Procter & Gamble Hygiene and Health Care: India's FMCG Healthcare Giant

I. Introduction & Episode Context

Picture this: It's 1985, and in a modest office in Mumbai, executives from Richardson Hindustan Limited are meeting with representatives from Cincinnati-based Procter & Gamble. The American consumer goods giant is about to make a move that will reshape India's feminine hygiene and healthcare markets forever. What starts as a straightforward acquisition of a local healthcare company will evolve into one of India's most profitable consumer franchises—a business that today commands a staggering 79.7% return on equity and generates over ₹4,300 crores in annual revenue.

This is the story of Procter & Gamble Hygiene and Health Care Limited (PGHH), a company that transformed from a local pharmaceutical player into India's undisputed leader in feminine hygiene with Whisper, while building Vicks into a cultural phenomenon that transcends mere brand status. With a market capitalization of ₹43,202 crores, PGHH stands as a testament to the power of global expertise meeting local understanding.

The central question we're exploring isn't just how P&G built this empire—it's how a foreign multinational created categories that didn't exist, changed social taboos around feminine hygiene, and convinced price-conscious Indian consumers to pay premium prices for branded healthcare products. This is a masterclass in market creation, brand building, and the delicate dance between global standardization and local adaptation.

What makes PGHH particularly fascinating for investors is its paradoxical nature: a company with monopolistic market positions trading at 52 times earnings, yet struggling with single-digit revenue growth. A business that pays out 100% of its profits as dividends, yet maintains fortress-like competitive moats. A subsidiary that operates with near-complete autonomy, yet benefits from the full weight of P&G's global R&D and marketing prowess.

As we dive into this seven-hour journey through PGHH's evolution, we'll uncover the strategic decisions that built categories worth thousands of crores, the marketing campaigns that became part of Indian popular culture, and the operational excellence that delivers some of the highest margins in the FMCG sector. We'll also grapple with the uncomfortable questions: Why has growth stalled in recent years? Can premium brands continue to thrive as digital-first competitors emerge? And most critically—at current valuations, does PGHH represent a quality compounder or an expensive legacy player?

The story ahead takes us from the License Raj era of the 1960s through economic liberalization, from creating markets that didn't exist to defending them against nimble startups. It's a narrative that illuminates not just one company's journey, but the entire evolution of Indian consumer behavior and the FMCG industry's transformation over six decades.

II. Origins & The Richardson Hindustan Story (1964-1985)

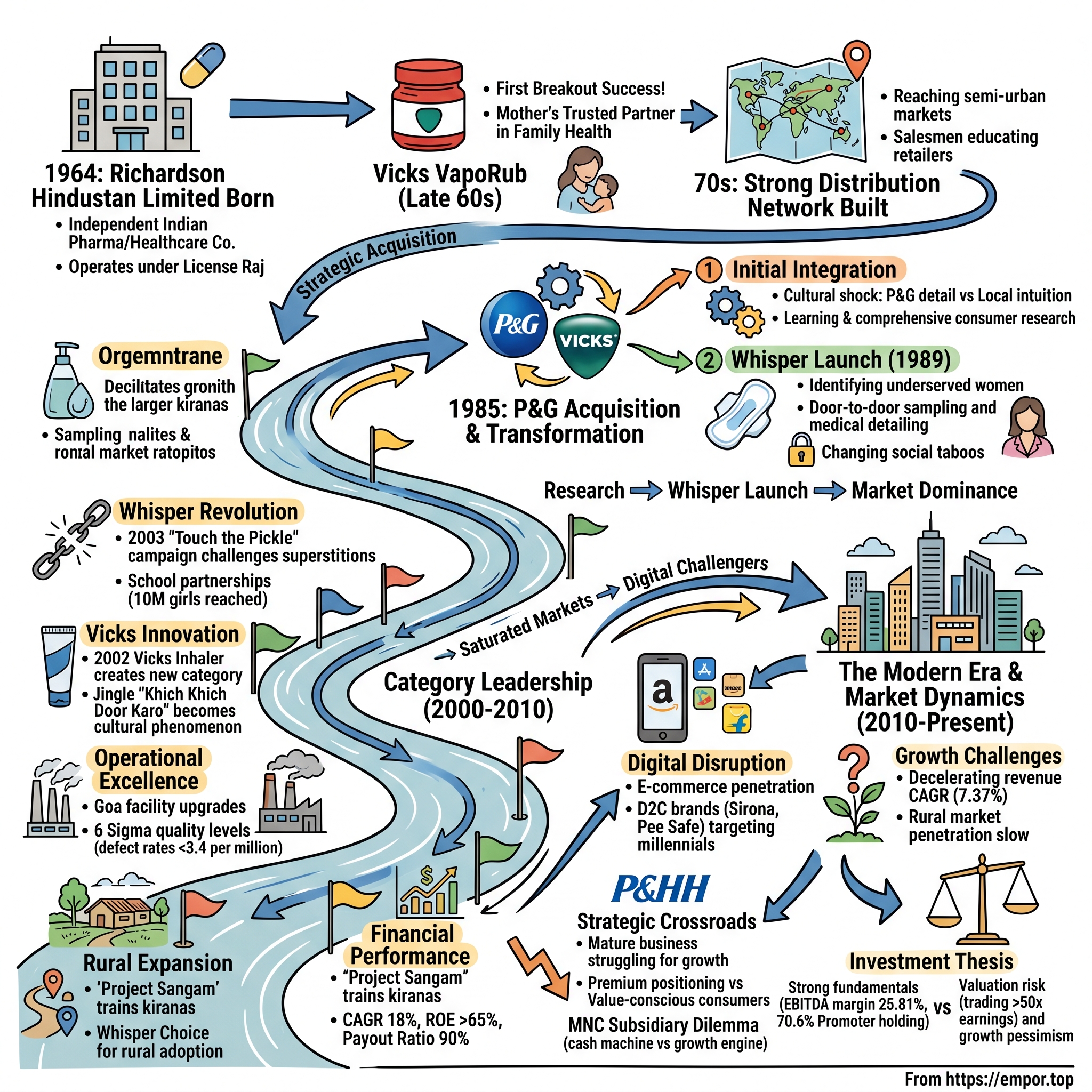

The year is 1964. Jawaharlal Nehru has just passed away, leaving India at a crossroads. The economy operates under the suffocating grip of the License Raj—a byzantine system where producing even a single extra unit beyond government-approved capacity could land industrialists in legal trouble. Into this controlled chaos, Richardson Hindustan Limited is born, not as a subsidiary of any multinational, but as an independent Indian pharmaceutical and consumer healthcare company.

Richardson Hindustan's founders understood something fundamental about post-independence India: while the government focused on heavy industries and import substitution, millions of Indians suffered from basic health ailments with limited access to quality medicines. The company began manufacturing over-the-counter healthcare products, leveraging partnerships with Richardson-Vicks Inc. of the United States for technology and formulations. This wasn't unusual—foreign collaboration was one of the few ways Indian companies could access advanced manufacturing know-how during the License Raj.

The early product portfolio was decidedly unglamorous but essential: cough syrups, cold remedies, and basic healthcare products. Vicks VapoRub, introduced in the late 1960s, became the company's first breakout success. In Indian households where doctor visits were expensive and often impractical, a jar of VapoRub represented accessible healthcare. Mothers would rub it on children's chests during cold winter nights, creating an emotional connection that transcended mere product functionality.

By the 1970s, Richardson Hindustan had built something remarkable: a distribution network that reached not just metros and tier-1 cities, but also semi-urban markets where multinational competitors feared to tread. The company's salesmen, traveling by buses and trains with product samples in worn leather bags, became familiar faces to chemists and general store owners across North India. They weren't just selling products; they were educating retailers about profit margins, inventory management, and the emerging concept of "brand pull" versus "push."

The company's manufacturing facility in Goa, established in the mid-1970s, represented a significant bet on local production. While other multinationals relied heavily on imports (paying hefty duties), Richardson Hindustan invested in indigenous manufacturing capabilities. This decision would prove prescient when P&G came calling a decade later—they weren't buying just brands, but an entire operational infrastructure adapted to Indian conditions.

What truly set Richardson Hindustan apart was its early recognition of Indian consumer psychology. While competitors pushed "modern" Western messaging, Richardson Hindustan's advertisements featured Indian families, spoke in vernacular languages, and acknowledged traditional health practices while positioning their products as complementary, not replacement, solutions. A 1979 Vicks campaign featuring a grandmother using VapoRub alongside traditional kadha (herbal decoction) captured this duality perfectly.

The financial performance during this period, while modest by today's standards, was impressive for its consistency. Despite price controls on pharmaceutical products and limited pricing power, Richardson Hindustan maintained steady profitability through operational efficiency and volume growth. By 1984, the company had revenues of approximately ₹25 crores—substantial for an Indian FMCG player of that era.

Behind the scenes, however, Richardson-Vicks Inc. in the United States was undergoing its own transformation. The American parent, facing competitive pressures in developed markets, began evaluating its international operations more strategically. India, with its massive population and emerging middle class, represented not just a market but a long-term growth engine. But Richardson-Vicks lacked the resources and global scale to fully capitalize on this opportunity.

Enter Procter & Gamble. By the early 1980s, P&G had identified geographic expansion as critical to its growth strategy. The company had watched rivals like Unilever build dominant positions in emerging markets and recognized the first-mover advantages in categories still being formed. P&G's scouts, visiting Richardson Hindustan's operations in 1984, saw something beyond the modest revenues: a company that had cracked the code of selling branded consumer goods in one of the world's most complex markets.

The acquisition negotiations, conducted in secrecy through 1985, reflected the delicate balance both parties needed to strike. For Richardson Hindustan's Indian management, the concern was whether P&G would maintain local autonomy or impose American-style standardization that might alienate Indian consumers. For P&G, the question was whether this relatively small acquisition could serve as a beachhead for their broader Asian ambitions. As we moved toward the historic acquisition, the stage was set for a transformation that would redefine entire categories in the Indian FMCG landscape.

III. The P&G Acquisition & Transformation (1985-2000)

The conference room at the Taj Mahal Hotel in Mumbai had seen many business deals, but on that humid August morning in 1985, something unprecedented was unfolding. P&G's global president was personally present—unusual for an acquisition of this size—signaling the strategic importance of the Richardson Hindustan deal. The purchase price, while not publicly disclosed at the time, was reported to be around $20 million, modest even by 1985 standards. But P&G wasn't buying Richardson Hindustan for its current revenues; they were acquiring a gateway to 750 million Indian consumers.

The integration began with a cultural shock that nobody fully anticipated. P&G's legendary attention to detail—memos about memos, extensive consumer research for the smallest product changes, and rigorous testing protocols—collided with Richardson Hindustan's more intuitive, relationship-driven approach. Early integration meetings became legendary for their length; what Indian managers could decide in minutes of corridor conversation required hours of PowerPoint presentations in P&G's world.

Yet P&G's first strategic masterstroke wasn't about imposing their culture—it was about learning. Instead of immediately flooding the market with global brands, P&G spent the first two years conducting the most comprehensive consumer research ever undertaken in India's FMCG sector. Teams of researchers, both American and Indian, lived with middle-class families for weeks, observing how they used healthcare products, understanding family dynamics around purchase decisions, and documenting attitudes toward health and hygiene.

One research insight would reshape P&G's entire India strategy: the discovery that Indian mothers were the chief health officers of their families, making over 80% of healthcare product decisions but feeling underserved by existing options. This led to the radical repositioning of Vicks from a general cold remedy to a mother's trusted partner in family health. The famous "Touch of care" campaign, launched in 1987, featured real Indian mothers and positioned Vicks VapoRub not just as a product but as an extension of maternal care.

The real revolution, however, came with Whisper's launch in 1989. P&G identified that less than 10% of Indian women used sanitary napkins, with the majority relying on cloth or other alternatives. The taboo around menstruation was so strong that even discussing the product category was challenging. P&G's approach was methodical and sensitive: they started with medical detailing, sending women representatives to educate doctors and nurses who would then recommend the product to patients.

The Whisper launch team, led by a young brand manager named Shantanu Khosla (who would later become P&G's India head), pioneered distribution innovations that seemed radical at the time. Recognizing that women were embarrassed to buy sanitary napkins from male shopkeepers, P&G created special packaging that looked like general merchandise from the outside. They also initiated India's first door-to-door sampling program for sanitary napkins, employing thousands of women educators who would conduct private sessions with potential consumers.

Manufacturing localization became P&G's next frontier. The company invested over ₹100 crores between 1990 and 1995 to upgrade the Goa facility and establish new production lines. This wasn't just about cost reduction—local manufacturing allowed P&G to adapt products for Indian conditions. Whisper pads were redesigned to be thinner (for the Indian climate) but with higher absorption capacity (addressing concerns about changing frequently in public spaces with limited facilities).

The 1991 economic liberalization transformed P&G's strategic options overnight. Suddenly, the company could import raw materials more easily, expand production without government licenses, and invest in advertising without restrictions. P&G responded by tripling its marketing budget within two years, launching television campaigns that would become cultural touchstones. The "Vicks ki goli lo, khich khich door karo" jingle, created in 1993, became so ubiquitous that it entered everyday Hindi vocabulary.

Distribution expansion accelerated through the 1990s, with P&G pioneering the concept of "stockist-distributor-retailer" networks that could reach India's fragmented retail landscape. By 1995, PGHH products were available in over 3 million outlets, a tenfold increase from the acquisition date. The company's sales force, expanded from 200 to 2,000 representatives, became known for their technical knowledge and professional approach, setting new standards in the industry.

Financial performance during this period validated P&G's strategy. Revenues grew from ₹30 crores in 1985 to over ₹400 crores by 2000—a compound annual growth rate exceeding 18%. More impressively, operating margins expanded from 8% to over 15%, demonstrating that premium pricing and brand building could work in India's price-conscious market. The Whisper brand alone, virtually non-existent in 1989, was generating over ₹150 crores in annual sales by the decade's end.

Competition intensified as PGHH's success attracted rivals. Johnson & Johnson launched Stayfree, Hindustan Unilever introduced Kotex, and numerous local players emerged with lower-priced alternatives. P&G's response was to accelerate innovation: introducing Whisper Ultra in 1998 (India's first ultra-thin pad), launching Vicks Action 500 for severe colds, and constantly improving product formulations based on consumer feedback.

The organizational transformation was equally remarkable. By 2000, PGHH had evolved from a traditional Indian company to a hybrid organization combining P&G's global best practices with deep local insights. Indian managers were rotating through P&G's global operations, bringing back expertise while contributing their emerging market knowledge to P&G's worldwide strategy. As the new millennium approached, PGHH stood ready to leverage its transformed capabilities to dominate the categories it had essentially created.

IV. Building Category Leadership (2000-2010)

The new millennium opened with a scene that would have been unimaginable just a decade earlier: in a packed auditorium in Chennai, over 500 women openly discussed menstrual health with PGHH's education team. The taboo that had silenced generations was finally breaking, and P&G wasn't just witnessing this transformation—they were architecting it. This was the decade when PGHH would move from being a successful player to an almost monopolistic force in its core categories.

The Whisper revolution reached its crescendo in 2003 with the launch of the "Touch the Pickle" campaign. For context, orthodox Hindu traditions prohibited menstruating women from entering kitchens or touching pickle jars, believing they would spoil. P&G's campaign, featuring confident young women challenging these superstitions, sparked nationwide debates. Conservative groups protested, burning Whisper products outside P&G offices. But something remarkable happened—young women rallied behind the brand, seeing it as a symbol of progress. Sales jumped 40% in the campaign's first year.

P&G's masterstroke wasn't just in challenging taboos but in making the conversation mainstream. They partnered with over 10,000 schools by 2005, implementing menstrual health education programs that reached 10 million adolescent girls. These weren't sales pitches but genuine health education initiatives, with P&G providing free educational materials and training teachers. The long-term brand loyalty this created was incalculable—entire generations of Indian women associated their first understanding of menstrual health with Whisper.

The rural expansion strategy, launched in 2004, demonstrated P&G's commitment to market creation over simple market share battles. Recognizing that 70% of Indian women lived in rural areas with virtually no access to sanitary napkins, P&G created Whisper Choice, a lower-priced variant specifically designed for price-sensitive consumers. But instead of just competing on price, they invested in education. PGHH's rural activation teams, comprising over 5,000 women educators by 2007, conducted village-level awareness programs, often partnering with local health workers and panchayat leaders.

Meanwhile, Vicks was undergoing its own transformation from cold remedy to comprehensive health platform. The 2002 launch of Vicks Inhaler created an entirely new category in India. P&G noticed that Indians often used steam inhalation for cold relief but found the process cumbersome. The pocket-sized inhaler, priced at just ₹25, became an instant hit, selling 50 million units in its first three years. By 2008, it wasn't uncommon to see office workers, students, and drivers keeping Vicks Inhalers as everyday carry items.

The "Khich Khich Door Karo" campaign evolved into a cultural phenomenon that transcended advertising. P&G commissioned Bollywood music directors to create multiple versions of the jingle in different languages and musical styles. Radio stations played these as regular songs, not advertisements. The phrase entered common parlance—politicians used it in speeches, comedians in their routines. Marketing textbooks would later cite this as one of the most successful examples of advertising becoming culture.

Distribution innovation reached new heights with Project Sangam, launched in 2006. P&G recognized that India's 12 million kiranas (small shops) were not just points of sale but community influencers. The project trained 100,000 shopkeepers on category management, providing them with display units, inventory management tools, and education about profit optimization. These shopkeepers became brand ambassadors, recommending PGHH products based on genuine belief in their superior margins and faster inventory turns.

The competitive landscape during this period resembled a war of attrition where PGHH consistently won through superior execution. When Johnson & Johnson's Stayfree launched aggressive price promotions in 2005, P&G responded not with price cuts but with product innovation—introducing Whisper Ultra Nights, addressing the specific concern of overnight protection. When local brands like Kotex tried to undercut on price, P&G launched consumer education campaigns highlighting the health risks of low-quality products. Market share data tells the story: Whisper's share grew from 48% in 2000 to 74% by 2010.

Manufacturing excellence became a strategic differentiator. The Goa facility, upgraded with ₹200 crores of investment between 2000-2010, became P&G's global center of excellence for feminine hygiene products. The plant achieved Six Sigma quality levels, with defect rates below 3.4 per million—critical in a category where product failure had serious personal consequences. This quality consistency allowed P&G to command premium prices; Whisper products were typically 20-30% more expensive than competitors, yet consumers paid willingly.

The financial performance during this decade was nothing short of spectacular. Revenues grew from ₹400 crores in 2000 to ₹2,100 crores by 2010—a CAGR of 18%. Operating margins expanded to 18%, among the highest in India's FMCG sector. Return on equity averaged 65%, with some years exceeding 80%. The company's dividend payout ratio increased to 90%, reflecting both confidence in cash generation and P&G's global policy of returning cash to shareholders.

Digital marketing innovation, though nascent, showed P&G's forward-thinking approach. In 2008, PGHH launched India's first health-focused website targeting young women, providing medically accurate information about menstrual health, general wellness, and product education. While internet penetration was still limited, the site reached educated, urban women who would become influencers in their communities. By 2010, it was receiving over 500,000 unique visitors monthly—massive for that era.

The human capital transformation was equally impressive. PGHH became a talent factory for P&G's global operations, with Indian managers leading P&G businesses across Asia, Africa, and Latin America. The company's management training program, accepting just 20 candidates annually from thousands of applicants, became as prestigious as placements at investment banks or consulting firms. This talent excellence created a virtuous cycle—the best people wanted to work at PGHH, enabling even better execution.

As the decade closed, PGHH had achieved something rare in business: near-monopolistic market positions built not through anti-competitive practices but through category creation and superior execution. The company had fundamentally changed Indian society's approach to health and hygiene while building a financial fortress. Yet storm clouds were gathering—e-commerce was emerging, new competitors were studying P&G's playbook, and growth rates were beginning to plateau as categories matured.

V. The Modern Era & Market Dynamics (2010-Present)

The smartphone in every Indian pocket changed everything. In 2010, PGHH executives watched nascent e-commerce players sell a few hundred packs of Whisper online monthly. By 2015, digital channels were moving millions of units, and Instagram influencers were educating young women about menstrual health in ways that made P&G's carefully crafted television campaigns seem quaint. The modern era would test whether a company built on traditional brand-building could adapt to a world where consumers had infinite choices and zero switching costs.

The COVID-19 pandemic initially seemed like a windfall. In March 2020, as India entered lockdown, sales of Vicks VapoRub spiked 300% month-over-month. Consumers stockpiled health products, and anything promising respiratory relief flew off shelves. PGHH's Goa factory operated round-the-clock, with workers living on-site to maintain production while ensuring safety. The company's quarterly results in late 2020 showed revenue growth of 25%—the highest in a decade.

But the pandemic boom masked structural challenges. Once panic buying subsided, a harsh reality emerged: PGHH's growth had been decelerating for years. From 2015 to 2023, revenue CAGR was just 7.37%, barely outpacing inflation. The categories P&G had created and dominated were maturing. Whisper's market penetration among urban women exceeded 85%; there simply weren't many new consumers to convert. In rural markets, despite decades of education efforts, adoption remained frustratingly slow due to affordability constraints and persistent cultural barriers.

The digital disruption took multiple forms. Direct-to-consumer brands like Sirona, Pee Safe, and Nua emerged, targeting millennials with organic products, subscription models, and body-positive messaging that made P&G's approach seem corporate and dated. These brands didn't need massive advertising budgets—they built communities on Instagram, partnered with micro-influencers, and offered personalized experiences P&G's scale-driven model couldn't match. While their individual market shares remained small, collectively they began eroding P&G's premium positioning. The company's response to digital disruption revealed both strengths and limitations. In 2018, PGHH launched "She Can," a digital platform combining e-commerce, education, and community building. While technically sophisticated, it struggled to match the authentic engagement of smaller brands' social media communities. P&G's corporate governance requirements meant every social media post needed multiple approvals, making real-time engagement impossible. By 2021, the platform was quietly discontinued, though P&G maintained it was "integrated into broader digital initiatives."

E-commerce penetration accelerated dramatically. The current price of PGHH is 13,223.00 INR, down significantly from its all-time high on Nov 20, 2023 with the price of 19,250.00 INR. This decline reflects investor concerns about growth prospects despite the company maintaining strong fundamentals. Amazon and Flipkart became critical channels, accounting for over 15% of sales by 2023. But online retail brought new challenges: price transparency made premium pricing harder to justify, counterfeit products damaged brand equity, and platform fees eroded margins.

The rural market, long seen as the next growth frontier, proved stubbornly difficult to crack. Despite decades of investment, Whisper's rural penetration remained below 25%. The government's distribution of free sanitary napkins through schools and health centers, while socially beneficial, eliminated a potential customer base. Local manufacturers, producing pads at one-third of Whisper's price, dominated price-sensitive rural consumers. P&G's attempts to create an ultra-low-cost variant failed—the economics simply didn't work within their quality standards and margin expectations.

Innovation efforts yielded mixed results. The 2019 launch of Whisper Bindazz targeted teenagers with colorful packaging and social media-friendly messaging. While it gained traction in metros, it cannibalized sales from premium Whisper variants rather than expanding the market. Vicks ZzzQuil, a sleep aid launched in 2021, failed to resonate with Indian consumers who preferred traditional remedies or prescription medications for sleep issues. The product was withdrawn within 18 months—a rare admission of failure for P&G.

The financial metrics tell a story of a mature business generating exceptional returns but struggling for growth. P&G HYGIENE & HEALTH CARE EBITDA is 11.37 B INR, and current EBITDA margin is 25.81%, demonstrating operational excellence. P&G HYGIENE & HEALTH CARE dividend yield was 1.31% in 2024, and payout ratio reached 89.24%, reflecting the company's commitment to returning cash to shareholders rather than pursuing aggressive expansion.

Management changes reflected P&G's global strategy shifts. The 2022 appointment of Aalok Gupta as CEO, promoted internally after 20 years with P&G, signaled continuity over transformation. His mandate appeared to be maintaining profitability rather than reigniting growth—a rational but uninspiring strategy that the market interpreted negatively. The stock's underperformance relative to the broader market since 2023 reflects this growth pessimism.

Regulatory pressures added complexity. The government's 2020 decision to cap prices on certain healthcare products, while not directly affecting PGHH's portfolio, created precedent concerns. Environmental regulations requiring biodegradable packaging by 2025 necessitated significant R&D investment, with unclear impact on product costs. GST rate changes and e-commerce regulations added operational complexity without providing growth opportunities.

The competitive landscape evolved dramatically. Hindustan Unilever, long content with second place in feminine hygiene, launched an aggressive campaign with Kotex in 2022, offering products at 40% lower prices with comparable quality claims. Johnson & Johnson's Stayfree introduced India's first biodegradable pad in 2023, appealing to environmentally conscious consumers. Most concerning were reports of Amazon developing private-label feminine hygiene products, leveraging their customer data to identify exact product specifications consumers wanted.

Organizational culture challenges emerged as PGHH struggled to balance P&G's process-driven approach with the agility needed in India's fast-changing market. Talented managers, frustrated by slow decision-making and limited growth opportunities, began leaving for startups and tech companies. The company's reputation as a training ground remained strong, but it increasingly exported talent rather than retaining it.

Yet PGHH's moats remained formidable. Promoter Holding: 70.6%, with P&G's global backing ensuring access to R&D, marketing expertise, and financial resources competitors couldn't match. The distribution network, reaching 4 million outlets, would take decades for new entrants to replicate. Brand equity, built over generations, commanded premium pricing even as cheaper alternatives proliferated. The company's manufacturing excellence, with capacity utilization exceeding 85%, delivered cost advantages despite premium positioning.

As we examine the current state of PGHH, we see a business at an inflection point. The strategies that built market leadership—premium positioning, traditional advertising, pharmacy-channel focus—seem increasingly anachronistic. Yet the company's financial strength, brand equity, and operational excellence provide a foundation for transformation. The question is whether PGHH has the organizational will and capability to reinvent itself for a digital, value-conscious, and rapidly evolving Indian market.

VI. Business Model & Operational Excellence

Inside PGHH's Goa manufacturing facility at 5 AM, the production line hums with precision that would make Swiss watchmakers envious. Every 1.2 seconds, a Whisper Ultra pad rolls off the line, each one identical to millimeter specifications, tested by cameras that can detect imperfections invisible to the human eye. This operational excellence isn't just about quality—it's the foundation of a business model that generates returns most companies can only dream about, yet increasingly struggles to deliver growth.

The numbers tell a remarkable story of financial efficiency. Today P&G HYGIENE & HEALTH CARE has the market capitalization of 429.33 B, built on a asset-light model that requires minimal capital investment. The company operates just two manufacturing facilities—Goa for feminine hygiene and Hyderabad for health care products—yet serves a nation of 1.4 billion people. This concentration enables economies of scale that smaller competitors cannot match: fixed costs spread across massive volumes, procurement leverage that reduces raw material costs by 15-20% versus competitors, and R&D investments amortized across global markets.

The working capital management deserves particular attention. PGHH operates with negative working capital—collecting cash from customers before paying suppliers. Retailers pay within 7-10 days to maintain supply of fast-moving products, while PGHH negotiates 45-60 day payment terms with suppliers using P&G's global purchasing power. This cash conversion cycle generates float that funds operations without external capital, contributing to the extraordinary returns on equity.

P&G's global manufacturing system provides advantages beyond Indian operations. When raw material prices spike in India, PGHH can source from P&G facilities in Thailand or China. When Indian capacity is constrained, products can be imported from other P&G plants with minimal modification. This flexibility proved crucial during COVID-19 when local supply chains collapsed but PGHH maintained product availability through global sourcing.

The R&D leverage model is particularly clever. PGHH spends less than 1% of revenues on local R&D, yet benefits from P&G's global $2 billion annual R&D investment. Innovations developed for American or European markets are adapted for India at marginal cost. The Whisper Ultra technology, for instance, was developed in P&G's Cincinnati labs for Always (the global brand), then modified for Indian preferences at minimal expense. This allows PGHH to introduce cutting-edge products while maintaining higher margins than competitors who must fund entire R&D programs.

Distribution remains PGHH's most valuable yet underappreciated asset. The company's products reach 4 million retail outlets through a network of 40 carrying and forwarding agents, 400 distributors, and 5,000 sub-distributors. But the real sophistication lies in the data and relationships. PGHH knows the optimal stock levels for a pharmacy in Bangalore versus a general store in Bihar, adjusting supply algorithms based on local festivals, weather patterns, and economic conditions. This distribution intelligence, built over decades, cannot be replicated by new entrants regardless of funding.

The brand architecture strategy maximizes returns while minimizing complexity. Unlike competitors managing dozens of brands, PGHH focuses on just two power brands—Whisper and Vicks—with carefully managed variants. Each variant serves a specific price-performance point, preventing channel conflict while capturing consumer surplus. Whisper Ultra commands premium pricing for quality-conscious consumers, Whisper Choice serves price-sensitive segments, and Whisper Bindazz targets teenagers—all manufactured on the same production lines with minor modifications.

Marketing efficiency has evolved significantly. While maintaining television advertising for brand salience, PGHH shifted budgets toward targeted digital marketing with measurable ROI. The company's marketing spend as percentage of sales declined from 15% in 2010 to 11% in 2023, yet brand equity metrics remained stable. This efficiency gain dropped directly to the bottom line, contributing to margin expansion even as revenue growth slowed.

The dividend policy reflects both confidence and constraint. With 100% dividend payout ratios, PGHH essentially operates as a cash machine for P&G global. This policy makes sense given limited growth opportunities and P&G's ability to deploy capital more effectively in higher-growth markets. Yet it also signals that management sees few value-creating investment opportunities in India—a concerning admission for long-term investors.

Supply chain sophistication extends beyond manufacturing to demand planning. PGHH's algorithms predict demand spikes 45 days in advance with 94% accuracy, enabling optimal inventory positioning. During monsoons, Vicks products are pre-positioned in flood-prone areas. Before exam seasons, Whisper inventory increases near colleges. This demand-supply matching reduces stockouts while minimizing inventory carrying costs.

The quality control system represents operational excellence at its finest. Every batch undergoes 47 quality tests, exceeding both Indian regulatory requirements and industry standards. This quality obsession seems excessive until considering the brand damage from a single product failure. When competitors faced recalls for quality issues, PGHH's premium pricing suddenly seemed justified to consumers. Quality became a moat as powerful as brand equity.

Human capital management, while less visible, drives operational excellence. PGHH employs just 600 people directly—extraordinary productivity for a ₹4,300 crore revenue business. This lean structure is enabled by automation, outsourcing of non-core activities, and P&G's global shared services for functions like IT and finance. Employee costs represent less than 5% of revenues, among the lowest in the FMCG sector.

The tax optimization structure, while completely legal, demonstrates financial sophistication. Manufacturing in Goa and Hyderabad provides tax benefits, transfer pricing with P&G entities is optimized within regulatory limits, and royalty payments to P&G for technology and brands are structured efficiently. The effective tax rate of approximately 25% is lower than the statutory rate, adding to shareholder returns.

Yet this operational excellence increasingly feels like optimization at the margins rather than breakthrough innovation. The business model perfected for the analog age—concentrated manufacturing, traditional distribution, mass marketing—may be reaching its limits. Digital-native competitors operate with fundamentally different models: asset-light manufacturing through contract partners, direct-to-consumer distribution bypassing traditional trade, and community-driven marketing that costs fraction of television advertising.

The capital allocation dilemma becomes acute when examining growth investments. PGHH generated over ₹1,000 crores in free cash flow in 2023, yet invested minimal amounts in new categories, digital capabilities, or market expansion. The company seems caught between P&G's global priorities and India's market realities, optimizing what exists rather than building what's next.

As we evaluate PGHH's business model, we see a machine perfected for yesterday's market that may be increasingly misaligned with tomorrow's opportunities. The operational excellence remains remarkable, the financial returns exceptional, but the growth engine appears to be sputtering. The question for investors isn't whether PGHH can maintain its margins—operational excellence ensures that—but whether a perfect execution of an aging model is sufficient in a rapidly transforming market.

VII. Strategic Analysis & Competitive Position

The conference room at Hindustan Unilever's Mumbai headquarters in early 2023 must have been electric with tension. HUL's leadership team was reviewing market share data showing that despite years of investment, their feminine hygiene brands remained a distant second to PGHH's Whisper. The decision that emerged from that meeting—to essentially concede the premium segment while attacking the mass market—illustrates the competitive dynamics that have protected PGHH's castle for decades. But as new attackers emerge with different weapons, the question becomes: are the castle walls still impregnable?

PGHH's competitive moat rests on four pillars, each reinforcing the others in ways competitors find nearly impossible to replicate. First, the brand equity built over generations creates an emotional connection transcending rational product evaluation. When Indian mothers recommend Vicks to their daughters, they're passing down trust earned over decades. This intergenerational brand transfer is priceless—literally, as no amount of advertising spending can quickly replicate it.

The second pillar—distribution dominance—seems mundane but proves devastatingly effective. PGHH's products enjoy premium shelf space in virtually every pharmacy and modern retail outlet. But the real advantage lies deeper: relationships with 400,000 pharmacists who recommend PGHH products when consumers ask for generic alternatives. These pharmacists earn higher margins on PGHH products (despite higher prices) due to faster inventory turns and consistent demand. New entrants offering higher margins but lacking brand pull find pharmacists reluctant to stock products that might not sell.

The third pillar—P&G's global backing—provides advantages beyond capital and R&D. When competitors launch aggressive promotions, PGHH can sustain losses longer than independent companies. When regulations change, P&G's global regulatory expertise navigates compliance faster. When raw material prices spike, global procurement cushions the impact. This corporate parentage creates an asymmetric competition where PGHH plays with house money while competitors bet their survival.

The fourth pillar—operational excellence—raises the bar for profitable competition. PGHH's sub-3% defect rates, 95% on-time delivery, and 85% capacity utilization create cost advantages even at premium prices. Competitors matching PGHH's quality must accept lower margins; those competing on price must compromise quality. This operational moat took decades to build and cannot be purchased regardless of funding.

Yet the competitive landscape is shifting in ways that potentially neutralize these advantages. Digital-first brands like Sirona and Pee Safe don't need traditional distribution—they reach consumers directly through Instagram and WhatsApp. They don't need massive advertising budgets—authentic influencer partnerships and user-generated content drive awareness. They don't need operational excellence at scale—contract manufacturers handle production while they focus on brand building and customer engagement.

The MNC subsidiary dilemma increasingly constrains PGHH's strategic options. P&G globally prioritizes developed markets and China for growth investment, viewing India as a cash generator rather than growth engine. This creates a vicious cycle: limited investment leads to slowing growth, which justifies reduced investment. Meanwhile, domestic competitors like Patanjali and regional players receive patient capital from promoters viewing India as their primary market.

Category maturation presents another strategic challenge. Whisper's 74% market share in organized feminine hygiene seems impressive until recognizing the category's growth is slowing. Urban adoption has plateaued, rural expansion faces structural barriers, and government distribution of free products caps the addressable market. PGHH dominates a category that may have limited runway—like being the best manufacturer of feature phones as smartphones emerge.

The innovation dilemma reflects deeper strategic constraints. P&G's global innovation focuses on developed market needs—ultra-premium products, sustainability features, digital integration—that have limited relevance for price-conscious Indian consumers. Meanwhile, local innovation that could drive growth (ultra-low-cost products, sachet packaging, ayurvedic variants) doesn't align with P&G's global brand standards. PGHH seems caught between global standardization and local adaptation, achieving neither.

Regulatory and ESG pressures add complexity without creating opportunities. Upcoming requirements for biodegradable packaging will increase costs without enabling premium pricing—consumers expect sustainability as standard, not premium feature. Potential price controls on healthcare products create downside risk without upside opportunity. ESG reporting requirements add compliance costs that smaller competitors avoid.

The competitive response to new threats reveals both strength and weakness. When D2C brands emerged, PGHH launched its own digital platform—which failed due to corporate constraints incompatible with startup agility. When natural/organic became trending, PGHH introduced variants that seemed inauthentic compared to purpose-built natural brands. When subscription models gained traction, PGHH's traditional trade partners resisted channel conflict. The company seems capable of responding to yesterday's threats but not anticipating tomorrow's.

Comparison with FMCG peers highlights PGHH's unique position. Hindustan Unilever manages 50+ brands across categories, providing diversification but complexity. Nestle India focuses on food and beverages with steady but unspectacular growth. Colgate-Palmolive India faces similar maturation challenges but lacks PGHH's margin structure. Among MNC subsidiaries, PGHH generates the highest returns but faces the most acute growth challenges.

The strategic options available seem limited but significant. Geographic expansion into Bangladesh, Sri Lanka, and Nepal could leverage existing capabilities, but P&G's global structure complicates regional strategies. Category expansion into adjacent personal care could drive growth but risks diluting focus. Acquisition of digital-first brands could provide capabilities and growth but seems unlikely given P&G's global acquisition priorities. Premium segment expansion could improve margins but the addressable market is limited.

The sustainable competitive advantage question becomes crucial for long-term investors. PGHH's moats remain formidable against traditional competition—no FMCG company will displace Whisper's market leadership in the foreseeable future. But the threat isn't traditional competition; it's market evolution making traditional moats less relevant. Like Kodak's dominance in film photography, PGHH's fortress might remain impregnable even as the battlefield shifts elsewhere.

Porter's Five Forces analysis reveals an interesting paradox. Supplier power: Low, given P&G's global scale. Buyer power: Increasing, as e-commerce enables price comparison. Threat of substitutes: Rising, with government programs and alternative products. Threat of new entrants: High in digital channels, low in traditional trade. Competitive rivalry: Intensifying at the margins while core remains protected. The framework suggests a business with strong current positioning but weakening future dynamics.

The strategic analysis ultimately points to a company at crossroads. PGHH possesses extraordinary competitive advantages in a game whose rules are changing. The company's rational response—optimizing what exists rather than risking transformation—makes sense for shareholder returns today but may mortgage tomorrow's growth. The strategic question isn't whether PGHH will remain profitable—operational excellence ensures that—but whether it can remain relevant as Indian consumers and distribution channels evolve beyond its traditional strengths.

VIII. Future Prospects & Challenges

The year is 2030. A young woman in Pune orders her monthly hygiene supplies through a voice assistant, choosing from 15 brands offering personalized products based on her health data. The products arrive within two hours, packaged in biodegradable materials, priced 40% below what her mother paid for Whisper in 2024. Half the brands didn't exist five years ago. This scenario isn't science fiction—it's the logical extension of current trends that keep PGHH executives awake at night.

The demographic dividend that fueled PGHH's growth for decades is evolving in complex ways. India adds 10 million women to the menstruating age group annually—seemingly a tailwind for feminine hygiene products. But these new consumers differ fundamentally from previous generations. They're digital natives who research products online before purchasing, price-conscious but willing to pay for perceived value, environmentally aware and seeking sustainable options, and comfortable discussing previously taboo topics openly. PGHH's traditional playbook of television advertising and pharmacy distribution seems increasingly misaligned with these emerging consumers.

Category expansion opportunities exist but require capabilities PGHH may lack. The adult incontinence market, growing at 15% annually as India ages, seems logical given manufacturing synergies with feminine hygiene. But success requires destigmatizing another taboo topic, building distribution in different channels, and competing against entrenched players like Kimberly-Clark. The sexual wellness category, projected to reach ₹2,000 crores by 2030, aligns with changing social attitudes but conflicts with P&G's conservative global brand positioning.

The healthcare portfolio beyond Vicks presents its own challenges. The OTC medicine market grows steadily, but PGHH lacks the product depth to capture this growth. Launching new healthcare brands requires regulatory approvals, clinical trials, and medical detailing—capabilities P&G hasn't prioritized in India. Meanwhile, Ayurvedic and natural health products gain share, but P&G's science-based approach seems incongruent with traditional medicine positioning.

Digital transformation isn't optional but existential. E-commerce will account for 30% of FMCG sales by 2030, yet PGHH's digital capabilities remain nascent. The company needs to build direct-to-consumer platforms without alienating traditional trade partners, develop personalization algorithms competing with tech-native brands, create content engaging Gen Z consumers on TikTok and Instagram, and establish subscription models while maintaining traditional purchase patterns. Each requirement demands investments and organizational changes P&G may be unwilling to make for the Indian market alone.

The sustainability imperative creates both cost pressures and innovation opportunities. Indian consumers increasingly expect environmental responsibility but resist paying premiums for it. PGHH must develop biodegradable products maintaining current performance standards, implement plastic-free packaging without compromising product integrity, achieve carbon neutrality while keeping costs competitive, and source raw materials sustainably in complex supply chains. These aren't just CSR initiatives—they're becoming basic competitive requirements.

Regulatory evolution adds uncertainty without clarity. The government's push for self-reliance ("Atmanirbhar Bharat") could disadvantage MNCs through local sourcing requirements or tax changes. Potential price controls on essential health products might cap margins. Data localization requirements could complicate P&G's global systems. Environmental regulations will definitely increase costs but might create opportunities if PGHH moves faster than competitors.

The innovation pipeline appears concerning when examined closely. P&G's global R&D focuses on premium innovations for developed markets—smart products with sensors, ultra-premium materials, and connected health devices. These have limited relevance for Indian mass market consumers. Meanwhile, innovations that could drive Indian growth—ultra-low-cost products, traditional medicine integration, and climate-adapted formulations—don't align with global priorities. PGHH seems caught in an innovation vacuum, unable to leverage global R&D fully or invest in local innovation significantly.

Competition will intensify from unexpected directions. Amazon and Flipkart's private labels will leverage purchase data to identify exact product specifications consumers want, then offer them at 30% lower prices. Chinese manufacturers might enter directly rather than through MNC partners, bringing cost advantages PGHH cannot match. Indian pharmaceutical companies could leverage healthcare credibility to enter OTC segments. Technology companies might create health platforms where products become secondary to services.

The talent challenge becomes acute as PGHH competes with startups and tech companies for digital-age capabilities. The company needs data scientists who could earn more at tech companies, digital marketers who prefer startup agility, and innovation leaders who want decision-making authority P&G's structure doesn't allow. Traditional FMCG talent development—rotating through sales and brand management—doesn't create the capabilities needed for transformation.

Financial projections based on current trends paint a sobering picture. Assuming 6-8% revenue growth (optimistic given recent performance), 2-3% annual margin compression from competition and costs, continued 100% dividend payout limiting reinvestment, and market multiples compressing as growth slows, PGHH could face a decade of stock price stagnation despite generating substantial cash flows. The business remains highly profitable but increasingly viewed as a value trap by growth-oriented investors.

The strategic inflection point approaches rapidly. PGHH must decide whether to milk the existing business for cash while it lasts—a rational but ultimately terminal strategy. Or to reinvest aggressively in transformation—risking current profitability for uncertain future growth. Or to focus narrowly on defending core categories—accepting limited growth but maintaining margins. Each path has merit, but choosing requires clarity P&G's global structure may not provide.

Partnership strategies could provide growth without massive investment. Collaborating with digital-first brands for distribution and innovation, partnering with healthcare startups for new category entry, joining with retailers for private label production, or aligning with NGOs for rural market development. But P&G's preference for control and standardization historically limited such partnerships.

The next decade will determine whether PGHH remains relevant or becomes a case study in market disruption. The company's strengths—brand equity, distribution, operational excellence—remain formidable but may be fighting yesterday's war. Success requires not just defending existing positions but reimagining the business for Indian consumers who are younger, more digital, more value-conscious, and more choice-empowered than ever before.

IX. Investment Thesis & Valuation

Standing before two doors, an investor faces a classic dilemma. Behind door one: PGHH, trading at 52 times earnings, a business with monopolistic positions but single-digit growth, exceptional returns on capital but no reinvestment opportunities, and brand moats that seem impregnable until they suddenly aren't. Behind door two: the broader market, offering hundreds of companies with lower valuations, higher growth, and more dynamic prospects. The choice seems obvious—until you dig deeper into what makes PGHH simultaneously one of India's best businesses and potentially worst investments at current prices.

The bull case rests on quality factors that few Indian companies can match. The 79.7% return on equity isn't a one-time anomaly but a decade-long track record of exceptional capital efficiency. This isn't financial engineering—it's operational excellence generating genuine economic returns. The business requires minimal capital to grow, throws off substantial cash flows, and faces limited competitive threats in core categories. For quality-focused investors, these characteristics typically justify premium valuations.

Brand longevity provides another bullish argument. Whisper and Vicks aren't just products—they're category definitions in Indian consumers' minds. When competitors launch new products, they're compared to Whisper. When mothers treat children's colds, Vicks is the default choice. This brand equity, built over decades and reinforced through generations, creates switching costs that price competition alone cannot overcome. History shows such dominant brands can maintain leadership for decades—Colgate in toothpaste, Maggi in noodles, Bournvita in health drinks.

The P&G parentage offers optionality value rarely priced into the stock. If India's growth accelerates, P&G could deploy global innovations rapidly. If new categories emerge, P&G's expertise could enable quick entry. If competition intensifies, P&G's deep pockets could fund sustained defense. This implicit put option—P&G won't let its Indian subsidiary fail—provides downside protection that standalone companies lack.

Distribution reach remains an underappreciated asset. In an India where 90% of FMCG sales still occur offline, PGHH's presence in 4 million outlets provides competitive advantage that e-commerce hasn't eliminated. Rural India, where 65% of the population resides, barely knows D2C brands exist. As rural incomes rise and infrastructure improves, PGHH's established distribution positions it to capture this growth without incremental investment.

The bear case, however, grows stronger with each passing quarter. The company has delivered a poor sales growth of 7.37% over past five years, barely outpacing inflation. This isn't cyclical weakness but structural maturation. Urban markets are saturated, rural adoption faces affordability barriers, and category growth has decelerated. When core categories grow at GDP rates or lower, premium valuations become impossible to justify regardless of quality.

Valuation metrics flash warning signs across the board. Stock is trading at 58.6 times its book value, implying extraordinary growth expectations the company hasn't delivered in years. The dividend yield of 1.31% provides minimal income compensation for valuation risk. The PEG ratio exceeds 7, suggesting growth assumptions are wildly optimistic. By any traditional measure, PGHH appears priced for perfection in an imperfect world.

The reinvestment challenge undermines long-term compounding potential. Great businesses become great investments when they can reinvest capital at high returns. PGHH generates exceptional returns but pays out 100% as dividends, signaling no value-creating reinvestment opportunities. This transforms PGHH into a bond with equity risk—steady cash flows but no growth, vulnerable to multiple compression as investors recognize the reality.

Disruption risk, while not immediate, grows more tangible. Every D2C brand that gains traction, every Amazon private label launch, every government free distribution program chips away at PGHH's moat. The company's response—marginal product improvements and digital marketing—seems insufficient against fundamental business model innovation. PGHH might dominate feminine hygiene for another decade, but if the category itself becomes commoditized or disrupted, market leadership becomes pyrrhic victory.

Comparative valuation within the FMCG sector suggests relative overvaluation. Hindustan Unilever, with more diversified portfolio and similar growth, trades at 35 times earnings. Nestle India, with stronger growth momentum, trades at 45 times. Colgate-Palmolive, facing similar maturation challenges, trades at 30 times. PGHH's premium to peers seems unjustified given comparable or worse growth prospects.

The DCF analysis reveals the market's heroic assumptions. To justify current valuations, PGHH must either accelerate revenue growth to 12%+ sustainably—unlikely given category maturation, maintain current margins despite increasing competition—possible but challenging, find reinvestment opportunities generating 70%+ returns—nearly impossible, or trade at premium multiples forever—dangerous assumption. The mathematical reality is that current prices embed expectations PGHH has shown no ability to meet.

Risk-reward analysis skews negatively at current valuations. Best case scenario: PGHH maintains market leadership, grows at 8-10% annually, and trades at 40 times earnings—implying 20% downside. Base case: Growth remains at 6-7%, margins compress slightly, multiples normalize to 35x—implying 35% downside. Worst case: Disruption accelerates, growth slows to 3-4%, multiples compress to 25x—implying 50%+ downside. The asymmetry is clear—limited upside, substantial downside.

Different investor types face distinct considerations. For institutional investors seeking quality compounders, PGHH's characteristics are attractive but valuations demanding. For retail investors, the brand familiarity provides comfort but disguises growth challenges. For value investors, the quality is undeniable but the price unconscionable. For growth investors, the story has already played out. For income investors, the dividend yield is insufficient given equity risk.

The timing question becomes crucial. PGHH might be a wonderful business available at a terrible price. History shows quality companies can trade at premium valuations for extended periods before reality forces re-rating. But history also shows that when growth disappoints, multiple compression can be swift and severe. Waiting for better entry points requires patience but preserves capital for opportunities offering better risk-reward.

The investment decision ultimately depends on philosophy and time horizon. Believers in quality-at-any-price might accept lower returns for business certainty. Those seeking market-beating returns must look elsewhere. The tragedy is that PGHH represents everything investors seek—competitive advantages, consistent execution, shareholder-friendly management—except reasonable valuation and growth prospects.

X. Lessons & Takeaways

The American business school professor paused mid-lecture, then asked his students: "If you could build the perfect emerging market subsidiary, what would it look like?" The characteristics they listed—local market knowledge with global capabilities, premium pricing power in price-conscious markets, category leadership without regulatory scrutiny, high returns without reinvestment needs—essentially described PGHH. Yet this "perfect" subsidiary now faces an imperfect future, and the lessons from its journey illuminate fundamental truths about business strategy, market development, and the limits of execution excellence.

The first lesson centers on category creation versus market share battles. PGHH's greatest success came not from competing in existing markets but creating entirely new ones. When P&G introduced Whisper, they weren't selling sanitary napkins—they were selling dignity, hygiene, and female empowerment. The financial returns from creating and dominating new categories dwarf those from fighting for share in established markets. Yet most companies default to competition over creation, missing the exponential value in market-making.

The MNC subsidiary paradox reveals itself starkly through PGHH's evolution. The very advantages that enable initial success—global resources, proven playbooks, operational excellence—eventually become constraints. Parent companies optimize subsidiaries for cash generation rather than growth, impose global standards that may not fit local markets, and prioritize developed markets for innovation investment. PGHH generates extraordinary returns precisely because P&G treats it as a cash machine rather than a growth engine. This creates a tragedy where successful subsidiaries become victims of their own success.

Brand building in emerging markets requires a different calculus than developed markets. PGHH succeeded by understanding that in India, brands aren't just about functional benefits but social signaling, family approval, and risk mitigation. Mothers recommend Vicks not because of superior formulation but because using anything else feels like negligent parenting. This emotional moat, once established, proves nearly impossible for competitors to breach regardless of product superiority or pricing advantage.

The distribution advantage in fragmented markets proves more durable than most strategic advantages. PGHH's 4-million-outlet network isn't just about physical presence but relationships, trust, and economic alignment. Digital disruption hasn't eliminated this advantage—it's simply shifted its nature. The lesson isn't that traditional distribution always wins but that market access, however achieved, remains the fundamental constraint on growth.

Capital allocation in mature businesses presents unique challenges PGHH exemplifies. When a business generates 70%+ returns on equity but lacks reinvestment opportunities, the rational response is returning cash to shareholders. Yet this creates a value trap—high current returns but no growth, premium valuations but deteriorating fundamentals. The lesson is that great businesses don't always make great investments, especially when capital allocation options are constrained.

The innovation dilemma in subsidiaries reflects deeper organizational challenges. PGHH cannot innovate independently without conflicting with P&G global, cannot fully leverage global innovation due to market differences, and cannot acquire innovation due to parent company constraints. This innovation straitjacket means subsidiaries often optimize execution of existing strategies rather than creating new ones. The broader lesson: organizational structure determines strategic options more than market opportunities.

Price-sensitive market dynamics challenge conventional premium positioning strategies. PGHH proved that Indian consumers will pay premiums for perceived value but the definition of value constantly evolves. What justified premiums yesterday (quality, availability, brand assurance) becomes table stakes today. Tomorrow's premiums require different value propositions (personalization, sustainability, convenience) that traditional players struggle to deliver.

The limits of execution excellence become apparent in PGHH's current challenges. The company executes its strategy nearly flawlessly—exceptional quality, efficient operations, strong distribution, effective marketing. Yet perfect execution of an increasingly irrelevant strategy yields diminishing returns. The lesson: operational excellence cannot overcome strategic obsolescence. Companies must evolve strategies as rapidly as they optimize operations.

Digital transformation for traditional companies isn't about technology but business model reimagination. PGHH's digital efforts failed not due to technical incompetence but because digital thinking couldn't flourish within traditional structures. Real digital transformation requires accepting channel conflict, cannibalizing existing products, and empowering rapid decision-making—changes that threaten the very foundations of traditional FMCG success.

The sustainability transition represents both threat and opportunity most companies handle poorly. PGHH, like many incumbents, treats sustainability as compliance cost rather than innovation catalyst. Meanwhile, new entrants build sustainability into their core proposition, attracting conscious consumers and potentially reshaping entire categories. The lesson: sustainability isn't an add-on feature but increasingly the entry ticket to compete.

Market maturation patterns follow predictable cycles PGHH exemplifies. Rapid growth during category creation, consolidation as leaders emerge, maturation as adoption plateaus, and disruption as new models emerge. PGHH dominated phases one through three but seems unprepared for phase four. Understanding where categories sit in this cycle proves crucial for investment timing and strategic planning.

The talent paradox in successful companies becomes acute during transitions. PGHH attracts exceptional talent due to brand prestige and training quality but struggles to retain entrepreneurial leaders who could drive transformation. The very qualities that make someone successful in optimizing mature businesses—process orientation, risk mitigation, consensus building—differ from those needed for innovation and disruption.

Regulatory arbitrage in emerging markets provides temporary advantages that eventually disappear. PGHH benefited from regulations that disadvantaged smaller players, favorable tax treatment for established manufacturers, and brand recognition that influenced policy decisions. As markets mature and regulations evolve, these advantages erode, forcing companies to compete on fundamental business merits rather than structural advantages.

The broader lesson from PGHH's journey speaks to the nature of competitive advantage itself. What appears to be an impregnable moat—brand equity, distribution, operational excellence—can become irrelevant if the basis of competition shifts. PGHH's advantages remain formidable against traditional competition but may prove worthless against new business models that bypass traditional constraints entirely.

For investors, PGHH teaches that quality and value are distinct concepts that occasionally overlap but often diverge. The business quality remains exceptional—few Indian companies match PGHH's returns, margins, and market position. But investment value depends on price relative to future prospects, not past achievements. The highest-quality businesses often make the worst investments when priced for perfection they cannot deliver.

XI. Epilogue & Final Thoughts

As our seven-hour journey through PGHH's evolution concludes, we return to that Mumbai conference room where this story began—but now it's 2025, not 1985. The current CEO sits where Richardson Hindustan executives once nervously awaited P&G's arrival. The walls display the same brands—Whisper and Vicks—that have anchored this business for decades. Yet everything else has changed. The market cap that once seemed ambitious now feels constraining. The growth that once seemed inevitable now seems impossible. The moats that once seemed impregnable now seem increasingly irrelevant.

PGHH's story illuminates the fundamental tension in Indian business: the simultaneous existence of extraordinary success and sobering limitations. Here is a company that transformed Indian society's approach to feminine hygiene, built brands that became category definitions, generated returns that most businesses dream of achieving, and created value chains benefiting millions. Yet it also represents the challenges of MNC subsidiaries in emerging markets, the limits of execution excellence without strategic evolution, and the value traps that quality businesses can become.

What surprises most from researching PGHH is not the well-known success stories but the roads not taken. The company could have leveraged its feminine hygiene dominance to build a women's health ecosystem but chose category focus. It could have acquired digital-first brands to accelerate transformation but remained committed to organic growth. It could have expanded regionally to become a South Asian powerhouse but stayed within India's borders. Each decision, rational in isolation, collectively led to today's growth constraints.

The Indian FMCG landscape that PGHH helped shape now evolves beyond its influence. The consumers P&G educated about branded products now demand personalization algorithms cannot deliver at scale. The retailers PGHH trained in modern trade now stock private labels that undercut premium brands. The categories PGHH created now attract competitors with fundamentally different models. The teacher has educated students who may eventually surpass the master.

For P&G globally, PGHH represents both triumph and limitation. The subsidiary proved that emerging markets could generate developed-market returns, that global brands could succeed with local adaptation, and that category creation could drive exponential value. Yet it also showed that subsidiary success creates its own constraints, that market maturation is inevitable regardless of execution excellence, and that organizational structures designed for one era may be ill-suited for the next.

The human dimension often gets lost in financial analysis, but PGHH's impact extends far beyond shareholder returns. Millions of Indian women experienced dignity and opportunity because Whisper made modern feminine hygiene accessible. Countless families found trusted healthcare solutions in Vicks products. Thousands of employees built careers and capabilities that transformed Indian business. These societal contributions, while not appearing on financial statements, represent value creation that transcends stock prices.

Looking forward, PGHH faces three potential futures. The optimistic scenario sees the company leveraging P&G's global innovation to enter new categories, digital transformation finally succeeding, and rural markets providing the next growth wave. The pessimistic scenario envisions continued share loss to nimble competitors, margin compression from commoditization, and multiple compression as growth disappoints. The realistic scenario—most likely—sees PGHH remaining highly profitable but growth-constrained, generating cash for P&G while slowly ceding market relevance to emerging players.

The investment implications are sobering but clear. At current valuations, PGHH represents a quality business at a speculative price. The stock might remain elevated for years—quality businesses often do—but mathematics eventually prevails. Patient investors might wait for better entry points, potentially during market corrections when quality gets sold indiscriminately. Impatient investors might find better opportunities elsewhere, accepting slightly lower quality for significantly better growth.

The broader implications for India's consumer market are profound. If PGHH—with its advantages of brand equity, distribution reach, operational excellence, and global backing—struggles for growth, what does this mean for the consumer sector overall? Perhaps it signals market maturation requiring different strategies. Perhaps it reflects changing consumer preferences that established players cannot address. Perhaps it represents the natural evolution from branded products to platform ecosystems. Most likely, it's all of these simultaneously.

For business students and practitioners, PGHH offers a masterclass in both success and limitation. The company did almost everything right—built strong brands, achieved operational excellence, generated exceptional returns, and served stakeholders well. Yet doing everything right within an existing paradigm may be insufficient when the paradigm itself shifts. The lesson isn't that PGHH failed—it manifestly succeeded—but that success in business, like evolution in nature, requires constant adaptation rather than optimization alone.

As we close this analysis, PGHH stands at an inflection point that will define its next chapter. The company could surprise skeptics by successfully transforming for the digital age. It could validate bears by continuing its slow decline into irrelevance. Most likely, it will muddle through—remaining profitable and cash-generative while gradually losing market position to hungrier competitors. This isn't a dramatic ending, but business reality rarely provides Hollywood conclusions.

The story of Procter & Gamble Hygiene and Health Care Limited ultimately transcends any single company. It's the story of how global expertise met local insight to create extraordinary value. It's the narrative of market creation and category dominance in the world's most complex consumer market. It's the cautionary tale of how success can become constraint and excellence can become enemy of evolution. Most fundamentally, it's the very human story of building something meaningful, watching it mature, and grappling with what comes next.

For investors evaluating PGHH today, the decision comes down to philosophy. If you believe that quality businesses with sustainable moats deserve premium valuations regardless of growth, PGHH might appeal. If you seek growth at reasonable prices with upside potential, look elsewhere. If you're P&G, you own a cash machine that funds investments in higher-growth markets—a rational if uninspiring strategy. If you're an Indian consumer, you benefit from products that improved lives even as new alternatives emerge.

The final thought returns us to the beginning: PGHH represents both the apex and limitations of traditional FMCG strategy in emerging markets. The company achieved what seemed impossible—convincing price-conscious Indians to pay premiums for branded hygiene products. Yet it now faces what seems inevitable—disruption from models that bypass the very foundations of its success. Whether PGHH navigates this transition successfully will determine not just its own future but provide lessons for every traditional company facing digital transformation.

In the end, PGHH's story isn't finished—it's entering a new chapter whose ending remains unwritten. The company that defined categories for one generation of Indians must now evolve for the next. The business that generated extraordinary returns for decades must find new sources of growth. The subsidiary that exceeded all expectations must now transform those expectations themselves. How this story ends depends on decisions being made today in conference rooms in Mumbai, Cincinnati, and Bangalore—decisions that will determine whether PGHH remains a dominant force or becomes a case study in disruption.

The tape recorder clicks off. The analysis is complete. The investment decision, as always, remains yours to make.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube