Orient Electric: The Master of the Indian Ceiling

I. Introduction & The "Quiet" Revolution

Walk into the showroom of any reasonably sized electrical retailer in Lucknow, Coimbatore, or Pune in the summer of 2026 and ask for "the most expensive ceiling fan you have." Nine times out of ten, the salesman points to a slim white blade with a soft matte finish, hanging at eye-level beneath a halogen spotlight. He flips a switch. The blade rotates. And then, almost theatrically, he says: "Sir, sun lijiye." Listen.

You strain. You hear the showroom AC. You hear the traffic outside. You don't hear the fan.

The salesman smiles, the way salesmen smile when a magic trick is going well. "Aeroquiet," he says. "Orient ka. Bilkul silent." Three times the price of a regular fan, sometimes four. And families across urban India have been buying them anyway, because for the first time in a century, an Indian ceiling fan has stopped sounding like an Indian ceiling fan.

This is a strange thing to build a business around, when you think about it. Indians have lived under whirring ceiling fans for three generations. The hum, the slight click, the gentle wobble — these are the soundtrack of an Indian summer afternoon.

Telling a market that has tolerated noisy fans since the 1950s that they should now pay a premium for quiet is roughly equivalent to telling Americans they should pay three times more for a refrigerator that doesn't hum. And yet, ओरिएंट इलेक्ट्रिक लिमिटेड Orient Electric Limited did exactly that — and made it stick.

Orient Electric is not a household name in the Anglosphere business press. It does not announce blockbuster acquisitions, it does not run viral ad campaigns, and its founders did not appear on the cover of Forbes Asia.

It is instead a member of the storied सी.के. बिड़ला ग्रुप CK Birla Group — one of the three principal branches of the Birla industrial dynasty, distinct from the more famous Aditya Birla Group and the Kumar Mangalam Birla empire.[^1] For most of its six-decade life, Orient was a quiet, profitable, vaguely industrial fan business — the kind of company that appeared as a footnote in equity reports, dismissed with phrases like "legacy player" or "regional brand."

Then, in May 2018, the company stopped being a footnote. It demerged from its parent ओरिएंट पेपर एंड इंडस्ट्रीज लिमिटेड Orient Paper & Industries Limited, listed on the BSE and NSE, and proceeded to do something that legacy industrial conglomerates in India almost never do: it actually behaved like a Fast-Moving Electrical Goods (FMEG) company.1

The thesis of this episode is simple but loaded. Can a division born inside a paper mill — a business with the metabolism of a cyclical commodity producer — successfully metamorphose into a modern, brand-led, design-forward consumer durables company, in a market where the gravitational pull of price competition is brutal and where the incumbents (हैवेल्स Havells India, क्रॉम्पटन Crompton Greaves Consumer Electricals, and पॉलीकैब Polycab India) have spent the last two decades sharpening their own swords?

This is the story of how Orient went from being someone else's side hustle to a standalone ₹2,700+ crore listed entity on the NSE.2 It is also the story of the Indian consumer durables industry itself — a market reshaped by demerger arithmetic, by LED disruption, by the Bureau of Energy Efficiency, and by the simple fact that 1.4 billion people get very, very hot in May.

The roadmap from here runs in roughly chronological order. We will begin with the long, slow industrial inheritance — the paper mill, the licence-raj Faridabad fan plant, the four decades of perfectly adequate, perfectly unexciting manufacturing. We will move into the mid-2000s commodity crisis that nearly relegated Orient to "regional player" status, then into the rebrand and the demerger that gave the business its second life. From there we will dwell on the Aero series — the campaign that crystallised Orient's premium intent — before turning to the management transitions of the post-listing decade, the segment-level architecture that most investors miss, and finally the bull/bear analysis that frames the next leg.

One last framing note before we begin. This is not a story about a moonshot or a unicorn. It is a story about an old company learning new tricks — and learning them in a country where execution at the dealer level matters infinitely more than execution in a pitch deck. The lessons are quieter than a SaaS rocket-ship, but for long-term Indian-equity investors, they are arguably more durable.

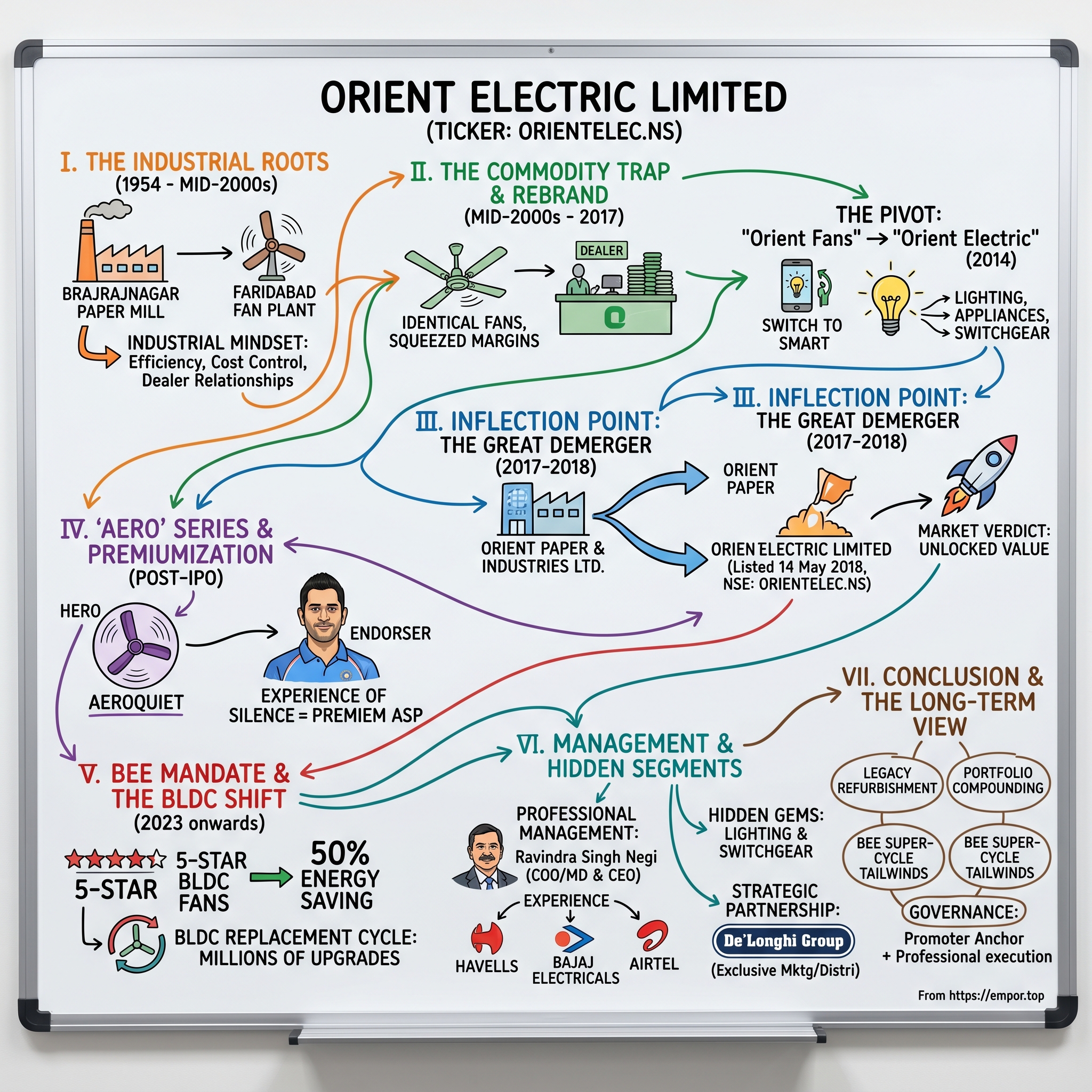

II. The CK Birla Heritage & Industrial Roots

To understand Orient Electric, you have to first understand the family that built it — and why, in 1954, a paper mill in Brajrajnagar, Odisha, decided that what India really needed was a ceiling fan.

The Birla name in Indian business is almost mythological. The patriarch, Ghanshyam Das Birla — closely associated with Mahatma Gandhi and a financier of the independence movement — established what became one of post-colonial India's three or four most important business houses.

By the 1960s, the Birla empire had split, as all great Indian business families eventually do, into branches. The branch that runs Orient Electric descends from B.M. Birla and, ultimately, his grandson Chandra Kant Birla, after whom the CK Birla Group takes its modern name.[^1]

This is the part that Western audiences usually miss: the CK Birla Group is the "other" Birla group. It is not the Aditya Birla Group of cement, aluminum, and Vodafone Idea fame.

It is a quieter, more diversified, more deliberately mid-sized industrial federation — with interests in auto components (Neosym, GMMCO), industrial bearings (NEI), building products (HIL Limited), IT services (Birlasoft), specialty paper (Orient Paper), and consumer electricals (Orient Electric).

The group describes itself as a roughly USD 3 billion enterprise, run with a federated philosophy: holding companies set capital allocation policy, but operating companies are largely autonomous.[^1]

The story starts not with electricals, but with cellulose. Orient Paper & Industries Limited was incorporated in 1936 in Calcutta and went on to become one of independent India's most important paper manufacturers.

For most of the 1940s and 1950s, this was a textbook example of late-colonial industrial strategy: build a paper mill where the forests and the rivers cooperate, sell into a captive domestic market, ride the post-Independence import-substitution wave.

So why, in 1954, did a paper company start making ceiling fans?

The answer is part economics, part politics, part raw opportunism. Newly independent India was a supply-constrained economy. Anything you could manufacture domestically, you could sell. The Industrial Policy Resolution of 1956 explicitly encouraged Indian capital to spread into engineering goods. Foreign competition was effectively walled off by import tariffs.

And ceiling fans, in a tropical country of 360 million people just starting to electrify, were not a niche product — they were closer to a basic utility. Orient Paper's promoters saw a strip of adjacent industrial logic: if you can run a paper mill, you can run a metal stamping line; if you can negotiate with copper suppliers for your mill's electrical systems, you can negotiate for fan motor coils.3

So the company started a fan division. It built a plant in Faridabad.

And for the next four decades, Orient Fans did what every Indian industrial brand of that era did: it produced solid, functional, perfectly reliable ceiling fans, sold through a sprawling network of dealers, on the basis of relationships and credit terms rather than brand pull.

This is the inheritance you have to keep in mind as the rest of the story unfolds. Orient was, for most of its life, the embodiment of what investors in India sometimes call the "industrial mindset" — a culture that respects efficiency, cost control, and dealer relationships, but is constitutionally suspicious of design budgets, brand ambassadors, and television commercials with shirtless cricketers. The company that listed on the NSE in 2018 had to consciously and deliberately overthrow that DNA.

That overthrow began roughly a decade before the IPO bell rang.

It is worth pausing on what "industrial mindset" actually meant inside Orient in this era. The company's senior executives, for the most part, had spent their entire careers inside Orient Paper or adjacent industrial cousins inside the group. Capital decisions were made by reference to plant utilization, raw material cost, and the kind of conservative debt-coverage ratios that any cyclical industrial business demands. The notion of spending five to seven percent of revenue on advertising — standard practice in branded consumer goods — would have looked like a fiscal indulgence. The notion of investing materially in industrial design — hiring product designers, building user-research capability — would have looked like a Western affectation. Indian industrial culture in this generation prized engineers, accountants, and dealer-managers; it had room for marketers, but only barely.

To understand what changed, it helps to remember that India itself changed. Through the 1990s and 2000s, household electricity penetration moved from roughly 50% to over 90%. Consumer credit, which barely existed in 1991, became routine by 2010. Television advertising reached the smallest towns through the cable revolution. The aspirational ceiling in the Indian middle class rose, slowly at first and then suddenly. By the early 2010s, the consumer who had bought a Crompton fan in 2002 because it was the only fan within reach was now, ten years later, willing to pay 40% more for a fan that looked nicer in the drawing room. Orient's leadership realized — somewhat later than Havells, somewhat earlier than several regional players — that the entire metabolic basis of the business was shifting beneath its feet.

III. Inflection Point 1: Breaking the Commodity Trap

By the mid-2000s, the Indian ceiling fan market had a problem. Or rather, the Indian ceiling fan market did not have a problem — but the legacy players inside it absolutely did.

Picture the dealer counter at an electrical wholesaler in Karol Bagh, Delhi, circa 2007. A contractor walks in, slaps down his BOM (bill of materials) for a forty-flat housing project, and says: "Pankha chahiye, sasta dena." Give me cheap fans. The dealer points to a stack of cardboard boxes — Crompton, Khaitan, Bajaj, Orient, Usha — and shrugs. They are nearly identical. The motors are similar. The blade profiles are similar. The aluminum housings are stamped at roughly the same Faridabad and Hyderabad plants. The contractor will pick whichever the dealer pushes hardest, and the dealer will push whichever vendor gave him the best margin or the longest credit period that quarter.

This is the commodity trap, in textbook form. Once your product becomes interchangeable in the buyer's mind, your only competitive lever is price — and price competition in a fragmented Indian market with hundreds of regional players is a guaranteed margin-compression machine.

Orient, in this period, was particularly vulnerable. Two competitors — Havells and the consumer electrical arm of Crompton Greaves — had quietly figured out something Orient had not: Indian consumers were rich enough now to want brands, not just products.

Havells, under the famously combative Anil Rai Gupta, had spent the late 2000s and early 2010s reinventing itself from a switchgear company into a full-spectrum FMEG brand, complete with high-profile cricket sponsorships and TV ads that ran during the IPL. Crompton, after being demerged from its parent in 2016, set off on a similar branding push.[^5]

Orient was being squeezed in the middle: not cheap enough to compete with regional unorganized players, not premium enough to win the brand-conscious urban shopper. It risked becoming what consultants politely call a "forgotten brand."

The pivot began under the leadership of Deepak Khetrapal, who had taken over as Managing Director and CEO of the consumer electric business in the early 2010s. Khetrapal, a former Tata Motors executive, brought something that the legacy Orient culture had been missing: a willingness to spend on the brand before the brand fully deserved the spend.

In 2014, the company formally rebranded from "Orient Fans" to "Orient Electric" — a small change of name with a large change of intent. The new identity signaled that fans were no longer the destination; they were the doorway.[^5]

Behind the new logo, Orient quietly broadened its product range into adjacent FMEG categories. Lighting was the obvious one. Home appliances — coolers, water heaters, small kitchen — were the next. Switchgear was the most ambitious, because it pulled Orient into a category where Havells was already entrenched and where the buying journey runs through electrical contractors rather than retail shoppers.

The technical shift inside the lighting business deserves its own footnote in Indian industrial history. Between roughly 2013 and 2018, Indian lighting transitioned from compact fluorescent lamps (CFLs) to एलईडी LED at a speed that astonished even the manufacturers. The government's UJALA program — which distributed hundreds of millions of subsidized LED bulbs through state electricity boards — collapsed the price of an LED bulb from over ₹300 to under ₹70 in roughly four years. Companies that had invested in CFL capacity were left with stranded assets. Companies that pivoted early to LED captured most of the upside.[^6]

Orient navigated this transition reasonably well, but not perfectly. The lighting business expanded, but it never quite caught Havells or the more focused players in the professional lighting niche. What the LED shift did do, however, was give the Orient management team a taste of what disruption inside a commodity category felt like — and it conditioned them to be more willing to lean into the next disruption, which was already visible on the horizon: the brushless DC (BLDC) ceiling fan.

The takeaway from this period is the one investors should remember when assessing any legacy Indian consumer brand. Escaping the commodity trap is not a marketing exercise; it is a multi-year capital and culture commitment. Orient began that commitment under Khetrapal, but it would take a corporate-structure earthquake to truly unlock it.

That earthquake arrived in 2017.

A quick word here on the LED disruption, because it is one of the great underappreciated industry stories of the 2010s. The compact fluorescent lamp had been the workhorse of Indian residential lighting through the 2000s, sold by every major electrical company in roughly the same form factor with roughly the same lifespan. When LEDs began to scale globally, Indian manufacturers initially saw them as a premium niche — too expensive, too unfamiliar. What changed the trajectory was a single piece of policy: the Energy Efficiency Services Limited (EESL) program, branded UJALA, which used aggregated demand and reverse auctions to push the per-unit cost of an LED bulb down by nearly 90% in four years. The price collapse forced every Indian lighting manufacturer into a brutal capacity decision. CFL plants were stranded. Some companies — Wipro Lighting, Bajaj Lighting, the legacy brands — never quite recovered the share they lost during the transition. Orient, which had only a moderate CFL footprint to defend, navigated the LED shift without catastrophic write-downs, but also without the kind of category leadership a Signify or a Surya enjoyed in adjacent niches.[^6] The lesson learned inside Orient was that disruption rewards the willingness to write off your own inventory before someone else writes it off for you — a lesson that would matter again when BLDC arrived in fans.

IV. Inflection Point 2: The Great Demerger (2017–2018)

The most under-discussed reason that Indian conglomerates underperform global benchmarks is something with a deeply boring name: the "conglomerate discount." When a single listed entity contains both a cyclical, capital-heavy commodity business and an asset-light, high-return consumer business, public markets struggle to price the package. Analysts cover one or the other but rarely both. Index inclusion is awkward. Capital allocation gets muddled, because the cash flow from the consumer business inevitably ends up funding the next capex cycle of the commodity business. The whole is worth meaningfully less than the sum of its parts.

By 2016, the CK Birla Group had been staring at this discount on its balance sheet for years. Orient Paper was a cyclical, energy-intensive, capital-hungry paper producer whose returns oscillated with pulp prices and rural demand. Orient's consumer electric business, sitting inside the same legal entity, was capital-light, brand-driven, and growing in the high teens. Holding them together was depressing the multiple on both.

In early 2017, the group's board took the decision that defined the modern company: a clean Scheme of Arrangement to demerge the consumer electric business out of Orient Paper & Industries Limited into a separate listed entity, Orient Electric Limited. The appointed date — the legal "effective" date of the transfer — was 1 March 2017, with the National Company Law Tribunal granting its sanction on 8 November 2017.4

The mechanics were elegant. Shareholders of Orient Paper received one equity share of Orient Electric (face value ₹1) for every one equity share of Orient Paper (face value ₹1) held on the record date of 12 January 2018.

No cash changed hands. No new dilution happened. Existing investors simply woke up one morning holding two separate stocks where they had previously held one.4

Then came the listing. On 14 May 2018, Orient Electric Limited began trading on both the BSE (under the code 541301) and the NSE (under the symbol ORIENTELEC). The market's verdict was immediate and unambiguous: the stock hit the upper circuit at ₹142 on its debut session, a roughly 27% premium to the discovered price.4 Within months, the listed market cap of Orient Electric had comfortably exceeded what the entire combined entity of Orient Paper had been worth before the split.

This is the part of the demerger story that matters most for long-term fundamental investors, and it deserves a moment of slow thinking. The demerger did not create new revenue. It did not change the underlying business operations. The same factories made the same fans, sold to the same dealers, on the same trade terms.

What the demerger changed was the cost of capital. Once Orient Electric became a pure-play FMEG company, it could be benchmarked properly against हैवेल्स Havells, क्रॉम्पटन Crompton, and Bajaj Electricals. It could be added to consumer-durable thematic indices. It could attract foreign institutional investors who screen on segment purity. Its currency for stock-based incentive plans suddenly became real.

The strategic logic here is worth generalizing. Demergers in India have an extraordinarily consistent track record when the demerged entity is the smaller, growth-ier, asset-light arm of an industrial parent. Crompton Greaves's split into its consumer business in 2016, Tata Motors' eventual hiving off of its passenger vehicle and EV businesses, the Bajaj group's repeated splits — the pattern is so clean that it has become a known strategy in Indian capital markets: when in doubt, demerge the consumer business and let it breathe.

For Orient, the demerger also forced a change in management posture. As part of Orient Paper, the consumer electric business had been measured on absolute profit contribution. As a standalone listed entity, it was suddenly measured on revenue growth, EBITDA margin, return on capital employed, and — crucially — segment commentary in every quarterly earnings call. Every product decision now had to survive analyst scrutiny. Capital allocation became more disciplined, because the parent could no longer paper over (pun fully intended) any inefficiency by netting it against the pulp business.

This new exposure to the harsh white light of public markets is what set the stage for what came next: a deliberate, advertising-led premiumization campaign that would prove to be Orient's defining commercial moment of the post-IPO era.

There is one further nuance to the demerger worth pulling out, because it is the kind of structural detail that long-term investors should internalize. The 1:1 share ratio meant that Orient Paper shareholders did not receive a windfall, but they did receive clarity.

A shareholder who had previously held a single, muddled, partially-cyclical paper-and-electricals position could now make discrete capital-allocation choices: sell the paper exposure, keep the electricals, or vice versa. Markets, in turn, could price each side on its own merits.

Within twelve months of listing, the combined market value of the two demerged entities exceeded what the pre-demerger entity had been worth on a similar revenue base — the classic empirical signature that the conglomerate discount had been real, and that removing it had been value-accretive.

There was also a softer, cultural payoff. Once Orient Electric existed as a standalone listed company, attracting talent into the business became materially easier. A young marketer or product manager joining a "consumer electric subsidiary of a paper company" sees a very different career path than one joining a listed FMEG brand that is benchmarked against Havells. The same is true of senior hires, of board appointments, of supplier negotiations, and of credit lines. The corporate-form change rewrote, slowly, every interaction the business had with the outside world.

V. The "Aero" Series & Premiumization Strategy

Walk into the conference room of any Indian consumer brand in the mid-2010s and you would have heard the same anguished question: "How do we get consumers to pay more for what looks like the same product?" The answer — articulated more clearly by Apple than by anyone else, but understood instinctively by good consumer marketers everywhere — is that you have to redefine what the product is.

Orient's answer, which began landing in stores around 2016 and reached full velocity post-IPO, was the "Aero" family of fans: Aeroquiet, Aerostorm, Aeroslim, and eventually an entire sub-brand built around the proposition that a fan was no longer a commodity utility but a lifestyle object.

The Aeroquiet, in particular, was the breakthrough product — an aerodynamically refined ceiling fan engineered to run materially quieter than conventional designs, marketed not on RPM or sweep or any of the technical metrics that fan companies had previously argued about, but on the experience of silence itself.[^5]

This is a small thing and a very big thing. For decades, Indian fan advertising had focused on speed ("ज़बरदस्त हवा" — tremendous breeze), or on aesthetic ("designer pankha"), or on durability ("25-year warranty"). Orient was the first major Indian player to advertise the absence of something — the absence of noise — as the principal benefit. That is the kind of advertising move you make when you believe your consumer has crossed the line from "I need a fan" to "I want a better fan." It is a luxury advertising move, in a category nobody thought of as luxury.

The campaign was anchored by महेंद्र सिंह धोनी MS Dhoni, the former Indian cricket captain and the most calmly authoritative celebrity endorser in the country at the time. Dhoni was a deliberate choice. He was not the explosive Virat Kohli; he was not the youthful Hardik Pandya. He was the man known across India for never raising his voice. Pairing his persona with the "silent fan" campaign was branding craftsmanship of a high order — the message was congruent at every level. Behind the scenes, this was less a one-off ad spend and more a complete repositioning, summarized by the "Switch to Smart" platform that connected fans, lighting, switchgear, and appliances under a single, premium-tilted umbrella.[^5]

The financial logic of premiumization, for those who haven't worked inside a consumer durables business, can sound subtle but is in fact violent. The Indian ceiling fan industry sells somewhere north of 50 million units a year. Roughly 70% of that, historically, has been sold at near-commodity Average Selling Prices (ASPs) of ₹1,200 to ₹1,800. A premium Aeroquiet retails closer to ₹4,500 to ₹6,000, and at the very top of the BLDC stack, fans cross ₹8,000.[^8]

When a manufacturer shifts even ten percentage points of its unit mix into the premium tier, the revenue uplift is enormous and the gross margin uplift is bigger still, because the premium component cost does not scale linearly with the premium retail price. The bill of materials for a premium ceiling fan is maybe 30 to 50% more expensive than a standard fan; the retail price is 200 to 300% more.

This is the playbook Orient executed, and it is the single most important reason why the post-demerger Orient Electric story is interesting at all. Without premiumization, the company would have remained a margin-compressed regional fan player. With it, Orient earned the right to be discussed in the same paragraph as Havells and Crompton — companies whose multiples reflect a structurally different return profile.

The premiumization push also dovetailed with a regulatory tailwind that arrived almost on cue: the BEE star-rating mandate for ceiling fans, which kicked in from 1 January 2023.5 We'll return to BLDC and that mandate in the bull case, but the relevant point here is that the Aero series gave Orient a head start on premium product architecture before the regulatory shift forced the entire industry up the value curve. By the time the rest of the industry was scrambling to ship 5-star BLDC fans, Orient already had a premium brand identity to attach them to.

Whether that head start is durable enough to survive the post-2023 wave of competitive BLDC launches from every other major fan brand — that is the more interesting investor question, and we'll meet it head-on in the bear case.

Two further observations on the Aero campaign era are worth setting down, because they connect cleanly to the company's current strategic posture. The first is that the campaign was a deliberate exercise in category education rather than pure brand-share warfare. Telling consumers that a quieter fan is worth paying more for required Orient to spend advertising rupees teaching the market what "quiet" means in a fan, why aerodynamics matter, and why an unbalanced blade produces audible noise. That kind of category-education spend is usually only economically rational for a category leader, because the spillover benefits competitors. Orient was, in effect, paying to expand the premium pie — and trusting that its brand and shelf presence would let it capture a disproportionate share of the expanded pie. Subsequent BLDC marketing by Havells, Crompton, and Bajaj has implicitly free-ridden on that education spend, but Orient remains the credibly "premium-quiet" brand in many consumers' minds, which is the moat the campaign was trying to build.

The second observation is about portfolio architecture. Aero was never just a SKU; it was a sub-brand designed to elevate the parent. Once the Aeroquiet and Aerostorm names earned credibility, Orient could extend the Aero halo onto adjacent fans, smart-home variants, and BLDC-specific lines without restarting the brand-build from zero. This is the same architectural move Apple uses with the "Pro" suffix and that Toyota uses with "Lexus": create a premium identity inside the master brand, let it accrete brand equity over years, then extend that equity to new categories as the timing permits. In Indian FMEG, this kind of sub-brand strategy is unusual; most competitors operate with a single master brand and a flat product line. Orient's willingness to invest in a separable premium identity is one of the genuinely distinctive marketing decisions in the recent history of Indian consumer durables.

VI. Current Management & The Governance Pivot

In Indian listed family-controlled companies, the boundary between "promoter" and "professional CEO" is one of the trickiest interfaces in corporate governance. Lean too far promoter-side and you get a company that runs on family whim; lean too far professional-side and you risk the alignment failure of a salaried CEO chasing short-term metrics. Orient Electric, in the eight years since its listing, has cycled through three substantively different management postures — and the cycle reveals quite a bit about how the CK Birla Group thinks about governance.

The first posture was Deepak Khetrapal's. Khetrapal was the architect of the demerger and the brand rebuild; he served as MD & CEO from the consumer electric days inside Orient Paper through the early post-listing years. His tenure is best understood as a "founder-equivalent" run — he took an industrial fan division and turned it into a listed consumer brand, and most of the strategic decisions Orient is still living off were taken in his era. He stepped back from the executive role as the company matured.

The second posture was the interim corporate steady-hand era under Rakesh Khanna, who served as MD & CEO during the difficult years of the BEE star-rating transition and the broader margin pressure that hit FMEG players across 2022 and 2023. Khanna, an industry veteran, was the public face of Orient when the BEE norms kicked in, and he was the one who described the star-rating mandate as a "massive shift" that would force the whole industry up the value chain.5

The current — and operationally most consequential — posture is Ravindra Singh Negi's. Negi was appointed Managing Director and CEO effective 31 May 2024, in a move that signaled something specific about the kind of leader Orient now believes it needs.6

Negi's resume is worth reading carefully because it tells you what the board is now optimizing for. Before joining Orient, he had been Chief Operating Officer of the consumer products business at Bajaj Electricals. Before that, he had run the Electrical Consumer Durables business at Havells — meaning he had spent years inside the playbook of Orient's single most important competitor.

And earlier still, he had run Bharti Airtel's Delhi and NCR telecom circle, a role that demanded mass-market consumer marketing, dense distribution management, and the kind of high-volume retail intuition that India's telecom wars built into an entire generation of executives.6 He is also a former chairman of the Indian Fans Manufacturers Association — the kind of industry-political appointment that signals deep relationships across the supplier and dealer ecosystems.

Read that resume in one sentence: Orient hired the person who knows how Havells and Bajaj actually win at the dealer counter. That is not a generic professional-CEO hire. That is a targeted, competitive hire — the board chose someone whose institutional memory is literally the playbook of the company Orient most needs to take share from.

Surrounding Negi is the broader governance structure of the CK Birla Group. The Promoter group has continued to hold a substantial stake in Orient Electric — roughly in the high 30s as a percentage of total equity, with the balance held by domestic mutual funds, foreign institutional investors, insurance companies, and the retail public.7 FII interest in Orient is notable in the context of the small-and-mid-cap FMEG universe; the company shows up in several India-consumption thematic funds.

The CK Birla family's governance style here is informative. They have steadily diluted the promoter stake from where it once was, but never to the point of losing control. Board representation is anchored by the family, but day-to-day execution is delegated to professional management.

ESOP and PSU plans have been used to align senior management with shareholder outcomes, with vesting tied substantially to EBITDA margin and revenue growth milestones rather than pure stock-price performance — a structurally healthier design than the more common "stock-price-only" ESOP that can encourage short-termism.

For a long-term investor, the practical implication is this: Orient is not a founder-led company in the romantic sense, but it is also not a faceless management-run conglomerate. The promoter is the long-term capital allocator and identity-keeper; the CEO is the operational and competitive strategist. The handshake between the two is what shareholders are really buying.

That handshake is now being tested across an unusually broad range of business segments.

One last governance observation worth recording: the post-listing journey has not been linear. The years between roughly 2021 and 2023 were challenging for Orient on multiple fronts simultaneously — input cost inflation hit the entire industry, the BEE transition forced bill-of-materials reengineering across the fan portfolio, and competitive intensity ratcheted higher as Crompton sharpened its post-demerger execution. The stock spent a meaningful stretch of that window underperforming the broader Nifty FMCG and consumer durables benchmarks. The board's response — first transitioning to Khanna as a stabilizing operator, then bringing in Negi with a sharper competitive mandate — reads, in retrospect, as a thoughtful sequencing rather than a panic move. Whether that read holds up depends on what the next four to eight quarters of operating performance deliver under the new leader.

VII. Hidden Businesses & Segment Analysis

If you were to read only the cover of an Orient Electric annual report, you would conclude that this is a ceiling fan company. If you read the segment notes, you would conclude something more interesting: this is a ceiling fan company that has been quietly building two adjacent businesses that, in aggregate, now contribute a meaningful and growing share of the top line — and a disproportionate share of the future optionality.

Orient reports its business in two segments: Electrical Consumer Durables (ECD), which contains fans, coolers, water heaters, kitchen appliances, and the broader home appliance portfolio; and Lighting & Switchgear (L&S), which contains LED lighting (consumer and professional), wires, and the rapidly expanding switchgear range.

In the year ended March 2026, ECD revenue ran at roughly ₹2,200 crore on an annualized basis, with the fourth quarter alone contributing ₹661 crore — up about 8% year-on-year — while the Lighting & Switchgear segment posted Q4 revenue of ₹287 crore, up nearly 16% year-on-year.8 In other words, the smaller segment is currently growing roughly twice as fast as the larger one. EBITDA in the same quarter was ₹77 crore at an 8.2% margin, expanding modestly from the prior year as the company worked through the post-BEE input cost normalization.8

That growth differential is the single most important fact about Orient's segment mix today, and it deserves a long look.

The ECD segment is the "cash cow." Fans throw off reliable cash, particularly in Q1 (the summer demand peak in India). They have the dealer network, the brand recognition, the manufacturing scale, and now — thanks to BLDC — a structural reason for consumers to upgrade.

The appliances inside ECD (mixer grinders, water heaters, room coolers, air coolers) are a tougher fight. Orient is challenging entrenched incumbents like Bajaj, Havells, Crompton, and the kitchen-specialist Preethi. None of those battles is easily won. But the ECD segment as a whole is a profitable, branded, scale-leveraged business with strong cash conversion.

The L&S segment is the more interesting story. Within it sits the "hidden gem" of the Orient portfolio — switchgear.

For non-Indian readers, a quick translation: switchgear in the Indian context refers to the family of electrical safety devices — miniature circuit breakers (MCBs), residual current devices (RCDs), distribution boards, modular switches — that sit between the household mains supply and the appliances.

The category is structurally attractive for three reasons. First, gross margins are typically 25 to 35%, materially higher than ceiling fans. Second, the demand is partially regulated — every new electrical installation requires switchgear by code, so the demand floor is real-estate-correlated rather than discretionary. Third, the buyer is the electrical contractor, which means once a brand wins the contractor's loyalty, switching costs are real (literally; rewiring a panel to swap brands is non-trivial).

Switchgear inside Orient has been a deliberate strategic priority for several years. The category puts Orient into direct competition with Havells (whose switchgear arm is the largest in the country), Legrand, Schneider, and ABB at the higher end. Orient does not yet command the share that any of those names do, but in growth terms, it is one of the highest-CAGR sub-segments inside the company, and it is the lever most likely to lift the consolidated EBITDA margin if it scales.

Within L&S, the lighting business is undergoing its own quiet transformation: from a commodity LED bulb business into a more professional and "smart" lighting business. The first is a price war; the second is a category where Orient can earn margin. The transition has been slow but steady, with smart lighting and IoT-enabled fixtures featuring more prominently in product launches.9

And then there is the M&A-shaped piece of the portfolio that, technically, is not M&A. In November 2018, Orient announced an exclusive marketing and distribution partnership with the Italian premium kitchen and personal-care major डी'लोंगी De'Longhi Group, covering the De'Longhi, Braun, and Kenwood brands in India.[^14]

In any other consumer market, the strategic playbook would have been to acquire a premium kitchen brand outright. In India, where domestic kitchen appliance acquisition multiples have inflated to levels where the math rarely works, a distribution partnership is an unusually capital-efficient way to plug a portfolio gap. Orient gets premium SKUs, a margin share, and brand-halo benefits — without paying acquisition premiums or absorbing integration risk. The Italian partner gets distribution into one of the largest consumer markets in the world without setting up a captive subsidiary.

Whether the De'Longhi partnership ever scales into a material revenue line is an open question; the size of the contribution has historically been small relative to Orient's core. But as a piece of strategic optionality, the deal is a textbook example of how to enter a crowded adjacent category without overpaying.

Pulling all of this together, Orient today is best understood not as a single business but as a portfolio: a mature ECD core that funds the business, a growing L&S segment that is taking share, and a small but credible premium-appliance optionality through the De'Longhi tie-up. The investor question is whether the L&S growth differential is durable enough to materially shift the consolidated revenue and margin mix over the next three to five years.

A short detour on the export and institutional channels, since they appear rarely in coverage but matter for the long-arc story. Orient has historically maintained a modest export business, primarily in fans, into markets in the Middle East, Africa, and parts of Southeast Asia where the climatic and electrical infrastructure profile mirrors India. Exports have never been more than a low single-digit share of revenue, and the company has not pursued the kind of branded international expansion that, say, Havells once attempted via its ill-fated Sylvania acquisition. The lesson Orient appears to have drawn from that cautionary tale is to stay disciplined on its home turf, where the demand growth is structural and the distribution moat is real, rather than chasing flag-planting in markets where the brand has no equity. Institutional sales — selling to real-estate developers, infrastructure projects, government tenders — have grown alongside the switchgear push. This channel is lumpier and less margin-rich than retail, but it builds relationships with electrical contractors and project consultants that pay dividends in future product cycles.

Within the appliances cluster of ECD, the strategic question is sharper. Air coolers in India are a structurally interesting category — high volume, seasonal demand, growing penetration outside metros — but margin-thin. Water heaters are the inverse: smaller volume, but stickier consumer purchase cycles, more meaningful margin, and a buyer who is more brand-conscious. Kitchen appliances, where Preethi, Philips, Bajaj, and Crompton dominate different sub-categories, are the toughest fight. Orient's segment commentary in earnings calls has consistently emphasized SKU rationalization and channel expansion in appliances rather than aggressive new-category entry, which is a sensible posture for a player that does not yet have an obvious right-to-win across all of kitchen.

VIII. 7 Powers & Porter's Five Forces Analysis

The most useful frameworks for analyzing a competitive position are the ones that survive translation from a Stanford MBA case study into the dust of an Indian dealer's warehouse. Hamilton Helmer's 7 Powers and Michael Porter's Five Forces are two such frameworks, and Orient Electric is a near-perfect case study for both.

Let's start with the 7 Powers.

The single most defensible power Orient holds today is what Helmer calls a Cornered Resource, expressed through the company's distribution network. Orient claims access to more than 125,000 retail touchpoints across India — a number that takes decades and tens of crores in trade margins to build.10

In Indian FMEG, distribution is not a soft moat. It is the moat. The contractor in Coimbatore will sell what is on his shelf. The shop in Patna will recommend what its credit-supplier insists on. A new entrant with a better product and a worse distribution network will lose against an incumbent with a worse product and a better distribution network, every single time, for years.

This is the structural reason Indian FMEG has so few new successful national brands — the price of entry is not the factory, it is the trade. Orient's network is real, sticky, and built on decades of relationships.

The second power is Brand — specifically what Helmer calls Affective Attachment. Orient has not yet reached the brand equity of Havells, but the Aeroquiet/Aero series rebranding has measurably moved its perception from "old-school regional" to "modern premium."

Brand power in FMEG is harder to measure than in say, beverages, but it shows up clearly in two places: the price premium a brand can command on identical-spec products, and the success rate of category extensions. Orient's premium pricing on Aero and BLDC products is meaningful evidence that the brand has real pull, not just shelf presence.

The third power, more nascent, is Scale Economies. Orient's centralized manufacturing in Faridabad (Haryana) and historic Calcutta-region facilities, combined with the company's investment in BLDC manufacturing capability, gives it cost-curve advantages relative to smaller regional players — though, importantly, not necessarily relative to Havells and Crompton, both of which operate at larger absolute scale. Scale economies in this industry tend to manifest in component procurement (motors, copper, aluminum), in SKU rationalization, and in the ability to amortize advertising across a national footprint.

What about powers Orient does not have? It does not yet have Switching Costs in the consumer fan business — a consumer who buys a Crompton fan today can buy an Orient fan in five years with zero friction. It does not have Network Economies. It does not have a meaningful Counter-Positioning advantage, because every major competitor sells essentially the same product mix. And it does not have a Process Power on the order of, say, Toyota in automotive — the manufacturing process is well-known across the industry.

So the honest 7 Powers reading is: Orient holds a strong Cornered Resource in distribution, a developing Brand, and a moderate Scale advantage. That is a credible competitive position, but not an impregnable one.

Now turn to Porter's Five Forces, framed in Indian-market terms.

The Threat of New Entrants is bifurcated. At the unorganized, low-end commodity ceiling fan tier, new entrants enter and exit constantly — the manufacturing equipment is cheap, the labor is available, and dozens of local brands compete in regional pockets.

But at the BLDC and "Smart Fan" tier, the entry barrier is suddenly material: BLDC motors require electronic control circuits, BEE 5-star certification, and meaningful R&D investment. The post-2023 BEE mandate has, paradoxically, made the high end of the market less contestable by new entrants while making the low end more contestable.

The Bargaining Power of Suppliers is moderate. The principal input costs are copper, aluminum, electronic components, and plastics — all globally traded commodities. Orient is too small to be a price-setter in any of these inputs, which means margin volatility in raw materials is a real and recurring feature of its earnings profile, not a bug.

The Bargaining Power of Buyers is concentrated not at the end-consumer level (any one household is negligible) but at the dealer and modern-trade level. Large electrical wholesalers and chains like Croma and Reliance Digital have meaningful negotiating leverage on terms, credit, and margin.

The rise of e-commerce (Amazon, Flipkart) has added another channel-power player into the mix — one that is willing to compress margins for share.

The Threat of Substitutes is interesting and category-specific. For ceiling fans, the substitute is the air conditioner — and as India's per-capita income rises, AC penetration is rising too.

This is a slow-moving but real long-term headwind to the volume curve in fans, partially offset by the BLDC-driven ASP uplift. For lighting, the substitute is essentially nothing — every building needs lights. For switchgear, again, essentially nothing — every building needs circuit protection.

The Intensity of Rivalry is the most important of the five forces in this industry and the one investors should weigh most heavily. Rivalry across Indian FMEG is brutal.

Havells, Crompton Greaves Consumer Electricals, Polycab, Bajaj Electricals, V-Guard, Finolex, and Anchor (Panasonic) all compete across overlapping product categories, all have national brand budgets, and all are sitting on healthy balance sheets. Margin discipline is constantly under pressure from competitive promotional activity, particularly during the Q1 summer season when fan volumes peak.

The composite reading: Orient operates in a structurally attractive demand environment (urbanization, electrification, real-estate growth, regulatory tailwind from BEE), with credible but not dominant competitive powers, against a set of well-capitalized national rivals. That is exactly the profile of a market-share-grower opportunity rather than a category-leader opportunity — which has implications for what investors should track.

A useful comparative lens here is to set Orient alongside its closest listed peers. Havells, the category bellwether, operates at roughly four to five times Orient's revenue, with a notably higher EBITDA margin, a deeper switchgear share, and a leadership position in the Lloyd-branded air conditioner business that Orient does not match. Crompton, the closest direct comparable on category mix, runs at roughly two times Orient's revenue with a comparable margin profile in fans but a different (and recently challenged) trajectory in pumps and appliances. Bajaj Electricals sits closer to Orient in revenue but with a meaningfully different category weighting toward kitchen and engineering procurement. Polycab is in a structurally different position, anchored in wires and cables — a wholesale-driven, B2B-tilted business — with consumer durables as a developing add-on. V-Guard plays a similar role in the South Indian market that Orient plays in the North. None of these competitors are weak; all of them are capitalized to spend through any temporary share war.

What makes the competitive map interesting is that the categories are blurring. Wire companies are entering fans. Fan companies are entering switchgear. Air conditioner companies are entering small appliances. Cross-category invasions have become routine, which means the relevant competitive question is no longer "who is best at fans" but "whose multi-category portfolio compounds fastest under shared distribution and shared brand spend." Orient's bet on the Aero sub-brand and the L&S segment scaling is, fundamentally, a bet on portfolio compounding. The bet either pays off as L&S becomes a third pillar alongside fans and appliances, or it gets absorbed into the same competitive squeeze every other mid-cap FMEG player has lived through.

IX. Bear vs. Bull Case

A clear-eyed view of Orient Electric demands sitting with both sides of the trade. The bull and bear cases here are not symmetric — one is a story about structural tailwinds and capital efficiency, the other is a story about competitive density and macro sensitivity. Both can be true at the same time.

The Myth vs. Reality Reset

Before getting to the two cases, it is worth puncturing two consensus narratives that show up in casual coverage of Orient.

Myth: "Orient is a fan company." Reality: in the year ended March 2026, fans are still the largest single revenue contributor, but the company's combined non-fan revenue — appliances, lighting, switchgear — has grown into a meaningful portion of the top line, and the growth rate of the L&S segment is materially higher than fans.8 Treating Orient as a pure fan stock dramatically understates the optionality in switchgear and professional lighting.

Myth: "The CK Birla Group is a sleepy legacy conglomerate." Reality: across the group's portfolio — Birlasoft in IT services, HIL in building products, Orient Electric in FMEG — the group has steadily moved its holdings toward modern, public-market-disciplined operating models. The "sleepy" label fit in 2005; it fits poorly in 2026.

The Bull Case

The first bull pillar is the Indian real estate and electrification supercycle. India is in the middle of a multi-decade infrastructure expansion that is upstream of every product Orient sells. New homes need fans. New homes need lights. New homes need switchgear.

The Real Estate Regulatory Authority (RERA)-era housing pipeline, the government's Pradhan Mantri Awas Yojana, and the gradual penetration of organized housing finance combine to create a demand floor that grows roughly with nominal GDP.

The second bull pillar is the BLDC replacement cycle. The Bureau of Energy Efficiency star-rating mandate that came into force on 1 January 2023 fundamentally reshaped the unit economics of the ceiling fan industry. A 5-star BLDC fan consumes up to 50% less energy than a conventional induction motor fan, and fans account for roughly 20% of household electricity in India.5

Once you do that math at a national scale — and once electricity tariffs continue their gradual upward drift — the consumer payback on upgrading to a BLDC fan inside two to three years becomes compelling. India has somewhere between 800 million and 1 billion ceiling fans in service. Even a slow replacement cycle implies tens of millions of fan upgrades a year over the next decade, at substantially higher ASPs than the install base.

The third bull pillar is the balance sheet. Orient has historically operated with negligible net debt and conservative working capital management. The asset-light model — manufacturing is meaningful but not capex-heavy relative to revenue — generates healthy return-on-capital-employed metrics through the cycle.

This is a critical defensive feature in an industry where competitors occasionally over-extend on inventory or distribution credit and pay the consequence in a tough year.

The fourth, quieter pillar is the management upgrade. The hiring of Ravindra Singh Negi from Bajaj Electricals (and previously Havells) is, in 7 Powers terms, an attempt to transfer institutional capability from the competition's playbook into Orient's organization.6

Whether that transfer succeeds is uncertain, but the direction of the bet is unambiguous.

The Bear Case

The first bear pillar is commodity price volatility. Copper and aluminum together account for a non-trivial share of the bill of materials in motors and wires. Spot price moves in either feed directly into gross margin in the next quarter or two, and Orient — like every other industry player — has limited ability to pass through cost spikes in real time without losing volume.

In bad quarters, margin compression of 100 to 200 basis points is not uncommon, and the stock tends to react sharply.

The second bear pillar is the discretionary spending sensitivity. While fans and basic lighting are quasi-staples, the appliances and premium portions of the portfolio are discretionary.

In any quarter when rural India or middle-class urban India tightens its belt, Orient feels it. The post-COVID FMEG slowdown in 2022 and 2023 was a clean reminder that "consumer discretionary" really does mean discretionary.

The third bear pillar is the brutality of competition in adjacent categories. In ceiling fans, Orient is in the top tier. In coolers and water heaters, it is one of many. In kitchen appliances, it is fighting Preethi, Philips, and Bajaj — all formidable incumbents. In professional lighting, it is fighting Signify (formerly Philips Lighting), Wipro, and Bajaj.

The risk is "diworsification" — the scattering of management bandwidth and capital across categories where Orient lacks a structural advantage, in the pursuit of a top-line story that does not translate into ROCE.

The fourth bear pillar is the multiple. Even after periods of stock weakness, Orient trades at a valuation that already prices in execution success. The bear's argument is not that the company is bad, but that the price already reflects most of the good news.

This is a different kind of risk than business risk — it is the risk that the gap between expected and delivered improvement is too narrow to leave room for a margin of safety.

Capital Deployment and the Diworsification Question

A specific second-layer diligence point on capital allocation: Orient operates with an asset-light philosophy, outsourcing or contract-manufacturing select categories rather than building captive capacity for everything. This keeps return on capital high in good years, but it raises a question for the more strategic-minded investor: in categories where the competitive moat is built on manufacturing capability (BLDC motors, premium switchgear), is the asset-light model strong enough? Or does Orient need to selectively build more captive capacity in the categories where vertical integration meaningfully widens the moat? This is the trade-off the current management team will increasingly have to navigate.

KPIs Worth Tracking

For long-term fundamental investors, three operating metrics matter more than the rest, and they are the ones serious tracking should center on:

-

Lighting & Switchgear segment revenue growth and EBIT margin. This segment is the highest-incremental-margin growth lever Orient has. If L&S compounds in the high teens and converts to consolidated margin expansion, the story works. If it stalls, the bull case weakens materially.

-

Premium fan mix as a percentage of total fan revenue. Orient does not break this out cleanly every quarter, but commentary in earnings calls and channel checks give a read. Premium share is the single best indicator of whether the brand strategy is translating into pricing power.

-

Operating EBITDA margin trajectory. Not the absolute level — which fluctuates with input costs — but the trajectory across a rolling four-quarter window. A trend of expanding EBITDA margin signals that the cost/price/mix engine is working. Stagnation signals competitive pressure is winning.

These are the three needles to keep an eye on. Everything else — quarterly volume, geographic mix, advertising spend — is supporting cast.

A brief, footnote-style aside on second-layer diligence items worth keeping in peripheral vision. On the regulatory side, future revisions to BEE star norms (which tend to ratchet upward every few years) will continue to reset the bill-of-materials economics for the entire industry — a tailwind for premium-positioned players, a headwind for low-cost importers. On the supply chain side, copper and aluminum price volatility and the share of imported electronics in BLDC motors create periodic working-capital tension; investors should track inventory days and gross margin together when assessing quarterly results, not in isolation. On the personnel side, key dealer and distributor relationships are often individual-led, and the company's bench depth in sales leadership beneath the CEO is something to watch over the medium term. Finally, on the optionality side, the De'Longhi/Braun partnership remains a small but interesting "free option" — if either party were to convert the arrangement into a deeper structural tie-up, the financial implications could be material relative to the current scale.

These overlays do not change the core story but they sharpen the texture of how to read each new disclosure.

X. Conclusion: Lessons in Legacy Refurbishment

There is a particular kind of Indian business story that does not get told often enough in global business media, and Orient Electric is one of its cleanest examples. It is the story of legacy refurbishment — the deliberate, multi-year transformation of an old industrial business into a modern consumer brand, without the dramatic flourishes of a Silicon Valley pivot or the visible glamour of a private-equity rollup.

The lessons are worth stating plainly.

First, demergers work when they correctly identify a mispriced sub-business. Orient Electric inside Orient Paper was a hidden growth asset wearing the metabolism of a paper company.

The 2018 listing did not change a single operating reality on the factory floor, but it changed the entire capital-markets identity of the business — and that change was worth real money to shareholders, almost immediately.

Second, brand rebuilds in Indian FMEG are slow but durable. The shift from Orient Fans to Orient Electric, the Aero series, the Dhoni endorsement, the "Switch to Smart" platform — none of these were single-quarter moves.

They compounded over years and required management willing to spend on brand before the brand fully earned it. The payoff shows up in the price premium consumers now accept on Aero and BLDC products.

Third, the unsexy parts of the portfolio are sometimes the most important ones. Switchgear is not glamorous. Nobody writes Twitter threads about MCBs.

But the segment's growth rate, margin profile, and contractor-loyalty dynamics make it a structurally more attractive business than ceiling fans, and Orient's slow patient build-out there will likely matter more to the next five years of the equity story than any single hero-product launch.

Fourth, the CK Birla Group's federated governance model — promoter-anchored but professionally-managed, with a deliberate preference for hiring the competition's best operators — is a quietly underestimated competitive advantage.

The hire of Ravindra Singh Negi was not a generic professional CEO appointment; it was a precision-targeted transfer of institutional capability from Havells and Bajaj into Orient. That kind of deliberate talent move is rare in Indian listed companies and worth noticing.

For investors tracking Orient Electric from here, the next two to three years will be defined by three things: the pace of the BLDC replacement cycle inside Indian households, the scaling trajectory of switchgear inside the Lighting & Switchgear segment, and the operating margin expansion delivered (or not) under the Negi-led management team.

The ceiling fan, that quiet workhorse of the Indian home, has been spinning over this country's living rooms for seventy years. The companies that make them have largely been treated as commodities. Orient Electric is in the middle of a serious, multi-year attempt to argue that this assumption was wrong all along — that the most ordinary object in the Indian household is, in fact, a premium consumer category waiting to be properly built. Whether that argument fully succeeds is the question its shareholders are paid to answer.

There is a final, broader thought worth ending on. The CK Birla Group's quiet, federated, professionally-managed style is not the kind of business model that lends itself to magazine cover stories. It does not produce a single charismatic founder around which a narrative can crystallize. It does not chase the dopamine of acquisitions for headlines. It does not optimize for quarterly drama. What it does, when it works, is produce an institution capable of patient capital allocation across decades — capable of taking a paper-mill side-hustle and turning it into a listed branded consumer business in roughly sixty-five years, capable of identifying when a sub-business has outgrown its parent corporate form, and capable of hiring the kind of executive talent whose institutional memory is the playbook of the competitor it most needs to beat.

That style of corporate behavior is rare globally. It is rarer still in Indian listed equity markets, where promoter-driven short-term capital allocation and family-control opacity are persistent issues. To the extent Orient Electric represents a clean example of the alternative — a promoter-anchored, professionally-managed, segment-disciplined, dividend-paying mid-cap with optionality on the most important consumption tailwinds in the world's most populous country — it is a case study worth following carefully, whatever any individual investor decides to do about the position. The next two to three years will tell us whether the story so far has been a beginning or a plateau.

References

References

-

Listing of Orient Electric Limited — Orient Electric Limited ↩

-

Orient Paper & Industries — Investors / Demerger Information ↩

-

Orient Electric debuts on stock exchanges and hits upper circuit at Rs. 142 — CK Birla Group Press Release, 2018-05-14 ↩↩↩

-

Ceiling fans get costlier as BEE's revised norms mandate star labelling — Business Standard, 2023-01-08 ↩↩↩

-

Orient Electric appoints Ravindra Singh Negi as MD & CEO — Exchange4media, 2024-05-31 ↩↩↩

-

Orient Electric zooms 20% on strong Q2 operational performance — Business Standard, 2024-10-28 ↩↩↩

-

Orient Electric to focus on smart lighting, IoT-enabled fans for growth — Zee Business ↩

-

Orient Electric Limited — Board of Directors and Company Overview ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube