NUVOCO: The Story of India's Fifth-Largest Cement Empire

I. Introduction & Episode Roadmap

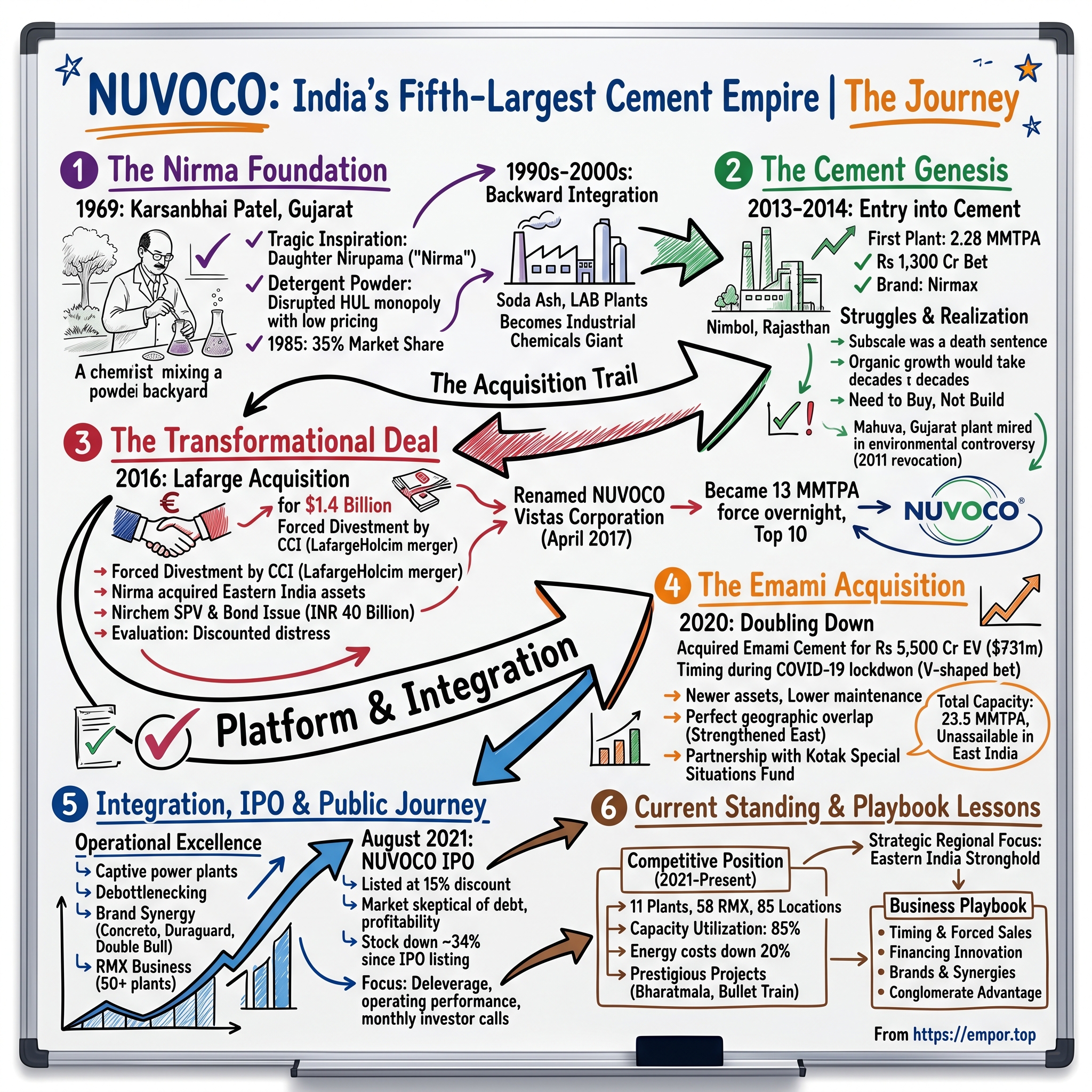

Picture this: A chemist in Gujarat, making detergent powder in his backyard, names it after his daughter who tragically died in a car accident. Fast forward five decades, and that same entrepreneur's empire now produces 23.82 million tonnes of cement annually, enough to build 40 Burj Khalifas every year. This is the unlikely journey of how Karsanbhai Patel's Nirma Group built NUVOCO—India's fifth-largest cement company through three audacious acquisitions in just five years.

The question that should fascinate any student of business strategy is this: How did a company that disrupted Hindustan Unilever in detergents pivot to become a cement powerhouse? And more intriguingly, why did they choose cement—one of the most capital-intensive, cyclical, and competitive industries in India?

NUVOCO's story isn't just about industrial expansion. It's a masterclass in opportunistic M&A, creative financing, and the art of buying distressed assets when global giants are forced to divest. Between 2016 and 2020, Nirma executed a triple play: acquiring Lafarge India for $1.4 billion, integrating those operations, then doubling down with the Emami Cement acquisition for another $731 million. The result? A company that went from zero cement capacity in 2013 to becoming a top-five player controlling critical infrastructure projects across India.

But here's where it gets interesting for investors: Despite this empire-building, NUVOCO's stock has fallen 34% since its 2021 IPO. The market clearly isn't buying the growth story—yet. Is this a value trap or a contrarian opportunity? To answer that, we need to understand how a detergent magnate became a cement baron, and whether the Nirma playbook that disrupted consumer goods can work in industrial commodities.

This episode traces three distinct eras: the Nirma foundation that created the war chest, the aggressive acquisition spree that built the platform, and the public markets reality check that's testing the thesis. Along the way, we'll unpack the financing innovations, integration challenges, and strategic pivots that transformed a single plant in Rajasthan into an industrial empire spanning 85 locations across India.

II. The Nirma Foundation: From Detergents to Diversification

In 1969, Karsanbhai Patel was just another government chemist in Gujarat's Mineral Development Corporation, earning ₹500 a month. But in his spare time, he was cooking up something revolutionary in his 100-square-foot backyard: a phosphate-free detergent powder that would eventually dethrone Hindustan Unilever's monopoly. The tragedy that sparked this innovation? His daughter Nirupama had died in a car accident, and he named his creation after her—Nirma, a portmanteau that would become synonymous with Indian entrepreneurial disruption.

The genius wasn't in the chemistry—it was in the pricing. While HUL's Surf commanded ₹13 per kilogram, targeting India's elite, Patel priced Nirma at ₹3.50. This wasn't just undercutting; it was market creation. He wasn't competing for HUL's customers; he was creating an entirely new category of consumers who had never bought packaged detergent before. By 1985, Nirma had captured 35% market share, forcing the multinational giant to launch Wheel as a defensive response.

But the detergent success contained the seeds of its own limitations. Local manufacturers began flooding the market with copycat products. Unlike HUL with its portfolio spanning premium to mass segments, Nirma was stuck in the value segment with limited pricing power. The brand that had disrupted the market was now being disrupted itself. Market share began eroding, not dramatically, but steadily enough to force a strategic rethink. Patel's response was classic conglomerate strategy: backward integration. By the early 2000s, Nirma had built soda ash and linear alkyl benzene (LAB) plants—the key ingredients in detergents. After the fall in market share, Nirma, which went for backend integration in the 1990s when it set up soda ash and linear alkyl benzene (LAB) plants, the key ingredients in soaps, started to behave like a commodity producer rather than an FMCG company. In 2007, they acquired US-based Searle Valley Minerals, making them one of the world's largest soda ash producers. The company that had disrupted FMCG was morphing into an industrial chemicals giant.

This transformation wasn't just defensive—it was prescient. Nirma had around 60% market share by then, selling more than 1.72 lakh tonnes. But by the 2010s, market share of the company had fallen to just 6%. The writing was on the wall: the detergent business that had created the empire was no longer the growth engine. Patel needed a new act. By today's scenario, Nirma Ltd. created the benchmark of the largest Soda Ash production per month in India, at its Chemical Complex at Bhavnagar, Gujarat with the production of 83,000 tonne Soda Ash production per month. Nirma, together with Saukem which was recently acquired by its associate Nirma Chemical Works Limited, is the largest producer of synthetic soda ash in India with a capacity of about one million tonnes per annum. The new acquisition will place Nirma among the top seven world producers of soda ash at a combined annual capacity in excess of two million tonnes.

What's fascinating here is the strategic pivot: as the consumer business declined, the industrial business thrived. The chemicals that were once inputs became the outputs. The company that had disrupted HUL was now supplying raw materials to its competitors. It was a masterclass in corporate evolution—when your front door closes, build a factory out the back.

This sets up our cement story perfectly. Because what Patel had learned from chemicals—that commodity businesses with scale and backward integration could generate stable cash flows—would become the template for his next conquest. The detergent magnate was about to become a cement baron.

III. The Cement Genesis: Nimbol and Early Struggles (2014–2016)

In November 2014, a convoy of trucks rolled into Nimbol, a dusty village in Rajasthan's Nagaur district. They carried the first equipment for what would become Nirma's maiden cement plant—a Rs 1,300 crore bet that a detergent company could crack one of India's most capital-intensive industries. The 2.28 million tonne facility wasn't just a diversification; it was a declaration of intent.

Nirma Group started cement manufacturing in 2014 from a single plant in Nimbol, with a newly established company Nuvoco Vistas Corporation. The timing seemed perfect. India's infrastructure boom was accelerating, cement demand was growing at 8-10% annually, and the industry was ripe for consolidation. But Patel's team quickly discovered that making cement wasn't like making detergent—you couldn't just undercut prices and grab market share.

The first reality check came from Gujarat. Nirma had ambitious plans for a 2 million tonne plant in Mahuva, leveraging proximity to their chemical operations. But environmental activists had other ideas. They claimed the plant would damage critical wetlands, launching protests and legal challenges that would drag on for years. In 2003, it announced plans for cement, but by 2016, the Gujarat plant was still mired in controversy, consistently running into trouble with environmentalists. The Mahuva saga would become a decade-long battle. In 2008, the Gujarat government sanctioned to Nirma Limited 268 hectares of land to construct a cement factory and 3,460 hectares for limestone mining. Around 5,000 people protested against the loss of agricultural land, which farmers used for onion and cotton cultivation. The Union Ministry of Environment and Forests (MoEF) on December 1, 2011 revoked the Environment Clearance it had granted to Nirma in 2008. While the National Green Tribunal would eventually overturn this in 2015, the damage was done—years lost, millions spent, reputation tarnished.

Meanwhile, the Rajasthan plant was operational but struggling. Without the Gujarat capacity, Nirma couldn't achieve the scale needed to compete with giants like UltraTech and ACC. The brand they had launched—Nirmax—was gaining traction in Northern and Western India, but 2.28 million tonnes was a rounding error in a market consuming 270 million tonnes annually.

The strategic rationale for cement was sound. Nirma supplementing its mainstream activity of FMCG and chemicals, Nirma is also setting up a 1.5 million tonne cement plant in Mahua, Bhanvagar district of Gujarat—this had been the plan since 2003. De-risking from detergents made sense. Leveraging their soda ash operations for vertical integration was logical. But execution was proving harder than strategy.

What Patel and his team realized was that organic growth in cement would take decades. In an industry where scale is everything—determining procurement costs, logistics efficiency, and market influence—being subscale was a death sentence. They needed a different approach. They needed to buy, not build.

This realization would lead to the most audacious deal in Nirma's history. Because 5,000 kilometers away in Switzerland, two cement giants were merging, and Indian regulators were about to force them to sell assets. Patel saw opportunity where others saw complexity. The detergent disruptor was about to become a deal-maker.

IV. The Lafarge Acquisition: The Transformational Deal (2016)

On a humid July morning in 2016, investment bankers at Kotak Mahindra's Mumbai office were fielding frantic calls. LafargeHolcim, the world's largest cement company born from a $50 billion mega-merger, had just accepted Nirma's bid for their Indian assets. The price: $1.4 billion. The shock wasn't just the size—it was the winner. How had a detergent company outmaneuvered JSW Cement and the deep-pocketed Piramal Group?

The backstory reads like a regulatory thriller. When Lafarge and Holcim announced their global merger in 2014, creating a cement behemoth with $44 billion in revenue, competition authorities worldwide grew nervous. In India, the Competition Commission (CCI) had a specific concern: the combined entity would dominate Eastern India with over 20% market share. Their solution was surgical—force LafargeHolcim to divest 5.15 million tonnes of capacity, essentially their entire Eastern India portfolio.

For LafargeHolcim, this was a fire sale they couldn't avoid. The global merger couldn't proceed without Indian approval, and India was too important a market to abandon. They needed a buyer, fast. Enter Karsanbhai Patel's son, Hiren, who had been quietly preparing for exactly this moment.

July 11, 2016: $1.4 billion deal announcement at enterprise value sent shockwaves through Dalal Street. The valuation was fascinating: $127 per tonne versus $151 in an aborted Birla Corp deal for similar assets just months earlier. Nirma wasn't paying top dollar—they were buying distress at a discount.

But here's where it gets interesting. Nirma didn't have $1.4 billion lying around. Their solution was financial engineering at its finest. They created a special purpose vehicle called Nirchem and went to the bond market with an INR 40 billion offering. The bonds, offered at 8.68% yield, were oversubscribed within hours. Indian debt investors, starved of quality corporate paper, jumped at the chance to fund a Nirma-backed acquisition. The assets themselves were impressive. Lafarge India operates three cement plants and two grinding stations with a total capacity of around 11 million tonnes per annum. More importantly, 7.8 million tonnes (70%) of this capacity was concentrated in Chhattisgarh, Jharkhand, and West Bengal—the heart of India's infrastructure boom corridor. The company also came with ready-mix concrete operations and an established distribution network.

But the real genius was in the deal structure. Nirma's consolidated adjusted net worth was Rs 3,900 crore and adjusted debt Rs 1,340 crore on March 31, 2016, leading to a debt-equity ratio of just 0.34. This conservative balance sheet gave them the credibility to tap bond markets aggressively. Investment bankers, Nirma will sell bonds worth about Rs 4,000 crore ($596 million) to fund the acquisition.

"This acquisition is a transformational step for the group's cement business. With a strong platform like Lafarge's India business, we plan to take the cement business to the next level," said Hiren Patel, managing director, Nirma. The younger Patel wasn't just buying assets—he was buying time. Building 11 million tonnes of capacity organically would have taken a decade and cost twice as much.

The Competition Commission's approval came through quickly—they were eager to close the LafargeHolcim merger. By the time the deal closed, Nirma had gone from a 2.28 million tonne bit player to a 13 million tonne force, catapulting them into India's top 10 cement producers overnight.

But here's what made this truly brilliant: Nirma didn't just buy capacity, they bought optionality. The Lafarge brand, the established dealer network, the customer relationships—all of this could be leveraged for future growth. And critically, they now had the scale to negotiate better freight rates, optimize logistics, and compete for large infrastructure contracts.

In April 2017, the company was renamed NUVOCO Vistas Corporation, signaling a new chapter. The name itself was strategic—distancing from both Nirma's detergent legacy and Lafarge's foreign origins, creating a fresh identity for the Indian market.

The transformation from detergent maker to cement major was complete. Or so it seemed. Because Hiren Patel had learned something from this deal: in a consolidating industry, the acquirer often becomes the acquired. To stay independent, NUVOCO needed to get even bigger. And another opportunity was about to present itself.

V. Building the Platform: Integration and Growth (2017–2020)

The Monday morning after the Lafarge deal closed, NUVOCO's new management team faced a sobering reality: they had just inherited 11,000 employees across five states, three different ERP systems, and a sales force that still answered the phone "Lafarge India." Integration would make or break the acquisition.

Hiren Patel took an unusual approach. Rather than impose Nirma's culture wholesale, he cherry-picked the best of both worlds. From Nirma came the cost discipline—every expense scrutinized, every efficiency pursued. From Lafarge came the technical expertise and safety protocols befitting a global cement major. The cultural fusion wasn't always smooth. Old-timers from Lafarge's Jojobera plant in Jharkhand bristled at Nirma's frugal travel policies. Nirma veterans struggled with Lafarge's complex reporting structures.

The operational improvements came fast. NUVOCO invested heavily in captive power plants, reducing energy costs by 15% within eighteen months. Debottlenecking initiatives at the Sonadih and Mejia plants added 800,000 tonnes of capacity without major capital expenditure. The company's capacity utilization jumped from 65% to 78% as they optimized production schedules across plants. Brand strategy became crucial. NUVOCO inherited a portfolio headache: Our Cement product portfolio comprising Concreto, Duraguard, Double Bull, PSC, Nirmax and Infracem addresses the complete spectrum. Rather than rationalize immediately, they positioned each for different segments. Concreto became the premium offering in Eastern India. Duraguard, the workhorse brand, targeted the trade segment. Double Bull emerged as the volume play, growing to 5 million tonnes in sales within five years.

The marketing push was aggressive but targeted. In 2019, NUVOCO became title sponsors of the Kolkata Knight Riders IPL team—a masterstroke for brand visibility in their Eastern stronghold. The "Poora Bharosa" (Complete Trust) campaign resonated with contractors who valued consistency over glamour. Trade loyalty programs, dealer financing schemes, and technical support centers sprouted across Bihar, West Bengal, and Jharkhand.

Geographic expansion followed a hub-and-spoke model. From their Eastern base, NUVOCO pushed into adjacent markets—Odisha, then Bihar, then deeper into Uttar Pradesh. They avoided head-to-head battles with UltraTech in Western India, instead focusing on markets where they could leverage proximity to plants for logistics advantage. The ready-mix concrete (RMX) business became a strategic differentiator. With more than 50+ plants across India, we are one of the leading industry players in the Ready-mix Concrete (RMX) industry. This wasn't just about selling cement in liquid form—it was about capturing value higher up the chain and building direct relationships with developers. The RMX network grew from 20 plants inherited from Lafarge to 58 plants by 2020, each one a forward integration play that improved margins and customer stickiness.

Innovation emerged from unexpected places. The Construction Development and Innovation Centre in Mumbai, a Lafarge legacy asset, began churning out specialized products. Duraguard WaterSeal Cement received India's first patent for water-resistant cement composition. The Ecodure line of green concrete tapped into the sustainability trend. These weren't volume plays—they were margin enhancers that justified premium pricing.

The numbers told the integration story. Revenue grew from Rs 5,500 crore in FY2017 to Rs 8,900 crore in FY2020. EBITDA margins improved from 12% to 16%. The Eastern market share solidified at around 15%, making NUVOCO the clear number two behind UltraTech. The platform was built. The integration was working.

But Hiren Patel wasn't satisfied. The cement industry was consolidating rapidly—UltraTech had acquired Century Textiles' cement business, Binani Cement, and was eyeing more targets. To remain independent, NUVOCO needed more scale. And in February 2020, just as the world was about to shut down for COVID-19, another opportunity presented itself: Emami Group wanted out of cement.

VI. The Emami Cement Acquisition: Doubling Down (2020)

On February 6, 2020, as news of a mysterious virus in Wuhan dominated headlines, NUVOCO's board was focused on something else entirely: acquiring Emami Cement for an enterprise value of Rs 5,500 crore. The timing seemed either brilliant or insane—nobody was quite sure which.

The Emami Group, famous for Boroplus and Navratna oil, had entered cement in 2006 through acquisitions, building an 8.3 million tonne portfolio across Bihar, Chhattisgarh, and Odisha. But cement had always been a financial investment for them, not a strategic commitment. With debt mounting and core FMCG businesses needing capital, they wanted an exit. Emami receiving US$731m for divestment would solve multiple problems at once.

NUVOCO's due diligence team, working through nights in Kolkata's Oberoi Grand hotel, discovered both opportunities and landmines. The assets were newer than Lafarge's, with lower maintenance requirements. The market overlap was perfect—strengthening NUVOCO's Eastern dominance without regulatory concerns. But the dealer network was weak, brand recognition minimal, and two plants were running at barely 50% utilization.

The financing structure showed how much NUVOCO had learned from the Lafarge deal. This time, they brought in a partner: Kotak Special Situations Fund investing INR 5 billion for financing. The private equity investment wasn't just about money—it was validation from sophisticated investors that the consolidation thesis was sound. The Rs 250 crore escrow deposit showing commitment demonstrated serious intent to skeptical sellers.

Then COVID-19 hit. March 2020 saw India enter the world's strictest lockdown. Construction stopped. Cement demand evaporated. The Emami board wavered—should they pull out? Wait for better times? But NUVOCO pressed ahead, arguing that the post-COVID infrastructure boom would be unprecedented. They were betting on a V-shaped recovery that many thought impossible.CCI approval in May 2020 was surprisingly smooth. The Competition Commission of India (CCI) approves acquisition of 100% of the total issued and paid-up share capital of Emami Cement Limited, on a fully diluted basis, by Nuvoco Vistas Corporation Limited. The combined operations will span three facilities in Chhattisgarh, two each in Rajasthan and West Bengal and one each in Bihar, Jharkhand, Odisha and Haryana. Unlike the Lafarge deal with its Eastern market concentration concerns, this was seen as healthy consolidation.

Deal completion July 14, 2020 came in the middle of India's lockdown. The integration team worked virtually, conducting plant visits via video calls, dealer meetings on Zoom. It was surreal—completing a $731 million acquisition without the principals ever meeting in person during the final stages.

Total capacity reaching 23.5mtpa post-acquisition made NUVOCO unassailable in Eastern India. But more importantly, it gave them critical mass for the next phase: going public. The combined entity now had the scale, geographic diversity, and growth trajectory that public market investors demanded.

The post-COVID recovery that NUVOCO had bet on materialized faster than expected. By Q3 2020, cement demand was roaring back, driven by rural housing, infrastructure spending, and pent-up urban demand. The Emami plants that had been running at 50% utilization were suddenly maxed out. Pricing power returned to Eastern markets as demand outstripped supply.

But here's what made the Emami deal truly strategic: it wasn't just about cement capacity. Emami came with limestone reserves, railway sidings, and most crucially, relationships with Eastern India's political and business establishment. In a business where permits, environmental clearances, and government contracts matter, these soft assets were invaluable.

The financing structure also evolved NUVOCO's capital markets sophistication. Bringing in Kotak's special situations fund as an equity partner pre-IPO was deliberate positioning. They were building a cap table that would appeal to public market investors—credible institutional backing that validated both the business model and the valuation.

By early 2021, the integration was ahead of schedule. The Emami plants were rebranded under NUVOCO's portfolio. Operational synergies of Rs 150 crore annually were identified and being captured. The dealer network was consolidated, eliminating overlaps and improving coverage. Most importantly, NUVOCO now controlled nearly 20% of Eastern India's cement capacity, making them the undisputed regional champion.

The stage was set for the next act: taking NUVOCO public. After two transformational acquisitions funded largely through debt, the balance sheet needed equity. And the Nirma family, after pouring billions into cement, wanted partial liquidity. The IPO would be the culmination of the seven-year journey from Nimbol's dusty construction site to Dalal Street's trading floors.

VII. The IPO and Public Markets Journey (2021)

The IPO roadshow in July 2021 was unlike any other. Fund managers joined virtually from Mumbai, Singapore, and London, while NUVOCO's management presented from a makeshift studio in Ahmedabad. COVID's second wave had just receded, and nobody was traveling. The pitch was simple: India's fifth-largest cement company, Eastern India dominance, two successful integrations completed, ready for the next growth phase.

The numbers looked compelling on paper. IPO timeline: August 9-11, 2021 bidding, listing August 23, 2021. The price band at ₹570 per share valued the company at approximately Rs 20,000 crore—reasonable by cement sector standards at around $115 per tonne of capacity. The offer included fresh equity of Rs 1,500 crore to reduce debt and provide growth capital.

But the roadshow revealed uncomfortable questions. Why had the company reported Net loss of 25.92 crores in 2021 vs profit of ₹249.25 crores in 2020? Management explained it as one-time integration costs and COVID impact, but investors weren't fully convinced. The debt levels, though manageable, were higher than peers. The Eastern India focus, while a strength, also meant exposure to a cyclical, price-competitive market.

Subscription details: 1.71x overall (QIB 4.23x, NII 0.66x, Retail 0.73x) told the real story. Qualified institutional buyers showed interest, but retail and high-net-worth individuals were skeptical. This wasn't the blockbuster IPO that investment bankers had promised. The grey market premium, usually a reliable indicator of listing performance, was negligible.

Disappointing listing: ₹485 on NSE, ₹471 on BSE—a 15% discount to the issue price. For retail investors who had bet on the Nirma brand and the cement story, it was a rude shock. The stock fell further in subsequent sessions, eventually finding support around ₹400. The market's message was clear: prove the integration story, show consistent profitability, then we'll reconsider. The post-IPO period became a reality check. Market cap fell from Rs 20,000 crore at issue to around Rs 13,000 crore within months. Analysts who had been bullish during the roadshow turned cautious. The criticism was consistent: too much debt, inconsistent profitability, unclear growth strategy, and overreliance on a single region.

Management's response was to focus on fundamentals. Debt reduction became priority one, with Rs 1,350 crore from IPO proceeds immediately deployed. Operational efficiency programs accelerated. The company began monthly investor calls—unusual for Indian companies—to rebuild credibility. Transparency improved, with detailed segment reporting and volume disclosures.

But the deeper issue was strategic. NUVOCO had built scale through acquisitions, but organic growth remained tepid. The Eastern India market, while their stronghold, was becoming increasingly competitive with new capacity additions from Dalmia Bharat and Shree Cement. Pricing power, the holy grail of the cement business, remained elusive.

The public markets journey taught NUVOCO a harsh lesson: being big isn't enough. Investors wanted predictable earnings growth, improving returns on capital, and a clear path to industry-leading margins. The company that had transformed from detergent maker to cement major now faced its next transformation: from deal-maker to operator.

Stock down 34% since IPO listing became a constant overhang. Every quarterly result was scrutinized for signs of turnaround. Every competitor announcement triggered questions about market share. The freedom of being private, where long-term bets could play out without quarterly scrutiny, was gone. Welcome to the public markets, where patience is measured in quarters, not years.

VIII. Modern Operations and Competitive Position (2021–Present)

Walking through NUVOCO's Jojobera plant in 2024 feels like stepping into the future of Indian cement manufacturing. Automated quality control systems monitor every batch. AI-powered predictive maintenance prevents breakdowns before they happen. The contrast with the manual operations of just five years ago is stark. This operational transformation has become NUVOCO's answer to investor skepticism.

Current footprint: 11 cement plants, 58 RMX plants, 16 offices across 85 locations represents one of India's most extensive cement networks. But it's the efficiency metrics that tell the real story. Capacity utilization has reached 85%, up from 65% at the time of the Lafarge acquisition. Energy costs per tonne have dropped 20% through alternative fuel usage and waste heat recovery systems.

Product portfolio: 60+ products from Construction Development and Innovation Centre sounds impressive, but the real innovation is in application engineering. NUVOCO's technical teams now sit with infrastructure contractors during project planning, recommending specific cement grades for different structures. This consultative selling approach has helped them win contracts for Prestigious projects: Bharatmala Pariyojana, Mumbai-Ahmedabad bullet train, Western Dedicated Freight Corridor. Brand portfolio: Concreto, Duraguard, Double Bull, PSC, Nirmax, Infracem has evolved from mere product names to distinct value propositions. Duraguard has emerged as the workhorse, Nuvoco's flagship brand Duraguard is one of the most popular cement brands in the Northern and Eastern markets of India. Double Bull, launched as a value brand, has surprised everyone by capturing 5 million tonnes in annual sales within five years—proof that the Nirma DNA of value pricing still works.

The competitive landscape remains brutal. Competition with UltraTech, ACC, Ambuja, Shree Cement intensifies every quarter. UltraTech, with over 130 million tonnes capacity, operates at a different scale altogether. Adani's aggressive expansion through Ambuja and ACC has added new pressure. But NUVOCO has found its niche: regional dominance strategy in Eastern India where they control approximately 15-20% market share versus single-digit shares nationally.

Digital transformation has quietly revolutionized operations. The "Nuvo Nirmaan" digital platform connects 20,000+ dealers directly to the company, eliminating intermediaries and improving margins. Real-time inventory tracking across plants prevents stockouts. Dynamic pricing algorithms optimize realization based on local market conditions. These aren't headline-grabbing innovations, but they're adding 2-3% to EBITDA margins.

Sustainability initiatives, once seen as compliance burden, have become competitive advantages. Alternative fuel usage has reached 9%, reducing both costs and carbon footprint. The company's cement-to-clinker ratio of 1.8 is among the best in the industry, meaning they produce more cement from less energy-intensive clinker. Green products like Ecodure command premium pricing from environmentally conscious developers. Financial performance tells a recovery story. Revenue from operations grew 8.96% YoY to Rs 2,872.70 crore during the quarter. Consolidated EBITDA improved by 35% y/y to Rs. 16.57 billion. The company reduced net debt by Rs. 3.84 billion y/y to Rs. 40.3 billion, resulting in net debt/EBITDA of 2.4x. After years of integration costs and one-time charges, the underlying business is finally showing its potential.

Current market cap: 15,142 Crore reflects cautious optimism. Yes, it's up from the IPO lows, but still below the issue price valuation. The market is waiting for consistent execution, not promises. Every quarter without a negative surprise builds credibility. Every basis point improvement in EBITDA margin gets noticed.

The regional focus is paying dividends. While pan-India players fight price wars, NUVOCO's Eastern stronghold provides stability. Infrastructure projects in Bihar, West Bengal, and Jharkhand are accelerating. The company's proximity to these markets—with plants within 200 kilometers of major consumption centers—provides a 10-15% logistics cost advantage over competitors shipping from distant locations.

Looking ahead, the strategy is clear: dominate the East, selectively expand in North, avoid head-to-head battles elsewhere. The recent announcement of a new grinding unit in Gujarat signals measured expansion, not empire-building. Management has learned that in cement, as in detergents, disciplined growth beats aggressive expansion.

The transformation from acquisitive growth to operational excellence is ongoing. But for the first time since the IPO, NUVOCO is being valued on its fundamentals rather than its story. The market may not love it yet, but it's starting to respect it.

IX. Playbook: Business & Investing Lessons

If you stripped away the corporate speak and financial jargon, NUVOCO's journey from detergent to cement teaches a masterclass in conglomerate strategy that would make even Warren Buffett take notes. The playbook isn't just about diversification—it's about timing, financing creativity, and the patient accumulation of industrial assets when others are forced to sell.

The Nirma way: From FMCG disruption to industrial consolidation represents a uniquely Indian approach to empire-building. Start with a cash-generative consumer business, use those cash flows to enter capital-intensive industries during downturns, then consolidate when global players face regulatory pressure. It's not sexy, but it works. The detergent business that everyone wrote off as declining? It funded two billion-dollar cement acquisitions.

Acquisition strategy: Buying distressed/forced sales at reasonable valuations is where NUVOCO separated itself from ego-driven conglomerates. The Lafarge deal at $127 per tonne when the previous buyer had agreed to $151. The Emami acquisition during COVID when nobody else would commit capital. These weren't opportunistic punts—they were calculated bets on assets with strong underlying fundamentals but temporary ownership issues.

Financing innovation: Bond markets, special purpose vehicles, PE partnerships showed sophistication rarely seen in Indian family businesses. The INR 40 billion bond issue for Lafarge wasn't just large—it was structured to minimize dilution while maintaining control. Bringing in Kotak's special situations fund for Emami provided validation and risk-sharing. This wasn't the typical promoter approach of either full equity or bank debt.

Integration playbook: Maintaining brands while extracting synergies solved the classic acquisition dilemma. Rather than rebranding everything to NUVOCO overnight, they kept Concreto, Duraguard, and Double Bull as distinct propositions while consolidating backend operations. Customer relationships remained intact while procurement, logistics, and overhead costs were ruthlessly optimized. The result: Rs 150 crore in annual synergies without market share loss.

Capital structure management: 0.34 debt-equity ratio pre-Lafarge gave them the balance sheet capacity to execute transformational deals. While competitors were overleveraged from organic expansion, NUVOCO had dry powder. This conservative approach to leverage—unusual for Indian promoters—provided flexibility when opportunities arose. Post-acquisitions, the focus immediately shifted to deleveraging, bringing net debt/EBITDA down to 2.4x.

Building in challenging markets: Environmental issues, regulatory approvals became competitive moats once overcome. The decade-long battle for the Mahuva plant taught painful lessons but also built institutional knowledge about navigating India's complex approval maze. This expertise became valuable when integrating acquired plants with their own compliance challenges.

The conglomerate advantage: Group backing and patient capital enabled long-term bets that public companies couldn't make. When the cement business posted losses, the profitable chemicals division provided cover. When environmental clearances delayed projects, the group had the patience to wait. This cross-subsidization and time arbitrage is the hidden superpower of well-run conglomerates.

But here's the contrarian lesson: sometimes the best strategy is not having a strategy. NUVOCO didn't enter cement with a master plan to become the fifth-largest player. They started with one plant, learned the business, then seized opportunities as they arose. This optionality-preserving approach—maintaining financial flexibility to act when others can't—might be the most valuable lesson.

The mistakes are equally instructive. The Mahuva environmental debacle showed the dangers of underestimating stakeholder opposition. The disappointing IPO pricing revealed that financial engineering can't substitute for consistent operating performance. The post-IPO stock performance demonstrates that market credibility takes years to build but moments to destroy.

For investors, NUVOCO presents a fascinating case study in multiple expansion potential. Trading at significant discount to larger peers despite similar assets and market positions, the stock is essentially a bet on execution. Can a promoter-driven, acquisition-led company transform into a professionally-managed, organically-growing institution? The jury's still out.

The deeper insight is about India's unique business environment. In developed markets, conglomerates trade at discounts. In India, they can be advantages—providing access to capital, regulatory relationships, and risk diversification that focused players lack. NUVOCO leveraged all three to build a cement empire from a detergent base.

The ultimate lesson might be about business mortality and reinvention. Nirma's detergent business, once a Harvard case study, is now a shadow of its former self. But instead of clinging to past glory, Patel built something entirely new. It's creative destruction at the corporate level—killing your old business model before the market does it for you.

X. Analysis & Bear vs. Bull Case

The investment case for NUVOCO splits the room like few other stocks on the Indian market. Bulls see a discount to replacement cost and a regional monopoly in the making. Bears see a leveraged bet on a cyclical industry with questionable capital allocation. Both sides have compelling data to support their thesis.

Bull Case:

Fifth-largest player with consolidation opportunity in an industry where scale determines survival. India's cement industry is still fragmented compared to global standards, with the top five players controlling only 55% market share versus 70-80% in developed markets. NUVOCO's 23.82 MMTPA capacity positions them perfectly for the next wave of consolidation—large enough to be a consolidator, not so large as to face antitrust issues.

Eastern India dominance with room for growth presents a defensible moat. The region contributes 20% of India's cement demand but is growing faster than the national average due to infrastructure catch-up. NUVOCO's ~20% market share in the East, backed by local manufacturing presence, creates pricing power that western-focused players can't match. The logistics advantage alone—saving Rs 200-300 per tonne versus competitors—provides a structural margin benefit.

Nirma Group backing providing stability isn't just about capital—it's about staying power. Unlike PE-owned cement assets that need exits, or listed companies facing quarterly pressures, NUVOCO can play the long game. The group's willingness to inject capital during downturns, as seen during COVID, provides counter-cyclical flexibility that pure-play cement companies lack.

Infrastructure boom potential in India reads like a cement producer's dream. The government's Rs 100 trillion infrastructure pipeline, focus on affordable housing, and urban development programs all translate directly to cement demand. With GDP growth at 7%+, cement demand typically grows at 1.2x GDP—implying 8-9% volume growth for the foreseeable future.

Operational improvements still possible represent the hidden upside. Current EBITDA margins at 15-16% lag industry leaders at 20%+. Even reaching industry average would add Rs 500 crore to annual EBITDA. The levers are clear: increase capacity utilization from 85% to 90%, raise alternative fuel usage from 9% to 15%, optimize product mix toward premium grades. None of this requires rocket science—just execution.

Bear Case:

Stock down 34% since IPO listing isn't just bad timing—it reflects fundamental concerns. The market has had three years to evaluate the story and remains unconvinced. Volume growth has been decent, but pricing power remains elusive. Without pricing power, cement becomes a commodity business where the lowest-cost producer wins—and NUVOCO isn't the lowest-cost producer.

Low interest coverage ratio concerns aren't academic—they're existential. With interest coverage at barely 2x, any demand downturn or price war could trigger covenant breaches. The Rs 40,000 crore debt pile, while manageable in good times, becomes an albatross in downturns. Unlike software or consumer companies that can cut costs quickly, cement plants have high fixed costs that can't be reduced.

Poor 5-year sales growth of 8.80% despite two major acquisitions suggests organic growth challenges. Strip out the Lafarge and Emami acquisitions, and organic volume growth has been anemic. This raises uncomfortable questions: Is the Eastern market as attractive as claimed? Can NUVOCO take share from established players? Or are they simply buying growth because they can't generate it?

Intense competition from larger players is intensifying, not moderating. UltraTech's aggressive expansion, Adani's unlimited capital backing Ambuja/ACC, and Dalmia's regional focus create a terrible industry structure. The top three players have announced 100+ MMTPA capacity additions—enough to crater pricing for years. NUVOCO's subscale position means they're price takers, not price makers.

Cyclical industry challenges compound the structural issues. Cement is the ultimate cyclical—capital intensive, commodity product, high fixed costs, and volatile demand. We're currently at peak margins after a post-COVID boom. History suggests mean reversion is coming. When it does, leveraged players suffer disproportionately.

The nuanced reality lies between these extremes. NUVOCO is neither the undiscovered gem bulls claim nor the value trap bears fear. It's a decent business bought at fair prices, operated reasonably well, but facing structural headwinds that limit multiple expansion potential.

The key variables to watch are revealing. First, Eastern India pricing dynamics—if NUVOCO can maintain price discipline in their core market, the bull case strengthens. Second, debt reduction trajectory—every quarter of deleveraging reduces downside risk. Third, competitive capacity additions—if industry supply growth moderates, pricing power returns.

The investment decision ultimately comes down to time horizon and risk tolerance. For patient, contrarian investors comfortable with cyclical exposure, NUVOCO offers asymmetric upside if execution improves. For quality-focused investors seeking compounders, better opportunities exist elsewhere.

The most intellectually honest assessment: NUVOCO is a "too hard" pile investment for most. Too many variables, too much execution risk, too dependent on industry dynamics beyond management control. It's not uninvestable, but it requires conviction that's hard to justify given alternatives.

XI. Epilogue & "If We Were CEOs"

Standing at the helm of NUVOCO in 2024 would feel like captaining a cargo ship through narrowing straits—the destination is clear, but the navigation requires precision. The company has scale, market position, and financial flexibility, but translating these assets into shareholder value remains the unsolved equation.

Focus areas: Operational excellence, debt reduction, market share gains would be the holy trinity of priorities. But prioritization matters more than ambition. First, fix the base business—get EBITDA margins to 18% through operational improvements before chasing growth. This means painful decisions: closing subscale RMX plants, rationalizing the dealer network, and potentially exiting marginal markets where NUVOCO lacks competitive advantage.

Technology adoption and sustainability initiatives shouldn't be buzzword bingo but ROI-driven investments. The digital dealer platform needs to become a genuine differentiator, not just a me-too initiative. Predictive maintenance using IoT sensors could reduce downtime by 20%. Dynamic pricing algorithms could improve realization by 2-3%. These aren't transformational individually, but collectively they compound into competitive advantage.

Brand consolidation vs. portfolio approach debate needs resolution. Currently, NUVOCO maintains six cement brands—a legacy of acquisitions that confuses customers and inflates marketing costs. The brave decision: sunset all brands except Duraguard and Concreto within three years. Yes, there's short-term disruption, but long-term marketing efficiency improves dramatically. Nirma proved that one strong brand beats five weak ones.

Geographic expansion opportunities exist, but discipline matters more than growth. The temptation to enter South or West India should be resisted unless acquiring distressed assets at attractive valuations. Instead, go deeper in existing markets—achieve 25% share in the East before expanding elsewhere. Market depth beats market breadth in commodity businesses.

M&A possibilities in fragmented market will arise as smaller players struggle with environmental compliance and capital requirements. But the next acquisition should be transformational, not incremental. Wait for a 10+ MMTPA opportunity that provides either geographic diversification or vertical integration into limestone reserves. Small bolt-ons dilute management focus without moving the needle.

ESG initiatives and green cement potential represent both obligation and opportunity. The pathway to net-zero cement is expensive but inevitable. Early investment in carbon capture technology, green hydrogen for kilns, and alternative binders positions NUVOCO for the post-carbon future. More pragmatically, green cement commands premium pricing from environmentally conscious developers—a rare source of differentiation in commoditized markets.

But the boldest CEO move would be addressing the ownership structure. The current holding through multiple layers of Nirma entities creates opacity that public markets discount. Simplifying to direct promoter holding, bringing in strategic investors, or even considering a merger with another regional player would unlock value. Sacred cows make poor shareholders.

The cultural transformation might be hardest. NUVOCO needs to evolve from a promoter-driven, acquisition-led company to an institution that outlasts its founders. This means professional management, independent board oversight, and succession planning that prioritizes competence over lineage. The Tata Group's transformation from family fiedom to professional institution provides the template.

Financial strategy requires similar evolution. The current approach of minimizing taxes through aggressive depreciation and interest deductions makes sense for a private company but destroys public market valuations. Showing consistent profits, paying predictable dividends, and providing transparent guidance would dramatically improve multiple expansion potential.

The uncomfortable truth is that NUVOCO might be worth more to someone else than as a standalone entity. If UltraTech offered 1.5x book value, should shareholders accept? If Adani wanted to add Eastern dominance to their portfolio? These aren't failure scenarios—they're value realization events that reward patient shareholders.

The ultimate CEO challenge is managing contradictions. Be aggressive in operations but conservative in capital allocation. Pursue growth but prioritize margins. Respect heritage but embrace change. Serve stakeholders but create shareholder value. It's a balancing act that few master.

Looking ahead five years, success looks like 20% EBITDA margins, 30 MMTPA capacity, net debt/EBITDA below 2x, and consistent dividend payments. The stock price would follow—probably doubling from current levels. Failure looks like margin compression, market share loss, and eventual distressed sale to a larger player.

The path forward is narrow but navigable. NUVOCO has the assets, market position, and backing to succeed. Whether they have the execution capability and strategic courage remains the billion-dollar question. For investors, it's a calculated bet on Indian management's ability to evolve from traders to builders to institutions.

The story that began with a chemist making detergent in his backyard hasn't ended—it's entering its most critical chapter. The next five years will determine whether NUVOCO becomes India's fifth cement major or merely a footnote in the industry's consolidation history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube