Narayana Hrudayalaya: The Story of Making World-Class Healthcare Affordable

I. Introduction & Episode Roadmap (8-12 min)

Picture this: A cardiac surgeon stands in the operating theater of one of India's busiest hospitals. Behind him, a line of patients stretches down the corridor—farmers, factory workers, domestic help. Each needs heart surgery. Each surgery costs more than most Indians earn in a decade. The surgeon performs 30 operations that day. The cost? Less than what a single procedure would cost in America.

This is not a fantasy. This is Tuesday at Narayana Hrudayalaya.

Devi Prasad Shetty (born 8 May 1953) is an Indian cardiac surgeon who is the chairman and founder of Narayana Health, a chain of 24 medical centers in India. What started as a single hospital in Bengaluru has evolved into something far more ambitious: a systematic assault on the cost structure of healthcare itself.

The numbers tell a story that shouldn't be possible. The company has a market cap of ₹35,252 Crore (up 43.2% in 1 year), operating 19 owned/operated hospitals, 2 heart centers, 18 clinics, and dialysis centers in India, plus 1 hospital in the Cayman Islands, totaling 40 healthcare facilities with 5,789 operational beds. But here's the paradox that defines everything: How does a company that performs heart surgeries for $1,600—when the same procedure costs $100,000 in the US—maintain world-class quality while remaining profitable as a public company?

Some call it "The Walmart of Healthcare." That's wrong. Walmart optimizes for existing demand. Narayana Hrudayalaya created demand where none existed—by making the impossible affordable. This isn't about cheap healthcare. It's about reimagining healthcare economics from first principles.

The story we're about to tell spans continents, challenges conventional wisdom, and asks a fundamental question: Can you build a sustainable business by serving those who've never been served before? The answer lies in the journey from a village in coastal Karnataka to operating theaters in the Cayman Islands, from treating Mother Teresa to listing on the NSE, from charity to scale.

Welcome to the Narayana Hrudayalaya story—where affordability isn't a compromise, it's the entire point.

II. Origins: The Doctor Who Saw Too Much Suffering (40-50 min)

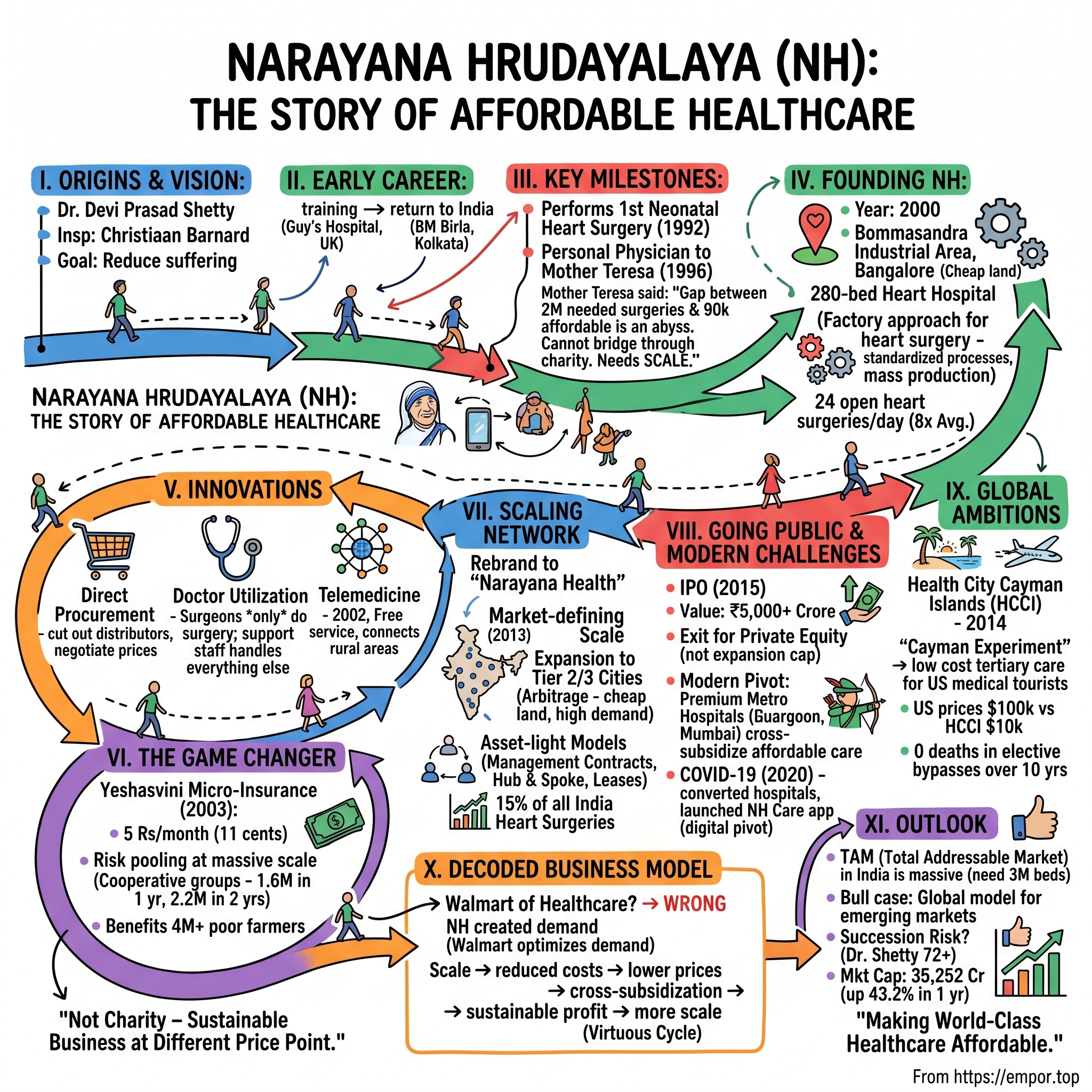

The year is 1969. In the coastal village of Kinnigoli in Karnataka's Dakshina Kannada district, a teenager reads about something extraordinary in the newspaper. Shetty was born in Kinnigoli, a village in the Dakshina Kannada district, Karnataka, India. The eighth of nine children, he decided to become a heart surgeon when he was a school student after hearing about Christiaan Barnard, the South African surgeon who had just performed the world's first heart transplant. For young Devi Prasad Shetty, this wasn't just news—it was destiny calling.

Think about the audacity of that dream. Here's a boy from a village where most people had never seen a stethoscope, deciding he would operate on human hearts. The gap between aspiration and reality was continental. But Shetty had something that mattered more than proximity to opportunity: an acute awareness of suffering.

He completed his MBBS in 1979, and post-graduate work in General Surgery from Kasturba Medical College, Mangalore. But India in the early 1980s wasn't where you learned to be a world-class cardiac surgeon. So Shetty did what ambitious Indian doctors did—he went to the UK, training at Guy's Hospital in London, one of the world's premier cardiac centers.

Here's where the story takes its first unexpected turn. Most Indian doctors who trained abroad in that era never came back. The brain drain was real and devastating. But Shetty returned to India in 1989, bringing with him not just surgical skills but a different way of thinking about healthcare delivery.

He started at B.M. Birla Hospital in Kolkata, and it was there, in the early 1990s, that two events would fundamentally reshape his worldview. First, in 1992, he accomplished a significant milestone by performing India's first neonatal heart surgery on a 21-day-old infant. The technical achievement was remarkable, but the real lesson was different: if you could operate on a 21-day-old heart in India, what else was possible?

The second event was even more transformative. In Kolkata he operated on Mother Teresa after she had a heart attack, and subsequently served as her personal physician. Dr. Shetty served as the personal physician to Mother Teresa in the year 1996, performing angioplasty on her following a myocardial infarction.

But here's what most people miss about the Mother Teresa connection: it wasn't just about prestige. Dr. Shetty saved Mother Teresa's life by performing angioplasty after her heart attack in 1996. He then became her personal physician for the last five years of her life. Their relationship grew beyond typical doctor-patient bonds. Mother Teresa often joined him during hospital rounds to watch him work with young patients.

Watch that image: one of the world's most famous advocates for the poor, walking through hospital wards with a cardiac surgeon, seeing child after child who needed surgery but couldn't afford it. The conversation that must have happened between them—though undocumented—shaped everything that came next.

The math was brutal and simple. "India requires close to 20 lakh heart surgeries a year," as Shetty would later say. That's 2 million people. But only 90,000 could afford it. The gap wasn't just large—it was an abyss. And bridging it through charity was mathematically impossible.

Here's the crucial insight that separated Shetty from other socially conscious doctors: He believes that the cost of healthcare can be reduced by 50 percent in the next 5–10 years if hospitals adopt the idea of economies of scale. Not through charity. Not through government subsidies. Through scale.

This wasn't bleeding-heart idealism. This was cold, hard business logic applied to a humanitarian crisis. If you could do 30 heart surgeries a day instead of 3, if you could negotiate equipment prices based on volume, if you could train surgeons in assembly-line efficiency while maintaining quality—then maybe, just maybe, you could crack the code.

By the late 1990s, Shetty had performed thousands of surgeries. He has performed more than 100,000 heart operations. But individual excellence wasn't the answer. The answer had to be systemic. It had to scale. And for that, he needed to build something entirely new.

The move from Kolkata back to Bangalore wasn't just geographical. It was strategic. Bangalore in the late 1990s was transforming into India's Silicon Valley. It had capital, talent, and most importantly, an ecosystem that understood scale. If you were going to revolutionize Indian healthcare, this was where you'd do it.

But even in Bangalore, the challenges were immense. Healthcare in India wasn't just expensive—it was fundamentally designed for the wealthy. Private hospitals catered to the rich. Government hospitals were overwhelmed and under-resourced. There was no middle ground. No one was solving for the missing middle—the hundreds of millions who weren't poor enough for government charity but couldn't afford private healthcare.

The fundamental problem wasn't just economic—it was philosophical. The entire global healthcare industry was built on a premise: quality costs money. More quality means more cost. It was as fundamental as gravity. But what if gravity was wrong? What if you could deliver higher quality at lower cost through radical efficiency?

"Japanese companies reinvented the process of making cars. That's what we're doing in healthcare," Shetty told the Wall Street Journal. "What healthcare needs is process innovation, not product innovation."

Think about that statement. He wasn't talking about inventing new surgical techniques or breakthrough drugs. He was talking about Toyota Production System for heart surgery. About Six Sigma for cardiac care. About turning healthcare into a process that could be optimized, standardized, and scaled without sacrificing outcomes.

The vision was crystallizing: Build a hospital that operates like a factory—but a factory where the product is human life, where efficiency serves compassion, where scale enables access. It sounded impossible. It sounded like a contradiction. It sounded exactly like the kind of challenge that someone who'd decided to become a heart surgeon in a coastal Karnataka village would take on.

By 2000, everything was in place. The experience, the vision, the location, and crucially, the initial funding from his father-in-law. The boy from Kinnigoli who'd dreamed of becoming a heart surgeon was about to build something that would make those dreams accessible to millions of others.

III. The Founding Vision: Building NH (2000-2008) (45-55 min)

The year 2000. Y2K had passed without the technological apocalypse everyone feared. But in a different corner of Bangalore, a different kind of disruption was beginning. Devi Shetty founded Narayana Hrudalaya (NH) in the year 2000 with a 280-bed heart hospital in Bangalore. The location choice was deliberate and telling: Bommasandra Industrial Area, on the outskirts of the city. Not the premium neighborhoods where Apollo and Fortis were setting up. The periphery. Where land was cheap and assumptions could be challenged.

In 2001, Shetty founded Narayana Hrudayalaya (NH), a multi-specialty hospital in Bommasandra on the outskirts of Bangalore. The facility spread over 25 acres, it is located in the Bommasandra Industrial Area on the Hosur Road in Bangalore. With the Phase I of the construction being completed, the hospital currently has six stories containing 500 beds and 10 operating theatres.

But here's what's remarkable: from day one, this wasn't positioned as a charity hospital or a compromise solution. The equipment was the same that you'd find at Cleveland Clinic. The surgeons were trained at the world's best institutions. The only thing different was the price tag—and the operational philosophy that made that price possible.

Let's talk about the economics, because the economics are everything. By 2001, Shetty set up the Narayana Hrudayalaya on a 25-acre campus in Bengaluru, with much of the funding coming from his father-in-law. This wasn't venture capital. This wasn't private equity. This was family money betting on a vision that most investors would have laughed out of the room. Why? Because the unit economics looked insane.

A heart surgery that cost $100,000 in the US, Shetty wanted to do for $2,000. Not by cutting corners—the success rates had to match or exceed international standards. Not by underpaying staff—though Indian healthcare salaries were lower, they still needed to attract top talent. The magic had to come from somewhere else: volume.

Narayana Hrudayalaya performs approximately 24 open heart surgeries and 25 catheterization procedures a day, almost eight times the average at other Indian hospitals. In cardiology, the hospital specialises in Interventional Cardiology, Electrophysiology and Pediatric Cardiology. Think about that: eight times the average. While a typical Indian hospital might do 3 heart surgeries a day, NH was targeting 24.

The assembly line analogy everyone uses is both right and wrong. Right because the efficiency gains came from repetition, specialization, and process optimization. Wrong because unlike cars, every patient was unique, every surgery had its complexities, every life mattered individually. The trick was to standardize everything that could be standardized—procurement, pre-op, post-op, administration—while maintaining flexibility in the actual medical care.

Here's a detail that captures the innovation: NH started buying medical supplies directly from manufacturers, cutting out distributors. When you're buying sutures for 24 surgeries a day, 365 days a year, you have negotiating power. When GE or Siemens knows you'll be their largest customer in India for certain equipment, they listen. The savings weren't incremental—they were transformational.

But the real innovation wasn't in procurement. It was in the fundamental rethinking of hospital design and doctor utilization. In a traditional hospital, a cardiac surgeon might spend hours on administrative work, consultations, and waiting. At NH, surgeons did surgery. Period. Everything else was handled by a support system designed for that singular focus.

In 2015, Forbes described how Shetty's hospitals made heart surgeries affordable in India: …because his doctors go from one operating table to the next with an assembly line precision that is rare in the Indian healthcare system. One surgeon, multiple operating theaters, continuous flow. While one patient was being prepped, another was under the knife, another in recovery. The surgeon moved between them like a conductor orchestrating a complex symphony.

The cultural challenge was immense. Indian healthcare, like healthcare everywhere, was built on hierarchy and tradition. Senior surgeons had their ways. Nurses had their protocols. Administrators had their systems. NH was asking everyone to reimagine their roles. Not everyone was ready for that.

There's a story from those early days that's telling. A senior surgeon from a prestigious hospital joined NH and quit after a week. His complaint? "I felt like a factory worker." Shetty's response was characteristic: "Good. Factory workers have perfected efficiency. We should learn from them." Not everyone got it. But those who did became evangelists.

The early results were promising but challenging. A total of 13000 coronary bypass grafting operations have been performed in the hospital. The hospital also acts as a philanthropist by charging less than the normal cost for procedures like angiogram and cardiac surgery to people who cannot afford to pay the huge costs. The volume was building, but the model needed validation beyond just surgical success.

Then came an innovation that nobody saw coming: telemedicine. The telemedicine service was started in the hospital in the year 2002 to cater mainly to the rural populace in the country. The telemedicine network of the hospital connects to countries like Malaysia, Mauritius and Pakistan. The telemedicine services provided by the hospital are free and more than 21000 cases have been referred using this service.

This wasn't just about technology. It was about extending the reach of expertise without the cost of physical infrastructure. A patient in rural Karnataka could get an ECG, transmit it to Bangalore, and get a cardiac consultation within hours. The cost? Negligible. The impact? Transformational.

By 2003, the hospital was performing something remarkable: "In fiscal 2015, Narayana Hrudayalaya performed 51,456 cardiology procedures, 14,036 cardiac surgeries, and 184,443 dialysis procedures"—though these numbers would come later, the foundation for this scale was being laid in these early years. The facility was proving that volume-based healthcare could work.

But Shetty understood something crucial: "India needs three million new beds for treatment and as of now, healthcare reaches to about 10-15% of the population," Shetty told the Times of India newspaper. "The government cannot build so many beds and it has to be done by private sector. Without a large capital backing, we cannot scale as healthcare needs capital."

This presented a paradox. To serve the poor, you needed scale. To achieve scale, you needed capital. To attract capital, you needed returns. To generate returns while serving the poor, you needed a model that nobody had proven could work. It was a circular problem that would have stopped most people. But Shetty had an idea that would change everything: micro-insurance.

The other challenge was talent. You couldn't run 24 surgeries a day without surgeons. But India wasn't producing enough cardiac surgeons. NH's solution? Become a teaching hospital. Train your own. But not the traditional way—the NH way. Residents at NH would see more surgeries in a month than most would see in a year elsewhere. They'd learn by doing, repeatedly, under supervision. It was medical education meets apprenticeship meets scale.

There was also the question of quality. How do you maintain quality when you're operating at such velocity? The answer was counterintuitive: the velocity itself improved quality. When a surgeon performs 10 procedures a day rather than 1, they see more variations, encounter more complications, develop more expertise. Practice doesn't just make perfect—at scale, practice makes exceptional.

The data started proving this out. NH's mortality rates weren't just competitive with expensive private hospitals—they were often better. The infection rates were lower. The recovery times were faster. It turned out that when you do something thousands of times, you get very, very good at it.

By 2008, what had started as a 280-bed hospital had evolved into something much larger. The model was proven. The operations were refined. But the real breakthrough—the innovation that would take NH from successful hospital to healthcare revolution—was just about to begin. It would come not from medicine or management, but from insurance. And it would start with farmers who'd never had insurance in their lives.

IV. The Game Changer: Yeshasvini Micro-Insurance Revolution (2003-2010) (50-60 min)

Picture the scene: It's 2003, and Devi Shetty is in a meeting with Karnataka government officials. The topic isn't healthcare delivery—it's agricultural productivity. The state's farmers are in crisis. Not just from failed monsoons or falling prices, but from something more insidious: medical debt. A single health emergency could wipe out generations of savings, forcing families to sell land that had been theirs for centuries. The officials want solutions. Shetty proposes something audacious: health insurance for farmers at 5 rupees per month.

The room goes silent. Five rupees. In 2003, that was about 11 cents. Less than the cost of a cup of chai. The officials think he's joking. He's not.

The Yeshasvini Insurance Scheme was launched on 1st June 2003, by the then Chief Minister of Karnataka, Mr S.M. Krishna. The scheme was first launched in the year 2003 to impact the resource-poor healthcare facilities and economic well-being across the state. The scheme benefits farmers from 30 districts in Karnataka and is managed by the Yeshasvini Cooperative Farmers Health Care Trust.

The math seemed impossible. How could you provide meaningful health coverage for 5 rupees per month? The answer lay in understanding risk pooling at massive scale and the unique structure of rural cooperatives. Yeshasvini Health Insurance Scheme was launched by the former Chief Minister of Karnataka, S.M.Krishna in the year 2003 to offer comprehensive coverage to farmers who are members of the state co-operative societies.

Here's the genius of the structure: Karnataka had millions of farmers organized into cooperatives. These weren't individuals buying insurance—entire cooperatives would enroll together. No adverse selection. No cherry-picking. Everyone in or everyone out. Cooperative society members enrolled under the Karnataka Cooperative Societies Act, 1957, Karnataka Souhardha Sahakari Act, 1997, or Multi-State Cooperative Societies Act, 2002 were eligible.

The premium structure evolved quickly. The 20-year-old Yeshasvini scheme, created with the Karnataka government, started with a monthly charge of Rs 5 per person which later went up to Rs 10. The program grew faster than expected, with 1.6 million farmers joining in the first year and 2.2 million in the second year. Even at 10 rupees, it was revolutionary.

But here's what made it work: the integration with NH's high-volume, low-cost model. For a minimum premium amount of ₹250 annually, farmers and their families in Karnataka can get coverage for various medical procedures up to ₹2.5 lakhs. The scheme covered 823 surgical procedures.

The operational innovation was as important as the financial one. Farmers didn't need to pay upfront and seek reimbursement—a impossibility for people living harvest to harvest. The insured can get a cashless procedure done at any network hospital empanelled under the scheme up to the prescribed limit. Show your Yeshasvini card, get treated, go home. No paperwork. No loans. No land sold.

The early results exceeded everyone's expectations. Arguably the world's largest health insurance scheme for the rural poor, the scheme commenced in 2003. Designed in ways that overcome several obstacles to providing health security for rural populations, the scheme covered, in its second year, about 2.2 million widely dispersed peasant farmers for surgical and out patient care for a low annual premium of approximately US$2.

But success brought its own challenges. The government was supportive but skeptical about long-term sustainability. Private hospitals initially refused to participate—the rates were too low. Even within NH, there were concerns about whether serving Yeshasvini patients at these rates was viable.

Shetty's response was to double down. He published the data: Yeshasvini patients had the same outcomes as private patients. The volume made up for the lower margins. More importantly, it proved the model. This wasn't charity—it was sustainable business at a different price point.

The ripple effects were extraordinary. More than 4 million poor farmers now have coverage through this initiative. Farmers who'd never seen the inside of a hospital were getting cardiac surgeries. Rural families weren't going bankrupt from medical emergencies. The state government was seeing improved agricultural productivity because farmers weren't abandoning their fields to pay medical debts.

He helped start the Yeshasvini Micro-Health Insurance Scheme and formed Narayana Health, revolutionizing overall accessibility to healthcare. The scheme became a template. Other states took notice. The success of Yeshasvini has inspired similar schemes in other Indian states, such as the Rajiv Arogyasree in Andhra Pradesh and the Kalaingar Insurance in Tamil Nadu.

The learning from Yeshasvini went beyond insurance. It taught NH crucial lessons about serving the bottom of the pyramid. These patients traveled long distances, often bringing extended families. They couldn't afford multiple trips. So NH redesigned its processes: diagnosis to discharge in minimal time. Family accommodation on campus. Simplified communication for patients who might be illiterate.

There's a story that captures the transformation. A farmer from northern Karnataka needed heart surgery. The total cost through Yeshasvini: 500 rupees (about $10). The actual cost to NH: 50,000 rupees. The surgery was successful. The farmer returned to his village and his fields. His story spread. Suddenly, heart surgery wasn't something that only happened to rich people in cities. It was possible. It was accessible. It was real.

The government partnership aspect was crucial but complex. The Yeshasvini Cooperative Farmers Health Care Trust is the monetary reservoir that manages the effective implementation of the Yeshasvini Scheme. The Yeshasvini Insurance Scheme is headed by the Chief Minister of Karnataka, and the Minister of Cooperation is also closely associated with it. Along with the Chief Minister and the Minister of Cooperation, 5 senior officers, a principal secretary, and several highly qualified doctors form the scheme's governing body. The Karnataka Government and the citizens together make contributions towards the trust.

This wasn't a typical government program. It was a public-private partnership where the government provided the framework and partial funding, cooperatives provided the organization and collection mechanism, and private hospitals like NH provided the services. It was collaborative capitalism at its best.

The data vindication came from unexpected sources. A study conducted by NABARD Consultancy services in the year 2007 reveals that 60 per cent of the beneficiaries expressed satisfaction with the scheme. For a government program in India to achieve 60% satisfaction was almost unheard of.

But Yeshasvini also revealed the limits of the charity model. Even at massive scale, even with government support, insurance alone couldn't solve the healthcare access problem. NH needed more capital to build more hospitals. They needed to expand beyond Karnataka. They needed to be in every major city and small town. And for that, they needed a different kind of scaling mechanism.

The lesson was clear: you could innovate on price, you could revolutionize insurance, you could achieve operational excellence. But at the end of the day, healthcare is a capital-intensive business. Buildings, equipment, talent—they all cost money. And while Yeshasvini proved the demand existed and the model worked, it also proved that to truly transform Indian healthcare, NH needed to think bigger.

By 2010, Yeshasvini was covering millions, NH was performing thousands of surgeries monthly, and the model was proven. But Shetty knew they were still only scratching the surface. India needed not one NH but hundreds. The question was how to build them. The answer would require rethinking not just healthcare delivery or insurance, but the very structure of how hospitals were built, owned, and operated. The next phase was about to begin, and it would transform NH from a successful hospital into a healthcare network that would span the nation.

V. Scaling Up: From Hospital to Healthcare Network (2008-2014) (40-50 min)

The conference room at NH's Bangalore headquarters, 2012. On the whiteboard: a map of India dotted with red pins. Each pin represents a city where NH should be but isn't. The math is sobering—to reach even 10% of Indians who need cardiac care, NH would need 200 hospitals. At the current pace of building one hospital every two years, that would take four centuries.

Shetty looks at the map and makes a decision that will fundamentally alter NH's trajectory: "We need to stop thinking like hospital builders and start thinking like a network."

In 2013, Narayana Hrudyalaya officially changed its identity to Narayana Health. This wasn't just rebranding—it was a declaration of intent. The company was no longer just about heart care (Hrudayalaya means "heart temple"). It was about health, period.

The expansion strategy that emerged was unlike anything the Indian healthcare industry had seen. While Apollo and Fortis were building gleaming towers in metro cities, NH was pursuing what can only be called "healthcare arbitrage." They identified tier-2 and tier-3 cities where land was cheap, competition was minimal, but demand was enormous. Jamshedpur, Mysore, Jaipur, Dharwad—places other chains ignored.

But the real innovation wasn't where they built—it was how. The traditional model required massive capital expenditure upfront. Buy land, construct building, purchase equipment, hire staff. NH pioneered multiple models that dramatically reduced capital requirements:

The Management Contract Model: Local entrepreneurs or trusts would build the facility. NH would manage it, bringing their operational expertise, brand, and systems. Revenue sharing rather than ownership. Asset-light expansion.

The Hub and Spoke Model: Not every facility needed to be a 500-bed hospital. NH created "heart centers"—smaller facilities focused on diagnostics and basic procedures, connected to main hospitals for complex surgeries. 7 heart centers (superspeciality units which are set up in a third party hospital) expanded their reach without massive investment.

The Lease Model: Existing hospitals with underutilized capacity would lease floors or wings to NH. Overnight, NH could add a cardiac unit to a general hospital, leveraging existing infrastructure while bringing their specialized expertise.

By 2014, the network had exploded. It has a network of 23 hospitals, 8 heart centres and 24 primary care facilities. But managing this network presented new challenges. How do you maintain quality across dozens of facilities? How do you ensure the NH model works in Jamshedpur the same way it works in Bangalore?

The answer came from an unexpected source: technology. NH built one of India's most sophisticated hospital information systems. Every surgery, every prescription, every outcome was tracked in real-time. Surgeons in Bangalore could review cases in Mysore. Best practices identified in one location were immediately propagated across the network. It was healthcare meets big data before "big data" became a buzzword.

The telemedicine initiative, started modestly in 2002, became a cornerstone of the network strategy. Narayana Hrudayalaya also has 17 Coronary Care units which are based in remote cardiac hospitals but are linked to Narayana Hrudayalaya. These units handle emergency cardiac-related cases and the patients are controlled and stabilised before the cardiac specialists are consulted.

But technology was just an enabler. The real scaling secret was people. NH created what was essentially a medical assembly line for talent production. Their residency programs weren't just about training doctors—they were about creating "NH doctors." Physicians who understood high-volume surgery, who thrived in the efficiency-focused environment, who believed in the mission of affordable care.

The economics of scale were finally kicking in fully. When you're buying MRI machines for 23 hospitals, vendors listen. When you're purchasing stents by the thousand, manufacturers negotiate. NH's purchasing power allowed them to drive costs down not just for themselves but effectively reset market prices for medical supplies in India.

There was also a subtle but important shift in the patient mix. While Yeshasvini farmers remained important, NH was increasingly serving India's emerging middle class—people with some money but not enough for Apollo or Fortis. The company discovered they could cross-subsidize: charge the middle class reasonable rates to subsidize free and discounted care for the poor.

Narayana Health hospitals serve anyone who needs care, regardless of their ability to pay. Each year, more than half of patients receive free or subsidized inpatient care, with an average discount of 15 percent. This is accomplished through philanthropy and a cross-subsidy model, in which higher-income patients pay more for nonclinical amenities, such as private recovery rooms. Since the total charges are still far below the cost of comparable services at other private hospitals, Narayana Health is still an attractive option for such consumers.

The clinical specialization strategy was particularly clever. While expanding geographically, NH also expanded vertically into new specialties—but selectively. Oncology, orthopedics, neurosurgery—specialties that could leverage the same high-volume, low-cost model. Each new specialty wasn't just an addition; it was a multiplication of the model's power.

By 2013, NH was performing procedures at a scale that boggled the mind. The group performs a remarkable 15% of all heart surgeries done in India, demonstrating its significant scale and expertise. Think about that—one hospital group doing 15% of an entire nation's heart surgeries. It wasn't just scale anymore; it was market-defining scale.

The transformation also required cultural evolution. The scrappy startup that Shetty founded was becoming a corporation. Systems replaced individual judgment. Protocols standardized operations. Some of the early entrepreneurial spirit was inevitably lost. But Shetty understood this was the price of scale. You couldn't transform Indian healthcare with one hospital, no matter how innovative.

There were failures too. Not every expansion worked. Some locations didn't generate expected volumes. Some partnerships soured. Some local markets proved more resistant to the NH model than expected. But the network effect meant individual failures didn't threaten the whole. The portfolio approach to expansion provided resilience.

International recognition started flowing. Harvard Business School wrote case studies. The Economist featured NH as a model for emerging market healthcare. International delegations arrived to study the model. The kid from Kinnigoli who wanted to be a heart surgeon was now reshaping global thinking about healthcare delivery.

But even as NH was conquering India, Shetty's ambitions were growing beyond national borders. If the model worked in India, why not elsewhere? If you could provide affordable healthcare to Indian farmers, why not Caribbean islanders? Or eventually, even Americans priced out of their own healthcare system?

The pieces were in place. The model was proven. The network was established. Capital markets were taking notice—private equity firms were circling, seeing the potential for returns in affordable healthcare. But Shetty had an even bolder idea. Instead of just expanding within the constraints of the Indian market, why not take the model to developed markets and compete directly with their bloated, expensive systems?

It sounded impossible. It sounded exactly like something NH would try. The next chapter would take them 10,000 miles from Bangalore to a small Caribbean island that most Indians couldn't find on a map. But that island might just be the key to revolutionizing not just Indian healthcare, but American healthcare too.

VI. International Ambitions: The Cayman Islands Experiment (2014-2016) (45-55 min)

The location seems absurd at first glance. The Cayman Islands—population 65,000, known primarily for offshore banking and cruise ship stops. Why would an Indian hospital chain focused on affordable care choose to build a facility in one of the world's most expensive jurisdictions?

The answer requires understanding geography, regulation, and the catastrophic failure of American healthcare economics. Look at a map: Grand Cayman sits 480 miles south of Miami. It's closer to the US than Hawaii is to California. It's within a four-hour flight of 150 million Americans. And crucially, it's outside the regulatory morass of US healthcare.

Devi Shetty founded Health City Cayman Islands. The 107,000 square foot facility opened in February 2014. But the genesis of this project went back years earlier, to conversations with an unlikely partner: Ascension Health, one of America's largest Catholic health systems.

Ascension partnered with Narayana Health and the Cayman government in 2012 to bring innovative, high-quality, low-cost tertiary healthcare services to the Cayman Islands. The result was Health City Cayman Islands (HCCI), a 104-bed tertiary care hospital on Grand Cayman. After working closely for nearly four years with leaders from Narayana and the government in an innovative public-private partnership to build the strengths and capabilities of HCCI, the hospital is now achieving its vision.

The strategic logic was brilliant. American healthcare prices had become so absurd—$100,000+ for cardiac surgery, $50,000+ for knee replacements—that even with travel costs, Americans could save 80-90% by going abroad. Medical tourism was already a billion-dollar industry. But most destinations had drawbacks: language barriers in Thailand, quality concerns in Mexico, distance to India.

The Cayman Islands solved these problems. English-speaking, British legal system, direct flights from major US cities, and now, with HCCI, world-class healthcare at Indian prices. The construction of a multispecialty hospital opening in February 2014 less than a 4-hour flight away from the United States and convenient to both Central and South America for patients who already travel to the United States for clinical care could reshape the US health care marketplace.

The economics were compelling. A cardiac bypass that cost $100,000 in Miami cost $10,000 at HCCI. Even adding flights and accommodation, American patients could save $75,000+. For uninsured or underinsured Americans—nearly 50 million people—this wasn't just savings. It was the difference between getting treatment and dying.

But building in the Cayman Islands presented unique challenges. Everything had to be imported—equipment, supplies, even construction materials. The facility had to be hurricane-proof—The 104-bed tertiary care hospital features a reinforced roof, walls, doors and windows, was built to withstand category 5 hurricanes, and shield all of its critical assets from flooding. Labor costs were multiples of India. This wasn't going to be as cheap as building in Bangalore.

The solution showcased NH's evolution as an organization. Health City is a 107,000-sq.-ft. hospital built on Grand Cayman Island in the Caribbean. Most remarkably for the health care industry, it was built to U.S. hospital standards in half the time and budget. The same type facility in the U.S. typically runs $1,000,000 per bed. Health City Cayman's hospital came in at $424,000 per bed. for less than half the cost!

How did they achieve this? Innovation at every level. The project was design-build, which allowed for the construction and design teams to work together to improve functionality, construction speed, and reduce cost. Third, they used pre-built components, such as prefabricated bathroom pods, to increase speed of construction. These were fabricated at the same time as the ICF structure was being erected, and shipped to the island 100% complete.

The early operations were challenging. Convincing Americans to travel for surgery required overcoming deep skepticism. The first patients were mostly Caymanians and medical tourists from other Caribbean islands. Volume was below projections. Critics questioned whether the model could work outside India's unique context.

Then came the results that silenced skeptics. HCCI has served more than 46,000 patients since opening its doors, with an initial focus on cardiac and orthopedic procedures and later expanding into other services. HCCI's medical teams, who treated patients from 60 countries just in 2016, champion innovation and have scored notable firsts in the region. HCCI became the first hospital in the English-speaking Caribbean to use robotic navigation for joint replacements and the first to install two artificial hearts or left ventricle assist devices.

The quality metrics were exceptional. Incidentally, there have been no deaths or reinterventions from elective coronary bypass surgery at Health City Cayman Islands over the past decade. Zero deaths in elective cardiac surgery over a decade. That's not just good—that's world-class by any standard.

HCCI also became an innovation laboratory for NH. Freed from Indian regulatory constraints and serving a more affluent patient base, they could experiment with new technologies and procedures. Health City Cayman Islands became the first English-speaking Caribbean facility to perform the TAVR procedure, which is the replacement of the heart's aortic valve through the blood vessels. Health City also became the only facility in the Americas to offer Cardiac Contractility Modulation (CCM) device implantation for the treatment of heart failure.

The partnership with Ascension brought American operational expertise. Joint Commission International accreditation—the gold standard for international hospitals—was achieved quickly. HCCI is a world-class hospital accredited by Joint Commission International that opened in 2014 and has received praise for its quality outcomes and caring, compassionate care.

But the real validation came from an unexpected source: American insurance companies. Some began quietly covering procedures at HCCI, recognizing the massive cost savings without quality compromise. A few self-insured American employers started sending employees to Cayman for elective procedures. The trickle was becoming a stream.

The facility's energy efficiency was another triumph. In the hot, humid Caribbean environment, with cooling needed every day of the year, electrical costs were projected at US$2.1 million annually. After the first year of operation, though, the actual costs were US$1,446,536, a savings of 31%. and second year costs were even lower. The combination of innovative construction and intelligent systems had created one of the most efficient hospitals in the tropics.

The Cayman project also revealed NH's growing sophistication in international partnerships. The development was made possible by an interesting confluence of public and private interests in developing medical tourism in Grand Cayman. They navigated complex negotiations with the Cayman government, which provided regulatory support and land. They structured the Ascension partnership to leverage American expertise while maintaining the NH model's core principles.

By 2016, HCCI was more than operational—it was proving a point. The NH model wasn't just for poor Indians. It could work anywhere healthcare costs had spiraled out of control. It could compete on quality with the best American hospitals while delivering care at a fraction of the cost.

Health City will eventually include a 2,000-bed multispecialty hospital developed over a period of 10 years on Grand Cayman. The long-term vision was audacious—not just a hospital but a healthcare city, eventually rivaling major American medical centers in scope if not in price.

However, tensions were emerging. After working closely for nearly four years with leaders from Narayana and the government in an innovative public-private partnership to build the strengths and capabilities of HCCI, the hospital is now achieving its vision. Ascension, facing its own challenges in the US market, would eventually exit the partnership in 2017, leaving NH as the sole operator. This was both challenge and opportunity—full control but also full responsibility.

The Cayman experiment taught NH crucial lessons about international expansion. You couldn't just transplant the Indian model wholesale. Local adaptation was essential. Labor costs would always be higher outside India. But the core insight—that healthcare could be delivered at high quality and low cost through operational excellence—was universally applicable.

More importantly, HCCI proved NH could compete globally. They weren't just a low-cost Indian provider. They were innovators in healthcare delivery who happened to be from India. The distinction mattered, especially as NH contemplated its next big move: going public.

The international validation from the Cayman Islands would prove crucial in the IPO roadshow. Here was proof that NH wasn't just arbitraging Indian labor costs. They had built something more fundamental—a better way to deliver healthcare. And that model was worth something to investors looking for the next big thing in one of the world's largest industries.

But even as HCCI was finding its footing, back in India, pressure was building. The company needed capital to fund expansion. Private equity investors who had backed NH years ago wanted exits. The Indian healthcare market was heating up with competition. The time had come for NH to take the ultimate step in its evolution from mission-driven startup to public corporation. The question was: could they maintain their social mission while satisfying shareholder demands for returns?

VII. Going Public: The IPO and Its Aftermath (2015-2018) (50-60 min)

December 10, 2015. The investment bankers from Axis Capital, IDFC Securities, and Jefferies India gather in NH's boardroom. On the table: the final prospectus for what would be one of India's most watched IPOs of the year. The price band has been set: ₹250.00 per share. The math is simple but the implications are profound: NH is about to be valued at over ₹5,000 crore (roughly $750 million).

But here's the twist that makes this IPO unusual: The issue is priced at ₹250 per share. Narayana Hrudayalaya IPO is a main-board IPO of 2,45,23,297 equity shares of the face value of ₹10 aggregating up to ₹613.08 Crores. And crucially—not a single rupee was going to the company for expansion.

This wasn't a growth capital raise. This was an exit. 3 investors - Pinebridge (through Ashoka Investment and Ambadevi Mauritius), JP Morgan and UK's CDC hold 29.85% stake, whose combined holding will shrink to 19.85% post IPO. Pinebridge and JP Morgan holding 21.96% stake at present, are part-exiting their 8 year old investment with IRR of just ~13% pa.

Think about the optics. A hospital chain built on serving the poor, going public primarily to give private equity firms their exit. The ironies were sharp. The contradictions obvious. Yet Shetty was pragmatic. Those investors had taken risks when nobody else would. They deserved their returns. And being public would bring other advantages—currency for acquisitions, credibility for international expansion, discipline in operations.

The roadshow was fascinating theater. Here was Shetty, the cardiac surgeon turned entrepreneur, sitting across from fund managers in Mumbai and Singapore, explaining why a hospital that charged $1,600 for heart surgery was worth a premium valuation. The pitch wasn't about margins—NH's EBITDA margins were in the low teens, well below Apollo's 20%+. It was about scale, growth, and the massive underserved market.

Narayana Hrudayalaya IPO bidding started from Dec 17, 2015 and ended on Dec 21, 2015. The shares got listed on BSE, NSE on Jan 6, 2016.

The IPO's reception was lukewarm. The initial public offer of healthcare services major Narayana Hrudayalaya Ltd (NHL) was subscribed 7 per cent on the first day of the issue on Friday. This wasn't the overwhelming response that other healthcare IPOs had received. Investors were skeptical. Could a low-cost model generate sustainable returns? Could NH maintain quality while serving price-sensitive patients? Could the founder's social mission coexist with shareholder capitalism?

The anchor investors provided some confidence. Narayana Hrudayalaya has raised Rs 184 crore from 15 anchor investors, including the Singapore government, at the upper price band. When Singapore's sovereign wealth fund invests, others pay attention.

But there was a moment that captured the tension perfectly. In the prospectus, buried in the fine print, was a note about retail discount. Earlier drafts had promised a discount for retail investors—a nod to NH's democratic ethos. Both the DRHP and even RHP (as recent as 8th December 2015) to the issue mention consideration of retail discount, which has not been given, when price band was announced on 10th Dec. This is similar to going back on the candy promised to a child! The discount was quietly dropped. The symbolism wasn't lost on anyone.

January 6, 2016. The Narayana Hrudayalaya IPO listing date is on Wednesday, January 6, 2016. The stock opens at ₹304, a 22% premium to the issue price. Then reality sets in. Within weeks, it's trading below the IPO price. The market's message is clear: prove it.

The immediate post-IPO period was challenging. Public market scrutiny was different from private investor patience. Every quarter mattered. Every metric was dissected. The pressure to improve margins was intense. Nearly a fourth of the issue is an offer for sale from existing promoters including Shetty and institutional shareholders Ashoka Investment and Ambadevi Mauritius. Promoters had sold shares too, though they maintained promoters hold 66.85%, which will decline to 64.85%, post IPO.

The strategic response was subtle but significant. Without abandoning the core mission, NH began to evolve its mix. The company realized that to fund affordable care, they needed higher-margin businesses. The answer: premium hospitals in metros.

From 2016 onwards, NH has increased its presence in New Delhi, Gurgaon and Mumbai, by opening premium multi specialty hospitals, in order to boost margins. This wasn't betrayal of the mission—it was evolution. The profits from a premium hospital in Gurgaon could fund free surgeries for farmers in Karnataka. It was Robin Hood economics, but transparent and sustainable.

The operational refinements accelerated. Listed companies face different scrutiny than private ones. Systems were formalized. Governance structures strengthened. Financial reporting became more sophisticated. The scrappy startup culture was giving way to corporate professionalism.

But public listing also brought unexpected benefits. Talent acquisition became easier—stock options meant something now. International partnerships were simpler—public companies had credibility. Most importantly, the discipline of quarterly earnings calls forced operational improvements that might have been delayed otherwise.

The market's initial skepticism began to fade as the numbers proved the model. Revenue grew consistently. The network expanded. Quality metrics remained strong. By 2018, the stock had found its level, and investors were beginning to understand what NH represented: not a traditional hospital chain, but a new model for healthcare delivery in emerging markets.

There were missteps. Some premium hospital launches disappointed. Competition in metros was fiercer than expected. Apollo and Fortis weren't standing still. Max Healthcare was growing aggressively. The easy wins were gone. Every expansion now required careful calculation.

The Cayman Islands expansion continued to evolve. Post-Ascension's exit in 2017, NH had full control but also full responsibility. "The commendable performance of this facility underpins the success our differentiated business model even in unexplored international territories like Caribbean Islands," Dr. Shetty said. "We remain confident about the prospects of this facility in terms of attracting international patients from the neighbouring islands in need of care. We greatly appreciate Ascension's support over the past five years as together we brought world-class healthcare to the Caribbean region."

The philosophical tensions were real and ongoing. Every earnings call included questions about margin improvement. Analysts wanted to know why NH didn't focus exclusively on higher-margin specialties. Why maintain the Yeshasvini contracts with their razor-thin margins? Why not be more like Apollo?

Shetty's answers were consistent but not always satisfying to Wall Street: This was the model. Scale over margins. Volume over price. Access over exclusivity. If investors wanted a high-margin hospital chain, there were other options. NH was building something different.

The public market journey was also educating NH about financial engineering. They learned to optimize working capital, manage debt more efficiently, and think about capital allocation more strategically. The CFO role, previously secondary to operations, became central to strategy.

By 2018, three years post-IPO, NH had found its rhythm as a public company. The stock had stabilized. The strategy was clear. The expansion continued. But new challenges were emerging. The government was launching Ayushman Bharat, the world's largest public health insurance scheme. Digital health startups were raising massive rounds. The competitive landscape was shifting.

More fundamentally, the question of succession was looming. Shetty was 65. The company was still very much founder-driven. Could NH's mission survive beyond its founder? Could the culture of affordable excellence persist in a public company focused on quarterly results? These weren't immediate crises, but they were shadows beginning to lengthen.

The IPO had been necessary—for the investors who needed exits, for the credibility required for expansion, for the capital markets validation of the model. But it had also changed NH fundamentally. The company that went public in 2016 was very different from the one that would face its biggest challenge yet: a global pandemic that would test every assumption about healthcare delivery.

VIII. Modern Challenges & Strategic Pivots (2018-Present) (45-55 min)

January 2019. The boardroom at NH headquarters carries an unusual tension. Emmanuel Rupert was made the MD & Group CEO in place of Ashutosh Raghuvansha following the latter's resignation in January 2019. This isn't just a CEO change—it's a generational transition. Raghuvanshi, who had been with NH since 2006, represented continuity. His departure signals something shifting in NH's DNA.

Emmanuel Rupert brings a different energy—more corporate, more focused on margins, more attuned to what public markets want. The founder remains chairman, but day-to-day operations are transitioning to professional management. It's a delicate balance: maintaining the mission while satisfying shareholders.

Then, March 2020. COVID-19 arrives like a tsunami. Every assumption about hospital operations gets shattered overnight. Elective surgeries—the bread and butter of any hospital—vanish. International patients disappear. The Cayman facility, dependent on medical tourism, faces an existential crisis.

But crisis reveals character. NH's response showcases both its operational excellence and its mission-driven DNA. Within weeks, entire hospitals are converted to COVID facilities. The high-volume operational model—designed for cardiac surgery—proves remarkably adaptable to managing COVID wards. The ability to handle large patient volumes, refined over two decades, becomes literally life-saving.

The financial hit is severe. 2020 sees revenues crater and margins evaporate. But NH's diversified network provides resilience. While metros struggle with lockdowns, smaller cities maintain some normalcy. While international operations stall, domestic insurance patients keep coming. The portfolio approach to expansion, sometimes criticized by analysts, proves its worth.

The pandemic also accelerates digital adoption. in 2020, it launched the NH Care app. This step was taken to ensure people could also take virtual consultations. What might have taken years happens in months. Teleconsultations, digital health records, remote monitoring—suddenly, NH's patients, including rural farmers, are comfortable with digital health.

Recovery from COVID is swift but uneven. By 2021, elective surgeries resume with pent-up demand. But the market has changed. Patients are more health-conscious but also more price-sensitive. Insurance penetration has increased but so has scrutiny of claims. Competition has intensified as everyone fights for the same pool of recovering demand.

The Cayman strategy evolves significantly. HCCI is currently offering tertiary healthcare services to medical tourists and Caymanians from its existing unit in East End...The estimated total project cost is $100 million (2021 Cayman expansion). Instead of just relying on American medical tourists, HCCI pivots toward serving the broader Caribbean region.

This summer, the grand opening of Health City Camana Bay – the institution's second hospital in Grand Cayman – will feature a neonatal intensive care unit (NICU), an emergency pavilion with a critical care unit, kidney transplant unit, and an extensive multispecialty program incorporating robotic surgery as well as the radiotherapy center. This isn't just expansion—it's deepening the commitment to the Caribbean market.

The strategic acquisitions accelerate. In 2022, the company acquired Sparsha Hospital in Bommasandra. This isn't about building from scratch anymore. It's about finding undervalued assets and applying the NH operational model to transform them.

2023 brings a moment of validation that matters more than any financial metric. Narayana Health set a Guinness World Record for conducting the highest number of ECGs in a single day at a single venue. Not only this, they achieved CAP accreditation for their laboratory services. With this, Narayana Narayana Hrudayalaya became the first hospital in South India and the fourth in India to receive this honour.

The margin improvement strategy shows results. The metro hospitals, initially struggling, begin to find their footing. From 2016 onwards, NH has increased its presence in New Delhi, Gurgaon and Mumbai, by opening premium multi specialty hospitals, in order to boost margins. These aren't abandoning the affordable model—they're creating a sustainable way to fund it.

The financial performance reflects this evolution. Mkt Cap: 35,252 Crore (up 43.2% in 1 year) as of late 2024. The stock price appreciation suggests the market is finally understanding NH's model: it's not about choosing between mission and margins. It's about using margins to fund mission.

The promoter stake tells another story. Promoter Holding: 63.8% and Promoter holding in Narayana Hrudayalaya Ltd has gone up to 63.85 per cent as of Dec 2024. Despite being public for nearly a decade, the founder and family maintain control. This isn't just about wealth—it's about ensuring the mission survives market pressures.

The dividend policy evolves too. The Board has approved final Dividend of Rs. 4.50/- per share for the year ended March 31,2025. For a company built on serving those who couldn't afford healthcare, paying dividends to shareholders seems ironic. But it's necessary—institutional investors need returns, and returns enable access to capital, and capital enables expansion to serve more patients.

The competition landscape has transformed dramatically. Apollo remains the premium leader. Fortis has found stability after years of turmoil. But new players are emerging. Digital health startups promise to disrupt traditional hospitals. Insurance companies are backward-integrating into healthcare delivery. The neat categories of the past are blurring.

NH's response is pragmatic evolution rather than revolution. They partner with digital health platforms rather than competing. They work with insurance companies rather than fighting them. The focus remains on what NH does best: high-volume, high-quality, affordable care.

The international expansion continues, but more carefully. Health City Cayman Islands has bought 500,000 shares for almost CI$4.1 million in Doctors Hospital Health System in the Bahamas. Narayana Health, which owns Health City Cayman Islands, has been looking for further investments in healthcare in the Caribbean. "Currently, we are engaged in discussions with several nations and exploring various opportunities in the region." This is the first investment for Health City Cayman Islands Ltd or Narayana Health, within the Caribbean, outside of the Cayman Islands.

The latest financial results show a maturing business. For the full year, net profit rose 0.11% to Rs 790.16 crore in the year ended March 2025 as against Rs 789.26 crore during the previous year ended March 2024. Sales rose 12.12% to Rs 5482.98 crore in the year ended March 2025 as against Rs 4890.21 crore during the previous year ended March 2024.

The Kammavari Sangham partnership announced recently shows NH isn't abandoning its asset-light expansion model. Kammavari Sangham will set-up hospital infrastructure with capacity of 110 beds in the Bengaluru South region. The project is expected to commence operations in the FY 2026-27. Under the terms of the agreement, Kammavari Sangham shall provide hospital facility to Narayana Hrudayalaya in the Bengaluru South region on a long-term basis. The company would run and operate the said hospital as per the terms of the agreement.

Looking ahead, the investment plans are substantial. "Looking ahead, we have plans to invest Rs 1,000 crore in India and the Cayman Islands"—a billion dollars in expansion, funded by operations and retained earnings rather than new equity.

The fundamental tension remains: how to be both affordable and profitable, both mission-driven and market-responsive. Every decision faces this duality. Open a new hospital in rural Bihar (mission) or metro Mumbai (margins)? Invest in new technology (quality) or reduce costs further (affordability)?

But perhaps this tension is the point. It forces discipline. It prevents mission drift in either direction—neither becoming a charity that can't sustain itself nor a corporation that forgets why it exists. The market provides accountability. The mission provides purpose. The balance, however difficult, might be exactly what enables NH to achieve what neither pure charity nor pure capitalism could: sustainable, scalable, affordable healthcare.

As 2025 unfolds, NH stands at an interesting inflection point. The founder is 72. The company is mature but still growing. The model is proven but constantly challenged. The mission remains clear but its implementation evolves. The next chapter—whether it's about succession, international expansion, or digital transformation—will test whether the NH model can survive and thrive beyond its founder. The answer will determine not just NH's future, but potentially the future of affordable healthcare delivery globally.

IX. The Business Model Decoded (35-45 min)

Let's dissect a heart surgery at NH like it's a manufacturing process—because in many ways, that's exactly what it is.

8:00 AM, NH Bangalore. Operating Room 3 is completing its first surgery. OR 4 is midway through. OR 5 is prepping. Dr. Ashwin moves from OR 3 to OR 4 seamlessly. No downtime. No waiting. By 6 PM, he'll have completed eight procedures. At Apollo down the road, their best surgeon might do two.

The math is elegant in its simplicity. Fixed costs—the OR, equipment, overhead—get divided by eight instead of two. The surgeon's salary, among the highest costs, gets allocated across four times the procedures. Suddenly, that $100,000 American surgery can be done profitably for $1,600.

But the real genius isn't in the division—it's in the multiplication. When you do eight surgeries daily, 2,900 annually, patterns emerge that you'd never see doing two daily. Complications become learning opportunities. Variations become data points. Excellence becomes inevitable through repetition.

By combining innovative technology and a highly efficient delivery system, Narayana Health is able to optimize productivity and minimize costs. Let's decode what "innovative" really means here. It's not about buying the latest robotic surgery system—though NH has those too. It's about innovation in process.

Take procurement. When you're using 10,000 stents annually instead of 100, you don't go through distributors. You call the manufacturer's CEO directly. You negotiate prices that would make American hospital administrators weep. A stent that costs $3,000 in the US, NH buys for $300. Same product, same manufacturer, 10x price difference through volume.

The supply chain innovation goes deeper. NH standardizes everything that can be standardized. Instead of surgeons having preferences for 20 different suture types, there are three. Instead of 50 different implant options, there are five. This isn't compromising choice—it's eliminating meaningless variation that adds cost without value.

The cross-subsidization model is particularly clever. This is accomplished through philanthropy and a cross-subsidy model, in which higher-income patients pay more for nonclinical amenities, such as private recovery rooms. Since the total charges are still far below the cost of comparable services at other private hospitals, Narayana Health is still an attractive option for such consumers. The health system's business model is sustainable because of its ability to attract so many patients who can pay full price.

Here's how it works in practice: A wealthy patient pays ₹2,00,000 for cardiac surgery with a private room. A middle-class patient pays ₹1,00,000 for the same surgery in a shared room. A farmer with Yeshasvini insurance pays ₹5,000. Same surgeon, same OR, same quality. The only difference is the room and amenities. The wealthy patient's payment covers the true cost for all three.

The talent model is revolutionary. Traditional hospitals hire experienced surgeons at massive salaries. NH grows its own. Fresh graduates join NH's residency program where they'll see more surgeries in a month than most residents see in a year. By year three, they're performing routine procedures. By year five, complex ones. The learning curve is compressed through volume.

He and his team have performed over 100,000 major heart surgeries, 30,000 of which were on children. This volume creates a virtuous cycle. More surgeries mean more experience. More experience means better outcomes. Better outcomes mean more patients. More patients mean more surgeries.

The daily P&L monitoring seems obsessive until you understand its purpose. Every department, every day, knows its financial performance. Not monthly or quarterly—daily. A cathlab that's underutilized on Tuesday gets additional marketing focus by Wednesday. An OR with higher infection rates gets immediate intervention. Problems don't fester for months—they're identified and solved in days.

The technology adoption strategy is counterintuitive. While other hospitals chase the latest expensive equipment for marketing purposes, NH asks a different question: Does this technology improve outcomes or reduce costs at scale? If not, they pass. They'll use a five-year-old MRI machine if it does the job. But they'll invest in telemedicine infrastructure that extends their reach to millions.

The quality control mechanisms are fascinating. When you're doing 30 surgeries daily, statistical quality control becomes possible. Control charts, Six Sigma, statistical process control—tools from manufacturing applied to healthcare. A deviation in infection rates that might take months to detect elsewhere gets flagged within days at NH.

The real estate strategy minimizes capital intensity. Why build in expensive metro centers when you can build on the periphery and patients will travel for affordable care? Why own buildings when you can lease floors? Why construct new when you can renovate existing? Every rupee saved on real estate is a rupee available for patient care.

The physician productivity metrics tell the story. An NH cardiac surgeon performs 400+ procedures annually versus 150 at traditional hospitals. But here's the counterintuitive part: NH surgeons don't work longer hours. They work more efficiently. Less time on paperwork, more time operating. Less time waiting, more time doing.

The insurance navigation is sophisticated. NH doesn't just accept insurance—they help create it (Yeshasvini), design products with insurers, and train insurance companies on efficient care delivery. They've turned insurance from a necessary evil into a strategic advantage.

The group performs a remarkable 15% of all heart surgeries done in India, demonstrating its significant scale and expertise. This isn't just market share—it's market-making. NH has fundamentally reset price expectations for cardiac care in India. Competitors have been forced to reduce prices or justify premiums.

The training infrastructure is a competitive moat. NH trains more cardiac surgeons than any institution in India. These surgeons, even if they leave NH, carry the high-volume mindset with them. They become ambassadors for the model, often referring complex cases back to NH.

The outcome data provides the ultimate validation. Incidentally, there have been no deaths or reinterventions from elective coronary bypass surgery at Health City Cayman Islands over the past decade. This isn't luck—it's the result of systemized excellence. When you do something thousands of times, you eliminate variables, reduce errors, achieve consistency.

But here's the most radical part of the model: transparency. NH publishes its outcomes, its prices, its volumes. In an industry built on information asymmetry, NH wins through transparency. Patients know what they'll pay, what outcomes to expect, what quality they'll receive.

The limitations of the model are important to understand. It works best for high-volume, standardized procedures. Cardiac surgery, cataracts, knee replacements—yes. Rare cancers, complex neurosurgery, experimental procedures—less so. NH succeeds by knowing what it's good at and scaling that relentlessly.

The financial engineering is sophisticated but secondary. Yes, NH optimizes working capital, manages debt efficiently, and thinks carefully about capital allocation. But these are enablers, not drivers. The fundamental driver remains operational excellence at scale.

Is it replicable? Partially. Others have copied elements—the high volume, the cross-subsidization, the transparency. But the complete model—the culture, the mission-driven efficiency, the willingness to serve all segments—that's harder to replicate. It requires not just understanding the mechanics but believing in the mission.

The model's elegance lies in its alignment. Doing more surgeries makes NH more profitable AND helps more patients. Reducing costs improves margins AND increases access. Training more surgeons builds competitive advantage AND addresses India's healthcare shortage. There are no trade-offs, only synergies.

This isn't the Walmart of healthcare. Walmart extracts value through supplier pressure and labor minimization. NH creates value through operational excellence and human development. It's closer to Toyota—relentless focus on efficiency in service of quality, not despite it.

The model continues evolving. Digital health, artificial intelligence, robotic surgery—each gets evaluated through the same lens: Does it improve outcomes or reduce costs at scale? If yes, adopt and adapt. If no, wait and watch. The discipline remains even as the tools change.

X. Playbook: Healthcare Innovation Lessons (25-35 min)

The conference room at Harvard Business School, 2018. The case study on Narayana Health has just been discussed by 90 MBA students. The concluding debate is heated: Is NH's model applicable to American healthcare? The class is split. Half see it as the solution to America's healthcare crisis. Half see it as impossibly context-specific to India. Both are right, and both are wrong.

Let's start with a fundamental distinction that most miss: affordable innovation versus frugal innovation. Frugal innovation strips features to reduce cost—think of those $2,500 cars with no air conditioning. Affordable innovation maintains or improves quality while dramatically reducing cost through process innovation. NH doesn't give you less healthcare for less money. It gives you the same or better healthcare through better processes.

Dr. Devi Prasad Shetty, an Indian cardiothoracic surgeon, is known for his efforts in making sure that quality healthcare can be affordable and accessible for every single individual, not only in India but all over the globe. This isn't about Indian innovation or emerging market innovation. It's about systematic rethinking of healthcare delivery anywhere costs have spiraled beyond reason.

Lesson 1: Government Partnership Is Essential But Not Sufficient

The Yeshasvini experience teaches a crucial lesson about public-private partnerships. Government provides reach, credibility, and often funding. But government alone can't innovate on delivery. The Yeshasvini Cooperative Farmers Health Care Trust is the monetary reservoir that manages the effective implementation of the Yeshasvini Scheme. The Yeshasvini Insurance Scheme is headed by the Chief Minister of Karnataka, and the Minister of Cooperation is also closely associated with it.

The key is structured collaboration where each party does what it does best. Government: policy, funding, access to populations. Private sector: operations, innovation, efficiency. When either tries to do both, the model fails. When they collaborate with clear roles, magic happens.

Lesson 2: Charity Doesn't Scale, Social Business Does

Shetty's early realization remains profound: "charity is not scalable." The math is immutable. There isn't enough philanthropic capital in the world to solve healthcare access through charity. But business models that align profit with purpose can scale infinitely.

The NH model proves you can serve the poorest while remaining profitable. Not through charity, but through cross-subsidization, volume economics, and operational excellence. The poor patient isn't receiving charity—they're part of a business model that works because of them, not despite them.

Lesson 3: Trust Is the Ultimate Currency in Emerging Markets

In markets where consumer protection is weak, information asymmetry is high, and quality varies wildly, trust becomes everything. NH built trust through radical transparency—publishing outcomes, standardizing prices, allowing scrutiny.

He then became her personal physician for the last five years of her life. Their relationship grew beyond typical doctor-patient bonds. Mother Teresa often joined him during hospital rounds to watch him work with young patients. The Mother Teresa connection wasn't just prestige—it was trust transfer. If NH was good enough for a saint, it was good enough for anyone.

Lesson 4: Vertical Integration in Healthcare Is About Control, Not Ownership

NH's model seems vertically integrated—they control everything from insurance design to post-operative care. But they don't own everything. They partner, lease, manage, collaborate. The key isn't ownership—it's control over the patient experience and outcome.

This is a crucial lesson for healthcare systems trying to integrate. You don't need to own every piece. You need to control the standards, processes, and outcomes. NH manages hospitals it doesn't own, partners with insurance it doesn't underwrite, uses equipment it leases. But it controls the model.

Lesson 5: Volume Changes Everything

The Western healthcare model is built on scarcity—fewer procedures at higher prices. NH inverts this: more procedures at lower prices. But this isn't just about economics. Volume fundamentally changes quality dynamics.

When you perform 30 heart surgeries daily, statistical quality control becomes possible. Variations become visible. Best practices emerge organically. Learning accelerates. The paradox is that doing more of something can make you better at it while making it cheaper—the opposite of conventional healthcare wisdom.

Lesson 6: Technology Is an Enabler, Not a Solution

NH's relationship with technology is pragmatic, not romantic. They don't adopt technology for its own sake. Every technology decision faces the same test: Does it improve outcomes or reduce costs at scale?

Telemedicine? Yes—it extends reach without infrastructure. Robotic surgery? Sometimes—for specific procedures where precision matters. AI diagnosis? Watching—potential is there but proof is pending. The discipline to resist technology for technology's sake is as important as the wisdom to adopt technology that matters.

Lesson 7: Culture Eats Strategy for Breakfast (Even in Healthcare)

You can copy NH's processes, economics, even facilities. But can you copy the culture of a cardiac surgeon happily moving between operating rooms like a production line worker? Can you copy nurses who see efficiency as compassion, not compromise? Can you copy administrators who view themselves as enablers of care, not controllers of cost?

The cultural transformation required is massive. It requires unlearning decades of healthcare hierarchy, tradition, and assumption. It requires believing that affordable and excellent aren't contradictions but companions.

Lesson 8: The Missing Middle Is the Real Market

Healthcare strategists obsess over the poor (government/charity focus) or the rich (premium hospital focus). NH discovered the massive missing middle—people with some money but not enough for traditional private healthcare. This isn't just an Indian phenomenon. It exists in every country where healthcare costs have outpaced income growth.

Serving this middle requires a different model. Not charity (they can pay something). Not premium (they can't pay everything). But something in between—affordable quality through operational excellence. This market is 10x larger than the premium segment but requires 10x more operational sophistication to serve profitably.

Lesson 9: Success Metrics Must Align with Mission

NH measures success differently. Yes, they track revenue, margins, and profits—they're a public company. But they also track surgeries performed for farmers, free surgeries provided, lives saved regardless of payment ability. What gets measured gets managed. If you only measure financial metrics, you'll only achieve financial outcomes.

The balanced scorecard approach—financial, operational, social—keeps the mission alive while satisfying stakeholders. It's not about choosing between margin and mission. It's about measuring both and managing the balance.

Lesson 10: Scaling Requires Standardization Without Losing Flexibility

The tension between standardization (needed for efficiency) and flexibility (needed for medical complexity) is real. NH's solution is elegant: standardize everything that doesn't affect medical outcomes, remain flexible on everything that does.

Procurement, administration, scheduling, billing—standardized ruthlessly. Surgical technique, clinical decisions, patient care—flexible based on need. This selective standardization enables scale without compromising care.

The Western Application Question

Could the NH model work in developed markets? The Cayman experiment suggests yes, with modifications. The core insights—volume improves quality, operational excellence reduces costs, transparency builds trust—are universal.

But the implementation would differ. Labor costs are higher. Regulations are stricter. Patient expectations are different. The model would need to adapt. But the fundamental principle—that healthcare can be excellent and affordable through operational innovation—remains valid.

American healthcare spends $12,000 per capita annually versus India's $75. Even adjusting for purchasing power and development levels, the gap is absurd. The NH model suggests this isn't inevitable—it's a choice. A choice to prioritize revenue over access, complexity over efficiency, tradition over innovation.

The Broader Implications

NH's success challenges fundamental assumptions about business and society. It suggests that serving the poor can be profitable. That social mission and business success can align. That innovation isn't just about technology but about business models that create value for all stakeholders.