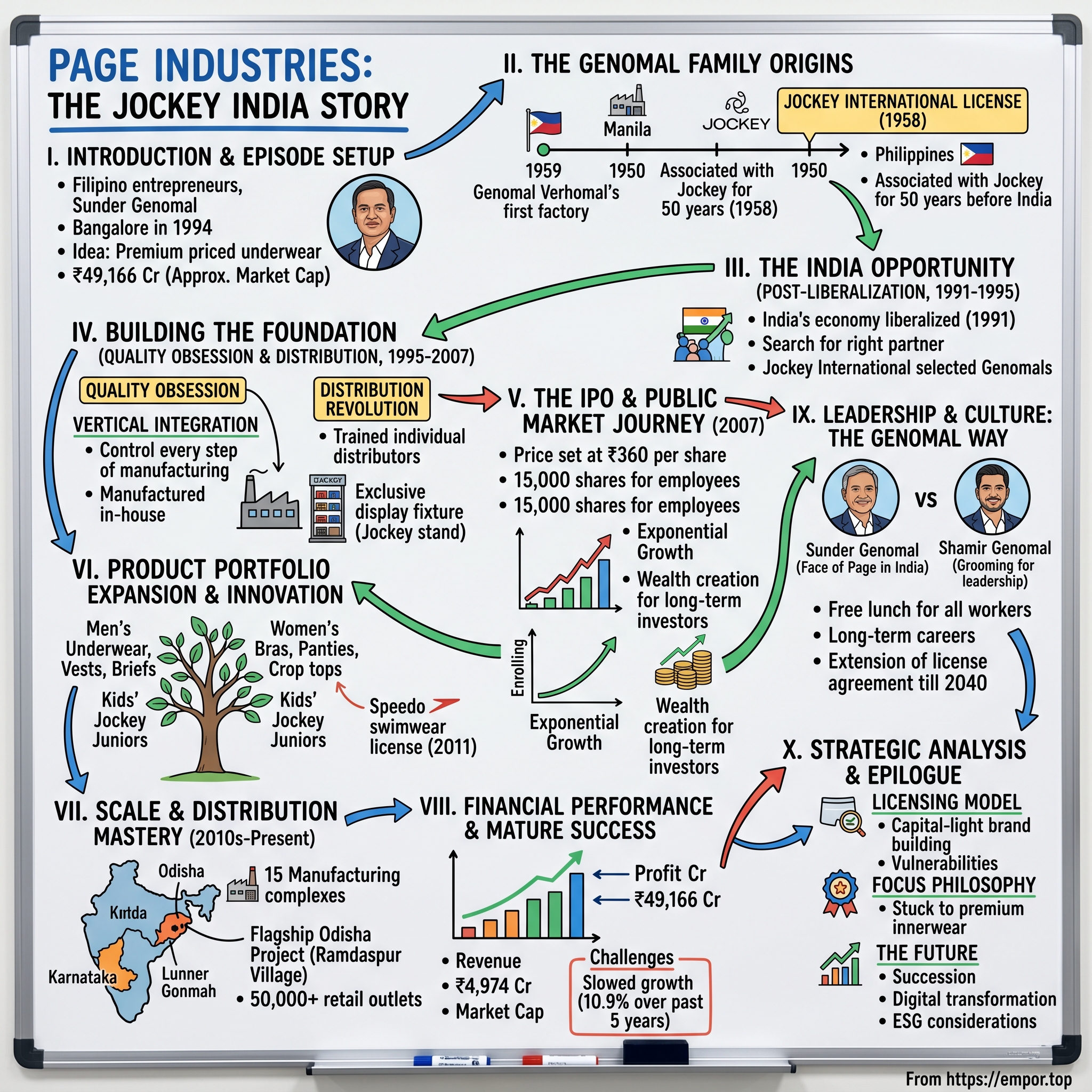

Page Industries: The Jockey India Story - From Manila to Mumbai

I. Introduction & Episode Setup

Picture this: A family of Filipino entrepreneurs who had never lived in India, never done business there, walks into Bangalore in 1994 with a radical idea—they're going to convince Indians to pay premium prices for underwear. In a country where innerwear was bought from street vendors by the kilogram, where brands meant nothing below the belt, where price sensitivity ruled every purchase decision. The audacity was breathtaking.

Today, Page Industries commands a market capitalization of approximately ₹49,000 crores, making it one of India's most valuable apparel companies. The company holds exclusive rights to manufacture and distribute Jockey products across India, Sri Lanka, Bangladesh, Nepal, Oman, Qatar, Maldives, Bhutan, and the UAE—a territory spanning 1.8 billion people. With revenues touching ₹4,974 crores and profits of ₹765 crores, Page has transformed from a startup betting on premium innerwear to a juggernaut that redefined how Indians think about their most intimate apparel. The story is even more remarkable when you consider the context. This wasn't Silicon Valley disruption or venture capital moonshots. This was old-fashioned manufacturing excellence meeting new-world brand building. The Genomal family, who had built their fortune distributing Jockey products in the Philippines for over three decades, saw what others missed: India's middle class wasn't just growing—it was ready to pay for quality in categories previously dominated by commodity thinking.

What unfolds over the next several hours is a masterclass in licensing done right, vertical integration as competitive advantage, and how to build premium brands in emerging markets. It's about family businesses that professionalize without losing their soul, about trusting relationships that span continents and decades, and about the power of focus when everyone else is diversifying.

Current metrics show revenue at ₹4,974 Cr, profit at ₹765 Cr, and a market cap of ₹49,166 Cr, but these numbers only hint at the deeper story. The company has delivered what some describe as "poor sales growth of 10.9% over past five years"—a sign that even the best stories face headwinds. The question isn't just how Page Industries became one of India's most successful consumer companies, but whether its playbook can navigate the next chapter of India's consumption story.

We'll explore how a company named after a promoter's mother became the standard-bearer for premium innerwear in India, why Jockey chose the Genomals over established Indian conglomerates, and what happens when manufacturing obsession meets brand discipline. Along the way, we'll uncover lessons about building enduring businesses in emerging markets—lessons that matter whether you're an entrepreneur, investor, or simply curious about how great companies are built.

II. The Genomal Family Origins: From Manila to Millionaires

The story begins not in India's bustling metros but in the Philippines of the late 1950s, where a young entrepreneur named Genomal Verhomal saw opportunity in the most basic of human needs—clothing. In 1959, he established his first factory, but the roots went deeper. The family business, V. Lilaram & Company, had been importing garments into Angeles, Pampanga since 1925. They understood fabric, understood trade, understood the delicate dance between quality and price that defines the garment business.

Then came 1958—a pivotal year. V. Lilaram & Company secured the exclusive license to distribute Jockey products in the Philippines. This wasn't just another distribution deal; it was the beginning of a relationship that would span continents and generations. Jockey, the American innerwear giant founded in 1876, was expanding globally, and the Genomals proved to be exactly the kind of partners they were looking for: detail-oriented, quality-obsessed, and thinking in decades rather than quarters.

The World War II years tested the family's mettle in ways that would shape their business philosophy forever. During the Japanese occupation of the Philippines, when collaboration meant survival but resistance meant honor, the Genomals made a choice that defined their character. They partnered with the Uy brothers to covertly supply Allied forces, risking everything for a cause they believed in. The bullets and bombs of war taught them lessons no business school could: the importance of trust, the value of courage, and how to operate under extreme uncertainty. When the war ended, both the Philippine government and Allied forces honored them for their service—recognition that meant more than any business award ever could. The partnership that would define the Genomals' future took a dramatic turn with their licensing arrangement. In 2008, Page renewed its licensing arrangements for the Jockey brand for 50 more years, till 2058, and 'thereafter to be continued in perpetuity every 50 years'—essentially a permanent partnership, renewable every half-century. This wasn't just a business deal; it was a testament to trust built over generations. The Genomal family had been associated with JOCKEY International Inc. for 50 years as their sole licensee in the Philippines before they ever set foot in India.

Three brothers would shape the family's destiny in the subcontinent: Nari, Ramesh, and Sunder (also known as Ashok) Genomal. Each brought different strengths to the table. Sunder, the youngest, would become the face of Page Industries in India—a British-Indian citizen born and raised in Manila, who had worked across Africa and the UK before taking on the India challenge. His brothers provided strategic support and capital, but it was Sunder who would relocate, who would build, who would transform an idea into an empire.

The family's business acumen was matched by their manufacturing expertise. "I grew up on the Jockey brand and, even as a kid, spent time at the manufacturing plant set up by my father as early as 1959, in Manila. It is still operational today." This wasn't theoretical knowledge learned in boardrooms; this was hands-on understanding of fabric, stitching, quality control—the unglamorous details that separate great products from good intentions.

What made the Genomals different wasn't just their money or their connections. It was their patient capital mentality, their willingness to think in decades rather than quarters, and their understanding that brand building in emerging markets requires a different playbook than in developed ones. They had seen how Jockey evolved from functional underwear to lifestyle brand in the Philippines. They understood that India, with its burgeoning middle class and changing social norms, was ready for the same transformation—but it would require patience, capital, and an obsessive attention to quality that most Indian manufacturers weren't willing to commit to. The stage was set for one of the most audacious market entry strategies in Indian consumer history.

III. The India Opportunity: Post-Liberalization Gold Rush (1991-1995)

The year 1991 changed everything. India's balance of payments crisis forced the government to liberalize the economy, dismantling the License Raj that had strangled enterprise for decades. Foreign brands that had been kept out or forced to exit were suddenly welcome again. For Jockey, this was a chance to correct a historical mistake.

Jockey first entered India in 1962 with Associated Apparels. Jockey re-entered India only post 1991 liberalization. The earlier venture had ended in 1973 when the Foreign Exchange Regulation Act (FERA) forced most foreign companies to either dilute their stake to 40% or exit. Jockey chose to exit. Two decades later, the doors reopened, and Jockey International was determined not to repeat past mistakes.

The search for the right partner was methodical. Jockey had been approached by a few large Indian business houses to license their brand. But the long association of the Genomal family with Jockey in South East Asia meant that the first right of refusal went to them. This wasn't sentimentality; it was strategic. The large Indian houses might have had deeper pockets and better connections, but the Genomals had something more valuable: they understood Jockey's DNA, having lived and breathed the brand for half a century.

The Genomal brothers decided to grab the opportunity, though they had not lived or done business in India. The audacity of this decision cannot be overstated. Here was a family with no Indian operations, no local relationships, no understanding of India's byzantine bureaucracy, betting everything on a market where premium innerwear was virtually non-existent. In 1993, Indians bought underwear by weight from street vendors. The idea of paying ten times more for a branded product seemed absurd. Before taking the plunge, Genomal toured India in 1993 and researched the undergarments market with the help of market research firm MARG. What he found was both discouraging and encouraging. The market for branded innerwear was virtually non-existent. But beneath the surface, fundamental changes were underway. India's middle class was growing, disposable incomes were rising, and younger consumers were beginning to associate brands with aspiration and quality of life.

The decision about where to base operations revealed the practical, almost whimsical side of entrepreneurship. Next came the question of choosing a base for headquarters in India; it was a tossup between Mumbai and Bangalore. "Even as I weighed the relative merits in my mind, it was finally the lovely Bangalore weather which proved to be the clincher," Sunder would later recall with a smile. Maybe the fact that, before Bangalore became synonymous with the IT boom, the city's largest employer was the textile industry had a role to play in the decision.

1994: Page Industries was founded by Sunder, Nari, and Ramesh Genomal. They held a 54% stake together, with the rest distributed among other family members and early investors. The company's name itself was a tribute to family—Page Industries was derived from the initials of the promoter's mother, Parpati Genomal (P.A.Ge). This personal touch would become a hallmark of how the Genomals did business: professional in execution, personal in relationships.

The trust Jockey International placed in the Genomals was extraordinary. Rick Hosley, then President of Jockey International, made a prediction that seemed outlandish at the time: the Genomals would lead the biggest licensee of Jockey in the world. In a country where people haggled over underwear prices in street markets, where the very idea of brand loyalty for innerwear seemed absurd, Hosley saw what others couldn't—that economic liberalization wasn't just changing policies, it was changing mindsets. And the Genomals, with their unique combination of manufacturing expertise, brand understanding, and patient capital, were perfectly positioned to capitalize on this transformation.

IV. Building the Foundation: Quality Obsession & Distribution Revolution (1995-2007)

1995 marked the beginning of operations in Bengaluru with Jockey manufacturing, but the real story was the philosophy that would guide every decision: an almost religious devotion to quality that bordered on obsession. "To get the kind of quality standards required by Jockey, we had to have control over every step of the manufacturing process," Sunder explained. In an industry where outsourcing was the norm, where margins were squeezed by farming out production to the lowest bidder, Page Industries made a contrarian bet: manufacture everything in-house. Even today, more than 95 per cent of all products sold in India are manufactured in-house. Only a small portion comprising mainly thermal wear is outsourced. But even there, the third party facilities are dedicated to Page and they control quality. This vertical integration went to extremes that seemed irrational to outsiders—Page even manufactured its own elastic, a component most apparel companies simply bought from suppliers. They provided free lunch for workers, unusual in Indian manufacturing. Every decision reflected a simple principle: if you want to charge premium prices, you must deliver premium quality, and you can't deliver premium quality without controlling every variable.

The distribution strategy was equally revolutionary. Till the advent of the Jockey brand in India, innerwear—briefs and vests for men; panties and bras for women—were a push-business where the retail touch point played a key influencing role. Page Industries changed the game. Rather than going after wholesale distributors who would push products into the market with little regard for brand positioning, they chose individual distributors who could be trained, monitored, and aligned with the brand's premium positioning.

The company introduced exclusive display fixtures—those distinctive Jockey stands that would become ubiquitous in Indian retail. They insisted on prominent in-store placement, bold marketing that made people comfortable discussing innerwear openly. This was cultural disruption masquerading as business strategy. In a country where buying underwear was often a furtive, embarrassing transaction, Page made it aspirational.

Building the right team was crucial. Between 1995 and 1997, Genomal assembled his core team to scale up execution. Pius Thomas, from telecom operator BPL, joined the company to look after finance. Shekhar Tiwari joined from Eureka Forbes to take charge of marketing and sales, and Vedji Ticku, also from Eureka Forbes, joined in 1997 as sales manager for the south zone. Thomas went on to become the CFO in 2012, while Ticku took over as CEO in 2016. These weren't just employees; they were missionaries for the premium innerwear revolution.

The early years tested every assumption. Like all new entrants, Page too had its own issues. The major one of those was establishing relationships with high quality raw material suppliers. The high cost of advertisement too remained a concern as the competition was cut throat on margins. Despite such attention to detail, Page Industries suffered losses for the first two years of its existence. Premium pricing in a price-sensitive market seemed like a recipe for disaster.

Then fortune smiled—or perhaps it was the invisible hand of market dynamics correcting inefficiencies. In 1997, TTK Tantex and in 2002 Associated Apparel fell prey to labor strikes and both exited the innerwear market, clearing northern and western India market for Jockey. Suddenly, Page's biggest competitors were gone, not beaten in the marketplace but destroyed by their own internal contradictions. The labor strikes that crippled TTK and Associated reflected a fundamental problem in Indian manufacturing—the tension between cost-cutting and quality, between treating workers as expenses versus investments.

Page's approach to labor was different. Free meals, better working conditions, investment in training—these weren't acts of charity but strategic investments in quality and consistency. When your entire value proposition depends on premium quality, you can't afford disgruntled workers or high turnover. The company that survived wasn't necessarily the one with the lowest costs, but the one that understood the true economics of quality.

By 2007, Page had built something remarkable: a profitable, growing business selling premium innerwear in a market that conventional wisdom said didn't exist. Revenue had grown from nothing to hundreds of crores. The distribution network spanned thousands of outlets across hundreds of cities. Most importantly, they had changed consumer behavior—Indians were now willing to pay premium prices for innerwear, seeing it not as a commodity but as an expression of lifestyle and self-care. The foundation was set for the next phase: going public and scaling to heights that even the optimistic Genomals couldn't have imagined.

V. The IPO & Public Market Journey (2007)

February 2007 marked a watershed moment. The IPO prospectus told a story of transformation: a company that had gone from zero to ₹100.94 crores in issue size in just twelve years. The IPO was a combination of fresh issue of 0.14 crore shares aggregating to ₹50.84 crores and offer for sale of 0.14 crore shares aggregating to ₹50.10 crores. The price was set at ₹360 per share—a number that would soon seem quaint.

The IPO bidding started from February 23, 2007 and ended on February 27, 2007, with shares getting listed on BSE and NSE on March 16, 2007. For retail investors, the minimum investment was ₹5,400 for 15 shares—not a small amount in 2007 India. The company even included a reservation of up to 15,000 shares for employees, a gesture that reflected the Genomals' understanding that wealth creation should be shared with those who built it.

The market's initial reception was measured but positive. At ₹360 per share listing, the company was valued modestly by later standards. But what happened next defied all expectations. For those who invested in Page at the IPO price of Rs 360, they were handsomely rewarded—a one lakh rupee investment at the IPO price would eight years later yield approximately Rs 36 lakh, not taking into account the regular dividends paid by the company.

The transformation from private to public company brought new disciplines and pressures. Quarterly results, analyst calls, shareholder meetings—the Genomals had to learn a new language while maintaining their manufacturing obsession. The public market's quarter-to-quarter focus could have derailed their long-term thinking, but they managed to balance both worlds.

What's remarkable about Page's public market journey is how the stock price reflected not just financial performance but a growing recognition of the company's unique position. From 5,000 staff at IPO, the company would grow exponentially. The stock price exceeded 7000 INR for the first time after growth of over 39.7% was announced in May 2014. This wasn't just wealth creation; it was validation of a business model that many had doubted.

The IPO also provided capital for expansion at a crucial time. The fresh issue proceeds went directly into building manufacturing capacity, strengthening distribution, and brand building. Unlike many IPOs that simply provide exits for early investors, Page's IPO was genuinely about growth capital. The Genomals maintained significant skin in the game, with the family retaining majority control even after the public offering.

Early public market performance exceeded all expectations. The stock became a darling of fund managers who saw in Page Industries something rare in Indian markets: a company with pricing power, consistent quality, and management that thought like owners because they were owners. The quarterly results showed steady growth, expanding margins, and most importantly, consistent execution of the strategy laid out in the IPO prospectus.

Building credibility in capital markets required more than just good numbers. The Genomals had to navigate the expectations of institutional investors who wanted aggressive expansion, retail investors who wanted dividends, and analysts who wanted guidance. They managed this by being boringly consistent—doing exactly what they said they would do, quarter after quarter. No surprises, no pivots, no "strategic realignments." Just steady execution of manufacturing premium innerwear and expanding distribution.

The public listing also brought unexpected benefits. It raised Page's profile with consumers, making Jockey seem even more premium because it was backed by a listed company. It helped in recruiting talent who could be offered stock options. It provided currency for potential acquisitions, though the company remained remarkably focused on organic growth. Most importantly, it created a scorecard that everyone could see, pushing the organization to maintain the high standards that had brought them success. The journey from ₹360 to over ₹40,000 per share would make Page Industries one of the greatest wealth creators in Indian stock market history.

VI. Product Portfolio Expansion & Innovation (2000s-2010s)

The evolution from men's underwear manufacturer to lifestyle brand happened gradually, then suddenly. Page's product range expanded from basic vests and briefs to encompass an entire wardrobe: boxer briefs, trunks, inner boxers, tank tops, t-shirts, polos, henleys, sweatshirts, jackets, hoodies, boxer shorts, shorts, bermudas, joggers, track pants, pyjamas, and pants for men. For women: bras, panties, crop tops, camisoles, kurta and kurti slips, sleep dresses, capris, leggings, hipsters, mid-waists, boy legs, bloomers, and shorties. Even accessories got the premium treatment: caps, handkerchiefs, masks, face towels, hand towels, bath towels, and an extensive range of socks.2011 marked a significant diversification when Page licensed Speedo swimwear from Pentland Group for India and Sri Lanka. This wasn't random portfolio expansion—it was strategic adjacency. Speedo, the world's leading swimwear brand, complemented Jockey's positioning perfectly. Both were global brands with heritage, both commanded premium pricing, and both required the same obsessive attention to quality that Page had mastered. The licensing agreement covered swimwear, water shorts, apparel, equipment, and footwear.

The timing seemed questionable. Swimming wasn't exactly mainstream in India. Public pools were rare, private pools rarer still. But Page saw what others missed: India's growing affluent class was traveling internationally, joining health clubs, building private pools. The market was nascent but growing. By financial year 2021-22, despite COVID lockdowns impacting pools and clubs, Speedo achieved a turnover of ₹168 million. As of March 2022, the brand was available in 1,340+ stores, 26+ EBOs, and 12+ Large Format Stores across 230+ cities.

The real innovation happened in product development. Twice-yearly meetings with Jockey USA and global licensees became crucibles of innovation. Page didn't just import designs; they adapted them for Indian body types, climate, and preferences. The 20-member R&D team worked on everything from fabric blends that worked in Indian humidity to sizing that fit Indian bodies better than international standards.

Women's innerwear presented unique challenges and opportunities. In a market dominated by unorganized players and cheap imports, Page introduced Indian women to properly fitted bras, quality fabrics, and designs that balanced modesty with style. They opened dedicated Jockey Woman stores—48 by recent count—creating safe, comfortable spaces for women to shop for intimate apparel. This wasn't just retail; it was cultural transformation.

The kids' segment followed a similar trajectory. Parents who had grown up wearing unbranded innerwear wanted better for their children. Jockey Juniors, with 71 dedicated EBOs, tapped into this aspiration. The kids wear market in India, worth about USD 14 billion in FY 2020 and expected to grow to nearly USD 23 billion by FY 2025, represented massive potential.

Innovation wasn't limited to products. Manufacturing processes constantly evolved. Page made its own elastic—a decision that seemed eccentric but ensured consistent quality across millions of pieces. They invested in automated cutting machines, advanced stitching equipment, and quality control systems that could detect defects invisible to the naked eye. The twice-yearly meetings with Jockey International weren't just about designs; they were knowledge transfer sessions where best practices from 140+ countries were shared and adapted.

The company's approach to innovation was distinctly unglamorous. No moonshots, no pivots into tech, no attempts to become a "platform." Just relentless, incremental improvement in making better underwear. They invested in studying how fabrics behaved after multiple washes, how elastic degraded over time, how different stitching patterns affected comfort. This obsession with minutiae might seem boring, but it created products that customers loved and repurchased—the ultimate validation in consumer goods.

Thermals became an unexpected success story. In a tropical country, selling thermal wear seemed counterintuitive. But Page recognized that millions of Indians traveled to colder climates, worked in air-conditioned offices, or lived in northern states with harsh winters. They didn't just import Jockey's international thermal line; they adapted it for Indian conditions and price points. The result: a product category that barely existed in organized retail became a significant revenue contributor.

The expansion into socks revealed Page's strategic discipline. Socks manufacturing required different machinery, different skills, different supply chains. Lesser companies might have outsourced. Page built dedicated facilities, trained specialized workers, and achieved the same quality standards that defined their core products. By recent counts, their socks capacity had expanded to multiple million pairs annually, with plans for 576 knitting machines after proposed expansions.

What tied all these product expansions together wasn't just the Jockey brand but the Page philosophy: if you're going to do something, do it right. No shortcuts, no compromises, no "good enough." This obsession with excellence across an expanding portfolio created a virtuous cycle. Customers who trusted Jockey for underwear tried their t-shirts. Those satisfied with t-shirts bought swimwear. The brand became synonymous not with a product but with a standard—a promise that whatever bore the Jockey name would be worth the premium price.

VII. Scale & Distribution Mastery (2010s-Present)

The numbers tell a story of relentless expansion: 15 manufacturing complexes spread across Bangalore, Hassan, Mysore, Gowribidanur, Tiptur, and Tirupur. Over 2.2 million square feet of manufacturing space. Capacity to produce 280 million pieces annually. But these statistics only hint at the operational excellence underneath. The flagship Odisha Project represents the next evolution in Page's manufacturing ambitions. Page Industries has commenced operations at its new 650,000 sq. ft. facility in Odisha. The facility in Ramdaspur Village, Cuttack District, includes a raw material warehouse, a men's innerwear manufacturing unit, and dedicated facilities for socks and elastics. Built on a 28.5-acre campus with planned expansion to 6.5 lakh sq. ft., this facility wasn't just about adding capacity—it was about geographical diversification and cost optimization while maintaining Page's exacting standards.

The distribution network tells an equally impressive story: 50,000 plus retail outlets in 1,800 cities, 1,131 Exclusive Brand Outlets including 48 Jockey Woman EBOs and 71 Jockey Juniors EBOs. Each exclusive outlet wasn't just a store but a brand temple—carefully designed spaces that elevated the shopping experience for what had traditionally been a commodity purchase.

The evolution from 223 exclusive outlets to over 1,100 didn't happen through aggressive franchising or capital dumping. Page was selective about partners, insisting on prime locations, proper training, and adherence to display standards. They understood that in India, the retail experience was as important as the product itself. A poorly maintained outlet could destroy years of brand building.

E-commerce presented both opportunity and challenge. Traditional retailers, who had been Page's backbone, viewed online sales as a threat. Page had to navigate this carefully, ensuring online prices didn't undercut offline partners while capturing the growing digital consumer base. Page Industries expects the share of e-commerce in the business mix to reach 10-12 percent over the next five years. This conservative target reflected their commitment to existing partners while acknowledging digital inevitability.

International expansion within licensed territories showcased another dimension of operational excellence. Operating in UAE, Sri Lanka, Bangladesh, Nepal, Oman, Qatar, Maldives, and Bhutan required understanding different regulatory environments, consumer preferences, and distribution challenges. Each market was approached methodically—starting with exports, then distributors, eventually exclusive outlets where volumes justified.

The manufacturing footprint expansion wasn't just about capacity but strategic positioning. Karnataka remained the heart—14 locations including Bangalore, Hassan, Mysore, Gowribidanur, and Tiptur. The single unit in Tamil Nadu (Tirupur) tapped into India's knitwear capital. Each location was chosen for specific advantages: skilled labor availability, proximity to raw materials, or logistics benefits.

Technology adoption happened quietly but significantly. Automated cutting reduced fabric waste. RFID tracking improved inventory management. ERP systems connected manufacturing to retail, enabling quick response to demand changes. But Page never fell for technology theater—no blockchain experiments, no AI grandstanding. Technology served operations, not headlines.

The company's approach to capacity expansion reflected their conservative DNA. While competitors outsourced to chase growth, Page methodically added owned capacity. The launch of this new facility marks a key milestone in Page Industries' capacity expansion journey. With growing demand for premium innerwear and athleisure wear across urban and semi-urban India, this plant is poised to cater to evolving consumer needs. Each new facility went through months of preparation, ensuring quality standards matched existing units before commercial production began.

Logistics and supply chain management became increasingly sophisticated. With thousands of SKUs across multiple brands, categories, and sizes, inventory management was a nightmare waiting to happen. Page invested in systems and processes that ensured the right product reached the right outlet at the right time. Stockouts meant lost sales; excess inventory meant working capital drain. The balance required constant calibration.

The human dimension of scaling often gets overlooked. From 5,000 employees at IPO to over 20,000 today, maintaining culture and quality standards required deliberate effort. Training programs, career progression paths, and the famous free lunches weren't just perks—they were investments in consistency. When your brand promise depends on the stitching quality of a worker in Hassan, that worker's satisfaction matters.

What's remarkable about Page's scaling is what didn't change. Quality standards remained uncompromising. The focus stayed on innerwear and closely adjacent categories. The manufacturing philosophy of vertical integration persisted. While the company grew from regional player to national champion, the DNA remained that of the Genomals' original vision: make the best products, control every variable, and trust that Indian consumers would pay for quality. The distribution mastery wasn't just about reaching more outlets—it was about maintaining standards across every touchpoint, ensuring that a Jockey purchase in Guwahati matched one in Gandhinagar.

VIII. The Numbers Game: Financial Performance & Market Position

Current metrics paint a picture of mature success: Revenue ₹4,974 Cr, Profit ₹765 Cr, Market Cap ₹49,166 Cr. These numbers represent a company that has successfully navigated the treacherous journey from startup to stalwart. But beneath the headline figures lies a more complex story of slowing growth, margin pressures, and questions about the future.

The company has delivered a poor sales growth of 10.9% over past five years—a descriptor that stings for a company accustomed to 20-30% annual growth rates. This deceleration isn't just about size; it's about market maturation, increased competition, and the limits of premium positioning in a price-sensitive market.

Stock volatility tells its own story: 3.78% with beta of 0.78, suggesting a stock that moves less dramatically than the broader market. This stability appeals to certain investors but frustrates others seeking higher returns. The stock's journey from ₹360 at IPO to peaks above ₹40,000 created tremendous wealth, but recent performance has been more pedestrian.

Promoter holding at 42.9%, decreased 3.23% over 3 years. This gradual dilution could signal many things: profit-taking by founders, estate planning, or simply portfolio diversification. While 42.9% still represents strong founder control, the trend bears watching. Markets often interpret promoter selling negatively, though the reasons can be entirely benign.

The competitive landscape has evolved dramatically. Rupa and Lux, traditional players, have upgraded their game. New entrants like Zivame in women's innerwear and various D2C brands targeting millennials have fragmented the market. International brands like Calvin Klein and Tommy Hilfiger have entered India's premium segment. The moat that once seemed impregnable now faces multiple assault points.

Unit economics reveal both strength and challenge. Gross margins remain healthy, driven by pricing power and operational efficiency. But selling and distribution expenses have increased as the company invests in new outlets, e-commerce, and brand building. The capital efficiency that characterized early growth has given way to more capital-intensive expansion.

The comparison with competitors is instructive. While Page trades at premium valuations—P/E ratios often exceeding 60—competitors like Rupa trade at fraction of these multiples. The market clearly assigns a quality premium to Page, but this also means expectations are high. Any disappointment in quarterly results triggers sharp corrections.

Revenue composition shows interesting trends. While men's innerwear remains the cash cow, women's and kids' segments are growing faster from smaller bases. Athleisure, particularly post-COVID, has emerged as a significant contributor. Speedo remains subscale despite years of investment. This portfolio evolution reflects both opportunity and execution challenges.

Working capital management deserves attention. As the company has expanded into more categories and channels, inventory days have increased. The cash conversion cycle has lengthened. While still healthy by industry standards, the trend suggests complexity is extracting a toll on capital efficiency.

Return metrics remain impressive but declining. ROE exceeding 50% sounds fantastic until you realize it was once above 70%. ROCE similarly has compressed as the asset base has expanded faster than profits. These are still exceptional numbers, but the trajectory raises questions about reinvestment opportunities and growth prospects.

The dividend policy reflects confidence and conservatism. Regular payouts, including special dividends, reward shareholders while retaining sufficient capital for growth. The balance suggests management confidence in cash generation but also acknowledgment that growth opportunities may be less abundant than before.

Geographic revenue distribution shows concentration risk. Despite international licenses, India dominates revenue contribution. The other markets—Sri Lanka, Bangladesh, Nepal, UAE—remain marginal contributors despite years of effort. This suggests either execution challenges or structural limitations in these markets.

Channel mix evolution tells another story. Traditional trade still dominates, but modern trade (organized retail) and e-commerce are growing faster. Each channel has different economics—modern trade demands higher margins, e-commerce requires different logistics capabilities. Managing this channel complexity while maintaining margins requires constant recalibration.

Price realization improvements have historically driven growth alongside volume expansion. But there are limits to premium pricing, especially as competition intensifies. The company's ability to continue extracting price increases without volume impact will determine future profitability.

The financial performance must be contextualized within the broader narrative. Page Industries transformed India's innerwear market, created tremendous wealth, and built an enduring brand. Current numbers—₹4,974 Cr revenue, ₹765 Cr profit—represent success by any measure. But markets are forward-looking, and the question isn't whether Page is successful today but whether it can reignite growth tomorrow. The numbers tell a story of a company at an inflection point, needing to prove that the next chapter can be as compelling as the last.

IX. Leadership & Culture: The Genomal Way

Sunder Genomal's recognition speaks volumes: Forbes #73 wealthiest Indian with an estimated net worth of approximately $1.9 billion, Ernst & Young Entrepreneur of the Year Award in 2017. But these accolades only hint at the leadership philosophy that built Page Industries. At 61, Sunder still plays basketball competitively, strums guitar at charity events—details that reveal a leader who hasn't let success calcify into complacency.

The management style blends family business intimacy with professional discipline. Sunder, who at 61 still likes to play basketball competitively, says spending time with employees on the factory floor is what keeps him going. Sunder also likes to strum the guitar at charity events. While brothers Nari and Ramesh are on the board, Sunder's son Shamir is clearly being groomed to take over the top job eventually. This isn't corporate theater—it's genuine engagement that permeates the organization.

The awards tell a story of consistent excellence. "Best Licensee of the Year" 7 times from Coopers-Jockey, 5 times from Jockey Inc. In 2010, the Company bagged the "International Licensee of the Decade" award for achieving record growth year after year, offering world class products and maintaining global quality standards across all operations. These aren't participation trophies—Jockey has licensees in 140+ countries. To be repeatedly recognized as the best requires exceptional execution.

The extension of the licence agreement till December 2040 showcases Jockey's confidence in Page Industries. This contract was up to 2030. Most licensing agreements run 5-10 years. Page earned a 20-year extension, then another 10 years on top. This unprecedented vote of confidence from Jockey International reflects a relationship that transcends typical licensor-licensee dynamics.

The focus philosophy seems almost quaint in an era of conglomerate ambitions. No unnecessary diversifications—when everyone was launching private labels, entering real estate, or backward integrating into cotton farming, Page stuck to what they knew: making and selling premium innerwear. This discipline required saying no to seemingly attractive opportunities, resisting banker pitches for acquisitions, avoiding the siren song of unrelated diversification.

Family business dynamics at Page avoid common pitfalls. There's no visible sibling rivalry, no messy succession battles, no professional-versus-family tensions that destroy many Indian businesses. The transition planning appears methodical—Shamir Genomal's grooming is happening gradually, transparently. He's earning his stripes rather than being helicoptered into leadership.

The culture manifests in unusual ways. Free lunch for all workers isn't just a perk—it's a statement about equality and care. Everyone from the shop floor to the C-suite eats the same food. This might seem trivial, but in status-conscious India, such gestures matter. They signal that while hierarchies exist, human dignity is universal.

The approach to talent is telling. When Page needed expertise, they hired from diverse industries—telecom, consumer goods, direct selling. They weren't looking for apparel industry veterans but for professionals who understood quality, systems, and consumer marketing. This cross-pollination brought fresh perspectives while the Genomal family provided industry knowledge and relationships.

Decision-making balances speed with deliberation. Major strategic decisions—like entering new categories or building facilities—take time, involving extensive research and planning. But operational decisions happen quickly, without bureaucratic delays. This dual-speed approach allows strategic patience while maintaining operational agility.

The relationship with Jockey International exemplifies trust-based business. Despite being a licensee, Page operates with unusual autonomy. Product development happens collaboratively, with Page's insights about Indian consumers influencing global designs. This isn't a master-servant relationship but a partnership between equals who respect each other's expertise.

Risk management reflects conservative instincts. No debt-funded expansion, no betting the company on new ventures, no "transformational" acquisitions. Growth is internally funded, organic, steady. This approach might seem boring to markets hungry for excitement, but it has delivered consistent results without existential risks.

The communication style—both internal and external—favors substance over style. Investor calls are straightforward, without buzzwords or grand visions. Annual reports focus on operational metrics rather than glossy narratives. This plain-speaking approach might underwhelm analysts seeking quotable soundbites, but it reflects authentic leadership.

Employee retention and development strategies emphasize long-term careers over short-term jobs. Many senior executives have been with Page for decades. This continuity ensures institutional knowledge preservation and cultural consistency. In an industry notorious for high attrition, Page's stability stands out.

The approach to competition mixes confidence with respect. As Sunder noted: "We are the best performers for Jockey among the 45 licensees it has across the world." There's pride without arrogance, achievement without complacency. Competitors are watched but not obsessed over. The focus remains internal—on improving products, processes, and customer experience.

Social responsibility happens quietly. No CSR grandstanding, no photo-ops with oversized checks. The company fulfills its obligations, supports communities around manufacturing facilities, but doesn't weaponize charity for marketing. This understated approach reflects the Genomal family's values—do good without seeking applause.

What emerges is a portrait of leadership that combines immigrant entrepreneurship, family values, professional management, and manufacturing excellence. The Genomal Way isn't easily replicable because it's not a strategy but a philosophy—one that values relationships over transactions, quality over quantity, and patience over haste. As Page Industries navigates its next phase, maintaining this culture while adapting to new realities will determine whether the company's best days are behind or ahead.

X. Strategic Analysis & Investment Lessons

The licensing model that underpins Page Industries offers both tremendous advantages and hidden vulnerabilities. Unlike owning brands outright, licensing provides instant credibility, global R&D access, and proven products without massive marketing investments. Page pays royalties to Jockey—typically 5-7% of sales—but gains access to designs, technology, and brand equity built over 140 years. This capital-light approach to brand building is genius until the license gets revoked or terms turn unfavorable.

The relationship with Jockey, spanning multiple generations and geographies, provides unusual stability. The license extension till 2040, then renewable for 50-year periods, essentially grants perpetual rights. But perpetual doesn't mean unconditional. Performance targets, quality standards, and brand guidelines must be maintained. Any significant breach could theoretically trigger termination, though the depth of the relationship makes this unlikely.

Brand building in commoditized categories requires a special alchemy. Page didn't just sell better underwear; they sold a lifestyle upgrade. They convinced Indian consumers that intimate apparel deserved the same attention as outerwear. This psychological shift—from functional necessity to personal expression—created pricing power in a category where none existed. The lesson: premium positioning requires changing consumer mindsets, not just product quality.

Competitive advantages layer upon each other creating compound moats. 50+ year Jockey relationship provides trust and knowledge transfer. Vertical integration ensures quality control. Distribution density creates availability advantages. Manufacturing scale drives cost efficiency. Each advantage alone is replicable; together they create formidable barriers.

Capital allocation at Page reflects remarkable discipline. No major acquisitions despite banker pitches. No unrelated diversification despite market fashion. No debt-funded expansion despite cheap capital availability. Instead: steady reinvestment in manufacturing, measured outlet expansion, and patient brand building. This boring approach delivered extraordinary returns precisely because it avoided the value destruction that characterizes most corporate adventures.

The systems knowledge accumulated over decades represents invisible capital. How to ensure consistent stitching across millions of pieces. How to manage inventory across thousands of SKUs. How to train retail partners for premium selling. How to adapt global designs for local preferences. This operational intelligence, encoded in processes and people, can't be acquired quickly regardless of capital availability.

Access to global R&D through Jockey provides innovation without investment. When moisture-wicking fabrics emerge, Page gets the technology. When new manufacturing techniques develop, Page learns them. When design trends shift, Page knows immediately. This borrowed innovation allows Page to stay current without massive R&D spending, focusing resources on execution rather than experimentation.

Why Page succeeded where others failed offers crucial lessons. Associated Apparels had Jockey earlier but couldn't manage labor relations. TTK had distribution but lacked brand building skills. VIP tried premium positioning but couldn't deliver consistent quality. Page combined operational excellence, brand building capability, and patient capital—a rare trifecta in Indian business.

The premium positioning playbook Page pioneered has broader applications. Start with uncompromising quality. Build distribution before demand. Invest in retail experience. Price for profitability not market share. Focus on consumption upgradation not market expansion. Be patient with returns. This approach works in any category where consumers are ready to pay for genuine superiority.

Market timing mattered enormously. The 1990s liberalization created the opportunity. Rising incomes enabled premium purchasing. Changing social norms made brand consciousness acceptable. Mall culture provided retail infrastructure. Page caught all these waves perfectly. The lesson: even great execution needs favorable conditions.

The focused diversification strategy—staying within innerwear and immediately adjacent categories—avoided complexity while capturing synergies. Each new category leveraged existing capabilities: manufacturing knowledge, distribution relationships, brand equity. This adjacency expansion is far less risky than unrelated diversification but still provides growth avenues.

Partnership approach with retail extends beyond transactional relationships. Page trains store staff, provides fixtures, ensures prominent placement, and maintains pricing discipline. Retailers become brand ambassadors rather than just distributors. This collaborative approach creates aligned incentives and sustainable advantages.

The sustainability of Page's model faces several tests. Can premium positioning survive economic downturns? Will new-age consumers remain brand loyal? Can the company adapt to digital commerce without alienating traditional partners? How will succession planning affect culture and execution? These questions don't have easy answers, but Page's track record suggests adaptive capability.

Risk factors often hide in success itself. High margins attract competition. Market leadership breeds complacency. Generational transition risks culture dilution. License dependency creates vulnerability. Stock market success raises expectations unsustainably. Managing these success-induced risks requires constant vigilance.

For investors, Page Industries offers several lessons. Quality commands valuation premiums but also performance expectations. Focused companies often outperform conglomerates. Operational excellence matters more than strategic brilliance. Patient capital compounds while impatient capital churns. Brand-building in everyday categories can create extraordinary value.

The strategic analysis reveals a company that succeeded through discipline rather than disruption, execution rather than innovation, focus rather than diversification. Whether these virtues remain valuable in a rapidly changing market will determine if Page Industries' next chapter matches its last. The lessons, however, endure regardless: build trust through consistency, create value through quality, and grow through patience rather than haste.

XI. Bear & Bull Cases

Bull Case: The Underpenetrated Opportunity

India's innerwear market presents a paradox of underpenetration. Despite Page's success, organized players control less than 20% of the market. The remaining 80% consists of unbranded, regional, and counterfeit products. As India's per capita income crosses $3,000—a threshold where discretionary spending accelerates—millions of consumers will upgrade from unbranded to branded innerwear. Page, with its distribution density and brand recognition, stands to capture disproportionate share.

The premium segment where Page operates is growing faster than the overall market. While total innerwear grows at 8-10% annually, the premium segment expands at 15-20%. This segment expansion isn't just about wealthy consumers; it's about middle-class consumers choosing quality over quantity. Buying three premium undergarments instead of six cheap ones represents a consumption pattern shift that favors Page.

Distribution infrastructure keeps expanding: The Company distributes pan India, including approximately 50,000 plus retail outlets in 1,800 cities and towns. The Company through its authorized franchisees has approximately 1,131 Exclusive Brand Outlets, including 48 Jockey Woman EBOs and 71 Jockey Juniors EBOs. Each new outlet, each new city penetrated, expands the addressable market. Rural India, still largely untapped, represents enormous potential as infrastructure improves and incomes rise.

Women's innerwear market is where Page's opportunity truly explodes. Currently contributing about 30% of revenue, this segment could equal or exceed men's contribution. Indian women increasingly prioritize comfort, fit, and quality in intimate apparel. Page's dedicated Jockey Woman stores and trained staff address cultural sensitivities while providing superior products. As women's workforce participation increases, spending on quality innerwear follows.

Adjacent category expansion offers growth without straying from core competence. Athleisure, already showing strong growth, benefits from health consciousness and casual work cultures. Kidswear taps into parental aspirations for quality. Each category leverages Page's manufacturing excellence and distribution network while addressing new consumption occasions.

International markets within the licensed territory remain nascent. Bangladesh's 170 million population, UAE's affluent consumers, Nepal and Sri Lanka's growing middle classes—all represent untapped potential. Page's conservative international expansion leaves room for acceleration as management bandwidth and market understanding improve.

Bear Case: The Maturation Challenge

The numbers don't lie: sales growth of 10.9% over past five years is described as "poor." For a company trading at premium valuations, double-digit growth is table stakes. This deceleration might not be temporary but structural, reflecting market saturation in core segments and cities. When your products are already available in 50,000 outlets across 1,800 cities, where's the next growth frontier?

Competition has intensified dramatically. D2C brands like Bombay Shaving Company (underwear line), international brands like Calvin Klein, and rejuvenated domestic players like Lux Industries all target Page's profitable niche. These aren't fly-by-night operators but well-funded, sophisticated competitors with differentiated strategies. D2C brands particularly appeal to younger consumers with social media marketing and subscription models that Page hasn't mastered.

The dependency on a single brand is concerning. Despite Speedo and minor experiments, Jockey contributes approximately 98% of revenue. This concentration creates vulnerabilities: any Jockey brand damage globally affects Page, any license term change impacts economics, any strategic shift by Jockey International could destabilize Page. Diversification attempts haven't succeeded, suggesting either execution issues or structural barriers.

Margin pressure appears inevitable. Input cost inflation, particularly in cotton and synthetic materials, can't always be passed to price-sensitive consumers. Rising retail rentals, increasing employee costs, and higher marketing spends to combat competition all pressure profitability. The operating leverage that drove margin expansion during growth phases works in reverse during slowdowns.

E-commerce disruption threatens Page's traditional moat. Online shopping removes the retail experience advantage Page carefully built. Price comparison is instant, brand switching friction is low, and new brands can reach consumers without massive distribution investments. Page's conservative e-commerce approach—targeting just 10-12% of sales—might be insufficient as consumer behavior shifts rapidly.

Valuation multiples leave no room for disappointment. Trading at P/E ratios exceeding 60, the stock prices in perfect execution and continued growth. Any earnings miss, guidance reduction, or strategic misstep triggers sharp corrections. High valuations also limit upside potential—even good performance might not drive appreciation if it's already expected.

Cultural shifts might work against premium innerwear. Sustainability consciousness makes consumers question frequent replacement cycles. Minimalism trends reduce wardrobe sizes. Work-from-home permanence decreases dressing-up occasions. These shifts don't eliminate innerwear demand but might cap premium segment growth.

Promoter stake reduction—down 3.23% over 3 years to 42.9%—raises subtle concerns. While still substantial, the trend suggests either profit-booking or declining confidence. Markets interpret promoter selling negatively, creating overhang on stock performance.

New-age competition operates with different economics. D2C brands accept losses for growth, funded by venture capital. International brands can subsidize India losses from global profits. These competitors can underprice Page structurally, not just tactically, forcing difficult choices between market share and margins.

The bear case isn't about Page becoming a bad company—it's about a great company facing the limits of growth in a maturing market with intensifying competition. High valuations mean even good performance might disappoint markets expecting greatness. The question isn't whether Page remains profitable but whether it can deliver returns justifying premium valuations.

XII. Epilogue: The Future of Page Industries

The next chapter of Page Industries will be written by a new generation, in a new market reality, facing new challenges. The transition from Sunder to Shamir Genomal represents more than succession—it's a test of whether family businesses can institutionalize excellence across generations. Shamir inherits not just a company but a culture, philosophy, and set of relationships built over decades. His challenge: maintaining what works while adapting what must change.

Digital transformation poses existential questions. Can Page create direct-to-consumer capabilities without alienating channel partners who built the business? Can they master social media marketing while maintaining premium positioning? Can they leverage data analytics for inventory optimization without losing the human touch that defines their retail experience? These aren't technology questions but strategic choices about the company's future identity.

The D2C evolution requires capabilities Page hasn't traditionally emphasized: content marketing, influencer relationships, subscription models, personalization algorithms. Building these capabilities organically takes time; acquiring them risks culture dilution. The company must navigate this carefully, perhaps through partnerships or measured experiments rather than dramatic pivots.

Sustainability and ESG considerations increasingly influence consumer choices and investor decisions. Page's manufacturing-heavy model faces scrutiny on environmental impact. Labor practices, always a strength, need continuous improvement to meet evolving standards. The company's response to these pressures will determine its social license to operate and access to conscious consumers.

India's consumption story itself faces uncertainty. Will premiumization continue despite economic volatility? Can discretionary spending growth sustain amid job market pressures? How will generational differences in brand loyalty affect businesses built on repeat purchases? Page's future depends not just on execution but on macro trends beyond their control.

The lessons from Page Industries' journey resonate beyond innerwear, beyond India, beyond family businesses. First, the power of focus: while diversification tempts, excellence in one domain often creates more value than mediocrity across many. Second, the importance of patient capital: building brands, distribution, and manufacturing excellence takes decades, not quarters. Third, the value of trust: the Genomal-Jockey relationship shows how trust-based partnerships outperform transactional relationships.

For entrepreneurs, Page demonstrates that disruption isn't the only path to success. Sometimes, executing basics exceptionally well in overlooked categories creates more value than chasing technological moonshots. The company didn't invent new products or business models; they simply made better underwear and convinced people to pay for it.

For investors, Page offers sobering reminders about valuation and growth. Great companies don't always make great investments if the price is wrong. Growth rates inevitably slow as companies scale. Today's moats might be tomorrow's legacy burdens. The margin of safety matters, especially for high-quality companies where perfection is priced in.

The cultural transformation Page enabled deserves recognition. They didn't just sell products; they changed how Indians think about intimate apparel. They made quality innerwear aspirational, branded underwear normal, and premium pricing acceptable. This psychological shift represents perhaps their greatest achievement—one competitors can't easily replicate.

Looking ahead, several scenarios could unfold. The optimistic case sees Page successfully navigating digital transformation, international expansion accelerating, and new categories contributing meaningfully to growth. The base case envisions steady but unspectacular growth, margins under pressure but sustainable, and stock price reflecting business fundamentals rather than momentum. The pessimistic scenario involves market share losses to nimble competitors, margins eroding under competition, and valuations compressing to sector averages.

What seems certain is that Page Industries' next decade won't resemble its last. The tailwinds of market creation, category premiumization, and distribution expansion are weakening. Future growth must come from market share gains, international expansion, or new categories—all harder than riding sectoral growth. The company that transformed Indian innerwear must now transform itself.

The final lesson might be the most important: business success is temporary, but business principles endure. Quality matters. Trust compounds. Focus beats diversification. Patient capital outperforms impatient capital. These principles made Page Industries; they'll determine whether the company thrives in its next chapter.

As monsoon clouds gather over Bangalore, where this story began, Page Industries stands at an inflection point. The company that convinced Indians to pay premium prices for underwear must now convince markets it can grow despite maturity, compete despite new threats, and evolve despite legacy success. The outcome isn't predetermined—it depends on decisions being made today in boardrooms and factory floors, in retail outlets and digital platforms, by a new generation carrying forward an old legacy.

The story of Page Industries isn't finished. Whether the next chapters match the drama and success of the first ones remains to be written. But regardless of what comes next, the company's journey from Manila to Mumbai, from startup to stalwart, from commodity to premium, stands as testament to what's possible when vision meets execution, when patience meets opportunity, when family businesses professionalize without losing their soul. In Indian business history, few stories match Page Industries' combination of audacity, excellence, and achievement. That legacy, regardless of future stock prices or growth rates, is secure.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube