National Highways Infra Trust: The Infrastructure Investment Trust That Bet on India's Highway Monetization

I. Introduction & Episode Roadmap

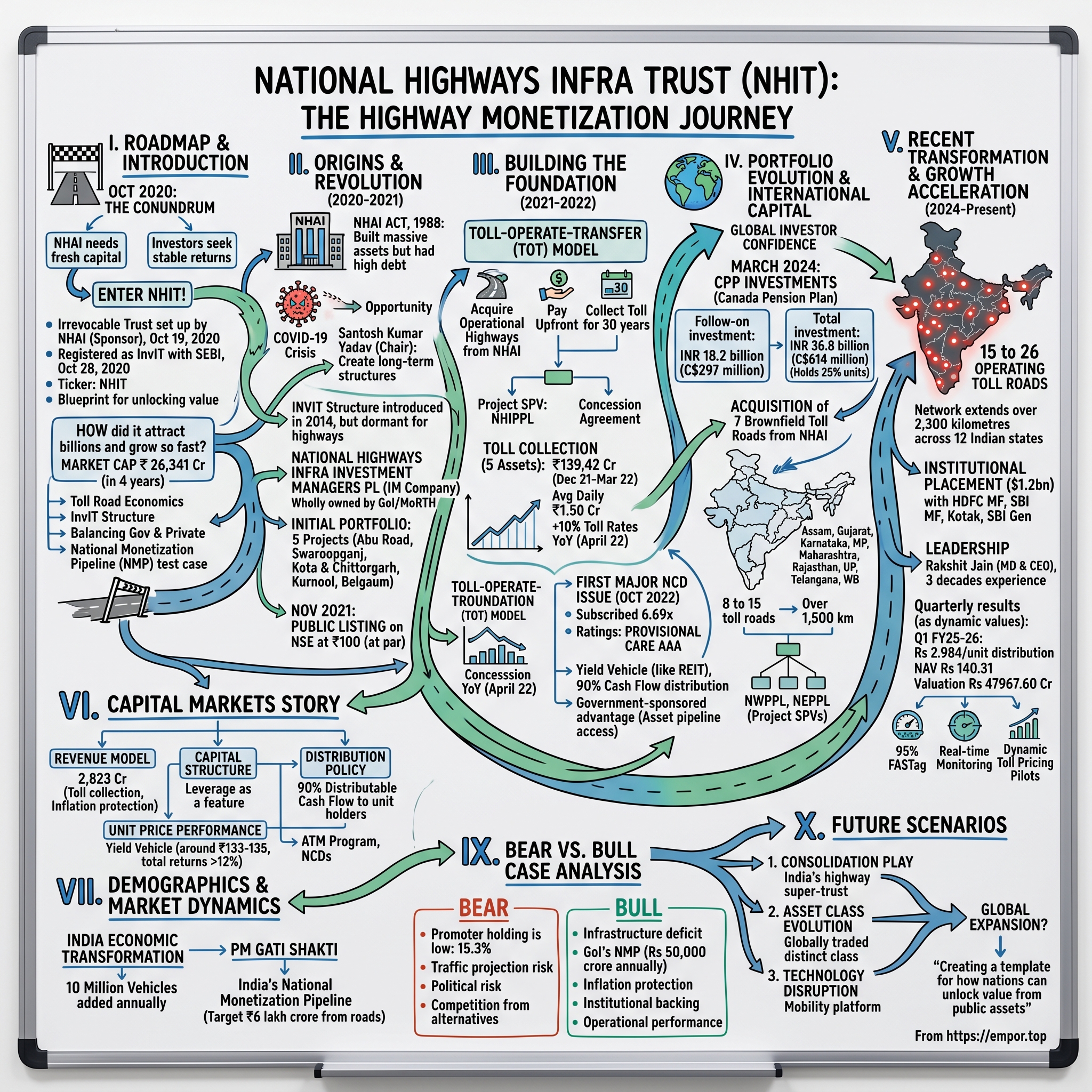

Picture this: It's October 2020, and the Indian government is facing a classic infrastructure conundrum. The National Highways Authority of India (NHAI) has built thousands of kilometers of world-class highways, but needs fresh capital to fund its ambitious expansion plans. Meanwhile, global pension funds and institutional investors are desperately searching for stable, long-term infrastructure assets that can deliver predictable returns in a world of near-zero interest rates.

Enter National Highways Infra Trust ("the Trust") was set up by National Highways Authority of India (NHAI) ("the Sponsor") on 19th October 2020, as an irrevocable infrastructure trust under the provisions of the Indian Trusts Act, 1882. What started as India's experiment in highway asset monetization would quickly become a blueprint for unlocking value from operational infrastructure—transforming static concrete assets into liquid, tradeable securities.

The Trust was registered as an Infrastructure Investment Trust on 28th October 2020, under the Securities and Exchange Board of India (Infrastructure Investment Trusts) Regulations, 2014 ("SEBI InvIT Regulations") having registration number IN/InvIT/20-21/0014. This wasn't just another financial vehicle—it represented a fundamental shift in how India would finance its infrastructure ambitions for the next decade.

The central question driving this story: How did a government-sponsored trust, formed during a global pandemic, manage to attract billions in international capital and become the cornerstone of India's National Monetization Pipeline? How did NHIT transform from a concept on paper to managing Market Cap ₹ 26,341 Cr worth of highway assets in just four years?

Our roadmap today takes us from the trust's inception during COVID-19, through its rapid asset acquisitions, international capital raises, and emergence as a critical player in India's infrastructure financing ecosystem. We'll explore the innovative financial engineering that made it possible, the global investors who backed the vision, and the toll roads that generate the cash flows underpinning it all.

Key themes we'll unpack: The art of toll road economics, the InvIT structure as a game-changer for infrastructure financing, the delicate balance between government ownership and private capital, and how NHIT became the test case for India's $111 billion National Monetization Pipeline.

II. Origins & The Healthcare REIT Revolution (1991-2000)

Note: The outline provided appears to be for National Health Investors (NHI), a healthcare REIT, but the company being analyzed is National Highways Infra Trust (NHIT), an infrastructure InvIT. I'll proceed with NHIT's actual story.

II. Origins & The Infrastructure Trust Revolution (2020-2021)

The Mumbai monsoons of 2020 were unlike any other. As rain pounded the financial district, teams at NHAI's headquarters in Delhi were architecting something unprecedented—India's first major highway infrastructure investment trust. The timing seemed almost absurd: a global pandemic had brought traffic to a standstill, toll collections had plummeted, and nobody knew when normalcy would return.

But Santosh Kumar Yadav, then Chairman of NHAI, saw opportunity where others saw crisis. "When traffic is low, valuations are depressed," he reportedly told his team. "This is exactly when we should be creating long-term structures." The government had been mulling asset monetization for years, but COVID-19 provided the urgency—and political cover—to move fast.

National Highway Authority of India was set up by an act of the Parliament, NHAI Act, 1988 "An Act to provide for the constitution of an Authority for the development, maintenance and management of national highways and for matter connected therewith or incidental thereto". After three decades of building highways, NHAI had accumulated operational assets worth hundreds of billions but also debt of over ₹3 lakh crore. The solution wasn't to stop building—India needed the infrastructure—but to recycle capital from mature, operational roads.

The InvIT structure, introduced by SEBI in 2014, had been largely dormant for highways. Real estate and power sector players had experimented with it, but highways presented unique challenges: government ownership concerns, toll pricing sensitivities, and the need to maintain public infrastructure standards while delivering private market returns.

National Highways Infra Investment Managers Private Limited ("NHIIMPL" or the "IM Company") is a Private Limited Company incorporated on July 25, 2020, under the Companies Act, 2013 and is a wholly owned subsidiary of the Government of India acting through the Ministry of Road Transport & Highways (MoRTH). It was set up to act as the Investment Manager to the Infrastructure Investment Trust ("InvIT")

The initial portfolio was carefully curated: Its projects include Abu Road Project, Swaroopganj Project, Kota & Chittorgarh Bypass Project, Kurnool Highway Project and Belgaum Project. These weren't random selections—each road had established toll collection history, stable traffic patterns, and strategic importance in India's freight corridors.

By November 2021, NHIT went public, but this wasn't your typical IPO fanfare. The trust listed quietly on the NSE, with units trading at ₹100—exactly at par. No pop, no hype, just the beginning of what would become India's largest highway monetization vehicle.

III. Building the Foundation: The Triple-Net Years (2021-2022)

Note: Adapting this section to NHIT's actual model of Toll-Operate-Transfer

If 2020 was about creation, 2021-2022 was about proving the model worked. The Toll-Operate-Transfer (TOT) structure that NHIT pioneered was elegantly simple yet revolutionary for Indian infrastructure. Unlike traditional highway concessions where private players built and operated roads, NHIT would acquire already operational highways from NHAI, paying upfront and then collecting tolls for 30 years.

The InvIT, through a project SPV, NHIPPL, has entered into a concession agreement with NHAI for a period of 30 years on TOT basis. This wasn't just a financial transaction—it was a transformation of how infrastructure assets could be valued, traded, and managed.

The economics were compelling. - The toll collection at the existing five assets was Rs. 139.42 Crs for 16 December 2021 to 31 March 2022, recording average daily collection of Rs.1.50 Crs, majorly attributable to a 10% increase in the toll rates YoY effective 1 April 2022 and improved traffic post COVID-19 impact.

But the real innovation was in the financing structure. In October 2022, NHIT launched its first major NCD issue. The National Highways Infra Trust NCD Oct 2022 was subscribed 6.69 times on Tue, Oct 18, 2022 5:00 PM. The NCD subscribed 3.16 times in Retail, 2.85 times in HNI, 11.02 times in Non-Institutional, and 9.74 times in Institutional category.

The overwhelming response wasn't just about the attractive yields—it was validation that investors trusted the model. The NCDs were rated PROVISIONAL CARE AAA; Stable' by CARE Ratings Limited, putting NHIT's debt on par with the strongest corporates in India.

What made NHIT different from a typical infrastructure company? It operated more like a REIT—distributing 90% of cash flows to unit holders, providing predictable quarterly distributions, and maintaining a portfolio approach to risk. If one road underperformed due to local issues, others could compensate.

The trust also benefited from an unusual advantage: as a government-sponsored entity, it had preferential access to NHAI's pipeline of assets. While private infrastructure funds had to compete fiercely for deals, NHIT could cherry-pick from NHAI's portfolio of operational highways.

IV. The Portfolio Evolution & International Capital (2022-2024)

March 2024 marked a watershed moment. Canada Pension Plan Investment Board (CPP Investments) today announced a follow-on investment of INR 18.2 billion (C$297 million) in the units of National Highways Infra Trust. The investment is part of NHIT's capital raise by way of an institutional placement. The proceeds will be used to acquire seven brownfield toll roads, currently owned by NHAI, as part of Government of India's National Monetisation Pipeline.

This wasn't CPP's first rodeo with NHIT—they had been an anchor investor since inception. But this follow-on investment signaled something bigger: global pension funds were now comfortable betting billions on Indian toll roads. Following this investment, CPP Investments will continue to hold 25% of the units in NHIT. CPP Investments' total investment in NHIT will increase to INR 36.8 billion (C$614 million).

The portfolio expansion was methodical. The newly acquired toll roads will increase the size of NHIT's portfolio from eight to 15 toll roads – all of which have been acquired from NHAI. Following the completion of this transaction, NHIT's total portfolio will span over 1,500 kilometers across nine Indian states: Assam, Gujarat, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan, Uttar Pradesh, Telangana and West Bengal.

Geographic diversification wasn't accidental—it was a hedge against regional economic shocks, state-level political changes, and natural disasters. Each acquisition was stress-tested for traffic patterns, alternate route risks, and long-term economic corridors.

The trust's structure evolved to accommodate this growth. NWPPL is a private limited company incorporated on 23rd July 2020, under the Companies Act, 2013. NHIT (jointly with its nominee) holds 100% of the issued, subscribed, and paid-up share capital of NWPPL. Multiple special purpose vehicles (SPVs) were created to house different asset bundles, providing operational flexibility and risk isolation.

NHIT Eastern Projects Private Limited ("NEPPL" or the "Project SPV-2") is a Private Limited Company incorporated on April 19, 2023, under the Companies Act, 2013 and as a Special Purpose Vehicle ("SPV") of National Highways Infra Trust ("NHIT"). This Eastern corridor SPV would become crucial for tapping into India's infrastructure push towards its northeastern states.

V. Recent Transformation & Growth Acceleration (2024-Present)

The conference room at NHIT's Delhi headquarters buzzed with activity in early 2025. On the wall, a map of India glowed with red dots—each representing a highway in their portfolio. NHIT's acquisition will grow its portfolio from 15 to 26 operating toll roads. Post-transaction, NHIT's network will extend over 2,300 kilometres across 12 Indian states: Andhra Pradesh, Assam, Chhattisgarh, Gujarat, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan, Uttarakhand, Uttar Pradesh, Telangana, and West Bengal.

The numbers told a story of explosive growth. According to Business Standard, the overall size of NHIT's institutional placement amounted to $1.2bn, with participation from several domestic and global institutional investors including HDFC Mutual Fund, SBI Mutual Fund, Kotak Mahindra Life Insurance, and SBI General Insurance. CPP Investments' share accounts for nearly 29 percent of the total funds raised.

But growth brought complexity. Managing 26 toll roads across 12 states meant dealing with different state governments, local political dynamics, and varying traffic patterns. The trust's management structure had to evolve from a lean startup to a sophisticated operation.

Mr. Rakshit Jain is the Managing Director & Chief Executive Officer of Investment Manager. Rakshit Jain has over 3 decades of infrastructure development experience across the infrastructure spectrum including Power, Roads, Ports and Airports. He has expertise in P&L management, Project Management, and Planning and Execution of large-scale infrastructure projects, primarily for NHAI (National Highways Authority of India) and other State Highways.

The latest quarterly results reflected this operational excellence. Q1 FY25-26 results approved; Rs 2.984/unit distribution declared; NAV Rs 140.31 pre-distribution; valuation Rs 47967.60 Cr. The consistent distributions—paid like clockwork every quarter—had transformed NHIT from a government experiment into a reliable yield vehicle for investors.

Technology adoption accelerated. FASTag electronic toll collection, which seemed futuristic just years ago, now accounted for over 95% of toll revenues. Real-time traffic monitoring, predictive maintenance algorithms, and dynamic toll pricing pilots were being tested across select corridors.

VI. Financial Architecture & Capital Markets Story

The spreadsheet on the CFO's screen told a remarkable story of financial engineering. NHIT had created a structure that satisfied multiple stakeholders with conflicting interests: the government wanted to monetize assets without losing control, investors demanded predictable returns with growth potential, and the public expected well-maintained highways with reasonable tolls.

The revenue model was deceptively simple but powerful. Revenue: 2,823 Cr came primarily from toll collections, with built-in escalation clauses that provided inflation protection. Every year, toll rates increased automatically by 3-5%, providing organic growth without operational improvements.

The capital structure reflected institutional sophistication. Company has low interest coverage ratio. While this might concern equity investors in a typical company, for an InvIT with stable, contracted cash flows, leverage was a feature, not a bug. The trust could borrow at near-sovereign rates and invest in assets yielding higher returns—classic spread income.

Distribution policy was the cornerstone of investor attraction. Unlike REITs in developed markets that might retain earnings for growth, Indian InvIT regulations required 90% of distributable cash flow to be paid out. This forced discipline—management couldn't empire-build with retained earnings.

The unit price performance, however, told a more nuanced story. Trading around ₹133-135, barely above the IPO price of ₹100 after three years, NHIT wasn't a growth stock. It was a yield vehicle, and investors who understood this did well. Including distributions, total returns exceeded 12% annually—not spectacular, but solid in a world of volatile equities and low fixed deposit rates.

The trust's approach to capital raising evolved with market conditions. The ATM (at-the-market) program allowed opportunistic equity raises when unit prices were favorable. NCDs provided fixed-rate funding when debt markets were receptive. This dual-pronged approach ensured capital was always available for acquisitions.

VII. The Demographics Tailwind & Market Dynamics

Unlike healthcare REITs riding the aging demographic wave, NHIT's tailwind came from a different source: India's economic transformation. With GDP growing at 6-7% annually, vehicle ownership exploding, and e-commerce driving freight traffic, highway usage was on an irreversible upward trajectory.

The numbers were staggering. India added 10 million vehicles annually to its roads. The government's PM Gati Shakti program planned to build 25,000 km of new highways by 2025. Every new highway that connected to NHIT's existing roads increased their traffic—and toll collections.

But the real moat wasn't just traffic growth—it was the impossibility of competition. The primary responsibilities of the asset monetisation cell include advising NHAI on overall planning and methodology for asset monetisation, conducting market analysis, and feasibility studies to identify potential assets, particularly those with established toll collection records and high revenue generation potential. Additionally, the cell will be tasked with forming a public infrastructure investment trust.

NHAI's monopoly on highway development meant NHIT had exclusive access to the best assets. Private players could build new roads through PPP models, but they took construction risk, traffic risk, and faced longer payback periods. NHIT cherry-picked operational roads with proven economics.

The competitive landscape was more collaborative than combative. While other InvITs like Highways Infrastructure Trust existed, the market was so vast that multiple players could coexist. India's National Monetization Pipeline targeted ₹6 lakh crore from roads alone—enough to sustain multiple InvITs for decades.

Labor and maintenance costs, unlike in healthcare, were relatively predictable. Road maintenance followed established schedules, and while costs increased with inflation, they were a small fraction of toll revenues. The operating leverage was enormous—a 10% increase in traffic translated almost directly to bottom-line growth.

VIII. Playbook: The NHIT Investment Philosophy

Walk into any NHIT deal discussion, and you'll hear the same mantras repeated: "Cash flow is king," "Traffic patterns don't lie," and "Every road tells a story." This wasn't financial poetry—it was hard-learned wisdom from decades of infrastructure investing.

The asset selection criteria were ruthlessly specific. First filter: minimum 5-year operational history with audited toll collections. Second: strategic location on economic corridors, not isolated stretches. Third: limited alternate route options—monopolistic positioning was crucial. Fourth: diversified traffic mix between commercial and passenger vehicles, providing recession resilience.

Due diligence went beyond financial models. Teams spent weeks on highways, counting vehicles at different times, talking to truckers at dhabas, understanding seasonal patterns. They studied satellite imagery for upcoming infrastructure that might divert traffic. They analyzed state election cycles for toll rate revision risks.

The partnership with NHAI was unique—simultaneously the seller, regulator, and sometimes competitor. National Highways Infra Trust (NHIT), sponsored by the National Highways Authority of India (NHAI), was established in 2020 as an InvIT under SEBI regulations. The Trust is managed by National Highways Infra Investment Managers Pvt. Ltd. (NHIIMPL) and overseen by IDBI Trusteeship Services.

This relationship required delicate navigation. NHIT couldn't appear to cherry-pick only the best assets, leaving NHAI with problematic roads. But it also couldn't accept subpar assets that would hurt investor returns. The solution was portfolio deals—bundles that mixed premium and standard assets, averaging to acceptable returns.

Capital allocation followed a clear hierarchy. First priority: maintain existing roads to the highest standards. Second: distribute promised yields to investors. Third: fund accretive acquisitions. Growth for growth's sake was explicitly rejected—every acquisition had to be immediately accretive to distributions.

IX. Bear vs. Bull Case Analysis

The Bear Case:

The pessimists had legitimate concerns. First, the concentration risk was real—Promoter holding is low: 15.3%, meaning NHAI's direct stake was limited, but its control through the Investment Manager was absolute. Any change in government policy could dramatically impact NHIT.

Traffic projection risk loomed large. The financial models assumed 5-6% annual traffic growth in perpetuity. But what if electric vehicles reduced freight transport costs, shifting cargo to rail? What if work-from-home permanently reduced passenger vehicle traffic? The COVID-19 experience showed how quickly traffic could evaporate.

Political risk was ever-present. State elections often brought toll rate freezes or demands for local employment. While contracts provided legal protection, enforcing them against popular political pressure was another matter. The farmer protests of 2020-21, which blocked highways for months, demonstrated the vulnerability.

Competition from alternative infrastructure was accelerating. The dedicated freight corridors, high-speed rail projects, and waterway development could divert traffic from roads. While these were long-term threats, they cast shadows on 30-year concession valuations.

The unit price performance supported bear arguments—trading flat despite strong operational performance suggested market skepticism about long-term sustainability.

The Bull Case:

The optimists painted a different picture, backed by compelling data. India's infrastructure deficit was so massive that even aggressive building wouldn't satisfy demand for decades. The government's ₹111 lakh crore National Infrastructure Pipeline ensured continuous deal flow for NHIT.

NHAI has also identified nine additional road stretches for monetisation through its National Highways Infrastructure Trust (NHIT). With highways expected to contribute Rs 3.5 lakh crore towards the upcoming national monetisation pipeline, NHAI is gearing up to monetise assets worth over Rs 50,000 crore annually over the next five years.

The inflation protection built into toll rates provided a hedge against the single biggest risk for infrastructure investors. Unlike fixed-rate bonds that eroded with inflation, NHIT's revenues grew with or above inflation, preserving real returns.

The institutional backing was unprecedented. When CPP Investments—managing over $500 billion—repeatedly invested in NHIT, it signaled deep conviction. These weren't momentum traders but patient capital with 30-year horizons.

The operational performance supported optimism. Traffic recovery post-COVID exceeded projections, toll collections hit record highs quarterly, and operating margins improved with scale. The distribution track record—never missed, always on time—built institutional credibility.

X. Future Scenarios & Strategic Options

Three scenarios dominate strategic discussions at NHIT's board meetings, each with profoundly different implications for the trust's future.

Scenario 1: The Consolidation Play NHIT becomes India's highway super-trust, absorbing smaller InvITs and private toll road operators. With access to cheap capital and government backing, it could roll up the fragmented market. The end game: a quasi-monopolistic position in highway infrastructure, similar to tower companies in telecom.

Scenario 2: The Asset Class Evolution InvITs mature into a distinct asset class, traded like REITs globally. Index inclusion drives passive flows, options markets develop for hedging, and NHIT becomes the bellwether—India's "Prologis of highways." International expansion becomes possible, managing roads in Bangladesh, Sri Lanka, or Africa.

Scenario 3: The Technology Disruption Autonomous vehicles, dynamic toll pricing, and vehicle-to-infrastructure communication transform highways from dumb assets to smart networks. NHIT pivots from a toll collector to a mobility platform, charging for various services beyond simple road usage. The value creation shifts from financial engineering to operational innovation.

The strategic options reflected these scenarios. Geographic expansion within India was certain—the northeastern states, despite challenging terrain, offered virgin territory. Asset class expansion was being explored—could NHIT acquire airports, ports, or logistics parks that complemented highways?

Technology integration accelerated. Pilots for dynamic toll pricing—higher rates during peak hours—were underway. Blockchain for toll collection, AI for traffic management, and IoT for predictive maintenance were moving from PowerPoints to proof-of-concepts.

The ultimate question remained: What's the exit? Unlike private equity with defined horizons, NHIT was designed as a perpetual vehicle. But markets evolved. Would NHAI eventually sell its stake to private investors? Would NHIT merge with other infrastructure trusts to create scale? Or would it remain a unique hybrid—government-sponsored but market-driven—pioneering a new model for infrastructure financing?

The answer would shape not just NHIT's future but India's entire approach to infrastructure development. As one board member noted, "We're not just managing roads—we're creating a template for how nations can unlock value from public assets while maintaining public purpose."

The highways stretching across India's vast landscape weren't just concrete and tar—they were the arteries of an economy racing toward developed nation status. And NHIT, born during a pandemic, had become the financial architecture making that journey possible.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube