PC Jeweller: The Glittering Rise and Spectacular Fall of India's Jewelry Chain

I. Introduction & Episode Roadmap

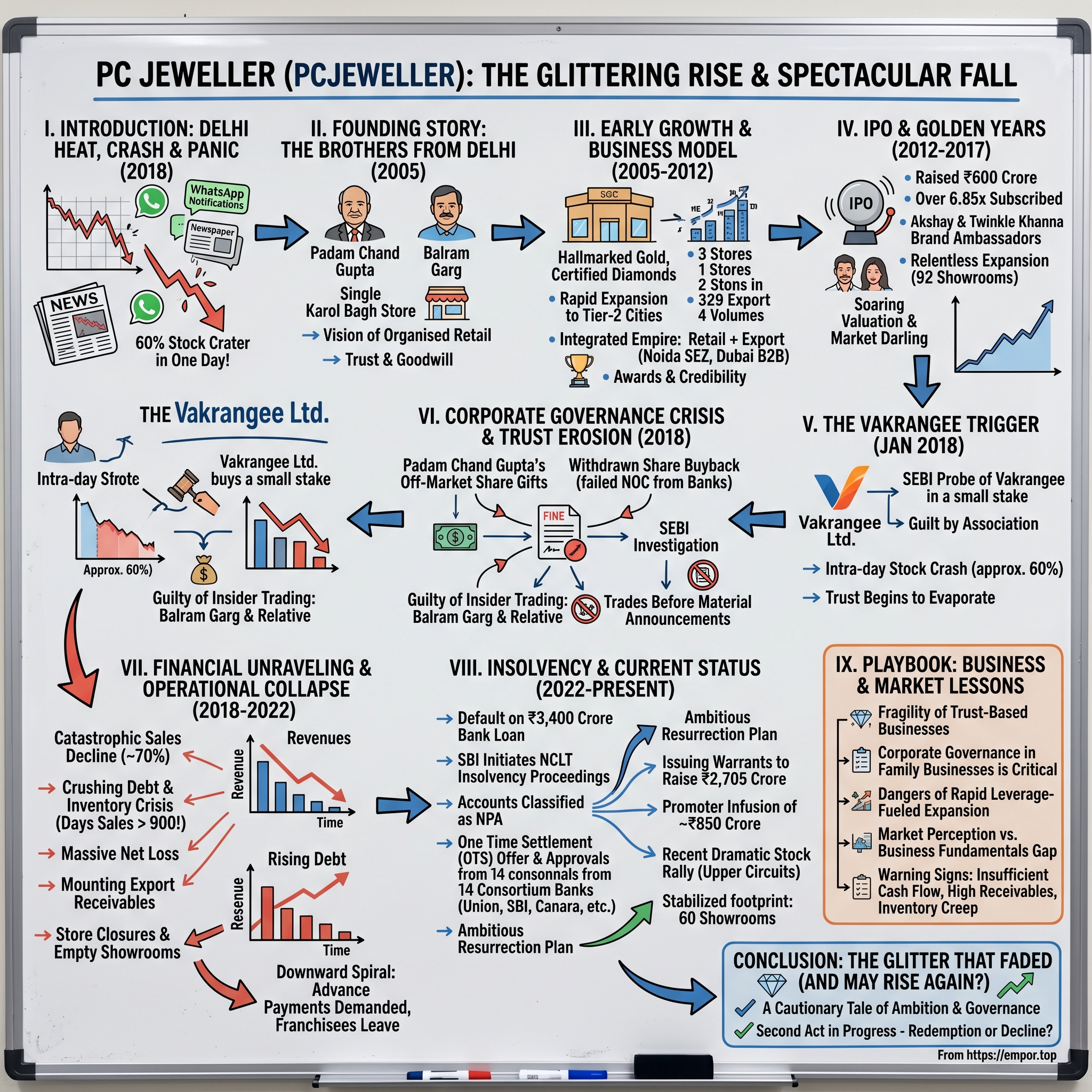

Picture this: A sweltering Delhi afternoon in 2018. Inside a gleaming PC Jeweller showroom in South Extension, customers browse gold necklaces and diamond rings, unaware that in Mumbai's financial district, the company's stock is cratering 60% in a single day. Within hours, WhatsApp groups of investors would buzz with panic, newspaper headlines would scream of corporate governance failures, and a jewelry empire built over 13 years would begin its spectacular unraveling. Between 2014 and 2018, PC Jeweller Limited transformed from a regional Delhi jewelry chain into one of India's stock market darlings, delivering returns that would make even the most aggressive venture capitalists envious. The stock rose dramatically—up 24.66% in three months, 63.20% in twelve months on the BSE, part of a multi-year bull run that saw the company's valuation soar to dizzying heights. Half a decade ago, this was the company every retail investor wanted in their portfolio.

But here's the central question that haunts this story: How did a single Karol Bagh store become an 80+ store empire worth billions, only to face insolvency proceedings initiated by State Bank of India over ₹3,400 crore in defaults? This is a tale of trust—the most precious commodity in the jewelry business—and how quickly it can evaporate. It's about rapid expansion fueled by debt, corporate governance that crumbled under scrutiny, and a spectacular fall that wiped out billions in market value.

The PC Jeweller saga encapsulates everything that can go wrong when a traditional family business scales rapidly in public markets without the governance infrastructure to match. It's Icarus, but with gold wings.

II. The Brothers from Delhi: Founding Story

The Karol Bagh neighborhood of Delhi has been a jewelry hub for generations, where gold merchants and craftsmen have plied their trade in narrow lanes filled with the glitter of precious metals. It was here, in April 2005, that two brothers decided to reimagine what Indian jewelry retail could become.

Padam Chand Gupta and Balram Garg weren't exactly newcomers to the trade—they came from a first generation business background. Prior to setting up PC Jeweller, the Gupta brothers were engaged in the family business of selling jewellery. But what set them apart was their vision: while most jewelers in 2005 operated from cramped shops with limited displays, the brothers imagined something grander.

Balram Garg named his new business PC Jeweller for his elder brother, Padam Chand Gupta—a gesture of respect that would later become ironic when corporate governance issues centered on the very same Padam Chand would trigger the company's downfall. But in 2005, this was simply two brothers with complementary skills: Padam Chand as the chairman with a 28% stake, and Balram as the managing director holding 36%.

"Mr. Garg's approach in business rests on his belief that nothing is impossible"—this wasn't just corporate speak. Balram Garg brought more than 30 years of experience in the jewellery industry to the venture. He understood something fundamental about the Indian jewelry market that was about to undergo a seismic shift.

In the early years, there was no concept of an organised player in the jewellery business. A jeweller would show you photos of rings or necklaces, perhaps a sample or two from his safe, but display was limited since inventory and investment were both limited. The brothers saw an opportunity in this chaos—the shift from unorganized to organized retail that was sweeping across India's consumer sectors.

"We developed our model based on customer psychology," Garg would later recall. That meant recognising that while customers will not hesitate to pay ₹10,000 or more for branded perfumes from just about any store, they won't do that with jewellery — they need reassurance that the store and seller aren't fly-by-night ventures.

"It is like operating a bank," Balram Garg would search for the perfect analogy. "Customers won't put their hard-earned cash just anywhere. Trust and goodwill can fill the coffers and the lack of these can empty them just as fast." This philosophy would prove prophetic—both in the company's meteoric rise and its eventual collapse.

The timing was perfect. India's economy was booming in the mid-2000s, disposable incomes were rising, and a new middle class was emerging that wanted the assurance of branded, certified jewelry over the traditional family jeweler. The brothers weren't just selling gold and diamonds; they were selling trust, transparency, and a modern shopping experience. What started as a single showroom in Karol Bagh would soon expand beyond Delhi, riding the wave of India's retail revolution.

III. Early Growth & Business Model (2005–2012)

The genius of PC Jeweller's early strategy wasn't just in selling jewelry—it was in building an integrated empire. The company's business model consists of opening large format, standalone stores at high street locations. This wasn't the cramped, traditional jewelry shop model; these were destination stores, designed to make jewelry shopping an experience rather than a transaction.

The company sells only hall marked jewellery and certified diamond jewellery—a critical differentiator in a market plagued by questions about purity and authenticity. Every piece came with a promise, backed by certification. In a business built on trust, these weren't just regulatory requirements; they were competitive weapons.

The expansion timeline reads like a military campaign. In 2007, Jeweller opened two more showrooms in Noida and Panchukla (Haryana). Company also commences export operations from the manufacturing unit at the Noida SEZ. This dual strategy—retail expansion coupled with export operations—would become a defining characteristic of PC Jeweller's growth model.

By 2008, the company opened showrooms in Faridabad and Dehradun. In 2009, operations commenced at manufacturing units in Selaqui and Dehradun, while new showrooms sprouted in Pitampura and Chandigarh. Each store opening wasn't just about geographic expansion; it was about planting flags in India's rapidly growing tier-2 cities before competitors could establish dominance. The export strategy was particularly clever. The Company's export business of gold jewellery is on a B2B basis through its dealers based in the Gulf via Dubai based firms. Dubai wasn't just a market—it was a gateway to the entire Middle East, where Indian jewelry had cultural resonance and where margins were significantly higher than domestic retail.

The awards started rolling in, validating the strategy. Awarded Highest Exporter and the Best Exporter in the gems and jewellery sector by the Noida SEZ, Department of commerce, Ministry of commerce and industry, Government of India for the year 2009-2010. These weren't just trophies for the boardroom; they were credibility markers that helped in everything from bank financing to attracting franchisees.

By 2011, the company made a critical transition—changing its status from private limited to public limited, setting the stage for what would become one of the most successful IPOs in the jewelry sector. Company opened eight showrooms in Ludhiana, Bilaspur, Pali, South Extension (New Delhi), continuing its relentless expansion.

What's remarkable about this period is the operational discipline. While competitors were either staying small and traditional or expanding haphazardly, PC Jeweller methodically built infrastructure—manufacturing facilities, export units, retail showrooms—creating a vertically integrated machine that could capture value at every stage of the jewelry value chain.

The company understood that in India, jewelry wasn't just about the product—it was about the experience, the trust, the relationship. Their large-format stores weren't just selling jewelry; they were selling aspiration, celebration, and most importantly, peace of mind through certification and hallmarking. As 2012 approached and the company prepared for its public listing, it had transformed from a single Karol Bagh store into a formidable player with manufacturing units, export operations, and a growing retail footprint that was ready to challenge the established giants.

IV. IPO & Golden Years (2012–2017)

The morning of December 27, 2012, marked a watershed moment. PC Jeweller had its initial public offering in December 2012, raising ₹600 crore to fund its expansion. The shares listed on both BSE and NSE at ₹135 per share, and the market's reception was enthusiastic—the IPO had been oversubscribed 6.85 times, with retail investors showing particular interest.

This wasn't just capital raising; it was validation. The company that had started with a single showroom just seven years earlier was now a public entity with a market capitalization that would soon soar into the billions. The IPO proceeds were earmarked for a specific purpose: to open 20 stores each year, targeting western and southern India where the company had minimal presence.

The numbers during this golden period were staggering. The company clocked a turnover of ₹4,018 crore in FY13, an impressive near-doubling from ₹2,209 crore just two years earlier. The company wasn't just growing; it was accelerating. In October 2017, the company made a move that signaled its arrival as a national brand: signing of Bollywood superstars Akshay Kumar and his wife Twinkle Khanna as brand ambassadors. This wasn't just celebrity endorsement; it was a statement of intent. The company, which had 85 retail stores across the country and plans to add 20 more by March, earmarked Rs 100 crore for marketing activities.

The ad campaign, directed by R. Balki, was sophisticated—no gaudy displays of wealth, but rather a story about relationships and the permanence of love, mirroring the permanence of jewelry. The association with the star couple was congruent to the brand's next leg of pan India expansion.

Product innovations kept pace with marketing. The company launched various jewelry collections, including Anant, Dashavatar, Bandhan, Amour, and the Wedding Collection. Each collection was targeted at different customer segments, from traditional wedding jewelry to contemporary office wear.

The competition during this period was fierce but PC Jeweller held its own. While Tanishq, backed by the Tata brand, dominated the premium segment, and regional players like Kalyan Jewellers expanded aggressively, PC Jeweller carved out its niche—premium enough to command respect, accessible enough to attract the aspirational middle class.

By March 2018, the company had 92 showrooms in 75 cities, out of which 82 showrooms were company-owned and remaining 10 franchisee showrooms. The stock market loved the story—a family business professionalizing, expanding rapidly, signing Bollywood stars, delivering consistent growth. Share prices climbed steadily, reaching yearly highs that made early investors wealthy.

But beneath this glittering surface, fault lines were developing. The rapid expansion was funded by debt, export receivables were growing mysteriously large, and the company's corporate governance practices hadn't evolved as quickly as its store count. The golden years were about to end, and the trigger would come from the most unexpected source.

V. The Vakrangee Trigger & Beginning of the End (January 2018)

January 25, 2018. Mark that date—it's when the music stopped. All it took was an IT firm Vakrangee Ltd buying shares of PC Jeweller worth 112 crore (a .51% stake). On paper, this was trivial—a minor stake purchase by a Mumbai-based technology company. In reality, it was the butterfly that triggered the hurricane.

Vakrangee on January 25 purchased 20 lakh shares of PC Jeweller for a little over Rs 112 crore through an open market transaction. The problem wasn't the transaction itself—it was the buyer. Vakrangee was being probed by market regulator SEBI for manipulating its shares.

The market's reaction was swift and brutal. February 2, 2018, became a day of reckoning. PC Jeweller share price saw heavy selling pressure crashing nearly 60 per cent in intra-day trade. The stock of PC Jeweller tanked 24.40 per cent to end at Rs 365.60 on BSE. During the day, it plummeted 59.65 per cent to Rs 195.10.

The management scrambled to contain the damage. "Promoters have not sold any shares. Our fundamental is strong," PC Jeweller, MD, Balram Garg told PTI. But trust, once broken, is nearly impossible to restore. Investors weren't just selling shares; they were abandoning ship.

The domino effect had begun. The small cap stock which closed at all-time high of Rs 586.75 on January 17, 2018 would never see those heights again. What made matters worse was the guilt by association—why would a company under SEBI investigation buy shares in PC Jeweller? Were there hidden connections? Undisclosed relationships?

Many believed that the software company was perhaps cozy with the jeweller. They rushed to the exit and PC Jeweller's shares tanked. The speculation was relentless. Some suggested PC Jeweller's promoters had business relationships with Vakrangee they hadn't disclosed. Others whispered about coordinated stock manipulation.

The tragedy here is that PC Jeweller might have been an innocent bystander. Vakrangee claimed it was merely a treasury investment based on the jeweler's future potential. But in markets driven by perception, the truth often matters less than what people believe. And what people believed was that something was rotten in the state of PC Jeweller.

Stock price trajectory: From yearly high of 600.65 level to falling more than 81%—these numbers tell a story of wealth destruction on an epic scale. Investors who had celebrated 1000% returns over four years watched in horror as their gains evaporated in weeks.

The Vakrangee trigger revealed a fundamental weakness in PC Jeweller's story: it had grown too fast, borrowed too much, and hadn't built the institutional safeguards necessary for a public company. When confidence cracked, there was nothing to stop the collapse. The golden years were officially over, and the corporate governance crisis that followed would transform a market darling into a cautionary tale.

VI. Corporate Governance Crisis & Trust Erosion (2018)

The Vakrangee incident was just the appetizer. The main course of corporate governance failures arrived in April 2018, and it involved the company's founding family directly. Padam Chand Gupta, the founder, had quietly gifted some shares to his relatives. It was an off-market transaction which meant it wasn't executed on the stock exchanges.

This revelation struck at the heart of investor confidence. Off-market transactions aren't illegal, but they raise questions: Why not execute on the exchange? What's the real value of these transactions? Are promoters quietly exiting while telling investors everything is fine?

One of its promoters, Padam Chand Gupta, had gifted some of his shares to his family members through off-market transactions. This triggered concerns over transparency and the quality of disclosures by PC Jeweller. The timing couldn't have been worse—coming right after the Vakrangee debacle, it looked like a pattern of opacity.

The company's response was a masterclass in how not to handle a crisis. In May 2018, the board announced a share buyback worth Rs 424 crore, at a price of Rs 350 per unit—a premium to the then-current market price. It was meant to signal confidence, to show that promoters believed in the company's future.

But then came July 16, 2018—a date that would live in infamy for PC Jeweller shareholders. The firm said it was withdrawing an offer related to buyback of equity shares. The stock crashed over 28% to 86.10 compared to the previous close of 119.95 points. The reason? The company failed to obtain a No Objection Certificate from its bankers.

This was devastating on multiple levels. First, it suggested the company's financial position was weaker than disclosed—why else would banks refuse? Second, it made management look either incompetent (for announcing a buyback without bank approval) or deceptive (for knowing it wouldn't happen but announcing anyway).Then came the SEBI investigation, and it was devastating. The market regulator, SEBI found four individuals guilty of insider trading (an act of trading on the basis of unpublished price-sensitive information). The individuals concerned were Balram Garg (Promoter), Amit Garg (Balram's nephew), Sachin Gupta, and Shivani Gupta (son and daughter-in-law of the company's chairman, late PC Gupta).

SEBI ordered impounding of alleged illegal gains of over Rs 8 crore. As a result of these charges, SEBI imposed an aggregate fine of Rs. 1 crore on the guilty and barred them from trading in the shares of the jewellery company for 1 year.

The investigation revealed a pattern of trades that coincided suspiciously with major corporate announcements. Shivani Gupta and related entities sold PC Jeweller shares between April 2 and July 13, 2018—just before the buyback withdrawal was announced. An entity owned by Amit Garg took short positions right before the withdrawal announcement. The timing was too perfect to be coincidental.

"Jewellery businesses are built on trust... PC Jeweller was no longer deemed a trustworthy company"—this wasn't just about stock prices anymore. It was about the fundamental currency of the jewelry business: credibility. When customers read headlines about insider trading, they don't think about securities regulations—they wonder if the gold they're buying is really 22 karat, if the diamonds are actually certified.

The corporate governance failures created a vicious cycle. Trust erosion led to falling sales, which led to financial stress, which led to more questionable decisions, which further eroded trust. The company that had spent years building its brand on hallmarked jewelry and certified diamonds was now synonymous with opacity and manipulation.

The irony was bitter. PC Jeweller had positioned itself as the trustworthy alternative to traditional jewelers, the organized player bringing transparency to an opaque market. Now it was being investigated for the very practices it claimed to stand against. The brothers who had named the company after each other—a gesture of mutual trust—were now at the center of allegations that would destroy everything they'd built.

VII. Financial Unraveling & Operational Collapse (2018–2022)

The numbers tell a story of catastrophic decline. Sales collapsed from nearly ₹10,000 crores in FY18 to a mere ₹3,000 in FY21—a 70% drop that would be fatal for any retailer, but especially devastating for a jewelry business with high fixed costs and inventory requirements. The inventory crisis was particularly telling. Days Sales of Inventory soared from 200 days in FY18 to over 900 days in FY20. Think about that—the company was holding inventory for nearly three years before selling it. In a business where gold prices fluctuate and fashion trends change, this was a death sentence.

The cash simply stopped coming in. What made this worse was the structure of PC Jeweller's business model. Gold jewelry is a capital-intensive business—you need to buy gold, craft it into jewelry, display it in expensive showrooms, and hope customers buy it. When sales stop, you're stuck with crores worth of gold that you've already paid for.

Export receivables became another nightmare. The company had built a significant B2B export business through Dubai dealers, which looked impressive on paper—high volumes, international presence. But these businesses were in no hurry to pay PC Jeweller. As the company's reputation crumbled, international partners became even more reluctant to settle dues.

The financial statements painted a grim picture. Standalone net loss of Rs 2.81 crore in 2018-19 vs net profit of Rs 567.4 crore previous year—this wasn't just a downturn; it was a collapse. Total income fell to Rs 8,461.17 crore during the 2018-19 fiscal from Rs 9,588.54 crore in the 2017-18 fiscal.

Debt accumulation accelerated as the company borrowed to meet working capital needs. But with sales collapsing and inventory piling up, the interest burden became crushing. Banks that had once eagerly financed the company's expansion became nervous creditors demanding repayment.

Store closures followed inevitably. The large-format showrooms that had been PC Jeweller's pride became albatrosses. Each store represented lakhs in rent, salaries, and operational costs—fixed expenses that couldn't be reduced even as footfalls disappeared. The company that had planned to open 20 stores annually was now desperately trying to close unprofitable locations.

Management tried various firefighting measures. They announced plans to reduce the export business, recognizing it had become a drain rather than a profit center. They attempted to convert company-owned stores to franchises, shifting the operational burden. They even explored demerging the export business entirely.

But it was too late. The trust deficit had created a downward spiral that couldn't be arrested. Suppliers demanded advance payments, customers stayed away, employees left for competitors, and franchisees refused to renew agreements. The operational infrastructure built for a ₹10,000 crore business couldn't survive on ₹3,000 crore in sales.

VIII. Insolvency & Current Status (2022–Present)

The endgame arrived in 2022. After years of mounting losses and shrinking operations, the culmination of challenges led to default on its ₹3,400 crore bank loan. The company that had once commanded a market capitalization in the billions couldn't pay its creditors.

SBI initiated legal action, thrusting PC Jeweller into insolvency proceedings. Public sector lender State Bank of India (SBI) has taken PC Jeweller to the National Company Law Tribunal (NCLT) with a plea to initiate insolvency proceedings against the city-based jewellery manufacturer and retailer claiming a default.

The details were staggering. Total exposure outstanding as on 31 March, 2023 amounting to Rs 3,626.09 crore includes provision for interest. The company had borrowed from 14 banks, with SBI alone owed Rs 1,060 crore, Union Bank Rs 530 crore, Punjab National Bank Rs 478 crore, and Indian Bank Rs 266 crore.

Company's accounts have been classified as NPA with its lenders since June 2021 and its resolution process had been underway. This classification as a Non-Performing Asset meant banks had lost faith in the company's ability to repay—a death certificate for any business dependent on working capital financing.

The current market position is dramatic. PC Jeweller's shares were locked in 5 per cent upper circuit at Rs 177.95, also its multi-year high on the BSE, on Monday's intra-day trade amid heavy volumes—a surprising resurrection for a company that seemed destined for liquidation just months earlier.

Union Bank of India, the second largest bank after State Bank of India amongst consortium banks of PC Jeweller in terms of its exposure, vide letter dated 15 June 2024 has conveyed its approval to the One Time Settlement (OTS) offer submitted by the Company. This was followed by a cascade of approvals: In July, PC Jeweller secured OTS approvals from Canara Bank, Bank of Baroda, and IndusInd Bank. "With this approval, all the fourteen consortium member banks have approved the OTS proposal submitted earlier by the Company," the company announced in September 2024.

The resurrection plan is ambitious. PC Jeweller Ltd plans to raise up to Rs 2,705 crore by issuing warrants on a preferential basis to promoters and investors, mainly to settle bank loans and for working capital requirements. Promoters will infuse around Rs 850 crore into the company by subscribing to warrants issued by the company. In a regulatory filing on Saturday, PC Jeweller informed that its board has approved the proposal to raise funds up to Rs 2,705.14 crore by preferential issue of fully convertible warrants. Around 75 per cent of the fund will be used for repaying bank loans and the rest 25 per cent for working capital requirements. He said the promoters would infuse Rs 850 crore into the company, while the remaining amount would be raised from investors.

What's remarkable is the speed of this turnaround. So far in the month of September, the stock has rallied 60 per cent. In three month, it zoomed 249 per cent, while, in the past one year, it has skyrocketed 577 per cent from the level of Rs 26.30 on the BSE. The same stock that was on the verge of insolvency proceedings is now contemplating stock splits and seeing upper circuit locks.

The operational footprint has stabilized, though significantly reduced from its peak. The company continues to maintain a wide network of 60 showrooms (including 6 franchisee showrooms) located in 44 cities spread across 15 states as of March 31, 2024—down from 92 showrooms at its peak but still a substantial presence.

IX. Playbook: Business & Market Lessons

The PC Jeweller collapse offers a masterclass in what can go wrong when traditional family businesses enter public markets without adequate governance structures. The lessons are harsh but invaluable.

Corporate governance in family businesses remains the central challenge. The off-market transactions, the insider trading allegations, the sudden buyback withdrawal—each incident eroded trust incrementally until the dam burst. Family businesses entering public markets must recognize that the informal practices that worked in private ownership become liabilities under public scrutiny. The market demands transparency, and any deviation is punished severely.

The fragility of trust-based businesses became painfully evident. Jewelry isn't just a product; it's a promise. When PC Jeweller's corporate governance came under question, customers didn't just doubt the company's stock—they doubted the purity of its gold, the authenticity of its diamonds. In trust-based businesses, corporate scandals don't just affect share prices; they destroy the fundamental value proposition.

Dangers of rapid expansion with high leverage proved fatal. PC Jeweller's aggressive store expansion was funded primarily by debt, creating a structure that required constant growth to service interest payments. When growth stopped, the entire edifice collapsed. The lesson: in capital-intensive retail businesses, sustainable growth trumps speed every time.

Market perception vs. business fundamentals created a devastating gap. PC Jeweller might have had strong fundamentals—manufacturing capabilities, prime retail locations, established brand—but once market perception turned negative, these assets became worthless. In public markets, perception often becomes reality, especially in consumer-facing businesses.

Warning signs investors missed were abundant in retrospect. The insufficient cash flow was evident in the financial statements—the company was growing revenues but not generating proportionate cash. The high export receivables to sales ratio suggested either operational inefficiencies or worse, financial engineering. Days Sales of Inventory creeping up should have been a red flag in a business where inventory management is critical.

The export business, in particular, deserved scrutiny. Why were receivables from Dubai dealers so high? Why were collection periods extending? These weren't just operational issues—they were symptoms of a business model under stress.

Regulatory environment and SEBI's role proved both protective and punitive. SEBI's investigation into insider trading was thorough and its penalties severe, sending a message about market manipulation. But the damage to PC Jeweller's reputation was irreversible. The regulatory framework worked, but at the cost of destroying a company that employed thousands.

The timing of regulatory action matters as much as the action itself. Had governance issues been addressed earlier through preventive measures rather than punitive action, the collapse might have been avoided. This raises questions about the balance between regulatory oversight and market development.

X. Industry Analysis & What This Means for Indian Jewelry

The PC Jeweller saga sent shockwaves through India's organized jewelry retail sector, coming at a time when the industry was already reeling from other high-profile failures. The impact extended far beyond one company's collapse.

Impact on organized jewelry retail in India was immediate and severe. Investors became wary of jewelry stocks, demanding higher risk premiums. Lenders tightened credit, making expansion difficult even for healthy companies. Customers questioned whether "organized" really meant "trustworthy" or was just marketing speak.

Comparison with survivors: Tanishq, Kalyan Jewellers reveals what PC Jeweller lacked. Tanishq had the Tata brand backing—when you buy from Tanishq, you're not just trusting a jeweler, you're trusting one of India's most respected corporate houses. Kalyan Jewellers, despite its own challenges, maintained stronger regional roots and better inventory management. Both survived because they had institutional strength beyond individual promoters.

The survivors also had more conservative expansion strategies. While PC Jeweller was opening 20 stores annually, Tanishq grew methodically, ensuring each store was profitable before expanding further. Kalyan focused on clusters, building density in specific regions rather than spreading thin across India.

Trust deficit in the sector post-Nirav Modi compounded PC Jeweller's problems. The Nirav Modi-Punjab National Bank fraud had already shaken confidence in the jewelry sector. When PC Jeweller's governance issues emerged, it reinforced the narrative that jewelry businesses were inherently risky, prone to financial engineering and regulatory violations.

This trust deficit affected even well-managed companies. Jewelry stocks traded at discounts, expansion plans were shelved, and international partnerships became harder to secure. The sector that should have been booming with India's growing prosperity was instead fighting for credibility.

Evolution of Indian consumer preferences accelerated during this period. Younger consumers, already moving toward lightweight, contemporary designs, became even more brand-conscious. They wanted jewelry from companies they could trust, with transparent pricing and clear certification. PC Jeweller's collapse reinforced these trends.

The shift to hallmarked jewelry accelerated. Consumers who might have accepted traditional jewelers' assurances now demanded BIS hallmarking. The government's decision to make hallmarking mandatory for gold jewelry was partly influenced by scandals that highlighted the need for standardization.

Future of jewelry retail: Online vs. offline became a critical question. While PC Jeweller had built its empire on large-format physical stores, new players were experimenting with online models. Companies like BlueStone and CaratLane (acquired by Tanishq) proved that jewelry could be sold online, especially to younger consumers comfortable with digital transactions.

But the PC Jeweller story also highlighted the importance of physical presence. Jewelry remains a high-touch category where customers want to see, feel, and try products. The future likely lies in omnichannel models—strong digital presence backed by physical stores for experience and trust-building.

The Indian jewellery retail sector's size in FY23 was close to $70 billion. Within this landscape, organised retail accounted for about 37 per cent, encompassing both national and regional players. Projections indicate that the jewellery retail market, poised for growth, is expected to reach approximately $145 billion by FY28. This optimistic outlook is attributed to the expanding economy, increased disposable income, a surge in consumer demand for gold, the upward trajectory of gold prices and rising interest in other categories such as diamonds, other precious stones and costume jewellery.

XI. Epilogue & Reflections

The PC Jeweller story isn't just about financial metrics and stock prices—it's about dreams built and destroyed, trust earned and lost, and the human cost of corporate failure. It serves as a cautionary tale, emphasizing the imperative of maintaining trust and transparency in business operations.

Key takeaways for entrepreneurs and investors are sobering. For entrepreneurs, the message is clear: growth without governance is a recipe for disaster. The transition from private to public ownership demands not just regulatory compliance but a fundamental shift in mindset. What works in Karol Bagh doesn't necessarily work on Dalal Street.

For investors, PC Jeweller reinforces the importance of looking beyond reported numbers. High growth rates, celebrity endorsements, and aggressive expansion plans might make for exciting stories, but sustainable businesses are built on cash generation, prudent capital allocation, and transparent governance.

The importance of institutional frameworks cannot be overstated. PC Jeweller needed independent directors who could challenge management, auditors who could spot irregularities, and internal controls that could prevent insider trading. These aren't bureaucratic obstacles—they're the guardrails that prevent companies from driving off cliffs.

The human cost: Employees, franchisees, shareholders remains the most tragic aspect. Thousands of employees lost their jobs, many in tier-2 cities where alternative employment was scarce. These weren't just numbers on a spreadsheet—they were skilled craftsmen, sales associates who had spent years building customer relationships, managers who had staked their careers on PC Jeweller's growth story.

Franchisees suffered particularly badly. Many had invested their life savings in PC Jeweller showrooms, believing in the brand's promise. When the company collapsed, they were left with expensive leases, unsold inventory, and shattered dreams. Unlike company-owned stores that could be closed by corporate decision, franchisees faced personal bankruptcy.

Shareholders, particularly retail investors who had held through the 1000% rise, watched their wealth evaporate. Many were middle-class investors who had seen PC Jeweller as their ticket to prosperity. The stock that was supposed to fund retirements and children's educations became worthless paper.

Final thoughts on corporate India's governance challenges point to systemic issues beyond PC Jeweller. The concentration of power in promoter families, the weakness of independent directors, the conflicts of interest in auditor appointments—these aren't unique to PC Jeweller. They're endemic to corporate India.

The regulatory response, while necessary, often comes too late. By the time SEBI investigates, by the time banks initiate insolvency proceedings, the damage is done. What's needed is proactive governance, where problems are identified and addressed before they become crises.

Yet there's also resilience in this story. The fact that PC Jeweller is attempting a comeback, that banks are willing to accept settlements, that the stock is rising again—this speaks to the fundamental strength of the business model, if not its execution. Perhaps the company that emerges from this crisis will be stronger, more transparent, more sustainable.

The jewelry business will continue because it's woven into India's cultural fabric. Weddings will happen, festivals will be celebrated, and gold will be bought. The question is whether the industry can learn from PC Jeweller's mistakes, building businesses that honor both tradition and modern governance standards.

Conclusion: The Glitter That Faded

PC Jeweller's journey from a single Karol Bagh store to potential insolvency and now attempted resurrection encapsulates the best and worst of Indian entrepreneurship. It's a story of ambition and overreach, of trust built over decades and destroyed in months, of a family business that couldn't adapt to public market demands.

The company that once promised to democratize jewelry buying, to bring transparency to an opaque industry, became a symbol of everything wrong with corporate governance. The brothers who named the company after each other, symbolizing trust and partnership, ended up at the center of insider trading allegations that destroyed their creation.

Yet the story isn't over. With all fourteen consortium banks approving the one-time settlement, with promoters infusing fresh capital, with the stock recovering dramatically, PC Jeweller is attempting something rare in Indian corporate history—a second act. Whether this resurrection succeeds or becomes another false dawn remains to be seen.

What's certain is that PC Jeweller has left an indelible mark on Indian retail, corporate governance, and investor consciousness. Every jewelry company that goes public will be scrutinized through the PC Jeweller lens. Every rapid expansion will be questioned. Every related-party transaction will be examined.

In the end, PC Jeweller's greatest contribution might not be the thousands of kilograms of gold it sold or the hundreds of stores it opened, but the lessons it taught about the importance of governance, the fragility of trust, and the perils of growing too fast. As the Indian jewelry market marches toward its projected $145 billion future, these lessons will hopefully prevent other glittering dreams from fading into cautionary tales.

The Karol Bagh store where it all began still stands, a reminder that every empire, no matter how grand, starts with a single step—and can end with a single misstep. For PC Jeweller, the journey continues, but whether it leads to redemption or further decline, only time will tell. What's certain is that the Indian jewelry industry, and indeed corporate India, will never be quite the same.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube