NephroPlus (Nephrocare Health Services Ltd): Scaling India's Dialysis Giant

I. Introduction & Episode Roadmap (0:00 – 0:10)

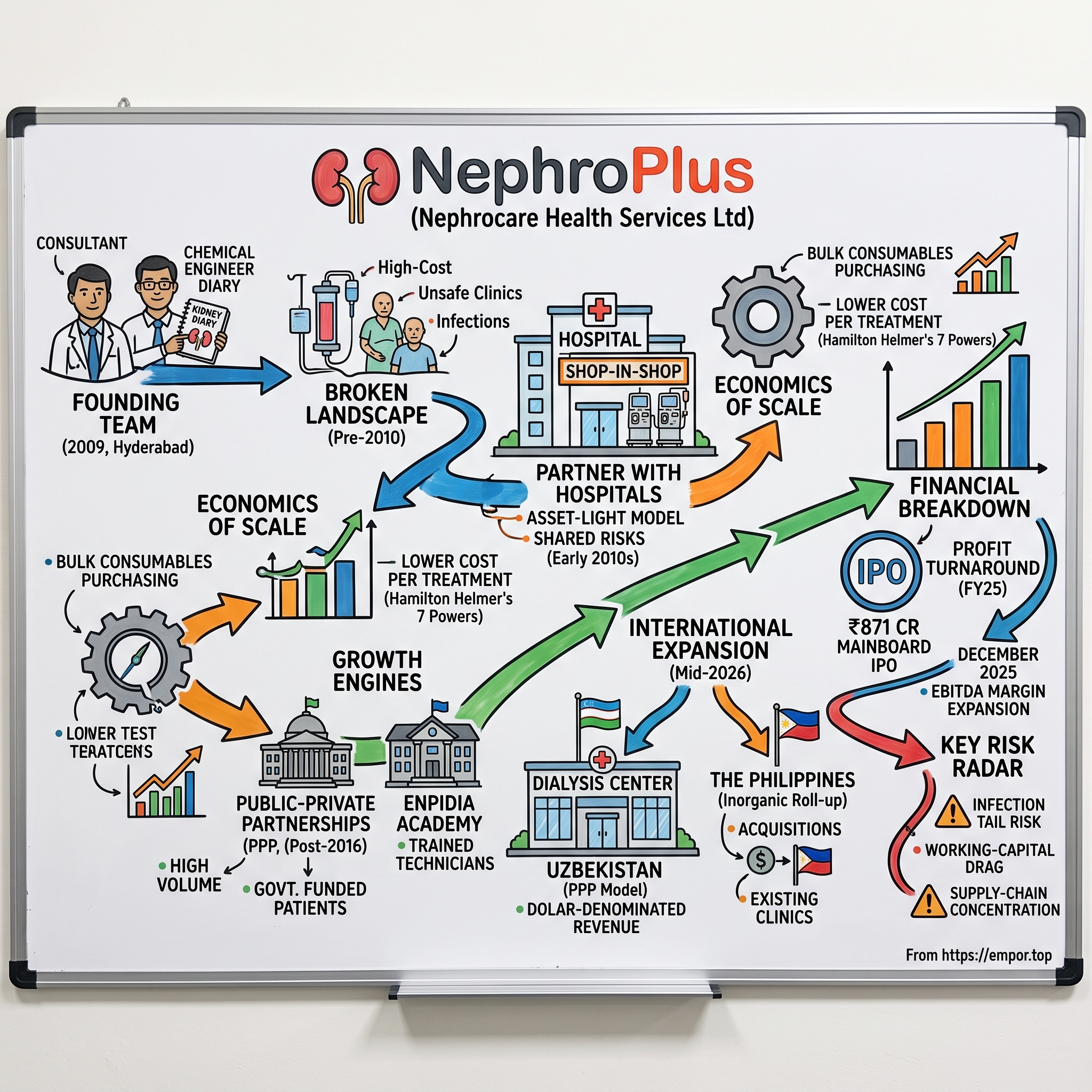

Let's start with the thesis, because it is unusually clean. A former McKinsey strategy consultant and a software engineer living with chronic kidney disease met over a blog, teamed up in Hyderabad in 2009, and built a dialysis chain that by fiscal 2025 was the largest in India by patients served, clinics operated, cities covered, treatments performed, revenue, and EBITDA.1 The company treated 29,281 patients and performed roughly 2.89 million dialysis treatments in India in FY25 alone,1 operated more than 500 clinics, expanded into Central Asia and Southeast Asia, and listed in a ₹871 crore mainboard IPO that opened on December 10, 2025.2 The stock debuted on December 17, 2025.15

But before we can tell that story we have to untangle a genuine trap that has caught retail investors, screeners, and even careless journalists.

The "Two Nephros" Paradox. There are two separate, unrelated public companies in India with almost identical names, and confusing them is an expensive mistake:

- Nephrocare Health Services Limited, which trades under the brand NephroPlus (NSE:

NEPHROPLUS, BSE:544647). This is the pan-India titan — roughly ₹756 crore of FY25 revenue, more than 500 clinics, international operations, and the December 2025 mainboard IPO.3 - Nephro Care India Limited (NSE SME:

NEPHROCARE-ST.NS), a much smaller, Kolkata-based regional operator that reported roughly ₹47 crore of revenue and listed on the NSE's SME platform in 2024. It is a different company with different owners.

The ticker attached to this article — NEPHROCARE-ST.NS — technically belongs to the smaller SME company. But the business story worth telling, the one that reveals how the economics of Indian dialysis actually work, is the story of NephroPlus (Nephrocare Health Services Ltd.). That is the true industry leader, the asset-light model that the whole sector now imitates, and the subject of the mid-2026 international acquisitions. So that is where we will spend our time, while keeping the smaller namesake in view as a useful contrast in what scale does and does not buy you.

Here is the road we will travel. First, the broken clinical landscape of early-2000s India, where dialysis was either unaffordable or unsafe. Then the invention of the "Shop-in-Shop" model that let NephroPlus scale without drowning in capital expenditure. Then the double-edged sword of government public-private partnerships. Then the real moat — the boring, powerful economics of buying consumables in bulk. And finally the mid-2026 international roll-up, the financials, the governance, and the genuine risks that a skeptical investor should be losing sleep over. Let's begin where every good origin story begins: with a person, not a company.

II. The Genesis: McKinsey, Passion, and a Kidney Diary (0:10 – 0:30)

In 1997, an 18-year-old named Kamal Shah was told his kidneys were failing. The diagnosis was atypical hemolytic uremic syndrome — a rare, brutal disorder in which the body's own defenses attack the small blood vessels, and among the casualties are the kidneys. For a teenager, this was supposed to be the end of the story: a life tethered to a machine, defined by what he could no longer do.

Kamal refused to accept that framing. Trained as a chemical engineer, he brought an engineer's stubborn curiosity to his own disease.5 Rather than treating dialysis as a clinical dead-end, he started documenting it — turning his experience into a blog that became known as "Kamal's Kidney Diary." He wrote about swimming, working, traveling, and living an active life while on dialysis, and in doing so he did something the entire medical establishment had failed to do: he mapped, in meticulous patient-level detail, every pain point in the Indian dialysis journey.5 The infections. The travel. The indifference. The fear. It was, in effect, a product-requirements document for a company that did not yet exist.

Somewhere in New Jersey, around 2008, a McKinsey strategy consultant named Vikram Vuppala was researching the fragmented Indian renal-care sector when he stumbled onto Kamal's blog.5 Vikram was an engineer by training who had gone on to a master's in computer science at the University of Illinois and an MBA from the University of Chicago's Booth School of Business before landing at McKinsey.6 He had the classic returning-diaspora itch: India's epidemic of diabetes and hypertension — the two leading causes of kidney failure — was exploding, and the infrastructure to treat its consequences was a shambles. What Vikram found in Kamal's writing was not a sob story but a blueprint, written by the one person who understood the problem from the inside.

The two men — both chemical engineers by original training, one a consultant, one a patient — connected, and in 2009 they founded NephroPlus in Hyderabad, joined by co-founders including Sandeep Gudibanda, an operator who would help scale the network, and Pullaiah Vuppala.5 The division of labor was almost poetic: Vikram brought the strategist's obsession with unit economics and scale; Kamal brought something no consultant could fake — the lived, daily reality of the customer.

The cultural pivot. That combination produced the company's defining early choice. Indian dialysis centers of the era were, by design and by neglect, depressing: dim rooms, anxious silence, patients treated as clinical problems to be processed. NephroPlus deliberately built the opposite. Kamal's patient-first philosophy became corporate DNA — bright centers, technicians trained in bedside manner, and a relentless message that a full life was possible on dialysis. The most vivid proof point was the "Dialysis Olympiad," an event where dialysis patients competed in athletic contests. It sounds like a marketing gimmick, and in part it was, but it was also a strategic statement: NephroPlus was selling not just a treatment but a way to keep living, and that emotional positioning would later translate into something investors care about a great deal — patient loyalty and low churn.

Turning that philosophy into a national footprint was a long, unglamorous grind, and it is easy to forget how improbable it once looked. In 2009 the idea that dialysis — low-margin, operationally miserable, and viewed by hospitals as a chore — could be built into a scalable, investable business was far from obvious. The early years were spent proving the unit economics one clinic at a time, earning the trust of nephrologists and hospital administrators who had no reason to hand a stranger their patients, and convincing capital that a chain of dialysis centers could ever be more than a low-return utility. The proof accumulated slowly and then quickly: from a single Hyderabad center the network grew into the hundreds of clinics across hundreds of cities, delivering on the order of two hundred thousand dialysis sessions a month before its IPO.16 That expansion is the connective tissue between the origin story and the financials — every one of those clinics is a small monument to a model that outsiders initially doubted could work at all.

What does this origin story tell an investor? Two things. First, that the company's differentiation was rooted in genuine domain empathy rather than a slide deck — harder for a competitor to copy than any piece of equipment. Second, and more soberingly, that a business built on a founder's personal mission carries key-person risk; the culture that makes NephroPlus distinctive is inseparable from the people who created it. Hold that thought. First we need to understand just how broken the market was that these two set out to fix.

III. The Broken Landscape: The Dialysis Crisis in Pre-2010 India (0:30 – 0:50)

Picture a family in a Tier-3 town in 2008. The father's kidneys have failed. The nearest dialysis machine is 120 kilometers away, in a private hospital in the state capital. He needs treatment three times a week, four hours each session, indefinitely, for the rest of his life. Do the arithmetic on the travel alone and you begin to understand why, in that era, a diagnosis of kidney failure in small-town India was often a quiet death sentence — not because the disease was untreatable, but because treatment was geographically and financially out of reach.

It helps to pause here and understand what dialysis actually is, because the economics flow directly from the biology. Healthy kidneys are the body's filtration plant: they scrub waste and excess fluid out of the blood around the clock. When they fail — most often as the end-stage consequence of diabetes or high blood pressure — that waste builds toward lethal levels. Hemodialysis substitutes a machine for the missing organ. The patient's blood is pumped out of the body, pushed through an artificial filter called a dialyzer — think of it as a bundle of thousands of hollow straws with semi-permeable walls — where waste and fluid pass across the membrane into a carefully mixed cleansing fluid, and the cleaned blood is returned. The catch is that it is slow and relentless: each session takes about four hours, and because the machine cannot store up cleaning the way a kidney does, it must be repeated roughly three times every week, for years, until either a transplant or death. That cadence — four hours, thrice weekly, indefinitely — is the single fact that governs everything: the travel burden, the recurring cost, the chair-utilization math, and the terrifying consequence of any lapse in sterility. A business selling this is really selling a subscription to survival, and its customers cannot churn without dire alternatives.

The scale of the underlying demand is staggering and worsening. India is often called the diabetes capital of the world, and diabetes and hypertension are the two great feeders of chronic kidney disease. The pool of patients who need dialysis runs into the hundreds of thousands and grows every year, yet only a fraction ever receive adequate treatment. That gap between need and access — enormous, structural, and expanding — is the demand backdrop against which the entire NephroPlus story unfolds.

The pre-2010 Indian dialysis market was split into two unappealing halves. On one side sat the high-cost private corporate hospitals, clustered in Tier-1 metros, charging on the order of ₹3,000–4,000 per session. For a family living on a few hundred rupees a day, that was simply impossible — and it was per session, several times a week, forever. On the other side sat a scatter of unregulated standalone "mom-and-pop" clinics, which were affordable precisely because they cut the corners that kept patients alive.

And here is the part that should make you wince. Dialysis involves running a patient's entire blood volume through an external filter — the dialyzer — many times over. If water purity, sterilization, or the reuse of dialyzers is not obsessively controlled, the machine becomes a superhighway for blood-borne infection. In poorly run Indian centers of that era, cross-infection with Hepatitis B and Hepatitis C was rampant, with infection rates in some multi-reuse centers reported to run extraordinarily high. A patient could walk in for a life-saving treatment and walk out with a life-shortening virus. The "cheap" option was frequently lethal on a delay.

Layer on the geography and the picture gets worse. The overwhelming majority of kidney-disease patients live in Tier-2, Tier-3, and rural India, while the overwhelming majority of dialysis machines were concentrated in Tier-1 cities. That mismatch forced the twice-weekly, hundred-kilometer pilgrimages, and unsurprisingly it produced brutal drop-out rates — patients who simply stopped coming and died within months of diagnosis, defeated by logistics rather than biology.

