Pine Labs: The Story of India's Offline Payment Monarch

I. Introduction & Episode Roadmap

Picture a checkout counter at a Croma electronics megastore in suburban Mumbai on a Saturday evening. A young couple has spent forty minutes debating whether they can afford the ₹1.4 lakh refrigerator they actually want versus the ₹70,000 one they came in to buy. At the till, the cashier swivels a small grey terminal toward them, taps a few keys, and a screen lights up: "Buy now, pay ₹11,700 a month for 12 months. No interest." The couple looks at each other. They walk out with the expensive fridge.

Neither of them will ever think about the box that made that decision possible. That box—and more importantly, the invisible web of banks, brands, and software stitched behind it—belongs to Pine Labs. And the quiet truth of modern Indian retail is that an extraordinary share of the country's high-value, in-store purchases of phones, laptops, televisions, and appliances flows across a counter where Pine Labs is sitting in the middle, taking a small clip of every transaction.

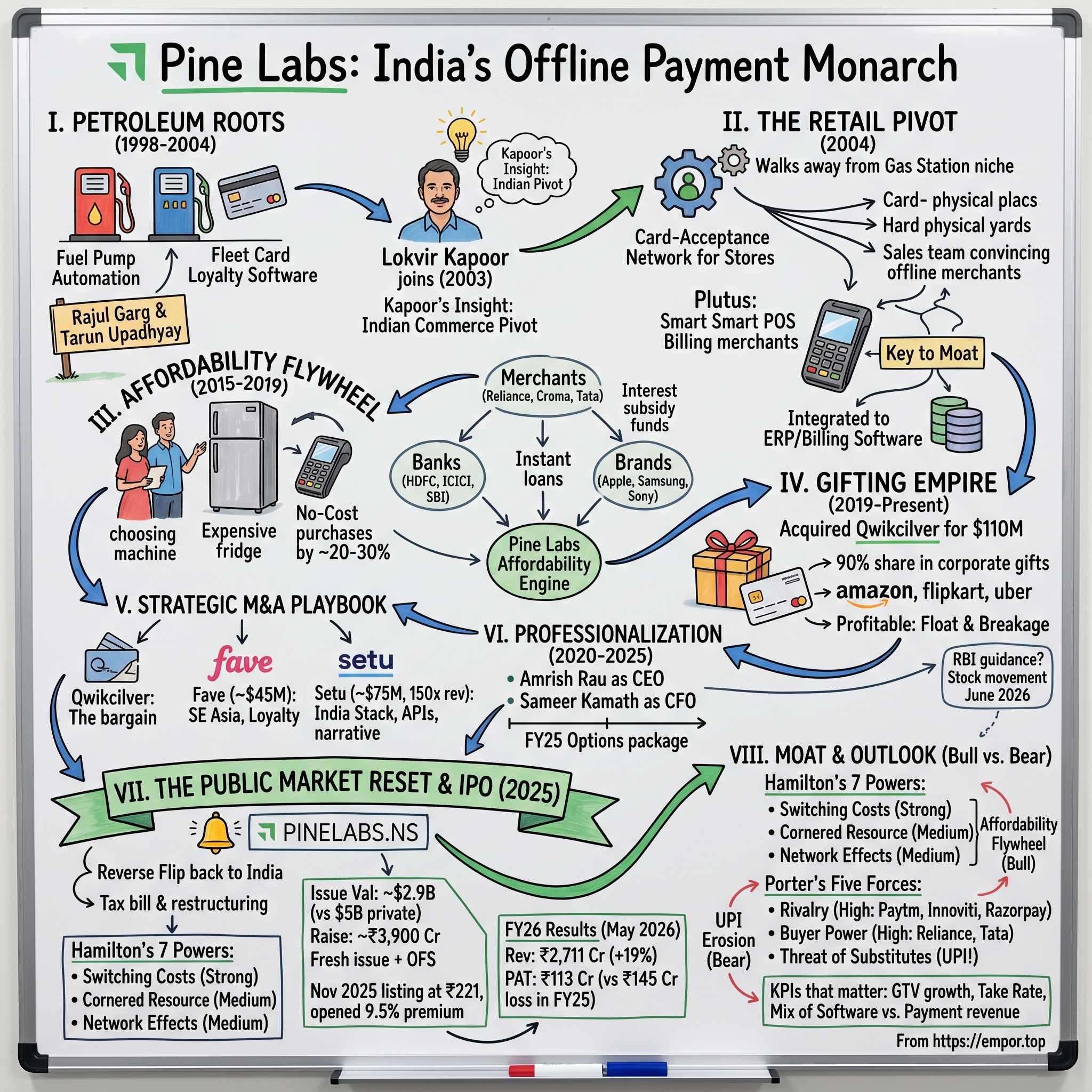

Here is the question that makes Pine Labs such a fascinating case study: how did a company that spent its first six years writing software for gas station fuel pumps and fleet-card loyalty programs become the financial nervous system of organized Indian retail, processing roughly $194 billion in gross transaction value in a single fiscal year?1

The instinct is to file Pine Labs under "Indian fintech" alongside the household names—Paytm, PhonePe, Razorpay. That instinct is wrong, and understanding why is the whole point. Pine Labs is not a consumer app that lives on your phone. It is an infrastructure layer that lives at the merchant's counter and inside the merchant's billing software. It does not chase the street-corner tea seller with a QR code. It hunts the largest enterprise retailers in the country—Reliance, Tata's Croma, Shoppers Stop—and embeds itself so deeply into their checkout operations that pulling Pine Labs out would mean re-architecting how the store rings up a sale.

This is also a story about a valuation reckoning. At the peak of the 2021–22 fintech bubble, Pine Labs carried a private valuation of roughly $5 billion.2 When the company finally went public on Indian exchanges in November 2025, it listed at an issue valuation closer to $2.9 billion—and the share price journey since has been humbling.3 In the gap between those two numbers lives one of the most important lessons in fintech: in private markets you can be valued on a dream, but in public markets, margins and cash flow eventually run the show.

Over the next sections we will trace the full arc. The unglamorous petroleum-software origins. The pivot to card acceptance under a CEO who saw a wave forming before almost anyone else. The "Plutus" platform that turned a cluttered counter into a single smart terminal. The genius of the "No-Cost EMI" affordability machine—the engine that powers the majority of the group's revenue. The hidden, almost embarrassingly profitable gifting empire bought for $110 million. The aggressive, sometimes eyebrow-raising acquisition spree. The professionalization under a celebrity fintech CEO. And finally, the reverse-flip drama and IPO that reset the entire story for public investors. Along the way we will run the business through Hamilton Helmer's 7 Powers and Porter's Five Forces to ask the only question that matters for a long-term owner: is the moat real, and is it durable?

Let's begin where almost nobody expects an Indian fintech story to begin—at a fuel pump.

II. The Petroleum Pivot: From Gas Stations to Retail Counters (1998–2004)

In 1998, India had barely begun its love affair with the credit card. The dot-com boom was inflating Western markets, Indian software services firms like Infosys and Wipro were minting their first fortunes, and the idea of a "fintech" company did not yet have a name. It was in this environment that Pine Labs was founded—not as a payments company, but as something far more prosaic: an automation business for petroleum retailing.

The original founders, Rajul Garg and Tarun Upadhyay, were technologists chasing a real but narrow problem. Fuel retailing in India was a sprawling, cash-heavy, fraud-prone business. Oil marketing companies wanted to digitize fleet cards—the prepaid and credit instruments that trucking companies and corporate fleets used to buy diesel—and to run loyalty programs that could lock in repeat business. Pine Labs built the software and the smart-card systems to make that happen. It was infrastructure work, deeply unglamorous, the kind of plumbing nobody writes magazine profiles about.

For its first several years, that is what Pine Labs was: a competent, low-profile B2B software shop wiring up gas stations. It was a real business, but it was a ceiling, not a launchpad. The total addressable market was capped by the number of fuel pumps and fleet operators in the country, and the margins were the margins of a hardware-and-integration vendor.

The inflection arrived in the person of Lokvir Kapoor, who joined in 2003. Kapoor's gift—and it is the gift that defines the entire first act of this company—was pattern recognition about where Indian commerce was heading. He looked past the fuel pumps and saw a much larger wave forming: the rapid expansion of India's urban middle class, the slow but unmistakable rise of debit and credit card penetration, and the beginnings of organized, branded retail replacing the unorganized bazaar. The same smart-card and terminal technology that read a trucker's fleet card could, with the right software, read a shopper's Visa card at a department store.

In 2004 came what we might call the Great Divorce. Garg and Upadhyay departed the company, and Kapoor took the wheel as the operating leader who would carry Pine Labs for the next decade and a half. With the founders gone, Kapoor made the defining call of his career: he walked Pine Labs away from gas-station automation and pointed it squarely at mainstream retail card acceptance. The company would stop being a niche petroleum vendor and start building a card-acceptance network for stores.

It is worth sitting with how unfashionable this choice was. While the glamour capital of the era was flowing toward internet startups writing elegant code for online audiences, Pine Labs chose the dirty, physical, door-to-door grind: convincing offline merchants to put a clunky dial-up terminal box on their counters, training their cashiers, and servicing the hardware when it broke. There was no viral growth, no app store, no overnight network. There was a sales team walking into shops, one counter at a time.

That decision to do the hard physical yards—to build presence at the point of sale rather than on a screen—planted the seed of everything that followed. Because once you own the counter, and once the merchant depends on the box sitting on it, you control a piece of real estate that no app can replicate: the exact moment, and place, where money changes hands. The next decade would be about transforming that humble box from a dumb card reader into something far more powerful.

III. The Smart Terminal Transition & The Plutus Revolution (2004–2014)

Walk into a mid-2000s Indian department store and look behind the cash register, and you would often see a small graveyard of terminals. One machine to accept Visa and Mastercard through one acquiring bank. Another, separate machine for American Express. Perhaps a third for a different bank's network, because that bank offered the store a better rate on a particular card type. Each terminal was a "dumb" device—a single-purpose card reader hardwired to a single acquiring relationship, with its own dial-up line, its own paper roll, its own reconciliation report at the end of the day.

For a busy enterprise retailer, this was an operational migraine. The terminals clogged precious counter space. Cashiers had to know which box to use for which card. Settlement and reconciliation became a nightly puzzle of matching three or four separate machine reports against the store's own sales ledger. It was slow, error-prone, and it scaled terribly as a chain added stores.

To understand the breakthrough Pine Labs delivered, it helps to demystify what a payment terminal actually does. When you swipe a card, the terminal has to route your transaction to an "acquiring bank"—the merchant's bank, which talks to the card network (Visa, Mastercard, Amex), which talks to your bank, which approves or declines. A dumb terminal can only talk to one acquiring bank. So if a store wanted the flexibility to route different cards through different banks—to get better rates, or to support more card types—it had no choice but to stack up multiple machines.

In 2012, Pine Labs released the answer: Plutus, a cloud-connected, unified multi-merchant point-of-sale platform. The simplest way to describe Plutus is that it turned the single grey box on the counter into a switchboard. One terminal could now accept any card, route the transaction to whichever acquiring bank made sense, and handle multiple networks—all through software, all reconciled in one place, all updated over the cloud rather than by a technician visiting the store. The cluttered terminal graveyard collapsed into a single intelligent device.

This was a genuine technical leap, but the more important strategic decision was about who Pine Labs sold it to. The easy, obvious market in Indian retail was the kirana—the millions of small mom-and-pop neighborhood shops. That is the market Paytm and others would later carpet-bomb with QR codes. Pine Labs deliberately went the other way. It systematically hunted Tier-1 enterprise retail: the organized chains and large-format stores run by the country's biggest corporate houses. Reliance Retail. Shoppers Stop. Tata's Croma. These were the monarchs whose counters processed the highest-value transactions in the country.

Why aim at the giants rather than the masses? Because of what Pine Labs did next, which was the masterstroke. It did not merely drop hardware on the counter and walk away. It integrated Plutus directly into the merchant's ERP and billing software—the core systems that run the store's inventory, pricing, and accounting. When a cashier rang up a sale, the billing system and the payment terminal spoke to each other automatically: the amount flowed straight from the bill to the card machine, and the payment confirmation flowed straight back into the store's books.

That integration is the quiet foundation of Pine Labs' entire moat, and it deserves to be understood plainly. Once your payment system is wired into the guts of how a 500-store chain rings up every single sale and closes its books every single night, you are no longer a vendor that can be swapped out over a weekend. Ripping out Pine Labs would mean re-integrating a new system across hundreds of stores, retraining thousands of cashiers, and risking the one thing a large retailer cannot tolerate: a checkout outage. The cost and risk of switching becomes enormous—and a high switching cost is one of the most durable competitive advantages a business can own.

By 2014, Pine Labs had quietly become the preferred plumbing of organized Indian retail. But a terminal that merely accepts cards, however smart, is still a modest business—you clip a thin fee on each swipe and compete on price. The genius of the next chapter was realizing that the terminal could become something else entirely: not a toll booth on payments, but a salesman for affordability.

IV. The Affordability Flywheel: How No-Cost EMIs Conquered Indian Retail (2015–2019)

To understand the single most important thing Pine Labs ever built, return to that couple at the Croma counter and ask a deceptively simple question: in a country where, even today, only a small minority of adults hold a credit card, how does a retailer sell a ₹1.4 lakh refrigerator to a middle-class family?

The answer that Lokvir Kapoor arrived at around 2015 is the intellectual core of the entire company, and it is worth stating as a principle: in an emerging market, affordability is the ultimate conversion tool. Western retail assumes a deep base of revolving consumer credit—the credit card that lets you carry a balance. India never had that base. What India had instead was a vast, hungry middle class with rising aspirations for premium electronics and appliances, and almost no easy way to spread the cost of a big purchase. Close that gap at the exact moment of decision, and you do not just complete a sale—you upsize it.

So Pine Labs built what is best described as a three-sided affordability engine, an elegant piece of financial choreography that connects three parties who individually could never have pulled this off:

Side one, the merchant counter. At checkout, the Pine Labs terminal can instantly display EMI (equated monthly installment) options—"pay this off over 6, 9, or 12 months." The customer chooses a plan in seconds, right there at the till.

Side two, the banks. Behind that EMI option sits an actual loan. Lenders like HDFC, ICICI, and SBI provide the consumer financing—effectively converting the card swipe into an instant installment loan—without the customer filling out a separate application.

Side three, the brands. Here is the clever bit that turns "EMI" into "No-Cost EMI." Someone has to pay the interest on that loan. In the most popular structure, the brand—Apple, Samsung, Sony—funds the interest subsidy out of its marketing budget, because it would rather discount the financing than discount the sticker price. The customer experiences it as magic: pay over a year, pay nothing extra. The interest didn't vanish; the brand quietly paid it to move more premium units.

Now watch how these three sides lock into a reinforcing loop—the network effect that makes the whole thing so hard to dislodge. The banks want to plug into Pine Labs because Pine Labs sits on the highest-value enterprise checkout counters in India, where the big-ticket loans actually originate. The brands want to fund subsidies through Pine Labs because that is precisely where their premium products get sold and where the affordability nudge converts a browser into a buyer. And the merchants demand Pine Labs terminals because an instant, no-cost EMI offer at the till drives a documented jump of roughly 20–30% in average order value—the couple walks out with the ₹1.4 lakh fridge instead of the ₹70,000 one. Each side makes the platform more valuable to the other two. The more banks and brands plug in, the better the offers; the better the offers, the more merchants want it; the more premium merchants on the network, the more banks and brands must be there.

The economic transformation this triggered for Pine Labs cannot be overstated. A company that sells card terminals is, at heart, a low-margin hardware vendor competing on the price of a box. A company that operates the affordability network is something else entirely. Pine Labs began earning transaction-processing fees on the EMI volume flowing through its rails and layering on software subscription fees for the value-added capabilities riding on the terminal. The grey box on the counter stopped being a cost center the merchant grudgingly paid for and became a productive financial hub that demonstrably grew the merchant's sales—which is exactly the kind of product a customer happily pays a recurring fee to keep.

This affordability engine—the in-store digital payments and merchant commerce business built around it—became the heart of Pine Labs, the largest single contributor to group revenue and the reason enterprise merchants stay locked in. It is also why the company could credibly argue, years later, that it was never really competing in the commoditized swipe-fee business at all. It was in the business of selling more refrigerators.

But a flywheel this good throws off something valuable as a byproduct: enormous, high-frequency visibility into what India's wealthier consumers are buying, where, and how they pay for it. The natural next move was to ask what else could be sold across those same rails. The answer turned out to be gift cards—and it became the most profitable thing Pine Labs ever touched.

V. The Gifting Empire: Qwikcilver & The Issuing Business (2019–Present)

Every great compounding business has a hidden engine—a segment that is less visible than the flagship but quietly does an outsized share of the heavy lifting on profit. For Pine Labs, that engine is gifting and prepaid, and most people who think they know Pine Labs as "the POS terminal company" have never heard of it.

The story starts in 2019, when Pine Labs deployed roughly $110 million to acquire Qwikcilver, the dominant Indian platform for gift cards, prepaid instruments, and stored-value programs.[^4] It was, at the time, a large bet for a company still best known for hardware on counters. With hindsight, it looks like one of the shrewdest acquisitions in Indian fintech history.

To grasp why, you have to understand what Qwikcilver actually does. When you buy an Amazon India gift card, top up a brand wallet, or receive a corporate reward voucher, there is a backend system that issues that card, tracks its balance, manages its redemption, and reconciles the money. Qwikcilver is that backend for a staggering portion of the market—commanding a roughly 90% share of India's corporate gift card and stored-value space, powering loyalty and gifting programs for giants including Amazon India, Flipkart, and Uber. It is infrastructure, again—the same architectural pattern as the POS business, but applied to prepaid value instead of card acceptance.

Now, why is this such a beautiful business? Two words that every investor should commit to memory: breakage and float.

Float is the simpler concept. When a corporation loads ₹100 crore onto gift cards in December for its employees and customers, that money sits in the system before it is spent down over the following months. Whoever holds and manages that balance enjoys the benefit of the cash sitting in the pipes—the float—much like an insurance company invests premiums before claims come due.

Breakage is the more remarkable phenomenon, and it is close to a license to print money. A meaningful percentage of gift cards are simply never redeemed. The ₹2,000 voucher that expires in a drawer. The ₹350 left over on a card nobody bothers to spend down. From an accounting standpoint, the value that was paid for but never claimed becomes income—and because there is no product or service to deliver against it, that income carries close to a 100% margin. It flows almost straight to the bottom line. At scale, across a 90%-share gifting platform, breakage and the associated economics turned Qwikcilver into a profit machine that helped drag the entire consolidated group toward GAAP profitability.

Which sets up the drama of June 2026. On June 15, 2026, a report by the publication Entrackr argued that proposed Reserve Bank of India rules on prepaid payment instruments could strike at gift-card "breakage income" and dent Pine Labs' profitability—and the stock fell as much as 5% before recovering most of the loss.45 Pine Labs responded fast and forcefully, issuing a formal clarification to the stock exchanges the same day, describing the report as "speculative, incorrect and misleading."6

The substance of the company's rebuttal is genuinely important for understanding the risk, so it is worth parsing carefully rather than taking either side at face value. Pine Labs' argument was structural: across its regulated products, it said it predominantly operates through co-branded program structures, under which any breakage from unspent prepaid balances belongs to the partner brand, not to Pine Labs. In other words, when an unredeemed balance sits on a co-branded card, the windfall accrues to the brand whose name is on the card, and Pine Labs earns its money from the platform and processing fees rather than from pocketing the unspent value. The company went further, stating that breakage has never been a material part of its revenue or profit pool, that it has never recognized such income in its P&L, and that even tighter RBI guidance would not meaningfully dent its business.67

For a long-term investor, the honest read is somewhere in the middle. The clarification is reassuring on the specific question of recognized breakage income, and the co-branded structure is a real insulator. But the episode is also a useful reminder that any business touching stored value in India operates under an active, evolving regulator, and that float and prepaid economics will always carry a regulatory overhang that can move the stock on a single news report. Whether breakage is "material" depends partly on definitions, and investors should track the eventual RBI guidance rather than treat the matter as fully closed.

Qwikcilver answered the question of how Pine Labs makes money at high margin. The next question—how it chose to spend the money it raised at peak-bubble valuations—reveals just as much about the company's judgment.

VI. Capital Allocation & The M&A Playbook (Setu, Fave, Qwikcilver)

There is no faster way to judge a management team than to look at how it spends other people's money on acquisitions. Buy cheap assets that compound, and you create enormous value. Overpay for narrative, and you torch it. Pine Labs, flush with capital from its 2021–22 fundraising at a $5 billion valuation, went on an acquisition spree that produced a revealing mix of all three outcomes—the bargain, the opportunistic grab, and the strategically necessary overpayment.

The value play: Qwikcilver ($110 million, 2019). We have already met this deal, so the verdict here is purely about capital allocation: this was cheap and extraordinarily lucrative. Bought before the bubble and before Pine Labs had any reason to overpay, Qwikcilver became the engine of the group's profitability, contributing a substantial slice of revenue—on the order of several hundred crore against the group's ₹2,711 crore FY26 total—at margins the core hardware business could never match.1[^4] If the rest of the M&A book had matched this hit rate, there would be little to debate.

The opportunistic buy: Fave (~$45 million, 2021). In 2021, Pine Labs acquired Fave, a Southeast Asian consumer loyalty, cashback, and QR-payments platform, for around $45 million—notably, in what amounted to a down-round, at a steep discount to Fave's peak private valuation.8 The verdict is "well-timed bargain hunting." Fave gave Pine Labs two things it wanted: a ready-made consumer loyalty and cashback layer to bolt onto its merchant relationships, and an instant foothold in Southeast Asia, particularly Malaysia and Singapore. That international beachhead matters more in 2026 than it did in 2021: Pine Labs' overseas revenue crossed ₹400 crore in FY26 as the company expanded its presence across roughly 22 countries, giving it a genuine, if still minority, international revenue stream.1 Buying a struggling asset in a downturn at 40-cents-on-the-dollar is precisely the kind of counter-cyclical move that creates value if you can integrate it—and the jury is still partly out on how much consumer-facing loyalty truly fits a B2B infrastructure company's DNA.

The strategically essential overpayment: Setu (~$75 million, 2022). This is the deal that makes financial analysts wince and strategists nod. In 2022, Pine Labs acquired Setu, an India Stack and open-banking API company, for a reported $70–75 million.[^10] The wince comes from the multiple. Setu was a tiny, early-stage business—generating only around $442,000 in revenue in FY21—which means Pine Labs paid something on the order of 150 times revenue.[^10] On any conventional yardstick, that is an absurd price.

So why do it? The answer is about narrative and positioning rather than near-term revenue, and it is a more sophisticated piece of strategy than the raw multiple suggests. Setu provided the building blocks of "India Stack"—the country's open digital financial infrastructure, including the Account Aggregator framework (which lets consumers securely share their financial data with their consent), OCEN (an open credit protocol), and a layer of modern financial APIs. To translate the jargon: India Stack is the set of government-backed digital rails that let any company plug into identity, payments, and consented data-sharing the way an electrician plugs into a wall socket. Owning a credible India Stack player let Pine Labs reframe itself for the public markets it was preparing to enter—from a "terminal hardware business," which carries low multiples, to an "API-first financial platform," which the market rewards more richly.

Was that reframing worth $75 million for a company doing less than half a million in revenue? A skeptic would call it buying a story. A defender would point out that the IPO narrative, the analyst framing, and the platform optionality Setu unlocked may well have added more than $75 million to how the public market eventually valued the whole enterprise. Both can be true. What the Setu deal reveals about Pine Labs' leadership is a willingness to spend aggressively on strategic positioning—a trait that, depending on the outcome, looks either visionary or undisciplined. Which brings us to the people who were steering all of this.

VII. The Professionalization: Amrish Rau & The Multi-Channel Pivot (2020–2025)

Founders build companies; professional operators institutionalize them. The transition between those two phases is one of the most delicate in any company's life, and Pine Labs navigated it in 2020 with a move that signaled real ambition.

Lokvir Kapoor—the man who had pivoted the company off the fuel pumps and onto the retail counter, and who had been the operating soul of Pine Labs for over fifteen years—stepped back from the CEO role to become Executive Chairman. In his place arrived B. Amrish Rau, and the choice told you exactly where Pine Labs wanted to go. Rau was fintech royalty in India. He had co-founded Citrus Pay, one of the country's early payment gateways, and had run PayU's India business—someone with a track record of building payment companies to institutional scale and, crucially, of getting them to outcomes. Recruiting Rau was a statement that Pine Labs intended to become a public-market-grade institution, not a founder-run shop.

The shareholding structure that emerged around this leadership reveals how carefully incentives were aligned with public-market performance. Rau holds an equity stake of roughly 2.35%—on the order of 17–18 million shares—and ahead of the IPO he was granted a substantial pre-IPO options package, reported at around 1.1 crore options, that anchored the bulk of his potential wealth to where the stock trades after listing rather than to a comfortable salary.[^11] His cash-and-equity compensation for FY25 was reported in the ₹9–10 crore range.[^11] The design is deliberate: by loading the upside into options that only pay if the public stock performs, the company tied its CEO's net worth to the same outcome its IPO investors care about. Kapoor, for his part, remained Executive Chairman with a stake of roughly 2.45%, keeping the founder-operator's voice and skin in the game even as day-to-day control passed to Rau.

The final piece of the professionalization puzzle clicked into place in August 2025, when Pine Labs recruited Sameer Kamath as Group CFO from Avendus Capital, one of India's most respected financial-advisory houses—a hire made pointedly ahead of the IPO.[^12] Bringing in a heavyweight CFO from the investment-banking world just before going public is a classic and deliberate move: you want a financial steward who can speak the language of institutional investors, tighten the numbers, and tell a clean profitability story. Under this finance leadership, the company completed the journey from a history of losses to a clean, GAAP-profitable ₹113 crore profit after tax in FY26—the kind of before-and-after that makes or breaks an IPO narrative.1

While the leadership was being upgraded, so was the product surface. In 2021, Pine Labs launched Plural, its online payment gateway—a direct push into the digital, card-not-present world where online-native champions like Razorpay already reigned. The logic was sound: Pine Labs owned the physical checkout; why not follow its enterprise merchants online and offer one provider across both the store and the website (the "omnichannel" pitch)? In practice, Plural remains a small piece of the pie—well under 5% of revenue—and it would be a mistake to oversell it. But it is strategically valuable optionality. It hedges the company against a future where commerce keeps migrating online, and it lets Pine Labs tell its largest customers a unified story. Whether Plural ever becomes a serious challenger to the online incumbents is an open question; for now it is a foothold, not a flag planted on conquered territory.

With a marquee CEO, a banker's CFO, an aligned cap table, and a multi-channel product, Pine Labs had assembled the apparatus of a public company. The deeper question for an investor is whether the underlying business has the kind of structural advantages that survive contact with fierce competition. For that, we turn to the frameworks.

VIII. Playbook: Hamilton's Powers & Porter's Forces

Strip away the narrative and the question for a long-term owner is cold and structural: what, exactly, stops a well-funded competitor from taking Pine Labs' business? Two frameworks help answer it—Hamilton Helmer's 7 Powers for the durability of the advantage, and Porter's Five Forces for the intensity of the competition.

Hamilton's 7 Powers, applied to Pine Labs.

The strongest power in the portfolio is switching costs, and we have already seen its mechanism: by integrating Plutus into enterprise merchants' ERP and cashier-billing systems, Pine Labs makes itself painful and risky to remove. A 500-store chain does not casually re-plumb its checkout. This is the bedrock of the moat, and it is genuinely strong—but it applies mainly to the large enterprise base, not to smaller merchants who can swap a standalone terminal more easily.

The second power is a cornered resource: the web of exclusive, multi-year commercial integrations with banks and brands that powers the affordability engine. Wiring up dozens of major banks and a long roster of consumer brands into a single, working no-cost-EMI network—with all the commercial negotiation, technical integration, and reconciliation that implies—is not something a newcomer can clone in a quarter. The relationships and the plumbing are the asset, and they took years to assemble. This is a strong, if not impregnable, advantage; relationships can in principle be reproduced by a determined, well-capitalized rival over time.

The third power is network effects, of the medium-to-strong variety—the three-sided merchant–bank–brand loop described earlier. It is a real flywheel, but it is worth being honest that it is not a winner-take-all consumer network like a social app; a large rival with its own enterprise base can sustain a competing loop.

The fourth, and most interesting, is counter-positioning—and here it is largely a past power that explains how Pine Labs got where it is. While Paytm, PhonePe, and BharatPe poured capital into micro-merchant QR codes and consumer cashbacks, chasing scale and ubiquity at razor-thin or negative margins, Pine Labs deliberately stayed in high-margin, enterprise, offline B2B commerce. The incumbents-of-the-moment could not easily follow without cannibalizing their own consumer-growth strategies. That counter-position is less of a live weapon today, now that everyone covets enterprise margins, but it shaped the durable base Pine Labs now defends.

What Pine Labs largely lacks is scale economies of the runaway kind, branding power with end consumers (most shoppers never know it's there), and process power. The moat is real, but it rests on switching costs and cornered relationships—not on an unassailable monopoly.

Porter's Five Forces.

The force that should worry an investor most is rivalry among existing competitors, which is very high and intensifying. Paytm dominates the micro-merchant world it counter-positioned against, with a vast installed base of QR codes and card-reader "soundboxes" numbering in the millions of active devices—a different segment today, but a well-capitalized neighbor that could push upmarket. Innoviti is the most direct enterprise rival, a specialist that has held a commanding share of payments at large organized-retail brands and competes head-on for exactly the Tier-1 accounts Pine Labs prizes. Razorpay, having absorbed Ezetap, brings genuine omnichannel power and a large fleet of POS terminals to bear, threatening to offer the unified online-plus-offline story Pine Labs wants to own. And BharatPe, through its all-in-one BharatPe One device, is pressing the mid-tier SMB market with aggressive pricing. The competitive set spans from below (SMB players moving up) and beside (enterprise specialists) and across (omnichannel platforms)—a genuinely crowded battlefield.

The second force that bites is the bargaining power of buyers, which is high precisely because Pine Labs chose to serve giants. A Reliance or a Tata can squeeze the merchant discount rate—the fee a merchant pays on card transactions—down to wafer-thin levels, because they bring enormous volume and can credibly threaten to take it elsewhere. This is the flip side of the enterprise strategy: the customers are sticky, but they are also powerful, and they use that power on price. Pine Labs' answer has been to migrate its monetization away from the squeezable swipe fee and toward software subscriptions and value-added credit services—revenue streams the customer is less able and less inclined to negotiate to zero, because they are tied to capabilities (affordability, analytics, gifting) that actively grow the merchant's sales.

The remaining forces are milder. The threat of new entrants at the enterprise tier is dampened by the very switching costs and cornered relationships described above—it is hard to start a no-cost-EMI network from scratch. Supplier power (banks, networks, hardware makers) is moderate. And the threat of substitutes is the one we will dwell on in the bear case, because it has a name: UPI.

The picture, then, is of a company with a real and defensible core, operating in a market with brutal rivalry and powerful customers. That tension is exactly what the public markets had to price when Pine Labs finally listed.

IX. The Public Market Reset: Domicile Flip & The November 2025 IPO (2025–Today)

Before Pine Labs could ring the bell on an Indian exchange, it had to perform an expensive piece of corporate surgery on itself. Like many Indian startups that had raised global capital in the 2010s, Pine Labs had domiciled its parent entity in Singapore—a sensible structure for attracting international investors, but a problem if you want to list on Indian exchanges under SEBI's rules. So the company executed a "reverse flip," moving its parent back to India.

This is not a paperwork formality. A reverse flip typically triggers a significant tax bill and forces a restructuring of the capitalization table, as a foreign holding structure is collapsed back into an Indian one. It was painful and costly—but for a company that wanted access to India's deep domestic investor base and a listing close to its customers and operations, it was the necessary price of admission. That so many Indian fintechs undertook the same migration around this period tells you how strongly the gravity of the Indian public market was pulling.

The debut itself came in November 2025. Pine Labs listed on both the NSE and the BSE under the ticker PINELABS, with the IPO bidding running November 7–11, 2025.3 The pricing tells the story of the era's reset. The company set a price band of ₹210–₹221 per share and priced at the top, raising roughly ₹3,900 crore—split between a fresh issue of about ₹2,080 crore (new money for the company) and an offer for sale of about ₹1,820 crore (existing investors cashing out).93 At the issue price, the public market valued Pine Labs at roughly $2.9 billion.[^14]

Hold that number against the $5 billion private valuation from 2022, and you see the defining feature of this listing: a haircut of more than 40% from the private peak.[^14] This was the post-bubble adjustment made visible. The company and its bankers chose to price for a successful debut rather than to extract the last rupee of bubble-era valuation—and indeed the stock opened at around ₹242 on listing day, a premium of roughly 9.5% over the issue price, valuing the company on debut north of $3.5 billion as it traded up.1011 In effect, money was deliberately left on the table, some of which accrued to the retail and institutional investors who got the allocation.

What the market was buying, by mid-2026, was a business that had finally answered the profitability question. The FY26 numbers, reported in May 2026, marked a genuine turning point: consolidated revenue of ₹2,711 crore, up about 19% from ₹2,274 crore the prior year, and—critically—a swing to a net profit of ₹113 crore, against a loss of ₹145 crore in FY25.1 EBITDA margins expanded from roughly 16% to 21%, operating cash flow rose sharply, and the company ended the year with a substantial net-cash position of around ₹2,449 crore on the balance sheet.112 Underneath the profit line, the operating engine kept growing: gross transaction value of roughly $194 billion (up about 50%), with UPI volumes processed on its platform surging 68%.1 The fourth quarter alone delivered around ₹701 crore of revenue and ₹59 crore of profit, the third straight profitable quarter.13

That profitability mattered because it silenced a specific and widespread skepticism: the belief that a payments processor simply could not earn a clean profit in India's zero-MDR UPI environment, where the most popular payment method generates no merchant fee at all. Pine Labs demonstrated that by monetizing software, affordability, and gifting rather than relying on swipe fees, the model could work.

And yet the share price has been a humbler teacher than the income statement. After the listing-day pop, the stock proved volatile and drifted well below its issue price over the following months, trading at levels that put it, by valuation, much closer to a stable financial utility than a high-growth tech name—on a sales multiple that long-term value-oriented investors found far more palatable than anything available during the bubble.14 The gap between a strong operating year and a soft stock is the recurring drama of post-bubble fintech, and it sets up the final question: bull or bear?

X. Conclusion & Investment Outlook (Bull vs. Bear Case)

Every business this contested deserves to have its strongest advocate and its harshest critic given the floor. Here is each.

The bull case. Pine Labs has done the single hardest thing an Indian fintech can do—it has crossed the profitability chasm, turning a ₹145 crore loss into a ₹113 crore profit in one year while still growing revenue at roughly 19%.1 That is not a one-quarter accounting flourish; it is multiple consecutive profitable quarters and a fundamentally re-based cost structure. The affordability engine remains deeply sticky and structurally aligned with the most powerful tailwind in the Indian economy: the secular expansion of consumer credit appetite. As more Indians want to finance more premium purchases, the volume flowing across Pine Labs' three-sided network should compound, and Pine Labs earns on that volume without taking the credit risk itself. Qwikcilver continues to dominate corporate gifting at margins the rest of the business can only envy, throwing off recurring, software-like economics. And after the valuation reset, the company trades with a meaningful buffer—shorn of its tech-bubble premium and priced more like a financial utility than a moonshot, which is a far more comfortable place from which to compound. The balance sheet, with its large net-cash position, gives management room to invest or acquire without distress.12

The bear case. The most serious threat is structural and it has a name: UPI. India's instant, free, bank-to-bank transfer system has already swallowed an enormous share of everyday payments, and the worry is that as UPI moves up the value chain—into the larger transactions that have historically run on cards—it erodes the economic rationale for the physical card POS terminal that anchors Pine Labs' merchant relationships. If the high-value swipe migrates to a free rail, the toll booth shrinks. Second is the enterprise margin squeeze we examined under Porter: Pine Labs' best customers are also its most powerful, and conglomerates like Reliance and Tata will keep compressing merchant fees, forcing the company to run ever faster on software and credit monetization just to stand still. Third is the competitive onslaught from every direction at once—Razorpay's omnichannel push, BharatPe's aggressive devices, and Innoviti's entrenched defense of the very enterprise-retail strongholds Pine Labs depends on. Add the regulatory overhang around prepaid and breakage economics, and the bear sees a good business being slowly ground between free rails, powerful buyers, and relentless rivals.

The KPIs that actually matter. Cut through the noise and a long-term owner should track a short list. First and most important, gross transaction value (GTV) growth alongside the take rate—the GTV tells you whether the platform is gaining or losing volume share, and the realized monetization per rupee of GTV tells you whether the buyers' bargaining power is winning the margin war. Watching one without the other is a trap; rising GTV at a collapsing take rate is a warning, not a victory. Second, the mix and growth of software-and-platform revenue versus pure payment processing—because the entire bull thesis rests on Pine Labs being a high-margin platform, not a low-margin terminal vendor, and that mix is the truth serum. A distant third worth a glance is the gifting/prepaid contribution and any movement in its regulatory treatment, given how much of group profit it quietly carries.

The Acquired verdict, in the spirit of the show, is not a price target or a grade—it is a characterization. Pine Labs is the ultimate blue-chip survivor of India's first-generation fintech bubble. While a generation of competitors wrote elegant code and burned capital chasing consumers on screens, Pine Labs spent two decades doing the unglamorous physical work of owning the counter, wiring itself into the merchant's books, and assembling a network of banks and brands that is genuinely hard to replicate. Whether that translates into a great stock from here depends on how the UPI substitution and margin-squeeze questions resolve—questions the public market is still actively pricing, one volatile quarter at a time. What is no longer in doubt is that the business underneath is real.

XI. Outro & Links

For readers who want to go to the primary record rather than take any narrator's word for it, the indispensable documents are Pine Labs' own SEBI IPO prospectus and the FY26 results disclosures, which contain the segment economics, the breakage and co-branding language, and the risk factors in the company's own words. The contemporaneous coverage of the November 2025 listing, the May 2026 turnaround results, and the June 2026 breakage clarification—cited throughout—together capture the moment this company stopped being a private story and became a public one. Read the prospectus risk factors first; they are blunter than any podcast.

References

-

Pine Labs posts ₹701 crore Q4 FY26 revenue with ₹59 crore net profit, annual revenue reaches ₹2,711 crore — The Tech Portal, 2026-05-25 ↩↩↩↩↩↩↩↩

-

Indian fintech firm Pine Labs eyes $2.9 billion valuation in reduced IPO — Reuters via TradingView, 2025-11 ↩

-

Pine Labs IPO opens November 7, sets price band at ₹210–221 — Business Standard, 2025-11-03 ↩↩↩

-

Inside Pine Labs' profit story: The gift card income stream set to take a hit — Entrackr, 2026-06-15 ↩

-

Why Pine Labs shares fell 5% before paring most of the losses — Business Today, 2026-06-16 ↩

-

Pine Labs dismisses Entrackr report as 'speculative, incorrect and misleading'; says gift card income concerns unfounded — Business Upturn, 2026-06-15 ↩↩

-

Pine Labs says media reports on breakage income are incorrect and misleading — Reuters via TradingView, 2026-06-15 ↩

-

Pine Labs IPO trimmed as investors decide to sell less at price band: CEO — Business Standard, 2025-11-03 ↩

-

Pine Labs jumps on market debut — Business Standard, 2025-11-14 ↩

-

Indian fintech firm Pine Labs lists at 9.5% premium in early trading — Reuters via MarketScreener, 2025-11-14 ↩

-

Pine Labs FY26: Revenue ₹2,711 Cr, PAT ₹113 Cr, Net Cash ₹2,449 Cr — Whalesbook, 2026-05 ↩↩

-

Pine Labs clocks PAT of Rs 59 crore in Q4 FY26 — Business Standard, 2026-05-26 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube