Patel Engineering: The Masters of the Underground

I. Introduction: The "Hidden" Infrastructure Giant

Picture a narrow, dimly lit construction adit in Arunachal Pradesh, two kilometres inside a mountain. The air is thick with diesel fumes and rock dust. A Tunnel Boring Machine the length of two football fields grinds forward at the geological pace of roughly twenty metres a day, chewing through Himalayan schist that has not seen sunlight in 50 million years. Every few hundred metres the geology changes — what the engineers call a "geological surprise" — and the entire crew has to stop, re-survey, and decide whether to push, retreat, or grout. Each day of delay costs roughly a crore.

This is the world पटेल इंजीनियरिंग Patel Engineering Limited lives in. And almost nobody in Indian markets — outside the small fraternity of infrastructure analysts — actually knows what they do.

Ask the average retail investor in मुंबई Mumbai to name India's big infra companies and you'll hear the same five names: लार्सन एंड टुब्रो Larsen & Toubro, अदानी Adani, रिलायंस Reliance, NCC, IRB. Patel Engineering rarely makes the list. And yet, by the time you finish reading this article, you'll understand that when the Government of India needs to bore a fifteen-kilometre headrace tunnel through the Himalayas, or build an underground powerhouse cavern the size of an aircraft hangar inside a mountain, or sink a vertical shaft 400 metres deep — they don't call L&T. They call PEL.

The numbers underline the specialism. The company has executed more than 300 kilometres of tunneling and contributed to over 85 dams across the subcontinent, and has been involved — in one form or another — in nearly every major hydroelectric project India has built in the last four decades.1 That is not a generalist's resume. That is a specialist's monopoly.

Here's the roadmap for the next two hours. We'll start in 1949, in the year of India's independence, with a Sindhi family that arrived in Bombay with not much more than their name and a willingness to do the work no one else wanted. We'll track their slow accumulation of competence in जलविद्युत hydroelectric engineering and सुरंग tunneling — the two narrowest, most technically demanding sub-segments of Indian civil construction. We'll then walk through what we call the "lost decade" — the 2008-to-2018 period when PEL almost destroyed itself by chasing the infrastructure super-cycle into real estate, thermal power, and toll roads. We'll dwell on the S4A debt restructuring of 2016 — one of the most consequential, least understood corporate turnarounds in Indian markets. And we'll end in the present, where PEL has re-positioned itself as the EPC contractor of choice for India's emerging पंप्ड स्टोरेज परियोजना Pumped Storage Project build-out — what the grid engineers, with mild exaggeration, call "the world's largest battery."

This is a story about an unfashionable company in an unfashionable industry that almost died, sold off most of itself to survive, and rediscovered why it existed in the first place. The lesson, if there is one, is something close to Charlie Munger's old line: stay inside your circle of competence. PEL forgot it for a decade. They remembered it just in time.

II. Foundation & The Specialized Niche

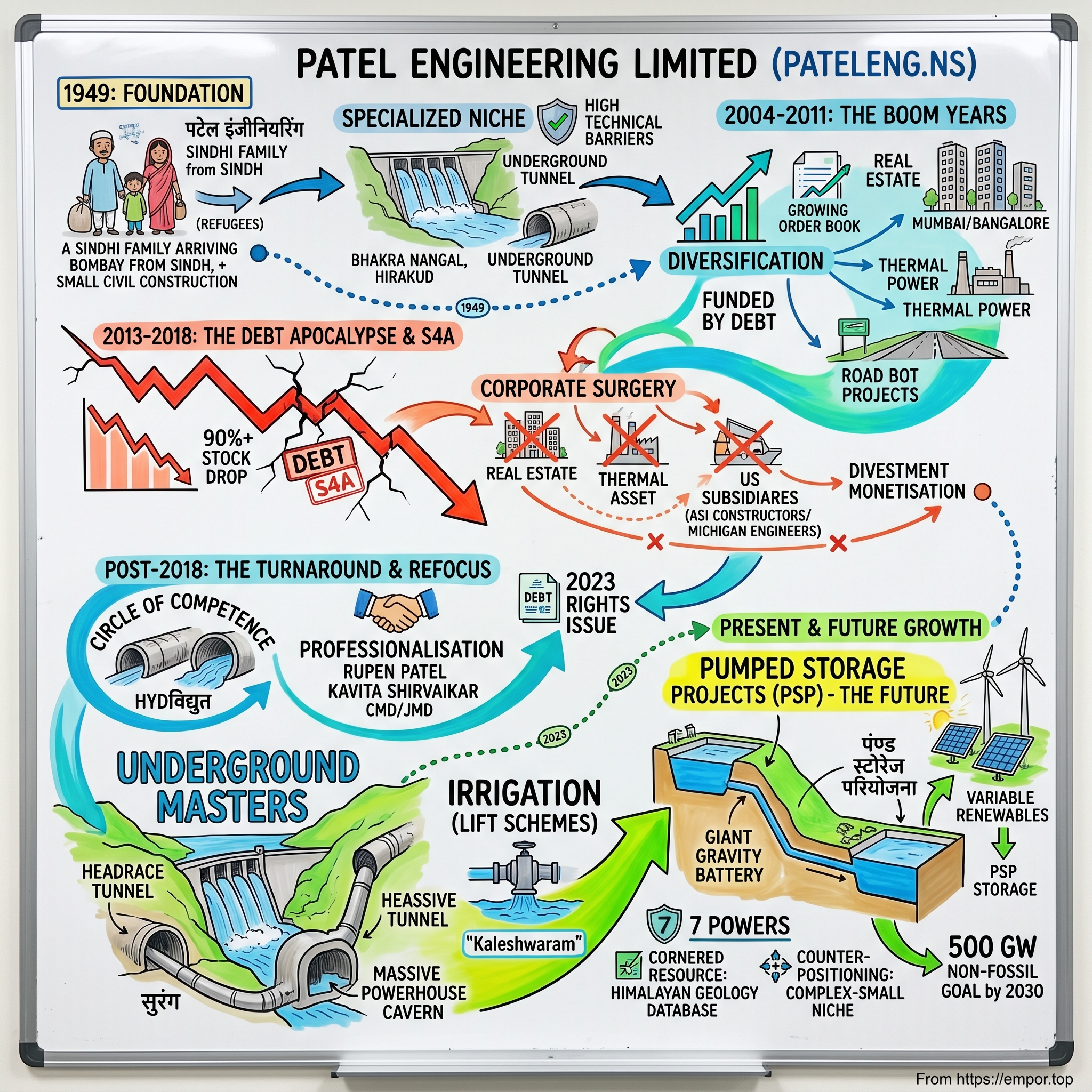

The Patel family did not arrive in Bombay as builders. They arrived as refugees.

The Partition of 1947 displaced roughly fifteen million people across the new India-Pakistan border, and among them was a stream of Sindhi families pushed out of सिंध Sindh province into Maharashtra and Gujarat. The Patels were among them. Two years after independence, in 1949, the family established Patel Engineering as a small civil construction outfit in Bombay, taking on the work that the British-era construction giants — Hindustan Construction Company, Gammon — considered too small or too remote to bother with.1

This is important context for understanding the company that exists today. PEL was not born inside the protected zamindari of the old industrial houses. It was born hungry, with no patronage, in a city where it had no real network. The only way to win was to do the technically hard work nobody else wanted.

The early 1950s in India were the dawn of what जवाहरलाल नेहरू Jawaharlal Nehru famously called the "temples of modern India" — the giant Soviet-style multipurpose dam projects that would generate hydroelectric power, irrigate millions of acres, and signal to the world that the newly independent republic could build at scale. Bhakra Nangal, Hirakud, Nagarjuna Sagar, the early stages of the दामोदर घाटी निगम Damodar Valley Corporation — these were the projects that defined the first three decades of Indian infrastructure.

PEL planted its flag in the hydro segment early and never really left. Why hydro? Two reasons, and they both matter for understanding the company even today.

First, the technical barriers in hydro and tunneling are extraordinarily high relative to road construction or building work. To win a hydro contract you need pre-qualification, and the pre-qualification process is brutal: you need to have already built a comparable project of comparable scale. This creates a powerful incumbency moat. A company that has built ten dams can bid on the eleventh; a company that has built none cannot bid on the first.

Second, the margins are structurally better. Generic road construction in India has long been a margin-thin, working-capital-heavy business where the winner is whoever can move dirt fastest at the lowest cost. Hydro and tunneling are different. The customer (almost always a public-sector enterprise like एनएचपीसी NHPC, एसजेवीएन SJVN, एनटीपीसी NTPC) is paying for engineering judgment as much as for execution. When something goes wrong inside a mountain — and something always does — the buyer wants a contractor whose people have seen this exact failure mode before.

By the 1980s and 1990s, PEL had become a fixture in Indian hydropower. They built dams. They built headrace tunnels (the long, gently sloping tunnels that bring water from a reservoir down to a powerhouse). They built underground powerhouses — caverns blasted out of solid rock, then lined with concrete, into which the turbines are installed. This is the work that does not photograph well. There is no glass facade, no LED-lit lobby. The output is a hole, and then water flowing through the hole, and then electrons.

The transition from family-run civil contractor to a modern EPC company happened gradually through the 1990s and early 2000s, as the second generation of the Patel family — and eventually Rupen Patel, who we'll spend more time on shortly — pushed the firm toward a more institutional structure. They listed on the stock exchanges, began publishing annual reports of the modern variety, and built out a professional engineering bench.

By the early 2000s, Patel Engineering occupied an unusual position in the Indian construction landscape: it was a mid-sized listed EPC firm with a disproportionately deep franchise in the most technically demanding corner of the industry. Most outside observers did not appreciate quite how good the moat was. Most insiders did. And in the next decade, the company would test that moat to its absolute breaking point — by trying to be something it was not.

III. The Boom, The Bust, and the "Lost Decade" (2004 – 2018)

In 2004 the world looked very different. The Sensex was climbing. Oil was cheap. The newly re-elected संयुक्त प्रगतिशील गठबंधन United Progressive Alliance government in Delhi was about to launch the most ambitious infrastructure program in independent India's history — the National Highways Development Project, the JNNURM urban renewal scheme, and a wave of hydro and ultra-mega power project clearances.

For a company like Patel Engineering, this should have been a golden decade. In some ways it was. The order book swelled. Revenue compounded at a rate that would have looked respectable inside any tech company. The stock — like every Indian infra stock — went vertical.

And then the management did what almost every Indian infra company did between 2004 and 2011. They diversified.

This is the part of the story where, if this were an Acquired podcast, Ben would lean back and David would say something dry about hubris. The diversification trap of the 2000s is one of the most studied case studies in Indian capital allocation, and PEL's version of it had the same essential pattern as everyone else's. The company moved into Bangalore and Mumbai real estate. They picked up thermal power assets. They built out a road BOT portfolio with long concession periods, where they would finance, build, own, and operate toll roads for fifteen or twenty years before transferring them back to the government. They acquired American subsidiaries to expand globally — ASI Constructors in dam construction, Michigan Engineers in micro-tunneling.[^4]

On paper, every one of these moves made sense in 2007. Real estate was compounding at 30% a year. Thermal power had captive coal allocations and assured offtake. Road BOTs were modelled out at 16% equity IRRs with conservative traffic assumptions. The American acquisitions brought in genuine technology — particularly micro-tunneling, which would later become an important capability for urban water and sewage projects in India.

The problem was that none of it was funded from internal accruals. It was funded with debt. And specifically, with the worst possible kind of debt: short-tenor, variable-rate, secured against assets that were either illiquid (real estate land banks) or had highly uncertain cash flows (BOT concessions, captive thermal plants whose coal blocks would eventually be de-allocated by the Supreme Court).

Then came 2011, and then 2012, and then the slow-motion train crash that the whole Indian infrastructure sector would call, for the rest of the decade, "the crisis."

Interest rates rose. The Reserve Bank tightened liquidity to fight inflation, pushing the marginal cost of funds for an over-leveraged infra company well into the mid-teens. Hydro projects in the Himalayas — including some PEL was executing — hit "geological surprises," the polite engineering term for the moment you bore into a mountain and discover that the rock is fractured, water-bearing, or under tectonic stress in ways the survey did not anticipate. Each surprise meant months of delay. Each month of delay meant working capital trapped at the project site. And the receivables from state-owned hydro buyers — एसजेवीएन SJVN, एनएचपीसी NHPC, state electricity boards — stretched from 90 days to 180 days to over a year.

By 2013, PEL was in serious trouble. The order book was full but the cash flows were not. The debt was real but the underlying assets were either non-earning or earning at rates well below the cost of carry. The stock fell more than 90% from its 2008 highs. For a brief, frightening window, there was an open question — discussed in hushed tones in Bombay's construction industry — about whether the firm would survive at all.

The inflection point came in 2016, when PEL became one of the first listed companies to invoke the Reserve Bank of India's तनावग्रस्त आस्तियों के स्थायी संरचना की योजना Scheme for Sustainable Structuring of Stressed Assets, mercifully shortened to S4A.4 The mechanics of S4A are worth understanding because they are unusual. Unlike a conventional debt restructuring, which simply extends tenors and reduces rates, S4A required the borrower's total debt to be split into two tranches: a "sustainable" portion (typically 50% or more) that the company would continue to service on commercial terms, and an "unsustainable" portion that would be converted into equity or equity-like instruments held by the lenders. In effect, the banks took ownership of the part of the debt the company could not actually pay.

It was, by any measure, a near-death experience. And it forced a question that the Patel family had to answer honestly: what business were they actually in?

The answer, when they finally arrived at it, was the same one their grandfather would have given in 1949. Tunnels. Dams. Hydropower. Water.

What followed was years of corporate surgery. Land banks in Bangalore and Mumbai were monetized.[^8] Stakes in BOT road assets were sold. The American subsidiaries were divested — Michigan Engineers was sold off in stages, with the residual stake exit reported by venture-capital trade press through the late 2010s.5 Thermal power exposure was wound down. The non-core subsidiaries that the company had assembled during the boom years were one by one cut loose.

By 2018 PEL was a smaller, leaner, far less glamorous company than it had been in 2008. The order book was concentrated in hydro and tunneling. The debt was lower, though still uncomfortable. The stock was a shell of its former self. But the foundations — the engineering team, the equipment fleet, the pre-qualification track record — were intact. The company had decided what it was, and what it was not.

What investors realized only later was that this surgical re-focusing had quietly positioned PEL for the single largest hydro-adjacent capex cycle India had ever seen.

IV. Current Management & Skin in the Game

Walk into the Patel Engineering headquarters in मुंबई Mumbai's विले पार्ले Vile Parle neighborhood and the first thing you notice is what is not there. There is no marble lobby. There are no public-relations consultants choreographing a corporate visit. The conference rooms are utilitarian. The walls are decorated with photographs of dams and tunnels — not awards, not lifestyle imagery, not the chairman cutting ribbons with politicians. It is a contractor's office, run by people who know they are contractors.

At the centre of this is Rupen Patel — Chairman and Managing Director, third generation of the founding family, and the executive who personally led the company through the S4A process and the strategic reset that followed.4

Rupen is not a typical Indian promoter-CEO. He does not give the kind of expansive prime-time television interviews that, say, an Adani or a Jindal scion gives. He talks, when he talks, almost entirely in operational terms — order book composition, finance cost trajectories, project execution milestones. The tone in earnings calls is closer to a CFO than to a charismatic founder.3 This is, in our view, exactly the right tone for a company whose past decade was defined by financial near-failure rather than financial excess.

Working alongside him is Kavita Shirvaikar, Joint Managing Director and Whole-Time Director, who came up through the finance function and was central to negotiating the S4A restructuring, the subsequent asset monetisations, and the 2023 rights issue.2 In a country where joint MDs at family-promoted infra companies are still overwhelmingly male and overwhelmingly drawn from the promoter family, Shirvaikar's elevation is itself a small but real signal about the professionalisation of the firm.

The shareholding structure tells the rest of the story. Promoter holding sits in the high 30s as a percentage of the company — meaningful skin in the game, but no longer the absolute promoter-controlled dominance that characterised the pre-crisis era.6 The float is held by a mix of domestic mutual funds, retail investors, and a steadily growing tail of FPI ownership. There is, importantly, no controlling foreign strategic, no private-equity overhang waiting to exit, and no listed holding-company parent skimming royalties.

The 2023 rights issue is worth dwelling on, because it tells you what the management is actually optimising for.[^3] A rights issue, in the Indian context, is one of the most promoter-aligned ways to raise primary equity capital. Existing shareholders — including the promoter family — are offered the right to subscribe to new shares at a discount, in proportion to their existing holdings. If the promoter family participates fully, their stake is maintained but they have to write a real cheque to do so. If they don't, they get diluted alongside everyone else.

The Patel family wrote the cheque. The proceeds went toward further debt reduction and working-capital strengthening, not toward an acquisition or a glamorous diversification. That is the kind of capital-allocation discipline that does not exist in a promoter family that has not been bruised. The Patels have been very bruised.

The internal incentive structure has shifted accordingly. In the pre-crisis decade, the implicit KPIs at PEL — like at most Indian infra companies — were top-line growth and order book size. Win the contract, book the revenue, raise the next round of debt against the order book, win the next contract. It was a model that worked beautifully until interest rates moved.

Post-S4A, the KPIs have visibly changed. Management commentary on earnings calls now leads with operating cash flow generation and finance cost reduction.3 The CFO function tracks net debt almost obsessively. Order book growth still matters, but it is now subordinated to order book quality — which contracts pay on time, which counterparties have good track records, which projects have low geological risk. This is what institutionalisation actually looks like, and it does not happen by accident. It happens because the people running the firm lived through a debt restructuring and never want to live through another one.

Which brings us, finally, to the part of the business that explains why the market has begun to pay attention again.

V. Hidden Gems: Micro-tunneling & Pumped Storage

Let us walk through what PEL actually builds today, because the segment mix has changed in ways that most casual observers have not caught up to.

The bread and butter remains hydro and tunneling, which together account for the majority of the revenue mix.1 This is the segment where the pre-qualification moat is strongest, the technical barriers are highest, and the margins — assuming the project doesn't go sideways — are the best in Indian construction. Inside this segment, the work is split roughly between three categories. There is conventional dam construction (the concrete arch and gravity dams that are the heroes of the old Nehru-era playbook). There is tunneling — both drill-and-blast and TBM (Tunnel Boring Machine) — primarily for hydroelectric headrace and tailrace tunnels. And there is underground powerhouse construction, which is essentially excavating a cavern several stories tall inside a mountain and then lining it with reinforced concrete to house the turbines.

The second segment is irrigation. The political economy of Indian irrigation is its own essay, but the short version is that state governments — particularly तेलंगाना Telangana and आंध्र प्रदेश Andhra Pradesh in the south — have been spending enormous sums on lift-irrigation schemes that pump water uphill from major rivers to irrigate dry plateaus. The Kaleshwaram project in Telangana is the most famous example; it involves pumping water from the गोदावरी Godavari river up several hundred metres of elevation through a chain of pumphouses and tunnels. This is, mechanically, very similar to hydroelectric construction. Same kinds of tunnels. Same kinds of underground caverns. Same equipment. Same skill set. PEL has won a meaningful share of this work.

The third segment, and the one investors are now most excited about, is पंप्ड स्टोरेज परियोजना Pumped Storage Projects — PSP.

If you have never thought about PSP before, here is the simplest possible explanation. A pumped storage project is two reservoirs at different elevations connected by tunnels. When the grid has surplus electricity — typically in the middle of the day, when solar is at peak generation — you use that surplus to pump water from the lower reservoir up to the higher one. When the grid needs electricity — typically in the evening, when solar drops off but demand peaks — you let the water flow back down through turbines and generate power. It is, in effect, a giant gravity battery. The round-trip efficiency is around 70% to 80%, which is competitive with lithium-ion batteries at grid scale, and the asset life is measured in many decades rather than years.

Why does this matter so much for India? Because the country has set itself a target of approximately 500 GW of non-fossil power capacity by 2030, with the bulk of incremental additions coming from solar and wind.[^8] Variable renewable generation creates a grid stability problem: the sun does not set on the same schedule as the evening demand peak. To make a renewable-heavy grid actually work, you need storage — and at grid scale, PSP is the cheapest, longest-duration storage technology that currently exists at commercial maturity.

The Central Electricity Authority's planning documents have laid out a pipeline of pumped storage projects totalling tens of gigawatts of nameplate capacity, with state utilities, central PSUs like NHPC and SJVN, and private players all in the bidding queue.[^12] Almost every one of those projects requires exactly the underground engineering capabilities — long tunnels, large caverns, complex headworks — that PEL has been building for seventy years.

This is where the "early mover" framing actually has teeth. PEL has been signing PSP contracts, both directly as EPC contractor and as the underground works partner to project developers, ahead of many of its larger generalist competitors. The pre-qualification advantage — those four decades of हिमालय Himalayan tunneling experience — translates directly into PSP eligibility, because PSP tunnel work is technically indistinguishable from hydroelectric tunnel work. You are simply moving water in both directions instead of one.

Crucially, PEL is now positioning itself almost entirely as the EPC contractor for these projects rather than as the project owner. This is a deliberate and very hard-won lesson from the previous decade. Owning the power plant means owning the merchant-power price risk, the long-term tariff risk, the PPA-counterparty risk, and the equity capital lock-in for fifteen to twenty years. Building the power plant and handing the keys to NHPC or SJVN means PEL gets paid in tranches as construction milestones are met, books a healthy EPC margin, and walks away. The same asset, with a radically different risk profile.

This is the asset-light pivot, and it is the single most important strategic decision the company has made in the last decade. It is also the reason the long-term return-on-capital arithmetic at PEL has the potential to look very different in this cycle than it did in the last one.

But the pivot is not without its risks, and to understand them you have to understand how PEL got into trouble through M&A in the first place.

VI. M&A & Capital Deployment: Benchmarking the Past

The M&A history of Patel Engineering is, in some ways, a perfect microcosm of the broader Indian corporate experience in the 2000s. Cross-border ambition. Technology acquisition. Premium valuations. And, ultimately, a painful unwind.

The two transactions that defined the era were the acquisition of ASI Constructors in the United States and the build-up of a controlling stake in Michigan Engineers, also US-based.[^4] Both were assembled in the boom years of the mid-to-late 2000s, both were thesis-driven (rather than financial-engineering deals), and both ended up being sold or substantially divested as part of the post-S4A surgery.

ASI Constructors was a specialist American dam and water-infrastructure contractor. The thesis was straightforward: Indian hydro contractors were dominant at home but had no real franchise abroad, and the US market — particularly the western states with their old dams in need of rehabilitation — offered both a margin and a diversification opportunity. The reality turned out to be different. American infrastructure procurement runs on a fundamentally different cadence than Indian procurement, with different contractual norms around risk allocation, different labour structures, and a customer base that strongly prefers incumbents with deep local relationships. The strategic rationale was sound, but the integration was harder than anticipated.

Michigan Engineers was a different bet — and in some ways the more interesting one. The acquisition brought into the group a mature micro-tunneling capability. Micro-tunneling is the technique used for urban infrastructure — water supply, sewage, telecom — where you need to install pipes underground without digging up the entire road above. It is exactly the technology Indian cities now need at scale, as urbanisation forces upgrades to sewage and water networks that were designed for populations a fraction of the current size. The technology transfer worked. PEL built up a domestic micro-tunneling capability that did not previously exist in India. But by the time the financial pressure of the debt crisis hit, the residual stake in the US entity had become a non-core distraction, and it was eventually exited as part of the broader monetisation programme.5

The benchmarking question — did they overpay? — has a nuanced answer. In nominal terms, yes. The acquisitions were funded substantially with debt at a time when both the dollar and Indian asset prices were near the top of the cycle, and the holding cost during the downturn was significant. In strategic terms, the verdict is more mixed. Micro-tunneling as a capability has paid for itself many times over. The American dam franchise, less so.

What is interesting is how completely the M&A playbook has now changed.

In the current era, PEL's capital deployment is almost entirely operational rather than corporate. Instead of buying companies, the firm buys specialised equipment — TBMs, drilling jumbos, micro-tunneling rigs, large-scale concrete batching plants — directly. This is a shift with profound strategic implications. Corporate M&A in construction always carries integration risk: the acquired firm's culture, contracts, key personnel, and goodwill all have to be absorbed. Buying a TBM has no such risk. The TBM either bores or it doesn't.

The economics also favour the equipment-led approach in the current pipeline. A modern TBM costs in the range of several tens of millions of dollars, but its useful life spans multiple major projects, and the pricing premium that a contractor can charge for "we already own the TBM and can mobilise next month" versus "we have to procure one, which takes 18 months" is substantial. In a sector where the customer's biggest fear is delay, owning the machinery is a meaningful competitive edge.

So the capital allocation framework today is: prioritise debt reduction, fund equipment capex from internal accruals and rights-issue proceeds, do not pursue inorganic growth that requires balance-sheet leverage, and let the order book compound organically off the pre-qualification moat.[^3] It is, frankly, the framework you would expect from a management team that has lived through the consequences of doing the opposite.

The next question — and the one institutional investors keep coming back to — is whether this framework is actually durable. To answer that, we need to put PEL through the two analytical frameworks that any serious investor in the company should be using.

VII. Strategic Framework: 7 Powers & Porter's 5 Forces

Hamilton Helmer's Seven Powers framework was not designed with Indian heavy-engineering contractors in mind, but two of its categories — Cornered Resource and Counter-Positioning — map almost too well onto Patel Engineering.

Cornered Resource: The Himalayan Geology Database. When you have been tunneling in the हिमालय Himalayas for four decades, you accumulate something that does not appear on any balance sheet but is enormously valuable: tacit, project-by-project knowledge of how specific rock formations behave under specific conditions. Which layers in which valleys are likely to be water-bearing. Where the tectonic stress concentrations are. Which grouting techniques work in which lithologies. What the optimal advance rate is for a given face. This is the kind of knowledge that lives in the heads of the senior site engineers and is partially codified in the firm's internal technical manuals.

It is genuinely difficult to replicate. A new entrant — even a well-capitalised foreign contractor — cannot simply buy this data. They would have to do the projects themselves, over decades, and live through the failures that produced the lessons. In a country whose mountain range is the youngest and most tectonically active on Earth, this is a real moat. The proof is in the pre-qualification tender documents: many Indian hydro and PSP tenders specify a requirement of "X kilometres of tunnel of Y diameter completed in similar geological conditions in the last Z years," and there is only a handful of contractors in the country who can tick all the boxes.

Counter-Positioning: The "Complex-Small" niche. Here is one of the more underrated structural advantages of being PEL's size in PEL's industry. There exists a category of project — call them Complex-Small — that is technically very demanding but financially modest by the standards of a giant conglomerate. Think a 2,000-crore underground powerhouse, or a 1,500-crore irrigation tunnel. For लार्सन एंड टुब्रो Larsen & Toubro, with its diversified business across defence, IT services, financial services, and mega-EPC, a contract of this size barely moves the needle. It does not justify the senior management attention. L&T's marginal bid is on the 20,000-crore HSR project, not the 2,000-crore tunnel.

For smaller generalist contractors, the same projects are too risky. The technical complexity is genuinely high, and a single mis-execution can wipe out a year's profit. So you end up with a middle band of contracts that are too small for the giants and too hard for the small players — and that band is where PEL has spent decades building its franchise.

Now to Porter's Five Forces.

Barriers to entry: very high. As discussed, pre-qualification requirements act as a multi-decade gating function. You cannot buy your way into Indian hydro contracting. You have to build the track record, and the track record takes thirty years to accumulate.

Bargaining power of buyers: high but bounded. The customers are almost all government — central PSUs and state utilities. They have monopsony power. They set contract terms. They sometimes pay slowly. But — and this is critical — they also have a small set of qualified bidders to choose from. The same pre-qualification wall that keeps new entrants out also limits the buyer's ability to play contractors off against each other. In any given complex underground tender, you might see three or four serious bidders. That is not a competitive bloodbath. That is something closer to an oligopoly.

Bargaining power of suppliers: moderate. The big equipment suppliers — Herrenknecht, Robbins for TBMs; Atlas Copco for drilling equipment — have pricing power, but the equipment is broadly interchangeable across contractors, so this is more of an industry-wide input cost issue than a firm-specific weakness.

Threat of substitutes: low. You cannot substitute for an underground powerhouse. The water is going to flow through a turbine inside a mountain or it is not going to generate hydroelectric power. There is no substitute technology that obsoletes large-scale hydroelectric or pumped storage construction.

Industry rivalry: moderate. In conventional civil construction, rivalry is intense and margin-destructive. In specialised underground work, the rivalry is more measured. The set of pre-qualified bidders is small, the projects are long-dated, and contractors often partner with each other on the largest jobs.

Put it all together and PEL's strategic position looks substantially better than the casual observation of "Indian mid-cap infra company" would suggest. The moat is real. It is just narrow and deep rather than wide and shallow, which makes it easy for generalist investors to miss.

But none of this is a guarantee, and the bear case has teeth.

VIII. The Narrative: Bull vs. Bear Case

Let's lay out both sides honestly, the way an Acquired episode would.

The Bull Case.

The first pillar is the size and visibility of India's hydro-adjacent pipeline. Between conventional hydro, pumped storage projects, irrigation tunneling, and increasingly strategic tunneling work (border roads, mountain rail tunnels), the addressable order pipeline over the next decade is structurally larger than at any point in PEL's history. The central government's renewables target — the push to roughly 500 GW of non-fossil capacity by 2030 — is the policy backdrop, and the pumped storage build-out is the natural complement to that target.[^8] PEL is one of a handful of contractors with both the pre-qualification and the equipment to capture this work.

The second pillar is the China-plus-one tailwind specific to underground engineering. Chinese tunneling firms have historically been competitive globally, but the broader geopolitical re-alignment — and India's specific posture toward Chinese contractors on strategic infrastructure — has effectively walled them out of the Indian market. That leaves the work to be split among a small set of domestic specialists and a handful of European contractors (Italians, Austrians) whose costs are substantially higher.

The third pillar is the balance sheet roadmap. The post-S4A trajectory has been steady deleveraging funded by a combination of asset monetisation, the 2023 rights issue proceeds, and improving operating cash flows.[^3] If management hits even moderate progress on this, the operating leverage of falling finance costs against a stable revenue base is mathematically powerful — every rupee of interest saved drops straight to the bottom line.

The Bear Case.

The first risk is the one PEL has always lived with: the "geological surprise." The Himalayas are the world's youngest mountain range. They are tectonically active. They are full of fractured rock, water-bearing layers, and stress concentrations that no surface survey can fully characterise. A single major tunnel collapse on a major project can stall execution for two to three years, trap hundreds of crores of working capital, and consume the senior engineering bench's attention. This is not theoretical — it has happened on multiple high-profile Indian hydro projects over the last two decades, with the long-troubled सुबनसिरी Subansiri Lower Hydroelectric Project being perhaps the most-cited example of how an underground project can become a multi-decade saga.[^11]

The second risk is receivables. PEL's customers are almost entirely government bodies. Government payment cycles in India can stretch, particularly when there is fiscal stress at the state level. A working-capital build-up of just one or two quarters of revenue can swing the company's leverage ratios materially. The post-S4A management has worked hard on receivables discipline, but the structural exposure cannot be eliminated.

The third risk is climate / regulatory. Large hydroelectric and PSP projects in ecologically sensitive Himalayan regions have, in recent years, attracted more rigorous environmental scrutiny — and in some cases, judicial intervention. Project clearances can be revoked. Construction can be halted by court order. The ESG overlay on Himalayan hydro is real and meaningful for any contractor whose order book is concentrated there.

The fourth risk is concentration. The Indian PSP build-out is a thesis that depends on continued policy support and continued PSU willingness to award contracts. If the pace of PSP awards slows — whether due to grid economics, financing constraints at the buyer level, or political change — PEL's growth runway compresses accordingly.

The "Acquired" take. Is this a commodity construction business or a specialised technology-enabled service? The honest answer is that in plain civil construction it would be a commodity, but in the very specific niche PEL operates in, it is genuinely closer to a specialised engineering service business with high incumbency advantages and meaningful counter-positioning against the giants. The category error that generalist investors make is benchmarking PEL against the broad EPC universe rather than against the much narrower set of pre-qualified Himalayan tunneling contractors.

Myth vs. Reality. The market consensus, until recently, treated PEL as a slow-recovery debt-restructuring story — a "special situations" name rather than a compounding business. The reality is that the debt restructuring is now largely behind the firm and the underlying business has been quietly re-positioned for a structurally larger pipeline than it has ever served before. Conversely, the more recent bull narrative — that this is a clean re-rating story with limited downside — under-weights how genuinely difficult underground execution remains. Both myths flatten what is, in fact, a complicated company with a real moat and a real risk profile.

The KPIs that matter. If you are a long-term investor in PEL, the two metrics worth tracking with discipline are: (1) net debt and the trajectory of finance costs as a percentage of revenue, because the entire equity story is leveraged to continued deleveraging; and (2) order book composition by segment, specifically the proportion of the book attributable to hydro, PSP, and underground works versus lower-margin generalist contracts, because mix shift toward the specialised end of the spectrum is the leading indicator of margin expansion. A distant third worth watching is the operating cash flow conversion ratio — how much of EBITDA actually makes it to cash — because in this industry that is the truest measure of execution quality.

IX. Epilogue & Lessons

The lesson of Patel Engineering is the lesson Charlie Munger has been giving for fifty years: figure out what you are good at, and then have the discipline to not do the other things.

For the better part of a decade between 2007 and 2017, PEL forgot the lesson. They were a tunneling and hydro company that decided to also be a real estate developer, a thermal power producer, a toll-road concessionaire, and a global construction conglomerate. Each of those decisions, taken individually, had a plausible business case. Taken together, they nearly killed the company. The S4A restructuring of 2016 was not a strategic master-stroke — it was a forced acknowledgment that the firm had drifted off its circle of competence and had to be dragged, painfully, back to it.4

What makes the story interesting from an investor's perspective is what came next. Plenty of Indian infra companies went through their own version of the debt crisis. Most of them either disappeared, were absorbed by competitors at distressed valuations, or are still — even now — limping along under the residual weight of their boom-era balance sheets. PEL is, in our reading, one of a small number that have actually completed the corporate surgery and emerged with both a cleaner balance sheet and a renewed strategic clarity.

It helps that the macroeconomic backdrop has rotated in their favour. The first wave of Indian infrastructure — the early-2000s boom — was dominated by roads, ports, and power generation. The current wave, what the policy discourse calls आत्मनिर्भर भारत Atmanirbhar Bharat-era infrastructure, has a different character: renewables and the storage required to make them work, strategic border infrastructure including mountain road and rail tunnels, water security including irrigation and inter-basin transfer projects, and urban water and sewage upgrades for a country that is still less than 40% urbanised. Almost all of this involves underground engineering. Almost all of it is in PEL's wheelhouse.

The broader story this fits into is what some Indian commentators have started calling "Infra 2.0" — the post-crisis infrastructure cycle that is structurally different from the pre-crisis one. Infra 2.0 is smaller in average ticket size but more technically demanding. It is funded with a different mix of equity and debt, often with a larger role for the central government and a smaller role for stretched private balance sheets. It rewards specialisation rather than scale-for-scale's-sake. And it punishes — far more quickly than the previous cycle did — the kind of capital indiscipline that almost destroyed companies like PEL the first time around.

There is one final reflection worth offering. The Patel family business has now existed for over seventy-five years. It was founded by a refugee from Sindh in the year of independence. It survived the licence-raj decades. It survived liberalisation. It nearly did not survive its own ambition. The fact that it is still standing today — leaner, narrower, and probably for the first time genuinely institutional in its capital allocation discipline — is itself an artefact worth contemplating. Few companies in any country get to live through this many cycles. Fewer still come out of a near-death experience with their original identity intact.

In the dim half-light of a Himalayan tunnel two kilometres inside a mountain, a Patel Engineering crew is, somewhere right now, advancing twenty metres a day through rock that has not seen the sun in 50 million years. They are not building anything that will photograph well. There will be no glass facade, no LED-lit lobby. There will be a hole, and then water flowing through the hole, and then electrons feeding into a grid that, increasingly, runs on the variable output of solar panels in राजस्थान Rajasthan and wind turbines in गुजरात Gujarat.

It is unglamorous work. It is, on the evidence of the last seventy-five years, the work this company was always meant to do.

References

References

-

Patel Engineering — Investor Relations / Financial Highlights, Patel Engineering Ltd ↩↩↩

-

Patel Engineering Q4 FY24 Earnings Call Transcript — Moneycontrol ↩↩

-

How Patel Engineering Is Digging Itself Out of a Hole — Forbes India ↩↩↩

-

Patel Engg to monetise land bank to reduce debt — Business Standard ↩↩

-

Patel Engineering — Corporate Filings and Shareholding Pattern, National Stock Exchange of India ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube