Nykaa: India's Beauty Empire Built Against All Odds

I. Cold Open & Episode Roadmap

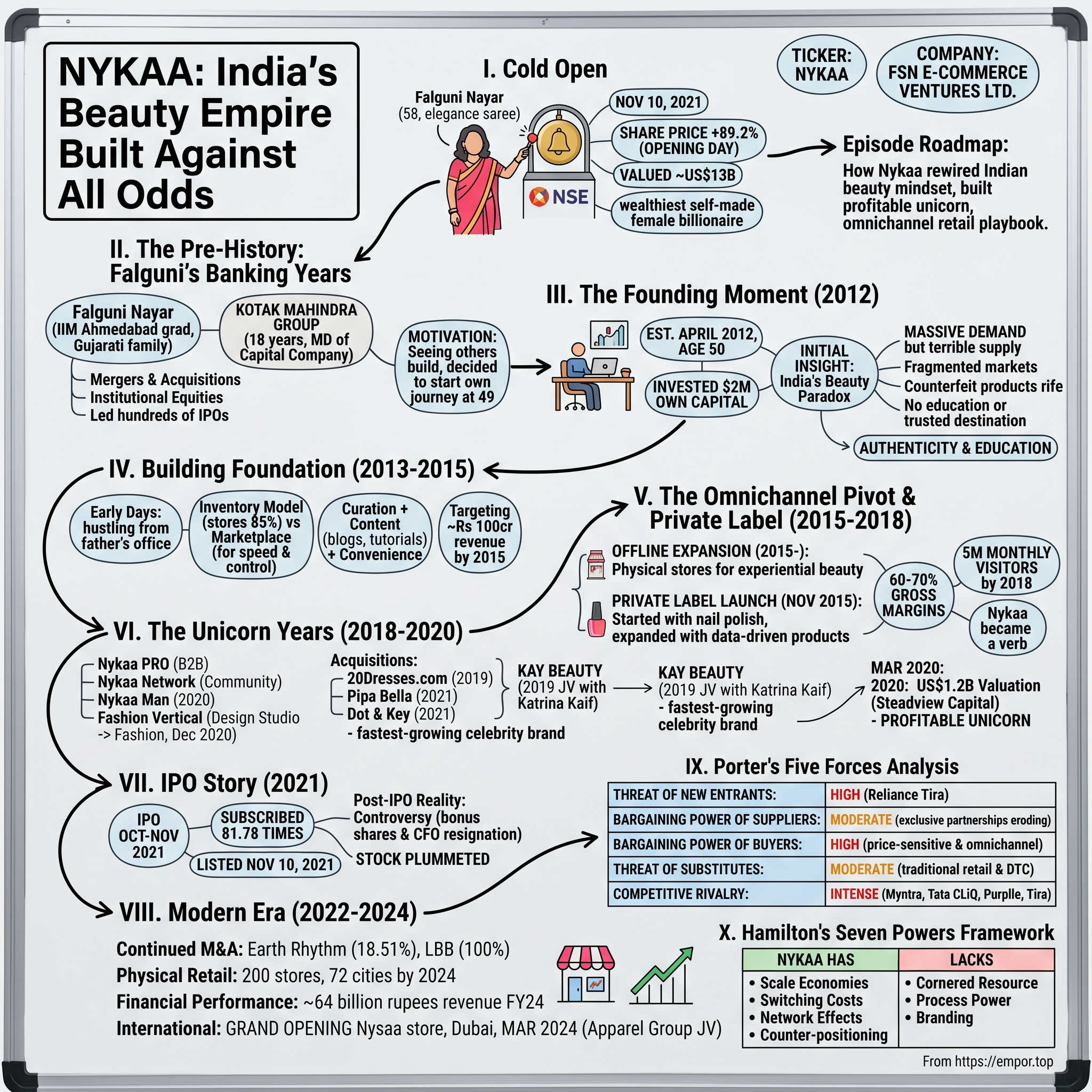

Picture this scene: November 10th, 2021, the National Stock Exchange in Mumbai. A 58-year-old woman in an elegant saree rings the opening bell as flashbulbs pop and traders applaud. Her company's share price has just risen by 89.2% on opening day, valuing the company at nearly US$13 billion. Falguni Nayar, who owned a 53.5% stake in the company, became India's wealthiest self-made female billionaire on the listing day. But this isn't a story about overnight success—it's about a former investment banker who quit her cushy job at 50 to sell lipstick online in a country where most people had never bought beauty products on the internet.

The paradox is delicious: here's a woman who spent 18 years where she also served as a managing director at Kotak Mahindra Capital Company, watching companies go public, making rain for others—and then decided to build something herself in a category everyone said wouldn't work. Beauty e-commerce in India? In 2012? When counterfeit products flooded the market and women preferred to touch and test before buying?

What we'll uncover today is how Nykaa didn't just crack the code on selling mascara online—they fundamentally rewired how 1.4 billion Indians think about beauty, built a profitable unicorn when everyone else was burning cash, and created a playbook for omnichannel retail that even Reliance is now copying. This is a masterclass in category creation, patient capital, and why sometimes the best entrepreneurs are the ones who start "too late."

II. The Pre-History: Falguni's Banking Years

To understand why Nykaa succeeded where others failed, you need to understand Falguni Nayar's previous life. In 1993, Nayar joined Kotak Mahindra Group after leaving her consultant job at A. F. Ferguson & Co. At Kotak Mahindra, she was initially the head of mergers and acquisitions (M&A) team, before going on to open institutional equities offices in London and New York City. In 2005, she was appointed as the managing director of Kotak Mahindra Capital, the investment banking unit, and director of Kotak Securities, the institutional equities arm.

Think about what this means: for nearly two decades, she had a front-row seat to India's economic transformation. At Kotak Investment Bank, she successfully guided the firm to be India's leading IPO Banker and was instrumental in closing a number of successful M&A deals including sale of Hutchison to Vodafone, Bharti – Walmart JV for India Retail amongst others. She wasn't just observing deals—she was architecting them, understanding capital structures, seeing what made companies succeed or fail at scale.

Nayar was born and raised in a Gujarati family in Mumbai, Maharashtra. Her father was a businessman and ran a small bearings company, assisted by her mother. She is a graduate in B.Com from Sydenham College of Commerce and Economics and a postgraduate from the Indian Institute of Management Ahmedabad (1985 batch). Growing up in a business family, she absorbed entrepreneurial instincts early, but channeled them into the corporate world first.

The itch to build something of her own grew slowly, then suddenly. By 2011, at 49, she'd seen hundreds of entrepreneurs walk through Kotak's doors, pitch their dreams, raise capital, and build empires. It was during this point that Falguni's past interactions with a number of successful entrepreneurs motivated her to pursue an entrepreneurial journey. The investment banker who'd helped others go public was ready to become the entrepreneur herself.

III. The Founding Moment & Initial Insight (2012)

The decision to leave Kotak wasn't impulsive—it was calculated, like everything else in Falguni's life. In April 2012, at the age of 50, she established Nykaa, investing $2 million of her own capital. No venture capital, no safety net, just her own money on the line. Once in an interview with Film Companion, Falguni Nayar shared how she was quite scared about leaving her job. The entrepreneur admitted that when she told her son about leaving her banking job and starting her own company, even he was in a bit of shock. Falguni also added that she asked her son to reveal whether her decision to open her own company could go horribly wrong, and he said, "Definitely".

But Falguni had spotted something others missed. India's beauty market was a paradox: massive demand but terrible supply. Women in tier-2 and tier-3 cities couldn't access international brands. Even in metros, the market was fragmented—you'd find L'Oréal in one store, Maybelline in another, luxury brands nowhere. Counterfeit products were rampant. There was no education, no guidance, no trusted destination.

In April 2012, Falguni Nayar, a former managing director at Kotak Mahindra Capital Company, founded Nykaa as an ecommerce portal curating a range of beauty and wellness products. The brand name Nykaa is derived from the Sanskrit word nayaka, meaning actress or "one in the spotlight". The website was first launched around Diwali 2012, and was available commercially in 2013.

The insight was elegantly simple: Indian women didn't need to be sold on beauty—they needed access, authenticity, and education. The aspiration was already there, rising with income levels and exposure to global trends through Bollywood and social media. What was missing was the infrastructure to serve that aspiration.

The name itself was strategic. "Nykaa"—derived from Sanskrit, meaning the protagonist, the one in the spotlight. Not about making women beautiful for others, but about being the hero of their own story. This positioning would prove crucial in building trust with Indian women navigating traditional expectations and modern aspirations.

IV. Building the Foundation (2013-2015)

The early days were unglamorous, a far cry from the investment banking boardrooms Falguni had left behind. She employed three people, when she started her business from her father's small office. No fancy tech team, no marketing budget, just hustle and an obsessive focus on getting the basics right.

The first critical decision: inventory model versus marketplace. While Amazon and Flipkart were building asset-light marketplaces, connecting sellers to buyers, Nykaa chose the harder path. Unlike bigger e-commerce players who prefer the marketplace model, Nykaa stores 85% of its inventory. "If you see it on the site, we have it in our warehouse. These leads to a much more superior users experience with extra fast delivery," Falguni explains. This meant higher capital requirements, inventory risk, and operational complexity. But it also meant complete control over authenticity—crucial in a market plagued by fakes.

The numbers in those early years were modest but meaningful. The company started with about 60 sales in the initial phase, but momentum built steadily. By 2015, they were targeting Rs 80-100 crore in revenue, with sights set on Rs 240-300 crore by March 2017. Each order was a victory, each repeat customer validation of the model.

But Nykaa's real innovation wasn't operational—it was editorial. They didn't just sell products; they created content. Beauty tutorials, product guides, skin type analyses, ingredient education. The company focused on three Cs – Curation (inventory-led business to ensure customers get authentic products), Content (educating customers on beauty and make up through blogs and video tutorials) and Convenience (making sure customers get a hasslefree experience). In a market where most women learned about makeup from friends or beauty parlor aunties, Nykaa became the trusted beauty advisor.

The turning point came in October 2015 with the first institutional funding—$9.5 million that would fuel the next phase of growth. But more importantly, that same year, Falguni made two decisions that would define Nykaa's future: launching private labels and going offline.

V. The Omnichannel Pivot & Private Label Launch (2015-2018)

The Offline Expansion Decision

In 2015, while the world was going digital-first, Nykaa made a contrarian bet: they opened physical stores. In 2015, the company expanded from online-only to an omnichannel model and began selling products apart from beauty. As of 2020, it retails over 2,000 brands and 200,000 products across its platforms. This wasn't a retreat from e-commerce—it was an acknowledgment that beauty is inherently experiential. Women want to swatch that lipstick, smell that perfume, feel that cream's texture.

The store formats were carefully differentiated. Nykaa Luxe for premium locations and international brands. Nykaa On Trend for mass premium. Beauty kiosks for high-traffic areas. Each format served a different customer segment and shopping mission.

Private Label Strategy

The private label launch in November 2015 started modestly—with nail polish. But this wasn't just about margins. Nykaa had data on what Indian women were searching for but couldn't find. Nude lipsticks for Indian skin tones. Long-wearing kajal that wouldn't smudge in Mumbai humidity. Face masks for pollution-stressed skin.

The portfolio expanded methodically. Nykaa Cosmetics for color cosmetics. Nykaa Naturals for the growing clean beauty segment. By 2019, Wanderlust Bath & Body collection for the millennial consumer seeking Instagram-worthy packaging with effective formulations. Each brand filled a specific gap, backed by data and consumer insights.

The economics were compelling: private labels offered 60-70% gross margins versus 30-40% for third-party brands. But more importantly, they created differentiation. You could buy MAC anywhere, but Kay Beauty? Only at Nykaa.

Growth Metrics

By 2018, the transformation was remarkable. Five million monthly website visitors. 100,000 orders with an average basket size of Rs 1,400. Available across 900 cities with 400+ brands and 40,000 products. Mobile contributing 50% of sales—crucial in a mobile-first country.

But here's what the numbers don't capture: Nykaa had become a verb. "Let me Nykaa it" entered the urban Indian lexicon. They weren't just selling beauty products; they were shaping beauty culture.

VI. The Unicorn Years: Scale & Competition (2018-2020)

Product Expansion

The platform evolved beyond basic e-commerce. In 2018, Nykaa PRO launched as a membership program for makeup artists and salon professionals—creating a B2B revenue stream while building industry relationships. The Nykaa Network became India's beauty community platform, where users created content, shared tips, and built followings.

In October 2020, the company launched Nykaa Man, India's first multi-brand ecommerce store for men's grooming. This wasn't just category expansion—it was recognition that Indian men were finally ready to move beyond Old Spice and Fair & Handsome.

Fashion Vertical Launch

December 2020 marked another pivot: The company expanded into fashion by launching Nykaa Design Studio, which was renamed to Nykaa Fashion. In December 2020, Nykaa Fashion launched its first store in Delhi, making the fashion business omnichannel. Fashion seemed like a natural adjacency—after all, beauty and fashion are complementary. But this would prove to be Nykaa's most challenging bet, competing against entrenched players like Myntra with different unit economics and consumer behavior.

Key Acquisitions

The M&A strategy was surgical. In May 2019, Nykaa acquired 20Dresses.com, a private women's styling platform. In 2021, Nykaa Fashion acquired the India fashion jewellery brand, Pipa Bella, and the Indian skincare brand, Dot & Key. Each acquisition wasn't just about adding brands—it was about acquiring capabilities, talent, and customer bases that would accelerate Nykaa's own development.

Celebrity Partnerships

The masterstroke came in 2019. Kay Beauty, which launched as a joint venture with India's biggest beauty retailer Nykaa in 2019. Falguni Nayar, founder & CEO, Nykaa, "The launch of Kay Beauty is a proud moment for Nykaa as India's first celebrity beauty brand. I have always been an admirer of Katrina's independent spirit and was inspired by her vision to create this unique collection. Over the past two years, Katrina and the team have worked with relentless passion and dedication to bring this vision to life. We are constantly looking at innovative beauty solutions to offer our customers and Kay Beauty will add a new facet to the Nykaa conversation."

This wasn't just celebrity endorsement—it was co-creation. Katrina Kaif wasn't just lending her name; she was involved in product development, positioning, marketing. The result? Kay Beauty became India's fastest-growing celebrity-founded beauty label, scaling up 56 percent year-on-year to ₹2.5 billion ($28.6 million) in gross merchandise value.

Unicorn Status

In March 2020, Nykaa raised ₹100 crore (US$12 million) from Steadview Capital at a valuation of US$1.2 billion, making it a unicorn startup. This was followed by another tranche of ₹67 crore (US$7.9 million) funding by Steadview in May 2020. But here's the kicker: unlike every other Indian unicorn, Nykaa was already profitable. In a world of growth-at-all-costs, Falguni had built a unicorn that actually made money.

VII. The IPO Story & Public Market Journey (2021)

Pre-IPO Preparations

The run-up to the IPO was methodical. Nykaa in a statement said that post the investment, the D2C skincare brand will join Nykaa's stable of owned brands. This is Nykaa's second acquisition of the year. In April, Nykaa acquired online jewellery brand Pipa Bella to capture the growing market for contemporary fashion jewellery in the country. Each acquisition strengthened the portfolio, adding capabilities that would resonate with public market investors.

The numbers told a compelling story. In the year that ended in March 2021, the parent company, FSN E-commerce Ventures, reported a revenue of Rs2,440 crore and a profit of Rs61 crore. While other startups were explaining their path to profitability, Nykaa was already there.

The IPO Event

FSN E-Commerce Ventures IPO opens on October 28, 2021, and closes on November 1, 2021. The FSN E-Commerce Ventures IPO listing date is on Wednesday, November 10, 2021. The IPO comprises of fresh issues of shares worth ₹630 crore and offer for sale of ₹4721.92 crore.

The market response was electric. Retail investors' portion was subscribed 12.24 times, while non-institutional investors' quota received 112.02 times subscription. The qualified institutional buyers (QIBs) portion was booked 91.17 times. Overall, the IPO was subscribed 81.78 times.

Nykaa was publicly listed on the NSE and BSE on 10 November 2021, and its price rose by 89.2% on opening day, valuing the company at nearly US$13 billion. For a few glorious months, Nykaa was the poster child of Indian startups—profitable, growing, and public.

Post-IPO Reality

But public markets are unforgiving. The honeymoon ended quickly as global tech stocks crashed and questions emerged about Nykaa's governance. The most controversial moment came in November 2022. The lock-in period for pre-IPO investors in Nykaa was scheduled to end on 10 November 2022, however, Nykaa announced a 5:1 bonus share issue immediately before the stock's much-anticipated sell-off. The bonus issue led to investors owning only 1/6th of the shares on the day lock-in expired while it has significantly changed the tax incidence for early-stage investors.

In November 2022, Nykaa issued 5:1 bonus shares to coincide with the expiry date of pre-IPO shareholders' lock-in period. The bonus issue resulted in the company's corporate governance practices receiving heavy criticism, with questions raised over the timing and motive of the issuance along with concerns of market manipulation and tax avoidance. Later that month, CFO Arvind Agarwal resigned from the company, even as the Securities and Exchange Board of India began scrutinizing the allotment of bonus shares.

The stock, which had touched highs of ₹2,574, plummeted to lows of ₹115. The beauty empire suddenly didn't look so beautiful to public market investors.

VIII. Modern Era: Profitability & Expansion (2022-2024)

Continued M&A Activity

Despite market volatility, Nykaa continued building. In 2022, Nykaa acquired an 18.51% stake in Indian skincare brand Earth Rhythm. It then completed the 100% acquisition of lifestyle content platform Little Black Book (LBB). Each acquisition was strategic—Earth Rhythm for clean beauty, LBB for content-commerce convergence.

Physical Retail Expansion

The offline expansion accelerated. By July 2024, Nykaa operated 200 stores across 72 cities, including tier-2 cities like Dehradun, Jaipur, Amritsar, and even Rourkela. The target: 180 outlets by 2024 was exceeded. This wasn't just about presence—each store was a marketing vehicle, a customer acquisition tool, a brand builder.

Financial Performance

The numbers vindicated the strategy. Starting with a revenue of only a little more than five billion Indian rupees, the yearly revenue amounted to over 64 billion rupees in the fiscal year 2024. Starting with a revenue of only a little more than five billion Indian rupees, the yearly revenue amounted to over 64 billion rupees in the fiscal year 2024. More impressively, profitability was maintained while investing in growth.

Nykaa's revenue from operations grew 24.1% to Rs 6,386 crore in FY24 from Rs 5,144 crore in FY23, its consolidated financial statements disclosed in the stock exchange filing show. The 24% scale and prudent cost mechanism helped Nykaa post a 90.5% increase in profit to Rs 40 crore in FY24 from Rs 21 crore in FY23.

The owned brands story was particularly compelling. Dot & Key achieved a GMV run rate of ₹600 crore. Kay Beauty grew 39% year-on-year. These weren't just margin enhancers—they were becoming destination brands in their own right.

International Expansion

Apparel Group, a leading retail conglomerate in the GCC, and Nykaa, India's largest, multi-billion-dollar omni-channel beauty retailer, proudly celebrated the grand opening of their inaugural Nysaa store in the GCC region at City Centre Mirdif on Friday, 1st March 2024. This significant event marked the successful beginning of a joint venture setup signed by two retail giants, blending Apparel Group's retail prowess in the GCC region with Nykaa's beauty expertise to offer a carefully curated, world-class shopping experience for consumers in Dubai.

The Middle East strategy was ambitious. Nykaa aims to open 70 stores in the GCC market under the Nysaa brand in the next five years. The company aims to achieve a 7% share in the GCC beauty market during this period, the company said during its 'Annual Investor Day'. The region has per capita spend of a whopping $500 on beauty and personal care products, one of highest globally.

IX. Porter's Five Forces Analysis

1. Threat of New Entrants: HIGH

The beauty e-commerce space has become a battlefield. Taking on listed giant Nykaa, oil-to-telecom conglomerate Reliance on Wednesday (April 5) announced the launch of its omnichannel beauty retail platform Tira. The launch event saw the company unveil the app and website for Tira as well as a 4,300 sq. ft. flagship store in Mumbai's Bandra Kurla Complex.

Reliance's Tira isn't just another competitor—it's an existential threat. Within its first year, Tira opened 11 stores and leveraged Reliance's 18,000+ retail touchpoints. If Reliance were to do nothing but just put a Tira kiosk in each of these stores, its physical distribution network would become 124 times that of Nykaa.

2. Bargaining Power of Suppliers: MODERATE

The exclusive partnerships that once defined Nykaa are eroding. When Dubai-based makeup artist Huda Kattan's brand Huda Beauty first came to India in January 2018, it inked an exclusive partnership with the largest online beauty platform in the country at the time — Nykaa. Cut to 2024, and Nykaa... The brand is now available on multiple platforms including Tira and Myntra. International brands have options, and they're exercising them.

But Nykaa's scale—3,400+ brands—still provides negotiating leverage. They're not just a retailer; they're a gateway to Indian consumers, with data and insights brands need.

3. Bargaining Power of Buyers: HIGH

Indian consumers are notoriously price-sensitive and increasingly omnichannel. They'll research on Nykaa, price-check on Amazon, and might buy on quick commerce for instant gratification. Loyalty is earned daily, not assumed.

The younger consumers in tier-2 and tier-3 cities are even more complex: aspirational yet practical, brand-conscious yet value-seeking, digital-native yet wanting physical experiences.

4. Threat of Substitutes: MODERATE

Traditional retail still commands 42% of beauty sales. The local cosmetics store, the trusted parlor aunty, the department store counter—these aren't disappearing. Direct-to-consumer brands are proliferating. Social commerce through Instagram and WhatsApp is growing. Each is a substitute for Nykaa's model.

5. Competitive Rivalry: INTENSE

While Nykaa has the advantage of being the first mover in many areas and commands a 25-30% market share in the online BPC market, new players have some tricks up their sleeves which might cause unease if not threaten Nykaa's position. Nykaa currently boasts the largest portfolio of brands in beauty and personal care in India with over 3,400 brands.

But the competitive landscape is fracturing. For example, Myntra will do very well in some categories but not all categories, Tata CLiQ palette has a very geo-specific approach, Purplle is very tier 2 and 3, Tira is trying to be premium, Nykaa even today is actually a little bit of everything.

X. Hamilton's Seven Powers Framework

Powers Nykaa Has:

1. Scale Economies: With 3,400+ brands and 200+ stores, Nykaa enjoys scale in procurement, logistics, and marketing that smaller players can't match. Every additional customer reduces per-unit costs.

2. Switching Costs: The Nykaa beauty profile, purchase history, reward points, and personalized recommendations create friction for customers considering alternatives. The app has become habit-forming for millions.

3. Network Effects: Through engaging and educational content, digital marketing, social media influence, robust CRM strategies, and the Nykaa Network community platform, Nykaa has built a loyal community of millions of beauty and fashion enthusiasts. More users create more content, attracting more brands, attracting more users.

4. Counter-positioning: The inventory model versus marketplace approach was counter-positioning against Amazon/Flipkart. By choosing the harder, capital-intensive path, they built a moat around authenticity.

Powers Nykaa Lacks:

5. Cornered Resource: Nykaa doesn't own any exclusive technology, supply chain, or resource that competitors can't replicate. Their advantages are operational, not structural.

6. Process Power: While Nykaa has built sophisticated operations, nothing about their process is inherently unreplicable. Given enough capital and time, competitors can build similar capabilities.

7. Branding: Strong, but not insurmountable. Sephora carries global prestige. Tira has Reliance's trust. The brand moat is real but not impenetrable.

XI. Bull Case vs. Bear Case

Bull Case:

India is where China was 15 years ago in beauty adoption. According to research, the Indian beauty market which currently stands at USD 19 billion, is expected to accelerate by 5x, presenting a staggering 90 billion opportunity to Nykaa. The BPC e-commerce market is expected to grow from 3 billion to 40 billion in 2037. As the share of upper & middle income households grows in India, the premium BPC market is expected to grow by 25% CAGR in the next 15 years.

International brands are prioritizing India as China becomes challenging. Post-COVID, the "self-care" movement has accelerated beauty adoption. Gen Z treats skincare as essential, not optional.

Nykaa's omnichannel advantage is real and hard to replicate. Nykaa's beauty vertical, which competes with Reliance's Tira and Abu Dhabi Investment Authority-backed Purplle, clocked a 24% rise in revenue at Rs 1,702.9 crore, while GMV grew 29% in the second quarter. They're not just surviving competition—they're thriving despite it.

Bear Case:

Regardless of the moves being made by competitors, Nykaa's market share is unlikely to be disrupted in a big way, Taurani says. "The challenge is for them to move beyond the 25-30% (market share). With quick commerce, vertical players, horizontal-based super apps doing BPC, I don't see Nykaa gaining more market share. I think in a realistic scenario, they can only maintain market share," he said.

The fashion vertical continues to struggle against established players like Myntra. High customer acquisition costs in a competitive market. Quick commerce changing consumer expectations—why wait two days when you can get it in 10 minutes?

Governance concerns post-IPO have damaged institutional investor confidence. The bonus share controversy wasn't just bad optics—it revealed a company still thinking like a private enterprise while operating in public markets.

XII. Key Inflection Points & Strategic Decisions

2012: Starting at 50 with own capital wasn't just about financial prudence—it was about patient capital. No VC pushing for growth at all costs, no pressure for quick exits.

2015: The omnichannel pivot before omnichannel was cool showed remarkable foresight. While pure-play e-commerce players were mocking physical retail as outdated, Nykaa understood beauty's experiential nature.

2015: Private label launch transformed unit economics. This wasn't just margin expansion—it was about owning the full stack, controlling the customer experience end-to-end.

2019: Kay Beauty, which launched as a joint venture with India's biggest beauty retailer Nykaa in 2019. Six years on (and about 26 in the making), the line has become India's fastest-growing celebrity-founded beauty label, scaling up 56 percent year-on-year to ₹2.5 billion ($28.6 million) in gross merchandise value. Celebrity partnerships done right—not just endorsement but co-creation.

2020: Achieving profitability during a pandemic when everyone else was bleeding cash demonstrated the resilience of the model and the discipline of management.

2021: IPO timing at peak valuations was masterful financial engineering. They caught the perfect window between COVID recovery optimism and tech winter.

2024: Commenting on the landmark moment, Falguni Nayar, Executive Chairperson, Founder & CEO, Nykaa, added, "Nysaa's first store in Dubai marks a significant milestone in our international foray. Our partnership with Apparel Group is a powerful collaboration of Nykaa's beauty leadership in India and their retail expertise in the GCC region. International expansion provides new growth vectors as domestic competition intensifies.

XIII. Playbook: Lessons for Founders & Investors

For Founders:

Category Creation Over Competition: Nykaa didn't compete with existing beauty retail—they created online beauty commerce in India. Find markets with structural inefficiencies, not just better mousetraps.

Content-Commerce Convergence: In experience categories, education drives adoption. Nykaa spent as much on content as logistics early on. The BeautyBook wasn't marketing—it was infrastructure.

Bootstrapping Discipline With Scale Ambition: Starting with your own capital enforces discipline, but don't let it limit ambition. Falguni waited three years before raising institutional capital, but when she did, she scaled aggressively.

Timing Isn't Everything, Execution Is: Starting at 50 in a "young person's game" didn't matter. Domain expertise, patient capital, and execution excellence matter more than founder age or timing.

Vertical Integration As Competitive Advantage: Private labels aren't just about margins—they're about differentiation, data ownership, and customer lock-in.

For Investors:

Founder Quality Trumps Everything: She has over 26 years of experience in e-commerce, investment banking and broking. Prior to founding Nykaa, she was associated with Kotak Mahindra Capital Company Limited for 18 years where she also served as a managing director. Domain expertise matters more than startup experience.

Market Timing Is About Penetration, Not Existence: India's beauty market existed for decades. What changed was internet penetration, smartphone adoption, and female workforce participation. Look for structural shifts, not surface trends.

Omnichannel Is The End State: Pure-play digital might win initially, but experience categories eventually demand physical presence. Fund companies with omnichannel DNA, not digital-only dogma.

Profitability Matters, Eventually: Nykaa proved you can grow fast and be profitable. In categories with good unit economics, there's no excuse for perpetual losses.

Competition Is A Validation, Not A Threat: Reliance entering beauty e-commerce validates the market size. First-mover advantage is real but execution advantage is more durable.

XIV. What Could Kill Nykaa?

Quick Commerce Revolution: If buying beauty products becomes as instant as ordering groceries, Nykaa's 2-day delivery advantage evaporates. Blinkit, Zepto, and Swiggy Instamart are already experimenting with beauty. The question isn't if but when.

Platform Shifts: Gen Z doesn't shop like millennials. They discover on Instagram, research on YouTube, buy on WhatsApp. If commerce moves entirely to social platforms, Nykaa's destination site model breaks.

Conglomerate Competition: It is no wonder that Reliance Retail will look at disrupting the market to emerge as a market leader as it has done in every segment. Reliance has infinite capital, existing retail footprint, and a history of category domination. Tata has brand trust and operational excellence.

International Giants Going Direct: Sephora entering India independently (Reliance acquired rights in 2023), Ulta Beauty's eventual entry, or Amazon creating a beauty vertical could fragment the market further.

Fashion Failure: The fashion vertical continues to be a drag on profitability and focus. If it becomes a money pit requiring constant investment without returns, it could derail the core beauty business.

Generational Shift: Gen Alpha might not want their mother's beauty platform. New brands, new platforms, new shopping behaviors could make Nykaa irrelevant to the next generation.

XV. Epilogue: The Nykaa Legacy

Nykaa's story transcends business metrics. In 2020, it became the first Indian unicorn startup headed by a woman. They proved that Indian companies could be profitable and high-growth, that 50 is not too late to start, that category creation beats competition.

They fundamentally changed how 1.4 billion Indians think about beauty. Pre-Nykaa, beauty was guilt, frivolity, Western corruption. Post-Nykaa, it's self-care, empowerment, expression. They didn't just sell lipstick—they sold permission to be beautiful on your own terms.

The template they created—content-commerce, omnichannel, private label, celebrity partnerships—is now the playbook everyone follows. When Reliance, with all its might, chooses to copy your model rather than reinvent it, you know you've built something foundational.

But the ultimate question remains: Can Nykaa maintain leadership as the category matures? As competition intensifies, margins compress, and growth slows, will they find the next S-curve? Can they expand internationally successfully? Will fashion ever work?

Falguni Nayar, Executive Chairperson, Founder and CEO Nykaa said, "Nykaa's success so far has been rooted in driving quality growth by foreseeing the potential in the lifestyle ecosystem and making future-forward investments. Our conviction and efforts in beauty over the last decade is now reflected in a market bound to become a 90 billion-dollar market over the next 15 years, with Nykaa continuing its industry-leading growth.

The answer might lie not in what Nykaa becomes, but in what it has already achieved. Sometimes, the greatest companies aren't the ones that dominate forever, but the ones that create categories, change cultures, and inspire others to dream bigger. By that measure, Nykaa has already won.

The investment banker who helped others IPO built something worth taking public. The woman who started at 50 proved age is just a number. The company that everyone said wouldn't work—selling beauty online in India—became the template everyone copies.

That's not just a business success. That's a redefinition of what's possible. And in the end, isn't that what the best entrepreneurs do? They don't just build companies. They expand our conception of what can be built.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube