Patanjali Foods: The Ayurvedic Empire's Audacious Acquisition

I. Introduction & Episode Setup

Picture this: A saffron-robed yoga guru walks into a bankruptcy court in 2019, bids ₹4,350 crore for a debt-laden edible oil company, and within months, watches its stock price explode by 8,800%. This isn't fiction—it's the extraordinary tale of how Baba Ramdev and his silent partner Acharya Balkrishna transformed Ruchi Soya into Patanjali Foods, creating one of India's most controversial yet valuable FMCG empires.

Today, Patanjali Foods commands a market capitalization of ₹65,489 crore and generates revenue of ₹34,157 crore. But beneath these impressive numbers lies a story of spiritual capitalism, financial engineering, and regulatory brinkmanship that would make even the most seasoned Wall Street operators take notice.

The central mystery isn't just how a company went from bankruptcy to becoming one of India's most valuable FMCG players—it's how two men with no formal business education built an empire by weaponizing nationalism, spirituality, and the dreams of millions of retail investors. This is a story about power, faith, and the audacious belief that ancient wisdom could disrupt modern capitalism.

Over the next few hours, we'll unpack how a small ayurvedic pharmacy in Haridwar became a ₹65,000 crore behemoth, why banks that lost billions on Ruchi Soya eagerly lent money to its new owners, and what happens when you mix yoga, nationalism, and high finance in the world's largest democracy.

II. The Yoga Revolution: Origins of Patanjali (1995–2006)

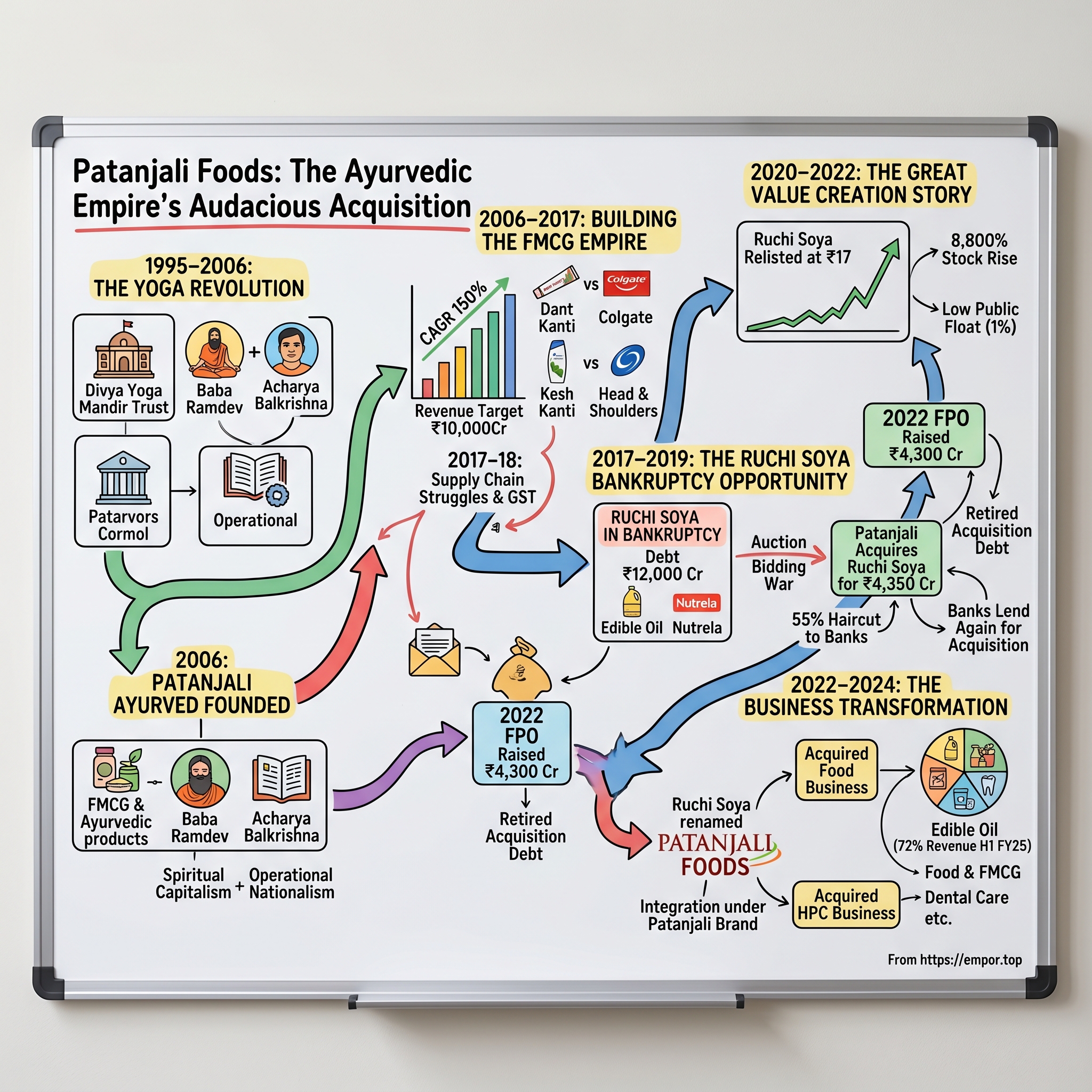

The story begins not in a boardroom, but at an ashram. On January 5, 1995, Balkrishna, Ramdev, and Acharya Karamveer founded Divya Yoga Mandir Trust at the Kripalu Bagh Ashram in Haridwar. Three young men with a vision to revive India's ancient healing traditions had no idea they were laying the foundation for what would become one of the country's most disruptive business empires.

The partnership at the heart of this empire was forged in the spartan dormitories of a gurukul. Ramdev met Balkrishna at Khanpur Gurukul in Haryana, where Balkrishna was his junior. While Ramdev, born Ram Kisan Yadav to a farming family, possessed natural charisma and oratory skills, Balkrishna brought scholarly depth and operational acumen. Balkrishna was born on August 4, 1972, in Haridwar to Nepalese immigrants, Sumitra Devi and Jay Vallabh Subedi originating from Syangja, Nepal.

The breakthrough came in 2002. Ramdev began organizing and conducting large yoga camps and broadcasting his yoga sessions on various TV channels. First on Sanskar in 2001, then Aastha from 2003, Ramdev's dawn yoga sessions became appointment viewing for millions of Indians. His ability to simplify complex yogic practices and present them with humor and relatability was revolutionary.

But teaching yoga was never the endgame. In 1995, when Ramdev was still a little-known yoga teacher in Haridwar, he and Balkrishna set up Divya Pharmacy under the aegis of Ramdev's guru, Swami Shankar Dev's ashram, to make Ayurvedic and herbal medicines. The medicines proved popular among yoga camp attendees, creating an organic distribution channel that would later become Patanjali's secret weapon.

The formal establishment came in 2006. Ramdev and Balkrishna founded Patanjali Ayurved, a fast-moving consumer goods company involved in manufacturing and trading of FMCG, herbal, and ayurvedic products. The timing was perfect—India's economy was booming, a new middle class was emerging, and there was growing disillusionment with Western medicine's side effects.

What made Patanjali different wasn't just the products—it was the positioning. Ramdev advocated for Indian nationalism in the tradition of the swadeshi movement through the production and sale of Patanjali Ayurved products, encouraging Indian citizens to reject multinational brands. Every purchase became an act of patriotism, every product a vote against foreign domination.

The ownership structure revealed the true power dynamics. Balkrishna owns 94% of the company and serves as its managing director, while Ramdev does not hold a stake in Patanjali Ayurved but is the face of the firm and endorses its products to his followers across his yoga camps and television programmes. This arrangement—Balkrishna as the owner, Ramdev as the evangelist—would prove both brilliant and controversial.

Followers of Ramdev, NRIs Sunita and Sarwan Poddar, helped kick-start the business with a loan, providing the initial capital that would fund Patanjali's early expansion. By positioning themselves as David against the Goliath of multinational corporations, they tapped into a deep vein of economic nationalism that was waiting to be mined.

So what for investors? The Patanjali origin story demonstrates the power of distribution innovation and brand positioning over product differentiation. While competitors focused on R&D and product quality, Patanjali built an emotional moat through spiritual and nationalist branding—a strategy that would prove nearly impossible for MNCs to replicate.

III. Building the Ayurvedic FMCG Empire (2006–2017)

The transformation from a small ayurvedic pharmacy to an FMCG giant didn't happen overnight, but when it did, it shook India's consumer goods establishment to its core. According to CLSA and HSBC, Patanjali was one of the fastest-growing FMCG companies in India in 2016.

The numbers were staggering. The company had sales of ₹5,000 crore in the 2015-16 financial year after growing by 150%, with a target revenue of ₹10,000 crore in 2016-17. To put this in perspective, it took Nestlé India 50 years to reach ₹10,000 crore in revenue. Patanjali was threatening to do it in a decade.

The product strategy was audacious in its simplicity: take every major FMCG category dominated by multinationals and launch an ayurvedic alternative at 20-30% lower prices. Dant Kanti against Colgate, Kesh Kanti against Head & Shoulders, Patanjali Honey against Dabur. Patanjali's toothpaste Dant Kanti, launched in March 2010, brought in revenues of ₹200 crore in 2014-15.

But the real innovation was in distribution. Patanjali didn't just sell products; it created an ecosystem. Yoga camps became product demonstrations. Television shows became infomercials. Ramdev readily acknowledges the role of media in his rise, saying "Patanjali ko bananey mein ek se 10 per cent humara role hai, baaki role media ka hai" (My role in Patanjali's rise is just 1-10%, the rest goes to media).

The operational mastermind behind this expansion was Balkrishna, who maintained an iron grip on every aspect of the business. All decisions related to marketing strategy and advertising were left to Balkrishna. From hiring senior management staff to dealing with advertisers, he did it all alone. This centralized control, while enabling rapid decision-making, would later raise corporate governance concerns.

By 2016, the company had nearly 4,700 retail outlets. Major retail chains created exclusive Patanjali aisles without the company spending a penny on slotting fees—unheard of in Indian retail. The brand had become a movement.

The competition was caught flat-footed. Hindustan Unilever, which had dominated Indian FMCG for decades, suddenly found its products being undercut by a yoga guru. Colgate-Palmolive watched its market share erode as consumers switched to herbal toothpaste. These weren't just business losses; they were ideological defeats.

Yet cracks were beginning to show. After revenue growth of over ₹10,000 crore between 2011 and 2017, Patanjali Ayurved's revenue dipped steeply to ₹8,135 crore in 2017-18, with only 2.38% growth in 2018-19. The company blamed demonetization and GST implementation, but the real issue was deeper: Patanjali had grown too fast, and its supply chain couldn't keep up.

Ramdev's philosophy was clear: "Humara ek simple funda hai: MNCs ko replace karna. We don't want to put anyone down, but would like to instil swadeshi pride so Indian money doesn't go out". This zero-sum worldview—us versus them, Indian versus foreign—would define Patanjali's strategy and set the stage for its most audacious move yet.

So what for investors? Patanjali's rapid growth phase reveals both the opportunity and risk in brands built on ideology. While emotional positioning can drive explosive growth, it also creates operational blind spots. The company's struggles with supply chain and quality control in 2017-18 show that operational excellence eventually matters more than marketing brilliance.

IV. The Ruchi Soya Bankruptcy Opportunity (2017–2019)

While Patanjali was stumbling with operational challenges, 1,000 kilometers away in Indore, a three-decade-old edible oil empire was collapsing. In December 2017, Ruchi Soya Industries entered into insolvency because of its total debt of about ₹12,000 crores.

The fall of Ruchi Soya was a classic tale of overleverage and poor timing. Founded in 1986 by Dinesh Shahra, Ruchi Soya initially started as a small solvent extraction plant in Madhya Pradesh. Over three decades, Shahra had built it into one of India's largest edible oil companies with brands like Nutrela, Mahakosh, and Ruchi Gold.

But ambition proved to be Shahra's undoing. Ruchi Soya embarked on an ambitious expansion spree, diversifying into unrelated businesses such as infrastructure, real estate, and renewable energy. This rapid expansion strained resources and diluted focus on the core edible oil business, primarily financed through debt.

The death blow came from Indonesia. In November 2011, Indonesia increased tax on crude edible oil exports and reduced duties on refined oil exports. The cost escalation hit margins of Ruchi Soya's 13 refinery units. Between 2013 and 2017, turnover dropped from ₹26,485 crore to ₹18,620 crore. A profit of ₹236 crore in 2013 turned into a loss of ₹1,257 crore in 2017.

Enter the insolvency courts. The National Company Law Tribunal admitted Ruchi Soya for bankruptcy proceedings, setting off one of India's most watched corporate insolvency cases. The company owed ₹12,000 crore to financial creditors, with State Bank of India, Central Bank of India, and Punjab National Bank among the largest lenders.

The bidding war that followed was intense. Adani Wilmar, which sells Fortune brand edible oil, was the initial frontrunner. But then came a surprise entrant: Patanjali Ayurved. For Ramdev and Balkrishna, this wasn't just an acquisition—it was destiny. Ruchi Soya had what Patanjali desperately needed: manufacturing infrastructure, distribution networks, and established brands in a category Patanjali hadn't cracked.

In December 2019, Patanjali Ayurved acquired the bankrupt Ruchi Soya for ₹4,350 crore. The structure of the deal was remarkable: Patanjali settled ₹4,350 crore of dues by infusing ₹1,100 crore equity and arranging another ₹3,250 crore via debt.

Here's where it gets interesting. Patanjali proposed to repay ₹4,053.19 crore to lenders, roughly 45% of their claims of ₹9,384 crore. SBI recovered ₹883 crore, Central Bank ₹397 crore, and PNB ₹361 crore. The banks took a 55% haircut—they lost more than half their money.

But the real magic trick was yet to come. The ₹3,250 crore debt that Patanjali arranged? It came from the same banks that had just taken massive losses on Ruchi Soya. These were the same lenders previously chasing Ruchi for repayment. But Ruchi Soya was considered a new entity after acquisition, so these bank loans were treated as fresh disbursals rather than bad loans.

The acquisition gave Patanjali instant scale in edible oils. The acquisition helped Patanjali acquire edible oil plants as also soyabean oil brands such as Mahakosh and Ruchi Gold. It was entering a ₹1,34,300 crore market that was growing at 25% annually.

So what for investors? The Ruchi Soya acquisition demonstrates the value creation potential in distressed assets when combined with strong branding and distribution. However, the financing structure—borrowing from the same banks that took haircuts—raises questions about banking sector incentives and the true cost of such acquisitions to the financial system.

V. The Great Value Creation (or Manipulation?) Story (2020–2022)

What happened next defied all logic of financial markets. The shares of Ruchi Ltd. were relisted on January 27, 2020. The shares opened at ₹17. Then began one of the most extraordinary rallies in Indian stock market history.

Shares of Ruchi saw a continuous 5% increase every day. This triggered circuit breakers every day, leading to trading suspension. This carried on for over 100 days until shares touched ₹706.95. This was followed by a fall to ₹519.80, seemingly a market correction. But post-May 27, the 5% per day rally began once again.

By June 2020, the numbers were mind-boggling. The stock reached ₹1,378.40, an 8,008% increase since January. On June 26, it hit ₹1,507.30 compared to its relisting price of ₹16.9—more than 8,800% returns in five months. The market capitalization had exploded to ₹44,592 crore, making it more valuable than established FMCG player Marico.

What was driving this insanity? The answer lay in the shareholding structure. A huge 99.03% stake or 29.29 crore shares were held by just 15 promoters. Of these, Patanjali Ayurveda held 14.25 crore shares or 48.17% stake. With only 1% of the stake held by the public—just 28.59 lakh units out of 29.58 crore outstanding shares, Ruchi Soya had become the ultimate low-float stock.

The rally attracted regulatory attention. In March 2022, as Ruchi Soya prepared to launch its FPO, Baba Ramdev made a statement that would haunt him. Speaking to investors, he promised to make them "crorepatis" (millionaires), suggesting the stock would continue its meteoric rise post-FPO. SEBI wasn't amused.

The FPO itself was a masterclass in financial engineering. In 2022, the company raised ₹4,300 crore through the Follow-on Public Offer under its brand name Ruchi Soya. At the upper price band of ₹650, this meant Patanjali would dilute around 19% at the upper end and 18% at the lower end.

Think about what just happened: Patanjali bought Ruchi Soya for ₹4,350 crore. Within two years, it raised ₹4,300 crore by selling less than 20% stake. It had essentially gotten the entire company for free while retaining 80% ownership.

A significant portion of these funds was used to retire the company's outstanding debt. The same debt that Patanjali had taken to buy the company in the first place. It was financial alchemy at its finest—or most questionable, depending on your perspective.

Market experts raised serious concerns. With low public shareholding, the share price wasn't reflecting actual value. Only after Patanjali lowered its stake would the stock reflect true value. The question was whether retail investors understood they were playing a game where the house—quite literally—owned 99% of the chips.

So what for investors? The Ruchi Soya rally exemplifies the dangers of low-float stocks and the importance of understanding shareholding structures. While early investors made extraordinary returns, the episode raises serious questions about market manipulation, regulatory oversight, and the protection of retail investors in India's capital markets.

VI. The Business Transformation (2021–2024)

With the financial engineering complete, Patanjali set about transforming Ruchi Soya into something bigger. The strategy was vertical integration on steroids—bring everything under one roof and rebrand it all as Patanjali.

In June 2021, Ruchi Soya acquired the biscuits and noodles business of Patanjali for ₹60 crore. This was just the beginning. In May 2022, it acquired the food business of Patanjali Ayurved for around ₹690 crore. The acquired portfolio was substantial: 21 products including ghee, honey, spices, juices and flour.

Then came the masterstroke: In June 2022, Ruchi Soya Industries was renamed Patanjali Foods. The transformation was complete. What had been a debt-laden commodity business was now positioned as a premium FMCG company carrying the Patanjali brand's spiritual and nationalist aura.

The business mix began shifting rapidly. Edible oils still dominated at 72% of revenue in H1 FY25 versus 93% in FY22, but the food and FMCG segment was growing fast. The company wasn't just selling cooking oil anymore—it was selling a lifestyle.

The integration revealed Balkrishna's operational philosophy. As he claimed: "We haven't pushed non-performing products into Ruchi Soya. We have removed non-performers in breakfast and biscuit categories. Ruchi is a public company, so products must be world class".

In November 2024, another major expansion: the company brought its Home & Personal Care (HPC) business into the fold. The HPC segment posted its first full quarter in Q4FY25, generating ₹728.48 crore in revenue. Since November 1, 2024, the segment brought in ₹1,148.85 crore.

The product portfolio now spanned everything from toothpaste to cooking oil to protein supplements. For Q4FY25, Dental Care accounted for ₹398.14 crore, Skin Care ₹178.49 crore, and Home Care ₹88 crore. This wasn't just diversification—it was an attempt to become India's answer to Unilever.

But challenges persisted. The overlap between Patanjali Ayurved and Patanjali Foods products created confusion. The Ruchi and Patanjali food portfolios had quite a few product overlaps such as ghee, honey and atta. The solution? A non-compete agreement ensuring Patanjali would never launch breakfast cereal or nutraceutical products that would conflict with Ruchi.

Distribution remained the secret weapon. The company leveraged Patanjali's existing network while maintaining Ruchi Soya's traditional channels. It was operating what were essentially two parallel distribution systems, giving it reach that competitors struggled to match.

So what for investors? The transformation of Ruchi Soya into Patanjali Foods shows how brand value can transform commodity businesses. However, the complex related-party transactions and product overlaps between entities create opacity that makes true value assessment difficult. Investors need to carefully parse segment performance rather than relying on headline numbers.

VII. Financial Engineering & Capital Structure

The financial transformation of Patanjali Foods reads like a Harvard Business School case study—if Harvard taught courses in aggressive financial engineering with a dash of regulatory arbitrage.

Consider the leverage journey: A company that entered bankruptcy with ₹12,000 crore in debt was acquired with ₹3,250 crore of new debt, which was then largely paid off using ₹4,300 crore raised from public markets. By FY25, Patanjali Foods claimed to be "almost debt free"—a remarkable transformation that deserves scrutiny.

The Q4 FY25 numbers tell the story of this transformation. The company reported Q4 net profit of ₹359 crores, registering growth of 73.8%. Revenue for Q4 FY25 and full year stood at ₹9,692.20 and ₹34,156.96 crores respectively. The profit growth was remarkable: Net profit rose 73.78% to ₹358.54 crore in Q4FY25. For the full year, net profit rose 70.08% to ₹1,301.34 crore.

But here's what's fascinating about the capital structure: despite being "debt-free," the company maintained aggressive working capital management typical of commodity traders. The business model essentially used supplier credit and advance payments from customers as free financing.

The profitability metrics revealed the ongoing transformation. EBITDA for Q4FY25 was ₹568.88 crores with an EBITDA margin of 5.87%. For FY25, the EBITDA margin was 6.09% while PAT margin was 3.80%. These aren't spectacular margins—they're typical of commodity businesses with some value addition.

The segment performance showed where real value was being created. The Edible Oil segment achieved quarterly sales of ₹6,764.07 crore in Q4FY25, marking 20.90% growth YoY. Branded edible oils contributed over 75% to this total. The segment reported EBITDA of ₹314.99 crore in Q4FY25, up from ₹134.27 crore in Q4FY24.

What about capital allocation? The company significantly ramped up advertising efforts. Advertising spend surged over threefold to ₹233.36 crore in FY25, compared to ₹71.45 crore in FY24. This dramatic increase in marketing spend suggested a shift from commodity trading to brand building.

The working capital dynamics were particularly interesting. In a commodity business, working capital can make or break profitability. Patanjali Foods managed this through a combination of supplier relationships (many dating back to Ruchi Soya days) and the Patanjali brand's ability to command better payment terms.

The dividend policy reflected newfound confidence. The Board recommended a final dividend of ₹2 per equity share (100%), and there was even talk of bonus shares—unusual for a company that had emerged from bankruptcy just five years earlier.

So what for investors? The financial engineering at Patanjali Foods demonstrates how bankruptcy can reset capital structures advantageously. However, the rapid transformation from leveraged commodity trader to "debt-free" FMCG company happened unusually fast. Investors should focus on cash flow generation rather than reported profits, as working capital changes can significantly impact true cash generation in commodity-linked businesses.

VIII. Controversies & Regulatory Battles

Behind the financial success lay a minefield of controversies that would make even the most battle-hardened corporate communications team break into a cold sweat. The regulatory and legal challenges facing Patanjali Foods weren't just business risks—they were existential threats.

The most damaging controversy erupted in 2024. In February 2024, the Supreme Court imposed a temporary ban on the company's advertisements and issued a contempt notice. The Supreme Court directed Patanjali to publish apologies in newspapers. Initially, Patanjali issued small apologies deemed insufficient. Consequently, Patanjali released larger apologies as instructed.

The contempt proceedings stemmed from misleading advertisements about the medicinal properties of Patanjali products. This wasn't a minor regulatory slap—the Supreme Court of India was directly intervening in the company's marketing practices. In August 2024, the Supreme Court closed contempt proceedings after accepting the apology tendered after they took steps to rectify their mistake.

The COVID-19 period brought its own disasters. Patanjali had launched Coronil, claimed as a cure for coronavirus. The Madras High Court fined the company ₹10 lakh for "exploiting fear and panic by projecting a cure for coronavirus." Patanjali withdrew the claim of Coronil being a cure for COVID-19.

Labor practices revealed another dark side of the spiritual capitalism model. Workers are paid ₹6,000 per month, working 12-hour shifts, six days a week. They are discouraged from asking for raises, with the rationale that working at the factory is considered "seva" (voluntary service). The irony of a company built on nationalist pride paying poverty wages wasn't lost on critics.

Corporate governance remained opaque. With Balkrishna owning 94% of Patanjali Ayurved, minority shareholders had virtually no say. The company operated more like a closely-held family business than a public corporation, despite handling public money through Patanjali Foods.

The Uttarakhand Licensing Authority added to the pile, revoking licenses for 14 Patanjali products after facing scrutiny from the Supreme Court over regulatory inaction. State-level regulators were finally waking up to years of questionable claims.

Even Balkrishna's citizenship had been questioned. In 2011, he was charged with cheating and forgery for acquiring fake degrees to procure an Indian passport. According to the CBI, his passport was issued on forged educational degrees and his Indian citizenship was questioned. The case was closed two years later due to lack of evidence.

Then there's the working culture that blended corporate hierarchies with ashram dynamics. Ramdev and Balkrishna are treated as gurus whose feet must be touched each time they enter an area. This wasn't just unusual corporate culture—it was a fundamental blending of spiritual authority with corporate power.

So what for investors? The regulatory and governance challenges at Patanjali Foods represent material risks that could impact future valuations. The Supreme Court interventions, labor practices, and corporate governance issues suggest a company operating outside conventional norms. Investors must price in regulatory risk and potential reputation damage when evaluating the stock.

IX. Playbook: Lessons in Unconventional M&A

The Patanjali-Ruchi Soya deal offers a masterclass in unconventional M&A that breaks every rule taught in business schools—and somehow still works. Let's decode the playbook that turned a ₹4,350 crore investment into a ₹65,000 crore empire.

Lesson 1: Spiritual Capital as Currency Traditional acquirers bring money; Patanjali brought devotion. The company's ability to tap into religious and nationalist sentiment created a currency more valuable than cash. When Ramdev spoke, millions listened—and bought. This spiritual capital allowed Patanjali to command premium valuations despite questionable fundamentals.

Lesson 2: Weaponizing Low Float The post-acquisition strategy was brilliant in its simplicity: keep 99% ownership, create scarcity, and watch the stock price explode. While regulators eventually intervened, the company had already extracted massive value through the FPO at inflated valuations. The lesson? In markets with weak regulation, financial engineering can create more value than operations.

Lesson 3: The Bailout Arbitrage The same banks that took haircuts on Ruchi Soya's original debt eagerly lent to Patanjali because the loans were classified as fresh disbursals rather than bad loans. This regulatory arbitrage—where a change in ownership resets credit history—created a perverse incentive that Patanjali exploited masterfully.

Lesson 4: Integration Through Ideology Most M&A fails at integration. Patanjali solved this by imposing its ideology wholesale. Every Ruchi Soya product became a Patanjali product. Every employee became a devotee. The integration wasn't just operational—it was spiritual. This totalitarian approach to integration, while ethically questionable, proved remarkably effective.

Lesson 5: Regulatory Capture Through Nationalism By wrapping itself in the flag, Patanjali made regulatory action against it seem anti-national. Every criticism became an attack on Indian culture. This positioning created a protective moat against regulatory scrutiny—though as the Supreme Court interventions showed, this protection had limits.

Lesson 6: Retail Investors as Exit Strategy The FPO wasn't really about raising capital—it was about creating an exit at astronomical valuations. By targeting retail investors with promises of wealth ("crorepati" dreams), Patanjali transferred risk from institutions to individuals. The retail investors who bought at ₹650 in the FPO provided liquidity for early investors to exit.

Lesson 7: Related-Party Transactions as Value Transfer The acquisitions of Patanjali businesses by Ruchi Soya—biscuits for ₹60 crore, food business for ₹690 crore—were related-party transactions that transferred value between entities controlled by the same people. This financial jugglery allowed profit shifting and tax optimization while maintaining the fiction of arms-length dealing.

So what for investors? The Patanjali playbook reveals how unconventional strategies can create massive value in markets with regulatory gaps. However, these strategies often involve wealth transfer rather than wealth creation. Investors should distinguish between financial engineering that creates genuine value and that which merely redistributes it from public markets to promoters.

X. Bear vs. Bull Case & Future Outlook

As we evaluate Patanjali Foods at its current ₹65,000 crore valuation, the investment case splits dramatically between believers and skeptics.

Bull Case: The Bharat Growth Story

The bulls see Patanjali Foods as perfectly positioned for India's consumption boom. With a market cap of $7.23 billion USD as of May 2025 and revenues of ₹34,289 crore in FY25, registering 7.3% YoY growth, the company has proven it can deliver consistent growth.

The FMCG transformation is gaining momentum. The Food and FMCG segment achieved its highest-ever quarterly revenue of ₹2,705 crore in Q4 FY25, rising 8% quarter-on-quarter, accounting for 32.57% of total revenue. As this mix improves, margins should expand beyond the current 6-7% EBITDA levels.

Rural distribution remains a massive opportunity. Patanjali's unique positioning—combining traditional values with modern products—resonates deeply in Bharat (rural India). With rural consumption growing faster than urban, this positions the company for sustained growth.

The balance sheet has been cleaned up, debt is minimal, and cash generation is improving. The company's ability to fund growth internally reduces dilution risk and suggests sustainable expansion ahead.

Bear Case: The Commodity Trap

The bears see a commodity business masquerading as an FMCG company. Despite all the transformation talk, edible oils still account for 72% of revenue. This is a low-margin, volatile business exposed to global commodity cycles.

Corporate governance remains problematic. The complex web of related-party transactions, the 94% ownership of Patanjali Ayurved by one individual, and the blending of spiritual and corporate authority create opacity that should worry minority shareholders.

Regulatory overhang is real and persistent. The Supreme Court interventions, misleading advertisement cases, and constant scrutiny suggest a company operating outside acceptable norms. One major regulatory action could crater the stock.

The valuation assumes FMCG multiples for what is essentially a commodity business with some branded products. At 50x P/E for a company with 6% EBITDA margins, the stock appears priced for perfection.

Competition is intensifying. HUL and ITC have launched their own ayurvedic brands. The moat of being the "nationalist" choice is eroding as mainstream players adopt similar positioning.

The Verdict

Patanjali Foods represents a unique bet on India's cultural and economic transformation. It's simultaneously a play on rural consumption, religious nationalism, and the formalization of traditional medicine. The company has proven it can generate profits, transform businesses, and create market value.

However, the valuation appears stretched given the operational reality. This is still primarily an edible oil business with corporate governance questions and regulatory challenges. The stock price seems to reflect more hope than fundamentals.

So what for investors? Patanjali Foods is a high-risk, high-reward bet on India's consumption story filtered through the lens of cultural nationalism. Conservative investors should wait for better entry points or clearer evidence of FMCG transformation. Aggressive investors might see opportunity in India's unique socio-economic dynamics. Either way, position sizing is crucial given the volatility and regulatory risks.

XI. Epilogue & Reflections

The Patanjali Foods story forces us to confront uncomfortable questions about modern capitalism. Is creating ₹65,000 crore in market value from a bankrupt company in five years a triumph of entrepreneurship or a cautionary tale about market manipulation? Can spiritual authority and corporate governance coexist? What happens when nationalism becomes a business model?

The success of Patanjali reveals deep truths about Indian society. In a nation still grappling with its colonial past, the promise of swadeshi (self-reliance) resonates powerfully. Ramdev and Balkrishna didn't just sell products—they sold pride, identity, and belonging. Every Patanjali purchase became an act of resistance against Western cultural hegemony.

Yet the controversies surrounding the company—from misleading advertisements to poor labor practices—suggest that wrapping capitalism in saffron robes doesn't make it more ethical. The ₹6,000 monthly wages paid to workers creating billions in value expose the hollowness of the nationalist rhetoric.

The financial engineering that transformed Ruchi Soya reflects both the opportunities and pathologies of India's capital markets. The ability to generate 8,000% returns through low-float manipulation, raise ₹4,300 crore from retail investors based on promises of wealth, and secure loans from banks that just took haircuts reveals a system that often rewards financial cleverness over productive enterprise.

For entrepreneurs, Patanjali offers powerful lessons. The company proved that in markets with cultural divides, positioning can be more powerful than product. It showed that distribution innovation—using yoga camps as retail channels—can disrupt established players. Most importantly, it demonstrated that in emerging markets, understanding cultural currents matters more than following Western business models.

For investors, the story is more cautionary. The spectacular returns generated by early Ruchi Soya investors came at the expense of those who bought during the FPO. The company's success required a unique confluence of factors—regulatory gaps, cultural moments, and market inefficiencies—that may not be replicable.

As India continues its economic journey, more Patanjalis will emerge—companies that blend tradition with modernity, spirituality with capitalism, nationalism with globalization. Understanding these hybrid models will be crucial for anyone seeking to participate in the India growth story.

The ultimate question remains: Is Patanjali Foods a ₹65,000 crore FMCG giant in the making, or a ₹4,350 crore commodity trader with exceptional marketing? The answer may determine not just the fate of one company, but the template for Indian capitalism in the 21st century.

In the end, the Patanjali Foods saga reminds us that in business, as in yoga, flexibility matters more than strength, and sometimes the most successful positions are the ones that seem impossible to everyone else.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube