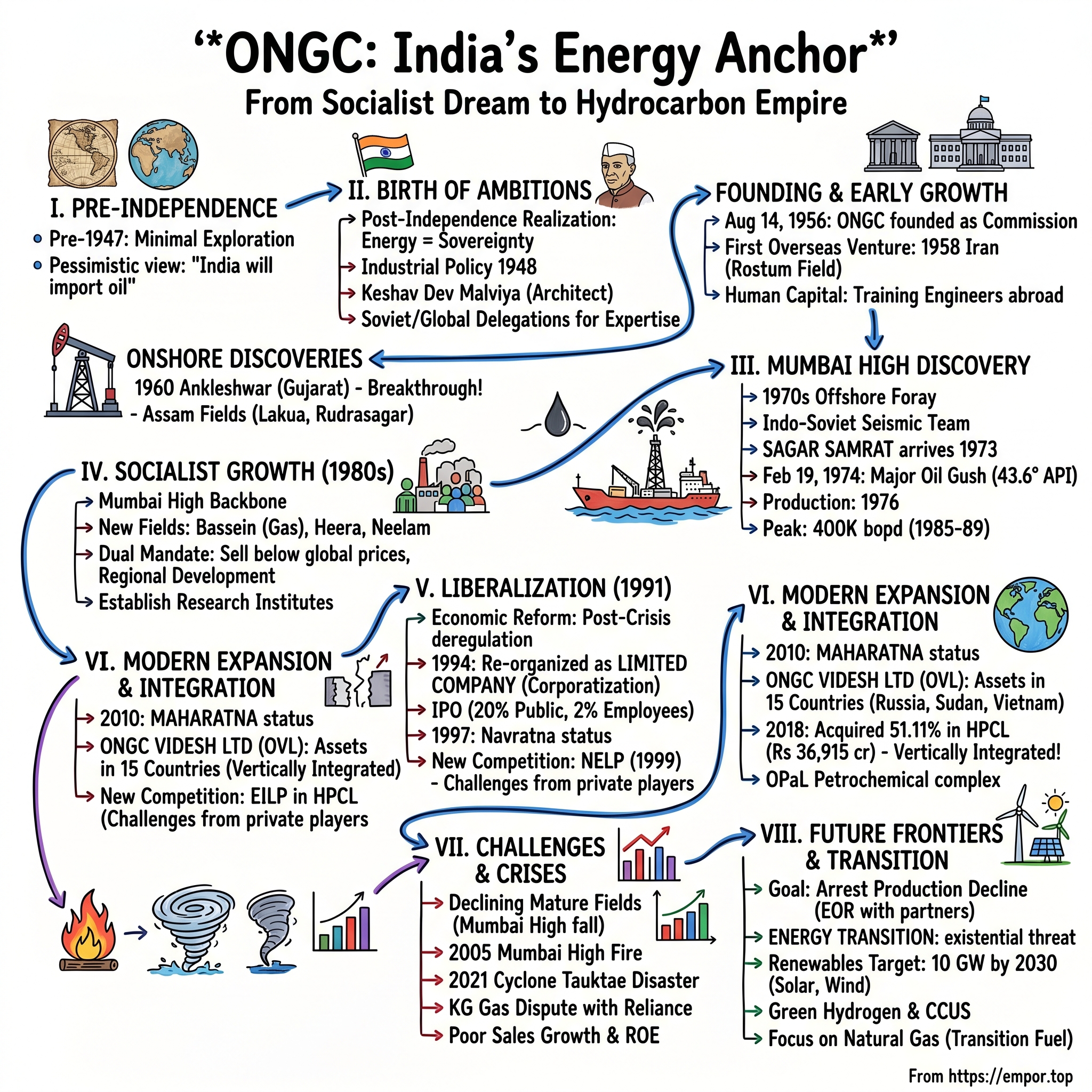

ONGC: India's Energy Anchor - From Socialist Dream to Hydrocarbon Empire

I. Introduction & Cold Open

Picture this: A company that produces 70% of India's crude oil and around 84% of its natural gas. A behemoth that discovered 7 out of the 8 producing Indian Basins, fundamentally transforming a nation's energy landscape. This is the story of Oil and Natural Gas Corporation Limited – ONGC – India's energy anchor and one of the most consequential companies in the country's post-independence history.

How did a government commission, born during India's socialist era amid skepticism about the country's hydrocarbon potential, discover Mumbai High and become the foundation of India's energy security? It's a tale that weaves together geopolitics, nation-building, technological ambition, and the eternal tension between state ownership and commercial imperatives.

The stakes couldn't be higher. In a world where energy security equals national security, where oil prices can topple governments and shape foreign policy, ONGC stands as India's shield against global energy volatility. Yet today, this Maharatna PSU faces unprecedented challenges: declining production from aging fields, the global energy transition threatening fossil fuels, and persistent questions about whether state ownership helps or hinders its potential.

What makes ONGC's journey particularly fascinating is how it mirrors India's own economic evolution – from closed socialist economy to liberalized market, from import dependence to self-reliance ambitions, from domestic focus to global aspirations. This is not just a corporate story; it's the story of modern India told through the lens of black gold.

II. Pre-Independence & The Birth of a Nation's Energy Ambitions

The story of ONGC begins long before its official founding, in the twilight of British rule. Before independence in 1947, the Assam Oil Company in the north-eastern and Attock Oil Company in the north-western part of the undivided India were the only oil-producing companies, with minimal exploration input. The major part of Indian sedimentary basins was deemed to be unfit for the development of oil and gas resources.

This pessimistic assessment would haunt India's energy planners for years. The conventional wisdom among foreign experts was clear: India was destined to be an oil importer. The geological surveys conducted during the colonial period had written off vast swathes of the subcontinent as barren of hydrocarbons. Only the fields in Assam, discovered in 1889, and some scattered operations in what would become Pakistan, showed any promise.

But independence brought with it new dreams and urgent necessities. After independence, the Central Government of India realized the importance of oil and gas for rapid industrial development and its strategic role in defence. Consequently, while framing the Industrial Policy Statement of 1948, the development of the petroleum industry in the country was considered to be of utmost necessity.

The geopolitical context of the early 1950s made this realization even more acute. The Cold War was heating up, and newly independent nations were learning that energy independence was inseparable from political independence. India watched as Iran nationalized its oil industry in 1951, triggering an international crisis. The message was clear: control over energy resources was fundamental to sovereignty.

Enter Keshav Dev Malviya, a visionary who would become the architect of India's hydrocarbon dreams. A delegation under the leadership of Mr. K D Malviya, the then Minister of Natural Resources, visited several countries to study the oil industry and to facilitate the training of Indian professionals for exploring potential oil and gas reserves.

Malviya's global tour was eye-opening. He saw how the Soviet Union had built a massive oil industry from scratch, how Romania had developed indigenous capabilities, and how even small nations were asserting control over their energy resources. But he also understood that India needed technical expertise it simply didn't possess.

Foreign experts from USA, West Germany, Romania and erstwhile USSR visited India and helped the government with their expertise. Finally, the visiting Soviet experts drew up a detailed plan for geological and geophysical surveys and drilling operations to be carried out in the 2nd Five Year Plan (1956-57 to 1960-61).

The Soviet involvement was particularly significant. Unlike Western oil companies that demanded concessions and profit-sharing agreements, the Soviets offered technical assistance with no strings attached – a model that appealed to Nehru's non-aligned, socialist vision. They brought with them not just drilling rigs and seismic equipment, but a fundamentally different philosophy: that a nation could and should control its own energy destiny.

This period also saw the beginning of India's human capital development in the oil sector. Young Indian geologists and engineers were sent to the Soviet Union, Romania, and other countries for training. These would become the first generation of ONGC's technical leadership – men and women who carried the dual burden of technical excellence and nation-building.

In April 1956, the Government of India adopted the Industrial Policy Resolution, which placed mineral oil industry amongst the Schedule 'A' industries, the future development of which was to be the sole and exclusive responsibility of the state.

This decision was momentous. It meant that unlike many other developing nations that would rely on international oil companies for exploration and production, India would build its own capabilities. It was an audacious gambit – a poor, newly independent nation deciding it could master one of the world's most capital and technology-intensive industries.

The philosophical underpinnings of this decision went beyond mere economics. For Nehru and the early planners, oil was too important to be left to private profit. It was the lifeblood of industrialization, the fuel of defense, the foundation of modern life. In their socialist worldview, such a critical resource had to be under public control, managed for national benefit rather than private gain.

III. Foundation Years: From Directorate to Commission (1955-1965)

The formal beginning of ONGC's journey started modestly. Pandit Nehru reposed faith in Shri Keshav Dev Malviya who laid the foundation of ONGC in the form of Oil and Gas division, under Geological Survey of India, in 1955. A few months later, it was converted into an Oil and Natural Gas Directorate.

But it quickly became apparent that a mere directorate, buried within the government bureaucracy, wouldn't have the autonomy or authority needed for such an ambitious undertaking. Soon, after the formation of the Oil and Natural Gas Directorate, it became apparent that it would not be possible for the Directorate with its limited financial and administrative powers as a subordinate office of the Government, to function efficiently. So in August 1956, the Directorate was raised to the status of a commission with enhanced powers, although it continued to be under the government.

It was founded on 14 August 1956 by the Government of India, with the commission being christened Oil & Natural Gas Commission on 14th August 1956. The date itself was symbolic – one day before Independence Day, signifying that energy independence was integral to political independence.

The main functions of the Oil and Natural Gas Commission subject to the provisions of the Act, were "to plan, promote, organize and implement programmes for development of Petroleum Resources and the production and sale of petroleum and petroleum products produced by it, and to perform such other functions as the Central Government may, from time to time, assign to it".

The early years were marked by both excitement and frustration. The commission's geologists and engineers, many fresh from training abroad, were eager to prove the skeptics wrong. They began systematic exploration in sedimentary basins across India, from the deserts of Rajasthan to the coasts of Gujarat, from the Gangetic plains to the Cauvery basin.

The Cambay basin in Gujarat yielded the first major success. In the inland areas, ONGC not only found new resources in Assam but also established new oil province in Cambay basin (Gujarat), while adding new petroliferous areas in the Assam-Arakan Fold Belt and East coast basins (both onshore and offshore). The discovery of oil in Ankleshwar in 1960 was a watershed moment – it proved that India had hydrocarbon resources beyond the traditional fields of Assam.

But perhaps the most intriguing early venture was ONGC's first overseas foray, which happened much earlier than most people realize. In 1958 the then Chairman, Keshav Dev Malaviya, held a meeting with some geologists in the Mussoorie office of the Geology Directorate where he accepted the need for ONGC to go outside India too in order to enhance Indian owned capacity for oil production. The argument in support for this step, by LP Mathur and BS Negi, was that Indian demand for crude would go up at a faster rate than discoveries by ONGC in India. Malaviya followed this up by making ONGC apply for exploration licences in the Persian Gulf. Iran gave ONGC four blocks and Malaviya visited Milan and Bartlesville, Oklahoma to request ENI and Phillips Petroleum to join as partners in the Iran venture.

This resulted in the discovery of the Rostum oilfield in the early 'sixties, very soon after the discovery of Ankleshwar in Gujarat. This was the very first investment by the Indian public sector in foreign countries and oil from Rostum and Raksh was brought to Cochin where it was refined in a refinery built with technical assistance.

This early international venture, largely forgotten today, reveals the ambitious vision of ONGC's founders. Even as they struggled to explore India's basins with limited resources and technology, they were already thinking globally. The Rostum discovery was particularly sweet – Indian geologists had found oil abroad even as foreign experts continued to doubt India's domestic potential.

Meanwhile, domestic exploration continued to yield results. In 1963, ONGC discovered oil and gas sites in Sivasagar district and established oilfields in Lakua, Gelekey, and Rudrasagar. Each discovery was celebrated as a national achievement, front-page news that gave Indians confidence that their country could achieve energy self-sufficiency.

The transformation from directorate to commission and then to a statutory body in October 1959 reflected the growing importance and success of the organization. In October 1959, the commission was converted into a statutory body by an act of the Indian Parliament, which enhanced powers of the commission further.

By 1965, ONGC had established itself as a credible exploration and production company. It had discovered new oil provinces, built indigenous capabilities, and even ventured overseas. The commission employed thousands of Indians – geologists, engineers, drillers, technicians – creating India's first generation of oil and gas professionals.

Nehru himself acknowledged this achievement. "Not only had India..set up her own machinery for oil exploration and exploitation... an efficient oil commission had been built where a large number of bright young men and women had been trained and they were doing good work" said Pandit JawaharLal Nehru, India's first Prime Minister to Lord Mountbatten, on ONGC in 1959.

Yet all these achievements would pale in comparison to what was about to come. ONGC's engineers and geologists had begun to look offshore, inspired by global trends and new technologies. The Arabian Sea beckoned, vast and unexplored. What they would find there would transform not just ONGC, but India itself.

IV. The Mumbai High Discovery: India's Oil Revolution (1970-1980)

ONGC went offshore in early 70's and discovered a giant oil field in the form of Bombay High, now known as Mumbai High. This simple sentence barely captures the drama, the technological audacity, and the transformative impact of what would become India's most important oil discovery.

The story begins in the mid-1960s with an unlikely collaboration. Mumbai High field was discovered by an Indo-Soviet team operating from the seismic exploration vessel Academic Arkhangelsky during mapping of the Gulf of Khambhat (earlier Cambay) in 1964–67, followed by a detailed survey in 1972. The Academic Arkhangelsky, a Soviet research vessel, represented the continuing technical cooperation between India and the USSR, but more importantly, it brought to India's waters advanced seismic technology that could peer beneath the seabed.

The context of the early 1970s cannot be understated. 1974, the world economy was struggling to come to terms with oil crises arisen out of oil embargo by middle east oil producing nations. The import price of oil hit all time high and countries like India were worst affected due to lack of significant indigenous hydrocarbon resources. The Yom Kippur War of 1973 had triggered the first oil shock, quadrupling prices overnight. For India, which imported most of its oil, this was an economic catastrophe. The country's foreign exchange reserves were depleting rapidly, inflation was soaring, and there was genuine fear about the country's ability to maintain energy supplies.

Against this backdrop of crisis, ONGC, precisely that time, was launching its most ambitious exploration effort in high seas about 90 nautical miles off Mumbai (then Bombay), fingers crossed but spirits high.

The technical challenges were immense. Offshore drilling was still a relatively new technology globally, and for India, it was completely uncharted territory. ONGC had to acquire specialized equipment and train personnel in entirely new skills. The crown jewel of this effort was the Sagar Samrat.

Jack up self-propelled, self-elevating drill ship aptly named Sagar Samrat - The Emperor of Seas, was custom built in Japan for shaping India's offshore foray. The Sagar Samrat was more than just a drilling platform; it was a symbol of India's technological ambitions. Custom-built in Japan's Mitsubishi shipyards, it could operate in waters up to 90 meters deep, its massive legs capable of lifting the entire platform above the highest waves.

Samrat had reached Bombay in May 1973 and thereafter drilled a well at Tarapur structure, without success but enormous learning for the engineers. Sagar Samrat, was next deployed at Well #1 in the Bombay High structure, 160 kilometres from Mumbai.

The drilling operation itself reads like a thriller. On February 3, 1974, the drill string went down to touch the sea bed. The well was "spudded". The term "spudded" – oil industry jargon for beginning to drill – marked the beginning of what everyone hoped would be a historic moment.

The drillers and Geologists were extra careful while drilling. It was well known that the oil and gas bearing zones normally drill faster. The instructions were clear to stop drilling the moment a 'drilling break'- unusually faster drilling speed- is noticed. The zones containing oil or gas would be 2 to 5 metres thick only and could be missed.

The tension on the platform was palpable. Every few meters of drilling could mean the difference between triumph and disappointment. The geologists monitored the drilling mud constantly, looking for traces of hydrocarbons. The drillers watched their gauges, alert for the telltale acceleration that might signal they had hit oil-bearing rock.

Then came the moment of truth. On February 19, 1974, at the break of dawn, the well was opened. Oil gushed out in great force at 500 PSI - that was the pressure of the fluids in the reservoir.

But it wasn't just that they had found oil – it was the quality and pressure that stunned the team. Studies had shown the viability of a big field with that kind of a pressure. Next to be measured was its gravity. It was 43.6 degrees- another astounding parameter. In oil field parlance, 43.6 degrees API was as good as gold.

The discovery's timing couldn't have been more fortuitous. As news of the discovery spread, it provided a massive psychological boost to a nation reeling from the oil crisis. India had found its own oil, and not just any oil – a giant field that could transform the country's energy equation.

The field commenced production in 1976. The speed from discovery to production – just two years – was remarkable, reflecting the urgency of India's energy needs. Mumbai High field reached its peak production rate of 400,000 barrels of oil per day (bopd) in 1985 and continued at the same rate until 1989.

The impact was transformative. As of 2004, it supplied 14% of India's oil requirement and accounted for about 38% of all domestic production. Mumbai High had become the backbone of India's oil production, generating billions of dollars in revenue and saving precious foreign exchange.

The technical achievements were equally impressive. ONGC had to develop entirely new capabilities – offshore platform construction, submarine pipeline laying, helicopter operations for crew changes, supply vessel management, and specialized safety protocols for offshore operations. Each challenge overcome added to India's growing technological confidence.

The field's development also spawned an entire ecosystem. The Bombay High complex eventually grew to include multiple platforms, connected by bridges and pipelines. Mumbai High crude has more than 60% paraffinic content while light Arabian crude has only 25% paraffin. This high-quality crude was particularly valuable, requiring less refining and yielding more valuable products.

But Mumbai High was more than just an oil field. It represented a turning point in India's post-independence history. This discovery, along with subsequent discoveries of huge oil and gas fields in Western offshore changed the oil scenario of the country. The Bassein field, discovered in 1976, added massive gas reserves. The Heera and Neelam fields followed, creating an entire offshore oil province.

The psychological impact cannot be overstated. For a nation that had been told its sedimentary basins were largely barren, Mumbai High was vindication. It proved that Indians could master complex technology, take massive risks, and succeed on a global scale. The sight of the flames from the platforms, visible from Mumbai's shores on clear nights, became a symbol of India's industrial might.

The discovery also shifted India's energy geography. Mumbai, already the country's commercial capital, now became its energy hub. Refineries were expanded, pipelines built, and an entire petroleum economy developed around the western offshore fields. The multiplier effects rippled through the economy – from steel for platforms to helicopters for transportation, from specialized vessels to trained manpower.

Yet even as ONGC celebrated Mumbai High's success, the seeds of future challenges were being sown. The field's prolific production created a sense of complacency. Why explore difficult frontier basins when Mumbai High was gushing oil? Why invest in enhanced recovery when natural flow was so strong? These questions would come back to haunt ONGC decades later.

V. The Socialist Era: Growth Under Government Control (1980-1991)

The 1980s represented ONGC's golden age under the socialist model. Mumbai High was producing at peak capacity, new offshore fields were coming online, and ONGC had established itself as one of India's most successful public sector undertakings. Yet this era also revealed the fundamental tensions between ONGC's commercial objectives and its role as an instrument of government policy.

The expansion of offshore operations during this period was remarkable. Beyond Mumbai High, ONGC developed the Bassein field, which became India's largest gas field, the Neelam field with its light sweet crude, and the Heera field with its complex reservoir structure. Each development pushed ONGC's technical capabilities further, requiring deeper drilling, longer pipelines, and more sophisticated production techniques.

By the mid-1980s, the Mumbai High complex had become one of the most productive offshore regions in the world. The infrastructure was impressive – dozens of platforms connected by bridges, hundreds of kilometers of submarine pipelines, gas processing facilities, and a sophisticated logistics network involving helicopters, supply vessels, and onshore support bases. ONGC had built capabilities that rivaled international oil companies, all with indigenous talent and mostly indigenous technology.

The human story of this period is equally compelling. ONGC employed over 48,000 people by the end of the 1980s, creating not just jobs but entire careers. The company's townships in Dehradun, Mumbai, and other locations became models of public sector efficiency, with schools, hospitals, and recreational facilities that were among the best in India. Working for ONGC carried prestige – it meant job security, good pay, and the satisfaction of serving the nation.

But the socialist model also imposed significant burdens. ONGC was required to sell crude oil and gas at administered prices, well below international rates. The subsidy burden was enormous – ONGC was essentially transferring billions of rupees to oil marketing companies and ultimately to consumers. While this kept inflation in check and made energy affordable, it severely constrained ONGC's ability to invest in exploration and technology.

The company also became an instrument of broader government policy. ONGC was required to explore in frontier areas where the geological prospects were poor but the political imperatives were strong. It had to maintain operations in remote locations as part of the government's regional development agenda. It became a provider of emergency response during natural disasters, a supporter of sports and cultural activities, and a major contributor to various government schemes.

International expansion during this period was limited but significant. ONGC's overseas ambitions, first expressed in the 1960s with the Iran venture, were revived but faced numerous constraints. The government was cautious about allowing precious foreign exchange to be invested abroad. There were also capability constraints – while ONGC had mastered operations in Indian conditions, competing internationally required different skills and risk appetites.

The technology development during this era deserves special mention. ONGC established the Institute of Drilling Technology, the Institute of Reservoir Studies, and other research facilities. It developed indigenous capabilities in seismic data processing, reservoir modeling, and drilling technologies. The Keshava Deva Malviya Institute of Petroleum Exploration in Dehradun became a center of excellence, training not just ONGC employees but petroleum professionals from across the developing world.

Yet by the late 1980s, cracks were beginning to show. Mumbai High's production had plateaued, and despite extensive exploration, no new giant fields were being discovered. The global oil industry was undergoing rapid technological change – 3D seismic, horizontal drilling, deepwater exploration – but ONGC's investment was constrained by the subsidy burden. International oil companies were consolidating and becoming more efficient, while ONGC remained bound by government procedures and bureaucratic decision-making.

The financial performance, while respectable, was far below potential. ONGC was generating massive revenues, but much of it was being siphoned off through administered pricing and dividend payments to the government. The company's reserves were healthy – ₹104.34 billion by the early 1990s – but insufficient for the massive investments needed to maintain production and explore new frontiers.

The debate about ONGC's future was intensifying. Should it remain a government department in all but name, focused on energy security and social objectives? Or should it be freed to operate as a commercial entity, competing with international oil companies on equal terms? This debate would soon be forced by circumstances beyond anyone's control.

VI. Liberalization & Corporatization: The 1991 Turning Point

The year 1991 marked a watershed not just for ONGC but for India itself. The country faced a balance of payments crisis, foreign exchange reserves had dwindled to barely three weeks of imports, and the International Monetary Fund's structural adjustment program demanded fundamental economic reforms. The liberalized economic policy, adopted by the Government of India in July 1991, sought to deregulate and de-license the core sectors (including petroleum sector) with partial disinvestments of government equity in Public Sector Undertakings and other measures.

For ONGC, liberalization presented both an existential challenge and an unprecedented opportunity. The petroleum sector, long considered a strategic government monopoly, was being opened to private and foreign competition. The comfortable certainties of the socialist era were ending.

As a consequence thereof, ONGC was re-organized as a limited Company under the Company's Act, 1956 in February 1994. This transformation from commission to corporation was more than a legal restructuring – it represented a fundamental shift in philosophy. ONGC would now have shareholders beyond the government, be subject to corporate governance norms, and be expected to generate returns comparable to private sector companies.

The Initial Public Offering (IPO) was a landmark event. ONGC became a public listed company in February 1994, with 20% of its equity were sold to the public and eighty per cent retained by the Indian government. At the time, ONGC employed 48,000 people and had reserves and surpluses worth ₹104.34 billion, in addition to its intangible assets.

The government's divestment continued in phases. First, 2% of shares were sold through competitive bidding to institutional investors. Then, in a move that was both politically astute and organizationally important, 2% of shares were offered to ONGC employees. This employee ownership created a new dynamic – workers were now also owners, with a direct stake in the company's commercial success.

In March 1999, ONGC entered into an interesting cross-holding arrangement with Indian Oil Corporation (IOC) and Gas Authority of India Limited (GAIL). This created interlocking ownership among India's major energy PSUs, a structure designed to prevent hostile takeovers while maintaining government control through indirect holdings.

The new competitive landscape was challenging. The New Exploration Licensing Policy (NELP), launched in 1999, allowed private and foreign companies to bid for exploration blocks on equal terms with ONGC. Suddenly, ONGC found itself competing with Reliance, Cairn Energy, British Gas, and other aggressive players who brought international technology and deep pockets.

The initial years of competition were humbling. A comparison of discoveries in the NELP regime shows that despite its large acreage and rich experience in Exploration and Production (E&P) sector, ONGC made lesser discoveries than new entrants like Gujarat State Petroleum Corporation (GSPC) and Reliance Industries Limited (RIL). Private companies, unencumbered by bureaucratic procedures and willing to take greater risks, made significant discoveries in blocks that ONGC had either not bid for or lost in competitive bidding.

The Krishna-Godavari basin became a particular point of controversy. Reliance's massive gas discovery in the KG-D6 block, adjacent to ONGC's acreage, raised questions about ONGC's exploration strategies and capabilities. The subsequent dispute over gas migration from ONGC's blocks to Reliance's wells would drag on for years, becoming a symbol of the new competitive tensions.

Yet corporatization also unleashed new energies within ONGC. Freed from some government constraints, the company began modernizing rapidly. It invested in 3D seismic technology, acquired advanced drilling rigs, and entered into technical collaborations with international service companies. The company's engineers and geologists, long constrained by bureaucratic procedures, began adopting international best practices.

The financial performance improved dramatically post-corporatization. The company began reporting profits comparable to private sector companies, though still constrained by the subsidy burden. The stock market listing created pressure for transparency and performance, with quarterly results scrutinized by analysts and investors.

In 1994, Oil and Natural Gas Commission was converted in to a Corporation, and in 1997 it was recognized as one of the Navratnas by the Government of India. The Navratna status granted ONGC greater autonomy in investment decisions, joint ventures, and international operations. It could now approve projects up to ₹1,000 crores without government approval, enter into technology agreements, and establish foreign subsidiaries.

This period also saw the revival of ONGC's international ambitions through ONGC Videsh Limited (OVL). What had begun as sporadic overseas ventures now became a systematic strategy to acquire oil and gas assets globally. The logic was compelling – as domestic reserves matured and competition intensified, international expansion offered both growth opportunities and risk diversification.

The transition wasn't without its tensions. ONGC's corporate culture, shaped by decades of public sector ethos, had to adapt to commercial imperatives. Performance management systems were introduced, variable pay was linked to production targets, and the comfortable certainties of lifetime employment were questioned. The company had to balance its social responsibilities with shareholder expectations, its role in energy security with profit maximization.

By the early 2000s, ONGC had successfully navigated the transition from commission to corporation. It remained India's dominant oil and gas producer, had maintained its technical excellence, and had begun expanding internationally. But new challenges were emerging – Mumbai High was declining, the subsidy burden was increasing, and global oil markets were becoming more volatile. The next phase of ONGC's evolution would test whether a state-owned company could truly compete in a globalized energy market.

VII. Modern Expansion: Videsh, Acquisitions & Maharatna Status

The new millennium marked ONGC's transformation into a global energy player. In November 2010, the Government of India conferred the Maharatna status to ONGC. This elite designation, reserved for select PSUs with global ambitions and strong fundamentals, granted ONGC unprecedented autonomy. The company could now make investments up to ₹5,000 crores without government approval, enter into joint ventures, and pursue international acquisitions aggressively.

The Maharatna status was recognition of ONGC's evolution, but it also came with heightened expectations. The company was now expected to become a global energy major, competing with international oil companies while maintaining its role as India's energy anchor.

ONGC Videsh's expansion during this period was remarkable. ONGC Videsh owns Participating Interests in 32 oil and gas assets in 15 countries. In terms of reserves and production, ONGC Videsh is the second largest petroleum company of India, next only to its parent ONGC. The transformation from sporadic overseas ventures to systematic international expansion reflected both capability development and strategic necessity.

The portfolio that OVL built was impressively diverse. ONGC Videsh has stake in 32 oil and gas projects in 15 Countries, viz. Azerbaijan (2 projects), Bangladesh (2 Projects), Brazil (2 projects), Colombia (4 projects), Iran (1 project), Iraq (1 project), Libya (1 project), Mozambique (1 Project), Myanmar (6 projects), Russia (3 projects), and several others including Sudan, Syria, and UAE.

Each acquisition told a story of ambition, risk, and geopolitical maneuvering. In 2003, ONGC Videsh Limited (OVL), the division of ONGC concerned with its foreign assets, acquired Talisman Energy's 25% stake in the Greater Nile Oil project. This Sudan acquisition was particularly significant – it marked ONGC's entry into Africa and demonstrated willingness to operate in challenging environments that Western companies were abandoning due to political pressure.

The Russia ventures became OVL's crown jewels. The Sakhalin-1 project in Russia's Far East, where ONGC held a 20% stake, was one of the largest foreign investments by an Indian company. The acquisition of 26% stake in Vankorneft in 2016 added massive reserves and production. These Russian assets provided not just oil and gas, but also exposure to Arctic drilling technologies and complex project management.

But the most transformative domestic acquisition came in 2018. On 30 January 2018, ONGC acquired 51.11% stake in Hindustan Petroleum Corporation Limited (HPCL), for Rs 36,915 crore. This was more than just an acquisition – it was a strategic reshaping of India's energy sector.

The acquisition of 51.11% equity share of Government of India in HPCL is slated to make ONGC the third largest refining power in the country. With this, ONGC is set to become India's first fully vertically integrated Energy Company with presence across the entire hydrocarbon value chain.

The HPCL acquisition represented ONGC's evolution from an upstream company focused on exploration and production to an integrated energy major. HPCL brought with it two major refineries, thousands of retail outlets, and established marketing networks. The combined entity could now capture value across the entire petroleum value chain – from wellhead to fuel pump.

The downstream integration continued with other ventures. ONGC's stake in Mangalore Refinery and Petrochemicals Limited (MRPL), acquired from the A.V. Birla Group in 2003, had already given it refining capabilities. The ONGC Petro additions Limited (OPaL) petrochemical complex in Dahej, commissioned in 2017, added petrochemical production to the portfolio.

The financial performance during this period reached unprecedented heights. ONGC manifested its resilience & outstanding performance by posting its highest-ever net profit of Rs 403,057 million in FY2022, driven by high oil prices following Russia's invasion of Ukraine. Net profit for the fiscal FY22 (April 2021 to March 2022) soared 258 per cent to Rs 40,305.74 crore from Rs 11,246.44 crore in the previous financial year. This as it got an average of $76.62 for every barrel of crude oil produced and sold in the fiscal as against $42.78 per barrel net realisation in the previous year.

The company's technical capabilities also evolved significantly. ONGC entered deepwater exploration, with discoveries in the Krishna-Godavari basin at water depths exceeding 1,000 meters. It developed expertise in unconventional hydrocarbons, including coal bed methane and shale gas. The company's service capabilities – in seismic acquisition, drilling, and well services – became so advanced that ONGC could execute entire projects without foreign assistance.

ONGC has a unique distinction of being a company with in-house service capabilities in all areas of Exploration and Production of oil and gas and related oil-field services. This capability, rare even among international oil companies, gave ONGC strategic advantages in cost control and technology development.

Yet this period also revealed persistent challenges. Despite massive investments, domestic production continued to decline. Mumbai High, once producing 400,000 barrels per day, had declined to about 134,000 barrels per day by 2024. The new discoveries were smaller, more complex, and more expensive to develop. The easy oil was gone.

The international ventures, while strategically important, faced their own challenges. Political instability affected operations in Sudan, Syria, and Libya. Low oil prices between 2014 and 2020 made some acquisitions look expensive in hindsight. The Russia assets, while productive, became geopolitically sensitive following the Ukraine crisis.

The subsidy burden, though reduced from earlier peaks, remained substantial. ONGC continued to provide discounts to oil marketing companies, cross-subsidizing fuel prices for Indian consumers. This "under-recovery" mechanism, while serving social objectives, constrained ONGC's ability to invest in high-risk, high-reward exploration.

VIII. Challenges & Crisis Management

The journey of any major energy company is punctuated by crises, and ONGC's story is no exception. These challenges – from deadly accidents to corporate disputes to natural disasters – tested the company's resilience and exposed vulnerabilities in its operations and governance.

The Mumbai High fire of 2005 remains one of the darkest chapters in ONGC's history. On 27 July 2005, a major fire destroyed the production platform, leaving at least 22 people dead despite rescue measures taken by the Indian Coast Guard. The fire, triggered when a vessel collided with the platform during monsoon conditions, caused damages estimated at $370 million and significantly impacted production from India's most important oil field.

The incident exposed serious gaps in offshore safety protocols and emergency response systems. The subsequent investigation revealed inadequate risk assessment, poor coordination between vessels and platforms, and insufficient emergency evacuation procedures. The tragedy led to a comprehensive overhaul of ONGC's offshore safety standards, but the reputational damage and human cost were irreversible.

Even more devastating was the Cyclone Tauktae disaster in 2021, which became one of the worst offshore accidents in India's history. A drillship of Oil and Natural Gas Corporation (ONGC) and three barges of private contractor Afcons working on the state-owned firm's oilfield went adrift after their anchors gave away in the storm on Monday night. A massive day-night operation by the Indian Navy, Coast Guards and ONGC vessels helped save those on the drillship and two barges, but only 186 out of 261 onboard accommodation barge Pappa 305 could be rescued. 37 persons are confirmed dead so far, while the remaining 38 are still missing.

The cyclone tragedy raised serious questions about ONGC's crisis management and decision-making. Inadequate advance notice and miscalculations of cyclone Tauktae's ferocity and its path may have contributed to a false belief that oilfield operations in the Arabian Sea need not be paused. The incident led to a Parliamentary inquiry that was scathing in its criticism.

The Committee in its further observation held ONGC guilty for none of their senior officials taking charge of the situation and guiding the teams at the Western offshore. "The Committee views this seriously as accountability goes on with authority and would like to recommend to the Ministry (Ministry of Petroleum and Natural Gas) that it should conduct thorough investigation about the responsibility of ONGC officials at various levels in this incident and take strict action against all those who are found negligent of duty," the Committee recommended.

The production decline from mature fields presented a different but equally serious challenge. Mumbai High's production had fallen dramatically from its peak. The field produces 134,000 barrels per day (21,300 m3/d) in 2024, compared to 400,000 barrels per day at its peak in the 1980s. Despite enhanced oil recovery efforts and continuous investment, the decline seemed irreversible.

The company's financial performance reflected these operational challenges. The company has delivered a poor sales growth of 10.8% over past five years. Company has a low return on equity of 13.6% over last 3 years. For a company with monopolistic advantages and massive reserves, these returns were disappointing, especially when compared to nimble private sector competitors.

Perhaps the most controversial challenge was the dispute with Reliance Industries over gas migration. ONGC was owed ₹ 92,000 crores from Reliance Industries Limited (Petrochemicals) for the use of blocks of oil fields. This was highlighted by the Comptroller and Auditor General of India (CAG), the overseer of expenditures of the Indian Government. However, as of 2018, this outstanding amount was still not paid by Reliance Industries Limited to ONGC.

While an international arbitration tribunal eventually ruled in Reliance's favor in 2018, the dispute highlighted ONGC's challenges in protecting its resources and commercial interests. The case raised questions about ONGC's technical capabilities in reservoir management and its ability to pursue complex commercial disputes.

Competition from private players intensified during this period. The CAG audit revealed an uncomfortable truth: Despite acquiring 89 prospective blocks out of 120 blocks upto VIII round of New Exploration Licensing Policy (NELP), ONGC made only 11 discoveries in 8 blocks. The Company did not complete its committed work in 25 prospective blocks and drilled only 30 out of 90 committed wells within the specified period.

These operational challenges were compounded by governance issues. The relationship between ONGC and its newly acquired subsidiary HPCL revealed integration challenges. Even after the Union Cabinet approval and ONGC buying out the entire government stake, HPCL for over one and half years refused to recognise ONGC as its promoter. It listed ONGC's shareholding of 51.11 per cent as a 'public shareholder' in as many as six quarterly shareholding filings with stock exchanges post-January 2018. HPCL listed the President of India with nil shareholding as its promoter in those filings.

Technological challenges also mounted. While ONGC had developed impressive capabilities over the decades, the global oil industry was moving toward more complex frontiers – ultra-deepwater, high-pressure high-temperature reservoirs, Arctic conditions, and unconventional resources. These required not just technology but also risk appetite and investment capacity that ONGC, constrained by government ownership and social obligations, struggled to match.

Environmental and social challenges added another layer of complexity. Climate change concerns were growing globally, and ONGC, as India's largest fossil fuel producer, faced increasing scrutiny. Local communities near ONGC operations increasingly demanded better environmental protection and greater sharing of resource revenues. The company had to balance its production imperatives with environmental and social responsibilities.

The human resource challenges were equally pressing. ONGC's workforce was aging, with many of its most experienced engineers and geologists approaching retirement. Attracting young talent became difficult as private sector companies and international firms offered better compensation and career growth. The public sector culture, while ensuring stability and job security, sometimes stifled innovation and entrepreneurship.

IX. Playbook: Lessons from a State-Owned Giant

ONGC's seven-decade journey offers unique insights into building and managing a state-owned enterprise in a critical sector. The playbook that emerges from this experience is relevant not just for other national oil companies but for any organization attempting to balance commercial objectives with national imperatives.

Building Technical Capabilities from Scratch

ONGC's most remarkable achievement was developing world-class technical capabilities starting from virtually zero. In 1956, India had no indigenous oil industry expertise. By the 1980s, ONGC could execute complex offshore projects independently. This transformation required patient investment in human capital, technology absorption, and learning-by-doing.

The key was the gradual progression from simple to complex operations. ONGC started with onshore exploration in known basins, moved to offshore shallow water, then to deep water. At each stage, it partnered with international experts, absorbed technology, and then indigenized it. The Institute of Drilling Technology, the Institute of Reservoir Studies, and other technical institutions created a knowledge ecosystem that sustained capability development.

Managing the Dual Mandate

ONGC's experience illuminates the perpetual tension between commercial success and social responsibility. As a state-owned enterprise, ONGC was expected to maximize profits while also subsidizing fuel prices, exploring in uneconomic areas for strategic reasons, and maintaining employment in remote locations.

The company managed this dual mandate through cross-subsidization and portfolio management. Profitable fields like Mumbai High generated surpluses that funded exploration in frontier basins. International ventures provided commercial returns that offset domestic obligations. The key was maintaining a portfolio balanced between commercial projects and strategic imperatives.

The Challenge of Government Ownership

Government ownership brought both advantages and constraints. The advantages included patient capital for long-term investments, political support for large projects, and protection from hostile takeovers. ONGC could undertake exploration in high-risk areas knowing that short-term losses wouldn't trigger shareholder revolts.

But the constraints were equally significant. Bureaucratic decision-making slowed responses to market opportunities. Political interference affected operational decisions. The subsidy burden constrained investment capacity. Perhaps most importantly, the safety net of government ownership sometimes bred complacency and risk aversion.

ONGC's most successful periods were when it enjoyed operational autonomy while maintaining government support. The Maharatna status represented an attempt to institutionalize this balance, though implementation remained challenging.

Long-term Thinking in a Cyclical Industry

Oil and gas is inherently cyclical, with prices swinging from boom to bust. ONGC's state ownership allowed it to maintain long-term perspectives through these cycles. During low price periods, when private companies slashed exploration budgets, ONGC continued investing, positioning itself for the next upturn.

This long-term orientation was particularly valuable in exploration, where success rates are low and payoffs take decades. ONGC's patient exploration in the Krishna-Godavari deep water, despite multiple dry wells, eventually yielded significant discoveries. Private companies might have abandoned such efforts under quarterly earnings pressure.

International Expansion Strategy

ONGC Videsh's evolution offers lessons in international expansion for emerging market companies. OVL's strategy was pragmatic rather than prestigious – it focused on assets that international oil companies were abandoning due to political risk or marginal economics, where ONGC's lower cost structure and higher risk tolerance provided advantages.

The company also leveraged India's diplomatic relationships and non-aligned foreign policy. In countries like Sudan, Syria, and Iran, where Western companies faced sanctions or political pressure, ONGC could operate relatively freely. This geopolitical arbitrage, while risky, provided access to significant reserves.

Vertical Integration as Hedge

The HPCL acquisition and downstream expansion represented a strategic hedge against oil price volatility. When crude prices fell, upstream profits declined but downstream margins expanded. This natural hedge provided earnings stability that pure upstream companies lacked.

The integration also provided market intelligence and customer relationships that pure upstream companies missed. ONGC could better understand demand patterns, product specifications, and market dynamics, informing its upstream investment decisions.

Innovation Within Constraints

Despite bureaucratic constraints, ONGC demonstrated significant innovation. The company developed new technologies for offshore operations in monsoon conditions, created innovative financing structures for international acquisitions, and pioneered new exploration techniques for Indian geology.

The key was creating pockets of excellence within the larger organization. The research institutes, the offshore operations team, and ONGC Videsh operated with relative autonomy and entrepreneurial culture, even as the parent organization remained bureaucratic.

Managing Stakeholder Complexity

As a state-owned enterprise, ONGC had to manage extraordinary stakeholder complexity – the government as owner and regulator, public shareholders, employees, local communities, environmental groups, and energy consumers. Each stakeholder had different and often conflicting expectations.

ONGC's approach was incremental accommodation rather than bold confrontation. It gradually reduced subsidies rather than eliminating them abruptly. It slowly modernized employment practices while maintaining job security. It increased transparency and corporate governance while preserving government control. This incremental approach avoided crises but also limited transformation.

X. Future Challenges & Energy Transition

ONGC stands at an inflection point. The global energy landscape is transforming with unprecedented speed, driven by climate concerns, technological disruption, and changing geopolitics. For a company whose identity is intertwined with fossil fuels, the challenges ahead are existential.

The immediate challenge is arresting production decline. ONGC believes the field still has a balance reserve of 80 million tonnes (610 million barrels) of oil and over 40 bcm of gas in Mumbai High alone. But extracting these reserves requires advanced enhanced oil recovery (EOR) techniques and massive investment.

ONGC is seeking international partnerships for this challenge. The company is looking for technical service partners with revenues exceeding $75 billion annually – essentially limiting the field to super-majors like ExxonMobil, Shell, or BP. These companies bring advanced EOR technologies like chemical injection, thermal recovery, and carbon dioxide flooding that could potentially recover an additional 10-15% of original oil in place.

The energy transition presents both threat and opportunity. Global oil demand is expected to peak within the next decade as electric vehicles proliferate and renewable energy expands. For ONGC, whose core business is oil and gas, this is an existential challenge. The company's response has been measured – investing in renewable energy through subsidiaries while maintaining that oil and gas will remain relevant for decades.

ONGC has announced plans for significant renewable energy investments. The company aims to add 10 GW of renewable energy capacity by 2030, primarily through solar and offshore wind projects. It's also exploring green hydrogen production, leveraging its offshore expertise for offshore wind farms, and carbon capture and storage using depleted oil fields.

But the transition faces internal resistance. ONGC's culture, capabilities, and infrastructure are built around hydrocarbons. Petroleum engineers and geologists, who form the company's technical core, have limited expertise in renewable energy. The financial returns from renewables are lower than traditional oil and gas projects. Most fundamentally, ONGC's identity as India's oil champion conflicts with a renewable future.

Competition is intensifying from unexpected quarters. Reliance Industries, once primarily an oil refining company, has announced massive renewable energy investments. Adani Group, with no oil and gas heritage, is building one of the world's largest renewable energy portfolios. These nimble private players, unencumbered by legacy assets and workforce, could potentially outmaneuver ONGC in the energy transition.

Geopolitical tensions add another layer of complexity. ONGC's significant investments in Russia, while commercially successful, have become politically sensitive following the Ukraine invasion. Oil and Natural Gas Corporation (ONGC) has faced criticism for maintaining business operations in Russia despite international sanctions imposed following Russia's invasion of Ukraine in 2022. The company continued to sell Russian Sokol crude oil to Indian refiners, drawing concerns over its role in supporting Russia's energy sector.

The company must navigate between India's energy security needs, which require maintaining Russian oil supplies, and potential secondary sanctions from Western nations. This geopolitical tightrope walking will become more challenging as great power competition intensifies.

The domestic policy environment is also evolving. The government has announced intentions to reduce its stake in PSUs, potentially including ONGC. While full privatization seems unlikely given ONGC's strategic importance, reduced government shareholding would fundamentally alter the company's character and objectives.

Natural gas is emerging as a transition fuel, and ONGC is positioning itself accordingly. The government's goal of increasing natural gas's share in the energy mix from 6% to 15% by 2030 creates opportunities. ONGC is developing gas fields, building pipelines, and investing in city gas distribution. Gas, while still a fossil fuel, produces lower emissions than oil or coal and could provide a bridge to a renewable future.

Technological disruption threatens traditional business models. Digital oilfields using artificial intelligence and Internet of Things could dramatically reduce operating costs. Automated drilling and robotic maintenance could transform offshore operations. ONGC must rapidly digitalize or risk being left behind by more agile competitors.

The financial challenges are mounting. The company has delivered a poor sales growth of 10.8% over past five years. Company has a low return on equity of 13.6% over last 3 years. With declining production, increasing costs, and massive investment needs, ONGC's financial performance is under pressure. The company must improve returns while investing in both traditional operations and energy transition.

Climate-related physical risks are becoming material. Cyclones in the Arabian Sea are becoming more frequent and intense due to climate change, threatening offshore operations. Rising sea levels could affect coastal infrastructure. Extreme weather events disrupt supply chains and operations. ONGC must adapt its infrastructure and operations for a changing climate while contributing to emissions reduction.

The social license to operate is evolving. Younger Indians, particularly in urban areas, are increasingly concerned about climate change and environmental degradation. ONGC must maintain public support while operating in an industry increasingly seen as contributing to climate crisis. This requires not just better environmental performance but also effective communication about the company's role in energy transition.

XI. Bear vs. Bull Case & Investment Analysis

As ONGC trades at a market capitalization of approximately ₹2.94 trillion with the government holding 58.9%, the investment case presents a fascinating study in contrasts. The bear and bull arguments are equally compelling, reflecting the fundamental uncertainties facing fossil fuel companies in an era of energy transition.

The Bear Case: Structural Decline and Transition Risk

The pessimistic view starts with production reality. Mumbai High, once ONGC's crown jewel, has declined from 400,000 barrels per day to just 134,000 barrels per day. Despite decades of exploration and billions in investment, no new Mumbai High has been discovered. The easy oil is gone, and what remains is technically challenging and economically marginal.

The financial metrics support the bear case. The company has delivered a poor sales growth of 10.8% over past five years. Company has a low return on equity of 13.6% over last 3 years. For a company with monopolistic advantages in India's oil and gas sector, these returns are disappointing. Private sector competitors have generated better returns with fewer advantages.

The energy transition represents an existential threat. Global oil demand is expected to peak by 2030, driven by electric vehicle adoption and renewable energy expansion. ONGC's core business – extracting and selling fossil fuels – faces long-term decline. The company's renewable energy investments, while notable, are subscale compared to specialized renewable players.

Government interference remains a persistent drag. Despite Maharatna status, ONGC continues to bear subsidy burdens, support government programs, and face political pressure in operational decisions. The HPCL acquisition, while strategically logical, was essentially forced by the government and executed at a premium valuation.

International ventures, while providing diversification, carry significant risks. The Russia exposure has become politically toxic. Middle East assets face geopolitical instability. African ventures operate in challenging environments. The international portfolio, built over decades, may become stranded as global energy transition accelerates.

The competitive landscape has permanently changed. The NELP regime ended ONGC's monopoly, and private players have proven more agile and efficient. In the CAG's assessment, ONGC made fewer discoveries than new entrants despite superior acreage and experience. This suggests structural rather than temporary competitive disadvantages.

The ESG (Environmental, Social, and Governance) overhang is growing. Global investors are divesting from fossil fuel companies. Indian financial institutions, while currently supportive, may face pressure to reduce exposure. ONGC's cost of capital could increase as ESG considerations become mainstream.

The Bull Case: Strategic Value and Transition Potential

The optimistic view starts with strategic importance. India's energy demand will double by 2040, and despite renewable growth, oil and gas will remain crucial for decades. ONGC's domestic reserves and production capabilities provide energy security that no private company can match. In a world of increasing geopolitical tension, this strategic value is priceless.

The valuation appears compelling. Trading at relatively modest multiples, ONGC offers a dividend yield exceeding 5%. Stock is providing a good dividend yield of 5.24%. For income-focused investors, ONGC provides steady returns backed by real assets and government support.

The infrastructure moat is formidable. ONGC operates platforms, pipelines, processing facilities, and logistics networks built over decades. Replacing this infrastructure would cost hundreds of billions of rupees and take decades. This physical network provides competitive advantages that new entrants cannot replicate.

The Mumbai High potential remains significant. ONGC believes the field still has a balance reserve of 80 million tonnes (610 million barrels) of oil and over 40 bcm of gas. With advanced EOR techniques and international partnerships, production could potentially be stabilized or even increased. Oil prices above $70 per barrel make even expensive EOR techniques economically viable.

The integrated model provides resilience. The HPCL acquisition transformed ONGC into an integrated energy company, providing natural hedges against oil price volatility. When crude prices fall, upstream margins compress but downstream margins expand. This integration provides earnings stability that pure-play companies lack.

Natural gas offers a bridge to the future. As India shifts from coal to gas for power generation and industrial use, ONGC's gas reserves become increasingly valuable. Gas, while still a fossil fuel, supports the energy transition as a cleaner alternative to coal and backup for renewable intermittency.

The international portfolio, despite challenges, provides optionality. Assets in Russia, Africa, and Latin America offer production growth potential. If geopolitical tensions ease, these assets could appreciate significantly. The portfolio provides diversification that domestic-focused companies lack.

Government support remains strong. Despite privatization rhetoric, the government is unlikely to abandon ONGC given its strategic importance. Financial support during crises, regulatory favoritism, and protected market share remain likely. The government's 58.9% stake aligns its interests with ONGC's success.

Comparative Analysis with Global NOCs

ONGC's valuation and performance must be contextualized against global national oil companies. Saudi Aramco, the world's most valuable oil company, trades at premium valuations reflecting its massive reserves and low production costs. Petrobras, Brazil's NOC, has undergone successful transformation, focusing on prolific pre-salt reserves while divesting non-core assets. Petronas, Malaysia's NOC, has successfully internationalized while maintaining domestic dominance.

Compared to these peers, ONGC appears undervalued but also underperforming. Its reserve replacement ratio lags behind Aramco and Petronas. Its production costs exceed Aramco's by a significant margin. Its international success falls short of Petronas's achievements. Yet ONGC's integrated model and domestic market position provide defensive characteristics that pure upstream NOCs lack.

The Investment Verdict

The investment case for ONGC ultimately depends on three key assumptions: the pace of India's energy transition, the government's commitment to PSU reform, and oil price trajectories. Bulls betting on ONGC are essentially wagering that India's energy transition will be slower than anticipated, that the government will grant greater operational autonomy, and that oil prices will remain elevated due to underinvestment in new supply.

Bears shorting ONGC are betting on accelerated energy transition, continued government interference, and structural decline in oil demand. They see ONGC as a value trap – optically cheap but facing terminal decline.

The truth likely lies between these extremes. ONGC will probably neither collapse nor thrive, instead mudding through as a steady but unspectacular investment. For Indian investors seeking exposure to the energy sector with limited downside, ONGC offers reasonable risk-reward. For global investors seeking growth and transformation, better opportunities exist elsewhere.

XII. Epilogue: Energy Security & Nation Building

As we reach the end of ONGC's remarkable journey, it's worth stepping back to consider what this company has meant for India and what its future might hold. ONGC is more than a corporate entity – it's a symbol of India's post-independence aspirations, a testament to indigenous capability development, and a critical pillar of national security.

The Mumbai High legacy alone justifies ONGC's existence. That discovery in 1974, coming amid the global oil crisis, saved India billions in foreign exchange and provided energy security when the country was most vulnerable. The psychological impact – proving that India could find and develop its own oil – was perhaps even more valuable than the oil itself.

ONGC's contribution to nation-building extends beyond hydrocarbons. The company created India's first generation of petroleum professionals, built world-class technical institutions, and demonstrated that Indian companies could compete globally in complex industries. The townships, schools, and hospitals ONGC built brought development to remote regions. The sports teams it sponsored produced Olympic athletes. The research institutions it established advanced India's scientific capabilities.

Yet ONGC also embodies the contradictions of Indian development. It represents both the achievements and limitations of the public sector model. It showcases indigenous capability development but also bureaucratic inefficiency. It demonstrates strategic thinking but also political interference. It embodies national pride but also missed opportunities.

The energy transition challenge facing ONGC mirrors India's own development dilemmas. How does a developing country balance growth with sustainability? How does it provide affordable energy to lift millions from poverty while addressing climate change? How does it compete globally while maintaining social objectives? ONGC's struggles with these questions reflect India's broader challenges.

Looking ahead, ONGC's relevance will depend on its ability to transform. The company that mastered offshore drilling must now master renewable energy. The organization that discovered Mumbai High must discover new business models. The institution that provided energy security through oil must provide energy security through diversification.

Can ONGC successfully navigate the energy transition? History suggests cautious optimism. The company has repeatedly defied skeptics – from those who said India had no oil to those who said ONGC couldn't compete with private players. Each time, ONGC adapted and survived, if not always thrived.

But the energy transition represents a different magnitude of challenge. It's not about finding new oil fields or mastering new drilling techniques. It's about reimagining the fundamental purpose of the company. It's about transforming an organization built around hydrocarbons into one that transcends them.

The path forward likely involves painful choices. ONGC may need to divest marginal assets, reduce workforce, and exit non-core businesses. It must accelerate digitalization, embrace new technologies, and develop new capabilities. Most fundamentally, it must balance its heritage as India's oil champion with its future as an energy company.

The government's role will be crucial. If it provides ONGC with genuine autonomy, adequate resources, and clear mandates, transformation is possible. If it continues to use ONGC as an instrument of political economy, decline is likely. The choice between these futures will shape not just ONGC but India's entire energy landscape.

International partnerships could accelerate transformation. Collaboration with global energy majors undergoing their own transitions could provide technology, capital, and expertise. Joint ventures in renewable energy, hydrogen, and carbon capture could leapfrog ONGC's capabilities. But such partnerships require ONGC to offer value beyond just access to Indian markets.

The financial markets will ultimately judge ONGC's transformation. If investors believe ONGC can successfully transition, valuations will reflect future potential rather than stranded assets. If skepticism prevails, ONGC could face a downward spiral of declining valuations, reduced investment capacity, and accelerating decline.

The human dimension deserves emphasis. ONGC employs tens of thousands of people whose lives and communities depend on the company's success. The petroleum engineers who spent careers finding oil must now embrace renewable energy. The offshore workers who risked their lives on platforms must adapt to new technologies. The transformation is not just corporate but deeply personal.

As India aspires to become a developed nation by 2047, ONGC's role in that journey remains undefined. Will it be a relic of the socialist past, gradually withering as energy transitions? Or will it reinvent itself as a modern energy company, leading India's transition to a sustainable future? The answer will emerge over the coming decade.

What's certain is that ONGC's story is far from over. The company that discovered Mumbai High, built India's petroleum industry, and provided energy security for decades has earned its place in India's economic history. Whether it can earn a place in India's energy future remains an open question – one that will be answered not in corporate boardrooms or government offices, but in the depths of the ocean, the expanse of solar farms, and the innovation of laboratories.

The final verdict on ONGC will be written by history. But if the past seven decades are any guide, betting against ONGC's ability to adapt and survive would be premature. The company that transformed India from an oil-poor nation to an energy power may yet transform itself for the new energy era. The journey from socialist dream to hydrocarbon empire was remarkable. The journey from hydrocarbon empire to energy leader could be even more so.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube