Pricol Limited: The Instrument Cluster King Splits Itself in Two

I. Introduction & Episode Roadmap

Picture the last time you swung a leg over a motorcycle in India — a Hero Splendor idling at a Coimbatore traffic light, a TVS Apache threading through Bengaluru gridlock, a Royal Enfield thumping down a Himalayan switchback. Now look down at the little pod of dials and screens between the handlebars: the speedometer, the fuel gauge, the trip meter, the glowing warning lamps. There's a better-than-even chance that the electronics staring back at you were designed and built by a company most Indians have never heard of, headquartered in a mid-sized textile-and-engineering town in western Tamil Nadu.

That company is Pricol Limited. It is, by almost any measure, the quiet king of the Indian instrument cluster — the dashboard is its castle, and it has held that castle for the better part of five decades. It sits behind the cockpit of a large share of the two-wheelers on Indian roads, most of the country's commercial trucks, and the overwhelming majority of its tractors and construction machines.16 And yet, if you asked a hundred retail investors to name it, you'd be lucky to find one who could.

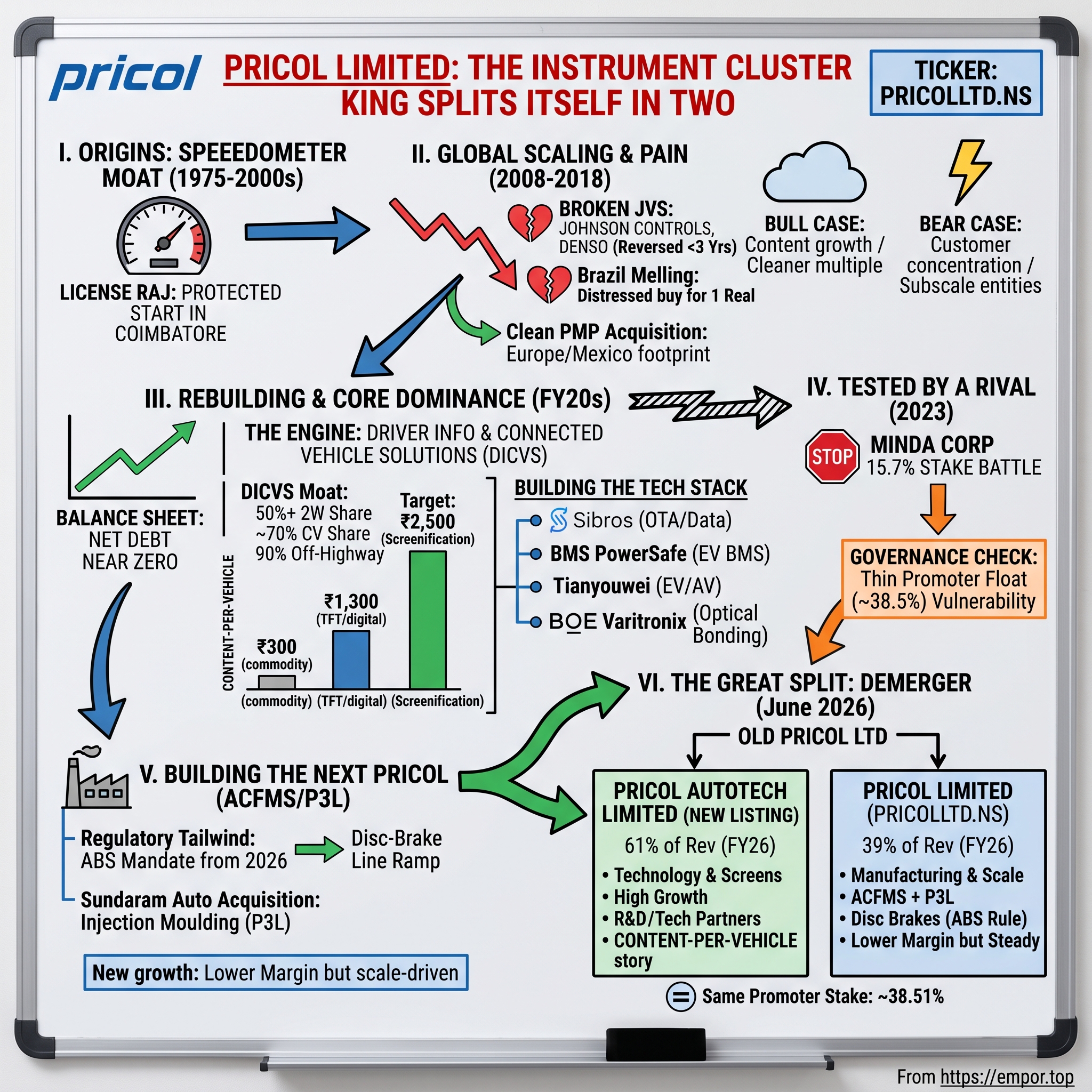

Here is the strange and genuinely interesting thing — the reason this is a story worth telling right now. In June 2026, the board of a company that spent fifty years building the single most dominant instrument-cluster business in India voted to demerge that very business out from under its own stock ticker. The crown jewel — the dashboards, the connected-vehicle software, the battery-management systems — is being spun into a brand-new listed entity called Pricol Autotech Limited. What remains under the old PRICOLLTD.NS ticker will be the smaller, less glamorous, more capital-intensive businesses: fuel pumps, oil pumps, disc brakes, and injection-moulded plastic.12

And it gets better. That demerger vote landed just six weeks after the founding Mohan family turned a generational page at the very top of the house — a matriarch stepping down as chairman after decades, her son taking the combined chairman-and-managing-director chair, a twenty-five-year-old granddaughter and an outside-trained strategy executive stepping onto the board — all in the same short window.35

So the question this article sets out to answer is deceptively simple, and it's the one any serious long-term investor should be asking: what do you actually own when you buy Pricol today, and what will you own a year from now?

To answer it honestly, we have to walk the whole arc. We'll start with the origins — a speedometer maker in license-era India. We'll sit through a painful decade of ambitious global joint ventures that mostly ended in reversal. We'll dissect exactly how Pricol came to own the instrument-cluster category, and whether that moat is as deep as it looks. We'll examine the newer, humbler businesses being left behind. We'll relive the 2023 episode when a listed rival quietly bought its way toward effective control. We'll scrutinize the 2026 leadership handover and the demerger itself. And we'll close with a clear-eyed bull and bear case. Throughout, we'll keep management's claims and the provable facts in separate columns — because the most useful thing we can do here is tell you not what Pricol says it is, but what the evidence says it is.

Let's start where it started: with a mechanical engineer and a dashboard dial.

II. Origins: From Speedometers to Coimbatore's Auto-Ancillary Champion (1975–2000s)

To understand Pricol you first have to understand Coimbatore, and to understand Coimbatore you have to understand that in India, industrial genius clusters in unlikely places. This is a city better known for cotton mills and wet grinders than for automotive electronics, tucked into the foothills of the Western Ghats, watered by the Noyyal river and cooled by the mountain gap that funnels breeze in from Kerala. But somewhere in the second half of the twentieth century, Coimbatore quietly became one of India's densest concentrations of small and medium engineering firms — pump makers, motor winders, foundries, machine shops. It was Tamil Nadu's answer to a mini industrial district, a place where a mechanical engineer with an idea could find a lathe, a supplier, and a skilled fitter within a few kilometres.

Into that milieu, in the mid-1970s, stepped Vijay Mohan. He was a mechanical engineer, and the vehicle for his ambition was a company called Premier Instruments & Controls Limited. Commercial production began in 1975 at what the company still calls Plant I in Coimbatore — and it's worth pausing on that date, because Pricol's own investor materials are careful to anchor the company's founding to 1975, not to some earlier or later year that occasionally floats around in secondary write-ups.6 The name "Pricol" itself is simply a compression of Premier Instruments & Controls; the firm formally shortened its trading identity over the years, eventually landing on Pricol Limited.

What did Vijay Mohan actually build? At the beginning, the humblest and most essential thing on a vehicle's dashboard: the speedometer. And around it, the whole family of instruments and sensors that tell a driver what the machine underneath them is doing — how fast, how much fuel, how hot, how far. This was not a glamorous product. But in the India of the 1970s and 1980s, it was a strategically protected one. This was the license raj — an economy walled off by import restrictions and industrial licensing, where a domestic manufacturer who could make a component indigenously, to acceptable quality, enjoyed a captive and growing market by default. India's two-wheeler and commercial-vehicle industries were expanding, foreign components were expensive and hard to import, and a local firm that mastered dashboard instrumentation was pushing on an open door.

It's worth dwelling on what "making a speedometer" actually demanded in that era, because it explains why the moat formed. A mechanical speedometer is a small marvel of precision engineering — a magnet spinning inside an aluminium cup, a hairspring, a calibrated needle, all of it tuned to translate the rotation of a wheel into a number a rider can trust at a glance, and to keep doing it through monsoon humidity, road vibration and a decade of abuse. Getting that right, at a price an Indian two-wheeler maker could stomach, was not trivial. Once a firm cracked it — and once an OEM had qualified that firm's instrument onto a bike or a truck — the incentive to go shopping for an alternative was close to zero. The part was cheap, the switching hassle was real, and the downside of a failed dashboard instrument (a rider who can't tell they're out of fuel) was reputationally ugly. So the relationships hardened early. Pricol wasn't just selling gauges; it was quietly wiring itself into the bill of materials of a generation of Indian vehicles.

That protected head start also shaped the company's temperament, in ways that echo right through to the 2026 demerger. This was never a Silicon Valley story of blitzscaling and pivots. It was a patient, engineering-led, family-supervised grind — reinvest, add a plant, qualify onto one more platform, hold the relationship. When India began dismantling the license raj in the 1991 liberalization, the comfortable moat of import protection started to erode, and Pricol had to learn to compete on merit against a widening field. The public listings that followed — Bombay in 1993, the National Stock Exchange in 1996 — were partly a response to that new world: a way to raise growth capital and put a market price on a business that had, until then, been valued mostly in the family's head.

That is the origin-myth kernel worth holding onto: Pricol's first and most durable advantage was not a brilliant technology leap. It was showing up early, in the right place, making an unglamorous but essential part well enough that Indian vehicle makers didn't have to look abroad — and then never letting go of that relationship. In an industry where a supplier gets "designed in" to a vehicle platform and then stays for the platform's entire multi-year life, being early and being reliable compounds quietly for decades.

The company scaled the way Indian manufacturers of that era scaled: plant by plant, geography by geography. It added a facility in Gurgaon in 1988 to be closer to the northern auto belt, and later expanded within Coimbatore at Chinnamathampalayam in 2004. It stepped onto the public markets in stages — listing on the Bombay Stock Exchange in 1993 and the National Stock Exchange in 1996 — giving the family both a currency for growth and, eventually, a public float that would matter enormously to our story later on.

Because from the very first day, this was a family business, and it stayed one. The Mohan family — Vijay, his wife Vanitha, and in time their sons Vikram and Viren — held the reins throughout. We'll keep this thread short for now, because the family drama pays off richly in later sections. But plant it in your mind: a founder-controlled, Coimbatore-rooted engineering company, built on the deeply un-flashy business of telling drivers how fast they're going, that turned a license-era head start into genuine category leadership. The question that would define the next chapter was what to do with that leadership — and specifically, whether to trade a piece of its independence for the scale and technology of the global giants. That temptation nearly cost the company its footing.

III. Scaling Through Partnership and Pain (2008–2018)

Every ambitious mid-cap eventually faces the same seductive proposition: the world's biggest players want to partner with you. For Pricol, the 2010s were the decade it said yes — twice — and learned, twice, what happens when a smaller company trades control for a global partner's technology and scale. If you want the single most useful lesson in this entire story, it's here. So let's walk through the wreckage carefully, because the pattern matters more than any one deal.

Two joint ventures, two reversals

The first partner was American. In March 2012, Pricol formed a fifty-fifty joint venture with Johnson Controls — the global seating-and-interiors and building-controls giant — housed in an entity called Johnson Controls Pricol Private Limited, which manufactured instrument clusters, displays and body electronics.11 On paper it was a coup: a Fortune-500-scale partner validating a Coimbatore component maker. In practice it lasted barely three years. By May 6, 2015, Pricol had bought out Johnson Controls' entire fifty-percent shareholding for a strikingly small sum — USD 3,151,853, a little over three million dollars.11 A partner enters at parity; three years later it exits for pocket change. That is not the price tag of a thriving venture.

The second partner was Japanese, and here Pricol went further — it ceded control. In April 2013, Pricol hived a set of its operations into a joint venture with デンソー Denso Corporation, the Toyota-affiliated components titan and one of the largest auto suppliers on earth. The structure told you everything: Pricol took the minority, roughly 49%, and Denso the controlling 51%. Two years later, the marriage was over. On March 18, 2015 — within days of the Johnson Controls exit — Pricol sold its remaining 49% stake back, and the entity became a wholly owned subsidiary of Denso Corporation of Japan.7 The consideration for Pricol's near-half of a business tied to one of the world's great component makers was about ₹20 crore — a modest figure that, like the Johnson Controls buyout, reads less like a triumphant exit and more like the unwinding of a bet that didn't pay.

Two attempts to trade control for global technology and scale; both reversed within roughly three years. It's worth asking on the record what that pattern reflects. The charitable reading is that Pricol was opportunistic — that it extracted what it needed and walked away cheaply. The skeptical reading, and the one an activist would press, is that a smaller partner without enough negotiating leverage tends to get squeezed, and that Pricol simply didn't have the hand it thought it held. Either way, the JVs left a scar and a data point we will return to in the analysis: when the global majors engage directly, Pricol has not obviously out-executed them.

A distressed bargain in Brazil

If the JVs were about ceding control, the next move was about grabbing an asset on the cheap. In January 2015, through a Spanish subsidiary, Pricol Espana, the company acquired 99.9% of Melling do Brasil — a Brazilian maker of oil pumps, water pumps, cold-start valves and aluminium castings, and one of the top two players in its niche in that country.8 The eye-catching part was the price: one Brazilian Real. A single Real — effectively a nominal consideration for a business that had booked around ₹3,011 million, roughly USD 301 million, in 2013 sales.8

A distressed-asset steal like that can be a masterstroke or a money pit, and honesty compels a flag here: the public record on how Brazil actually turned out is thin. Pricol's stated ambition at the time was to draw something on the order of ₹375 crore of revenue from Brazil within three years.8 Whether that target was ever hit is not something the accessible sources establish. So treat Melling as an open thread, not a proven win — a reminder that "we bought it for one Real" is a great headline and a lousy substitute for tracked results.

Housekeeping, related parties, and a corporate reincarnation

The mid-decade also saw a cluster of internal reshuffles worth naming briefly, because they touch governance. In the 2014–15 period, Xenos Automotive — a Coimbatore vehicle-security and lighting company majority-owned by the Mohan family — was merged into Pricol via a scheme of amalgamation. When a promoter-owned private company folds into the listed entity, it deserves a neutral governance flag: these related-party transactions carry an inherent self-dealing risk, whatever the merits of the specific deal. Then in 2016 came a piece of corporate reincarnation that still confuses data platforms today: a 2011-incorporated subsidiary absorbed the erstwhile Pricol Limited and was itself renamed Pricol Limited that November. That's why some screens show the stock's trading history beginning only around 2017 — the listed vehicle you buy today is, in a technical sense, a younger legal shell wrapped around a fifty-year-old business.

A first footprint abroad — and a pandemic gut-check

In 2017 came a cleaner, more strategically legible deal. Pricol acquired 100% of the wiping-systems business of PMP Auto Components — a business with roughly ₹250 crore of turnover and, crucially, manufacturing plants in the Czech Republic, Mexico and India, supplying wiper systems to Volkswagen, Fiat, Škoda and John Deere.12 This was Pricol's first real manufacturing footprint outside India, a foothold in Europe and North America it hadn't previously had.12 It was the kind of bolt-on that made sense — a defined product, a real customer book, and geographic reach.

Step back and the decade reads as a single, expensive tuition bill. Pricol spent the 2010s reaching outward — for global partners, for foreign assets, for a manufacturing footprint on three continents — and much of that reaching either reversed or left no clear evidence of payoff. The through-line is a company that knew it was a genuine leader at home but kept testing whether it could translate that into something bigger on the world stage, and kept finding the answer ambiguous. That's not a damning verdict; plenty of good companies serve their apprenticeship in failed expansions. But it does inform how an investor should weigh management's more recent confidence. When the team now says it can build a standalone technology business, or ramp a brand-new disc-brake line to 30% share, the fair response is not cynicism but memory: this is a management that has over-reached before, and the discipline it has shown since FY20 is precisely what has to hold for the current, far larger bets to work.

Then reality intervened. Around FY2020, as the pandemic hit and the Indian auto cycle rolled over, Pricol's revenue growth stalled and the company slipped into a consolidated net loss. It was the low point — a leveraged balance sheet, a demand shock, and a decade of expensive lessons behind it. What happened next is the more impressive part of the story, and it splits into two: how the core business fought its way to genuine leadership, and how the balance sheet was rebuilt. We turn to the first of those now.

IV. The Core Business: Winning the Instrument Cluster War

Here is the engine room. This is the business that built Pricol, that still throws off the majority of its revenue, and that — in the twist we'll get to — is about to be lifted out of the ticker entirely. Inside the company it goes by a mouthful of a name: Driver Information & Connected Vehicle Solutions, or DICVS. Strip away the acronym and it's the dashboard and its digital nervous system — instrument clusters, connected-vehicle telematics, sensors, and battery-management systems. In FY25 it was roughly 70% of group revenue; in FY26 it clocked ₹2,424.63 crore, or 61.17% of the total.62 Whatever else Pricol is, it is first and foremost a maker of the thing that tells you how fast you're going.

How Pricol actually wins — with evidence, not adjectives

It's easy to call a company a "market leader." It's more useful to show the share. Domestically, Pricol's grip on the instrument cluster is extraordinary and unusually well-documented. Depending on the source and the year, it holds somewhere between roughly half and two-thirds of the domestic two-wheeler cluster market — LKP Securities pegs it near 50%, other coverage nearer 65%.616 In commercial vehicles it commands about 70%. And in off-highway machines — construction and agricultural equipment — its share runs to roughly 90%, near-monopoly territory, though its position specifically in tractors is closer to 50%.616 Globally, Pricol is frequently described as the second-largest instrument-cluster maker by volume, behind only Japan's 日本精機 Nippon Seiki.16

What does that leadership mean competitively? Two things. First, it's relationship-and-qualification-based, not brand-based. An automaker "designs in" a supplier's cluster to a vehicle platform years before launch, through a grinding qualification cycle, and then keeps that supplier for the platform's whole life. That creates real switching costs — the moat here is the multi-year, engineered-in relationship, and we'll test its durability later. Second, the shape of the competition is unusual. Pricol's most direct domestic rival is Uno Minda (formerly Minda Industries) — but that comparison reveals a genuine "big fish, small pond" dynamic. Uno Minda is a vastly larger, more diversified auto-electronics conglomerate, carrying a market capitalization many multiples of Pricol's. Yet specifically in instrument clusters, it's the smaller player — roughly 15% share against Pricol's dominant position. Pricol is a minnow beside Uno Minda overall and a whale beside it in the one pond that matters most to Pricol. In digital clusters globally, the serious names are Continental, デンソー Denso, Visteon, Bosch and Nippon Seiki — the majors whose willingness (or not) to prioritize India is one of the real latent threats to the whole thesis.

The economic engine: content-per-vehicle

If share is the width of the moat, content-per-vehicle is the thing that makes it deeper every year — and it's the single most important idea in the Pricol story. A "cluster" used to be a mechanical needle on a dial, a cheap commodity worth a few hundred rupees. As vehicles digitize, that needle becomes a monochrome LCD, then a full-color TFT screen — essentially a small, ruggedized computer with graphics. Each step up the ladder multiplies the price of the part. Management's own framing, echoed by sell-side coverage: the blended value of a cluster has climbed from roughly ₹300 a decade ago to about ₹1,300 today, with a mid-term ambition of around ₹2,500.6 The mechanism behind that is a mix shift — Pricol guides its own TFT/digital/mechanical product mix moving from roughly 5%/75%/20% today toward something like 20%/80%/nil by FY28.6

Translate that into plain English, because it's the crux of the bull case. Even if Pricol never sold a single additional cluster — even if two-wheeler volumes flatlined — the company could keep growing simply because the same dashboard is worth three or four times as much as it used to be, and rising. That's the "screenification" thesis: the car and bike interior is turning into a screen, and Pricol gets paid more every time a mechanical dial becomes a display. It's a genuinely attractive structural tailwind. The honest caveat is that it also invites the deepest-pocketed global players into the segment, precisely because a ₹2,500 part is worth fighting over in a way a ₹300 part never was.

To feel why the price ladder is so steep, it helps to understand what actually changes as a cluster climbs it. A mechanical cluster is stamped metal, a motor, and a needle — a mature, low-value commodity. An LCD cluster swaps the dial for a monochrome or basic-color screen driven by a modest microcontroller; think of the jump from a wristwatch to a basic digital display. A full-color TFT cluster is a different animal entirely — it's a small, automotive-grade computer running graphics software, with a bright high-resolution panel, a capable processor, memory, thermal management, and a software layer that renders animated gauges, maps, call alerts and warning logic. LKP's coverage frames the pricing gap starkly: an LCD cluster fetches several times an analogue one, and a TFT cluster can command ten to fifteen times the price of a plain mechanical gauge.6 So the mix shift isn't a modest upsell — it's a re-rating of the product itself, from a stamped-metal commodity into an electronics-and-software assembly. That is why management can talk about average product value more than doubling over a two-to-three-year horizon even in a flat vehicle market, and why the same factory floor can throw off materially more revenue per unit shipped.6

The subtler point — and the one that ties the dashboard to the whole "connected vehicle" push — is that once the cluster is a computer, it becomes the natural home for everything else the vehicle wants to do digitally: over-the-air updates, telematics, diagnostics, navigation, and the human-machine interface. That's the logic behind the Sibros and display partnerships. Pricol isn't just selling a prettier gauge; it's positioning the cluster as the cockpit's central nervous system, the screen through which the connected features arrive. Whether it can hold that position against OEMs that would rather own the software themselves is one of the genuine open questions in the story.

Return for a moment to the Uno Minda comparison, because the "big fish, small pond" dynamic is worth sitting with — it's one of the more instructive competitive setups in Indian auto components. Uno Minda is the broad conglomerate: switches, lighting, acoustics, alloy wheels, sensors, a sprawling electronics portfolio, and a market value many times Pricol's. If you were picking a diversified auto-electronics compounder, you'd probably reach for Uno Minda first. And yet in the single product where Pricol lives — the instrument cluster — Pricol is the incumbent king and Uno Minda the challenger with a fraction of the share. This is the paradox an investor has to hold: Pricol is simultaneously the smaller, less diversified, more concentrated company and the dominant player in its chosen pond. Depth in one product versus breadth across many is a real strategic fork, and the demerger — which doubles down on focus rather than breadth — is Pricol answering that fork emphatically in favor of depth.

A technology stack being built, not just claimed

The skeptic's rejoinder to any "we're becoming a tech company" story is: prove it. To Pricol's credit, the evidence here is concrete and dated, not aspirational. Starting in 2021, the company assembled a web of partnerships aimed squarely at the software and display layers it couldn't build alone. In February 2022 it signed a five-year alliance with Sibros Technologies — a Silicon Valley connected-vehicle software firm backed by Google and Qualcomm venture arms — to handle over-the-air software updates, vehicle-data analytics and remote diagnostics across Indian and ASEAN markets, with Pricol supplying the hardware and firmware and Sibros the cloud platform.13 In June 2022 it took an exclusive license from France's BMS PowerSafe to manufacture EV battery-management systems locally.6 In October 2023 it struck a technology and supply pact with China's Heilongjiang Tianyouwei Electronics on EV and autonomous-vehicle technology — a deal that deserves a neutral flag for the China-partner geopolitical and technology-transfer exposure it carries in the current trade climate. In July 2025 it licensed switch and throttle-by-wire technology from Italy's Domino S.r.l. for two-wheelers across India and Southeast Asia.14 And in September 2025 it signed an MoU with 京东方 BOE Varitronix — part of BOE Technology Group, the world's largest display maker — to localize the optical bonding of LCD and TFT displays in India.15

Read as a whole, that stack is doing something specific: assembling, license by license, the pieces of a modern digital cockpit — the screen, the bonding, the software, the connectivity, the battery brain — that a mechanical-dial company could never have built from scratch. It functions as a partially "cornered" technology position. The fair question, which we'll press in the demerger section, is how much of it was negotiated on the strength of the combined group's scale, and how portable it really is to a standalone entity.

The concentration risk hiding inside the growth story

Now the part the growth narrative tends to skip. Pricol's customer roster reads like a who's-who of Indian mobility — Hero MotoCorp, TVS Motor, Bajaj Auto, Royal Enfield and Honda in two-wheelers; Tata Motors, Ashok Leyland and Mahindra in cars and commercial vehicles; John Deere, JCB and TAFE in off-highway; and export wins with the likes of BMW, Ducati and Harley-Davidson. Its penetration of Tata Motors is telling: on the Q4 FY26 call, management noted that something like 75–80% of Tata's car lineup uses Pricol clusters.17 That's the product leadership talking.

But leadership and dependence are two sides of one coin. Pricol's top five customers together account for roughly 65% of its domestic sales — a concentration that has crept the wrong way over the years, from the mid-50s a few years ago into the mid-60s now.16 The five names — TVS, Hero, Bajaj, Tata Motors and JCB — are among the most powerful buyers in Indian mobility. So sitting directly opposite Pricol's admirable product leadership is very real buyer power. When a handful of giant OEMs supply two-thirds of your domestic revenue, they hold meaningful leverage over price, and a single lost platform hurts. It is the quiet counterweight to the screenification story — and a KPI we'll flag for ongoing tracking.

One more thing to fix in your mind before we move on, because it's the hinge of the whole article: this business — the category leadership, the content-per-vehicle tailwind, the technology stack, the marquee customers — is the business that is about to leave the PRICOLLTD.NS ticker. Which raises the obvious question: what, exactly, is being left behind?

V. Building the Next Pricol: ACFMS, Precision Products, and the Sundaram Deal

If Section IV was the cathedral, this is the foundry next door — grittier, lower-margin, and, after the demerger, the whole of what "Pricol Limited" will be. So it's worth taking seriously on its own terms rather than as an afterthought, because for anyone holding the post-split ticker, this is the company.

Two businesses define the future Pricol. The first is ACFMS — Actuation, Control & Fluid Management Systems — which covers fuel-pump modules, oil and water pumps, and, most consequentially, a newly built disc-brake line. In FY25 it was roughly 30% of group revenue.6 The second is Precision Products, or P3L — injection-moulded plastic components — built around the acquisition of Sundaram Auto Components' injection-moulding business. Together they are a lower-margin, more capital-intensive, more commoditized set of activities than the dashboards upstairs. That's not a criticism; it's a description. Fuel pumps and moulded plastic compete on cost and scale, not on cornered display technology, and an investor in the future Pricol Limited should size their expectations accordingly.

A regulatory tailwind you can put a date on

The most exciting thing in the "new" Pricol is disc brakes, and the reason is a regulation. Effective January 1, 2026, India mandated anti-lock braking systems (ABS) on all two-wheelers — a rule that instantly enlarges the addressable market for two-wheeler braking hardware. Why does an ABS mandate pull disc brakes along with it? Because anti-lock braking, which pumps the brake to stop the wheel from locking and skidding, works hand-in-glove with disc-brake hardware; mandating the electronic safety system effectively pushes more of the two-wheeler fleet away from old-fashioned drum brakes toward discs. Previously, ABS was compulsory only on larger bikes; extending it across the board means millions of additional units a year now need the braking content Pricol is tooling up to supply. Pricol has built a disc-brake line squarely into that demand, with mass production for a major two-wheeler OEM guided to begin in the first quarter of FY27 off an initial capacity of half a million units, and management having already expanded planned disc-brake capacity from around ₹1.2 billion to ₹3 billion, chasing orders from six OEMs and a targeted 30% market share.6 Here's the honest framing: a government mandate is about the cleanest demand driver a component maker can ask for — it creates the market by fiat, on a fixed date, for everyone at once. The execution risk is entirely on Pricol's side of the fence: can it ramp a brand-new product line, on schedule, to automotive quality, and win share in a segment where it is a newcomer rather than the incumbent king? A 30% target from a standing start is ambitious against established braking specialists. That ramp is one of the concrete near-term proof points to watch, and it's worth remembering that a regulatory tailwind lifts every supplier chasing the same mandate — the tailwind is shared; the share is not.

The Sundaram deal — did Pricol overpay?

The P3L business was essentially bought, not built. On December 2, 2024, Pricol agreed to acquire the injection-moulding business of Sundaram Auto Components — part of the TVS Group — for ₹215.3 crore, a debt-free, all-cash deal executed through a wholly owned subsidiary, expected to add roughly ₹730 crore to consolidated topline.9 The completion followed in early 2025. Now, "was it a good deal?" is exactly the kind of question that deserves numbers rather than assertion, so here they are.

On the price: ₹215.3 crore worked out to about 3.4x EV/EBITDA on the target's FY24 figures.6 That is cheap — meaningfully below Pricol's own double-digit trading multiple, which means that if Pricol simply runs the asset as-is, the acquisition is accretive on multiple arbitrage alone. The cheapness has a plausible explanation that isn't "Pricol is a genius": this was a motivated seller reallocating capital under its own group strategy, not a competitive auction, and the plant was running at only around 60% utilization at takeover against a nominal 80%. In other words, Pricol bought an under-loaded asset from a willing seller at a low multiple. The early operating evidence is encouraging — management has pointed to margins improving within a couple of quarters of taking over — and targets a doubling of the business by FY28. Set against the murky, untracked Melling experience from a decade earlier, the Sundaram deal looks like the more disciplined and legible piece of capital allocation. But "looks like" is the operative phrase; the value creation is early, and the proof will be in the FY27–FY28 margin and utilization numbers, not the entry multiple.

The battery-management wildcard

There's one more piece bridging the two Pricols: battery-management systems for EVs. As of the Q3 FY26 call, BMS was in final development with a large two-wheeler customer, targeted for mass production within four to five quarters, built on that France-licensed technology.619 It's a genuine option on the EV transition — but note that management itself has flagged BMS as initially margin-dilutive, which is a useful tell about the economics of the "new" Pricol: several of its most exciting growth lines are, in their early innings, lower-margin than the dashboard business being spun away. The reader should hold both facts at once — real regulatory and EV tailwinds on one hand, a structurally thinner-margin, more capital-hungry engine on the other. Whether that engine can stand on its own as a separately listed company is a question the market will get to price directly, and soon.

Before we get to the split that forces that question, though, we need to rewind three years — to the moment a rival tried to take the whole thing over the open market.

VI. Tested by a Rival: The 2023 Minda Corporation Stake Battle

Every founder-controlled company tells itself a comforting story: we're in control, our shareholders are loyal, no one can touch us. In February 2023, Pricol's management learned in the bluntest possible way how fragile that story can be when your promoter float is thin and your business is a category leader.

On February 17, 2023, Minda Corporation — a listed auto-components maker, and a genuine competitor of Pricol's in instrument clusters (and note: this is Minda Corporation, a distinct company from the larger Uno Minda / Minda Industries) — quietly acquired a 15.7% stake in Pricol through open-market purchases, spending roughly ₹400 crore at around ₹209 a share.10 It was initially framed as a passive "financial investment." It caught Pricol's management flat-footed. And it should have: at the time, the Mohan family's promoter holding sat at only about 36.5%.10 Do that arithmetic and the vulnerability jumps out — a direct rival had, in a single day, assembled a stake nearly half the size of the founding family's, entirely on the open market, with no need for anyone's permission.

Then it escalated. In early May 2023, Minda Corporation moved to raise its stake to 24.5%, seeking Competition Commission of India (CCI) approval to do so. That crossed a line, in Pricol's telling, from financial investment to something that looked like a march toward influence or control by a competitor. Pricol formally objected to the CCI, arguing the two companies were direct rivals in instrument clusters and that letting one build a controlling-adjacent stake in the other threatened competitive neutrality — and it took the fight to the Madras High Court.10 On May 24, 2023, a division bench of the court handed Pricol interim relief, restraining the CCI from taking Minda's application on file.10 Legally cornered and with its path to a larger stake blocked, Minda Corporation ultimately exited the entire position through block deals.

A myth worth clearing up. Poke around Pricol's history and you'll occasionally hear it half-remembered as a company that weathered some sort of "fraud" or "embezzlement scandal." It's worth stating plainly, because narrative accuracy matters: that story does not check out in the record. The genuine governance flashpoint in Pricol's modern history is not an internal fraud — it's this Minda Corporation stake battle, a hostile approach by an outside rival exploiting a thin promoter float. Conflating the two would get the risk exactly backwards. The lesson here isn't "watch the insiders steal"; it's "watch how little of the company the founders actually own." That's a different, and for this business a more relevant, kind of vulnerability.

Management addressed the episode live on the Q4 FY23 earnings call on May 11, 2023 — a useful window into how leadership characterized the threat in real time, in the thick of it.20 But the deeper significance is strategic, and it feeds directly into the bull-bear case. This was a rare, almost unheard-of instance of one Indian auto-component supplier directly challenging another for effective control — and it happened because Pricol's promoter float was low enough to make it possible. A well-run, category-leading business is not, it turns out, immune to being tested for control when the founders own barely more than a third of it. That single structural fact — a modest promoter stake — is one we'll carry into the analysis, because it did not go away after Minda left. It is arguably the reason the family's next moves, in 2026, deserve such close reading.

VII. Current Management: A Family Business Turns a Generational Page Mid-Transformation

Now we arrive at the human heart of the story — and at a genuinely unusual piece of corporate choreography. Because in a single six-week stretch in the spring of 2026, the Mohan family did two enormous things at once: it changed the guard at the very top of the company, and it set in motion the largest corporate restructuring in Pricol's history. Doing either one alone would be a major event. Doing both together invites a pointed question we'll come back to: was this a premeditated, well-sequenced plan, or something more reactive?

The May 2026 handover

The dates matter, so here they are. On May 14, 2026 — the same day it reported FY26 results — Pricol announced a leadership transition. Vanitha Mohan stepped down as chairman after decades of service to the company.3 Her son, Vikram Mohan — a production engineer who had spent close to three decades inside Pricol, most recently as managing director — took over the combined role of Chairman and Managing Director.3 Alongside him, two new faces joined the board, subject to shareholder ratification. Madhura Mohan, twenty-five years old and the third-generation family member — a business-and-management graduate of Brunel University in London, associated with the company since September 2023 — was appointed an Executive Director, focused on customer relationships and ESG.5 And Siddharth Manoharan, thirty-five, an electronics-and-communication engineer from PSG College of Technology with a dual MBA from 复旦大学 Fudan University's School of Management and MIT's Sloan School, and nine years inside the Pricol group driving strategy, M&A and partnerships, became Group Executive Director for Business Strategy.5 All of it goes to shareholders for ratification at the 15th Annual General Meeting on August 5, 2026.45

Rounding out the executive bench: P.M. Ganesh, CEO and Executive Director, is an internal promote who joined Pricol as Chief Marketing Officer back in 2013 — continuity in the operating seat. And the finances have been run since July 2022 by CFO Priyadarsi Bastia, a chartered accountant with prior stints across the Murugappa Group, KPMG and Shanthi Gears — an outside professional in the numbers chair. So the shape of the team is a familiar Indian family-business hybrid: family control at the top and on the board, professionals in the CEO and CFO seats, and the next generation being installed with real titles rather than ceremonial ones.

Reading management by its behavior, not its adjectives

The most honest way to judge a management team is to watch what it did over time, not what it says about itself. On that test, Pricol's recent record is genuinely respectable in places, and worth crediting.

Start with the balance sheet, because this is where behavior speaks loudest. Coming out of the FY20 low — a loss-making year with meaningful leverage — management drove debt down hard and kept it down. By the end of FY26 the company carried only a sliver of net debt, a net-debt-to-equity ratio down near rounding-error territory, and management has publicly committed to keeping leverage conservative even as it funds a heavy capex program.17 That is a multi-year deleveraging effort followed through, not just promised — the single clearest piece of evidence that the team means what it says about financial discipline.

The dividend history tells a consistent story. Pricol paid no dividend for roughly seven years — through the deleveraging and reinvestment phase — and then, having earned the room, resumed modestly: a ₹2-per-share interim dividend declared in November 2025, at a conservative payout ratio near 10%.18 No evidence of a share buyback in a decade. This is capital allocation that prioritizes the balance sheet and reinvestment over shareholder payouts — defensible for a company funding a disc-brake ramp, a BMS launch and a demerger simultaneously, though income-oriented holders should know not to expect much yield.

Then there's guidance discipline, which is where you separate teams that set targets from teams that hit them. On the May 2023 call — the same one where they addressed the Minda fight — management targeted roughly ₹4,000 crore of revenue by FY26, with visibility to about ₹3,600 crore.20 FY26 actual came in at ₹3,963.85 crore.3 The target was essentially met. Now, the honest asterisk: a material chunk of that came from consolidating the acquired Sundaram/P3L business rather than pure organic growth. So the credit is real but qualified — they set a three-year number and hit it, partly by buying revenue. That's a fair thing to say out loud rather than round up to "management always delivers."

And promoter conduct on the governance dimensions we can check looks clean: the FY26 encumbrance disclosures show no promoter share pledging — no hidden leverage against the family stake.18

But independence requires flagging what isn't clean, and there's a real disclosure gap. In accessible sources, there was no detailed ESOP or management-incentive structure and no formal written capital-allocation policy to be found — precisely the documents that would let an outside investor judge whether management's pay is aligned with per-share value creation. That's a gap a diligent investor should close by pulling the Corporate Governance Report from the annual report directly, rather than assuming the best.

Who owns it — and the question the ownership raises

As of March 2026, promoters held 38.51% of Pricol — spread across Pricol Holdings and the individual family members, each holding single-digit percentages.1 Foreign institutions held around 15.6%, domestic institutions around 12.4%, and the public the remaining third, with names like Franklin India Small Cap Fund and Goldman Sachs's India equity portfolio among the disclosed institutional holders. Notice that the promoter stake — 38.51% — is barely higher than the ~36.5% that left the door open to Minda Corporation three years earlier. The float is still thin.

Which brings us to the credibility question this section has been building toward. A founding family that retains operational control, hands the chairmanship to the next generation, installs a twenty-five-year-old third-generation member and an outside-trained strategist on the board, and launches the largest restructuring in company history — all inside the same six weeks — is doing a great deal at once. An investor is entitled to ask, without cynicism, whether the succession looks premeditated and orderly or reactive and compressed, and what the whole sequence signals about the balance between genuine board independence and family control at a company that a rival tried to swallow just three years ago. The answer isn't knowable from the outside yet. But the demerger — the second half of that six-week flurry — is where the family's intentions get their sharpest test.

VIII. The Great Split: Demerging Pricol Autotech (June 2026)

So we arrive at the twist the whole article has been circling. On June 27, 2026, Pricol's board approved a Scheme of Arrangement to demerge the DICVS business — the instrument clusters, infotainment, telematics and battery-management systems, the crown jewel of Section IV — into a newly created entity, Pricol Autotech Limited.1 The mechanism is a clean 1:1 share swap: for every Pricol Limited share you hold, you receive one Pricol Autotech share, with no cash changing hands.12 What stays behind under the old ticker is exactly what we walked through in Section V — ACFMS and Precision Products.2

Let's be precise about the scale of what's being carved out, because it reframes everything. DICVS generated ₹2,424.63 crore in FY26 — 61.17% of the entire consolidated company.2 This is not a tidy-up of a stray division. It is the separation of the clear majority-revenue, historically higher-margin business from the remainder. On day one, both resulting entities will have identical shareholding — promoters 38.51%, public 61.49% — and both intend to list on the NSE and BSE.1 The scheme remains subject to approval by the National Company Law Tribunal and the stock exchanges, so as of this writing it is pending, not done — the AGM on August 5, 2026 is the near-term milestone, with NCLT approval the longer pole in the tent.12

The rationale — and the harder questions underneath it

Management's stated logic, articulated around the board's approval, is that the two businesses have grown different enough to deserve separate homes: create "two focused and independent business platforms" to enable faster decision-making, reduce operational complexity, and improve capital allocation.12 Unpack that and you get a genuinely coherent argument. DICVS is pitched as a technology-and-software business — one that needs its own R&D intensity, its own semiconductor and display-partner relationships, and an equity story that a growth investor can value on content-per-vehicle and screenification. ACFMS-plus-P3L is pitched as a manufacturing-and-scale business — one tied to production volumes, regulatory mandates like the ABS rule, and the blocking-and-tackling of cost and capacity. On that framing, welding the two together forces every investor to underwrite a blended thing they might prefer to value separately, and forces one capital-allocation process to serve two very different cost-of-capital profiles.

That's the bull version of a demerger, and it's not a straw man. But an independent read has to press on the questions the press release leaves unanswered — and they're the ones that will actually determine whether this creates value or just cost.

First, the subscale problem. Does splitting the higher-growth DICVS business away from the more capital-intensive ACFMS/P3L genuinely unlock value — cleaner allocation, a sharper equity story for each — or does it manufacture two smaller listed companies, each now facing the working-capital swings and end-market cyclicality that the combined entity could previously smooth over? A single company can let a strong quarter in dashboards cushion a weak one in fuel pumps. Two companies can't.

Second, the shared plumbing. What happens to the manufacturing, R&D and customer-relationship overhead the two businesses currently share? Splitting a house in two rarely halves the running costs; more often it duplicates the corporate functions, the listing compliance, the board and the leadership teams. That's real, recurring cost that has to be earned back through sharper focus.

Third — and this is the sharpest one — portability of the technology stack. Was the impressive web of partnerships we catalogued in Section IV (Sibros, BOE, Domino, the China pact) negotiated on the strength of the combined group's scale and balance sheet? A world-leading display maker or a Silicon Valley software firm signs with a partner partly for its heft and its customer reach. Peel DICVS out into a standalone Pricol Autotech, and it's a fair question whether those terms travel intact — or whether some of the leverage that won them sat with the group, not the segment.

What an investor in PRICOLLTD.NS actually needs to internalize

It's also worth situating this in the broader Indian market context, because demergers have become a fashionable value-unlocking tool — and the track record is genuinely mixed. The theory is elegant: a conglomerate discount collapses when you let each business trade on its own multiple, and a fast-growing unit no longer subsidizes a slow one in investors' blended math. Sometimes that works and the sum of the parts re-rates handsomely. Other times the parts simply inherit the parent's problems at a smaller scale, plus a fresh set of standalone-company costs — two boards, two compliance apparatuses, two management teams to pay. The 1:1, no-cash structure Pricol chose is shareholder-friendly in the narrow sense that no one is being asked to write a cheque and no dilution is imposed; every existing owner simply wakes up holding two stocks instead of one. But "no cash changes hands" is not the same as "value is created." The value question turns entirely on whether the market pays more for the two halves apart than it did for the whole — and that verdict won't be in until Pricol Autotech actually trades.

Here is the plain-English bottom line, and it's the answer to the question we opened with. Today, the PRICOLLTD.NS ticker still reflects the combined business — dashboards and fuel pumps together. After the demerger completes, an investor's economic exposure to the instrument clusters, the connected-vehicle software and the content-per-vehicle tailwind — everything that made Pricol famous — will live in the new Pricol Autotech shares received through the swap, not in Pricol Limited itself. Pricol Limited, the surviving ticker, will be the smaller, lower-margin, more capital-intensive ACFMS-plus-P3L company. Same shareholders, two stocks, two very different stories. Buy the ticker today and you're buying the combination on its way to becoming two things. That is not a criticism of the deal; it is simply the fact pattern any buyer needs to hold clearly in mind — because the market has not yet told us how it will price the two halves apart versus the whole.

Which is exactly the terrain of the final analysis: is this a category leader whose parts are worth more unbundled, or a well-run company adding complexity and cost to a franchise that was working?

IX. Playbook, Powers & Analysis

Time to war-game it. We'll run the pre-split instrument-cluster core through two lenses investors know — Michael Porter's Five Forces and Hamilton Helmer's 7 Powers — then name the handful of KPIs that actually matter, map the risk radar to specific business mechanisms, and lay out the bull and bear cases without a thumb on the scale.

Porter's Five Forces on the cluster core

Buyer power — moderate to high, and the single biggest structural check on the business. With the top five customers supplying roughly two-thirds of domestic sales, and those customers being some of the most powerful OEMs in Indian mobility, the buyers hold real leverage over price and terms.16 Pricol's product leadership pushes back — a Tata Motors that runs Pricol clusters across 75–80% of its cars can't switch casually17 — but the concentration is rising, not falling, and that's the wrong direction for a supplier.

Supplier power — real but narrowing. The critical inputs are semiconductors and display components. Management has flagged chip shortages on recent calls, and there's a structural roughly six-month lag before raw-material and chip-cost inflation can be passed through to OEM pricing — a margin squeeze that shows up whenever input costs spike.17 Pricol's global scale in clusters gives it some negotiating heft on component pricing, but it is a price-taker on silicon, not a price-setter.16

Threat of new entrants — low at the front door, real at the side door. No start-up is going to win a two-wheeler cluster platform overnight; the multi-year OEM design-in and qualification cycle is a genuine barrier. The real threat is the global majors — Continental, デンソー Denso, Nippon Seiki — choosing to prioritize India as clusters become ₹2,500 screens worth fighting for, or OEMs deciding to pull connected-vehicle software in-house. The unwound Denso and Johnson Controls JVs are the cautionary data point here: when the giants engaged directly, Pricol didn't obviously out-execute them.

Rivalry — moderate, concentrated. Day to day, the direct contest is mainly against Uno Minda in clusters — intense but not fragmented. Pricol's dominant share buys it pricing stability the way a category leader usually enjoys.

Substitutes — low in the near term. Every vehicle needs a driver-information system; the substitution risk is less "another product" than "the OEM builds the software layer itself," which loops back to the new-entrant/vertical-integration threat.

The 7 Powers read

Of Helmer's seven sources of durable advantage, the one Pricol most clearly possesses is switching costs — the long qualification cycles and design-in relationships that keep a cluster supplier embedded for a platform's life. That's reinforced by a partial cornered resource: the growing stack of exclusive technology licenses (Domino, BMS PowerSafe, the BOE tie-up) that competitors can't simply replicate.14156 Where the case is thinner is scale economies and cost leadership — the failed global JVs are direct evidence against assuming Pricol can out-scale or out-cost the majors on their terms. There's no obvious network economy or branded consumer pull; end drivers don't choose their dashboard. So the honest 7 Powers verdict: a real, relationship-and-technology moat around the core, but not an impregnable cost or scale fortress — a leadership built on being embedded and being early, which is durable until a bigger player decides the prize is worth the fight.

The KPIs that actually matter

Cut through the noise and there are three numbers worth tracking:

-

Content-per-vehicle / ASP trend (the ₹300 → ₹1,300 → targeted ₹2,500 arc). This is the clearest single read on whether the screenification thesis keeps compounding, and it matters most for Pricol Autotech once it lists. If ASP keeps climbing as the mix shifts to TFT, the growth story is intact regardless of vehicle-volume cycles.6

-

Top-5 customer concentration. It has moved from the mid-50s toward two-thirds of domestic sales even as the business grew — a direct gauge of who holds the power in Pricol's most important relationships.16 If it keeps rising, buyer power is winning; if it stabilizes or falls, Pricol is diversifying its dependence.

-

Post-demerger Pricol Limited (ACFMS + P3L) standalone EBITDA margin, and the disc-brake / BMS ramp. This is the concrete proof of whether the "new," smaller Pricol has a credible margin and growth story on its own — or whether it's the leftover business dressed up as a fresh start. Watch the disc-brake mass-production start in Q1 FY27 and the BMS launch timeline.6

Risk radar — mechanism by mechanism

The risks worth naming are the ones with a clear business channel. Two-wheeler cyclicality and EV transition — a downturn in bike volumes hits the core directly, and while management insists its margins are propulsion-agnostic (a cluster is a cluster whether the vehicle burns petrol or electrons), that claim has not been stress-tested through a full EV-share inflection. Customer concentration, already covered, is a standing risk to pricing. Semiconductor and raw-material cost pass-through lag compresses margins for roughly two quarters whenever input costs jump.17 Execution risk now includes the novel challenge of running two listed entities where there was one. The thin promoter float (~38.5%) has already, once, attracted a rival's stake-building — that vulnerability persists.1 And the China partnership (Tianyouwei) carries geopolitical and technology-transfer exposure in a tense trade environment.

The bull case

Pricol is a genuine category leader with evidenced — not merely asserted — market share and a structural content-per-vehicle tailwind that can grow revenue even in flat vehicle markets.616 It has a deleveraged balance sheet, a largely-delivered guidance record, and two credible growth lines — disc brakes and BMS — riding real regulatory and EV tailwinds.1736 The demerger, if it works as intended, sharpens capital allocation, gives each business its own equity currency for future M&A, and lets the market pay a proper technology multiple for the dashboard business it currently buries inside an auto-ancillary conglomerate.

The bear case

The moat is relationship-based, and the customers on the other side of those relationships are growing more concentrated and more powerful, not less.16 The company's two prior attempts to partner with global majors both unwound cheaply within three years — a real question mark over its staying power if Continental, Denso or Nippon Seiki decide to compete hard for the ₹2,500-screen prize.711 The promoter float is thin enough that the business has already been tested for control once.10 A generational succession and the largest restructuring in company history landed in the same month, with thin public disclosure on management incentives.5 And the demerger itself carries the unglamorous risk that splitting one working company into two adds duplicated cost and cyclicality-exposure without adding commensurate value — two subscale entities where there was one that could smooth its own bumps. The surviving Pricol Limited, specifically, will be the lower-margin, more commoditized half, and it has to prove a standalone margin story it has never had to prove before.

Net of all that, this is neither a slam-dunk compounder nor a value trap — it's a real category leader making a genuine strategic bet on itself, with the outcome hinging on execution the market can't yet see. Which is exactly why the next twelve months are the ones to watch.

X. Epilogue & What to Watch

Stand back from the detail and the shape of the thing is almost cinematic. A mechanical engineer in Coimbatore starts making speedometers in the license-raj 1970s. Half a century of incremental, unglamorous execution turns that into genuine, evidenced leadership in the one part of every vehicle a driver actually looks at. Along the way the company burns its fingers twice reaching for global partners, gets bought for a single Real in Brazil, gets nearly cornered by a rival on its own share register, rebuilds its balance sheet, and then — at the very moment it hands the company to its next generation — decides to split its crown jewel out into a separate stock.

The near-term catalysts are concrete and dated. Watch the National Company Law Tribunal for approval and a timeline on the demerger. Watch the August 5, 2026 AGM, where shareholders ratify the new board.45 Watch Pricol Autotech's eventual listing, and — this is the interesting one — watch how the market prices the two resulting entities separately versus the combined pre-split multiple, because that spread is the market's verdict on whether this split creates value or merely rearranges it. And watch FY27 guidance, and whether disc-brake mass production and the BMS launch actually land on schedule, because those are the proof points for the smaller company left holding the old ticker.

The lasting business lesson is a subtle one, and it's bigger than Pricol. A company can build a genuine, evidenced product-leadership position through decades of patient execution — and still face real, unresolved strategic uncertainty about whether to keep that asset, split it, or partner it away. Leadership in a product is not the same as certainty about what to do with it. And a low promoter float is a permanent reminder that even a well-run, category-leading business isn't automatically immune to being tested for control.

So we end where we began, with the only question that really matters for anyone thinking about owning this. Pricol today is a quiet market leader deciding, in real time and in full public view, what kind of company it wants to be next. Buy the stock now and you are buying that decision mid-flight — a combined business on its way to becoming two, one a technology-and-screens story, the other a pumps-brakes-and-plastic story, with the same family holding just over a third of both. Whether that unbundling sharpens the story or simply doubles the overhead is the wager. Know which of those two companies you actually want to own — because in a year, the market will have handed you shares in both.

References

-

Pricol Demerger Explained: Value Unlocking or Just a Split? — INDmoney ↩↩↩↩↩↩↩↩

-

Pricol Board Approves Strategic Demerger of DICVS Business to Pricol Autotech — ScanX, 2026-06-27 ↩↩↩↩↩↩↩

-

Pricol FY26 Revenue Rises 51.24%; Company Announces Leadership Transition — Autocar Professional, 2026-05-15 ↩↩↩↩↩

-

Pricol Board Approves Leadership Overhaul; Reports 51.24% Revenue Growth in FY26 — ScanX, 2026-05-14 ↩↩

-

Pricol Limited — Board Meeting Outcome & Director Appointments, BSE filing, 2026-05-14 (PDF) ↩↩↩↩↩↩

-

LKP Securities — Pricol Limited Initiating Coverage: "Instrumental in Screenification", 2025-07-18 (PDF) ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Pricol exits joint venture with Denso — Autocar Professional, 2015-03-18 ↩↩

-

Pricol Completes Acquisition of Melling (Brazil) — PR.com, 2015 ↩↩↩

-

Pricol acquires Sundaram Auto Components' injection moulding business for Rs 215.3 crore — Autocar Professional, 2024-12-02 ↩

-

Pricol gets relief from Madras High Court in tussle with Minda Corp — Business Standard, 2023-05-25 ↩↩↩↩↩

-

Pricol buys Johnson Controls' 50% stake in JV for $3.1 mn — Daily Excelsior, 2015 ↩↩↩

-

Pricol acquires PMP wiping systems business — The Machinist, 2017 ↩↩

-

Pricol inks strategic technology alliance with Sibros — Autocar Professional, 2022-02-23 ↩

-

Pricol Limited partners with Italy's Domino S.r.l. for two-wheeler control systems — Autocar Professional, 2025-07-15 ↩↩

-

Pricol signs MoU with BOE Varitronix to localize TFT optical bonding in India — Business Upturn, 2025-09-30 ↩↩

-

PRICOL Ltd — Consistently Performing Stocks — Finvezto Compass ↩↩↩↩↩↩↩↩↩↩

-

Pricol Ltd (BOM:540293) Q4 2026 Earnings Call Highlights — Yahoo Finance/GuruFocus, 2026-05-15 ↩↩↩↩↩↩

-

Pricol jumps as Q2 PAT spurts 42% YoY to Rs 64 cr; declares ₹2 interim dividend — Business Standard, 2025-11-07 ↩↩

-

Pricol Q3 FY26 Earnings/Results Summary — InvestyWise, 2026-01-30 ↩

-

Pricol Limited (PRICOLLTD) Q4 FY23 Earnings Concall Transcript — AlphaStreet, 2023-05-11 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube