Power Mech Projects: The Infrastructure Contractor That Built India's Power Grid

Introduction & Episode Roadmap

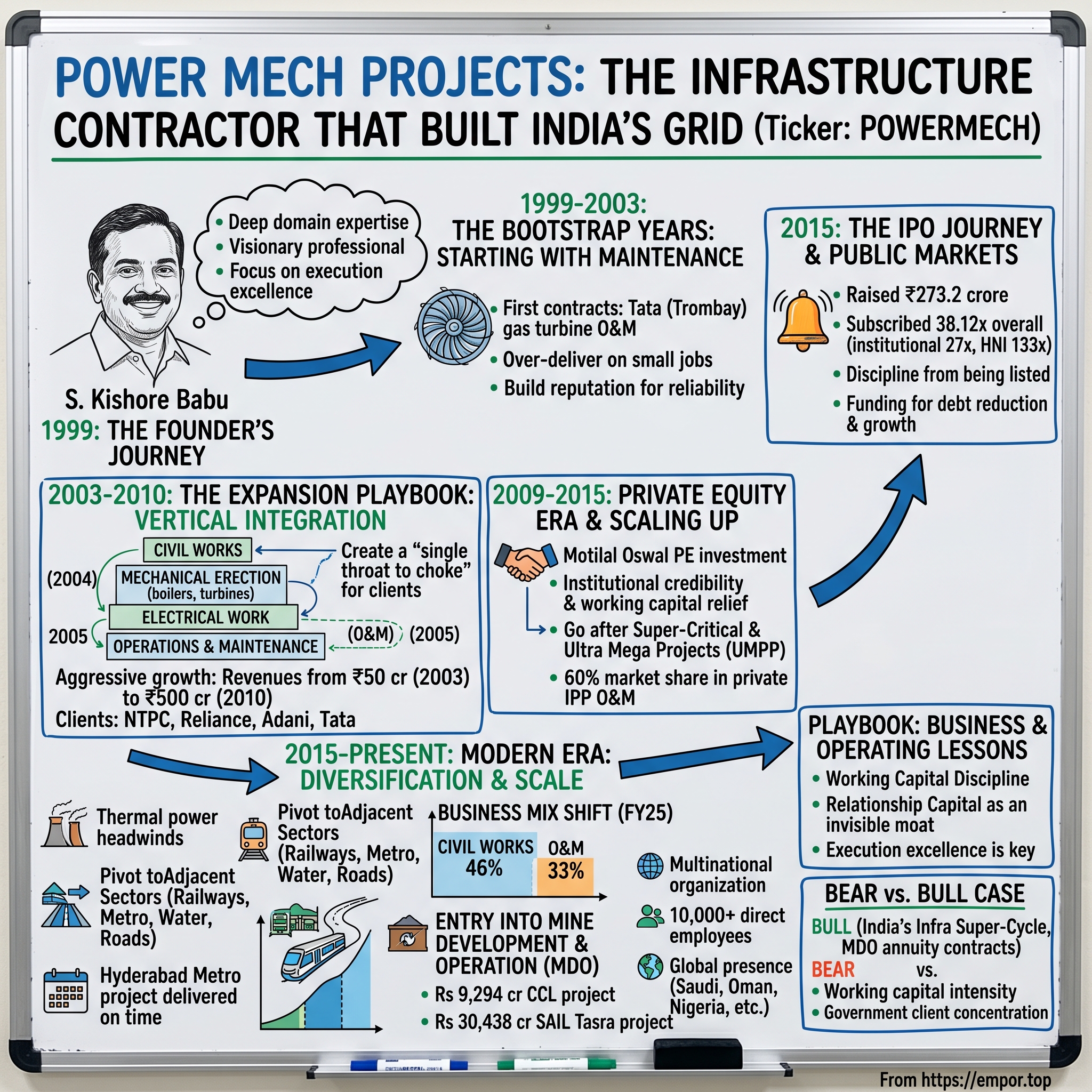

Picture this: It's 1999, the cusp of a new millennium. India's power grid is creaking under the weight of rapid economic growth. Blackouts are routine. Industrial plants run diesel generators as backup becomes primary. In this chaos, a 40-year-old engineer named S. Kishore Babu sees opportunity where others see insurmountable challenge. With 14 years of field experience but no significant capital, he incorporates Power Mech Projects Limited—a company that would eventually command a ₹9,800 crore market capitalization and become the backbone contractor for India's power infrastructure transformation.

The central question isn't just how an engineer built one of India's largest power infrastructure services companies. It's how he did it through pure execution excellence in an industry notorious for delays, cost overruns, and corporate graveyard stories. This is a story about timing markets perfectly, bootstrapping without venture capital, and building a vertically integrated powerhouse that would eventually service everything from ultra-mega power projects to metro railways.

What makes Power Mech fascinating isn't the typical tech startup trajectory of explosive growth and venture funding rounds. Instead, it's a methodical march through India's infrastructure boom—starting with humble turbine maintenance contracts, expanding into erection and commissioning of entire power plants, then diversifying across the infrastructure spectrum. Along the way, Babu and his team would navigate the treacherous waters of working capital management, client concentration risk, and the cyclical nature of infrastructure spending.

The themes we'll explore cut to the heart of building in emerging markets: How do you bootstrap a capital-intensive business? What happens when your biggest competitive advantage is simply showing up on time in an industry where nobody does? And perhaps most importantly—how do you ride a nation's infrastructure wave without getting crushed when the tide goes out?

The Founder's Journey & Pre-History

S. Kishore Babu wasn't your typical startup founder. By 1999, he'd already spent 14 years in the trenches—literally—working on construction and maintenance of power plants across India. While Silicon Valley celebrated twenty-something dropouts, Babu represented something different: deep domain expertise meeting entrepreneurial ambition at exactly the right moment in history.

Colleagues from his pre-Power Mech days describe him as a "gifted entrepreneur, visionary and professional" who could see around corners in the power sector. But what exactly did he see in 1999 that others missed? The answer lies in understanding India's power sector transformation of the 1990s.

The decade had begun with India's historic economic liberalization in 1991. Foreign investment was welcomed, license raj was being dismantled, and private sector participation in power generation—previously a government monopoly—was finally allowed. By the mid-1990s, international players like Enron were setting up massive power projects (including the infamous Dabhol plant). But here's what most people missed: while everyone focused on generation capacity, the real bottleneck was in execution—the physical work of erecting, testing, and commissioning these complex installations.

India's power deficit was staggering. The country needed to add roughly 10,000 MW of capacity annually just to keep pace with GDP growth. Yet the entire ecosystem of contractors who could actually build these plants was woefully inadequate. BHEL (Bharat Heavy Electricals Limited), the state-owned behemoth, couldn't handle the volume. International contractors were expensive and often struggled with Indian conditions. The market was screaming for professional, reliable execution partners.

The Electricity Act discussions happening in parliament during 1999 would culminate in the landmark 2003 Act, fundamentally restructuring India's power sector. Babu, with his field experience, could see this tsunami of opportunity building. But unlike many entrepreneurs who spotted the same trend, he understood something crucial: in infrastructure, relationships and execution track record matter more than capital or technology.

His founding vision was deceptively simple yet revolutionary for the Indian infrastructure sector: deliver quality work, maintain safety standards, and—most importantly—finish on time. In an industry where delays were not just common but expected, where "Indian Standard Time" was a running joke, Babu positioned Power Mech as the antithesis of business as usual. This wasn't just a business strategy; it was almost a moral stance. As he would later tell employees, "When we commit to a timeline, that commitment is sacred. A delayed power plant isn't just a business problem—it means hospitals without power, factories shut down, families in darkness."

The timing couldn't have been better. India's GDP was growing at 6-7% annually, industrial production was booming, and the infrastructure deficit was becoming a national crisis. The stage was set for one of India's great infrastructure stories. But first, Babu had to prove his tiny company could deliver where giants stumbled.

The Bootstrap Years: Starting with Maintenance (1999-2003)

The origin story of Power Mech reads like a David and Goliath tale, except David started by polishing Goliath's shoes. The company's first major contract wasn't building a power plant or even installing major equipment—it was overhauling and maintaining gas turbines for Tata at their Trombay facility in Mumbai. This wasn't glamorous work. Maintenance contracts meant working during plant shutdowns, racing against time to service equipment and get plants back online. But for a bootstrap company with no capital and no track record, it was perfect.

Think about the genius of this approach. Maintenance work required expertise but minimal capital investment. You didn't need to buy expensive equipment or maintain large inventories. Payment cycles were shorter than construction projects. Most importantly, you got intimate access to plant operations and built relationships with plant managers—the same people who would later influence vendor selection for expansion projects.

Babu's strategy was to over-deliver on these small contracts. When a maintenance job was scheduled for 15 days, Power Mech would finish in 12. When quality standards called for X, they delivered X plus 20%. This wasn't just about impressing clients; it was about building a reputation in an industry where everyone knew everyone. Plant managers would move between companies, and they'd remember the contractor who made their shutdown seamless versus the one who caused delays.

Within 18 months, word spread through the tight-knit power sector community. Power Mech was reliable. They showed up on time, worked safely, and—critically—understood the technical nuances of power equipment. This reputation opened doors that money couldn't buy.

The breakthrough came in 2002, just three years after founding. BHEL, India's pioneering power equipment manufacturer and installer, needed a subcontractor for ETC (Erection, Testing & Commissioning) work on AFBC boilers—1X63 TPH and 2X165 TPH units. This was several leagues above maintenance work. ETC contracts meant you were responsible for taking equipment from boxes to operational status, a complex dance of mechanical, electrical, and instrumentation work that could make or break a power project's timeline.

For context, BHEL selecting a three-year-old company for ETC work was almost unheard of. But Babu had been smart about building his team. He'd recruited veterans from established contractors and BHEL itself—engineers who brought not just technical knowledge but also crucial understanding of BHEL's processes and expectations. When Power Mech's team showed up for technical discussions, BHEL saw familiar faces who spoke their language.

The talent strategy deserves special attention because it would become a Power Mech signature. Instead of hiring fresh engineers cheap, Babu paid premium salaries to attract experienced professionals from established players. A senior project manager from L&T might see a 40-50% salary bump to join Power Mech. This was expensive for a bootstrap company, but Babu understood that in project execution, experience was everything. One delayed project due to inexperienced management could destroy a young company's reputation forever.

Cash flow management during these early years was a high-wire act. Infrastructure projects have notoriously long working capital cycles. You might execute work in January, submit bills in February, get them approved in April, and receive payment in June—if you're lucky. Meanwhile, you're paying salaries, equipment rentals, and material costs upfront. Many infrastructure contractors die not from lack of work but from cash flow strangulation.

Power Mech survived through a combination of financial discipline and creative structuring. They negotiated advance payments where possible, even accepting lower margins for better payment terms. They built relationships with equipment rental companies, getting extended credit based on personal guarantees from Babu. Most importantly, they maintained a laser focus on collections, with Babu personally calling clients for overdue payments.

By 2003, Power Mech had established three critical assets: a reputation for reliable execution, a team of experienced professionals, and working relationships with major players like BHEL and Tata. The foundation was set for explosive growth. But first, they needed to answer a strategic question that would define their next decade: should they remain specialists or become generalists?

The Expansion Playbook: Vertical Integration (2003-2010)

The year 2003 marked an inflection point for Power Mech, and not just because India's landmark Electricity Act was finally passed. Babu faced a strategic crossroads that would determine whether Power Mech remained a profitable niche player or evolved into something much larger. The decision? Vertical integration—but not the kind you'd study in business school.

Instead of integrating backward into manufacturing or forward into power generation, Power Mech integrated horizontally across the entire project execution value chain. If you were building a power plant, you needed someone for civil construction (foundations, buildings), mechanical erection (boilers, turbines), electrical work (generators, switchyards), and eventually operations and maintenance. Traditionally, these were handled by different contractors, creating coordination nightmares and finger-pointing when delays occurred.

Babu's insight was that clients desperately wanted a single throat to choke—one contractor who could handle multiple aspects of project execution. But building these capabilities wasn't simple. Civil construction required different equipment, skills, and working capital patterns than mechanical erection. O&M was a services business with recurring revenues but thin margins. Each vertical had its own culture, economics, and competitive dynamics.

The expansion started with civil works in 2004. Power Mech began taking on foundation work for the same plants where they were doing mechanical erection. This created immediate synergies—they were already mobilized at the site, had relationships with project managers, and understood the overall project timeline. The civil work might be less profitable than specialized ETC work, but it gave Power Mech greater control over project execution and de-risked their revenue streams.

The real game-changer was entering the O&M business in 2005. While construction projects were lumpy and dependent on capacity addition cycles, O&M provided steady, predictable cash flows. A typical O&M contract might run for 5-10 years with annual escalations. More importantly, being the O&M contractor gave you inside track on future expansion projects at the same plant. You became part of the furniture, trusted and embedded in operations.

By 2007, Power Mech was simultaneously executing projects across India—from NTPC's massive thermal plants in Orissa to private sector projects in Gujarat. The geographic expansion wasn't random; it followed India's power capacity addition map. Wherever new plants were being built, Power Mech established project offices, hired local workers, and built relationships with state electricity boards.

The numbers tell the story of this aggressive expansion. From revenues of roughly ₹50 crore in 2003, Power Mech grew to over ₹500 crore by 2010—a 10x increase in seven years. But more impressive than top-line growth was the diversity of their order book. By 2010, they were working with virtually every major power sector player: NTPC (the state-owned giant), Reliance Power, Adani Power, Tata Power, and numerous state electricity boards.

The Ultra Mega Power Projects (UMPP) announcement by the Indian government in 2006 validated Babu's vertical integration strategy perfectly. These 4,000 MW behemoths required contractors who could handle massive scale and complexity. When Reliance Power's Sasan UMPP in Madhya Pradesh needed contractors, Power Mech was ready with capabilities across civil, mechanical, and O&M. They won multiple packages worth hundreds of crores, cementing their position as a tier-1 contractor.

Client concentration was a conscious strategy during this phase, though it would later become a risk factor analysts would flag. Power Mech deliberately chose to deepen relationships with a few large clients rather than spread thin across many small ones. With NTPC, for instance, they started with one plant, delivered exceptionally, and then got invited to bid for every subsequent project. By 2010, NTPC contributed nearly 30% of revenues—concentration risk, yes, but also a massive vote of confidence from India's largest power generator.

The vertical integration playbook created a virtuous cycle. Civil work got them early entry into projects. Mechanical erection established their technical credentials. O&M gave them recurring revenues and deep client relationships. Each capability reinforced the others, creating competitive moats that pure-play contractors couldn't match. A client could award multiple packages to Power Mech knowing they'd coordinate internally rather than blame each other for delays.

But this rapid expansion created its own challenges. Working capital requirements ballooned as Power Mech took on larger projects with longer execution cycles. The company was profitable but cash-starved, constantly juggling payments to suppliers while waiting for client receivables. By 2009, it became clear that bootstrapping had taken them as far as it could. To compete for the next level of mega-projects, they needed patient capital. Enter private equity.

The Private Equity Era & Scaling Up (2009-2015)

The meeting that would transform Power Mech from a bootstrap success to an institutional-grade company happened in a nondescript Mumbai conference room in early 2009. Across the table from Kishore Babu sat representatives from Motilal Oswal Private Equity, one of India's most respected domestic funds. The financial crisis was ravaging global markets, but India's infrastructure story remained intact. Motilal Oswal was hunting for companies that could ride the next wave of power sector growth, and Power Mech fit their thesis perfectly.

The initial investment of ₹40 crore might seem modest by today's unicorn standards, but for Power Mech, it was transformational. This wasn't just about money—though the working capital relief was crucial. Institutional backing from Motilal Oswal served as a Good Housekeeping seal of approval. Banks became more willing to extend credit lines. Clients felt more comfortable awarding large contracts. Suppliers offered better payment terms.

The PE investment came in tranches, eventually reaching 19.89% ownership by the pre-IPO stage. But Motilal Oswal was a patient investor, understanding that infrastructure businesses don't follow the typical venture capital J-curve. They were betting on India's massive infrastructure deficit and Power Mech's proven execution capabilities.

With fresh capital and institutional credibility, Power Mech went after the big fish—super-critical and ultra-mega power projects that represented the cutting edge of thermal power technology. Super-critical plants operate at higher temperatures and pressures, delivering better efficiency but requiring more sophisticated installation and maintenance capabilities. The learning curve was steep, but Power Mech's approach was characteristic: hire the best talent from companies already doing this work, invest in training, and over-deliver on the first few projects to build credibility. The numbers validated the strategy. Power Mech became the largest service provider in the O&M space with backward and forward integration, eventually capturing a dominant market share. In the highly profitable O&M business, they achieved a 60% market share among private Independent Power Producers (IPPs) by the pre-IPO stage—a staggering achievement for a company that started with turbine maintenance just a decade earlier.

International expansion began tentatively in 2011 with a project in Nigeria, followed by work in Bangladesh, Nepal, and the Middle East. These weren't vanity projects to claim "global presence" in investor presentations. Each international foray was carefully chosen—markets with power deficits similar to India's, where Power Mech's experience with challenging conditions would be an advantage rather than a liability.

The order book tells the story of this phase better than any narrative could. From roughly ₹800 crore in 2009, it swelled to over ₹3,400 crore by early 2015. But more important than size was composition—a healthy mix of civil works, mechanical erection, and long-term O&M contracts. The client list read like a who's who of Indian power: NTPC, Reliance Power, Adani Power, Tata Power, plus numerous state utilities.

By 2014, with the IPO on the horizon, Power Mech had transformed from a bootstrap contractor to an institutional-grade infrastructure company. They employed over 5,000 people directly and managed another 15,000 contract workers. They had project sites across 15 Indian states and four countries. Most importantly, they had something money couldn't buy—a reputation for delivering complex projects on time in an industry where delays were the norm.

The PE era had served its purpose. Motilal Oswal's investment had provided not just capital but credibility. Their presence on the board brought governance discipline that would be crucial for public market investors. But as 2015 approached, it was clear that Power Mech had outgrown private equity. The next phase of growth would require access to public markets, and Kishore Babu was ready to ring the bell.

The IPO Journey & Public Markets (2015)

The boardroom at IIFL Capital's Mumbai office was packed on August 6, 2015. Tomorrow morning, Power Mech's IPO would open for subscription. The price band was set at ₹615-640 per share, valuing the company at roughly ₹900 crore. For a company that started with maintenance contracts worth lakhs, this was a moment of validation. But Kishore Babu wasn't celebrating yet—he knew the real test would be investor response.

The IPO structure was carefully crafted. Of the ₹273.2 crore being raised, ₹136.2 crore would come from fresh shares issued by the company, while ₹137 crore represented an offer for sale by existing shareholders, primarily Motilal Oswal's PE fund looking for an exit after six successful years. The fresh capital would be used for debt reduction and working capital—unglamorous but essential for a capital-intensive business.

The anchor investor round on August 5 set the tone. DSP BlackRock, SBI Mutual Fund, and IDFC Mutual Fund committed ₹82 crore, providing crucial validation from institutional investors. These weren't momentum chasers but fundamental investors who understood infrastructure cycles and working capital dynamics.

When subscription opened on August 7, the response was electric. By the time bidding closed on August 11, the IPO was subscribed 38.12 times overall. But the real story was in the category-wise breakdown. The institutional investor category was subscribed 27 times, while the high net worth individual segment saw a whopping 133 times subscription. Even retail investors, typically cautious about infrastructure plays, subscribed around three times.

What drove this enthusiasm? Part of it was timing—India's infrastructure story was gaining momentum under the new Modi government's ambitious plans. But investors also saw something deeper in Power Mech: a proven execution track record in an industry plagued by delays, a diversified business model combining construction and recurring O&M revenues, and most importantly, a management team that had consistently delivered on promises.

The listing day on August 26, 2015, brought a reality check. Power Mech listed at ₹585.75 against the offer price of ₹640—an 8.5% discount. For retail investors hoping for listing gains, this was disappointing. But Babu and his team weren't building for listing day pops. They were playing a longer game.

The post-IPO period tested management's mettle. Public market investors demanded quarterly performance, detailed disclosures, and constant communication—a far cry from the patient PE investors they were used to. The stock languished for months, trading below issue price as broader markets corrected and infrastructure stocks fell out of favor.

But Power Mech used this period to execute on their promises. IPO proceeds were deployed exactly as outlined in the prospectus. Debt was reduced, improving interest coverage ratios. Working capital management improved with better banking relationships post-listing. Most importantly, they continued winning and executing large orders, building credibility with public market investors quarter by quarter.

Looking back, the IPO wasn't just a fundraising event—it was a transformation. The company that had bootstrapped for 10 years and relied on one PE investor for another six was now accountable to thousands of shareholders. The discipline this imposed—regular board meetings, quarterly earnings calls, detailed annual reports—made Power Mech a more professional organization.

The IPO also provided currency for growth. Stock options could now attract top talent. The listed status opened doors with international clients who preferred publicly traded vendors. Banks were more willing to provide non-fund based limits crucial for bidding on large projects. In many ways, going public was like getting a AAA credit rating in the infrastructure contracting world.

Modern Era: Diversification & Scale (2015-Present)

The five years following the IPO would test every assumption investors had made about Power Mech. India's power sector, which had driven the company's growth for fifteen years, hit unprecedented headwinds. Thermal power plants—Power Mech's bread and butter—were being cancelled or delayed as renewable energy became cheaper and environmental concerns mounted. By 2018, nearly 40,000 MW of thermal capacity was stranded without power purchase agreements. The industry that had made Power Mech was suddenly in crisis.

Lesser companies might have panicked. But Babu and his team had been preparing for this transition even before the IPO. The strategy wasn't to abandon power—that expertise was too valuable—but to apply their project execution capabilities to adjacent sectors hungry for professional contractors.

The pivot started with railways and metro projects. If you could erect a 800 MW boiler weighing thousands of tons, surely you could handle railway electrification or metro station construction? The technical skills were transferable, but the business dynamics were different. Railway projects meant dealing with a new bureaucracy, different payment cycles, and unique safety requirements. Power Mech invested heavily in training, hired railway sector veterans, and most importantly, started small with manageable projects to build credibility.

By 2020, the strategy was paying off. Power Mech was working on railways, metro, roads & water projects on an EPC basis. The Hyderabad Metro project became a showcase—delivered on time with zero safety incidents, earning them credibility for larger urban infrastructure projects.

The business mix evolution tells the story. Civil Works grew to represent 46% of revenues by FY25, while O&M expanded to 33%. The O&M business deserves special attention—Power Mech became the largest service provider in the O&M space with backward and forward integration. While construction projects were lumpy and cyclical, O&M provided steady cash flows through multi-year contracts with built-in escalations. The most audacious diversification came in 2021-2023 with entry into Mine Development and Operation (MDO). Power Mech was awarded a Mine Development and Operation project from Central Coalfields Limited (CCL), a subsidiary of Coal India Limited, aggregating to Rs 9,294 cr over the contract period, primarily comprising mine infrastructure development, removal of overburden and extraction of coking coal at Kotre Basantpur Pachmo OCP located in Ramgarh and Bokaro Districts, Jharkhand. This was followed by an even larger contract—the Tasra Open Cast Project from Steel Authority of India with an estimated value of Rs 30,438 crores over the contract period.

These weren't just large numbers—they represented a fundamental shift in Power Mech's business model. The MDO contract primarily comprised mine infrastructure development, removal of overburden and extraction of coking coal, crushing, transportation, setting up coal washery of 3.5 MTPA capacity, with total coal extraction reserves of 96.78 MT with an annual capacity of 4 MTPA. For context, the SAIL order was four times larger than Power Mech's overall market capitalisation of over Rs 6,000 crore at the time.

The MDO contracts showcased Power Mech's evolution from a services company to an asset-light mining operator. They weren't buying mines but operating them for owners, earning fees based on production volumes. The Tasra project alone could add peak turnover of around Rs 1,200 crores plus escalation annually, providing sustainable growth in both top and bottom lines for a longer period.

Financial performance during this period validated the diversification strategy. Market cap reached 9,969 Crore with Revenue of 5,520 Cr and Profit of 366 Cr. The business mix had successfully shifted—Civil Works represented 46% in FY25, while O&M contributed 33% as the largest service provider in O&M space with backward and forward integration.

The human capital story was equally impressive. The company that started with a few dozen employees has grown to be a multinational organization, employing over 10,000 direct and over 20,000 indirect manpower. This wasn't just headcount growth—Power Mech had built specialized teams for railways, mining, water projects, each with domain expertise matching traditional players in those sectors.

International operations expanded thoughtfully rather than aggressively. Power Mech established a global presence in Saudi Arabia, Oman, Kuwait, Bangladesh, Nepal, Bhutan & Nigeria, focusing on markets with similar infrastructure challenges where Indian execution expertise provided competitive advantage.

The renewable energy transition, which many saw as an existential threat to Power Mech, became another opportunity. Solar and wind projects needed civil construction, electrical work, and O&M services—capabilities Power Mech already possessed. They pivoted quickly, winning solar EPC contracts and positioning themselves as technology-agnostic infrastructure contractors.

By 2024, Power Mech had transformed from a power sector contractor to a diversified infrastructure services company. The power sector still mattered, but it no longer defined them. They'd successfully navigated the most challenging transition any company faces—evolving beyond their founding market without losing their core competencies.

Playbook: Business & Operating Lessons

The Working Capital Intensity Challenge

Infrastructure contracting is a cash-eating monster, and Power Mech's journey offers a masterclass in feeding the beast without getting devoured. The typical project cycle looks deceptively simple: win contract, execute work, submit bills, get paid. Reality is brutally different. You might execute work worth ₹100 crore in January, submit bills in March after client verification, get approval in May after multiple revisions, and receive payment in August—if you're lucky.

Meanwhile, you're paying salaries every month, equipment rentals weekly, and material suppliers demand advance payments or at best 30-day credit. The math is unforgiving: at any point, Power Mech has 4-6 months of revenues locked in receivables while funding operations from either retained earnings or expensive working capital loans.

The company's solution wasn't revolutionary but required discipline most competitors lacked. First, they negotiated milestone-based payments rather than time-based billing wherever possible. Second, they maintained a dedicated collections team that treated receivables like a military operation—daily follow-ups, escalation matrices, and CEO-level interventions when needed. Third, and most importantly, they walked away from contracts with poor payment terms, even if it meant slower growth.

Relationship Capital: The Invisible Moat

In Silicon Valley, network effects create winner-take-all dynamics. In Indian infrastructure, relationships play a similar role but operate differently. Power Mech understood that in B2B infrastructure, trust drives order wins more than price or even technical capabilities.

Consider how EPC contracts are actually awarded. Yes, there's a tender process with technical and financial bids. But before the tender is even floated, there are months of pre-bid discussions, site visits, and technical clarifications. The contractor who's worked with the client before, who understands their unstated preferences, who has senior executives on speed dial—that contractor has an insurmountable advantage.

Power Mech systematically built this relationship capital. When a project manager from NTPC moved to Adani Power, Power Mech's relationship moved with them. When a state electricity board engineer became a consultant, they became Power Mech's advocate in technical discussions. This wasn't corruption—it was the natural advantage of proven competence and familiarity.

The Vertical Integration Advantage

Most contractors specialize—civil contractors do civil work, mechanical contractors handle equipment installation. Power Mech's vertical integration across the project lifecycle created three distinct advantages that competitors struggled to replicate.

First, coordination becomes internal rather than contractual. When the civil team is running behind schedule, the mechanical team knows immediately and can adjust their mobilization accordingly. No blame games, no formal notices, no contractual disputes—just internal problem-solving.

Second, client value proposition improves dramatically. Plant owners hate managing multiple contractors. With Power Mech, they get a single point of accountability. If something goes wrong, there's no finger-pointing between civil and mechanical contractors—Power Mech owns the entire problem and solution.

Third, and least obvious, vertical integration creates information advantages. Being present across the project lifecycle means Power Mech knows about upcoming expansions before they're formally announced. The O&M team hears about maintenance challenges that will require capital expenditure. The civil team learns about new projects during foundation work. This information edge translates into better win rates on competitive bids.

Managing Concentration Risk

By 2015, Power Mech faced a classic dilemma—their largest clients contributed disproportionate revenues. NTPC alone could account for 30% of order book in some years. Conventional wisdom suggested diversification, but Power Mech took a contrarian approach.

Instead of spreading thin across many clients, they went deeper with core clients while gradually expanding the definition of "core." The logic was compelling: winning the first contract with a new client is expensive—extensive documentation, reference checks, trial projects. But the second contract is easier, the third almost automatic. Why not maximize share of wallet with existing clients?

The risk mitigation came not from client diversification but from service diversification. Even if NTPC was 30% of revenues, it might be spread across 10 different plants, 5 different service lines, with staggered contract periods. A problem at one plant or with one service wouldn't tank the entire relationship.

Execution Excellence as Competitive Moat

In infrastructure contracting, everyone claims execution excellence. Power Mech actually delivered it, and the difference created a moat competitors couldn't cross with capital or connections alone.

The secret wasn't revolutionary—detailed project planning, daily progress monitoring, proactive problem-solving. But the discipline of doing this every day, on every project, for decades, created institutional muscle memory. A Power Mech project manager could walk onto a site and immediately spot deviation from plan. Safety officers would shut down work for violations that others might overlook. Quality inspectors rejected work that was "good enough" but not perfect.

This execution discipline showed up in metrics that mattered to clients. On-time completion rates above 95% in an industry where 70% was considered good. Safety incidents below industry averages despite working in hazardous environments. First-time-right quality metrics that reduced rework and delays.

Building for Cycles

Infrastructure is cyclical—boom periods of massive capacity addition followed by lean years of overcapacity. Power Mech survived multiple cycles by building a business model that could flex without breaking.

During boom periods, they scaled using contract labor rather than permanent employees for execution roles. Project management and technical roles were permanent, but site labor could scale up 5x during busy periods and scale down during slowdowns. This meant higher costs during boom times but survival during downturns.

The O&M business provided ballast during volatile periods. When new project orders dried up, O&M contracts continued generating cash. This recurring revenue stream, though lower margin than construction, provided stability that pure-play contractors lacked.

Most importantly, they maintained a conservative balance sheet even during aggressive growth phases. When competitors leveraged up to chase growth, Power Mech maintained debt-to-equity ratios below 1x. This meant leaving money on the table during booms but having dry powder to acquire distressed assets or talent during downturns.

The playbook that emerges isn't about innovation or disruption—concepts that dominate modern business thinking. It's about execution, relationships, and financial discipline maintained over decades. In infrastructure contracting, boring is beautiful, and Power Mech made boring an art form.

Bear vs. Bull Case & Valuation Analysis

Bull Case: Riding India's Infrastructure Super-Cycle

The bull thesis for Power Mech starts with a simple observation: India needs to spend $1.4 trillion on infrastructure by 2030 to sustain GDP growth. This isn't speculation—it's mathematical necessity. With GDP targeting 7-8% growth and infrastructure typically needing to be 1.2x of GDP growth rate, the spending is inevitable. The question isn't whether this money will be spent, but who will capture the opportunity.

Power Mech's positioning couldn't be better. They've successfully diversified beyond power into railways, metros, mining, and water infrastructure—all sectors seeing massive government allocation. The MDO business alone represents enormous long-term value with 2 MDO contracts from Coal India (Kotre Basantpur Pachmo Open cast project of Rs 9,294 Cr for 25 years) and SAIL (Tasra Open cast project of Rs 30,483 Cr for 28 years). These aren't just contracts—they're 25+ year annuities that provide revenue visibility most contractors can only dream of.

The execution track record deserves premium valuation. In an industry where delays and cost overruns are endemic, Power Mech's consistent delivery creates a trust premium with clients. This shows up in negotiated contracts rather than just competitive bidding, better payment terms, and repeat orders. When NTPC needs something done urgently, they don't tender—they call Power Mech.

The O&M business provides a cushion most contractors lack. As the largest service provider in O&M space with backward and forward integration, Power Mech has built recurring revenues that smooth out project execution lumpiness. These contracts typically run 5-10 years with annual escalations, providing inflation protection and cash flow visibility.

Management quality and conservatism should comfort long-term investors. Kishore Babu has built this business over 25 years without major stumbles. No aggressive acquisitions, no unrelated diversification, no financial engineering. Just steady execution and gradual capability building. In a sector littered with corporate governance issues, Power Mech's clean track record is worth a premium.

The international opportunity remains largely untapped. Middle East countries are investing heavily in infrastructure, and Indian contractors have cost advantages over European competitors. Power Mech's existing presence provides a beachhead for expansion without the risks of greenfield international ventures.

Bear Case: Structural Headwinds and Execution Risks

The bear case starts with working capital intensity that won't go away. No matter how efficient Power Mech becomes, the infrastructure contracting model requires massive working capital. Government clients, their primary customers, are notoriously slow payers. As revenues grow, working capital needs grow proportionally, creating a permanent cash drain that limits return on equity.

Client concentration remains concerning despite diversification efforts. Government entities—whether NTPC, Coal India, or state utilities—still dominate the order book. These clients have monopsony power, squeezing margins during tender processes and delaying payments during fiscal constraints. One adverse government policy or budget cut could materially impact revenues.

The power sector's structural decline poses long-term challenges. While Power Mech has diversified, thermal power expertise remains their core competency. As India pivots to renewable energy, this expertise becomes less valuable. Solar and wind projects require different skills, have different economics, and face fierce competition from specialized renewable contractors.

Competition is intensifying from larger, better-capitalized players. L&T, with its massive balance sheet, can bid more aggressively and absorb working capital pressure better. Chinese contractors, despite political headwinds, offer compelling price points. Regional contractors are moving up the value chain. Power Mech's mid-size positioning—too big to be nimble, too small to dominate—could become a disadvantage.

Project execution risks are multiplying with scale and complexity. The MDO contracts, while lucrative, involve operational complexities Power Mech hasn't faced before. Mining is different from construction—environmental clearances, land acquisition, community relations add layers of risk. One major project failure could damage reputation and financial position significantly.

Technology disruption might seem distant but is approaching. Modular construction, automation, and project management software are changing how infrastructure is built. Companies that don't invest in technology risk being left behind. Power Mech's traditional approach, while successful historically, might become a liability.

ESG concerns are becoming material. Coal mining, thermal power—these aren't sectors ESG-focused funds want exposure to. As global capital increasingly screens for ESG compliance, Power Mech might face higher capital costs or reduced institutional interest despite strong fundamentals.

Valuation Considerations

At current levels around ₹3,100 per share, Power Mech trades at roughly 27x trailing earnings and 2.8x book value. This seems expensive for a construction company but might be justified for an infrastructure services platform with long-term contracted revenues.

The MDO contracts change the valuation math significantly. These aren't typical construction contracts but multi-decade operating agreements. If you value the MDO business like an infrastructure asset (using DCF with reasonable assumptions), and the traditional business on earnings multiple, the sum-of-parts suggests meaningful upside.

However, the market might be missing execution risks in these large contracts. The Tasra project alone is four times larger than Power Mech's market capitalisation, creating enormous operational leverage—both positive and negative.

Peer comparison is challenging because Power Mech's business mix is unique. Pure-play contractors trade at lower multiples but don't have O&M annuities. Mining services companies command higher multiples but don't have Power Mech's infrastructure diversification. Perhaps the best comparison is to infrastructure operators like IRB Infra, though Power Mech's asset-light model is fundamentally different.

For long-term investors, the key question isn't whether Power Mech is cheap or expensive today, but whether India's infrastructure build-out will continue for decades and whether Power Mech can maintain execution excellence while scaling. If both answers are yes, current valuation might prove conservative. If either falters, multiple compression could be severe.

Epilogue: The Next Chapter

The story of Power Mech Projects from 1999 to today—from a bootstrap contractor to a ₹9,800 crore market cap infrastructure platform—is remarkable enough. But what comes next might be even more interesting.

India stands at an infrastructure inflection point. The government's ₹111 lakh crore National Infrastructure Pipeline isn't just another announcement—it's an existential necessity for an economy aspiring to reach $5 trillion. Roads, railways, metros, water supply, sewage treatment, ports, airports—everything needs to be built or rebuilt. The opportunity is measured in decades, not years.

Power Mech's positioning for this super-cycle is intriguing. They're not the largest—L&T will win the marquee projects. They're not the most specialized—sector-specific players might have technical edges. But they might be the most adaptable, with proven ability to enter new sectors and scale capabilities. The MDO contracts provide multi-decade revenue visibility that funds expansion into new areas without dilution or excessive leverage.

The challenges ahead are real and mounting. Talent acquisition becomes harder as the industry scales—where do you find 10,000 more skilled workers? Technology adoption can't be delayed much longer; BIM, automation, and AI will reshape construction whether Power Mech is ready or not. Environmental and social governance isn't optional anymore; markets will punish companies that don't adapt.

If we were running Power Mech, three priorities would dominate. First, technology investment—not as IT spending but as fundamental transformation of project execution. Second, talent development at scale—internal universities, apprentice programs, whatever it takes to build human capital. Third, capital allocation discipline—the temptation to chase growth through aggressive bidding must be resisted.

What would success look like a decade from now? Not necessarily a ₹50,000 crore market cap, though that's possible if execution continues. Success would be Power Mech becoming to Indian infrastructure what Accenture became to IT services—not the biggest, but the most trusted executor of complex, mission-critical projects.

The biggest risk isn't competition or technology or even economic cycles. It's institutional sclerosis—the gradual loss of entrepreneurial energy that built the company. Can a ₹10,000 crore company maintain the hunger of a startup? Can professional managers preserve the founder's execution obsession? These soft factors, impossible to quantify, might matter more than order books or margins.

For investors evaluating Power Mech today, the framework shouldn't be traditional metrics alone. This is a bet on India's infrastructure transformation and Power Mech's ability to remain relevant through that transformation. The company that started maintaining gas turbines in 1999 is now operating coal mines and building metros. What will they be doing in 2035?

The answer to that question—more than any financial projection—will determine whether Power Mech becomes a multi-bagger or a value trap. The building blocks are in place: proven execution, strong relationships, diversified capabilities, and conservative management. Whether that's enough to navigate the next chapter remains an open question, but one worth watching closely.

Key Takeaways for Founders and Investors

For Founders: - Bootstrap as long as possible—Power Mech waited 10 years before raising institutional capital - Domain expertise beats general intelligence in B2B infrastructure - Reputation compounds faster than capital in trust-based industries - Vertical integration can create moats even in commoditized services - Patient capital (PE/public markets) should align with business cycles, not force them

For Investors: - In infrastructure, execution track record predicts future performance better than any metric - Working capital intensity is permanent; factor it into return expectations - Government client concentration is both risk and moat—evaluate carefully - Long-term contracts (like MDO) change valuation math—think like infrastructure investors - Management conservatism in cyclical industries is worth paying premium for

The Power Mech story ultimately isn't about an IPO that made early investors wealthy or a stock that multiplied 5x from listing. It's about building critical infrastructure for a developing nation while creating shareholder value—proof that in some businesses, slow and steady doesn't just finish the race but wins it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube