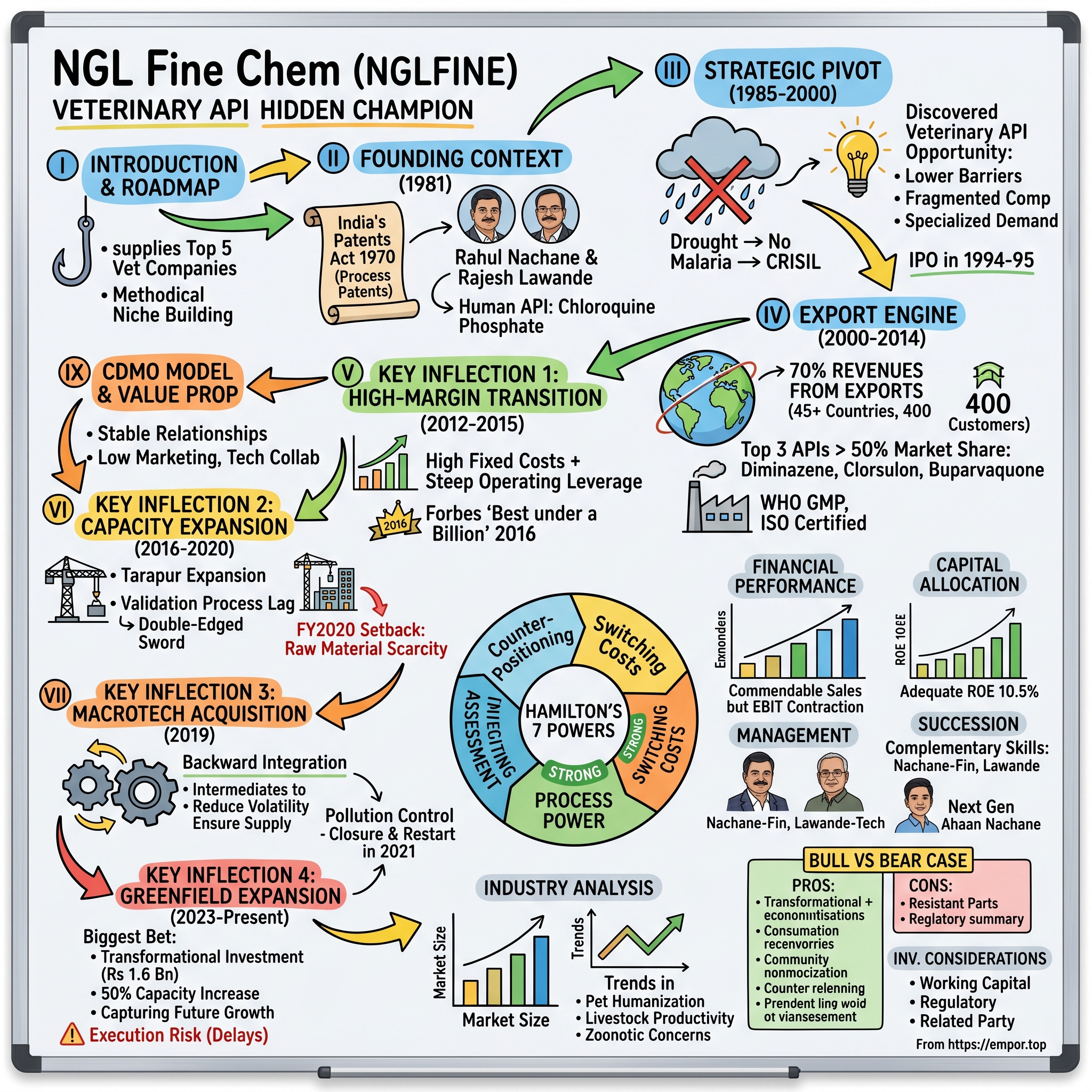

NGL Fine-Chem: The Hidden Champion of Veterinary APIs

I. Introduction & Episode Roadmap

Picture this: A small pharmaceutical company operating out of Navi Mumbai, founded in the twilight of India's License Raj era, now supplies critical veterinary Active Pharmaceutical Ingredients to five of the world's ten largest animal healthcare companies. Its products treat parasitic infections in cattle across African savannahs, protect companion animals in European homes, and ensure livestock health in Latin American farms. Yet most investors have never heard of it.

NGL Fine-chem Ltd is a manufacturer of pharmaceuticals and intermediates for usage in veterinary and human health. The company caters to various global companies to custom manufacture high quality pharmaceuticals with reliability and flexibility.

The hook for this story isn't explosive growth or a charismatic founder disrupting an industry. It's something far more instructive for investors: the methodical construction of a defensible niche in a fragmented market where complexity becomes the moat. NGL Fine Chem positions itself as "The Largest Veterinary API Manufacturer from India with an Extensive Portfolio of 30+ APIs and 25+ Years of Manufacturing experience with 4 State of the Art Manufacturing Facilities."

How does a company with annual revenues of roughly $44 million become indispensable to global pharmaceutical giants with revenues measured in billions? The answer lies in understanding the peculiar economics of veterinary pharmaceutical ingredients—a market where the molecules are complex but the volumes are small, where regulatory barriers create switching costs measured in years, and where being the best at something nobody else wants to do becomes a strategy unto itself.

The core competence of NGL Fine Chem Ltd. is its complex multi step organic synthesis which is used for the construction of generic API's and intermediates. This isn't glamorous work. Antiprotozoals, anthelmintics, ectoparasiticides—these are the unglamorous building blocks of animal health, treating everything from trypanosomiasis in African cattle to intestinal worms in European dogs.

The story spans four decades, from India's early pharma industry through drought-induced pivots, strategic acquisitions, and the current greenfield expansion that represents the biggest bet in company history. For investors interested in specialty chemicals, contract manufacturing, and the art of building sustainable competitive advantages, NGL Fine-Chem offers a masterclass in finding your niche and owning it completely.

II. Founding Context & India's Pharma Landscape

The Birth of an Industry

NGL Fine-Chem Limited was incorporated on December 18, 1981 as a Private Limited Company in the State of Maharashtra. The Company has got its registered office and factory at New Bombay.

To understand NGL Fine-Chem's origin, one must understand India's pharmaceutical landscape in 1981. The Government's Patents Act 1970 established new recommendations and amendments to the 1911 Act. This new Patents Act recognised process patents, but not product patents, which meant that the patenting regime was focused solely on manufacturing. The number of patents granted between 1970-1971 and 1980-1981 fell by three-quarters. This period saw a huge rise in the number of domestic pharma companies.

This was India's golden window for pharmaceutical entrepreneurship. The process patent regime allowed Indian companies to reverse-engineer molecules without paying royalties, creating a generation of firms that would eventually make India the "pharmacy of the world." In the 1980s and 1990s, the country had an indigenous API manufacturing sector supported by public sector units and sensible government policies. At the time, India was self-sufficient in APIs and thus competitive on the global stage.

The Founders' Vision

The company was founded by Rahul Nachane and Rajesh Lawande. Incorporated in 1981, by Mr Narayan Lawande, NGL Fine-Chem Limited sells a variety of items that cater to farm animal, and has successfully made inroads in addressing markets in over 45 countries.

The company started off as a human API company in 1981, with a single manufacturing unit in Navi Mumbai. In 1994, NGL Fine Chem went public, but the following years saw many ups and downs.

The original business strategy was straightforward—manufacture Chloroquine Phosphate, one of the world's most widely used antimalarial drugs. In the early 1980s, malaria remained endemic across much of India, creating consistent demand for this essential medicine. For a young pharmaceutical company, it seemed like a safe bet: a proven molecule, established manufacturing processes, and a large domestic market.

The Antimalarial Foundation

The choice of Chloroquine Phosphate as the company's first product reflected both opportunity and pragmatism. United States government-sponsored clinical trials for antimalarial drug development showed unequivocally that chloroquine has a significant therapeutic value as an antimalarial drug. It was introduced into clinical practice in 1947 for the prophylactic treatment of malaria. By the 1980s, manufacturing processes for this molecule were well-established, making it accessible for Indian pharmaceutical startups.

The company set up manufacturing facilities in what was then New Bombay (now Navi Mumbai), part of Maharashtra's planned satellite city designed to decongest the commercial capital. This location would prove strategically important—close to ports for eventual exports, integrated into Maharashtra's industrial ecosystem, and accessible to the growing pool of pharmaceutical talent in the Mumbai metropolitan region.

For the first few years, the business operated as one might expect: steady production, domestic sales, gradual capacity building. But nature had other plans.

III. The Strategic Pivot: From Human Pharma to Veterinary APIs (1985-2000)

When the Rains Failed

The mid-1980s delivered a lesson that would permanently alter NGL Fine-Chem's trajectory. In 1985-86, severe drought conditions gripped much of India, bringing with them an unexpected consequence for the pharmaceutical industry: the virtual collapse of malaria incidence.

The logic was grimly simple. Malaria spreads through mosquitoes, which breed in standing water. Without monsoons, mosquito populations plummeted, and with them, demand for antimalarial drugs. The company's carefully planned Chloroquine Phosphate business faced an existential crisis not from competition or execution failure, but from an absence of the very disease it was designed to treat.

For a young company with limited capital and a single-product strategy, this was a make-or-break moment. The drought demonstrated with painful clarity the risks of concentration—in product, in therapeutic area, in geographic market. NGL Fine-Chem needed to diversify, but into what?

Discovering the Veterinary Opportunity

The pivot to veterinary APIs emerged from a combination of opportunism and strategic insight. The animal health market offered several advantages that would define NGL Fine-Chem's future:

Lower regulatory barriers: Veterinary pharmaceuticals, particularly in developing markets, faced less stringent regulatory requirements than human drugs. This meant faster approval times, lower compliance costs, and quicker paths to revenue.

Fragmented competition: While human pharmaceutical APIs attracted intense competition from both domestic and international players, veterinary APIs remained relatively uncrowded. The market was simply too small to attract the attention of larger players.

Complex molecules, specialized demand: NGLFCL primarily manufactures veterinary pharmaceutical APIs and intermediates, catering to the antiprotozoal and anthelmintic therapeutic segments. Its products are used in the animal healthcare industry. These therapeutic categories—treatments for parasitic infections in animals—required specialized synthesis capabilities that served as natural barriers to entry.

Export potential: The developing world, particularly Africa and Latin America, had enormous livestock populations requiring exactly the kind of antiparasitic treatments NGL Fine-Chem could manufacture. These markets offered growth potential without the regulatory complexity of developed economies.

Building the Product Portfolio

The company has ~39 APIs (37 Veterinary APIs, 2 Human APIs), ~4 Intermediates, and ~12 finished dosage forms, in the categories of Anthelmintics, Antiprotozoals, Ectoparasiticides, and Phosphorus Supplements.

The product strategy that emerged from this period focused on molecules that shared several characteristics: they required complex multi-stage synthesis, they served markets too small for major pharmaceutical companies to prioritize, and they addressed critical animal health needs in developing economies.

Anthelmintics treat worm infestations—a persistent challenge in livestock across the developing world. Antiprotozoals address parasitic infections like trypanosomiasis (sleeping sickness in cattle), babesiosis, and coccidiosis. Ectoparasiticides target external parasites like ticks and fleas. Each category requires different synthesis capabilities, and together they formed a portfolio that was both defensible and scalable.

Going Public

In 1994-95, NGL Fine-Chem completed its initial public offering, raising capital to fund expansion. The Company carried out refurbishment of the plant and commenced its manufacturing activities in 2000-01. In 2004-05, the Scheme of Amalgamation of Alpha Organics Private Limited and Konarak Textile Industries Private Limited with the Company became effective on 4th March 2005.

The IPO marked a transition from survival-mode entrepreneurship to structured growth. Capital raised would fund capacity expansions, regulatory certifications, and the development of customer relationships that would define the company for decades to come.

The key insight from this period: sometimes the best strategy isn't to fight for share in a crowded market, but to find a market where you can become essential. The drought that nearly destroyed NGL Fine-Chem ultimately created a company with a far more sustainable business model than its original antimalarial focus would have allowed.

IV. The Export Engine & Global Expansion (2000-2014)

Building the Global Footprint

By the turn of the millennium, NGL Fine-Chem had completed its transformation from a domestic antimalarial manufacturer to an export-oriented veterinary API specialist. The company earns about 70% of its revenues from exports.

NGL Fine-Chem Limited manufactures and sells pharmaceuticals and intermediates for usage in veterinary and human health in India, Europe, the Asia Pacific, the United States, and internationally. The company offers animal health pharmaceutical ingredients, such as homidium chloride, nitroxynil, clorsulon, parvaquone, buparvaquone, isometamidium chloride hydrochloride, toldimfos sodium, butaphosphan, imidocarb dipropionate, triclabendazole, rafoxanide, diminazene aceturate, s-methoprene, carprofen, diminazene diaceturate, ractopamine HCI, toltrazuril, decoquinate, amitraz, marbofloxacin, flunixin meglumine, praziquantel, fenbendazole, and xylazine hydrochloride.

This product list reveals the company's strategy: rather than competing head-to-head with large manufacturers on commodity APIs, NGL Fine-Chem focused on specialty molecules where its expertise in multi-stage organic synthesis created genuine differentiation.

The CDMO Model

NGL Fine Chem operates as a CDMO specializing in multi stage organic synthesis of generic APIs and fine chemicals. Their service portfolio includes custom synthesis, process development and manufacturing. They claim to expertise in multi-stage organic synthesis of APIs and fine chemicals. The company is WHO GMP and ISO 9001:2008 certified and has kilo and pilot labs and 3 manufacturing facilities.

The Contract Development and Manufacturing Organization (CDMO) model proved crucial to NGL Fine-Chem's growth. Rather than developing and marketing its own finished products, the company focused on being the best possible supplier to global animal health majors. This approach offered several advantages:

Stable relationships: Once a customer validated an NGL Fine-Chem API for their formulations, switching to another supplier required extensive re-validation—a process that could take months to years.

Lower marketing costs: B2B sales to a handful of major customers required far less investment than building consumer brands.

Technical collaboration: Working closely with global pharmaceutical companies kept NGL Fine-Chem at the forefront of manufacturing processes and quality standards.

Regulatory Certification and Market Access

All existing plants are WHO-GMP, ISO 9001:2000 accredited. These certifications weren't just bureaucratic checkboxes—they were essential for accessing global markets. WHO GMP certification, in particular, opened doors to government procurement programs across developing economies, where tender processes often required WHO-approved manufacturers.

NGL Fine-Chem is a veterinary API manufacturer with its products being used in the animal health industry. The company has a strong and growing international presence in Latin America, Asia and Europe.

Customer Relationships That Span Decades

NGL is now a well-known Company with solid client ties with more than 400 customers in more than 45 countries. The majority of the Company's products are aimed at the Livestock industry, which accounts for around 65% of the global market for animal APIs and intermediates.

The livestock focus proved prescient. While companion animal markets (dogs, cats) were concentrated in developed economies with stringent regulatory requirements, livestock markets in developing regions offered faster growth with more accessible regulatory frameworks. Africa, Latin America, and Asia all had expanding livestock populations requiring exactly the antiparasitic treatments NGL Fine-Chem specialized in manufacturing.

NGL continues to maintain a strong market share of more than 50% for its top three APIs (Diminazene, Clorsulon and Buparvaquone), supported by competitive cost proposition since it is partly backward integrated for basic chemicals.

This market share data is remarkable. In a fragmented global market, maintaining 50%+ share for specific molecules demonstrates exactly the kind of specialization and customer lock-in that creates sustainable competitive advantage. These aren't commodity products where the lowest-cost producer wins; they're complex molecules where reliability, quality consistency, and technical support matter as much as price.

V. Key Inflection Point #1: The High-Margin Product Transition (2012-2015)

The Profitability Breakthrough

The period between 2012 and 2015 marked NGL Fine-Chem's emergence from a competent specialty manufacturer to a genuinely profitable one. The transformation wasn't about volume growth—it was about product mix and capacity utilization.

The credit rating agency, CRISIL, highlighted the entry of NGL Fine Chem Ltd into high-margin products as the reason for the sharp improvement in the profitability in its report in January 2015.

In FY2015, when NGL Fine Chem Ltd reached high capacity utilization for its plants, it reported high-profit margins. The credit rating report in January 2015 by CRISIL noted that NFC's operational performance was supported by diverse product portfolio and customer base.

This is a pattern common to specialty chemical manufacturers: profitability depends not just on what you make, but on how well you utilize your assets. The fixed costs of pharmaceutical manufacturing—regulatory compliance, quality systems, specialized equipment, trained personnel—mean that incremental production generates disproportionate profits once you cross the capacity utilization threshold.

Understanding the Economics

The mechanics of this transition are worth understanding for anyone analyzing specialty manufacturers:

High fixed costs: Pharmaceutical API manufacturing requires substantial investment in facilities, quality systems, and regulatory compliance. These costs are largely fixed regardless of production volume.

Steep operating leverage: Once fixed costs are covered, additional production drops almost entirely to the bottom line (minus raw materials and direct labor).

Product mix matters: Not all APIs generate equal margins. High-margin products typically involve more complex synthesis, greater technical expertise, and stronger competitive positions.

The Forbes Recognition

The company was part of the 'Best under a Billion' list of the top 200 publicly traded companies in the Asia-Pacific region, among 7 other Indian companies in 2016.

The Forbes Asia recognition validated what investors were beginning to notice: NGL Fine-Chem had evolved from a struggling small-cap into a genuinely high-quality business with improving fundamentals. For a company with limited institutional coverage, this kind of third-party validation provided credibility that self-promotion never could.

What This Tells Us About the Business Model

The high-margin transition revealed something fundamental about NGL Fine-Chem's competitive position: its moat wasn't primarily about scale or cost leadership. It was about complexity.

The molecules NGL Fine-Chem manufactures require "complex multi-stage organic synthesis"—processes that can involve 8-12 discrete chemical reactions, each with its own yield optimization, purification requirements, and quality controls. Mastering these processes takes years of accumulated expertise, and that expertise creates barriers that are difficult for new entrants to overcome.

VI. Key Inflection Point #2: Major Capacity Expansion (2016-2020)

The Tarapur Expansion

In the FY2016 annual report, NGL Fine Chem Ltd intimated to its shareholders that it has started work on a capacity expansion plant in Tarapur, which it expects to complete by Q1-FY2018 for ₹25 cr.

The decision to expand capacity at Tarapur represented management's confidence in continued demand growth. An investor would note that during FY2016, the company had started work on a major capacity expansion project at its existing plant in Tarapur. The necessary statutory consents have been received and construction has commenced.

The Validation Process Challenge

The company elaborated to its investors that whenever it comes up with a new manufacturing capacity, then for some time, it has to produce sample products (validation batches), which are sent to the regulators and the customers. Only once the samples are approved by the regulators and the customers, then the commercial production starts. This process takes time ranging from a few months to years.

This validation process is a double-edged sword for pharmaceutical manufacturers. On one hand, it creates significant barriers to entry—new competitors can't simply build a plant and start selling; they must go through the same multi-year validation process. On the other hand, it means that capacity expansions don't generate immediate returns. There's a significant lag between capital investment and revenue generation.

The trial runs of the expansion project started in FY2018.

Project Delays and Cost Overruns

However, the project started witnessing delays both in the terms of time as well as cost. In the next year's annual report (FY2017), the company disclosed that, now, the project would cost ₹30 cr and would be completed in Q3-FY2018 (Oct.-Nov. 2017).

This pattern of delays and cost overruns is worth noting. From the above discussion, an investor would appreciate that NGL Fine Chem Ltd promised to complete the Navi Mumbai plant in Q1-FY2012; however, it could complete it only with a delay of about one year in Q1-FY2013. Therefore, it seems that NGL Fine Chem Ltd can improve its project execution further, which can save the investors time and cost overruns.

The FY2020 Setback

The expansion was barely complete when external factors delivered a sharp reminder of the industry's vulnerabilities. NGL's operating and net margins improved to 31.1% and 22%, respectively, in FY2021 from 14.5% and 5.5%, respectively, in FY2020. This was driven by an improved revenue profile and product mix, operating efficiency, softening in raw material prices and lower operating expenditures.

The FY2020 weakness stemmed from raw material scarcity affecting two high-margin products. This highlighted a persistent vulnerability: NGL Fine-Chem's profitability depends on raw material availability and pricing, factors largely outside management's control.

The operating margins, however, witnessed a sharp contraction to 21.9% in Q2 FY2022 from 31.1% in Q1 FY2022 because of rising raw material prices and inability of the company to fully pass on these costs to customers given the short-term nature of contracts.

This raw material dependency would become an important factor in management's next strategic move.

VII. Key Inflection Point #3: The Macrotech Acquisition (2019)

The Strategic Rationale

NGL Fine-Chem's most recent deal was a Merger/Acquisition with Macrotech Polychem. The deal was made on 15-May-2019.

While analysing NGL Fine Chem Ltd, an investor would notice that until FY2019, the company used to report only standalone financials. However, in May 2019, the company acquired a 100% stake in Macrotech Polychem Private Limited for Rs. 700 Lakhs, which includes the value of equity shares and loan given to Macrotech to repay its existing liabilities.

At Rs. 7 crore (~$900,000), this wasn't a headline-grabbing acquisition. But it represented something strategically important: backward integration into pharmaceutical intermediates.

NGL had acquired a 100% stake in Macrotech Polychem (MPPL) in May 2019. MPPL manufactures pharmaceutical intermediates and serves as the backward integrated unit for the company.

Why Backward Integration Matters

The raw material vulnerability exposed in FY2020 underscored the strategic logic of the Macrotech acquisition. By controlling production of key intermediates, NGL Fine-Chem could:

- Reduce exposure to intermediate supplier pricing volatility

- Ensure more reliable supply of critical inputs

- Potentially improve overall margins by capturing intermediate-stage profits

- Enhance quality control throughout the production chain

With 95% in-house manufacturing and backward integration, it aims to maintain cost competitiveness. This vertical integration strategy enables NGL Fine Chem to exert better control over quality parameters and cost structures.

The Pollution Control Challenge

The acquisition wasn't without complications. On March 6, 2021 NGL Fine-Chem Limited announced that Maharashtra Pollution Control Board (MPCB) has issued a notice directing the closure of operations of its subsidiary: Macrotech Polychem Private Limited (MPPL) in Tarapur for alleged violation of the Water (Prevention and Control of Pollution) Act, 1974.

NGL Fine Chem Ltd had to shut down operations in its Tarapur plants in February 2021 due to certain violations of effluent permissions. This was resolved and the operations restarted in April 2021. This has been a general problem in that area over the past few years.

The pollution control notice was resolved relatively quickly, but it highlighted a risk inherent in chemical manufacturing: regulatory compliance isn't optional, and failures can result in production disruptions that directly impact revenues.

Additionally, NGL Fine Chem has completed an expansion in its subsidiary, Macrotech, which has added new capacities for intermediates.

VIII. Key Inflection Point #4: The Current Greenfield Expansion (2023-Present)

The Biggest Bet in Company History

A greenfield expansion at Tarapur is in progress, with an estimated Rs 1.6 billion investment. This expansion will increase production capacity by 50%, allowing the company to meet rising demand for new products.

At Rs. 160 crore (~$19 million), this expansion represents a transformational investment for a company with current revenues around Rs. 350-380 crore. The thesis is straightforward: global demand for veterinary APIs continues to grow, and NGL Fine-Chem needs capacity to capture that growth.

Pursuant to Reg.30 SEBI (LODR) Regulations 2015, the Company has invested totally around Rs.119.83 Cr till quarter one of F.Y.2025-26 towards the expansion work at our plant S-18 to cater to the future growth.

Civil construction is underway, and Rs 0.8 bn has already been invested in the project.

The Execution Risk

This expansion carries meaningful execution risk. The company's historical project execution, as noted earlier, has shown patterns of delays and cost overruns. A 50% capacity expansion on a timeline of several years creates significant operating leverage—if demand materializes as expected, returns could be substantial. If demand disappoints or costs escalate, the expansion could burden the balance sheet without corresponding revenue growth.

The management remains confident that the ongoing capacity expansions and strategic initiatives will help the company regain growth momentum. However, the near-term performance will depend on demand recovery and stabilizing pricing trends in key markets.

Strategic Positioning

The timing of this expansion is notable. The global veterinary API market continues to grow, driven by secular trends in pet ownership, livestock farming, and animal healthcare spending. By expanding capacity now, NGL Fine-Chem positions itself to capture growth rather than be constrained by capacity limitations.

NGL Fine Chem is also focusing on product diversification to reduce dependence on a few key APIs. The company has a pipeline of new products that it aims to introduce in the coming years.

IX. Current Business Model Deep Dive

Revenue Composition

The company is a manufacturer of pharmaceuticals and intermediates for usage in veterinary and human health. Its product includes Active Pharmaceutical Ingredients (APIs) animal health, APIs human health, Intermediates and Finished dosage form, of which maximum revenue is generated from Veterinary APIs. Its geographical segments include India, Europe, Asia Pacific, United States, and Rest of the world.

The business model reflects decades of strategic refinement:

Product Mix: 37 Veterinary APIs, 2 Human APIs, ~4 Intermediates, ~12 finished dosage forms

Geographic Distribution: 70% exports, concentrated in developing markets

Customer Concentration: Relationships with 5 of top 10 global animal health companies

Manufacturing: 4 facilities (Tarapur and Navi Mumbai), WHO-GMP and ISO certified

The CDMO Value Proposition

Their business is modelled around the changing customer demands and our ability to offer value-added innovative solutions to meet and even exceed these demands. Their commitment to their customers is reflected in terms of their consistent service and support. They work with a four pronged solution approach and offer them the best in terms of: Product Quality, Reliability, Cost Effectiveness, Registration Support.

This value proposition reflects the priorities of global pharmaceutical customers: quality that meets regulatory standards, reliable supply that doesn't disrupt their production schedules, competitive pricing that allows reasonable margins, and technical support that simplifies the regulatory process.

Employee Growth as a Business Proxy

NGL Fine Chem has 371 employees as of Oct 24. The total employee count is 22.4% more than what it was in Oct 23.

A 22% increase in headcount in a single year suggests significant expansion—whether in production capacity, product development, or commercial activities. For a specialty manufacturer where talent and expertise are critical competitive advantages, this hiring pattern indicates confidence in future growth.

The Customer Relationship Challenge

On the sales side, the company continues to have just probably a handful of customers. Most sales are on respond basis—more 3-month sales booking or 4-month sales booking. There are just about 4 or 5 customers who talk about a yearly sales contract.

A notable characteristic of NGL Fine Chem Ltd's business model is the absence of long-term contracts with most of its customers.

This is a critical point for investors: despite strong market positions and switching costs, NGL Fine-Chem operates largely on short-term orders rather than multi-year contracts. This creates revenue volatility and makes forecasting challenging, even if the underlying business relationships are stable.

X. Industry Analysis: The Veterinary API Market

Market Size and Growth

The global veterinary API market, valued at US$8.0 billion in 2022, stood at US$8.5 billion in 2023 and is projected to advance at a resilient CAGR of 6.9% from 2023 to 2028, culminating in a forecasted valuation of US$11.9 billion by the end of the period.

The Global Veterinary Active Pharmaceutical Ingredients (API) Market was valued at USD 7.9 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 16 billion by 2034. This steady growth is largely fueled by increasing pet ownership, rising awareness about animal health, and advancements in veterinary technologies.

Key Growth Drivers

The veterinary active pharmaceutical ingredient (API) market is growing due to various factors, including the increased occurrence of transboundary and zoonotic diseases, a rise in the global animal population and pet ownership, and the implementation of improved disease control and prevention measures. As a result, there is a growing demand for veterinary medicines and animal health products, which is expected to drive the development of the veterinary API industry.

The market benefits from several secular trends:

Pet humanization: Pet owners increasingly view their animals as family members and are willing to spend accordingly on healthcare.

Livestock productivity: Growing global demand for animal protein drives investment in livestock health.

Zoonotic disease concerns: COVID-19 heightened awareness of animal-to-human disease transmission, increasing focus on animal health monitoring.

Regulatory tightening: Higher standards for food safety and animal welfare drive pharmaceutical usage.

The Companion Animal Opportunity

The companion animals segment is projected to grow at a CAGR of 7.6%, reaching USD 10.7 billion by 2034. This growth is attributed to the increasing trend of pet humanization and the willingness of pet owners to invest in preventive and therapeutic healthcare.

While NGL Fine-Chem has historically focused on livestock markets, the companion animal segment offers higher growth rates and potentially better margins. The question for the company is whether it can develop products and relationships that capture this growth.

Chemical APIs Remain Dominant

Chemical-based APIs held the largest share of 58.2% in 2024 due to their cost-efficiency, long shelf life, and ease of mass production. These APIs are widely used in treating a range of conditions like infections and inflammation and serve as the foundational building blocks for many veterinary drugs. Their pharmacological properties make them suitable for combination with other ingredients, enhancing their therapeutic efficacy. Continuous improvements in chemical synthesis technologies are also supporting the increased adoption of these APIs across various veterinary applications.

This is reassuring for NGL Fine-Chem, which specializes in chemical synthesis rather than biologics. While biologics represent a growing segment, chemical APIs remain the foundation of veterinary pharmaceuticals and are likely to maintain their dominance for the foreseeable future.

XI. Competitive Landscape & Porter's Five Forces

The Competitive Arena

The prominent players in the global Veterinary API Market are Phibro Animal Health Corporation (US), Fabbrica Italiana Sintetici S.p.A. (Italy), Sequent Scientific Ltd. (India), Excel Industries Ltd. (India), NGL Fine-Chem Ltd. (India), Insulnsud Pharma (Spain), Menadiona Sl (Spain), Rochem International Inc. (US), and Shaanxi Hanjiang Pharmaceutical Group Co. Ltd. (China).

NGL Fine-Chem operates in a market with several categories of competitors:

Global pharmaceutical majors' internal production: Companies like Zoetis, Boehringer Ingelheim, and Elanco maintain some in-house API production

Dedicated veterinary API specialists: Sequent Scientific (India), Excel Industries (India), Fabbrica Italiana Sintetici (Italy)

Chinese manufacturers: Increasingly competitive on price but facing quality and supply reliability concerns

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

The barriers to entry are substantial: - Complex multi-stage organic synthesis expertise requires years to develop - Regulatory approvals (WHO GMP, customer validation) take months to years - Capital intensity: Rs. 160 Cr (~$19M) for 50% capacity expansion - Relationship stickiness with established customers creates natural barriers

However, the barriers aren't insurmountable for well-capitalized competitors, particularly those with existing pharmaceutical expertise.

2. Bargaining Power of Suppliers: MEDIUM-HIGH

The ratings also consider the vulnerability of the company's profitability to volatility in raw material prices and forex movement. Given the nature of short-term contracts, the company's operating profitability remains exposed to the adverse movements in the raw materials prices that cannot be passed onto the customers.

Raw material prices depend significantly on crude oil prices, creating exposure to commodity volatility. The Macrotech acquisition was partly designed to address this vulnerability through backward integration.

3. Bargaining Power of Buyers: MEDIUM

On one hand, switching costs are high (re-validation required) and qualification timelines create stickiness. On the other hand, large customers have significant negotiating leverage, and the short-term contract structure limits pricing power.

NGL Fine Chem Ltd mentioned to the investors that the competition is so severe that even for the products where it has more than 50% market share, it is not able to dictate prices to the customers. The competitors are always ready to cut prices and take market share away from it.

4. Threat of Substitutes: LOW

APIs are essential active ingredients with no direct substitutes. While biologics are emerging, chemical APIs remain dominant at 58% market share and will continue to be essential for most veterinary treatments.

5. Industry Rivalry: MEDIUM-HIGH

The company faces strong competition, which often leads to price cutting among players, limiting its pricing power.

The market is consolidated but competitive. Niche focus provides some insulation, but competitors are capable of entering specific product categories.

XII. Hamilton's 7 Powers Analysis

1. Scale Economies: MODERATE

In FY2015, when NGL Fine Chem Ltd reached high capacity utilization for its plants, it reported high-profit margins.

Scale benefits primarily flow through capacity utilization rather than pure volume. The company remains relatively small (~$44M revenue) compared to global pharmaceutical players.

2. Network Effects: WEAK

B2B API manufacturing doesn't generate direct network effects. There are no winner-take-all dynamics or network-based competitive advantages.

3. Counter-Positioning: STRONG

This is perhaps NGL Fine-Chem's most powerful source of competitive advantage. The company focuses on niche veterinary APIs while larger pharmaceutical players prioritize human drugs. The complexity of these products creates a natural moat—the molecules are too specialized for commodity manufacturers and too small for major pharmaceutical companies to prioritize.

The growth is happening in these markets now because the European and US markets are more or less maturing. So, our focus is completely the rest of the world, not the regulated markets.

4. Switching Costs: STRONG

Whenever the company comes up with a new manufacturing capacity, for some time, it has to produce sample products (validation batches), which are sent to the regulators and the customers. Only once the samples are approved by the regulators and the customers, then the commercial production starts. This process takes time ranging from a few months to years.

The validation process creates substantial switching costs. Customers can't simply substitute one API supplier for another—they must go through an extensive re-validation process that can take years.

5. Branding: MODERATE

The company was part of the 'Best under a Billion' list of the top 200 publicly traded companies in the Asia-Pacific region, among 7 other Indian companies in 2016.

NGL Fine-Chem has built reputation for quality and reliability with global pharma majors. However, as a B2B supplier, brand power is limited compared to consumer-facing businesses.

6. Cornered Resource: MODERATE

The company possesses multi-decade expertise in specific compound classes and proprietary processes for complex molecules. Key management continuity provides institutional knowledge. However, these resources aren't truly "cornered"—competitors could theoretically develop similar capabilities over time.

7. Process Power: STRONG

The core competence of NGL Fine Chem Ltd. is its complex multi step organic synthesis which is used for the construction of generic API's and intermediates. Their team comprises industry professionals who are consistently developing innovative technologies. They have well equipped research lab, versatile pilot plant employed with modern analytical solutions and a kilo lab facility. They emphasize on process development and have strong connections with academia.

Process Power is the foundation of NGL Fine-Chem's competitive position. The institutional knowledge in handling complex molecules, continuous improvement in manufacturing processes, and decades of accumulated expertise create genuine differentiation.

Overall Assessment

NGL Fine-Chem's moat is built primarily on Process Power, Switching Costs, and Counter-Positioning—a classic specialty chemicals playbook. The business doesn't have the explosive growth potential of a company with network effects, but it has the stability and defensibility that comes from being genuinely good at something complex and essential.

XIII. Financial Performance & Recent Challenges

Historical Performance

Annual revenue of NGL Fine Chem is $42.6M as on Mar 31, 2024.

For the full financial year 2024-25, net profit declined by 48.89% to ₹21.12 crore, as compared to ₹41.32 crore in the previous year (FY24). However, sales rose by 8.73% to ₹368.26 crore in FY25, up from ₹338.69 crore in FY24.

This divergence between revenue growth and profit decline reveals the margin pressure currently facing the business.

Recent Headwinds

NGL Fine Chem reported a weak financial performance for the December 2024 quarter, leading to a sharp fall in its share price. Rising expenses and lower revenue have impacted profitability, raising investor concerns. The company's net profit for the quarter stood at 12.8 million, a significant decline from Rs 100.3 m reported in the same period last year. This steep drop in profit is mainly due to higher costs and lower revenue growth. Increased raw material prices and operational expenses have reduced margins.

Total revenue for the quarter was Rs 890 m, a sharp decline from Rs 916.3 m in the previous year. The decline in revenue suggests weaker demand or pricing pressure in key markets. A slowdown in export sales and competitive pricing in the domestic market have contributed to this drop.

The Cyclical Nature

The most perplexing aspect of NGL Fine-Chem's current performance is the disconnect between revenue growth and profitability. Over the past five years, the company has delivered commendable sales growth of 17.35% CAGR, yet EBIT growth has contracted at 5.13% CAGR over the same period. This divergence suggests persistent margin pressure, rising operating expenses, or a shift towards lower-margin product segments.

This disconnect between top-line and bottom-line growth is the central challenge facing NGL Fine-Chem today. The expansion investments are consuming capital without yet generating proportional returns, and competitive pressures are limiting the ability to pass through cost increases.

Capital Allocation

Company has a low return on equity of 10.5% over last 3 years.

A 10.5% ROE is adequate but not exceptional. It reflects the capital-intensive nature of pharmaceutical manufacturing and the recent investments in capacity expansion that haven't yet generated full returns.

Promoter Stability

Promoter holding in NGL Fine Chem Ltd has gone up to 72.74 per cent as of Sep 2025 from 72.74 per cent as of Dec 2024.

High promoter holding (72.74%) signals alignment of interests and provides stability. The family's significant ownership stake means their wealth is tied to the company's long-term success.

XIV. Management & Governance

The Leadership Team

With 36 years of expertise in the pharmaceutical sector, Mr Nachane brings a wealth of knowledge and experience to the table. As a Chartered Accountant and Master of Management Studies, he has a strong foundation in finance and business management. Since 1992, he has been serving as a full-time Director of the Company, actively involved in operations since 1989. In his role, he held the responsibility for NGL's marketing, production and general management.

Rahul Nachane's background combines financial expertise (CA) with business management training (MMS) and deep operational experience. This combination is valuable in a business where cost control, customer relationships, and operational excellence all matter.

Mr. Rajesh Lawande brings with him 22 years of valuable experience in the pharmaceutical sector. With an M.Sc. in Chemistry from IIT Bombay and a PGDM in Management from IIM Lucknow, he possesses a strong educational background that complements his practical expertise.

The combination of Nachane's financial/commercial expertise and Lawande's technical/scientific background creates a leadership team with complementary skills—one focused on customers, finance, and strategy, the other on chemistry, process development, and manufacturing.

Succession Planning

In June 2021, Mr Ahaan Nachane, son of Mr Rahul Nachane has joined the company as a vice president. The presence of younger family members at executive positions within the group, while the senior members are still handling responsibilities, looks like a good succession plan. This is because the young members can learn about the fine nuances of the business under the guidance of senior members until the seniors decide to take retirement.

The introduction of the next generation provides visibility into succession planning. For a founder-led business, this reduces key-man risk and suggests institutional continuity.

Governance Considerations

Directors of NGL Fine-chem are RAJESH NARAYAN LAWANDE, PALLAVI SATISH PEDNEKAR, DHANANJAY NARENDRA MUNGALE, JAYARAM SITARAM, RAHUL JAYANT NACHANE, AJITA RAHUL NACHANE and SARALA MENON.

The board includes both family members and independent directors, providing a mix of ownership perspective and external oversight. The presence of independent directors is important for corporate governance, though the high promoter holding (72.74%) means controlling shareholders have significant influence over company decisions.

XV. Bull vs. Bear Case

The Bull Case

Structural Tailwinds in Animal Health

The Global Veterinary API Market is estimated to grow at a CAGR of 7.4% to reach USD 16 billion by 2034. This steady growth is largely fueled by increasing pet ownership, rising awareness about animal health, and advancements in veterinary technologies. Consumers are becoming more inclined to treat animals with the same level of healthcare they expect for themselves. The growing prevalence of zoonotic diseases has also intensified the urgency for reliable treatments.

Capacity Expansion Positions for Growth

A greenfield expansion at Tarapur is in progress, with an estimated Rs 1.6 billion investment. This expansion will increase production capacity by 50%, allowing the company to meet rising demand for new products.

The management remains confident that the ongoing capacity expansions and strategic initiatives will help the company regain growth momentum.

Strong Competitive Position

NGL continues to maintain a strong market share of more than 50% for its top three APIs (Diminazene, Clorsulon and Buparvaquone), supported by competitive cost proposition since it is partly backward integrated for basic chemicals.

High Switching Costs

The validation process creates customer stickiness measured in years. Once qualified, suppliers aren't easily displaced.

Aligned Ownership

72.74% promoter holding ensures management has skin in the game.

The Bear Case

Margin Pressure

NGL Fine-Chem's inability to maintain historical PAT margins above 12% (achieved in FY21 with 21.8% margins) despite higher revenues suggests either commoditisation of its product portfolio or intensifying competition.

Lack of Long-Term Contracts

A notable characteristic of NGL Fine Chem Ltd's business model is the absence of long-term contracts with most of its customers.

Customer Concentration Risk

Dependence on a handful of major customers creates vulnerability if any key relationship changes.

Raw Material Volatility

The company's profitability remains exposed to adverse movements in raw materials prices that cannot be passed onto customers given the short-term nature of contracts.

Execution Risk on Expansion

The Rs. 160 Cr expansion represents significant execution risk. The company's historical project execution has shown patterns of delays and cost overruns.

Regulatory Headwinds

The stringent regulatory approval process restrains the growth of this market.

XVI. Key Performance Indicators for Investors

For investors tracking NGL Fine-Chem, three KPIs deserve particular attention:

1. Capacity Utilization Rate

This single metric encapsulates both demand health and operational efficiency. When capacity utilization is high (80%+), operating leverage drives margins higher. When it's low, fixed costs weigh on profitability. Given the current expansion, tracking capacity utilization will reveal whether new capacity is finding productive use or creating excess burden.

2. EBITDA Margin Trend

EBITDA margins reveal the underlying profitability of operations before financing and accounting effects. The historical volatility (ranging from mid-teens to 30%+) makes tracking the trend essential. Sustained margin improvement would validate the expansion thesis; continued compression would signal structural challenges.

3. Export Revenue Growth

With 70% of revenues from exports, the health of international markets directly determines company performance. Export revenue growth captures both volume trends and pricing dynamics in NGL Fine-Chem's core markets.

XVII. Playbook: Business & Investing Lessons

1. The Power of Strategic Pivots

NGL Fine-Chem's transformation from failed antimalarial manufacturer to veterinary API leader demonstrates that early setbacks can force strategic clarity. The drought that destroyed the original business model ultimately created a more defensible one.

2. Finding the Niche Within the Niche

Antiprotozoals and anthelmintics aren't glamorous, but they're defensible. The company chose to be excellent at something too small for major pharmaceutical companies to prioritize and too complex for commodity manufacturers to replicate.

3. Complexity as a Moat

Multi-stage organic synthesis creates barriers that scale doesn't. The institutional knowledge accumulated over decades can't be purchased or replicated quickly.

4. Customer Intimacy in B2B

Decades-long relationships with global pharmaceutical majors create stability that transactional businesses lack. The validation process transforms suppliers into partners.

5. Patience with Capacity Investments

The 2-3 year validation cycles require long-term thinking. Investors expecting immediate returns from capacity expansion will be disappointed; those with patience may be rewarded.

6. Vertical Integration at the Right Time

The Macrotech acquisition addressed a genuine strategic vulnerability (raw material dependence) at a reasonable price. It exemplifies focused vertical integration rather than empire-building.

7. Promoter Alignment Matters

72%+ promoter holding ensures that management wealth is tied to company success. This alignment reduces agency problems common in professionally-managed companies.

XVIII. Investment Considerations

What to Watch

Near-Term: Quarterly revenue and margin trends; progress on Tarapur expansion; raw material cost dynamics

Medium-Term: Capacity utilization post-expansion; new product launches; customer concentration trends

Long-Term: Competitive positioning as market evolves; succession execution; strategic response to industry consolidation

Material Regulatory & Accounting Considerations

Pollution Control: The company has faced regulatory notices regarding effluent treatment. Environmental compliance remains an ongoing operational requirement.

Related Party Transactions: The office space rented by the company belongs to the promoters. There are also several transactions with Nupur Remedies Pvt. Ltd for consultancy services. These transactions warrant monitoring to ensure arm's-length pricing.

Working Capital Intensity: The ratings remain constrained by NGL's moderate scale of operations and high working capital intensity of business emanating from receivables and elevated inventory holding cycle. High working capital requirements limit free cash flow generation.

NGL Fine-Chem represents a classic specialty manufacturing story: a company that found its niche through necessity, built expertise through persistence, and created competitive advantages through complexity. The current expansion represents management's conviction that the market opportunity justifies significant capital investment.

For investors, the question isn't whether NGL Fine-Chem is a good company—its market positions, customer relationships, and technical capabilities are genuinely strong. The question is whether current valuations appropriately reflect both the growth opportunity and the execution risks inherent in a significant capacity expansion during a period of margin pressure.

The company has earned its position among India's leading veterinary API manufacturers through four decades of focused execution. Whether the next decade delivers comparable returns depends on successful expansion execution, margin recovery, and continued market growth in an industry where being essential to global pharmaceutical giants creates enduring value.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube