PCBL Chemical Limited: The Carbon Black to Specialty Chemicals Transformation Story

I. Cold Open & Episode Thesis

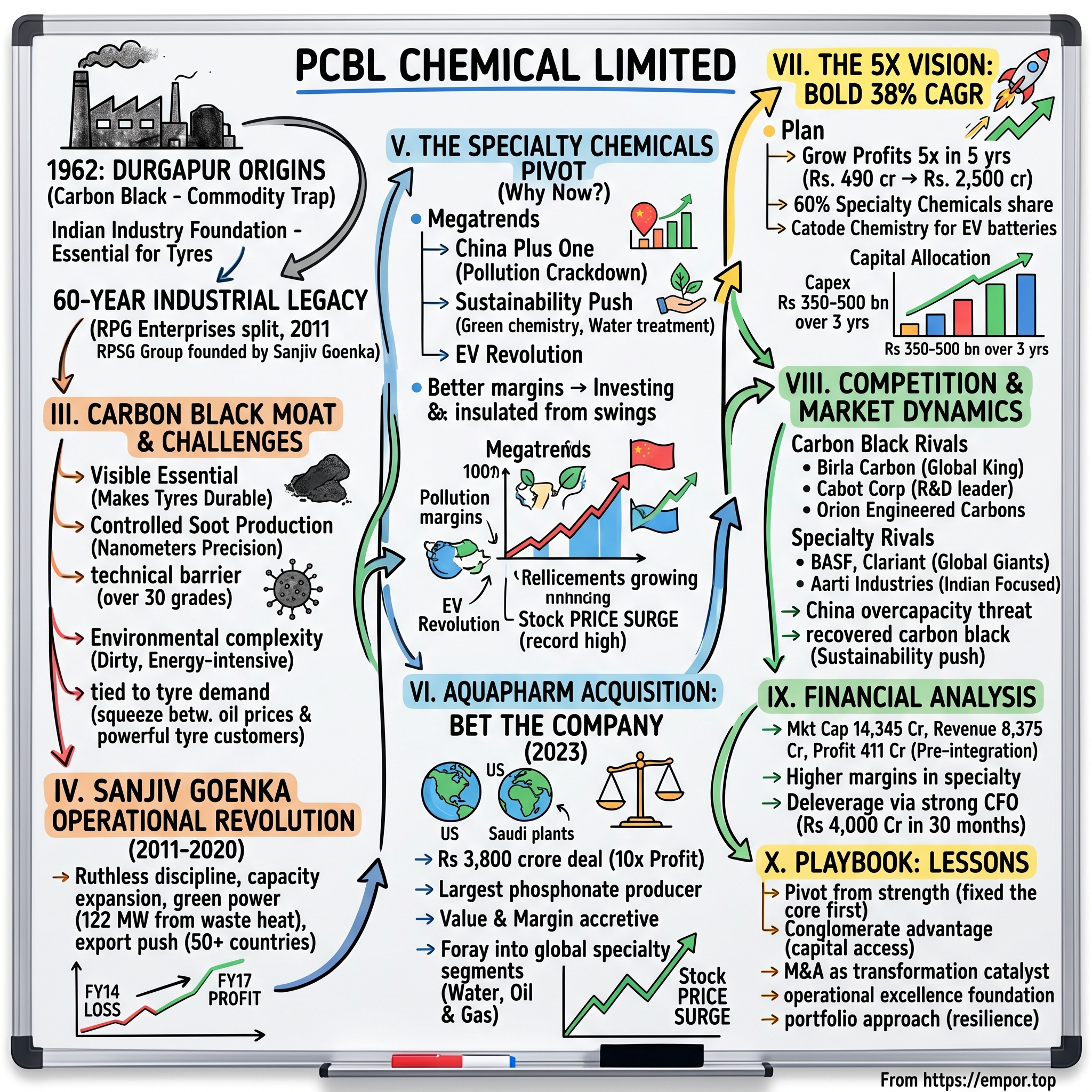

Picture this: A grimy carbon black factory in Durgapur, West Bengal, circa 1962. Black dust coats everything—the machinery, the walls, the workers' faces. This is where PCBL's story begins, in the industrial heartland of newly independent India, manufacturing the unglamorous but essential ingredient that makes tires black and durable. Fast forward to 2024: The same company just bet $455 million—more than its annual profit—on acquiring a specialty chemicals firm, with its chairman confidently declaring a 5x profit growth target in five years.

How does a 60-year-old carbon black manufacturer transform into what could become India's specialty chemicals powerhouse? This is the story of PCBL Chemical Limited, a company that embodies the evolution of Indian industry itself—from license raj survivor to global ambitions, from commodity trap to value-added dreams.PCBL today stands at a fascinating inflection point. With a market cap of ₹14,345 crore, revenue of ₹8,375 crore, and profit of ₹411 crore, it's a profitable, established player. But here's where it gets interesting: India's largest and the world's 7th largest carbon black producer, with a total capacity of 790 KTPA, is betting everything on becoming something entirely different—a global specialty chemicals powerhouse.

The Aquapharm acquisition for Rs 3,800 crore isn't just another deal. It's a declaration of intent, a pivot so dramatic that chairman Sanjiv Goenka is promising to grow profits five-fold in five years. That's a 38% CAGR—the kind of growth rate you expect from a hot tech startup, not a 64-year-old industrial company.

This transformation story touches every major theme in modern Indian business: the evolution from commodity manufacturing to value-added products, the challenge of family business succession, the opportunity presented by China's changing role in global supply chains, and the eternal question of whether conglomerates can create or destroy value. It's also a story about timing—why now, after six decades in carbon black, is the moment to reinvent?

Our journey will take us from the dusty origins in post-independence India through the operational revolution under Sanjiv Goenka, to the bold specialty chemicals bet that will define PCBL's next chapter. We'll examine whether this is brilliant strategy or dangerous overreach, and what it means for investors trying to understand where Indian manufacturing is headed.

II. The Goenka Dynasty & Industrial Legacy

The year is 1830. A young man named Ramdutt Goenka arrives in Calcutta from the desert state of Rajasthan, carrying little more than ambition and a head for numbers. He starts as a banker, then becomes an agent for British trading houses—the classic Marwari business trajectory of that era. What Ramdutt couldn't have imagined was that his descendants would build one of India's most powerful business dynasties, spanning everything from tires to tea, power to retail.

The Goenkas perfected the art of being intermediaries in colonial India, turning relationships and trust into capital. By the early 20th century, they had graduated from agents to owners, acquiring jute mills, tea estates, and trading operations. But it was K.P. Goenka who would make the leap into modern industry with PCBL in 1960.K.P. Goenka set up PCBL in 1960, starting production at Durgapur with a modest capacity of 14,000 MT per annum. The timing was strategic—India had just embarked on its second Five Year Plan, emphasizing heavy industrialization. Carbon black, essential for tire manufacturing, was a critical import substitution opportunity. This wasn't just business; it was nation-building.

The Goenka empire-building philosophy was unique: they were takeover artists before the term existed. While the Tatas built from scratch and the Birlas expanded organically, the Goenkas perfected the art of acquiring distressed assets and turning them around. In the 1970s, Rama Prasad Goenka leveraged the family's wealth to take over a variety of industries, many stressed due to socialistic policies and "License Raj," acquiring them relatively cheaply and using financial resources and business acumen to make them viable.

In 1979, Keshav Prasad Goenka split his business empire among his three sons, with Rama Prasad establishing RPG Enterprises with Phillips Carbon Black, Asian Cables, Agarpara Jute and Murphy India as constituents. PCBL thus became the foundation stone of what would become one of India's most aggressive conglomerates.

The real drama unfolds in 2011. The Group's businesses were divided between Rama Prasad Goenka's sons, Harsh and Sanjiv, with RP-Sanjiv Goenka Group founded on July 13, 2011, under Sanjiv Goenka's chairmanship. This wasn't just a family split—it was a generational shift in business philosophy. While Harsh inherited the traditional businesses including tires and infrastructure, Sanjiv got power, retail, and crucially, PCBL.

Sanjiv Goenka represents the third generation of Marwari businessmen who are comfortable with both spreadsheets and spirituality, McKinsey consultants and family retainers. He inherited not just businesses but a playbook: find undervalued assets, inject capital and management bandwidth, and scale aggressively. But unlike his father and grandfather who thrived in the License Raj by managing relationships, Sanjiv would have to compete in a liberalized economy where execution matters more than connections.

The conglomerate structure, often criticized by modern management theorists, actually provides PCBL with unique advantages. The group's power business provides energy security for carbon black manufacturing—a significant cost component. The retail presence through Spencer's offers consumer insights. The sports franchises (including IPL's Lucknow Super Giants) provide brand visibility. And critically, the group's financial strength allows for patient capital and bold bets—like the Aquapharm acquisition.

Understanding PCBL requires understanding this dynasty's DNA: the willingness to bet big on industrial assets, the patience to execute turnarounds, and the ambition to transform commodity businesses into specialty plays. It's a particularly Indian story of how family businesses evolve—not through Silicon Valley-style disruption, but through patient accumulation of industrial capabilities.

III. Carbon Black 101: The Invisible Essential

Here's a question that stumps most people: What makes tires black? The answer is carbon black—a material so ubiquitous yet so invisible that most of us have never heard of it despite touching it every day. Without carbon black, your car tires would be white (like natural rubber), would degrade in months instead of years, and would have about as much road grip as a bar of soap.

Carbon black is essentially pure carbon in the form of extremely fine particles, produced by the incomplete combustion of heavy petroleum products. Think of it as controlled soot production—but with precision that would make a Swiss watchmaker jealous. The particles are typically 10 to 500 nanometers in size, with surface areas that can exceed 1,500 square meters per gram. To put that in perspective, a teaspoon of carbon black has the surface area of a football field.

The manufacturing process is where the technical moat begins. You're essentially managing controlled explosions at temperatures exceeding 1,400°C, breaking down hydrocarbon feedstock into carbon and hydrogen. The trick isn't just making carbon black—it's making exactly the right grade with consistent particle size, structure, and surface chemistry. PCBL produces over 30 different grades, each optimized for specific applications. A truck tire needs different carbon black than a passenger car tire, which needs different properties than a conveyor belt. Carbon black is produced through thermal decomposition or partial combustion of hydrocarbons such as oil or natural gas, with characteristics varying by manufacturing process, and the furnace process being the most commonly used method today. The production furnace uses a closed reactor to atomize feedstock oil under carefully controlled conditions, where it vaporizes and then pyrolyzes in the vapor phase to form microscopic carbon particles.

What makes carbon black production particularly challenging is the environmental complexity. This isn't clean manufacturing—it's inherently dirty, energy-intensive, and requires sophisticated pollution control. The carbon black segment operates through five manufacturing units strategically located at Durgapur, Kochi, Palej, Mundra, and Chennai's Tiruvallur District. Each location was chosen for specific advantages: proximity to refineries for feedstock, port access for exports, or nearness to tire manufacturers.

The global market dynamics are fascinating. China dominates global production, but that's both an opportunity and a threat. Environmental crackdowns in China periodically constrain supply, creating price spikes that benefit Indian producers. But China's massive scale also means they can flood markets when operating at full capacity. The tire industry consumes about 70% of global carbon black production, with the remainder going into plastics, inks, and coatings.

PCBL has built significant technical capabilities over six decades. They're not just making commodity carbon black—they produce over 30 grades including specialty blacks for high-performance applications. With a total capacity of 790 KTPA (678 KT for rubber black and 112 KT for specialty black), PCBL commands over 40% market share in India and ranks as the world's 7th largest player.

The moat in carbon black isn't just technical—it's also regulatory and environmental. Setting up a new carbon black plant requires massive capital investment, environmental clearances that can take years, and the ability to manage complex logistics of feedstock procurement and product distribution. Modern plants must also integrate energy recovery systems—PCBL generates 122 MW per hour of green power from waste heat, turning an environmental liability into an asset.

But here's the challenge that sets up our story: Carbon black is fundamentally a commodity business tied to tire demand. Margins are squeezed between volatile oil prices (your raw material) and powerful tire manufacturers (your customers). It's a good business, but not a great one. Which brings us to Sanjiv Goenka's operational revolution and the quest to transform PCBL into something more.

IV. Sanjiv Goenka's Operational Revolution (2011-2020)

The year is 2012. Sanjiv Goenka, newly in charge after the family split, walks into PCBL's boardroom with a team of McKinsey consultants. What happens next would become corporate legend—or infamy, depending on who tells the story. The entire senior leadership team walks in collectively and accuses him of "behaving like an owner." Goenka's response? "I realized then that these people will not allow change and that I needed to change them. "This wasn't just corporate theatre—it was a defining moment. Goenka's decision to bring in an external consultant wasn't well-received, with the entire senior leadership coming collectively and accusing him of "behaving like an owner," uneasy about Goenka and McKinsey asking too many questions. "I realised then that these people will not allow change and that I needed to change them," says Goenka candidly.

The PCBL he inherited was a paradox. Despite being the largest supplier of carbon black in India and one of the largest in the world, the company was struggling with low profitability and even incurred losses in FY13 and FY14. The company had the assets, the market position, and the technical capabilities, but it was bleeding money.

What followed was ruthless operational discipline. Goenka and his McKinsey team tore through every aspect of the business—raw material procurement, production efficiency, customer contracts, working capital management. Sacred cows were slaughtered. Long-serving executives who resisted change were shown the door. New talent was brought in from outside the industry.

The transformation wasn't just about cost-cutting. Goenka pushed aggressive capacity expansion, adding strategically located plants. The Mundra unit in Gujarat, commissioned in 2009, gave PCBL port access for exports. The Chennai plant, commissioned in 2023, positioned the company closer to South Indian tire manufacturers. Each expansion was calculated to reduce logistics costs and improve customer service.

Green power integration became a strategic differentiator. PCBL generates 122 MW per hour of green power, turning the energy-intensive nature of carbon black production from a liability into a competitive advantage. This wasn't just environmental virtue signaling—it was hard-nosed economics. Energy costs can account for 15-20% of carbon black production costs, and having captive renewable power insulates PCBL from grid price volatility.

The export push was equally aggressive. PCBL became a strong global player with a significant customer base in 50+ countries, competing directly with Chinese producers in markets from Southeast Asia to Africa. This geographic diversification reduced dependence on the Indian market and provided natural hedging against currency fluctuations.

The results spoke for themselves. The result was a gradual improvement in PCBL's profitability starting in FY15. Compared with a net loss of Rs 88 crore in FY14, the company posted a net profit of Rs 68 crore in FY17, on a total operating turnover of Rs 1,946 crore.

But Goenka's ambitions went beyond just fixing PCBL's operational issues. He was already thinking about the next phase—moving beyond carbon black into higher-margin businesses. The operational turnaround was just table stakes, proving he could execute. The real game was transformation.

What's remarkable about this period is how Goenka balanced multiple priorities. While revolutionizing PCBL, he was simultaneously acquiring Firstsource (the BPO company) for Rs 400 crore in 2012, restructuring Spencer's Retail, and laying the groundwork for what would become the specialty chemicals pivot. This wasn't a one-company turnaround story—it was a conglomerate-wide operational revolution.

The McKinsey playbook—data-driven decision making, performance metrics, accountability—became the RPSG way. But unlike many consultant-driven transformations that lose steam once the consultants leave, Goenka institutionalized these changes. He brought in professional managers, created performance-based compensation structures, and most importantly, stayed deeply involved in operational details.

By 2020, PCBL was a fundamentally different company than the one Goenka inherited in 2011. Profitable, efficient, with modern plants and global reach. But the carbon black business, even optimized, had inherent limitations. Which brings us to the critical question: Why pivot to specialty chemicals now?

V. The Specialty Chemicals Pivot: Why Now?

Imagine you're Sanjiv Goenka in 2020. You've successfully turned around PCBL, the company is profitable, and you're generating decent returns. Most executives would declare victory and coast. But Goenka sees what others miss: carbon black is a commodity trap, and the trap is about to get worse.

The fundamental problem with carbon black is brutally simple—you're selling an undifferentiated product to concentrated, powerful customers. The top 10 tire manufacturers globally account for over 60% of carbon black demand. When Michelin or Bridgestone wants to squeeze margins, they can play suppliers against each other. Your only differentiators are price, quality consistency, and delivery reliability—necessary but not sufficient for premium returns. The numbers tell the story. Specialty chemicals have better margins, and are more insulated from commodity price swings. If a customer likes your product, they tend to stick around. India's specialty chemical industry is valued at $41.90 billion and approximately 20% of the total chemicals market in India, the specialty chemicals sector has been playing a pivotal role in driving the chemicals industry's growth.

But it's not just about margins. Three global megatrends are creating a once-in-a-generation opportunity for Indian specialty chemicals:

China Plus One: China's exit from the market was catalysed when China started cracking down on pollution in its chemical factories, shutting many of them down. That made a lot of global buyers look for alternative suppliers — and India stepped up. Environmental regulations in China have permanently raised their cost structure, making Indian producers competitive even without protectionism.

Sustainability Push: Water treatment chemicals, biodegradable chelating agents, and green chemistry solutions are growing at double-digit rates globally. These aren't commodities where the lowest price wins—customers pay premiums for performance and environmental compliance.

Electric Vehicle Revolution: EVs require different specialty chemicals than internal combustion engines—thermal management fluids, battery electrolytes, lightweight composite materials. The shift to EVs doesn't eliminate chemical demand; it transforms it into higher-value applications.

In the chemicals segment, PCBL already ranks among the top 3 global producers of phosphonates, offering over 275 products, with phosphonates contributing over 50% of revenue. This wasn't built overnight—it's the result of decades of R&D and customer relationships. But to truly transform PCBL, incremental growth in specialty chemicals wasn't enough. They needed a game-changing acquisition.

The timing for a specialty chemicals pivot is particularly favorable. The Indian chemicals industry is valued at US$220b, and projected to grow by approx. 9% p.a. during 2020-25 to reach US$300b by FY 2025. The sector is expected to hit the US$1t mark by FY 2040.

What makes specialty chemicals particularly attractive is the customer stickiness. Unlike carbon black where customers constantly benchmark prices, specialty chemical relationships are technical partnerships. Once your product is specified into a customer's formulation—whether it's a paint, a pharmaceutical, or a water treatment system—switching costs are high. Reformulation requires extensive testing, regulatory reapproval, and production line adjustments.

The intellectual property aspect is equally important. While you can't patent carbon black, specialty chemicals offer opportunities for proprietary formulations, process innovations, and application patents. This creates defensible moats that commodity businesses simply can't build.

But here's the challenge: Building a specialty chemicals business organically takes decades. You need R&D capabilities, customer relationships, regulatory approvals, and manufacturing expertise across hundreds of products. Which is why Sanjiv Goenka's next move would shock the market—and potentially transform PCBL forever.

VI. The Aquapharm Acquisition: Bet the Company Move

November 2023. PCBL's board meets for what insiders describe as the most consequential decision in the company's 63-year history. On the table: acquiring Aquapharm Chemicals for Rs 3,800 crore—nearly ten times PCBL's annual profit. For context, this wasn't just a large acquisition; it was a bet-the-company move that would fundamentally alter PCBL's DNA.Aquapharm wasn't just any specialty chemicals company. Founded by the Mangwani family, it had quietly built itself into India's largest phosphonate producer and a globally top-three player in water treatment chemicals. Aquapharm Chemicals Private Limited reported a consolidated turnover of Rs 2,008.8 crores for the fiscal year ending on March, 2023, with manufacturing facilities not just in Pune but also in the United States and Saudi Arabia.

The financials were compelling: ACPL clocked sales of Rs 2,009 crore as of FY23, gross margins of 31 per cent, EBITDA of Rs 417 crore (EBITDA margins 21 per cent) and PAT of Rs 280 crore. Those 21% EBITDA margins compared to PCBL's carbon black margins in the low teens represented exactly the kind of business transformation Goenka was seeking.

But what really excited Goenka wasn't just the numbers—it was the strategic fit. Sanjiv Goenka Chairman PCBL said "Aquapharm is a leading specialty chemicals company and is India's largest phosphonate producer. The acquisition is value accretive and margin accretive and is in the space of fast growing high margin chemicals. It's a platform which offers a lot of growth and high margins. It's a unique opportunity and we are delighted to take this opportunity."

Phosphonates are the unsexy workhorses of the specialty chemicals world. They prevent scale formation in industrial water systems, act as chelating agents in detergents, and serve as corrosion inhibitors in oil fields. Not glamorous, but absolutely essential. And critically, once a phosphonate formulation is specified into a customer's process—whether it's a refinery, a power plant, or a detergent manufacturer—switching costs are prohibitively high.

The deal structure revealed Goenka's financial engineering skills. In a filing with the stock exchanges, PCBL stated that the board of directors, at its meeting held on November 28, 2023, in principle approved the acquisition. The company intends to acquire, either directly or through one of its affiliates, 212,172 shares of ACPL, for an aggregate consideration of Rs 3,800 crores (subject to agreed adjustments), representing 100 per cent of the issued and paid-up share capital. The financing would come through a mix of internal accruals and external fundraising.

PCBL expects to cumulatively generate around Rs 4,000 of EBITDA/CFO over next 30 months (PCBL+ACPL) which will help indirectly fund the acquisition (repay debt). This wasn't reckless leverage—it was calculated risk-taking based on strong cash flow visibility.

The market reaction was immediate and dramatic. Shares of PCBL surged 6 per cent to hit a record high of Rs 269.85 on the BSE in Wednesday's intra-day trade after the company announced on Tuesday it plans to acquire speciality chemical company Aquapharm Chemicals Pvt. Ltd. (ACPL) for Rs 3,800 crore. Thus far in the month of November, the stock price of PCBL has rallied 35 per cent, while since April it has more than doubled or zoomed 133 per cent.

But the real significance of Aquapharm goes beyond immediate financials. The deal would mark PCBL's foray into global specialty segments of water treatment chemicals, and oil & gas chemicals. These are markets with structural tailwinds—water scarcity driving treatment demand, stricter environmental regulations requiring better industrial water management, and the oil & gas industry's constant need for specialty chemicals to enhance recovery and reduce corrosion.

The integration challenges are non-trivial. Aquapharm's culture, built by entrepreneurial founders, needs to mesh with PCBL's more corporate structure. The technology platforms are different—carbon black is essentially one product with many grades, while Aquapharm offers hundreds of distinct formulations. Customer relationships need careful management during the transition.

Yet Goenka seems confident. The acquisition creates immediate scale in specialty chemicals—taking PCBL from a minor player to a significant force overnight. It provides a platform for further acquisitions and organic growth. Most importantly, it fundamentally changes PCBL's investment narrative from a cyclical commodity play to a structural growth story.

The Aquapharm acquisition also reveals Goenka's broader strategy. The company also hinted at some sizeable acquisition on the Li-on battery front, suggesting this is just the first move in a multi-step transformation. The vision is clear: build a multi-platform global specialty chemicals business through a combination of acquisitions and organic growth.

What's particularly clever about the Aquapharm deal is how it leverages PCBL's existing strengths. The company's global distribution network for carbon black can now carry Aquapharm's products. PCBL's relationships with industrial customers—refineries, chemical plants, manufacturers—are perfect channels for water treatment chemicals. The R&D capabilities in carbon surface chemistry translate surprisingly well to understanding phosphonate interactions.

But perhaps the boldest aspect of this acquisition is what comes next—the 5X vision that has both excited and terrified investors.

VII. The 5X Vision: Bold or Delusional?

Stand in any boardroom and declare you'll grow profits five-fold in five years, and you'll likely be escorted out by security. But when Sanjiv Goenka makes this claim for PCBL, people listen. Not because he's prone to hyperbole—quite the opposite. This is the man who turned around PCBL from losses to profits, who built Firstsource into a global BPO player, who paid $940 million for an IPL team. When Goenka makes a bold prediction, it's backed by spreadsheets, not wishful thinking. Sanjiv Goenka exudes confidence about being able to grow its profits 5 times in 5 years. In percentages, this translates to a CAGR of 38%! Goenka earlier highlighted that PCBL plans to expand its specialty blacks segment, aiming for profit growth of at least 5x over the next five years, expects its profit to reach between Rs. 2,400 crores and Rs. 2,500 crores, up from the current Rs. 490 crore, and expects margins to rise to 17-18 percent from 16 percent.

Let's break down the math. Starting from Rs 490 crore in profit, reaching Rs 2,400-2,500 crore means adding roughly Rs 2,000 crore in incremental profit. Where does this come from?

Aquapharm Contribution: The acquired business already generates Rs 280 crore in profit. Post-integration synergies and scale benefits could push this to Rs 400-500 crore. That's one-quarter of the target right there.

Specialty Chemicals Growth: PCBL aspires to grow the share of specialty chemicals in PCBL's overall business to 60% in the coming five years which will also lead to higher margins. With Aquapharm as a platform, bolt-on acquisitions and organic expansion could add another Rs 500-700 crore.

Carbon Black Optimization: Even the commodity business has room to grow. The specialty expansion of 20,000 MTPA at Mundra plant is underway and expected to commission this year, raising the Specialty Blacks capacity to 1.12 lakh MTPA. Brownfield expansion of 90,000 MTPA carbon black is also started at the Chennai facility, boosting total capacity to 8.8 lakh MTPA.

New Ventures: PCBL will also enter the cathode chemistry for electric vehicle (EV) batteries. It has acquired Kinaltek in Australia for this purpose and has successfully tried this on a pilot scale. This could be the wild card that takes profits beyond the 5X target.

The capital allocation is equally ambitious. Over the next 12 to 18 months, PCBL will be spending about Rs 350 bn. Over the next three years, the company plans to invest about Rs 500 bn. This isn't just maintenance capex—it's transformation spending on a massive scale.

What makes this vision credible rather than delusional? First, the track record. Goenka has already delivered dramatic turnarounds at PCBL and other group companies. Second, the market dynamics are favorable—specialty chemicals are growing at double-digit rates globally, and India is gaining share. Third, the execution capability is proven—PCBL has successfully integrated acquisitions and built new plants on time and budget.

But there are significant risks. Integration challenges with Aquapharm could delay synergy realization. The specialty chemicals market is competitive, with established players like BASF, Clariant, and Chinese companies fighting for share. Technology disruption—new chemistries, bio-based alternatives—could obsolete existing products. And critically, funding this growth requires taking on debt at a time when interest rates are elevated.

The market's reaction has been telling. Following the announcement of the RP-Sanjiv Goenka Group (RPSG)'s five-year growth plans by Chairman Sanjiv Goenka, RPSG Group companies—primarily PCBL and CESC—have seen their overall market capitalisation increase by more than Rs. 16,000 crores in just one month. PCBL's market capitalization shot up to ₹18,306 crore, reflecting investor belief in the transformation story.

Yet skeptics have valid concerns. ICICI Securities noted: "The acquisition price looks decent and is broadly in line with what PCBL trades and with better margins. It is however an unrelated diversification." The shift from carbon black to specialty chemicals isn't a natural adjacency—it requires different capabilities, customer relationships, and competitive dynamics.

The 5X vision ultimately rests on Goenka's ability to execute multiple transformations simultaneously—integrating Aquapharm, scaling specialty chemicals, optimizing carbon black, and potentially entering battery materials. It's an ambitious agenda that would challenge any management team. But then again, betting against Sanjiv Goenka has rarely been profitable.

VIII. Competition & Market Dynamics

The competitive landscape in both carbon black and specialty chemicals reads like a game of three-dimensional chess. In carbon black, PCBL faces global giants with deep pockets and massive scale. In specialty chemicals, they're entering a market where relationships and technical expertise matter more than production capacity. Understanding these dynamics is crucial to evaluating whether PCBL's transformation can succeed. In the global carbon black arena, PCBL is David facing multiple Goliaths. The carbon black market is consolidated. The top five players account for more than 50% of the market share. The major companies for the carbon black market include Birla Carbon, Orion Engineered Carbon, Cabot Corporation, Jiangxi Black Cat Carbon Black Co.

Birla Carbon: The undisputed king, part of the Aditya Birla Group, operates globally with 16 facilities across 12 countries, producing 2 million tonnes annually. They're three times PCBL's size and have the advantage of being part of a $60 billion conglomerate. Their recent acquisition of Nanocyl SA in October 2023, strengthening its position in battery materials for lithium-ion batteries, shows they're not standing still.

Cabot Corporation: The American giant with 140+ years of history and deep pockets for R&D. In November 2024, Cabot declared increasing prices for carbon black globally, demonstrating pricing power that smaller players like PCBL struggle to match. Their focus on specialty blacks and advanced materials puts them directly in PCBL's transformation path.

Orion Engineered Carbons: The European powerhouse with 14 manufacturing facilities across the globe and the world's oldest carbon black plant in Germany. In 2023, Orion unveiled its first circular specialty carbon black for polymers, showing innovation capabilities that set industry standards. Their partnerships with tire recycling firms position them well for the sustainability trend.

The Chinese players present a different challenge. Companies like Jiangxi Black Cat operate with massive scale advantages and lower cost structures, though environmental regulations have constrained their growth. When China sneezes, the global carbon black market catches a cold—supply disruptions in China can create temporary opportunities for Indian players, but the long-term threat of Chinese overcapacity always looms.

In India, PCBL's 40% market share looks dominant, but it's constantly under threat. Himadri Speciality Chemical, Rain Industries, and Goa Carbon are all expanding capacity. The barriers to entry in carbon black aren't insurmountable—any company with access to feedstock and environmental clearances can build a plant.

The specialty chemicals competitive landscape is even more complex. Here, PCBL (post-Aquapharm) faces a different set of rivals:

Global Specialty Chemical Giants: BASF, Clariant, Solvay, and Evonik have decades of experience, thousands of products, and deep customer relationships. They can bundle products, offer global supply contracts, and invest billions in R&D. PCBL's specialty chemicals revenue would be a rounding error for these companies.

Indian Specialty Players: Companies like Aarti Industries, Vinati Organics, and Clean Science have built focused specialty chemical businesses with impressive margins and growth rates. They've proven that Indian companies can compete globally in specialty chemicals, but they've also shown how difficult it is to build these businesses.

Chinese Competition: Despite environmental crackdowns, Chinese specialty chemical companies remain formidable competitors, especially in phosphonates where they have significant capacity. Their ability to operate at lower margins during downturns makes them dangerous competitors.

The technology disruption threat is particularly acute. Electric vehicles don't just change tire demand—they change the entire materials landscape. EV batteries need different chemicals than combustion engines. Autonomous vehicles might dramatically reduce tire wear through optimized driving. 3D printing could disrupt traditional manufacturing processes that use carbon black.

Sustainability pressures are reshaping competition. Recovered carbon black from tire recycling is becoming commercially viable. Companies like Pyrum Innovations and Alpha Carbone are scaling up production. While recovered carbon black can't yet match virgin quality for all applications, it's improving rapidly and appeals to environmentally conscious customers.

What's PCBL's competitive advantage in this landscape? It's not scale (Birla is bigger), technology (Cabot has better R&D), or cost (China is cheaper). PCBL's advantage is agility—the ability to serve Indian customers better than global players while being more sophisticated than local competitors. The Aquapharm acquisition gives them a specialty chemicals platform to build on, but they're still playing catch-up.

The market dynamics are shifting in ways that could benefit PCBL. The "China Plus One" strategy means global companies need alternative suppliers. India's manufacturing push under "Make in India" creates local demand. Environmental regulations are leveling the playing field by raising costs for polluting producers. But these same dynamics attract new competitors and intensify rivalry among existing players.

PCBL's strategy appears to be creating a unique position—not trying to out-Birla Birla in carbon black, but building a hybrid model that combines commodity and specialty chemicals. It's a narrow path to walk, requiring excellent execution and a bit of luck. The competition won't stand still while PCBL transforms itself.

IX. Financial Analysis & Unit Economics

The numbers tell the story of transformation—and tension. PCBL's current financials show Mkt Cap: 14,345 Crore, Revenue: 8,375 Cr, Profit: 411 Cr. It is trading at not too expensive PE of 25 with ROE of over 16%. PCBL debt is around 1.5x. These metrics reflect a profitable, moderately leveraged company—but one about to undergo radical change.

Let's dissect the unit economics of both businesses:

Carbon Black Economics: The carbon black business is all about scale and efficiency. Raw materials (carbon black feedstock and tar oil) account for 60-70% of costs. Energy adds another 15-20%. The gross margins typically range from 25-30%, but EBITDA margins compress to 12-15% after accounting for fixed costs. The business is highly capital intensive—setting up a 100,000 TPA plant requires Rs 300-400 crore investment. Return on capital employed (ROCE) in the carbon black business typically ranges from 12-15%, decent but not spectacular.

Specialty Chemicals Economics: ACPL clocked sales of Rs 2,009 crore as of FY23, gross margins of 31 per cent, EBITDA of Rs 417 crore (EBITDA margins 21 per cent) and PAT of Rs 280 crore. These 21% EBITDA margins compared to carbon black's low teens represent a fundamental improvement in business quality. The working capital requirements are lower—specialty chemicals customers often pay advances for custom products. The asset turnover is higher since you're selling knowledge and formulations, not just processed carbon.

The Aquapharm acquisition math is particularly interesting. At Rs 3,800 crore for Rs 280 crore of profit, PCBL paid roughly 13.5x P/E—not cheap, but reasonable for a growing specialty chemicals business. The acquisition is expected to be EPS accretive from year one, assuming successful integration.

PCBL expects to cumulatively generate around Rs 4,000 of EBITDA/CFO over next 30 months (PCBL+ACPL) which will help indirectly fund the acquisition (repay debt). This suggests confidence in cash generation capabilities, critical for managing the increased leverage.

The capital allocation framework going forward is ambitious. Over the next 12-18 months, the group plans to allocate ₹35,000 crore for capex, though this is for the entire RPSG group, not just PCBL. The PCBL-specific expansion plans are more modest but still significant—specialty blacks capacity expansion and brownfield carbon black projects.

The debt position post-Aquapharm needs careful monitoring. Adding Rs 3,800 crore of acquisition debt to existing borrowings will push net debt/EBITDA to around 3-3.5x, higher than the current 1.5x but manageable if integration proceeds smoothly. The interest coverage ratio will decline but should remain healthy above 3x.

Working capital dynamics differ significantly between the two businesses. Carbon black has a typical cash conversion cycle of 60-70 days—you need to hold feedstock inventory, production takes time, and customers (tire companies) have negotiating power on payment terms. Specialty chemicals can have a negative working capital cycle for custom products where customers pay advances.

The margin progression story is compelling. The chairman stated in an interview that the company's margins are projected to expand from 16% to 18%. This 200 basis point improvement might seem modest, but on Rs 10,000+ crore revenue base, it translates to Rs 200 crore of additional EBITDA.

The CAPEX requirements going forward are substantial but manageable. Carbon black expansion can be done in brownfield mode at Rs 3,000-3,500 per ton, significantly cheaper than greenfield. Specialty chemicals capacity additions are even more capital efficient—often just requiring additional reactors and storage tanks rather than entirely new plants.

Return on capital employed (ROCE) should improve with the specialty chemicals mix. While carbon black generates 12-15% ROCE, specialty chemicals can deliver 20-25% ROCE. As the mix shifts toward specialty, overall ROCE should trend toward 18-20%, justifying premium valuations.

The financial engineering aspect of the Aquapharm deal deserves attention. By using a mix of debt and internal accruals, PCBL maintains flexibility. They could potentially refinance at lower rates once integration is proven, or even consider an equity raise if market conditions are favorable.

Currency exposure is a hidden factor. With significant exports and imported feedstock, PCBL has natural hedging to some extent. The Aquapharm acquisition adds international operations, further diversifying currency risk. A weakening rupee generally helps profitability, making exports more competitive.

Tax optimization opportunities exist post-acquisition. Aquapharm's international operations could allow for better tax planning. The specialty chemicals business might qualify for certain incentives under production-linked incentive (PLI) schemes.

The key financial risk is integration execution. If Aquapharm's margins deteriorate during integration, or if customer losses occur, the financial math changes dramatically. A 300 basis point margin compression at Aquapharm would wipe out Rs 60 crore of EBITDA, making the debt burden harder to bear.

Yet the financial upside is equally dramatic. Goenka earlier highlighted that PCBL plans to expand its specialty blacks segment, aiming for profit growth of at least 5x over the next five years, expects its profit to reach between Rs. 2,400 crores and Rs. 2,500 crores, up from the current Rs. 490 crore. Achieving this would transform PCBL into one of India's most valuable chemical companies.

X. Playbook: Lessons for Operators & Investors

The PCBL story offers a masterclass in industrial transformation, with lessons that extend far beyond chemicals. Here's the playbook for operators and investors watching similar transitions:

When to Pivot from Commodity to Specialty: The timing of PCBL's pivot is instructive. They didn't move when carbon black was struggling (2013-14)—that would have been desperation. They moved when the business was fixed, profitable, and generating cash (2023). Lesson: Transform from a position of strength, not weakness. You need the cash flow from the commodity business to fund the specialty transformation. Too early, and you lack resources; too late, and you miss the opportunity.

The Conglomerate Advantage in Emerging Markets: PCBL benefits enormously from being part of the RPSG Group. Access to capital, management talent, government relationships, and cross-selling opportunities all matter in India. Unlike developed markets where conglomerate discounts are common, emerging markets often see conglomerate premiums. The key is active management—Sanjiv Goenka's hands-on approach, versus the passive holding company model, makes the difference.

Family Business Succession Done Right: The 2011 split between Harsh and Sanjiv Goenka could have been messy. Instead, it was clean, allowing both brothers to pursue their visions. The lesson: Clear separation is better than continued joint ownership with diverging visions. Sanjiv's subsequent transformation of his inherited businesses shows that next-generation leaders can be change agents, not just caretakers.

M&A as Transformation Catalyst: The Aquapharm acquisition isn't just about buying earnings; it's about buying capabilities, customer relationships, and most importantly, time. Building Aquapharm's position organically would take 10-15 years. The lesson: Use M&A to leapfrog into new businesses, but ensure you have the management bandwidth to integrate. PCBL's measured approach—one large acquisition, then digest—is smarter than serial acquisition sprees.

Building Global from India: PCBL's global ambitions face the challenge all Indian companies face: How do you compete globally from an emerging market base? Their strategy is instructive: Dominate the home market first, use exports to build relationships, then acquire international assets. The Aquapharm facilities in the US and Saudi Arabia give PCBL legitimate global production capabilities, not just an export story.

The Technology Adoption Framework: PCBL isn't trying to be a technology leader—they're being smart followers. Let Cabot and BASF spend billions on R&D, then license or adapt proven technologies. The investment in green power generation shows pragmatic technology adoption—proven technology that provides immediate economic benefits. The EV battery materials venture is more speculative but sized appropriately as an option, not a bet-the-company move.

Capital Allocation Discipline: Despite the bold 5X vision, PCBL maintains capital allocation discipline. The carbon black business still gets maintenance capex and modest expansion, providing stable cash flows. The specialty chemicals transformation is funded through one large acquisition plus organic growth, not a series of risky bets. The debt levels, while elevated post-acquisition, remain within reasonable bounds.

Managing Multiple Stakeholders: Public company transformation is harder than private—you need to bring along public shareholders, debt investors, employees, and customers. PCBL's communication strategy is noteworthy: Bold enough to excite investors (5X growth!) but with enough operational detail to maintain credibility. Regular investor calls, plant visits, and transparent reporting build confidence during transformation.

The Importance of Market Timing: PCBL's transformation coincides with favorable macro trends: China Plus One, Make in India, global supply chain diversification, and ESG pressures. This isn't luck—it's reading the macro environment and moving accordingly. The lesson: Major transformations should align with, not fight against, macro trends.

Operational Excellence as Foundation: Before attempting transformation, PCBL fixed its core operations. The 2012-2020 period of operational improvement created the foundation for transformation. You can't transform a broken business; you need operational excellence as the platform for strategic change.

Risk Management in Transformation: PCBL's approach to risk is nuanced. They're taking strategic risk (new business, large acquisition) while managing operational risk (keeping existing business stable) and financial risk (maintaining reasonable leverage). Too often, companies take all three risks simultaneously and fail.

The Portfolio Approach: Rather than betting everything on specialty chemicals, PCBL is building a portfolio: commodity carbon black for cash flow, specialty blacks for growth, specialty chemicals for margins, and options in battery materials. This portfolio approach provides resilience—if one bet fails, others can compensate.

Cultural Transformation: The hardest part isn't strategy or financing—it's culture. Moving from a commodity mindset (cost and efficiency) to specialty mindset (innovation and customer intimacy) requires different people, processes, and values. Goenka's willingness to change management in 2012 shows that cultural transformation sometimes requires personnel change.

For Investors: The Transformation Multiple: Markets typically value successful transformations at premium multiples. If PCBL successfully becomes a specialty chemicals company, it should trade at specialty chemicals multiples (20-25x P/E) rather than commodity multiples (10-15x P/E). The stock price appreciation potential isn't just from earnings growth but multiple expansion.

The Execution Premium: In emerging markets, the ability to execute complex transformations is rare. Companies that demonstrate this capability—like PCBL appears to be doing—deserve premium valuations. The execution track record becomes a moat itself, attracting better talent, partners, and investors.

XI. Bear Case vs. Bull Case

Bear Case: Why This Could Go Wrong

The bear case for PCBL starts with the fundamental challenge of EV disruption. Electric vehicles aren't just changing powertrains; they're reshaping the entire automotive supply chain. EVs are heavier than conventional vehicles, which increases tire wear, but they also enable regenerative braking, which reduces it. More critically, autonomous vehicles could reduce global vehicle miles traveled by 50% through ride-sharing and optimization. Fewer miles means fewer tire replacements, directly hitting carbon black demand.

The integration execution risk is substantial. Aquapharm has been run by its founders as an entrepreneurial venture. Integrating it into a corporate structure while maintaining its innovation culture and customer relationships is notoriously difficult. History is littered with specialty chemicals acquisitions that destroyed value through poor integration—customer defections, key employee departures, and cultural mismatches.

The valuation looks expensive for what remains predominantly a commodity business. Trading at PE of 25 with ROE of over 16%, PCBL is priced for perfection. Any execution stumbles, margin compression, or slower-than-expected growth could trigger significant multiple compression. The market is pricing in successful transformation, leaving little room for error.

Global recession risks loom large. Carbon black demand is highly correlated with industrial production and automotive sales. A global slowdown would hit both volume and pricing. Specialty chemicals, while more resilient, aren't immune to economic cycles. Customer destocking, project delays, and price pressures during recessions can significantly impact profitability.

Competition is intensifying, not easing. Birla Carbon's acquisition of Nanocyl shows large players aren't standing still. Chinese overcapacity in both carbon black and specialty chemicals remains a structural overhang. When Chinese producers need cash, they dump products globally at marginal cost, destroying pricing for everyone.

The technology risk extends beyond EVs. Bio-based alternatives to carbon black are advancing rapidly. Recovered carbon black from tire pyrolysis is becoming commercially viable. New materials like graphene could eventually replace carbon black in certain applications. PCBL's R&D spending, while increased, may not be sufficient to stay ahead of technological disruption.

Debt levels post-Aquapharm acquisition leave little room for error. At 3-3.5x net debt/EBITDA, PCBL has limited financial flexibility. If cash flows disappoint or integration costs exceed expectations, the company could face covenant pressures. Rising interest rates globally make refinancing risk real.

Bull Case: Why This Could Be Brilliant

The bull case starts with the addressable market opportunity. Industry addressable market size is vast and there seems to be no substitute for tyres or carbon black to make them yet. Even with EV disruption, global tire demand continues growing, driven by increasing vehicle populations in emerging markets. India's vehicle penetration is still just 30 per 1,000 people versus 800+ in developed markets—massive growth runway remains.

The specialty chemicals structural growth story is compelling. Water scarcity, environmental regulations, and industrial growth drive sustained demand for water treatment chemicals. Over this time, a bunch of Indian companies started focusing on the specialty side. And with that, we slowly started becoming a bigger player in the global specialty chemical export market. For some products — like dyes, pigments, or surfactants — we are already among the world's top exporters. This shift was catalysed by China's exit from the market. A few years ago, China started cracking down on pollution in its chemical factories, shutting many of them down. That made a lot of global buyers look for alternative suppliers — and India stepped up.

The management track record inspires confidence. Goenka has already delivered one successful turnaround at PCBL, taking it from losses to profitability. His broader track record across RPSG companies shows consistent execution ability. When experienced operators make bold predictions, they often have information and insights that outsiders lack.

India's manufacturing advantage is real and growing. Labor costs remain competitive, the regulatory environment is improving, and government support through PLI schemes provides tailwinds. PCBL's established infrastructure, relationships, and capabilities position it perfectly to capture India's industrial growth.

PCBL has recently acquired Aquapharm, a speciality chemical company, for 3850 cr and management's confidence about growth is coming from this acquisition. It aspires to grow the share of specialty chemicals in PCBL's overall business to 60% in the coming five years. This isn't incremental change—it's fundamental business model transformation. If successful, PCBL becomes a completely different company deserving of specialty chemicals valuations.

The synergy potential is significant and achievable. Cross-selling Aquapharm products to PCBL's carbon black customers is natural. Using PCBL's global distribution network for Aquapharm products reduces selling costs. Operational synergies in procurement, logistics, and overhead could add Rs 50-100 crore to EBITDA.

The balance sheet strength, despite increased leverage, remains adequate. The company's ability to generate Rs 4,000 crore of operating cash flow over 30 months provides a clear path to deleveraging. Asset-light specialty chemicals growth requires less capex than carbon black expansion, improving cash generation.

Market dynamics favor established players. Environmental regulations create barriers to entry. Customer relationships in specialty chemicals are sticky. PCBL's combined scale post-Aquapharm makes it a meaningful player globally, not just in India.

The Verdict:

The bear and bull cases are both credible, which explains the market's volatile reaction to PCBL's transformation story. The outcome likely depends on execution over the next 18-24 months. If Aquapharm integration proceeds smoothly and specialty chemicals growth accelerates, the bull case dominates. If integration challenges emerge or macro conditions deteriorate, the bear case becomes reality.

For investors, this presents a classic risk-reward calculation. The downside might be 30-40% if transformation fails, but the upside could be 100-200% if successful. Your view depends on your assessment of management's execution ability and your tolerance for transformation risk.

XII. Final Analysis & Predictions

Is This India's BASF in the Making?

The comparison to BASF is ambitious but not entirely fantastical. BASF started as a dye manufacturer in 1865 and transformed itself into the world's largest chemicals company through relentless innovation, strategic acquisitions, and geographic expansion. PCBL's journey from carbon black to specialty chemicals echoes this evolution, albeit compressed into decades rather than centuries.

What PCBL has going for it is timing. India's chemicals industry is where China's was 20 years ago—poised for explosive growth with improving capabilities and cost advantages. The regulatory tailwinds from China's environmental crackdowns create a once-in-a-generation opportunity for Indian chemical companies to capture global share.

But becoming India's BASF requires more than market opportunity. It demands sustained R&D investment, technological leadership, and the ability to attract world-class talent. PCBL's current R&D spending, while increased, remains a fraction of global leaders'. Building innovation capabilities takes decades, not years.

The Next 5 Years: Will They Hit 5X?

PCBL plans to expand its specialty blacks segment, aiming for profit growth of at least 5x over the next five years, expects its profit to reach between Rs. 2,400 crores and Rs. 2,500 crores, up from the current Rs. 490 crore. Let's stress-test this projection.

The math is aggressive but not impossible. Starting from Rs 490 crore base, reaching Rs 2,400 crore requires adding Rs 1,910 crore in incremental profit. Aquapharm contributes Rs 280 crore immediately. Assuming 15% annual growth in the combined specialty chemicals business yields another Rs 400 crore over five years. Carbon black volume growth and margin expansion could add Rs 500 crore. The remaining Rs 730 crore would need to come from new initiatives, acquisitions, or better-than-expected execution.

The key variables are margin expansion and successful integration. If EBITDA margins reach 18% as projected on Rs 15,000 crore revenue (achievable with 20% annual growth), that's Rs 2,700 crore EBITDA. With Rs 300 crore depreciation and Rs 400 crore interest, PBT would be Rs 2,000 crore, yielding Rs 1,500 crore PAT—falling short of the 5X target but still representing tremendous growth.

My prediction: PCBL achieves 3.5-4X profit growth over five years—falling short of the 5X ambition but still delivering exceptional returns. The shortfall comes from integration challenges and competitive pressure on margins, partially offset by better-than-expected volume growth.

What Could Go Wrong?

The biggest risk isn't what's visible but what's unknowable. A breakthrough in tire technology that eliminates carbon black. A global pandemic that reshapes transportation. A financial crisis that freezes credit markets. These tail risks can't be modeled but could derail any transformation.

More predictable risks include execution failures. If key Aquapharm customers defect to competitors, if integration costs balloon, if culture clashes prevent synergy realization—any of these could turn the acquisition into a value destroyer. The history of Indian companies making large acquisitions is mixed at best.

Regulatory changes could upset the apple cart. Environmental regulations that ban certain phosphonates. Tax changes that eliminate export incentives. Labor laws that prevent restructuring. In India's complex regulatory environment, policy shifts can dramatically impact business models.

Competition could intensify beyond expectations. If Birla Carbon or global players decide to aggressively defend their position through pricing actions, margins could compress dramatically. Chinese players, despite environmental pressures, could flood markets with excess capacity during their economic downturns.

Investment Decision Framework

For investors considering PCBL, here's a framework for decision-making:

Buy if you believe:

- Management can execute complex M&A integration

- Specialty chemicals margins are sustainable despite competition

- India's manufacturing story has multi-decade runway

- The conglomerate structure adds rather than destroys value

- 15-20% earnings CAGR justifies current valuations

Avoid if you believe: - EV disruption will severely impact tire demand near-term - Integration risks outweigh synergy potential - China will remain the dominant low-cost producer - Commodity chemicals will face structural headwinds - Current valuations price in perfect execution

Hold and watch if you believe: - The story is compelling but execution uncertain - Next 2-3 quarters will provide clarity on integration - Macro conditions need to stabilize before committing - Valuation needs to correct for better risk-reward

My assessment: PCBL represents a compelling transformation story with above-average execution risk. For investors with 5+ year horizons and tolerance for volatility, it's an attractive bet on India's chemical industry evolution. For conservative investors seeking predictable returns, better opportunities exist elsewhere.

The ultimate question isn't whether PCBL can transform—it's whether they can transform fast enough. The window of opportunity from China's retrenchment won't stay open forever. Global chemical companies are also eyeing India. The race is on, and PCBL has placed its bet. Time will tell if Sanjiv Goenka's boldness pays off or becomes a cautionary tale of transformation ambition exceeding execution capability.

XIII. Recent News

The latest quarterly results paint a nuanced picture of PCBL's transformation journey. PCBL Chemical Ltd's revenue jumped 54.77% since last year same period to ₹2,575.29Cr in the Q3 2024-2025, reflecting the Aquapharm consolidation. However, PCBL Chemical Ltd's net profit fell -37.07% since last year same period to ₹93.05Cr in the Q3 2024-2025, with net profit margin fell -59.34% since last year same period to 3.61%.

These numbers reveal the integration challenges and margin pressures that often accompany major acquisitions. The revenue growth is impressive but profit compression suggests either integration costs, competitive pricing pressure, or operational challenges in merging two distinct businesses.

For Q4 FY2024, PCBL Ltd has seen mixed performance - while the operating profit and net sales were the highest in the last five quarters, the profit before tax and interest cost have decreased. The interest cost has also increased by 234.23% quarter on quarter, indicating increased borrowings from the Aquapharm acquisition.

The stock market reaction has been volatile. PCBL Chemical Q1 Results: Stock tanks 5% after topline, margin fall from last year, reflecting investor concerns about execution. Yet the stock has still delivered strong returns over longer periods, suggesting underlying confidence in the transformation story.

Management updates remain optimistic. The company filed its 64th AGM notice and FY 2024-25 Integrated Report with audited financials and strategic updates in August, maintaining guidance for long-term growth despite near-term margin pressures.

Industry developments continue to favor PCBL's strategy. Environmental crackdowns in China persist, supporting pricing for both carbon black and specialty chemicals. The push for electric vehicles and sustainability continues creating new opportunities in battery materials and green chemicals.

The stock currently trades around ₹390, with day range between ₹389.05 - ₹400.50, showing continued investor interest despite volatility. The market cap of ₹14,345 Crore reflects significant value creation from the transformation announcement, though below peak levels.

Recent operational updates show progress on capacity expansion plans. The specialty blacks expansion and brownfield carbon black projects remain on track, suggesting operational execution continues despite integration challenges.

XIV. Links & Resources

Official Company Resources: - PCBL Annual Reports: www.pcblltd.com/investor-relation/financials/annual-reports - Quarterly Results: www.pcblltd.com/investor-relation/financials/quarterly-results - Corporate Presentations: www.pcblltd.com/communication - Stock Exchange Filings: NSE India portal for PCBL

Industry Research: - International Carbon Black Association (ICBA) Resources - Indian Chemical Council Industry Reports - Specialty Chemicals Market Analysis by KPMG, EY, PwC - China Carbon Black Industry Association Reports (for competitive intelligence)

Technical Resources: - Carbon Black Manufacturing Process Guidelines - Phosphonates Chemistry and Applications - Water Treatment Chemicals Technical Papers - Tire Industry Requirements for Carbon Black Specifications

Regulatory & Compliance: - Competition Commission of India Filings for Aquapharm Acquisition - Environmental Clearance Documents for Plant Expansions - SEBI Disclosures and Corporate Governance Reports - Production Linked Incentive (PLI) Scheme Details for Chemicals

Market Intelligence: - Screener.in PCBL Analysis - Trendlyne Financial Data - MarketsMojo Quarterly Result Analysis - Industry Trade Publications

Management Interviews & Insights: - Sanjiv Goenka's Vision Interviews (CNBC, ET Now) - Analyst Conference Call Transcripts - Industry Conference Presentations - Forbes India and Business Today Features on RPSG Group

Competition Analysis: - Birla Carbon Annual Reports and Sustainability Reports - Cabot Corporation Investor Presentations - Orion Engineered Carbons Financial Filings - Chinese Carbon Black Manufacturers Export Data

Academic & Technical Papers: - "Carbon Black: Science and Technology" - Technical Reference - "Specialty Chemicals in India: Growth Dynamics" - Industry Studies - "Water Treatment Chemicals Market Evolution" - Research Papers - "EV Impact on Traditional Auto Supply Chains" - Academic Analysis

Investment Research: - Broker Reports (ICICI Securities, Motilal Oswal, HDFC Securities) - Rating Agency Reports on PCBL Debt - Equity Research Reports Post-Aquapharm Acquisition - Peer Comparison Studies

This analysis represents an independent assessment based on publicly available information as of August 2025. It should not be considered as investment advice. Potential investors should conduct their own due diligence and consult with financial advisors before making investment decisions. The transformation of PCBL from a carbon black manufacturer to a specialty chemicals player represents both significant opportunity and substantial risk. The outcome will depend on execution over the coming years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube