Precision Wires India Limited: The Enamelled Engine of Modern India

I. Introduction: The Invisible Backbone

There is a sound you have heard your entire life but have never consciously registered. It is the low, almost imperceptible hum of a transformer mounted on a pole outside your apartment block at 2 a.m. in a Mumbai summer. It is the soft whir of a पंखा pankha ceiling fan oscillating above a तांबा copper-roofed temple in सूरत Surat. It is the high-frequency whine of a विद्युत वाहन EV Tata Nexon EV accelerating away from a traffic signal at Marine Drive. It is the click of a Voltas air conditioner kicking into compressor mode in a Gurgaon high-rise on a 47-degree afternoon.

Every one of those sounds, every single one, is the sound of a copper wire wound thousands of times around a steel core and coated in a chemical varnish so thin you cannot see it with the naked eye. Strip away that wire and the modern Indian economy goes dark. Strip away the coating on that wire — the enamel that prevents two adjacent windings from kissing each other and short-circuiting — and the entire global electrification project, the great संक्रमण transition from hydrocarbon to electron, simply does not happen.

This is the story of the company that, more than any other in South Asia, makes that coating work. Precision Wires India Limited — known to its customers as PWIL, to its retail shareholders as PRECWIRE, and to its founding family simply as "the Wires business" — is the kind of company that the Indian retail investor never quite falls in love with the way they fall in love with रिलायंस Reliance Industries or टाटा Tata. There are no Bollywood-style founder myths. There is no consumer brand. There are no flashy quarterly press conferences. There is, instead, a 50,000+ metric-tonne-per-year industrial machine that quietly supplies copper winding wires to almost every motor, transformer, generator and refrigerator manufacturer of consequence on the subcontinent.1

So why are we doing two and a half hours on a "boring" wire company? Two reasons. First, because the world is electrifying at a pace and at a depth that has no historical analogue. The internal combustion engine, which dominated the 20th century, is being replaced by the electric motor — and an electric motor is, fundamentally, copper wire wound around a core. The coal-fired grid is being replaced by a hybrid grid of solar, wind, hydro and nuclear, all of which require staggering amounts of new transmission and transformation capacity. Every megawatt of new generation needs miles of new wire.

Second, because PWIL is a perfect case study in a pattern we love at Acquired: the "boring" industrial business that, on closer inspection, has built a moat so quiet and so cumulative that competitors cannot replicate it without spending a decade and a small fortune on rejected batches. The enamel chemistry. The OEM certification cycles. The relationships with the तांबा copper cathode importers. The hedging book. The metallurgical know-how. Each one, individually, looks trivial. Together, they form a process power that has kept this family-run business at the top of the Indian winding-wire heap for three and a half decades.

This is also a story about a family. The Mehtas — मेहता परिवार — have run this company from a single rented unit in मुंबई Mumbai in 1989 to a publicly listed enterprise with manufacturing footprints in सिलवासा Silvassa and पालेज Palej, Gujarat.[^2] They are not flashy. They do not appear on the cover of business magazines very often. They are, in their own description, "hands-on industrialists" — people who know the difference between polyesterimide and polyamide-imide enamel coatings the way a sommelier knows the difference between a Burgundy and a Bordeaux.

Over the next two hours, we'll take you from the dusty लाइसेंस राज License Raj era in which this company was conceived, through the liberalisation boom of the 1990s, the white-goods explosion of the 2000s, the great capex cycle of the 2010s, and into the present-day विद्युतीकरण electrification moment in which PWIL finds itself sitting on top of one of the most attractive structural tailwinds in Indian industrial history. We'll dive deep into the chemistry, the capital allocation, the management lineage, and the seven-powers analysis. And we'll ask the question that every long-term fundamental investor eventually asks of every category leader: is this a category king, or is it just the tallest dwarf in a commodity room?

Buckle in. We're going to wind ourselves around this story very carefully.

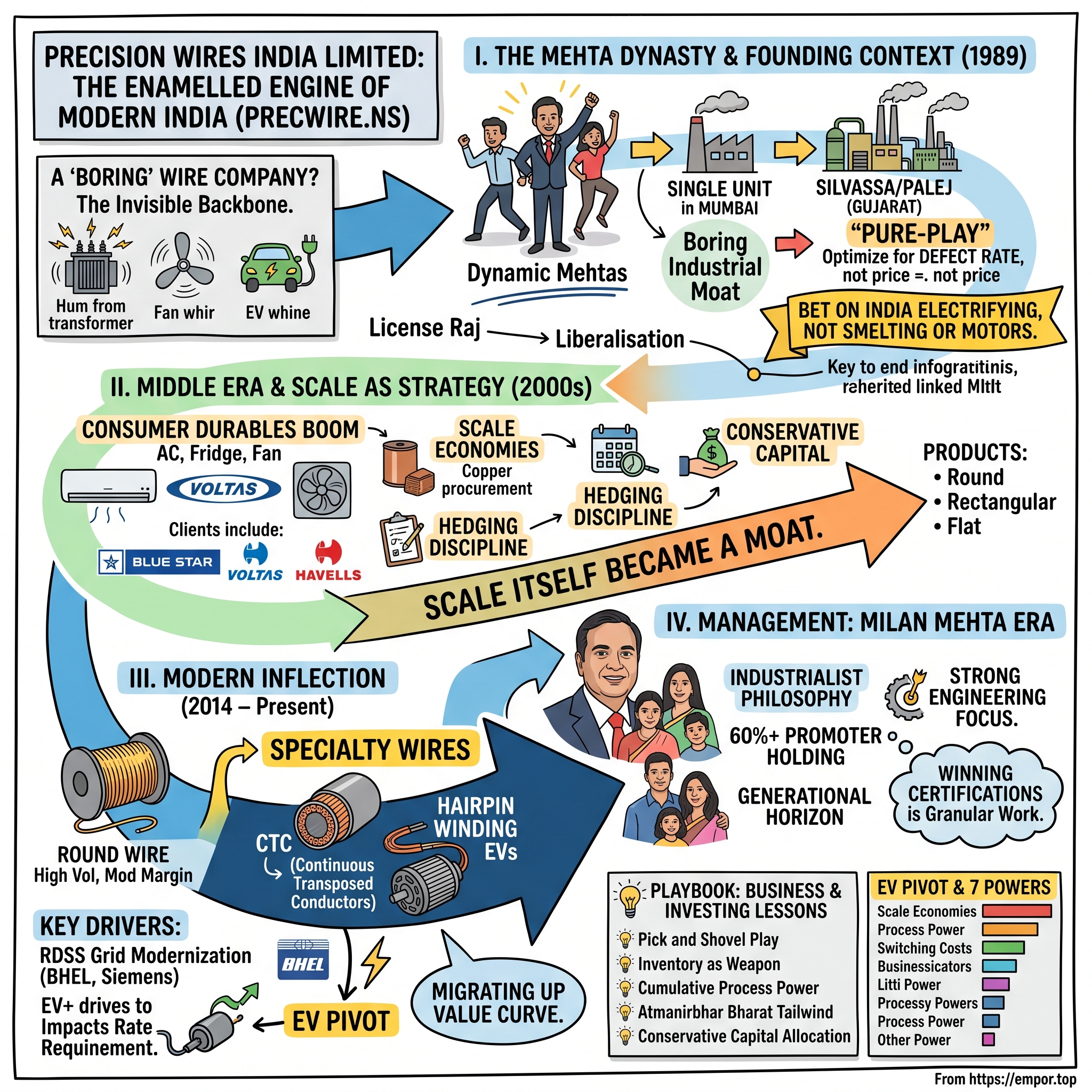

II. The Mehta Dynasty & Founding Context

Picture India in 1989. Rajiv Gandhi is still the Prime Minister, although his political fortunes are crumbling. The Berlin Wall is about to fall. Manmohan Singh's liberalisation reforms are still two years and one balance-of-payments crisis away. The Indian economy is operating under the elaborate permission-and-quota apparatus that everyone, even at the time, had begun calling the लाइसेंस राज License Raj — a system in which an entrepreneur could spend more time waiting for an industrial license than actually building the factory the license eventually authorised.

It is in this context that a small Gujarati-Marwari trading family, the Mehtas, looked at the Indian electrical industry and noticed something nobody else seemed particularly excited about. India was about to electrify on a massive scale. Every village. Every town. Every factory floor. And while everyone was thinking about the glamour businesses — the cables, the switchgear, the transformers themselves — almost nobody was thinking about the unglamorous component sitting inside the transformer: the enamelled copper winding wire.

The Mehtas incorporated Precision Wires India Limited in 1989.2 The name was not an accident. There were already wire-drawing units in the country. There were already enamelling units. But "precision" — the word, and the philosophy — was the wedge they chose to drive into the market. Their bet was simple: the Indian industrial customer of the future would not pay extra for a wire, but they would absolutely refuse to buy a wire whose enamel coating cracked under thermal stress. As Indian manufacturing matured, the defect rate would become the deciding variable. Not price. Not capacity. Defect rate.

This is a subtle but important insight, and it tells you a lot about how the Mehtas thought about the business from day one. Copper wire, at its most basic, is a commodity. Anyone with a wire-drawing machine and a furnace can pull a copper rod into a thinner copper strand. But the enamel — the thin polymer film, anywhere from 20 to 80 microns thick, that wraps the wire so that adjacent windings inside a motor or transformer don't short-circuit when they touch each other — the enamel is chemistry. It is a controlled, repeatable, painstakingly tuned chemical and metallurgical process. Get it slightly wrong and the wire will fail after six months in a Bombay monsoon. Get it right and it lasts 25 years in a steel mill furnace room.

In the late 1980s, the Mehtas focused obsessively on this layer. While competitors were optimising for tonnes-per-month output, PWIL was optimising for consistency of enamel thickness across thousands of kilometres of drawn wire. This is the kind of decision that does not show up in a balance sheet for fifteen years. And then, suddenly, it shows up everywhere — because OEMs only certify suppliers whose batch-to-batch defect rates fall below some tiny threshold.

The geography of the founding matters. The early manufacturing was rooted in the industrial belt of Gujarat and the union territory of दादरा और नगर हवेली Dadra and Nagar Haveli — specifically Silvassa, an enclave that, thanks to historical tax incentives, had quietly become one of the densest concentrations of small and medium electrical-component manufacturers in the country.2 Silvassa offered cheap land, generous tax holidays, and, critically, a workforce that had been training on electrical winding for a generation. The Mehtas later added Palej in Gujarat, sitting on the industrial corridor between अहमदाबाद Ahmedabad and वडोदरा Vadodara.1

What's interesting, looking back, is what the Mehtas did not do. They did not vertically integrate upstream into copper smelting — they left that to हिंदालको Hindalco and स्टरलाइट Sterlite. They did not vertically integrate downstream into motor or transformer manufacturing — they did not want to compete with their own customers. They picked one slice of the value chain — the conversion of copper rod into enamelled winding wire — and they decided to be the best in South Asia at that one slice. In the language of strategy, they ran a "pure-play" strategy in a market full of conglomerates. In the language of the Acquired playbook, this is the focused-supplier-to-an-expanding-end-market move that, executed patiently, can compound for forty years.

The bet, ultimately, was a bet on India itself. A bet that this country, with its expanding middle class, its rapidly industrialising economy, and its enormous unmet demand for electric motors of every shape and size, would over the next several decades become one of the largest consumers of enamelled copper winding wire in the world. That bet, viewed from 2026, looks rather prescient.

But getting there required a second, harder bet: that scale itself would become a moat.

III. The Middle Era & Scale as a Strategy

If the late 1980s and early 1990s were about establishing the technical reputation of the brand, the 2000s were about turning that reputation into industrial mass. This is the era in which PWIL stopped being a high-quality boutique wire-maker and started becoming the biggest wire-maker.

The pivot is set against a roaring macro backdrop. India between 2003 and 2008 was, in retrospect, in the early innings of a once-in-a-generation consumer durables boom. ब्लू स्टार Blue Star, वोल्टास Voltas, गोदरेज Godrej, व्हर्लपूल Whirlpool India, एलजी LG India, सैमसंग Samsung India, बजाज Bajaj Electricals, हैवेल्स Havells — every single one of them was rapidly scaling air conditioner, refrigerator, washing-machine and fan production to feed a middle class that had suddenly discovered, post-liberalisation, that they could actually afford an inverter AC. Every single one of those appliances has at least one and often several electric motors. Every single one of those motors needs winding wire.

PWIL read this signal early. The strategic question they asked themselves around 2002-2003 was: can we be the supplier-of-record to every major white-goods OEM in India? The answer was yes, but only if they had two things: first, the volume capacity to actually serve a fast-growing customer like a Voltas without becoming a bottleneck; and second, the technical certification at each customer to be on the approved-vendor list.

So they built. The Palej facility was scaled up. The Silvassa lines were upgraded.1 The wire portfolio was extended from simple round copper conductors used in पंखा pankha motors to more sophisticated specifications for compressor motors, fractional horsepower motors, hermetic motors for refrigerators, and submersible pump motors. Each new specification required a separate certification cycle at each OEM. Each certification cycle took anywhere from six to eighteen months. Each one, once won, created what economists like to call a switching cost — and what production engineers call "stop calling me, the wire works."

This is where economies of scale start to compound non-obviously. PWIL's biggest cost item, by a very long margin, is copper. Copper is a globally traded commodity whose price swings violently with the LME (London Metal Exchange). For a wire manufacturer of any size, copper procurement is the single most important operational discipline. Buy at the wrong time and you lock in losses for an entire quarter. Buy at the right time, on the right basis, and you generate margin out of pure procurement discipline.

PWIL's scale gave it three structural advantages in copper procurement. First, the ability to buy directly from हिंदुस्तान कॉपर Hindustan Copper, बिड़ला कॉपर Birla Copper (Hindalco), and international cathode suppliers, bypassing the middlemen who eat margin from smaller competitors. Second, the ability to operate a back-to-back hedging model in which they hedge copper exposure forward against fixed customer orders — eliminating directional risk on the metal. Third, working capital efficiency: scale lets you turn inventory faster, freeing up cash that smaller players would have tied up in copper rod sitting in a warehouse.

Now contrast PWIL's capital posture with the typical Indian SME wire manufacturer of the 2000s. The typical SME took on heavy bank debt to expand. The typical SME, when copper prices crashed in 2008-2009 alongside the global financial crisis, found itself sitting on copper rod inventory worth substantially less than the loans they had taken to buy it. Many simply did not survive the cycle. PWIL did survive — and emerged from it with a stronger balance sheet, lower relative debt, and the ability to pick up market share organically from peers who could no longer service their OEMs.

This is the playbook lesson buried in the middle era of PWIL's life. Conservative capital allocation in an industry where most peers leverage themselves to the moon is, by itself, a moat. You don't need a patent. You don't need a brand. You just need to be the supplier still standing when copper goes from $8,000 a tonne to $3,000 a tonne and back to $9,000 a tonne over an eighteen-month window. In an industry where customers fear nothing more than a supplier disappearing mid-contract, being the supplier who never disappears is itself the differentiator.

By the end of the 2000s, PWIL had locked in supplier relationships with most of the meaningful white-goods OEMs in India. The wire flowing into Voltas window ACs, Crompton ceiling fans, LG refrigerator compressors, and submersible pumps headed to Punjab tubewells was, by then, increasingly likely to have started life as a copper rod entering a PWIL drawing machine in Silvassa.

The next leg of the story, however, would require a different kind of scale — not just bigger, but better. Higher specification. Higher margin. Higher barrier-to-entry. The kind of wire that sits inside a 765 kV power transformer or a hairpin stator in an electric vehicle.

IV. The Modern Inflection: 2014 – Present

Walk into the Palej manufacturing complex around 2015 and you would have seen a transition in progress. The familiar bays of round-wire drawing machines were still there, humming away, churning out the bread-and-butter SKUs that fed the appliance industry. But adjacent to them, increasingly, was new equipment — heavier, more sophisticated, more specialised. Rectangular wire mills. Flat wire mills. And, in a quietly walled-off section that the company did not particularly advertise, the production lines for सीटीसी CTC — Continuous Transposed Conductors.

This is the modern PWIL story, and it is the story that matters most for any investor trying to model the next five to ten years.

Let's start with the capacity numbers, because they tell the macro story succinctly. Over the decade from roughly 2014 to 2024, PWIL roughly doubled its production capacity, taking total installed enamelled winding wire capacity to over 50,000 metric tonnes per annum across its plants.1[^2] That is a meaningful number in the Indian context — it makes PWIL, by a comfortable margin, the largest enamelled winding wire producer in South Asia and one of the larger ones in Asia outside China and Japan.

But the more interesting story is what kind of wire that capacity is now producing.

For the first 25 years of its life, PWIL was overwhelmingly a "round wire" company. Round wire — exactly what it sounds like, a cylindrical copper conductor with an enamel coating — is the workhorse of small motors. Fan motors. Pump motors. Compressor motors. The output is high. The margin is modest. The competition is broad. Every regional wire-maker can do round wire to some specification.

Starting roughly in the mid-2010s, PWIL began deliberately tilting its product mix toward rectangular and flat wire. Why does this matter? Because rectangular wire is what high-efficiency motors use. When you wind a motor stator with rectangular conductors instead of round ones, you can pack more copper into the same physical slot — the cross-section utilisation jumps from roughly 70% with round wire to over 90% with rectangular wire. More copper per unit volume means more torque, less heat, higher efficiency. For high-end industrial motors, traction motors in trains, and — critically — electric vehicle motors, rectangular wire is not a preference. It is a requirement.

The most strategically important product in this mix, and the one that deserves a deep dive, is सीटीसी CTC — the Continuous Transposed Conductor. This is the product that, for any investor thinking about PWIL's terminal value, is doing more heavy lifting than any other line item on the SKU list.

Here is the simplest possible explanation of what CTC is and why it matters. Inside a large power transformer — the kind that sits at a substation and steps voltage up from 11 kV to 220 kV, or steps it down from 400 kV to 132 kV — there is a winding made of many parallel copper strands. If you simply bundled these strands together as straight parallel conductors, you would run into a nasty physics problem: the magnetic field inside the transformer would induce slightly different voltages along different strands, creating circulating currents between them, which would heat the transformer, waste energy, and shorten its life.

CTC solves this problem by transposing the strands — physically rotating them around each other along the length of the conductor in a precisely engineered pattern, so that on average each strand spends equal time at every position in the bundle. Net result: induced voltages cancel out, circulating currents disappear, and the transformer runs cool and efficient. This is, mechanically, a phenomenally difficult thing to manufacture. The transposition has to be exact. The enamel on each strand has to be flawless because if even one strand short-circuits to its neighbour, the whole point of transposition collapses. And the conductor has to be wrapped in additional paper insulation that itself has to be perfectly applied.

There are not many companies in the world that can make CTC at scale. There are even fewer in India. PWIL is one of them, and it has been building that capability over the last several years to position itself for an enormous Indian opportunity: the modernisation of the Indian power grid.

The Government of India's RDSS Revamped Distribution Sector Scheme, alongside the broader transmission build-out plans of the Ministry of Power, is one of the largest single capex programmes in Indian infrastructure today.[^4] India is, simultaneously, building out renewable energy capacity at a pace that requires vast new transmission infrastructure to evacuate power from solar parks in Rajasthan and wind farms in Tamil Nadu to load centres in the north and east. Every new transformer in that build-out — and we are talking about thousands of them — needs CTC. The Indian transformer industry, dominated by names like भेल BHEL, सीमेंस Siemens India, एबीबी ABB India, क्रॉम्प्टन ग्रीव्स Crompton Greaves, and वोल्टैम्प Voltamp, is the customer set. PWIL is one of the very few approved suppliers.

The CTC business deserves an investor's attention because it has three characteristics that the round-wire business does not: higher gross margins (because the value-add of transposition and insulation is substantial), higher barriers to entry (because the certification cycle at a transformer OEM can run two to three years), and longer-cycle demand visibility (because transformer order books extend further into the future than appliance order books). It is, in the language of strategy, a business within a business.

There is one decision in this era worth flagging because it tells you something about Mehta family capital discipline. During the 2018-2020 industrial slowdown in India, several smaller and weaker wire-makers in the Gujarat and Maharashtra belt came under serious financial stress. There was talk in the trade press of distressed-asset sales. Several investors at the time wondered openly whether PWIL would acquire a peer to consolidate the industry. They did not. They chose, instead, to continue compounding organically. The bear interpretation: missed opportunity, conservative to a fault. The bull interpretation: integrating a distressed wire factory means integrating somebody else's quality problems, somebody else's labour culture, somebody else's defect rates, into a brand that took thirty years to build. Hard pass. The Acquired-listener interpretation: this is what पूंजी आवंटन capital allocation discipline actually looks like, and it is exactly what you want from a family-run industrial business with a multi-decade horizon.

The other benchmark worth mentioning is राम रत्न वायर्स Ram Ratna Wires — PWIL's closest publicly listed Indian peer. Ram Ratna is a perfectly capable competitor, but it has historically operated at a lower scale and with a somewhat different product mix.[^5] PWIL's strategic moves in CTC and rectangular wire have, over the last decade, opened up a meaningful product-mix premium versus Ram Ratna and the rest of the field. That premium is not large enough to be a wide moat on its own, but combined with the OEM relationships and the scale, it adds up.

V. Management: The Milan Mehta Era

If you have ever sat in an Indian industrial company's earnings call, you know there is a very particular cadence to a founder-family-led conversation with the sell-side. There is none of the rehearsed PR-team polish you get from a multinational subsidiary. There is, instead, a slightly impatient, technically detailed, deeply opinionated voice that occasionally pauses mid-sentence to debate a metallurgical point with the chief financial officer. That voice, on PWIL's calls, belongs to मिलन मेहता Milan Mehta.[^6]

Milan Mehta is the Vice Chairman and Managing Director of Precision Wires India Limited, and he is, in many ways, the operational and strategic centre of gravity of the current generation of the company.[^6] He represents the continuity of the founding family's hands-on engineering philosophy — the conviction that to lead a winding-wire business, you have to know the wire. Not from a slide deck. From the factory floor.

The Mehta family, collectively, holds a promoter shareholding of north of 60% in PWIL, according to the company's NSE filings.3 That number, by itself, is one of the most important pieces of information any long-term investor needs to internalise about this business. Promoter holding of 60%-plus tells you, immediately, three things. First, the family has skin in the game — their personal wealth tracks the share price almost one-for-one. Second, hostile takeover is mathematically impossible. Third, the management horizon is generational, not quarterly.

Compare this to the typical multinational subsidiary CEO in India, whose tenure is three to four years and whose incentive package vests against trailing eighteen-month earnings targets. That CEO will, rationally, optimise for the next earnings call. Milan Mehta is optimising for his children. This is a profoundly different incentive structure, and it shows up in the decisions PWIL makes — the willingness to spend on long-cycle CTC capacity that will only fully monetise in 2028, the willingness to walk away from low-margin commodity round-wire orders that would have padded short-term revenue but compressed margin mix, the willingness to maintain a conservative balance sheet through cycles.

The incentive design in PWIL is interesting precisely because it is so unflashy. Executive compensation, particularly for the promoter directors, leans heavily on profit-linked commissions but at moderate rates, with the bulk of family wealth coming from share ownership rather than salary. There is no exotic stock-option overhang. There is no aggressive ESOP dilution. This is, again, a family that has chosen to compound at industrial-business rates rather than to extract.

Stylistically, the Mehtas have always run PWIL as what they themselves describe as "industrialists' company." Walk into the Palej facility on a random Wednesday and you are not unlikely to find Milan Mehta in a shop floor walk-through, talking to the line supervisor about defect counts on the previous shift, or in the QC lab examining a thermal-stress sample. This is not theatre for visiting analysts. It is how the business has been run since 1989. The family's edge — the thing that has allowed them to stay number one in a brutally cost-competitive industry for three and a half decades — is the depth of their technical engagement with the actual product.

There is a passage from an interview Milan Mehta gave to CNBC TV18 in August 2023, around the company's Q1 earnings, that captures the philosophy well.[^8] Asked about the company's capex plans and the EV opportunity, he framed it not as a stock-price catalyst but as an engineering challenge: which OEMs would qualify which grades of rectangular wire, on what timelines, with what specification creep — and what the company would have to do, line by line, to be ready when the certifications closed. That is a managing director who understands his product at a granular level. That is also a managing director who is, by training and by temperament, an industrialist before he is a corporate executive.

One subtle but important point on the management front: succession. PWIL is now in the second generation of Mehta family leadership, with the family having handled the generational transition reasonably smoothly — a non-trivial accomplishment in Indian family business history, where succession disputes have been known to vaporise multi-decade enterprises overnight. The fact that the family has continued to operate as a cohesive unit, with clearly delineated executive roles, is itself a quiet structural positive.

The flip side, of course, is the concentration of leadership in one family. Key-person risk is real. The depth of the management bench below the Mehta directors is something that any long-term holder should keep on their watchlist — not as a present concern, but as a future one. The professionalisation of management, particularly in functions like supply chain, hedging, technology and OEM-relationship management, will be the work of the next decade.

But for now, the Milan Mehta era of PWIL is characterised by a kind of disciplined ambition. Expand capacity, but only in the right segments. Pay down debt, but maintain the working capital to ride out copper volatility. Win the CTC certification at every major Indian transformer OEM. Position the rectangular-wire portfolio for the EV motor opportunity that is now unmistakably coming. Do all of this without leveraging the balance sheet, without overpaying for inorganic growth, and without distracting the engineering team from the daily work of pulling defects out of the production line.

It is a quiet, patient, multi-decade kind of leadership. And it is exactly the kind that the EV pivot now demands.

VI. The EV Pivot & 7 Powers Analysis

There is a particular moment, in every Acquired episode, where the framework comes out. We invoke Hamilton Helmer. We map the powers. We look for sources of durable competitive advantage that survive not just the next quarter but the next decade. This is that moment for PWIL.

But before we get to the framework, let us understand the specific opportunity that has, more than any other single development, re-rated this business in the mind of the long-term Indian industrial investor. That opportunity is the electric vehicle.

An EV motor is, at its physical core, a stator and a rotor wound with copper conductors. In a low-end EV, you can use round-wire windings — same as in a refrigerator compressor, just more of it. In a high-performance EV — the kind built by टाटा मोटर्स Tata Motors for the Nexon EV, by महिंद्रा Mahindra for the XUV400, by MG मोटर MG Motor India for the ZS EV, by बीवायडी BYD for the Atto 3 — the motor uses what is called a hairpin stator. Hairpin winding is, conceptually, what it sounds like: rectangular copper conductors bent into hairpin shapes and inserted into the stator slots, then welded together at the ends to form continuous windings.

Hairpin construction is not optional for high-performance EV motors. It is the global standard. It is what every Tesla motor uses. It is what every premium German EV motor uses. And it requires flat rectangular enamelled copper wire of extremely tight tolerance — the kind of wire that, until very recently, India simply imported.

PWIL has been positioning itself, very deliberately, to be the primary domestic supplier of this wire for the Indian EV ecosystem.[^8] The technical leap from rectangular wire for industrial motors to hairpin-grade rectangular wire for EV motors is non-trivial — it involves tighter dimensional tolerances, more exotic enamel chemistries that can survive automotive thermal cycling, and the ability to supply consistent batches across vehicle production runs that may stretch over years. But it is exactly the kind of leap that thirty-five years of enamel chemistry expertise prepares you for.

Now let us run the Hamilton Helmer 7 Powers analysis on PWIL as it stands today. We are going to find that PWIL has a meaningful claim to three of the seven powers, partial claims to two more, and is exposed on the remaining two.

Scale Economies. PWIL has clear scale economies in copper procurement, which is by far the largest input cost. Buying copper cathode in tens of thousands of tonnes per year, hedged on a back-to-back basis, gives the company a structural unit-cost advantage versus regional competitors who buy in hundreds of tonnes. Scale also gives PWIL the production-engineering bandwidth to run dozens of SKUs in parallel — a capability that smaller competitors simply cannot match. Verdict: solid scale power, particularly in the round-wire and lower-end rectangular-wire segments.

Process Power. This is where PWIL's deepest moat lives, and it is the one that almost no equity analyst writes about adequately. Enamel application is not a turnkey process. It is a chemistry-driven, line-tuned, batch-by-batch engineering discipline in which the variables that drive defect rates — line speed, oven temperature curve, enamel viscosity, ambient humidity, copper surface preparation — have to be controlled to a level of precision that takes years to learn. PWIL has been refining its enamel application process since 1989. A new entrant could buy the same equipment tomorrow and still spend five years driving its defect rate down to PWIL's level. Verdict: this is the headline power, the one that holds the moat together.

Switching Costs. Once an OEM — say, a क्रॉम्प्टन Crompton for ceiling fans, or an LG for refrigerator compressors, or a BHEL for transformers — has certified PWIL's wire for a specific application, the cost of switching to a new supplier is meaningful but not insurmountable. The new supplier has to be re-tested for the same application. Field performance has to be tracked over months or quarters. For high-end applications like CTC for transformers or hairpin wire for EVs, the switching cost is higher still — re-certification can take twelve to twenty-four months. Verdict: meaningful switching costs at the high end of the product mix, modest switching costs at the commodity end.

Cornered Resource. PWIL does not have a meaningfully cornered resource. Copper is globally available. The enamel chemicals are sourced from specialty suppliers in India and abroad. There is no proprietary input. Verdict: no power here.

Counter-Positioning. PWIL is not in counter-positioning. It is a scale leader competing on industrial fundamentals, not a disruptive challenger flipping an incumbent's business model. Verdict: no power here.

Branding. Limited B2B brand power. The PWIL name carries weight inside procurement departments at OEMs, but there is no consumer brand. Verdict: minor power.

Network Economies. None to speak of in this kind of industrial business. Verdict: no power.

Now overlay Porter's Five Forces. Buyer power is moderate-to-high — the OEMs that PWIL supplies are themselves large companies (LG, Voltas, Whirlpool, BHEL) with significant bargaining leverage. Supplier power is mitigated by PWIL's own scale in copper procurement and by the global liquidity of copper cathode markets. Threat of substitutes is the big strategic question we will return to in the bear case — specifically, aluminium substitution. Threat of new entrants is meaningfully limited by the combination of capital intensity and process know-how. Rivalry among existing competitors is high in the commodity round-wire segment, much lower in the specialty CTC and high-tolerance rectangular wire segments.

The overall takeaway is this: PWIL has built, over thirty-five years, a process-power moat that is unusually durable for a "commodity" business. The moat narrows in the cheapest end of the product line and widens dramatically in the most specialised end. The strategic imperative — the thing that the EV and CTC pivots are really about — is to keep the centre of gravity of the product mix migrating up the specialty curve, where the moat is widest.

If they succeed, PWIL spends the next decade quietly compounding. If they fail to make that mix shift, PWIL becomes a price-taker in a commodity business with very ordinary returns on capital.

The Mehtas know this. The capex is going where the mix shift is going.

VII. Playbook: Business & Investing Lessons

Step back from the specific case of PWIL and you can extract several reusable lessons from this story. These are the kinds of patterns that, once you start looking for them, you begin to see in other industrial businesses across the Indian and global landscape. Acquired listeners will recognise the shape — these are the rules of thumb that the most patient long-term investors return to again and again.

Lesson 1: The "Pick and Shovel" Play. In every major industrial transition, the most reliable returns are often not earned by the companies building the headline product. They are earned by the companies supplying the boring, essential, hard-to-substitute components. During the California gold rush, the people who got rich were the ones selling picks, shovels and Levi's jeans to the miners, not the miners themselves. In the Indian electrification story, the question is not just who will build the best EV motor or the best power transformer. The question is who will supply the wire inside every one of them. PWIL is the pick-and-shovel play on Indian electrification, in the same way that ASML is the pick-and-shovel play on global semiconductor manufacturing or Linde लिंडे is the pick-and-shovel play on industrial gases. The lesson generalises: in any industry-wide transition, look upstream for the indispensable component supplier.

Lesson 2: Inventory as a Weapon, Not a Liability. For a wire manufacturer, copper is both the largest input and the largest source of P&L volatility. The naive approach is to treat inventory as a working capital line item to be minimised. The sophisticated approach — PWIL's approach — is to treat copper inventory and hedging as a tactical weapon. Buy copper when prices are favourable. Hedge forward against fixed customer orders to lock in the spread between purchase cost and selling price. Manage the inventory turn so that you are never caught long when prices collapse or short when prices spike. The companies that get this right earn margin out of pure operational discipline. The companies that get it wrong — and there are many, every cycle — get destroyed by their own raw material. The lesson here is broader than copper. In any business where the input is a globally traded commodity, treat input procurement as a strategic competency, not an administrative function.

Lesson 3: The "Boring" Moat. There is a romantic notion in business writing that moats come from disruptive innovation — the network effect, the platform monopoly, the proprietary algorithm. The PWIL moat is the opposite of all of that. It is the moat that comes from doing one boring thing slightly better than everyone else, year after year, for decades. It is the moat of pulling 0.1% more defects out of the production line every year for thirty years. It is the moat of being the supplier that the OEM never has to think about. It is the moat of being so reliably second-nature in the customer's procurement function that the procurement manager would have to actively justify a switch. This kind of moat is hard to build and almost impossible to disrupt. The lesson generalises: in industrial businesses, durable competitive advantage often comes not from breakthrough innovation but from cumulative process refinement that competitors cannot replicate in a hurry.

Lesson 4: आत्मनिर्भर भारत Self-Reliant India as Industrial Tailwind. The Indian government's broader policy push toward import substitution and domestic manufacturing — which falls under the umbrella of the आत्मनिर्भर भारत Self-Reliant India campaign launched in 2020 — has created a real, measurable tailwind for domestic industrial suppliers like PWIL.[^4] When the government incentivises domestic transformer manufacturing, the transformer makers in turn prefer to source their CTC domestically. When the Production-Linked Incentive schemes push domestic EV motor manufacturing, the motor makers want to source their hairpin wire domestically. PWIL benefits from this without being explicitly named in any policy document. The lesson is that government policy can be a long, slow, structural tailwind for a well-positioned upstream supplier — but only if that supplier has already done the technical work to be ready to take advantage when the policy lands.

Lesson 5: Conservative Capital Allocation Survives Cycles. This lesson is so obvious that it almost feels insulting to write it, and yet it is the lesson that the Indian SME industrial sector forgets every single cycle. Leverage feels free when commodity prices are rising. It feels lethal when they collapse. PWIL has been deliberately conservative on debt for thirty-five years, has chosen organic growth over inorganic, and has weathered every cycle without distress. Boring on the way up. Indestructible on the way down. The lesson: in cyclical industrial businesses, the strongest competitive moat may simply be the willingness to be the last balance sheet standing when the music stops.

Lesson 6: Be the Supplier the OEM Cannot Lose. Once you understand that the real switching cost in B2B industrial supply is not financial but operational and reputational, you understand why PWIL's certification relationships with major OEMs are worth so much more than they show up on any balance sheet. A motor manufacturer cannot afford a winding-wire failure in the field. The reputational cost of a recalled compressor or a burnt-out transformer winding is a thousand times the unit cost of the wire itself. So the OEM will always, always, choose the supplier with the lowest field-failure rate over the supplier with the lowest unit price. PWIL has spent three decades getting itself onto that list, at that position, at every meaningful OEM in India. That is the asset that does not appear on the balance sheet, and it is the asset that is hardest for a competitor to replicate.

These six lessons travel. They apply to PWIL specifically, but they also apply to any number of quiet industrial compounders across India, Southeast Asia, and the broader emerging-market industrial complex. They are the patterns that long-term fundamental investors look for when they are trying to separate genuine competitive advantage from temporary cyclical tailwinds.

The question is, of course, whether PWIL itself will continue to embody these lessons over the next decade. That depends, in significant part, on which of two competing futures actually arrives.

VIII. Bear vs. Bull Case & The Future

Every Acquired episode eventually arrives at the moment of synthesis: the bull case, the bear case, and the honest weighing of the two. For PWIL, both cases are easy to articulate and, importantly, neither is obviously wrong. Reasonable investors can read the same set of facts and arrive at very different views about where this company sits in 2031.

The Bear Case.

Start with copper price volatility. PWIL operates on relatively thin gross margins because copper is such a large share of input cost. Even with disciplined hedging, a sharp directional move in LME copper can compress quarterly margins or, conversely, deliver windfall gains that are operationally meaningless. For investors who want operating leverage stories with smooth quarterly progression, PWIL is not that. There is always quarter-to-quarter noise in the reported numbers driven by copper.

Then there is the aluminium substitution risk. Aluminium winding wire is cheaper than copper winding wire by a meaningful margin. Historically, copper has dominated because copper has higher conductivity and longer service life. But as cost-pressure intensifies in the low-end appliance segment — fans, low-end pumps, low-end motors — aluminium has been making inroads. If a significant fraction of the appliance motor market migrates to aluminium, the volume base of PWIL's commodity wire business contracts. The mitigating fact is that the high-end of PWIL's mix — CTC for transformers, hairpin wire for EV motors — is overwhelmingly copper-only by physics, so the substitution risk is mostly concentrated in the lower-margin segments. But the volume hit, if it comes, would still hurt.

The third bear lever is competitive entry. Global specialty wire-makers — Japanese, Korean, European — have technologies that, in some sub-segments, exceed PWIL's. If those players choose to enter India aggressively, either through joint ventures with existing Indian players or through greenfield investments under the Production-Linked Incentive umbrella, PWIL would face well-funded competition at exactly the high-margin end of the market it is migrating toward. The defensive answer is that India's process-power gap closes slowly, and global players moving into India still have to certify wire-by-wire at Indian OEMs — but it is not a defence that holds forever.

The fourth bear consideration is execution risk on the EV ramp. Hairpin winding for EV motors is a non-trivial technical step up from industrial rectangular wire, and the certification cycle at automotive OEMs is famously brutal. If PWIL's certification timelines slip, the EV opportunity narrative loses some of its lift. Investors who have priced in the EV ramp may find themselves disappointed by a six-quarter delay.

Finally, the perennial bear concern in any family-run business: governance and succession. The Mehta family has run PWIL exceptionally well. But concentration of executive control in one family inherently carries key-person risk, succession risk, and capital-allocation-discipline risk over multi-decade horizons. None of these is an immediate concern. All of them are tail risks worth tracking.

The Bull Case.

The bull case for PWIL is, in one phrase, the भारतीय विद्युतीकरण Indian electrification thesis. Over the next decade, India will electrify on a scale comparable only to what China did between 2003 and 2013. EV penetration, today still modest, will compound. White-goods penetration in tier-two and tier-three cities — air conditioners particularly — will continue its inexorable rise as incomes climb and the climate gets hotter. The transmission and distribution grid will be rebuilt and expanded to handle a renewable-heavy generation mix. Every single one of these tailwinds drives winding wire demand. And PWIL is positioned to capture an outsized share.

If the bull case plays out, PWIL's revenue mix shifts increasingly toward CTC and hairpin EV wire over the next five years, blended gross margins expand modestly as a result, and absolute volume grows alongside the underlying market. The capacity that the company has been building, deliberately and conservatively, becomes the choke point that defines how much wire the Indian motor and transformer industries can produce. In that scenario, the moat widens.

The bull case is reinforced by आत्मनिर्भर भारत Self-Reliant India and PLI-driven import substitution. If the Indian government continues to incentivise domestic manufacturing of motors, transformers and vehicles, the domestic share of the winding-wire market grows at the expense of imports. PWIL, as the scaled domestic incumbent, benefits more than anyone.

Synthesis and the "Category King" Question.

Putting the two cases against each other, the picture is roughly this. PWIL has a genuine moat in the high end of its product mix, a meaningful but narrower moat in the middle, and very little defensive position at the bottom end. The strategic imperative is product-mix migration upward. The macroeconomic backdrop is strongly favourable. The execution risks are real but manageable. The governance setup is strong but not infinite-horizon-proof.

Is PWIL a "category king" in the Acquired sense? The framework defines a category king as the dominant player in a category that itself is large and growing. PWIL is, by a comfortable margin, the largest enamelled winding wire manufacturer in South Asia. The category — winding wire for an electrifying India — is large, growing, and structurally favoured by both demographics and policy. Within India, yes, PWIL has a reasonable claim to category king status. Globally, the picture is more nuanced; PWIL is a regional champion, not yet a global one.

KPIs to Track.

For investors looking to keep an honest scorecard on PWIL going forward, three KPIs matter more than any others, and they capture the strategic story in three numbers.

First: product mix percentage from specialty wires (CTC plus rectangular plus hairpin) as a share of total revenue. This is the single best measure of whether the strategic migration up the value curve is actually happening or whether the company is still anchored in commodity round wire. The direction of this number, year over year, tells you whether the moat is widening or narrowing.

Second: EBITDA per tonne or contribution margin per tonne of wire sold. Revenue per tonne can be misleading because it moves with copper prices. Contribution margin per tonne strips out the copper pass-through and reveals what PWIL actually earns from its conversion work. Rising contribution margin per tonne over multiple years is the cleanest signal that the mix is improving and pricing discipline is holding.

Third: OEM certification milestones in CTC and hairpin wire. This is less a quantitative metric and more a qualitative scorecard. Investors should watch for announcements or disclosures about new OEM approvals — particularly with major Indian transformer makers and EV motor manufacturers — as the leading indicator of future revenue flow.

Track those three things and you are tracking the actual strategic position of the business, not the noise of copper prices and quarterly cyclicality.

IX. Outro & Epilogue

So what is the legacy of the Mehtas at PWIL? It is, in many ways, the story of Indian industrial development itself compressed into one company. A family that started in 1989, when India was still operating under the लाइसेंस राज License Raj, that bet on a deeply unsexy product, that focused obsessively on a single layer of the value chain, that scaled methodically without ever falling for leverage, that survived multiple commodity cycles and at least two macroeconomic crises, and that emerged on the other side as the largest South Asian player in a category that the modern world cannot live without.

It is also a reminder of a broader truth about how economies actually work. The companies that get the headlines — the consumer brands, the technology platforms, the marquee conglomerates — are riding on the backs of dozens of "invisible" suppliers that nobody outside their specific industry has ever heard of. The transformer that powers your neighbourhood substation. The compressor in your refrigerator. The motor in your washing machine. The traction unit in your EV. Each one of them depends on a wire, and that wire depends on a chemistry, and that chemistry depends on a manufacturing process that someone, somewhere, has been refining for thirty-five years.

The Mehta family has been that someone. PWIL has been that somewhere. The wire has been the connective tissue between an industrialising India and the electrified India of the next decade.

For long-term fundamental investors, the question is not whether PWIL's story is interesting. It is. The question is whether the next chapter — the CTC ramp, the EV hairpin opportunity, the continued grid modernisation, the further migration up the value curve — can be executed with the same patience and the same discipline that defined the first thirty-five years. That, ultimately, is the bet.

The wire keeps winding. The country keeps electrifying. The hum you hear at 2 a.m. is the sound of a thesis playing out.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube