Pitti Engineering: The Engineering Backbone of India's Industrial Revolution

I. Introduction & Episode Roadmap

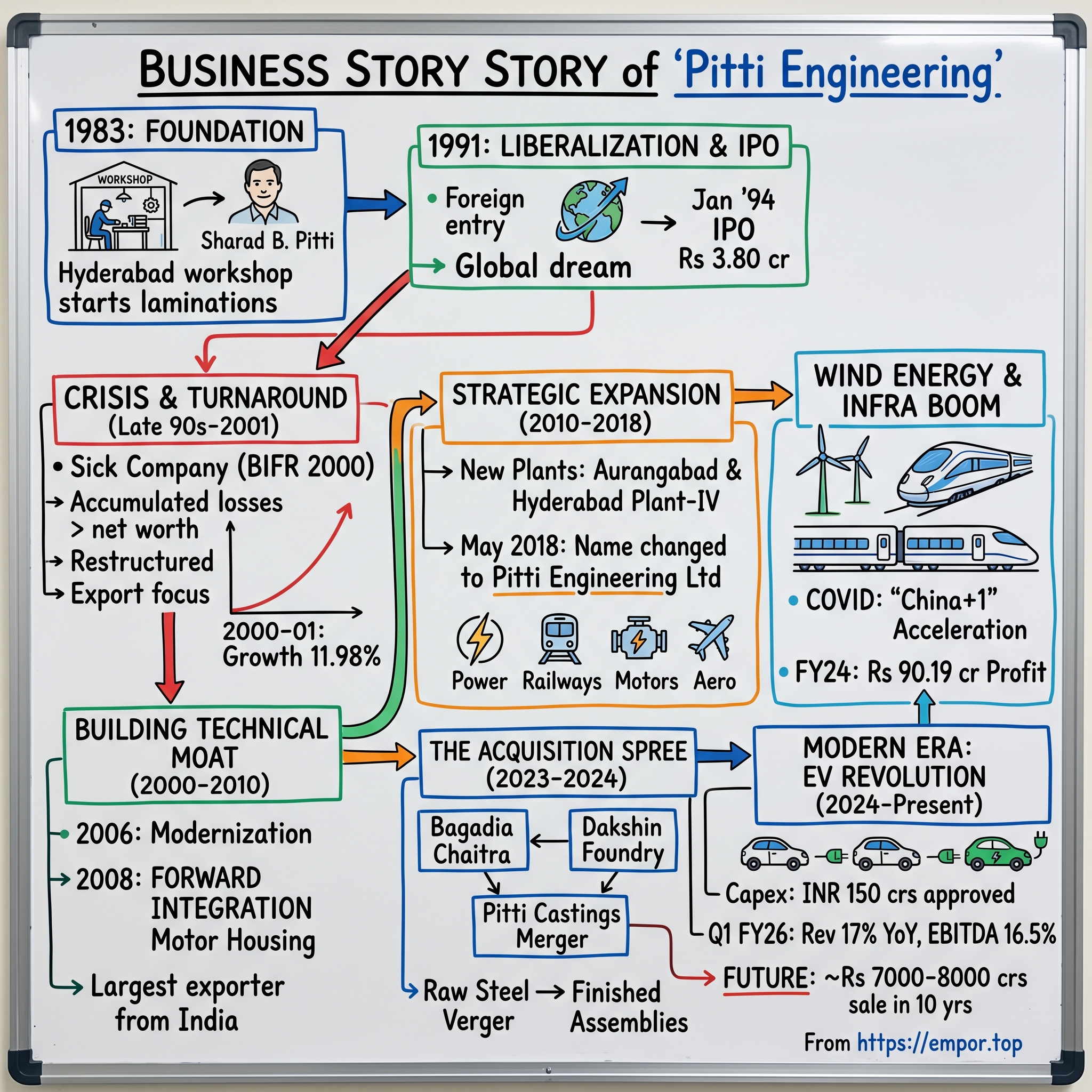

Picture this: A small workshop in Hyderabad, 1983. The clatter of metal against metal echoes through the humid air as workers shape electrical steel into precise laminations. This wasn't just another manufacturing startup—it was the birth of what would become India's engineering backbone, supplying critical components to everything from wind turbines to bullet trains. The man behind it: Sharad B. Pitti, a visionary who saw opportunity where others saw commodity manufacturing.

Shri Sharad B Pitti, founder of the Company is a visionary leader who pioneered lamination manufacturing in India. Pitti Laminations Limited promoted by Sharad B. Pitti, was founded in 1983 and is India's largest and most reputed manufacturer of Electrical Steel Laminations, Motor Cores, Sub-Assemblies, Die-Cast Rotors and Press Tools. What started as Pitti Laminations Limited would undergo a remarkable transformation over four decades, becoming the critical supplier to India's infrastructure boom and renewable energy revolution.

The puzzle at the heart of this story isn't just how a lamination manufacturer survived the liberalization era and emerged stronger—it's how they built a technical moat in what many consider a commoditized business. How did a company making seemingly simple metal components become indispensable to Fortune 500 giants like GE, Siemens, and ABB? And perhaps more intriguingly, how did they time every major industrial wave perfectly—from India's early power generation needs to the current EV revolution?

Today, Pitti Engineering Ltd has a market capitalisation of Rs 3,682 crore, serving customers across five continents. But this isn't just a story about scaling manufacturing—it's about building technical expertise that becomes irreplaceable, about vertical integration that creates competitive advantages, and about riding multiple S-curves of industrial growth simultaneously.

Our journey will take us through the License Raj era where getting permits was harder than building factories, through the economic liberalization that opened global markets, into the infrastructure boom of the 2000s, and finally to today's energy transition. We'll explore how strategic acquisitions, starting with the recent Bagadia Chaitra deal, are positioning Pitti for the next decade of growth. And we'll examine whether their ambitious target of reaching ₹7,000-8,000 crore in revenue over the next decade is achievable or aspirational.

II. Origins & Foundation (1983-2000)

The year was 1983, and India was a different country. The License Raj still controlled every aspect of industrial production—you needed government permission to expand capacity, import machinery, or even change your product mix. In this stifling environment, Pitti Engineering Limited (Formerly known as Pitti Laminations Limited) was incorporated on September 17 1983 in Hyderabad, then part of undivided Andhra Pradesh.

Sharad B. Pitti wasn't your typical industrialist. While others chased glamorous sectors, he saw opportunity in the unglamorous world of electrical steel laminations—the core components that go into every electric motor and generator. These thin sheets of specially treated steel, stacked and assembled, form the heart of rotating electrical machines. Without them, nothing moves—no pumps, no generators, no industrial motors.

The early years were about survival and learning. We have the distinction of being the first lamination manufacturer in India and the first company in the State of Andhra Pradesh to be certified as an ISO 9002 Company in the year 1993. This early focus on quality wasn't just about certificates—it was about building credibility with customers who had alternatives.

The company's initial capacity was modest, but the ambition was not. They started with basic laminations, learning the nuances of electrical steel—how grain orientation affects efficiency, how coating thickness impacts performance, how tolerances of mere microns can make or break a motor's efficiency. Every order was a learning opportunity, every customer complaint a chance to improve.

Then came 1991—India's economic liberalization. Suddenly, the protective walls came down. Foreign companies could enter India, but Indian companies could also dream of global markets. For Pitti, this was both threat and opportunity. The threat was clear: global giants with better technology and deeper pockets. The opportunity was less obvious but more profound: access to global customers who valued quality and reliability over just price.

The company came out with a public issue of 19 lac shares at a premium of Rs 10 per share, aggregating Rs 3.80 cr, in Jan.'94. The proceeds of the issue were utilised to part-finance the Rs 5.6-cr project to expand the company's product range of electrical-grade stampings. This IPO, modest by today's standards, was transformative. It provided capital for modernization just as India's power sector was beginning its expansion phase.

The mid-1990s brought both growth and crisis. In 1994-95, PLL expanded its capacity to 4000 tpa. It has launched a second expansion programme to raise the capacity from 4000 tpa to 6000 tpa at an estimated cost of Rs 4.80 cr. But aggressive expansion in a volatile economy took its toll. By the late 1990s, mounting losses led to a harsh reality: At the end of the financial year 1998-99, the companys accumulated losses exceeded its net worth, therefore the company would be treated as a Sick Industrial Company under the provisions of the Sick Industrial Companies (special provisions) Act, 1985.

The BIFR (Board for Industrial and Financial Reconstruction) declaration in 2000 could have been the end. Many companies didn't survive this stigma. But for Pitti, it became a crucible that forged a more resilient organization. Under the oversight of State Bank of India as operating agency, they restructured operations, focused on cash generation, and most importantly, doubled down on what they did best—making high-quality laminations.

The company has registered a growth of 11.98% in the turnover during the year 2000-01.Therefore the turnover of the company is stood at Rs.2520.09 lakhs during the year 2001 as against Rs.2250.42 lakhs in the previous year. Though the improvement in sales volume is nominal, larger revenue has derived from commercialization of tool room and relatively higher exports during the year.

This turnaround wasn't dramatic—it was grinding, methodical work. Focus on exports, which offered better margins and payment terms. Develop the tool room capabilities, which allowed customization and faster prototyping. Build relationships with global customers who would become long-term partners. By the end of this period, the foundation was set for the next phase of growth.

III. Building Technical Moat & Export Capabilities (2000-2010)

The new millennium brought new energy to Pitti. Having survived the BIFR crisis, the company emerged leaner and more focused. But survival wasn't the goal—dominance was. The strategy was clear: become so technically proficient that customers couldn't easily switch suppliers, even if they wanted to.

The Phase I New Plant with an installed capacity of 4000 MT per annum commenced commercial operations on 13th April, 2005. This wasn't just capacity addition—it was a statement of intent. The new facility incorporated lessons learned over two decades: layout designed for flexibility, equipment chosen for precision, processes built for consistency.

But the real transformation came in 2006. The expansion-cum-modernisation project of the Company was commissioned in Sep' 06. This modernization was comprehensive—new notching machines that could handle larger diameters, deburring equipment that guaranteed burr levels under 5 microns, and crucially, investment in testing equipment that could validate quality at every stage.

Then came a pivotal strategic decision: forward integration. The Forward Integration Project of Motor Housing was commissioned on January 28, 2008. This move up the value chain was more than just adding machining capabilities. It meant Pitti could now offer assembled cores, tested and ready for winding. For customers, this reduced their vendor base, simplified logistics, and most importantly, provided single-point accountability for quality.

The export story during this period was remarkable. From being a struggling domestic player, Pitti transformed into We are proud to be the largest exporter of laminations from India. This wasn't achieved through price competition alone. The key was understanding that different markets had different needs. European customers obsessed over efficiency—every fraction of a percentage point mattered. American customers focused on reliability and consistency. Asian customers wanted flexibility and quick turnarounds.

Setup in 2006, with state of the art facilities like Titan Make CNC VTL(s), Wotan Make CNC HBM(s), Mitsui Seiki CNC HMC(s), Mitsui Seiki CNC VMC(s) and LK CMM(s) among others. Machine shop is also equipped with Grit Blasting and Painting Facilities including Drying Chambers. This machine shop wasn't just about adding capacity—it was about capability. Now they could machine castings up to several tons, maintaining tolerances that few in India could achieve.

The 2008 financial crisis could have derailed this momentum. Global orders dried up, payments were delayed, and credit became scarce. But Pitti had learned from their late-1990s crisis. They had diversified their customer base across geographies and industries. When power generation orders slowed, railway modernization picked up. When developed markets stuttered, emerging markets continued growing.

Established in 2008, the foundry has since developed over 250 components for varied industries like Railways Off Highway Vehicles, Earthmoving equipment's, Compressors, Windmills, Power Sector, Transmission parts,Oil and Gas, etc. This foundry addition was strategic—it provided backward integration for castings while opening new customer segments.

By 2010, the transformation was complete. From a single-product lamination manufacturer, Pitti had evolved into an integrated engineering solutions provider. They could take a customer's drawing and deliver a finished, tested assembly—handling everything from raw material procurement to final quality certification. The technical moat was built not through any single capability but through the integration of multiple capabilities that created switching costs too high for customers to bear.

The numbers tell the story of this transformation. From revenues of ₹25 crores in 2001, the company had grown multifold by 2010. But more importantly, the customer list now read like a who's who of global engineering: The company is a key and critical supplier to its customers which are mostly the Fortune 200 MNCs like GE, Alstom, Siemens, ABB, Cummins, etc.

IV. The Strategic Expansion Era (2010-2018)

The 2010s opened with India in the midst of an infrastructure boom. Power plants were being built at record pace, metro systems were expanding, and industrial growth was accelerating. For Pitti, this presented an opportunity to scale beyond what founders might have imagined. But scaling in manufacturing isn't just about adding machines—it's about orchestrating complexity across multiple locations while maintaining quality and efficiency.

The company's strategy during this period was distinctive: instead of building one massive facility, they chose strategic locations closer to customer clusters. This reduced logistics costs, improved response times, and most importantly, deepened customer relationships through proximity.

During the year 2017-18, the Company had commenced operations at the Aurangabad and commenced commercial production at Hyderabad (Plant -IV). The Aurangabad facility was particularly strategic—located in Maharashtra's auto and industrial belt, it provided access to a different customer base while serving as a natural hedge against regional disruptions.

The Hyderabad Plant-IV represented the culmination of three decades of learning. Every aspect was optimized: layout designed for lean manufacturing, equipment selected for flexibility and precision, processes digitized for real-time monitoring. This wasn't just another factory—it was a statement about where Indian manufacturing could compete globally.

But perhaps the most significant change during this period was the recognition that "Pitti Laminations" no longer captured what the company had become. The Company changed the name to 'Pitti Engineering Limited' from Pitti Laminations Limited on 9 March 2018. Company's name was renamed from Pitti Laminations Limited' to Pitti Engineering Limited', effective from May 08, 2018.

Mr. Akshay S. Pitti, Vice-Chairman & Managing Director, said, "The Company's offerings have evolved, based on its core business, strongly rooted research and industry led innovation. The name change was planned to align with the advancement in our skills and capabilities to cater to a varied range of basic engineering products for developing an integrated supply chain for our customers."

The name change was more than cosmetic—it signaled a fundamental shift in positioning. No longer were they just suppliers of components; they were engineering partners who could solve complex manufacturing challenges. The product portfolio by now spanned an impressive range: from tiny laminations for medical equipment to massive assemblies for wind turbines, from precision-machined railway components to specialized parts for aerospace applications.

During this period, the company also began to see the fruits of their earlier investments in technology and quality. They weren't competing on price anymore—they were competing on capability. When a wind turbine manufacturer needed laminations that could withstand harsh offshore conditions, Pitti could deliver. When a railway equipment manufacturer needed assemblies that met stringent European safety standards, Pitti had the certifications and processes.

The diversification across end-user industries was deliberate and strategic. The Company caters to the needs of the power generation, transportation, industrial motors, locomotives, aerospace, automobile, earth moving and mining, oil and gas and infrastructure industries. This wasn't random expansion—each sector was chosen for its growth potential and synergy with existing capabilities.

By 2018, the company had built three state-of-the-art manufacturing facilities, employed over 1,000 people, and was serving customers across five continents. The installed capacity had grown to 32,000 TPA of laminations and is being expanded further, in stages to 50,000 TPA. But more than physical expansion, this era was about building organizational capabilities—systems, processes, and culture that could sustain growth.

V. Wind Energy & Infrastructure Boom (2018-2023)

If the previous decade was about building capability, this period was about capturing opportunity. India's energy transition was accelerating, railway modernization was in full swing, and global supply chains were being reconfigured. For a company with Pitti's capabilities, it was like multiple growth vectors converging simultaneously.

The renewable energy story was particularly compelling. India had set ambitious targets for wind and solar capacity, and every megawatt of wind power needed specialized laminations for generators. These weren't ordinary laminations—they needed to handle variable speeds, harsh environments, and operate efficiently across a wide range of conditions. Pitti's decades of expertise positioned them perfectly for this boom.

Its products are used in hydro and thermal generation, wind energy, mining, cement, steel, sugar, construction, lift irrigation, freight rail, passenger rail, mass urban transport, e-mobility, appliances, medical equipment, oil and gas, and other industrial applications. This diversification wasn't just about risk mitigation—it was about capturing the full value of India's industrial transformation.

The railway modernization presented another massive opportunity. India's push for indigenous manufacturing through programs like Make in India meant that foreign OEMs needed local partners. But not just any partner—they needed suppliers who could meet global quality standards while navigating India's complex business environment. During the year 2020-21, Company incorporated a Wholly Owned Subsidiary (WoS) viz., Pitti Rail and Engineering Components Limited on 5th October 2020.

This subsidiary wasn't just organizational restructuring—it was about focus. The railway business had different dynamics: longer development cycles, stringent safety requirements, and different commercial terms. By creating a dedicated entity, Pitti could serve this sector better while maintaining focus in other areas.

The COVID-19 pandemic in 2020 could have disrupted this momentum, but it actually accelerated certain trends. Global companies started seriously pursuing "China Plus One" strategies, looking for alternative suppliers in India. Pitti, with its proven track record and existing relationships, was perfectly positioned to capture this shift.

The export growth during this period was remarkable. From being primarily a domestic player two decades ago, exports now contributed approximately 30-35% of revenues, serving customers across five continents. But this wasn't just about selling the same products globally—it was about developing specific solutions for different markets. Revarnishing lines for the European market, where efficiency standards were highest. Specialized coatings for Middle Eastern markets, where equipment faced extreme temperatures. Custom assemblies for North American customers, who valued integration and single-source supply.

Government of India by FY30 plans to achieve a 500GW non-fossil fuel-based capacity through solar and wind power. This massive expansion meant thousands of wind turbines, each requiring hundreds of kilograms of specialized laminations. For Pitti, this wasn't just a market opportunity—it was validation of their strategic positioning over the previous decade.

The financial performance during this period reflected this operational success. For the year ended 2024, Pitti Engineering Ltd had posted a profit of Rs 90.19 crore on a total income of Rs 1,218.65 crore. But perhaps more importantly, the company was now debt-free, with strong cash generation providing flexibility for the next phase of growth.

VI. The Acquisition Spree & Vertical Integration (2023-2024)

The year 2024 marked a pivotal inflection point in Pitti's growth strategy. After four decades of primarily organic growth, the company embarked on an aggressive acquisition strategy that would fundamentally reshape its competitive position. This wasn't desperation or empire-building—it was calculated strategic positioning for the next phase of industrial growth.

The centerpiece of this transformation was the Bagadia Chaitra acquisition. Pitti Engineering Limited (PEL) on March 11, 2024 said that it has signed an agreement with Bagadia Chaitra Industries Private Limited (BCIPL) and its shareholders to acquire 100% of the equity share capital of BCIPL at an enterprise valuation of Rs 124.92 crore. In addition, PEL will infuse up to Rs 40 crore as new capital into BCIPL, to repay its existing debt.

The strategic rationale was compelling. PEL's acquisition of BCIPL will give it a strategically important manufacturing base in Bangalore, one of the largest consumption centers of motor and generator components in south India. But this was about more than geography. BCIPL brought capabilities in smaller laminations and aluminum die-cast rotors, complementing Pitti's strength in larger components.

The company plans to reorganize its business to the right location as it ships 6000 tonnes from Aurangabad facilities to Bangalore and 4000 tonnes from Bangalore to Aurangabad. So, by relocating these two businesses to the right location of consumption centers, it will reduce logistical costs which will enable margin growth. This operational synergy alone could add 100-150 basis points to margins—significant in a business where every basis point matters.

But Bagadia Chaitra was just the beginning. Similarly, it acquired 100% equity of Dakshin Foundry Private Limited in July 2024, making Dakshin Foundry a wholly owned subsidiary. The Dakshin Foundry acquisition addressed a different strategic need: securing raw material supply and backward integration into castings. In an industry where raw material costs constitute 60-70% of revenues, controlling this part of the value chain provided both cost advantages and supply security.

The merger with Pitti Castings added another dimension. In 2023-24, the Scheme of Amalgamation between Pitti Castings Private Limited (PCPL) and Pitti Rail and Engineering Components Limited (PRECL) with the Company of achieving vertical integration, broaden the Company's footprint across the supply chain and enhance Company's margins and profitability became effective on October 24, 2024. In terms of the said Scheme, 1 equity share of the Company of face value of Rs 5 each, fully paid-up for every 55 equity shares of PCPL of Rs 10/- each, fully paid up were issued to the Company through the Share Exchange Ratio.

This series of acquisitions transformed Pitti from a components manufacturer to an integrated engineering solutions provider. They could now control the entire value chain—from raw steel to finished, tested assemblies. For customers, this meant single-source procurement, consistent quality, and simplified logistics. For Pitti, it meant better margins, reduced working capital cycles, and importantly, deeper customer stickiness.

Akshay Pitti, Vice Chairman and Managing Director of Pitti Engineering Limited said, "We are very excited to welcome BCIPL's leadership team, and their employees to the Pitti group. The acquisition of BCIPL is an important step in this direction as it is strategically relevant, provides enhanced operational strength and adds customer base."

The integration of these acquisitions was methodical. Rather than imposing Pitti's systems wholesale, they took a selective approach—maintaining what worked while upgrading what didn't. BCIPL's customer relationships in South India were preserved and leveraged. Dakshin's foundry expertise was enhanced with Pitti's quality systems. The combined entity emerged stronger than the sum of its parts.

Financially, these acquisitions were structured prudently. Despite the aggressive expansion, It plans to be debt free by FY26. This wasn't financial engineering—it was disciplined capital allocation, using strong cash flows from existing operations to fund strategic growth.

VII. Modern Era: EV Revolution & Global Ambitions (2024-Present)

As we enter the present era, Pitti Engineering stands at the confluence of multiple megatrends. The electric vehicle revolution, renewable energy expansion, railway electrification, and industrial automation—each represents a multi-decade growth opportunity. The company's recent performance suggests they're executing well on this opportunity.

Pitti Engineering Ltd (BOM:513519) reported a 17% year-on-year growth in consolidated revenue for Q1 FY26, reaching INR457 crores. EBITDA increased by 30% year-on-year, with margins improving to 16.5%, up from 14.8% in Q1 FY25. These aren't just good numbers—they represent successful execution during a period of global uncertainty and supply chain disruptions.

The guidance for the future is ambitious but grounded in reality. Company is on track of achieving a sale of ~Rs. 7000-8000 crs in 10 years. In terms of volume it plans to achieve 1,50,000 MT of sheet metal sales. This represents roughly a 6-7x increase from current levels—aggressive, but not unprecedented in Indian manufacturing.

The capacity expansion underway supports these ambitions. Capital Expenditure: INR150 crores approved for capacity expansion over the next 18 months. More specifically, The expansion includes increasing annual sheet metal capacity from 90,000 MT to 1,08,000 MT, machining capacity from 6,48,000 hours to 7,20,000 hours, and castings capacity from 18,600 MT to 24,600 MT.

But capacity is just enabler—the real story is about market positioning. In the EV space, every electric motor needs laminations, and the requirements are more stringent than traditional motors. Higher speeds mean tighter tolerances. Better efficiency requirements mean superior material properties. Thermal management becomes critical. Pitti's decades of expertise in specialized laminations positions them perfectly for this transition.

The export story continues to strengthen. On the international front, our exports business continues to grow steadily, contributing 31% to revenues in Q1FY26. But there are challenges too. Our exposure to the U.S. is about 9-10% of total revenue. The tariffs are significant, but we expect customers to absorb them. We are exploring shifting production within global supply chains if necessary.

The operational metrics tell a story of a business hitting its stride. During the quarter, capacity utilisation reached 82 per cent for machined hours, 70 per cent for sheet metals, and 69 per cent for castings. These utilization levels suggest room for growth without significant additional investment—a sweet spot for margin expansion.

Akshay S Pitti, Managing Director & CEO said: "We delivered a strong start to FY26 with revenue growing 17% YoY to Rs 457 crore for Q1FY26, EBITDA increasing by 30% to Rs 75 crore, and PAT rising 17% to Rs 23 crore. Demand from end-user industries remains strong, supported by healthy order enquiries and bookings. Our backward integration capabilities and diversified product portfolio, which caters to multiple industries, position us well to tap into the expanding domestic market."

The product mix evolution is particularly interesting. Sales volume for stator frames (core drop) grew by 28 per cent, shafts (machined components) rose by 19.8 per cent, and integrated assemblies of stator frames or rotor shafts (laminations) increased by 15.8 per cent. The faster growth in value-added products like assembled stator frames suggests successful execution of the margin expansion strategy.

New customer wins continue to validate the strategy. A second platform for alternators for data centres was secured from an existing customer, expected to generate over Rs 200 million in revenue at peak. Data centers represent a new growth vector—with AI and cloud computing driving massive data center buildouts, the demand for reliable power generation and backup systems is exploding.

VIII. Financial Performance & Market Journey

The financial evolution of Pitti Engineering reads like a textbook case of value creation through operational excellence and strategic positioning. From its modest IPO in 1994 to becoming a multi-thousand crore enterprise, the journey offers lessons in building wealth through industrial manufacturing—a sector often overlooked by investors enamored with technology and consumer businesses.

The public market journey began modestly. The company came out with a public issue of 19 lac shares at a premium of Rs 10 per share, aggregating Rs 3.80 cr, in Jan.'94. That ₹20 share (₹10 face value plus ₹10 premium) has delivered spectacular returns for patient investors. The stock's recent performance has been particularly impressive: Pitti Engineering Ltd share price moved down by 3.85% on BSE in the last month, but zooming out reveals the real story.

The long-term wealth creation has been remarkable. From the depths of the BIFR crisis in 2000, when the stock likely traded in single digits, to today's levels approaching ₹1,000, patient investors have been rewarded handsomely. The market capitalisation of Rs 3,682 crore represents substantial value creation from humble beginnings.

Recent financial performance justifies the market's confidence. For the year ended 2024, Pitti Engineering Ltd had posted a profit of Rs 90.19 crore on a total income of Rs 1,218.65 crore. This translates to a net margin of approximately 7.4%—respectable for an engineering business, with room for improvement as the product mix shifts toward higher-value assemblies.

The margin expansion story is already playing out. EBITDA Margin: Improved to 16.5%, up 170 basis points from 14.8% in Q1 FY25. This 170 basis point improvement in one year demonstrates the operating leverage in the business model. As utilization increases and product mix improves, these margins should expand further.

The order book provides visibility into future growth. The order book of the company as of Dec 31st 2023 stands at Rs.898 crs. For FY25, it is targeting 50,000 MT as sales volume. An order book of nearly ₹900 crores against annual revenue of ₹1,200 crores provides reasonable visibility, though not excessive coverage—suggesting strong execution capabilities and customer confidence rather than over-booking.

Working capital management has been a focus area. The increase in working capital cycle from 57 to 75 days and the decision to stop factoring export receivables have impacted finance costs. While the working capital cycle has extended, this is partly strategic—building inventory to manage supply chain uncertainties and extending credit to win new customers. The decision to stop factoring suggests confidence in cash generation.

The capital allocation philosophy deserves attention. Despite aggressive acquisitions, the company maintains discipline: It plans to be debt free by FY26. This isn't just financial conservatism—it's strategic flexibility. In cyclical industries, the companies that maintain strong balance sheets during upturns can capitalize on opportunities during downturns.

Analyst expectations reflect confidence in the growth story. Pitti Engineering aims for 10% volume growth in FY26, targeting revenues of ₹2,000 crore for FY26 and ₹2,100–2,200 crore for FY27, supported by enhanced capacity utilization and a shift towards value-added products. These targets imply a revenue CAGR of approximately 15% over the next two years—aggressive but achievable given the capacity additions and market opportunities.

The shareholding pattern reveals interesting dynamics. Promoter holding in Pitti Engineering Ltd has gone up to 54.18 per cent as of Mar 2025 from 53.58 per cent as of Sep 2024. Increasing promoter stake at current valuations signals management confidence in future prospects.

IX. Playbook: Business & Investing Lessons

After four decades of building Pitti Engineering, several powerful lessons emerge that transcend the specific industry and offer insights for both operators and investors. These aren't theoretical frameworks but battle-tested strategies that helped transform a small lamination workshop into an engineering powerhouse.

Building Technical Moats in Commoditized Industries

The first and perhaps most counterintuitive lesson: you can build moats in seemingly commoditized businesses. Laminations are essentially shaped metal sheets—hardly seems like a defensible business. But Pitti proved that the moat isn't in the product but in the ecosystem around it.

They built this moat through multiple layers: technical expertise that allows them to hit tolerances competitors can't, quality certifications that take years to obtain, relationships with global OEMs that value consistency over cost, and integrated capabilities that create switching costs. When a wind turbine manufacturer sources laminations from Pitti, they're not just buying metal sheets—they're buying reliability, technical support, and supply chain simplification.

The Power of Vertical Integration—When Done Right

Vertical integration has fallen out of favor in the age of asset-light business models, but Pitti shows when it makes sense. Their backward integration into castings through Dakshin Foundry and forward integration into assemblies wasn't about control—it was about capability and economics.

By controlling the casting process, they could ensure material quality and reduce procurement cycles. By offering assembled and tested products, they could capture more value and create stickier customer relationships. The key was integrating where it created genuine value, not just to expand the empire.

Timing Market Cycles vs. Creating Them

Pitti didn't create the renewable energy boom or the railway modernization wave—they positioned themselves to capture value when these waves arrived. The investments in capacity and capability preceded the demand surge. When India announced ambitious renewable energy targets, Pitti already had the certifications and capacity. When global companies pursued China+1 strategies, Pitti had the track record and relationships.

This requires patient capital and conviction—investing in capabilities before demand materializes fully. It also requires the discipline to not chase every opportunity. Pitti stayed focused on rotating electrical machines even as adjacent opportunities beckoned.

Managing Working Capital in Engineering Businesses

Engineering businesses are working capital intensive—there's no escaping it. Raw materials need to be stocked, production cycles are long, and customers expect credit terms. Pitti's approach was pragmatic: optimize where possible but accept that some working capital investment is the cost of growth.

Their recent extension of working capital cycles from 57 to 75 days might seem like deterioration, but it's strategic. In a high-growth phase, extending credit to win new customers and building safety stock to manage supply uncertainties can be value-creating decisions. The key is ensuring that the returns on incremental sales exceed the cost of additional working capital.

Export Strategy and Global Customer Relationships

Building an export business from India in engineering products requires more than competitive pricing. Pitti's success came from understanding that different markets value different attributes. They didn't try to serve all markets with the same product—they developed specific solutions for specific needs.

Equally important was their investment in certifications and quality systems that global customers demanded. Getting certified by a European railway authority or an American power generation company takes years and significant investment. But once achieved, these certifications become competitive moats.

Strategic M&A for Capability Building vs. Scale

Pitti's recent acquisitions weren't about getting bigger—they were about getting better. Bagadia Chaitra brought access to South Indian markets and capabilities in smaller components. Dakshin Foundry provided backward integration and control over critical inputs. Each acquisition filled a specific strategic gap rather than just adding revenue.

The integration approach was equally thoughtful. Rather than forced standardization, they maintained what worked while upgrading what didn't. This preserved the value of acquired businesses while capturing synergies—a difficult balance that many acquisitive companies fail to achieve.

X. Analysis & Bear vs. Bull Case

Standing at the current juncture, Pitti Engineering presents a fascinating investment debate. The company sits at the intersection of multiple structural growth themes while facing genuine challenges that could constrain value creation. Let's examine both sides with the rigor they deserve.

Bull Case: The Convergence of Multiple Megatrends

The optimistic view starts with the addressable market expansion. India's infrastructure spending is not a cyclical upturn but a structural shift. Government of India by FY30 plans to achieve a 500GW non-fossil fuel-based capacity through solar and wind power. Each gigawatt of wind capacity requires hundreds of tons of specialized laminations. At current market shares, this alone could double Pitti's wind energy business.

The EV revolution presents an even larger opportunity. Every electric vehicle needs motors—for propulsion, power steering, window operations, and numerous other applications. These motors require laminations with specifications far more stringent than traditional applications. Pitti's expertise in high-precision laminations positions them perfectly for this transition. Unlike solar panels or batteries where Chinese dominance seems insurmountable, laminations for motors remain a localized business due to logistics costs and customization needs.

Railway modernization adds another growth vector. India's push for high-speed rail, metro expansion, and freight corridor development requires thousands of traction motors and auxiliary systems. The recent focus on indigenous manufacturing through programs like Atmanirbhar Bharat means foreign OEMs must localize production—and they need capable partners like Pitti.

The successful M&A integration track record suggests management can execute complex strategies. The Bagadia Chaitra acquisition already shows promise, with operational synergies becoming visible. If management can successfully integrate and optimize recent acquisitions while maintaining organic growth, the revenue target of ₹7,000-8,000 crores doesn't seem unrealistic.

Export potential remains underappreciated. With China+1 strategies accelerating and global supply chains being redesigned for resilience, Pitti's established relationships with global OEMs become increasingly valuable. Their proven ability to meet international quality standards and deliver consistently positions them to capture a larger share of global sourcing.

Bear Case: The Challenges of Commoditization and Capital Intensity

The skeptical view starts with the fundamental nature of the business. Despite all the technical capabilities, laminations remain a commodity product where pricing power is limited. When raw material costs rise, passing them through to customers involves negotiations and lags. When customers face pressure, they inevitably squeeze suppliers. The 7-8% net margins reflect this reality—decent but not exceptional.

Capital intensity remains a structural challenge. Every growth phase requires substantial capital investment. The current ₹150 crore capex is just the latest in a continuous cycle. Unlike software or services businesses where growth requires minimal incremental capital, Pitti must constantly invest to grow. This limits free cash flow generation and return on capital employed.

Competition isn't standing still. Global players like Tempel Steel, Cogent Power, and various Chinese manufacturers have deeper pockets and technological advantages. In India, numerous smaller players compete aggressively on price. As the market grows, competition will intensify, potentially pressuring margins.

Dependency on government spending and policy adds volatility. Renewable energy growth depends on policy support and grid infrastructure development. Railway modernization depends on government capital allocation. Any slowdown in public infrastructure spending could significantly impact growth prospects.

Customer concentration, while improving, remains a concern. Large OEMs have significant negotiating power and can squeeze suppliers during downturns. The loss of a major customer or program could materially impact revenues. Additionally, as these OEMs face their own pressures—whether from Chinese competition or technology transitions—they'll inevitably pass pressure down the supply chain.

The Balanced View

The truth likely lies between these extremes. Pitti has demonstrated an ability to navigate cycles and emerge stronger. Their technical capabilities and customer relationships are real moats, even if not impregnable ones. The growth opportunities are genuine, even if execution won't be linear.

The key variables to watch include capacity utilization rates (currently at 70-82%, suggesting room for growth), export percentage (currently 31%, with potential to reach 40-45%), and EBITDA margins (currently 16.5%, with potential for 18-20% as product mix improves). The company's ability to maintain growth while achieving their debt-free target by FY26 will be a crucial test of execution capability.

For investors, Pitti represents a play on India's industrial transformation. It's not a glamorous technology story or a consumer brand with pricing power. It's a nuts-and-bolts business that makes components essential for modern infrastructure. The investment case depends on one's view of India's infrastructure spending, the pace of energy transition, and management's ability to execute in an increasingly complex environment.

XI. Epilogue & Looking Forward

As we stand in late 2024, looking at Pitti Engineering's journey from a small Hyderabad workshop to a ₹3,600 crore market cap engineering conglomerate, the transformation seems almost inevitable in hindsight. But nothing about this journey was predetermined. It was built decision by decision, capability by capability, relationship by relationship.

The next decade presents both the greatest opportunities and the most significant challenges in the company's history. Pitti Engineering aims for 10% volume growth in FY26, targeting revenues of ₹2,000 crore for FY26 and ₹2,100–2,200 crore for FY27. These near-term targets seem achievable given current momentum. But the longer-term ambition of reaching ₹7,000-8,000 crores in a decade requires everything to go right—market growth, successful execution, and favorable policy environment.

The transition to electric mobility could be transformative. If India achieves even half its EV adoption targets, the demand for specialized motors and therefore laminations would exceed current manufacturing capacity by multiples. But this transition also brings risks—new technologies, new competitors, and new customer requirements. Pitti's ability to adapt and evolve will be tested.

The global opportunity is particularly intriguing. As supply chains reconfigure for resilience rather than just efficiency, India's position as a democratic, English-speaking manufacturing alternative to China becomes increasingly valuable. Pitti, with its established credentials and relationships, is well-positioned to capture this shift. But success requires navigating geopolitical complexities, managing currency fluctuations, and maintaining quality across increasing volumes.

The management transition deserves attention. While Sharad B. Pitti remains Chairman, the operational leadership has successfully transitioned to the second generation under Akshay S. Pitti. This transition, often treacherous in Indian family businesses, seems to have been handled well. The younger generation brings international exposure and modern management practices while respecting the foundational values of quality and customer service.

For long-term fundamental investors, several metrics bear watching: capacity utilization trending toward 85-90% would signal the need for next expansion phase; export percentage exceeding 40% would validate the global competitiveness thesis; EBITDA margins sustaining above 18% would confirm successful value addition; and working capital days reducing below 70 would indicate improving operational efficiency.

The broader lesson from Pitti's journey transcends the specific company. It demonstrates that Indian manufacturing can compete globally not just on cost but on capability. It shows that patient capital and consistent execution can build substantial value even in seemingly mundane industries. And it proves that the intersection of engineering excellence and market opportunity can create enduring competitive advantages.

As India stands at the cusp of potentially its greatest infrastructure buildout, companies like Pitti Engineering will play a crucial but often invisible role. Every time a train accelerates smoothly, a wind turbine generates power, or an electric vehicle silently glides by, there's likely a Pitti component enabling that motion. It's not glamorous, but it's essential—and that's perhaps the most sustainable business model of all.

The story of Pitti Engineering is far from over. Whether the next chapter will see them achieve their ambitious targets or face unforeseen challenges remains to be written. But one thing is certain: the company that emerged from near-bankruptcy in 2000 to become India's engineering backbone has already defied considerable odds. For investors and observers alike, the journey ahead promises to be as interesting as the path already traveled.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube