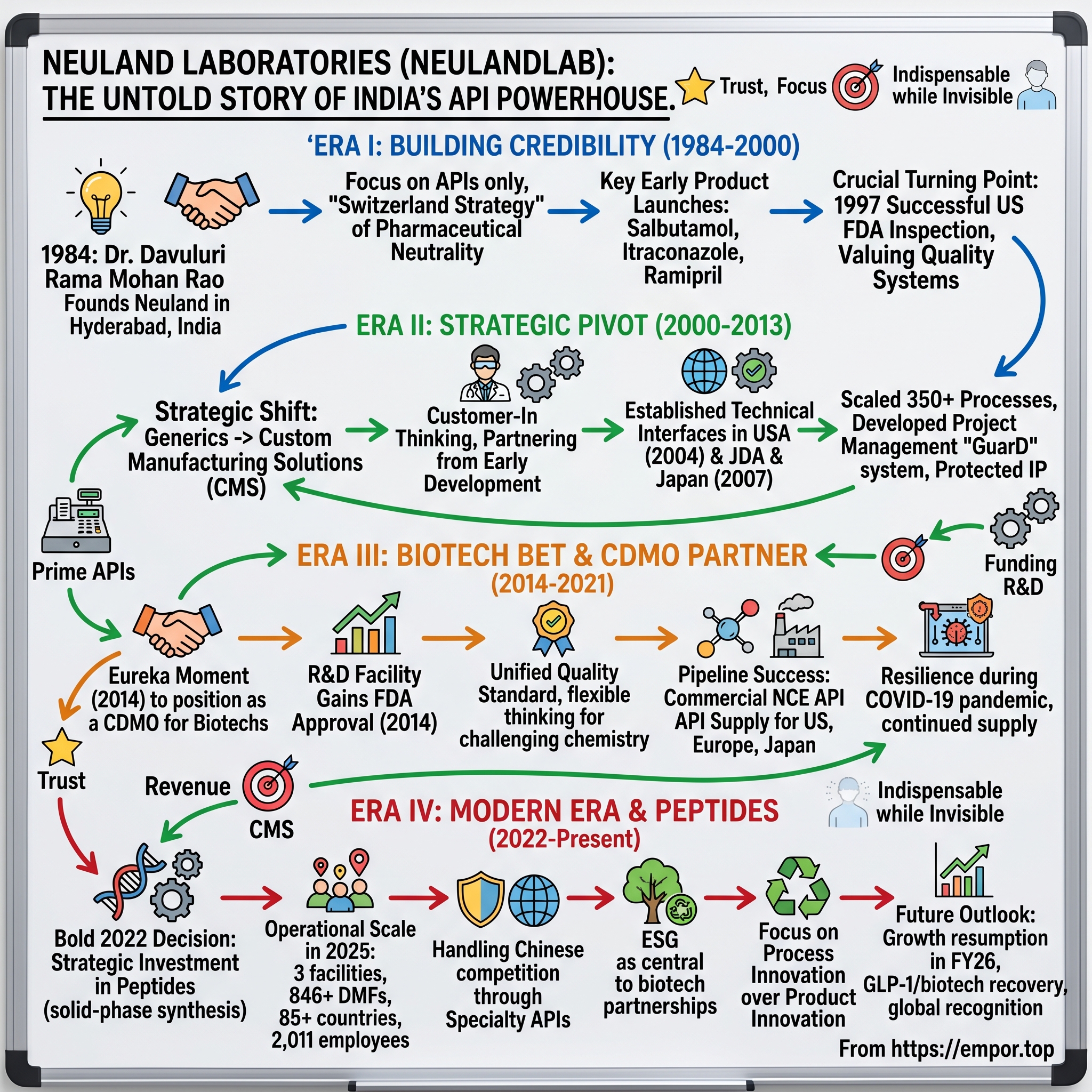

Neuland Laboratories: The Untold Story of India's API Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 1997, and a small pharmaceutical company from Hyderabad is about to face its moment of truth. The FDA inspectors have arrived at Neuland Laboratories' facility—a make-or-break audit that would determine whether this 13-year-old Indian company could play in the global pharmaceutical big leagues. For founder Dr. Davuluri Rama Mohan Rao, watching from his office as inspectors combed through every process, every document, every corner of his manufacturing plant, this wasn't just about regulatory compliance. It was validation of a radical bet: that an Indian company could build world-class pharmaceutical capabilities from scratch.

Today, Neuland Laboratories stands as a ₹16,055 crore market cap company, generating ₹1,330 crore in revenue, supplying critical drug ingredients to over 85 countries. But here's what makes this story fascinating—while Indian pharma giants like Sun Pharma and Dr. Reddy's built empires by selling finished drugs, Neuland deliberately chose to remain invisible to consumers. They would be the arms dealer, not the soldier. The ingredient supplier, never the brand owner.

The question that drives this deep dive: How did a company founded in 1984, in pre-liberalization India, transform from a small-scale chemical manufacturer into a trusted partner for global biotech companies developing cutting-edge therapies? It's a story of strategic restraint—knowing what battles not to fight—as much as ambition.

This journey unfolds across four distinct eras: the foundational years building credibility in regulated markets (1984-2000), the strategic pivot from commoditized generics to custom manufacturing (2000-2013), the bold biotech bet that transformed the company (2014-2021), and the current phase of peptide investments and global scaling (2022-present). Each transition required not just operational excellence but a fundamental reimagining of what an Indian pharmaceutical company could be.

Three themes emerge repeatedly: First, the power of focus—Neuland's unwavering commitment to APIs only, even when vertical integration tempted. Second, trust as currency—in pharmaceutical manufacturing, one quality failure can destroy decades of reputation. Third, the art of being indispensable while invisible—creating value without threatening customers.

As we'll see, Neuland's story isn't just about pharmaceutical manufacturing. It's about navigating the treacherous waters between commoditization and specialization, between growth and discipline, between local roots and global ambitions. Let's begin where all great business stories start—with a vision that seemed impossible at the time.

II. The Founding Story & Dr. Rao's Vision

The origin story of Neuland Laboratories begins not in a boardroom or laboratory, but in the halls of Notre Dame University in the 1970s. Dr. Davuluri Rama Mohan Rao, a young chemistry PhD student from India, discovered something that would shape his entire career—not in his own research, but in the legacy of Reverend Julius Nieuwland, a Holy Cross priest who had invented synthetic rubber (neoprene) at Notre Dame decades earlier. The revelation was profound: breakthrough chemistry could emerge from unexpected places, and more importantly, India didn't need to remain merely a consumer of pharmaceutical innovation.

Dr. Rao returned to India armed with his doctorate and a decade of experience at Glaxo India, where he'd risen through senior positions, witnessing firsthand how multinational pharmaceutical companies operated. By 1984, at age 43, he faced a choice that would define not just his career but an entire industry segment: continue climbing the corporate ladder at a prestigious MNC, or venture into the uncertain world of Indian pharmaceutical manufacturing.

The India of 1984 was vastly different from today's economic powerhouse. The country operated under the License Raj, foreign exchange was scarce, and the pharmaceutical industry was dominated by multinationals who imported most active ingredients. Indian companies that did exist focused primarily on reverse-engineering and formulations. The idea of an Indian company competing globally in pharmaceutical ingredients seemed audacious, if not delusional.

But Dr. Rao saw an opening others missed. The global pharmaceutical industry was undergoing a fundamental shift—drug companies were beginning to outsource non-core activities to focus on drug discovery and marketing. Meanwhile, India's process chemistry capabilities, honed through years of reverse-engineering under patent-light regimes, had created a pool of talented chemists who could develop cost-effective manufacturing processes. The convergence was perfect, if someone could bridge the quality gap.

In 1984, with modest capital and enormous ambition, Dr. Rao founded Neuland Laboratories in Hyderabad. The city wasn't yet "Cyberabad"—it was still finding its identity beyond being a historical capital. But it offered something crucial: proximity to chemical manufacturing hubs, access to skilled chemists from local universities, and state government support for pharmaceutical ventures.

The company's first breakthrough came in 1986—just two years after founding—with the successful commercialization of salbutamol sulphate and albuterol sulphate, respiratory drugs used in asthma treatment. These weren't random choices. Dr. Rao had identified APIs where Indian companies could compete on cost while meeting international quality standards. The respiratory segment was growing globally, patents were expiring, and most importantly, the chemistry was complex enough to create barriers to entry but not so complex as to be beyond Neuland's capabilities.

The strategic decision that would define Neuland's next four decades was made early: the company would focus exclusively on APIs—the active pharmaceutical ingredients that actually cure diseases—rather than formulations that patients consume. This wasn't the obvious choice. Formulations offered higher margins, direct brand building opportunities, and were what most Indian pharmaceutical companies pursued. Dr. Rao's logic was counterintuitive but brilliant: by staying in APIs, Neuland would never compete with its customers. It could sell to everyone—Indian formulators, global generics companies, even innovator pharmaceutical companies—without conflict.

This "Switzerland strategy" of pharmaceutical neutrality required immense discipline. When opportunities arose to forward-integrate into finished dosages—and they arose frequently—Neuland declined. When customers suggested joint ventures for formulation plants, Neuland politely refused. The company would be the arms dealer, never the soldier.

By 1994, after a decade of operations, Neuland took another bold step—going public. This wasn't just about raising capital; it was about institutionalizing the company, creating governance structures that would outlast its founder. The IPO prospectus revealed a company with ambitious plans: multiple manufacturing sites, R&D facilities, and most crucially, the intention to seek US FDA approval.

The cultural DNA Dr. Rao embedded was distinctive. While competitors often took shortcuts—using inferior raw materials when customers wouldn't notice, or maintaining different quality standards for regulated vs. unregulated markets—Neuland adopted a "one quality standard" philosophy. Every batch, whether destined for Africa or America, would meet the highest specifications. This seemed economically irrational in the short term but would prove prescient.

Dr. Rao's vision extended beyond business metrics. He saw Neuland as proving a larger point: that Indian companies could be trusted partners in the global pharmaceutical supply chain, not just low-cost alternatives. This required changing perceptions, one audit at a time, one customer at a time, one successful delivery at a time. The real product wasn't just APIs—it was trust, wrapped in white crystalline powder.

III. The Early Years: Building Credibility (1984–2000)

The transformation of Neuland from a local API manufacturer to a globally recognized supplier didn't happen overnight—it was a 16-year grind through the unglamorous work of building systems, surviving price wars, and most critically, earning regulatory approvals that would serve as the company's passport to global markets.

The 1994 IPO had provided capital, but money alone couldn't buy what Neuland needed most: credibility in regulated markets. The global pharmaceutical industry operated on a simple but brutal principle—one contaminated batch, one failed inspection, one documentation error could destroy years of relationship building. For an Indian company in the 1990s, the skepticism was even higher. Global buyers questioned whether Indian manufacturers could maintain consistent quality when labor was cheap and regulatory oversight was perceived as lax.

The pivotal moment arrived in 1997. After three years of preparation—installing equipment that exceeded requirements, training operators in documentation practices that seemed excessive for the Indian market, and conducting multiple mock audits—Neuland invited the US FDA for its first inspection. For context, in 1997, fewer than a dozen Indian pharmaceutical facilities had FDA approval. This wasn't just a regulatory checkbox; it was a credibility transformation.

The FDA inspection was theater of the highest stakes. Inspectors examined everything: raw material sourcing, analytical methods, batch records, deviation investigations, even the training records of individual operators. They interviewed employees randomly, checked for data integrity, looked for signs of hidden practices. For Dr. Rao and his team, watching inspectors spend days combing through their facility, the tension was palpable. One significant observation could delay approval by years.

When the approval letter arrived—no critical observations, full compliance—it wasn't just Neuland that won. It validated the broader thesis that Indian companies could meet global standards. The approval immediately changed customer conversations. Procurement teams that wouldn't return calls suddenly wanted meetings. Pricing discussions shifted from pure cost comparisons to value propositions. The FDA approval was, in essence, a membership card to the global pharmaceutical supply chain club.

But credibility without products meant nothing. Between 1992 and 2000, Neuland systematically expanded its portfolio, choosing molecules with specific strategic intent. Itraconazole, an antifungal with complex stereochemistry, demonstrated technical capabilities. Ipratropium Bromide, another respiratory drug, leveraged existing customer relationships from the salbutamol success. Mirtazapine, an antidepressant, opened doors to CNS-focused companies. Ramipril, a cardiovascular drug, entered Neuland into one of the largest therapeutic segments globally.

Each product launch was a calculated bet. Developing an API required 18-24 months of process development, stability studies, and validation batches before generating any revenue. The investment could reach millions of dollars with no guarantee of returns—if a competitor developed a superior process or if demand shifted, the entire investment could be worthless.

The competitive landscape was brutal. Chinese manufacturers, backed by provincial governments and operating with lower environmental standards, could offer prices 30-40% below Indian levels. Neuland faced a choice: match Chinese prices and destroy margins, or find a different basis for competition. The company chose the latter, competing on reliability rather than just price. When Chinese suppliers faced plant shutdowns due to environmental violations, when their documentation didn't meet audit standards, when their delivery timelines slipped—Neuland was there as the reliable alternative.

Quality systems became Neuland's religion. While competitors might maintain different standards for different markets—premium quality for the US and Europe, acceptable quality for semi-regulated markets, and basic quality for unregulated markets—Neuland maintained uniform standards. This "one plant, one quality" philosophy seemed economically irrational. Why spend extra on quality for markets that didn't demand it? The answer became clear during customer audits. When inspectors could randomly sample any batch and find identical standards, trust deepened exponentially.

The organization Dr. Rao built reflected this obsession with systems. Unlike the hierarchical, family-dominated structures common in Indian companies, Neuland created process-driven operations. Standard operating procedures (SOPs) governed everything. Deviations were investigated with forensic intensity. Quality assurance had veto power over commercial decisions. These weren't just paper exercises—they were cultural embedding of the idea that in pharmaceutical manufacturing, consistency trumps everything.

By 2000, Neuland had filed over 20 Drug Master Files (DMFs) with various regulatory agencies. Each DMF represented not just a product but a complete manufacturing and quality dossier that regulatory agencies could reference. It was intellectual property of a different sort—not patents, but proven processes that customers could rely upon. The DMF portfolio became Neuland's library of trust, each filing a testament to the company's capabilities.

The financial performance during this period was steady rather than spectacular. Revenues grew from ₹10 crore in 1990 to approximately ₹100 crore by 2000—a respectable but not explosive trajectory. Margins were compressed by Chinese competition and the heavy investments in quality systems. But Dr. Rao wasn't optimizing for short-term financial metrics. He was building institutional capabilities that would compound over decades.

The human capital story was equally important. Neuland became a training ground for quality and regulatory professionals. The company hired fresh chemistry graduates and trained them not just in synthesis but in documentation, not just in production but in compliance. Many would leave for higher-paying opportunities at MNCs, but this diaspora became ambassadors for Neuland's capabilities. When they moved to customer companies, they remembered Neuland's reliability.

As the millennium turned, Neuland stood at an inflection point. It had proven that an Indian company could meet global quality standards. It had survived Chinese price competition. It had built a portfolio of products and customers. But the generic API business was becoming increasingly commoditized. Margins were shrinking, competition was intensifying, and differentiation was disappearing. The company needed a new strategy, one that leveraged its hard-won credibility while escaping the commodity trap. The answer would come from an unexpected source: the emerging biotech industry's need for specialized manufacturing partners.

IV. The Strategic Pivot: From Generic APIs to Custom Manufacturing (2000–2013)

The dot-com bubble had just burst when Neuland's leadership gathered for a strategic planning session in 2000. The generic API business that had sustained the company's first 16 years was becoming a race to the bottom. Chinese manufacturers were adding capacity at unprecedented rates, Indian competitors were multiplying, and customers were treating APIs as commodities—switching suppliers for 5% price differences. Dr. Rao posed a question that would reshape the company: "What if we stop trying to sell what we can make, and start making what customers need?"

This shift from product-out to customer-in thinking was radical for an Indian API manufacturer. The traditional model was straightforward: identify off-patent molecules, develop cost-effective processes, and compete on price. The new model Neuland envisioned was fundamentally different: partner with pharmaceutical companies from the early development stage, customize processes for their specific needs, and become embedded in their supply chain before the drug even reached the market.

The timing was fortuitous. The pharmaceutical industry was undergoing its own transformation. Big Pharma companies, facing patent cliffs and R&D productivity challenges, were outsourcing more activities. Small biotech companies, funded by venture capital post-Human Genome Project, needed manufacturing partners who could scale their discoveries. The Contract Research and Manufacturing Services (CRAMS) industry was nascent but growing rapidly.

In 2004, Neuland established its US operations—not a sales office, but a technical interface. The team, led by pharma industry veterans, could speak the language of American biotech companies, understand FDA requirements intimately, and most importantly, provide project management in customers' time zones. This wasn't just about convenience; it was about becoming part of the customer's extended team rather than remaining a distant supplier.

The Japan subsidiary, established in 2007, followed similar logic but with a twist. Japanese pharmaceutical companies valued long-term relationships over transactional efficiency. They wanted suppliers who understood concepts like 'omotenashi' (hospitality) and 'kaizen' (continuous improvement). Neuland's Japanese office, staffed with bilingual technical experts, became a bridge between Indian cost-efficiency and Japanese quality obsession.

The technical capabilities required for custom manufacturing were dramatically different from generic APIs. In generics, you optimized for cost—using cheaper solvents, maximizing yields, minimizing steps. In custom manufacturing, you optimized for the customer's specific needs—maybe they needed a particular polymorph, a specific particle size distribution, or ultra-low impurity levels. This required flexible thinking and technical versatility.

Between 2004 and 2013, Neuland scaled up over 350 processes—each one unique, each one a puzzle to solve. Some were for Big Pharma companies taking drugs through clinical trials. Others were for generic companies needing specialized processes to avoid patent infringement. Still others were for biotech companies with complex molecules that traditional manufacturers couldn't handle.

The project management infrastructure Neuland built was as important as its chemistry capabilities. Each project had defined milestones, regular customer communication, and risk mitigation strategies. The company developed what would later be branded as the "Neuland GuarD" system—a comprehensive project management approach that gave customers visibility into progress while protecting intellectual property.

The intellectual property dance was delicate. Unlike generic APIs where processes were Neuland's IP, in custom manufacturing, innovations often belonged to customers. Neuland had to build Chinese walls between projects, ensure team members signed specific confidentiality agreements, and sometimes even create physical separation between different customer projects. This IP hygiene, rare among Indian manufacturers at the time, became a key differentiator.

The business model economics were compelling but required patience. A custom manufacturing project might take 5-7 years from initial engagement to commercial manufacturing—through preclinical, Phase I, II, III trials, and regulatory approval. Many projects would fail (the drug wouldn't work or the customer would run out of money), but successful ones could generate revenues for decades. It was venture capital economics applied to manufacturing.

By 2013, Neuland had filed over 400 DMFs worldwide—a staggering number that reflected both the generic portfolio and custom projects. Each DMF represented deep process knowledge, regulatory expertise, and customer trust. The company was no longer just competing with other API manufacturers; it was competing with the in-house manufacturing capabilities of pharmaceutical companies themselves.

The strategic decision to remain API-only, even as custom manufacturing opportunities arose, proved prescient. When Neuland approached a Big Pharma company for a custom synthesis project, there was no fear that Neuland would later compete in the finished drug market. When a biotech needed a manufacturing partner for its lead compound, Neuland's pure-play positioning eliminated channel conflict concerns.

The human capital transformation was profound. The company evolved from employing primarily chemists and chemical engineers to adding project managers, regulatory specialists, quality experts, and business development professionals with deep pharmaceutical industry experience. The R&D team expanded from basic process development to include analytical development, formulation support (even though Neuland didn't make formulations, understanding them helped optimize APIs), and specialized capabilities like crystallization science.

Financial performance during this period reflected the strategic transition. While revenues grew steadily, the real value creation was in the pipeline of custom manufacturing projects and the relationships with innovator companies. By 2013, custom manufacturing solutions (CMS) had become a significant revenue contributor, with higher margins and stickier customer relationships than generic APIs.

The 2008 financial crisis tested this strategy. Several biotech customers went bankrupt, Big Pharma companies consolidated and rationalized suppliers, and funding for new drug development dried up. Neuland survived by maintaining a balance—custom manufacturing for growth and differentiation, generic APIs for cash flow and stability. This portfolio approach, lacking the elegance of pure-play strategies, proved remarkably resilient.

As 2013 ended, Neuland faced a new opportunity. The biotech industry, recovered from the financial crisis and fueled by breakthrough science in areas like oncology and rare diseases, needed specialized manufacturing partners more than ever. These weren't just traditional small molecules anymore—they were complex compounds, some requiring peptide chemistry, others needing contained handling for highly potent substances. Neuland's next transformation would require not just new capabilities but a fundamental bet on where pharmaceutical innovation was heading.

V. The Biotech Bet: Becoming a CDMO Partner (2014–2021)

The eureka moment came during a 2014 customer visit. A Bay Area biotech CEO, walking through Neuland's facility, made an observation that would catalyze the company's next evolution: "You have the quality systems of Big Pharma, the flexibility of a startup, and the cost structure of India. Why aren't you positioning yourself as a CDMO for biotechs like us?" The term CDMO—Contract Development and Manufacturing Organization—represented more than semantic evolution from contract manufacturer. It implied partnership from development through commercialization, not just production of defined processes.

The biotech landscape of 2014 was experiencing a golden age. Breakthrough therapies in oncology, rare diseases, and immunology were emerging from small companies funded by venture capital and IPO proceeds. These companies had brilliant science but no manufacturing infrastructure. They needed partners who could take a gram of compound synthesized in an academic lab and scale it to tons for commercial supply—all while meeting regulatory requirements across multiple geographies.

Neuland's R&D facility received FDA approval in 2014, a critical milestone that most competitors overlooked. This wasn't just another manufacturing site approval; it was validation that Neuland's development work met FDA standards. Biotech companies could now start development projects with Neuland knowing that the same team, same facility, and same quality systems would carry through to commercial manufacturing. This continuity eliminated a major risk in the drug development process—technology transfer between development and manufacturing sites.

The business reorganization into two clear verticals—Generic Drug Substances (GDS) and Custom Manufacturing Solutions (CMS)—wasn't just administrative reshuffling. It reflected fundamentally different business models, customer needs, and organizational capabilities. GDS operated on scale, efficiency, and cost optimization. CMS operated on flexibility, technical complexity, and customer intimacy. The employees, metrics, and even cultural norms differed between divisions.

The customer portfolio evolution told the story. Large MNCs like Pfizer and Novartis used Neuland for specific APIs where they'd discontinued internal manufacturing. Mid-sized pharma companies partnered for entire portfolios, viewing Neuland as their extended manufacturing arm. But the real growth came from biotech companies—organizations with names unknown to the public but developing potentially breakthrough therapies. These relationships started small (kilograms for clinical trials) but could scale massively upon FDA approval.

By 2021, Neuland was manufacturing seven NCE (New Chemical Entity) APIs commercially for US, Europe, and Japan. Each represented a drug that had never existed before, where Neuland had been involved from early development through commercial launch. The pride in the organization was palpable—they weren't just making generic copies anymore; they were enabling new medicines to reach patients.

The regulatory moat deepened significantly during this period. FDA inspections became routine rather than events. European regulators, Japanese PMDA, Brazilian ANVISA—Neuland hosted them all, often multiple times per year. Each successful inspection added another layer to the trust fortress. When a biotech needed to file an NDA (New Drug Application), Neuland's regulatory track record eliminated a major risk factor.

The technical capabilities expanded into specialized areas. Controlled substances requiring DEA licenses, highly potent APIs requiring contained manufacturing, complex multi-step syntheses with chiral centers—Neuland developed expertise in niches where many competitors feared to tread. The company's ability to handle challenging chemistry became its calling card in the biotech community.

The uninterrupted supply achievement, seemingly mundane, was actually remarkable. From 2014 to 2021, despite natural disasters, the COVID-19 pandemic, and supply chain disruptions, Neuland never had a drug shortage that impacted patient supply. This reliability, measured not in percentages but in zeros (zero disruptions), became a powerful selling point. When a biotech CEO's drug was the only treatment option for a rare disease patient, supply reliability trumped cost considerations.

Project wins during this period read like a who's who of pharmaceutical innovation. While customer names often remained confidential, the therapeutic areas spoke volumes: breakthrough cancer treatments, novel antibiotics for resistant infections, treatments for rare genetic disorders affecting children. Neuland wasn't just a supplier; it was an enabler of medical progress.

The organizational culture evolved to match biotech customer needs. Where Big Pharma relationships were formal and structured, biotech partnerships were intimate and flexible. A biotech CEO might call directly with a technical question. Scientists from both organizations collaborated on process optimization. The relationship was less vendor-customer and more extended team.

Investment in infrastructure accelerated. New R&D labs for process development, analytical capabilities for increasingly complex molecules, pilot plants that could mimic commercial conditions—each investment was made with biotech needs in mind. The company added capabilities in flow chemistry, biocatalysis, and other emerging technologies that biotechs were incorporating into their molecular designs.

The COVID-19 pandemic, arriving at the tail end of this period, validated the CDMO strategy in unexpected ways. While generic API demand fluctuated wildly, custom manufacturing projects continued steadily—drugs in clinical trials still needed to be supplied, approved drugs still needed manufacturing. The resilience of the CMS model during global disruption convinced management to double down on the strategy.

Financial performance reflected the strategic success. CMS revenues grew to ₹637 crore, with margins significantly higher than generic APIs. More importantly, the revenue quality improved—multi-year contracts, sole-source positions, and partnerships where price was secondary to reliability. The customer concentration decreased as the biotech portfolio expanded, reducing dependence on any single molecule or customer.

By 2021's end, Neuland had transformed from an API manufacturer that did some custom work to a CDMO that also maintained a generic portfolio. The identity shift was complete. But the pharmaceutical industry wasn't standing still. New modalities like peptides, oligonucleotides, and antibody-drug conjugates were emerging. The next phase of growth would require Neuland to push beyond traditional small molecule chemistry into the frontier of pharmaceutical innovation.

VI. Modern Era: Peptides, Scale, and Global Recognition (2022–Present)

The board meeting in early 2022 was unusually contentious. The proposal on the table: invest over ₹300 crore in peptide manufacturing capabilities—a technology platform entirely different from Neuland's small molecule expertise. The debate wasn't about the market opportunity (the GLP-1 agonist revolution was already visible) but about strategic focus. Should a company that had succeeded through disciplined focus on small molecule APIs venture into the complex world of peptide synthesis? The decision to proceed would mark Neuland's boldest bet since going international.

The peptide investment, officially announced in 2022, wasn't reactive to the Ozempic/Wegovy phenomenon—though that certainly validated the decision. It emerged from watching customer pipelines. Increasingly, biotech companies were developing peptide-based drugs for metabolic diseases, oncology, and rare disorders. These molecules required solid-phase synthesis, a fundamentally different chemistry from Neuland's traditional solution-phase processes. It meant new equipment, new expertise, new quality considerations.

The execution has been methodical. Rather than rushing to capture the GLP-1 gold rush, Neuland focused on building foundational capabilities. The company hired peptide chemistry experts from established players, invested in automated synthesizers, and most critically, developed purification capabilities for complex peptides. The facility, expected to be operational by 2025, represents not just capacity addition but capability transformation.

Current operational scale tells a story of institutional maturity. Three FDA-inspected facilities running multiple shifts, 846+ DMFs filed globally (a number that speaks to both breadth and regulatory expertise), operations across 85+ countries, and 2,011 employees as of January 2025. These aren't just numbers—they represent organizational complexity that few Indian pharmaceutical companies have successfully managed.

The Prime APIs segment, contributing roughly 15 mature large-volume molecules, became the cash flow engine funding growth investments. Levetiracetam (anti-epileptic) and Mirtazapine (antidepressant) emerged as anchor products, generating steady revenues even as Chinese competition intensified. The strategy here shifted from volume growth to value optimization—finding customers who valued supply security over marginal cost savings.

The Chinese reopening in 2023 brought expected challenges. Chinese API manufacturers, constrained during COVID, returned with aggressive pricing and capacity additions. Prices for several generic APIs dropped 20-30% within months. Neuland's response was strategic retreat—ceding share in commoditized molecules while strengthening positions in complex chemistries and regulated markets where Chinese suppliers faced trust deficits.

The specialty and custom synthesis portfolio became the differentiation driver. These weren't molecules you could find in standard catalogs—they were customer-specific, often involving complex intellectual property arrangements, always requiring deep technical collaboration. The revenue per kilogram might be 10-100x that of generic APIs, justifying the intensive resource allocation.

Technology differentiation emerged as a subtle but powerful competitive advantage. While competitors focused on cost reduction through scale, Neuland invested in process intensification—continuous flow chemistry, biocatalysis, advanced crystallization techniques. These technologies didn't just reduce costs; they enabled syntheses that were impossible with conventional methods. When a biotech needed a specific polymorph or chirality, Neuland's technical toolkit provided solutions.

The organizational structure evolution reflected business complexity. The company now operates with sophisticated matrix management—therapeutic area teams cutting across functional departments, project management offices coordinating global activities, and digital systems enabling real-time visibility into operations. This isn't the hierarchical Indian company of the 1990s; it's a global organization that happens to be headquartered in India.

Recent financial performance shows both resilience and stress. Q4 FY25 revenues of ₹328.36 crore and net profit of ₹27.81 crore represent solid operational performance, but the 59% year-over-year profit decline and 15% revenue drop highlight industry headwinds. The margin compression from Chinese competition and customer inventory adjustments tested the business model. Yet management's confidence in FY26 recovery, backed by a strong order book and new product launches, suggests temporary rather than structural challenges.

The employee growth to 2,011 professionals tells a human capital story. With 17% of the workforce in R&D and teams managing 40+ simultaneous projects, Neuland has built intellectual infrastructure that transcends individual expertise. The knowledge management systems, the standard operating procedures, the institutional memory—these intangible assets are perhaps more valuable than the physical manufacturing facilities.

ESG initiatives, once peripheral, have become central to customer relationships. Biotech companies, under pressure from investors and regulators, increasingly evaluate suppliers on environmental impact, labor practices, and governance standards. Neuland's investments in solvent recovery, water recycling, and renewable energy aren't just compliance checkboxes—they're competitive necessities.

The innovation pipeline reveals strategic intent. Beyond peptides, Neuland is exploring antibody-drug conjugate (ADC) payloads, highly potent APIs for targeted cancer therapies, and continuous manufacturing platforms. Each represents a bet on where pharmaceutical innovation is heading, requiring investments years before revenue materialization.

Customer testimonials, rarely public but powerful when shared, consistently highlight three themes: reliability when others failed, flexibility when requirements changed, and transparency when problems arose. A biotech executive recently noted: "During COVID, when our Chinese supplier disappeared and our Indian backup had quality issues, Neuland delivered. That's worth more than any cost savings."

As 2025 progresses, Neuland stands at another inflection point. The peptide investments are nearing completion, the CDMO portfolio is expanding, and the generic API business, while challenged, remains cash-generative. The company that Dr. Rao founded 40 years ago to make basic APIs has evolved into something far more complex—a critical node in the global pharmaceutical supply chain, invisible to patients but indispensable to drug developers.

VII. The Business Model & Unit Economics

Understanding Neuland's economics requires peeling back layers of complexity that most investors overlook. The headline numbers—₹1,330 crore revenue, ₹176 crore profit—tell you what happened but not why it's sustainable or where it's heading. The real story lies in the interplay between two fundamentally different business models operating under one roof, each with distinct economics, risk profiles, and growth trajectories.

The two-pronged approach seems simple on paper: non-exclusive APIs (Prime and Specialty) generate steady cash flows while Custom Manufacturing Solutions (CMS) drives growth and differentiation. But the execution complexity is staggering. Imagine running a commodity business requiring ruthless efficiency alongside a specialty business demanding artisanal attention—in the same facilities, with shared overhead, but completely different customer expectations.

The R&D investment strategy—consistently around 8% of revenues—appears unremarkable until you decompose it. About 40% goes to maintaining and defending the generic portfolio: finding new synthetic routes, improving yields, reducing impurities. Another 40% supports custom projects: scaling up customer processes, solving technical challenges, developing analytical methods. The remaining 20% funds future bets: peptides, continuous manufacturing, new technology platforms. This allocation reflects a portfolio approach to innovation—some investments for today's cash, others for tomorrow's growth.

The 200 DMFs filed worldwide by 2023 represent a hidden asset rarely valued properly. Each DMF costs ₹50-80 lakhs to develop and file, meaning Neuland has invested over ₹100 crore in this regulatory library. But the return isn't linear—it's exponential. A single DMF might generate ₹10 crore annually for a decade. More importantly, this portfolio creates switching costs. When a customer references Neuland's DMF in their drug application, changing suppliers requires regulatory amendments that can take years.

Workforce allocation reveals operational priorities: 17% in R&D, managing 40+ simultaneous projects. But dig deeper: within R&D, about 30% are PhD chemists working on complex syntheses, 25% are analytical chemists ensuring quality, 20% are regulatory specialists managing submissions, and 25% are project managers coordinating activities. This isn't just scientific expertise—it's organizational capability to manage complexity at scale.

The capital intensity challenge is real but misunderstood. Yes, pharmaceutical manufacturing requires significant fixed assets—reactors, analytical equipment, utilities. But the working capital dynamics are equally important. A custom project might require purchasing specialized raw materials months before production, holding inventory for customer-specific requirements, and extending credit terms to biotech customers conserving cash. The cash conversion cycle can extend to 180+ days for custom projects versus 90-120 days for generic APIs.

Margin dynamics tell different stories for each business. Generic APIs operate on gross margins of 35-40%, compressed by Chinese competition and customer bargaining power. But CMS projects can achieve 50-60% gross margins, especially for complex molecules or when Neuland has sole-source positions. The blended margins that investors see obscure this underlying reality. A shift in mix toward CMS—even with flat revenues—can dramatically improve profitability.

The unit economics of a typical custom project illustrate the model's attractiveness. Initial engagement might generate ₹50 lakhs in development fees. Clinical trial supplies through phases generate ₹2-5 crore annually. Upon commercialization, revenues can jump to ₹20-50 crore annually, sometimes more. The lifetime value of a successful project can exceed ₹200 crore, though the probability of reaching commercialization is only 10-15%. It's venture economics applied to manufacturing.

Customer concentration risk appears manageable on paper—no single customer exceeds 15% of revenues. But dependency runs deeper. The top 10 customers represent 60% of revenues, and more critically, 75% of margins (they buy higher-value products). Losing any major customer would impact not just revenues but capacity utilization, overhead absorption, and investment returns.

The pricing power paradox is fascinating. In generic APIs, Neuland is largely a price taker—global supply and demand determine rates. But in custom manufacturing, pricing is value-based. A biotech developing a rare disease drug might pay 10x the per-kilogram rate of a generic API because the alternative—building their own facility—would cost hundreds of crores and take years.

Fixed cost leverage becomes critical at scale. The same quality systems, regulatory infrastructure, and management overhead that support ₹1,000 crore revenue could support ₹2,000 crore with minimal additions. This operating leverage means that revenue growth drops disproportionately to the bottom line—a 20% revenue increase might drive 40% profit growth.

The return on capital employed (ROCE) calculation requires nuance. The book ROCE might be 15-20%, respectable but not exceptional. But this aggregates high-ROCE custom projects (where customers often fund capacity) with capital-intensive generic APIs. The incremental ROCE on new CMS projects can exceed 30%, while new generic API investments might return 12-15%.

Currency dynamics add another layer. With 70% of revenues from exports but 60% of costs in rupees, Neuland benefits from rupee depreciation. A 5% rupee decline might add 200 basis points to margins. But this isn't just translation gain—it's competitive advantage against developed market competitors.

The reinvestment requirements vary dramatically by business. Generic APIs need continuous investment to stay competitive—new routes, better equipment, expanded capacity. CMS requires lumpy investments—a new contained facility for highly potent APIs, analytical equipment for complex molecules, the current peptide platform. The capital allocation decisions determine not just growth but strategic positioning.

Working capital management tells a cultural story. Indian pharmaceutical companies traditionally operated on generous credit terms, both given and taken. Neuland's discipline here—collecting receivables within 90 days, negotiating supplier terms, managing inventory turns—frees cash for growth investments. The difference between 120-day and 90-day receivables might seem trivial, but at ₹1,300 crore revenues, it's ₹100 crore of cash.

The financial resilience during downturns reveals model strength. When generic API prices collapsed 30% in 2023, the company remained profitable. When biotech funding dried up in 2022, the generic portfolio provided stability. This portfolio balance—neither pure-play generic nor pure-play CDMO—lacks the elegance that investors prefer but provides the resilience that survival requires.

VIII. Playbook: Building a Global CDMO

The formula for building a global CDMO from India seems deceptively simple: combine Indian cost advantages with Western quality standards. But if it were that simple, there would be dozens of Neulands. The reality is that success requires mastering paradoxes that break most companies: being flexible yet reliable, cost-effective yet quality-obsessed, global yet rooted, growing yet focused.

The trust equation that Neuland cracked has three variables, each necessary but insufficient alone. Quality is table stakes—every batch must meet specifications, every time, without exception. Regulatory compliance is the license to operate—not just passing inspections but embracing the spirit of regulations. But reliability—delivering on promises when supply chains break, when raw materials disappear, when disasters strike—that's what transforms vendors into partners.

The "never compete with customers" principle sounds obvious but requires extraordinary discipline. When Neuland developed a breakthrough process for a blockbuster drug, the temptation to forward-integrate must have been overwhelming. The margins would triple, the brand recognition would soar. But the moment Neuland launched a finished dosage, every formulator customer would become a potential competitor. The long-term value of remaining Switzerland exceeded any short-term gain from integration.

The Neuland GuarD system, developed over decades, exemplifies operational excellence. It's not revolutionary technology—it's disciplined project management adapted for pharmaceutical complexity. Each project has defined phases, gates, deliverables, and risk assessments. Weekly customer calls, monthly steering committees, quarterly business reviews—the rhythm of communication builds confidence. When problems arise (and they always do), the system ensures early detection, rapid escalation, and transparent resolution.

Building for the long term in an industry obsessed with quarterly earnings requires unusual ownership structures and leadership mindsets. The Rao family's continued involvement—now in its second generation—provides continuity that public market pressures might otherwise erode. When a biotech partner needs assurance that Neuland will exist in 10 years to supply their drug, family ownership becomes a competitive advantage.

Managing complexity at Neuland's scale breaks traditional organizational models. Fifty-plus APIs across therapeutic categories, each with unique synthesis routes, regulatory requirements, and customer specifications. The information management alone is staggering—thousands of standard operating procedures, millions of batch records, billions of data points. Yet the system works because complexity is embedded in processes, not dependent on individuals.

The FDA approval strategy reveals sophisticated regulatory thinking. Rather than viewing inspections as hurdles, Neuland treats them as capability-building exercises. Pre-inspection preparation involves the entire organization—mock audits, gap analyses, remediation projects. Post-inspection, regardless of outcome, teams conduct retrospectives to identify improvement opportunities. This continuous improvement mindset transformed regulatory compliance from cost center to competitive advantage.

The art of surviving in a commoditized industry while maintaining differentiation requires strategic schizophrenia. In generic APIs, Neuland must match Chinese efficiency—automated processes, minimal waste, maximum asset utilization. In custom manufacturing, it must provide Swiss precision—artisanal attention, perfect documentation, zero defects. Running both models in parallel, sometimes in the same facility, requires organizational ambidexterity few achieve.

Technology adoption follows a pragmatic philosophy: adopt what adds value, avoid what adds complexity. Neuland wasn't first to implement enterprise resource planning (ERP) or laboratory information management systems (LIMS), but when it did, implementation was thorough. The company evaluates new technologies—artificial intelligence for process optimization, blockchain for supply chain transparency—but only adopts those with clear return on investment.

The human capital strategy deserves special attention. In an industry where talented chemists are scarce and mobile, Neuland retained expertise through a combination of competitive compensation, professional development, and something intangible—pride in enabling new medicines. When employees see their work resulting in treatments for previously incurable diseases, retention becomes about purpose, not just pay.

Customer relationship management transcends traditional sales. The best business development professionals at Neuland are technical experts who speak the customer's language. They discuss stereochemistry and polymorphism, not just price and delivery. Relationships develop over years, often decades. When a Neuland BD director retires, customers mourn the loss of a trusted advisor, not just a vendor contact.

The partnership mentality extends beyond customers to suppliers. Raw material vendors aren't just squeezed for lowest prices—they're developed as partners. Neuland shares forecasts, provides technical support, sometimes even helps finance capacity expansion. This collaborative approach proved invaluable during COVID when raw material allocation went to trusted partners, not highest bidders.

Risk management philosophy balances growth with prudence. The company maintains multiple suppliers for critical materials, redundant capacity for key products, and financial reserves for unexpected events. This conservatism might limit growth rates but ensures survival through cycles. When competitors leveraged aggressively and collapsed during downturns, Neuland's prudence became prescience.

The innovation strategy focuses on process rather than product innovation. While pharmaceutical companies discover new molecules, Neuland discovers better ways to make them. This process innovation—finding shorter routes, eliminating hazardous reagents, improving yields—creates value that's harder to copy than product innovation. A competitor might reverse-engineer a molecule but not the accumulated process knowledge.

Global operations require cultural translation beyond language. American customers value direct communication and quick decisions. Japanese partners prize consensus and long-term thinking. European regulators expect thorough documentation and conservative approaches. Neuland's ability to adapt communication, negotiation, and operational styles to different cultural contexts enables global reach from an Indian base.

The succession planning, often overlooked in founder-led companies, shows institutional maturity. The second generation isn't just inheriting ownership—they're earning leadership through operational experience. Working their way through different functions, spending time with customers, understanding the business from ground up. This apprenticeship model ensures continuity without stagnation.

The lesson for aspiring CDMOs is sobering: building trust takes decades, losing it takes moments. Every batch, every interaction, every commitment adds to or subtracts from the trust account. Neuland's 40-year journey shows that in pharmaceutical manufacturing, there are no shortcuts to credibility. The playbook isn't secret—it's just extraordinarily difficult to execute consistently over decades.

IX. Analysis & Bear vs. Bull Case

The investment case for Neuland Laboratories presents a fascinating study in contrasts. Bulls see a unique asset—one of the few Indian companies successfully transitioning from commoditized generics to specialized CDMO services. Bears see a company caught between two worlds, lacking the scale for commodity competition and the specialization for premium pricing. Both perspectives have merit, and the truth likely lies in understanding which factors will dominate over different time horizons.

The Bull Case: Compounding Quality in a Growing Market

The five-year performance metrics tell a compelling growth story: 66% net profit CAGR and 14% sales CAGR aren't just numbers—they represent successful execution of a difficult strategy transition. Companies rarely achieve such profit growth while transforming their business model. This isn't financial engineering or multiple expansion; it's operational improvement dropping to the bottom line.

Trading at 10.5x book value might seem expensive, but context matters. The book value understates economic reality—it doesn't capture the value of 846+ regulatory filings, customer relationships built over decades, or the intellectual property embedded in process knowledge. More importantly, the replacement cost of Neuland's capabilities—three FDA-approved facilities, proven CDMO track record, established customer base—would far exceed book value.

The biotech relationship moat deserves special attention. Switching costs in pharmaceutical manufacturing are enormous—not just regulatory amendments but revalidation, stability studies, and risk of supply disruption. Once Neuland is embedded in a drug's supply chain, displacement is rare unless service failures occur. With seven NCE APIs in commercial production, these relationships generate recurring revenues for patent life plus several years.

The peptide investment positions Neuland for the next wave of pharmaceutical innovation. The GLP-1 agonist boom is just beginning—obesity, diabetes, and now indications in cardiovascular and kidney disease. The peptide market is expected to grow at 8-10% annually through 2030. Neuland's entry isn't too late; it's timed for when capacity constraints will drive customers to qualified alternatives.

Regulatory approvals across multiple jurisdictions create competitive barriers that strengthen over time. Each successful inspection adds to the track record that risk-averse pharmaceutical companies value. New entrants might match Neuland's cost structure, but they can't quickly replicate 40 years of successful regulatory history. In pharmaceuticals, trust is earned in decades, lost in moments.

The business mix evolution toward higher-margin CMS revenues could drive multiple expansion. As custom manufacturing approaches 60-70% of revenues (from current 48%), the market might revalue Neuland closer to pure-play CDMO multiples. The difference between trading at 15x earnings (commodity API multiple) versus 25x earnings (CDMO multiple) represents significant value creation without operational changes.

Management's confidence in FY26 recovery isn't just hope—it's based on tangible developments. The peptide facility coming online, new customer projects reaching commercial stage, and the anniversary of Chinese pricing pressure all point toward earnings recovery. The order book visibility and customer commitments suggest management has reasonable basis for optimism.

The operational leverage inherent in the model means revenue recovery will disproportionately impact profits. With fixed costs already absorbed, incremental revenues from new projects or volume recovery will largely flow to the bottom line. A 15-20% revenue increase could drive 40-50% profit growth—the kind of non-linear outcome that creates investment returns.

The Bear Case: Structural Challenges in a Difficult Industry

The recent performance deterioration can't be dismissed as temporary. A 59% net profit decline and 15% revenue drop suggest fundamental challenges, not just cyclical weakness. When a company misses estimates this badly, it often indicates management doesn't fully understand their business dynamics or competitive position.

Promoter holding at 32.7%, down from higher levels three years ago, raises questions. Insiders selling into strength might signal their assessment of future prospects. While some reduction for liquidity or diversification is normal, the trend bears watching. When founders reduce stakes, outside investors should ask why.

Chinese competition isn't going away—it's intensifying. As China's domestic market slows, manufacturers are aggressively pursuing export markets. Their cost advantages—subsidized utilities, lower environmental compliance costs, government support—are structural, not cyclical. Neuland can't match Chinese pricing without destroying margins, but not matching means losing volume.

The dependency on a few key molecules creates vulnerability. Levetiracetam and Mirtazapine generate disproportionate profits. If either faces new competition, supply gluts, or demand shifts, the impact would be severe. Portfolio concentration is particularly risky in generic APIs where switching costs are low and customer loyalty minimal.

Capital intensity remains a fundamental challenge. The peptide investment, while strategic, requires hundreds of crores with uncertain returns. If the facility doesn't achieve target utilization or if peptide pricing follows the generic API pattern of rapid commoditization, the return on investment could disappoint. Meanwhile, this capital could have been returned to shareholders or invested in proven businesses.

The CDMO market is becoming increasingly competitive. Every Indian pharmaceutical company wants to be a CDMO—higher margins, better growth, premium valuations. But as supply increases, customer bargaining power grows. The "trust premium" that Neuland earned over decades might erode as competitors match quality standards and regulatory compliance.

Customer concentration, while improved, remains concerning. The top 10 customers generating 60% of revenues creates vulnerability to relationship changes. A single customer loss—from acquisition, insourcing, or relationship deterioration—could materially impact results. This concentration is particularly risky given the long sales cycles for new customers.

The lack of product innovation limits pricing power. While process innovation is valuable, it's less defensible than novel molecules. Competitors can eventually match process improvements, but they can't copy patented compounds. Neuland's position as a service provider, not an innovator, caps value creation potential.

Weighing the Balance

The bull-bear debate ultimately centers on time horizon and belief in management execution. Bulls betting on five-year outcomes can point to structural industry trends—increasing outsourcing, biotech innovation, manufacturing complexity—that favor established CDMOs. Bears focused on next twelve months see margin pressure, Chinese competition, and execution risks.

The truth likely involves both narratives playing out simultaneously. Neuland will probably face continued pressure in generic APIs while building differentiation in custom manufacturing. Success requires threading the needle—maintaining enough generic API business for scale and cash flow while transitioning toward higher-value services without losing focus.

For investors, the key variables to monitor are clear: CMS revenue growth rate, peptide facility utilization, customer concentration trends, and regulatory track record. If Neuland executes its transition while maintaining operational excellence, the bull case could deliver substantial returns. If execution falters or industry dynamics deteriorate faster than expected, the bear case warnings will prove prescient.

X. Epilogue & Future Outlook

Standing at Neuland's Hyderabad headquarters today, you see a company at an inflection point that mirrors its founding forty years ago. Just as Dr. Rao bet in 1984 that India could manufacture to global standards, current management is betting that Neuland can evolve from manufacturer to innovation partner. The difference is that this transformation must occur while maintaining operations that supply critical medicines to millions of patients globally—rebuilding the plane while flying it.

Management's expectation of growth resuming in FY26 isn't just corporate optimism—it's based on specific catalysts converging. The peptide facility will complete validation and begin commercial production. Several custom manufacturing projects in Phase III trials are expected to receive approval, transitioning from clinical to commercial supply. The anniversary effect of Chinese pricing pressure means comparisons become easier. And the biotech funding environment, while not returning to 2021 peaks, is showing signs of recovery.

The peptide opportunity deserves special attention because it represents more than capacity addition—it's Neuland's entry into the future of pharmaceutical innovation. Beyond the obvious GLP-1 opportunity, peptides are increasingly used in oncology, immunology, and rare diseases. The technology platform Neuland is building—solid-phase synthesis, advanced purification, analytical capabilities for complex molecules—positions it for wherever peptide innovation leads.

Next-generation therapies present both opportunity and challenge. Antibody-drug conjugates, oligonucleotides, and cell and gene therapy components require capabilities beyond traditional small molecules. Neuland must decide whether to pursue these adjacencies or maintain focus on areas of proven expertise. The temptation to chase every trend must be balanced against the discipline that enabled success.

Industry consolidation accelerates Neuland's strategic importance. As Big Pharma acquires biotech companies, they often rationalize supply chains, preferring fewer, more capable suppliers. Neuland's scale, track record, and broad capabilities position it as a consolidation beneficiary. Conversely, if Neuland itself becomes an acquisition target, its unique positioning—profitable, growing, with strategic assets—could command premium valuations.

The ESG transformation isn't just compliance theater—it's becoming a commercial imperative. Pharmaceutical companies, under pressure from investors and regulators, increasingly evaluate suppliers on environmental impact. Neuland's investments in green chemistry, renewable energy, and water recycling aren't just cost centers—they're becoming qualification criteria for new business. The company that manages to be both low-cost and low-impact will win the next decade.

The human capital challenge looms large. As Neuland grows more complex—multiple technologies, global customers, increasing regulations—it needs increasingly sophisticated talent. Competition for pharmaceutical expertise is global, and Hyderabad must compete with Basel, Boston, and Shanghai for talent. The company's ability to attract, develop, and retain world-class professionals will determine its trajectory more than any single strategic decision.

What would success look like in five years? The optimistic scenario sees Neuland as a ₹3,000 crore revenue company with CMS contributing 70%, margins expanded through operational leverage, and recognition as one of the top five CDMOs globally for complex APIs and peptides. The company would be manufacturing 15-20 commercial NCE APIs, with deep relationships across the biotech ecosystem.

The pragmatic scenario is more modest but still attractive: ₹2,000 crore revenues, balanced between generic and custom manufacturing, steady margins despite competitive pressure, and continued operational excellence. Neuland would remain a reliable, profitable, growing company—not spectacular but solid, generating consistent returns for shareholders while enabling medical innovation.

The risk scenario can't be ignored: Chinese competition destroys generic API margins, biotech funding remains constrained limiting custom opportunities, peptide investments fail to generate returns, and Neuland becomes subscale in an consolidating industry. The company would survive but stagnate, generating cash but not growth, eventually becoming an acquisition target at modest premiums.

The institutional legacy that Dr. Rao built transcends financial metrics. Neuland proved that Indian companies could be trusted with critical pharmaceutical manufacturing. It demonstrated that competing on quality and reliability, not just cost, was both possible and profitable. It showed that remaining focused—saying no to tempting diversifications—could create more value than conglomerate expansion.

For investors evaluating Neuland today, the central question isn't whether the company will survive—its track record, customer relationships, and financial strength ensure continuity. The question is whether Neuland can maintain its historical trajectory of transformation, evolving from service provider to innovation partner, from vendor to value creator.

The pharmaceutical industry needs companies like Neuland more than ever. As drug development becomes more complex, specialized, and globalized, the role of trusted manufacturing partners becomes critical. The company that can combine emerging market cost structures with developed market quality standards, entrepreneurial flexibility with institutional reliability, will capture disproportionate value.

Looking ahead, Neuland's story remains unfinished. The next chapter—whether it's about successful transformation, steady execution, or strategic combination—will be written by how well the company navigates the tensions inherent in its position: between commodity and specialty, between scale and focus, between independence and partnership.

What's certain is that forty years after Dr. Rao founded Neuland with a vision of Indian pharmaceutical excellence, that vision has been validated. What remains to be seen is whether the next forty years will be about maintaining that excellence or transcending it. For a company that has consistently exceeded expectations by staying focused on what others overlooked—the unglamorous but essential work of making medicines safely, reliably, and efficiently—betting against continued success seems premature.

The story of Neuland Laboratories ultimately isn't about financial engineering or strategic brilliance—it's about operational excellence compounded over decades. In an industry where trust is the ultimate currency and reliability the highest virtue, Neuland has built something rare: a reputation that transcends transactions. Whether that reputation translates into superior returns for investors depends on execution, market dynamics, and strategic choices yet to be made. But for patients depending on medicines Neuland manufactures, for biotech companies trusting Neuland with their innovations, and for employees building careers on Neuland's foundation, the value creation has already been substantial.

The untold story of India's API powerhouse is still being written. And if history is any guide, it will continue to surprise those who underestimate the power of focused execution in an unfocused world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube