Oswal Pumps: How a Small Haryana Pump Maker Became India's Solar Agriculture Champion

I. Introduction & Cold Open

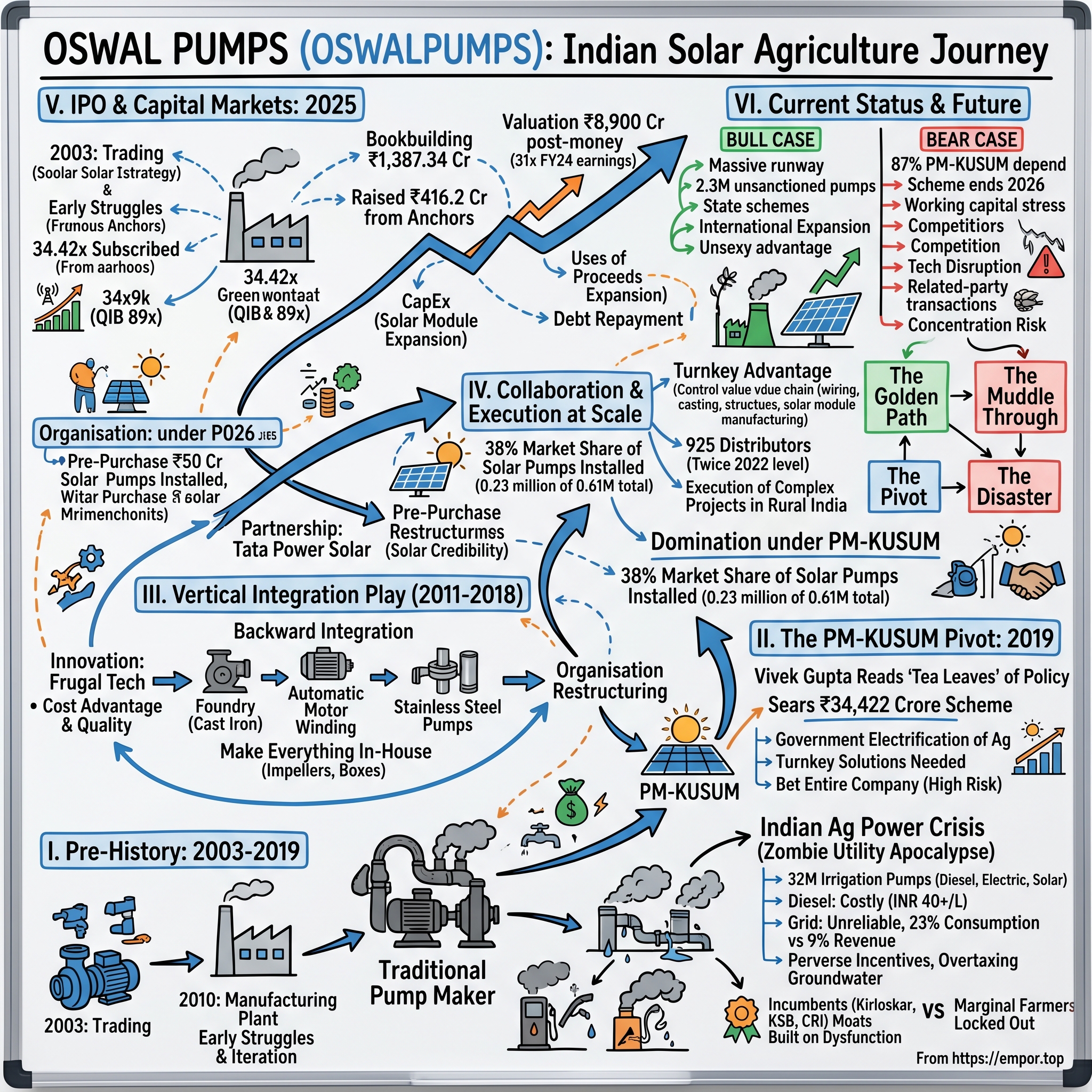

Picture this: A dusty industrial estate in Karnal, Haryana, 2019. Inside a modest conference room, Vivek Gupta, the second-generation scion of Oswal Pumps, stares at a government notification that just landed on his desk. The PM-KUSUM scheme—₹34,422 crores allocated for solar-powered irrigation. His competitors at Kirloskar and KSB are skeptical. "Another government scheme," they mutter, "full of red tape and delayed payments." But Vivek sees something different. He sees the future of Indian agriculture, and he's about to bet his entire company on it.

Fast forward to today: Oswal Pumps commands a staggering 38% market share of all solar pumps installed under PM-KUSUM. The company that started as a small-time pump trader in 2003 now sports a ₹8,900 crore market cap, with 88% of its revenue flowing directly from government coffers. It's a transformation so complete, so audacious, that it redefines what it means to ride a policy wave in India. But here's what makes this story truly remarkable: This isn't just another boring infrastructure play. It's a masterclass in how to transform a commodity business into a growth rocket by aligning perfectly with government policy. When others zigged toward exports and diversification, Oswal zagged hard into government tenders. The result? By March 31, 2024, Oswal supplied approximately 0.18 million solar-powered agricultural pumps, representing around 43.8% of the total installed under the PM Kusum Scheme.

Think about that for a moment. A company with no prior solar experience before 2019 now dominates India's most ambitious agricultural electrification program. It's as if a local restaurant chain suddenly became McDonald's primary burger supplier overnight—except the stakes here involve feeding a nation and transforming its energy infrastructure.

This is the story of how a traditional pump manufacturer read the tea leaves of policy change, made an all-in bet that would terrify most boards, and emerged as the unlikely champion of India's solar agriculture revolution. It's about family businesses, patient capital, and the peculiar dynamics of selling to the Indian government. Most importantly, it's about what happens when unsexy industrial companies collide with sexy renewable energy narratives—and win.

II. The Pre-History: Indian Agriculture's Power Crisis

To understand Oswal Pumps' rise, you first need to grasp the powder keg of problems that made India's agricultural electricity situation ripe for disruption. It's 2019, and India's farms are caught in a vicious cycle that would make any economist weep.

India has an estimated 32 million irrigation pumps operating that use diesel, electric, or solar power. Of these, ten million run on diesel—burning through fuel at rates that would horrify any environmental activist. The remaining pumps depend on grid electricity, but here's where it gets interesting: While the share of electricity consumed by agricultural consumers is nearly 23%, revenue realization from agricultural consumers is only about 9%. Agricultural electricity subsidies are equivalent to about 25% of India's fiscal deficit, twice the annual public spending on health or rural development.

Think about that for a moment. The government is essentially running the world's largest energy charity program for farmers, hemorrhaging money at a scale that would make even the most profligate venture capitalist blush. State electricity boards across India are technically bankrupt, kept alive only by periodic government bailouts. It's a zombie utility apocalypse, Indian-style.

But the subsidy addiction creates perverse incentives everywhere. In states like Punjab and Haryana—India's agricultural powerhouses—electricity is either free or so heavily subsidized it might as well be. The result? Farmers install oversized pumps, leave them running all day, and extract groundwater like there's no tomorrow. Government regulators have stopped electric pump subsidies in Punjab, Haryana, Rajasthan, Karnataka, Tamil Nadu, and Uttar Pradesh to discourage farmers from pumping due to the overextraction of groundwater.

Meanwhile, in states where electricity isn't subsidized or is unreliable (which is most of them), farmers turn to diesel. At greater than INR 40/l since price deregulation in 2014, diesel is more expensive than agricultural electricity rates in most Indian states. A typical farmer running a 5 HP diesel pump for irrigation spends ₹40,000-60,000 per season on fuel alone—often more than their children's education costs.

The competitive landscape pre-2019 reflected this dysfunction perfectly. Kirloskar Bros, founded in 1888, dominated with their robust cast-iron pumps built like tanks—because they needed to be. When your electricity supply fluctuates between 160V and 280V (when it should be 220V), and power cuts are as predictable as monsoon delays, you need equipment that can take a beating. KSB India, the German engineering giant's local subsidiary, captured the premium segment with pumps that cost twice as much but lasted three times as long. CRI Pumps from Coimbatore owned the energy-efficiency narrative, crucial when every unit of electricity saved meant real money.

These incumbents had built their moats around the existing dysfunction. Their business models assumed that electricity would remain subsidized but unreliable, diesel would stay expensive but available, and farmers would continue this dance of desperation season after season. They sold pumps the way arms dealers sell weapons—profiting from an endless conflict with no resolution in sight.

The irrigation crisis went deeper than just power. Higher capacity pumps can effectively meet the irrigation needs of only 32 per cent of farmers who own land over one hectare. Whereas micro solar pumps, which are typically less than 1 hp in size, can meet the irrigation needs of 68 per cent of farmers who are marginal farmers and own land less than one hectare. Yet the entire pump industry was oriented toward selling bigger, more powerful pumps to fewer, larger farmers. The marginal farmers—the backbone of Indian agriculture—were essentially locked out of mechanized irrigation.

Enter renewable energy as the potential game-changer. Solar pumps had been around since the 1990s, but they were expensive toys for NGO demonstration projects. The economics simply didn't work: a 5 HP solar pump system cost ₹4-5 lakhs versus ₹30,000 for a diesel pump. Even with zero operating costs, the payback period stretched beyond a decade—longer than most farmers' planning horizons.

But by 2018, something fundamental had shifted. Solar panel prices had crashed 90% in a decade. The Indian government, facing both a fiscal crisis from electricity subsidies and international pressure on climate commitments, needed a way out. PM KUSUM is a significant initiative by the Government of India and the Ministry of New and Renewable Energy (MNRE) aiming to deliver clean energy to over 35 lakh farmers by solarizing their agriculture pumps.

The stage was set for disruption. The incumbent pump manufacturers, comfortable in their oligopoly, saw solar as a niche—maybe 5-10% of the market eventually. They had no idea that a small pump maker from Karnal was about to rewrite the entire playbook.

What Kirloskar, KSB, and CRI failed to see was that PM-KUSUM wasn't just another subsidy scheme. It was a fundamental restructuring of how agricultural power would work in India. And while they debated whether to enter this "risky" segment, Vivek Gupta at Oswal Pumps was already drawing up plans to bet everything on it.

III. Origin Story: From Trading to Manufacturing (2003–2010)

The year is 2003. George W. Bush has just declared "Mission Accomplished" in Iraq, the Human Genome Project is complete, and in a small industrial plot in Karnal, Haryana, Padam Sain Gupta is staring at a pile of imported Chinese pump components, wondering if he's making the biggest mistake of his life.

Padam Sain wasn't supposed to be here. Like many Haryana businessmen of his generation, he'd started as a trader—buying pumps from manufacturers, adding a margin, selling to farmers. It was a comfortable existence: no factory overhead, no worker unions, no quality complaints to handle directly. Just relationships and razor-thin margins. But Padam Sain saw something others didn't: the Chinese were coming, and they were bringing pumps that cost half what Indian manufacturers charged.

"If you can't beat them, join them," he might have thought. But Padam Sain took a third path: learn from them, then beat them at their own game. He started M/s Oswal Electricals (Pumps) as a sole proprietorship, initially assembling pumps from imported components. It wasn't manufacturing in the true sense—more like sophisticated Lego assembly for adults. But it was a start.

The early product line was deliberately unglamorous: low-speed monoblock pumps, the Maruti 800s of the pump world. These were 0.5 to 2 HP pumps that moved water slowly but steadily, perfect for small farmers filling overhead tanks or irrigating kitchen gardens. While Kirloskar was selling 10 HP submersibles to large farmers, Padam Sain was selling 1 HP surface pumps to farmers with half an acre. It was the bottom of the pyramid, but in India, that's where the volume lives.

By 2007, the business had grown enough to require a more formal structure. The takeover of M/s Oswal Electricals from sole proprietorship to private limited company wasn't just paperwork—it was a generational transition. Vivek Gupta, Padam Sain's son, fresh from engineering college with ideas about "quality systems" and "backward integration," was pushing for change.

Vivek was a different breed from his father. Where Padam Sain relied on relationships and intuition, Vivek brought spreadsheets and process charts. He'd spent time at trade shows in China and Germany, watching how real manufacturers operated. He'd seen the advanced testing equipment at KSB's facility, the precision casting at Kirloskar's foundry. And he'd come back convinced that Oswal couldn't survive as an assembler. They needed to become manufacturers—real manufacturers.

The father-son dynamic was classic Indian family business theater. Board meetings (which consisted of Padam Sain, Vivek, and occasionally Vivek's mother serving tea) would stretch late into the night. Padam Sain would argue for caution: "Why fix what's not broken?" Vivek would counter with market data: "Chinese pumps are getting 2% cheaper every year. Our margins will disappear in five years."

The 2008 financial crisis, paradoxically, settled the argument. Credit dried up, imported components became expensive as the rupee crashed, and suddenly having local manufacturing capability didn't seem like such a bad idea. The decision was made: Oswal would build its own factory.

The 2010 manufacturing plant in Karnal wasn't born from a McKinsey strategy deck or private equity investment thesis. It was bootstrapped with personal savings, loans against family property, and a lot of prayer. The location was strategic though—Karnal sits at the heart of Haryana's agricultural belt, close to both suppliers and customers. Land was (relatively) cheap, labor was available, and the state government was offering incentives for manufacturing.

The initial setup was modest: a 5,000 square meter shed, some basic metalworking equipment, and a testing tank that leaked for the first three months. The first pumps that rolled off the production line were, to put it charitably, works in progress. Quality control meant Vivek personally testing every tenth pump. When customers complained, which they did often, Vivek would drive to their farms himself to fix the problems.

But here's what set Oswal apart even in these early, struggling days: they listened. When farmers complained that pump impellers wore out too quickly, they experimented with different alloys. When retailers said packaging was poor, they redesigned their boxes. When mechanics said pumps were hard to repair, they simplified the design. This wasn't sophisticated customer research—it was survival-driven iteration.

The competitive landscape they entered was brutal. Kirloskar had been making pumps since 1911. They had brand recognition that money couldn't buy—ask any Indian farmer about pumps, and "Kirloskar" would be the first name mentioned. KSB brought German engineering credentials. CRI had government relationships built over decades. Local players like Shakti Pumps and Texmo had regional strongholds.

Oswal's strategy, if you could call it that, was to be the Toyota Corolla of pumps: not the best at anything, but good enough at everything, and cheaper than the competition. They targeted the dealers that bigger brands ignored—the ones in tehsil towns rather than district headquarters, the ones who also sold seeds and fertilizers, the ones who extended credit to farmers during bad monsoons.

The early struggles were real and numerous. In 2009, a batch of 500 pumps had to be recalled due to faulty bearings—nearly bankrupting the company. Payment cycles stretched to 120 days as dealers delayed payments and farmers defaulted. Vivek jokes now about how he knew every money lender in Karnal by first name, but at the time, it wasn't funny.

Yet slowly, order by order, dealer by dealer, Oswal built a presence. By 2010, they were selling 10,000 pumps a year—a rounding error for Kirloskar, but enough to keep the lights on. More importantly, they'd learned the business from the ground up. They understood not just how to make pumps, but why farmers bought them, how dealers financed them, when demand peaked, and where the margin pools were.

The 2010 plant opening ceremony was a modest affair—some marigold garlands, a small puja, sweets distributed to workers. Padam Sain, in his speech, thanked employees and predicted they'd one day compete with the big brands. People smiled politely, thinking it was founder optimism. Nobody, including probably Padam Sain himself, imagined that within a decade, his company would dominate India's largest agricultural infrastructure program.

But that's the thing about origin stories—they only make sense in reverse. At the time, Oswal Pumps was just another small manufacturer in a crowded market, trying to survive. The seeds of future dominance—the manufacturing capability, the dealer relationships, the deep understanding of farmer needs, and most importantly, the willingness to make big bets—were all being planted. They just didn't know it yet.

IV. The Vertical Integration Play (2011–2018)

The conference room at Kirloskar's Pune headquarters, 2012. The executive team is reviewing supplier contracts when someone mentions a small Haryana pump maker who's started making their own castings. "Oswal Pumps?" the supply chain head chuckles. "They'll burn through cash and come back to buying from foundries within two years. Vertical integration is for companies with scale."

He was wrong. Dead wrong.

Vivek Gupta's vertical integration strategy started not from some grand vision, but from a vendor meeting gone bad. In 2011, Oswal's main casting supplier—who provided the pump bodies that housed all the mechanical components—announced a 15% price increase with two days' notice. Vivek pleaded, negotiated, even threatened to switch suppliers. The vendor's response was blunt: "Go ahead. Every foundry in North India is raising prices. Steel costs are up, labor costs are up. You pump assemblers will pay, or you'll shut down."

That night, Vivek made a decision that would define Oswal's next decade: if suppliers could hold them hostage, they wouldn't use suppliers. Oswal would make everything itself.

The backward integration started with cast iron casting—the messiest, most capital-intensive part of pump manufacturing. Setting up a foundry in 2011 wasn't just expensive; it was considered foolish. The minimum efficient scale for a foundry was massive, environmental clearances were nightmarish, and the technical expertise required was scarce. But Vivek saw it differently. Every competitor outsourced casting. If Oswal could master it, they'd have a cost advantage that couldn't be replicated quickly.

The foundry setup was a comedy of errors that somehow worked. The first furnace, bought second-hand from a closing factory in Faridabad, had to be transported on three trucks and reassembled like a giant jigsaw puzzle. The initial castings were so poor that workers joked they could be used as modern art sculptures. The quality control reject rate hit 40% in the first month.

But here's where Oswal's scrappy DNA paid off. Instead of hiring expensive consultants, Vivek recruited retired engineers from Kirloskar and BHEL—men in their 60s who'd forgotten more about casting than most people ever knew. He paid them consulting fees that seemed astronomical for Oswal but were pocket change compared to what McKinsey would charge. These gray-haired gurus spent months on the shop floor, teaching workers how to read the color of molten metal, how to design gates and risers, how to control cooling rates.

Simultaneously, Oswal tackled automatic motor winding and lacing. Electric motors are the heart of any pump, and winding—the process of wrapping copper wire around the motor core—determines efficiency and lifespan. Most small manufacturers outsourced this to specialized shops in Delhi's Mayapuri industrial area. Oswal bought winding machines and, more importantly, poached two master winders from a competitor with salary offers they couldn't refuse.

The integration went deeper. Pumps need impellers (the rotating components that actually move water), shafts, bearings, seals, and dozens of smaller components. One by one, Oswal brought these in-house. By 2012, they were even making their own packaging boxes—because why pay someone else's margin on cardboard?

2012 also marked Oswal's entry into stainless steel fabricated pumps. This wasn't just adding another product line; it was a technological leap. Stainless steel pumps lasted longer, resisted corrosion better, and could handle aggressive water (high in salts and minerals) that destroyed cast iron pumps. But working with stainless steel required different skills—welding instead of casting, fabrication instead of molding, precision cutting instead of rough grinding.

The learning curve was steep and expensive. The first batch of stainless steel pumps leaked at the joints. The second batch had impellers that cavitated (created bubbles that damaged the pump). The third batch worked but cost twice what they could sell them for. Vivek's finance manager, an old-school accountant who'd been with the company since the trading days, would present monthly P&L statements with increasingly red numbers, muttering about "ambitious experiments."

But Vivek had studied Toyota's production system and was convinced that vertical integration, combined with continuous improvement, would eventually pay off. He instituted daily production meetings where workers could suggest improvements. A junior engineer suggested a slight change in impeller blade angle that improved efficiency by 3%. A foundry worker figured out how to reduce metal wastage by modifying the casting molds. Tiny improvements, but they added up.

The Karnal facility expansion during this period was organic and chaotic. New sheds sprouted up wherever there was space. The factory layout looked like it was designed by someone playing Tetris badly. Material flow was so convoluted that components sometimes traveled 500 meters within the factory to move 50 meters as the crow flies. But it worked, somehow.

By 2015, Oswal had achieved something remarkable: they could produce a pump from raw materials to finished product without any external dependency except basic commodities like steel and copper. The 41,076 square meter facility wasn't just big—it was comprehensive. Visitors (usually dealers being wooed or bankers being reassured) would be taken on tours that started at the foundry and ended at the testing station, a journey that showcased Oswal's transformation from trader to true manufacturer.

The financial impact was significant. While competitors faced margin pressure from suppliers, Oswal's gross margins expanded from 15% in 2011 to 28% by 2016. When copper prices spiked in 2017, Oswal had already stockpiled six months of inventory, bought when prices were low. When a truckers' strike paralyzed North India in 2018, Oswal kept producing while competitors' assembly lines stopped for want of components.

But vertical integration brought challenges too. Capital was tied up in machinery instead of market expansion. Management bandwidth was stretched managing foundry workers, winding technicians, fabrication specialists, and assembly line operators—each requiring different skills and management styles. Quality issues in one department could cascade through the entire production chain.

The export beginnings during this period were modest but strategic. They also export their products to 22 countries, primarily in Africa and the Middle East—markets where Indian pumps had a reputation for being more robust than Chinese alternatives but cheaper than European options. These weren't large orders—a container here, a container there—but they provided valuable foreign exchange and, more importantly, exposed Oswal to international quality standards.

Creating competitive moats through manufacturing excellence sounds like MBA-speak, but for Oswal, it was survival. Every competitor could buy pumps from China and sell them cheaper. But could they guarantee quality? Could they customize products for specific requirements? Could they deliver in 15 days when Chinese suppliers took 45? Oswal's integrated manufacturing meant they could say yes to all three.

The "Make Everything In-House" strategy reached its logical extreme by 2018. Oswal was making components that even Kirloskar outsourced. They'd developed proprietary alloys for impellers that lasted 20% longer. Their motor efficiency ratings exceeded BEE (Bureau of Energy Efficiency) standards. They could produce 50 different pump models without retooling, a flexibility that bigger players with specialized production lines couldn't match.

By 2018's end, Oswal wasn't just another pump manufacturer. They'd built a vertically integrated production machine that could pivot quickly, customize extensively, and compete on both cost and quality. They had no idea that within a year, the government would announce a scheme that would reward exactly these capabilities. But when PM-KUSUM arrived, Oswal was ready in a way their competitors simply weren't.

V. The PM-KUSUM Pivot: Betting the Company (2019–2021)

March 8, 2019. The Cabinet Committee on Economic Affairs, chaired by Prime Minister Modi, approves the Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM) scheme. The press release is dry, bureaucratic: PM KUSUM is a significant initiative by the Government of India and the Ministry of New and Renewable Energy (MNRE) with an outlay of ₹34,422 crores. Most industry players skim it, file it away, plan to review it later.

Vivek Gupta reads it three times. Then he calls an emergency meeting.

"Cancel all travel, all other meetings," he tells his secretary. "Get everyone in the conference room. And I mean everyone—production, finance, sales, even maintenance."

What Vivek saw that others missed wasn't just the scheme's size, but its structure. PM-KUSUM wasn't just subsidizing solar pumps; it was creating an entirely new business model. Component-C involved solarizing 15 lakh existing grid-connected agriculture pumps up to 7.5 HP capacity. By converting traditional pumps into solar-powered ones, farmers can significantly reduce their dependence on grid electricity. Component B focused on installing new standalone solar pumps. The government would provide 30% subsidy, states would add another 30%, and farmers would pay just 40%.

But here's the kicker: the scheme prioritized turnkey solutions. The government didn't want to buy pumps, panels, and controllers separately and figure out integration. They wanted vendors who could supply, install, commission, and maintain complete solar pumping systems. It was a fundamental shift from product sales to solution delivery.

The conference room debate that day was fierce. The old guard, led by the finance manager, was skeptical. "Solar pumps are 10 times the cost of regular pumps. Farmers won't pay even 40%. And government schemes? Remember what happened with the last irrigation scheme? Payments delayed by two years!"

The sales head was worried about different risks: "Our entire dealer network sells conventional pumps. They don't know solar. We'll have to rebuild from scratch."

The production head was blunt: "We make pumps. Good pumps. We don't know anything about solar panels or controllers or inverters."

But Vivek had done his homework. He pulled up a spreadsheet showing diesel consumption in Indian agriculture—₹48,000 crores annually. Then electricity subsidies—another ₹90,000 crores. "This isn't just a scheme," he said. "It's the government acknowledging that the current model is broken. They can't afford these subsidies anymore. Solar is the only way out. And whoever moves first will own this market."

The decision to pivot wasn't made that day, but the die was cast. Over the next three months, Vivek orchestrated one of the most dramatic strategic shifts in Indian manufacturing history. While competitors formed committees to study the scheme, Oswal started hiring solar engineers. While others debated participation, Oswal was already talking to solar panel manufacturers.

The collaboration with Tata Power Solar Systems Limited in 2019 was Oswal's masterstroke. Tata Power had the solar expertise but needed reliable pump partners for their turnkey bids. Oswal had pumps but needed solar credibility. It was a marriage of convenience that would soon become a partnership of dominance.

The early collaboration was awkward. Tata Power's engineers, used to grid-scale solar projects, would specify components with 25-year lifespans. Oswal's engineers, used to agricultural rough-and-tumble, would point out that nothing survived 25 years in an Indian farm. Meetings would stretch for hours debating waterproofing standards, cable specifications, mounting structures that could withstand both monsoons and monkey attacks.

But this friction produced innovation. The teams developed pump controllers that could handle voltage fluctuations that would fry normal electronics. They designed mounting structures that doubled as cattle sheds (farmers loved dual-use infrastructure). They created maintenance protocols simple enough that village technicians could handle basic repairs.

Under Vivek Gupta's leadership, the company's embrace of the renewable energy pivot went beyond just adding solar to their product mix. He restructured the entire organization around it. The R&D budget, traditionally 2% of revenue, was increased to 8% with most funds directed toward solar integration. He hired 50 engineers in six months—more than Oswal had hired in the previous five years combined.

The strategic bet was enormous and risky. Oswal committed to pre-purchasing solar components worth ₹50 crores—more than their entire previous year's profit. They signed MOUs with state nodal agencies before having the capability to deliver. Vivek personally guaranteed bank loans to fund working capital, putting family assets on the line.

2021 marked the full transformation when Oswal added complete turnkey solar pumping systems to their portfolio. This wasn't just adding installation services. It meant creating training programs for technicians, establishing service centers in remote areas, developing mobile apps for system monitoring, and building a supply chain that could deliver to villages without proper roads.

The competition's skepticism during this period was both understandable and fatal. A senior executive at Kirloskar reportedly said, "Let Oswal burn their fingers with government tenders. We'll focus on our core market." KSB India's strategy was to wait and watch, maybe participate selectively in large tenders. CRI Pumps decided to focus on exports, viewing PM-KUSUM as too risky.

Shakti Pumps was the only major competitor that took PM-KUSUM seriously, but they hedged their bets, allocating only 30% of capacity to solar pumps while maintaining focus on conventional products and exports. It was the prudent strategy. It was also the wrong one.

Oswal's all-in approach created unexpected advantages. When solar panel prices spiked in late 2020 due to polysilicon shortages, Oswal had already locked in prices through forward contracts. When the government modified technical specifications in early 2021, Oswal's engineers had been working with ministries and understood the changes before they were announced. When farmers complained about complex claim procedures, Oswal stationed their own staff at block offices to help with paperwork.

The turnkey advantage became clear during execution. A typical PM-KUSUM installation involved: site survey, soil testing, foundation work, structure assembly, panel mounting, pump installation, controller setup, grid connection (for Component C), testing, commissioning, training, and documentation. Competitors assembling consortiums for each project spent weeks coordinating. Oswal did everything with one team, one timeline, one accountability structure.

By December 2021, the results were showing. Oswal had won tenders in Haryana, Rajasthan, and Uttar Pradesh. They'd installed 5,000 solar pumping systems—more than they'd sold conventional pumps the entire previous year. Revenue had doubled. More importantly, they'd learned the business—the real business of selling to government, managing large projects, handling working capital cycles that stretched to 180 days.

But the real validation came from an unexpected source. John Deere, the American agricultural giant exploring Indian market entry, approached Oswal for a potential partnership. Not Kirloskar, not KSB, but Oswal. The due diligence team was impressed by one thing above all: Oswal's ability to execute complex projects in rural India. "You've figured out the last mile," the lead analyst said. "That's the hardest part."

The bet was paying off, but the biggest wins were still ahead. What Vivek didn't know was that the competition's skepticism had given Oswal an 18-month head start that would prove insurmountable. By the time others realized PM-KUSUM was real and substantial, Oswal had already built the capabilities, relationships, and track record that would make them nearly unbeatable.

VI. Execution at Scale: The PM-KUSUM Domination (2022–2024)

The war room at Oswal's Karnal headquarters, January 2022. Maps of India cover every wall, marked with colored pins—red for tenders lost, yellow for bids submitted, green for wins. The green pins are starting to dominate, clustering across Haryana, spreading into Rajasthan, creeping into Uttar Pradesh. Vivek Gupta stands before his team, exhausted but exhilarated: "This isn't business anymore. This is a mission."

By 31 December 2024, Oswal had delivered over 2.3 lakh solar pumps under the PM Kusum Scheme, directly or indirectly, accounting for a 38.04% share of all such installations in India (approx. 0.23 million out of 0.61 million). Think about that number. More than one in three solar pumps installed under India's flagship agricultural scheme came from a company that didn't make solar products just three years earlier.

The scale-up story from 2022 to 2024 reads like a startup fantasy, except this was heavy manufacturing, not software. In FY24, nearly 85% of its revenue came from solar water pumping systems sold under PM-KUSUM. Between FY22 and FY24, revenue more than doubled. Net profit grew from ₹17 crores to ₹97 crores. But these numbers don't capture the operational miracle happening on the ground.

Consider what executing a single PM-KUSUM tender actually involves. The Uttar Pradesh government issues a tender for 5,000 solar pumps across 15 districts. Winning requires the lowest price, but also proving you can deliver. Oswal's tender team, led by a former PWD engineer who knew every procurement officer's quirks, would work 20-hour days preparing bids. They'd factor in transportation costs to remote villages, account for local wage variations, estimate installation challenges during monsoon season, and still somehow underbid competitors who had lower manufacturing costs.

Winning was just the beginning. Each installation required: surveying farms accessible only by dirt tracks, negotiating with farmers suspicious of new technology, managing local contractors who'd never seen solar panels, dealing with village politics where the pradhan's cousin demanded the first installation, handling payment delays that stretched to six months, and maintaining systems in areas where the nearest electrician was 50 kilometers away.

As of December 31, 2024, the company has executed orders for 38,132 solar pumping systems directly under the PM Kusum Scheme. It has also supplied 145,578 pumps to players participating under the scheme, and 7,255 pumps as turnkey systems through participating players. This dual strategy—direct execution and supply to other contractors—was genius. When Oswal couldn't handle direct installation due to capacity constraints, they supplied pumps to competitors. When competitors couldn't procure pumps fast enough, Oswal stepped in with turnkey solutions.

Building the distribution army was a military operation masquerading as sales expansion. Oswal Pumps claims to have an extensive distribution network in India, comprising 925 distributors as of December 31, 2024, nearly double the 473 they had just two years ago. But these weren't traditional pump dealers. Oswal created a hybrid network—part educator, part installer, part service center.

Each new distributor underwent a week-long training program at Karnal. They learned not just product specifications but solar basics, government scheme details, subsidy application processes, and basic troubleshooting. Oswal created WhatsApp groups for each state where distributors shared installation photos, discussed problems, and celebrated wins. When a distributor in rural Rajasthan figured out how to prevent peacocks from damaging solar panels (a real problem), the solution was shared across the network within hours.

The turnkey advantage became Oswal's secret weapon. Their integration across the value chain gives them massive control over cost, quality, and delivery. They build it all: winding wires, cables, castings, solar cell cutting, and structures. Even solar modules (since Jan 8, 2024, via Oswal Solar Structure Pvt Ltd). That means fewer bottlenecks and more consistency.

When polysilicon prices spiked in 2022, vertically integrated Oswal could absorb costs better than competitors assembling systems from multiple vendors. When shipping containers became scarce, Oswal's complete in-house production meant fewer supply chain dependencies. When technical specifications changed mid-project (a common government habit), Oswal could modify designs within days, not weeks.

January 2024 marked another pivotal moment: Oswal Solar Structure Pvt Ltd commenced solar module manufacturing. This wasn't just adding another product—it was closing the loop. Oswal could now manufacture every single component of a solar pumping system. No Indian competitor had this level of integration. Even Chinese manufacturers, who dominated global solar supply chains, typically specialized in either pumps or panels, not both.

Managing working capital during this explosive growth was like juggling chainsaws while riding a unicycle. Selling to the government or through government channels is a slow game. Payments are delayed, receivables pile up and inventory builds as projects get staggered. That's perhaps why Oswal had 66% of its revenues stuck in trade receivables (up from 30% in 2024), about 40 days of inventory (goods sitting in storage) and a working capital cycle (the time it takes to convert inventory and receivables into cash) of 142 days.

The cash flow management bordered on financial acrobatics. Oswal would pay suppliers within 30 days to maintain relationships, but receive government payments after 180 days. The gap was funded through a complex web of working capital loans, invoice discounting, and occasionally, Vivek's personal guarantees. The finance team created a daily cash flow model that tracked every rupee, predicting payment delays with uncanny accuracy based on which bureaucrat was handling the file.

Government payment cycles became so predictable in their unpredictability that Oswal developed a proprietary scoring system for different state agencies. Haryana paid in 120 days, reliably. Rajasthan took 150 days but always paid in full. Uttar Pradesh was wild—sometimes 90 days, sometimes 200, depending on state elections and budget cycles. This intelligence guided bidding strategies—higher margins for slow-paying states, aggressive pricing for reliable ones.

The operational complexity was staggering. By 2024, Oswal was managing: installations across 15 states simultaneously, 200+ installation teams, 50+ government relationships, 900+ dealer relationships, inventory worth ₹200 crores, and receivables exceeding ₹400 crores. And yet, they maintained a 95% on-time delivery rate—unheard of in government contracting.

The human story behind these numbers is equally remarkable. Oswal's project managers, mostly engineers in their late 20s, would spend months in rural areas, living in small hotels, eating at highway dhabas, troubleshooting installations under scorching sun. One manager in Rajasthan reported installing pumps during a locust swarm. Another in UP had to negotiate with a local strongman who demanded "protection money" for installations. These weren't Silicon Valley problems—this was the real India, where business happened despite, not because of, infrastructure.

In FY 2024, a staggering 85.72% of revenue (INR 626.92 crore) came from PM Kusum-related sales. This climbed to 87.26% for the 9M FY25. The concentration was extreme, dangerous even. But Vivek's philosophy was simple: "When you find a gold mine, you don't dig a little bit everywhere. You dig deep."

The competition's response during this period ranged from denial to panic. Kirloskar finally launched a solar pump division in late 2023—four years after PM-KUSUM began. KSB India partnered with a solar EPC player but struggled with coordination. Shakti Pumps, the only serious competitor, was growing but at half Oswal's pace. Oswal's closest listed peer, Shakti Pumps, also rode the KUSUM wave. But it diversified early by building a solid export book, launching EV chargers and automation systems and selling to private irrigation clients.

By the end of 2024, Oswal wasn't just participating in PM-KUSUM—they were defining it. Government officials would consult Oswal engineers on technical specifications. Policy documents referenced Oswal's installation protocols. Competitors benchmarked against Oswal's delivery times. The small pump maker from Karnal had become the unofficial standard for solar pump deployment in India.

But success brought scrutiny. PM-KUSUM-based solar pumping systems still accounted for over 87% of Oswal's revenue in nine months ended FY25. And that's a problem because the scheme is nearing its original target as well as its deadline in March 2026. Unless a Phase II or new subsidy framework is announced, Oswal's revenue stream could start drying up in less than a year.

The question wasn't whether Oswal had won the PM-KUSUM race—they had, decisively. The question was what came next. And that question would soon be answered by capital markets in a way nobody expected.

VII. The IPO and Capital Markets Story (2025)

The boardroom of Oswal Pumps, May 2025. The investment bankers from IIFL have been talking for three hours, presenting slides filled with valuation multiples, peer comparisons, and market timing analyses. Vivek Gupta finally interrupts: "You're telling me public market investors will pay 30 times earnings for a company dependent on government schemes?" The lead banker doesn't miss a beat: "Sir, they'll pay 40 times for the India solar story. You're not selling pumps—you're selling the future."

The decision to go public wasn't made in that room, or even that year. It had been brewing since 2023, when Oswal's working capital requirements started stretching the limits of private financing. But the trigger was simpler: ambition. Vivek wanted to build India's first truly integrated renewable agriculture company, and that required capital at a scale no bank would provide.

Oswal Pumps IPO is a bookbuilding of ₹1,387.34 crores. The issue is a combination of fresh issue of 1.45 crore shares aggregating to ₹890.00 crores and offer for sale of 0.81 crore shares aggregating to ₹497.34 crores. The structure was telling—nearly two-thirds fresh capital for growth, one-third providing liquidity to promoters who'd funded the company's growth with personal guarantees for years.

The roadshow presentations in early June were theater of the highest order. Vivek, who'd never worn a suit regularly until six months ago, was now fluent in the language of TAM (Total Addressable Market), ROCE (Return on Capital Employed), and ESG metrics. In Mumbai, facing a room full of mutual fund managers, he was asked the obvious question: "What happens when PM-KUSUM ends?"

His answer was rehearsed but genuine: "When we started making pumps in 2003, nobody asked what happens when farmers stop needing water. PM-KUSUM isn't our business—irrigation is. The scheme is just the current chapter."

Oswal Pumps IPO raises ₹416.20 crore from anchor investors. Oswal Pumps IPO Anchor bid date is June 12, 2025. The anchor book was a who's who of Indian institutional investors—mutual funds that rarely agreed on anything were unanimous on Oswal. The message was clear: the smart money saw something beyond the obvious risks.

Oswal Pumps IPO bidding started from June 13, 2025 and ended on June 17, 2025. The allotment for Oswal Pumps IPO was finalized on Wednesday, June 18, 2025. The shares got listed on BSE, NSE on June 20, 2025.

The subscription period was a masterclass in momentum building. Day 1 saw cautious interest—0.14 times subscription, mostly from retail investors testing waters. But then something shifted. WhatsApp groups of retail investors started buzzing about the "next solar story." YouTube finance influencers discovered Oswal's market share numbers. By Day 3, the frenzy was real.

The Oswal Pumps IPO is subscribed 34.42 times by Jun 17, 2025 17:04. The retail portion was oversubscribed 3.6 times, but the real story was in the Qualified Institutional Buyers (QIB) category—oversubscribed 89 times. Fund managers who'd allocated cautiously on Day 1 were revising bids upward by Day 3.

Oswal Pumps IPO price band is set at ₹614 per share. The issue is priced at ₹614 per share. The pricing was aggressive—at the top of the indicated range. At ₹614 per share, Oswal was valued at roughly ₹8,900 crores post-money, or about 31 times FY24 earnings. For context, Kirloskar Brothers was trading at 18 times, Shakti Pumps at 22 times.

The valuation implied enormous faith in two things: PM-KUSUM's extension beyond 2026, and Oswal's ability to maintain margins despite competition. Neither was certain. Yet investors were buying the narrative, not just the numbers.

As of 18 June 2025, Oswal Pumps IPO GMP stood at ₹60. The expected listing price is ₹674, i.e., a 9.77% gain per share over the upper price band. The grey market premium told its own story. While not spectacular by 2025 IPO standards (some tech IPOs were listing at 100% premiums), it suggested steady institutional support rather than pure retail speculation.

Listing day, June 20, 2025, Mumbai. The opening bell at NSE is about to ring. Vivek Gupta stands with his family—father Padam Sain, mother, wife, his children—all wearing traditional clothes, ready for the ceremonial gong. Twenty-two years after starting as a pump trader, Oswal Pumps is about to become a public company.

The stock opens at ₹634, a modest 3.3% premium to the issue price. Not the explosive "pop" that makes headlines, but solid. By noon, it's trading at ₹674, up nearly 10%. The market is saying: we believe, cautiously.

Vivek Gupta, Amulya Gupta, Shivam Gupta, Ess Aar Corporate Services Private Limited, Shorya Trading Company Private Limited and Singh Engcon Private Limited are the company promoters. Post-IPO, promoter holding stood at 75.7%—they'd sold just enough to meet regulatory requirements while maintaining firm control. This wasn't an exit; it was a fund-raise.

The use of proceeds revealed the real strategy. Funding certain capital expenditures of the company – INR 89.37 crore · Investment in the wholly-owned subsidiary, Oswal Solar, in the form of debt or equity, for funding the setting up of new manufacturing units at Karnal, Haryana – INR 419.16 crore · Pre-payment/ re-payment, in part or full, of certain outstanding borrowings availed by the company – INR 235 crore

The largest chunk—₹419 crores—was for the solar module manufacturing expansion. Oswal wasn't just riding the PM-KUSUM wave; they were preparing for whatever came next. The debt repayment would clean up the balance sheet, reduce interest costs, and provide flexibility for future acquisitions.

Post-IPO performance in the first week was volatile. The stock touched ₹720 on Day 3 before settling back to ₹680 levels. Sell-side analysts were divided. Some initiated coverage with "Buy" ratings, citing the renewable energy mega-trend. Others were cautious, highlighting customer concentration risks.

A research note from a prominent brokerage captured the dilemma perfectly: "Oswal Pumps presents the classic growth versus risk trade-off. The company has demonstrated exceptional execution in capturing government-driven demand. However, with 87% revenue concentration in PM-KUSUM and the scheme ending in March 2026, investors are essentially betting on policy continuity—always a dangerous assumption in India."

The retail investor response was more emotional than analytical. On social media, Oswal became a symbol of "atmanirbhar Bharat"—self-reliant India. Small investors who'd missed the Adani Green and Tata Power rallies saw Oswal as their chance to participate in the renewable revolution.

One Reddit post went viral: "My grandfather was a farmer who paid ₹50,000 yearly for diesel. Oswal's solar pumps would have saved him ₹40,000 annually. I'm investing not for returns, but because this company is solving real problems." It had 10,000 upvotes.

Meanwhile, in Karnal, away from the market noise, the factory floor was buzzing with different energy. Workers who'd received ESOP allocations worth ₹10-50 lakhs were suddenly paper millionaires. The welding supervisor who'd been with the company since 2010 could now afford to send his daughter to engineering college in Delhi. The vertical integration strategy had created wealth at every level.

But Vivek wasn't celebrating. The day after listing, he called an all-hands meeting. "The easy money is behind us," he told the assembled managers. "Now we're playing with public money. Every quarter matters. Every number will be scrutinized. The market gave us capital, but it also gave us a ticking clock."

He was right. The real test wasn't the IPO—it was what came next. Could Oswal diversify beyond PM-KUSUM? Could they maintain margins as competition intensified? Could they manage the transition from entrepreneur-driven to professionally-managed? The capital markets had placed their bets. Now Oswal had to deliver.

VIII. Business Model Deep Dive

The Excel model on the analyst's screen at a Mumbai mutual fund is a thing of beauty—or horror, depending on your perspective. Row after row of assumptions about Oswal Pumps' business model, each cell linked to dozens of others, creating a web of dependencies that would make a spider jealous. The analyst mutters to himself: "If PM-KUSUM ends and they can't replace that revenue, this whole thing unravels like a cheap sweater."

He's not wrong. But he's not entirely right either.

Oswal Pumps claims to be the fastest-growing vertically integrated solar pump manufacturer in India in terms of revenue growth over the last three financial years, achieving a compound annual growth rate (CAGR) of 45.07 percent between FY22 and FY24. This isn't just growth—it's explosive expansion that would make even tech companies jealous. But unlike software companies scaling with zero marginal cost, Oswal's growth requires steel, copper, silicon, and sweat.

The three-pillar strategy sounds simple when Vivek explains it to investors: solar pumps for PM-KUSUM, grid-connected pumps for traditional markets, and turnkey systems for government contracts. In reality, it's three different businesses masquerading as one, each with distinct economics, working capital cycles, and competitive dynamics.

Pillar 1: Solar pumps under PM-KUSUM generate 85.72% of revenue but operate on government procurement rules. Gross margins are healthy at 35-40% because of vertical integration, but payment cycles stretch to 180 days. The government takes its time paying, but it always pays—eventually.

Pillar 2: Grid-connected pumps sold through dealers generate just 10% of revenue but have 45-day payment cycles and 25% gross margins. This is the bread-and-butter business that keeps cash flowing while waiting for government payments.

Pillar 3: Turnkey systems are the complexity multiplier. Margins can hit 45% because Oswal controls the entire value chain, but project execution risk is enormous. One delayed installation due to monsoons or farmer protests can turn a profitable quarter into a mediocre one.

The company posted an impressive EBITDA margin of 30.12% for the nine months ended 31 December 2024 — the second-highest among listed peers. This margin expansion story is where the magic—and the risk—lives. In FY22, EBITDA margins were 12%. By 9M FY25, they'd nearly tripled. How? Three words: scale, integration, and pricing power.

Scale came from volume. When you're producing 200,000 pumps versus 20,000, fixed costs get distributed across more units. The Karnal factory, built for tomorrow's demand rather than today's, started hitting utilization sweet spots. The same engineer who designed pumps could now optimize production for 10x volumes.

Integration meant Oswal captured margins at every step. When competitors bought castings at ₹100/kg, Oswal produced them at ₹60/kg. When others sourced motors at ₹5,000 per unit, Oswal made them for ₹3,000. These weren't massive differences per unit, but multiply by 200,000 units and you're talking real money.

Pricing power came from an unexpected source: execution reliability. In government contracts, the lowest bidder doesn't always win. Technical scores matter. Past performance matters. When Oswal could point to 38,000+ successful installations, they could price 5-7% higher than untested competitors and still win contracts.

But the government dependency trade-off is real and terrifying. In FY 2024, a staggering 85.72% of revenue (INR 626.92 crore) came from PM Kusum-related sales. This climbed to 87.26% for the 9M FY25. This isn't concentration risk—it's concentration certainty. If PM-KUSUM sneezes, Oswal catches pneumonia.

The working capital intensity reads like a horror story for cash flow purists. That's perhaps why Oswal had 66% of its revenues stuck in trade receivables (up from 30% in 2024), about 40 days of inventory (goods sitting in storage) and a working capital cycle (the time it takes to convert inventory and receivables into cash) of 142 days.

Consider what this means practically. Oswal ships pumps worth ₹100 crores in January. They pay suppliers ₹60 crores in February. They pay workers ₹10 crores monthly. But payment from the government arrives in July. For six months, that ₹100 crore sale is just a number on paper while real cash goes out the door.

This cash flow mismatch would kill most businesses. Oswal survives through a complex financial juggling act. Invoice discounting from banks (at 12% annual rates), supplier credit negotiations, strategic inventory management, and occasionally, promoter loans during crunch periods. The CFO jokes that he spends more time managing cash than managing accounts.

The competitive advantages are real but replicable. Oswal's moats aren't deep; they're wide. Vertical integration can be copied—it just takes capital and time. Government relationships can be built—it just takes patience and performance. Technical expertise can be hired—it just takes money.

But combining all three while maintaining execution speed? That's harder. When the Rajasthan government wants 5,000 pumps installed before elections, they don't call Kirloskar's corporate office. They call Vivek's mobile. When farmers in UP complain about pump failures, Oswal's engineers are on-site within 48 hours, not 48 days.

This responsiveness isn't systemized—it's cultural. The same family business DNA that investors worry about (key man risk, informal processes) is what enables rapid decision-making. A competitor's procurement committee would take three months to approve what Vivek approves in three minutes.

The unit economics tell the real story. A typical 5 HP solar pumping system sells for ₹3 lakhs. Oswal's costs break down as: Solar panels (outsourced): ₹1.2 lakhs, Pump and motor (in-house): ₹40,000, Controller and electronics: ₹20,000, Structure and installation: ₹30,000, and Sales and admin allocation: ₹20,000. This leaves roughly ₹70,000 gross profit per system, or 23% gross margin.

But when Oswal manufactures solar panels in-house (post-2024), that ₹1.2 lakh cost drops to ₹80,000. Suddenly, gross profit jumps to ₹1.1 lakhs, or 37% gross margin. This is the vertical integration payoff—not just cost reduction, but margin transformation.

The technology angle is often overlooked. Oswal isn't doing cutting-edge R&D, but they're masters of frugal innovation. The company claims to have made several engineering improvements, such as replacing stainless steel components with sheet metal alternatives and optimising valve thickness using investment casting, to reduce costs without compromising quality.

These sound like minor tweaks, but consider the impact. Replacing a stainless steel impeller with a specially-coated cast iron one saves ₹500 per pump. Across 200,000 pumps, that's ₹10 crores straight to the bottom line. An optimized valve design reduces material usage by 100 grams—negligible per unit, but 20 tonnes of steel saved annually.

Distribution economics deserve special attention. Oswal Pumps claims to have an extensive distribution network in India, comprising 925 distributors as of December 31, 2024. But these aren't traditional distributors buying inventory and taking risk. Under PM-KUSUM, distributors are more like installation partners. They don't hold inventory; they execute projects.

This asset-light distribution model is genius. Oswal doesn't need to fund dealer inventory or manage returns. Distributors earn 5-7% commission on installations, paid only after government payment is received. Risk is shared, capital is preserved, and alignment is perfect.

The margin expansion story from FY22 to FY24 reads like a textbook case study. EBITDA grew from ₹38.52 crores to ₹321.01 crores (9M FY25 annualized). But this isn't just volume growth. Operating leverage kicked in as fixed costs were spread over larger revenue. Negotiating power with suppliers improved as purchase volumes increased. Product mix shifted toward higher-margin turnkey solutions. Government contracts allowed for better pricing as Oswal's track record improved.

But hidden in these improving metrics are warning signs. Receivables are growing faster than revenue. Inventory turns are slowing as Oswal stocks up for anticipated demand. Related party transactions with the new solar subsidiary complicate the consolidated picture. The auditor's notes mention "emphasis of matter" regarding revenue recognition timing.

The bear case writes itself: PM-KUSUM dependency, working capital stress, competitive threats, and technology disruption risk. If the government shifts to direct cash transfers instead of pump subsidies, Oswal's model breaks. If Chinese manufacturers enter with 30% cheaper products, margins evaporate. If new solar technology makes current pumps obsolete, inventory becomes scrap.

The bull case is equally compelling: India needs 3 million solar pumps, only 0.7 million installed. State electricity boards save ₹90,000 crores annually by shifting to solar. Climate commitments require agricultural electrification. No competitor has Oswal's execution track record. The integrated manufacturing provides a sustainable cost advantage.

The truth, as always, lies somewhere in between. Oswal's business model is simultaneously brilliant and fragile, innovative and dependent, scalable and constrained. It's a high-wire act performed without a net, where success depends on government policy, execution perfection, and capital market patience.

IX. Power & Playbook: Lessons from the Oswal Story

A venture capitalist in Bangalore, reading Oswal's annual report, shakes his head in disbelief. "They're doing everything wrong according to Silicon Valley playbook," he tells his partner. "Customer concentration, government dependency, capital intensity, working capital nightmare. And yet they're printing money." His partner responds: "Maybe we need a different playbook for India."

She's onto something.

Power #1: Riding Policy Tailwinds - When Government Becomes Your Biggest Customer

The conventional wisdom says never depend on government contracts. They're slow, political, unreliable. Oswal flipped this on its head. When the government is spending ₹34,000 crores on a mission-mode project, you don't nibble at the edges—you go all in.

But riding policy tailwinds requires a special skill set. You need to understand not just the policy, but the politics behind it. PM-KUSUM wasn't just about solar pumps—it was about reducing agricultural subsidies, meeting climate commitments, and winning rural votes. Oswal aligned with all three narratives.

The key insight: Government schemes in India aren't just funding mechanisms—they're political movements. The scheme might end, but the political imperative (rural electrification, farmer welfare) never does. Oswal bet not on PM-KUSUM, but on the permanence of agricultural priority in Indian politics.

This creates a playbook: identify schemes aligned with long-term political priorities, move faster than bureaucracy expects, build execution credibility before competitors wake up, and become so embedded that you shape policy, not just respond to it.

When Ministry officials now draft solar pump specifications, they call Oswal engineers for input. That's not just market share—that's market shaping.

Power #2: Vertical Integration in Emerging Markets - Control Your Destiny

In Silicon Valley, vertical integration is dead. Asset-light, platform models rule. But in India's agricultural heartland, Oswal's full-stack approach is winning. Why?

Because in emerging markets, you can't rely on the supply chain. When Oswal needed quality castings, suppliers couldn't deliver consistently. When they needed timely delivery, logistics companies failed. When they needed installation expertise, contractors botched jobs. So they did everything themselves.

This isn't inefficiency—it's insurance. When Chinese solar panel supplies got disrupted in 2022, Oswal kept producing. When copper prices spiked, they'd already stockpiled. When competitors faced component shortages, Oswal's integrated facility hummed along.

The lesson extends beyond manufacturing. Oswal integrated forward into installation and service because rural infrastructure is unreliable. They integrated backward into raw materials because supplier quality was inconsistent. They integrated horizontally into solar modules because depending on others meant losing control.

Power #3: Family Businesses and Patient Capital in India

Vivek Gupta, Amulya Gupta, Shivam Gupta, Ess Aar Corporate Services Private Limited, Shorya Trading Company Private Limited and Singh Engcon Private Limited are the company promoters. The promoter holding of 75.7% post-IPO would terrify governance advocates. But this concentrated ownership enabled decisions no professional management would make.

What professional CEO would bet 80% of revenue on one government scheme? What independent board would approve building a foundry with borrowed money? What quarterly-earnings-focused management would accept 180-day payment cycles?

Family ownership provided patient capital when banks wouldn't lend, decisive leadership when committees would deliberate, and long-term thinking when markets demand quarterly results. Vivek could make five-year bets because he wasn't worried about next year's bonus.

But it goes deeper. In rural India, business is personal. When a farmer in Haryana buys an Oswal pump, they're not buying from a corporation—they're buying from "Gupta ji's company." That social capital, built over generations, can't be replicated by private equity or professional management.

The Concentration Risk Paradox: All Eggs in One Government Basket

The company generates over 85% of revenue from government-backed PM Kusum scheme orders — a clear concentration risk. Every MBA program would call this insane. Every risk management framework would flag this as fatal. Yet it might be Oswal's smartest move.

Consider the alternative. Suppose Oswal had "diversified" - 20% exports, 20% retail, 20% industrial, 20% agriculture, 20% government. They'd be competing against specialists in each segment, with subscale positions everywhere. Instead of 38% market share in one segment, they'd have 3-4% in five segments.

Concentration created capabilities. Because Oswal only focused on PM-KUSUM, they became exceptional at government contracting, rural installations, solar-pump integration, and agricultural customer service. These capabilities are transferable—the next government scheme, the next agricultural technology, the next rural infrastructure push.

Speed vs. Quality: The Execution Trade-offs

Oswal's rapid scaling came with compromises. Early installations had 10% failure rates. Customer complaints spiked in 2022. Quality control struggled to keep pace with quantity demands.

But here's the counterintuitive insight: in emerging markets, speed often beats quality. Not because quality doesn't matter, but because being first creates forgiveness for imperfection. Farmers receiving their first solar pump were more tolerant of teething issues than they would be of the fifth competitor offering marginally better quality.

Oswal's approach: Launch at 80% quality, fix problems in real-time, use customer feedback for rapid iteration, and build quality once scale is achieved. By the time competitors achieved 95% quality, Oswal had 50% market share and improving quality.

Building Distribution in Rural India - The Last Mile Challenge

The company claims to have introduced the 'Oswal Shoppe' initiative in 2024 to enhance retail visibility and deepen engagement with its distributors and retailers. Currently, it has 248 Oswal Shoppes, primarily located in Haryana, Punjab, Uttar Pradesh, and Rajasthan.

The Oswal Shoppe model reveals deep understanding of rural retail dynamics. These aren't stores—they're community centers where farmers gather, share experiences, and make collective decisions. The shop owner isn't just a retailer—he's an influencer, advisor, and financier.

Traditional companies try to bypass these intermediaries with direct-to-farmer models. Oswal embraced them, making distributors partners in the PM-KUSUM mission. Training programs turned them into solar evangelists. Commission structures aligned their interests. The result: a distribution army that competitors can't easily poach.

The Unsexy Advantage

Pumps are boring. Solar pumps are slightly less boring. This lack of glamour kept venture capital away, reduced competitive intensity, and allowed steady execution without hype. While everyone chased the next unicorn, Oswal built a real business with real profits.

The lesson: In India, unsexy plus essential equals opportunity. Water, power, sanitation, agriculture—these sectors lack Silicon Valley allure but have massive social and economic impact. Companies solving boring problems for millions often outperform those solving interesting problems for thousands.

Information Asymmetry as Competitive Advantage

Oswal's deep rural presence created information advantages. They knew which districts would get scheme funding before it was announced (local politicians talk). They understood actual pump demand versus reported statistics (dealers know reality). They could predict payment delays based on state election cycles (pattern recognition from experience).

This ground-level intelligence enabled better inventory planning, smarter bidding strategies, and optimal capital allocation. While competitors relied on government reports and consultant studies, Oswal had 925 distributors providing real-time market feedback.

The Platform Hidden in the Product

What looks like a pump company might actually be an agricultural services platform in disguise. Today, Oswal installs pumps. Tomorrow, they could install cold storage, solar dryers, or agricultural IoT devices. The hard part—reaching farmers, building trust, creating service infrastructure—is done.

This optionality is valuable but unpriced. Markets value Oswal as a pump manufacturer with government concentration risk. But they might be missing the platform opportunity: data on 200,000+ farmers, service infrastructure across rural India, and relationships with agricultural communities.

Capital Allocation Genius or Madness?

Investing ₹419 crores in solar manufacturing when PM-KUSUM ends in 2026 seems crazy. Or brilliant. If solar becomes mandatory for all agricultural infrastructure, Oswal is positioned perfectly. If it doesn't, they have very expensive factory equipment.

This binary bet is characteristic of family businesses—they make concentrated bets that diversified companies wouldn't. When it works, it looks like genius. When it fails, it looks like hubris. The jury's still out on Oswal.

X. Bear vs. Bull Case & Future Scenarios

Two fund managers at a Mumbai coffee shop, September 2025, arguing over Oswal Pumps. The stock has been volatile, swinging 20% monthly based on PM-KUSUM extension rumors.

"You're crazy to hold this," says the bear. "It's a house of cards waiting for a policy breeze."

"You're blind to miss this," counters the bull. "It's the AWS of rural infrastructure, just getting started."

Both might be right.

The Bull Case: Massive Runway Ahead

Start with the numbers that make bulls salivate. India has 140 million farmers. Approximately 30 million use irrigation pumps. Of these, 10 million still use diesel, burning through ₹48,000 crores annually. Another 20 million use subsidized electricity, costing state governments ₹90,000 crores yearly. India's solar pump market has strong growth potential, with 0.122 crores of pumps sanctioned under the PM Kusum Scheme, but only 0.077 crore (63%) installed as of March 2025. States like Maharashtra, Haryana, Rajasthan, Uttar Pradesh, and Punjab make up 84% of sanctioned pumps. With 14.4 crore farmers in India—11.4 crore lacking pumps and 30% still using diesel—there is a large untapped demand for solar irrigation solutions.

The math is kindergarten-simple: 3 million pumps needed, 0.7 million installed, 2.3 million to go. At ₹3 lakhs per installation, that's a ₹7 lakh crore opportunity. Even capturing 30% market share means ₹2 lakh crores in revenue over the next decade.

But the real bull case goes beyond PM-KUSUM. India's agricultural transformation is inevitable. Climate commitments require net-zero emissions by 2070. Agricultural diesel consumption must drop to zero. Grid electricity is unviable for remote farms. Solar is the only solution that works economically, environmentally, and politically.

State governments are waking up to this reality. Maharashtra announced its own solar pump scheme with ₹10,000 crore allocation. Karnataka is planning something similar. UP is exploring solar-powered cold storage. These state schemes could be larger than PM-KUSUM.

The technology trajectory favors Oswal. Solar panel costs continue dropping 5-7% annually. Battery storage is becoming viable, enabling 24-hour pumping. IoT integration allows remote monitoring and predictive maintenance. Oswal's installed base of 200,000+ pumps becomes a platform for selling these upgrades.

International expansion is nascent but promising. The company claims to have supplied products to 22 countries, including Australia, Egypt, Iraq, Italy, Lebanon, Libya, Nepal, Saudi Arabia, the United Arab Emirates (UAE), and Yemen. Africa alone needs 50 million solar pumps. Middle East countries are investing heavily in agricultural self-sufficiency. Oswal's proven low-cost manufacturing could dominate these markets.

First-mover advantages compound over time. Oswal's data on pump performance across different soil types, water tables, and crop patterns is invaluable. Their trained technician network can't be replicated quickly. Farmer trust, built through successful installations, creates switching costs competitors can't overcome.

Manufacturing capabilities extend beyond pumps. The same facilities producing pumps can make industrial motors, water treatment equipment, and renewable energy components. The solar module facility positions Oswal for rooftop solar, agricultural solar farms, and energy storage systems.

The financials support aggressive growth. With ₹890 crores in fresh capital and debt-free status post-IPO, Oswal can fund expansion without dilution. Operating leverage means incremental revenue drops straight to bottom line. ROCE of 35%+ means growth creates substantial value.

Policy support seems assured. No political party can afford to antagonize farmers. Renewable energy is a global priority with diplomatic benefits. Rural employment from solar installations wins votes. The policy tailwind isn't ending—it's accelerating.

The Bear Case: Concentrated Risks Everywhere

But bears have equally compelling arguments. Start with the obvious: PM-KUSUM-based solar pumping systems still accounted for over 87% of Oswal's revenue in nine months ended FY25. And that's a problem because the scheme is nearing its original target as well as its deadline in March 2026. Unless a Phase II or new subsidy framework is announced, Oswal's revenue stream could start drying up in less than a year.

Government dependency creates multiple vulnerabilities. Policy reversal after elections could halt everything. Budget constraints might reduce allocations. Implementation delays are routine—PM-KUSUM itself is two years behind schedule. Any delays in PM Kusum execution could affect cash flows significantly.

Competition is heating up. Kirloskar finally launched a dedicated solar division. Tata Power is backward integrating into pump manufacturing. Chinese manufacturers are eyeing India post-PLI scheme benefits. Startups with asset-light models are entering with innovative financing. The 38% market share is unsustainable as the market matures.

Working capital stress could trigger a crisis. Company has high debtors of 160 days. Working capital days have increased from 41.7 days to 86.4 days. If government payments delay beyond 200 days, Oswal needs additional financing. Banks are already overleveraged to the company. Any credit crunch could halt operations.

Technology disruption is a real threat. Drip irrigation reduces pump requirements by 60%. Precision agriculture with moisture sensors optimizes water usage. Drought-resistant seeds decrease irrigation dependency. If irrigation demand structurally declines, Oswal's TAM shrinks dramatically.

Quality issues could destroy reputation overnight. Rural installations face harsh conditions—extreme heat, dust, voltage fluctuations, and minimal maintenance. A batch failure affecting thousands of farmers would create PR nightmares and legal liabilities. One viral video of pump failures could undo years of brand building.

The economics might not sustain without subsidies. At ₹3 lakhs, solar pumps have 7-10 year payback periods for farmers. Without 60% subsidy, adoption would plummet. If government shifts to direct benefit transfers or input subsidies, the entire business model breaks.

Execution complexity is underappreciated. Managing 900+ distributors, 200+ installation teams, and thousands of government relationships requires operational excellence Oswal hasn't demonstrated at scale. One major project failure could trigger penalty clauses worth hundreds of crores.

Related-party transactions with the solar subsidiary raise governance concerns. Transfer pricing between entities could mask true profitability. The family-run structure lacks professional management depth. Key man risk with Vivek Gupta is extreme—the company is essentially uninvestable if something happens to him.

Valuation assumes perfection. At 31x P/E, any disappointment triggers correction. Growth deceleration, margin compression, or working capital deterioration could halve the stock price. The IPO pricing left little room for error.

Future Scenario Planning

Scenario 1: The Golden Path (30% probability) PM-KUSUM Phase II announced with ₹50,000 crore allocation. State schemes add another ₹30,000 crores. Oswal maintains 35% market share while diversifying into solar rooftops and energy storage. Revenue reaches ₹5,000 crores by FY28 with 25% EBITDA margins. Stock triples to ₹2,000.

Scenario 2: The Muddle Through (40% probability) PM-KUSUM extended but with reduced allocation. Competition intensifies, reducing market share to 20%. Margins compress to 15% EBITDA. Growth slows to 15% CAGR. Stock trades sideways between ₹500-800, disappointing growth investors but generating decent cash flows.

Scenario 3: The Pivot (20% probability) PM-KUSUM ends without replacement. Oswal aggressively pivots to exports and industrial pumps. Revenue drops 40% initially but recovers through new markets. Transformation takes 3 years with significant execution risk. Stock crashes to ₹300 before recovering to ₹600.

Scenario 4: The Disaster (10% probability) Government shifts to cash transfers, eliminating pump subsidies. Chinese competition destroys margins. Working capital crisis forces distressed asset sales. Oswal becomes a case study in concentration risk. Stock falls below ₹200.

The probability-weighted expected value suggests fair value around ₹750-800, implying limited upside from current levels. But the distribution is highly skewed—massive upside if bulls are right, substantial downside if bears prevail.

So What for Investors?

For growth investors: This is a derivative play on India's agricultural transformation. If you believe in the renewable energy mega-trend and government's commitment to farmers, Oswal offers leveraged exposure. But size positions accordingly—this isn't a sleep-well-at-night holding.

For value investors: Wait for better entry points. The company is priced for perfection despite obvious risks. A 30-40% correction from temporary concerns could create compelling value. The business quality is real; the price isn't right yet.

For traders: Volatility is your friend. Policy announcements, quarterly results, and subsidy updates create 10-15% swings. Playing these moves requires staying plugged into ground-level information and government corridors.

For long-term fundamental investors: The jury's out. Oswal could be India's next infrastructure champion or a cautionary tale about government dependency. The answer depends on political economy factors beyond company control. This is as much a political bet as a business investment.

XI. Epilogue: What Happens Next?

December 2025. Vivek Gupta stands in the same Karnal conference room where, six years ago, he decided to bet everything on PM-KUSUM. The walls are now covered with awards, newspaper clippings, and photos with ministers. But his expression is troubled. The scheme ends in three months, and Delhi is silent about extensions.

"Papa was right about one thing," he tells his management team. "In business, you're only as good as your next order."

The next chapter of Oswal's story is being written in real-time, and it could go multiple directions.

International Expansion Possibilities

Oswal's international strategy is taking shape, but it's different from the typical Indian corporate playbook. Instead of acquisitions or greenfield factories, they're exploring technology transfer partnerships. The model: provide design and manufacturing expertise to local partners in Africa and Middle East, earning royalties and technical fees without capital investment.

A pilot project in Kenya is underway. Oswal is training local technicians to assemble pumps from knocked-down kits, providing quality certification and brand licensing. If successful, this asset-light international model could generate 20% of revenues by 2030 without working capital strain.

But international markets aren't India. African governments are less stable, payment risks are higher, and currency fluctuations add complexity. The same government dependency that worked in India could be fatal in Nigeria or Ethiopia.

Diversification Beyond Government Schemes

The post-PM-KUSUM strategy is emerging. Oswal is exploring three adjacencies:

Agricultural cold storage powered by solar. India loses ₹90,000 crores annually to post-harvest waste. Solar-powered cold storage at farm gates could be transformational. Oswal's installation infrastructure and farmer relationships position them well. But this requires new technology competencies and higher capital investment.