The economic imperative. For India's lower-middle class, kidney disease was — and largely remains — a financial catastrophe. Health insurance penetration was thin, most spending was out-of-pocket, and the relentless cadence of dialysis drained household savings until there was nothing left. This is the crucial backdrop for everything that follows: NephroPlus was not entering a mature market and competing on price. It was entering a vacuum, where the real competition was not another chain but the twin failures of unaffordability and unsafety. The prize for whoever could deliver standardized, safe, affordable dialysis at scale was enormous — but "at scale" was exactly the problem, because building dialysis centers the traditional way was ruinously expensive. Solving that capital problem is where the real business innovation begins.

IV. Crucial Pivot: Inventing the Asset-Light "Shop-in-Shop" Model (0:50 – 1:15)

Here is the trap that had kept Indian dialysis fragmented for decades. A single dialysis center is a surprisingly capital-hungry thing to build. You need real estate in a location patients can reach. You need a specialized reverse-osmosis water-treatment plant, because ordinary tap water will poison a dialysis patient. You need medical-gas lines, backup power, dialysis machines at lakhs of rupees each, and a trained clinical staff. Sink all that capital into a greenfield clinic and you wait years to fill the chairs and earn it back. Build them one at a time and you will still be a regional player when your grandchildren retire. The math simply does not allow a standalone-clinic chain to scale quickly. That was the wall every would-be consolidator hit.

NephroPlus walked around the wall instead of through it. Its central insight — the "Shop-in-Shop," or SIS, model — was to stop building the shops at all and instead move into shops that already existed. The company partnered directly with existing private and corporate hospitals, from large chains to regional groups, and set up dialysis units inside them.

The division of labor was elegant. The hospital contributed the physical space, the electricity and water, the location, and — most valuable of all — immediate access to its own flow of patients and its brand credibility. NephroPlus brought everything specialized: it installed the machines, imported and managed the consumables, hired and trained the technicians, and ran the unit day-to-day under strict, standardized clinical protocols. The patient got a NephroPlus-quality dialysis experience inside a hospital they already trusted.

Why would a hospital hand over a department like this? Because for most hospitals, dialysis is a headache, not a jewel. It is operationally fiddly, requires specialized staff and water engineering, runs on thin margins, and generates none of the glamour or profit of surgery, ICU beds, or transplants. It is, in the language of retail, a loss-leader — something you offer because patients need it, not because it makes money. Outsourcing it to a specialist freed the hospital's management bandwidth and capital for the high-margin work it actually wanted to do, while still keeping dialysis available under its roof. For the hospital, it was found money and one fewer problem.

There is a subtler reason the hospital could hand this off cleanly: the genuinely hard parts of dialysis are invisible to the casual observer. The most dangerous variable in the whole process is water. A dialysis patient is exposed to hundreds of liters of water across a week — vastly more than they would ever drink — and if that water carries bacterial contamination or the wrong mineral balance, the consequences run from chronic illness to death. Running a dialysis unit therefore means running an industrial-grade reverse-osmosis water plant and testing it obsessively, mastering sterilization protocols, and managing the safe reuse of dialyzers. This is specialized process engineering dressed up as a hospital department, and it is exactly the kind of thing a generalist hospital does poorly and a focused operator does well. NephroPlus's edge in the Shop-in-Shop model is not that it owns machines — anyone can buy a machine — but that it industrializes the unglamorous safety infrastructure and enforces it identically across hundreds of sites. That standardization is both the source of its clinical reputation and, as we will see, the single point of failure that could undo it.

The model also created optionality the company is only now beginning to exploit. Once you have built a machine to standardize dialysis outside a hospital, the logical frontier is to push it all the way into the patient's home — a higher-margin, premium service for those who can afford convenience and want to escape the thrice-weekly commute to a center entirely. Home dialysis remains a small line today, but it is the natural upmarket extension of the same asset-light logic, and management has flagged it as a growth avenue worth watching.

For NephroPlus, the model was transformative. It stripped out the two slowest, riskiest, most capital-intensive parts of building a clinic — real estate and patient acquisition — and let the company add capacity at a fraction of the cost and time of a greenfield build. Machines started paying themselves back far faster because they walked into an existing patient pool rather than waiting for one to form. Marketing risk largely evaporated. This is the origin of the "asset-light" descriptor that follows the company everywhere: NephroPlus owns the clinical expertise, the supply chain, and the brand, but leans on partners for the bricks.

It is worth being clear-eyed about the trade-off, because asset-light is not free. Sharing a roof means sharing economics — the hospital takes its cut — and it means NephroPlus's fate at any given site is partly tied to a landlord it does not control. A partner hospital that changes strategy, gets acquired, or sours on the relationship can put a clinic at risk. The model buys speed and capital efficiency at the price of some control and some margin. But in a market starved for safe capacity, speed was worth almost any price. And there was an even larger, even faster source of volume waiting — this time with the government writing the checks.

V. The Public-Private Partnership (PPP) Growth Engine (1:15 – 1:35)

In 2016, the Indian government did something that would reshape the economics of dialysis nationwide: it launched the Pradhan Mantri National Dialysis Programme, a scheme to provide free dialysis to poor patients in public district hospitals. For a company like NephroPlus, this was a firehose of demand pointed directly at the population it had been trying to reach all along — the Tier-2, Tier-3, and rural patients who could never afford private care.

The public-private partnership model works like the Shop-in-Shop's governmental cousin. NephroPlus (and its competitors) bid to run dialysis centers inside government district hospitals across states such as Andhra Pradesh, Telangana, and Uttarakhand. The government provides the space and guarantees payment at a capped, tendered rate per session; NephroPlus supplies the machines, consumables, technicians, and management, and treats patients — often entirely free at the point of care, with the state footing the bill.

The upside is scale of a kind the private model alone could never deliver. PPPs took NephroPlus into remote districts, filled its machines with high volumes of government-funded patients, and spread its fixed clinical overhead across a vastly larger treatment base. Every incremental treatment on an already-staffed machine is highly efficient, so volume at a capped price can still be worth having. And there is a mission dimension that matters to the company's identity and its investor story alike: PPPs are how NephroPlus reaches millions of low-income patients who would otherwise go untreated.

The downside is written into the same contract. Capped tender rates mean structurally thin margins — this is high-volume, low-price work by design. Dependence on state fiscal budgets introduces political and budgetary risk: a cash-strapped state can delay, renegotiate, or fail to renew. And the single most dangerous feature is the receivable cycle. Government bodies are notoriously slow payers; receivables on PPP contracts can stretch to 180, even 360 days. That means NephroPlus must fund months of consumables, salaries, and overhead out of its own pocket before the state reimburses it — a working-capital drag that can strangle an under-capitalized operator no matter how many patients it treats.

The mechanics of these contracts reward exactly the capabilities NephroPlus spent a decade building. A state issues a tender specifying the districts to be served, the machines required, and a fixed price per session; operators bid, and the low, credible bidder wins a multi-year mandate to run centers across a cluster of hospitals. Winning profitably at a capped price is only possible if your per-treatment cost is genuinely lower than a rival's — which loops straight back to the consumables-sourcing advantage and the in-house technician pipeline. In other words, the same scale that makes the private business profitable is what makes the government business survivable. A small operator can win a PPP tender by bidding aggressively, but it will often bleed to death fulfilling it, because it lacks the cost structure and the balance sheet to carry both thin margins and long receivables. This is why the PPP channel, despite its low headline margins, quietly reinforces the leader's dominance: it is a game that punishes the undercapitalized, and NephroPlus is the best-capitalized player in the room.

This is the strategic tension at the heart of the PPP engine, and it is one an investor should watch closely. Volume flatters the top line and utilization metrics; it does far less for margins and can actively hurt cash flow. A company can be busy, growing, and celebrated for its social impact while its balance sheet quietly bleeds working capital to the government. The only sustainable way to run this game is to have a low cost of capital and a robust balance sheet — precisely the things a successful IPO is meant to provide. So the PPP segment is best understood not as a profit center but as a volume-and-mission engine that must be funded and disciplined by profits earned elsewhere. Which raises the obvious question: where does the real profit come from? The answer is a moat so unglamorous that it is easy to miss — the economics of buying in bulk.

VI. Scale Economics: Hamilton Helmer's 7 Powers in Action (1:35 – 2:00)

If you want to understand why NephroPlus makes money and a corner dialysis clinic does not, forget the branding and the Olympiads for a moment and look at the invoice for consumables. Every dialysis treatment burns through a kit of single-use and reusable supplies: the dialyzer (the filter itself), the blood tubing lines, the acid and bicarbonate concentrates, the disinfectants. Across a network doing millions of treatments a year, consumables are the single largest operating-cost block. Control that number and you control the P&L. This is where NephroPlus's real moat lives, and it maps almost perfectly onto Hamilton Helmer's framework of durable competitive "powers."

Scale economies — the bilateral sourcing engine. The core power is embarrassingly simple: when you buy dialyzers by the millions, you pay far less per unit than a clinic buying them by the hundreds. NephroPlus centralizes procurement across its entire network and negotiates directly with the global giants of the industry — companies such as Fresenius Medical Care and Nipro — and increasingly commissions white-label contract manufacturing of its own proprietary consumables. The evidence that this works shows up cleanly in the disclosed numbers: consumables fell from roughly 32.6% of operating revenue in FY23 to about 25.7% in FY25, and further toward 23% in the first half of FY26.47 That roughly ten-percentage-point swing, on the largest cost line in the business, is most of the story of how the company's margins expanded. A small standalone clinic — including, tellingly, a smaller regional SME peer — simply cannot summon that purchasing leverage. It pays near list price and lives on whatever is left.

The analytical point worth underlining: this is a genuine structural advantage, not an accounting artifact or a one-off price cycle. It compounds — the bigger the network, the better the terms, the lower the cost, the more competitive the pricing, the more the network grows. That flywheel is the closest thing in Indian dialysis to a self-reinforcing moat.

This is also the cleanest place to cash in the "Two Nephros" distinction we drew at the outset, because the contrast is illuminating rather than merely a naming quirk. Nephro Care India Limited — the Kolkata-based SME whose ticker sits atop this article — is a perfectly real dialysis business, but at a fraction of the scale, revenue in the tens of crores rather than the hundreds, and a regional rather than national footprint. It is not a smaller version of NephroPlus so much as a demonstration of what the absence of scale looks like: without national purchasing volume, it pays closer to list price for the same dialyzers and concentrates; without an in-house academy, it competes for technicians in the open market; without a dollar-denominated international segment, it lives entirely at the mercy of domestic pricing. Two companies, nearly identical names, the same clinical service — and radically different economics, separated almost entirely by scale. For an investor, the pair is a live case study in why, in a consumables-heavy service business, size is not a vanity metric but the whole ballgame.

Switching costs. Once a patient settles into a NephroPlus center, leaving is genuinely risky. They have built trust with specific technicians who know their vascular access, their tolerances, their history. A new provider means unfamiliar hands, unknown water quality, and a real, non-trivial infection risk during the transition. For a treatment done thrice weekly for years, that stickiness is powerful, and it is why patient churn tends to be low once a relationship is established.

Counter-positioning. A traditional corporate hospital cannot easily become NephroPlus without dismantling the very reasons it outsourced dialysis in the first place. To compete head-on it would have to rebuild a specialized consumables supply chain, a separate clinical operating structure, and a dedicated training pipeline — a lot of low-margin effort to reclaim a department it was glad to hand away. The incumbent's own economics discourage it from copying the challenger.

Cornered resource — Enpidia Academy. Here is the constraint nobody outside the industry appreciates: the binding bottleneck in Indian dialysis is not machines or money, it is trained technicians. Certified dialysis technicians are scarce, slow to train, and easily poached. NephroPlus's answer was to build its own training school, the Enpidia Academy, which feeds a steady stream of technicians directly into its network of 500-plus clinics.14 It is a closed-loop labor supply — the company manufactures the very input everyone else is fighting over. In Helmer's terms, that is a cornered resource, and in practical terms it is what lets NephroPlus keep opening clinics while competitors stall for want of staff.

Process power and brand. There is a fifth advantage that is easy to underrate: the accumulated operational know-how of running hundreds of clinics to an identical standard, and the brand trust that flows from it. In a market where the alternative was once a coin-flip on catching Hepatitis, "NephroPlus" came to mean a credible promise of safety — and in healthcare, a trusted brand is not vanity, it is a demand magnet that lowers patient-acquisition cost and gives partner hospitals a reason to want the name on the door. This power is quieter than the others and harder to measure, but it is the reason a patient chooses a NephroPlus unit over an unbranded clinic across the street even at a similar price. The emerging extension of this is vertical integration into proprietary, white-label consumables — if NephroPlus can increasingly manufacture or contract-manufacture its own dialyzers and concentrates rather than buying them from Fresenius or Nipro, it captures the supplier's margin on top of its own. That shift is still early and unproven at scale, and it introduces its own manufacturing and quality-control risks, but it is the logical next move for a company whose single biggest cost is the thing it currently buys from others. Watch whether the proprietary-consumables share of its supply actually rises; it is the clearest signal of whether the sourcing moat is deepening or merely holding.

Put those powers together and you have a business that is cheaper to supply, harder to leave, awkward to copy, and self-sufficient in scarce labor. That is a real competitive position. But every one of these powers has a domestic ceiling — Indian pricing is regulated, competitive, and capped — which is precisely why management looked abroad for the next leg of growth.

VII. The International Blueprint & M&A Strategy (2:00 – 2:20)

Walk into the dialysis center NephroPlus built in Tashkent and the first thing that strikes you is the sheer scale: 160 machines arrayed in one facility, among the largest such centers anywhere in the world, in a country most Indian healthcare companies would never think to enter. That a Hyderabad dialysis chain came to operate one of the planet's biggest dialysis centers in Uzbekistan is not an accident of ambition — it is the logical endpoint of a hard financial constraint back home.

The uncomfortable truth about the Indian dialysis market is that being the best operator in it does not let you charge like one. Between PPP rate caps, price-sensitive patients, and competition, domestic pricing has a low ceiling. A treatment that a payer in a richer country might reimburse at a hundred dollars fetches a fraction of that in India. So if you have built the region's best dialysis operating machine, the logical move is to point it at markets where the same treatment earns more. That is the entire strategic rationale for NephroPlus's international push.

Uzbekistan — the proof of concept. The company's Central Asian entry came through a landmark deal: it won Uzbekistan's first major healthcare public-private partnership, a project structured with the help of the International Finance Corporation and financed by the Asian Development Bank.89 In April 2023, ADB signed a financing package of up to $8.39 million with the company's local entity, Nephrocare Health Services Central Asia — comprising a loan of up to $5.03 million from ADB's own resources and up to $3.36 million administered from the Leading Asia's Private Infrastructure Fund.8 Under the arrangement, NephroPlus designed, built, and now operates four dialysis centers in Tashkent city, the Republic of Karakalpakstan, and the Khorezm region.8 The flagship Tashkent facility was built with 160 dialysis machines, making it one of the largest single dialysis centers in the world, and all four centers became operational, serving well over a thousand patients a year including, for the first time in Uzbekistan, home-based peritoneal dialysis for remote patients.9

Why does Uzbekistan matter so much more than its size suggests? Because it validated a repeatable template: a government-guaranteed, multi-year, hard-currency revenue stream at pricing materially above Indian levels, won on the strength of NephroPlus's operating credibility and blessed by multilateral institutions. It is the PPP model the company already knew — but denominated in dollars and priced for a market that pays more.

The Philippines — the inorganic roll-up. If Uzbekistan was greenfield done carefully, the Philippines was the opposite playbook: buy what already exists. Rather than wait years for greenfield regulatory approvals, NephroPlus moved to consolidate a fragmented Philippine dialysis market by acquiring operating clinics outright. Through 2025 and into 2026 it strung together a series of deals — acquiring Renal Therapy Solutions and adding clusters of clinics across the archipelago13 — and in June 2026 it crossed a symbolic threshold, opening its 50th Philippine clinic in Orion, Bataan, with a stated ambition to keep adding roughly 15–16 clinics a year.11 The individual transactions were modest in size: dialysis-center assets in Paranaque City for about PHP 32.64 million (roughly ₹5 crore),10 and further assets, such as those from Pag-Asa Dialysis and Diagnostic Center, agreed in June 2026 for about PHP 80.64 million.12

Did they overpay? This is the question a disciplined investor should ask of any roll-up, because acquisition sprees are where empire-building masquerades as strategy. On the disclosed logic, the Philippine deals look reasonable rather than reckless: management has framed the assets as acquired at mid-single-digit multiples of historical EBITDA, and the arithmetic that makes them attractive is the revenue gap — average revenue per treatment in the Philippines runs far above India's, so a clinic bought at an Indian-style multiple but earning Philippine-style revenue should pay itself back quickly, on the order of a few years rather than the longer horizon of a domestic greenfield build. Buying existing clinics also means buying existing patients and existing real estate, skipping the two slowest parts of the build. The strategy is coherent. The caveat is equally clear: a rapid cross-border roll-up of small, previously independent clinics is an integration and clinical-governance test, and the risks — inconsistent standards, cultural friction, quality control at a distance — are real and will only show up in the numbers later. For now, the international thesis is promising and partly proven, not yet fully earned.

It is worth applying a skeptic's discount to the international margin story specifically, because "higher revenue per treatment" is not the same as "higher profit," and the gap between them is where cross-border ambitions often disappoint. Operating in Uzbekistan and the Philippines means absorbing local wage inflation, unfamiliar regulatory regimes, and — crucially — currency exposure. A dollar-pegged Uzbek contract looks wonderful until you remember that costs are partly in local currency and profits must eventually be repatriated across volatile exchange rates and differing tax regimes. The multilateral backing from the IFC and ADB mitigates political risk in Central Asia, but it does not eliminate the operational reality that running clinics thousands of kilometers from Hyderabad, in languages and legal systems the founding team did not grow up in, is materially harder than opening the next clinic in Andhra Pradesh. The international segment is the most exciting part of the equity story and also the part with the least track record and the widest error bars. Investors should treat its rich reported margins as a promise the company is still in the early innings of keeping.

What the international push has already begun to do, though, is bend the company's financial trajectory — and that trajectory is dramatic.

VIII. Financial Breakdown & Turning the Profit Corner (2:20 – 2:40)

For most of its life, NephroPlus was the classic Indian growth company: expanding furiously, admired widely, and losing money. The interesting part of the financial story is the moment that changed — the corner where scale finally overwhelmed cost and the business flipped from cash-burning to cash-generating.

Start with the top line, which tells the growth story plainly. Consolidated revenue climbed from roughly ₹437 crore in FY23 to about ₹566 crore in FY24 and then to ₹755.8 crore in FY25 — a compound annual growth rate in the neighborhood of 31–32% over two years.37 Of that FY25 revenue, domestic operations contributed about ₹515.5 crore and international operations about ₹240.3 crore,3 which tells you how quickly the overseas push has scaled: international is no longer a rounding error but roughly a third of the top line.

Now the part that matters more — profitability. EBITDA rose from around ₹48.6 crore in FY23 to roughly ₹100.9 crore in FY24 and about ₹166.6 crore in FY25,7 and the EBITDA margin roughly doubled, from about 11.1% in FY23 to about 22.0% in FY25.37 We have already met the two engines behind that doubling: the collapse in consumables cost as a share of revenue, and a geographic mix tilting toward higher-priced international treatments. The result was the headline event of the financial story — the profit turnaround. NephroPlus went from a net loss in FY23 to a net profit of ₹67.1 crore in FY25, nearly doubling from about ₹35.1 crore the year before.3 The company was, at last, demonstrably profitable rather than merely promising.

The right way to read this is with both eyes open. On one hand, doubling EBITDA margin while growing revenue at 30%-plus is genuine operating leverage — evidence that the model scales, not just grows. On the other, a two-year run of margin expansion driven partly by a favorable mix shift is not a law of nature; consumables cannot fall as a share of revenue forever, and the international margin premium invites competition and, eventually, regulatory attention. The turnaround is real. Its durability is the open question.

There is also a gap that every investor should insist on interrogating: the distance between reported profit and actual cash. A dialysis network of this kind is capital-intensive at the edges — machines wear out and must be replaced, new clinics must be fitted out, water plants maintained — and, as we saw, the PPP business ties up cash in slow government receivables. Reported EBITDA and net profit are genuine achievements, but they flatter the picture relative to free cash flow, which is why the company used a meaningful chunk of its IPO proceeds to pay down debt rather than to fund an acquisition spree. The honest way to hold this business in your head is that it has proven it can generate accounting profit; it has not yet proven, over a full cycle, that it can convert that profit into abundant free cash while simultaneously funding growth and carrying government receivables. That conversion — not the growth rate — is the real test of whether NephroPlus is a compounder or a capital sink dressed as one.

The segment texture matters because the blended numbers hide very different businesses. Broadly, the domestic private Shop-in-Shop and standalone clinics are the cash cow — the largest revenue share at healthy margins. The domestic PPP business is high-volume but thin-margin and working-capital-hungry, as we saw. And the international segment, though still the smallest slice, carries by far the richest margins and the fastest growth, which is exactly why management treats it as the future engine of consolidated profitability. An investor's mental model should therefore not be "a dialysis company growing at 30%" but rather "three quite different businesses stapled together, whose blended margin depends heavily on how fast the richest slice grows relative to the thinnest."

Utilization is the operating heartbeat underneath all of it. Across its network of 500-plus clinics, average machine utilization ran in the mid-70s percent,4 and management has said it deliberately caps utilization around 85% to preserve safety buffers and avoid staff burnout — a revealing choice, because it means the company is intentionally leaving some revenue on the table in exchange for clinical safety and staff retention. That is either admirable discipline or a self-imposed ceiling, depending on your temperament; for a business whose ultimate risk is a fatal infection outbreak, erring toward the safety buffer is defensible. All of which brings us to the people making these trade-offs, and whether their incentives line up with yours.

IX. Management, Governance, and Capital Allocation (2:40 – 2:50)

A dialysis company is, in the end, a trust business wearing a healthcare uniform, and trust starts at the top. The reassuring feature of NephroPlus's leadership is that the founders never left. Vikram Vuppala remains the strategist and chief executive; Sandeep Gudibanda remains in senior operational leadership; and — crucially — Kamal Shah still leads Patient Services, the function that keeps the company's clinical protocols anchored to the patient's actual experience rather than a spreadsheet's. That last detail is not sentimental. It is a governance signal: the person with the strongest personal stake in never harming a dialysis patient is the person overseeing how patients are treated.

Shareholding and alignment. By the time of the IPO, this was no scrappy startup cap table. The promoter group had grown to include Vikram Vuppala alongside a roster of institutional backers — Bessemer Venture Partners, Investcorp entities, and related holding vehicles — with the International Finance Corporation and 360 ONE among the other significant shareholders.14 Pre-IPO promoter holding stood near 78.9%, declining to about 71.49% after the issue.14 The presence of a development-finance institution like the IFC on the register is worth pausing on: it brings not just capital but a governance and clinical-standards expectation, and it aligns naturally with the company's stated mission of expanding access. The flip side of a cap table this heavy with private-equity and venture investors is the obvious one — financial sponsors eventually want liquidity, and the offer-for-sale portion of the IPO was where some of them began to take it.

To understand how the register got this crowded, it helps to trace the fifteen-year capital journey behind it, because it explains both the company's firepower and the pressure now sitting on the stock. NephroPlus was never a bootstrapped operation — it raised a total of roughly $205 million across thirteen funding rounds from more than thirty investors, beginning with its first round back in 2010.16 The pattern is the familiar one for capital-hungry Indian healthcare: successive private rounds funding the land-grab, with Bessemer and the IFC as long-term anchors. In 2021, the company raised about $24 million (roughly ₹180 crore) in a Series E round led by IIFL Asset Management alongside existing backers.16 Then came the pivotal Series F in May 2024 — a roughly $103 million round led by Singapore-based Quadria Capital that valued NephroPlus at more than ₹2,000 crore and, tellingly, allowed Investcorp to take a partial exit while Quadria stepped in.17 That transaction is the tell an investor should register: private-equity ownership in this business has been changing hands and seeking liquidity for years, and the December 2025 IPO was the natural next station on that line, not a bolt from the blue. The presence of sophisticated healthcare investors who have repeatedly re-underwritten the company at rising valuations is a point in the bull's favor; the equally clear reality that those investors are in the business of eventually selling is a point the bear will keep on the table.

The IPO and capital allocation. The December 2025 listing was a ₹871.05 crore book-built issue: a fresh issue of ₹353.4 crore plus an offer for sale by existing shareholders, priced in a band of ₹438–460 per share on a ₹2 face value.215 The market's reception was polite rather than euphoric — subscription was muted on the first day before filling out,14 and the stock listed on December 17, 2025 at ₹490 against the ₹460 upper band, a listing gain of roughly 6.5%.15 That tepid-but-positive debut is itself a useful data point: the market liked the business but was not willing to pay a fantasy multiple for a capital-intensive, working-capital-heavy healthcare operator, however fast-growing.

What matters more than the pop is where the fresh money went. The company earmarked roughly ₹136 crore of proceeds for repaying or pre-paying borrowings and about ₹129 crore for capital expenditure on new clinics,1 with the balance for general corporate purposes. Read plainly, that is a deleveraging-and-growth allocation: pay down debt to relieve the working-capital strain that the PPP model imposes, then fund domestic clinical expansion — while steering strategically away from slow, capital-heavy greenfield builds and toward the asset-light hospital partnerships and discounted international acquisitions we have already discussed. It is a coherent, disciplined use of proceeds on paper. The test, as always, is execution over the next several years — whether debt actually falls, whether the acquisitions integrate, and whether management resists the roll-up temptation to keep buying simply because it can.

On management credibility, an honest assessment has to acknowledge how little public track record exists to judge. As a company that listed only in December 2025, NephroPlus has not yet stood before public-market investors through a full cycle of quarterly guidance, missed targets, and the explanations that follow — the raw material from which credibility is actually built or destroyed. What can be said is that the founding team has stayed intact and operationally engaged across fifteen years and multiple private funding rounds, that sophisticated healthcare investors repeatedly re-underwrote the business at rising valuations, and that the pre-IPO strategy narrative — asset-light domestic scaling, PPP volume, international margin expansion — has been broadly consistent across its filings and its actions. Those are encouraging signs, not proof. The real diligence begins now, on the public earnings calls to come: whether management sets specific targets and hits them, whether it explains misses candidly rather than blaming the weather or the government, and whether the disciplined-capital-allocation language of the prospectus survives contact with the temptation of cheap acquisitions and a rising share price. Sophisticated investors will be listening for concrete answers, and the first few quarters of transcripts will tell them more than any glossy IPO document could. Which is the perfect place to hand the microphone to the skeptics.

X. Risk Radar & Activist/Skeptical Investor Stress Test (2:50 – 3:00)

Every compelling growth story deserves a hostile cross-examination, and NephroPlus offers a skeptical investor plenty to work with. Let's put the bear in the room and let it talk.

The working-capital drag — the balance-sheet threat. We flagged it in the PPP discussion, but it belongs at the top of the risk list because it is structural, not hypothetical. State-government contracts pay late — sometimes very late — and a company funding months of consumables and salaries before reimbursement is one budget crisis away from a cash squeeze. A sharp lengthening of receivable days from Indian states could force NephroPlus to lean on expensive working-capital facilities, converting an accounting problem into a real one. An activist would zero in here and ask a pointed question: how much of the celebrated growth is profitable cash and how much is receivables the company is effectively lending to the government at zero interest? The answer determines whether the PPP engine is an asset or a liability.

The infection tail risk — the existential threat. This is the risk that could end the company rather than merely dent it. The entire enterprise rests on a promise: come to NephroPlus and you will be dialyzed safely. A single high-profile cross-infection outbreak — Hepatitis B or C, or HIV — traceable to technician error, a water-system failure, or a sterilization lapse would be catastrophic in a way that transcends any one clinic. It would shatter the brand equity built over fifteen years, invite heavy regulatory penalties, and give every partner hospital a reason to cancel its Shop-in-Shop agreement overnight. This is the low-probability, ruinously-high-severity event that management's 85% utilization cap and centralized protocols are explicitly designed to prevent — and it is precisely why those safety choices, which cost margin, are rational rather than timid.

Technician attrition — the labor threat. The Enpidia Academy is a genuine advantage, but it is a pipeline, not a fortress. Skilled dialysis technicians and nurses are in global demand, and the wage gap between India and Western Europe or the Gulf is a powerful magnet. If emigration and poaching accelerate faster than the academy can graduate replacements, labor costs spike, quality risk rises, and the very moat that lets NephroPlus keep opening clinics narrows. The company is, in a sense, training staff for the world; the risk is that the world hires them away.

Supply-chain concentration — the hardware threat. NephroPlus does not manufacture dialysis machines. It depends on a small number of German and Japanese suppliers — Fresenius, Nipro, and their peers — for the core hardware. Bulk-buying gives it pricing leverage on consumables, but on the machines themselves it is a price-taker exposed to supply disruptions, currency moves, and tariff changes on imported medical equipment, any of which could inflate capital budgets at exactly the wrong moment.

The regulatory-pricing threat — the margin ceiling. India's government is not a passive payer; it is an active price-setter with both the tools and the political incentive to squeeze. Whether through the tender rates on public schemes or broader price-control mechanisms on medical services and devices, a decision to cut reimbursement in the name of affordability would land directly on NephroPlus's most defensible domestic margins. This is the uncomfortable inverse of the company's social-good story: the very fact that dialysis is essential and that the state is the largest ultimate payer makes it a natural target for populist price intervention. An operator cannot easily pass such cuts on to patients who have no money and no alternative, so the hit flows straight to the P&L. It is precisely because this risk is real that management's international pivot toward dollar-priced, contractually guaranteed revenue is strategic rather than opportunistic — it is a deliberate hedge against the political economy of its home market.

Add to these the softer governance questions an activist would raise — a private-equity-heavy register with sponsors seeking exits, an accelerating cross-border acquisition pace that could outrun clinical oversight, and a founder-dependent culture — and you have a serious, if not disqualifying, risk ledger. None of these is a reason the story fails; each is a reason to watch it closely. The point of the stress test is not to reach a verdict but to know exactly what would falsify the bull case. With the risks named, we can distill what the whole saga actually teaches.

XI. The Playbook: Durable Business & Investing Lessons (3:00 – 3:10)

Strip away the specifics of kidneys and clinics, and the NephroPlus story leaves behind a few transferable lessons that apply well beyond dialysis.

Lesson 1: Outsource the low-margin, complex friction — and it can become someone else's high-margin machine. The Shop-in-Shop model worked because one company's headache is another company's specialty. A hospital's operationally miserable, thin-margin dialysis department became, in the hands of a focused operator with scale and standardized protocols, an asset-light compounding engine. The general principle: when an industry is full of players doing something reluctantly and badly, there is often a business to be built by doing that one thing obsessively well and taking it off everyone else's hands. The value is created not by inventing something new but by unbundling and specializing.

Lesson 2: Lived customer experience is a moat that spreadsheets cannot reverse-engineer. NephroPlus's cultural differentiation traces directly to a founder who was himself the customer. That empathy, translated into standard operating procedures — the bright centers, the technician training, the insistence that patients can live full lives — produced retention that a corporate competitor with more capital struggles to replicate, because it cannot fake the source. The investing takeaway is to look for companies whose customer-facing advantage is rooted in genuine, hard-to-copy understanding rather than marketing spend, while remembering the corresponding fragility: advantages tied to specific founders carry key-person risk.

Lesson 3: In emerging-market services, centralized procurement is where margins are won or lost. The single most important number in this entire story was not revenue growth or clinic count — it was consumables as a percentage of revenue, and its steady decline as scale kicked in. For any service business built on a repeated, consumable-heavy transaction, the transition of the biggest variable cost from a price you accept into a price you dictate is often the whole margin story. Build the centralized purchasing muscle early, before you need it, because it is the flywheel that turns scale from a vanity metric into a profit engine.

There is a meta-lesson threaded through all three, worth naming because it is where NephroPlus is genuinely instructive for anyone studying emerging-market healthcare. The company did not invent dialysis, did not invent the machines, and did not invent the government scheme that funds much of its volume. What it did was assemble ordinary, available ingredients — hospital partnerships, bulk procurement, a training school, standardized protocols — into a system that no single competitor had bothered to build at national scale. Competitive advantage in a fragmented, essential-service market often comes not from a breakthrough but from the patient, unglamorous work of standardizing and scaling something everyone else does badly. That is a less exciting story than a technology moonshot, but for a fundamental investor it is frequently a more durable one, because operational excellence compounds quietly and is far harder to disrupt than a patent. The corresponding caution is that operational advantages, unlike patents or network effects, must be re-earned every single day at every single site — one negligent technician, one contaminated water system, and the reputation that took fifteen years to build can be lost in a news cycle.

These lessons are the durable residue of the story. But an investor lives in the present tense, so let's close by looking forward — at the case for and against, and the handful of numbers that will tell you which way it is breaking.

XII. Episode Outro, 3 KPIs to Watch, & Bull vs. Bear Case (3:10 – 3:20)

Let's war-game the future the way a long/short desk would, using the frameworks we have leaned on throughout.

First, know the battlefield. The Indian dialysis services market — worth on the order of half a billion dollars and growing toward roughly $0.9 billion by the end of the decade18 — is unusual in that the "organized" segment is small but rapidly consolidating, and NephroPlus is the runaway leader within it. Its competitors fall into three camps, and each competes on a different axis. The global giants — Fresenius Medical Care and B. Braun — bring manufacturing muscle, integrated supply chains, and deep clinical credibility, and they are strongest in hospital-based, higher-acuity units rather than the volume-scaled network game.18 DaVita, the American dialysis heavyweight, competes on premium quality in metros and Tier-1 cities but runs a far smaller Indian footprint.18 And then there are the regional and physician-led players — Apex Kidney Care, strong in the south on nephrologist relationships and affordable pricing, alongside newer PPP-focused challengers such as DCDC Kidney Care.18 The strategic point is that no single competitor attacks NephroPlus across all three of its channels — private Shop-in-Shop, PPP, and international — at once. Its edge is not that it is the best at any one thing but that it is the only player operating the full board at national scale. That is a defensible position, but it is not an unassailable one: a well-capitalized global operator that decided to buy its way to Indian scale could compress the moat quickly, and the consolidation the sector is undergoing cuts both ways.

The bull case rests on the flywheel compounding. Through a Porter's Five Forces lens, NephroPlus sits in a structurally decent position: the threat of new entrants is blunted by the capital, technician-training, and clinical-trust barriers we have described; buyer power is fragmented across individual patients and standardized government tenders; and the company's scale gives it unusual leverage over its consumable suppliers. In Helmer's terms, it holds at least three real powers — scale economies in procurement, switching costs at the patient level, and a cornered resource in its training academy. If the bull thesis plays out, the international segment keeps growing its high-margin dollar revenue, consumables costs keep grinding lower through vertical integration and white-label manufacturing, and new premium lines such as home dialysis expand the addressable market upmarket. That is a company whose margins and returns on capital rise as it scales — the definition of a compounder.

The bear case is that the same forces cut the other way. The most acute competitive pressure comes not from rivals but from the government as a price-setter: a regulatory crackdown on pricing under public healthcare schemes could cap the domestic engine's economics permanently. Buyer power, in other words, is concentrated in a single, budget-constrained, politically motivated payer. Layer on the working-capital fragility of stretched PPP receivables, the execution and clinical-governance risk of a fast international roll-up, and the ever-present tail risk of an infection event, and the bear does not need the business to be bad — only for the margin expansion to stall and the cash conversion to disappoint. A company that grows revenue at 30% while its cash flow lags and its receivables balloon is not a compounder; it is a treadmill.

Which future is unfolding will not be visible in the revenue headline. It will show up in three numbers, and these are the ones worth tracking:

-

Average Revenue Per Treatment (ARPT). This is the cleanest read on whether the international and premium mix-shift — the entire margin thesis — is actually working. Rising ARPT means the higher-value geography and services are pulling their weight; flat or falling ARPT means the growth is coming from low-price volume that flatters the top line and little else.

-

Consumables cost as a percentage of revenue. The heartbeat of the bilateral-sourcing moat. As long as this keeps drifting down, the scale flywheel is intact. If it plateaus or reverses, the single most important margin engine has run out of road, and the multiple-doubling in EBITDA margin will not repeat.

-

PPP days sales outstanding (DSO). The truest measure of whether the government-volume engine is a strength or a slow leak. Stable or improving DSO means the working-capital risk is contained; a lengthening trend is the early warning that the balance sheet is financing the states — and the first place a cash squeeze would show. Watch it alongside overall operating cash conversion, because a growing company whose reported profit keeps outrunning its cash collection is telling you something the income statement alone will not.

Watch those three, and the rest of the story more or less narrates itself. NephroPlus has done the genuinely hard thing — it built the region's most sophisticated dialysis operating machine out of one of its most broken markets, and turned the corner from losses to real profit. Whether it becomes a durable compounder or a busy, capital-hungry grower depends on execution the numbers will reveal quarter by quarter. And through it all, it is worth remembering that the whole enterprise began not with a business plan but with an 18-year-old who refused to let a diagnosis write the end of his story — and then wrote a very different one instead.

References

-

NephroPlus IPO to open on Dec 10; check price band, issue size & other key details — Business Today, 2025-12-04 ↩↩↩↩

-

Nephroplus IPO Opens 10 Dec: ₹871 Cr Issue, Price ₹438-₹460 — HDFC Sky, 2025-12 ↩↩

-

Nephrocare Health Services Ltd — Consolidated Financials, Screener.in, 2026 ↩↩↩↩↩

-

IPO Note: Nephrocare Health Services Limited — GEPL Capital, 2025-12-09 ↩↩↩

-

How NephroPlus became India's largest dialysis chain — The Ken, 2025 ↩↩↩↩

-

Nephrocare Health Services Ltd — IPO Note, SBI Securities via Chittorgarh, 2025-12 ↩↩↩↩

-

ADB, NephroPlus Sign Loan for Dialysis Centers in Uzbekistan — Asian Development Bank, 2023-04 ↩↩↩

-

Uzbekistan: Dialysis PPP — International Finance Corporation, 2023 ↩↩

-

NephroPlus to acquire dialysis center assets in Paranaque City, Philippines — Business Standard, 2026-06-10 ↩

-

NephroPlus Philippines strengthens nationwide presence with 50 clinics — The Manila Times, 2026-06-24 ↩

-

Nephrocare Unit Acquires Philippines Dialysis Center Assets for PHP 80,640,000 — ScanX, 2026-06 ↩

-

NephroPlus Acquires Philippines Dialysis Center to Anchor Global Network Scale — Trade Brains, 2026-06-25 ↩

-

Nephrocare Health Services IPO: Public Issue Sees Muted Demand On Day 1 — Outlook Money, 2025-12 ↩↩↩

-

Nephrocare Health IPO Details 2026 — InvestorGain, 2025-12 ↩↩↩

-

NephroPlus — Funding Rounds & List of Investors, Tracxn, 2025 ↩↩↩

-

Investcorp announces partial exit from NephroPlus as Quadria Capital steps in — Investcorp, 2024-05 ↩

-

Dialysis Services Focused Insights Report 2024-2029 — Key Vendors: B. Braun, Baxter, DaVita, Fresenius Medical Care, NephroPlus — ResearchAndMarkets via Business Wire, 2024-10-02 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube