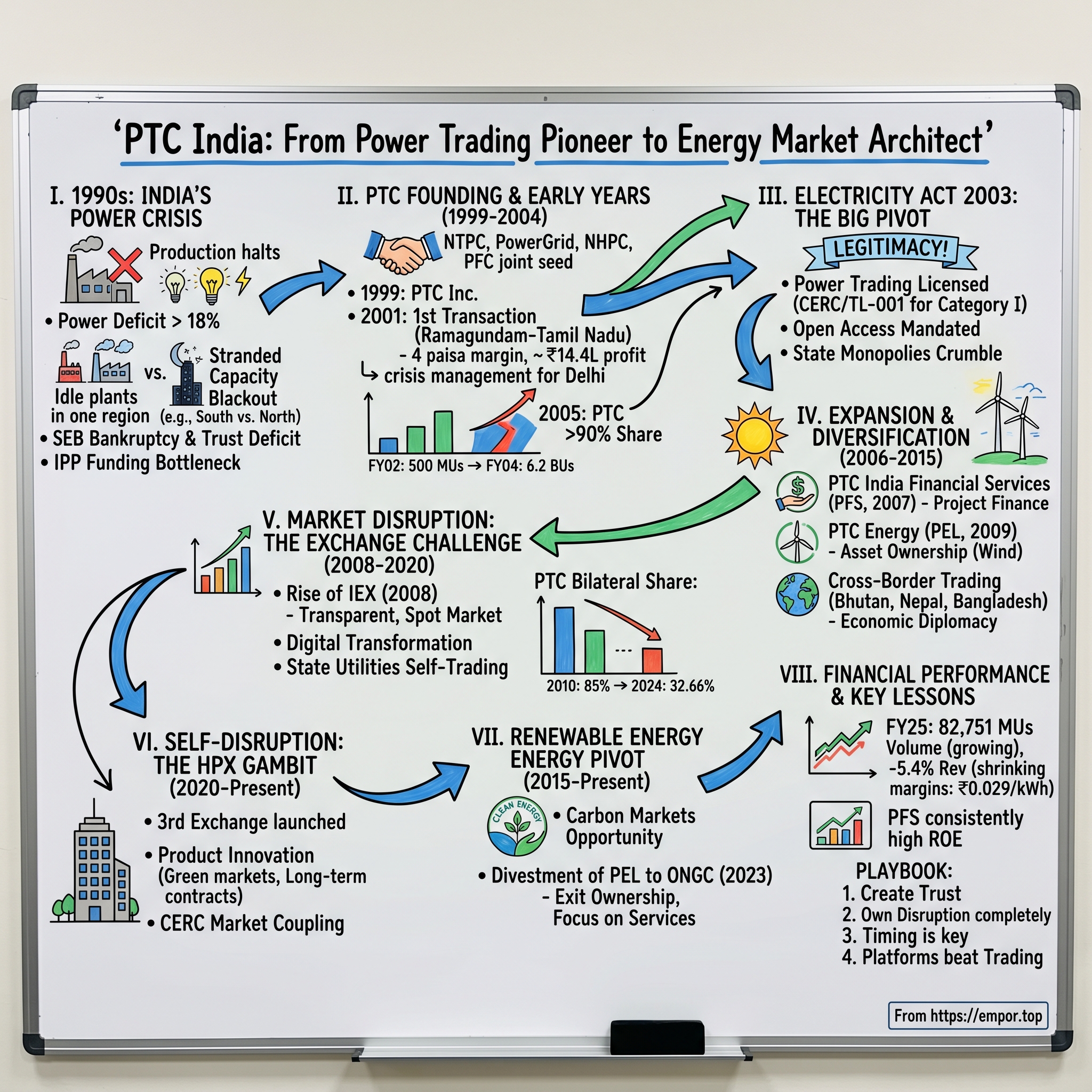

Picture this: It's 1999, and India's power sector is in chaos. Entire cities plunge into darkness for hours daily. Industries shut down production lines. Villages have never seen electric light. Yet in one corner of the country, power plants sit idle with excess capacity while another region desperately needs every megawatt it can get. The grid infrastructure exists to connect them, but there's no mechanism—no market, no trader, no trusted intermediary—to move power from surplus to deficit regions.

Enter PTC India, a company that would not just trade power but essentially create India's power trading market from scratch. How did this government-initiated startup capture over 90% market share, watch it erode to 32% as the very exchanges it helped create ate its lunch, and still remain the country's largest power trader? This is a story of market creation, self-disruption, and the fundamental question every infrastructure company faces: do you remain the pipes or become the platform? Today, PTC India trades 82,751 Million Units (MUs) annually, making it the country's largest power trader with 32.66% market share. The company that began as a desperate solution to India's crippling power crisis has evolved into something far more complex: a conglomerate spanning power trading, financial services, renewable energy, and now, power exchanges.

This is the Acquired-style deep dive into PTC India—a company that quite literally created its own market, then watched as that very market began to eat away at its dominance. It's a tale of government initiative meeting private enterprise, of monopolies crumbling under the weight of their own success, and ultimately, of whether a market creator can survive the market it created.

II. Pre-Formation Context: India's Power Crisis (1990s)

In 1991, as India embarked on economic liberalization, the power sector remained trapped in a socialist nightmare. State Electricity Boards (SEBs) controlled generation, transmission, and distribution with the efficiency of a government ration shop. Industrial production would halt mid-shift when the grid failed. Urban households invested in inverters and generators like they were buying insurance policies. Rural India? Many villages had never seen an electric bulb illuminate.

The numbers were staggering. Peak power deficit routinely exceeded 18%. Energy shortage touched 11%. But here's the maddening part: while northern states suffered 8-10 hour power cuts daily, southern states like Karnataka had surplus capacity sitting idle. Himachal Pradesh's hydroelectric plants generated excess power during monsoons that nobody could buy. Tamil Nadu's thermal plants ran at partial capacity while industries in Punjab begged for electricity. The infrastructure existed—220kV and 400kV transmission lines crisscrossed the nation—but there was no mechanism to move power from surplus to deficit regions.

The government's mega power policy of 1995 aimed to add 40,000 MW through private investment. Independent Power Producers (IPPs) lined up with proposals. International players like Enron (remember Dabhol?) entered with fanfare. But they faced a fundamental problem: who would buy their power? SEBs were essentially bankrupt, notorious for payment defaults. Banks wouldn't finance projects without payment security. IPPs couldn't sign Power Purchase Agreements (PPAs) without creditworthy counterparties.

This wasn't just an infrastructure problem—it was a trust deficit. A generator in Chhattisgarh didn't trust an SEB in Maharashtra to pay for power. An IPP with a 25-year investment horizon couldn't bet on the creditworthiness of a state utility that changed leadership every election cycle. The sector needed an intermediary, a trusted broker who could aggregate demand, guarantee payments, and create a market where none existed.

By 1998, the Ministry of Power recognized this gap. India didn't just need more generation capacity—it needed a power market. Other countries had power trading companies. Nordic countries had Nord Pool. The UK had its bilateral trading system post-deregulation. Even within India, some informal power banking arrangements existed between states, but these were ad-hoc, seasonal, and often politically motivated.

The solution emerged from an unlikely place: not from private enterprise, but from the very public sector companies that epitomized the old system. NTPC, PowerGrid, Power Finance Corporation (PFC), and NHPC—the four horsemen of India's public power sector—came together with a radical proposal. They would seed a power trading company, provide initial capital and credibility, but run it as a commercial entity. This public-private hybrid would become PTC India, incorporated on April 16, 1999.

The timing was both perfect and terrible. Perfect because India desperately needed this institution. Terrible because power trading as a concept didn't legally exist. There was no regulatory framework, no licenses, no rules. PTC would have to create the market while simultaneously proving the market needed to exist. They were building the plane while flying it, with the entire power sector watching skeptically from the ground.

III. The Founding Story & Early Years (1999-2004)

The boardroom at NTPC's headquarters in April 1999 witnessed an unusual gathering. Four public sector giants—NTPC, PowerGrid, PFC, and NHPC—were birthing a private company. Each brought something critical to the table: NTPC had generation expertise and surplus power, PowerGrid controlled transmission corridors, PFC understood project finance, and NHPC brought hydroelectric trading experience from their seasonal surplus management. Together, they capitalized PTC India with ₹10 crores, a laughably small amount for the ambition at hand.

The first CEO, a former NTPC executive who understood both the technical and political complexities of Indian power, faced an immediate challenge: PTC existed in a legal grey zone. Power trading wasn't recognized as a distinct activity under the Indian Electricity Act of 1910 or even the Electricity Supply Act of 1948. Technically, what PTC proposed to do—buy power from one entity and sell to another for profit—could be challenged as illegal arbitrage.

July 2001 marked PTC's first real transaction, and it was vintage India: complicated, multi-party, and requiring political finesse. A textile mill cluster in Coimbatore needed 50 MW urgently to fulfill an export order. Tamil Nadu's grid was deficit. But NTPC's Ramagundam plant in Telangana had spare capacity. The problem? No commercial mechanism existed for inter-state power transactions beyond government-to-government arrangements.

PTC's solution was ingenious. They signed back-to-back agreements: buying from NTPC at ₹2.20 per unit, adding a trading margin of 4 paise, and selling to the Tamil Nadu utility at ₹2.24. They convinced State Bank of India to open a letter of credit for payment security. PowerGrid allocated transmission corridor. What should have been a simple transaction took three months of negotiations, but it worked. That 4 paise margin on 50 MW for 30 days generated PTC's first profit: roughly ₹14.4 lakhs.

By 2002, PTC had cracked the code. They developed standard contracts that SEBs could sign without lengthy negotiations. They created a payment security mechanism using escrow accounts that gave generators confidence. Most importantly, they built a trading desk that operated 24/7, matching supply and demand in real-time—something unheard of in India's power sector where everything moved at government speed.

The numbers started compounding. FY2002: 500 million units traded. FY2003: 2.8 billion units. FY2004: 6.2 billion units. Trading margins expanded from 4 paise to 6-8 paise per unit as PTC's value became evident. Revenue jumped from ₹24 crores to ₹193 crores in just two years. They were signing up every IPP desperate for payment security and every SEB looking for reliable supply.

But the real breakthrough came from an unexpected quarter. The Delhi government, facing severe power crisis in summer 2003, approached PTC in desperation. Could PTC arrange 300 MW immediately? Within 48 hours, PTC had aggregated power from six different sources across four states, managed transmission corridor allocation, and arranged payment security. Delhi's lights stayed on. The media coverage was enormous. Suddenly, PTC wasn't just a trading company—they were crisis managers, problem solvers, the guys you called when the grid was failing.

This success attracted attention from international players. Glencore, the global commodity trading giant, approached PTC for a joint venture. Morgan Stanley wanted to understand the Indian power market through PTC's lens. The World Bank cited PTC as a model for power market development in emerging economies. The company that didn't legally exist three years ago was now being studied at Harvard Business School.

The momentum made the IPO decision inevitable. In March 2004, PTC filed its red herring prospectus, seeking to raise ₹93.6 crores at ₹16 per share. The offering was modest—just 25% equity dilution—but the response was electric. The issue was oversubscribed 1.6 times, with institutional investors taking up 82% of the offer. On April 7, 2004, PTC listed on NSE at ₹16.80, a 5% premium. Not spectacular, but solid.

What investors were really buying wasn't just a trading company—it was optionality on India's power market development. The Electricity Act 2003, passed just months before the IPO, had legitimized PTC's business model. Power trading was now officially recognized as a licensed activity. Open access was mandated. Multiple generators and multiple buyers could now transact freely. The market PTC had illegally pioneered was now legally sanctioned. The rebel had become the establishment.

IV. The Electricity Act 2003: Power Trading Gets Legal Recognition

The Electricity Act 2003 wasn't just legislation—it was vindication. For four years, PTC had operated in legal limbo, their entire business model hanging on creative interpretations of archaic electricity laws. Now, with one stroke of the President's pen, power trading became a recognized, licensed activity under Section 12 of the Act. PTC's pioneering service had literally written itself into law.

The Central Electricity Regulatory Commission (CERC) moved quickly to establish the framework. By June 2004, they had issued the first power trading licenses, creating three categories. Category I—unlimited trading volumes, no restrictions. Category II—inter-state trading with volume caps. Category III—intra-state trading only. PTC, unsurprisingly, received the first Category I license, Serial Number CERC/TL-001. It was like being handed license plate number 1 in a country that just discovered automobiles.

But the real revolution was open access. Section 42 of the Act mandated that transmission and distribution networks must provide non-discriminatory access to all players. Any generator could sell to any consumer above 1 MW consumption, using the transmission highway. State utilities lost their monopoly overnight. This wasn't deregulation—it was demolition of six decades of state control.

PTC's trading floor in their Barakhamba Road office became the nerve center of India's emerging power market. Twenty traders worked in shifts, manning phones that connected to every major generator and distribution company. They had developed proprietary software that tracked real-time generation across 200+ power plants, transmission corridor availability across PowerGrid's network, and demand patterns from 28 states. This was high-frequency trading before anyone in India knew what that meant.

The margins were intoxicating. While the regulated trading margin was capped at 4 paise per unit by CERC, PTC was earning much more through structured products. A typical deal: Karnataka needed 200 MW for its summer peak. PTC would aggregate 50 MW from NTPC's surplus, 75 MW from a Gujarat IPP, 40 MW from Chhattisgarh captive plants, and 35 MW from merchant capacity. Each source had different pricing, payment terms, and transmission charges. PTC's skill was in packaging this into a single contract for Karnataka at a blended rate that still left 6-8 paise margin per unit.

By FY2005, PTC was trading 12 billion units annually. Market share? North of 90%. The only competition came from state utilities doing bilateral trades, but these were relationship-based, not market-based. When Reliance wanted to sell surplus power from their Jamnagar refinery, they called PTC. When Delhi Metro needed assured supply for their expanding network, they called PTC. When Bhutan's massive Tala hydro project needed an Indian off-taker, they called PTC.

The Bhutan story deserves special mention. In 2005, Bhutan was commissioning the 1,020 MW Tala project, their largest infrastructure investment ever. The entire output was meant for India, but managing payments from multiple Indian buyers, transmission scheduling, and seasonal variations was complex. PTC stepped in as the sole aggregator, signing a government-to-government backed agreement. They would buy Tala's entire output and redistribute it across India, ensuring Bhutan got paid on time, every time. This wasn't just trading—it was economic diplomacy.

Competition was inevitable but came slower than expected. In 2006, Adani entered power trading, leveraging their generation assets. In 2007, Tata Power Trading launched, using their century-old utility relationships. Smaller players like Jindal and Lanco started trading arms. But PTC's first-mover advantage was insurmountable. They had the relationships, the payment security mechanisms, the transmission corridor allocations, and most importantly, the trust.

The numbers reflected this dominance. FY2006: Revenue ₹478 crores, PAT ₹38 crores. FY2007: Revenue ₹743 crores, PAT ₹52 crores. The stock, which had listed at ₹16, touched ₹54 by end of 2007. P/E multiples of 35x—the market was pricing PTC not as a trading company but as the infrastructure for India's power market.

But within PTC's boardroom, a strategic debate was brewing. Should they remain pure traders, taking minimal balance sheet risk and earning regulated margins? Or should they become something bigger—a full-stack energy company with generation assets, financial services, and yes, even their own exchange? The decision they made would define the next decade and plant the seeds of their own disruption.

V. Expansion & Diversification: Building an Energy Conglomerate (2006-2015)

The conference room on the 7th floor of PTC's new headquarters at August Kranti Marg hummed with tension in September 2006. The board was reviewing a radical proposal: instead of just trading power, why not finance power projects? The logic was compelling. PTC's trading desk saw every project in the country—they knew which developers delivered, which PPAs were bankable, which state utilities paid on time. This information asymmetry was worth monetizing.

PTC India Financial Services (PFS) was born in March 2007 with a ₹200 crore capital commitment. But this wasn't just another infrastructure finance company. PFS would focus exclusively on energy value chain financing—generation, transmission, distribution, fuel supply, equipment manufacturing. The CEO, poached from ICICI's project finance division, brought a team that understood both banking and power sectors. Within six months, PFS had sanctioned ₹1,000 crores to wind projects in Tamil Nadu, small hydro in Himachal, and biomass plants in Punjab.

The timing was perfect. India's 11th Five Year Plan targeted 78,000 MW capacity addition. Banks were hitting sectoral exposure limits to power. NBFCs were wary of 20-year project loans. PFS filled this gap with structured products: construction finance that converted to term loans, equipment financing for Chinese wind turbines that Indian banks wouldn't touch, bridge loans for developers awaiting equity infusion. By 2010, PFS's loan book exceeded ₹5,000 crores.

While PFS was financing others' projects, PTC decided to own generation assets themselves. PTC Energy Limited (PEL), incorporated in 2009, started acquiring wind projects. The strategy was opportunistic—buy distressed assets from over-leveraged developers, improve capacity utilization through better maintenance, and sell power through PTC's trading desk. The first acquisition: a 28 MW wind farm in Karnataka bought at 40% of project cost from a defaulting textile company.

By 2013, PEL owned 288.8 MW of wind capacity across Madhya Pradesh, Karnataka, and Andhra Pradesh. These weren't trophy assets—they were trading tools. When Tamil Nadu needed emergency power during wind season, PEL could supply immediately. When renewable energy certificates (RECs) traded at premium, PEL generated extra revenue. The vertical integration was working—PTC traded the power, PFS financed the projects, PEL owned the assets.

But the masterstroke was cross-border trading. Nepal's 60 MW Khimti project was struggling to evacuate power to India due to transmission constraints and payment issues. PTC structured an innovative solution: they would buy the entire output, manage transmission through the Muzaffarpur-Dhalkebar cross-border line, and aggregate demand from Bihar and UP utilities. The deal required negotiations with four governments, but PTC pulled it off.

Bangladesh came next. Their persistent power shortage needed 250 MW imports from India. PTC became the designated nodal agency, managing everything from transmission scheduling to currency hedging. The complexity was staggering—power flowed from NTPC plants in West Bengal, through the Indian grid, across the Bheramara-Baharampur interconnection, into Bangladesh's grid, all while managing two currencies, two regulatory regimes, and real-time load variations.

By FY2014, cross-border trading contributed nearly 24% of PTC's volumes, with Bhutan alone accounting for 15 billion units annually. This wasn't just business—PTC had become an instrument of India's neighborhood diplomacy. When Bangladesh faced acute shortage, PTC arranged emergency supply within hours. When Bhutan's hydro projects needed evacuation during surplus monsoon generation, PTC found buyers across India.

The diversification seemed to be working. FY2015 revenue crossed ₹15,000 crores. The stock touched ₹45, giving PTC a market cap over ₹1,300 crores. Three listed entities in the group—PTC, PFS (which IPO'd in 2011), and soon PEL—created a holding company structure that analysts loved. This was no longer a trading company but an integrated energy conglomerate.

Yet, beneath this success, structural shifts were occurring. Power exchanges, which PTC had helped establish, were gaining volume. Industrial consumers were buying directly from generators. State utilities were developing their own trading capabilities. The market PTC had created was evolving beyond PTC's control. The question wasn't whether disruption would come, but whether PTC would disrupt itself or be disrupted.

VI. The Market Disruption: Rise of Power Exchanges (2008-2020)

The irony was delicious. In 2007, PTC's board approved a ₹8 crore investment to co-promote Indian Energy Exchange (IEX) along with Financial Technologies. They were literally funding their own disruption. The logic seemed sound then—exchanges would handle spot transactions while PTC focused on term contracts. Exchanges needed traders to provide liquidity. It would be a symbiotic relationship. That assumption would prove catastrophically wrong.

IEX launched on June 27, 2008, with a single product: day-ahead electricity contracts for next-day delivery. First day volume: 45 MW. PTC's traders, watching from their dealing room, weren't worried. They were moving 200,000 MW daily through bilateral contracts. What could an electronic exchange matching buyers and sellers for tomorrow's power do to their business of managing month-long, year-long, even 25-year PPAs?

By 2010, the answer was becoming clear. IEX wasn't just matching orders—they were creating price discovery. For the first time in India's history, there was a transparent, real-time price for electricity. Every generator, every consumer, every trader could see what power was worth at any given moment. The Kashmir winter price spike, the May afternoon surge, the monsoon surplus collapse—all visible on a screen. This transparency was revolutionary and threatening in equal measure.

Power Exchange India Limited (PXIL), backed by NSE and NCDEX, launched in October 2008, creating competition in exchanges themselves. But IEX's first-mover advantage proved insurmountable. By 2012, IEX commanded 98% of exchange volumes. PXIL struggled at 2%. The network effects were brutal—liquidity attracted more liquidity, creating a winner-take-all dynamic that PTC understood from their own monopoly experience.

The numbers told the story of disruption. Exchange volumes grew from 2.8 billion units in FY2010 to 28 billion units in FY2015 to 52 billion units in FY2020. More importantly, the nature of trading changed. Earlier, a distribution company needing power would call PTC, negotiate terms, sign contracts, arrange payment security—a process taking days or weeks. Now, they could log into IEX, place an order, and receive power the next day. No negotiation, no relationship management, no trading margin beyond the minimal exchange fee.

PTC's response was textbook innovator's dilemma. They couldn't abandon bilateral trading—it still formed 80% of volumes and generated higher margins. But they couldn't ignore exchanges either. They became the largest trader on IEX, using it for balancing their bilateral positions. When their long-term contract had surplus, they sold on IEX. When they faced deficits, they bought from IEX. They were simultaneously IEX's biggest customer and biggest competitor.

The market share erosion was relentless but gradual. FY2010: PTC at 85% of bilateral trading. FY2015: 58%. FY2020: 41%. FY2024: 32.66%. Every year, a few percentage points shifted to exchanges or aggressive competitors like Adani and Tata Power Trading. PTC remained the largest trader by volume, but the moat was shrinking. Margins compressed from 6-8 paise to 3-4 paise per unit as competition intensified.

Management's strategy sessions became increasingly tense. Should they fight exchanges by offering better terms on bilateral contracts? Should they focus on complex, structured products that exchanges couldn't handle? Should they double down on cross-border trading where their government relationships provided an edge? Every option had merit, but none addressed the fundamental disruption.

The pandemic accelerated the shift. During the 2020 lockdown, when physical meetings were impossible and documentation was challenging, exchange volumes surged. Industries preferred the simplicity of click-and-buy power over complex negotiations. Even state utilities, traditionally relationship-driven, started using exchanges for their short-term requirements. The digital transformation that PTC had resisted was being forced upon the entire sector.

By late 2020, PTC's board made a decision that shocked the market: they would launch their own exchange. If you can't beat disruption, lead it. But this time, they wouldn't just be a co-promoter. They would be the primary sponsor of India's third power exchange, eventually named Hindustan Power Exchange (HPX). The student would become the teacher, the disrupted would become the disruptor. Whether this gambit would succeed remained to be seen.

VII. The Third Exchange Gambit: HPX/Pranurja (2018-Present)

The email from CERC arrived on August 20, 2020: "Application approved for establishing India's third power exchange." PTC's CEO read it twice. After two years of regulatory battles, shareholding restructuring, and skeptical market commentary, Hindustan Power Exchange had clearance to operate. But approval was just the beginning of an uphill battle against IEX's 98% market dominance.

The genesis traced back to 2018 when PTC incorporated Pranurja Solutions Limited with BSE and ICICI Bank. The shareholding structure itself told a story of regulatory chess. CERC regulations capped promoter ownership at 25% each, forcing PTC, BSE, and ICICI to dilute from their initial 33% holdings. European Energy Exchange (EEX) was brought in for technology. State utilities like Gujarat and Haryana were offered stakes for political cover. The cap table looked like a UN Security Council—everyone had a voice, nobody had control.

HPX's strategy differentiated itself through product innovation. While IEX focused on day-ahead and term-ahead markets, HPX launched with longer-duration contracts—weekly and monthly products that bridged the gap between spot and bilateral markets. They introduced India's first green term-ahead market, allowing renewable generators to sell power for future delivery. The technology platform, built by EEX, offered features IEX didn't: multi-currency settlement for cross-border trades, sophisticated hedging instruments, and API-based trading for algorithmic players.

But technology alone doesn't break monopolies. HPX needed liquidity, and liquidity needed anchors. PTC committed to routing 30% of their short-term trades through HPX. BSE leveraged its relationships with financial institutions. ICICI brought corporate clients. Yet after six months of operations, HPX's market share struggled at 2-3%. The same network effects that had crushed PXIL were working against HPX.

The game-changer came from an unexpected regulatory intervention: market coupling. In September 2021, CERC proposed that all three exchanges should discover price jointly while maintaining separate operations. Instead of three fragmented markets with different prices for the same delivery slot, there would be one unified price discovery with orders routed to achieve best execution. European markets had implemented similar coupling successfully. India would be the first Asian market to attempt it.

IEX fought viciously. Their petitions to CERC argued market coupling would destroy innovation, increase operational complexity, and benefit inefficient exchanges at the cost of efficient ones. Translation: it would destroy their monopoly. The legal battles stretched through 2022, with stay orders, appeals, and counter-appeals. PTC, through HPX, found itself in the unusual position of fighting its own co-promoted entity from 2007.

Behind the legal drama, HPX was building alliances. Distribution companies frustrated with IEX's dominance quietly supported competition. Renewable generators liked HPX's green market initiatives. Industrial consumers appreciated the longer-duration products. By FY2023, HPX had captured 6% market share—small, but growing. Revenue crossed ₹50 crores. The exchange was operationally profitable, a milestone PXIL took five years to achieve.

The strategic value went beyond direct economics. HPX gave PTC intelligence on price formation, order flow, and market microstructure. When a large industrial needed 500 MW for next month, HPX saw the order first, allowing PTC's trading desk to position accordingly. When renewable generators wanted to sell forward contracts, HPX's platform provided the matching engine while PTC provided the counterparty. The exchange and trading businesses created synergies neither could achieve alone.

Market coupling finally went live in April 2024, despite IEX's protests. Early results were mixed. Price convergence happened as expected, but operational glitches frustrated participants. HPX's share increased to 8%, partly due to coupling, partly due to IEX's customers experimenting with alternatives. PXIL, surprisingly, benefited most, jumping from 1% to 4% share as coupling reduced IEX's routing advantages.

The billion-dollar question remained unanswered: Could HPX ever meaningfully challenge IEX? The precedents weren't encouraging. Globally, first-mover power exchanges retained dominance—Nord Pool in Scandinavia, EEX in Germany, PJM in the US. But India's power market was still nascent, growing 15% annually. If HPX could capture even 20% share of a market expected to reach 500 billion units by 2030, the economics would be transformative. The third exchange gambit was a long game, and PTC was playing it with the patience of a company that had spent decades building markets from scratch.

VIII. Renewable Energy Pivot & Green Markets (2015-Present)

The morning of December 12, 2015, as negotiators in Paris hammered out the climate agreement, PTC's strategy team huddled in their Delhi office with a different concern. India had just announced a 175 GW renewable energy target by 2022. Solar costs were plummeting. Wind capacity was exploding. The entire economics of power trading—built on moving thermal power from coal plants—was about to be disrupted by intermittent, decentralized, zero-marginal-cost renewable energy.

PTC's first response was tactical: become the largest trader of renewable energy. They signed agreements with every major wind and solar developer. ReNew Power's 500 MW portfolio, Adani Green's Tamil Nadu projects, Azure's rooftop solar aggregation—PTC traded them all. But renewable trading was fundamentally different. A coal plant could guarantee 100 MW round-the-clock. A solar farm produced nothing at night and peaked unpredictably based on cloud cover. Wind generation varied hourly. This intermittency made bilateral contracts challenging and pushed volumes toward exchanges where real-time matching was easier.

The Renewable Energy Certificate (REC) market offered better opportunities. Introduced in 2011, RECs allowed renewable generators to separate the green attributes from electricity and trade them independently. PTC became the dominant REC trader, handling 40% of volumes by 2016. When textile mills in Tamil Nadu needed RECs to meet renewable purchase obligations, PTC sourced them from wind farms in Gujarat. When distribution companies faced penalties for missing green targets, PTC arranged emergency REC procurement. The margins—₹50-100 per REC—were multiples of electricity trading margins.

CRISIL's SP 1A rating, the highest grade under Ministry of New and Renewable Energy's (MNRE) framework, gave PTC credibility in the renewable sector. But credibility wasn't enough. The company needed assets. Through PEL, they had accumulated 288.8 MW of wind capacity, but these were aging assets with 15-20% capacity factors. The new generation of wind turbines achieved 35-40%. Solar was reaching grid parity. The build-versus-buy decision became critical.

The board chose a hybrid approach. For solar, PTC would trade but not own, recognizing that Chinese manufacturers and aggressive developers like Adani and Azure had structural advantages. For wind, they would modernize existing assets through repowering—replacing old 500 kW turbines with modern 2 MW machines on the same land. For emerging technologies like battery storage and green hydrogen, they would wait and watch, using their trading platform to understand economics before committing capital.

The Green Day Ahead Market (GDAM), launched on IEX in October 2021, created new opportunities. For the first time, renewable energy could be traded separately from conventional power with distinct price discovery. PTC leveraged their renewable relationships to become the largest GDAM trader within months. When Rajasthan's solar farms had surplus generation during winter afternoons, PTC found buyers in Delhi's commercial complexes seeking green power. When Karnataka's wind farms peaked during monsoons, PTC exported the green electricity to industries meeting sustainability targets.

But the renewable transition also threatened PTC's core business. Peer-to-peer renewable trading platforms were emerging, allowing solar rooftop owners to sell directly to neighbors. Blockchain-based energy trading promised to eliminate intermediaries. Battery storage would reduce the need for real-time balancing that traders provided. The distributed energy future might not need PTC at all.

The strategic response came in 2023: exit ownership, focus on trading and services. The decision to divest PEL to ONGC for ₹175 crores seemed like retreat, but it was actually advancement. Owning 289 MW of aging wind assets tied up capital and management bandwidth while contributing marginally to profits. Trading 10,000 MW of renewable power generated better returns with zero balance sheet risk. The sale also crystallized a one-time gain of ₹457 crores, delighting investors who saw it as value unlocking.

Carbon markets represented the next frontier. As India prepared to launch its own carbon trading scheme in 2024, PTC positioned itself as the natural intermediary. They had relationships with every major emitter through power trading. They understood certificate markets from REC trading. When CERC released draft carbon credit regulations in November 2024, PTC was among the first to apply for carbon trading authorization.

The renewable pivot was working, partially. Green power trading volumes grew 30% annually. REC trading remained profitable. Carbon markets showed promise. But these couldn't fully offset the structural decline in thermal power trading margins. The fundamental question persisted: In a renewable-dominated grid with peer-to-peer trading and real-time balancing through batteries, what role would a traditional power trader play? PTC's answer would determine whether they remained relevant in India's energy transition or became a fossil fuel-era relic.

IX. Financial Performance & Market Dynamics

The numbers tell a story of resilience and erosion in equal measure. FY2025 trading volume reached 82,751 Million Units, a 10.5% increase from the previous year. Yet revenue declined 5.4% to ₹15,546 crores. This paradox—growing volumes, shrinking revenue—encapsulated PTC's fundamental challenge. Trading margins had compressed to ₹0.029 per kWh, barely covering operational costs.

The margin compression wasn't just competition—it was structural. CERC's trading margin regulations, designed to prevent profiteering, capped margins at 7 paise per unit for inter-state trading. But market forces pushed realized margins even lower. When five traders competed for the same bilateral deal, margins collapsed to 2-3 paise. When exchanges offered instant execution at 0.5 paise equivalent cost, bilateral traders had little pricing power.

Segment analysis revealed the strategic shifts. Long-term trading, once 60% of volumes, had shrunk to 35% as generators preferred merchant sales during high price periods. Medium-term contracts, typically 3-month to 1-year duration, held steady at 30%, offering better margins than spot but less commitment than long-term. Short-term trading, the most competitive segment, had grown to 35% of volumes but contributed only 20% of profits.

Cross-border trading partially offset domestic margin pressure. The Bhutan portfolio, with government-to-government backing and limited competition, maintained 8-10 paise margins. Nepal trades, though smaller, generated 12-15 paise through complex transmission management. Bangladesh exports, requiring real-time coordination across two grids, justified 6-8 paise margins. Together, cross-border contributed 30% of profits despite being 24% of volumes.

The subsidiary performance painted a mixed picture. PFS, the financing arm, consistently delivered 15-18% ROE with a loan book exceeding ₹8,000 crores. Their net interest margins of 3.5% seemed massive compared to PTC's trading margins. The market valued PFS at ₹2,800 crores, almost 60% of PTC's own market cap, raising questions about sum-of-parts valuation.

HPX remained subscale but improving. FY2024 revenue of ₹73 crores and operational profit of ₹8 crores validated the exchange model, but the ₹450 crore investment hadn't yet generated acceptable returns. Market coupling implementation in 2024 boosted prospects, but IEX's dominance remained daunting. Analysts modeled scenarios where HPX captured 20% share by 2030, implying a ₹2,000 crore valuation, but execution risk was substantial.

Competition dynamics had fundamentally changed. The top five traders controlled 78.74% of market share—PTC at 32.66%, NTPC Vidyut Vyapar Nigam (NVVN) at 17.21%, Adani at 11.03%, Tata Power Trading at 10.30%, and Arunachal Pradesh Power Corporation at 7.54%. Each brought different advantages: NVVN had government backing, Adani had generation assets, Tata had century-old utility relationships. PTC's traditional advantages—first-mover status, payment security mechanisms, regulatory relationships—were neutralizing.

Stock performance reflected this transition. From the IPO price of ₹16 in 2004, PTC had delivered a 20-year CAGR of merely 8.5%, underperforming both Nifty and power sector indices. The dividend yield of 7%+ attracted value investors, but growth investors had long departed. P/E multiples of 6-7x suggested the market viewed PTC as a mature, ex-growth utility rather than a dynamic trading platform.

Working capital management became crucial as margins thinned. PTC's receivable days increased from 45 to 73 as payment delays from state utilities worsened. The company maintained ₹2,000+ crores in receivables at any point, essentially providing free credit to the power sector. Interest costs on working capital borrowings often exceeded trading margins on underlying transactions. The business model was becoming working capital arbitrage rather than value-added trading.

The bull case rested on market growth overwhelming share loss. India's power demand was growing 7% annually. By 2030, short-term market volumes could reach 500 billion units. Even with 25% market share, PTC would trade 125 billion units, 50% higher than current volumes. At normalized margins of 4 paise, this implied profit potential of ₹500 crores from trading alone. Add PFS's growing loan book, HPX's potential exchange upside, and carbon market opportunities—the sum-of-parts could justify ₹8,000-10,000 crore valuation.

The bear case was equally compelling. Exchanges would continue grabbing share. Margins would compress further. Cross-border opportunities were limited by transmission constraints. Renewable trading favored real-time platforms over bilateral contracts. Carbon markets might bypass traditional intermediaries. In this scenario, PTC becomes a melting ice cube—profitable today but shrinking toward irrelevance. The next decade would determine which narrative prevailed.

X. Playbook: Lessons from India's Power Market Pioneer

Creating Markets from Nothing

PTC's first lesson is profound: sometimes the market doesn't exist because nobody tried to create it. In 1999, everybody knew India needed power trading, but nobody knew how to start. PTC's founders didn't wait for perfect regulations or proven models. They started trading in legal grey zones, created standard contracts from scratch, and convinced skeptical utilities one transaction at a time. The market followed the trader, not vice versa.

The key was solving trust before solving scale. That first transaction in 2001—50 MW from NTPC to Tamil Nadu—took three months to negotiate but established the template. Payment security through letters of credit. Back-to-back contracts eliminating PTC's balance sheet risk. Real-time transmission coordination. Each element addressed specific trust deficits. Once trust was established, scale followed exponentially.

The Innovator's Dilemma in Infrastructure

PTC's exchange story is a masterclass in self-disruption gone wrong. They co-promoted IEX in 2007, thinking exchanges would complement bilateral trading. Instead, IEX cannibalized PTC's business while using PTC's market development as foundation. The lesson isn't to avoid disruption but to own it completely. PTC should have either stayed out of exchanges entirely or gone all-in with majority control. Half-measures in disruption are fatal.

The HPX gambit represents a second attempt at self-disruption, but with lessons learned. This time, PTC maintained strategic control, aligned the exchange with their trading business, and focused on differentiated products. Whether too late remains uncertain, but the approach—full commitment, strategic synergies, patience for long-term outcomes—reflects institutional learning.

Regulatory Relationships as Moat and Trap

PTC's regulatory relationships were their greatest asset and eventual liability. Being CERC's first licensee, the government's chosen vehicle for cross-border trading, MNRE's highest-rated renewable trader—these created massive advantages. But regulatory favor is a double-edged sword. When CERC capped trading margins, PTC couldn't protest vigorously without seeming ungrateful. When market coupling was proposed, PTC had to support it despite hurting their exchange investment.

The lesson: regulatory advantages are powerful but temporary. They should be used to build sustainable competitive advantages—technology platforms, customer relationships, operational excellence—that persist beyond regulatory favor. PTC's mistake was assuming regulatory relationships would remain their primary moat.

Platform Versus Trading Business Models

PTC faced a fundamental choice: be a trader taking positions and managing risk, or be a platform enabling others to trade. They chose both, creating inherent conflicts. The trading desk competed with exchange ambitions. Risk management protocols limited platform innovation. Capital allocation suffered from divided priorities.

Successful infrastructure companies usually pick one model. CME doesn't trade futures; it provides the platform. Goldman Sachs trades but doesn't run exchanges. PTC's attempt to do both created strategic confusion that persists today. The lesson: in infrastructure markets, platform economics usually beat trading economics, but only if you commit fully to the platform model.

Timing Market Evolution

PTC's history reveals the importance of timing in market evolution. They entered power trading at the perfect moment—after economic liberalization but before full competition. They launched PFS just as infrastructure financing gaps emerged. They started cross-border trading as regional cooperation increased. But they were late to exchanges, late to renewable trading, late to digital transformation.

The pattern suggests institutional inertia. First movers become comfortable with existing models and miss transition points. The lesson: market creators must constantly reimagine their markets. Today's innovation becomes tomorrow's legacy infrastructure. Companies that created markets must be willing to destroy and recreate them.

Managing Government DNA in Commercial Entities

PTC's public sector parentage created unique advantages and challenges. The advantages: instant credibility, government relationships, patient capital. The challenges: bureaucratic decision-making, political interference, inability to match private sector compensation. PTC navigated this reasonably well through independent boards and commercial culture, but the DNA showed during critical moments—the delayed digital transformation, the cautious international expansion, the consensus-seeking approach to competition.

The lesson: government-initiated commercial entities need exceptional governance to succeed. Independent directors must truly be independent. Management compensation must be market-linked. Political pressures must be resisted. PTC achieved partial success here, better than typical PSUs but not matching pure private players.

Ecosystem Building Versus Value Capture

PTC built India's power market ecosystem—payment mechanisms, standard contracts, trading protocols, even competitors. But they captured only a fraction of the value created. IEX, which PTC helped establish, has a market cap exceeding PTC's despite doing one-tenth the volume. The renewable developers PTC nurtured through early trading support became billion-dollar enterprises. The ecosystem thrived; the creator struggled.

This raises fundamental questions about value capture in market creation. Should PTC have been more aggressive in extracting value? Should they have vertically integrated more completely? Or is ecosystem building inherently a positive-sum game where creators must accept smaller shares of larger pies? PTC's experience suggests market creators need clear value capture strategies from day one, not as an afterthought.

XI. Bear vs Bull Case & Future Outlook

The Bear Case: Structural Decline Accelerating

The pessimistic view starts with market structure. Exchanges now handle 55% of short-term transactions, up from 11% in 2010. This isn't cyclical—it's structural. Every year, more utilities, generators, and consumers become comfortable with exchange trading. The convenience of click-and-buy power beats relationship-based bilateral trading. PTC's market share in bilateral trading might stabilize around 30%, but bilateral trading itself is shrinking relative to exchanges.

Competition is intensifying from unexpected directions. State utilities are establishing their own trading desks—Gujarat, Maharashtra, and Telangana already trade independently. Renewable developers are forward-integrating into trading. Technology platforms are enabling peer-to-peer trading. The intermediary role that PTC pioneered is being disintermediated by technology and direct relationships.

Margin compression appears terminal. Current margins at ₹0.029 per kWh barely cover operational costs. Competition and regulatory caps prevent margin expansion. Meanwhile, working capital costs are rising as payment cycles elongate. The business model of earning 2-3 paise per unit while financing 60-day payment cycles generates returns below cost of capital. This isn't a business—it's a public service.

HPX's exchange ambitions face mathematical impossibility. IEX's 98% market share creates network effects that market coupling can't break. European markets took decades to implement successful coupling. India's power market, with its state-level complexities and political interference, makes coupling even harder. HPX might survive as a niche player, but challenging IEX's dominance requires miracles, not strategy.

The renewable transition undermines PTC's core advantages. Distributed generation doesn't need inter-state traders. Battery storage eliminates real-time balancing requirements. Blockchain-based smart contracts can handle bilateral trades without intermediaries. The future grid—decentralized, digitized, decarbonized—has no obvious role for traditional power traders.

Financial metrics confirm the decline. Revenue growth is negative in real terms. ROE has fallen below cost of equity. The stock trades at historic low multiples, suggesting market expects terminal decline. Even the dividend yield, while attractive at 7%, reflects capital return from a shrinking business rather than growth-funded payouts.

The Bull Case: Transformation and Hidden Value

The optimistic view acknowledges challenges but sees transformation opportunities. India's power demand will double by 2035. Even with declining market share, absolute volumes will grow. PTC's 82,751 MU volume today could become 150,000 MU by 2030 through market growth alone. At normalized margins, this generates substantial cash flows to fund transformation.

HPX represents optionality, not necessity. Market coupling, despite implementation challenges, will eventually redistribute exchange volumes. European markets saw second and third exchanges capture 30-40% share post-coupling. If HPX achieves even 20% share of a 500 billion unit market by 2030, the valuation could exceed ₹3,000 crores. PTC's 22% stake would be worth ₹700 crores, nearly 15% of current market cap.

Cross-border opportunities are underappreciated. The South Asian regional grid is nascent. Bangladesh's 7,000 MU imports could triple. Nepal's hydroelectric potential of 40,000 MW needs Indian markets. Sri Lanka and Myanmar could join the regional grid. As the designated nodal agency with government relationships, PTC is uniquely positioned to capture this growth. Cross-border margins at 8-10 paise are triple domestic margins.

The subsidiary value exceeds market recognition. PFS alone, growing at 15% with 18% ROE, deserves a ₹4,000 crore valuation. PTC's 65% stake is worth ₹2,600 crores. Add HPX potential, working capital, and investments—the sum-of-parts reaches ₹7,000-8,000 crores against current market cap of ₹5,000 crores. This isn't growth speculation—it's value already created but not recognized.

Carbon markets could be transformative. India's carbon market, launching in 2025, could reach $10-15 billion by 2030. PTC's relationships with every major emitter and experience in certificate trading position them as natural intermediaries. Carbon trading margins could be 10x electricity margins. Even 10% market share generates ₹500-750 crores annual profit potential.

Management quality suggests navigation capability. The successful PEL divestment, PFS value creation, and HPX launch demonstrate strategic flexibility. The company isn't wedded to legacy models. They're actively exploring battery storage, green hydrogen, and energy-as-a-service models. The next strategic pivot could surprise markets as dramatically as the 2007 PFS launch.

The Realistic Path: Steady Transformation

Reality likely falls between extremes. PTC won't disappear but won't dominate either. They'll remain India's largest power trader by inertia and relationships, trading 100-125 billion units annually at compressed but stable margins. The trading business becomes a cash cow funding transformation, not a growth engine.

Value creation shifts to subsidiaries and new ventures. PFS continues growing, potentially exceeding parent company value. HPX captures 10-15% exchange share through differentiation, not dominance. Carbon trading contributes meaningful but not transformative profits. The holding company structure allows capital allocation to highest-return opportunities.

The stock re-rates modestly as transformation progresses. Current P/E of 6-7x expands to 10-12x as market recognizes subsidiary value and carbon potential. Dividends remain attractive, supported by trading cash flows and subsidiary dividends. Total returns of 12-15% annually—not spectacular but solid for a transforming utility.

XII. Epilogue: What Would We Do?

Standing at PTC's strategic crossroads today, the path forward requires brutal honesty about what's working and what's not. The bilateral power trading business that built PTC is in terminal decline. Fighting this reality wastes resources and management attention. The future lies in platforms, financial services, and emerging markets where PTC's institutional capabilities create genuine advantage.

First, we would accelerate the platform pivot. HPX needs aggressive investment, not cautious experimentation. Commit ₹500 crores over three years to build technology, acquire talent, and create liquidity. Partner with international exchanges for derivatives products. Launch innovative contracts—weather derivatives, renewable forecasting products, battery storage optimization. Make HPX the innovation leader, not IEX's follower. Accept short-term losses for long-term position.

Second, double down on PFS while exploring strategic options. The financing subsidiary is PTC's crown jewel, generating superior returns with secular growth. But trapped within PTC's structure, it trades at conglomerate discount. We would explore strategic alternatives: merge with larger NBFCs for scale, partner with international infrastructure funds for capital, or spin off completely to unlock value. PFS deserves independent growth capital and valuation, not parent company constraints.

Third, pivot international from trading to development. Cross-border trading generates good margins but limited growth. The real opportunity is developing regional transmission infrastructure. Partner with multilateral agencies to build India-Nepal transmission lines. Co-develop pumped hydro storage in Bhutan for regional balancing. Create a South Asian power pool modeled on European market coupling. Move up the value chain from trader to infrastructure developer.

Fourth, embrace the renewable disruption completely. Exit thermal trading gradually—it's a melting ice cube. Build capabilities in emerging areas: green hydrogen trading, battery storage optimization, virtual power plant aggregation, carbon credit origination. Partner with technology companies for blockchain-based renewable certificates. The renewable future needs new intermediaries, not traditional traders.

Fifth, fix the capital structure. PTC trades at holding company discount because value is trapped in subsidiaries. Implement a clear capital allocation framework: return trading business cash flows to shareholders through buybacks, reinvest subsidiary profits for growth, and use asset sales for special dividends. The market rewards clarity and capital discipline, not conglomerate complexity.

Culturally, inject private sector urgency. PTC's public sector DNA served well during market creation but inhibits transformation. Hire technology and trading talent from exchanges, startups, and international markets. Implement variable compensation linked to profit, not just revenue. Create innovation labs experimenting with new business models. Accept failures as learning, not career-ending mistakes.

Most importantly, communicate a clear vision. PTC's story today is confused—are they traders, financiers, exchange operators, or renewable players? The market hates confusion. Define a clear identity: "India's Energy Transition Platform"—financing the transition through PFS, enabling price discovery through HPX, facilitating regional integration through cross-border infrastructure, and capturing emerging opportunities in carbon and hydrogen markets.

The timeline is critical. PTC has perhaps five years before bilateral trading becomes economically unviable. The transformation must happen within this window using trading cash flows. Delay means irrelevance. Speed means survival and potential prosperity.

Would this strategy work? History suggests companies rarely transform successfully—Kodak couldn't pivot to digital, Nokia couldn't adapt to smartphones, traditional utilities struggle with renewable disruption. But PTC has advantages: diversified revenue streams, strong balance sheet, government relationships, and demonstrated ability to create new businesses. The question isn't capability but willingness to cannibalize legacy for future.

The alternative—maintaining status quo, protecting bilateral trading, hoping for regulatory support—guarantees slow decline. PTC would become India's power market museum, historically important but commercially irrelevant. The company that created India's power market deserves better. Whether it achieves better depends on decisions made today, not tomorrow.

In the end, PTC India's story is still being written. They created a market from nothing, watched it evolve beyond their control, and now face existential choices about their future. The next chapter could be decline into irrelevance or transformation into something entirely new—an energy platform company that happens to trade power, not a power trader trying to become a platform. The difference isn't just semantic. It's survival.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube