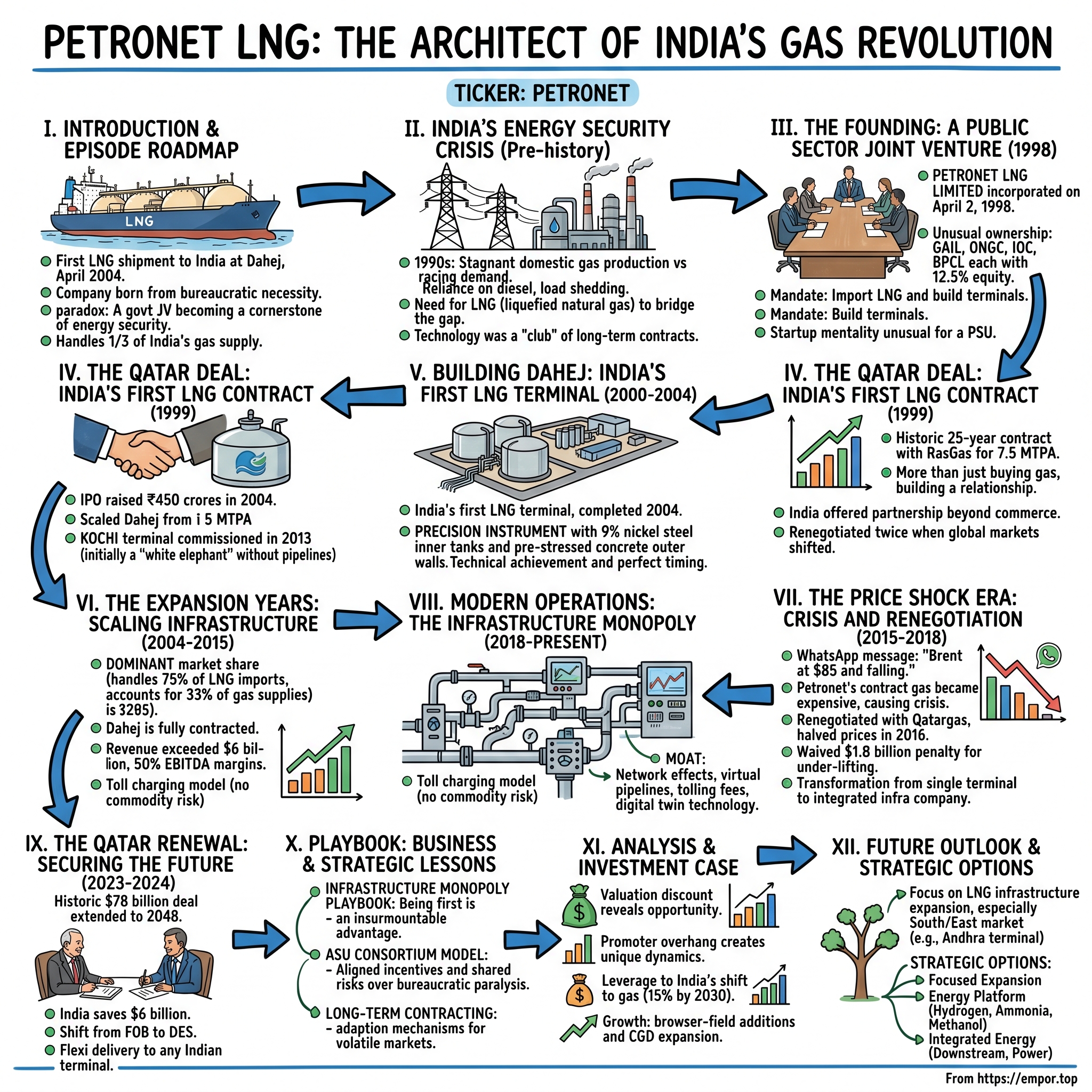

Petronet LNG: The Architect of India's Gas Revolution

I. Introduction & Episode Roadmap

Picture this: It's April 2004, and a massive LNG carrier—the size of three football fields—approaches India's western coast. On board: 138,000 cubic meters of liquefied natural gas cooled to minus 162 degrees Celsius. This isn't just another cargo delivery. It's the first-ever LNG shipment to India, arriving at a terminal that didn't exist four years earlier, built by a company that many thought would fail. The vessel docks at Dahej, Gujarat, marking the moment India entered the global LNG trade. Behind this historic arrival stands Petronet LNG—a company born from bureaucratic necessity that would transform into India's most profitable gas infrastructure giant.

Here's the paradox that defines Petronet: How did a government-created entity, structured as a joint venture between four competing public sector oil companies, become the cornerstone of India's energy security? Today, Petronet handles one-third of India's total gas supply, operating terminals that process 22.5 million metric tons of LNG annually. Its Dahej terminal alone meets more than one-third of India's LNG demand. The company's market capitalization hovers around $5.4 billion, with revenues exceeding $6 billion—remarkable for what started as a special-purpose vehicle with no assets, no expertise, and no precedent in India.

The Petronet story isn't just about building terminals and importing gas. It's about infrastructure as nation-building, the delicate dance of energy diplomacy with Qatar, and riding—perhaps defining—India's energy transition. This is a company that signed a 25-year contract worth billions when India had zero LNG infrastructure, then successfully renegotiated it twice when global markets shifted. It's about creating a business model so robust that despite operating in a commodity market known for volatility, Petronet delivers consistent returns through its tolling structure.

What makes this story particularly compelling for investors is the moat Petronet has built. In infrastructure businesses, being first isn't just an advantage—it's often insurmountable. Petronet didn't just build terminals; it created an ecosystem. The pipelines that connect to its facilities, the customer relationships built over two decades, the operational expertise in handling cryogenic materials—these form barriers that money alone cannot replicate.

As we unpack this story, we'll explore several key themes. First, how Petronet navigated the peculiar dynamics of being owned by four state-controlled companies that often compete with each other. Second, the Qatar relationship—arguably one of India's most successful energy partnerships—and how it evolved from a simple supply contract to a strategic alliance. Third, the infrastructure monopoly playbook: how Petronet leveraged first-mover advantage in a capital-intensive sector to create an unassailable position. And finally, what Petronet's journey tells us about India's energy future as the country aims to increase gas from 6% to 15% of its energy mix by 2030.

This isn't just a corporate history—it's the story of how India solved its gas deficit, one shipment at a time, through an unlikely vehicle that became indispensable.

II. The Pre-History: India's Energy Security Crisis

The lights went out again in Delhi. It was 1997, and power cuts—euphemistically called "load shedding"—were as predictable as monsoons. Industries ran on diesel generators, urban households stockpiled candles, and India's economic ambitions seemed perpetually constrained by energy shortages. The country's gas production had stagnated at around 20 billion cubic meters annually, while demand was racing past 30 billion. The math was simple and brutal: India needed energy it couldn't produce.

To understand why Petronet exists, you need to grasp the desperation of India's energy situation in the 1990s. The country's domestic gas fields—primarily the Mumbai High basin discovered in 1974—had plateaued. ONGC, the national oil company, was drilling furiously but finding little. The Krishna-Godavari basin showed promise but wouldn't deliver for years. Meanwhile, India's economy had just liberalized in 1991, unleashing pent-up industrial demand. Fertilizer plants, power stations, and petrochemical complexes all wanted gas—cleaner than coal, cheaper than oil, more reliable than intermittent renewables.

The political economy of energy in India added layers of complexity. Gas wasn't just a commodity; it was a tool of statecraft. The government controlled prices, allocated supplies, and subsidized consumption. Fertilizer plants got priority—food security trumped everything. Power plants came next. Industries got whatever remained, usually not much. This allocation raj created bizarre distortions: factories relocated based on gas availability, not market logic. Cities with pipeline connections boomed while others stagnated.

Enter LNG—liquefied natural gas. The technology wasn't new; Japan had been importing LNG since 1969. But for India, it represented a radical shift. LNG meant you could import gas from anywhere—Qatar, Australia, Nigeria—compress it to 1/600th of its volume, ship it in specialized tankers, and regasify it at destination. No pipelines across hostile territories, no geopolitical complications with Pakistan or Bangladesh. Just ships, terminals, and contracts.

Yet the global LNG market of the late 1990s was nothing like today's liquid, spot-market-driven trade. It was a club—long-term contracts, dedicated infrastructure, prices linked to oil. Japan and South Korea dominated demand. Qatar and Indonesia controlled supply. Breaking into this club required three things India lacked: massive upfront capital, technical expertise in cryogenics, and creditworthy buyers willing to sign 20-year contracts.

The numbers told a stark story. Building an LNG terminal cost $500-700 million minimum—roughly 0.1% of India's GDP then. The specialized ships cost $200 million each. You needed at least two for reliable supply. The regasification technology was proprietary, controlled by a handful of global engineering firms. And the gas itself? Sellers wanted 20-25 year commitments with take-or-pay clauses—you paid whether you took delivery or not. Private companies faced a catch-22. The government offered them gas allocations but at controlled prices that made imports unviable. Industrial users wanted gas but couldn't get firm supply commitments. State electricity boards, the primary power buyers, were bankrupt and couldn't honor payment obligations. Most of these developments were spurred by the liberalization of the 1990s, yet the energy sector remained trapped in pre-liberalization structures.

This was the crisis Petronet was created to solve. But solving it would require navigating India's labyrinthine bureaucracy, managing international relations with Middle Eastern suppliers, and building world-class infrastructure in a country where such projects routinely failed. The stage was set for either a spectacular success or an equally spectacular failure.

III. The Founding: A Public Sector Joint Venture (1998)

The conference room at Shastri Bhawan, New Delhi's bureaucratic nerve center, was packed on a humid August morning in 1997. Four titans of India's public sector oil companies sat across from Ministry of Petroleum officials, each calculating risks and opportunities. GAIL's chairman wanted to maintain dominance in gas distribution. ONGC sought outlets for future production. Indian Oil and Bharat Petroleum needed diversification beyond refining. The solution they crafted was uniquely Indian: create a joint venture where everyone wins—or at least, no one loses alone.

Petronet LNG Limited was incorporated on April 2, 1998, with an unusual ownership structure: GAIL, ONGC, Indian Oil Corporation, and Bharat Petroleum Corporation each held 12.5% equity. The remaining 50% was earmarked for financial institutions and public shareholders—a structure designed to spread risk while maintaining state control. This wasn't just financial engineering; it was political choreography. By giving four major PSUs equal stakes, the government ensured no single entity could dominate, while collective ownership guaranteed political support across ministries.

The mandate was deceptively simple: import LNG and build terminals to regasify it. The execution would prove anything but simple. India had never built an LNG terminal. The country lacked engineers trained in cryogenic technology. No Indian company had experience negotiating long-term gas contracts with international suppliers. The closest precedent was Japan's LNG program, but Japan had started in 1969 with American technical assistance and deep pockets. India in 1998 had neither.

The early team at Petronet reads like a who's who of India's energy establishment. A.K. Balyan, GAIL's nominee, became the first managing director. Engineers were seconded from the four promoters, creating a melting pot of corporate cultures. ONGC's upstream specialists clashed with Indian Oil's downstream experts. GAIL's pipeline engineers debated terminal designs with BPCL's refinery teams. Out of this creative chaos emerged a startup mentality unusual for a PSU—move fast, take calculated risks, deliver results.

The challenges cascaded immediately. International LNG suppliers viewed India skeptically—a country with chronic payment delays, currency volatility, and no LNG infrastructure. Banks hesitated to finance a project with no precedent. Environmental clearances required for coastal terminals meant navigating multiple ministries. The Dahej site in Gujarat, chosen for the first terminal, was largely marshland requiring massive land reclamation.

Yet Petronet had one crucial advantage: government backing without government bureaucracy. As a joint venture, it could move faster than traditional PSUs. Board decisions didn't require ministry approval. Procurement could bypass lengthy tender processes. Most importantly, the four promoter companies provided not just capital but ecosystems—GAIL's pipeline network, IOC's marketing reach, ONGC's technical expertise, BPCL's operational experience.

The governance structure reflected this delicate balance. The board had sixteen directors—four nominees from each promoter, ensuring equal representation. The chairmanship rotated among promoters. Operational decisions required consensus, forcing collaboration over competition. This structure, criticized initially as unwieldy, proved remarkably effective. When disagreements arose—and they did frequently—the shared risk ensured compromise rather than deadlock.

By early 1999, Petronet had assembled a team, identified terminal sites, and begun preliminary engineering. But the real test lay ahead: securing LNG supply. Without a long-term contract with a reliable supplier, the terminals would be expensive monuments to ambition. The hunt for gas would take Petronet's negotiators from the boardrooms of Tokyo to the palaces of Doha, culminating in a deal that would define India's energy landscape for the next quarter-century.

IV. The Qatar Deal: India's First LNG Contract (1999)

The delegation from Petronet landed in Doha on a scorching July morning in 1999, the heat shimmering off the tarmac like a preview of the negotiations ahead. Led by A.K. Balyan, the team included lawyers, engineers, and crucially, a diplomat from India's Ministry of External Affairs. They weren't just negotiating a commercial contract; they were crafting an energy partnership that would bind India and Qatar for generations. Across the table sat executives from RasGas, Qatar's LNG giant, who held all the cards—proven reserves, existing infrastructure, and a queue of eager buyers from Japan and Korea.

The negotiations stretched over 72 hours of continuous sessions. The Indians pushed for flexibility—lower volumes initially, with ramp-up provisions. The Qataris wanted certainty—firm commitments, take-or-pay clauses, creditworthy guarantees. The breakthrough came when India offered something unique: a partnership beyond commerce. Indian companies would help develop Qatar's downstream sector. Indian workers would staff Qatari projects. This wasn't just buying gas; it was building a relationship.

On July 31, 1999, the deal was signed: 7.5 million tonnes per annum for 25 years, starting 2004. The initial pricing formula—$2.53 per million British thermal unit at a crude oil price of $20 per barrel—seemed reasonable in 1999's oil market. The contract included an unusual provision: RasGas would supply "rich" LNG containing higher ethane and propane content, valuable for India's petrochemical industry. This wasn't standard lean gas but a premium product that would later prove both blessing and curse.

The geopolitical dimensions ran deep. Qatar, a small nation surrounded by larger neighbors, sought diverse partnerships beyond traditional buyers. India offered a massive market and strategic depth. For India, Qatar represented energy security without the complications of pipeline politics with Pakistan or Iran. The relationship transcended energy—by 2020, eight million Indians would work in Gulf countries, with Qatar hosting 700,000, creating economic interdependencies beyond hydrocarbons.

But even as champagne flowed in Doha, storm clouds gathered. Oil prices, stable at $20 per barrel in 1999, would spike to $147 by 2008, making the contract increasingly expensive. The take-or-pay provisions, standard in LNG contracts, would become albatrosses when spot prices crashed post-2014. The rich gas specification, initially attractive, would later complicate operations when ONGC's petrochemical plant faced delays.

The 2003 renegotiation marked Petronet's diplomatic maturity. As oil prices rose, the original formula became untenable. Petronet's negotiators, led by new CEO Prosad Dasgupta, convinced RasGas to cap prices at $20 per barrel equivalent for the first five years (2004-2009). This saved India hundreds of millions but required delicate handling—Qatar could have easily sold the volumes to other buyers at higher prices. The agreement reflected Qatar's long-term view: preserving the Indian relationship mattered more than short-term gains.

The contract's structure revealed sophisticated risk management. Volumes were denominated in million British thermal units, not tonnes, protecting against quality variations. Delivery terms were FOB (Free on Board), meaning India arranged shipping—complex but allowing control over logistics. The take-or-pay threshold was set at 90%, providing some flexibility while ensuring Qatar's revenue certainty. Payment terms included letter of credit provisions, addressing Qatar's creditworthiness concerns while managing India's foreign exchange exposure. The shipping arrangements revealed another layer of complexity. Petronet chartered vessels through a consortium of Shipping Corporation of India and Japanese shipping companies—a structure reflecting both resource constraints and strategic thinking. India lacked LNG shipping expertise; partnering with Japanese firms provided technology transfer while keeping Indian interests paramount through SCI's participation.

The foundation laid in 1999 would prove remarkably durable—the contract was successfully extended in 2024 for another 20 years, making it one of the longest-running LNG relationships globally. But first, Petronet had to build something India had never seen: a terminal capable of handling ships carrying cargo at minus 162 degrees Celsius.

V. Building Dahej: India's First LNG Terminal (2000-2004)

The morning of November 15, 2000, marked a turning point at Dahej, a sleepy fishing village on Gujarat's coast. Earth movers roared to life, beginning construction of what would become India's energy lifeline. The site seemed unpromising—tidal mudflats stretching to the horizon, no infrastructure for miles, temperatures hitting 45 degrees Celsius in summer. Yet within four years, this desolate stretch would house one of Asia's most sophisticated LNG terminals.

Construction started in 2000, with the 5MTPA facility commencing operation in April 2004. The engineering challenges were staggering. LNG terminals aren't just ports—they're precision instruments. The storage tanks alone required technology India had never deployed: full containment systems with inner tanks of 9% nickel steel (which remains ductile at cryogenic temperatures), surrounded by pre-stressed concrete outer walls capable of containing the entire contents if the inner tank failed. Each of the six tanks could hold 160,000 cubic meters—enough to supply Delhi's gas needs for a month.

The marine infrastructure posed equal challenges. Two jetties with 2.4-kilometer trestles had to be built into the Arabian Sea, designed to handle ships with drafts up to 12 meters. The seabed required dredging to minus 14 meters, removing millions of cubic meters of silt. The berthing structures needed to accommodate vessels ranging from 70,000 to 265,000 cubic meters capacity, with loading arms capable of transferring LNG at 12,000 cubic meters per hour while compensating for tidal variations of up to 11 meters.

But the real complexity lay in the regasification process—converting LNG back to gas. Petronet chose Open Rack Vaporizers (ORVs), using seawater to warm the LNG. This sounds simple but required handling 150,000 cubic meters of seawater per hour, with elaborate systems to prevent marine growth, manage temperature differentials, and ensure the discharge didn't harm marine ecosystems. The facility needed 36 vaporizers, each standing 30 meters tall, operating in harsh coastal conditions with salt spray and cyclonic winds.

The human story behind Dahej's construction reads like an industrial epic. The project director, V.K. Mishra, seconded from GAIL, moved his family to Bharuch, the nearest town 50 kilometers away. He spent four years on-site, often sleeping in temporary shelters, managing 3,000 workers speaking a dozen languages. Japanese engineers from Toyo Engineering supervised cryogenic systems. French specialists from Technip handled marine structures. Indian contractors learned by doing, with zero margin for error—a single weld failure in an LNG tank could cause catastrophic damage.

The commissioning phase in early 2004 brought its own drama. The first cool-down of the tanks—gradually lowering temperature from ambient to minus 162 degrees—took 72 hours of round-the-clock monitoring. Engineers checked thousands of sensors for thermal stress, watching for the slightest anomaly. When the first ship, carrying cargo from Qatar's Ras Laffan terminal, approached Dahej in April 2004, the entire senior management of Petronet was present. The unloading took 18 hours—every valve operation double-checked, every pressure reading scrutinized.

What made Dahej remarkable wasn't just its technical achievement but its timing and execution. Comparable terminals globally took 5-6 years to build; Dahej was operational in four. The project came in under budget—₹2,500 crores against sanctioned ₹2,750 crores. Most critically, it worked flawlessly from day one, handling 2.5 million tonnes in its first year of operation, ramping to full capacity by year two.

The terminal's success had ripple effects beyond gas supply. It established India's credibility in global LNG markets—Qatar saw India could execute complex infrastructure. It created an ecosystem of expertise—Indian engineers who worked on Dahej would go on to build terminals across Asia. It demonstrated that PSUs, often criticized for inefficiency, could deliver world-class projects when properly motivated and structured.

The expansion trajectory was equally impressive. Capacity grew from 5 MTPA in 2004 to 10 MTPA by 2009, then 15 MTPA by 2016, eventually reaching 17.5 MTPA. Each expansion was completed without disrupting ongoing operations—like performing surgery while running a marathon. The terminal that started with two tanks now has six, with infrastructure to add more. From a single jetty, it expanded to two, capable of handling simultaneous operations.

But Dahej was just the beginning. Even as the first vessels unloaded at Gujarat's coast, Petronet was planning its next move: bringing LNG to India's south through a terminal at Kochi, a project that would test the company's resilience in entirely different ways.

VI. The Expansion Years: Scaling Infrastructure (2004-2015)

The boardroom at Petronet's Delhi headquarters buzzed with nervous energy on January 31, 2004. The company was about to attempt something audacious: an initial public offering just months before its first terminal became operational. Critics called it premature—selling shares in a company with no revenue, untested operations, and massive capital commitments. CEO Prosad Dasgupta saw it differently: "We're not selling our past; we're selling India's energy future."

The IPO raised ₹450 crores, with shares priced at ₹15 each. Retail investors were skeptical, but institutions understood the thesis. The Asian Development Bank made a strategic investment, acquiring 5.2% equity, lending credibility to the venture. The listing coincided with the Dahej terminal's commissioning, creating momentum that would define Petronet's expansion decade.

Scaling from 5 MTPA to 10 MTPA at Dahej by 2009 required more than adding tanks and vaporizers. The entire ecosystem needed upgrading. Pipeline connectivity expanded from a single 30-inch line to GAIL's HVJ network to multiple connections reaching industrial clusters in Gujarat, Rajasthan, and eventually Delhi. Petronet pioneered the concept of "virtual pipelines"—using cryogenic trucks to deliver LNG to customers beyond pipeline reach, opening markets previously impossible to serve.

The Kochi terminal represented a different challenge altogether. Announced in 2007, it was meant to bring gas to India's energy-starved south. But Kochi became Petronet's trial by fire. Land acquisition faced local protests. Environmental clearances took years, with concerns about impact on fishing communities. The global financial crisis of 2008 complicated financing. Construction, started in 2010, faced delays from monsoons, labor disputes, and technical challenges unique to Kerala's coastal conditions.

When Kochi finally commissioned in August 2013—three years behind schedule—it faced an ironic problem: no customers. The pipeline connecting the terminal to consumers didn't exist. For months, this 5 MTPA facility operated at less than 10% capacity, burning cash while waiting for GAIL's pipeline to reach Bangalore. Critics pounced, calling it a white elephant. Within Petronet, it became a lesson in system thinking—terminals without pipelines are expensive monuments.

The customer acquisition strategy during this period revealed sophisticated market development. Petronet didn't just wait for demand; it created it. The company partnered with city gas distribution companies, helping them expand CNG stations and piped gas networks. It worked with fertilizer plants to switch from naphtha to gas, providing technical support for retrofitting. Power plants designed for coal were incentivized to add gas turbines. Each new customer became an anchor, justifying pipeline extensions that brought more customers online.

The financial engineering was equally clever. Petronet's business model—charging tolling fees for regasification regardless of gas prices—provided steady returns even as global LNG markets gyrated. The company maintained EBITDA margins above 50% consistently, generating cash for expansion without additional equity dilution. Debt was structured carefully, with rupee loans for domestic construction and dollar financing for import infrastructure, creating natural hedges.

The expansion years also saw Petronet's transformation from a single-terminal operator to an integrated infrastructure company. The company ventured into port operations, with Dahej becoming a multi-cargo port handling chemicals and containers alongside LNG. A petrochemical project was conceptualized, leveraging ethane-rich gas from Qatar. Trading operations expanded, with Petronet sourcing spot cargoes for customers beyond its contracted volumes.

Organizationally, Petronet evolved from a startup mentality to institutional maturity. The initial team of seconded employees gave way to direct recruits—engineers trained specifically for LNG operations. Safety systems reached global benchmarks, with Dahej achieving five million man-hours without lost-time incidents. The company developed proprietary expertise in tropical conditions—most global LNG knowledge assumed temperate climates; Petronet had to innovate for India's heat and humidity.

The 2004 IPO investors who held their shares saw remarkable returns. By 2015, the stock had appreciated over 1000%, with consistent dividends adding to total returns. But more importantly, Petronet had delivered on its strategic promise. Gas consumption in India grew from 30 billion cubic meters in 2004 to 50 billion by 2015, with imports comprising 40% of supply. Petronet handled the majority of these imports, cementing its position as infrastructure monopolist.

Yet even as Petronet celebrated expansion milestones, storm clouds gathered on the horizon. Global LNG markets were transforming. The shale gas revolution in America, new supplies from Australia, and slowing demand from traditional buyers like Japan created a buyer's market. The comfortable long-term contracts that defined Petronet's first decade would soon face their greatest test, forcing the company to reimagine its business model in an era of abundance rather than scarcity.

VII. The Price Shock Era: Crisis and Renegotiation (2015-2018)

The WhatsApp message landed like a bombshell on CFO R.K. Garg's phone in October 2014: "Brent at $85 and falling." Within weeks, oil would crater below $50, eventually touching $26 by early 2016. For Petronet, whose Qatar contract priced LNG at 12.7% of Brent crude, this should have been celebration time. Instead, it triggered the company's worst crisis since inception. The reason? Spot LNG prices fell even faster than oil, making Petronet's contracted gas suddenly expensive.

The numbers were brutal. Petronet was lifting only 30-32% of its contractual 7.5 million MT annual volumes by late 2015, as customers found spot cargoes at half the price of term contracts. Under take-or-pay provisions, Petronet still owed payment for 90% of contracted volume whether lifted or not. By 2016, fifty-two cargoes had been deferred, creating a liability exceeding $1 billion. The company that had built India's gas infrastructure now faced an existential threat from the very contracts that enabled it.

The pricing formula that seemed reasonable in 1999—12.7% of Brent with a floor and ceiling based on 60-month Japanese Crude Cocktail average—had become an albatross. When oil hit $147 in 2008, the ceiling protected Petronet. But the floor meant that even as spot LNG traded at $6-7 per MMBtu, Petronet's contracted gas cost $12-13. Indian customers, facing their own pressures, simply refused to buy. Power plants switched to coal. Fertilizer companies invoked force majeure. City gas distributors bought spot cargoes directly.

Inside Petronet's headquarters, crisis management became the daily routine. CEO Prabhat Singh, who took charge in 2014, faced a Hobson's choice: enforce contracts and alienate customers who were also shareholders (remember, IOC, BPCL, and GAIL were both promoters and buyers), or absorb losses that could cripple the company. The board meetings during this period, according to insiders, were "bloodbaths"—each promoter protecting its interests as buyer while demanding returns as shareholder.

The renegotiation with Qatar became a delicate diplomatic dance. In December 2015, RasGas agreed to nearly halve prices from $12-13/MMBtu to $6-7/MMBtu, effective January 2016 through late 2028, introducing market dynamics through a revised crude-linked formula. But this wasn't charity—Qatar faced its own pressures. New LNG projects in Australia and the US had created global oversupply. Japan, traditionally Qatar's largest buyer, was restarting nuclear plants post-Fukushima, reducing LNG demand. Qatar needed to preserve market share, and India represented future growth. The deferred cargo problem created a unique dilemma. Petronet had asked Qatargas to deliver in 2022 the 50 cargoes that were deferred in 2015, as it was decided that India could seek the cargoes anytime during the remainder of the contract that ends in 2028, and in case Qatar was unable to meet the request, the deferred cargoes could be delivered in 2029. This flexibility, negotiated during the crisis, showed both parties' commitment to the long-term relationship despite short-term turbulence.

The global LNG market transformation during this period was seismic. The US, which had been planning to import LNG as recently as 2010, became an exporter by 2016. Australia brought seven new projects online. Qatar faced competition it hadn't seen before. The comfortable seller's market that defined LNG trade for decades evaporated almost overnight. Buyers gained leverage, demanding shorter contracts, destination flexibility, and price reviews.

For Petronet, the crisis forced strategic introspection. The company's entire business model assumed stable long-term contracts with predictable margins. Now it needed to operate in a volatile spot market while managing legacy contract obligations. The response was creative: Petronet began offering "tolling plus" services—storage, truck loading, break-bulk operations—anything to monetize infrastructure beyond basic regasification.

The organizational strain was palpable. Key executives who had built careers on the Qatar relationship suddenly found their expertise devalued. Young traders who understood spot markets gained influence. The board, previously focused on expansion, now scrutinized every cargo, every customer commitment. Quarterly earnings calls became exercises in damage control, with analysts grilling management on take-or-pay liabilities.

Yet from crisis emerged opportunity. A penalty for taking less-than-contracted volumes amounting to about $1.8 billion on Petronet was waived by RasGas, demonstrating Qatar's long-term commitment to the Indian market. The renegotiated terms allowed Petronet to compete with spot prices while maintaining supply security. Most importantly, the crisis proved Petronet's resilience—despite the worst market conditions in its history, the company remained profitable, maintained operations, and preserved stakeholder trust.

By 2018, as markets stabilized and spot prices began rising again, Petronet emerged leaner and smarter. The company had learned to hedge, to trade opportunistically, to manage contracts dynamically rather than passively. The price shock era, painful as it was, prepared Petronet for its next phase: leveraging its infrastructure monopoly in an increasingly competitive and complex global gas market.

VIII. Modern Operations: The Infrastructure Monopoly (2018-Present)

The control room at Dahej terminal hums with quiet efficiency at 3 AM on a typical Tuesday. Twenty-four screens display real-time data—tank levels, pipeline pressures, ship positions, weather patterns. An operator notices a minor pressure fluctuation in vaporizer bank three, adjusts flow rates with two clicks, problem solved. This scene, replicated 24/7/365, represents the culmination of Petronet's journey from startup to infrastructure behemoth. Today's Petronet isn't just India's largest LNG company—it's an irreplaceable cog in the nation's energy machinery.

The numbers tell a story of dominance rarely seen in infrastructure sectors. Petronet owns and operates 2 regasification terminals at Dahej (Gujarat) and Kochi (Kerala) with a combined capacity of 22.5 MMTPA, accounting for 33% of gas supplies in the country and handling ~75% of LNG imports in India. The Dahej terminal alone processes more molecules of natural gas daily than most countries' entire gas systems. Revenue for FY 2022-2023 reached ₹46,663 crores, with EBITDA margins consistently above 50%—remarkable for what's essentially a utility business.

But the real moat isn't capacity—it's the ecosystem Petronet has created. The Dahej terminal connects to six major pipeline systems, reaching customers across fifteen states. The facility handles not just standard LNG carriers but also small-scale vessels, ISO containers, and truck loading—serving everyone from steel plants needing thousands of tonnes daily to small industries requiring a few truck-loads weekly. This flexibility, built over two decades, cannot be replicated without massive investment and time.

The tolling model represents financial engineering at its finest. Petronet charges customers approximately $0.50-0.75 per MMBtu for regasification services, regardless of underlying gas prices. When spot LNG trades at $5 or $25, Petronet's margin remains constant. The company doesn't take commodity risk—that's for traders and end-users. This model provides predictable cash flows that debt investors love and equity investors sometimes misunderstand, wondering why Petronet doesn't capture more value during price spikes.

Diversification efforts reveal strategic thinking beyond traditional LNG operations. The petrochemical project at Dahej, though delayed, positions Petronet to capture value from ethane and propane separated from rich gas. Port operations have expanded, with Dahej handling liquid cargo, generating additional revenue from existing marine infrastructure. The company is exploring small-scale LNG distribution, targeting industrial customers beyond pipeline reach—a market potentially worth billions as India pushes for gas adoption.

The competitive landscape appears deceptively simple. Several new LNG terminals have been built—Mundra, Ennore, Dhamra—yet Petronet's market share remains dominant. Why? Network effects. Customers prefer Petronet because that's where the liquidity is—multiple suppliers, multiple buyers, creating a spot market within the terminal. Pipeline companies prioritize connections to Petronet facilities. Shipping companies schedule around Dahej's berthing slots. It's a self-reinforcing cycle that strengthens with each cargo.

Technology adoption, often overlooked in infrastructure companies, has been crucial. Petronet implemented digital twin technology for predictive maintenance, reducing unplanned downtime to near zero. Blockchain pilots for documentation have cut cargo clearance time from days to hours. AI algorithms optimize tank utilization, allowing the company to handle 20% more volume without adding storage capacity. These aren't headline-grabbing innovations, but they compound into operational excellence.

The financial performance reflects this operational superiority. Return on equity consistently exceeds 20%. Debt-to-equity ratio remains below 0.5, providing flexibility for expansion. Dividend payout ratios above 60% satisfy income-focused investors while retaining enough capital for growth. The stock, despite volatility during commodity cycles, has delivered 15% annual returns over the past decade—beating most infrastructure peers.

Human capital management reveals sophistication unusual for a PSU-promoted entity. Petronet employs fewer than 500 people—remarkable for a company handling a third of India's gas supply. Average employee cost exceeds ₹30 lakhs annually, attracting top talent. The company runs India's only LNG terminal operations training center, creating industry-wide expertise while ensuring operational continuity.

Risk management has evolved from basic hedging to sophisticated portfolio optimization. Petronet now offers customers various contract structures—take-or-pay, interruptible, seasonal—allowing risk allocation based on customer preference and paying capacity. The company maintains strategic storage, selling flexibility services to traders who pay premiums for optionality. Currency hedging, critical given dollar-denominated imports, uses natural hedges where possible and derivatives where necessary.

The regulatory relationship remains complex but manageable. As infrastructure provider, Petronet operates under "common carrier" principles—providing non-discriminatory access to all users. Tariffs require regulatory approval, limiting pricing power but providing certainty. The company has mastered working within these constraints, optimizing returns through volume growth and operational efficiency rather than price increases.

ESG considerations, increasingly important for international investors, show mixed progress. The company's role in replacing coal with cleaner gas positions it well for energy transition. But methane leakage, though minimal, remains a concern. Petronet has committed to net-zero operations by 2035, investing in renewable energy for terminal operations and exploring carbon capture at industrial customer sites. Whether these efforts satisfy increasingly stringent ESG criteria remains uncertain.

Today's Petronet stands as validation of patient capital and strategic focus. The company that started with no assets now operates infrastructure valued at over ₹20,000 crores. The firm that imported its first cargo in 2004 now handles one-third of India's gas supply. The joint venture many predicted would fail due to promoter conflicts has delivered exceptional returns for two decades. As India pushes toward 15% gas in its energy mix by 2030, Petronet's infrastructure monopoly positions it at the center of this transformation—a privilege earned through execution, not granted by decree.

IX. The Qatar Renewal: Securing the Future (2023-2024)

The atmosphere in the conference room at India Energy Week in Goa was electric on February 6, 2024. Energy ministers, global CEOs, and industry veterans packed the venue, but all eyes focused on two men at the signing table: Qatar's Energy Minister Saad al-Kaabi and Petronet CEO A.K. Singh. After months of intense negotiations that nearly derailed over geopolitical tensions, they were about to sign one of the world's largest LNG contract extensions—a deal that would define Indo-Qatari energy relations for another generation.

The historic $78 billion deal extended LNG imports until 2048, with India saving approximately $0.8 per million British thermal unit at renewed terms, translating into savings of $6 billion over the contract period. The 7.5 million tonnes per annum would continue flowing, but everything else had changed. The price breakthrough alone justified years of patient negotiation—in an era of volatile energy markets, securing a long-term discount worth $6 billion showcased sophisticated commercial diplomacy.

The transition from FOB (Free on Board) to DES (Delivered Ex-Ship) terms represented more than technical detail—it was strategic realignment. Under the new agreement, LNG supplies would be made on delivered (DES) basis commencing from 2028 till 2048, meaning Qatar would now handle shipping. For Petronet, this eliminated shipping risk and vessel management complexity. For Qatar, it meant deploying its massive fleet strategically, optimizing global logistics. Both parties won.

The "rich" to "lean" gas transition unveiled another layer of complexity. In the revised contract, QatarEnergy would supply 'lean' gas stripped of ethane and propane, though Qatar would continue to supply 'rich' gas as long as they didn't have a facility to utilise ethane and propane. This accommodation reflected the delayed ONGC petrochemical complex at Dahej—a $4 billion project designed specifically for Qatar's ethane-rich gas. The flexibility shown by both parties demonstrated relationship depth beyond commercial transaction. The negotiation backdrop included unusual tension. There were heightened tensions when a Qatar court sentenced eight former Indian Navy officials to death in October 2023 for allegedly spying for Israel. In December-end, their sentence was commuted, and they were eventually released by February 2024, just as the LNG deal was being finalized. The timing wasn't coincidental—energy security and diplomatic relations intertwined in ways that transcended commercial contracts.

The strategic implications ran deeper than headlines suggested. The 20-year extension, securing energy supply till 2048, represented one of the longest-running LNG relationships globally. For India, targeting 15% gas in its energy mix by 2030, Qatar's commitment provided the foundation. For Qatar, facing competition from US shale gas and Australian projects, India's market—growing, stable, politically aligned—offered what spot markets couldn't: certainty.

The delivery flexibility built into the new agreement revolutionized logistics. Sources said the new deal would allow Indian buyers to decide which terminal in India would receive cargoes, unlike existing deals where Qatar delivered LNG only at Dahej. This freedom to decide on arrival terminals would result in additional savings in cost for transporting fuel through pipelines within the Indian grid—potentially hundreds of millions over the contract life.

The commercial terms, while confidential, revealed sophisticated structuring. The elimination of the fixed charge component (previously 52 cents per MMBtu) represented pure savings. The slope adjustment—though exact figures weren't disclosed—aligned pricing more closely with prevailing market conditions. Industry sources suggested the new formula incorporated Asian spot price indices alongside oil linkage, providing natural hedging against market dislocations.

Qatar's commitment extended beyond the main contract. The second deal for 1 million tonnes a year, entered into in 2015, would be negotiated separately, sources said. Additionally, Qatar agreed to help develop India's gas market through technical assistance for small-scale LNG, support for gas-based industries, and potential investment in downstream infrastructure. This wasn't just supplier-buyer relationship but strategic partnership.

The deal's structure addressed past problems elegantly. Take-or-pay provisions remained but with greater flexibility—allowing volume deferrals during market disruptions without penalties. Price review mechanisms were built in at five-year intervals, preventing the kind of crisis that occurred in 2015-2016. Crucially, both parties committed to dispute resolution through negotiation rather than arbitration, reflecting relationship maturity.

For Petronet, the renewal validated its business model. Despite new terminals coming up, despite spot market growth, the company's Qatar relationship remained irreplaceable. The deal guaranteed baseload volumes through 2048, providing revenue visibility that few infrastructure companies enjoy. It also positioned Petronet as India's primary gas infrastructure provider for another generation—a moat that competitors couldn't cross.

The signing ceremony concluded with Minister al-Kaabi's words: "We are here to serve the market in India and we hope to be part of the expansion of the economy and requirements and the energy sector." Behind diplomatic language lay commercial reality: Qatar needed India's growing market as much as India needed Qatar's reliable supply. The renewal wasn't just extending a contract—it was cementing an energy alliance that would shape both nations' futures through mid-century.

X. Playbook: Business & Strategic Lessons

Walk into any business school case discussion on infrastructure investing, and Petronet's story challenges conventional wisdom at every turn. The company shouldn't exist—four competing state-owned companies don't typically create successful joint ventures. It shouldn't dominate—infrastructure built by committee rarely achieves operational excellence. It shouldn't be profitable—regulated utilities with government oversight rarely generate 20% returns on equity. Yet Petronet did all three. Understanding how reveals lessons that transcend sectors and geographies.

The Infrastructure Monopoly Playbook emerges as Petronet's core strategic insight. In capital-intensive sectors, being first isn't just an advantage—it's often insurmountable. Petronet didn't just build terminals; it created the entire ecosystem. Every pipeline that connects to Dahej, every customer relationship built over two decades, every operational protocol developed through trial and error—these form compound moats. A competitor can build a terminal in three years and $500 million. They cannot build twenty years of embedded infrastructure and relationships.

Consider the network effects at play. Shipping companies schedule around Dahej's slots because that's where cargo consolidation happens. Pipeline companies prioritize connections to Petronet facilities because that's where supply certainty exists. Customers prefer Petronet not from loyalty but from liquidity—multiple suppliers and buyers create spot markets within terminals. Each additional user strengthens the network, raising switching costs for existing users. It's Facebook for molecules—the value isn't the platform but the network.

The PSU Consortium Model offers counterintuitive lessons about risk-sharing and political alignment. Conventional wisdom suggests that multiple government stakeholders create bureaucratic paralysis. Petronet proved the opposite—when structured correctly, PSU partnerships can move faster than solo ventures. The key was aligned incentives: each promoter contributed what it did best (GAIL's pipelines, IOC's marketing, ONGC's technical expertise, BPCL's operations) while sharing risks equally. Board decisions required consensus, forcing collaboration over competition. When conflicts arose—and they did frequently—shared ownership ensured compromise rather than deadlock.

The political economy dimension proved crucial. Having four major PSUs as promoters meant Petronet had champions across ministries. When environmental clearances were needed, when land acquisition faced challenges, when regulatory approvals got stuck—there was always a promoter with the right connections to unlock bottlenecks. This wasn't corruption but coordination—aligning stakeholder interests to achieve national objectives.

Long-term Contracting in Volatile Markets showcases sophisticated risk management. Petronet's Qatar contract, signed when India had zero LNG infrastructure, seemed recklessly risky. Yet it worked because both parties understood they were trading different risks. Qatar wanted volume certainty and relationship stability—it got 25-year commitments from a creditworthy buyer. India wanted supply security and price predictability—it got guaranteed volumes with formulaic pricing. When markets shifted dramatically (oil at $147, then $26), both parties renegotiated rather than litigated, preserving long-term value over short-term gain.

The lesson extends beyond energy: in volatile markets, successful long-term contracts require mechanisms for adaptation. Petronet's agreements included price reviews, volume flexibility, force majeure provisions—safety valves that prevented contracts from breaking under stress. More importantly, relationships mattered more than contracts. When spot prices crashed in 2015, Qatar could have enforced take-or-pay provisions for billions. Instead, it renegotiated, understanding that preserving the India relationship mattered more than maximizing immediate returns.

The Tolling Business Model represents financial engineering brilliance. Petronet doesn't buy and sell gas—it charges fees for regasification services. This means the company makes money whether gas costs $3 or $30 per MMBtu. Revenue depends on volume, not price. Margins stay consistent regardless of commodity cycles. For equity investors seeking growth, this model seems boring—no windfall profits during price spikes. For debt investors and long-term shareholders, it's beautiful—predictable cash flows that compound over decades.

The model's elegance extends to risk allocation. Commodity price risk sits with traders and end-users who can hedge or pass through costs. Volume risk is managed through take-or-pay contracts and diversified customer base. Credit risk is minimized through upfront payments and letters of credit. Operational risk, the only risk Petronet truly owns, is managed through world-class maintenance and redundancy. It's risk unbundling at its finest—each party bears the risks they're best equipped to manage.

Network Effects in Infrastructure deserve special attention. Unlike software where network effects are obvious, infrastructure network effects are physical and permanent. Every pipeline connected to Dahej increases the terminal's value. Every customer added expands the market for all users. Every operational improvement—faster unloading, lower boil-off, better scheduling—benefits the entire ecosystem. These effects compound: a terminal with 100 users is more than 10 times as valuable as one with 10 users.

The competitive implications are profound. New terminals can offer lower prices, better service, newer technology—and still fail to attract customers. Why? Because customers value ecosystem access over terminal features. It's why Mundra terminal, despite being privately operated with competitive pricing, captures a fraction of Petronet's volume. Infrastructure monopolies aren't built through regulation or protection but through network density that becomes self-reinforcing.

Government Relations as Core Competency might seem like rent-seeking, but Petronet demonstrates legitimate value creation through regulatory navigation. The company doesn't lobby for protection but for policy clarity. It works with regulators to develop safety standards, environmental protocols, pricing mechanisms that balance stakeholder interests. This collaborative approach—unusual for infrastructure companies that often fight regulators—created trust that translated into operational flexibility.

Consider how Petronet handled the transition to "common carrier" status, where it must provide non-discriminatory third-party access. Rather than resist, Petronet embraced the model, recognizing that more users meant better utilization, stronger network effects, and ultimately higher returns despite regulated tariffs. It's judo strategy—using regulatory force to strengthen competitive position.

International Partnerships Beyond Transactions shaped Petronet's evolution from importer to strategic player. The Qatar relationship transcended commercial contract—it became energy diplomacy. Technical partnerships with Japanese companies provided expertise while maintaining Indian control. Collaboration with international engineering firms transferred knowledge while building domestic capability. Each partnership was structured for mutual benefit rather than one-sided extraction.

The meta-lesson is that infrastructure businesses are ultimately relationship businesses. Technology can be bought, capital can be raised, assets can be built—but relationships that enable complex projects in challenging environments take decades to develop. Petronet's success came not from any single advantage but from weaving together relationships—with government, suppliers, customers, communities—into a network that became its ultimate moat.

XI. Analysis & Investment Case

The numbers tell a compelling story, but not the one most investors expect. Petronet trades at a market capitalization of $5.43 billion against trailing revenues of $6.03 billion—seemingly reasonable for an infrastructure utility. Dig deeper, and contradictions emerge. EBITDA margins consistently exceed 50%, extraordinary for capital-intensive infrastructure. Return on equity hovers around 20%, double typical utility returns. Yet the stock trades at just 15 times earnings, a discount to both Indian markets and global LNG peers. This valuation disconnect reveals both opportunity and complexity in understanding Petronet's investment case.

The Promoter Structure creates unique dynamics. With PSU promoters holding 50% and effectively controlling the company, minority shareholders ride along on decisions made for strategic rather than purely financial reasons. This isn't necessarily negative—PSU ownership provides political support and business stability—but it means traditional activist strategies won't work. You're buying into India's energy strategy as much as Petronet's business model.

The promoter overhang occasionally creates opportunities. When ONGC or IOC face fiscal pressure, market fears of stake sales pressure Petronet's stock despite no fundamental impact. Conversely, when government announces gas infrastructure initiatives, Petronet benefits from policy tailwinds regardless of direct impact. Understanding these dynamics—reading between ministry announcements and PSU board meetings—becomes crucial for timing entry and exit.

Competitive Positioning appears unassailable, but requires nuance. Petronet's 75% market share in LNG imports seems dominant, yet this understates true competitive strength. The company doesn't just have market share—it has infrastructure lock-in. Dahej's 17.5 MMTPA capacity is fully contracted through 2030. Pipeline connections, customer relationships, operational expertise—these create switching costs that market share statistics don't capture.

New competition faces brutal economics. Building a greenfield terminal requires $500-700 million investment, 3-4 year construction, environmental clearances, and pipeline connectivity. Even then, utilization depends on securing anchor customers who are mostly locked into long-term contracts with Petronet. It's telling that despite India's gas demand growing 50% since 2015, Petronet's market share has declined only marginally. The pie grew faster than competitors could bite.

Yet disruption risks exist. Floating storage and regasification units (FSRUs) offer faster, cheaper deployment than onshore terminals. Small-scale LNG technology enables distribution without pipeline infrastructure. Green hydrogen could eventually displace natural gas in certain applications. None of these threats are immediate, but they highlight that Petronet's moat, while deep, isn't eternal.

Growth Drivers remain robust despite the company's maturity. India's gas consumption is projected to grow from 65 BCM currently to 103 BCM by 2030, driven by fertilizer demand, city gas distribution expansion, and industrial fuel switching. Even maintaining current market share would mean 60% volume growth for Petronet. But the real opportunity lies in infrastructure expansion—the planned Andhra Pradesh terminal, capacity additions at existing facilities, and value-added services.

The economics of expansion are compelling. Brownfield capacity additions at Dahej cost roughly $30-40 million per MMTPA versus $100+ million for greenfield capacity. With established operations and existing infrastructure, incremental returns on invested capital exceed 30%. It's the infrastructure equivalent of software—high upfront costs but near-zero marginal costs for additional capacity.

City gas distribution represents an underappreciated catalyst. As India expands piped gas to 300+ districts, Petronet becomes the essential supply backbone. Each new CNG station, each household connection, each industrial conversion increases baseload demand for Petronet's infrastructure. The company doesn't need to win these customers—it serves whoever serves them.

Key Risks cluster around three themes: regulatory, market, and transition. Regulatory risks include potential tariff cuts, though history suggests regulators balance consumer interests with infrastructure viability. Market risks center on global LNG oversupply pressuring volumes and margins, though Petronet's tolling model provides insulation. Transition risks—India's renewable ambitions, hydrogen economy development—represent long-term challenges to gas demand itself.

The China precedent offers sobering perspective. China's gas demand grew 4x from 2005-2020, yet terminal operators saw margins compress as competition intensified and government prioritized energy security over returns. Could India follow similar trajectory? Possibly, but India's fragmented market structure and Petronet's embedded position provide better protection than Chinese peers enjoyed.

Currency exposure deserves attention. With revenues in rupees but significant costs dollar-denominated, rupee depreciation pressures margins. Petronet hedges tactically but doesn't eliminate currency risk entirely. A sharp rupee depreciation—always possible given India's current account dynamics—could temporarily pressure profitability despite operational strength.

The Investment Thesis crystallizes around three pillars. First, Petronet offers leveraged exposure to India's structural shift toward gas—if gas reaches 15% of energy mix by 2030 as targeted, Petronet's volumes could double. Second, the infrastructure monopoly generates predictable, high-margin cash flows that compound over decades—boring but beautiful for long-term investors. Third, the Qatar contract extension through 2048 provides visibility rare in commodity-linked businesses.

Valuation suggests modest expectations despite strong fundamentals. At 15x P/E, markets price Petronet like a utility despite returns resembling a specialty chemical company. The 4% dividend yield provides income while waiting for rerating. Most importantly, replacement cost exceeds market capitalization—you're buying $8 billion of irreplaceable infrastructure for $5.4 billion market cap.

The intelligent investor recognizes Petronet isn't a trade but a holding. The company won't double overnight on earnings beats or acquisition announcements. Instead, it will compound steadily as India's gas consumption grows, as infrastructure utilization improves, as competitive moats deepen. It's a widow-and-orphan stock disguised as an energy play—precisely the kind of misunderstanding that creates opportunity.

For those worried about stranded asset risk from energy transition, consider this: even aggressive renewable scenarios show gas demand growing through 2040 as backup for intermittent solar and wind. Petronet's infrastructure has 20+ year economic life remaining. By the time hydrogen or other alternatives threaten gas demand, today's investors will have collected decades of dividends and capital appreciation. Sometimes the best investments aren't about catching the future but monetizing the present.

XII. Future Outlook & Strategic Options

Standing at Dahej terminal's control room, gazing at expansion plans spread across the conference table, Petronet's leadership faces choices that will define the company's next chapter. India's stated ambition—increasing gas from 6% to 15% of energy mix by 2030—implies tripling consumption. Even capturing current market share means massive growth. But the strategic questions run deeper: How does Petronet evolve from infrastructure operator to energy transition enabler? Can it replicate its LNG success in emerging fuels? Should it remain focused or diversify?

India's Gas Ambition provides the fundamental growth backdrop. The numbers are staggering: current consumption of 65 BCM must reach 200 BCM for 15% energy share. That requires 5-6 new LNG terminals, thousands of kilometers of pipelines, hundreds of city gas networks. Petronet sits at the center of this expansion, not just as beneficiary but as enabler. Every policy announcement, every infrastructure project, every industrial conversion strengthens Petronet's position.

Yet execution challenges loom large. India's pipeline network remains fragmented—the proposed National Gas Grid exists mostly on paper. State-level politics complicate right-of-way acquisition. Regulated gas prices for fertilizer and power create market distortions. Most critically, at $10+ per MMBtu, imported LNG remains expensive versus coal for power generation and industry. Without policy support—carbon pricing, pollution penalties, gas mandates—the 15% target appears aspirational.

Expansion Plans reveal strategic priorities. The third terminal with 5 million tons capacity in Andhra Pradesh, targeting India's eastern and southern markets underserved by existing infrastructure, could commence by 2027. Unlike Dahej and Kochi, this facility would incorporate latest technology—floating storage options, small-scale distribution capabilities, potential hydrogen compatibility. The location offers access to industrial clusters transitioning from coal while serving growing city gas networks.

But the real expansion happens at existing terminals. Dahej's capacity could reach 22.5 MMTPA through brownfield additions. Kochi, finally achieving decent utilization after pipeline connectivity, could double capacity. These expansions offer 30%+ returns on capital—far exceeding new terminal economics. It's the infrastructure equivalent of software updates—leveraging existing assets for marginal growth.

The Hydrogen Economy presents both opportunity and threat. Green hydrogen, produced from renewable electricity via electrolysis, could eventually replace natural gas in many applications. But "eventually" means decades, and meanwhile, blue hydrogen—produced from natural gas with carbon capture—offers transition opportunity. Petronet's terminals could handle hydrogen with modifications, its customer relationships provide distribution channels, its operational expertise translates across gases.

The company's hydrogen strategy remains nascent but pragmatic. Rather than massive upfront investment, Petronet focuses on hydrogen-readiness—ensuring new infrastructure can handle hydrogen blending, partnering with technology providers for pilot projects, maintaining optionality without betting the company. It's strategic hedging at its finest—positioned to benefit if hydrogen scales while not dependent on it.

International Expansion offers growth beyond India's borders. Sri Lanka represents immediate opportunity—the island nation needs LNG infrastructure but lacks capital and expertise. Petronet's proposed joint venture would replicate its India model: build terminal, secure supply, develop market. Bangladesh, Vietnam, Myanmar offer similar possibilities. The playbook is proven; the question is execution in different regulatory and political environments.

Yet international expansion carries risks Petronet hasn't faced domestically. Currency exposure multiplies, political risk escalates, operational complexity compounds. The company's conservative approach—joint ventures with local partners, government-to-government agreements, limited capital commitment—suggests recognition of these challenges. Petronet won't become a global player overnight, but selective expansion could provide growth as Indian infrastructure matures.

Technology Evolution shapes competitive dynamics. Small-scale LNG technology enables distribution without pipelines, reaching customers previously uneconomical to serve. Petronet's truck loading facilities at both terminals position it to capture this market. Floating terminals offer faster deployment and lower capital intensity—Petronet's expertise could translate to FSRU operations. Virtual pipeline networks using ISO containers could extend Petronet's reach without physical infrastructure.

Digital transformation, often overlooked in infrastructure discussions, offers efficiency gains. Predictive maintenance using IoT sensors and AI could reduce operating costs 10-15%. Blockchain-based documentation could accelerate cargo handling. Dynamic pricing algorithms could optimize capacity utilization. These aren't revolutionary changes but incremental improvements that compound over time—exactly the kind of advantages that strengthen infrastructure moats.

Climate Transition represents existential question marks. Natural gas, marketed as "bridge fuel" between coal and renewables, faces increasing scrutiny. Methane leakage negates climate benefits if not controlled. Renewable electricity plus battery storage increasingly competes with gas peaking plants. Carbon border adjustments could penalize gas imports. The comfortable narrative of gas as climate solution grows more complex.

Petronet's response emphasizes gas's role in reliable, affordable energy transition. Intermittent renewables need backup; batteries remain expensive for long-duration storage; hydrogen infrastructure will take decades to develop. Meanwhile, gas can immediately replace coal in industry and diesel in transport, delivering emission reductions today rather than tomorrow. It's pragmatic argument that resonates in India where development needs trump climate ambition.

Strategic Options crystallize around three scenarios. The "focused expansion" path doubles down on LNG infrastructure—more terminals, greater capacity, deeper market penetration. The "energy platform" path diversifies into adjacent molecules—hydrogen, ammonia, methanol—leveraging infrastructure and relationships. The "integrated energy" path moves downstream—power generation, petrochemicals, industrial parks—capturing more value chain.

Each path offers different risk-return profiles. Focused expansion provides highest probability of success but potentially limited upside as market matures. Energy platform offers optionality for emerging fuels but requires capabilities Petronet hasn't demonstrated. Integrated energy promises higher margins but demands capital and expertise beyond current competencies. The likely outcome combines elements of all three—pragmatic expansion with selective diversification.

The meta-question facing Petronet is whether to remain infrastructure utility or become energy major. The company's history suggests conservative evolution rather than revolutionary transformation. But India's energy transition demands ambition beyond incrementalism. Can a PSU-promoted joint venture demonstrate entrepreneurial agility? Can operational excellence translate to strategic innovation? Can Petronet reinvent itself as it reinvented India's gas market?

The answer lies partly in governance evolution. New independent directors bring international expertise and fresh perspectives. Professional management gains autonomy from promoter interference. Performance metrics shift from volume to value creation. Employee stock options align long-term incentives. These seem like minor adjustments, but they could unlock potential that structure currently constrains.

Looking ahead to 2030 and beyond, Petronet's future seems secure but not spectacular. The company will grow with India's gas market, generate steady returns, pay reliable dividends. For investors seeking excitement, this disappoints. For those understanding infrastructure economics, it's exactly the predictable compound return that builds wealth. Petronet won't be the next technology unicorn, but it might be something rarer—a boring business that quietly becomes indispensable to India's energy future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube