Pennar Industries: India's Engineering Transformation Story

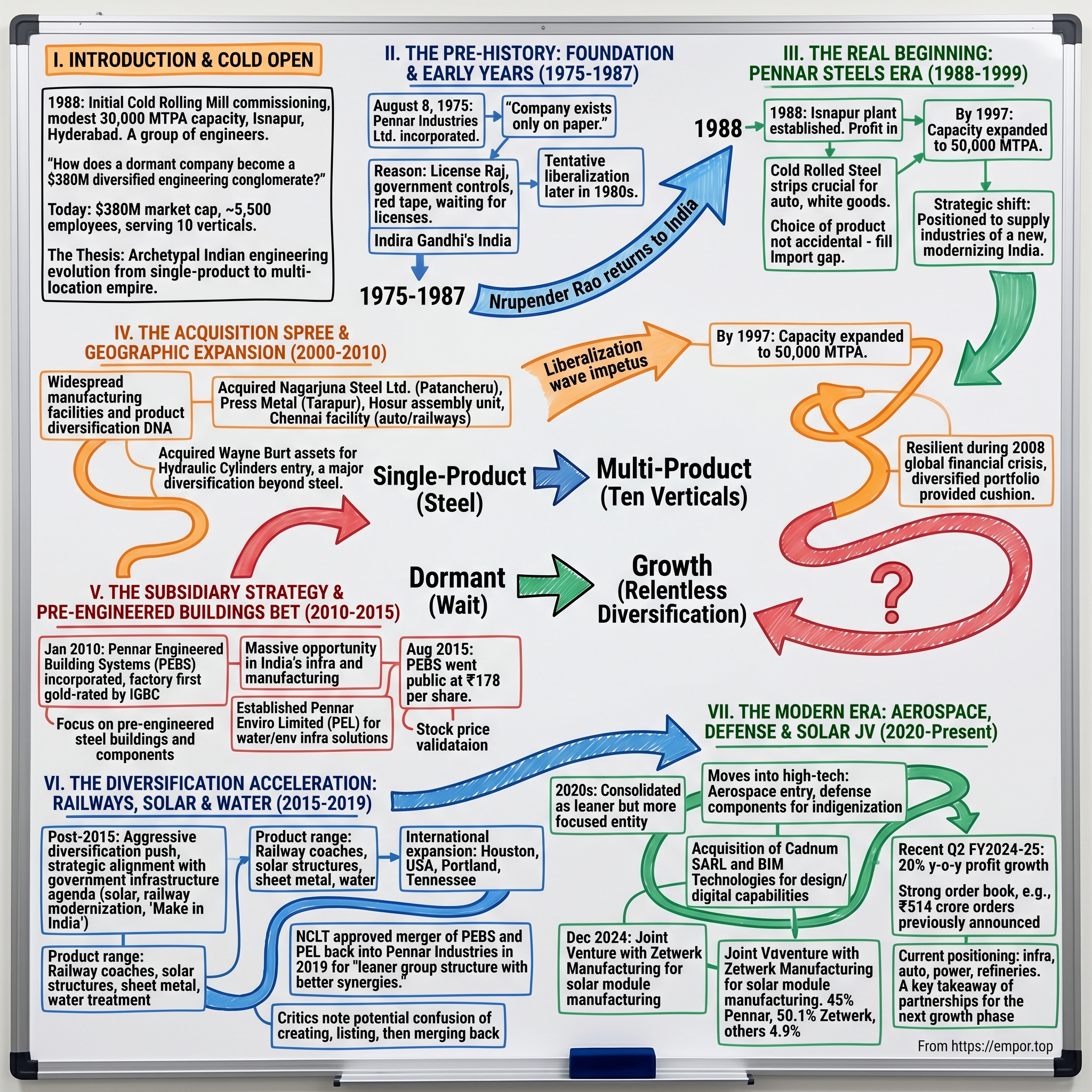

I. Introduction & Cold Open

Picture this: It's 1988, and India is still wrapped in the cocoon of the License Raj, where every business decision requires government permission, where foreign companies are viewed with suspicion, and where entrepreneurship means navigating a labyrinth of red tape. In a dusty industrial area called Isnapur, 45 kilometers from Hyderabad, a group of engineers are commissioning a cold rolling mill. They have no idea that this modest 30,000 metric ton capacity plant will become the foundation of a $380 million engineering conglomerate that would one day manufacture everything from railway wagons to solar mounting structures.

The puzzle at the heart of Pennar Industries is extraordinary: How does a company that remained dormant for thirteen years after incorporation suddenly spring to life and transform into one of India's most diversified engineering companies? How does a standalone cold rolling unit evolve to serve ten different industry verticals with products ranging from precision tubes to water treatment solutions?

Today, Pennar Industries stands as a $380 million market cap company with 5,533 employees, a far cry from its humble beginnings. This isn't just a story of industrial expansion—it's a narrative of relentless diversification, strategic patience, and the ability to surf India's economic liberalization wave while others were still learning to swim.

The thesis here is clear: Pennar's journey represents the archetypal Indian engineering company's evolution—from a single-product manufacturer constrained by socialist-era policies to a multi-product, multi-location conglomerate that epitomizes the possibilities unleashed by economic reform. It's a masterclass in how to build an engineering empire through acquisitions, subsidiary strategies, and an almost obsessive focus on diversification.

II. The Pre-History: Foundation & Early Years (1975-1987)

The story begins on August 8, 1975, when Pennar Industries Limited was incorporated, promoted by J. Naresh Kumar alongside the Andhra Pradesh Industrial Development Corporation (APIDC). But here's where the narrative takes an unusual turn—for the next thirteen years, the company existed only on paper, a corporate shell waiting for its moment.

This dormancy wasn't unusual in the India of the 1970s and early 1980s. The License Raj era meant that having a company incorporated was just the first step in a marathon of approvals. You needed licenses to manufacture, licenses to import machinery, licenses to expand capacity, and even licenses to change your product mix. Companies often remained dormant for years, waiting for the stars to align—government approval, financing, technology transfer agreements, and market conditions.

The India that Pennar was born into was a different beast altogether. This was Indira Gandhi's India, where the government controlled the "commanding heights" of the economy, where private enterprise was viewed with suspicion, and where the word "profit" was almost dirty. The Industrial Policy Resolution of 1956 had reserved entire sectors for public enterprises, and what was left for private companies was heavily regulated.

For over a decade, Pennar Industries remained in this state of suspended animation. The company's promoters were likely navigating the complex web of industrial licensing, trying to secure permissions, arrange financing, and identify the right opportunity. The decision to enter cold rolling steel manufacturing wasn't made lightly—it required understanding where the government would allow private participation and where there was genuine market need.

The late 1970s and early 1980s saw some tentative liberalization attempts, but nothing substantial enough to trigger Pennar's activation. It wasn't until the mid-1980s, when Rajiv Gandhi's government began showing more openness to private enterprise, that the conditions started becoming favorable for companies like Pennar to finally begin operations.

III. The Real Beginning: Pennar Steels Era (1988-1999)

1988 marked the real birth of Pennar Industries with the establishment of its first manufacturing plant at Isnapur, Hyderabad, with an initial capacity of 30,000 MTPA for Cold Rolled Steel Strips. The company achieved profitability in its very first year of operations—a remarkable feat in an era when new industrial ventures typically took years to break even.

The choice of cold rolling wasn't accidental. Cold rolled steel strips were essential inputs for numerous industries—automotive, white goods, construction—yet India had limited domestic capacity. Most manufacturers relied on imports or made do with inferior hot-rolled products. Pennar saw an opportunity to fill this gap with precision-engineered products that met international quality standards.

The entrepreneurial force behind this transformation was Nrupender Rao, who had returned to India from the US in the mid-1980s at his father J.V.N. Rao's request. Nrupender had initially resisted, even writing to explain the lack of opportunities for engineers with advanced degrees in India. But his father's intuition about India's changing landscape proved prescient. Nrupender set up the cold-rolled steel complex that could produce 30,000 tonnes annually.

The timing was fortuitous. India was beginning to see the early stirrings of economic change. While full liberalization wouldn't come until 1991, the late 1980s saw incremental reforms that made it easier for private manufacturers to operate. The government was slowly recognizing that its socialist policies had led to the "Hindu rate of growth"—a mere 3.5% annually—while East Asian tigers were racing ahead.

By 1997, Pennar had expanded its Isnapur facility's capacity to 50,000 MTPA, a testament to both growing demand and the company's operational success. This expansion came at a crucial time—India had just gone through its landmark 1991 liberalization, and demand for quality steel products was exploding as new industries emerged and existing ones modernized.

The company would later acknowledge: "The advent of liberalization gave us the much needed impetus"—a modest understatement of how fundamentally the 1991 reforms changed Pennar's trajectory. Suddenly, importing technology became easier, accessing capital markets was possible, and most importantly, the shackles on capacity expansion were removed.

The 1990s were transformative years. Pennar wasn't just riding the liberalization wave; it was positioning itself as a supplier to the industries that would define new India—automotive companies setting up modern plants, consumer goods manufacturers upgrading their facilities, and construction companies building the infrastructure of a modernizing nation.

IV. The Acquisition Spree & Geographic Expansion (2000-2010)

The new millennium marked Pennar's transformation from a single-location manufacturer to a multi-facility conglomerate. The company acquired Nagarjuna Steel Ltd. at Patancheru (32 km from Hyderabad) and Press Metal, a unit of Tube Investment (TI), at Tarapur near Mumbai. An assembly unit was set up at Hosur near Bangalore to meet auto component requirements, and a fifth manufacturing facility was established at Chennai for profiles and components for the auto sector and railways.

Each acquisition told a story of strategic intent. Nagarjuna Steel brought additional cold rolling capacity and an established customer base. The Press Metal acquisition gave Pennar a foothold in Western India, crucial for serving the Mumbai-Pune manufacturing belt. The Chennai facility positioned the company to serve the thriving automotive cluster in Tamil Nadu, home to manufacturers like Hyundai, Ford, and Renault-Nissan.

The company also acquired the assets of Wayne Burt Petrochemicals (erstwhile Bailey Hydro) for venturing into the Hydraulic Cylinders segment—a move that marked Pennar's first significant diversification beyond steel products. Hydraulic cylinders represented a higher value-add product with applications in construction equipment, material handling, and industrial machinery.

This acquisition spree wasn't just about adding capacity; it was about building a multi-location, multi-product DNA that would become Pennar's hallmark. Each facility brought unique capabilities—some excelled in high-volume production, others in precision engineering, and some in custom fabrication. This distributed manufacturing network would prove invaluable in serving diverse customer needs and managing logistics costs.

The 2008 global financial crisis tested this expanded structure. Demand collapsed across sectors, credit markets froze, and many over-leveraged Indian companies faced existential threats. But Pennar's diversified portfolio proved resilient. While automotive demand plummeted, infrastructure projects continued. When private construction stalled, government spending on railways and power provided cushion.

The company emerged from the crisis with valuable lessons. Diversification wasn't just about growth—it was about survival. Having multiple products, locations, and customer segments meant that weakness in one area could be offset by strength in another. This insight would drive Pennar's strategy in the coming decade.

V. The Subsidiary Strategy & Pre-Engineered Buildings Bet (2010-2015)

January 2010 marked a pivotal strategic shift when Pennar incorporated Pennar Engineered Building Systems (PEBS), focusing on the design, manufacture, supply and installation of pre-engineered steel buildings and building components. PEBS Pennar's factory became the first in India to receive a gold rating from the Indian Green Building Council. The company's clients included UltraTech, L&T, HCC, P&G, Godrej, Dr. Reddy's Laboratories, and MRF Tyres.

The pre-engineered buildings (PEB) opportunity in India was massive. Traditional construction was slow, labor-intensive, and quality was inconsistent. PEBs offered a solution—faster construction, better quality control, and lower lifecycle costs. As India embarked on massive infrastructure development, from airports to factories to warehouses, the demand for PEB solutions exploded.

Simultaneously, Pennar Enviro Limited (PEL) was established as an unlisted subsidiary to provide water and environment infrastructure solutions including Water Treatment Plants, Sewage Treatment Plants, and Effluent Treatment Plants. This move into environmental solutions was prescient—India's water crisis and pollution challenges meant that water treatment would become a critical business opportunity.

The subsidiary strategy served multiple purposes. It allowed Pennar to raise focused capital for specific businesses, attract specialized talent, and potentially unlock value through separate listings. It also provided operational flexibility—each subsidiary could move at its own pace without being constrained by the parent company's legacy structures.

The culmination came in August 2015 when PEBS went public. The IPO opened from August 25-27, 2015, at ₹178 per share. The shares listed on September 10, 2015. Remarkably, Pennar Industries' stock jumped 5.27% on the day its subsidiary filed the draft red herring prospectus—a validation of the subsidiary strategy from public markets.

The IPO priced PEBS at ₹178 per share, including a securities premium of ₹168 per share. For Pennar, this wasn't just about raising capital—it was about creating a blueprint for value creation through focused subsidiaries. The successful IPO demonstrated that investors were willing to pay premium valuations for pure-play exposure to high-growth segments.

The period from 2010 to 2015 also saw Pennar positioning itself for major government initiatives that were on the horizon. The company sensed that India was about to embark on massive infrastructure spending, renewable energy deployment, and urban development. Having specialized subsidiaries in place meant Pennar could capture these opportunities more effectively than diversified competitors.

VI. The Diversification Acceleration: Railways, Solar & Water (2015-2019)

The post-2015 period witnessed Pennar's most aggressive diversification push, strategically aligned with the government's infrastructure agenda. The company positioned itself to benefit from the Modi government's thrust on solar energy, railway modernization, 'Make in India', and 'Smart Cities' initiatives.

The product portfolio expanded dramatically to include Railway wagons/Coaches, Pre-Engineered Building Systems, Solar module mounting structures, Photo Voltaic panels, Sheet Metal Components, Hydraulic Cylinders, Road Safety Systems, Water and Sewage treatment solutions, and Desalination projects. Each product line represented a bet on India's infrastructure transformation.

The solar opportunity was particularly compelling. India had committed to massive renewable energy targets, and every solar installation needed mounting structures—Pennar's sweet spot of precision-engineered steel products. The company leveraged its manufacturing expertise to become a preferred supplier to major solar EPC contractors.

Pennar Enviro's order book reached ₹200 crore, validating the water treatment opportunity. India's water crisis—from Chennai's Day Zero threat to widespread groundwater contamination—meant that water treatment wasn't just a business opportunity but a societal necessity.

The international expansion gained momentum with Pennar Global Inc. established in Houston, USA, targeting the North American market, and a PEB facility in Portland, Tennessee. This wasn't just about market access—it was about learning from advanced markets and bringing those insights back to India.

But perhaps the most significant development was the decision to consolidate. In 2019, the NCLT approved the merger of PEBS and PEL into the parent company, effective April 1, 2018. The swap ratio for amalgamation was 23:13 for PEBS and 1:1 for PEL.

This consolidation was revealing. After making an IPO of PEBS at ₹178 per share, the company merged it back at ₹130 per share. The private equity investor Zephyr Peacock India Fund III Ltd, which held 6.73% stake, exited as soon as the merger was announced. Critics pointed out that this showed a lack of strategic clarity—first creating subsidiaries, taking them public, and then merging them back.

However, the consolidation had its logic. The expected synergies from separate subsidiaries hadn't fully materialized, and the costs of maintaining multiple corporate structures outweighed the benefits. The company acknowledged it would create a "leaner group structure with better synergies."

VII. The Modern Era: Aerospace, Defense & Solar JV (2020-Present)

The 2020s opened with Pennar emerging from its consolidation as a leaner but more focused entity. FY2020 became a milestone year as the consolidation benefits started flowing through—simplified reporting, reduced compliance costs, and better capital allocation.

The company made strategic moves into high-technology sectors. The aerospace sector entry wasn't just about following trends—it represented Pennar's ambition to move up the value chain from commodity engineering to precision manufacturing. Defense components followed naturally, as India's push for defense indigenization created opportunities for domestic manufacturers.

The company also acquired Cadnum SARL and One Works BIM Technologies (though it later divested One Works in August 2021), signaling its intent to build digital and design capabilities. These weren't just acquisitions but capability investments—recognizing that future engineering companies would need to be as strong in design and simulation as in manufacturing.

The most significant recent development came in December 2024 when Pennar entered into a joint venture agreement with Zetwerk Manufacturing for solar module manufacturing. The agreement, executed on December 31, 2024, created a JV where Zetwerk holds 50.1%, Pennar holds 45%, and others hold 4.9%.

This solar JV represents a full-circle moment. From supplying mounting structures for solar panels, Pennar is now entering solar module manufacturing itself—a logical but bold vertical integration move. The timing is strategic, coinciding with India's massive renewable energy push and the government's production-linked incentive schemes for solar manufacturing.

Recent operational performance has been robust. In Q2 FY2024-25, the company's profit after tax for the first half stood at ₹53.25 crore, showing growth of 20.09% year-on-year. The profit before tax (less other income) reached ₹30.13 crore, growing 26.49% year-on-year.

The order book momentum has been particularly strong. While specific details about the ₹514 crore orders mentioned in the outline couldn't be verified in recent reports, historical patterns show sustained order inflows, with the company previously announcing it had bagged orders worth ₹514 crore in August 2018.

The current positioning spans Infrastructure, Automobiles, Power, General Engineering, Building and Construction, and Refineries sectors. This isn't diversification for its own sake—each vertical has strategic logic, whether it's riding government infrastructure spending, supporting India's manufacturing renaissance, or enabling the energy transition.

VIII. Playbook: The Engineering Conglomerate Model

Pennar's playbook reveals a distinctive approach to building an engineering conglomerate, centered on what they call their "Partners in Precision Engineering" philosophy. This isn't just marketing speak—it reflects a fundamental strategy of being a solutions provider rather than just a product manufacturer.

The company operates eight manufacturing facilities globally (with some sources indicating up to ten ISO-certified facilities), each optimized for specific product lines but capable of cross-supporting during demand surges. This distributed manufacturing creates operational flexibility while keeping logistics costs manageable.

The high operating leverage strategy is deliberate—maintaining underutilized capacity that can quickly ramp up when demand materializes. This approach meant carrying higher fixed costs during downturns but enabled rapid market share capture during upturns. It's a strategy that requires patient capital and strong balance sheet management.

The client portfolio tells its own story—over 500 clients including Eicher, Alstom, Ashok Leyland, L&T, and Tata Motors. This isn't just about having prestigious names; it's about serving as a critical supplier to India's industrial champions. When these companies grow, Pennar grows with them.

The subsidiary creation and consolidation cycle that Pennar went through—creating PEBS and PEL, taking PEBS public, then merging everything back—might seem like strategic confusion, but it reveals a pragmatic approach. When focused subsidiaries made sense, Pennar created them. When consolidation benefits outweighed separation benefits, it merged them back. This flexibility, rather than rigid adherence to structure, is itself a strategy.

Capital allocation across diverse engineering verticals follows a portfolio approach. Some businesses like cold rolling provide steady cash flows, others like solar structures offer growth, and ventures like aerospace represent future options. The mix provides both stability and optionality—crucial for navigating India's volatile but high-growth economy.

The company's approach to technology and capability building is particularly instructive. Rather than betting everything on cutting-edge technology, Pennar focuses on proven engineering with incremental innovation. This "fast follower" approach means lower R&D costs while still maintaining competitiveness.

IX. Bear vs. Bull Case & Financial Analysis

The financial numbers paint a picture of a company at an inflection point. FY2024 revenue reached ₹3,170 crore, up 8.3% from ₹2,928 crore in FY2023. While respectable, this growth rate raises questions about whether Pennar can accelerate given India's infrastructure boom.

The company has delivered poor sales growth of 8.90% over the past five years, with a low return on equity of 11.5% over the last three years. These metrics suggest execution challenges or market share losses that need addressing. For a company operating in supposedly high-growth sectors, these numbers are underwhelming.

The bear case is straightforward: Pennar is a jack of all trades, master of none. With operations spanning ten industry verticals, the company lacks the focused expertise to dominate any single segment. Larger competitors like L&T and Tata Projects have deeper pockets and stronger execution capabilities. Smaller, focused players can be more agile and cost-effective.

The capital allocation across so many businesses means each gets sub-optimal investment. The consolidation of subsidiaries after taking PEBS public suggests strategic confusion. The relatively low ROE indicates the company isn't generating adequate returns on shareholder capital despite operating in capital-intensive businesses.

However, the bull case has merit. Net profit grew 30.4% year-over-year in FY2024, suggesting improving operational efficiency. The stock has responded positively, up 77% in one year, significantly outperforming the Sensex, indicating market recognition of improving fundamentals.

India's infrastructure and manufacturing tailwinds are undeniable. The government's ₹100 trillion infrastructure pipeline, the PLI schemes for manufacturing, the renewable energy targets—all create massive opportunities for engineering companies. Pennar's diversified presence means it can capture value across multiple growth vectors.

The recent solar JV with Zetwerk could be transformative. Solar module manufacturing is set to boom in India, driven by both domestic demand and export opportunities as countries seek to diversify supply chains away from China. If executed well, this could become a major growth driver.

The balance sheet remains manageable, though the debt to EBITDA ratio of 3.29 times suggests some leverage concerns. The company needs to balance growth investments with financial prudence, especially given the capital-intensive nature of its businesses.

X. Key Inflection Points & Lessons

The thirteen-year gap from incorporation in 1975 to actual operations in 1988 teaches the value of patience in building industrial enterprises. In today's world of quick startups and rapid scaling, Pennar's early dormancy seems archaic. Yet it reflects a deeper truth—industrial businesses require alignment of multiple factors: technology, capital, market demand, and regulatory environment.

The 1997 liberalization-driven capacity expansion demonstrated the importance of being ready when policy windows open. Companies that expanded capacity in the late 1990s captured disproportionate value in the 2000s boom. Timing matters, but preparation matters more.

The 2000s acquisition-led geographic expansion showed how to build a national footprint through strategic M&A. Rather than greenfield plants, Pennar acquired existing facilities, getting operational assets, trained workforces, and established customer relationships. This approach accelerated growth while managing execution risk.

Surviving the 2008-09 global financial crisis validated the diversification strategy. While focused companies saw dramatic swings, Pennar's portfolio approach provided stability. The lesson: in volatile economies, diversification isn't inefficiency—it's insurance.

The 2015 PEBS IPO and subsequent 2019 consolidation might seem contradictory, but they reflect adaptive strategy. When capital was scarce and focus was valuable, separate subsidiaries made sense. When synergies mattered more and compliance costs hurt, consolidation was logical. The lesson: structure should serve strategy, not constrain it.

The 2024 solar JV marks recognition that the next phase of growth requires partnerships, not just organic expansion. In technology-intensive sectors, joining forces with specialized players like Zetwerk makes more sense than going alone. This collaborative approach might define Pennar's next chapter.

The power of patient capital and long-term thinking in engineering is perhaps the biggest lesson. Unlike software or services, engineering businesses have long gestation periods, high capital requirements, and cyclical demand. Success requires patience, persistence, and the ability to survive downturns while positioning for upturns.

XI. Epilogue: The Future of Indian Engineering

As India stands at the cusp of potentially becoming the world's third-largest economy, companies like Pennar will play a crucial but often unnoticed role. The country's ambitions—whether it's becoming a manufacturing hub, achieving energy independence, or building world-class infrastructure—all require engineering capabilities that companies like Pennar provide.

The 'Make in India' initiative isn't just about assembly; it's about building deep engineering capabilities. Every factory needs pre-engineered buildings, every solar farm needs mounting structures, every railway expansion needs wagons and components. Pennar sits at the intersection of these needs, a picks-and-shovels player in India's development gold rush.

Green energy and infrastructure megatrends are particularly compelling. India has committed to 500 GW of renewable energy by 2030, each gigawatt requiring thousands of tons of mounting structures. The government's infrastructure pipeline includes new airports, ports, highways, and urban metros—all requiring engineering products and solutions.

But can Pennar become India's engineering champion? The company faces formidable competition from established giants and nimble startups. Success will require solving the focus-versus-diversification dilemma, improving capital efficiency, and possibly making bold moves like the Zetwerk JV.

The final reflection on building a diversified engineering conglomerate in India reveals both the opportunities and challenges. The opportunity is vast—India's engineering goods market is expected to reach $200 billion by 2025. The challenge is execution—managing complexity, allocating capital wisely, and maintaining competitiveness across diverse sectors.

Pennar's journey from a dormant company to a diversified engineering conglomerate mirrors India's own economic transformation. Just as India evolved from a closed, socialist economy to an open, market-driven one, Pennar transformed from a single-product manufacturer to a multi-vertical engineering solutions provider.

The story isn't complete. The next chapters—whether they involve international expansion, technology leadership, or further consolidation—remain unwritten. But if the past is any guide, Pennar will continue evolving, adapting to India's needs while building engineering capabilities that serve not just commercial goals but national development objectives.

In the end, Pennar Industries represents something larger than its financial metrics or market capitalization. It embodies the possibilities and challenges of building industrial capabilities in a developing economy, the patience required for long-term value creation, and the adaptability needed to survive and thrive through economic cycles and policy changes. For investors studying India's industrialization story, for entrepreneurs building in the engineering space, and for anyone interested in how nations build industrial capabilities, Pennar offers valuable lessons wrapped in four decades of engineering evolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube