NSE: The World's Largest Derivatives Factory

I. The Hook: The Largest Exchange You Can't Buy Yet (0:00 – 10:00)

Picture a trading floor. Not a physical one with men in colored jackets shouting at each other—those have largely disappeared. Picture the digital one. The one where, on any given Thursday, more options contracts change hands than at the New York Stock Exchange, the Chicago Board Options Exchange, Eurex, and the Korea Exchange combined. Picture a screen that glows through the night in Mumbai, in Surat, in Lucknow, in ten thousand small apartments and basement offices from Kerala to Ludhiana, where a college student in flip-flops, a small-business owner on his lunch break, and a former homemaker turned day-trader are all placing bets on whether the Nifty 50 index will close ten points higher or lower by 3:30 PM.

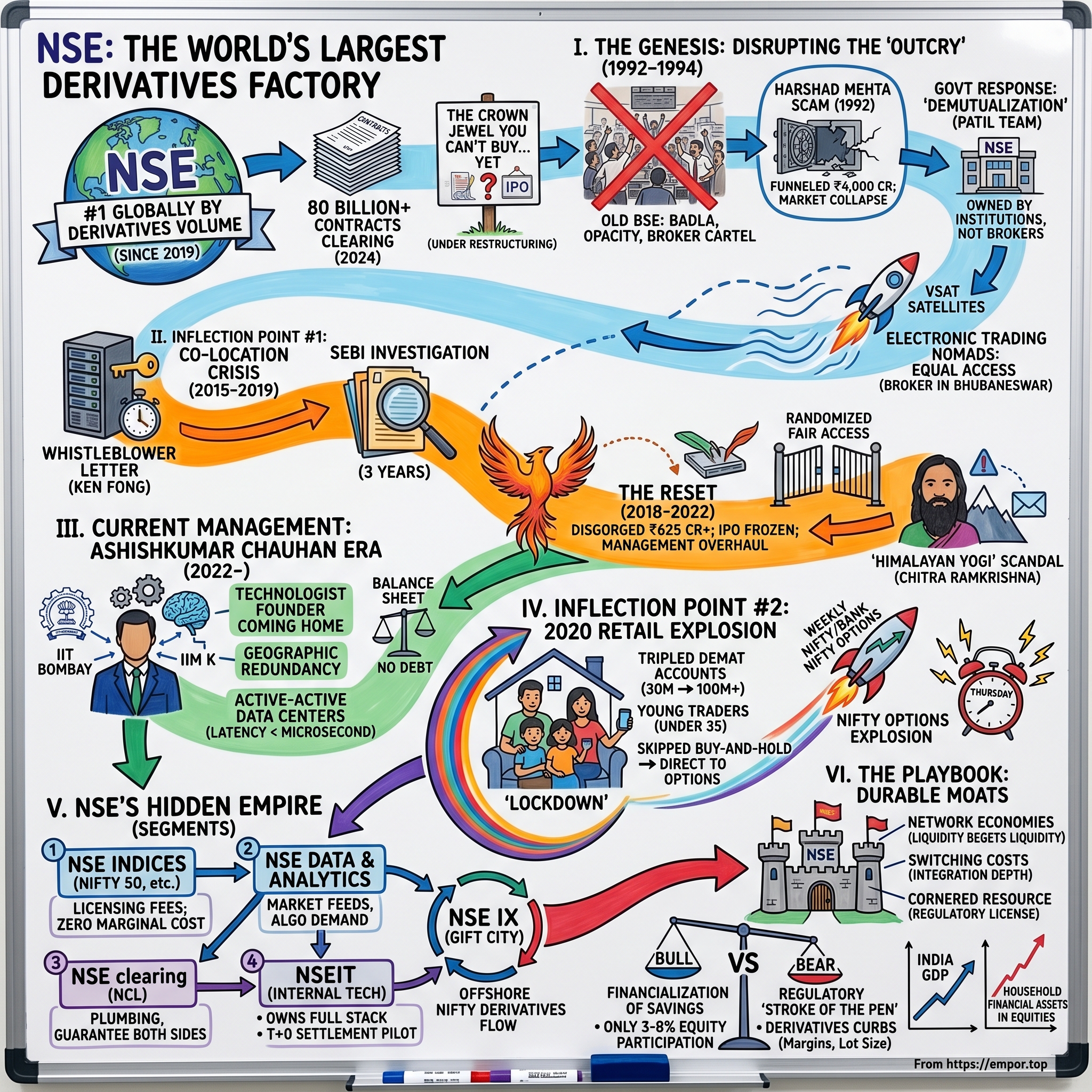

That trading floor belongs to the National Stock Exchange of India. And in the world of 2026, it is—by contract volume—the single largest derivatives venue on planet Earth.

Not the second largest. Not "one of the largest." The largest, by a factor so wide it makes the global rankings look like a printing error. In 2024, NSE cleared more than eighty billion contracts in a single calendar year, with the old American giants trailing far behind. The Futures Industry Association, which has been counting these things since before most of NSE's retail traders were born, has published its Global Derivatives Volume rankings every year, and NSE has occupied the top spot continuously since 2019. Most of the world has barely noticed.

Here is the paradox that makes this one of the most fascinating stories in global finance: this colossus—this exchange that prints cash the way the Federal Reserve prints paper—is still privately held. It has been "about to IPO" for the better part of a decade. Every few months, a business newspaper in Mumbai runs a headline promising the listing is "imminent." Every few months, a bureaucratic hurdle appears, a regulatory review drags on, a shareholder squabble flares up, and the filing gets kicked down the road.

So the thesis of this episode is simple, and it rolls out over the next three hours in increasing layers of texture. It goes like this. NSE was born in 1992 as a government-mandated disruptor, designed from day one to break the cartel that had strangled Indian capital markets for a hundred years. It was built by a small band of technocrats who understood something the rest of Indian finance did not: that electronic trading would eat physical trading the way Amazon ate Borders. In the thirty-plus years since, NSE has not just captured the Indian equities market—it has become, in a very real sense, the operating system of the Indian economy. Every time a foreign fund bets on India, every time a pensioner's SIP gets routed into a mutual fund, every time a retail trader in Jaipur places a weekly option, it touches NSE's rails.

And now, as the Indian household savings pool—historically parked in gold, land, and fixed deposits—finally starts migrating into financial assets, NSE sits at the center of what might be the largest capital formation event in human history.

But here is the catch, and it runs through everything that follows: you cannot simply own a piece of it. Not yet. And understanding why is a story about technology, politics, one spectacular scandal, a recovery, and a regulator that keeps a watchful, sometimes heavy hand on the tiller. This is the story of how a quiet utility became a profit machine, how a profit machine became a national symbol, and why the whole thing is now sitting at the edge of the deepest pool of domestic capital the world has ever seen.

Let's go back to the beginning. Before the electronic order book. Before the Nifty. Before the Sensex even really mattered to anyone outside of the old brokers' gymkhanas in South Bombay. Let's go back to the summer of 1992, when Indian finance broke.

II. The Genesis: Disrupting the "Outcry" (10:00 – 25:00)

If you had walked into Dalal Street in April 1992, you would have seen the old world of Indian finance in full, operatic glory. The Bombay Stock Exchange—founded in 1875, older than the Tokyo Stock Exchange, older than almost every modern bourse except London and New York—was the beating heart of Indian capital. And it beat the old way. The trading floor was a mosh pit of brokers in white shirts, waving paper chits, screaming across a circular pit called the "ring," settling trades with hand signals and handshakes and a kind of clubby bonhomie that had survived two world wars and independence itself.

Upstairs, in the members' lounge, the families who had controlled BSE for generations sipped tea. They owned the seats. They controlled the clearing. They set the rules. And they had a nickname for the system that made it all hum: "Badla." Badla was a peculiarly Indian invention—a forward-trading mechanism that let speculators carry positions from one settlement cycle to the next, with interest, paid to whoever was willing to fund the leverage. It was opaque, it was profitable for the well-connected, and it produced a market that behaved less like an exchange and more like a Vegas casino with the house, the dealers, and half the players all being cousins.

Into this world walked Harshad Mehta.

Mehta was a broker—small-time at first, then enormous. In the late 1980s and early 1990s, he figured out that India's fragmented, paper-based banking system could be gamed. He used forged bank receipts to funnel roughly ₹4,000 crore—around $1.3 billion at the time, a staggering sum in an economy that had just been liberalized—out of the banking system and into equities. He ran up the Sensex from under 1,000 in late 1990 to over 4,500 by April 1992, a rise of more than four-fold in eighteen months. He was profiled in magazines as the "Big Bull." He drove a Lexus. He lived in a penthouse with a mini-golf course.

Then, on April 23, 1992, a journalist named Sucheta Dalal broke the story in The Times of India. The scam unraveled in weeks. The Sensex collapsed. Banks discovered they were holding hot air instead of collateral. Thousands of small investors were wiped out. And the clubby, self-regulating, family-owned BSE was suddenly in the crosshairs of a government that could no longer look away.

The response came from an unlikely quarter. Manmohan Singh, then Finance Minister, had just unleashed the 1991 liberalization reforms. P. Chidambaram and a young regulatory thinker named R. H. Patil were asking a simple, radical question: what if India had an exchange that was not owned by its brokers? What if it was owned by the public—by banks, by insurance companies, by the government itself—and run by professional managers, with brokers as customers rather than owners?

This was the concept of "demutualization," and in 1992 it was a foreign idea in India. But the government pushed ahead. In November 1992, the National Stock Exchange of India was incorporated, with IDBI Bank, LIC, SBI, and a handful of other public sector financial institutions as founding shareholders. Patil became its first Managing Director. The team he recruited was small, young, and—crucially—technical.

They made one fateful decision in those first months. They decided that NSE would have no trading floor. None. No ring. No chits. No Badla. Every trade would be electronic, matched by a central computer, routed through satellite dishes—VSATs—installed on rooftops from Delhi to Chennai. They licensed matching-engine technology from a company called TCS, itself then a sleepy Tata subsidiary, and they built what would eventually become one of the fastest, most scalable electronic exchanges anywhere in the world.

Why did this matter? Because it did something the old BSE could not or would not do: it democratized access. A broker in Bhubaneswar, previously forced to route his clients' orders through a Bombay middleman who took a hefty cut, could now plug into NSE directly via a satellite terminal and trade on equal footing with the biggest broker on Dalal Street. Prices tightened. Spreads collapsed. And because the order book was electronic and anonymous, the old informal system of "I'll do you a favor if you do me one" simply stopped working.

NSE launched its Wholesale Debt Market segment in June 1994 and its Capital Market—equities—segment in November 1994. Within eighteen months, by sheer force of cheaper, faster, cleaner execution, it had overtaken BSE in daily turnover. By the end of the decade, BSE was a distant second and fading. The family members who had owned the old bourse spent years fighting rear-guard actions, lobbying regulators, and trying to catch up technologically. They mostly failed.

What really defined NSE's DNA, though, was not just the technology. It was the philosophical choice to be a technology company that happened to run an exchange, rather than an exchange that happened to have some technology. Every CEO since Patil has been either a technologist or an operator with deep technical instincts. Every major product launch—from index futures in 2000, to options on individual stocks, to the weekly options that would later set off the retail explosion—has been an engineering project first and a financial product second.

That DNA is still there today. It is also what got NSE into its biggest crisis.

III. Inflection Point #1: The Co-Location Crisis & The Great Reset (25:00 – 50:00)

Fast-forward to January 2015. A whistleblower letter arrived at the Securities and Exchange Board of India—SEBI, the country's capital markets regulator. The letter was not addressed to any individual. It was signed only as "Ken Fong, Singapore." It ran to a few pages, and it made a very specific allegation: certain algorithmic trading firms, paying for NSE's "co-location" service—the ability to place their servers inside NSE's own data center in Mumbai, cheek-by-jowl with the matching engine—were receiving market data microseconds before their competitors. Microseconds, in the world of high-frequency trading, are everything. A consistent edge of even a few microseconds can translate into tens of millions of rupees a day in extracted alpha.

The letter named specific firms. It alleged that NSE's tick-by-tick data dissemination system, which pushed order-book updates to subscribers over a TCP/IP multicast protocol, had a structural quirk: the first server to connect to a particular dissemination queue would receive data marginally ahead of the second, the second ahead of the third, and so on. Well-connected brokers had allegedly learned to connect to the "best" queue, giving them a persistent, predictable latency advantage over everyone else.

What followed was one of the longest, messiest regulatory investigations in Indian financial history. SEBI opened a formal probe. Forensic auditors from Deloitte and E&Y were commissioned. Internal NSE emails were exhumed. Former employees were questioned. The investigation ran for three years, produced multiple reports, and eventually resulted, in April 2019, in a SEBI order that disgorged roughly ₹625 crore—about $75 million at the time—of profits the exchange had allegedly made from the tainted co-location facility, plus interest. The order also barred NSE from accessing the capital markets for six months, which effectively froze the IPO that had been lined up for 2016.

The financial penalty, honestly, was the smaller story. The bigger story was what the co-location case did to NSE's leadership and culture.

Chitra Ramkrishna, who had risen from being one of R. H. Patil's original hires in 1992 to becoming NSE's Managing Director and CEO in 2013, was at the center of the storm. Her mentor and predecessor, Ravi Narain, also came under scrutiny. But the most extraordinary twist came in 2022, when SEBI, after years of digging, released a supplementary order revealing that Ramkrishna had for years been taking strategic and personnel decisions in consultation with a mysterious "Himalayan yogi"—an unidentified spiritual advisor to whom she had shared confidential board material, organizational charts, and appointment decisions, all by email. The revelation turned a serious governance failure into a tabloid sensation. Ramkrishna was fined, a former group operating officer named Anand Subramanian—whose appointment was allegedly orchestrated through the yogi's guidance—was barred from the markets, and the Central Bureau of Investigation filed charges.

For anyone who had watched NSE grow through the 1990s and 2000s, this was an astonishing fall from grace. The exchange that had been built as a clean, institutional alternative to BSE's clubby family-run culture had developed, over two decades of success, its own clubby, insular, opaque culture. The regulator, the board, and eventually the public all agreed that a complete reset was needed.

That reset unfolded between 2018 and 2022 and reshaped the institution. Limaye, who had come in as CEO in 2017 from IDFC, stabilized operations, put in place professional governance norms, opened up the board to more independent directors, and—critically—normalized the relationship with SEBI. The regulator, understandably, had moved from being a distant overseer to a hands-on supervisor who reviewed major technology changes and product approvals in detail. Compliance staffing tripled. The co-location facility was redesigned, with queue-based access replaced by a randomized, algorithmically fair delivery system that made it structurally impossible for any participant to "jump the line."

What looked, from outside, like a bureaucratic nightmare was actually the best thing that could have happened to the institution. In capital markets, trust is not a nice-to-have—it is the product. An exchange whose fair-play promise is in doubt is an exchange whose liquidity will eventually migrate. By forcing NSE to rebuild from the governance up, SEBI inadvertently saved the franchise. The "clubby" era ended. A hyper-regulated, transparent, procedurally rigorous era began.

It is impossible to understand the NSE of 2026 without understanding this period. The exchange you see today—with its quarterly compliance disclosures, its independent director majorities, its external audits of the matching engine, its carefully choreographed interactions with the regulator—is a direct product of the co-location crisis. The scar tissue is visible in everything from how press releases are worded to how executive compensation is structured.

And the very last act of the reset was to bring back the one person who, more than any other, had been there at the creation and could close the loop.

IV. Current Management: The Ashishkumar Chauhan Era (50:00 – 75:00)

In the summer of 2022, Vikram Limaye's five-year term came to an end. The search committee, operating under the watchful eye of SEBI and the Ministry of Finance, screened candidates from across Indian and global finance. But the name that kept surfacing, almost inevitably, was one that had a slightly improbable history with the institution.

Ashishkumar Chauhan had been employee number fifteen at NSE in 1993. A young IIM Kolkata graduate with an undergraduate degree in mechanical engineering from IIT Bombay, Chauhan had been part of the small team that designed and built the exchange's original electronic trading system. He is widely credited, alongside Ravi Apte and a handful of others, as one of the architects of NSE's first satellite-based network and its original matching engine. In the NSE history books, he is a founding technologist in all but name.

Then, in 2000, he left. Over the next decade he worked across Reliance Industries and on various ventures, and in 2010 he was recruited by—of all places—the Bombay Stock Exchange. BSE, by then a distant second to NSE in every metric that mattered, wanted a technologist to drag it into the modern era. Chauhan took the job. Over the next twelve years, he ran BSE as its CEO, oversaw its demutualization, took it public in 2017, and built its StAR mutual fund platform into one of the largest in India. He could not make BSE catch NSE in equity derivatives—nobody could—but he made it a credible, modern, profitable exchange.

So in July 2022, when NSE's board announced that its new Managing Director and CEO would be Ashishkumar Chauhan, the narrative was almost too perfect. The founding technologist, who had built the rival from the outside, was coming home to lead the original back to public markets.

Chauhan's style is, to put it charitably, unusual for a modern CEO. He tweets voluminously—often classical Sanskrit verses, historical asides about Indian mathematics, pictures of chai and monsoon skies in Mumbai. He has a PhD focus on financial markets that dates to his IIM days. In investor meetings he is known for long, discursive answers that move from Fibonacci sequences to Chanakya's Arthashastra to a crisp latency statistic about order book depth. Bankers either love him or find him bewildering. Either way, they listen.

His substantive contribution since 2022 has been threefold.

First, he has completed the technology overhaul that the co-location scandal made urgent. In 2021, while Chauhan was still at BSE, NSE had suffered one of the most embarrassing trading halts in its history—a four-hour, market-wide outage on February 24 that shuttered both cash and derivatives markets and drew a public rebuke from SEBI. The root cause was a telecom link failure that cascaded through the risk management system. Under Chauhan, the entire technology stack has been re-platformed with geographic redundancy, active-active data centers, and a dramatically expanded capacity ceiling. Order latencies at peak load are well inside the microsecond range, and the exchange has now gone multiple years without a material outage.

Second, he has restructured the incentive system. Executive compensation across NSE used to be heavily weighted toward volume-based performance pay—an arrangement that, in retrospect, had contributed to the culture problems of the pre-2015 era by nudging management to prioritize short-term trading activity over long-term institutional health. The new scheme, approved by the board's nomination and remuneration committee, emphasizes longer vesting periods, balance-sheet stability metrics, and a governance scorecard tied to SEBI compliance outcomes. It is a quieter, less sexy compensation architecture, and it is exactly the sort of thing a post-scandal institution needs.

Third, he has been the public face of NSE's push toward its IPO. Every quarter, he has been the one answering questions about when the listing will finally happen. The answer, honestly, is a moving target—SEBI has been methodical, some would say glacial, about approving the various conditions: resolution of pending co-location-era disputes, clean-up of pre-IPO shareholder transfers, settlement of legacy litigations. As of the current filing activity in early 2026, the path is clearer than it has been in years, but no firm date has been disclosed.

And then there is the shareholder base, which deserves its own moment of appreciation because it is genuinely one of the more unusual ownership structures in global finance. NSE has no single promoter. Under SEBI's stock exchange ownership rules, no individual or institutional shareholder may hold more than 5% (with certain domestic financial institutions allowed up to 15%). The result is a diffuse, almost parliamentary ownership: LIC, SBI, and other Indian public sector giants hold meaningful but capped stakes; global private equity and growth investors—Tiger Global, Temasek, certain sovereign wealth vehicles, a cluster of pension funds—hold smaller slices; and a long tail of domestic brokers, small financial firms, and former employees collectively round out the cap table. It is, as one Mumbai banker put it, "a corporate republic"—nobody is in charge, everyone has a seat, and the management team is genuinely accountable to a board that is not controlled by any single faction.

For investors, this structure matters for one simple reason: it means NSE's IPO, when it happens, will not be a promoter-led listing of a family business. It will be a widely held, institutionally owned, SEBI-supervised float—closer in character to how LSEG or HKEX trade than to most Indian listings. Which brings us to the demand side: who actually uses this exchange, and why did the volume explode.

V. Inflection Point #2: The 2020 Retail Explosion (75:00 – 100:00)

On March 24, 2020, Prime Minister Narendra Modi went on television at 8 PM and announced that India—all 1.4 billion of it—would enter a nationwide lockdown in four hours. The stock market, which had already been in free-fall for weeks, opened the next morning with the Nifty 50 at around 7,500, down roughly 40% from its pre-pandemic high. Shops closed. Factories halted. Millions of young, educated, middle-class Indians found themselves at home, with jobs on hold or salaries cut, and a cheap 4G smartphone in their pocket loaded with an app they had never opened before.

The app, for most of them, was called Zerodha. Or Upstox. Or, a little later, Groww. These were the new discount brokers—pure digital, zero-commission or near-zero-commission, built on NSE's APIs, designed for phones. They had existed since 2010 in the case of Zerodha, which was founded by the Kamath brothers, Nithin and Nikhil, in Bangalore with a few hundred thousand rupees of family capital. For years they had been a curiosity—slick tools, low fees, but a small user base dwarfed by full-service giants like ICICI Direct and HDFC Securities.

The lockdown changed everything. From roughly 30 million demat accounts in India at the end of 2019, the number roughly tripled to over 100 million by 2023 and kept climbing. Today, well over 180 million demat accounts are on file, with the majority belonging to first-time investors under the age of 35. The Kamaths became, for a brief moment in 2022, the youngest self-made billionaires in the country.

But the more interesting story was not the number of accounts. It was what those accounts did once they were opened.

In most markets—the U.S., the U.K., Europe, Japan—new retail investors start by buying and holding. They open an account, buy a few big-name stocks or an index fund, and check the balance once a month. The American retail investor of the 1990s and 2000s was, by and large, a long-only customer. Even the Robinhood generation of 2020–2021, famous for meme-stock chaos, mostly traded equities, not complex derivatives.

India was different. India skipped the buy-and-hold phase almost entirely and went straight to options.

Why? Several overlapping reasons. First, cash is king in the retail Indian imagination—the idea of tying up capital for years in a stock you cannot touch runs counter to generations of gold-and-fixed-deposit culture. Options, by contrast, offered "small money, big action"—a weekly Nifty call costing a few hundred rupees could return ten times that amount in an afternoon, or it could go to zero. Second, NSE had, over the prior decade, introduced weekly expiry options on the Nifty 50 and Bank Nifty indices. Where monthly expiries gave you one "lottery day" a month, weekly expiries gave you four or five, and a product ecosystem of short-duration, high-gamma contracts exploded around them. Third, the Indian tax code taxed long-term capital gains on equities modestly but treated options as "speculative" with a different—and for active traders, often more favorable—treatment of losses.

The resulting trading pattern was extraordinary. On any given Thursday—the default weekly expiry day for the Nifty 50—NSE's systems process tens of billions of rupees in notional derivatives volume, concentrated into the final two hours of the trading day, with retail participants accounting for a supermajority of the contracts by count (though a smaller share by notional value). The ecosystem around this—option-selling strategies taught on YouTube, Telegram channels with hundreds of thousands of subscribers, low-cost algorithmic trading platforms that let a retail user deploy a five-leg options strategy from a phone—has become a genuine subculture.

For NSE, this transformation changed the identity of the exchange. Before 2020, NSE was primarily a listing and trading venue—a place companies went to raise capital and where institutional investors went to allocate it. After 2020, it became something more complicated: a high-velocity behavioral platform, one where the median user was a 26-year-old with a mid-tier engineering degree looking to make a side income on weekly options. The word "exchange" started to feel inadequate. A broker in Mumbai quipped that NSE had become "the Steam platform of Indian finance"—a distribution channel for financial products that had an entertainment feel, complete with leaderboards, user-generated content, and a direct-to-consumer relationship with millions of end users.

SEBI, naturally, took notice. Starting in 2023 and accelerating through 2024 and 2025, the regulator introduced a series of measures aimed at what it called "speculative excess": higher margins on short option positions, a reduction in the number of weekly expiry contracts per exchange, larger lot sizes on index options (which effectively raised the minimum capital required to trade), and extensive public education campaigns highlighting that the vast majority of active retail options traders—studies from SEBI itself put the figure at more than 90%—lose money on a net basis. Some of these measures visibly affected volumes. Weekly options turnover dipped after each incremental tightening, before rebounding as traders adapted.

This is one of the most important analytic tensions for anyone thinking about NSE today. The retail derivatives boom has been an immense, almost obscene profit tailwind for the exchange. It has also created a regulatory overhang that no amount of technology or marketing can neutralize. The exchange's top line is now meaningfully more sensitive to SEBI policy than at any point in its history.

But derivatives trading, explosive as it is, is only one of the businesses running inside this holding structure. The most under-appreciated part of the NSE story is not the index options business. It is everything that sits next to it.

VI. The Hidden Empire: Segments & "Hidden" Businesses (100:00 – 130:00)

On a quiet floor of NSE's headquarters in the Bandra Kurla Complex, a team of maybe two hundred people runs a business that generates revenue with margins that would make a SaaS founder weep. This is NSE Indices Limited, the wholly-owned subsidiary that owns, calculates, and licenses the Nifty family of indices. The Nifty 50, Nifty Bank, Nifty Next 50, Nifty 500, a dozen sectoral indices, a handful of smart-beta products—all of them are the intellectual property of this one subsidiary. And every exchange-traded fund, every index mutual fund, every structured product, every research report that uses the name "Nifty" pays a licensing fee.

Think about what this business actually is. It is a software licensing business with zero marginal cost. Once the index methodology is designed, the daily calculation runs on a handful of servers. Adding another ETF that tracks the Nifty 50 does not add meaningful cost to NSE Indices—it just adds another royalty stream. As the Indian ETF market has grown from roughly $4 billion in 2015 to well over $100 billion by 2025, the fees that flow into NSE Indices have compounded quietly, at growth rates that outpace the underlying exchange business, and at margins that approach those of a pharmaceutical patent.

The irony is that most Indian retail investors have no idea this business exists. They know they are buying "the Nifty." They do not know there is a company whose sole job is to define and calculate what "the Nifty" is, and to charge for the privilege of calling any product by that name.

Next to NSE Indices sits NSE Data & Analytics. This is the business that sells market data. Real-time tick-by-tick feeds to institutional traders. End-of-day files to mutual funds. Historical data to academics and quant shops. Bandwidth licenses to news terminals and broker platforms. It is a quiet business, with its own small team, and it has been one of the fastest-growing segments of NSE for the past five years—because as algorithmic and high-frequency trading have expanded, the demand for granular, low-latency data has become almost insatiable.

There is a parallel in global finance that helps here. Look at Bloomberg, or at Refinitiv, or at the market data arms of the NYSE and CME. Market data has evolved, over the last two decades, from an incidental byproduct of exchange operations into one of the most profitable, fastest-growing product categories in finance. The margins are SaaS-like. The customer stickiness is high. And because exchanges have a natural monopoly on the data generated on their own venues, the pricing power is real.

NSE Data & Analytics is still small relative to what it could be. The pricing architecture is, by global standards, conservative. As Indian markets institutionalize, this line item has enormous room to expand—and because the marginal cost is effectively zero, most of that growth drops straight to operating margin.

Then there is NSE Academy, the education arm. On the surface, it looks like a nice corporate social responsibility line—training the next generation of Indian financial professionals, certifying college students in basics of markets and investing. In practice, it is something sharper: the top of the funnel. Every student who passes through an NSE Academy certification is an informed potential participant in NSE markets. Every broker back-office employee who takes an NSE Academy dealer certification is a professional whose instinct will be to route to NSE rather than BSE. It is brand building and workforce development rolled together, and it operates across thousands of campuses in India and, increasingly, in Nepal, Bhutan, the Gulf, and East Africa.

Then the offshore play. NSE International Exchange (NSE IX) operates out of the GIFT City International Financial Services Centre in Gandhinagar, Gujarat—a specially designated jurisdiction with foreign-exchange liberalization, tax benefits, and regulatory rules closer to Singapore or Dubai than to mainland India. For years, Indian stock futures, especially the Nifty 50 futures, traded offshore in Singapore on SGX. Foreign funds who wanted exposure to Indian equities without the hassle of onshore regulation routed through SGX Nifty. In 2019, a licensing dispute led NSE to withdraw its data from SGX, and by 2020 the two exchanges had agreed a formal transition: all offshore Nifty derivatives would migrate to GIFT City, to be traded on NSE IX.

This was a quiet win of enormous strategic value. Suddenly, the entire pool of foreign institutional demand for Nifty exposure was flowing through an NSE-owned venue. The volumes have grown rapidly. GIFT City, as a regulatory jurisdiction, has turned out to be an unexpectedly pragmatic, efficient place to trade, and NSE IX has become a meaningful profit center in its own right.

And sitting under all of this, like foundation bolts holding up a building, is NSE Clearing Limited—NCL. The clearing corporation is the central counterparty to every trade executed on NSE. When a retail trader buys a Nifty option and an institutional trader sells it, they are not really transacting with each other. They are both transacting with NCL, which steps between them, guarantees both sides, collects margin, manages risk, and settles the trade. This is the "plumbing" of the exchange—the part nobody notices until something breaks—and in times of extreme volatility (the 2020 pandemic crash, the 2024 election-day session when the Nifty had its largest-ever intraday move), it is what keeps the system solvent.

The economics of clearing are less flashy than the indices business, but they are durable. Margin-related income, fees on settlement, interest on the pool of cash collateral—all of it compounds with volume. And because regulators (rightly) require a clearing corporation to be conservatively capitalized and structurally separated from the trading venue, NCL also gives NSE a reputational moat: institutional investors are more willing to trade on a venue whose clearing house they trust.

Putting these segments together, the picture of NSE's economic engine becomes clearer. The headline equity trading and equity derivatives transaction fees are the largest line item—but the margin structure, growth profile, and strategic optionality of the indices, data, clearing, and international businesses mean the story is much richer than a simple "trading fee plus treasury income" narrative. Each segment feeds the others. More listings means more Nifty weightage candidates. More indices means more ETFs. More ETFs means more passive flows. More passive flows means more data subscriptions. More data subscriptions means more HFT activity. More HFT activity means more transaction fees. More transaction fees means more clearing margin. The flywheel is unusually tight for a financial institution of this size.

Which brings up the question: with all this cash flowing in, what has the company done with it?

VII. M&A and Capital Deployment (130:00 – 150:00)

If you run a monopoly exchange in a fast-growing market, you do not actually need to do very much M&A. Your core business compounds on its own. Your data and indices businesses compound on top of it. Your capital expenditure is modest—mostly data centers, servers, and bandwidth—and your regulatory constraints discourage leverage. The natural end state is a balance sheet fat with cash, looking for something to do.

NSE has largely resisted the temptation to turn that cash into risky adventures. It has not, for example, tried to buy a bank. It has not launched a clearing house in another country. It has not, despite endless speculative reports, gone on a spree of global exchange acquisitions in the style of ICE's purchase of NYSE Euronext or the LSE Group's purchase of Refinitiv.

Instead, it has played a quieter game of vertical integration and capability build-out.

The most discussed acquisition of the past several years was the 2020 purchase of Cogencis, a real-time news and data provider with a strong presence in Indian fixed income and FX markets. The rationale was clean: NSE's data business was growing, but it was heavily oriented toward equities. Cogencis brought a fixed-income and macro-news capability, plus an institutional client book that overlapped with NSE's target customer set. The deal was executed through NSE Data & Analytics, the price was modest by global standards, and the integration has been incremental rather than transformational.

The natural comparison case is the London Stock Exchange Group's 2021 acquisition of Refinitiv, which closed at roughly $27 billion and fundamentally remade LSEG into a data-and-analytics company with a trading venue attached. The Cogencis deal was a rounding error by comparison—but it pointed in the same direction. Exchanges, globally, are becoming data businesses first and matching engines second. NSE's management has clearly internalized this and is building toward it, but at a pace and scale calibrated to Indian reality.

The more consequential vertical-integration story is NSE IT—NSEIT Limited, the wholly-owned technology subsidiary that builds, operates, and maintains the trading, clearing, risk-management, and ancillary systems on which the exchange runs. In most markets, exchanges license their core technology from vendors—Nasdaq runs on its own INET platform, but LSE, HKEX, and various smaller exchanges rely on third-party vendors like Aquis, Cinnober, or MillenniumIT. NSE's choice to own the full stack internally means it does not pay software licensing fees, it does not wait on vendor release cycles for new products, and—most importantly—it does not face vendor risk when it needs to innovate.

The tradeoff is that NSE has to carry a large internal engineering organization. NSEIT employs several thousand engineers, and its operating cost is real. But the payoff is control. When NSE wanted to launch weekly options, it did so on its own timeline. When it needed to re-platform after the 2021 outage, it did so with its own teams. When SEBI demanded, in 2023, a faster introduction of T+0 settlement—same-day settlement of equity trades, a capability few global exchanges have—NSE delivered a pilot within months, again because it owned the stack.

In capital allocation terms, the overall pattern has been: pay a generous but not extravagant dividend (which puts cash back to the diverse shareholder base, many of whom are publicly accountable institutional investors); retain enough to fund technology investment and regulatory capital; and hold a cash buffer large enough to absorb any conceivable regulatory penalty or operational stress event. The balance sheet is conservative to the point of being deliberately under-levered. There is no debt of note. The investment portfolio—large, because margin income and float capital are meaningful—is held in high-quality government and corporate bonds.

For an investor thinking about this business in the run-up to an IPO, the capital allocation story is relatively simple: NSE is not a company that is going to create value through clever M&A or financial engineering. It is a company that is going to create value because the underlying Indian capital markets are going to grow, and the exchange's fees are going to compound with that growth. Management's job is not to be a deal-maker. It is to be a stable, conservative, technically excellent operator. On that dimension, the post-reset leadership has generally delivered.

Which leaves us with the big analytical question: what makes this business structurally valuable? Why, in a world of contested, fragmenting, digitally disrupted venues, does NSE continue to compound? The answer, as always in business, is about durable competitive advantage.

VIII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces (150:00 – 170:00)

Exchanges are, in theory, commoditizable. The matching logic is well-understood. The technology is available. The regulators, at least in principle, could license a dozen venues in any given jurisdiction. And yet, in practice, almost every country in the world has exactly one dominant stock exchange. The United States, with two major exchange families and a handful of alternative trading systems, is an outlier. In most markets, the winner takes virtually all. This concentration is not an accident. It is the result of some of the most powerful structural economics in all of commerce.

The single most important power is network economies. Liquidity begets liquidity. If a trader wants to buy 10,000 shares of a particular company, they want to trade where 10,000 shares can be bought quickly, anonymously, and with minimal price impact. That means they go to the venue where other traders are. Those traders, in turn, go there because that is where the first trader is. It is a positive feedback loop that, once it tips, becomes almost impossible to dislodge.

In India, that tipping point happened sometime in 1996 or 1997, when NSE's equity trading volumes overtook BSE's. Once the institutional flow migrated, the retail flow followed. Once the retail flow was there, the foreign flow followed. Once the foreign flow was there, the derivatives market—which naturally consolidates on the venue with the deepest underlying cash market—followed. By the mid-2000s, NSE commanded more than 80% of Indian equity trading volume, a share it has roughly maintained for two decades. In equity derivatives, the share is effectively monopolistic; BSE has tried multiple times to build a credible alternative, and each time has ended up with sub-5% market share within six to eighteen months of launch.

The second power is switching costs, which compound on top of network effects. An institutional broker that has integrated with NSE's APIs, co-located its servers in NSE's data center, trained its back-office staff on NSE's clearing workflow, and embedded NSE's risk-management conventions into its own systems does not switch to BSE casually. Even if BSE offered an identical product at half the price, the migration cost—software rewrites, staff retraining, regulatory re-filings, client communications—would be enormous. The same is true, at smaller scale, for retail brokers, for custodians, for data vendors. Everyone in the ecosystem is built on NSE. Switching is not "a vendor change"—it is a full replatforming project that no rational CFO would sign off on.

The third power, unique to financial infrastructure, is the cornered resource of the regulatory license. In India, you cannot "start a stock exchange" in any meaningful sense. SEBI is the gatekeeper, and the process for licensing a new exchange is so onerous—capital requirements, technology certifications, corporate governance standards, settlement infrastructure, compliance staffing—that the country has, over the last thirty years, seen exactly two credible national equity exchanges: BSE and NSE. A regional exchange in Ahmedabad or Calcutta could not compete. The Multi-Commodity Exchange exists for commodities but cannot trade equities. The Metropolitan Stock Exchange has struggled for relevance. The license is, genuinely, a cornered resource.

These three powers—network economies, switching costs, and cornered resource—overlap and reinforce each other. They are the three most durable forms of competitive advantage in Hamilton Helmer's 7 Powers framework, and NSE has all three in abundance.

Applying Porter's Five Forces clarifies the picture further.

Threat of new entrants: very low. Between the regulatory moat and the network-effect moat, a de novo entrant would need to clear both simultaneously. No one has.

Bargaining power of suppliers: low. NSE's main "suppliers" are technology vendors (largely in-sourced via NSEIT), real estate (modest), and connectivity (commoditized). None has pricing power.

Bargaining power of buyers: low to moderate. Retail traders have zero individual bargaining power. Institutional traders have some—they can threaten to route flow internationally, to GIFT City, to SGX (now largely unavailable), or to off-exchange venues. But for Indian equity derivatives specifically, the liquidity is at NSE, and alternatives are not meaningful.

Threat of substitutes: moderate to low. Cryptocurrency was the big theoretical substitute for retail risk-taking, but India's regulatory and tax treatment of crypto (effectively a 30% flat tax on gains with no loss offset) has largely suppressed crypto as a mass-retail product. Real estate remains a competitor for savings allocation, but is structurally illiquid. Gold remains culturally important but is slowly losing allocation share. The most plausible substitute is probably an offshore venue for sophisticated investors—but for the mass retail market, NSE has no real substitute.

Rivalry: low. BSE is the only credible domestic competitor, and it has been structurally behind NSE in equity derivatives for over two decades. Its recent strategy has been to focus on selected niches—SME listings, mutual fund distribution, a revamped Sensex derivatives product—rather than head-on competition in index derivatives.

In aggregate, this is one of the most favorable competitive landscapes of any large-cap financial business in the world. The comparison set matters. Hong Kong Exchanges and Clearing enjoys a similar monopoly within its jurisdiction, but faces political uncertainty. CME Group is diversified across many asset classes but competes with ICE and the equity-options complex in the U.S. Deutsche Börse runs a strong European franchise but shares share with Euronext and LSE. NSE, by comparison, sits atop a domestic market that is both concentrated and growing, with a regulator that has methodically institutionalized the franchise rather than challenged it.

So what are the key performance indicators that actually matter for tracking this business going forward? Three rise above the rest. First, equity derivatives average daily turnover—specifically the notional turnover in index options, which is the core profit engine. Second, the derivatives-to-cash volume ratio, which is a structural indicator of market character; if the ratio compresses materially following regulatory action, the top line is at risk. Third, the number of active unique trading clients, which is the best forward indicator of retail mindshare and the primary leading indicator of secondary product uptake—indices, data, clearing margin. If these three metrics are healthy, the financials tend to follow.

One more thing is worth saying about the "myth versus reality" of this business. The consensus narrative is that NSE is a "bet on Indian GDP growth." That is, at best, half right. NSE is not a GDP bet. It is a bet on the financialization of Indian household savings—a narrower but more powerful thesis. India's nominal GDP has grown nicely over the past twenty years, but the financial-asset share of household savings has grown much faster, from roughly 20% in the early 2000s to close to 40% today, with equities and equity mutual funds growing from a rounding error to well over 15% of household financial assets. That shift, and its continued progression, is the real NSE thesis.

IX. Analysis: Bull vs. Bear Case (170:00 – 180:00)

Let's lay out the tension clearly.

The bull case begins with a single statistic that, once internalized, reframes the entire investment narrative. Depending on the methodology used, somewhere between 3% and 8% of Indian households hold equities directly or through mutual funds. In the United States, the comparable figure is above 60%. In South Korea, above 40%. In Taiwan, above 30%. Even in Brazil and Mexico—emerging markets with far less per-capita income than India will soon enjoy—the figure is in the low teens to high teens.

Now consider the trajectory. India's household savings pool, which sits at roughly $800 billion to $1 trillion annually depending on the measurement window, has been migrating steadily out of gold, real estate, and bank deposits into financial products. Systematic Investment Plans—the Indian version of dollar-cost-averaged monthly mutual fund investing—have grown from virtually nothing a decade ago to over 100 million active plans today. The average ticket size is small, but the aggregate flow is massive, and almost all of it ultimately lands in Indian equities.

If household equity participation in India rises from the current high-single-digits to even 20%—a fraction of the mature-market figure—the implied growth in trading activity, assets under management, index-linked products, and data licensing is enormous. The mathematics of exchange economics, with their fixed-cost-dominated operating model, mean that most of that incremental revenue falls to the bottom line. In the fullness of time, NSE becomes one of the most valuable financial institutions on Earth, sitting at the center of what might be the largest capital formation event in a generation.

The bear case is shorter but sharper.

It is regulatory. Specifically, it is the "stroke of the pen" risk that SEBI or the Ministry of Finance could, in a sustained fit of concern about retail speculation, impose measures that structurally curtail the derivatives business. The tools available are numerous: raising securities transaction tax on options (which has happened), mandating higher margins (which has happened), reducing the number of weekly expiries (which has happened), eliminating weekly expiries altogether (which has been discussed), restricting retail access to complex derivatives through suitability filters (which has been discussed), or—at the most extreme—requiring that all index options be cash-settled on a longer horizon rather than weekly. Each of these measures would hit the top line of NSE's derivatives business, which, by some estimates, accounts for 60% to 70% of total revenues.

A reasonable scenario sketch: if regulatory tightening reduces derivatives turnover by 30% to 40% over a twelve-to-eighteen-month window, the impact on NSE's consolidated revenue and operating income would be in the mid-twenties-percent range. That is not existential, but it is meaningful. And unlike most competitive risks, this one cannot be managed away through better execution—it is entirely in the hands of a regulator whose statutory mandate is investor protection.

Valuation context is the final piece. The global comparables—Hong Kong Exchanges, CME Group, ICE, Deutsche Börse, LSEG, B3 in Brazil, Japan Exchange Group—trade at a range of price-to-earnings multiples typically between the high teens and the high twenties, with the data-heavy names (LSEG in particular) at the higher end and the pure-exchange names in the middle. NSE's growth rate, in most recent years, has comfortably outpaced these peers, and its margin structure is as good or better than the best. The question, at the moment of IPO, will be whether the market applies a "scarcity premium" (the only pure-play exposure to the financialization of India) or a "regulatory discount" (the overhang of SEBI actions). Historically, public markets have tended to reward scarce, high-growth, high-margin, platform-economic businesses with premium multiples, and then to mark them back down only when execution falters or the underlying market stops growing.

The ultimate investor question, then, is not so much about NSE the company as about the timing and terms of its eventual listing. The business is structurally attractive; the management is post-reset and technically credible; the moats are deep. What remains uncertain is price.

Second-layer considerations worth flagging: the pending resolution of legacy co-location litigation, which could produce either tail-risk headlines or a clean closure; the extent of SEBI's appetite for additional derivatives curbs in 2026 and beyond; the pace and structure of the IPO itself, which has been a moving target; notable shifts in the shareholder base, particularly any stake sales by pre-IPO private equity holders, which could create supply/demand dynamics around the listing; and the strategic evolution of GIFT City, which could become either a marginal offshore venue or a meaningful second profit center depending on how foreign-portfolio capital flows develop.

X. Epilogue & Closing (180:00 – 185:00)

Step back and think about what the National Stock Exchange of India actually is, in the fullness of its history, its economics, and its cultural role.

It is a utility. It is a monopoly. It is a data company. It is a technology company. It is a licensing business. It is the plumbing of a trillion-dollar equity market. It is the casino floor of a hundred million retail traders. It is the bridge between the savings of Indian households and the capital needs of Indian businesses. It is, in every meaningful sense, the operating system of the Indian economy.

None of that was inevitable. In 1992, the idea that a brand-new, technology-first, demutualized exchange could, within a decade, displace a 120-year-old incumbent with deep political and social roots was regarded as fanciful. In 2015, when the co-location scandal broke, the idea that NSE could emerge stronger, cleaner, and more institutionally legitimate than before was regarded as unlikely. In 2020, when COVID shut the country down, the idea that the ensuing retail explosion would make NSE the largest derivatives venue in the world was not anticipated by anyone. Each inflection point has, in retrospect, looked like the result of a particular set of choices—most of them made by a small number of technologists, regulators, and operators who understood that exchanges are, at their core, trust businesses, and that trust is a compounding asset.

The business, as of 2026, sits at a remarkable juncture. The retail wave has crested and is now being regulated at the edges, but the structural growth in Indian financial-asset allocation has barely started. The institutional framework has been rebuilt after the scandal. The technology stack has been re-platformed. The leadership is stable and technically credible. And the IPO, after almost a decade of delay, is closer than it has ever been.

In the gold rush of Indian growth, everyone else is digging for gold; NSE owns the only shovel shop in town. The shovels are electronic. They print contracts by the billion. And the rush, by every measure that matters, is still in its early innings.

Top Links for Further Reading

- NSE's History of Electronic Trading: The 1994 VSAT Revolution

- Zerodha's IPO Portal: NSE IPO Overview & Financials

- SEBI Order on Co-location: The Management Reset

- The "Ashishkumar Chauhan" Profile: From Founding Member to CEO

- FIA Global Rankings: NSE as the World's Largest Derivatives Exchange

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube