PSP Projects: The Engineering Mastermind Behind the World's Largest Office

I. Introduction & The "Pentagon Killer"

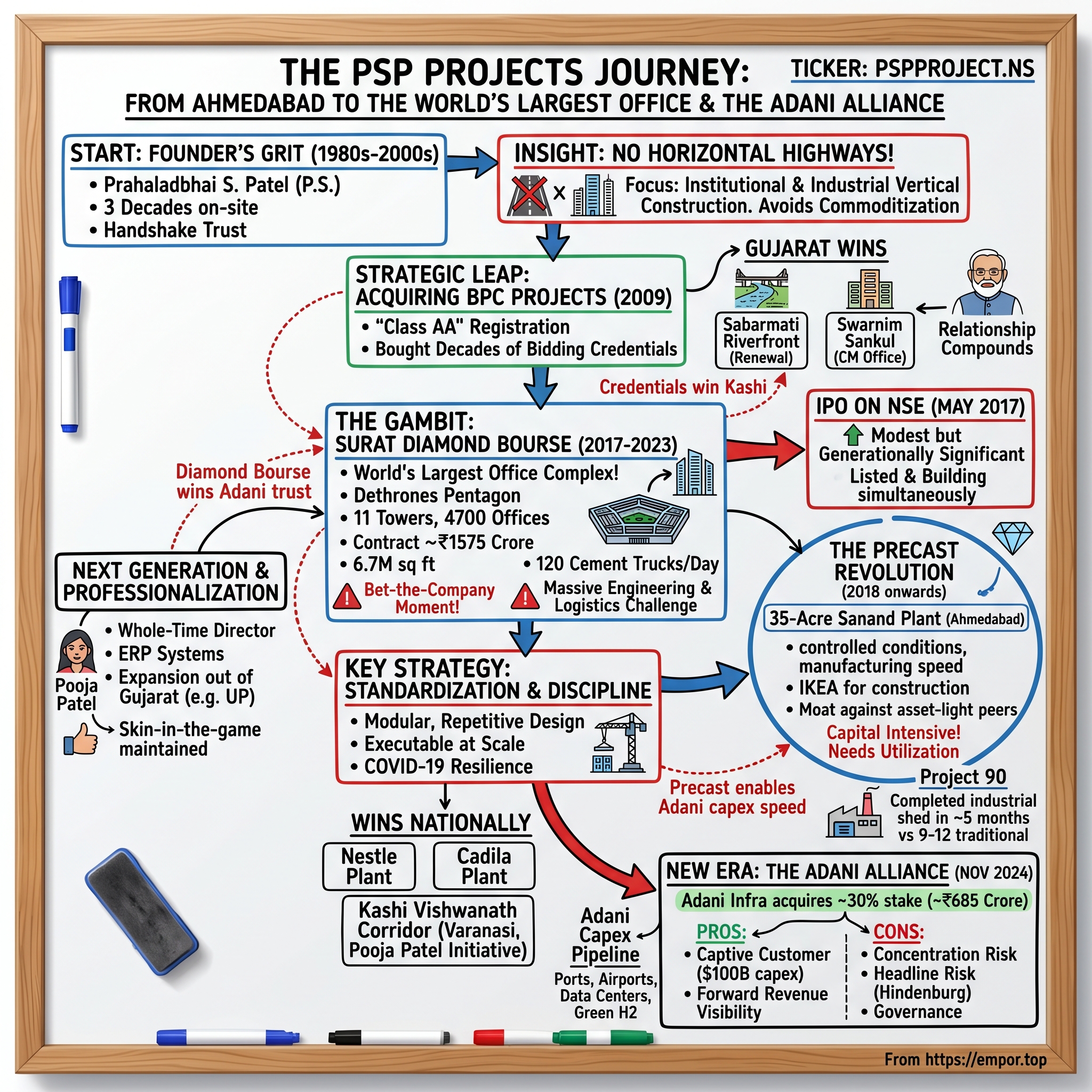

On a humid December morning in 2023, Indian Prime Minister Narendra Modi walked through a glass-and-stone canyon in the western Indian city of Surat. Behind him stretched eleven interconnected towers—a structure so vast it had displaced the Pentagon as the largest office building on Earth. The complex sprawled across 35.5 acres, contained 4,700 offices linked by a central spine, and could house over 65,000 diamond traders who, until that day, had been crammed into the narrow lanes of Mumbai's Opera House district1.

The Pentagon, by comparison, had reigned as the world's largest single-occupant office building since 1943—a Cold War colossus born of wartime urgency. It took eight decades to dethrone it. And the company that did the dethroning was not Larsen & Toubro. It was not Shapoorji Pallonji, whose tendrils reach back to the construction of the Taj Mahal Palace Hotel. It was a 16-year-old engineering contractor from Ahmedabad with revenues that, on the day it won the Surat contract, were less than what the project itself would cost.

That company is પીએસપી પ્રોજેક્ટ્સ લિમિટેડ PSP Projects Limited. And the story of how a regional Gujarati builder beat global heavyweights to deliver the સુરત ડાયમંડ બોર્સ Surat Diamond Bourse is, in many ways, the story of modern Indian infrastructure itself—a story of audacity, frugality, family stewardship, and an almost obsessive focus on doing one thing extremely well.

But the December 2023 ribbon-cutting was not even the most significant inflection point in PSP's recent history. That came eleven months later, in November 2024, when a press release crossed the wires confirming what the market had only whispered about: અદાણી ઇન્ફ્રા Adani Infra (India) Limited had acquired a roughly 30% stake in PSP Projects from the founding Patel family, in a deal valued at approximately ₹685 crore[^2]. With one transaction, India's most aggressive industrial conglomerate had effectively converted PSP into its in-house execution arm. The company that built the world's largest office had just become the contractor of choice for the country's most ambitious capex program.

This is the story of how a civil engineer named પ્રહલાદભાઈ એસ. પટેલ Prahaladbhai S. Patel—known to almost everyone simply as "P.S." or "Prahalad bhai"—built PSP Projects from a single registered office in Ahmedabad in 2008 into a Tier-1 institutional builder whose order book reads like a tour of contemporary India: the Sabarmati Riverfront, the Gujarat Chief Minister's Office, the Surat Diamond Bourse, the કાશી વિશ્વનાથ ધામ Kashi Vishwanath Corridor in Varanasi, manufacturing plants for કેડિલા હેલ્થકેર Cadila and Nestle, and now, increasingly, the industrial backbone of the Adani empire.

It is a story about how to scale a family contracting business without losing the discipline that made it work in the first place. It is a story about the difference between buying revenue and earning it, between asset-heavy and asset-light strategies, and between being one of fifty bidders on a road project and being the only builder in the room with the credibility to pour 120 trucks of concrete a day for 400 days straight.

And it is, ultimately, a story about cornered resources—the trust of a state government, the muscle memory of executing institutional projects on time, and the precast concrete plant in સાણંદ Sanand that may turn out to be the most consequential capital allocation decision the company has ever made.

Let's go back to where it all started.

II. The Founder's Grit: Prahaladbhai S. Patel

To understand PSP Projects, you must first understand a peculiar fact about Gujarati commercial culture: contracts are still, to a remarkable degree, a function of personal trust. The Patels of Gujarat are one of India's most entrepreneurial communities, and within that community, civil contracting is a craft passed down with the rigor of guild apprenticeship. You learn it on a job site, not in a boardroom.

Prahaladbhai S. Patel was born into that tradition. By the time he founded PSP in 2008, he had already spent nearly three decades on construction sites across Gujarat—pouring foundations, supervising labor gangs, managing material costs in an era when "ERP" meant a notebook and a pencil. He had run a proprietorship and worked in family ventures, and he had built a reputation among Ahmedabad's industrial and institutional clients as a man whose handshake meant the deadline would be hit2.

What Patel lacked, on the day he incorporated PSP Projects in August 2008, was scale. He was 53 years old. He had, by his own account, watched a generation of younger contractors leapfrog him by raising private capital and chasing road projects under the National Highways Development Programme. Patel did not chase roads. He found them, in his telling, too commoditized—too dependent on government payment cycles, too prone to litigation, too thin on margin. He wanted to build things that stood up vertically, not things that stretched horizontally.

This is the first thing to understand about PSP. From the founding day, the company refused to be a "highways contractor." It refused even to be a generalist EPC firm. It positioned itself as an institutional and industrial builder—hospitals, offices, factories, government complexes, religious corridors. That positioning would, fifteen years later, prove to be one of the most valuable strategic decisions in the company's history. But in 2008, it just looked like a small Gujarati contractor who did not want to leave Gujarat.

Then came the first real strategic move—and it was a piece of corporate finance, not engineering.

In 2009, less than a year after incorporation, PSP acquired BPC Projects, a Gujarat-based contractor that held a "Class AA" registration with the state's Roads & Buildings Department2. To outsiders, this looked like a routine bolt-on. To insiders, it was a brilliant piece of capital allocation. In Indian public works contracting, registration class is a regulatory chokepoint. A "Class AA" certificate lets you bid on the largest government projects; building such a credential from scratch can take a decade of progressively larger contracts, each one a chicken-and-egg problem of needing experience to win the bid that gives you the experience. By acquiring BPC, Patel bought a decade of bidding credentials in a single stroke.

This is the kind of move that separates good contractors from great ones. The Tata Group did something similar when it acquired Corus to leapfrog into European steel; the lesson is the same. When credentials, licenses, or relationships are the binding constraint on growth, the smartest use of capital is often to buy them rather than build them.

Armed with its new Class AA registration, PSP began winning the kind of work that would define its identity. The first headline win came with the સાબરમતી રિવરફ્રન્ટ Sabarmati Riverfront Development Project, the urban renewal showcase that turned a polluted stretch of Ahmedabad's river into a 22-kilometer promenade. Then came the સ્વર્ણિમ સંકુલ Swarnim Sankul—the new Chief Minister's Office complex in Gandhinagar, completed under the tenure of a then-Gujarat-CM named Narendra Modi4.

That relationship—a small, reliable contractor delivering high-profile government buildings on time for a Chief Minister who would soon become Prime Minister—is the kind of cornered resource that does not appear on any balance sheet but compounds quietly for years. By the early 2010s, PSP had become the default short-list contractor for institutional buildings in Gujarat. Not because it was the cheapest, but because it was the most predictable.

Predictability is an underrated virtue in Indian construction. The industry is littered with the corpses of contractors who underbid to win a project and then watched their margins evaporate as costs rose, payments stalled, and litigation dragged on. Patel's discipline was to bid only on projects he was confident he could deliver, and then to deliver them with a paranoid focus on the project schedule. That discipline would soon be tested at a scale nobody in Indian construction had ever attempted.

III. The સુરત ડાયમંડ બોર્સ Surat Diamond Bourse Gambit

In late 2017, a tender circulated in the trade press that sounded, frankly, deranged. A consortium of diamond merchants in Surat—the city that cuts and polishes roughly 90% of the world's rough diamonds—wanted to build a single, integrated trading complex that would consolidate the entire industry under one roof. The brief called for 6.7 million square feet of usable space, 4,700 modular offices, eleven 15-story towers radiating from a central spine, and a budget that, by the time the dust settled, would exceed ₹3,400 crore in construction value1.

When the tender opened, the giants of Indian construction—Larsen & Toubro, Shapoorji Pallonji, Tata Projects—all looked at it. And then most of them walked away. The economics were brutal: the merchants who would occupy the building were also funding it, so they wanted the cheapest credible builder, not the most prestigious. The timeline was aggressive. The design was almost obsessively standardized—every office had to be modular, every floorplate identical, every finish replicated thousands of times. It was less a prestige project and more an industrial-scale repetition exercise.

PSP Projects won the contract in March 2017, valued at approximately ₹1,575 crore in its initial scope3. To put that in perspective, PSP's revenue in the previous full fiscal year had been around ₹500 crore. The company had just signed up to execute, single-handedly, a project worth more than three times its annual sales—at a fixed price, on a fixed timeline, in a city it did not yet have an office in.

This was a bet-the-company moment. If PSP failed to deliver Surat Diamond Bourse on time, on budget, and to spec, the company would not survive. If it succeeded, it would graduate from being a regional Gujarati contractor to being a national Tier-1 institutional builder. Patel bet the company.

The engineering challenge was almost beyond comprehension. At peak construction in 2019-2020, PSP was pouring concrete at a rate that builders describe in almost mythological terms: 120 ready-mix trucks per day, every day, for roughly 400 days3. The site employed over 10,000 workers across multiple shifts. The logistics alone required PSP to operate as a small city—housing, feeding, sequencing, training, and supervising a workforce larger than most Indian listed companies.

And here is where the discipline learned from twenty smaller projects compounded into something extraordinary. PSP had developed, over a decade of institutional building, a near-religious commitment to standardization—of materials, of schedules, of subcontractor management. At Surat, that standardization was the only thing that made the project executable. Every floor was a copy of the floor below. Every office was a copy of the office next door. Every concrete pour followed the same sequence. The repetition that made the building boring to design made it tractable to build.

The timing was almost cinematic. PSP had completed its initial public offering on the National Stock Exchange in May 2017, raising approximately ₹211 crore at an issue price of ₹210 per share[^5]. The IPO was modest by Indian standards but generationally significant for the Patel family—it converted a family contracting business into a publicly listed company with a market currency for future deals. And it happened almost simultaneously with the start of the Surat job. PSP listed on the exchange and began construction on the world's largest office in the same year.

Construction continued through the COVID-19 pandemic, which halted Indian construction sites for weeks in 2020 and disrupted labor migration for months afterward. The project missed its original target completion date but came in with what most observers regarded as remarkable schedule discipline given the circumstances. When Prime Minister Modi inaugurated the complex in December 2023, PSP had effectively built, over a six-year arc, the most discussed single structure in the Indian construction industry's modern history1.

The financial significance was profound but easy to misread. The Surat Diamond Bourse, on its own, did not transform PSP's earnings—construction is a low-margin business, and the contract was priced for the buyer, not the builder. What it transformed was PSP's credibility. After Surat, no Indian builder could credibly say PSP was a small regional player. After Surat, every large industrial client in India knew that PSP could deliver at scale. After Surat, the order book ceased to be the constraint on growth. The constraint became execution capacity—and that, conveniently, was already being addressed in a 35-acre industrial plot a short drive from PSP's Ahmedabad headquarters.

IV. The "Hidden" Business: The Precast Revolution

If you have followed Indian construction stocks for the past decade, you know the recurring frustrations: monsoons that erase three months of productive site time every year, labor shortages that intensify with every state's MGNREGA program, and quality variation that turns even well-designed buildings into latent litigation risks. These are not problems unique to PSP. They are problems endemic to site-based construction in India.

In 2018, while the Surat Diamond Bourse was still ramping up, PSP began quietly investing in a solution. The company acquired a 35-acre plot in Sanand, the same industrial belt outside Ahmedabad that hosts Tata Motors' Nano plant and a growing cluster of automotive suppliers. The plan was to build one of India's largest dedicated precast concrete facilities—a factory, essentially, that would manufacture structural building components under controlled industrial conditions and then ship them to construction sites for assembly[^6].

To understand why this matters, think of construction the way you would think of furniture. You can hire a carpenter to build a cabinet in your kitchen, with the carpenter cutting wood, hammering joints, and finishing the surface on-site over several weeks. Or you can buy a flat-pack cabinet from IKEA, which arrives in standardized panels manufactured under factory conditions, and you assemble it in your kitchen in an afternoon. Site-based construction is the carpenter. Precast is IKEA.

The advantages of the factory model are well-established globally. Quality is more consistent because you control temperature, humidity, and curing conditions. Labor productivity is higher because workers specialize in repeated tasks. Weather is no longer a constraint because the components are built indoors. And critically, the on-site assembly phase—the part exposed to monsoons, labor shortages, and project delays—shrinks dramatically. A building that would take 18 months of site work might take 4-6 months of site work if 70% of the structural elements arrive pre-built.

The capital commitment was significant for a company PSP's size. The initial investment in the Sanand facility was approximately ₹109 crore, with subsequent expansions taking total invested capital substantially higher[^6]. For a company that had historically run an asset-light contracting model—rented equipment, leased offices, deployed labor through subcontractors—buying an industrial plant and committing to capital depreciation was a philosophical shift. PSP was no longer purely a services company. It was now also a manufacturer.

The strategic logic was twofold. First, precast gave PSP a structural cost advantage on the kind of repetitive industrial buildings—warehouses, factories, data centers—that India's manufacturing push was beginning to demand in volume. Second, and less obviously, precast gave PSP a moat against new entrants. Anyone with a contractor's license can bid on a building contract. Very few have the capital and operational capability to build a 35-acre precast facility and then run it at the utilization rates needed to justify the depreciation.

The early showcase project for the Sanand facility was what PSP internally called "Project 90"—an effort to complete a large industrial shed for a major client in 148 days, using extensive precast elements[^7]. The timeline was, by industry standards, absurd. Comparable projects executed with traditional site-based methods typically took 9-12 months. PSP completed it in roughly five. The client, satisfied, became a repeat customer. Other industrial clients took notice.

By the early 2020s, precast had become a "business within a business" at PSP. Its margins are structurally higher than the contracting business, because the manufacturing economics are different from the services economics. Its growth ceiling is, in principle, much higher—a single plant can serve dozens of projects simultaneously, whereas a single project requires a dedicated site team. And its operational leverage is enormous; the marginal cost of producing one more precast panel, once the plant is paid for, is dramatically lower than the marginal cost of building one more square foot on-site.

The honest assessment is that precast is still a work in progress at PSP. Utilization rates have been variable, particularly during periods when the order pipeline for amenable projects has been uneven. Margins from the precast business are not yet at the level that the strategic case suggests they should reach. But the direction of travel is unambiguous. The company is methodically converting itself from a pure services contractor into a hybrid construction-technology firm—and the Sanand plant is the physical embodiment of that transition.

When investors talk about PSP's "industrial-heavy" capital structure as a critique—why is a contractor sinking capital into a plant when its peers are running asset-light?—they are missing the strategic point. Asset-light is a great model when you are bidding on commoditized work. When you are building a defensible moat in industrial construction, the asset is the moat. And the moat, increasingly, was about to find itself a captive customer.

V. Management: The Next Generation & Professionalization

Walk into PSP's headquarters in Ahmedabad and the first thing you notice is how unceremonious it is. There is no glass tower. There is no atrium. There is, instead, a working office where the founder still spends most of his day. Prahaladbhai S. Patel, now in his early seventies, holds the title of Chairman and Managing Director and has shown no public inclination to step back from operational decisions2. He is, by all accounts, still the person who personally sizes up every large bid, who reviews material cost movements weekly, and who picks up the phone when a state government wants to discuss a delayed payment.

This kind of founder centrality is both the great strength and the great vulnerability of Indian family-owned contractors. The strength is that the founder's discipline, relationships, and judgment are baked into every decision—nothing gets bid that the founder would not personally execute. The vulnerability is succession. The graveyard of Indian contracting is full of firms that thrived for one generation and collapsed in the next, undone by sibling disputes, professional management transitions handled poorly, or founders who simply refused to let go.

PSP has been working on this problem for the better part of a decade, and the answer has a name: Pooja Patel.

Pooja Patel, P.S. Patel's daughter, joined PSP's executive ranks in the 2010s and has progressively taken on broader operational responsibility. She holds the title of Whole-Time Director and has been the driving force behind the company's process modernization—the implementation of ERP systems, the build-out of internal project management dashboards, and the structured expansion into geographies outside Gujarat[^8].

The Uttar Pradesh expansion is, in many ways, Pooja Patel's signature initiative. For most of its history, PSP's competitive advantage was anchored in Gujarat—local labor, local subcontractors, local relationships, local regulatory familiarity. Replicating that anywhere else was a problem nobody had really cracked. The first big test was the काशी विश्वनाथ धाम Kashi Vishwanath Dham Corridor in Varanasi, a politically high-profile project to redevelop the temple complex in Prime Minister Modi's parliamentary constituency, inaugurated in December 2021[^9].

Varanasi is not Ahmedabad. The labor pool is different, the supply chain is different, the political stakes are higher, and the project itself—weaving a modern infrastructure corridor through one of the oldest continuously inhabited cities on Earth—is technically and politically delicate. PSP's successful execution of the Kashi Vishwanath Corridor was the proof point that the company could operate outside Gujarat at scale. It was also the moment that established Pooja Patel as a leader who could win and run large, complex, multi-stakeholder projects.

The cultural shift inside PSP has been deliberate. The first generation built the company on relationships and personal supervision. The second generation is layering on systems, processes, and data-driven project management without disrupting the discipline that the first generation built. The promoter family has retained substantial economic alignment—Patel family holdings stood at approximately 68% of equity before the Adani transaction in late 2024[^2]. That kind of concentrated skin-in-the-game is what allows long-cycle decisions like the Sanand precast investment to be made without quarterly second-guessing.

The professional management bench around the family has been built up gradually rather than parachuted in. Senior leadership in engineering, finance, and project management has been drawn substantially from people who grew up inside PSP, supplemented selectively by external hires in functions like investor relations and corporate strategy. The CFO seat in particular has become more institutional over time, reflecting the demands of being a listed company with an increasingly complex capital structure—the QIP in April 2024 raising approximately ₹244 crore was, among other things, an exercise in capital markets sophistication that the company would not have been ready for ten years earlier[^10].

The incentive structure is, by Indian listed-company standards, conservative. Promoter salaries are not excessive; ESOPs have been used sparingly; and overhead costs as a percentage of revenue have remained low even as the company has scaled[^8]. The result is a contracting firm that operates at higher margins than its mid-tier peers despite running a leaner organizational structure. The cultural lesson—that you can scale a family business by adding systems without adding bureaucracy—has been one of the quieter but more durable strategic advantages PSP has built.

And then, in late 2024, the question of what kind of company PSP would become next was answered by a phone call from Ahmedabad's other famous Patel family.

VI. The Adani Era & Capital Deployment Benchmarking

The deal landed on November 19, 2024, with the kind of formal restraint that Indian disclosure rules require. અદાણી ઇન્ફ્રા Adani Infra (India) Limited, a wholly-owned subsidiary of the Adani Group, would acquire a 30% stake in PSP Projects via a combination of secondary share purchase from the promoter family and an open offer to public shareholders, with the total transaction sized at approximately ₹685 crore[^2]. The acquirer reserved the option to take its eventual holding higher pending regulatory clearances and open-offer subscription levels[^2].

The market reaction was complicated. PSP's share price reacted positively on the announcement—the strategic logic of a captive customer with a hundred-billion-dollar capex pipeline buying into your execution arm is hard to argue with. But the longer-term reaction was more nuanced. Concentration risk had just become a real conversation. So had the question of what kind of company PSP would be in five years: an independent listed contractor with the Adani Group as a major customer, or, effectively, a captive engineering subsidiary that happened to retain a public listing.

The strategic logic from the Adani side was straightforward. અદાણી ગ્રુપ Adani Group, controlled by ગૌતમ અદાણી Gautam Adani, has publicly committed to a capital expenditure program in the range of $100 billion across ports, airports, green hydrogen, data centers, cement, and renewable energy through the end of the decade. Executing that capex at speed requires an army of EPC contractors, and the largest of them—L&T, Tata Projects, Shapoorji Pallonji—are independent firms with their own client relationships, their own pricing power, and their own scheduling priorities. Owning a meaningful stake in a Tier-1 builder with proven execution discipline gave Adani a captive partner who would prioritize Adani projects without the friction of arms-length negotiation.

The strategic logic from PSP's side was harder to articulate publicly but easy to understand commercially. EPC contracting is a feast-or-famine business. Order books are lumpy, payment cycles are unpredictable, and the typical Indian listed contractor trades at compressed multiples because investors discount the cyclicality of forward revenue. Becoming Adani's preferred builder did not eliminate that cyclicality, but it dramatically reduced the "order book anxiety" that hangs over the sector. PSP's forward revenue visibility, post-Adani, became materially more durable than the average mid-cap EPC firm.

The capital allocation contrast with peers is instructive. Consider केएनआर कन्स्ट्रक्शन्स KNR Constructions, a similarly-sized listed contractor focused largely on road and irrigation projects. KNR has built its growth through a financial model that emphasizes asset recycling—building roads under hybrid annuity model contracts, holding them through the construction and early operations phase, and then selling the operating assets to long-duration infrastructure investors to recycle capital into new bids. It is an elegant financial model, but it is fundamentally a financial model.

PSP has chosen the opposite path. The Sanand precast plant is the kind of asset that does not recycle. It generates operating leverage through utilization, not through sale-and-leaseback or InvIT monetization. The capital structure is industrial, not financial. The growth depends on filling the plant with high-utilization projects, not on flipping completed assets to pension funds. Both models are defensible. They produce very different companies.

The Adani deal pushes PSP further down its industrial path. Adani's capex program—steel plants, cement units, data centers, copper smelters—is exactly the kind of repetitive, large-scale industrial construction work that the precast facility was built to serve. The strategic fit is tight enough that you could plausibly argue the Sanand plant was, in effect, future-proofed for a customer the company did not yet have. It now has that customer.

The risks of concentration are real and worth naming clearly. A single anchor customer accounting for a large share of forward revenue is a vulnerability, regardless of how creditworthy that customer is. A single anchor customer that has been the subject of a public short-seller report—the હિન્ડેનબર્ગ રિસર્ચ Hindenburg Research report on Adani Group in January 2023 wiped tens of billions of dollars off the conglomerate's market value before a partial recovery—introduces a layer of headline risk that no other EPC firm carries to the same degree. The Adani Group has weathered that episode, but the question of how the broader conglomerate manages its own debt load and reputational profile is now also, indirectly, a question for PSP shareholders.

The other risk worth naming is governance. When a single industrial group owns 30% of a public contractor and is simultaneously its largest customer, the alignment of interests is asymmetric. Adani benefits if PSP prices its work attractively. Minority shareholders benefit if PSP prices its work to maximize margins. The mechanisms for resolving that tension—related-party transaction disclosures, audit committee scrutiny, independent director oversight—exist in the regulatory framework. Whether they will be sufficient in practice is one of the open questions that the next several years will answer.

The optimistic reading, and probably the right one for now, is that Adani's strategic interest is in maintaining a high-functioning execution platform that can deliver his capex on time. That requires PSP to remain profitable, well-capitalized, and operationally disciplined. A captive contractor squeezed to zero margin is not useful to anyone. The structural alignment, properly managed, is closer to symbiosis than predation.

VII. Strategy: Hamilton Helmer's 7 Powers & Porter's 5 Forces

To analyze a company like PSP through the lens of હેમિલ્ટન હેલ્મર Hamilton Helmer's 7 Powers framework is to acknowledge upfront that construction is, in general, a powers-poor industry. Buildings are local. Labor is mobile. Capital is plentiful. Customers are sophisticated. Switching costs are essentially zero between projects. The default state of the industry is brutal commodity competition.

So the question is: what powers, if any, does PSP actually have?

Scale Economies. PSP's clearest source of scale economics is the Sanand precast plant. A precast facility has the cost structure of a manufacturing plant—high fixed costs, low marginal costs—and produces a competitive advantage that scales with utilization. At low utilization, the plant is a capital sink. At high utilization, it allows PSP to deliver industrial buildings at a cost and speed that pure site-based contractors cannot match. Adani's anchor demand pushes utilization toward the level where the scale advantage becomes structural. This is the most important strategic dynamic to watch over the next five years.

Counter-Positioning. This is the most subtle but possibly the most durable of PSP's powers. The legacy of Indian construction is a "cost-plus" mindset: bid low, win the contract, then negotiate scope changes and time extensions to recover margin. PSP, by leaning into precast and disciplined scheduling, has positioned itself against that legacy model. Its value proposition to clients is speed and predictability, not lowest-bid. Larger competitors like L&T can match PSP on capability, but their cost structure—built around traditional site execution and complex multi-segment operations—makes it expensive for them to pivot to a precast-heavy model. Smaller competitors can match PSP on price, but they cannot match the capital intensity of the Sanand plant. PSP sits in a strategic gap where the giants are too slow to copy it and the minnows are too small to match it.

Cornered Resource. PSP's track record on institutional buildings—government complexes, religious corridors, diamond bourses, hospitals—is a specific kind of expertise that takes years to build and is not transferable through capital alone. The Gujarat government's trust in PSP, built over a decade of on-time delivery on politically high-profile projects, is a relationship-based asset that no competitor can buy. The expansion to Uttar Pradesh via the Kashi Vishwanath project has begun to extend that asset geographically. The Adani relationship now adds a second cornered resource: privileged execution access to one of India's largest forward capex programs.

The other four powers—Switching Costs, Network Economies, Branding, and Process Power—are weaker for PSP. Switching costs from a contractor are minimal at the project level. Network effects do not really apply in EPC. Brand matters less for B2B institutional clients than for consumers. Process power—the kind of accumulated operational know-how that defines a company like Toyota—is something PSP is building but has not yet definitively achieved.

Turning to માઇકલ પોર્ટર Michael Porter's 5 Forces:

Bargaining Power of Buyers. Historically very high. PSP's early customer mix was dominated by government clients with payment cycles that ran on political calendars rather than commercial ones, and by single-project private clients who could squeeze margins ruthlessly during tender negotiations. The shift in the buyer mix over the past five years—toward industrial clients like ઝાયડસ Zydus Lifesciences, Nestle, and now the Adani Group—has improved this dynamic substantially. Industrial clients value speed and reliability over rock-bottom pricing, because their construction spend is a fraction of the total opportunity cost of a delayed plant.

Bargaining Power of Suppliers. Moderate. Steel, cement, and ready-mix concrete are commoditized inputs with multiple suppliers and reasonably efficient price discovery. Labor supply is the more variable factor, and labor shortages during peak construction seasons can compress margins on fixed-price contracts. The precast plant partially insulates PSP from labor-cost shocks by substituting capital for site labor.

Threat of New Entrants. Low for projects requiring institutional credentials, high for commoditized work. New entrants cannot easily replicate PSP's twenty-year track record, but they also do not need to—they can compete on smaller, simpler projects and grow from there. The threat to PSP is not new entrants displacing them on existing work; it is new entrants compressing pricing on the work PSP would otherwise pick up as next-generation pipeline.

Threat of Substitutes. Low. Buildings remain buildings. The substitute for a precast factory shed is a site-built factory shed—same product, different production method. The substitute for an office complex is, at most, a different office complex. There is no analogous "software" disrupting the physical construction of large industrial buildings.

Rivalry. Intense in commoditized segments like highway construction, ports, and standard commercial buildings—segments PSP has consciously avoided. Moderate to low in the segments PSP actually operates in: institutional buildings, large industrial precast, and high-profile government projects. The strategic decision to avoid roads, made by P.S. Patel essentially on instinct in the company's first years, has compounded into a significant structural advantage on competitive intensity.

The net of all this is a contractor that has carved out a niche genuinely differentiated from the commodity center of Indian construction. The powers are not as durable as those of, say, a software platform or a regulated utility. But they are real, they are growing, and they are reinforced by capital allocation choices that compound over time.

VIII. Bear vs. Bull Case & Playbook Lessons

The bear case on PSP Projects begins with concentration risk and ends with execution risk, with several uncomfortable considerations in between.

The single largest concentration concern is now અદાણી ગ્રુપ Adani Group itself. After the November 2024 transaction, Adani is simultaneously PSP's largest non-promoter shareholder and, plausibly, its largest customer over the next five years[^2]. Any disruption to the Adani capex program—whether driven by capital market stress, regulatory action, commodity cycle inversion, or governance shocks at the conglomerate level—would flow directly into PSP's order book. The headline risks around the Adani Group have not disappeared; they have, in effect, become two-step risks for PSP shareholders.

The second concentration concern is geographic. Despite the Uttar Pradesh expansion via Kashi Vishwanath, PSP's revenue base remains heavily skewed toward Gujarat. A state-level economic or political shock—a change in state government attitudes toward project award processes, a slowdown in Gujarat's industrial capex cycle, or a regulatory change affecting precast economics—would hurt PSP disproportionately relative to a peer with a more diversified footprint.

The third concern is the structural margin profile of Indian EPC. Even in PSP's best-margin segments, operating margins remain in the high single digits to low double digits. Compared to global construction technology firms operating at 15-20% EBITDA margins, the Indian contracting structure is structurally lower-margin due to commodity input costs, labor variability, and customer payment cycles. The QIP raise of approximately ₹244 crore in April 2024 added equity capital but also added the future obligation to deploy that capital at attractive returns[^10]. If the precast plant does not run at high utilization, the return on that incremental capital becomes a real question.

The fourth concern is working capital. Construction is a working-capital-intensive business in India, where progress payments from government clients can stretch beyond 90 days and receivables management is a persistent operational drag. PSP has historically managed this better than peers, but expanding scale tends to magnify working capital problems before it solves them. CARE Ratings has tracked these dynamics through its ongoing credit assessment of the company[^12].

The fifth concern is governance complexity post-Adani. Related-party transactions between PSP and Adani Group entities will require careful disclosure and arms-length pricing. Minority shareholders will need to trust that audit committee oversight is genuinely independent. The base rate on these arrangements in Indian listed companies is, charitably, mixed.

Now the bull case.

The most important bull-case argument is structural, not cyclical. PSP is in the process of transforming itself from a "Service Company"—where revenue is a function of headcount, labor, and project-by-project bidding—into a "Construction Technology Company," where revenue is increasingly a function of capital deployed in industrial-scale precast manufacturing and process-driven project execution. This transition, if completed, would re-rate the company in two ways: higher structural margins from precast operating leverage, and higher multiples from the durability premium that investors apply to capital-deployed industrial businesses versus people-deployed service businesses.

The second bull-case argument is the Adani anchor. India's industrial capex cycle is in early innings. The combination of the central government's manufacturing push, the production-linked incentive programs across sectors, and the global supply chain diversification away from China is generating a multi-year tailwind for industrial construction. Adani is positioned to capture an outsized share of that capex. PSP, in turn, is positioned to capture an outsized share of Adani's construction spend.

The third bull-case argument is the optionality on geography. The Uttar Pradesh proof-point opens the possibility of a national institutional-buildings franchise. The Kashi Vishwanath success has been followed by additional UP-based projects, and the model is reproducible to Madhya Pradesh, Karnataka, Tamil Nadu, and other large states where institutional construction pipelines exist. The brand can travel; whether it does will depend on execution capacity, not opportunity.

The fourth argument is the founder-driver effect. P.S. Patel remains personally engaged in operations, but the second-generation transition to Pooja Patel is advanced enough that the company is no longer one-person-deep on key talent[^8]. The combination of founder continuity, second-generation modernization, and institutional shareholder oversight is the kind of governance structure that compounds well over decades, not quarters.

Playbook lessons, drawing the threads together:

First, buy credentials when you can. The 2009 BPC Projects acquisition is one of the cleanest examples in Indian construction of using inorganic M&A to leapfrog a regulatory chokepoint. The lesson generalizes: when a binding constraint on your growth is a credential, license, or relationship, the right capital allocation is often acquisition, not organic build-out.

Second, choose your customers carefully. The decision to avoid road construction—made when roads were the glamour segment of Indian infrastructure—looks like a strategic error in retrospect until you study what happened to the margin profile of road-focused contractors. PSP's deliberate concentration in institutional and industrial work, segments where buyer sensitivity to price was lower than buyer sensitivity to execution, compounded into a structural margin advantage over fifteen years.

Third, invest in moats before the demand arrives. The Sanand precast plant was built before the Adani relationship existed. The capital-deployed industrial moat created its own demand by providing a capability that customers like Adani found uniquely valuable.

Fourth, family stewardship can outperform professional management—if the family makes the transition deliberately. The PSP succession structure, with Pooja Patel layered on top of P.S. Patel's continued operational engagement, is a model of generational handoff that more Indian family firms could study.

The key performance indicators to track: at most three, focused on what actually moves the underlying business.

The first KPI is precast plant utilization—what share of Sanand's installed capacity is being absorbed by active projects. This is the variable that, more than any other, determines whether PSP's strategic transition from service to manufacturing is succeeding.

The second KPI is order book composition and concentration—specifically the percentage of forward order book attributable to Adani Group entities, balanced against orders from non-Adani industrial and institutional clients. The healthier reading is a growing absolute order book where Adani is a meaningful but not overwhelming share, indicating both customer diversification and an Adani relationship working as designed.

The third KPI is operating margin trajectory—not the level, but the direction of change. PSP's structural margin should expand as precast utilization rises and as the industrial-customer mix becomes more dominant in revenue. Stagnant or declining margins through a period of rising revenue would be the leading indicator that the strategic transition is not converting to financial returns.

Watch those three. The rest is noise.

IX. Epilogue

Step back from the spreadsheets and the order books and the strategic frameworks for a moment, and consider what P.S. Patel actually built.

In 2008, a 53-year-old civil engineer in Ahmedabad incorporated a contracting business. He had no institutional capital, no national presence, and no obvious source of competitive advantage other than the quiet credibility he had accumulated on construction sites across Gujarat over the preceding three decades. He started by buying the credentials he needed to bid on serious work, built a reputation on a handful of government projects in his home state, and used that reputation to win, in 2017, a contract several times the size of his entire business.

That contract turned out to be the largest office building in the world. The company that delivered it was, by then, listed on the National Stock Exchange, had begun building one of India's largest precast concrete plants, and had quietly developed a track record that made it the natural execution partner for the country's most aggressive industrial capex program. By late 2024, India's largest industrial conglomerate had bought 30% of the company. By 2026, PSP Projects had become, in effect, the construction backbone of an Indian capex cycle whose scale has no precedent.

The arc is, in some sense, the arc of modern India. A small Gujarati contractor with relentless focus and a refusal to compete in commoditized markets became, over sixteen years, a Tier-1 institutional builder operating at the center of the country's largest industrial transformation. The story is not over—the Adani relationship is young, the precast facility is still ramping, the second-generation transition is still in progress. But the platform is in place, the capabilities are real, and the credibility is genuine.

P.S. Patel's legacy, viewed from 2026, is not the Surat Diamond Bourse. It is the company that built the Surat Diamond Bourse and then kept going. He took a family contracting business and converted it into a publicly listed industrial platform without losing the discipline that made it work. He chose his customers and his market segments with patience that, at the time, looked conservative and, in retrospect, looks visionary. He invested in industrial assets before the demand arrived and built relationships before they paid off.

For long-term investors thinking about Indian infrastructure exposure, PSP is a case study in a broader question: what does it look like when a family-owned contractor successfully transitions from a regional services business to a national industrial platform? The answer is messy, slow, and dependent on a thousand small operational decisions. But the answer, in PSP's case, is also visibly happening.

The next five years will tell whether the Adani relationship turns out to be a source of compounded growth or a source of compounded concentration risk. They will tell whether the Sanand precast plant achieves the utilization rates that the strategic case requires. They will tell whether Pooja Patel's second-generation leadership extends PSP's geographic footprint into the states where the next institutional building cycle will play out.

But the foundations—the credentials, the customer relationships, the capital commitments, the family stewardship, the operational discipline, the moat-building investments made before they were required—those foundations were laid carefully and they were laid well.

For a company that did not exist seventeen years ago, that is not a small thing.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube