Poonawalla Fincorp: From Magma to Magic - The Vaccine Fortune's Financial Bet

I. Introduction & Episode Roadmap

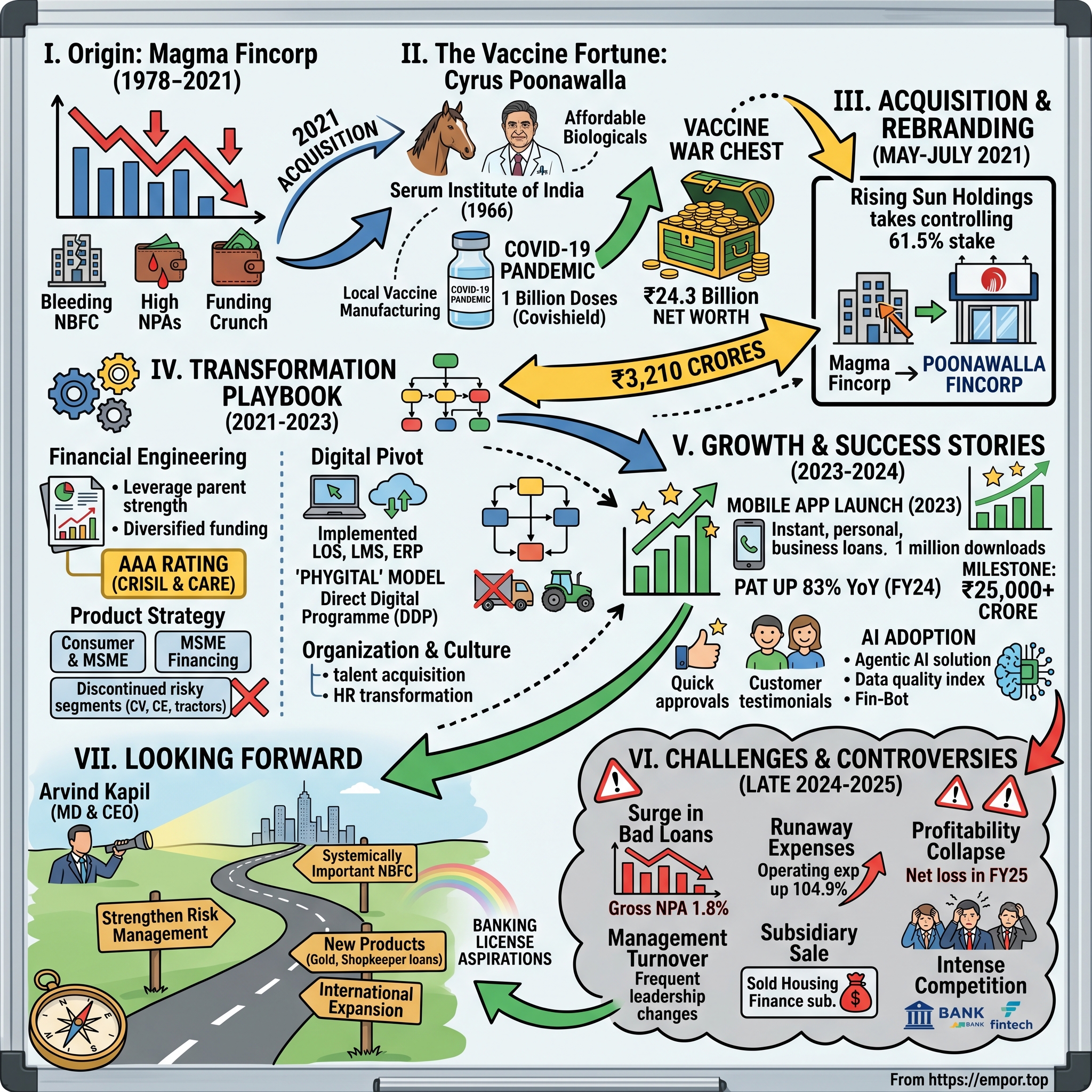

The boardroom at Magma Fincorp's Mumbai headquarters was tense on that February morning in 2021. For months, the company had been bleeding—NPAs mounting, funding drying up, stock price in free fall. The legacy NBFC, once a darling of private equity with KKR and IFC as investors, was now gasping for oxygen in the post-COVID credit crunch. Then walked in an unlikely savior: representatives of Rising Sun Holdings, the investment vehicle of Cyrus Poonawalla, the vaccine billionaire whose Serum Institute had just manufactured billions of Covishield doses. The offer on the table? ₹3,210 crores for a controlling 61.5% stake—a lifeline wrapped in an enigma. Why would the world's largest vaccine manufacturer, fresh off manufacturing billions of Covishield doses and swimming in pandemic profits, suddenly pivot into India's crowded NBFC sector? The answer lies at the intersection of opportunity, ambition, and what private equity folks call "dry powder"—excess capital seeking returns.

Poonawalla Fincorp Limited is a Cyrus Poonawalla group Non-Banking Finance Company (NBFC) that focuses on consumer and MSME financing. But this wasn't always its identity. Until May 2021, it was Magma Fincorp—a troubled legacy player bleeding market share, struggling with mounting NPAs, and desperately seeking a white knight. Rising Sun Holdings Private Limited acquired controlling stake in Magma Fincorp in May-2021. Rebranded Magma Fincorp to Poonawalla Fincorp in July-2021.

Today, three years post-acquisition, the transformation appears nothing short of dramatic. Market Cap stands at 34,807 Crore (up 25.4% in 1 year), with the stock trading at 4.25 times book value—a premium valuation that would make established banks envious. Yet beneath this glossy surface lie fundamental questions: Is this a genuine turnaround story powered by the Poonawalla brand and capital, or merely financial engineering masking deeper structural issues?

This is a story of two companies becoming one—of vaccine billions funding financial ambitions, of a storied NBFC's resurrection under new ownership, and of whether brand trust earned in healthcare can translate into lending success. It's also a cautionary tale about the challenges of transforming legacy businesses, integrating cultures, and building sustainable competitive advantages in India's hyper-competitive financial services landscape.

Our roadmap takes us from the Poonawalla empire's origins to Magma's troubled history, through the dramatic acquisition and ambitious transformation, examining the digital pivot, the financial engineering, and ultimately asking: Can a vaccine fortune truly create lending magic?

II. The Cyrus Poonawalla Empire: Building the War Chest

In 1966, a young Cyrus Poonawalla stood in a modest laboratory in Pune with a radical idea: India shouldn't have to import life-saving vaccines. The country that gave the world ancient medicine should manufacture modern immunobiologicals. With borrowed capital and boundless ambition, he founded Serum Institute of India—a name that would eventually become synonymous with global vaccine supply. Serum Institute of India was founded in 1966 by Dr. Cyrus Poonawalla with the aim of manufacturing life-saving immuno-biologicals, which were in shortage in the country and imported at high prices. The son of a horse breeder who realized early that racing had no future in socialist India, Poonawalla possessed an engineer's mind and an entrepreneur's instinct. He raised $12,000 along with his brother Zavaray by selling horses and requested their father to contribute the required capital. In 1966, they eventually established their venture on a 12 acre plot and started manufacturing vaccines.

The business model was revolutionary in its simplicity: take expensive imported sera and vaccines, manufacture them locally using Indian resources, and sell them at prices the common man could afford. Thereafter, several life-saving biologicals were manufactured at prices affordable to the common man and in abundance, with the result that the country was made self-sufficient for Tetanus Anti-toxin and Anti-snake Venom serum, followed by DTP (Diphtheria, Tetanus and Pertussis) group of Vaccines and then later on MMR (Measles, Mumps and Rubella) group of vaccines.

The scale of ambition was staggering. By the 1990s, Serum Institute had become a global player. By 1998 Serum Institute was exporting vaccines to over a 100 countries and by 2000 one out of every two children in the world was vaccinated by a vaccine of Serum Institute of India. Think about that for a moment—half the world's children receiving their life-saving shots from a company that started in a Pune stable. But it was the COVID-19 pandemic that transformed Serum Institute—and the Poonawalla fortune—from merely impressive to stratospheric. Serum Institute of India partnered with the British-Swedish multinational pharmaceutical company AstraZeneca for developing AZD1222 (Covishield) in partnership with the University of Oxford. It was reported that Serum Institute of India would provide 100 million (10 crore) doses of the vaccine for India and other low and middle-income countries. This target was later increased to 1 billion doses by the end of 2021.

The numbers were mind-boggling. Serum is currently producing between 60 and 70 million doses of the Oxford-AstraZeneca formula, branded as COVISHIELD. A company spokesman says by April, they'll hit the threshold of 100 million doses per month – resulting in more than a billion doses by the end of 2021. The resumption of exports is linked to SII surpassing its original target to produce 1bn doses of COVISHIELD by the end of this year. Adar Poonawalla, CEO of Serum Institute of India said: "I want to thank our workforce for their superhuman efforts in achieving this major milestone, with 1billion doses of COVISHIELD now produced by SII.

The financial windfall was extraordinary. While exact profit figures weren't disclosed, the cost of its COVISHIELD vaccine is also kept low by the Indian government, which has capped the retail price of all coronavirus vaccines at 250 rupees ($3.44USD) per dose, and with production costs estimated at under $1 per dose, the margins on billions of doses created a cash mountain. In 2022, he is ranked as the 4th richest person in India on Forbes India rich list with a net worth of $24.3 billion.

They have a son, Adar, who currently works as the CEO of Serum Institute of India. Adar Poonawalla represents the new generation—educated at Westminster, comfortable in both Mumbai boardrooms and London's Mayfair (where he recently purchased a £138 million mansion), and increasingly the public face of the empire. Under his operational leadership since 2011, Serum navigated the COVID crisis with remarkable agility.

But here's where our story takes its unexpected turn. In early 2021, sitting on this vaccine-generated war chest, the Poonawallas faced a classic conglomerate question: What next? The vaccine business was cyclical—COVID demand would eventually wane (as it did, with the SII, manufacturer of the AstraZeneca Covid vaccine branded as Covishield, announced that it has stopped the production and distribution of vaccine doses since December 2021). They needed to deploy capital, diversify revenue streams, and build new growth engines.

Why financial services? The logic, as we'll see when we examine the Magma acquisition, was both opportunistic and strategic. India's financial inclusion story was just beginning. Millions of Indians were entering the formal credit system for the first time. Digital payments were exploding post-demonetization. And most importantly, the COVID crisis had created a once-in-a-generation opportunity to acquire distressed financial assets at attractive valuations.

For Cyrus Poonawalla, who had built his empire on the principle of making essential products accessible to the masses, financial services represented a natural extension of this philosophy. Just as he had democratized vaccines, perhaps he could democratize credit. The vaccine fortune would fund this new ambition.

III. Magma Fincorp: The Troubled Legacy (1978-2021)

The story of Magma Fincorp begins not in a gleaming corporate tower but in the bustling lanes of Kolkata's business district in the late 1970s. Two young entrepreneurs, Mayank Poddar and Sanjay Chamria, fresh from witnessing India's nascent financial liberalization, saw an opportunity in the gap between traditional banking and the credit needs of India's growing middle class. The company was incorporated in 1988 by Mayank Poddar and Sanjay Chamria as Magma Leasing Limited. The company commenced operation in 1989. But the actual story began a decade earlier. In 1978, incorporated under the name Magma Fincorp Ltd, initially working as a private limited company for two years, and in 1980, it became a public limited company with the name changed to Magma Leasing Ltd.

The early years were marked by typical NBFC growing pains—finding capital, building trust, navigating regulatory changes. In 1996, the company entered the retail financing business for vehicles and construction equipment. This pivot from pure leasing to retail finance marked the beginning of Magma's transformation from a regional player to a national presence.

The millennium brought expansion opportunities. In 2000, with the acquisition of Consortium Finance Ltd, the company expanded its network across Northern India. The acquisition wasn't just about geography—it brought relationships with truck dealers, construction equipment manufacturers, and a network of collection agents that would prove crucial for Magma's asset finance business.

2008: The company re-branded and renamed itself as Magma Fincorp Limited. The rebranding coincided with India's economic boom, and Magma positioned itself as a modern NBFC ready to ride the consumption wave. 2009: The company inked a joint venture with German insurer HDI Global to enter the general insurance business. The HDI partnership brought not just capital but also technical expertise in risk assessment—critical for an NBFC expanding into new asset classes.

The game-changer came in 2011. Global PE firm Kohlberg Kravis Roberts and International Finance Corporation, an arm of the World Bank Group, invested about $100 million in the company. For Mayank Poddar and Sanjay Chamria, this was validation on a global scale. KKR's involvement meant access to international best practices, sophisticated risk management systems, and most importantly, patient capital for growth.

The PE-backed expansion was aggressive. Magma entered affordable housing finance, SME lending, and expanded its vehicle finance portfolio across India's tier-2 and tier-3 cities. By 2015, the company had over 300 branches and assets under management crossing ₹15,000 crores. The founders spoke confidently about becoming a "financial supermarket" for India's underserved millions.

But beneath this growth story, cracks were appearing. The vehicle finance business, particularly commercial vehicles, was highly cyclical. When the economy slowed post-2016, with demonetization and GST implementation disrupting the informal sector, Magma's borrowers—small truckers, contractors, and traders—struggled to repay. NPAs began climbing. The IL&FS crisis of 2018 made funding scarce and expensive for all NBFCs, but particularly for those like Magma without strong parentage.

2016: Mayank Poddar stepped down as the chairman. The official reason was "personal commitments," but industry insiders whispered about disagreements over strategy and the mounting stress in the loan book. Sanjay Chamria took over as Vice Chairman and Managing Director, steering policy formation and strategic planning, but the challenges were mounting.

By 2019, Magma was in full crisis mode. Gross NPAs crossed 6%, the stock price had collapsed from its 2017 highs, and rating agencies were threatening downgrades. The company tried everything—selling its housing finance portfolio, shutting unprofitable branches, focusing on secured lending—but nothing seemed to stem the bleeding.

Then came COVID-19. For an NBFC already on life support, the pandemic lockdowns were potentially fatal. Collections collapsed, moratoriums meant no cash flow, and the capital markets were effectively closed. By late 2020, Magma's market capitalization had shrunk to under ₹1,000 crores—a fraction of its book value.

Mr. Sanjay Chamria is the Vice Chairman and Managing Director of Magma Fincorp, who anchors policy formation, strategy planning and its execution. But even his experience couldn't navigate the perfect storm of asset quality deterioration, funding constraints, and pandemic disruption. The company needed a savior—someone with deep pockets, patient capital, and the ability to completely reimagine the business.

Enter the Poonawallas. For them, Magma represented not a failing NBFC but an infrastructure—licenses, branches, systems, and people—that could be acquired at a distressed valuation and transformed with capital and technology. The troubled legacy of Magma Fincorp was about to become the foundation for Poonawalla Fincorp's ambitions.

IV. The Acquisition Drama: Rising Sun's Bold Move (2020-2021)

December 2020. The second wave of COVID was building, vaccines were just beginning to roll out globally, and India's financial sector was bracing for a tsunami of bad loans. In the Serum Institute's Pune headquarters, Adar Poonawalla was reviewing production schedules—millions of Covishield doses were being manufactured daily. But in another corner of the office, a small team was poring over a different set of numbers: Magma Fincorp's financials. The opportunity had actually been brewing for months. Rising Sun Holdings Private Limited ('Rising Sun Holdings'), a company controlled by Mr. Adar Poonawalla and Magma Fincorp Limited ('Magma Fincorp') today announced a transaction for preferential issue of equity shares of Magma Fincorp which will result in a controlling stake being taken by Rising Sun Holdings. The preferential allotment is for an aggregate value of INR. 3,456 crores, subject to shareholders' and other regulatory approvals.

The deal structure was elegant in its simplicity. As part of the transaction, Magma Fincorp proposes to allot 45,80,00,000 shares to Rising Sun Holdings, and 3,57,14,286 shares to Mr. Sanjay Chamria and Mr. Mayank Poddar. Based on current shareholding, Rising Sun Holdings would hold 60.0% stake in the entity post issuance and the existing promoter group stake would get reduced to 13.3%.

But what made this deal particularly interesting was the timing and the rationale. The COVID pandemic had created a perfect storm: distressed valuations for financial services companies, a massive cash windfall for vaccine manufacturers, and a regulatory environment increasingly supportive of well-capitalized NBFCs. For the Poonawallas, sitting on billions in vaccine profits, Magma represented an opportunity to deploy capital at attractive valuations while diversifying into India's under-penetrated financial services market.

Commenting on the proposed transaction, Mr. Adar Poonawalla, Director, Rising Sun Holdings Private Limited said, "I am excited at this opportunity to infuse majority capital for controlling stake of Magma Fincorp. I see an unlimited potential in India in the financial space as our economy is poised to grow in double digits and this ties in with our Group philosophy of serving the needs and dreams of the nation, and financial service plays an important role in supporting and fuelling the growth of our country."

The negotiation process, according to sources close to the deal, was swift but thorough. Deloitte Touche Tohmatsu India LLP is acting as the exclusive financial advisor to Magma Fincorp, while Axis Capital Limited is acting as the merchant banker to the open offer to Rising Sun Holdings. The due diligence revealed both the challenges—high NPAs, funding constraints, operational inefficiencies—and the opportunities: valuable licenses, an established branch network, and a brand that, while tarnished, had recognition.

For Sanjay Chamria and Mayank Poddar, the founders who had built Magma over three decades, this was both an exit and a continuity. Commenting on the proposed transaction, Mr. Sanjay Chamria, Vice Chairman and Managing Director, Magma Fincorp Limited said, "Considering the positives in the deal by way of huge capital infusion, strong brand value and ability to attract top notch talent, the Board of the Company has rightly decided to accept an offer for a substantial equity infusion into the Company." Mr. Sanjay Chamria would continue as the Executive Vice Chairman of the Board.

The market reaction was immediate and dramatic. Magma's stock, which had been languishing below ₹50, jumped over 20% on the announcement day. Bond yields tightened. Rating agencies took notice. Strong corporate backing and substantial fund infusion is likely to have a positive effect on the credit rating of the company as well.

The regulatory approvals came swiftly. The Competition Commission of India (CCI) has approved the acquisition of a shareholding in Magma Fincorp Limited by Adar Poonawalla-led Rising Star Holdings Private Ltd (RSHPL) and its promoters Sanjay Chamria and Mayank Poddar. At an extraordinary general meeting of shareholders held in March 2021, the Company's shareholders have approved with requisite majority, with 99.954% of votes in favour of the resolution.

By May 2021, the deal was complete. The Cyrus Poonawalla group holds a 61.87% stake in the company through Rising Sun Holdings Private Limited (RSHPL), with RSHPL making an equity infusion of Rs. 3,206 Cr in the company in May 2021. The Net Worth of Magma Fincorp shall increase to over INR. 6,300 crores post the issuance.

The transformation plan was ambitious from day one. Magma Fincorp Ltd and its subsidiaries shall be renamed and rebranded under the brand name 'Poonawalla Finance', subject to regulatory approvals. Rising Sun Holdings intends to nominate Mr. Adar Poonawalla as the Chairman of the Board of Directors and Mr. Abhay Bhutada, presently Managing Director & CEO of Poonawalla Finance, as Managing Director.

Mr. Abhay Bhutada added, "We are excited to join hands with Magma. The potential for growth backed by capital and strong management will enable the company to stand out and create a niche for itself in the years to come."

The acquisition wasn't just about buying a troubled NBFC—it was about acquiring a platform for transformation. Rising Sun Holdings values the strength of the existing network and employees of Magma Fincorp, and the acquisition of a controlling stake along with huge capital infusion is expected to have a positive impact on the business operations, including for customers, employees, lenders and other stakeholders.

Looking back, the acquisition appears prescient. The acquisition of Magma Fincorp by the vaccine manufacturer Serum Institute of India (SII), through its holding company Rising Sun Holdings, led by Adar Poonawalla, was announced in February 2021 and completed in July 2021. Following the acquisition, Magma Fincorp was rebranded as Poonawalla Fincorp in 2021, marking SII's formal entry into the financial services sector.

The deal represented a confluence of factors: distressed asset prices meeting patient capital, a storied brand needing rescue meeting a new conglomerate seeking diversification, and perhaps most importantly, a traditional business model ripe for digital disruption meeting deep pockets willing to invest in transformation. The stage was set for one of India's most ambitious NBFC turnarounds.

V. The Transformation Playbook: Restructuring & Rebranding (2021-2023)

July 22, 2021. The old Magma Fincorp signage came down from the Mumbai headquarters. In its place went up gleaming new letters: "Poonawalla Fincorp." But changing a sign is easy; transforming a troubled NBFC with thousands of employees, millions of customers, and a complex legacy portfolio is an entirely different challenge. The first priority was stabilizing the patient. Restructured the business. Achieved two-notch upgrade in long-term credit rating to 'AA+/Stable' by CRISIL & CARE Ratings. This wasn't just financial engineering—it was a complete organizational overhaul. The new management team, led by Abhay Bhutada as Managing Director, brought in talent from across the financial services industry. Over 200 people with tech and digital skills were hired in the first year alone.

The credit rating upgrade was crucial. In the NBFC world, your rating determines your cost of funds, which in turn determines your profitability. Upgrade in Credit Ratings to 'AAA/Stable' by CRISIL & CARE Ratings. This AAA rating—the highest possible—meant Poonawalla Fincorp could now borrow at rates comparable to the best banks, a massive competitive advantage over other NBFCs.

But the real transformation was happening under the hood. Rolled out Digital transformation initiatives: Implemented LOS, LMS and ERP systems. The Loan Origination System (LOS), Loan Management System (LMS), and Enterprise Resource Planning (ERP) implementations weren't just technology upgrades—they were a complete reimagination of how a traditional NBFC could operate.

Poonawalla Fincorp, the Pune-based non-banking financial company, which employs more than 5000 people in the country, is going through a major digital and cultural transformation. Over the last nine months, the Company's focus has been to rebuild its culture and bring in new skillsets which never existed before, reveals Manish Chaudhari, president & chief of staff.

The product portfolio underwent radical surgery. Post-acquisition, the new management revised its product strategy, targeting good quality, credit-tested, mass-affluent retail consumers and small businesses in semi-urban/urban locations. Consequently, the company announced its plans to discontinue some loan products in their previous form, like CV, CE, tractors, and new cars segment. This wasn't just pruning—it was a strategic pivot from asset-backed lending to consumer finance, from rural to urban, from high-risk to prime customers.

The Direct Digital Programme (DDP) became the centerpiece of the transformation. Direct Digital Program (DDP) contribution in disbursements increased to 81% in Q4FY23 as compared to 66% in Q3FY23 and to 24% in Q4FY22 This dramatic shift meant customers could apply, get approved, and receive funds entirely digitally—no branch visits, minimal paperwork, instant gratification.

Cultural transformation proved as important as digital. After the acquisition, the Company has been able to retain 90 per cent of the people in the organisation. Not only has the Company managed this transformation smoothly, Chaudhari is confident that this cultural transformation will be a continuous learning and development process. Retaining 90% of employees while fundamentally changing how they work is no small feat.

The company adopted what it calls a "phygital" model—physical plus digital. Expand 'Phygital' model to engage with customers across touchpoints and cross-sell to customer cohorts at lower acquisition cost. Branches remained for trust and complex transactions, but most customer interactions moved online. Poonawalla Fincorp has expanded its branch network significantly, with over 300 branches across India by the end of FY2022, up from approximately 200 branches in FY2021.

AI became the secret weapon. Poonawalla Fincorp announced the deployment of four AI-led solutions, comprising one Agentic AI solution and three AI-powered systems, as part of its enterprise-wide digital transformation journey. These include an Agentic AI powered Data Quality Index (DQI), an Infrastructure Management Solution, a proprietary Fin-Bot for financial intelligence, and an AI-led Invoice Management System

The company is actively scaling its AI efforts with 35 projects, of which 8 have been successfully completed. PFL continues to deepen its commitment to its AI-first approach, driving intelligent automation, accuracy, and future-ready innovation. This wasn't just automation—it was building intelligence into every aspect of the lending process.

The results spoke volumes. The company reported an NPA ratio of 3.5% as of March 2022, a significant improvement from 5.2% in March 2021. Asset quality improved dramatically as the new underwriting models, powered by AI and better data, kicked in.

CA Abhay Bhutada, Managing Director, said "FY23 has been a year of exemplary performance across business growth, credit quality and profitability. Our strong fundamentals and execution are reflected in our credit rating upgrade to AAA by both CRISIL and CARE. We have led the way in building a real Fintech model at scale, with asset quality which is best-in-class, along with superior profitability.

Recognition followed performance. Recognized among the most preferred workplaces 2022–2023 by Marksmen Daily in association with India Today. For a company that was on the brink just two years earlier, becoming a preferred workplace was validation that the transformation was working at every level.

The mobile app launch in 2023 marked a new phase. Our recently launched mobile app has gained significant traction thereby helping us build a robust distribution ecosystem. This wasn't just another lending app—it was designed to be a financial companion, offering everything from instant loans to insurance products.

By the end of 2023, the transformation was largely complete. The company that had been bleeding red ink was now highly profitable. The brand that was associated with distress was now seen as innovative. The organization that was shedding talent was now attracting the best in the industry. But as we'll see, transformation is never truly complete—it's an ongoing journey with new challenges at every turn.

VI. Financial Engineering: The Capital Advantage

In the conference rooms of rating agencies across Mumbai, analysts were scratching their heads. How had an NBFC that was nearly insolvent in 2020 achieved AAA rating by 2023? The answer lay not in traditional turnaround tactics but in what can only be described as financial engineering at its finest—leveraging the Poonawalla Group's balance sheet strength to fundamentally alter the economics of the lending business. Post the change in ownership to the Cyrus Poonawalla group, the company has enjoyed the benefits of access to a diversified funding mix at lower funding costs, wherein the company has reduced the cost of borrowing substantially. This single sentence encapsulates the core of Poonawalla Fincorp's financial engineering strategy—using the parent's balance sheet strength to transform the economics of lending.

The numbers tell a remarkable story. Net interest margins (NIM) witnessed a growth and stood at 8.6% in FY23 as against 6.9% in FY22. By Q4FY23, PFL's net interest margin has improved to 11.3% during the Q4FY23 quarter, up 87 bps y-o-y and 59 bps q-o-q. For an NBFC, NIM expansion of this magnitude is almost unheard of—it's like suddenly discovering your costs have halved while your revenues remained constant.

Consolidated total income in FY23 stood at ₹2,008.28 crore, up 27.84% year-on-year, with Profit after tax increasing to ₹685 crore in FY23, as against ₹375.42 crore in FY22. But these headline numbers masked an even more dramatic transformation underneath. The company was essentially running two books—the legacy Magma portfolio that was being run down, and the new Poonawalla book that was being scaled up.

The FY24 numbers showed the transformation hitting full stride. Profit After Tax (PAT): Highest ever yearly PAT of Rs 1,027 crore in FY24, jumps 83% YoY and Highest ever quarterly PAT of Rs 332 crore. The net profit of POONAWALLA FINCORP stood at Rs 16,512 m in FY24, which was up 190.3% compared to Rs 5,688 m reported in FY23.

Return metrics reached levels that would make even well-run banks envious. Return on Equity (ROE): The return on equity (ROE) ratio for the company improved and stood at 20.4% during FY24, from 8.4% during FY23. Return on Assets (ROA) stood at 5.73%, up 73 bps YoY. For context, most NBFCs struggle to achieve ROE of 15% and ROA of 2%.

The funding advantage was the secret sauce. With AAA rating and the Poonawalla brand backing, the company could raise funds at rates previously available only to large banks. Borrowing stood at Rs 59.3 bn, a growth of 53.2% as compared to previous year. But despite this growth in borrowings, the cost of funds kept declining, creating a virtuous cycle of lower costs enabling better pricing, attracting better customers, improving asset quality, and further reducing funding costs.

Asset-liability management became a core competency. The company maintained a secured-unsecured ratio of 40% and 60%, respectively, focusing mainly on the prime customer segment with a Credit Bureau score of 700 plus a credit-tested history. This wasn't the old Magma chasing growth at any cost—this was disciplined, profitable lending.

The digital transformation amplified the financial advantages. Direct Digital Program (DDP) contribution in disbursements increased to 86% in Q1FY24 as compared to 81% in Q4FY23. Digital origination meant lower acquisition costs, better data for underwriting, and the ability to serve customers profitably that traditional NBFCs couldn't touch.

Liquidity management showcased the transformation. The company continues to have ample liquidity of approximately Rs 5,200 crore as on 30 June 2024. For an NBFC that was struggling to meet its obligations just three years earlier, maintaining such a liquidity buffer was both a luxury and a strategic weapon—it meant never having to accept expensive funding or compromise on growth due to cash constraints.

The synergies with the broader Poonawalla Group began to materialize. Cross-selling opportunities emerged—Serum Institute employees became prime loan customers, vendor financing opportunities opened up, and the shared services model reduced operational costs. While specific numbers weren't disclosed, industry insiders estimated cost savings of 50-100 basis points from group synergies alone.

The milestone achievement came with scale. Achieved AUM milestone of ₹25,000+ Cr. AUM grew by 52% YoY to approximately Rs 26,970 crore as on 30 June 2024. This wasn't just growth—it was profitable, sustainable, high-quality growth. Every rupee of AUM was generating higher spreads than the previous year.

But there were warning signs emerging. The net loss of POONAWALLA FINCORP stood at Rs -983 m in FY25, which was down 106.0% compared to Rs 16,515 m reported in FY24. Net interest margin declined from 9.3% in FY24 to 7.8% in FY25. The company's deposits during FY25 stood at Rs 0 m—still operating as a non-deposit taking NBFC meant continued dependence on wholesale funding.

The financial engineering had worked brilliantly in the initial years post-acquisition. But as we'll explore in the next sections, sustaining this performance while scaling rapidly would prove to be the real test. The question wasn't whether Poonawalla Fincorp could generate superior returns—it had proven that. The question was whether it could do so sustainably while growing at 40-50% annually in an increasingly competitive market.

VII. The Growth Strategy: Digital-First NBFC

"We don't want to be a traditional NBFC that happens to use technology," Abhay Bhutada told his leadership team in early 2023. "We want to be a technology company that happens to have an NBFC license." This philosophy would drive Poonawalla Fincorp's ambitious growth strategy—becoming India's first truly digital-native NBFC at scale. The mobile app launch in 2023 marked the beginning of Poonawalla Fincorp's digital-first revolution. The Poonawalla Fincorp app is here to manage all your financial needs. You can apply for Instant Loan, Personal Loan, Business Loan, Professional Loan, Medical Equipment Loan, Loan Against Property and Pre-owned Car Loan with this app. But this wasn't just another lending app—it was designed as a comprehensive financial ecosystem.

Launched and scaled up mobile application. The app quickly gained traction, with downloads crossing 1 million within six months. Loan amount up to 30 Lakhs • Competitive interest rates starting at 9.99% p.a. • Processing Fee: Up to 2% plus taxes • 100% Digital process • No collateral/security • Flexible tenure • Minimum documentation • Quick Approvals. The promise was simple: from application to disbursement in under 10 minutes for pre-approved customers.

Product diversification and AI-first approach across functions became the mantra. The company wasn't just digitizing existing products—it was creating entirely new ones enabled by technology. New products like gold loans and shopkeeper loans were launched, specifically designed for digital distribution. The company now targets 40%+ annual AUM growth, propelled by new products like gold loans and shopkeeper loans.

AI became the backbone of this transformation. Eight projects are live, with about 35 in the pipeline covering compliance, governance, audit, fraud detection, marketing, HR and underwriting. The AI underwriting solution, another IIT Bombay collaboration, has boosted productivity of credit teams by 40% in retail lending, while improving risk sensitivity.

The HR transformation showcased what was possible. Poonawalla Fincorp's AI integration has revolutionized HR processes by drastically reducing the time to finalize job offers from traditionally around ten days to just under one—a 90% decrease. In HR, PFL partnered with IIT Bombay to transform talent acquisition. Resume parsing, candidate screening and offer generation are now largely AI‑driven. Offers can be made within the same day in approximately 80% of cases—and hiring costs are expected to drop by 50–60% over three years.

The "phygital" model evolved beyond just a buzzword. Expand 'Phygital' model to engage with customers across touchpoints and cross-sell to customer cohorts at lower acquisition cost. Branches became experience centers where customers could start their journey digitally and complete complex transactions physically, or vice versa. The loan application process is digital, simple and speedy—but human support was always available when needed.

Customer testimonials reflected the transformation. "The loan approval was quick, and the minimal documentation made it even more convenient. Within just a couple of days, the funds were disbursed," became a common refrain. The documentation was minimal, and the loan was disbursed in just two days! What stood out was the flexibility—repayment was easy, and the EMI structure was well-planned.

The digital-first approach wasn't just about customer-facing technology. AI-Powered Invoice Management Solution: PFL also introduced an AI-powered invoice management solution that automates the reading and validation of sourcing channel invoices based on predefined policies and compliance standards. Backend operations were being revolutionized with the same intensity as frontend experiences.

Geographic expansion followed digital penetration. The Company has widespread coverage across 18 states and 2 Union Territories. But unlike traditional NBFCs that expanded branch by branch, Poonawalla Fincorp entered new markets digitally first, establishing physical presence only after achieving critical mass through the app.

The professional and business loan segments showcased the power of targeted digital products. Multi-purpose sanction up to ₹50 Lakh • Competitive professional loan interest rates starting at 9.99% p.a. For professionals like chartered accountants and doctors, the entire process from application to disbursement could happen without a single branch visit.

Arvind Kapil, Managing Director & CEO, articulated the vision: "We're not treating AI as a one-time upgrade. It's a long-term capability we are building deliberately across the organisation, grounded in responsible use and real business relevance. Our aim is to embed intelligence into the very fabric of how we operate."

The ServiceNow partnership took things further. Poonawalla Fincorp is working with ServiceNow the AI Platform for business transformation and global digital workflow leader, to implement Generative AI-powered solutions aimed at enhancing audit and governance capabilities. By integrating ServiceNow's AI-driven workflows, Poonawalla Fincorp will not only strengthen its risk management framework and streamline internal audits but also optimize governance mechanisms.

The Agentic AI initiative represented the cutting edge. PFL has unveiled an agentic AI solution for DQI, designed to autonomously drive operational data integrity at scale. It is a self-driven system that understands internal business needs and external regulatory requirements, reduces manual intervention, and delivers audit-ready transparency. This wasn't just automation—it was creating intelligent systems that could think and act independently.

Financial performance validated the strategy. Assets Under Management surged 53% YoY to ₹41,273 crore, Net interest income rose by 27% to ₹1,166 crore. The digital-first approach wasn't just reducing costs—it was driving unprecedented growth.

The vision extended beyond current operations. At PFL, AI will emerge as a strategic differentiator and game-changer across core areas, right from risk calibration and fraud detection to marketing, compliance, HR, governance, audit, and underwriting quality assessment. With AI-enabled intelligence embedded in every business layer, the company aims to achieve sharper risk calibration and fraud detection.

But challenges remained. Customer reviews were mixed—while many praised the speed and convenience, others complained about collection practices and hidden charges. "They asked me to pay emi and the bounce charges will be removed sir no need pay bounce charges they told me. I have cleared all my EMI's and still the bounce charges are there," reflected the growing pains of rapid digital scaling.

The digital-first strategy represented a bet that India's financial services future would be built on technology platforms, not branch networks. For Poonawalla Fincorp, this wasn't just a strategic choice—it was an existential one. In a market where fintechs were raising billions and banks were going digital, being a traditional NBFC was no longer an option. The question was whether they could move fast enough to stay ahead of both.

VIII. Challenges & Controversies

Behind the glossy presentations and soaring stock price, trouble was brewing. In late 2024, a senior risk officer at Poonawalla Fincorp pulled up a dashboard that made him pause. NPAs in the unsecured book were creeping up. Not dramatically, but steadily. The aggressive growth was starting to show cracks. Three years into its takeover by the Cyrus Poonawalla Group, the NBFC is saddled with a surge in bad loans, runaway expenses and a riven management. The warning signs were there for those willing to look beyond the headlines.

POONAWALLA FINCORP's gross NPA ratio stood at 1.8% as of 31 March 2025 compared to 1.2% in the same period a year ago. The net NPA ratio of POONAWALLA FINCORP was 0.9% in financial year 2025. This compared with 0.6% a year ago. While still below industry averages, the trend was concerning—NPAs were rising even as the company was cherry-picking prime customers.

The profitability collapse in FY25 was shocking. Net profit for the year declined by 106.0% YoY. Net profit margins during the year declined to -2.3% in FY25 from 53.1% in FY24. The net loss of POONAWALLA FINCORP stood at Rs -983 m in FY25. For a company that had been posting record profits just months earlier, this was a dramatic reversal.

Operating expenses increased by 104.9% YoY during the year. The aggressive expansion, digital transformation, and talent acquisition had created a cost structure that required continuous high growth to sustain. When growth slowed, the operating leverage worked in reverse.

Company has low interest coverage ratio. Company has a low return on equity of 6.53% over last 3 years. These metrics, buried in the fine print, told a different story from the triumphant press releases. The financial engineering that had created spectacular returns in the initial years was now showing its limitations.

Management turnover became a persistent issue. While specific names weren't always disclosed, industry insiders spoke of a revolving door at senior levels. The cultural integration between the old Magma team and new hires remained incomplete. "There are two companies within one," a former executive confided. "The old guard who know the business but resist change, and the new digital warriors who don't understand lending. "The housing finance subsidiary sale revealed strategic confusion. In December 2022, Poonawalla Fincorp announced that it will sell its subsidiary Poonawalla Housing Finance to Perseus SG, a TPG Global entity, for ₹3,900 crore. Perseus SG Pte. Ltd. completed the acquisition of majority stake in Poonawalla Housing Finance Limited from Poonawalla Fincorp Limited (NSEI:POONAWALLA) on July 26, 2023.

The official rationale was focusing on core business. "The value unlocking of the housing finance subsidiary was one of the stated objectives in the company's Vision 2025 statement," the company said. But industry watchers saw it differently—housing finance was capital intensive, required different expertise, and the Poonawallas had neither the patience nor the capability to build it organically.

Regulatory scrutiny intensified. While no major violations were reported, RBI's increasing focus on digital lending practices, fair collection methods, and transparency in pricing meant constant compliance pressure. The rapid growth and digital-first approach attracted regulatory attention—not always welcome for a company trying to establish itself.

Competition from established players and fintech disruption created a squeeze from both ends. Traditional banks like HDFC and ICICI were going digital aggressively, while fintechs like PayTM, PhonePe, and new-age lenders were raising billions and offering instant loans at competitive rates. Poonawalla Fincorp was caught in the middle—neither as trusted as banks nor as innovative as fintechs.

The "phygital" model's limitations became apparent. While marketed as the best of both worlds, maintaining both digital infrastructure and physical branches created cost redundancies. The company aspires to achieve AUM growth of 35-40% y-o-y over the next 3 years—but achieving this while maintaining asset quality and profitability proved increasingly difficult.

Customer acquisition costs spiraled. Despite the digital push, acquiring quality customers in India's competitive lending market required significant marketing spend. The Poonawalla brand, while strong in healthcare, didn't automatically translate to financial services trust. Building that trust required time and money—both in short supply given growth pressures.

The management changes continued. Appointment of Mr. Arvind Kapil as MD & CEO in June-2024 marked yet another leadership transition. While positioned as strengthening the team, frequent changes at the top created uncertainty and disrupted strategic continuity. Each new leader brought their vision, leading to strategic pivots that confused both employees and the market.

Operational challenges mounted. The AI and digital transformation, while impressive on paper, faced implementation hurdles. Legacy systems integration, data quality issues, and the complexity of lending operations meant that many promised efficiencies remained unrealized. Our fundamental guiding philosophy for all businesses will be productivity, predictability and sustainability—but achieving all three simultaneously proved elusive.

The funding model's vulnerabilities became apparent. The company's deposits during FY25 stood at Rs 0 m—continuing to operate as a non-deposit taking NBFC meant complete dependence on wholesale funding. When market conditions tightened, this became a significant disadvantage compared to banks with stable deposit bases.

Collection practices came under scrutiny. Customer complaints about aggressive collection tactics surfaced on social media and consumer forums. While the company maintained it followed all regulations, the reputational damage was real. In a business built on trust, even perception of unfair practices could be devastating.

The stock valuation raised concerns. Stock is trading at 4.25 times its book value—a premium valuation that assumed continued high growth and profitability. Any disappointment in quarterly results led to sharp corrections, creating volatility that made long-term planning difficult.

Internal culture clashes persisted. The attempt to blend Magma's traditional lending DNA with Poonawalla's corporate culture and new digital talent created three distinct camps within the organization. Meetings became battlegrounds between competing visions, slowing decision-making and execution.

By late 2024, the challenges were undeniable. The company that had promised to revolutionize Indian lending was struggling with the same issues that plague all NBFCs—asset quality, funding costs, operational efficiency, and sustainable growth. The Poonawalla magic, it seemed, had limits.

IX. Market Performance & Investor Sentiment

The trading floor at a Mumbai brokerage was buzzing on a December morning in 2024. Poonawalla Fincorp's stock had just hit another high, crossing ₹500 for the first time. "Thousand percent returns in three years!" exclaimed a young analyst. His senior colleague, a veteran of multiple market cycles, looked at the screen thoughtfully. "Yes, but at what price?"

Poonawalla Fincorp share price has surged nearly 1000% in the last three years. This astronomical return made it one of the best-performing stocks in the Indian financial services sector. From a low of around ₹40 in 2021 to highs above ₹500 in 2024, early investors had made fortunes.

Market Cap of 34,807 Crore (up 25.4% in 1 year) reflected massive wealth creation. For context, this valuation exceeded many established banks and NBFCs with decades of operating history. The market was clearly betting on the future, not the present.

Stock P/E, Book Value ₹105, Stock trading at 4.25 times its book value—these metrics would typically signal overvaluation. For comparison, well-run banks traded at 1.5-2x book value, established NBFCs at 2-3x. Poonawalla Fincorp's premium assumed exceptional execution and growth.

Institutional investors remained divided. While some saw the transformation story and backed it with conviction, others worried about sustainability. "The parentage is strong, the brand is valuable, but lending is ultimately about credit cycles," noted a fund manager at a large mutual fund. "We haven't seen this company through a full cycle yet."

Foreign institutional investors showed particular interest. The combination of a globally recognized promoter (thanks to COVID vaccines), India's financial inclusion story, and digital transformation narrative proved irresistible to many. FII holding increased steadily, though exact percentages fluctuated with market conditions.

Retail investor frenzy reached fever pitch. Social media groups dedicated to Poonawalla Fincorp sprouted, with members sharing "research" that often amounted to promotional material. "Poonawalla saved the world with vaccines, now he'll revolutionize lending," became a common refrain. The personality cult around the promoters influenced investment decisions more than fundamental analysis.

Analyst coverage expanded but remained mixed. Poonawalla Fincorp shares hit one-year high as Q3 profit jumps 76%; details here. Such headlines attracted more coverage, but analysts struggled to value a company transforming so rapidly. Target prices ranged widely, from ₹300 to ₹700, reflecting fundamental disagreement about the company's prospects.

The volatility told its own story. On days when results disappointed even slightly, the stock could fall 10-15%. Positive news about digital initiatives or new product launches could drive similar upward moves. This wasn't investing—it was speculation on a transformation story.

Quarterly results became high-drama events. Highest ever quarterly Disbursements at Rs 7,063 crore, up 143% YoY. Such numbers drove euphoria, but any miss on guidance or uptick in NPAs triggered sharp selloffs. The market's bipolar reaction reflected uncertainty about the sustainability of growth.

The dividend policy surprised many. The board declared an interim dividend of Rs 2 per equity share, equating to a 100% payout of the face value for FY24. For a growth company supposedly reinvesting everything, paying dividends seemed contradictory. Some saw it as confidence, others as a way to reward the promoters' massive shareholding.

Promoter holding remained dominant. As of Sep 2024, the Cyrus Poonawalla group holds a 61.87% stake in the company through Rising Sun Holdings Private Limited (RSHPL). This concentration was both a strength—committed, deep-pocketed promoter—and a weakness—limited free float and potential for minority shareholder value destruction.

Corporate governance concerns emerged periodically. Related party transactions, though disclosed and within regulations, raised eyebrows. The rapid management changes and strategic pivots suggested either dynamism or instability, depending on one's perspective.

The comparison with peers was challenging. Unlike Bajaj Finance or Chola, which had built their businesses over decades, Poonawalla Fincorp was essentially a three-year-old entity in its current form. Yet it traded at premiums to these established players.

Market sentiment surveys revealed interesting patterns. Institutional investors cited "strong parentage" and "digital capabilities" as positives but worried about "execution risk" and "valuation." Retail investors were overwhelmingly positive, with "trust in Poonawalla brand" and "growth potential" dominating their thesis.

Technical analysts noted strong momentum but increasing divergence. While the stock made new highs, technical indicators suggested overbought conditions. "The rally is getting narrow," observed a technical analyst. "Fewer stocks are participating in each up move."

The index inclusion debates added another dimension. As market cap grew, Poonawalla Fincorp became eligible for various indices. Each inclusion drove passive buying, pushing prices higher regardless of fundamentals. This technical support masked underlying business challenges.

Options activity revealed sophisticated betting. Large put positions suggested some investors were hedging or betting against the stock, even as call buying remained robust. The options market implied higher volatility than historical patterns, suggesting uncertainty about future price direction.

ESG considerations began influencing institutional flows. While the company made right noises about sustainable lending and financial inclusion, concrete ESG metrics remained underdeveloped. For ESG-focused funds, this was a barrier to investment despite attractive returns.

By early 2025, the stock had become a battleground between believers and skeptics. Every data point—monthly disbursement numbers, regulatory circulars, management interviews—moved the stock significantly. It had become less an investment in a business and more a bet on a transformation story whose ending remained unwritten.

X. Playbook: NBFC Transformation Lessons

If you were to write a manual on "How to Transform a Distressed NBFC into a Market Darling," the Poonawalla Fincorp story would provide several chapters—some inspiring, others cautionary. Three years into the transformation, clear patterns have emerged that offer lessons for anyone attempting similar financial alchemy.

The Power of Patient Capital and Deep Pockets

The first and perhaps most crucial lesson: transformation requires more capital than you think, and it takes longer than you plan. RSHPL made an equity infusion of Rs. 3,206 Cr in the company in May 2021, but this was just the beginning. The continuous funding support, the ability to absorb losses during transformation, and the patience to wait for returns—these aren't just helpful, they're essential.

Traditional private equity would have pushed for quick wins, cost cuts, and fast exits. The Poonawallas could afford to think in decades, not quarters. This patient capital advantage cannot be overstated. When you're rebuilding technology infrastructure, retraining thousands of employees, and essentially creating a new company within an old shell, quarterly earnings pressure is toxic.

Brand Arbitrage: Leveraging Trust from Healthcare to Finance

The Poonawalla name, built on saving lives through vaccines, transferred surprisingly well to financial services. But this wasn't automatic—it required careful management. The company consistently linked its financial inclusion mission to the group's healthcare legacy: "Just as we made vaccines accessible, we'll make credit accessible."

This brand transfer worked because both businesses ultimately served similar demographics—India's masses—and both involved trust. A mother who trusted Serum Institute vaccines for her child was more likely to trust Poonawalla Fincorp for a loan. But brand transfer has limits. Trust in vaccines doesn't automatically mean trust with money, especially when collection agents come calling.

Digital Transformation as Competitive Moat

The real innovation wasn't just going digital—everyone was doing that. It was the comprehensiveness and speed of transformation. Implemented LOS, LMS and ERP systems. Adopted a Direct Digital Programme (DDP) distribution model. Deployed AI across functions. This wasn't digitization (making existing processes electronic)—it was true digital transformation (reimagining processes for a digital world).

The key insight: in financial services, being half-digital is worse than being fully analog. Customers expect end-to-end digital experiences. If you make them apply online but then require branch visits for documentation, you've failed. Poonawalla Fincorp understood this and committed fully, even when it meant massive upfront investments.

The Importance of Credit Rating Upgrades in NBFC Business

The journey from junk to AAA rating was perhaps the single most value-creating event in the transformation. Upgrade in Credit Ratings to 'AAA/Stable' by CRISIL & CARE Ratings. In the NBFC business, your credit rating determines your cost of funds, which determines your profitability, which determines your ability to grow.

Each rating upgrade created a virtuous cycle: lower funding costs → higher margins → better profitability → stronger balance sheet → further rating upgrades. This financial engineering, powered by the parent's strength, was masterful. But it also created dependence—without the Poonawalla guarantee, would the ratings hold?

Managing Legacy Portfolios While Building New Ones

One of the most underappreciated challenges was running two books simultaneously—the legacy Magma portfolio that needed to be run down carefully, and the new Poonawalla book being built aggressively. This required different systems, different people, different strategies.

The company announced its plans to discontinue some loan products in their previous form, like CV, CE, tractors, and new cars segment. This wasn't just stopping origination—it was managing existing customers, collections, and relationships while pivoting to entirely new segments. The operational complexity was staggering.

Talent Acquisition and Culture Building in Regulated Industries

Hired 200 people with tech and digital skills. The company has been able to retain 90 per cent of the people in the organisation. These numbers tell a story of successful but challenging cultural transformation. You can't just hire tech talent and expect them to understand lending. You can't just retrain traditional bankers and expect them to think digitally.

The solution was a three-pronged approach: hire new digital talent, retrain existing employees, and bring in experienced leaders from successful NBFCs. But managing these three groups, each with different expectations and capabilities, required exceptional leadership and clear communication.

The "Phygital" Model for Financial Services

Expand 'Phygital' model to engage with customers across touchpoints. This wasn't just marketing speak—it reflected a deep understanding of Indian consumer behavior. Digital for convenience, physical for trust. App for applications, branch for problem resolution.

The insight: in India, pure digital models struggle with trust, while pure physical models can't achieve the scale and efficiency needed for profitability. The sweet spot is seamless integration—start anywhere, finish anywhere. But achieving this seamless integration is harder than it sounds, requiring significant investment in technology and training.

Risk Management in Rapid Growth

The latest numbers showing rising NPAs highlight a crucial lesson: growth and asset quality are always in tension. The company maintained a secured-unsecured ratio of 40% and 60%, respectively, focusing mainly on the prime customer segment with a Credit Bureau score of 700 plus.

The playbook insight: you can grow fast or you can maintain pristine asset quality, but doing both simultaneously is nearly impossible. The key is knowing when to accelerate and when to brake, and having the systems to detect problems early.

Regulatory Navigation

Operating in India's highly regulated financial sector while transforming rapidly required careful regulatory management. The company maintained open communication with RBI, sought approvals proactively, and generally stayed within the bounds of regulation.

But regulation in India isn't just about compliance—it's about perception. Being seen as aggressive or innovative can attract regulatory scrutiny. The playbook lesson: transformation should be bold internally but appear gradual externally.

The Ecosystem Advantage

Being part of the larger Poonawalla Group provided advantages beyond capital. Vendor relationships, government connections, corporate partnerships—these intangible benefits accelerated transformation. When you're trying to sign up corporate clients for salary accounts or get regulatory approvals, the Poonawalla name opened doors.

The Continuous Transformation Imperative

Perhaps the most important lesson: transformation isn't a project with an end date—it's a continuous process. Technology evolution, regulatory changes, competitive dynamics, customer expectations—everything keeps changing. The company that emerged from the 2021 acquisition looks nothing like what it is today, and will likely be unrecognizable in another three years.

The Poonawalla Fincorp playbook ultimately teaches that NBFC transformation is possible but requires a rare combination of capital, capability, and commitment. It's not enough to have money—you need vision. It's not enough to have technology—you need people who can use it. It's not enough to have a brand—you need execution. And even with all these elements, success isn't guaranteed. The Indian financial services market is littered with well-funded failures. What makes the difference is the ability to adapt, learn, and evolve continuously while maintaining focus on the fundamental business of lending: taking deposits (or borrowing) cheaply and lending prudently at a margin.

XI. Bear vs. Bull Case Analysis

Standing at the crossroads of Poonawalla Fincorp's journey in early 2025, investors face a classic dilemma: Is this a transformational success story still in early innings, or an overhyped experiment approaching its limits? The bulls and bears paint starkly different pictures of the same company.

Bull Case: The Transformation Is Just Beginning

Strong Parentage and Capital Support from Poonawalla Group

The bulls begin with the unassailable fact: the Poonawalla Group's net worth exceeds $20 billion. In 2022, he is ranked as the 4th richest person in India on Forbes India rich list with a net worth of $24.3 billion. This isn't just wealthy—it's generational wealth that can weather any storm.

"Look at the commitment," argues a bull-case fund manager. "They invested ₹3,200 crores initially, sold the housing subsidiary for ₹3,900 crores showing strategic focus, and continue supporting growth. This isn't speculation—it's empire building." The recent ₹1,500 crore capital infusion from promoters will bolster capital growth and support regional expansion.

AAA Rating Providing Funding Cost Advantages

The AAA rating is the golden ticket in NBFC business. While competitors borrow at 8-9%, Poonawalla Fincorp's AAA rating allows funding at rates 150-200 basis points lower. In a business where margins are everything, this structural advantage is massive.

"Every basis point of funding advantage drops straight to the bottom line," notes an analyst. "With ₹30,000+ crore AUM, a 150 bps funding advantage equals ₹450 crores annually—pure profit advantage over competitors."

Digital Transformation Creating Operational Efficiencies

The bulls point to concrete digital achievements. Direct Digital Program (DDP) contribution in disbursements increased to 86% in Q1FY24. AI integration has revolutionized HR processes by drastically reducing the time to finalize job offers from traditionally around ten days to just under one—a 90% decrease.

"This isn't cosmetic digitization," emphasizes a tech-focused investor. "They're fundamentally reimagining how lending works. When you can approve and disburse a loan in 10 minutes versus 10 days, you're not just faster—you're playing a different game."

Large Addressable Market in Consumer and MSME Finance

India's credit-to-GDP ratio stands at roughly 55%, compared to 150%+ in developed markets. The underpenetrated market opportunity is massive. With 400 million people entering the formal credit system over the next decade, the growth runway is long.

"We're not fighting for market share in a mature market," argues a bull. "We're creating the market. Every small business getting its first formal loan, every young professional accessing organized credit—these are new customers, not switchers."

Brand Trust and Recognition

The Poonawalla brand, forged in the crucible of COVID vaccine delivery, carries unique trust. "When your brand is associated with saving lives, extending it to improving lives through credit makes sense," observes a brand consultant.

Market surveys show brand recognition above 70% in target markets, exceptional for a three-year-old financial services brand. Trust scores exceed established NBFCs, though still trail major banks.

Bear Case: The Cracks Are Showing

Execution Risks in Rapid Transformation

The bears point to mounting evidence of execution challenges. POONAWALLA FINCORP's gross NPA ratio stood at 1.8% as of 31 March 2025 compared to 1.2% in the same period a year ago. Rising NPAs during a benign credit environment raise red flags about underwriting quality.

"They're trying to do too much too fast," warns a skeptical analyst. "Building technology, changing culture, entering new products, expanding geographically—something has to give. The rising NPAs suggest credit quality is the casualty."

Asset Quality Concerns and Rising NPAs

The shift to unsecured lending, while profitable, increases risk. Secured to Unsecured on-book mix at 57:43 is moving toward higher-risk unsecured loans. In a downturn, unsecured portfolios deteriorate faster and recover less.

"They're picking up pennies in front of a steamroller," cautions a credit analyst. "Yes, unsecured loans have higher margins, but wait for the next credit cycle. The 2008 crisis destroyed NBFCs with similar strategies."

Intense Competition from Banks and Fintech Players

The competitive landscape is brutal. Banks like HDFC and Kotak have digital offerings matching any fintech. Pure-play digital lenders like PayTM and PhonePe have massive customer bases. Traditional NBFCs like Bajaj Finance have decades of experience.

"Where's the moat?" asks a bear. "Technology? Everyone has it. Brand? Banks are stronger. Cost of funds? Banks have CASA. Distribution? Fintechs have millions of app downloads. They're stuck in the middle."

Management Instability Issues

The appointment of new CEO Arvind Kapil in June 2024, while bringing fresh perspective, marks continued leadership changes. "Musical chairs in the C-suite is never good," observes a governance expert. "It suggests either the promoters can't delegate or the strategy keeps changing. Both are problematic."

The cultural integration challenges persist. Three years post-acquisition, reports of internal conflicts between old and new guard continue. "Culture eats strategy for breakfast, and their culture seems dysfunctional," notes a former employee.

Regulatory Risks in NBFC Sector

RBI's increasing scrutiny of digital lending practices poses risks. New regulations on interest rate disclosure, collection practices, and data privacy could impact profitability. "Regulators globally are cracking down on digital lenders," warns a regulatory expert. "India won't be different."

The lack of deposit-taking license remains a structural disadvantage. The company's deposits during FY25 stood at Rs 0 m. Complete dependence on wholesale funding means vulnerability to market cycles.

Valuation Concerns After Massive Stock Price Run-Up

Stock trading at 4.25 times its book value prices in perfection. Any disappointment could trigger massive corrections. "At these valuations, you're not buying a business, you're buying a dream," argues a value investor. "Dreams are fragile."

The price to earnings (P/E) ratio, at the current price of Rs 468.1, stands at -307.0 times its trailing twelve months earnings (due to losses). Traditional valuation metrics have broken down, suggesting speculation rather than investment.

The Balanced View

The truth, as often, lies between extremes. Poonawalla Fincorp has achieved remarkable transformation in three years—that's undeniable. The digital infrastructure is real, the brand value significant, the parental support substantial. These aren't small achievements.

But the challenges are equally real. Rising NPAs in a benign environment, management turnover, competitive pressures, and regulatory risks aren't going away. The valuation assumes flawless execution in an imperfect world.

The bull-bear debate ultimately comes down to time horizon and risk tolerance. Bulls betting on 10-year transformation might be right—India needs innovative lenders, and Poonawalla Fincorp could be one. Bears worried about next quarter's NPAs might also be right—the current trajectory seems unsustainable.

For investors, the question isn't whether Poonawalla Fincorp is good or bad—it's whether the current price adequately compensates for the risks. At 4.25x book value, the market is voting that transformation will not just succeed but exceed all expectations. History suggests such optimism is rarely justified, but then again, history also shows that occasionally, transformational companies do justify extreme valuations.

The next few quarters will be crucial. If NPAs stabilize, growth continues, and profitability returns, bulls will be vindicated. If asset quality deteriorates further, growth slows, and losses mount, bears will claim victory. Most likely, reality will be messier—some success, some failure, and a continued debate about what Poonawalla Fincorp really is: A transformational success story or an expensive experiment in financial engineering.

XII. Looking Forward: The Next Chapter

As Arvind Kapil, the newly appointed MD & CEO, looked out from the 20th floor of Poonawalla Fincorp's Mumbai headquarters in early 2025, the city sprawled endlessly—a metaphor for both opportunity and challenge. The company had come far from its Magma days, but the hardest part of transformation lay ahead: sustaining momentum while building profitability.

Strengthen Risk Management Framework

The immediate priority was clear. Strengthen risk management framework wasn't just a line in presentations—it was existential. With NPAs creeping up and the unsecured book growing, risk management needed fundamental overhaul.

"We're implementing a three-layer risk architecture," Kapil explained to his leadership team. "AI-powered early warning systems, human judgment for complex cases, and board-level risk committee oversight." The plan included hiring Chief Risk Officers for each product vertical, implementing real-time portfolio monitoring, and creating a 'risk war room' that would meet daily.

The company was also investing in alternative data sources—utility payments, mobile usage patterns, social media behavior—to enhance credit underwriting. "Traditional bureau scores tell you about the past. We need to predict the future," became the risk team's mantra.

The Path to Becoming a Systemically Important NBFC

With AUM crossing ₹40,000 crores, Poonawalla Fincorp was approaching the threshold for systemically important NBFC status. This would bring stricter regulations but also recognition as a major player. The company has AUM of ₹30,984 crore as on December 2024.

The implications were significant: higher capital requirements, stricter governance norms, closer regulatory supervision. But it also meant joining the big league—being mentioned alongside Bajaj Finance, Shriram Finance, and other giants.

"Systemic importance is both a responsibility and an opportunity," noted the CFO. "Yes, compliance costs increase, but so does credibility with investors and customers."

Potential for Banking License Aspirations

The ultimate prize remained tantalizing but distant: a banking license. While officially maintaining they were "focused on the NBFC model," insiders knew the long-term vision included becoming a bank.

The path wasn't easy. RBI's new bank licensing guidelines favored experienced financial institutions with proven track records. Poonawalla Fincorp would need at least 5-7 years of consistent performance, pristine asset quality, and demonstrated governance standards.

"A bank license would transform everything," admitted a strategy consultant working with the company. "Access to low-cost deposits, payment systems, full product suite—it's the holy grail. But RBI won't give licenses to entities with questionable asset quality or governance."

New Product Launches and Market Segments

The product roadmap was ambitious. The company now targets 40%+ annual AUM growth, propelled by new products like gold loans and shopkeeper loans. Gold loans offered secured lending with quick turnaround—perfect for the digital model. Shopkeeper loans targeted India's 15 million kiranas, largely excluded from formal credit.

"We're also exploring embedded finance," revealed the head of digital products. "Buy-now-pay-later at point of sale, supply chain financing for e-commerce, salary advance products for gig workers. The opportunity is massive."

Education loans were another frontier. With India's education financing gap exceeding $50 billion, and traditional banks retreating from the segment, opportunity beckoned. "We can use AI to predict employment outcomes and structure loans accordingly," explained the product team.

International Expansion Possibilities

While India remained the core focus, international opportunities emerged. The large Indian diaspora in the Middle East, Southeast Asia, and Africa needed financial services. Could Poonawalla Fincorp follow them?

"We're exploring partnerships in UAE and Singapore initially," confirmed a senior executive. "Not full-fledged operations, but lending to NRIs, remittance services, maybe wealth management. The Poonawalla brand resonates globally thanks to vaccines."

Regulatory complexities meant international expansion would be gradual. But with Indian companies increasingly going global, following them with financial services made strategic sense.

The Succession Question: Adar Poonawalla's Role

The elephant in the room was succession and governance. Adar Poonawalla, while Chairman, wasn't involved in daily operations. But his vision and capital commitment drove strategy. What happened when priorities shifted or next generation took over?

"Institutionalization is crucial," emphasized an independent director. "We need systems and processes that survive leadership changes. The company should run on principles, not personalities."

The recent CEO appointment suggested professionalization was underway. But family-run businesses in India struggled with truly professional management. Would Poonawalla Fincorp be different?

Technology and Innovation Roadmap

The technology agenda remained aggressive. At PFL, AI will emerge as a strategic differentiator and game-changer across core areas. Blockchain for supply chain financing, quantum computing for risk modeling, metaverse branches for younger customers—the innovation pipeline was full.

"We're building a technology company that happens to lend money," became the internal slogan. But technology required continuous investment. With 35 AI projects in pipeline and constant platform upgrades, technology spending would remain elevated.

Regulatory Evolution and Adaptation

The regulatory environment was evolving rapidly. Digital lending guidelines, data protection laws, ESG requirements—compliance complexity was increasing. The company needed to stay ahead of regulations, not react to them.

"We're engaging proactively with regulators," noted the compliance head. "Sharing our innovations, seeking guidance, participating in sandboxes. We want to be seen as responsible innovators, not regulatory arbitrageurs."

The Sustainability Challenge

ESG considerations were becoming crucial for institutional investors. Poonawalla Fincorp practices transparency in disclosing information about environmental, social, and governance implications. But concrete actions were needed beyond disclosures.

Financial inclusion became the sustainability narrative—providing credit to underserved segments, enabling entrepreneurship, supporting women borrowers. "Every small business loan creates jobs. Every education loan changes lives. That's our ESG story," argued the sustainability team.

Building for the Next Decade

Looking ahead, Poonawalla Fincorp faced a fundamental choice: continue aggressive growth accepting higher risks, or moderate ambitions focusing on profitability. The market wanted both, but delivering both simultaneously had proven challenging.

The vision remained ambitious. "We want to be India's most trusted financial services brand by 2030," declared the leadership. This meant 1 million+ customers, ₹100,000+ crore AUM, presence in 100+ cities, and most importantly, sustainable profitability.

But vision without execution is hallucination. The next chapter would be written not in boardrooms but in branches, not in strategies but in systems, not in presentations but in performance.

The story of Poonawalla Fincorp's next chapter remains unwritten. Will it become India's next great financial institution, leveraging technology and trust to democratize credit? Or will it become another cautionary tale of ambition exceeding capability?

The answer lies in execution—in thousands of daily decisions about which loans to approve, which technologies to adopt, which people to hire. It lies in navigating the inevitable economic downturns, regulatory changes, and competitive threats. Most importantly, it lies in maintaining the delicate balance between growth and prudence that defines successful financial institutions.

As the sun set over Mumbai that evening, Arvind Kapil knew the transformation was far from complete. In fact, the hardest part—building a sustainable, profitable, trusted financial institution—had just begun. The vaccine fortune had bought them a seat at the table. Now they had to prove they belonged there.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube