The Trail-Commission Machine: How PB Fintech Built India's Insurance Gateway

I. Introduction & Episode Roadmap

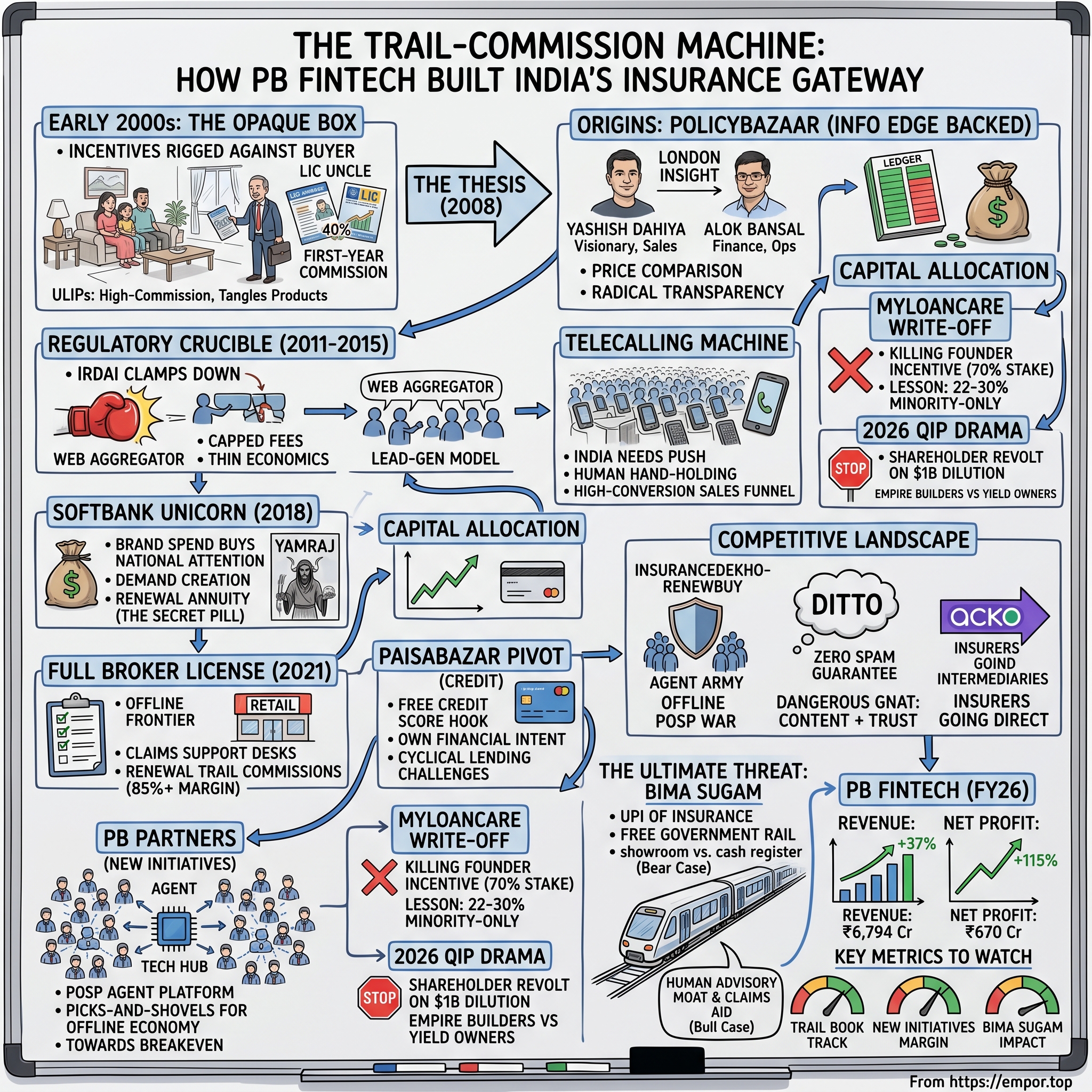

Picture a living room in suburban India in the early 2000s. The ceiling fan turns slowly. Tea is poured. And across the coffee table sits a man your family has known for years — the neighborhood "LIC uncle," the insurance agent who attends weddings, remembers birthdays, and arrives at exactly the moment your salary clears. He opens a glossy brochure, talks warmly about your children's future, and produces a form. You sign. What you have just bought, in most cases, is a Unit Linked Insurance Plan — a tangled hybrid of investment and insurance whose first-year commission, often 30 to 40% of your premium, has just disappeared into the uncle's pocket. You do not know this. You will not know it for years, possibly not until you try to make a claim and discover the fine print works against you.

This was the Indian insurance market: opaque, relationship-driven, and structurally rigged against the buyer. Insurance was not bought in India. It was sold — pushed, really — by an army of agents whose incentives pointed in precisely the wrong direction. The product that paid the agent the most was almost never the product the customer needed most.

Now fast-forward to 2026. A single listed company, PB Fintech — parent of Policybazaar and Paisabazaar — sits at the center of Indian insurance distribution. It commands the overwhelming share of online insurance aggregation. In the year ended March 2026, the platforms it operates channeled nearly ₹30,000 crore — roughly $3.5 billion — in total insurance premium, a 42% jump over the prior year.1 And buried inside that flow is the prize that consumer-internet founders dream about: a recurring, ultra-high-margin "trail commission" annuity, where the company collects a slice of every policy renewal for years after the sale, at margins north of 85%.2

This is one of the most fascinating business models in the public markets anywhere. It is part search engine — the place where the Indian middle class begins almost every insurance decision. It is part high-velocity sales floor — a telecalling operation so aggressive it became a cultural punchline. And it is part fintech ecosystem, with a credit marketplace, an agent-enablement platform spanning 99% of India's pin codes, and overseas ambitions stretching to Dubai.

It is also a company that, by all rights, should not exist. The Indian insurance establishment despised it. The regulator nearly strangled it in the cradle, issuing rules in 2011 that treated price-comparison websites as a threat to be contained rather than an innovation to be encouraged. Twice, PB Fintech's founders had to tear up the business model and rebuild it to survive a regulatory regime that kept moving the goalposts.

So how did a transparency-first comparison website — the kind of thing the entire industry was built to suppress — become the gatekeeper of Indian insurance? And now that it has finally turned the corner into staggering profitability, with consolidated operating revenue of ₹6,794 crore and net profit surging to ₹670 crore in FY26,1 is the moat real, or is the Indian government about to build a free public highway right around it?

Here is the roadmap. We start in the opaque box of early-2000s Indian insurance and the founder who saw a better way in London. We trace the regulatory crucible and the pivot into credit with Paisabazaar. We follow the SoftBank money, the legendary "Yamraj" ad campaign, and the telecalling machine. We dissect the single most important decision the company ever made — voluntarily surrendering its license to become a full broker. We do a hard post-mortem on capital allocation, from the MyLoanCare write-off to the 2026 fundraising drama. We war-game the competition — the InsuranceDekho–RenewBuy colossus and the tiny, dangerous, "anti-spam" disruptor Ditto. And we end with the question that hangs over everything: Bima Sugam, the government's "UPI of insurance," and whether it hollows out the entire model. Let's get into it.

II. The Origins: Scraping the Indian Insurance Opaque Box

Every origin story has a moment where the founder sees the thing that everyone else has stopped seeing. For Yashish Dahiya, that moment came not in India but in Europe.

Dahiya's résumé reads like a checklist of Indian meritocratic aspiration: IIT Delhi for engineering, IIM Ahmedabad for the MBA, then INSEAD in France, with a stint at Bain & Company in between. By the mid-2000s he was in London, running an online travel business called eBookers and later a venture in the price-comparison space. And it was there, immersed in the British internet economy, that he encountered something that did not exist back home: a website where you could see every insurer's quote for the same product, side by side, ranked by price, with nobody whispering in your ear. Moneysupermarket and its peers had made insurance a transparent, shoppable commodity in the UK. The contrast with India was almost violent. In London, the customer held the power. In Delhi, the agent did.

That contrast became the thesis. In 2008, Dahiya returned to India and, with co-founder Alok Bansal — a finance and operations mind who would become the yin to Dahiya's relentless sales-driven yang — launched Policybazaar.[^2] The initial ambition was almost charmingly modest by today's standards: not to sell anything, not to disrupt anyone, just to build a website that showed you what insurance products cost. Pure information. Pure transparency. Let the sunlight in and let customers decide.

The man writing the early cheques understood the bet better than anyone. PB Fintech's first institutional backer was Info Edge — the Sanjeev Bikhchandani-founded internet holding company best known for the jobs portal Naukri and, later, for an early stake in Zomato. Info Edge wrote Policybazaar one of its very first cheques around 2008 and held on through more than a decade of struggle, eventually owning a stake of roughly 19% by the time of the IPO.3 Bikhchandani's playbook — back a category-defining internet marketplace early, then sit on your hands for ten years while it compounds — was being run a third time, after Naukri and Zomato. That patient capital mattered enormously, because Policybazaar would need years of patience before it produced a single rupee of profit.

It is also worth introducing the second founder properly, because the company's character is a product of the pairing. If Dahiya was the evangelical, sales-obsessed front man — the kind of operator who measures his self-worth in conversion rates — Alok Bansal was the disciplined finance and operations counterweight, an alumnus of the same elite institutional circuit who would spend the next decade keeping the books, the unit economics, and the regulatory relationships from coming apart at the seams. Indian startups that endure tend to have this two-body structure: a visionary who sells the dream and a builder who makes the dream solvent. Policybazaar had both.

It is worth pausing on how radical the transparency idea was in the Indian context, because the structure of the market made it an act of war. Indian insurers — led by the state-owned behemoth LIC and a handful of private players — distributed almost entirely through human agents. Those agents were paid on commission, and the commission structure was lopsided toward the most profitable-for-the-insurer, least-good-for-the-customer products. The ULIP, that investment-insurance hybrid, was the worst offender: front-loaded fees, opaque charges, and first-year commissions so fat that an entire cottage industry existed simply to churn customers from one ULIP into another.

The timing made it worse. Policybazaar launched into the teeth of India's great ULIP reckoning. Around 2009 and 2010, the mis-selling of unit-linked plans had become so egregious — agents churning customers, surrender charges devouring savings, buyers discovering their "investment" had lost money to fees — that it triggered an open turf war between two regulators, with the securities regulator SEBI arguing these products were really mutual funds in disguise and the insurance regulator IRDAI defending its territory. The government ultimately settled it in IRDAI's favor and capped ULIP charges, but the episode laid bare exactly the rot Policybazaar's comparison engine threatened to expose. A generation of Indians had just been burned. They were primed, finally, to want transparency — even if the industry that had burned them was not ready to provide it.

A website that let a customer compare a ULIP's true cost against a plain, cheap term plan was, to the incumbent industry, financial heresy. If buyers could actually see that a ₹500-a-month term policy gave them ten times the life cover of a ₹5,000-a-month ULIP, the entire mis-selling economy would wobble. So the insurers did not exactly roll out the welcome mat. Many simply refused to share data, refused to integrate, and treated the upstart comparison site as a parasite. Policybazaar's early years were a grind of begging insurers for quote data and trying to convince a public that had never "shopped" for insurance that shopping was even possible.

And then, just as the model was finding its feet, the regulator arrived — not as a referee, but as a roadblock. Which is where the story turns from a startup tale into a survival saga.

III. The Regulatory Crucible & The Paisabazaar Pivot

The Insurance Regulatory and Development Authority of India — IRDAI — was not built to encourage disruption. It was built to protect a system of physical, agent-led distribution and to keep solvency-conscious order in a market where ordinary people were entrusting their life savings. To the regulator's eye around 2011, a "web aggregator" comparing policies and earning fees for sending leads to insurers looked less like progress and less regulated, and more like an unsupervised middleman inserting itself into a sensitive financial transaction.

So IRDAI clamped down. It built a formal regulatory cage around web aggregators, codified over the following years, that dictated exactly how comparison sites could display quotes, how they could rank them, and — most painfully — how much they could earn. The economics were deliberately thin. Aggregators were boxed into a lead-generation model: show the comparison, pass the customer to the insurer, collect a small, capped, regulated referral fee. The fat brokerage commissions that flowed to traditional agents were off-limits. Policybazaar had to re-architect its business to fit inside the cage, and for a stretch it survived on the regulatory equivalent of breadcrumbs.

Here is where Dahiya's defining insight as an operator emerged, and it is the opposite of the transparency dream he started with. He realized that in India, the romantic vision of customers calmly comparing policies and clicking "buy" was a fantasy. Indians did not buy insurance off a screen. They needed a human — to explain, to reassure, to follow up three times, and to close. Insurance in India was a push product, and no amount of clean web design changed that cultural fact.

So Policybazaar did something that, on paper, contradicted its founding ideals: it built a telecalling machine. The passive search directory grew a giant, tech-enabled call center bolted onto the front. When you entered your phone number to "see a quote," you were not really browsing — you were entering a high-conversion sales funnel staffed by trained agents who would call, and call again, until you converted. It was an uneasy marriage of Silicon Valley front-end and Indian boiler-room back-end, and it worked. The website generated the intent; the humans monetized it. This hybrid — digital demand generation plus human closing — became the company's DNA and, years later, the source of both its dominance and its reputational baggage.

The scale of that human layer is what most observers underestimate. This was never a few dozen people answering phones; it grew into thousands upon thousands of trained advisors, organized by product line, measured on conversion, and fed a constant stream of warm leads by the website. Running a sales floor of that size — hiring, training, scripting, quality-controlling, and retaining people in a high-churn industry — is an operational discipline most pure-internet companies never have to develop. It is unglamorous, it is expensive, and it is exactly the kind of capability that does not appear in a software company's cost structure. Whether you view this as a weakness (people don't scale like code) or a strength (the human layer is a moat competitors can't replicate overnight) is one of the central debates about the business, and we will return to it.

If the company already owned the customer's financial trust at the moment they were thinking about money, why stop at insurance? In 2014, PB Fintech launched its second pillar: Paisabazaar, a marketplace for credit — credit cards, personal loans, home loans.[^2] The logic was elegant. The hardest, most expensive thing in consumer finance is acquiring a customer who trusts you with their financial decisions. Policybazaar had already paid that acquisition cost. Paisabazaar simply asked: now that they trust us with insurance, why not lending?

Paisabazaar's cleverest move was figuring out how to acquire credit customers almost for free, and it did so with a deceptively simple product: the free credit score. Long before "check your CIBIL score" became a national reflex, Paisabazaar offered Indians a free, repeatable look at their credit health. The hook was psychological genius. People are anxious about their creditworthiness and will return monthly to check it, the way one checks a wound to see if it's healing. Each visit was a free, intent-rich touchpoint — a customer telling Paisabazaar, in effect, "I care about my credit and I might want to borrow." When the score was good, the platform could surface a pre-qualified loan or a card; when it was poor, it could nurture the customer toward improvement and capture them later. It turned a cost center — customer acquisition — into a recurring, trust-building habit, and it gave Paisabazaar a proprietary read on borrower quality that pure lead-buyers lacked.

Paisabazaar scaled into one of the largest digital credit-acquisition platforms in the country, becoming the front door through which a huge share of India's online loan and credit-card seekers passed. Total lending disbursals across the platform reached roughly ₹30,740 crore in FY26, up about 50% year over year.1 But credit also taught PB Fintech a brutal lesson about cyclicality that insurance never did. Lending-lead generation lives and dies by the banks' appetite to lend. And in late 2023, the Reserve Bank of India — worried about a frothy boom in unsecured consumer credit — raised the risk weights banks must hold against unsecured personal loans. Lenders pulled back almost overnight. The flow of easy personal loans that fed Paisabazaar's revenue thinned, hitting the segment hard through FY25 and forcing a rapid pivot toward secured products — loans against property, gold loans — where the unit economics are lower but the demand more durable.

It is worth dwelling on what the Paisabazaar pivot reveals about PB Fintech's deeper strategy, because it is the same move the company would run again and again. The insight is that the scarce, valuable asset is not insurance distribution or credit distribution specifically — it is financial intent at the moment of trust. Once you have a consumer's attention at the instant they are making a money decision, and once they believe you are on their side, you can sell them adjacent financial products at a fraction of the cost a cold competitor would pay. Insurance bought the trust; credit monetized it again; the agent platform and overseas markets would extend the same logic later. Every expansion was a variation on one theme: own the trusted financial front door, then keep widening what you can sell through it. The risk, of course, is that not every adjacency is as good as the last — credit's cyclicality proved that — but the underlying machine for entering new categories cheaply is genuinely rare.

It was a preview of a theme that recurs throughout PB Fintech's life: the regulator giveth, the regulator taketh away, and the survivors are the ones who can rebuild the engine while the plane is still flying. Which brings us to the moment the money arrived — and the engine got a lot bigger.

IV. SoftBank, Scale, and the Telecalling Machine

In June 2018, the most important phone call in Indian startup history was, metaphorically, ringing off the hook for everyone. Masayoshi Son's SoftBank Vision Fund — the $100 billion firehose that was, in those years, blasting capital into market-leading consumer platforms across the globe — turned its gaze to Indian insurance. SoftBank led a funding round of more than $200 million into Policybazaar, valuing the company at roughly $1 billion and minting it as a unicorn.4 Eight months earlier the company had been valued at around $500 million; the SoftBank round doubled that overnight.4

What do you do with a SoftBank-sized war chest in a push-product market? You buy the entire nation's attention. Policybazaar poured the capital into brand, and the centerpiece was one of the most memorable advertising campaigns in modern Indian television: "Yamraj," the Hindu god of death. In ad after ad, the mustachioed deity would materialize beside an oblivious middle-class husband, gesturing toward him and confronting the audience with the most effective insurance sales question ever devised: what happens to your wife and children if you are suddenly gone, and you have no cover? It was darkly funny, culturally resonant, and devastatingly effective. It took the abstract dread of mortality — the thing the LIC uncle used to monetize one living room at a time — and broadcast it to hundreds of millions of homes at once.

There was a subtler reason the campaign worked, rooted in a quirk of the product. Most things you advertise, the customer already wants — they just have to choose your brand. Insurance is different: the customer doesn't want it at all. The job of an insurance ad is not brand preference; it is demand creation — manufacturing the very desire to buy from scratch. "Yamraj" did exactly that. It took a thought most people actively suppress — my own death and what it would do to the people I love — and forced it into the open with enough dark humor that viewers laughed instead of changing the channel. That is a fundamentally harder marketing problem than selling soap, and solving it at national scale is why the spend translated into category ownership rather than just awareness.

The strategic genius was not the creative. It was the spend behind it. Policybazaar outspent essentially every competitor combined, and in doing so it bought something more valuable than any single sale: it bought search intent. By the late 2010s, when an Indian consumer began to think "I should get term insurance" or "I need health cover," the brand that surfaced in their mind — and then in their browser — was Policybazaar. The company effectively became the default top of the funnel for an entire category. That is a position you cannot easily rent; you have to buy it, expensively, over years, and then defend it. SoftBank's money let Policybazaar buy it before anyone else could.

But the funnel only converts because of the machine at the bottom of it, and here we have to be honest about the thing that made Policybazaar both dominant and disliked. If you entered your phone number on the site in the late 2010s, you did not get a quiet email. You got calls. Lots of them — by some users' accounts, ten calls within five minutes, then follow-ups for days. The outbound telecalling operation was a finely tuned conversion engine, optimized down to the script and the callback timing, and it printed sales. For a push product in a market that needed human hand-holding, it was arguably the correct strategy, and the financial results eventually proved it.

This is also where the bill came due. Owning national search intent through brand, and converting it through a small army of telecallers, is staggeringly expensive — and for years it meant Policybazaar was an enthusiastic cash-incinerator. The company outspent every rival combined precisely because it could; SoftBank-style capital let it inflate a customer-acquisition-cost bubble that competitors simply could not match, effectively pricing them out of the auction for the middle class's attention. Critics, not unreasonably, asked whether a business that spent two rupees to make one would ever invert the ratio. The answer, as it turned out, lay in a part of the model that the heavy upfront spend was quietly building but that didn't show up in the early P&L: every customer acquired at a loss today was a renewal annuity tomorrow. The spend looked insane on a single-year view and rational on a ten-year view — which is exactly the kind of bet that only patient capital and a founder with conviction can sustain through the years of red ink. Holding that conviction while the losses mounted, and while public-market investors fled in 2022, was the hardest thing management ever had to do.

Yet every strength casts a shadow. The relentlessness that drove conversion also branded Policybazaar, in the minds of a growing cohort of younger, urban, high-income customers, as "the spam company." You gave them your number once and you paid for it forever. That reputation seemed like a minor cost when conversion rates were soaring. But it quietly created a structural opening — a slot in the market for someone to come along and promise the exact opposite. We will meet that someone later. First, the company had to solve a deeper problem: it was leaving most of the market on the table, because it was legally forbidden from touching it.

V. The Direct Broker Pivot & The Physical Frontier

For all its dominance online, Policybazaar in 2020 was a giant standing on one leg. The web-aggregator license that had let it survive the regulatory crucible was also a cage with a low ceiling. As an aggregator, it could compare and refer, but it could not act as a full intermediary. It could not run physical branches. It could not put boots on the ground to help a grieving family file a death claim. And critically, it could not earn full brokerage commissions — it was stuck collecting thinner, regulated lead-generation fees while roughly 90% of India's insurance was sold, in person, by agents the company could not employ or earn from.

So in June 2021, Policybazaar made the boldest move in its history: it voluntarily gave up its web-aggregator license and obtained a full Direct Insurance Broker license from IRDAI.5 Dahiya later revealed the company had been courting the regulator for this for three years.5 On the surface it looked like a lateral bureaucratic swap. In reality it was the pivot of the decade, and it rewired the entire business.

Why did this change everything? Because a broker can do all the things an aggregator cannot. A broker can build offline networks. A broker can open retail storefronts where a customer can walk in, sit across from a human, and ask the questions they would never trust a website to answer. A broker can run physical claims-assistance desks — and in insurance, the claim is the only moment that actually matters, the moment when the entire promise is tested. And a broker can collect direct brokerage commissions on the policies it places, including the recurring renewal trail. The license transformed Policybazaar from a referral middleman into a full-stack intermediary that owns the customer relationship from the first comparison to the final claim payout.

The timing of the license was no accident either — it coincided with a structural shift in what Indians wanted to buy. The pandemic had done in two years what a decade of "Yamraj" advertising could not: it made health and term insurance feel urgent rather than optional. Suddenly the abstract god of death was at everyone's door, and demand for genuine "protection" products — pure term life and health cover, the low-margin-for-the-insurer, high-value-for-the-customer products that the old mis-selling economy had always neglected — exploded. These are precisely the products where advisory and claims support matter most, and precisely the products on which a broker can build a durable, renewing relationship. By FY26, protection products including health and term were the company's fastest-growing engine, with related premiums rising more than 50% year over year.1 The broker license let Policybazaar ride that wave with a full toolkit rather than a referral slip.

This is what unlocked the "phygital" strategy — physical plus digital. Policybazaar began opening physical points of presence across Indian cities, not to replace the website but to backstop it with trust. For a high-stakes, low-frequency, anxiety-laden purchase like life or health insurance, the existence of a real office you could visit, and a real human who would help with a claim, materially changed the conversion calculus. The website got you in the door; the physical infrastructure closed the trust gap that pure digital never could in India.

The claims piece deserves special emphasis, because it is the most underappreciated part of the whole strategy. In insurance, every promise is theoretical until the day you make a claim. That is the moment of truth — and historically, in India, it was also the moment of maximum dread, because the customer was alone against an insurer's claims department with every incentive to find a reason to deny. By building on-ground claims-assistance teams that advocate for the customer at exactly that moment, Policybazaar inverted the relationship. It stopped being just the place you bought the policy and became the entity that fought for you when it mattered. That is the kind of experience that turns a one-time transaction into a renewed relationship — and a renewed relationship, as we will see, is where all the money is. A customer who has been helped through a claim does not shop around at renewal; they stay. The broker license, in other words, did not just add revenue lines. It bought the company the right to earn customer loyalty in the only currency insurance customers truly value.

But the broker license solved only the company's own selling. It did nothing, by itself, about the vast offline army — the hundreds of thousands of individual agents in tier-2 and tier-3 towns who still control the majority of Indian insurance sales and who were never going to start their careers on Policybazaar.com. To capture them, the company built something different: PB Partners.

PB Partners is Policybazaar's POSP — Point of Sales Person — platform, and it is best understood as picks-and-shovels for the offline agent economy. Instead of competing with the neighborhood agent, PB Partners arms him. A local advisor logs into Policybazaar's technology, uses it to instantly quote and compare products from dozens of insurers, and issues the policy through the platform, splitting the commission. The agent gets a vastly better toolkit than any single insurer could give him; Policybazaar gets a slice of business it could never have reached from a screen.

This is not a side-plot. It is a heavyweight. PB Partners sits inside the "New Initiatives" segment, which in FY26 generated roughly ₹2,715 crore in revenue, growing about 43% year over year, and the platform had scaled to over 450,000 advisors present across 99% of India's pin codes — including the tier-4 and tier-5 towns where insurance penetration has historically been thinnest.6 The economics work like a B2B2C marketplace: the local agent supplies the relationship and the trust, Policybazaar supplies the technology and the insurer connections, and they share the commission. For years the segment ran at a loss as the company spent to acquire advisors and build coverage. But the operating leverage is now showing: adjusted EBITDA margins for New Initiatives improved from around –9% to about –4% in FY26, with management guiding the POSP losses toward near-zero in FY27.6 In plain terms, the land-grab phase is ending and the profit phase is beginning.

Owning both the online funnel and the offline agent network is a formidable position. But how a company spends its money is as revealing as how it makes it — and here PB Fintech's record is genuinely mixed.

VI. Capital Allocation & The M&A Playbook: The Post-Mortem of MyLoanCare & the QIP Drama

To understand PB Fintech's capital-allocation story, start at the moment it got the keys to the public market's vault. In November 2021, PB Fintech went public in one of the marquee Indian tech IPOs of that frothy season. The offering raised about ₹5,710 crore at an issue price of ₹980 per share — roughly ₹3,750 crore of fresh capital into the company plus an offer-for-sale that let early backers cash out — and the stock listed on November 15, 2021, jumping sharply on debut to trade well above its issue price.7 It was the era of the great Indian internet listing wave: Zomato had gone public months earlier, Nykaa and Paytm were in the same window, and public investors were, briefly, willing to pay almost any price for digital growth.

That euphoria did not last. Like nearly every name in that cohort, PB Fintech's stock cratered through 2022 as global rates rose and the market's appetite for unprofitable growth evaporated — the shares more than halved from their early highs, and Info Edge, the patient backer, watched a chunk of its paper fortune evaporate alongside it. The lesson, which management absorbed the hard way, was that the public market would no longer fund a story; it wanted profits. The path from that 2022 trough to the FY26 numbers we'll close on is the story of a company that grew up under public scrutiny. But first it had to make its mistakes — and the cash from that IPO funded the most instructive one.

Fresh off the listing and flush with public-market cash, PB Fintech went shopping. It acquired a 70.1% majority stake in MyLoanCare, a Gurugram-based loan aggregator, for about ₹40.41 crore.8 On paper it was a sensible bolt-on for the Paisabazaar credit business. In practice, it became the company's most instructive failure — a clean case study in how good intentions and a bad ownership structure destroy capital.

The problem was not the market or the product. The problem was incentives, and specifically what we might call the founder-incentive problem. The moment PB Fintech took a controlling 70% stake, MyLoanCare stopped being its founder's company. Gaurav Gupta, who had built the business over more than a decade, was now running someone else's asset, with a minority economic interest and majority of the upside flowing elsewhere. The fire that makes founders work like their lives depend on it — because financially, they do — was structurally extinguished. Gupta exited as CEO in early 2024.8 The business burned cash, hit liquidity trouble, and PB Fintech was ultimately forced to impair the investment, writing down roughly ₹44.62 crore — more than the original purchase price once follow-on funding was included.8

What makes this episode admirable rather than merely embarrassing is how candidly Dahiya owned it. He publicly called majority acquisitions a weak spot and drew a precise, quantified lesson: 70% was the wrong number. The right number, he argued, sits somewhere around 22–30% — enough to matter strategically, but small enough that the founder still owns the outcome and still runs the business like it's theirs, because it is.8 PB Fintech codified this into an explicit "minority-only investment" policy, and has applied it to subsequent bets such as its stake in the healthtech firm Visit Health. It is a rare thing to watch a company convert a write-off into a permanent governing principle. The MyLoanCare loss was small in rupees; the discipline it bought was not.

There is a broader investing lesson buried here that applies far beyond PB Fintech. The single most common way acquirers destroy value in founder-built businesses is by buying control and inadvertently killing the thing they paid for — the founder's obsessive ownership. A founder running a 70%-owned subsidiary for someone else's balance sheet is a salaried manager who happens to have started the company; the asymmetry of upside that made them extraordinary is gone, and what remains is, predictably, ordinary. The genius of the 22–30% minority frame is that it threads the needle: large enough that the founder takes your call and aligns strategically, small enough that they still wake up every morning owning the vast majority of their own outcome. It is the difference between buying a business and renting access to a motivated founder's energy — and PB Fintech learned, at a tuition of roughly ₹45 crore, which one actually compounds.

That discipline got tested again in early 2026 — this time over a far larger sum, and in full public view. In February 2026, reports emerged that PB Fintech was preparing to raise around $1 billion through a Qualified Institutional Placement to fund an aggressive global M&A push.9 The market's reaction was not gratitude. It was a revolt. Shareholders dumped the stock — trading volumes spiked to multiples of the normal daily average as investors voted with their feet — and the share price slid double digits.9

The investor logic was straightforward and, frankly, hard to argue with. Why dilute existing shareholders by a billion dollars when the company was already sitting on a substantial cash pile and finally minting real profits? A QIP issues new shares; new shares shrink every existing holder's slice. And the stated use — overseas acquisitions, a category in which this very management had just impaired its last big buy — did not inspire confidence. The proposed deal looked, to many holders, like founders with global ambitions reaching for the dilution lever right after promising shareholder-friendly discipline. PB Fintech hit pause, publicly stating that neither the board nor management was pursuing a QIP at that time, and signaling it would consult shareholders before revisiting the idea.9 Reports later suggested the company might revive the raise once it had completed that outreach.10

The episode crystallized the central tension in PB Fintech as a public company: the founders think like empire-builders — UAE expansion, a reinsurance ambition in GIFT City, a billion dollars of dry powder for global deals — while a meaningful slice of their shareholder base now thinks like yield-conscious owners who would rather see that cash compound inside a proven, high-margin domestic machine. Whose vision wins will shape the next decade. And the urgency of the empire-building is sharpened by what is happening on the competitive battlefield back home.

VII. The Core Engine: Competitive Landscape & The "Anti-Sales" Ditto Threat

For most of its life, Policybazaar's competitive worry was diffuse — a long tail of small aggregators and the offline incumbents. That changed in 2025, when the fragmented field consolidated into a genuine second pole. InsuranceDekho, the insurtech spun out of the Girnar (CarDekho) group, agreed to merge with RenewBuy in a share-swap deal valuing the combined entity at roughly ₹7,400 crore.11 The merged business was set to command a premium book of around ₹6,000 crore — roughly five times the standalone scale of either platform — instantly creating the clear number two in Indian insurance distribution.11

Here is what makes the rivalry interesting: the two giants are strong in different terrain. Policybazaar owns the online aggregator search — the digital top of the funnel, the place where urban, English-reading, self-directed buyers begin. The InsuranceDekho–RenewBuy combine, by contrast, is built on the physical, agent-led POSP model, dominant in the tier-2 and tier-3 towns where insurance is still sold face to face by a local advisor who speaks the customer's dialect. The merger created a single entity with the scale to fight PB Partners hand-to-hand for those hundreds of thousands of small-town agents. The battle for online intent is largely settled in Policybazaar's favor; the battle for the offline agent network is now a real war between two well-capitalized armies.

But the threat that should keep management up at night is not the giant. It is the gnat — a tiny, surgically precise competitor named Ditto Insurance, built by the team behind the wildly popular Finshots financial newsletter and backed by Zerodha's Rainmatter fund.12 Ditto is a direct, almost philosophical, attack on the thing that made Policybazaar rich: the telecalling machine.

Ditto's entire pitch is a refutation of the spam reputation. It guarantees zero spam — no outbound sales calls, ever. If you want advice, you book an appointment with an advisor; the company does not chase you. And here is the masterstroke: Ditto's advisors are paid flat salaries with no sales commissions whatsoever. That single design choice realigns the entire incentive structure. The advisor has no reason to push you toward the highest-commission product, because there is no commission. They are paid to give you honest advice, including "you don't need this policy." In a market historically defined by mis-selling, that is a radical promise — and it is precisely the promise Policybazaar structurally cannot match, because its conversion machine runs on outbound contact and commissioned closing.

The economics underneath are quietly lethal. Ditto acquires customers almost for free by piping them from the Finshots newsletter's enormous organic readership — a captive audience of exactly the financially literate, high-income, telemarketing-averse millennials who most resent the old model. While Ditto remains small — revenue was around ₹52 crore in FY24, a rounding error against PB Fintech's thousands of crore12 — its customer-acquisition cost advantage and its trust with the most desirable demographic make it a reputational threat far larger than its revenue suggests. It cannot beat Policybazaar on scale. It does not need to. It just needs to make "Policybazaar" a synonym for the past among the customers of the future.

What makes Ditto genuinely instructive — and not just a feel-good underdog story — is that it represents a different theory of customer acquisition. Policybazaar's model is interruption: buy attention through advertising, then convert it through outbound contact. Ditto's model is permission: earn attention by giving away genuinely useful financial education through Finshots, build trust over months of free reading, and let the customer raise their hand when they're ready. The first model scales with capital; the second scales with content and patience. For most of internet history the interruption model won, because it was faster and capital was cheap. But as customers grow allergic to spam and as a media property can compound an audience over years, the permission model develops a structural cost advantage that capital cannot easily buy back. Whether that advantage stays niche or eventually scales is, honestly, the most interesting open question in the whole competitive set — and it is one Policybazaar's own DNA makes it poorly suited to answer.

There is a third front in this war that operates by an entirely different logic: the insurers themselves going direct. The clearest example is ACKO, a digital-first general insurer that manufactures its own products and sells them straight to consumers, deliberately cutting out distributors to avoid paying commission and to own the customer relationship end to end. ACKO is not an aggregator competing for the same listing slot; it is a supplier that has decided it would rather not be on the shelf at all. For Policybazaar, this is the more philosophically threatening model, because it attacks the premise that an intermediary needs to exist. The counterargument — and it is a strong one — is that direct-to-consumer insurance still has to solve the same brutal demand-creation problem that "Yamraj" solved, and most insurers are simply not good at marketing to a public that doesn't want their product. Building your own demand engine is expensive and slow; renting Policybazaar's is fast. So the largest, most marketing-capable insurers may peel away to go direct, while the long tail stays dependent on the aggregator. The supplier power is real, but it is concentrated, not universal.

Step back and the competitive map has three distinct theaters. Online intent: Policybazaar dominates, and that is largely decided. The offline agent network: a genuine two-army war between PB Partners and the InsuranceDekho–RenewBuy combine, still being fought town by town. And the war for the next generation's trust: a quiet, asymmetric skirmish where a tiny salaried-advisor model and a handful of direct insurers are nibbling at the most attractive customers. The incumbent is winning two of three handily. It is the third — the reputational, trust-and-incentives war — where its own legacy machine is its biggest liability. This is textbook counter-positioning, and it sets up the framework discussion perfectly: a small entrant succeeding precisely because the incumbent cannot copy it without breaking its own model.

VIII. Playbook: Hamilton's 7 Powers & Porter's 5 Forces Applied

Let's run PB Fintech through the two frameworks every business-strategy nerd reaches for, because the company is an unusually clean illustration of where its moat is deep and where it is alarmingly shallow.

Start with Hamilton Helmer's 7 Powers. The first and most obvious is scale economies, and here the power is high. Policybazaar's dominant share of online insurance search lets it spread its two largest costs — the brand advertising that buys national intent, and the technology platform that powers comparison and issuance — across a vastly larger base of policies than any rival. The "Yamraj"-era ad spend per acquired customer falls every year the brand stays dominant; a sub-scale competitor trying to buy the same intent pays a far higher unit cost. That is a self-reinforcing advantage as long as the company stays on top of the funnel.

Second, network effects, at medium power. Policybazaar is a two-sided marketplace: more customers attract more insurers, and a fuller roster of insurers attracts more customers. The telling proof is that even the most reluctant suppliers — including the state-owned giant that spent years resisting comparison platforms — eventually have to list, because the platform is where the buyers are. But this power is only medium, not high, because the network is not exclusive: insurers can and do list on multiple platforms simultaneously, so the effect concentrates demand without truly locking suppliers in.

Third — and this is the real magic — switching costs, expressed through what we'll call the renewal flywheel. When a customer buys a policy through Policybazaar, the renewals tend to flow back through Policybazaar automatically, year after year. On those renewals the company collects a trail commission at margins above 85%, and for products like health and life that trail can persist for a decade or more.2 The result is an annuity-like stream that compounds with every new cohort sold. This is why the company's profitability inflected so violently once the book matured: the renewal/trail run-rate grew from about ₹436 crore to ₹633 crore in a single year through FY25, with management guiding it toward roughly ₹800 crore exiting the year.2 Each year's new sales don't just add new revenue; they add a new layer of near-permanent, near-free-margin renewal revenue on top of all the prior layers. That stacking is the closest thing in Indian consumer fintech to a true compounding machine.

The simplest way to picture it: imagine a landlord who pays a large, one-time cost to build an apartment, and then collects rent on it every year for fifteen years with almost no further effort. The build cost — the advertising and the telecaller's time to win the customer — is painful and front-loaded. But once the policy is sold and the customer renews on autopilot, each year's trail commission arrives at the company's door requiring essentially no new spending; it is rent on work already done. Now imagine building a new apartment every year, on top of all the apartments you've already built, each one quietly paying rent. After a decade you are collecting fifteen vintages of rent simultaneously while only paying to build the newest one. That is the renewal book, and it is why a business that looked like a bottomless money pit during its building years flipped so suddenly and so violently into profit once the back catalogue of policies grew large enough to throw off more rent than the new builds cost to acquire. The danger, naturally, is anything that interrupts the rent — a customer who lets a policy lapse, a competitor who poaches the renewal, or a government rail that lets the tenant pay rent to someone else. Which is the entire reason the next question matters so much.

Fourth, counter-positioning — which is low power for PB Fintech, and is in fact being wielded against it. As we just saw, Ditto's salaried, no-outbound, no-commission model is something Policybazaar cannot replicate without dismantling the very telecalling engine that drives its conversions. That is the classic counter-positioning trap: the incumbent declines to copy the entrant not because it can't see the strategy, but because copying it would cannibalize its own profit model. It is the one power in the framework where PB Fintech is on the wrong side.

Two more powers deserve a mention. Brand is real but partial: "Policybazaar" is genuinely synonymous with insurance comparison for hundreds of millions of Indians, which lowers acquisition cost and lends credibility to a high-trust purchase — yet the same brand carries the spam baggage that Ditto exploits, so it is an asset with an asterisk. And process power — the accumulated, hard-to-copy organizational know-how of running a tech-plus-human conversion machine at massive scale, integrating with dozens of insurers' creaky back-end systems, and managing claims advocacy across thousands of agents — is underrated. None of that is glamorous, and none of it shows up in a pitch deck, but it is the kind of operational moat that takes a competitor a decade of trial and error to rebuild. It is also exactly what a government rail, however well-funded, cannot simply legislate into existence.

This is the right place for a quick myth-versus-reality check, because the consensus story about Policybazaar is lazy in two directions. The bull myth is that it's a pure, capital-light internet platform with software margins — reality: it is a heavily human business, with thousands of telecallers and claims staff and a sprawling offline agent network, and its profitability comes less from software economics than from the renewal annuity stacking on top of a costly acquisition machine. The bear myth is that it's just a glorified lead-generation site with no moat — reality: the broker license, the claims infrastructure, the renewal trail, and the process power add up to something far stickier than a comparison page. The truth sits in the uncomfortable middle: a real moat, built on a cost structure that is heavier and a model that is more human than the "internet platform" label implies.

Now Porter's Five Forces, briefly. Threat of new entrants is low: replicating Policybazaar means building a national consumer brand, securing a hard-won broker license, and integrating with 50-plus insurers — a decade-long, capital-soaking endeavor. Bargaining power of suppliers is medium-to-high: the largest, most digitally native direct insurers — a player like ACKO, for instance — can and sometimes do bypass aggregators entirely, selling direct to own the customer and dodge the commission. The more an insurer believes it can build its own demand, the less it needs Policybazaar. And the threat of substitutes is the existential one — high enough to deserve its own section, because the substitute in question is not a competitor at all. It is the government.

IX. Bear vs. Bull & The Ultimate Threat: Bima Sugam

Here is the scenario that defines the bear case, and it does not come from InsuranceDekho or Ditto. It comes from a government-backed digital public infrastructure project called Bima Sugam — billed, in the now-standard Indian shorthand, as the "UPI of insurance."

To understand why that phrase is both a promise and a threat, you have to understand UPI. India's Unified Payments Interface was a government-sponsored public rail that made digital payments instant, interoperable, and effectively free — and in doing so, it commoditized payments and squeezed the intermediaries who had once charged fees to move money. Bima Sugam aims to do the same for insurance: a single, centralized, low- or zero-commission portal where any citizen can buy, renew, and — crucially — settle claims across every insurer, as a piece of national infrastructure rather than a profit-seeking middleman.

The bear case writes itself. Today, part of what a customer pays in premium funds the brokerage commission that flows to a distributor like Policybazaar. If Bima Sugam lets insurers offer the identical policy with that distribution margin stripped out, the same coverage could appear on the government rail at a meaningful discount — perhaps 15-20% cheaper. In that world, the rational customer uses Policybazaar to do what it does best, compare and research, and then completes the actual transaction on Bima Sugam to pocket the saving. Policybazaar becomes the showroom while the government becomes the cash register — the worst possible position for an intermediary. The high-margin renewal trail, the very flywheel we just praised, would erode as renewals migrate to the free rail. This is a genuine, structural risk, and any honest investor has to hold it front of mind.

The bull case rests on a single, deeply Indian truth that has been the through-line of this entire story: insurance is still a push product. Consumers do not wake up wanting to buy term or health insurance the way they wake up wanting to pay a merchant. They have to be found, educated, nudged, reassured, sold, and — at the only moment that truly counts — helped through a claim when they are grieving or sick or frightened. Bima Sugam can be a brilliant rail. What it cannot easily replicate is the human advisory and claims-support apparatus — a network running to the order of 15,000 people — that Policybazaar has spent fifteen years and enormous capital building. A free pipe does not sell a reluctant customer, and it does not sit on the phone with a widow walking her through a death claim. If anything, a frictionless public rail could lower the industry's cost of fulfillment while leaving the hard part — demand generation and trust — exactly where it sits today, with the distributors who own the relationship. The bull would argue Bima Sugam commoditizes the plumbing PB Fintech never wanted to own anyway, while leaving the high-value advisory layer intact.

It is worth pressure-testing the UPI analogy itself, because analogies smuggle in conclusions. When UPI commoditized payments, it did hollow out the economics of moving money — but payments were a genuinely low-value-add, high-frequency utility that nobody enjoyed and everybody did constantly. Insurance is the inverse: high-value-add, low-frequency, emotionally fraught, and something nobody does without prompting. The very features that made payments perfect for a free public rail — frequency, simplicity, the customer already wanting to transact — are absent in insurance. A rail works brilliantly when the demand already exists and only the plumbing is friction. It works far less well when the hard part is manufacturing the demand and holding the customer's hand through fear and complexity. That asymmetry is the crux of the bull case, and it is why thoughtful skeptics of the bear case argue Bima Sugam may end up resembling the account-aggregator framework — useful infrastructure that quietly improves the back end without dethroning the customer-facing brands. But it is genuinely unknowable today, and an intellectually honest investor holds both scenarios at once rather than pretending the question is settled.

Which view is right will not be settled for years, and it depends heavily on execution details of a government platform that, as of mid-2026, is still maturing. What is not in doubt is who is steering PB Fintech through it. Yashish Dahiya remains Group CEO, holding roughly 3.3% of the company, with Alok Bansal as Executive Vice-Chairman holding around 0.9%. Their alignment with shareholders is real but unusual in shape: both men drew eye-watering compensation in FY25 — Dahiya around ₹641.3 crore and Bansal around ₹247.9 crore — figures driven almost entirely by the fair value of stock options exercised, not cash salary.13 That distinction matters, because the same dynamic explains the steady drumbeat of founder share sales that periodically spooks the market, such as the block deal in late May 2026 in which the two co-founders together sold about 0.82% of the company for ₹665 crore to a roster of institutions including Goldman Sachs and Morgan Stanley.14 On the surface, founders selling looks like a vote of no confidence. The company's explanation is more prosaic: exercising those massive ESOPs triggers enormous personal Indian tax liabilities, and a substantial portion of the share sales simply funds the tax bill rather than signaling an exit. Investors should watch the pattern, but it is consistent with mechanics, not flight.

A few overhangs belong on any honest watch-list. The first is regulatory: as a licensed broker, the company operates under IRDAI's continuous supervision, and that supervision has teeth — a PB Fintech unit has been fined by the regulator before, a reminder that the same authority that nearly strangled the company in 2011 still holds the pen.16 The second is the heavy reliance on stock-based compensation, which is real economic cost even when it doesn't hit cash, and which dilutes shareholders steadily; the eye-popping FY25 founder pay figures are the visible tip of a broader ESOP expense that investors should track against operating profit. And the third is governance optics around the steady founder selling — defensible on tax mechanics, but worth monitoring for any change in pace or explanation. None of these is disqualifying. All of them are the ordinary cost of owning a founder-led, regulator-bound, equity-incentivized growth company, and naming them is simply the price of clear sight.

It is also worth taking the founders' global ambition seriously rather than dismissing it as empire-building, because there is early evidence it can work. PB Fintech's UAE business — replicating the Policybazaar model for the Gulf's large, insurance-hungry expatriate population — turned full-year profitable for the first time in FY26, with premium there growing more than 50% year over year.1 That is a meaningful proof point: the model is not uniquely Indian; it can be exported to markets with the same structural problem of opaque, push-sold insurance. Layered on top is an ambition in GIFT City, India's nascent international financial center, where the company has eyed reinsurance broking — a higher-up-the-value-chain, institutional business that would diversify it beyond retail distribution as global reinsurance capital flows into the zone.15 This is the optionality the QIP was meant to fund. The bull would say: a management team that just proved it can export the model and is reaching for adjacent, higher-margin pools deserves dry powder. The bear would counter: this is the same team that bought MyLoanCare, and overseas M&A is where focused operators go to lose money. Both can be true, which is precisely why the 2026 fundraising standoff was so charged — it was a referendum on whether to trust the founders with a second act.

And the financial backdrop against which all this plays out is the most remarkable transformation in the story. This was a company that, just a few years ago, was a celebrated cash-incinerator, posting quarterly losses in the hundreds of crore as it bought a nation's attention. In FY26 it reported consolidated operating revenue of ₹6,794 crore, up roughly 37%, with net profit surging about 115% year over year to ₹670 crore and the net margin widening from 6% to about 10%.1 The shape of that math is the whole thesis in miniature: revenue grew fast, but profit grew more than three times faster. That gap is operating leverage — the renewal trail and the maturing New Initiatives book dropping through to the bottom line at high incremental margins while the costly acquisition machine that built the base stays roughly fixed. A company that can grow profit at multiples of revenue is, by definition, climbing a leverage curve, and PB Fintech has clearly stepped onto it. The question for the next decade is not whether the leverage is real — FY26 settled that — but how long the curve runs before competition or Bima Sugam flattens it. The single most important number for a long-term owner to track from here is not headline revenue; it is the trajectory of that high-margin renewal/trail book, because it is the truest measure of whether the moat is compounding or eroding. Two secondary gauges round out the dashboard: the New Initiatives segment's march toward breakeven, which tests whether the offline land-grab can become profitable rather than merely large; and any concrete progress on Bima Sugam, which is the one external variable that could change the entire thesis. Watch those three, and you are watching the business.

X. Outro & Epilogue

There are three lessons in the PB Fintech story that outlast any single quarter, and they are worth holding onto regardless of where the share price goes from here.

The first is the power of moving up the value chain at the right moment. PB Fintech spent its first decade as a tightly regulated intermediary, boxed into a thin lead-generation model by a regulator that viewed it with suspicion. The decision to surrender the comfortable web-aggregator license and become a full broker was, in hindsight, the hinge on which the entire business turned — it converted a referral service into an ecosystem owner that controls the customer from first quote to final claim, and it unlocked both the physical frontier and the renewal trail that now drive the profits. Founders rarely give up a license that defines them; the willingness to do so when the larger prize demands it is what separated PB Fintech from the competitors it left behind.

The second is the discipline to recognize a capital-allocation error early and convert it into a permanent rule. The MyLoanCare write-off was small in absolute terms, but management's response — naming the mistake publicly, diagnosing the founder-incentive problem precisely, and codifying a minority-only investment policy — turned a loss into institutional wisdom. The 2026 fundraising reversal showed that lesson is still being tested, with founders' empire-building ambitions running ahead of shareholders' appetite for dilution. How that tension resolves will tell us a great deal about whether the discipline holds.

And the third is simply the extraordinary, almost hypnotic, operating leverage of a renewal trail-commission book. A business that collects 85%-plus margins on payments it did almost nothing to earn this year, stacked on top of every cohort it ever sold, is the kind of compounding annuity that most companies can only dream of building. The open question — the one Bima Sugam poses and the next several years will answer — is whether that annuity is a fortress or merely a toll booth on a road the government is about to make free.

For listeners who want to go deeper, the richest primary sources are PB Fintech's own investor-relations disclosures and annual reports, the SEBI prospectus filings from the 2021 IPO, and the company's quarterly results — all of which lay out the segment economics in far more detail than any secondary coverage. Thanks for reading.

References

-

PolicyBazaar parent PB Fintech posts record FY26 revenue of Rs 6,794 crore — Indian Startup News, 2026 ↩↩↩↩↩↩

-

Policybazaar parent PB Fintech's Q2 FY25 profits soar on the back of insurance premiums — YourStory, 2024-11 ↩↩↩

-

Info Edge founder wants a hat-trick after Zomato, PolicyBazaar success — Business Standard, 2020-09-01 ↩

-

SoftBank Group's Vision Fund invests over $200 million in PolicyBazaar — Business Standard, 2018-06-25 ↩↩

-

Policybazaar gets insurance broking licence from IRDAI — India TV News, 2021-06 ↩↩

-

PB Fintech Hits Record Rs 6,794 Cr Revenue, Profit Jumps in FY26 — Whalesbook, 2026 ↩↩

-

PB Fintech (Policybazaar) IPO — Date, Price, Issue Details — Chittorgarh, 2021-11 ↩

-

PB Fintech to steer clear of majority-stake acquisitions following MyLoanCare experience — M&A Critique ↩↩↩↩

-

PB Fintech Cancels QIP Plan After Shareholder Backlash — Inc42, 2026-02-06 ↩↩↩

-

PB Fintech Is Said to Revive $1 Billion Fundraise After Outreach — Bloomberg, 2026-02-06 ↩

-

InsuranceDekho–RenewBuy Merger: India's new phygital insurtech powerhouse — YourStory, 2025-11 ↩↩

-

Ditto | The fintech trying to be human — Z-Connect by Zerodha ↩↩

-

India's Top 5 Highest-Paid CXOs FY25 — Channel iam, 2026-05-25 ↩

-

Co-founders of Policybazaar parent PB Fintech sell 0.82% stake for ₹665 cr — Business Standard, 2026-05-30 ↩

-

GIFT City is attracting global reinsurance capital at scale, says PB Fintech's Singh — Reinsurance News, 2026 ↩

-

India insurance regulator fines PB Fintech unit 50 million rupees — MarketScreener ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube