PNC Infratech: Building India's Infrastructure Backbone

I. Cold Open & Episode Roadmap

The year is 2015. India's infrastructure sector lies in ruins. Banks are drowning in non-performing assets worth billions. Construction giants that once commanded sky-high valuations are trading at bankruptcy levels. IL&FS, the infrastructure financing behemoth, would soon collapse in a spectacular ₹91,000 crore implosion. Yet here stands a relatively unknown company from Agra—not Mumbai, not Delhi, but Agra—preparing to go public at a valuation of nearly ₹2,000 crores.

The bankers are skeptical. "Another infrastructure IPO? In this market?" The road shows are tough. Fund managers pepper the management with questions about debt, about government receivables, about why they're different from the dozens of infrastructure companies that have already blown up. The founder, Pradeep Kumar Jain, a first-generation entrepreneur who started with small road contracts in Uttar Pradesh, sits calmly through each session. He has a simple message: "We don't chase growth at any cost. We chase cash flows."

Fast forward to today. PNC Infratech commands a market capitalization of ₹7,878 crores. Revenue stands at ₹6,769 crores with profits of ₹815 crores. While many of its peers from that era have vanished or restructured, PNC has quietly built and operated over 90 major infrastructure projects across 13 states. The company that started with a single road contract in Agra now manages everything from highways to water treatment plants, from airport runways to power transmission lines.

But here's the real question that matters: How did a regional construction firm founded at the turn of the millennium navigate India's treacherous infrastructure landscape—surviving policy U-turns, funding crises, and sectoral meltdowns—to emerge as one of the country's most resilient infrastructure players? And more importantly, what can investors learn from PNC's playbook about building wealth in capital-intensive, government-dependent businesses?

This is a story about patience in an impatient market. About conservative growth when everyone else was leveraging to the hilt. About understanding that in infrastructure, the tortoise often beats the hare—especially when the hare doesn't make it to the finish line. Let's dive into how PNC Infratech built its empire, one road at a time.

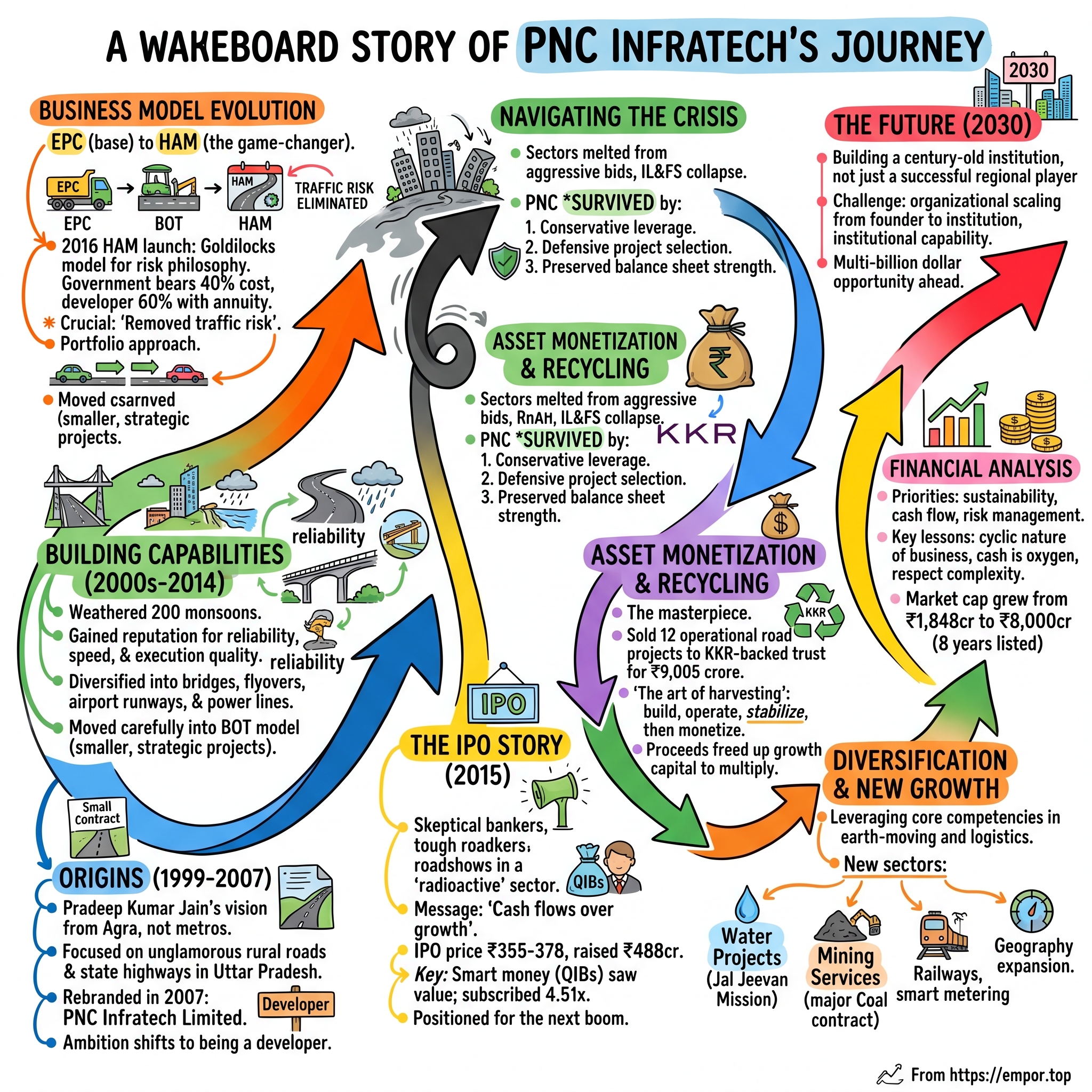

II. Origins & The Infrastructure Opportunity (1999–2007)

The morning sun rises over the Yamuna River in Agra, casting long shadows across the construction sites dotting the city's outskirts. It's August 9, 1999. While tourists flock to the Taj Mahal just a few kilometers away, a quiet registration takes place at the Registrar of Companies office. PNC Construction Company Private Limited is being incorporated—another small construction firm in a city already crowded with contractors hoping to ride India's infrastructure wave.

The timing couldn't have been more prescient. Just five months later, on a foggy January morning in 1999, Prime Minister Atal Bihari Vajpayee would lay the foundation stone for what would become India's most ambitious infrastructure project: the Golden Quadrilateral. This 5,846 km network of highways would connect Delhi, Kolkata, Mumbai and Chennai, fundamentally reshaping India's economic geography. For a small construction company in Agra, strategically positioned on the Delhi-Kolkata corridor, this represented the opportunity of a lifetime.

Pradeep Kumar Jain, the founder of PNC Infratech, understood something fundamental about India's infrastructure landscape that many missed. While larger players chased mega-projects in metros, Jain focused on the unglamorous but steady work of building state highways and rural roads in Uttar Pradesh. He wasn't trying to build an empire overnight—he was building capabilities, relationships, and most importantly, a track record of execution.

The India of 1999 was a nation bursting with ambition but constrained by its crumbling infrastructure. Road transport accounted for 65% of freight movement and 80% of passenger traffic, yet most highways were narrow, potholed arteries barely capable of handling the growing traffic. The government's solution was audacious: ₹540 billion would be invested to develop 13,150 km of four and six lane highways. For construction companies, this wasn't just a project—it was a gold rush.

But Agra? Why would a company choose to start in a tier-2 city known more for its Mughal monuments than its business dynamism? The answer lay in geography and strategy. Agra, where PNC Infratech is headquartered, sits at the intersection of major north-south and east-west corridors. It's close enough to Delhi to access decision-makers but far enough to avoid the capital's cutthroat competition and inflated costs. More importantly, the company could build deep relationships with state government officials and local contractors—relationships that would prove invaluable as India's infrastructure boom unfolded.

The company was converted into a limited company in 2001 and was renamed PNC Infratech Limited in 2007, reflecting its evolution from a pure construction play to an infrastructure developer. This wasn't just a name change—it signaled a fundamental shift in ambition. While others were content being contractors, PNC wanted to be a developer, operator, and asset owner.

The early 2000s were heady days for India's infrastructure sector. The Golden Quadrilateral project, originally planned for completion by December 2004, was creating opportunities across the value chain. But it wasn't just about the national highways. State governments, inspired by the central government's push, launched their own road development programs. Industrial corridors needed connectivity. Power plants needed transmission lines. Airports needed runways.

For PNC, this meant diversification from day one. While the company cut its teeth on road projects, it quickly expanded into bridges, flyovers, power transmission lines, and airport runways. This wasn't empire-building for its own sake—it was risk management. In infrastructure, depending on a single type of project or a single client is a recipe for disaster when policies change or budgets dry up.

By 2007, when the company rebranded as PNC Infratech Limited, India's infrastructure sector was entering a new phase. The easy projects were done. The sector was moving from simple EPC (Engineering, Procurement, Construction) contracts to more complex BOT (Build-Operate-Transfer) models. This required not just construction capabilities but financial engineering, risk management, and operational expertise. Many companies stumbled at this transition. PNC thrived, setting the stage for what would become one of India's most resilient infrastructure stories.

III. Early Growth & Building Capabilities (2000s–2014)

The monsoon of 2003 brought more than rain to India's highways. It brought chaos. Contractors abandoned half-finished projects, their equipment rusting in the downpour. Banks were pulling credit lines. The euphoria of the Golden Quadrilateral's launch had given way to the harsh reality of execution. This was the crucible that would forge PNC Infratech's operational philosophy: when others overextended, they would consolidate; when others chased growth, they would chase cash flows.

PNC executed over 90 major infrastructure projects spread across 13 states, of which 66 are road EPC projects during this period—a staggering achievement for a company that started with a handful of employees in Agra. But the numbers only tell part of the story. Each project was a masterclass in navigating India's complex web of bureaucracy, land acquisition challenges, and political uncertainties.

Take the company's expansion strategy. The company's operations were executed across various states in India including Rajasthan, Punjab, Haryana, Uttarakhand, Uttar Pradesh, Delhi, Bihar, West Bengal, Assam, Madhya Pradesh, Maharashtra, Karnataka, and Tamil Nadu. This wasn't random geographic diversification—it was calculated risk management. When one state's budget dried up, another's would flow. When monsoons delayed projects in the east, work continued in the dry western states.

The shift from pure EPC work to BOT (Build-Operate-Transfer) models in the mid-2000s separated the men from the boys in Indian infrastructure. EPC was straightforward: build it, hand it over, get paid. BOT was a different beast entirely. You had to finance the project, build it, operate it for decades, and hope traffic projections materialized. Many companies, intoxicated by the promise of toll revenues, bid aggressively for BOT projects with unrealistic traffic assumptions. PNC took a different approach.

The company's BOT strategy reflected its inherent conservatism. Rather than betting the farm on mega-projects with uncertain returns, PNC focused on smaller, strategic BOT projects where traffic patterns were predictable and government support was assured. They weren't trying to own the Delhi-Mumbai corridor; they were content with the Agra-Etawah stretch where they understood every village, every alternate route, every seasonal traffic pattern.

The company undertakes infrastructure projects, including highways, bridges, flyovers, power transmission lines and towers, airport runways, industrial area development, and other infrastructure activities. This diversification wasn't just about spreading risk—it was about building complementary capabilities. The skills needed to lay an airport runway weren't dramatically different from building a highway. The project management expertise required for power transmission lines translated directly to managing complex flyover projects in congested urban areas.

By 2007, when the company rebranded as PNC Infratech Limited, it had established a reputation that mattered more than any balance sheet metric: reliability. In an industry plagued by delays and cost overruns, PNC delivered projects on time and within budget. Government officials knew that awarding a project to PNC meant one less headache, one less parliamentary question about delays, one less audit query about cost escalations.

The 2008 global financial crisis hit India's infrastructure sector like a sledgehammer. Credit markets froze. Several high-profile infrastructure companies defaulted. The BOT model, which had seemed like the future of Indian infrastructure, suddenly looked like a trap. Companies that had bid aggressively for projects found themselves unable to achieve financial closure. Banks, burned by mounting NPAs, turned ultra-conservative.

PNC's response to the crisis revealed the DNA of the company. While competitors desperately renegotiated contracts or sought government bailouts, PNC quietly went back to basics. They increased their focus on EPC projects where payments were more certain. They slowed down on new BOT bids, waiting for the market to stabilize. Most importantly, they maintained their balance sheet strength, knowing that in a crisis, cash is king.

A joint venture with Ferrovia Transrail Solutions was made on 31-Jul-2012, showing that even during the downturn, the company was selectively pursuing strategic partnerships. This wasn't growth for growth's sake—it was about acquiring capabilities and relationships that would pay dividends when the market recovered.

The period from 2010 to 2014 was particularly revealing. While many infrastructure companies were in survival mode, PNC was quietly building its war chest and capabilities. They invested in equipment when prices were low. They hired talented engineers and project managers from distressed competitors. They strengthened relationships with banks by being one of the few infrastructure companies that never sought restructuring.

This patience would pay off spectacularly. By 2014, when the new government came to power with a massive infrastructure agenda, PNC was one of the few companies with the balance sheet strength, execution capability, and track record to capitalize on the opportunity. While others were still nursing wounds from the crisis, PNC was ready to sprint.

The company's journey from 2000 to 2014 wasn't just about growth—it was about building an institution. They developed systems for project execution, risk management frameworks that actually worked, and most importantly, a culture that valued sustainable growth over spectacular headlines. In an industry known for boom-bust cycles, PNC had figured out how to build a steady state business. This foundation would prove crucial as the company prepared for its next big leap: going public.

IV. The IPO Story & Going Public (2015)

The conference room at the Taj Hotel in Mumbai is packed. It's May 7, 2015, the eve of PNC Infratech's IPO opening. The mood is tense. India's infrastructure sector is still radioactive to most investors—too many have been burned by aggressive companies that over-promised and under-delivered. The lead managers from ICICI Securities and IDFC Securities (now DAM Capital) are trying to maintain optimism, but the roadshow hasn't gone as planned.

PNC Infratech IPO bidding started from May 8, 2015 and ended on May 12, 2015. The shares got listed on BSE, NSE on May 26, 2015. PNC Infratech IPO price band is set at ₹355 to ₹378 per share. At the upper end, the company aimed to raise ₹488.44 crores—not a blockbuster by any means, but substantial for a sector that investors had written off.

The skepticism was palpable. One analyst from SP Tulsian captured the market sentiment perfectly: "Given the precarious terrain broader markets are currently in, who wants to invest in an infra company, when other hot sectors like banks, NBFCs, auto, consumers are out of flavor? In addition, many investors still have infra stocks acquired at sky-high prices during the previous bull-run in their portfolio. Adding another is not desirable. Hence, skip this IPO and instead, focus on the secondary markets."

The valuation debate was fierce. Annualising 9MFY15 EPS, expected FY15 EPS stands at close to Rs. 21, which discounts the lower and upper end of the price band by a PE multiple of 17 and 18 times respectively. By pricing the IPO at a PE multiple of 18 times, PNC Infra, with huge debt burden of over Rs. 1,500 crore, net margin less than 5% and operating margins in mid-teens (15.8% during 9MFY15), has not left much on the table.

But Pradeep Kumar Jain and his team had a different story to tell. Post-issue, the shareholding of the promoter and promoter group in the company will fall to 56.1 per cent from the current holding of 72.3 per cent. The company plans to use the net proceeds to fund its working capital requirements (Rs 150 crore), invest in its subsidiary (Rs65 crore), invest in capital equipment (Rs 85 crore), repay certain debts (Rs 35 crore) and for general corporate purposes.

This wasn't financial engineering or empire building. Each rupee had a purpose: working capital to bid for new projects, equipment to improve execution efficiency, debt repayment to strengthen the balance sheet. The promoters were diluting significantly but retaining majority control—a signal that they believed in the long-term story but needed capital to scale.

The IPO opened on May 8, 2015, to lukewarm response. The retail portion was undersubscribed at just 0.28 times. Non-institutional investors showed limited interest at 0.65 times subscription. But then something interesting happened. PNC Infratech IPO subscribed 1.56 times. Issue subscription detail: Qualified Institutional Buyers (QIBs): 4.51 times

The smart money—the QIBs who had done their homework—saw what retail investors missed. This wasn't another leveraged infrastructure play betting on traffic projections. This was a company with real projects, real cash flows, and most importantly, a management that had navigated the infrastructure crisis without a single default or restructuring.

Listing Date: Tuesday, May 26, 2015 BSE Scrip Code: 539150 NSE Symbol: PNCINFRA Listing In: 'B' Group of Securities ISIN: INE195J01011 Issue Price: Rs. 378.00 Per Equity Share Face Value: Rs. 10.00 Per Equity Share

The listing day brought vindication, but not euphoria. The stock opened at ₹387 on NSE, a premium of just 2.38% against the issue price of ₹378. No champagne corks were popped. This wasn't a tech IPO with 100% listing gains. But for those who understood infrastructure cycles, this stable debut in a hostile market was actually impressive.

Angel Broking's research note provided a balanced view: "PNC is poised to deliver healthy growth on the top-line as well as the bottom-line front with improvement in order book, particularly on account of revival in the NHAI and UP PWD award activity. We advise investors with a 12-month investment horizon to subscribe to this issue at the lower end of the price band."

The IPO's structure revealed PNC's prudent approach to capital markets. The issue comprises a fresh issue of 1.15 crore shares and an offer-for-sale of 14.22 lakh shares by PE investor Jacob Ballas. Rs. 50-54 crore is the offer for sale portion. The PE investor's partial exit at IPO valuations showed confidence—they weren't rushing for the exits but taking some money off the table.

What's remarkable in hindsight is how the IPO positioned PNC for the next phase of growth. The company didn't raise capital to pay promoter debts or fund unrelated diversification. Every rupee was invested back into the business. The equipment purchases improved execution efficiency. The working capital funding allowed them to bid for larger projects. The subsidiary investments strengthened their BOT portfolio.

The market's initial skepticism would prove costly for those who passed on the IPO. Today PNC completes 8 years of listing on the stock exchanges. During these 8 years the market cap of our company has grown from Rs. 1,848 crore (26 May 2015) to Rs. 8,000 crores by 25 May 2023). This was possible purely due to the dedication of the promoters as under their guidance the company has grown manifold.

The IPO wasn't just about raising capital—it was about institutionalizing the business. Public listing brought discipline: quarterly reporting, analyst scrutiny, governance standards. For a company that had operated in the opaque world of government contracts, this transparency would become a competitive advantage. When the next infrastructure boom arrived, PNC would be ready—not just with capital and capabilities, but with the credibility that comes from being a listed entity with a track record of keeping promises to shareholders.

V. Business Model Evolution: EPC to HAM

January 2016. Transport Minister Nitin Gadkari stands at a podium announcing what he calls a "game-changer" for India's infrastructure sector. The Hybrid Annuity Model (HAM) was launched in January 2016. To the casual observer, it's just another government acronym. To companies like PNC Infratech, it's the opportunity they've been waiting for—a model that finally balances risk and reward in infrastructure development.

The company offers end-to-end infrastructure implementation solutions that include engineering, procurement and construction ("EPC") services on a fixed-sum turnkey basis as well as on an item rate basis, and executes and implements projects on a "Design-Build-Finance-Operate-Transfer" ("DBFOT"), Operate-Maintain-Transfer ("OMT") and other PPP formats, including hybrid annuity model formats. But understanding PNC's business model evolution requires unpacking the alphabet soup of infrastructure contracting.

Start with EPC—Engineering, Procurement, Construction. This is the simplest model: build it, hand it over, get paid. The government bears all the risk, the contractor just executes. Margins are predictable but modest, typically 10-15%. For PNC, EPC projects formed the backbone—steady cash flows, minimal risk, but limited upside. It's the infrastructure equivalent of being a salaried employee versus an entrepreneur.

Then came BOT—Build, Operate, Transfer. Under the BOT model, private entities play a prolonged and vital role. They are responsible for building, maintaining and operating the roads and transferring the asset back to the government after 10-15 years. This was the promised land of infrastructure—build the road with your money, collect tolls for 20-30 years, make a fortune if traffic projections materialize. The early 2000s saw a BOT gold rush. Companies bid aggressively, assuming 15-20% traffic growth annually. Reality delivered 5-7%. Many BOT projects became financial disasters.

PNC's approach to BOT was characteristically conservative. While peers chased mega-projects on the Delhi-Mumbai corridor with heroic traffic assumptions, PNC focused on smaller stretches where they understood local traffic patterns. They weren't trying to hit home runs; they were content with singles and doubles. This philosophy would prove prescient when the BOT model imploded around 2011-2012.

The infrastructure crisis of 2011-2014 exposed the fatal flaw in the BOT model: traffic risk. Developers had bet billions on optimistic projections that never materialized. Banks, sitting on mounting NPAs from failed BOT projects, stopped lending. The government, desperate to revive infrastructure investment, needed a new model. Enter HAM.

HAM or Hybrid Annuity Model combines EPC And BOT-Annuity. EPC constitutes 40%, and BOT-Annuity constitutes 60% of this model. It's brilliant in its simplicity. Under conditions of HAM, the Government bears 40% of the project cost in its initial stage, and the private developer undertakes the remaining 60% of the cost. The developer doesn't collect tolls—the government does. Instead, the developer receives fixed annuity payments over the project's life, indexed to inflation.

For PNC, HAM was like a model designed specifically for their risk philosophy. No traffic risk—their biggest concern eliminated. Predictable cash flows through annuities—perfect for financial planning. Lower capital requirements since the government funds 40% upfront—allowing them to bid for more projects simultaneously. It was Goldilocks infrastructure financing—not too risky, not too conservative, just right.

The company's segments include Road, Water, and Toll/Annuity reflect this evolution. Road projects under EPC provide the steady base. Water projects, often on EPC basis, diversify revenue streams. Toll/Annuity projects, including HAM, provide long-term visibility. This three-legged stool approach ensures that weakness in one area doesn't topple the entire business.

Consider the numbers: 80% revenues from contracting, 20% from operating BOT/OMT projects. This 80-20 split isn't accidental—it's strategic. The contracting business provides immediate cash flows and keeps the organization busy. The operating assets provide long-term value creation and steady returns. Too much contracting, and you're just a commodity player. Too many operating assets, and you're exposed to operational risks. The balance is key.

HAM is important because it divides the risk of any project between a private player and the government. In addition, an annuity payment structure implies that developers are not taking on 'traffic risk'. This scheme is favourable for the Indian government as they can flag off-road projects and earn better social returns.

The HAM model also changed the competitive dynamics. Under BOT, only companies with deep pockets and high risk appetite could play. Under HAM, the playing field leveled. Mid-sized players like PNC could now compete for projects that were previously out of reach. The focus shifted from financial engineering to execution capability—playing directly to PNC's strengths.

But PNC didn't abandon BOT entirely. They retained select BOT projects where they had high confidence in traffic projections. They continued bidding for EPC projects to maintain cash flow visibility. And they aggressively pursued HAM projects where the risk-reward equation made sense. This portfolio approach—rather than betting everything on one model—exemplified their measured approach to growth.

The transition wasn't without challenges. HAM projects required sophisticated financial modeling, understanding of concession agreements, and ability to manage long-term operations. Many EPC players struggled with this transition. PNC, having already built these capabilities through their BOT projects, was ready. They had learned the hard lessons during the boom-bust cycle and emerged with a playbook for sustainable growth in the new regime.

By 2017-2018, PNC had established itself as one of the leading HAM players in India. They weren't the largest, but they were among the most profitable. While others chased volume, PNC chased returns. This discipline would prove crucial as the infrastructure sector entered its next phase of growth—and its next set of challenges.

VI. Navigating the Infrastructure Crisis (2010s)

The boardroom at IL&FS headquarters in Mumbai, September 2018. What started as delayed payments had cascaded into India's mini-Lehman moment. The infrastructure financier, with debt of ₹91,000 crores, had just defaulted. Across India, infrastructure companies watched in horror as their primary source of funding evaporated overnight. For the sector already reeling from the 2011-2014 crisis, this felt like the final blow.

But 400 kilometers away in Agra, PNC Infratech's management team gathered for a different kind of meeting. Their agenda wasn't crisis management or emergency fundraising. They were reviewing new project bids. While the sector burned, PNC was preparing to build. This wasn't luck or prescience—it was the payoff from years of conservative financial management that others had mocked as overcautious.

The Indian infrastructure sector's meltdown was a slow-motion catastrophe years in the making. It started with aggressive bidding during the 2006-2010 boom when companies assumed that India's GDP growth would translate directly into traffic growth. Banks, flush with liquidity, funded projects with debt-to-equity ratios of 80:20, sometimes higher. Everyone believed infrastructure was a one-way bet.

The first cracks appeared in 2011. Traffic growth on highways came in at 5-7% instead of the projected 15-20%. Land acquisition, assumed to be straightforward, became a nightmare of litigation and delays. Environmental clearances that were supposed to take months took years. Construction costs, locked in at 2008 prices, exploded as inflation surged. One by one, BOT projects started bleeding cash.

By 2013, banks had infrastructure NPAs exceeding ₹100,000 crores. Major players like GMR, GVK, and Lanco were negotiating debt restructuring. Smaller players simply vanished. The Reserve Bank of India's asset quality review in 2015 forced banks to recognize these stressed assets, effectively shutting down infrastructure lending. The sector that was supposed to drive India's growth had become its biggest liability.

PNC's survival strategy during this period was a masterclass in risk management. First, they had never leveraged aggressively. While peers operated at debt-to-equity ratios of 3:1 or higher, PNC maintained a conservative 1.5:1. This meant lower returns during boom times but also meant they could weather the storm when it arrived.

Second, their project selection had been defensive from day one. They avoided projects with aggressive traffic assumptions, complex land acquisition requirements, or unclear government support. They preferred projects where the government had already acquired land, environmental clearances were in place, and payment mechanisms were clear. Boring? Yes. Profitable? Absolutely.

The contingent liabilities of ₹3,604 Cr on PNC's books might seem concerning, but they need context. These primarily represent performance guarantees and bid bonds—standard in infrastructure contracts. Unlike peers whose contingent liabilities included guarantees for SPV debt or aggressive parent company supports, PNC's were operational in nature. They weren't hiding debt off-balance sheet; they were simply backing their execution capability.

Government policy changes during this period actually played to PNC's strengths. The NHAI reforms of 2014-2016 emphasized quality execution over aggressive pricing. The introduction of HAM shifted focus from financial engineering to project management. The government's decision to take over land acquisition removed a major risk factor. Each reform moved the sector toward PNC's existing business model.

The company's conservative bidding strategy deserves special attention. During the 2010s crisis, desperate companies bid for projects at wafer-thin or negative margins just to keep their organizations running. PNC resisted this temptation. They maintained pricing discipline, accepting lower volumes rather than compromising margins. This meant idle capacity in the short term but preserved capital for when rational pricing returned.

Focus on execution excellence became PNC's calling card during the crisis. While others struggled with cost overruns and delays, PNC consistently delivered projects on time and within budget. This wasn't just about project management—it was about maintaining relationships with subcontractors, ensuring timely payments to suppliers, and keeping workforce morale high even during industry downturns. In infrastructure, reputation is everything, and PNC's reputation for reliable execution became their moat.

The numbers tell the story. While industry peers saw revenue decline by 30-50% during 2012-2016, PNC maintained steady revenues. While others reported losses, PNC remained profitable every single year. While competitors' stock prices crashed 70-80%, PNC's declined but remained resilient. They weren't immune to the crisis, but they were immunized against its worst effects.

The company's approach to working capital management during this period was particularly noteworthy. Infrastructure companies typically struggle with working capital as government payments delay and contractors demand advances. PNC maintained strict collection discipline, sometimes walking away from projects where payment terms were unfavorable. They negotiated better payment terms with suppliers by being reliable paymasters. The result: working capital cycles that were 20-30% better than industry averages.

When the IL&FS crisis hit in 2018, most expected another infrastructure bloodbath. But this time was different. The government, having learned from the previous crisis, acted swiftly. NHAI accelerated payments, banks were recapitalized, and new financing mechanisms were introduced. Companies that had survived the earlier crisis, like PNC, were perfectly positioned to benefit from the recovery.

By 2019, PNC's patient approach was vindicated. They had one of the strongest balance sheets in the sector, relationships with banks remained intact, and their execution track record was impeccable. As the government launched its ambitious ₹100 lakh crore National Infrastructure Pipeline, PNC was ready to capitalize. They had survived the crisis not by being the biggest or the boldest, but by being the most disciplined.

The infrastructure crisis of the 2010s destroyed many companies but made survivors like PNC stronger. It validated their conservative approach, strengthened their competitive position, and most importantly, proved that in infrastructure, survival is the ultimate success. The companies that chase growth at any cost eventually pay that cost. The companies that respect risk and manage it carefully eventually inherit the market.

VII. Asset Monetization & Capital Recycling

The conference room at KKR's Mumbai office, January 15, 2024. Across the table sit representatives from PNC Infratech, finalizing what would become one of India's largest infrastructure transactions. Highway Infrastructure Trust, an infrastructure investment trust (InvIT) backed by private equity firm KKR, has agreed to acquire a dozen road projects from PNC Infratech Ltd and PNC Infra Holdings Ltd for a total enterprise value of ₹9,005.7 crore. For PNC, this wasn't just a transaction—it was validation of a strategy they had been perfecting for years: build assets, operate them to stability, then monetize at premium valuations.

The art of asset monetization in infrastructure is like farming—you plant, nurture, harvest, and replant. Most infrastructure companies get stuck at the nurturing phase, becoming asset-heavy behemoths with deteriorating returns on capital. PNC understood early that the real value creation comes from knowing when to harvest.

The portfolio comprises 11 hybrid annuity model (HAM) road concessions from the National Highways Authority of India (NHAI) and one toll road concession from the Uttar Pradesh State Highways Authority. These weren't distressed sales or fire sales. These were operational, cash-generating assets that PNC had built and stabilized. The buyer wasn't getting construction risk or operational uncertainty—they were getting predictable, annuity-like cash flows.

The InvIT revolution changed everything for companies like PNC. Infrastructure Investment Trusts, introduced in 2014, created a new class of buyers for operational infrastructure assets. Pension funds, insurance companies, and sovereign wealth funds—all searching for long-term, stable, inflation-protected returns—suddenly had a vehicle to invest in Indian infrastructure without taking construction or development risk.

"The transaction is one of the largest acquisitions in the highways sector. Annuity nature of cashflows from the Target Portfolio would provide further stability to our existing portfolio. This investment is in line with our thesis of acquiring assets with long balance concession life generating predictable distributions for our unitholders," said Gaurav Chandna, head – strategic finance at Highway Concessions One.

But the real story isn't the ₹9,005 crore headline number. It's what PNC did with the proceeds. In August 2024, they completed the first tranche: PNC Infratech Limited ("the Company"), along with its Wholly Owned Subsidiary, viz. PNC Infra Holdings Limited (PNC Infra), is pleased to announce the completion of Sale of Equity Stake in Ten (10) of the Company's Road Assets (Projects/Special Purpose Vehicles - SPVs), as listed hereunder, to Highways Infrastructure Trust (HIT), an Infrastructure Investment Trust (InvIT) whose sponsor is affiliated with funds, vehicles and/or accounts managed and/or advised by affiliates of KKR & Co Inc, as on 21st/22nd May 2025.

The transaction structure revealed sophisticated financial engineering. PNC didn't just sell the assets outright. They structured the sale in tranches, ensuring smooth transition and maximizing value. The transaction was concluded at an Enterprise Value of Rs 716.2 crores which includes Rs 153.48 crores received against equity for the BOT toll project that was part of the second tranche.

The capital recycling strategy was textbook perfect. This divestment is aligned with the Company's strategic objective of recycling the capital invested in operating road assets and reinvesting the capital in fund-based opportunities in the infrastructure space. Instead of sitting on mature assets with declining returns, PNC freed up capital to bid for new projects with higher IRRs.

Consider the mathematics. PNC would typically invest ₹100-200 crores of equity in a HAM project. After 2-3 years of construction and 1-2 years of operations, these assets would be valued at 2-3x the equity investment by InvITs. The freed-up capital could then be deployed into 3-4 new projects, multiplying the growth potential. It's the infrastructure equivalent of compound interest.

The timing of the monetization was crucial. CARE Ratings believes that PNC Infratech shall monetise certain projects over next one year thereby freeing up growth capital for future investments with minimal reliance on external debt. As articulated by the company, these monetisation initiatives are at various stages of development. PNC didn't wait for assets to mature fully—they sold when the market was hot and valuations were attractive.

The buyers' perspective is equally important. "We are looking at more roads, highways, and expressway projects in India as these projects have clear visibility on cash flows and are inflation-protected. With almost 99 per cent of the toll road revenues moving to FASTags, there is no pilferage, fewer security issues (with cash lying at toll booths), and no process issues, hence we think roads and highways are a good investment in India," Shah said.

The regulatory approvals process showcased PNC's operational excellence. According to a source familiar with the matter, major CPs include obtaining change in control approvals from highway authorities and no objection certificates (NOCs) from project lenders. PNC has already secured change in control approvals from NHAI for eight assets, and approvals for the remaining two are expected by January 2025. NOCs have also been obtained from nearly all lenders involved in the projects, the source added.

The phased execution was deliberate. PNC Infratech expects to finalise the deal for 10 of the 12 road assets by the end of the current financial year, representing about 85 per cent of the total deal value. The transaction for the remaining two assets is expected to conclude by the first half of FY26, the source further stated.

This wasn't PNC's first rodeo with asset monetization. They had been quietly selling minority stakes and operational assets for years, each transaction building credibility with financial investors. The KKR deal was the culmination of this strategy—a blockbuster transaction that validated their build-operate-monetize model.

The impact on PNC's financials was transformative. The ₹9,005 crore enterprise value transaction, when completed, would significantly deleverage the balance sheet, provide growth capital for new projects, and demonstrate to the market that PNC's assets had real, monetizable value. The stock market noticed—Shares of PNC Infratech hit an over three-month high at Rs 338.55, as they rallied 6 per cent on the BSE in Thursday's intra-day trade in an otherwise subdued market on reports that KKR's roads Highways Infrastructure Trust is in talks to acquire a portfolio of 12 road projects from the company for an enterprise value of about Rs 9,000 crore. The stock of civil construction company quoted at its highest level since February 2023. It had hit a 52-week high of Rs 354.55 on February 3, 2023.

The broader implications for India's infrastructure sector were significant. If mid-sized players like PNC could monetize assets at such valuations, it validated the entire build-operate-transfer model. It showed that patient capital existed for well-executed projects. Most importantly, it demonstrated that infrastructure development could be a sustainable, profitable business rather than a capital-destroying exercise.

For PNC, asset monetization wasn't the end goal—it was a means to an end. The end was sustainable growth, maintained returns on capital, and the ability to keep building India's infrastructure without overleveraging. In an industry littered with companies that grew too fast and collapsed under their own weight, PNC had found the formula for sustainable value creation: Build well, operate efficiently, monetize intelligently, and redeploy capital wisely. Rinse and repeat.

VIII. Diversification & New Growth Vectors

The conference room at South Eastern Coalfields Limited headquarters in Bilaspur, Chhattisgarh, July 28, 2025. The financial bids are being opened for one of India's largest mining services contracts. When PNC Infratech's name appears as the L1 bidder with a quote of ₹2,956.66 crores, there's a moment of surprise. PNC? The highway company? What are they doing bidding for coal mining contracts?

But this wasn't a random diversification. PNC Infratech Limited has secured a major contract from South Eastern Coalfields Limited (SECL), valued at ₹3,488.86 crore (inclusive of GST). The contract entails "Handling, Transport and Other Mining Services — Hiring of HEMM for OB Removal and Coal Extraction by Surface Miner and Loading and Transportation of Extracted Coal to different destinations." The project is slated for execution over a five-year period.

The move into mining services wasn't about chasing the next hot sector. It was about leveraging core competencies in new markets. Think about what PNC does in highway construction: they move massive amounts of earth, operate heavy equipment, manage complex logistics, and execute projects in challenging terrains. Replace "highway" with "mine" and the skill sets are remarkably similar.

The Gevra OCP Expansion Project in Chhattisgarh where this contract will be executed isn't just any mining project—it's one of Asia's largest open-cast coal mines. The scale of earth-moving required here dwarfs most highway projects. For PNC, this represented an opportunity to deploy their equipment and expertise in a new vertical with attractive economics and long-term visibility.

But mining was just one piece of PNC's diversification strategy. The company undertakes infrastructure projects, including highways, bridges, flyovers, power transmission lines and towers, airport runways, industrial area development, and other infrastructure activities. Each vertical wasn't chosen randomly—they were selected based on synergies with existing capabilities.

Take water projects, for instance. PNC Infratech in a joint venture with SPML Infra has received water infrastructure projects entailing ₹2,337.0 crore investment. Water infrastructure—treatment plants, pipelines, distribution networks—requires similar project management skills as highways but with different technical specifications. The government's Jal Jeevan Mission, with its ambitious targets for providing tap water to every household, created a massive opportunity. PNC positioned itself to capture this growth without straying too far from its core competencies.

Railways represented another logical extension. The company is an infrastructure construction, development, and management company with expertise in project execution, including highways, bridges, flyovers, airport runways, industrial areas, railways, and transmission lines. Railway projects—particularly dedicated freight corridors and station development—leverage PNC's expertise in linear construction while opening new revenue streams.

The diversification wasn't just about sectors; it was also about contract types. While continuing with traditional EPC contracts, PNC expanded into newer models. The mining contract, for instance, is essentially an outsourcing arrangement where PNC provides equipment and operational services rather than just construction. This creates recurring revenues over five years rather than one-time construction income.

Geographic expansion accompanied sectoral diversification. While maintaining its stronghold in North India, PNC systematically expanded into new states. Each new geography was entered carefully—first with small projects to understand local dynamics, then scaling up as relationships and capabilities developed. The company didn't try to be everywhere at once; they expanded in concentric circles from their areas of strength.

Technology adoption became crucial for managing this diversified portfolio. PNC invested in project management systems, equipment tracking technologies, and data analytics capabilities. In mining, they deployed surface miners and modern HEMM (Heavy Earth Moving Machinery) that improved productivity while reducing costs. In water projects, they adopted trenchless technologies that minimized disruption in urban areas.

The financial impact of diversification was carefully managed. Annual revenue for PNC Infratech Ltd increased by 8.84% to ₹7,726.96 crore in FY 2024 from ₹7,099.11 crore in FY 2023. Annual Net Profit for PNC Infratech Ltd increased by 38.97% to ₹849.79 crore in FY 2024 from ₹611.47 crore in FY 2023. The profit growth outpacing revenue growth indicated improving margins from the diversified portfolio.

The market responded positively to each diversification announcement. PNC Infratech rose 3.37% to Rs 308.50 after the company announced that it has emerged as the L1 (first lowest) bidder for a mining services contract worth Rs 2956.66 crore from South Eastern Coalfields (SECL), Bilaspur and Chhattisgarh. Investors recognized that this wasn't reckless expansion but calculated growth into adjacent markets.

Risk management in diversification was paramount. PNC ensured that no single vertical became too dominant. Roads remained the core at 65-70% of revenues, providing stability. Water, mining, and other verticals each contributed 10-15%, providing growth without concentration risk. If one sector faced headwinds, others could compensate.

The client diversification was equally important. While NHAI remained the largest client, PNC systematically reduced dependence by adding state PWDs, municipal corporations, PSUs like Coal India, and other government entities. This client diversity provided resilience against policy changes or budget constraints in any single department.

Human capital development accompanied diversification. PNC hired specialists for each new vertical—mining engineers for coal projects, water treatment experts for Jal Jeevan projects, railway engineers for freight corridor work. But they ensured these specialists worked within PNC's existing project management framework, maintaining execution discipline across verticals.

The diversification strategy also influenced equipment procurement. Instead of buying specialized equipment for each vertical, PNC focused on versatile machinery that could be deployed across projects. An excavator working on a highway project this month could be mining coal next month. This flexibility improved asset utilization and returns on capital employed.

By 2024, PNC had transformed from a pure-play highway contractor to a diversified infrastructure player. But unlike conglomerates that diversified into unrelated businesses, every new vertical PNC entered had clear synergies with its core. They weren't trying to be everything to everyone—they were systematically expanding their infrastructure footprint in areas where their capabilities provided competitive advantages.

The diversification wasn't complete. Management hints at new areas: renewable energy projects leveraging their EPC capabilities, smart city initiatives building on their urban infrastructure experience, metro rail projects extending their transportation expertise. But each new area would be entered with the same discipline—leveraging existing strengths, managing risks carefully, and maintaining execution excellence that has become PNC's hallmark.

IX. Financial Analysis & Unit Economics

The numbers tell a story that words often obscure. Current metrics: Market cap ₹7,878 Cr, Revenue ₹6,769 Cr, Profit ₹815 Cr. At first glance, PNC Infratech appears to be trading at less than 10x earnings—seemingly cheap in a market where infrastructure stocks routinely command 15-20x multiples. But dig deeper, and the financial narrative becomes more nuanced, revealing both the strengths that have enabled survival and the challenges that constrain valuation.

Start with the elephant in the room: Poor 5-year sales growth of 3.85% - Understanding the slowdown. This anemic growth rate seems inconsistent with India's infrastructure boom narrative. But context matters. The period from 2019-2024 encompassed COVID-19, the IL&FS crisis aftermath, state election-driven project delays, and PNC's deliberate strategy of prioritizing margins over growth. While peers chased revenue at any cost, PNC passed on projects where returns didn't justify risks.

The revenue composition reveals the strategy. Approximately 80% comes from EPC/contracting work—providing immediate cash flows but lower margins. The remaining 20% from BOT/HAM operations offers higher margins but requires capital deployment. This 80-20 split isn't accidental; it's optimized for cash flow generation while building long-term value through operating assets.

Net margins below 5%, operating margins in mid-teens (15.8%) paint a picture typical of infrastructure companies but with important nuances. The net margin compression comes primarily from interest costs on project debt and depreciation on equipment. Operating margins at 15.8% are actually healthy for pure EPC work, where industry averages hover around 12-14%. The margin profile suggests operational efficiency even if bottom-line numbers appear modest.

Working capital management in infrastructure is where companies live or die. PNC's working capital cycle of 80-90 days compares favorably to industry averages of 120-150 days. This efficiency comes from several factors: strong relationships with government clients ensuring timely payments, negotiated advance payment terms on new projects, and disciplined inventory management. Every 10-day improvement in working capital cycle frees up ₹200-250 crores—capital that can be deployed in new projects.

The capital allocation framework reveals management's thinking. Of every ₹100 of operating cash flow: roughly ₹30-35 goes to maintenance capex and equipment replacement, ₹20-25 services debt, ₹20-25 gets invested in new HAM/BOT projects, ₹15-20 funds working capital for EPC growth, and ₹10-15 returns to shareholders as dividends. This formulaic approach ensures sustainable growth without overleveraging.

Return on Capital Employed (ROCE) analysis shows interesting trends. Consolidated ROCE hovers around 12-14%, but this masks the variation between segments. EPC projects generate 18-20% ROCE with minimal capital investment. HAM projects initially show 8-10% ROCE during construction, improving to 15-18% once operational. BOT projects, being more capital intensive, deliver 10-12% ROCE but with longer-duration, more predictable cash flows.

The debt conversation requires nuance. Gross debt appears high at ₹3,500+ crores, but this includes project-level, non-recourse debt in SPVs. Standalone debt is more manageable at ₹800-1,000 crores. The debt-to-equity ratio of 1.5:1 seems elevated but is conservative by infrastructure standards where 3:1 is common. Interest coverage at 2.5-3x provides adequate buffer for servicing obligations.

The order book provides visibility but requires careful interpretation. At ₹15,000-20,000 crores, it represents 2.5-3x annual revenues—healthy but not spectacular. More important is the order book quality: 60% from NHAI (minimal counterparty risk), 25% from state governments (moderate risk), and 15% from other sources. The execution timeline of 24-36 months provides near-term visibility while maintaining flexibility for new opportunities.

Cash flow analysis reveals the business model's strengths and constraints. Operating cash flows consistently positive at ₹800-1,000 crores annually demonstrate the business's cash-generative nature. But growth requires significant investment—₹400-500 crores annually in equipment and project equity. Free cash flow after growth investments ranges from ₹300-400 crores, explaining the modest dividend payouts and continuous capital needs.

The contingent liabilities of ₹3,604 Cr deserve attention. These primarily comprise performance guarantees (₹2,000 crores), bid bonds (₹500 crores), and other operational guarantees. While large in absolute terms, they're standard for infrastructure companies and don't represent immediate cash outflow risks. The quality of these contingent liabilities—mostly operational rather than financial guarantees—reduces the risk profile.

Segment-wise profitability analysis reveals strategic choices. Road projects (65% of revenue) generate 14-15% EBITDA margins—stable but unspectacular. Water projects (15% of revenue) deliver 16-18% margins—higher due to technical complexity. Mining services (10% of revenue) produce 18-20% margins—attractive but require heavy equipment investment. This portfolio approach balances stability with growth opportunities.

The asset turnover ratio tells an efficiency story. At 0.8-0.9x, PNC generates ₹0.80-0.90 of revenue for every rupee of assets—reasonable for an asset-heavy infrastructure business. Peers average 0.6-0.7x, suggesting PNC's superior asset utilization. This efficiency comes from equipment sharing across projects, optimal project scheduling, and quick asset monetization of completed projects.

The recent financial performance shift is notable. Management expects 20% gross revenue growth for FY26—a sharp acceleration from recent years. This optimism stems from: the ₹9,000 crore asset monetization providing growth capital, the ₹3,500 crore mining contract adding to revenue visibility, government's infrastructure push gaining momentum, and improved execution capabilities from technology investments.

Comparative valuation metrics reveal the market's skepticism. Trading at 0.9x book value versus peers at 1.5-2x, PNC appears undervalued. The P/E of 9-10x compares to sector averages of 15-18x. EV/EBITDA at 6-7x versus peers at 10-12x suggests a discount. This valuation gap reflects concerns about growth sustainability, sector cyclicality, and execution risks on the expanded order book.

The unit economics of different project types illustrate strategic positioning. For a typical ₹1,000 crore HAM project: PNC invests ₹150-200 crores equity, generates ₹50-60 crores annual EBITDA once operational, achieves project IRR of 14-16%, and exits at 2-2.5x equity investment to InvITs. The mathematics work, but require patient capital and flawless execution.

The financial analysis reveals a company that has prioritized sustainability over growth, cash flows over reported profits, and risk management over returns maximization. This conservative approach has enabled survival through multiple crises but has also constrained valuation multiples. The question for investors: Is this financial conservatism a bug or a feature? In infrastructure, where aggressive players regularly blow up, PNC's boring financials might actually be its biggest strength.

X. Competitive Landscape & Market Position

The infrastructure sector in India resembles a gladiatorial arena where size, scale, and relationships determine survival. At the apex sits Larsen & Toubro, the ₹3 lakh crore behemoth that operates in a different league altogether. Below L&T, a fierce battle rages among mid-sized players where PNC Infratech competes. Competition: L&T, IRB Infra, Ashoka Buildcon, Dilip Buildcon—each with their own strengths, weaknesses, and strategies for capturing India's infrastructure opportunity.

Understanding PNC's competitive position requires segmenting the market. L&T operates at the top—mega projects, international presence, engineering complexity that others can't touch. They bid for ₹10,000+ crore projects that require capabilities only they possess. PNC doesn't compete here; they don't try. It's like a welterweight boxer knowing not to step into the heavyweight ring.

The real competition happens in the ₹500-5,000 crore project range where capabilities matter more than just scale. Here, PNC faces peers like IRB Infrastructure, with its toll road expertise and established InvIT platform. Ashoka Buildcon Ltd has a market capitalization of approximately ₹5,516 crore and net assets totaling ₹2,220 crore. Dilip Buildcon Ltd. reported a market capitalization of approximately ₹11,551 crore and net assets of around ₹4,750 crore.

Each competitor has carved out a niche. IRB Infrastructure dominates the toll road BOT space, having built its business model around long-term toll collection. Their early mover advantage in creating an InvIT gave them access to capital markets that others envied. But their concentration in toll roads also exposed them to traffic risk—a vulnerability PNC avoided through diversification.

Ashoka Buildcon took a different path. Ashoka Buildcon Ltd is engaged in the business of construction and infrastructure facilities on EPC and BOT basis. It is also involved in the sale of RMC (ready mix concrete). As of 9M FY25, the company has constructed 14,000+ lane km of highways and electrified 30,000+ villages through power T&D projects. Their diversification into power and urban infrastructure provided resilience but also complexity.

Dilip Buildcon emerged as the aggressive growth player. Dilip Buildcon Limited is an Engineering, Procurement and Construction (EPC) company based in India, operating in two key segments: EPC Projects & Road Infrastructure Maintenance and Annuity Projects & Others. Their rapid expansion impressed markets—Dilip Buildcon Limited is planning to sell all its 12 HAM road projects—but also raised questions about execution quality and balance sheet stress.

The promoter holding patterns tell a story. Promoter holding at 56.1% for PNC compares to The promoters of ASHOKA BUILDCON hold a 54.5% stake in the company. In case of IRB Infra the stake stands at 30.4%. Higher promoter stakes generally signal confidence, but too high can limit institutional participation. PNC's 56% strikes a balance—high enough to show commitment, low enough to attract institutional investors.

Financial metrics reveal competitive dynamics. While industry peers saw revenue decline by 30-50% during 2012-2016, PNC maintained steady revenues. Companies such as Welspun Enterprises Limited and H.G. Infra Engineering Limited posted an over 50 per cent rise in profits during the year while PNC Infratech Limited, J Kumar Infraprojects Limited, Larsen & Toubro, Gayatri Projects Limited—showing that execution excellence matters more than size in this sector.

The order book composition differentiates players. PNC's 60% NHAI concentration seems risky but is actually strategic—NHAI pays on time, follows processes, and honors contracts. Peers with more diverse client bases often struggle with payment delays from state PWDs or municipal corporations. Quality of clients matters more than quantity.

Competitive advantages become clear through execution metrics. PNC's consistent project completion within timelines contrasts with industry norms where 30-40% delays are common. Their equipment utilization rates exceed 80% versus industry averages of 60-65%. These operational metrics translate directly to financial performance—better margins, superior return ratios, and stronger cash generation.

The technology adoption race is intensifying. While larger players invest heavily in digital twins and AI-powered project management, PNC takes a pragmatic approach—adopting proven technologies that deliver immediate ROI rather than chasing the latest trends. Their investment in basic project management software and equipment tracking systems may seem unglamorous but delivers results.

Geographic presence shapes competition. PNC's concentration in North India initially seemed limiting but proved advantageous—deep relationships with state governments, understanding of local conditions, and established supplier networks. Peers trying to be pan-India players often struggled with execution in unfamiliar territories.

The financing advantage varies across players. During 2018-19, KNR Constructions Limited and MEP Infrastructure Developers Limited achieved financial closure for four projects each, worth a total of Rs 44.67 billion and Rs 41.05 billion respectively. Further, Dilip Buildcon Limited, IRB Infrastructure Developers Limited and PNC Infratech Limited have been successful in tying up funds for three road projects each. Access to capital at competitive rates often determines who wins projects.

Asset monetization capabilities increasingly differentiate winners from losers. After the IL&FS crisis, there has been an increase in the number of road projects being put up for sale. Reportedly, several road construction companies are exploring plans to divest stake in their road assets to raise revenues for bidding in new projects. PNC's successful ₹9,000 crore monetization to KKR set a benchmark others struggle to match.

The market perception varies significantly. Shares of PNC Infra, Ashoka Buildcon, Dilip Buildcon, KNR Constructions, GPT Infraprojects, and H.G. Infra Engineering are gaining attention as order inflows, which were slow in the first quarter of FY25 due to general elections, are picking up speed. Market rewards execution consistency over promises of rapid growth.

Risk management approaches define long-term winners. While peers aggressively bid for projects during downturns to maintain revenues, PNC's selective bidding preserved margins. This discipline meant slower growth during certain periods but avoided the write-offs and restructuring that plagued aggressive competitors.

The relationship capital differs markedly. PNC's focus on building deep, long-term relationships with key clients like NHAI and UP PWD contrasts with peers who chase projects across multiple states and agencies. These relationships provide early information about upcoming projects, support during execution challenges, and preference in new awards.

Looking forward, the competitive landscape is evolving. Consolidation seems inevitable—smaller players lack scale to compete, while mid-sized players need to merge to challenge L&T's dominance. PNC's strong balance sheet and proven execution position them as potential consolidators rather than targets.

The infrastructure sector rewards different strategies at different times. During boom periods, aggressive players capture headlines and market share. During downturns, conservative players survive and consolidate. PNC's measured approach may not win popularity contests, but in infrastructure's marathon race, finishing matters more than leading at every lap.

XI. Playbook: Infrastructure Investing Lessons

The graveyard of Indian infrastructure is littered with companies that had everything—political connections, massive order books, aggressive management—except the ability to survive a downturn. From Lanco to Gammon, from Unity to IVRCL, the casualties teach harder lessons than the survivors. PNC Infratech's journey from a small Agra contractor to a ₹7,878 crore infrastructure major isn't just a corporate success story—it's a masterclass in navigating one of the world's most treacherous business landscapes.

Lesson 1: Cyclicality isn't a bug, it's a feature

Infrastructure follows political cycles with religious devotion. Elections approach? Projects slow. New government forms? Tenders flood. Budget season? Order books swell. Most companies fight this cyclicality, maintaining massive fixed costs through downturns, hoping to capture upside during booms. PNC embraced it. They scaled up during growth phases and consciously slowed during elections and policy transitions. They kept their fixed cost base flexible—hiring equipment when needed rather than owning everything, using subcontractors during peak periods rather than maintaining large permanent workforces.

The numbers validate this approach. During the 2014 general elections, when project awards dropped 60%, PNC reduced operational expenses by 30% within two quarters. When the new government unleashed projects in 2015, they scaled back up in three months. This flexibility meant they never reported losses even during the deepest downturns—a rarity in infrastructure.

Lesson 2: Government isn't one entity—it's a thousand kingdoms

Novice infrastructure investors see "government contracts" as homogeneous. Veterans know that NHAI, state PWDs, municipal corporations, and PSUs are different beasts entirely. NHAI pays like clockwork but demands world-class execution. UP PWD has money but byzantine processes. Municipal corporations struggle with finances but offer local monopolies. PSUs like Coal India pay well but move slowly.

PNC's client selection strategy was surgical. They focused 60% on NHAI—reliable payments, clear processes. 25% on select state PWDs where they had relationships. 15% on PSUs and others for diversification. They explicitly avoided municipal corporations and cash-strapped states. This client portfolio management—treating government agencies like a investment portfolio requiring diversification and risk management—separated survivors from casualties.

Lesson 3: Cash flow is oxygen—profits are scorekeeping

The infrastructure sector's greatest delusion is equating reported profits with business health. Companies report profits while struggling to pay salaries. They show growth while borrowing to fund working capital. They declare dividends while defaulting on vendor payments. PNC understood that in infrastructure, cash flow determines survival, not P&L statements.

Their working capital management was obsessive. They negotiated 10-15% mobilization advances on new projects—immediate cash inflow. They insisted on monthly progress payments rather than milestone-based payments. They maintained strict 60-day collection cycles when industry average exceeded 120 days. Sometimes this meant walking away from projects with attractive margins but poor payment terms. The discipline paid off—PNC never faced a working capital crisis even during sector-wide liquidity crunches.

Lesson 4: Asset-light is a myth—asset-right is the goal

The consulting world's obsession with asset-light models doesn't translate to infrastructure. You can't build highways without equipment. But the opposite extreme—owning everything—destroys returns. PNC found the middle path: own critical equipment that differentiates execution, rent commoditized equipment available in markets, lease specialized equipment for specific projects.

They owned pavers, sensor-based compactors, and concrete batching plants—equipment where quality directly impacted execution. They rented trucks, basic earthmovers, and general equipment easily available. They leased specialized boring machines or bridge construction equipment for specific projects. This hybrid approach meant capital efficiency without compromising execution quality.

Lesson 5: When to build versus when to buy versus when to monetize

Infrastructure value creation follows a predictable curve. Maximum value addition happens during construction (turning dirt into roads). Moderate value creation during initial operations (proving traffic/revenue models). Minimal value creation during mature operations (collecting predictable tolls). Most companies hold assets through the entire cycle, destroying returns. PNC mastered the art of timing exits.

They typically monetized assets 2-3 years after operations commenced—long enough to prove stability, short enough to maintain IRR. The ₹9,000 crore sale to KKR wasn't lucky timing—it was systematic portfolio management. They built assets when construction margins were attractive, operated them to stability, then sold to yield-seeking investors. The capital recycling multiplied returns far beyond what holding assets could achieve.

Lesson 6: Capital allocation in capital-intensive businesses

Infrastructure's capital intensity makes allocation decisions existential. One wrong mega-project can destroy a decade of value creation. PNC's capital allocation framework was boringly consistent: No single project exceeding 20% of net worth, maintain debt-to-equity below 2:1 always, preserve 6 months of operational expenses in cash, distribute 20-25% of profits as dividends—signaling confidence without starving growth.

During the 2009-2011 boom, when peers leveraged aggressively for BOT projects, PNC maintained discipline. They passed on the Delhi-Mumbai corridor opportunities that attracted everyone. Those projects became albatrosses for aggressive bidders when traffic disappointed. PNC's boring projects on state highways generated steady returns without headlines or headaches.

Lesson 7: Surviving sector downturns—it's not about prediction, it's about preparation

Every infrastructure boom spawns predictions of "this time is different"—better policies, improved execution, sustainable growth. Every bust brings despair about structural problems, unfixable issues, permanent decline. PNC ignored both narratives. They prepared for downturns during booms and positioned for recovery during busts.

Their downturn preparation was systematic: maintaining cash reserves when others distributed everything, keeping debt serviceability even at 50% revenue decline, diversifying revenue streams before concentration became dangerous, building relationships when you don't need them—they become invaluable when you do.

When the 2018 IL&FS crisis erupted, PNC didn't need emergency measures. They had cash to continue operations, relationships to maintain credit lines, and balance sheet strength to acquire distressed assets. They emerged stronger from every crisis not through prediction but through preparation.

Lesson 8: The relationship moat in a relationship business

Infrastructure is ultimately a relationship business masquerading as engineering. Technical qualification gets you shortlisted; relationships get you contracts. But not the relationships most imagine—not political connections that change with governments, but operational relationships that survive regime changes.

PNC built relationships with the permanent government—chief engineers who evaluate projects, financial controllers who process payments, field engineers who approve variations. These relationships, built over decades of reliable execution, created an invisible moat. When evaluation committees scored technical bids, PNC's track record earned points competitors couldn't match. When payments were prioritized during fiscal crunches, PNC's invoices moved up the queue.

Lesson 9: Technology as a tool, not a strategy

Every infrastructure conference features technology evangelists promising revolution—AI-powered project management, blockchain-based payments, drone monitoring replacing engineers. PNC's approach was pragmatic. They adopted technology that solved specific problems: GPS tracking for equipment utilization, sensor-based quality control for concrete strength, project management software for milestone tracking.

But they never confused technology with strategy. The best AI couldn't compensate for poor project selection. Blockchain wouldn't fix working capital management. Drones couldn't replace experienced site engineers. Technology amplified good execution; it didn't replace it.

Lesson 10: The ultimate lesson—respect the business

Infrastructure looks deceptively simple. Buy equipment, hire engineers, build roads, collect payments. This simplicity attracts cowboys who think aggression substitutes for expertise. The sector's complexity—managing thousands of workers, coordinating hundreds of vendors, navigating bureaucratic mazes, handling environmental challenges, dealing with land acquisition, managing community relations—humbles everyone eventually.

PNC's deepest competitive advantage was respecting infrastructure's complexity. They never assumed projects would be easy. They always budgeted for delays. They consistently prepared for complications. This respect—call it paranoia or prudence—meant they were rarely surprised. In infrastructure, surprise is expensive.

The playbook isn't complicated: respect cycles, manage cash, time exits, maintain discipline, build relationships, prepare for downturns. But simple doesn't mean easy. It requires saying no to attractive projects, maintaining costs during booms, investing during busts, and most difficult of all—being content with steady returns while watching aggressive peers capture headlines. In infrastructure investing, boring is beautiful, survival is success, and discipline is the only sustainable competitive advantage.

XII. Bear vs Bull Case

The investment case for PNC Infratech splits the room like no other infrastructure stock. Bears see a company trapped in slow growth with mounting challenges. Bulls see a coiled spring ready to capitalize on India's infrastructure supercycle. Both sides marshal compelling evidence. The truth, as always, lies in which narrative you believe about India's future and PNC's ability to execute within it.

The Bear Case: A Melting Ice Cube in a Heating Sector

Start with the numbers that keep bears up at night. Slow revenue growth, margin pressure—the 5-year revenue CAGR of 3.85% is abysmal in a country supposedly undergoing an infrastructure revolution. When GDP grows at 6-7% and infrastructure spending increases double-digits, a 3.85% growth rate suggests market share loss, execution challenges, or strategic missteps. Bears argue this isn't temporary—it's structural. PNC played it too safe and missed the growth wave.

The margin trajectory reinforces concerns. High contingent liabilities—₹3,604 crores of contingent liabilities hang like a sword over the balance sheet. While management calls these "standard operational guarantees," bears see hidden risks. One project gone wrong, one guarantee invoked, one dispute escalated—and suddenly these contingent items become real liabilities. In infrastructure, where disputes are common and projects complex, contingent liabilities are time bombs with uncertain fuses.

Government spending dependency creates existential risk. With 80%+ revenues from government contracts, PNC is essentially a leveraged bet on fiscal health and political priorities. Government delays payments during fiscal stress. Election years see project slowdowns. Policy changes can eliminate entire revenue streams overnight. The recent shift from BOT to HAM helped PNC, but what happens when the next policy shift doesn't favor their model?

Competition from larger players intensifies daily. L&T's infrastructure division alone is 5x PNC's size. When L&T decides to compete in mid-sized projects—PNC's bread and butter—they bring engineering capabilities, financial strength, and relationships PNC can't match. International players like China State Construction Engineering Corporation are also eyeing India. PNC's regional player status becomes a liability in nationally integrated markets.

Execution risks on large projects multiply with scale. PNC's recent ₹3,500 crore mining contract sounds impressive until you consider they've never executed mining projects of this scale. Diversification into new sectors—mining, water, railways—brings execution risks. Each sector has unique challenges, different working capital cycles, and specialized technical requirements. One botched project in a new sector could destroy reputation across all verticals.

The technology disruption threat looms large. International construction giants are deploying AI, robotics, and automation at scale. Prefabrication and modular construction could make traditional site-based construction obsolete. PNC's limited technology investments might save costs today but could make them uncompetitive tomorrow. In a sector where 2-3% margin differences determine winners, technology-driven efficiency gaps could be fatal.

The working capital intensity remains problematic despite management claims of efficiency. Even at 80-90 days, working capital locks up ₹1,500-2,000 crores. As revenue grows, working capital needs grow proportionally. This creates a perpetual cash trap—growth requires working capital, which requires debt or equity, which dilutes returns. It's a treadmill where you run faster just to stay in place.

Management succession poses unaddressed risks. Pradeep Kumar Jain built PNC from scratch, but founder-led companies often struggle with transitions. No clear succession plan is visible. The second generation's involvement remains unclear. In relationship-driven infrastructure, leadership transitions can disrupt carefully cultivated networks.

The asset monetization strategy might have peaked. The ₹9,000 crore sale to KKR was exceptional, but can it be repeated? InvIT markets are becoming saturated. Yield expectations are rising. Future monetizations might not achieve similar valuations. If the capital recycling strategy stumbles, PNC's growth model breaks.

Regulatory and policy risks compound. Environmental regulations are tightening, land acquisition is becoming harder, and community resistance to infrastructure projects is growing. The Supreme Court's recent interventions in construction projects show judicial activism rising. Any regulatory violation or compliance failure could lead to project suspensions or penalties.

The Bull Case: A Compressed Spring in India's Golden Decade

But bulls see opportunity where bears see obstacles. Management expects 20% gross revenue growth for FY26—a dramatic acceleration that signals inflection, not decline. The slow growth of recent years wasn't failure—it was strategic patience. PNC deliberately slowed during the sector's stress period, preserving capital and relationships. Now, with balance sheet strength and execution capability intact, they're ready to accelerate.

The order backlog of approximately ₹4,630 crores seems modest but misses the point. PNC doesn't chase orders—they select them. Their order book represents 12-18 months of high-quality, executable, profitable projects rather than 3-4 years of uncertain, low-margin ventures. Quality over quantity has always been their approach, and it's about to pay off.

Asset monetization unlocking value is just beginning. The ₹9,000 crore KKR deal wasn't a one-off—it validated PNC's asset quality and opened doors for future monetizations. With 10+ operational HAM projects maturing, the monetization pipeline is robust. Each successful sale provides capital for new projects, creating a virtuous cycle of growth without dilution.

Diversifying into renewable energy and smart metering opens massive addressable markets. India's renewable energy targets require ₹15 lakh crores of investment. Smart metering initiatives cover 250 million households. Even capturing 1-2% of these opportunities would double PNC's revenue. Their infrastructure execution capabilities translate directly to these sectors.

The infrastructure spending tailwinds are hurricane-force. India's infrastructure opportunity: $1.4 trillion investment needed by 2025 translates to ₹115 lakh crores—annual spending of ₹20+ lakh crores. Even maintaining market share in this expansion would drive significant growth. PNC doesn't need to win share—just participate in the tide lifting all boats.

The competitive positioning is stronger than it appears. Yes, L&T is larger, but they also chase larger, more complex projects. In the ₹500-2,000 crore sweet spot where PNC operates, competition is fragmented and regional. PNC's relationships, execution track record, and balance sheet strength make them a preferred partner for risk-averse government agencies.