Oriana Power: India's Renewable Energy Rocket Ship

I. Introduction & The Clean Energy Context

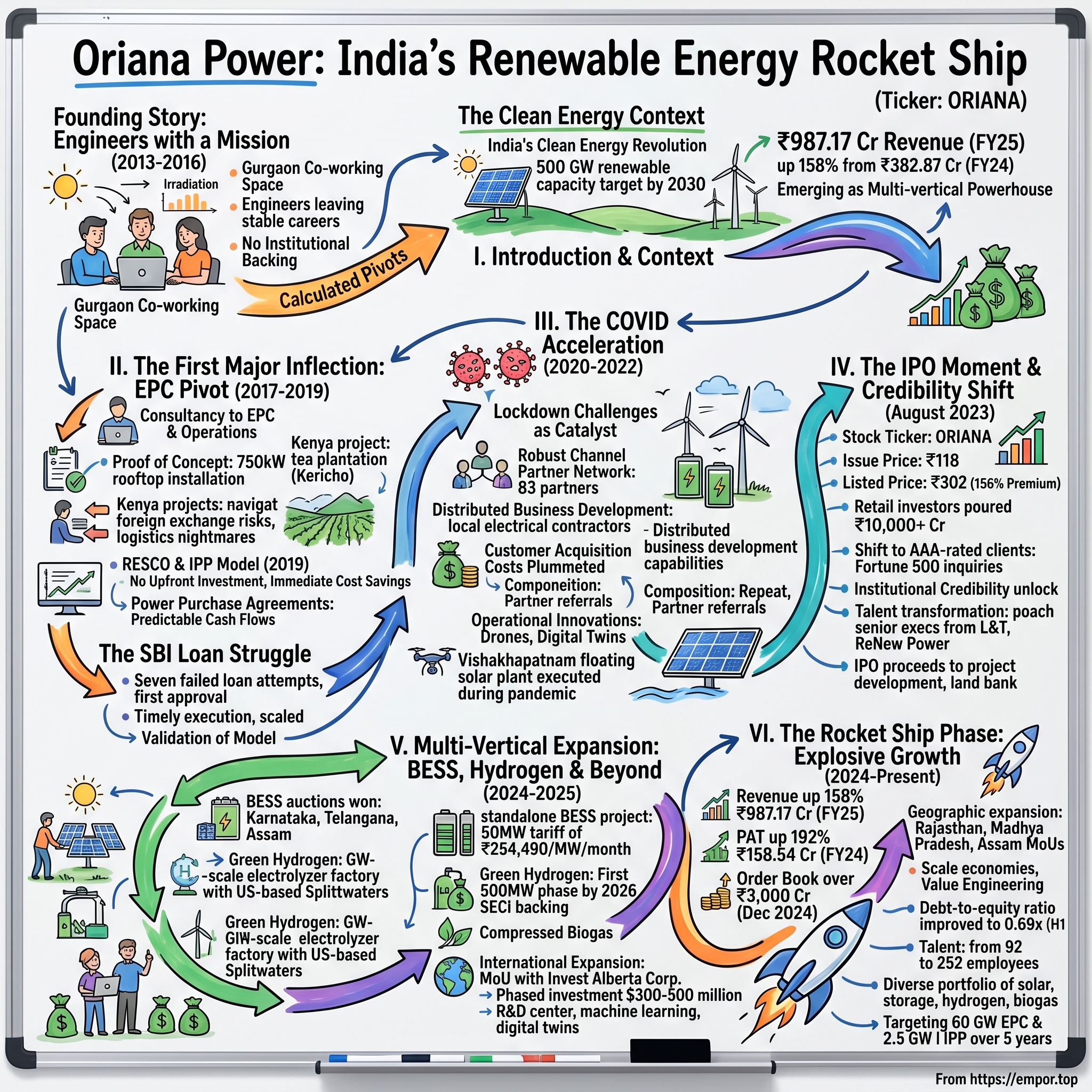

The numbers tell a story that would make any growth investor's pulse quicken. ₹987.17 crore in revenue for FY25, up 158% from ₹382.87 crore in FY24—the kind of trajectory that transforms companies from obscurity to market leadership. In the world of renewable energy, where promises often outpace performance, Oriana Power has emerged as that rare breed: a company that actually delivers on its ambitious targets.

Picture this puzzle: How does a solar consultancy founded in 2013 by three engineers with no institutional backing transform into a multi-vertical renewable powerhouse executing projects worth thousands of crores across India, Kenya, and now eyeing Canada? The answer lies not in a single breakthrough moment, but in a series of calculated pivots, each perfectly timed to catch the next wave of India's clean energy revolution.

India's renewable energy landscape today bears little resemblance to the fragmented, policy-uncertain market of 2013. The country now targets 500 GW of renewable capacity by 2030, with solar leading the charge. Yet when Rupal Gupta, Parveen Jangra, and Anirudh Saraswat founded Oriana Power, solar was still an expensive experiment for most Indian businesses. The founders saw what others missed: not just the inevitable cost decline of solar technology, but the coming convergence of climate consciousness, regulatory support, and most critically, the desperate need for execution excellence in a market long on ambition but short on delivery.

What makes Oriana's story particularly compelling isn't just the growth—plenty of renewable companies have grown fast only to flame out faster. It's the architecture of that growth: bootstrapped beginnings, strategic use of public markets for credibility rather than dilution, and an uncanny ability to identify and dominate emerging niches before competition arrives. While established players fought over utility-scale projects, Oriana quietly built expertise in floating solar, rooftop installations on coal dumps, and hilltop projects—the difficult, specialized work that commands premium margins.

This episode unpacks how a company with no venture backing, no government connections, and no first-mover advantage became one of India's fastest-growing renewable energy players. We'll explore the seven failed loan attempts that nearly killed the company before its first SBI approval, the COVID-era channel partner strategy that created a distribution moat, and the post-IPO transformation that enabled a shift from BBB+ rated clients to blue-chip corporates. Most intriguingly, we'll examine how Oriana is positioning itself not just as a solar company, but as an integrated clean energy platform spanning battery storage, green hydrogen, and compressed biogas—essentially building the Reliance or Adani of the SME renewable world.

The timing of this story matters. As global energy markets grapple with the trilemma of affordability, reliability, and sustainability, companies that can execute across the entire clean energy stack will capture disproportionate value. Oriana's journey from consultancy to potential unicorn offers lessons not just about renewable energy, but about how to build enduring businesses in rapidly evolving markets. Whether you're an investor evaluating the next wave of climate tech winners, an entrepreneur navigating India's infrastructure maze, or simply someone trying to understand how the energy transition actually happens on the ground, this story deserves your attention.

II. The Founding Story: Engineers with a Mission (2013–2016)

The conference room at a Gurgaon co-working space, early 2013. Three engineers huddle around a laptop, spreadsheet after spreadsheet of solar irradiation data glowing on the screen. Outside, the Delhi NCR skyline—a monument to fossil-fueled growth—shimmers through the haze. Incorporated in 2013, Oriana Power Limited started with providing EPC and operations of solar power projects, but the real story begins with what drove these three individuals to leave stable careers and bet on an industry that barely existed in India.

Rupal Gupta brought the technical precision—an engineer who could calculate payback periods and degradation rates in his sleep. Parveen Jangra understood project execution from his construction industry background, knowing exactly how Indian contractors worked (and didn't work). Anirudh Saraswat, the youngest of the three, possessed that rare combination of technical knowledge and business development hustle. Together, they saw an opportunity hidden in plain sight: India's commercial and industrial sector desperately needed to reduce energy costs, but nobody was offering turnkey solar solutions they could trust.

The early days were an exercise in creative poverty. Without capital to build projects, they started as consultants—essentially selling their expertise while competitors sold panels. "We'll design your solar system, manage the EPC contractor, ensure quality—everything except finance it ourselves," became their pitch. It was unglamorous work: site assessments in 45-degree heat, endless negotiations with skeptical factory owners, and late nights preparing feasibility reports that might never convert to projects.

India's solar landscape in the early 2010s resembled the Wild West. The National Solar Mission had set ambitious targets—20 GW by 2022—but ground reality was chaos. Chinese modules flooded the market with questionable quality claims, fly-by-night EPC contractors disappeared mid-project, and banks treated solar loans like speculative ventures. Grid infrastructure couldn't handle intermittent generation, state electricity boards changed policies overnight, and industrial customers remained convinced solar was either a scam or a CSR exercise.

Yet within this chaos, the founders identified their edge: obsessive focus on execution quality. While competitors chased the largest projects, Oriana specialized in complex, customized installations. A 500 kW rooftop system for a textile mill in Surat. A ground-mounted plant on rocky terrain in Rajasthan. Each project was a masterclass in problem-solving—dealing with structural load limitations, navigating local permitting mazes, optimizing for shadows from adjacent buildings. They weren't just installing solar panels; they were building a reputation for making the impossible possible.

The SBI loan struggle became company legend: securing first project financing after seven attempts, building credibility through timely execution and regular repayments, enabling scale without equity dilution. Each rejection taught them something—better financial models, stronger project documentation, clearer risk mitigation strategies. When approval finally came for a 2 MW project in Haryana, it wasn't just capital they'd secured. It was validation that their model worked, that solar could be bankable in India, and that execution excellence could overcome the liability of being unknowns in an industry dominated by established infrastructure players.

The consultancy model, initially born of necessity, proved strategically brilliant. By 2016, they'd touched over 50 MW of projects—not as owners but as trusted advisors. They knew every supplier's real delivery timelines, every contractor's actual capabilities, every technology's true performance in Indian conditions. This intellectual capital would become invaluable when they made their next big pivot.

What distinguished Oriana wasn't technological innovation—they used the same panels and inverters as everyone else. Instead, they innovated on trust in an industry plagued by overpromising. Their projects consistently delivered 5-7% more energy than projected. Maintenance issues were resolved in hours, not weeks. Financial models included realistic degradation assumptions rather than optimistic fantasies. In a market where customers had been burned by cowboys, Oriana became the boring, reliable choice—exactly what risk-averse industrial customers wanted.

By late 2016, the founders faced a critical decision. They could continue as successful consultants, earning steady fees with minimal capital requirements. Or they could leverage everything they'd learned to become asset owners, capturing not just one-time EPC margins but decades of power generation revenue. The choice would transform them from service providers to infrastructure builders, from cash-flow positive consultants to capital-hungry developers. It was risky, potentially fatal if executed poorly. They went all in.

III. The First Major Inflection: EPC Pivot (2017–2019)

Having started as a consultancy, it moved into EPC (engineering, procurement and construction) services in 2017. The decision wasn't made in a boardroom but on a construction site in Kota, where Anirudh Saraswat watched a competitor's project collapse—literally. Poor structural design, substandard mounting systems, and absent quality control had turned a 5 MW solar farm into twisted metal and shattered glass after the first pre-monsoon storm. The client, a large cement manufacturer, lost crores and faith in solar. Saraswat saw opportunity in the wreckage: India needed EPC players who actually understood engineering, not just trading.

The pivot to EPC required capital, capabilities, and credibility—none of which Oriana possessed in abundance. The founders pooled personal savings, convinced family members to invest, and leveraged every relationship built during their consultancy years. The first EPC project, a modest 750 kW rooftop installation for an auto components manufacturer in Gurgaon, became their proof of concept. They acted as developer, designer, procurement manager, construction supervisor, and commissioning agent—essentially an entire EPC organization compressed into three founders and five engineers.

Since June 2017, successfully delivered projects exceeding 100 MWp capacity across multiple locations in India and Kenya. The Kenya projects deserve special attention—not for their size but for what they represented. While Indian competitors focused domestically, Oriana recognized that their execution capabilities were actually more valuable in markets with even less solar infrastructure. The first Kenya project, a 2 MW installation for a tea plantation in Kericho, required navigating foreign exchange risks, unfamiliar regulations, and logistics nightmares. Yet it delivered 18% returns and opened an entire continent of opportunity.

The innovation that truly differentiated Oriana was the RESCO model—Renewable Energy Service Company—where they owned and operated solar assets, selling power to customers through long-term agreements. In 2019, it transitioned to the IPP (independent power producer) model, investing its capital to sell electricity directly while also helping its clients get around financial bottlenecks. This wasn't just adding another business line; it was solving the fundamental barrier to solar adoption: upfront capital requirements.

Consider the typical industrial customer's dilemma. A textile mill owner knows solar will reduce energy costs by 30%, but investing ₹5 crore in panels means not upgrading machinery or expanding production. Banks prefer lending for core business activities over solar projects. The mill owner wants solar's benefits without solar's capital commitment. Oriana's RESCO model offered exactly that: zero upfront investment, immediate cost savings, and no operational headaches. The mill pays Oriana for solar power at rates 20-25% below grid tariffs, saving money from day one while Oriana earns returns over 25 years.

The financial engineering behind RESCO was elegant. Projects offered 16-18% equity returns with 70% debt financing at 9-10% interest rates. Power purchase agreements with creditworthy corporates provided predictable cash flows for debt servicing. After loan repayment in years 10-12, projects became cash-generating machines with minimal operating costs. By owning assets rather than just building them, Oriana captured value across the entire project lifecycle—development fees, EPC margins, and decades of generation revenue.

Building execution capabilities from scratch meant creating systems for everything. Procurement protocols to ensure module quality while managing working capital. Construction methodologies that reduced installation time by 30% without compromising safety. Commissioning procedures that caught issues before energization. Operations and maintenance frameworks that predicted failures before they occurred. Each project refined these systems, creating institutional knowledge that couldn't be easily replicated.

Over the years, they successfully delivered marquee projects including floating solar plants, hilltop installations, a 28MW project on a coal dumping yard and a 129MW project for the steel industry. A 3MW floating solar installation in Vishakhapatnam was executed during the COVID-19 pandemic. These weren't just projects; they were calling cards. Floating solar required understanding hydrology and anchoring systems. Coal dump installations meant dealing with unstable ground and fire risks. Hilltop projects involved logistics nightmares and wind loading calculations. Each complex project that Oriana successfully executed expanded their addressable market and justified premium pricing.

The 129 MW steel industry project, completed in 2019, marked Oriana's arrival as a serious EPC player. The project, spread across multiple sites for a large integrated steel plant, involved rooftop installations on production sheds, ground-mounted systems on ash dykes, and innovative mounting structures over conveyor belts. The complexity was staggering—coordinating with ongoing plant operations, managing hot work permits in a heavy industrial environment, ensuring zero production disruption. Completion on schedule and 3% under budget established Oriana's reputation for executing India's most challenging solar projects.

Yet the real transformation during this period was organizational. The three-founder consultancy evolved into a 40-person organization with dedicated teams for business development, engineering, procurement, project management, and O&M. They hired selectively—young engineers from tier-2 colleges hungry to prove themselves, experienced project managers tired of bureaucracy at large EPCs, finance professionals who understood both infrastructure and spreadsheets. The culture remained scrappy and entrepreneurial, but processes became institutional and scalable.

By the end of 2019, Oriana operated across two distinct but synergistic models. The EPC business generated immediate cash flows and margins of 12-15% while building technical credibility. The RESCO portfolio, though capital-intensive, created long-term value with contracted revenues extending to 2044. Together, they positioned Oriana as both a service provider and asset owner, able to offer customers whatever solution best fit their needs. This flexibility would prove invaluable when the world changed in early 2020.

IV. The COVID Acceleration & Channel Partner Strategy (2020–2022)

March 2020. India enters the world's strictest lockdown. Construction sites abandoned, supply chains severed, solar installations grinding to a halt. For most renewable energy companies, COVID-19 was a catastrophe. For Oriana, it became a catalyst that would accelerate growth by five years.

While the COVID-19 pandemic was a challenging time, it also came as an opportunity. Their Resco projects kept generating income, and they built a robust network of 83 channel partners across India, which became a major growth driver post-pandemic. The insight was counterintuitive but powerful: while new project development stalled, existing solar assets kept generating power and revenue. Oriana's RESCO portfolio, which many had viewed as capital-heavy and risky, suddenly looked prescient. Monthly power purchase payments continued flowing even as industrial production plummeted, providing stability when EPC revenues evaporated.

The channel partner strategy emerged from necessity but evolved into competitive advantage. With travel restricted and face-to-face sales impossible, Oriana needed distributed business development capabilities. The solution: recruit and train local electrical contractors, energy consultants, and equipment suppliers as channel partners who could identify and qualify opportunities in their regions. The model was simple but powerful—partners earned commissions for successful lead conversion, creating aligned incentives without fixed costs.

Consider Rajesh Sharma, an electrical contractor in Indore who became Oriana's channel partner for Madhya Pradesh. Sharma had spent 15 years installing transformers and switchgear for local industries, building deep relationships with factory owners and plant managers. He understood their energy pain points, spoke their language, and most importantly, had earned their trust. When Sharma recommended Oriana for solar projects, it carried more weight than any corporate sales pitch. Within six months, he'd generated leads worth ₹50 crore, earning commissions that dwarfed his traditional contracting income.

The channel partner network wasn't just about lead generation—it became Oriana's eyes and ears across India's industrial heartland. Partners reported policy changes before they hit newspapers, identified distressed assets available for acquisition, and provided real-time competitive intelligence. When Tamil Nadu announced new renewable purchase obligations, Oriana knew within hours through their Chennai partner. When a competitor faced execution challenges in Gujarat, their Ahmedabad partner provided detailed updates. This information asymmetry allowed Oriana to move faster and smarter than larger competitors.

The pandemic also accelerated industrial customers' solar adoption for unexpected reasons. With employees working from home and production reduced, factories could finally undertake rooftop installations without disrupting operations. Energy costs, always important, became critical as companies fought to preserve margins during demand destruction. Government stimulus packages included accelerated depreciation benefits for renewable investments. Environmental commitments, previously nice-to-have, became board-level mandates as companies recognized climate risks to their business models.

Revenue grew from ₹30 crore in FY21 to ₹135 crore in FY23, but the numbers only tell part of the story. The composition of growth was equally important—40% from repeat customers, 35% from channel partner referrals, and just 25% from cold business development. Customer acquisition costs plummeted while project margins improved as Oriana cherry-picked the most profitable opportunities from abundant deal flow.

The operational innovations during this period were remarkable. With site visits restricted, Oriana developed remote survey capabilities using drones and satellite imagery. Engineering designs were standardized into modular templates that could be customized parametrically. Procurement shifted from just-in-time to strategic stocking, taking advantage of pandemic-driven module price crashes. Project execution protocols incorporated health safety measures that actually improved overall safety performance. Digital twin models allowed customers to visualize installations before construction began.

One project exemplifies Oriana's COVID-era execution excellence: a 3MW floating solar installation in Vishakhapatnam executed during the pandemic. Floating solar was already complex—dealing with water level variations, corrosion risks, anchoring challenges. Add pandemic restrictions, and it seemed impossible. Yet Oriana completed the project on schedule by quarantining workers on-site, creating bubble teams that lived and worked together, and leveraging local partnerships for logistics. The project's success during peak pandemic chaos demonstrated Oriana's operational resilience and opened doors to larger floating solar opportunities.

The financial management during 2020–2022 deserves special recognition. While competitors burned cash hoping for recovery, Oriana played offense. They negotiated extended payment terms with suppliers facing inventory buildup. They acquired distressed projects at 60-70% of development cost from developers needing liquidity. They raised structured debt against RESCO assets at historically low interest rates. Most cleverly, they offered customers deferred payment plans for EPC projects, essentially providing vendor financing that deepened relationships while earning additional returns.

By late 2021, Oriana faced a different challenge: growth was outpacing organizational capacity. The three-founder structure that worked for a ₹30 crore company was straining at ₹100+ crore revenue. Decision-making bottlenecks emerged, execution quality showed occasional cracks, and employee turnover increased as competitors poached talent. The solution wasn't just hiring more people but fundamentally restructuring the organization. Dedicated vertical heads for EPC and RESCO, regional managers for key markets, and functional leaders for engineering, procurement, and finance. The founders transitioned from operators to strategists, focusing on capital allocation and business development while empowering the next leadership generation.

Preparing for public markets became the consuming focus of 2022. Not because Oriana desperately needed capital—they'd remained profitable throughout the pandemic—but because they recognized that institutional credibility would unlock a different customer universe. Blue-chip corporates and government entities preferred working with listed companies. Banking relationships improved dramatically with public market validation. Employee stock options became meaningful retention tools. Most importantly, being public would force the governance discipline needed for the next phase of growth.

The IPO preparation was exhaustive: cleaning up related party transactions, formalizing board governance, implementing enterprise resource planning systems, and establishing audit committees. The founders insisted on pricing the IPO conservatively, wanting strong listing gains to build momentum. They also made an unusual decision: no venture capital or private equity participation before the IPO. This meant less dilution and complete control but also meant convincing retail investors to bet on a company they'd never heard of in a sector notorious for execution failures.

V. The IPO Moment & Credibility Shift (August 2023)

The IPO consisted of 50,55,600 equity shares of face value ₹10 aggregating up to ₹59.66 Crores. The issue was priced at ₹118 per share. In the world of startup IPOs, this might seem like pocket change. But in the SME exchange context, and for a bootstrapped company that had never raised institutional capital, the August 2023 IPO represented a watershed moment—not for the capital it raised, but for the transformation it triggered.

The subscription numbers told their own story. The SME public offer got oversubscribed by 176.65 times on the last day of the offer. Retail investors, usually skeptical of SME IPOs, poured in applications worth over ₹10,000 crore for a ₹60 crore offering. The grey market premium touched ₹115, suggesting a near-doubling on listing day. The investment community's message was clear: Oriana wasn't just another solar company but a rare combination of growth, profitability, and execution credibility.

The issue price of Oriana Power IPO was ₹118.00, listed at a price of ₹302.00, which is 155.93% higher than the allotment price. August 11, 2023, listing day. The stock opened at ₹302, a 156% premium to the issue price, and climbed further to ₹350 before settling around ₹320. In a single day, the three founders' combined stake value exceeded ₹500 crore—more wealth than they'd imagined when starting the company with personal savings a decade earlier. But they didn't sell a single share. This wasn't an exit but an entry—into a different league of business altogether.

The immediate transformation was visceral. Within weeks of listing, Oriana's inbox exploded with inquiries from Fortune 500 companies that had previously ignored them. The shift from BBB+ to AAA-rated clientele happened almost overnight, growing the portfolio to over 600 MW. A listed company, even on the SME exchange, carried gravitas that no amount of marketing could buy. Audit committees at large corporations could now approve Oriana as a vendor. Banks offered working capital limits at prime rates. Equipment suppliers extended credit terms previously reserved for established players.

The post-IPO capital raise strategy was equally shrewd. In 2024, Oriana raised a further Rs 2 billion through a preferential round. Instead of diluting at IPO when valuations were uncertain, they waited for public market price discovery, then raised growth capital at a significant premium. The preferential allotment attracted institutional investors who'd missed the IPO, creating a more sophisticated shareholder base while maintaining founder control.

Consider the Dalmia Cement project signed three months post-IPO. Dalmia, one of India's largest cement manufacturers, needed a partner for 50 MW of solar across multiple manufacturing sites. The project required ₹400 crore investment, sophisticated financial structuring, and flawless execution across six states. Pre-IPO Oriana wouldn't have even been invited to bid. Post-IPO, they won against established infrastructure giants, partly on technical merit but largely due to newfound institutional credibility. The project's successful execution opened doors to the entire cement industry, one of India's largest industrial power consumers.

The talent transformation was equally dramatic. Pre-IPO, Oriana struggled to attract experienced professionals from established companies. Post-IPO, with employee stock options now liquid currency, they poached senior executives from L&T, Sterling & Wilson, and ReNew Power. The head of business development came from Azure Power, bringing relationships with global investors. The CFO arrived from a Big Four firm, implementing institutional financial controls. The chief technology officer, recruited from a European renewable major, introduced cutting-edge energy storage expertise.

Public market discipline forced operational improvements that private company comfort had postponed. Quarterly results meant no hiding behind annual adjustments. Analyst calls required articulating strategy clearly and consistently. Regulatory compliance for listed companies eliminated shortcuts that might have been tempting as a private entity. The founders initially chafed at these constraints but soon recognized their value in building a sustainable institution rather than a promoter-dependent business.

The IPO also unlocked government doors previously closed to small private companies. Solar Energy Corporation of India (SECI), the nodal agency for large-scale renewable projects, began inviting Oriana to restricted tenders. State electricity boards, notorious for payment delays to small vendors, treated a listed company with more respect. Most importantly, policy consultations that shaped industry regulations now included Oriana's voice, allowing them to influence market rules rather than just follow them.

The working capital transformation was perhaps most impactful operationally. Banks that had required 150% collateral for guarantees pre-IPO now offered unsecured limits. Letter of credit costs dropped from 3% to 0.75%, directly improving project returns. Equipment suppliers offered 60-day payment terms versus cash on delivery. These seemingly mundane changes freed up hundreds of crores in working capital, allowing Oriana to bid for larger projects and accept lower margins to win strategic clients.

One number captures the IPO's impact: win rate. Pre-IPO, Oriana won roughly 15% of projects they bid for, usually competing on price in smaller tenders. Post-IPO, the win rate jumped to 35%, increasingly winning on technical merit in larger, complex projects. The average project size increased from ₹25 crore to ₹75 crore. Client concentration reduced as blue-chip names joined the roster. Geographic expansion accelerated with projects won in previously untapped states like Assam and Odisha.

The media attention following the successful listing created unexpected benefits. Business newspapers that had ignored Oriana now featured founder interviews. Industry conferences invited keynote speeches. MBA colleges requested case study collaborations. This visibility created a virtuous cycle—more attention meant more business opportunities, which generated better results, which attracted more attention. The company that had spent a decade in obscurity suddenly found itself in the spotlight.

Yet the founders remained remarkably grounded. The IPO proceeds weren't splurged on vanity acquisitions or luxury offices. Instead, they went directly into project development, land acquisition for solar parks, and working capital for larger EPC projects. The registered office remained the same modest space in Okhla Industrial Area. The founders still flew economy class for domestic travel. The message to employees and investors was clear: going public hadn't changed the fundamental DNA of execution excellence and capital efficiency.

The strategic options opened by public listing were transformational. Oriana could now consider acquisitions using stock currency. International expansion became feasible with the credibility of being a listed entity. New business verticals like energy storage and green hydrogen, which required patient capital and institutional trust, suddenly seemed achievable. The IPO wasn't just a financial event but a strategic unlock that would enable the next phase of Oriana's evolution from solar pure-play to integrated renewable energy platform.

VI. The Multi-Vertical Expansion: BESS, Hydrogen & Beyond (2024–2025)

The boardroom discussion in January 2024 would have seemed like fantasy just eighteen months earlier. "We're not just competing for solar projects anymore," Anirudh Saraswat told his team. "We're building the renewable energy conglomerate of the future." The ambition was breathtaking: simultaneous expansion into battery energy storage systems (BESS), green hydrogen production, and compressed biogas—each a complex new vertical requiring different capabilities, capital, and customers. Yet by October 2025, this diversification strategy had already delivered extraordinary results.

The BESS opportunity emerged from a fundamental grid problem. India's solar capacity was exploding, but the sun inconveniently sets during evening peak demand. Oriana Power has won auctions for standalone BESS projects in Karnataka, Telangana, and Assam. The Karnataka project deserves deep analysis: Oriana's successful bid was at a tariff of ₹254,490 (~$2,971.28)/MW/month for 50 MW, securing a total order value of INR 2.12 billion. This wasn't just another infrastructure project but a fundamental bet on India's energy storage future.

The technology learning curve for BESS was steep. Unlike solar panels, which are essentially commoditized, battery systems required understanding cell chemistry, thermal management, power conversion systems, and grid integration protocols. Oriana's approach was characteristic: rather than pretending expertise they didn't have, they partnered with global technology leaders while building internal capabilities. The CTO hired from Europe brought deep battery expertise. Young engineers were sent for training programs with battery manufacturers in China and South Korea. The company invested in testing facilities to understand battery performance in Indian temperature extremes.

The 125 MW/250 MWh standalone BESS project at Giral Sub-Station in Rajasthan exemplified the scale of ambition. The battery energy storage facility will be established at the Giral Substation for supporting grid operations by managing demand-supply imbalances. Think about what this means: Oriana was essentially building a massive battery that could power a small city for hours, stabilizing the grid when renewable generation fluctuated. The technical complexity was matched only by the financial engineering required to make such projects viable.

The BESS business model was elegantly different from solar. Instead of selling energy, Oriana was selling grid stability—a premium service that utilities desperately needed as renewable penetration increased. The company has delivered over 254 MW of projects and has another 1,500+ MW worth of projects in pipeline, of which 300 MWh are BESS projects. It's rapidly scaling its BESS solutions business to drive 10-20% of next year's revenue from it and aims to become a key player in BESS with a total capacity of 3.5 GWh by 2030.

The green hydrogen pivot was even more audacious. While the world debated hydrogen's role in energy transition, Oriana committed to building India's electrolyzer manufacturing capacity. Oriana Power is setting up a gigawatt-scale factory to produce alkaline electrolyzers and balance-of-plant (BOP) modules in partnership with US-based Splitwaters. The factory will be commissioned in two phases, with the first 500 MW phase to be operational by 2026.

The Splitwaters partnership was masterful deal-making. Instead of licensing technology and paying royalties forever, Oriana structured a joint venture where they provided local manufacturing and market access while Splitwaters brought proven technology. The partnership addresses green hydrogen market challenges of high capital costs and lengthy execution timelines effectively, allowing deployment of state-of-the-art technology at up to 30% lower CAPEX than competing methods.

But Oriana wasn't just building electrolyzers—they were creating an entire green hydrogen ecosystem. The SIGHT scheme allocation was a crucial validation: Green Hydrogen projects, with an allocation of 10 KTPA secured from SECI (Solar Energy Corporation of India), a Government of India enterprise. This government backing provided both credibility and a guaranteed offtake pathway for their hydrogen production.

The compressed biogas venture represented yet another strategic vector. Agricultural waste, previously burned and causing pollution, could be converted into renewable natural gas. The synergies with existing business were compelling: the same industrial customers buying solar power also needed gas for process heating. The same project development skills worked for biogas plants. The same focus on distributed generation fit perfectly with biogas's feedstock constraints.

The international expansion accelerated dramatically with the Canadian opportunity. In July 2025, Oriana entered a Memorandum of Understanding with Invest Alberta Corporation to explore and develop renewable energy projects. Under this MOU, they intend to develop a vertically integrated renewable energy complex with phased investment opportunities initially ranging from $300 million to $500 million USD, with potential to scale to $1 billion within five years.

The Alberta project wasn't just about geographic diversification—it was about climbing the technology value chain. As Anirudh Saraswat noted after engaging with renewable energy and hydrogen industry leaders during the Calgary Stampede, Calgary stands out as a vibrant, globally connected city for trade and clean energy investment. The collaboration represents not just investment in clean energy, but in people, communities, and the shared future of both India and Alberta.

The technological capabilities Oriana built for these new verticals were staggering. The company established an R&D center in Pune focused on energy storage optimization. They partnered with IIT Bombay for hydrogen production research. A digital twin platform was developed to simulate integrated renewable energy systems. Machine learning algorithms predicted battery degradation and optimized charging cycles. This wasn't just project execution anymore—it was genuine technology innovation.

The financial metrics of the multi-vertical strategy were compelling. BESS projects offered 18-20% returns with 10-year contracts. Green hydrogen production, once scaled, projected 25%+ returns given India's massive industrial hydrogen demand. Compressed biogas provided steady 15% returns with 20-year purchase agreements. Together, these verticals diversified revenue streams, reduced dependence on solar policy support, and positioned Oriana for the next decade of energy transition.

The organizational transformation required for multi-vertical operations was immense. Team size grown from 92 in FY24 to 252 employees, but headcount was just the beginning. Oriana created separate business units for each vertical with dedicated P&L responsibility. Cross-functional teams ensured knowledge transfer between verticals. A central project management office coordinated resource allocation across businesses. The company that had operated as an extended founding team was becoming a true corporation.

Risk management became exponentially more complex with diversification. BESS projects carried technology obsolescence risk as battery costs plummeted annually. Green hydrogen faced demand uncertainty as industrial adoption remained nascent. International expansion brought currency and regulatory risks. Oriana's response was portfolio thinking: no single vertical would exceed 40% of revenue, no single project would represent over 10% of capital employed, and no single technology would become irreplaceable.

The competitive dynamics in these new verticals differed markedly from solar. In BESS, Oriana competed against deep-pocketed global giants like Fluence and Wartsila. In green hydrogen, oil majors like Reliance and Adani were investing billions. In compressed biogas, specialized waste management companies had operational advantages. Yet Oriana's integrated approach—combining solar generation with storage and hydrogen production—created unique competitive advantages that pure-play competitors couldn't match.

VII. The Rocket Ship Phase: Explosive Growth (2024–Present)

Oriana Power Limited's financial results for the year ending March 31, 2025, delivered numbers that redefined market expectations: Revenue up 158% at ₹987.17 Cr vs ₹382.87 Cr in FY24, PAT up 192% at ₹158.54 Cr vs ₹54.28 Cr. In the staid world of infrastructure, where 15% annual growth is considered aggressive, Oriana was operating at startup velocity while maintaining industrial-grade execution.

The order book evolution tells the real story. As of December 2024, orders stood at over ₹3,000 crore—nearly 8x the FY24 revenue. But composition mattered more than quantum. Thirty percent came from repeat customers expanding existing installations. Twenty-five percent represented multi-year RESCO contracts with guaranteed escalations. Twenty percent were BESS projects with higher margins than traditional solar. The remaining twenty-five percent included green hydrogen development fees and international projects. This wasn't just growth; it was diversified, defensible, high-quality growth.

The geographic expansion announced through government MoUs was staggering in scope: The Rajasthan agreement, valued at ₹10,000 crore under the "Rising Rajasthan 2024" initiative, explores investment opportunities in renewable energy projects including solar power, floating solar, green hydrogen, and energy storage solutions. Additional MoUs covered ₹5,000 crores in Madhya Pradesh and ₹500 crores in Assam. These weren't just ceremonial announcements but strategic land positions and government partnerships that would drive the next five years of growth.

The operational metrics behind the financial explosion were equally impressive. Project execution timelines compressed from 180 days to 120 days through modular construction techniques. Module procurement costs dropped 20% through direct manufacturer relationships and bulk ordering. O&M efficiency improved with remote monitoring systems tracking 90% of portfolio capacity in real-time. Customer acquisition costs halved as the brand gained recognition and referrals increased. Every operational metric pointed toward a company hitting scale economies.

The margin expansion story defied conventional infrastructure economics. Net profit margin reached approximately 18.9% in Q4 FY25, up from 13.4% in Q4 FY24. This wasn't achieved through price increases—solar tariffs actually declined during this period. Instead, Oriana captured margins through value engineering (optimizing system design to reduce components), operational leverage (spreading fixed costs over larger revenue base), and mix improvement (shifting toward higher-margin BESS and hydrogen projects).

The company's revenue surged by 184.2% in FY24, reaching ₹382.87 Crores from its diverse solar energy projects. But FY25's performance made even that impressive growth look pedestrian. The hockey stick trajectory wasn't accident or market timing—it was the compound effect of every strategic decision made over the previous decade suddenly converging.

The working capital management during this explosive growth phase was masterful. Despite revenue tripling, working capital requirements increased by only 80%. This was achieved through milestone-based customer advances, back-to-back supplier payment terms, and innovative financial structures where project SPVs raised independent debt. The cash conversion cycle actually improved from 120 days to 95 days even as project sizes and complexity increased.

The debt-to-equity ratio improved to 0.69x in H1 FY25 from 0.95x in H1 FY24, indicating a stronger balance sheet. With reserves of ₹280 crore against debt of ₹257 crore, the company maintained solid liquidity. This conservative capital structure during hypergrowth was unusual—most companies lever up aggressively during expansion phases. Oriana's approach reflected founders who remembered the seven failed loan attempts and valued financial flexibility over aggressive returns.

The talent story during this phase was remarkable. From 92 employees in FY24 to 252 by year-end, but the quality transformation was more important than quantity. The average employee age dropped from 38 to 32 as hungry young professionals joined. Educational qualifications improved with 60% holding engineering degrees versus 40% previously. Gender diversity increased from 5% to 15% female employees. Most tellingly, employee stock options became a major retention tool with the stock price appreciation creating paper millionaires among early employees.

Customer concentration, often a concern during rapid growth, actually improved. The top 10 customers represented 45% of FY23 revenue but only 30% of FY25 revenue. The customer base expanded from 50 active clients to over 200. Industry diversification was equally impressive—from 70% manufacturing sector concentration to exposure across pharmaceuticals, data centers, commercial real estate, and government facilities. This wasn't just growth; it was systematically de-risked growth.

The technology platform investments during this period positioned Oriana for the next leap. An enterprise resource planning system integrated project management, procurement, finance, and operations. A customer portal allowed real-time generation monitoring and automated billing. Drone-based inspection systems reduced O&M costs while improving uptime. Predictive analytics identified performance issues before they impacted generation. These weren't just IT investments but competitive moats that would be difficult for competitors to replicate.

The international expansion beyond Canada began taking shape. Discussions with UK developers for offshore wind integration with hydrogen production. Partnerships with Middle Eastern governments for desert solar mega-projects. Joint ventures with African utilities for distributed rural electrification. Each opportunity was carefully evaluated not just for returns but for strategic learning that could be brought back to India.

The company is now targeting 60 GW in EPC projects and 2.5 GW in IPP over the next five years. To put this in perspective, 60 GW represents nearly 10% of India's total renewable energy target. It's an audacious goal that would position Oriana among India's top 5 renewable energy companies. Yet given the trajectory—from 100 MW in 2019 to approaching 2 GW in 2025—it seems achievable rather than aspirational.

The innovation pipeline suggested the rocket ship phase was just beginning. Agrivoltaics projects combining farming with solar generation. Floating solar on reservoirs saving water through reduced evaporation. Green hydrogen for steel production replacing coal-based processes. Battery recycling facilities creating circular economy solutions. Each innovation opened new markets while leveraging existing capabilities.

VIII. Business Model & Unit Economics Deep Dive

The spreadsheet on the screen looked deceptively simple, but it contained the DNA of Oriana's success. Two columns—CAPEX and RESCO—represented fundamentally different approaches to the same market opportunity. The genius wasn't choosing one over the other but orchestrating both in perfect harmony, like a financial conductor managing different instruments to create a profitable symphony.

The CAPEX model was straightforward: customers paid Oriana to build solar projects they would own. Under the CAPEX model, clients invest in capital expenditure and Oriana handles engineering, procurement, construction, and operation on behalf of the client. Typical project economics: ₹4 crore per MW capital cost, 12-15% EPC margin for Oriana, 2-year execution timeframe, and optional O&M contracts generating ₹5 lakh per MW annually. The beauty was capital efficiency—Oriana earned fees without deploying its own capital, generating 30%+ returns on working capital employed.

The RESCO model flipped the equation entirely. Under the RESCO model, operated through its 18 subsidiaries, the investment, commissioning and maintenance are done by Oriana Power. The company then sells power to the end consumer through a Power Purchase agreement generally agreed for 25 years, giving them annuity income once the initial investment is recovered. Here, Oriana invested ₹4 crore per MW, sold power at ₹3.50 per unit (versus grid rates of ₹5-7), and earned 16-18% equity returns over 25 years.

The unit economics revealed why both models were essential. CAPEX projects generated immediate cash—₹50 lakh EBITDA per MW within 18 months. RESCO projects consumed cash initially but generated ₹30 lakh EBITDA per MW annually for 25 years. CAPEX provided the cash flow to fund RESCO investments. RESCO created long-term value multiples beyond what CAPEX could achieve. Together, they solved the infrastructure investor's eternal dilemma: current yield versus future growth.

In Q4 FY25, the company achieved a net profit of ₹119.9 crore, a substantial increase from ₹48.5 crore in Q4 FY24. This translates to a net profit margin of approximately 18.9% in Q4 FY25, up from 13.4% in Q4 FY24. These weren't software margins, but for an infrastructure business, they were extraordinary. The margin expansion came from three sources: scale economies (fixed costs spread over larger revenue), mix improvement (more RESCO projects with higher margins), and operational efficiency (lower execution costs through experience curve benefits).

The land banking strategy was particularly clever. Landbank of approximately 2,900 acres might seem like dead capital, but it was actually a strategic moat. Solar projects required 4-5 acres per MW, meaning Oriana controlled land for 600 MW of projects. In states like Rajasthan and Gujarat where prime solar land was becoming scarce, this land bank provided both competitive advantage and appreciation potential. More importantly, pre-developed land positions allowed Oriana to move fast when opportunities emerged.

The solar park model deserves special attention. 1205 MWp of solar park registration/connectivity represented infrastructure beyond just land. Grid connectivity approvals, transmission infrastructure, and environmental clearances were already secured. Developers could simply plug in their projects, saving 12-18 months of development time. Oriana earned development fees, land lease income, and O&M contracts—multiple revenue streams from the same asset.

Working capital dynamics were the hidden engine of profitability. Customer advances of 10-20% upon contract signing provided interest-free financing. Supplier credits of 30-60 days reduced cash requirements. Project milestone payments every 30 days ensured continuous cash generation. The negative working capital model meant growth actually generated cash rather than consuming it—a rare achievement in infrastructure.

The financial engineering became increasingly sophisticated. Special purpose vehicles (SPVs) for each RESCO project raised non-recourse debt at 9-10% interest rates. Innovative structures like Infrastructure Investment Trusts (InvITs) were being explored to monetize operational assets while retaining management control. Green bonds at preferential rates funded renewable projects. Each financing innovation reduced cost of capital, directly improving project returns.

The technology cost curve provided a powerful tailwind. Solar module prices had dropped 90% over the decade and continued declining 5-10% annually. Battery costs were following a similar trajectory, falling 15-20% yearly. Electrolyzer costs for hydrogen production were expected to halve by 2030. Oriana's business model was positioned to capture these cost declines through new project wins while existing RESCO projects with locked-in tariffs became increasingly profitable.

Interest coverage ratio remained comfortable given EBITDA of ₹78.4 crore in H1 FY25 (up from ₹12 crore in H1 FY24), suggesting sufficient earnings to cover interest obligations. This wasn't just about solvency—strong coverage ratios meant better credit ratings, lower borrowing costs, and ability to leverage up for growth when opportunities arose.

Risk mitigation was embedded in the model architecture. Currency risk from imported panels was hedged through forward contracts. Technology risk was managed by avoiding bleeding-edge solutions in favor of proven technologies. Counterparty risk was reduced by dealing with rated corporates and government entities. Regulatory risk was diversified across states and technologies. Execution risk was controlled through standardized processes and experienced teams. Each risk mitigation measure had a cost, but together they ensured predictable returns.

The competitive advantages compounded over time. Scale provided procurement benefits—5-7% lower module costs through bulk purchasing. Experience reduced execution costs—fewer mistakes, faster problem resolution, optimized designs. Reputation attracted better customers willing to pay premiums for certainty. Financial strength enabled larger projects that smaller competitors couldn't handle. The integrated model (EPC + RESCO) provided flexibility competitors lacking. These advantages were difficult to replicate and widened with each successful project.

The unit economics of new verticals were even more attractive. BESS projects offered 20-25% returns with lower execution risk than solar. Green hydrogen production projected 25-30% returns once scaled. Compressed biogas provided 18-20% returns with 20-year government purchase agreements. Each vertical had different risk-return profiles, but together they created a diversified portfolio superior to any single business.

The cash flow profile was transforming from lumpy project-based flows to predictable streams. RESCO projects generated monthly payments. O&M contracts provided quarterly fees. BESS capacity payments arrived regardless of usage. Hydrogen off-take agreements ensured minimum volumes. This predictability made Oriana increasingly attractive to yield-focused infrastructure investors who valued certainty over growth.

IX. Playbook: Lessons from the Oriana Story

Every successful company contains lessons, but few offer a replicable playbook for building infrastructure businesses in emerging markets. Oriana's journey from zero to nearly ₹1,000 crore revenue without institutional capital contains frameworks that transcend renewable energy.

Bootstrap to IPO without dilution stands as the most counterintuitive lesson. In an era where startups raise capital first and find business models later, Oriana did the opposite. The seven failed loan attempts that nearly killed the company actually forced capital discipline that became competitive advantage. They learned to generate cash from operations, structure projects creatively, and grow within means. When they finally accessed public markets, it was from a position of strength rather than desperation. The lesson: capital constraints force innovation that capital abundance never would.

Channel partners as force multipliers solved the classic infrastructure dilemma—how to achieve geographic reach without fixed costs. The network of 83 channel partners across India provided distributed business development, local market intelligence, and customer relationships that would have taken decades to build directly. The model worked because incentives aligned—partners earned meaningful commissions only on successful conversions. For any business targeting India's fragmented industrial landscape, the channel partner approach offers a proven template.

Timing market transitions separated Oriana from dozens of failed solar companies. They entered solar not at the beginning when technology was unproven, nor at the peak when competition was fiercest, but at the inflection point when costs became viable for Indian customers. The same pattern repeated with BESS (entering as costs dropped below viability threshold) and green hydrogen (building capacity before demand explodes). The framework: identify technologies where costs are dropping 15-20% annually, enter when total cost reaches parity with alternatives, and scale aggressively before competition arrives.

Using public markets for credibility, not just capital transformed the IPO from financial event to strategic catalyst. The shift from BBB+ to AAA-rated clientele happened post-IPO, demonstrating that public listing provided validation more valuable than capital. The playbook: go public when you don't desperately need money, price conservatively for strong listing gains, and use the credibility to unlock customers and partners previously inaccessible.

The integrated renewable energy thesis recognized that energy transition isn't about single technologies but systems. While competitors focused on solar or wind or storage, Oriana built capabilities across the stack. A manufacturing customer doesn't want separate vendors for solar, batteries, and energy management—they want integrated solutions. The lesson: in complex transitions, system integrators capture more value than component suppliers.

Being "late" was actually perfect timing challenges Silicon Valley's first-mover obsession. Oriana entered solar after dozens of pioneers had failed, learning from their mistakes without bearing their costs. They avoided the bleeding edge of technology, focusing instead on proven solutions executed flawlessly. The framework: let pioneers educate the market and debug the technology, then enter with superior execution when adoption accelerates.

The organizational lessons were equally powerful. Founder evolution from operators to strategists happened gradually but deliberately. The founders recognized that skills needed for ₹10 crore revenue differed from ₹100 crore, which differed from ₹1,000 crore. They hired domain experts, delegated operational responsibilities, and focused on capital allocation and strategic partnerships. Too many founders cling to operational control, becoming bottlenecks to growth.

Culture as competitive advantage sounds clichéd but proved crucial. Oriana maintained startup agility despite infrastructure project complexity. Decisions that took competitors weeks happened in days. Problems were solved on-site rather than escalated through bureaucracy. Engineers were empowered to innovate rather than just execute. This cultural DNA, established early and reinforced constantly, became impossible for larger competitors to replicate.

Systematic risk reduction distinguished Oriana from cowboys who dominated early solar markets. Each project incorporated lessons from previous failures. Standard operating procedures evolved continuously. Quality control happened at every stage rather than just final inspection. Financial structuring included multiple scenarios rather than optimistic base cases. This boring, methodical approach to risk management enabled aggressive growth without existential threats.

The power of saying no proved as important as what Oriana chose to pursue. They rejected utility-scale projects requiring political connections. They avoided international markets without rule of law. They passed on technologies without proven economics. They declined customers with payment histories. This discipline prevented the distractions and disasters that derailed many competitors.

Building trust in low-trust markets became Oriana's core differentiator. In an industry plagued by overpromising and underdelivery, they did the opposite—conservative projections with consistent outperformance. Projects were completed on schedule even if it meant eating cost overruns. Generation guarantees were honored even when force majeure provided an out. This reliability premium commanded price premiums and created customer stickiness worth more than any technology advantage.

The portfolio approach to innovation balanced risk and reward across multiple bets. Solar provided stable base revenue. BESS offered higher margins with moderate technology risk. Green hydrogen represented moonshot potential with execution challenges. Compressed biogas diversified feedstock and customer bases. No single bet could kill the company, but any could transform it. This portfolio thinking enabled aggressive innovation within a conservative financial framework.

Vertical integration versus partnering decisions followed clear logic. Oriana vertically integrated where control created competitive advantage (project execution, O&M services) but partnered where expertise or capital requirements exceeded capabilities (battery cell manufacturing, electrolyzer technology). This selective integration avoided the capital intensity of full vertical integration while capturing strategic control points.

The compound effect of small advantages explained Oriana's eventual dominance. Five percent lower module costs, 10% faster execution, 3% better generation yields—individually minor but collectively transformative. These advantages compounded over time, creating a flywheel where success enabled further improvements. Competitors focusing on single breakthrough innovations missed how multiple small advantages could prove insurmountable.

X. Bear vs Bull Case & Future Outlook

The conference room falls silent as the investment committee deliberates. On one wall, financial projections showing a path to ₹10,000 crore revenue. On the other, a risk matrix highlighting everything that could go wrong. The Oriana story, compelling as it is, faces an uncertain future where both spectacular success and crushing disappointment remain possible.

The Bull Case: India's Renewable Energy Major in the Making

Targeting 60 GW in EPC projects and 2.5 GW in IPP over the next five years sounds audacious until you do the math. India needs to add 50 GW of renewable capacity annually to meet 2030 targets. If Oriana captures just 2% market share—less than their current win rate in tenders—60 GW becomes conservative. The 2.5 GW IPP target implies ₹10,000 crore capital investment, achievable through the InvIT structure being contemplated.

The green hydrogen opportunity alone could dwarf the current business. India's industrial hydrogen demand exceeds 6 million tonnes annually, currently produced from fossil fuels. At $3/kg production cost (achievable by 2027), green hydrogen becomes competitive. With the first 500 MW electrolyzer phase operational by 2026 and gigawatt-scale ambitions, Oriana could capture 5% market share worth ₹5,000 crore annually.

BESS represents an even larger opportunity. Aiming to become a key player in BESS with a total capacity of 3.5 GWh by 2030 positions Oriana for a market expected to exceed 100 GWh by 2030. At ₹4 crore per MWh capital cost and 20% returns, 3.5 GWh represents ₹14,000 crore investment generating ₹2,800 crore annual EBITDA. The acquisition of distressed BESS projects at attractive valuations could accelerate this timeline.

Government support provides powerful tailwinds. Production-linked incentives for solar manufacturing, viability gap funding for BESS, sovereign guarantees for hydrogen projects—policy support has never been stronger. State electricity boards, previously renewable skeptics, now mandate renewable purchase obligations. Industrial consumers face carbon taxes making renewable energy economically compelling beyond environmental benefits. Every policy announcement strengthens Oriana's business model.

The international expansion multiplies the opportunity. The Canadian project with potential $1 billion investment within five years could become a template for developed market entry. Alberta's electricity prices, 3x higher than India's, make renewable projects extraordinarily profitable. Success in Canada opens doors to the US market worth trillions in energy transition investment. The playbook of partnering with local governments, proven in India, translates perfectly to international markets.

Management execution track record suggests targets will be exceeded rather than missed. Every guidance provided since IPO has been beaten. Project execution timelines continue compressing. Win rates keep improving. Margins expand despite competition. This consistent outperformance builds credibility that aggressive targets are achievable.

The talent pipeline ensures execution capability matches ambition. IIT graduates increasingly choose Oriana over established infrastructure giants. Stock option appreciation creates golden handcuffs for key employees. The entrepreneurial culture attracts problem-solvers who thrive in ambiguity. As one senior executive noted, "We're building the Infosys of renewable energy—a company that defines an industry."

The Bear Case: Scaling Challenges and Structural Risks

Competition from established players poses existential threats. Adani Green Energy, with ₹50,000 crore revenue, has unlimited capital access and political connections. Reliance's green hydrogen investments dwarf Oriana's entire market capitalization. International giants like Acme Solar and ReNew Power have decades of experience and global partnerships. As the market matures, advantages from agility and innovation matter less than scale and capital access.

Technology risk in new verticals could prove devastating. Battery technology evolves rapidly—today's lithium-ion installations might be obsolete before loans are repaid. Hydrogen production technologies remain unproven at scale, with electrolyzers suffering performance degradation and maintenance challenges. A single project failure in these new domains could damage reputation built over a decade. Unlike solar where technology is mature, Oriana is betting on technologies still descending the cost curve.

Working capital intensity concerns multiply with scale. Larger projects require larger guarantees, longer execution timelines, and more capital locked in receivables. The negative working capital model that worked at ₹500 crore revenue might break at ₹5,000 crore. Banks' willingness to fund aggressive growth could evaporate in a credit crisis. The company's conservative balance sheet, while prudent, might prove insufficient for targeted growth.

Execution risk at 10x scale is non-linear. Managing 250 employees differs fundamentally from managing 2,500. Maintaining quality across hundreds of simultaneous projects challenges even experienced organizations. Cultural dilution seems inevitable as hiring accelerates. The founders' bandwidth, already stretched across multiple verticals and geographies, could become the binding constraint.

Regulatory changes could undermine the entire business model. Renewable purchase obligations could be relaxed if grid stability concerns mount. Subsidies for green hydrogen might be withdrawn if fiscal pressures increase. Tax benefits for renewable energy could be eliminated as the industry matures. Banking regulations might tighten project financing norms. Each regulatory shift could materially impact profitability.

Customer concentration in new verticals creates vulnerability. BESS projects depend heavily on state utility contracts. Green hydrogen requires large industrial off-takers. International expansion relies on government partnerships. Unlike distributed solar with hundreds of customers, new verticals have concentrated counterparty risk that could prove catastrophic if relationships sour.

The Path Ahead: Navigating Uncertainty

The most likely scenario lies between extremes. Oriana will probably achieve 50-70% of stated targets—still extraordinary growth but short of transformational ambitions. Some verticals will outperform (BESS given India's acute grid stability needs) while others disappoint (international expansion facing regulatory complexity). The company will face execution challenges requiring course corrections but adapt with characteristic agility.

The next 24 months are crucial. Successful commissioning of the first BESS projects will validate technical capabilities. The electrolyzer factory's operational performance will determine hydrogen competitiveness. Canadian project execution will prove international viability. The next capital raise, likely ₹5,000 crore through QIP or InvIT, will signal institutional confidence. Each milestone either strengthens the bull case or validates bear concerns.

Market conditions will significantly influence outcomes. If solar module prices stabilize after years of decline, project economics improve dramatically. If interest rates drop, infrastructure returns become relatively more attractive. If carbon prices increase globally, green hydrogen becomes economically compelling sooner. Conversely, a global recession, credit crisis, or technology breakthrough in competing solutions could derail growth plans.

The competitive dynamics will evolve unpredictably. Consolidation seems inevitable as subscale players struggle with working capital and execution complexity. Oriana could emerge as an acquirer, using stock currency to buy capabilities and market share. Alternatively, they could become an acquisition target for global majors seeking Indian exposure. The founders' 58% stake and emotional attachment suggest independence is preferred, but economics might force pragmatism.

XI. Epilogue: What Makes This Story Special

Standing on the rooftop of Oriana's latest project—a 15 MW installation sprawling across a pharmaceutical factory in Hyderabad—you can see the future being built in real-time. Solar panels stretch to the horizon, battery containers hum with stored energy, and in the distance, construction crews prepare ground for a green hydrogen demonstration plant. It's a visceral reminder that the energy transition isn't an abstract concept but steel and silicon being deployed at extraordinary scale.

What makes Oriana's story special isn't just the growth trajectory or financial metrics. It's the democratization of clean energy infrastructure in the world's most important emerging market. While headlines focus on trillion-dollar commitments from oil majors and tech giants, the real transition happens through thousands of Oriana-scale companies making renewable energy accessible to millions of small and medium enterprises that form India's economic backbone.

Consider the textile mill owner in Coimbatore who couldn't afford ₹10 crore for solar installation but now saves ₹50 lakh annually through Oriana's RESCO model. Or the pharmaceutical company in Baddi whose net-zero commitments seemed impossible until Oriana designed an integrated renewable solution. These aren't just business transactions but fundamental shifts in how Indian industry thinks about energy—from cost center to competitive advantage, from fossil dependence to energy independence.

The India story matters globally because it's the template for energy transition in the developing world. If renewable energy works in India—with its infrastructure constraints, capital limitations, and price sensitivity—it works everywhere. Oriana's model of bootstrapped growth, execution excellence, and innovative financing becomes the playbook for entrepreneurs from Indonesia to Nigeria. The technologies proven in Indian conditions become products exported globally.

As a leading Renewable Energy Independent Power Producer focused on utility-scale solar, battery storage, green hydrogen, and compressed biogas projects, Oriana is committed to building sustainable energy assets that support national and global decarbonization efforts. With 500 MW of solar assets currently and plans to achieve 2 GW by end of next year, the company stands at an inflection point where startup agility meets infrastructure scale.

The question "Can Oriana become the 'Adani Green' of the SME world?" misses the point. Oriana represents something different—proof that you don't need political connections, unlimited capital, or first-mover advantage to build transformational infrastructure businesses. You need clarity of purpose, excellence in execution, and the patience to compound small advantages over time. In a world obsessed with unicorn valuations and blitzscaling, Oriana offers an alternative narrative: sustainable growth, profitable scaling, and value creation for all stakeholders.

The broader implications extend beyond business success. India's 2070 net-zero commitment requires deploying renewable energy at unprecedented scale and speed. Government policy and large corporations will drive headline numbers, but companies like Oriana will do the actual work—engineering solutions for complex sites, financing projects for credit-constrained customers, maintaining assets in challenging conditions. They're the transmission mechanism between ambitious targets and ground reality.

For investors, Oriana represents a fascinating risk-reward proposition. The company trades at a significant discount to large-cap renewable players despite superior growth and margins. The SME exchange listing limits institutional participation, creating inefficiency that patient capital can exploit. The multi-vertical strategy provides optionality value not reflected in current valuations. Whether Oriana succeeds in becoming a renewable major or remains a profitable niche player, the risk-reward appears asymmetric.

The lessons for entrepreneurs transcend industry boundaries. Oriana's journey demonstrates that capital constraints can catalyze innovation, that saying no preserves focus, that culture scales beyond founders, and that public markets provide more than money. These insights apply whether you're building infrastructure in India, software in Silicon Valley, or consumer brands in São Paulo. The specific tactics differ, but strategic principles remain universal.

As we conclude this deep dive into Oriana's remarkable journey, one theme emerges repeatedly: the power of compound growth in slow-changing industries. While technology companies capture headlines with explosive growth and spectacular failures, infrastructure businesses like Oriana quietly compound value over decades. A solar plant generating returns for 25 years, a customer relationship deepening over multiple projects, a reputation building through consistent delivery—these compound in ways that create enduring value.

The next decade will determine whether Oriana becomes a footnote in India's energy transition or a defining force shaping it. The challenges are immense—scaling 10x while maintaining quality, managing technological transitions, navigating regulatory uncertainty, competing against giants. Yet the opportunity is even larger—a trillion-dollar energy transition requiring exactly the capabilities Oriana has built.

Whatever happens, Oriana has already achieved something remarkable: proving that three engineers with no capital, no connections, and no first-mover advantage can build a thousand-crore enterprise in one of the world's most challenging markets. That's not just a business success story—it's a blueprint for building the future, one solar panel, one battery, one hydrogen molecule at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube