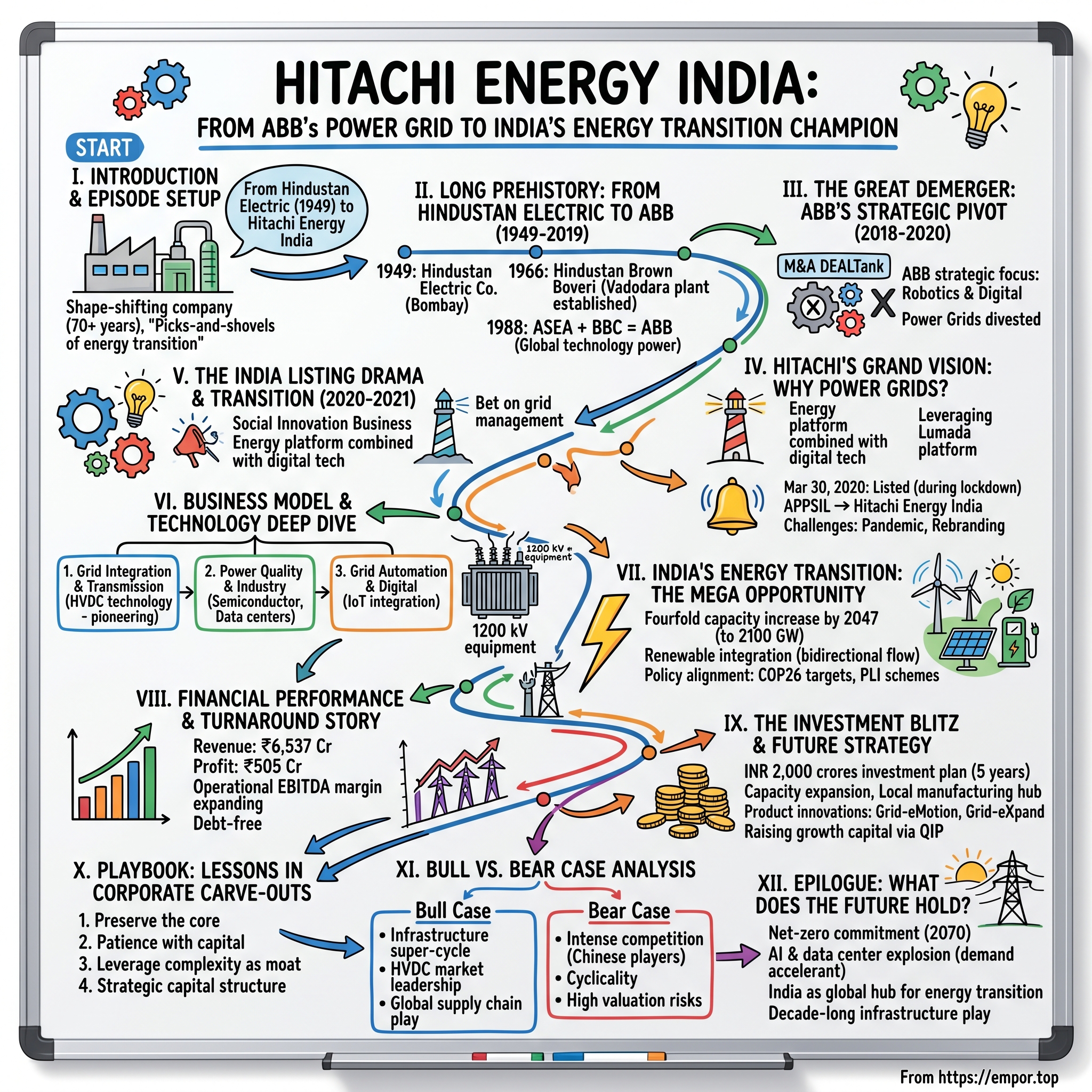

Hitachi Energy India: From ABB's Power Grid to India's Energy Transition Champion

I. Introduction & Episode Setup

Picture this: It's March 30, 2020. India has just entered its first nationwide COVID lockdown. Streets are empty, markets are in freefall, and the BSE Sensex has crashed 24% in a month. Amidst this chaos, a 71-year-old power equipment company quietly rings the opening bell at the National Stock Exchange. No fanfare, no celebration dinners, just a Zoom call and digital signatures. This was the unceremonious birth of ABB Power Products and Systems India Limited—a company that would, within four years, transform into Hitachi Energy India and deliver returns that would make even the most aggressive growth investors take notice.

Today, Hitachi Energy India commands a market capitalization of ₹90,460 crore, up an astounding 84.3% in just the past year. But this isn't just another pandemic success story or a simple tale of market timing. This is the story of how a company that started installing transformers in newly independent India became the backbone of the nation's $5 trillion economy ambitions—and how a Japanese industrial giant saw an opportunity that others missed.

The protagonist of our story isn't just one company, but a shape-shifting entity that has worn many corporate identities over seven decades: from Hindustan Electric Company to Brown Boveri, from ABB to Hitachi Energy. Each transformation reflects not just corporate maneuvering but fundamental shifts in global power dynamics, technological evolution, and India's own journey from a protected economy to an infrastructure powerhouse.

What makes this story particularly fascinating is the timing. Just as the world pivots toward renewable energy and electric mobility, just as India announces plans to add power grid capacity equivalent to the entire European Union by 2040, and just as artificial intelligence drives unprecedented electricity demand—this company finds itself at the intersection of every major energy trend. It's the kind of positioning that makes you wonder: was this brilliant strategy or beautiful serendipity?

The questions we'll explore go beyond the usual corporate biography. How does a company maintain technological leadership through multiple ownership changes? What happens when Swiss precision engineering meets Japanese kaizen philosophy in the chaos of Indian infrastructure projects? And perhaps most intriguingly: why would ABB, one of the world's most successful industrial conglomerates, sell off what many considered its crown jewel—and why would Hitachi pay $6.4 billion for it during a global trade war?

This is also a story about the unsexy becoming essential. Power transformers and switchgear don't capture headlines like electric vehicles or solar panels. Yet without them, the entire energy transition falls apart. It's the picks-and-shovels thesis for the 21st century: while everyone focuses on generating clean energy, someone needs to move that energy from where it's produced to where it's consumed. And in India, increasingly, that someone is Hitachi Energy.

So what for investors: The company's current valuation reflects both its monopolistic positioning in critical infrastructure and the massive capital expenditure cycle ahead. But understanding whether this is the beginning or the peak requires diving deep into seven decades of history, multiple corporate transformations, and the complex dynamics of India's energy transition.

II. The Long Prehistory: From Hindustan Electric to ABB (1949-2019)

The year was 1949. India had been independent for exactly two years. Jawaharlal Nehru stood before the Constituent Assembly speaking of "temples of modern India"—his poetic term for dams, steel plants, and power stations. In this atmosphere of nation-building fervor, a small electrical equipment company called Hindustan Electric Company began operations in Bombay, importing and installing power equipment for a country that had barely 1,362 MW of installed power capacity for 350 million people.

The company's early engineers—many trained in pre-war Europe—worked by lamplight in makeshift offices, calculating transmission line specifications on slide rules. Their first major project was helping electrify the Bhakra Nangal Dam, Nehru's favorite temple. The Swiss connection came early: Brown Boveri & Company, founded in Baden, Switzerland in 1891, saw opportunity in India's industrialization dreams and partnered with local entrepreneurs to form Hindustan Brown Boveri in 1966.The transformation from Hindustan Electric Company to Hindustan Brown Boveri Ltd. represented more than a name change—it was India's attempt to leapfrog technological generations through foreign collaboration. The License Raj era, with its Byzantine permit system and import restrictions, created a peculiar dynamic: foreign companies needed Indian partners to navigate the bureaucracy, while Indian companies needed foreign technology to build modern infrastructure. In 1962, the company established its first manufacturing facility in Vadodara, Gujarat—a decision that would prove prescient. The Maneja production facility rolled out its first product: a 25 kV circuit breaker for Indian Railways. Fifty years later, from the same location, they would produce 1200 kV equipment—the voltage level had increased fifty-fold, a perfect metaphor for India's industrial journey.

The real transformation came in 1988 with one of the most significant mergers in industrial history. ASEA of Sweden and Brown, Boveri & Cie of Switzerland merged to create ABB, with the new company headquartered in Zurich, employing 160,000 people worldwide and generating revenues of approximately $15-17 billion. For the Indian operations, this meant access to a global technology powerhouse and integration into supply chains that spanned continents.

What followed was three decades of steady expansion punctuated by the peculiar rhythms of Indian infrastructure development. During the 1991 liberalization, ABB India (as it was now known) positioned itself perfectly: foreign enough to bring world-class technology, Indian enough to navigate local complexities. The company built transformers for the Delhi Metro, switchgear for IT parks in Bangalore, and transmission equipment for steel plants in Jharkhand.

By 2019, ABB India had become a ₹12,000 crore revenue giant with 40+ locations across the country. But beneath this success lay a strategic tension. ABB's global leadership was increasingly focused on digital industries, robotics, and automation—sexy, high-margin businesses with software-like economics. Power grids, despite being ABB's historical core and technological forte, were capital-intensive, cyclical, and increasingly commoditized. The stage was set for one of the most complex corporate divorces in Indian corporate history.

So what for investors: The 70-year prehistory reveals a crucial insight: this business has survived and thrived through multiple ownership changes, economic cycles, and technological disruptions. The institutional knowledge embedded in facilities like Vadodara—where three generations of engineers have worked on progressively complex projects—creates a moat that's nearly impossible to replicate, regardless of who owns the equity.

III. The Great Demerger: ABB's Strategic Pivot (2018-2020)

On December 17, 2018, Ulrich Spiesshofer, ABB's CEO, stood before analysts in Zurich with an announcement that shocked the industrial world: ABB would sell 80.1% of its Power Grids division to Hitachi for $11 billion enterprise value. The cash consideration of $6.4 billion represented one of the largest industrial M&A deals of the decade. For a company whose very identity was built on power infrastructure, this was like Apple selling the iPhone business. The strategic rationale was compelling from ABB's perspective. ABB intended to focus on key market trends including the electrification of transport and industry, automated manufacturing, digital solutions, and increased sustainable productivity. Power grids, despite generating solid revenues, had the lowest profit margin of 9.8% among ABB's four units. For CEO Spiesshofer, who had resisted activist investor Cevian Capital's calls to divest the unit since 2016, the improved performance of the business finally created the right moment to sell. For the Indian operations, the demerger was a Herculean task. ABB India's board approved the demerger of company's power grids business to ABB Power Products and Systems India Ltd (APPSIL), with minority shareholders issued one share of APPSIL for every five shares held in ABB India. The power grids business accounted for 38.4% of ABB India's total turnover, representing ₹4,172 crore in FY2018.

The complexity lay not just in the numbers but in the operational surgery required. Imagine separating conjoined twins who had shared organs for decades—that's what splitting Power Grids from ABB India felt like. Shared factories had to be divided, employees reassigned, IT systems untangled, and decades of integrated supply chains restructured. All this while maintaining operations for critical infrastructure that couldn't afford even a day's disruption.

The Indian arm formally announced its listing on March 30, 2020, as ABB Power Products and Systems India Limited, with the divestment of ABB's Power Grids global business to Hitachi on track for completion by the end of Q2 2020. The timing couldn't have been more dramatic—or worse, depending on your perspective.

The negotiation dynamics between ABB and Hitachi revealed fascinating cultural and strategic differences. ABB, under pressure from activist investors and focused on capital-light businesses, wanted a clean exit with maximum value realization. Hitachi, led by CEO Toshiaki Higashihara, saw a once-in-a-generation opportunity to leapfrog into global energy infrastructure leadership. The resulting structure—Hitachi taking 80.1% initially with an option to acquire ABB's remaining 19.9% after three years—reflected both parties' needs: ABB got immediate cash while retaining some upside, and Hitachi got control with a pathway to full ownership.

So what for investors: The demerger created a pure-play power infrastructure company at precisely the moment when such assets were being undervalued by markets obsessed with software and digital transformation. For contrarian investors, this represented a classic case of buying productive assets when financial engineering obscures fundamental value.

IV. Hitachi's Grand Vision: Why Power Grids? (2018-2020)

Toshiaki Higashihara wasn't supposed to be a visionary. When he became Hitachi's CEO in 2016, the soft-spoken engineer was seen as a safe pair of hands to continue his predecessor's restructuring efforts. But Higashihara harbored grander ambitions. He envisioned Hitachi not as a sprawling conglomerate but as a focused "Social Innovation Business"—corporate speak that actually meant something profound: using digital technology to solve humanity's biggest infrastructure challenges. In his keynote speeches, Higashihara talked about the evolution of Hitachi's Social Innovation Business, which utilizes digital technologies, and about Sustainable Development Goals (SDGs) and the realization of Society 5.0. The Power Grids acquisition was the centerpiece of this vision. As Higashihara explained: "Today's agreement between ABB and Hitachi is a significant turning point in the global power and energy markets at a time when digital technology is fundamentally changing our society and the pattern of energy demand and supply is diversifying. Hitachi will combine ABB's strengths in the power grids business with our digital technology to build an energy platform that contributes to innovating the energy business."

The strategic rationale went deeper than press release platitudes. Hitachi's internal analysis revealed that the global power transmission and distribution market would grow to $100 billion by 2020. More critically, they saw that the future of energy wasn't just about generation—solar panels and wind turbines were becoming commoditized. The real value would be in managing the complexity of a distributed, digitalized, bidirectional grid where electric vehicles could feed power back, where AI would balance supply and demand in real-time, and where renewable intermittency required sophisticated grid management.

Hitachi's Lumada platform—their IoT and data analytics solution—needed real-world applications to prove its value. What better proving ground than managing 30% of the world's power grids? The combination of ABB's operational technology with Hitachi's digital capabilities created possibilities that neither company could achieve alone: predictive maintenance algorithms trained on millions of transformers, AI-optimized power flow management, and digital twins of entire national grids.

The cultural integration challenge was real but surmountable. Swiss-Swedish ABB Power Grids represented European engineering excellence—methodical, process-driven, conservative. Hitachi brought Japanese manufacturing philosophy—continuous improvement, consensus-building, long-term thinking. The initial months saw friction: ABB managers frustrated by Japanese decision-making speed, Hitachi executives puzzled by European work-life boundaries. But gradually, a hybrid culture emerged. The Swiss brought precision to Hitachi's digital ambitions; the Japanese brought patience to ABB's quarterly pressures.

Initial market skepticism was understandable. Cevian Capital AB, which had become one of ABB's largest shareholders and had pushed for the breakup, applauded the move. But many analysts questioned whether Hitachi, traditionally focused on Japan and Asia, could manage a global power grids business. The $6.4 billion price tag seemed steep for a business with sub-10% margins. Rating agencies worried about integration risks and the capital intensity of the power equipment sector.

Yet Higashihara's vision extended beyond financial metrics. Hitachi was engaged in the Social Innovation Business that uses digital technology to upgrade social infrastructure systems, such as railroads and power transmission and distribution systems, to improve the quality of life. This wasn't just M&A; it was a bet on the future architecture of human civilization.

So what for investors: Hitachi's acquisition thesis rested on a profound insight: in an electrifying world, the company that controls the nervous system of the energy transition—the grids—holds asymmetric power. The initial skepticism reflected short-term thinking; Hitachi was playing a decades-long game where network effects and switching costs would create an impregnable moat.

V. The India Listing Drama & Transition (2020-2021)

March 30, 2020. As ABB Power Products and Systems India Limited rang the opening bell at the NSE, Mumbai was a ghost town. The Indian arm of ABB's Power Grids business formally announced its listing on the BSE Limited and the National Stock Exchange of India Limited as ABB Power Products and Systems India Limited. No photographers, no champagne, no handshakes—just executives in masks maintaining social distance while the country grappled with the world's strictest lockdown.

The timing seemed catastrophic. The Sensex had crashed 40% from its peak. Foreign institutional investors were fleeing emerging markets. Industrial activity had ground to a halt. Power demand had collapsed as factories shuttered. Yet here was a capital-intensive infrastructure company making its debut in perhaps the worst possible market conditions since 2008.

Behind the scenes, the transition team had been working around the clock since December 2019 when the demerger became effective. The pandemic added layers of complexity nobody had anticipated. Factory workers couldn't report to sites. Engineers couldn't travel for equipment installation. Japanese executives from Hitachi couldn't fly to India for integration meetings. Everything had to be managed virtually—from IT system migrations to employee town halls to customer relationship transfers.

The divestment of ABB's Power Grids global business to Japan's Hitachi was on track with completion targeted for the end of the second quarter 2020. Despite the pandemic chaos, the global transaction proceeded on schedule. By July 1, 2020, Hitachi ABB Power Grids was officially born as a joint venture, with Hitachi holding 80.1% and ABB retaining 19.9%.

The Indian entity faced unique challenges. Unlike other markets where the transition was primarily a rebranding exercise, India required a complete corporate restructuring. Thousands of employees had to be transferred from ABB India's payroll to the new entity. Contracts with Indian Railways, Power Grid Corporation, and state electricity boards—some dating back decades—needed to be novated. GST registrations, import-export licenses, and environmental clearances all required updates. The final piece of the transformation puzzle fell into place in October 2021 when ABB Power Products & Systems India announced its rebranding as Hitachi Energy India Limited, following the rebranding of its parent company to Hitachi Energy. Meanwhile, globally, on December 22, Hitachi Ltd acquired full ownership of the company by purchasing the remaining 19.9% stake, completing the transition from joint venture to wholly-owned subsidiary.

The rebranding wasn't just cosmetic. It signaled a fundamental shift in identity and ambition. N Venu, Managing Director and CEO of Hitachi Energy India, emphasized the company's six-decade heritage while pointing to the future: "About 80 percent of our products are manufactured locally and we are the single-point source for Hitachi Energy's global supply of certain products". The company was no longer just serving India; it was becoming a global manufacturing hub within Hitachi's network.

The pandemic, paradoxically, accelerated certain aspects of the transition. Virtual meetings eliminated travel time, allowing for more frequent coordination between teams in Tokyo, Zurich, and Bengaluru. The crisis created urgency that cut through bureaucratic delays. Customers, desperate to maintain critical infrastructure during lockdowns, became more collaborative and flexible about contract modifications.

By the time the dust settled in late 2021, Hitachi Energy India had emerged as a different entity than what anyone had envisioned in December 2018. The company had not just survived a demerger, a global acquisition, a pandemic, and a rebranding—it had somehow thrived through them all. The stock, which had listed at ₹1,400 in March 2020, was already trading above ₹2,000 by year-end, validating the market's growing confidence in the transformation.

So what for investors: The pandemic listing, initially seen as disastrous timing, actually provided a low base that amplified subsequent returns. More importantly, the crisis-forged integration created operational resilience and management depth that would prove invaluable as India's infrastructure spending accelerated post-COVID. Sometimes the worst time to list becomes the best time to buy.

VI. Business Model & Technology Deep Dive

Walk into Hitachi Energy's testing facility in Maneja, Vadodara, and you encounter a cathedral of electricity. A 2,400 kV test bay—one of only three in the world—subjects transformers to artificial lightning strikes. The thunderous crack of each test discharge contains more energy than a small town uses in a day. This isn't just engineering; it's controlling the fundamental forces of nature at industrial scale.

After starting operations in 1949, Hitachi Energy established its first factory in Vadodara in 1962, and today has over 7,500 employees across 19 factories in eight manufacturing locations. But the scale tells only part of the story. The real competitive advantage lies in the accumulated tacit knowledge—the kind you can't download from a technical manual or reverse-engineer from a product teardown.

Consider the manufacturing process for a 1200 kV transformer. The copper windings alone contain enough metal to build 50 cars. But it's not about the copper—it's about winding it with micrometer precision while accounting for electromagnetic forces that would rip apart a poorly designed structure. Each transformer is essentially custom-built, with design modifications for altitude, ambient temperature, seismic activity, and grid harmonics at the installation site. This isn't manufacturing; it's industrial craftsmanship at massive scale.

The company serves utility and industry customers, with a complete range of engineering, products, solutions, and services in areas of Power technology. The portfolio breaks down into several critical segments:

Grid Integration & Transmission: This is where Hitachi Energy's HVDC (High Voltage Direct Current) technology shines. The company has the distinction of pioneering this technology and today more than half the HVDC links in India are leveraging this innovative solution. HVDC is to electricity transmission what fiber optics was to telecommunications—a fundamental technology shift that enables previously impossible applications. You can transmit power over thousands of kilometers with minimal losses, connect asynchronous grids, and even lay cables underwater.

Power Quality & Industry Applications: Beyond transmission, the company provides specialized equipment for industries where power quality isn't just important—it's existential. A semiconductor fab can lose millions from a microsecond voltage dip. A data center needs power reliability measured in "nines"—99.999% uptime means less than 5 minutes of downtime per year. Hitachi Energy's solutions for these segments command premium pricing because the cost of failure dwarfs the equipment cost.

Grid Automation & Digital Solutions: This is where the Hitachi acquisition thesis becomes tangible. By integrating ABB's operational technology with Hitachi's Lumada IoT platform, the company can offer predictive maintenance for transformers, real-time grid optimization, and cybersecurity solutions for critical infrastructure. A transformer equipped with sensors and analytics can predict its own failure weeks in advance—transforming a catastrophic outage into scheduled maintenance.

The moat in power grid equipment is deeper than most realize. First, there's the capital intensity—a transformer factory requires hundreds of crores in equipment and years to reach optimal efficiency. Second, there's the trust factor—utilities don't experiment with critical infrastructure. If you've supplied reliable transformers for 50 years, you're not getting displaced by a startup with 10% lower prices. Third, there's the ecosystem lock-in—spare parts, maintenance protocols, and technical standards create switching costs that make enterprise software look fluid by comparison.

But perhaps the most underappreciated moat is regulatory certification. Each market has unique technical standards, testing requirements, and certification processes. A transformer designed for the European grid can't simply be shipped to India—it needs redesign for Indian conditions, testing by Indian authorities, and type certification that can take years. This isn't protectionism; it's physics. India's grid frequency, voltage levels, and environmental conditions create genuine technical requirements that favor local manufacturing and deep local expertise.

The company's manufacturing footprint reflects this reality. The Vadodara complex alone spans 55 acres, with separate facilities for power transformers, distribution transformers, and components. But modern manufacturing here looks nothing like the factory floors of the 1960s. Robots handle the heavy lifting, lasers cut steel with millimeter precision, and digital twins simulate electromagnetic fields before physical production begins. Yet skilled technicians still hand-wrap insulation on transformer cores—some tasks remain irreducibly human.

Recent order wins illustrate the business model's evolution. The company won a major order from Adani Mumbai Electric Infrastructure to provide an HVDC transmission system linking Kudus to Mumbai—an 80-kilometer, 1,000 MW link that will increase the city's power supply by almost 50% with minimal losses. This isn't just selling equipment; it's providing a complete solution including design, installation, commissioning, and decades of maintenance. The switching costs after such an installation are astronomical.

So what for investors: The business model combines the recurring revenues of industrial services with the pricing power of critical infrastructure. While gross margins appear modest compared to software companies, the return on incremental capital is exceptional once the fixed cost base is established. This is a toll road for electrons—boring, essential, and extraordinarily profitable at scale.

VII. India's Energy Transition: The Mega Opportunity

The numbers are staggering enough to induce vertigo. By 2047, India anticipates power demand to reach 708 gigawatts. To meet this, the country needs to increase capacity by four times, to 2,100 gigawatts. To put this in perspective, that's adding the equivalent of the entire current U.S. power generation capacity—twice over. As per International Energy Agency (IEA), to continue its energy transition journey, India needs to add a grid the size of the European Union by 2040.

This isn't speculative futurism—it's already happening. The Indian national electric grid has an installed capacity of 467.885 GW as of 31 March 2025. Renewable energy plants, which also include large hydroelectric power plants, constitute 46.3% of the total installed capacity. India's electricity demand is set to exceed 700 GW by 2047, 2.5 times the current levels. To meet this voluminous requirement, and its 2030 targets, the country needs to scale up its renewable capacity beyond 50 GW annually.

The transformation isn't just about adding capacity—it's about reimagining the entire architecture of the power system. Traditional grids were designed for one-way power flow: from large central plants to distributed consumers. The new grid must handle bidirectional flows, with rooftop solar feeding back into the system, electric vehicles acting as mobile batteries, and industrial consumers becoming prosumers. This complexity creates unprecedented demand for sophisticated grid equipment and management systems.

Government policies have aligned to create a perfect storm of opportunity. The Production Linked Incentive (PLI) schemes for solar manufacturing and advanced chemistry cell batteries, the National Infrastructure Pipeline with ₹111 lakh crore allocated for infrastructure, and aggressive renewable energy targets have created clear market signals. The targets announced at COP26 include reaching 500 GW non-fossil energy capacity by 2030; fulfilling 50% of its energy requirements through renewable energy by 2030; reducing total projected carbon emissions by one billion tons from now to 2030.

The competition landscape reveals Hitachi Energy's strategic positioning. L&T, the domestic engineering giant, competes aggressively in EPC but lacks the technology depth in HVDC. Siemens Energy, post its own spin-off drama, faces its own integration challenges. GE's power business has been in perpetual restructuring mode. Chinese players like TBEA and XD Group offer price competition but face trust deficits in critical infrastructure. This leaves Hitachi Energy in a sweet spot—technology leader with local manufacturing, global backing with Indian roots.

The renewable energy boom has specific implications for grid equipment. Battery storage is particularly well suited to the short-run flexibility that India needs to align its solar-led generation peak in the middle of the day with the country's early evening peak in demand. By 2040, India has 140 GW of battery capacity in the STEPS, the largest of any country. Each battery installation requires sophisticated power conversion equipment, grid integration systems, and control software—all areas where Hitachi Energy has deep capabilities.

The data center explosion adds another dimension. The IEA's analysis found that the increase in consumption is mainly driven by growing energy use for industrial production, increased demand for air conditioning, accelerating electrification led by the transport sector, and the rapid expansion of data centers. A single large data center can consume as much power as a small city, but with zero tolerance for outages. This creates demand for ultra-reliable power systems, often with multiple redundancies—exactly the kind of high-margin, sophisticated equipment that Hitachi Energy specializes in.

The electrification of transport presents yet another growth vector. India's ambitious electric vehicle targets mean not just charging stations but grid reinforcement to handle the load. A highway fast-charging station can draw as much power as a small factory. Multiply this across thousands of locations, and you need massive grid upgrades—new transformers, switchgear, and control systems.

So what for investors: The energy transition isn't optional for India—it's existential. With electricity demand growing at 6%+ annually and renewable capacity additions accelerating, the companies that enable this transition hold asymmetric value. Hitachi Energy sits at the intersection of every major trend: renewable integration, grid modernization, industrial electrification, and energy storage. The next decade will see more investment in India's power infrastructure than the previous seven combined.

VIII. Financial Performance & Turnaround Story

The numbers tell a story of transformation that would make any turnaround specialist jealous. Revenue: ₹6,537 Cr, Profit: ₹505 Cr—but these headline figures mask the dramatic journey underneath. When the company listed in March 2020, it was bleeding cash, laden with legacy contracts, and facing an uncertain future. Today, it stands debt-free with record order backlogs and margins expanding quarter after quarter. The recent third quarter results tell the story best. At the close of December 31, 2024, the Company recorded its highest-ever order backlog of INR 18,994.4 crore, providing revenue visibility for the coming quarters. Revenue was up 31% YoY at INR 1672.4 crore in the October-December 2024 quarter. But the real story is in the margin expansion: Operational EBITDA jumped 108.5% YoY to ₹168.9 crore, with margins expanding from 6.3% to 10.1%.

The transformation began with operational discipline. Legacy contracts from the ABB era—signed when market dynamics were different—had to be executed even if unprofitable. Management took the hit upfront, clearing these albatrosses while simultaneously renegotiating payment terms on new contracts. The focus on collections bore fruit: the company becoming debt-free as of December 31, 2024, a remarkable achievement for a capital-intensive business.

For the full year ending March 31, 2024, orders were at INR 5536.3 crores up 14% (excl HVDC) from the corresponding last twelve months, while revenue stood at INR 5246.8 crores with a 17% increase. These aren't just growth numbers—they represent a fundamental shift in business mix toward higher-margin segments.

The export story deserves special attention. The share of exports grew to over 40% of total orders in Q3FY25. This isn't low-value commodity exports but sophisticated equipment to markets like Australia, Indonesia, Canada, Croatia, and Azerbaijan. When an Australian utility trusts you with critical infrastructure, it validates your global competitiveness. The export pricing is typically 20-30% higher than domestic sales, directly flowing to the bottom line.

The margin improvement journey reveals sophisticated execution. First, product mix optimization—moving from standard transformers to specialized equipment for data centers and renewable integration. Second, operational efficiency gains through digitalization and automation at manufacturing facilities. Third, pricing discipline—walking away from low-margin orders even if it meant lower revenues in the short term. Fourth, aftermarket services expansion—service contracts now constitute 11% of orders, with 40%+ gross margins.

The working capital management transformation is particularly impressive. In the power equipment business, it's common to have 150+ days of working capital cycle. Hitachi Energy has brought this down to under 100 days through better inventory management, faster collections, and negotiating advance payments on large orders. The HVDC project advances have created a war chest for growth without diluting equity or taking debt.

The order book composition reveals the strategic positioning. The surge in orders was significantly influenced by large HVDC projects—one to transmit renewable energy from Khavda in Gujarat to Nagpur in Maharashtra, another from Bhadla III in Rajasthan to Fatehpur in Uttar Pradesh. These aren't just orders; they're decade-long relationships with assured revenues and high switching costs.

So what for investors: The financial turnaround from listing disaster to debt-free profitability in four years demonstrates exceptional execution. More importantly, the record order backlog of nearly ₹19,000 crore—equivalent to 3+ years of current revenue—provides unprecedented earnings visibility. With margins expanding, debt eliminated, and exports growing, the company has transformed from a turnaround story to a compounding machine.

IX. The Investment Blitz & Future Strategy

The October 2024 announcement sent shockwaves through the market: Hitachi Energy plans to invest around $250 million USD (INR 2,000 crores) in its operations in India over the next five years. This wasn't just maintenance capex—it was a statement of intent. The investment is part of the company's larger $6 billion USD investment plans in manufacturing, engineering, digital, R&D, and partnerships across all major markets globally.

The investment breakdown reveals strategic priorities. Key highlights of the investments include a significant capacity expansion of the large power transformers factory, upgraded testing capabilities for specialty transformers, and the relocation of the bushings factory. But the real story is in the new product introductions that these investments enable.

Grid-eMotion for EV charging: This isn't just another charging solution—it's a complete grid-to-vehicle ecosystem. The technology enables ultra-fast charging (350kW+) while managing grid stability. With India targeting 30% EV penetration by 2030, every highway, every mall, every office complex will need this infrastructure. Hitachi Energy isn't selling chargers; it's selling the backbone of electric mobility.

Grid-eXpand portfolio: As renewable energy creates grid instability (solar generates during day, wind is intermittent), Grid-eXpand provides modular solutions for grid reinforcement. Think of it as plug-and-play infrastructure—instead of building new substations taking years, you can add capacity in months. The product launches targeted at the 100+ GW annual renewable additions expected by 2030.

Variable Shunt Reactors: The company received orders for the first made-in-India Variable Shunt Reactor—a critical component for managing reactive power in long-distance transmission. This localization reduces import dependency and positions India as a manufacturing hub for sophisticated grid equipment globally.

The digital transformation deserves special attention. Plans are underway to expand the network control solutions offering and develop and manufacture localized Grid eXpand and Grid eMotion. Additionally, the company will introduce its maiden medium voltage offering—REF650—to the Indian market. This isn't just adding products; it's building an ecosystem where physical equipment and digital intelligence converge.

The global supply chain play is perhaps most underappreciated. Furthermore, concerted efforts will be made to nurture the supplier base in India for India and the world. India is becoming Hitachi Energy's global manufacturing hub for certain products. When a transformer made in Vadodara gets installed in a European wind farm or an African mining operation, it validates India's manufacturing prowess and creates a virtuous cycle of investment and capability building.

The capital raise strategy shows financial sophistication. To support its investment plan in India, the Company initiated a Qualified Institutional Placement (QIP) and raised INR 2,520.82 crores. Rather than relying on debt or internal accruals alone, the company tapped equity markets at peak valuations, minimizing dilution while maximizing growth capital. The timing—when the stock was near all-time highs—shows management's capital allocation acumen.

The investments in traction transformers for Indian Railways reveal another growth vector. The capacity of the traction transformers factory will also be boosted to support the modernization of the Indian railway network. With India planning high-speed rail corridors and electrifying its entire rail network, traction transformers become a multi-decade growth opportunity. The company partnered with Indian Railways to indigenously develop Scott Transformers that will be central to powering high-speed rail.

So what for investors: The ₹2,000 crore investment program, funded through equity rather than debt, positions the company for the next leg of growth without compromising balance sheet strength. More importantly, the focus on localization and new product development creates optionality—each new product line is a call option on emerging infrastructure trends. With the parent committing $6 billion globally and India being a top-5 market, expect continued capital allocation that drives both growth and returns.

X. Playbook: Lessons in Corporate Carve-outs

The Hitachi Energy story offers a masterclass in executing complex corporate separations. Most carve-outs fail—cultural clashes, IT system disasters, customer defections, key talent exodus. Yet here, a 70-year-old business was successfully separated, rebranded twice, and integrated into a Japanese conglomerate, all while delivering record financial performance. How?

Lesson 1: Timing is Everything (Even When It Seems Wrong) The March 2020 listing during COVID lockdown seemed like disaster. Yet it created unique advantages. Employees, unable to job-hop during lockdown, stayed put. Customers, desperate to maintain critical infrastructure, remained loyal. Competitors, distracted by their own crisis management, couldn't poach contracts. Sometimes the worst time becomes the best time if you can survive the storm.

Lesson 2: Preserve the Core While Changing Everything Else Hitachi understood something profound: the value wasn't in the ABB brand or systems—it was in the accumulated engineering knowledge and customer relationships. They kept the entire technical team, maintained the Vadodara manufacturing excellence, and retained customer-facing personnel. But they changed everything else—IT systems, financial processes, corporate structure. It's like renovating a house while keeping the foundation intact.

Lesson 3: Use Complexity as a Moat The demerger created enormous complexity—thousands of contracts to renegotiate, hundreds of regulatory approvals, IT systems to separate. Most companies would see this as a burden. Hitachi Energy used it as an opportunity. Each successfully renegotiated contract strengthened relationships. Each regulatory approval created barriers for competitors. Complexity, managed well, becomes competitive advantage.

Lesson 4: The Power of Patient Capital Hitachi could have pushed for immediate synergies, forced integration, demanded quick returns. Instead, they took a five-year view. They allowed the Indian management to run operations while providing technology and capital support. This patience paid off—margins expanded gradually but sustainably, orders grew without compromising pricing discipline.

Lesson 5: Build New Identity While Honoring Legacy The journey from ABB Power to Hitachi Energy wasn't just a rebranding—it was identity reconstruction. The company acknowledged its 75-year heritage (from Hindustan Electric to Hindustan Brown Boveri, ABB Power Grids, Hitachi ABB Power Grids, and now Hitachi Energy) while articulating a new vision. Employees could take pride in their history while embracing the future.

Lesson 6: Capital Structure as Strategic Weapon The journey to becoming debt-free wasn't just about financial metrics. It was about strategic flexibility. With no debt, the company could take larger projects, offer better payment terms, and invest counter-cyclically. The recent QIP raise at peak valuations shows sophisticated capital management—raising equity when expensive, deploying when opportunities arise.

Lesson 7: Managing Multiple Stakeholders Through Transition The company had to manage: ABB (the seller wanting maximum value), Hitachi (the buyer wanting smooth integration), employees (worried about job security), customers (concerned about service continuity), investors (skeptical about the complex structure), and regulators (ensuring compliance). They did this through radical transparency—regular communication, clear timelines, and most importantly, consistent execution that built trust.

Lesson 8: Turn Regulatory Requirements into Business Advantages The demerger required numerous regulatory approvals—SEBI for listing, CCI for competition clearance, RBI for foreign investment. Rather than seeing these as hurdles, the company used each approval as validation. "SEBI-approved" and "CCI-cleared" became trust signals for customers and investors.

So what for investors: Corporate carve-outs typically destroy value through execution risk, talent loss, and customer defection. Hitachi Energy's successful navigation shows that with patient capital, cultural sensitivity, and operational excellence, carve-outs can create tremendous value. The playbook here—preserve the core, be patient with integration, use complexity as advantage—applies to any investor evaluating separation situations.

XI. Bull vs. Bear Case Analysis

Bull Case: The Infrastructure Super-Cycle Thesis

The bull case rests on immutable physics and economics. India's electricity demand growing at 6%+ annually isn't a projection—it's thermodynamics. Every air conditioner installed, every electric vehicle charged, every data center built increases baseload demand. The grid must expand or the economy stops. There's no alternative.

The infrastructure buildout ahead is unprecedented. Adding 700 GW by 2047 means installing Germany's entire power capacity every two years. The renewable transition adds complexity—managing intermittent supply requires sophisticated equipment that only a handful of companies globally can provide. Hitachi Energy's 50%+ share in Indian HVDC projects creates path dependency—once you're embedded in critical infrastructure, switching costs become prohibitive.

Technology leadership in HVDC isn't just about market share—it's about setting standards. When Hitachi Energy designs a transmission system, it defines specifications that become industry norms. Competitors must ensure compatibility, effectively following Hitachi's lead. This standard-setting power is vastly underappreciated by markets focused on quarterly earnings.

The parent backing from Hitachi provides patient capital and technology transfer that standalone competitors can't match. Hitachi's $6 billion global investment program ensures continuous R&D flow. The Lumada platform integration creates digital moats that pure-play equipment manufacturers can't replicate.

Improving margins tell the real story. Operational EBITDA margins expanding from 6.3% to 10.1% in a year isn't just operational efficiency—it's pricing power manifesting. As customers realize the criticality of reliable grid equipment, price becomes secondary to performance. A transformer failure can black out a city; a penny saved on procurement can cost millions in outages.

The debt-free status in a capital-intensive industry is like bringing a gun to a knife fight. Competitors struggling with working capital can't match payment terms. The recent QIP raise of ₹2,520 crore at peak valuations provides war chest for growth without dilution concerns.

Export growth to 40% of orders demonstrates global competitiveness. When Australian utilities—operating in one of the world's most stringent regulatory environments—buy from India, it validates manufacturing quality. These aren't price-driven commodity exports but sophisticated equipment where India combines engineering capability with cost advantage.

Bear Case: The Cyclicality and Competition Concerns

The bear case starts with mean reversion. Company has a low return on equity of 12.2% over last 3 years. In capital-intensive industries, returns above cost of capital attract competition. Chinese manufacturers, backed by state capital, could dump products to gain market share. The technology moat in power equipment isn't as deep as in semiconductors or software—reverse engineering is possible.

Government procurement dependency creates political risk. Most orders come from state utilities or government infrastructure projects. Payment delays, project cancellations, and policy changes can disrupt cash flows. The recent Tamil Nadu government's decision to renegotiate power purchase agreements shows political risk is real.

Competition from Chinese players is intensifying. Companies like TBEA and XD Group offer 20-30% lower prices. While quality and service concerns exist today, Chinese manufacturers improved dramatically in solar panels and batteries—why not transformers? The "China +1" strategy helps today but might not last forever.

Execution risks on mega projects remain substantial. HVDC projects are multi-year commitments with fixed-price contracts. Cost overruns, delays, or technical failures can wipe out years of profits. The company's aggressive order booking might be storing up problems for future quarters.

Working capital intensity remains concerning. Despite improvements, the business still requires significant working capital. As order books grow, working capital needs could balloon, requiring either debt or dilutive equity raises. The recent QIP, while well-timed, shows the ongoing capital intensity.

Technology disruptions could challenge the business model. Grid-scale batteries might reduce transmission infrastructure needs. Distributed generation through rooftop solar could bypass traditional grids. Quantum computing could revolutionize grid management, making current equipment obsolete.

Valuation at 21.5 times book value prices in perfection. Any disappointment—margin compression, order loss, execution delays—could trigger significant multiple compression. The stock's 84% run-up in one year might have pulled forward years of returns.

The Synthesis: Probabilistic Thinking

The truth likely lies between extremes. The bull case's structural drivers are real—India's infrastructure needs aren't optional. But the bear case's concerns about competition and cyclicality are valid. The key is position sizing and time horizon.

For investors with 5+ year horizons, the structural tailwinds likely dominate cyclical headwinds. The infrastructure super-cycle is early innings—we're in year 2 of a 20-year build-out. Short-term volatility from order timing or margin pressure creates entry opportunities for patient capital.

The competitive threats are real but manageable. Chinese competition forces pricing discipline but won't eliminate the business—critical infrastructure buyers prioritize reliability over cost. Technology disruption is gradual in infrastructure—even revolutionary changes take decades to implement at grid scale.

So what for investors: The asymmetry favors bulls but demands selective entry. The structural drivers are too powerful to ignore, but the valuation demands patience. The strategy: build positions during crisis periods (like COVID), hold through the super-cycle, but be prepared for volatility. This isn't a trade; it's a decade-long infrastructure play where time arbitrage beats timing the market.

XII. Epilogue: What Does the Future Hold?

Standing at the Vadodara facility today, watching robots position 500-ton transformers while engineers analyze real-time data from equipment installed decades ago, you witness something profound: the physical and digital worlds converging at infrastructure scale. This isn't just manufacturing—it's the materialization of civilization's nervous system.

India's net-zero commitments by 2070 aren't aspirational—they're existential. With air pollution killing millions annually and climate change threatening agricultural productivity, the energy transition becomes a survival imperative. This creates policy certainty rare in infrastructure investing. Governments may change, but the direction of travel remains constant.

The AI and data center boom adds an unexpected accelerant. A single ChatGPT query consumes 10x the electricity of a Google search. As India builds AI capability—from government's IndiaAI mission to private AI labs—electricity demand could surprise even aggressive forecasts. Data centers need not just power but perfect power quality—exactly Hitachi Energy's sweet spot.

Technology disruptions will reshape but not replace the grid. Grid-scale storage makes renewable integration feasible but requires sophisticated power conversion equipment. Hydrogen production needs massive electrical input and specialized transformers. Even quantum computing needs classical infrastructure to interface with the physical world. Each disruption creates new equipment demands rather than eliminating existing needs.

The potential for further consolidation seems inevitable. The global power equipment industry has too many subscale players for the investment required. GE's struggles, Siemens Energy's challenges, and smaller players' capital constraints suggest consolidation ahead. Hitachi Energy, with its strong balance sheet and parental support, could be consolidator rather than consolidated.

Yet the biggest opportunity might be hiding in plain sight: India as the global manufacturing hub for energy transition equipment. Just as China dominated solar panel manufacturing, India could own grid equipment manufacturing. The combination of engineering talent, manufacturing capability, and domestic market scale creates competitive advantages hard to replicate.

The company's evolution from colonial-era Hindustan Electric to global technology leader Hitachi Energy mirrors India's own transformation. Both journeys—company and country—are far from complete. The next chapter might be the most exciting yet: where a company that helped electrify India helps electrify the world.

For long-term investors, Hitachi Energy India represents a rare convergence: structural growth, technological moat, financial transformation, and management execution. It's boring until you understand it, then it becomes beautiful—the kind of business that compounds wealth not through speculation but through enabling civilization's progress.

The story that began with Swiss engineers installing transformers in newly independent India has evolved into something far grander: an Indian company with Japanese ownership and global ambitions, positioned at the intersection of every major energy trend. From ABB's power grid to India's energy transition champion—the transformation is complete, but the journey has just begun.

As we look toward 2047—India's centenary of independence and the target for 700 GW power demand—Hitachi Energy won't just be witnessing history; it will be writing it, one transformer, one transmission line, one grid solution at a time. In the end, this isn't just a business story—it's the story of how humanity will power its future, and why the companies that enable that future deserve our attention, analysis, and perhaps, our investment.

Final Reflection for Investors: Great infrastructure investments share a paradox: they're simultaneously boring and revolutionary. Boring because the business model is predictable—sell critical equipment to customers who have no choice but to buy. Revolutionary because they enable societal transformations that define centuries. Hitachi Energy India sits at this intersection, offering patient investors the opportunity to compound wealth by funding civilization's advancement. In a world obsessed with the next quarter, perhaps the greatest edge is thinking in decades.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube