Piramal Pharma: The Phoenix of Indian Pharmaceuticals

I. Introduction & Episode Roadmap

The boardroom at Piramal Tower in Mumbai's Lower Parel was electric with tension on that May morning in 2010. Ajay Piramal, the soft-spoken patriarch who had built one of India's most formidable pharmaceutical empires, was about to sign away his life's work. The documents before him represented Abbott Laboratories' $3.72 billion acquisition of Piramal Healthcare's branded generics business—the largest pharmaceutical deal in Indian history. As his pen hovered over the signature line, one board member reportedly whispered, "Are we really doing this?" Piramal smiled, signed, and quietly said, "Sometimes you have to destroy something beautiful to create something extraordinary."

That moment encapsulated the audacious bet that would define the next chapter of Indian pharmaceuticals. Here was a businessman voluntarily dismantling a $7 billion empire he'd spent three decades building, betting he could construct something even greater from the ashes. It was either visionary genius or spectacular hubris. Today, with Piramal Pharma trading as an independent entity on the NSE with a market capitalization of ₹25,177 crore and revenues touching ₹9,134 crore, we can finally answer that question.

The story of Piramal Pharma isn't just another corporate chronicle—it's a masterclass in strategic patience, capital allocation, and the art of corporate rebirth. While most business leaders spend their careers building empires, Ajay Piramal has done it twice in the same industry, each time with radically different playbooks. The first empire was built on branded generics and domestic market dominance. The second, still under construction, rests on three pillars that barely existed in the first iteration: contract development and manufacturing (CDMO), complex hospital generics, and consumer healthcare. Today, Piramal Pharma stands among the Top 3 CDMO players in India and ranks 13th globally, though it notably doesn't appear in the top 10 global CDMOs dominated by giants like Lonza, Thermo Fisher, and Catalent. The company has transformed into a sophisticated operation spanning 17 global development and manufacturing facilities with a distribution network in over 100 countries. More impressively, for the first time in the company's history in FY24, revenue earned on innovation programs surpassed that of generic projects, with innovation revenue growing from 35% of total in FY19 to more than 50%, representing a CAGR of 20%.

This episode unpacks three intertwined narratives. First, the strategic genius—or madness—of voluntarily dismantling a successful pharmaceutical empire at its peak. Second, the operational marathon of rebuilding from scratch in completely different segments of the pharmaceutical value chain. Third, the financial engineering of demerging and listing a new entity in public markets, testing whether the sum of parts can exceed the whole.

What makes this story particularly compelling for investors and business students alike is its contrarian nature. In an era where pharmaceutical companies globally are pursuing consolidation and scale, Piramal chose fragmentation and focus. While peers were building branded generics empires in emerging markets, Piramal pivoted to become a behind-the-scenes partner to global innovators. When Indian pharma was celebrating domestic market dominance, Piramal was quietly building capabilities in complex manufacturing that few understood or valued at the time.

The questions we'll explore cut to the heart of corporate strategy: How do you value optionality in business? What's the cost of being early versus being right? Can you build institutional knowledge twice in the same industry? And perhaps most intriguingly—in a family-controlled business, how do you balance personal legacy with shareholder value?

As we journey through this saga, we'll discover that the Piramal story isn't just about pharmaceuticals. It's about the art of creative destruction, the patience of compound growth, and the audacity to bet everything on a vision that wouldn't pay off for more than a decade. Whether this bet ultimately succeeds or fails, the playbook written along the way offers profound lessons for anyone thinking about business transformation, capital allocation, and the true meaning of long-term value creation.

II. The Piramal Legacy & Early Empire Building

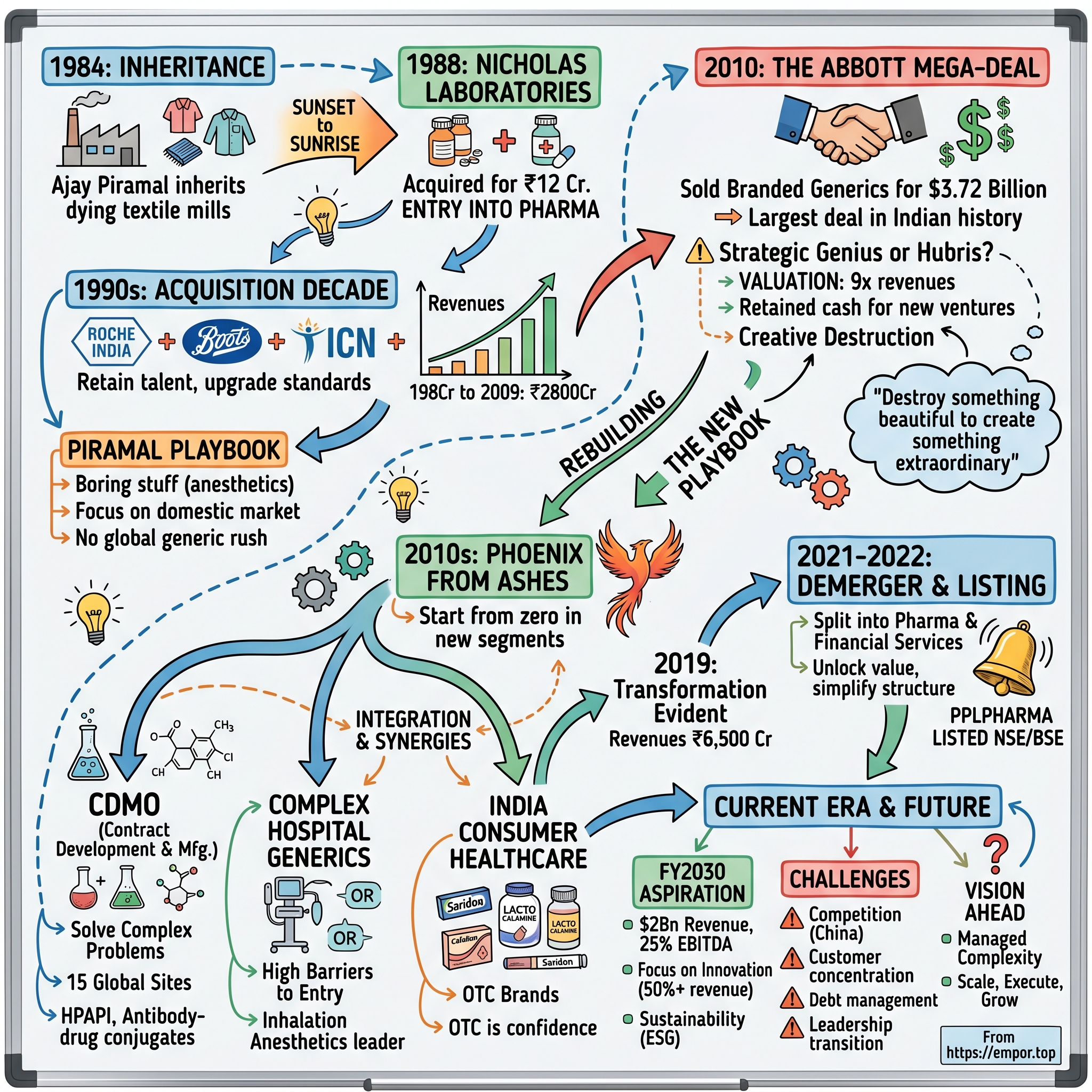

The Mumbai textile mills of 1984 were dying. Cotton dust hung in the air of abandoned factories, machinery rusted in monsoon humidity, and workers' protests echoed through empty compounds. It was here, amid this industrial graveyard, that 29-year-old Ajay Piramal inherited a textile business nobody wanted. His father and uncle had just passed away in quick succession, leaving behind Piramal Enterprises—a traditional Marwari family business built on textiles, a sector everyone knew was finished. The smart money was getting out. Ajay Piramal had other plans.

"I looked at textiles and saw sunset," Piramal would later tell Forbes India. "But I also saw cash flow that could fund a sunrise." This philosophy—using declining businesses to fund growth sectors—would become his signature move, repeated multiple times over four decades. But first, he needed to find his sunrise industry.

The answer came in 1988, in the form of Nicholas Laboratories. Founded by British colonialists in 1933, Nicholas had become a sleepy pharmaceutical company by the 1980s, manufacturing vitamin formulations and basic drugs for the Indian market. The company was available for ₹12 crore—a fortune for a textile businessman, but Piramal saw something others missed. India's pharmaceutical market was about to explode. The population was growing, healthcare spending was rising, and the government was loosening regulations on drug manufacturing. More importantly, Nicholas came with something money couldn't easily buy: manufacturing licenses, distribution relationships, and a trusted brand name among Indian doctors.

The acquisition was financed entirely through debt, a move that raised eyebrows in Mumbai's conservative business circles. The Marwari community, known for its cash-based, risk-averse approach to business, watched in horror as one of their own leveraged everything on an unfamiliar industry. "People thought I'd gone mad," Piramal recalled in a 2019 interview. "A textile man buying pharma? With borrowed money? It was unheard of."

But Piramal wasn't just buying a company; he was buying a platform. Within months of the acquisition, he began implementing what would become the Piramal playbook: retain the best talent, upgrade manufacturing standards, and most crucially, use the acquired company as a base for further acquisitions. Nicholas Laboratories' managing director, S.R. Wagle, was not only retained but promoted, becoming Piramal's trusted lieutenant for the next two decades. This approach—keeping and empowering existing management—was revolutionary in an era of hostile takeovers and management purges.

The 1990s became Piramal's decade of voracious acquisition. In 1991, he acquired Roche's India operations, gaining access to sophisticated manufacturing technology and a portfolio of high-margin drugs. The price tag of ₹28 crore seemed steep, but the deal included Roche's manufacturing facility in Baddi, Himachal Pradesh—a plant that would later become one of India's most efficient pharmaceutical factories. The Roche acquisition also brought something intangible but invaluable: Swiss-German manufacturing discipline and quality standards that would permeate throughout Piramal's operations.

Each acquisition followed a pattern. Piramal would identify undervalued assets—usually foreign multinationals struggling with India's bureaucracy or family-owned businesses lacking succession planning. He'd negotiate aggressively on price but generously on management retention. Post-acquisition, he'd invest heavily in upgrading facilities to global standards while maintaining the acquired brand's market relationships. It was private equity tactics before private equity existed in India.

By 1995, Piramal Healthcare had assembled a portfolio that included antibiotics from Nicholas, vitamins from Roche, and through subsequent deals, everything from antimalarials to painkillers. But the real masterstroke was the company's focus on what Piramal called "the boring stuff"—high-volume, low-glamour medicines that every hospital needed but few companies wanted to perfect. While competitors chased blockbuster drugs, Piramal dominated categories like surgical anesthetics and medical gauze.

The culture Piramal built was equally distinctive. In an industry notorious for aggressive sales tactics and doctor kickbacks, Piramal Healthcare took a different approach. The company's motto—"Doing Well and Doing Good"—wasn't just corporate speak. Sales representatives were trained as medical educators, providing genuine value to doctors through continuing education programs. The company pioneered patient assistance programs, providing free medicines to those who couldn't afford them. This wasn't charity; it was brand-building. Doctors who saw Piramal helping their poorest patients became loyal prescribers for life.

The financials reflected this strategy's success. From revenues of ₹18 crore in 1988, Piramal Healthcare grew to ₹400 crore by 2000, and ₹2,800 crore by 2009. EBITDA margins consistently exceeded 20%, remarkable for a domestic-focused pharmaceutical company. The company's return on equity averaged 25% through the 2000s, making it one of the most profitable pharmaceutical companies in Asia.

But perhaps the most remarkable aspect of this period was what Piramal didn't do. He resisted the temptation to go global prematurely, unlike peers like Ranbaxy and Dr. Reddy's who were pouring resources into challenging U.S. patents. He avoided the biosimilars boom, despite banker pressure to enter this "hot" sector. He stayed away from research and development of new chemical entities, even as the government offered massive tax breaks for R&D spending. "I'm a businessman, not a scientist," he'd say. "I know my limitations."

This discipline extended to the balance sheet. Despite aggressive acquisitions, Piramal Healthcare maintained a net debt-to-equity ratio below 0.5x throughout the 2000s. Each acquisition was quickly de-leveraged through operational improvements and cash generation. The company never raised equity capital after its IPO, funding all growth through internal accruals and modest debt. This conservative financial management would prove crucial when the biggest opportunity of Piramal's career appeared in 2010.

By 2009, Piramal Healthcare had become India's fourth-largest pharmaceutical company by domestic sales, with a particular stranglehold on certain therapeutic categories. In respiratory medicines, the company commanded a 25% market share. In vitamins and minerals, it was 30%. The company operated five FDA-approved manufacturing facilities, employed 8,000 people, and had products registered in 85 countries. It was, by any measure, a pharmaceutical success story.

Yet Ajay Piramal was restless. At industry conferences, he'd speak about "inflection points" and "discontinuous growth." Close associates noticed he was spending more time with investment bankers than with pharmaceutical executives. He'd built an empire through patient accumulation, but something fundamental was shifting in his thinking. The next chapter would shock everyone—including his own board of directors.

III. The Abbott Mega-Deal: Selling at the Peak (2010)

The Oberoi Hotel's presidential suite in Mumbai had witnessed many deals, but nothing quite like what was unfolding on that humid evening in March 2010. Miles White, CEO of Abbott Laboratories, had flown in from Chicago with a small army of bankers and lawyers. Across the table sat Ajay Piramal, accompanied only by his CFO and a single advisor. The contrast was deliberate—Piramal wanted to project confidence, not desperation. The Americans had come to him, after all.

"Miles, I'm not interested in selling," Piramal opened, even though everyone in the room knew this was precisely why they were there. "But I'm always interested in listening." White smiled. He'd done his homework on Indian negotiating tactics. The dance had begun.

The backstory of how Abbott and Piramal reached this moment reveals much about global pharmaceutical strategy circa 2010. Abbott, a $35 billion American giant, was facing a crisis of growth. Its blockbuster drug Humira was printing money, but the company's pipeline was thin, and emerging markets—particularly India—were becoming crucial for future growth. Abbott's existing Indian operation was subscale, ranking 15th in a market dominated by local players who understood the complex dynamics of Indian healthcare: the price-sensitive consumers, the powerful chemist lobbies, the relationship-driven doctor networks.

White's strategic team had evaluated every major Indian pharmaceutical company. Sun Pharma was too expensive and too proud to sell. Cipla's Yusuf Hamied would rather die than sell to a multinational. Dr. Reddy's was focused on the U.S. market. That left Piramal Healthcare—large enough to matter, Indian enough to have credibility, but led by someone pragmatic enough to do a deal if the price was right.

For Piramal, the timing was exquisite. He'd been tracking global pharmaceutical trends and saw storm clouds gathering. The domestic Indian market, while growing at 15% annually, was becoming hypercompetitive. Price controls were expanding. The government was threatening to impose stricter regulations on marketing practices. Most worryingly, Indian companies were destroying value by competing on price in international markets. "We were in a race to the bottom," Piramal later told Economic Times. "I could see margins compressing over the next decade."

There was also a personal element. At 55, Piramal had been running the pharmaceutical business for 22 years. His children—Nandini and Anand—were still young, studying abroad. He wasn't ready to retire, but he was ready for a new challenge. "I'd built the business once. The thrill was gone. I wanted to build something again," he'd confide to close friends.

The negotiation itself became legendary in Indian corporate circles. Abbott's opening offer was $2.8 billion—already the largest pharmaceutical deal in Indian history. Piramal's response was to walk away from the table. "Thank you for your interest, but we're not sellers at that price," he said, gathering his papers. White's team was stunned. They'd offered a 40% premium to comparable transactions.

What followed was a six-week chess match conducted through intermediaries. Piramal had hired Peter Goodson from Goldman Sachs, one of the few bankers who understood both American acquisition logic and Indian seller psychology. Goodson's advice was counterintuitive: "Don't negotiate on price initially. Negotiate on structure."

This proved brilliant. Instead of haggling over billions, Piramal focused on deal structure that would maximize value for his shareholders. He proposed a unique earnout mechanism: $2.12 billion upfront, plus four annual payments of $400 million each, contingent on the business meeting certain milestones. This structure served multiple purposes. It pushed the headline value to $3.72 billion—a psychologically important number that represented 9x revenues. It deferred taxes for Piramal shareholders. And it gave Abbott comfort that they weren't overpaying for a deteriorating asset.

The valuation multiple—9x trailing revenues and approximately 45x earnings—raised eyebrows globally. Financial Times called it "stratospheric." Forbes termed it "the deal that defied gravity." To understand why Abbott paid such a premium, you need to understand what they were really buying.

First, they were acquiring market position. Piramal's branded generics portfolio would immediately make Abbott the largest pharmaceutical company in India, leaping from 15th to 1st position overnight. In a market growing at 15% annually and expected to reach $50 billion by 2020, leadership position was worth billions in net present value.

Second, they were buying relationships. Piramal's 5,000-person sales force had relationships with 200,000 doctors across India. Building such a network would take Abbott at least a decade and potentially billions in investment. These relationships were particularly strong in tier-2 and tier-3 cities, where future growth would come from.

Third, they were acquiring capabilities. Piramal's manufacturing facilities were FDA-approved and could produce medicines at a fraction of Western costs. The company's regulatory team understood India's byzantine approval processes. Its distribution network reached 250,000 pharmacies. This infrastructure was impossible to replicate quickly.

But perhaps most importantly, Abbott was buying time. Every year of delay in entering the Indian market meant ceding ground to competitors like Pfizer and Novartis, who were also scrambling for position. In pharmaceuticals, where patent cliffs and market windows are everything, time has extraordinary value.

The announcement on May 21, 2010, sent shockwaves through corporate India. The Times of India led with "Piramal Pulls Off Deal of the Century." The stock market's reaction was euphoric—Piramal Healthcare's stock jumped 20% in minutes, triggering circuit breakers. The rupee strengthened against the dollar as foreign investors poured money into India, seeing the deal as validation of Indian asset values.

Yet not everyone was celebrating. Many Piramal employees felt betrayed. "We'd built this company with our sweat and blood, and now it was being sold to Americans?" one senior manager told BusinessWorld. Others worried about job security, despite Abbott's promises to retain all employees. The pharmaceutical industry association expressed concern about increasing foreign control of Indian healthcare.

Piramal addressed these concerns in a town hall that became part of corporate folklore. "We're not abandoning ship," he told 3,000 employees gathered in Mumbai. "We're building a bigger ship. Those who want to stay with Abbott will have global careers. Those who want to join me in the next adventure will build something even greater." He announced that key executives would receive retention bonuses totaling ₹100 crore, funded from his personal proceeds.

The integration process revealed both parties' sophistication. Abbott retained the entire Piramal sales force, maintaining continuity in doctor relationships. They kept the Piramal brand name for certain products, understanding its local equity. Manufacturing facilities continued operating without disruption. The earnout milestones—tied to revenue growth and market share—were met every year, validating both the business quality and Abbott's execution.

For Piramal, the post-deal period was liberating. The first tranche of $2.12 billion arrived in September 2010. After taxes and transaction costs, Piramal Enterprises was left with approximately ₹8,000 crore in cash—an enormous war chest by Indian standards. The financial media speculated wildly about his next move. Would he retire? Buy another pharmaceutical company? Enter a completely different industry?

In a masterful move of capital allocation, Piramal announced a ₹2,500 crore buyback—returning 30% of the proceeds to shareholders while keeping enough firepower for future acquisitions. The buyback, executed at ₹600 per share, was oversubscribed 3x, with foreign institutional investors clamoring for more. It established Piramal's reputation as a shareholder-friendly operator, crucial for his future capital market activities.

The Abbott deal's long-term implications extended far beyond the immediate participants. It established a new valuation paradigm for Indian pharmaceutical assets, triggering a wave of foreign acquisitions. Daiichi Sankyo acquired Ranbaxy. Mylan bought Matrix Laboratories. Global pharmaceutical companies realized they needed Indian operations, and the only quick way to get them was through acquisition.

For the Indian pharmaceutical industry, the deal marked a turning point. It proved that Indian companies could command global valuations if they built differentiated assets. It also demonstrated that selling to foreigners wasn't necessarily a betrayal—it could be a strategic victory if timed and structured correctly.

Years later, when asked about the secret to getting such a spectacular valuation, Piramal offered a simple insight: "I sold them the future, not the present. Abbott wasn't buying our 2010 revenues. They were buying our 2020 market position. I just made sure we priced in that decade of growth upfront."

The Abbott deal would go down in business school case studies as a textbook example of value maximization. But for Ajay Piramal, it was merely the end of Act One. The curtain was already rising on Act Two, and this time, he would build something that couldn't be bought—only earned through decades of patient execution.

IV. The Rebuilding Years: Phoenix from the Ashes (2010–2020)

The Piramal Enterprises boardroom in October 2010 felt like a war room where the general had dismissed his entire army. Ajay Piramal stood before a whiteboard, marker in hand, facing his core team—the survivors who hadn't joined Abbott. The board was empty except for three words: "CDMO," "Critical Care," and "Consumer." Below each, a single number: zero.

"Ladies and gentlemen," Piramal began, his voice carrying the weight of the moment, "we have ₹8,000 crore in the bank and absolutely no pharmaceutical business. Most people would call this retirement. I call it the most exciting day of my professional life."

His CFO, Vivek Valsaraj, who'd been with him since the Nicholas days, raised the obvious question: "Ajay, we just sold the domestic formulations business for a record valuation. Why not buy a similar business internationally? Why these three completely different segments?"

Piramal's answer would define the next decade: "Because everyone else is doing formulations. The future isn't about making pills—it's about solving complex problems that others can't or won't solve."

This philosophy—choosing difficulty over ease, complexity over simplicity—would guide every decision in the rebuilding years. But first, Piramal needed to understand what exactly he was rebuilding toward. He embarked on what insiders called his "learning tour"—six months of traveling to pharmaceutical companies, CDMOs, and chemical plants across the world, often showing up unannounced, notebook in hand, asking questions like a business school student rather than a billionaire.

In Basel, at Lonza's headquarters, he spent three days understanding the CDMO business model. In New Jersey, he toured Catalent's facilities, marveling at their biologics capabilities. In Ireland, he studied the tax advantages that made it a pharmaceutical manufacturing hub. Each visit added pieces to a mental puzzle he was assembling.

The CDMO opportunity was particularly intriguing. The global CDMO market was valued at $119.80 billion in 2023 and anticipated to reach $249.22 billion by 2033, growing at a CAGR of 7.6%—though in 2010, the market was smaller but growing rapidly. Pharmaceutical companies were increasingly outsourcing manufacturing to focus on drug discovery and marketing. But most Indian CDMOs were stuck in low-value generic manufacturing. Piramal saw an opportunity to build something different: a CDMO that could handle complex molecules, controlled substances, and highly potent APIs that required specialized handling.

The first major move came in December 2010 with the acquisition of Coldstream Laboratories in Lexington, Kentucky, for $30 million. It was a small deal by Piramal standards—the Abbott proceeds could fund 50 such acquisitions—but strategically crucial. Coldstream brought FDA-approved facilities for injectable manufacturing and, more importantly, American customers who would never have considered an Indian manufacturer.

"The seller thought I was crazy paying $30 million for a business doing $15 million in revenue," Piramal recalled. "But I wasn't buying revenues. I was buying a passport into the U.S. CDMO market."

The integration of Coldstream revealed the challenges ahead. American workers were skeptical of Indian ownership. Customers worried about quality standards dropping. Competitors spread rumors about imminent outsourcing to India. Piramal's response was counterintuitive: he increased U.S. headcount, raised wages above industry standards, and committed $10 million for facility upgrades. When the plant manager asked why, Piramal replied, "Trust is earned in drops and lost in buckets. We're filling the bucket."

While building the CDMO business, Piramal was simultaneously executing on the second pillar: complex hospital generics. This wasn't about making simple generic tablets. It was about manufacturing products with such high barriers to entry—technical, regulatory, or capital—that only a handful of companies worldwide could compete.

The crown jewel acquisition came in 2012: the inhalation anesthetics business from Rhodia, a French chemical company, for €135 million. The business included manufacturing facilities in the UK and U.S., along with a portfolio of sevoflurane and isoflurane products used in surgical procedures worldwide. These weren't just drugs; they were precision-manufactured gases requiring specialized equipment, handling protocols, and deep regulatory expertise.

The Rhodia deal almost fell apart at the eleventh hour. During due diligence, Piramal's team discovered environmental liabilities at the UK facility that Rhodia hadn't disclosed. The bankers advised walking away. Instead, Piramal flew to Paris, met Rhodia's CEO, and negotiated a unique solution: Rhodia would remediate the environmental issues while Piramal would pay an additional €10 million to retain key technical staff for three years. "I needed their knowledge more than I needed a discount," he explained.

The third pillar—consumer healthcare—seemed the most straightforward but proved the most culturally challenging. Piramal acquired several over-the-counter brands, including the iconic Saridon painkiller brand from Roche. But OTC marketing required a completely different mindset from prescription drugs. Instead of targeting doctors, you needed to influence consumers directly. Instead of medical education, you needed advertising. Instead of hospital relationships, you needed retail distribution.

Piramal made an unconventional hire: Kedar Sohoni, a former Hindustan Unilever executive who'd never worked in pharmaceuticals but understood Indian consumers intimately. Sohoni's first presentation to the board was revolutionary: "Stop thinking like a pharmaceutical company. Saridon isn't a drug—it's a solution to Monday morning headaches. Lacto Calamine isn't skincare—it's confidence for teenage girls."

The transformation wasn't smooth. Between 2010 and 2015, Piramal Pharma (still part of Piramal Enterprises) burned through nearly ₹3,000 crore in acquisitions and organic investments. Revenues were growing, but profits were elusive. The CDMO business faced customer concentration issues. The hospital generics business struggled with price pressure. The consumer business was losing market share to aggressive competitors.

Critics were brutal. "Piramal is trying to be everything to everyone," wrote one analyst in 2014. "He should have stuck to financial services [another business Piramal had entered] instead of attempting this pharmaceutical renaissance." The stock price reflected this skepticism, with Piramal Enterprises trading at a conglomerate discount despite the valuable individual businesses.

Internally, the challenges were even greater. The company was trying to integrate 17 different acquisitions across 12 countries, each with its own culture, systems, and processes. The Coldstream team couldn't understand why they needed to report to Mumbai. The UK anesthetics team resented oversight from Americans. The Indian consumer team felt neglected compared to the global businesses.

Piramal's solution was radical for an Indian conglomerate: extreme decentralization. Each business unit got its own CEO with full P&L responsibility. Country heads could make acquisition decisions up to $50 million without board approval. R&D budgets were controlled locally, not centrally. The only non-negotiable requirements were safety standards, quality metrics, and financial reporting.

This approach created its own problems. By 2016, Piramal Pharma had effectively become three separate companies sharing a corporate parent. The CDMO business was winning large contracts but struggling with capacity utilization. The hospital generics business had great products but weak distribution. The consumer business had strong brands but limited innovation. There were no synergies—the theoretical benefit of the three-pillar strategy.

The breakthrough came from an unexpected source: customer feedback. In 2017, Pfizer approached Piramal with an unusual request. They needed a partner who could develop an API, formulate it into an injectable, and handle fill-finish manufacturing—essentially, end-to-end services that spanned all three of Piramal's divisions. It was a $200 million contract, but more importantly, it validated Piramal's integrated strategy.

This led to a reorganization that finally unlocked synergies. The CDMO business started leveraging the hospital generics team's expertise in sterile manufacturing. The hospital generics business used the CDMO's customer relationships to enter new markets. The consumer business accessed the CDMO's formulation capabilities for product innovation. Suddenly, the three pillars were supporting each other rather than standing alone.

By 2019, the transformation was evident in the numbers. Revenues had reached ₹6,500 crore, up from essentially zero in 2010. The CDMO business was generating 45% of revenues with 18% EBITDA margins. Hospital generics contributed 35% of revenues with 25% margins. Consumer healthcare, while smallest at 20% of revenues, had the highest margins at 30%. The company was profitable, growing, and most importantly, differentiated.

But Ajay Piramal wasn't satisfied. At a company retreat in 2019, he presented a new challenge: "We've proven we can rebuild. Now we need to prove we can lead. I don't want to be the 13th largest CDMO globally. I want to be in the top 5. I don't want to be a player in hospital generics. I want to dominate certain categories. I don't want consumer brands. I want consumer franchises."

This ambition would require something the company had avoided for a decade: accessing public markets as a pure-play pharmaceutical company. The conglomerate structure that had enabled the rebuilding was now constraining growth. Investors couldn't properly value a company that was part pharma, part financial services. Talent wanted stock options in a focused company, not a conglomerate. Customers wanted to partner with specialists, not generalists.

The stage was set for the next transformation: the demerger and independent listing of Piramal Pharma. It would be Ajay Piramal's final act as architect of the pharmaceutical business, and perhaps his most important. The student who'd learned from global best practices was ready to graduate—and compete with his former teachers.

V. The Demerger & IPO Story (2021–2022)

The virtual board meeting on March 27, 2021, was unlike any in Piramal Enterprises' history. Board members joined from Mumbai, London, New York, and Singapore—pandemic geography forcing what would normally be an in-person discussion of monumental importance. Ajay Piramal's face filled the screen, his expression unusually tense. "Gentlemen and ladies," he began, "today we propose to split a ₹50,000 crore enterprise into two. It's either the best decision we'll ever make, or..." he paused, allowing the alternative to hang unspoken in the digital ether.

The document before the board was titled "Project Phoenix: Composite Scheme of Arrangement." It outlined a complex financial engineering exercise that would separate Piramal Enterprises Limited (PEL) into two distinct entities: Piramal Pharma Limited (PPL), housing all pharmaceutical businesses, and a retained PEL focused on financial services and real estate. It was corporate surgery of the highest order, requiring regulatory approvals from the RBI, SEBI, stock exchanges, and the National Company Law Tribunal.

The rationale was compelling but contentious. Deepak Parekh, independent director and HDFC chairman, voiced what many were thinking: "Ajay, conglomerates trade at a discount, yes. But they also provide stability. Are we solving one problem only to create two?"

Piramal's response revealed years of frustration: "Our pharmaceutical business is valued at 8x EBITDA within the conglomerate structure. Pure-play pharma companies trade at 15-20x. We're destroying ₹15,000 crore of value because investors can't understand what we are. Worse, we can't use our stock as currency for acquisitions because sellers don't want conglomerate paper."

The mechanics of the demerger were Byzantine in complexity. The scheme provided for 4 equity shares of ₹10 each of Piramal Pharma for every 1 share of ₹2 each held in PEL. But this simple ratio masked enormous complexity. There were tax implications to consider—Indian tax law had only recently made demergers tax-neutral for shareholders. There were debt allocations to negotiate—₹6,800 crore of debt needed to be split between the entities. There were employee stock options to restructure, vendor contracts to bifurcate, and IT systems to separate.

The most contentious issue was leadership succession. Ajay Piramal, at 66, would remain chairman of both entities. But operational leadership needed clarity. In a move that surprised many, he appointed his daughter Nandini Piramal, then 44, as chairperson of Piramal Pharma. It was a bold choice—Nandini had founded and run Piramal's healthcare insights business but had never directly managed pharmaceutical operations.

"Are we ready for this?" asked Nandini at a family dinner, according to sources close to the family. Ajay's response was characteristic: "Nobody's ever ready. But you're more ready than you think."

The regulatory approval process became a marathon. The NCLT raised concerns about creditor protection. SEBI wanted assurances about minority shareholder rights. The income tax department scrutinized the tax neutrality claims. Each regulator's query triggered weeks of legal responses, financial modeling, and stakeholder consultations.

Meanwhile, market conditions were deteriorating. The second COVID wave hit India in April 2021, killing thousands daily and crushing market sentiment. Pharmaceutical stocks, which had surged during the pandemic, were correcting sharply as vaccine optimism grew. Investment bankers advised postponing the demerger. "The market won't give you the valuation you deserve," warned Goldman Sachs.

Piramal's decision to proceed regardless reflected his reading of deeper trends. "Markets are cyclical, but structural changes are permanent," he told his team. "We're not timing the market; we're positioning for the next decade."

The shareholder approval meeting on September 17, 2021, was historic. Conducted virtually due to ongoing pandemic restrictions, over 3,000 shareholders logged in. The institutional investors were supportive—they'd long advocated for simplifying Piramal's structure. But retail shareholders were skeptical. One elderly shareholder from Kolkata asked, "Mr. Piramal, I bought your shares because I trusted you with my money. Now you're giving me two companies. Which one should I keep?"

Piramal's answer was diplomatic but revealing: "Keep both if you can. But if you must choose, ask yourself: do you want growth or stability? Pharma will be growth. Financial services will be stability."

The vote was overwhelming: 99.3% approval. But the real challenge lay ahead—preparing Piramal Pharma for independent listing. The company needed its own board of directors, audit committee, risk management framework, and investor relations function. It needed to establish credit ratings, banking relationships, and working capital facilities independent of the parent.

Peter DeYoung, the American CEO of Piramal Pharma Solutions, faced particular challenges. "We went from being a division of a conglomerate to needing our own everything—treasury, legal, HR, IT. It was like building a plane while flying it," he told employees.

The IT separation alone consumed ₹200 crore and 18 months of effort. Two thousand applications needed to be split or replicated. Data warehouses had to be segregated. Email systems needed separation. Even seemingly simple things like the company website required complete reconstruction.

More challenging was establishing Piramal Pharma's equity story for public market investors. The company hired Nandini Shenoy from Cipla as head of investor relations. Her first investor presentation draft was 180 slides long. "You're not selling the company," Ajay told her. "You're selling three simple ideas: we're differentiated, we're growing, and we're investable. Everything else is detail."

The refined equity story centered on Piramal Pharma's unique positioning. Unlike pure CDMOs like Divi's Laboratories, it had branded products. Unlike branded generics players like Sun Pharma, it had a services business. Unlike most Indian pharmaceuticals companies, it had a truly global footprint with 60% of revenues from developed markets. The tagline became: "Global Scale, Indian Roots, Differentiated Portfolio. "The listing day, October 19, 2022, arrived with unusual Mumbai weather—clear skies instead of the typical October humidity, which some took as an auspicious sign. The equity shares of Piramal Pharma Limited were listed and admitted to dealings on BSE and NSE on October 19, 2022. The bell-ringing ceremony at BSE was emotional. Ajay and Nandini Piramal stood together, three generations of the family present, as the iconic gong resonated through the historic trading floor.

According to market analysts, Piramal Pharma share listing price was expected to be around 200-250. The actual opening trade validated these expectations, with the stock beginning its independent journey in that range. The demerger ratio had been carefully structured—equity shareholders of PEL as on the demerger record date received 4 equity shares of face and paid-up value of Rs 10 each of the Company for every 1 equity share of face and paid-up value of Rs 2 each held in PEL.

The market's initial reception was cautiously optimistic. Unlike typical IPOs with their frenzied first-day pops, Piramal Pharma's listing was more subdued, reflecting the complexity of valuing a newly independent entity with three distinct business segments. Institutional investors who had pushed for the demerger were satisfied—they finally had a pure-play pharmaceutical investment. Retail investors who had held Piramal Enterprises for its financial services exposure suddenly found themselves owning a pharmaceutical company they hadn't explicitly chosen.

The first earnings call as an independent company, in January 2023, set the tone for the new era. Nandini Piramal, now firmly established as chairperson, articulated a vision that was both ambitious and realistic: "We're not trying to be everything to everyone. We're building depth in three chosen areas where we believe we can be global leaders."

The demerger had achieved its primary objective—creating focused entities that investors could value appropriately. But it had also done something more subtle: it had forced Piramal Pharma to define itself not in relation to its parent or its history, but on its own terms. The safety net of conglomerate diversification was gone. The training wheels were off.

For Ajay Piramal, watching his daughter ring the listing bell represented both an ending and a beginning. The company he'd rebuilt from scratch after the Abbott sale was now standing on its own, ready to compete with global giants. Whether it would soar or struggle remained to be seen, but one thing was certain: Piramal Pharma was no longer just a chapter in the Piramal Group story. It was writing its own book.

VI. Business Deep Dive: The Three Pillars

A. CDMO Business (Contract Development & Manufacturing)

The conference room at Piramal's Lexington facility in Kentucky could have been mistaken for a United Nations summit. Around the table sat representatives from Pfizer, Novartis, Gilead, and three biotech companies whose names were covered by NDAs. They weren't there to negotiate prices or timelines. They were there to solve a problem that had stumped their internal teams: how to manufacture a new antibody-drug conjugate that was so potent, exposure to even microscopic amounts could be lethal.

Peter DeYoung, CEO of Piramal Pharma Solutions, opened with characteristic directness: "Gentlemen, what you're asking for doesn't exist anywhere at commercial scale. The good news is, we've been preparing for this question for five years."

This moment encapsulated the CDMO strategy Piramal had been executing since 2010: positioning itself not as the cheapest manufacturer, but as the solver of impossible problems. Over the past five years, innovation revenue has grown from 35% of total to more than 50%, representing a CAGR of 20%. The 50% figure represents work performed for pharma innovator customers across discovery, development and on-patent commercial manufacturing.

The CDMO business operates from a globally integrated network of facilities in North America, Europe, and Asia, with 15 CDMO sites with major presence in North America (4), Europe(2) and India (9). But the real differentiation isn't geography—it's capability. While competitors focused on either small molecules or large molecules, Piramal built expertise in both. While others specialized in either development or commercial manufacturing, Piramal offered end-to-end services from drug discovery through commercial launch.

The crown jewel of the CDMO portfolio is the high potency API (HPAPI) capability. These are molecules so powerful that manufacturing them requires specialized containment facilities, robotic handling systems, and workers in astronaut-like protective suits. The global market for HPAPI manufacturing is dominated by a handful of players, and Piramal had methodically built capabilities to join this exclusive club.

"We realized early that everyone could make ibuprofen," explained Dr. Ganesh Naik, Head of API Development. "But how many could safely handle compounds that are effective at nanogram doses? That's where the margins are. That's where the relationships are built."

The numbers validated this strategy. The growth in innovation revenue is consistent with Piramal Pharma's success in delivering high value services, including high potency active pharmaceutical ingredients (HPAPIs), antibody-drug conjugations, peptide APIs, sterile fill/finish, and integrated programs. The company has successfully delivered more than 125 integrated programs to date, each representing a multi-year relationship with pharmaceutical innovators.

But the CDMO business isn't without challenges. Customer concentration remains a persistent issue, with the top 10 customers accounting for over 60% of revenues. The business is also inherently lumpy—a single project cancellation can impact quarterly results significantly. Competition from Chinese CDMOs offering prices 30-40% lower is intensifying, forcing Piramal to continuously move up the complexity curve.

The solution has been to focus on "sticky" services where switching costs are high. Once a drug is approved using Piramal's manufacturing process, changing manufacturers requires extensive regulatory revalidation. This creates an annuity-like revenue stream that can last for decades. It's a lesson learned from studying Lonza and Catalent: win the development project, and you often win the commercial manufacturing contract by default.

B. Complex Hospital Generics (Critical Care)

The operating room at Johns Hopkins Hospital is a symphony of precision. The anesthesiologist draws sevoflurane into specialized vaporizer, calculating the exact concentration needed to keep the patient unconscious but not too deep. The drug, manufactured at Piramal's Bethlehem, Pennsylvania facility, represents a category that most pharmaceutical companies ignore: products that are generic in patent status but anything but generic in complexity.

Piramal Critical Care (PCC) is a leading, global player in inhaled anesthetics hospital generics, maintaining a wide presence across the USA, Europe and more than 100 countries worldwide. The portfolio reads like a medical school pharmacology textbook: sevoflurane, isoflurane, and desflurane for anesthesia; intrathecal baclofen for spasticity; injectable opioids for post-surgical pain. These aren't pills you can stamp out by the millions. They're precision products requiring specialized manufacturing, handling, and distribution.

The Bethlehem facility, acquired from Rhodia in 2012, is a case study in barriers to entry. Manufacturing inhaled anesthetics requires equipment that can handle volatile organic compounds, quality control systems that can detect impurities at parts-per-billion levels, and a distribution network that can maintain cold chain integrity from factory to operating room. The capital investment required to replicate these capabilities runs into hundreds of millions of dollars—for a market that's growing at only 3-4% annually.

"It's the pharmaceutical equivalent of selling picks and shovels during a gold rush," explained Dr. Vivek Sharma, Head of Complex Hospital Generics. "Everyone's chasing the next blockbuster drug. We're making sure surgeons can operate tomorrow morning."

The moat around this business is regulatory as much as technical. Each product requires approval not just from FDA but from individual hospital formulary committees. Switching from one supplier to another requires retraining anesthesiologists, recalibrating vaporizers, and accepting litigation risk if something goes wrong. As a result, once Piramal wins a hospital system, they rarely lose it.

The financial profile reflects these dynamics: gross margins exceeding 60%, customer retention rates above 95%, and predictable, recession-resistant demand. During COVID-19, when elective surgeries were cancelled globally, revenues dipped only 15%—far less than the 40-50% declines seen in other pharmaceutical categories.

Yet the business faces its own challenges. The market is oligopolistic, with Baxter, AbbVie, and Piramal controlling most of the global supply. This concentration has attracted regulatory scrutiny, with some countries implementing price controls on essential anesthetics. There's also the constant threat of new entrants, particularly from China, though so far none have successfully navigated the regulatory and technical barriers.

The strategy going forward is selective expansion. Rather than competing across all hospital products, Piramal is focusing on specific procedures where it can dominate. Intrathecal therapies for pain management is one such area, where Piramal is investing $50 million in new manufacturing capabilities. The logic is simple: own the niche completely rather than being a small player in a large market.

C. India Consumer Healthcare

The pharmacy on Linking Road in Mumbai's Bandra suburb is a microcosm of Indian healthcare. Behind the counter, next to prescription antibiotics and diabetes medications, sits a familiar white and blue box: Saridon. The customer doesn't need a prescription. She doesn't even need to ask. She simply says "headache," and the pharmacist reaches for Saridon—a transaction repeated millions of times daily across India.

This is the third pillar of Piramal Pharma: consumer healthcare products that have become part of India's cultural fabric. The portfolio includes brands that span generations: Saridon for headaches, Lacto Calamine for skin problems, Supradyn for vitamins, I-Pill for emergency contraception, and Little's for baby care. Combined, these brands generate over ₹1,500 crore in annual revenues with EBITDA margins exceeding 30%.

But managing consumer brands requires a fundamentally different mindset from the other two businesses. As Kedar Sohoni, brought in from Hindustan Unilever to run the division, discovered: "In CDMO, you're B2B. In hospital generics, you're B2B2C. In consumer healthcare, you're talking directly to a mother worried about her child's fever at 2 AM. It's a completely different game."

The transformation of these heritage brands has been remarkable. Saridon, acquired from Roche, was repositioned from just another painkiller to "India's headache expert." The marketing campaign, featuring Bollywood celebrities describing their "Sirf Ek Saridon" (Just One Saridon) moments, increased brand recall by 40%. Lacto Calamine, traditionally seen as medicinal, was reimagined as a beauty essential for young women, with influencer partnerships and Instagram campaigns driving a 60% increase in sales among 18-25 year-olds.

The distribution strategy has been equally innovative. While competitors fought for shelf space in modern retail, Piramal doubled down on traditional trade—the 800,000 small pharmacies that still account for 85% of India's pharmaceutical retail. The company's sales force doesn't just sell; they educate pharmacists on when to recommend each product, turning them into brand ambassadors.

Digital transformation has opened new frontiers. The company launched direct-to-consumer platforms, WhatsApp consultation services, and subscription models for vitamins. During COVID-19, when physical pharmacies were inaccessible, online sales grew 300%, validating the omnichannel strategy.

But the consumer business faces intense competition. Global giants like GSK and P&G have deeper pockets for advertising. Local players like Mankind and Emami compete aggressively on price. New-age brands backed by venture capital are disrupting traditional categories with Instagram-first strategies.

The response has been to leverage the unique advantages of being part of a pharmaceutical company. Unlike pure consumer companies, Piramal can develop clinically validated formulations. Unlike pure pharmaceutical companies, it understands consumer marketing. This hybrid capability has enabled innovations like Little's baby products with pharmaceutical-grade safety standards but consumer-friendly packaging and communication.

Synergies and Integration

The real magic happens when the three pillars work together. Integrated programs offer compelling value propositions to customers such as reduced time-to-market, simplified operational complexity, and reduced supply chain costs. A recent example: a U.S. biotech developing a complex oncology drug needed API manufacturing (CDMO), sterile fill-finish (Complex Hospital Generics expertise), and eventually planned an OTC version (Consumer Healthcare capability). Instead of managing three vendors, they worked with one—Piramal.

These integrated offerings are becoming a key differentiator. While competitors might excel in one area, few can offer the breadth of services Piramal provides. It's not just about cross-selling; it's about solving complex problems that span multiple capabilities.

The financial impact is significant. Integrated programs command premium pricing—typically 15-20% higher than standalone services. They also create stickier relationships; customers using multiple Piramal services have a churn rate below 5%, compared to 15% for single-service customers.

Looking ahead, the three-pillar strategy is evolving from parallel tracks to an integrated ecosystem. The company is investing in digital platforms that allow customers to seamlessly access all services, creating what management calls a "pharmaceutical solutions marketplace." It's ambitious, complex, and exactly the kind of challenge that Piramal has proven it can handle.

VII. Partnerships & Joint Ventures

The negotiation table at the Taj Mahal Hotel in Delhi, March 2019, was split down the middle—literally. On one side sat the Allergan team, led by their Asia-Pacific president, armed with McKinsey presentations and Harvard Business School case studies. On the other, Ajay Piramal with just two associates, a single sheet of paper, and a philosophy that had guided him for decades: "In a good partnership, both sides should feel they've won."

The deal under discussion would create one of India's most formidable ophthalmology pharmaceutical enterprises. The company has a 49% ownership interest in a joint venture with Allergan India Pvt. Ltd (AbbVie US pharmaceutical company holds a 51% ownership interest), which is one of the leading pharmaceutical company in Ophthalmology formulations in India. But this wasn't just about market share or financial returns. It was about a strategic philosophy that set Piramal apart: using partnerships not just to grow, but to learn.

"Most Indian companies view joint ventures as necessary evils," Piramal explained to his board before signing. "We view them as universities where we pay tuition in equity but graduate with capabilities money can't buy."

The Allergan partnership exemplified this approach. Allergan brought Botox, Lumigan, and other high-margin ophthalmology products. Piramal brought distribution reach into tier-2 and tier-3 Indian cities where Allergan had struggled to penetrate. But the real value lay in knowledge transfer. Allergan's regulatory expertise in biologics, their physician education programs, their approach to medical aesthetics—all became part of Piramal's institutional knowledge.

The structure was deliberately crafted to align incentives. While Allergan held 51% control, major decisions required supermajority approval, effectively giving Piramal veto power. Profit sharing was proportional to equity, but investment requirements were proportional to capabilities contributed. This meant Allergan funded most of the medical education initiatives while Piramal handled distribution expansion.

Within 18 months, the joint venture had exceeded all projections. Revenues grew 45% year-over-year. Market share in glaucoma medications jumped from 12% to 23%. But more importantly for Piramal, they had learned how to manage biological products, setting the stage for their next strategic move.

That move came in 2022 with a 33.33% minority investment in Yapan Bio, a Hyderabad-based biotechnology company specializing in biologics and vaccine development. This wasn't just a financial investment—it was Piramal's entry ticket into the future of pharmaceuticals.

Yapan Bio, founded by former Dr. Reddy's scientists, had developed a proprietary platform for producing biosimilars at 40% lower cost than conventional methods. They had also created a novel vaccine delivery system that could maintain stability without cold chain—potentially revolutionary for developing markets. What they lacked was commercial scale and regulatory expertise—exactly what Piramal could provide.

The partnership structure was unusual. Instead of a traditional joint venture, Piramal took a minority stake but secured exclusive commercialization rights for Yapan's products in 45 countries. They also placed two Piramal executives in Yapan's C-suite: a Chief Commercial Officer and a Head of Regulatory Affairs. This gave them operational influence without the burden of majority ownership.

"We're not trying to control Yapan," explained Nandini Piramal at the announcement. "We're trying to amplify them. They innovate, we commercialize. It's a partnership of complementary capabilities."

The early results have been promising. Yapan's biosimilar version of bevacizumab, a cancer drug, received approval in India within 18 months of Piramal's investment—half the typical timeline. The companies are now working on five additional biosimilars, with Piramal's regulatory team accelerating approval processes across multiple markets.

But partnerships haven't always been smooth. A 2018 joint venture with a Chinese API manufacturer collapsed when quality issues emerged during due diligence. A collaboration with a European CDMO ended in arbitration over intellectual property rights. These failures taught valuable lessons about partner selection, structure, and governance.

The learning led to what Piramal calls its "Partnership Playbook"—a formal framework for evaluating, structuring, and managing collaborations. Key principles include:

Capability Complementarity: Partners must bring something Piramal lacks and value what Piramal offers. Pure financial partnerships rarely work.

Aligned Timelines: Both parties must have similar investment horizons. Mismatched expectations about exit timing have killed many promising ventures.

Cultural Compatibility: Beyond financials and strategy, teams must be able to work together. Piramal now conducts "cultural due diligence," including joint workshops before signing deals.

Clear Governance: Decision rights, dispute resolution mechanisms, and exit clauses must be crystal clear from day one. Ambiguity is the enemy of partnership.

Knowledge Transfer Mechanisms: Formal processes for sharing expertise, from personnel exchanges to joint training programs, must be built into the partnership structure.

These partnerships are increasingly critical to Piramal's strategy. The pharmaceutical industry is becoming too complex for any single company to master all capabilities. Biologics, gene therapy, personalized medicine—each requires specialized expertise that would take decades to build internally. The partnership strategy extends beyond major deals. Piramal has created an ecosystem of smaller collaborations—technology transfers with Korean companies, distribution agreements with African firms, research partnerships with European universities. Each adds a piece to the capability puzzle.

Looking forward, partnerships will become even more critical. The company is exploring collaborations in cell and gene therapy, an area requiring billions in investment and decades of expertise to enter independently. They're also evaluating partnerships with digital health companies, recognizing that the future of pharmaceuticals isn't just about molecules but about data and patient engagement.

"We're building a network, not just a company," Nandini Piramal explained at a recent investor conference. "In the pharmaceutical industry of the future, no one company will have all the answers. Success will come from orchestrating capabilities across partners."

VIII. Modern Era: Challenges & Opportunities (2022–Present)

The emergency board meeting on July 28, 2025, convened at 6 AM Mumbai time—an unusual hour reflecting the urgency of the situation. The Q1 FY26 results were about to be announced, and they weren't pretty. Revenue from Operations stood at ₹ 1,934 crores vs ₹ 1,951 crores in Q1FY25. EBITDA margin at 9% vs 11% in Q1FY25. The company had posted a net loss of ₹82 crore in the first quarter of FY26, mainly due to the destocking of one of its large on-patent commercial products.

Nandini Piramal, now firmly in charge as chairperson, addressed the virtual gathering with characteristic directness: "Let's not sugarcoat this. We're facing headwinds. But let's also not forget—we've navigated storms before."

The challenges facing Piramal Pharma in the modern era are fundamentally different from those of the rebuilding years. It's no longer about establishing capabilities or winning customers. It's about executing in an environment of unprecedented complexity and competition.

The CDMO business, once Piramal's growth engine, is facing intense pressure. The company's EBITDA dropped by 26 per cent year-on-year to ₹165 crore. The culprit was inventory destocking—a phenomenon sweeping the global pharmaceutical industry as companies burned through COVID-era stockpiles. But the deeper issue was structural: biotech funding had dried up, with venture capital investment in life sciences down 40% from peak levels. Small biotechs, which comprised 60% of Piramal's CDMO customers, were delaying projects, canceling programs, or going bankrupt altogether.

The competition had also intensified dramatically. Chinese CDMOs, despite geopolitical tensions, were winning business with prices 30-40% below Western competitors. Indian peers like Divi's Laboratories and Laurus Labs were expanding aggressively. Global giants like Lonza and Catalent were consolidating smaller players, creating scale advantages Piramal couldn't match.

Peter DeYoung, CEO of Piramal Pharma Solutions, presented a sobering analysis to the board: "We're caught in the middle. Too small to compete with the giants on scale, too expensive to compete with the Chinese on price. We need to find our niche or risk becoming irrelevant."

The strategy that emerged was bold: double down on complexity. Successfully closed USFDA inspection at Aurora facility (Canada) with zero observations. Continue to maintain our 'Zero OAIs' status since 2011—a track record few competitors could match. The company would focus on the most difficult-to-manufacture products—highly potent APIs, antibody-drug conjugates, controlled substances—where regulatory expertise and quality track record mattered more than price.

The Complex Hospital Generics business faced different challenges. While demand for anesthetics remained stable, pricing pressure from hospital group purchasing organizations was intensifying. In the U.S., three GPOs controlled 90% of hospital purchasing, using their scale to squeeze margins from suppliers. Meanwhile, new competitors from India and China were entering the market with biosimilar versions of Piramal's key products.

The response was vertical integration. Piramal began manufacturing key raw materials in-house, reducing dependency on Chinese suppliers and improving margins. They also expanded into adjacent categories—pain management, anti-infectives—leveraging their hospital relationships. Piramal's consumer healthcare segment recorded a 15 per cent increase year-on-year, reaching ₹302 crore.

The India Consumer Healthcare business was the bright spot, but even here, challenges loomed. E-commerce was disrupting traditional pharmacy distribution. New-age brands backed by venture capital were spending aggressively on digital marketing. Regulatory scrutiny on OTC advertising was increasing. The government was considering price controls on essential medicines, which could impact margins.

The digital transformation became imperative, not optional. Piramal launched direct-to-consumer platforms, invested in data analytics to understand consumer behavior, and partnered with e-pharmacies for distribution. They also accelerated new product development, launching 27 new products and 24 new SKUs in FY24, with another 21 products and 31 SKUs in FY25.

But the biggest opportunity—and challenge—lies in the company's FY2030 vision. Withstanding the near-term challenges, we believe we are on track to achieve our FY2030 aspirations of becoming a US$2bn revenue company with 25% EBITDA margin and high-teen ROCE. This would require doubling revenues and more than doubling margins in just five years—an ambitious target even in favorable conditions.

The path to $2 billion requires several things to go right simultaneously. The CDMO business needs to win several large integrated programs. The hospital generics business needs to successfully launch new products without cannibalizing existing ones. The consumer business needs to maintain growth while improving margins. And all of this needs to happen while managing debt, investing in capacity, and navigating regulatory requirements across multiple geographies.

The sustainability agenda adds another layer of complexity. Assigned an ESG rating of '61' for FY2024 by NSE Sustainability Ratings and Analytics Limited, but investors increasingly demand more. The company has committed to carbon neutrality by 2040, requiring massive investments in renewable energy and process optimization. Water usage, always a concern in pharmaceutical manufacturing, needs to be reduced by 50% per unit of production. Waste management, particularly of hazardous chemicals, requires continuous innovation.

The leadership transition adds both opportunity and risk. Nandini Piramal brings fresh perspective and energy, but lacks the deep industry relationships her father built over decades. The senior management team is aging, with several key executives approaching retirement. Attracting and retaining talent is increasingly difficult, with global pharmaceutical companies offering packages Piramal can't match.

The macroeconomic environment provides both tailwinds and headwinds. India's pharmaceutical market is growing at 8-10% annually, driven by increasing healthcare access and aging demographics. But currency volatility, with the rupee weakening against the dollar, impacts the cost of imported raw materials. Geopolitical tensions, particularly between the U.S. and China, create both opportunities (as companies seek alternatives to Chinese suppliers) and risks (as supply chains fragment).

Despite these challenges, there are reasons for optimism. The company's diverse portfolio provides resilience—when one segment struggles, others can compensate. The global trend toward outsourcing in pharmaceuticals continues to accelerate. India's reputation as a reliable supplier of quality medicines is improving. And Piramal's track record of navigating difficult transitions gives confidence in management's ability to execute.

The modern era for Piramal Pharma is thus one of managed complexity. It's about balancing growth with profitability, global ambitions with local realities, innovation with execution. It's about competing with companies ten times their size while maintaining the agility of a startup. Most importantly, it's about proving that the phoenix that rose from the ashes of the Abbott sale can soar, not just survive.

As Nandini Piramal concluded the July board meeting: "We're not where we want to be today. But remember, neither were we in 2010 when we started from zero. The difference is, this time we know exactly what we're building toward."

IX. Playbook: Business & Investing Lessons

The Art of Selling at the Peak: Timing the Abbott Deal

In the pantheon of great business exits, Ajay Piramal's sale to Abbott stands as a masterclass in timing. But the real lesson isn't about luck or market timing—it's about recognizing when your competitive advantages are eroding before the market does.

By 2010, Piramal could see what others couldn't: the Indian branded generics market was about to become a bloodbath. Price controls were expanding. Competition was intensifying. Margins were peaking. Most importantly, the business model of selling me-too drugs through doctor relationships was becoming obsolete. Digital health records, evidence-based medicine, and insurance-driven formularies would eventually commoditize what Piramal had spent decades building.

The genius was in selling not just a business, but a dream. Abbott wasn't buying Piramal's 2010 reality—they were buying India's 2020 potential. Every presentation emphasized India's growing middle class, expanding healthcare coverage, and demographic dividend. The financial projections showed hockey-stick growth. The narrative was about becoming the gateway to a billion-person market.

This creates a crucial lesson for investors: the best time to sell is when everyone wants to buy. When your industry is on magazine covers, when private equity is circling, when strategic buyers are desperate for growth—that's precisely when you should consider exiting. The corollary is equally important: the best time to buy is when nobody else wants to, which is exactly what Piramal did after the sale, rebuilding in unfashionable segments like CDMO and hospital generics.

Capital Allocation Mastery: From Pharma to Finance and Back

The ₹15,000 crore Piramal received from Abbott could have been deployed in countless ways. He could have retired. He could have bought real estate. He could have become a venture capitalist. Instead, he did something remarkable: he simultaneously entered financial services (creating what would become Piramal Finance) while rebuilding pharmaceuticals from scratch.

This portfolio approach to capital allocation reflects deep wisdom about risk and return. Financial services provided steady, predictable cash flows. Pharmaceuticals offered higher growth but with more volatility. Real estate (another business Piramal entered) provided asset backing and inflation protection. Together, they created a portfolio that could weather any storm.

The lesson for investors is profound: diversification isn't just about owning different stocks. It's about owning different business models, different sources of cash flow, different risk profiles. Piramal's approach—using stable businesses to fund risky ones, using mature businesses to subsidize growing ones—is corporate finance at its finest.

The ₹2,500 crore buyback after the Abbott sale deserves special mention. Rather than hoarding cash or making desperate acquisitions, Piramal returned capital to shareholders when he couldn't find attractive opportunities. This discipline—knowing when not to invest—is perhaps rarer and more valuable than knowing when to invest.

Building Competitive Advantages in Commoditized Markets

The pharmaceutical industry, particularly generics and contract manufacturing, is brutally commoditized. Products are identical. Customers are price-sensitive. Switching costs are low. Yet Piramal built defensible positions in these seemingly indefensible markets.

The strategy was elegantly simple: complexity as a moat. In CDMO, while others competed on price for simple molecules, Piramal focused on highly potent APIs requiring specialized handling. In hospital generics, while others made tablets, Piramal manufactured inhaled anesthetics requiring sophisticated delivery systems. In consumer healthcare, while others sold commoditized vitamins, Piramal built brands with emotional resonance.

This teaches a crucial lesson: in commoditized industries, the only sustainable advantage is doing what others can't or won't do. It's not about being cheaper—someone will always be cheaper. It's about being different in ways that matter to customers and are hard to replicate.

The Value of Patient Capital and Long-Term Thinking

From 2010 to 2020, Piramal Pharma burned through billions rebuilding the business, with minimal profits to show for it. Most public market investors would have revolted. Activist investors would have demanded asset sales or management changes. Yet Piramal, controlling the company through family ownership, could afford to be patient.

This patience paid off. The CDMO business, which lost money for five years, now generates 18% EBITDA margins. The hospital generics business, which required massive upfront investment, now has 25% margins. The consumer business, built brand by brand, now commands premium pricing.

The lesson is clear: building sustainable competitive advantages takes time—often a decade or more. Public markets, with their quarterly earnings obsession, rarely provide this time. This is why family-controlled businesses, private equity-owned companies, and founder-led firms often outperform in the long run. They can afford to be patient when others can't.

Managing Through Cycles: From Hero to Zero to Hero

Piramal's journey from pharmaceutical hero (pre-2010) to zero (selling everything) to hero again (rebuilding from scratch) offers profound lessons about business cycles and personal resilience.

Most executives define themselves by their businesses. Selling would mean admitting failure or losing identity. Piramal's ability to emotionally detach from his creation—to see it as a business, not a baby—enabled him to maximize value. His willingness to start over, at age 55, in the same industry where everyone knew his history, required extraordinary courage and humility.

For investors, this teaches the importance of separating ego from investment decisions. The best investors are ruthlessly objective about their holdings. They don't fall in love with companies. They don't hold losers to avoid admitting mistakes. They certainly don't define themselves by their portfolios.

Demerger as Value Creation Tool

The 2022 demerger of Piramal Pharma from Piramal Enterprises wasn't just financial engineering—it was value creation through simplification. The conglomerate structure, while useful during the rebuilding phase, had become a constraint. Investors couldn't properly value the businesses. Management couldn't properly incentivize employees. Partners couldn't properly assess creditworthiness.

The demerger unlocked value in multiple ways. It allowed proper valuation of each business. It enabled focused management attention. It created currency (listed shares) for acquisitions. It improved employee retention through targeted stock options. Most importantly, it forced each business to stand on its own merits.

This highlights a crucial principle: corporate structure should follow business strategy, not vice versa. When structure becomes a constraint, it's time to restructure. The transaction costs, regulatory hassles, and execution risks are worth it if the end result is a more focused, valuable enterprise.

Family Business Governance in Public Markets

The Piramal story offers nuanced lessons about family businesses in public markets. The family maintains only 34.9% ownership, yet effectively controls the company through board composition and management positions. This creates both advantages (long-term thinking, aligned interests) and challenges (succession risk, minority shareholder concerns).

The transition from Ajay to Nandini Piramal as chairperson was carefully orchestrated over years, not months. She was given increasingly important responsibilities, from running small divisions to leading the entire pharmaceutical business. This gradual transition, while maintaining continuity, offers a template for other family businesses navigating succession.

Yet questions remain. What happens when the third generation comes of age? How does the company balance family interests with minority shareholders? Can professional managers coexist with family members in senior positions? These tensions, inherent in family-controlled public companies, require constant navigation.

The Meta-Lesson: Business as Creative Destruction

Perhaps the most profound lesson from the Piramal saga is that business, at its best, is an act of creative destruction. Piramal destroyed a successful branded generics business to create a CDMO platform. He destroyed a conglomerate structure to create focused entities. He destroyed comfortable market positions to enter difficult but defensible niches.

This willingness to destroy what you've built—before someone else destroys it for you—is perhaps the rarest business skill. It requires seeing around corners, anticipating market shifts, and most difficultly, acting on those insights when everything seems fine.

For investors, this means constantly questioning investment theses, especially for successful companies. The seeds of failure are often sown in success. The businesses that seem invincible often prove most vulnerable. And sometimes, the best investment decision is to sell winners, not losers—a psychologically difficult but financially rewarding discipline that Ajay Piramal mastered better than most.

X. Analysis & Investment Case

Bull Case: The Constellation of Possibilities

The optimistic case for Piramal Pharma rests on multiple expansion drivers converging simultaneously. The global CDMO market, growing at 7.6% annually, provides a robust backdrop for the company's largest segment. But Piramal isn't just riding the market—it's gaining share through differentiation.

The shift in the CDMO business toward innovation is particularly compelling. With innovation revenue crossing 50% for the first time, representing a 20% CAGR over five years, Piramal is successfully moving up the value chain. These aren't commodity manufacturing contracts but strategic partnerships with biotech innovators developing next-generation therapies. The economics are fundamentally different: higher margins, longer contracts, deeper relationships.

The complex hospital generics business offers a different but equally attractive proposition: defensive growth. These products—inhaled anesthetics, intrathecal therapies—are essential for hospital operations. Demand is recession-proof, pricing is stable, and competition is limited due to high regulatory and technical barriers. With capacity expansions underway and new product launches planned, this division could surprise on the upside.

The India consumer healthcare business, growing at 15% annually, taps into powerful secular trends. Rising disposable incomes, increasing health consciousness, and expanding distribution through e-commerce create multiple growth vectors. The brands—Saridon, Lacto Calamine, I-Pill—have multigenerational recognition and pricing power that's rare in Indian consumer markets.

Operational leverage is perhaps the most underappreciated aspect of the bull case. Much of the heavy investment is behind the company. The 17 global facilities are built and operational. The regulatory approvals are in place. The customer relationships are established. As revenues grow, an increasing proportion should flow to the bottom line, potentially driving margin expansion from the current 9% EBITDA margin toward the targeted 25% by FY2030.

The management's FY2030 vision of $2 billion revenue isn't fantasy—it implies a 12% CAGR from current levels, reasonable given the market growth and company's competitive position. If achieved with 25% EBITDA margins, we're looking at $500 million in EBITDA, which at sector multiples of 15-20x could value the company at $7.5-10 billion, nearly 3-4x the current market capitalization.

Bear Case: The Weight of Reality