Neogen Chemicals: The Alchemist of India's EV Future

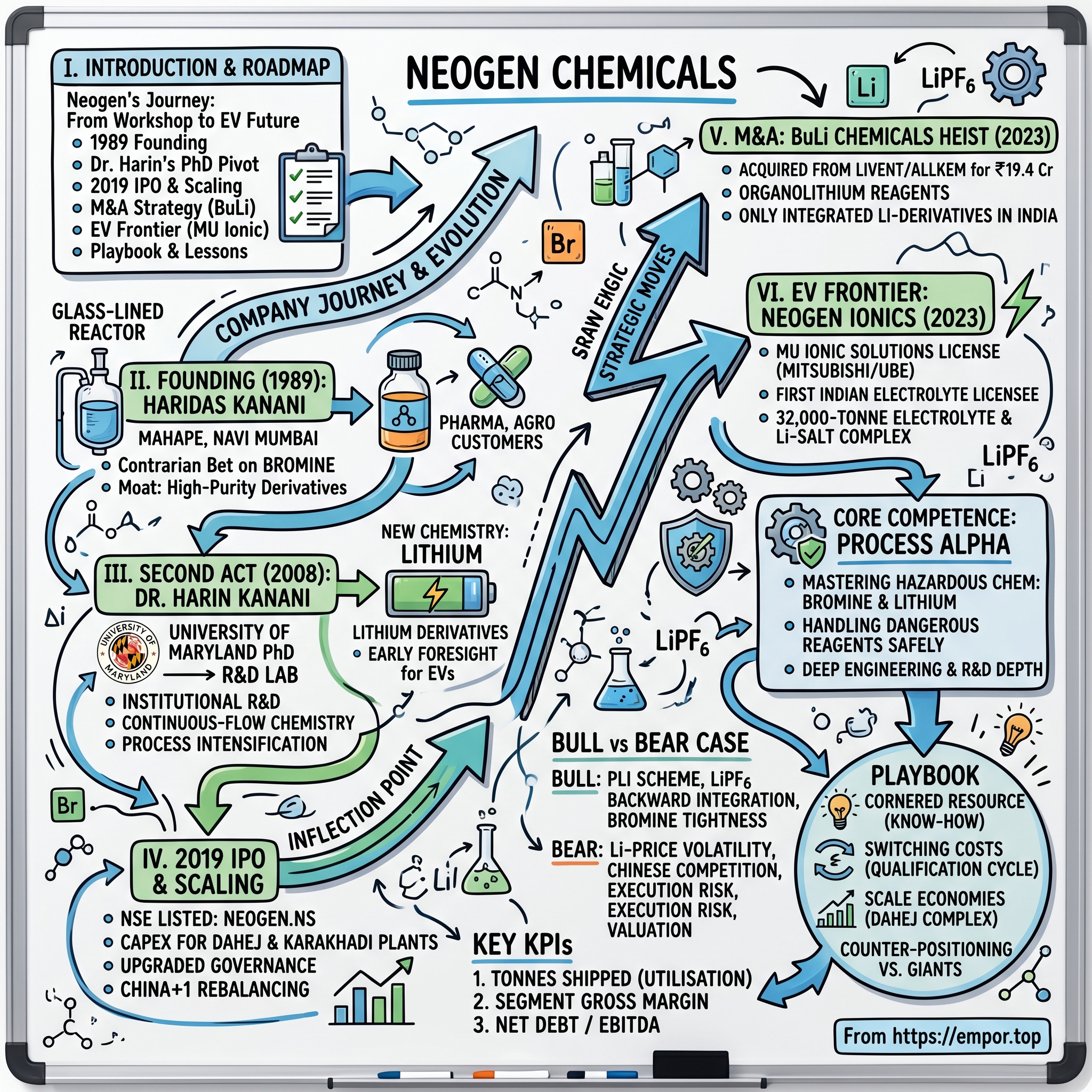

I. Introduction & Episode Roadmap

Picture a small, glass-lined reactor sitting in a workshop in Mahape, on the industrial outskirts of Navi Mumbai (नवी मुंबई), sometime in the late 1980s. Inside it, an amber liquid is sloshing gently—elemental bromine, one of the most corrosive, fume-spitting, skin-burning elements on the periodic table. Most Indian chemical entrepreneurs of that era would not touch the stuff. The Germans handled it. The Israelis dominated it. The Americans tolerated it. And in India, a quiet chemical engineer named Haridas Thakarshi Kanani (हरिदास ठाकरशी कनानी) decided he would master it.

That decision, taken when most of his peers were chasing easier money in dyes, agrochemicals, and bulk drugs, is the seed of an extraordinary multi-decade arc. Today, the company he founded—Neogen Chemicals Limited—is not just one of India's purest plays on bromine specialty chemistry. It is also the first Indian licensee of Japanese electrolyte technology from MU Ionic Solutions, a joint venture of 三菱ケミカル Mitsubishi Chemical and UBE Corporation, and it is building what could become the largest electrolyte and lithium salts complex on the subcontinent.[^1] Neogen, in other words, is quietly trying to become the chemical backbone of India's electric-vehicle dream.

The thesis of this episode is simple, but easy to miss if you only read the quarterly press releases. Neogen is not a "chemicals" story. It is a process alpha story—the rare ability to commercially master two notoriously hazardous chemistries, bromine and lithium, that scare almost everyone else off. Process alpha is what lets the company pivot from making pharma intermediates in 1989 to powering EV batteries in 2026 without changing its DNA. The reactors are the same. The hazard discipline is the same. The customer is just different.

The pivot itself reads like a chess move. In April 2023, Neogen signed a global technology license with MU Ionic Solutions Corporation for lithium-ion battery electrolytes—the first such grant ever given to an Indian company.[^2] A month later, in May 2023, it completed the acquisition of BuLi Chemicals India from Livent USA at a price that, as we'll see, looks in hindsight like the bargain of the decade.1 Then it incorporated a battery-materials subsidiary, Neogen Ionics, and started building electrolyte and lithium-salt capacity at multiples of anything that had existed in India before. The market noticed. The stock began trading at multiples reserved for energy-transition stories, not boring bromine.

So how did a father-son duo—one a self-made workshop chemist, the other a University of Maryland PhD—turn a corrosive, dangerous, unfashionable element into a ticket to India's EV supply chain? Where does the moat actually sit? Why did Livent sell BuLi for a song? And what does Neogen's 32,000-tonne electrolyte ambition tell us about the next decade of Indian specialty chemicals?

Here's the roadmap for tonight. First, we'll go back to 1989 and meet the original "Bromine Man of India" and understand why bromine is a moat that hides in plain sight. Then we'll bring in Dr. Harin Kanani (हरिन कनानी) and watch how a PhD pivoted a family-owned workshop into an institutional R&D-led enterprise. We'll relive the 2019 IPO, walk through the BuLi acquisition, decode the Mitsubishi electrolyte license, and stress-test the Neogen Ionics gigafactory bet against Hamilton Helmer's 7 Powers and Porter's 5 Forces. We'll end with the bull and bear cases, the KPIs that matter, and the central question—is Neogen really an "energy-material" company priced like an "energy-material" company, or is it still a specialty chemical company in disguise?

Strap in. This one travels from a 200-kg-a-month bromine workshop to a 32,000-tonnes-per-annum electrolyte ambition. The compound is different. The alchemy is the same.

II. The Founding: Haridas Kanani and the "Bromine Man" Era

The late 1980s in India were not a kind time to start a chemical company. The License Raj (लाइसेंस राज) was still alive, foreign exchange was rationed, and the bulk of "specialty chemicals" used in Indian pharma and agrochemical manufacturing was imported—from West Germany, Israel, the United States, and a rapidly industrialising China. For a chemical engineer with no political backing and no large family business, the path of least resistance was to become a small trader, or perhaps to make a low-margin commodity like soda ash. Almost nobody chose elemental bromine.

Haridas Kanani did. Trained as a chemical engineer, with a stubborn intellectual curiosity about why hazardous chemistry was always outsourced to "foreign" companies, he set up Neogen Chemicals in 1989. The first plant was at Mahape, in the new industrial belt of Navi Mumbai, and the first products were small-batch bromine derivatives—organic compounds in which a bromine atom is attached to a carbon backbone, useful as intermediates in pharma, agrochemicals, and later flame retardants.2

To understand why this was such a contrarian bet, you have to understand bromine itself. It is one of only two elements that is liquid at room temperature—the other being mercury. It is dense, deep red-brown, and breathes off corrosive vapour that attacks lungs, eyes, and almost any metal. Storing it requires glass-lined steel reactors, sealed pipework, and a fierce safety culture. Transporting it across India in the late 1980s was, frankly, terrifying. The result was a kind of negative selection: anyone who could avoid bromine, did. And so a small moat formed for whoever had the patience to learn it properly.

The Kanani household, by all accounts, was austere and engineering-obsessed. Haridas was the kind of founder who treated every reactor like a personal pet. Plant operators recall him on the shop floor late into the night, watching reaction temperatures, sniffing the vent gas (which is exactly as dangerous as it sounds) to check whether the run was on track. There was no MBA, no consulting deck. There was a notebook, a stopwatch, and an obsessive willingness to repeat a process two hundred times to nudge yield from 78% to 82%. In a country where most family businesses were built on trading or arbitrage, this was an unusual species: an Indian process company, run by a man who genuinely loved the chemistry.

By the mid-1990s, the small product list had expanded. Neogen had begun making advanced intermediates used in antiepileptic drugs, in agro actives, in photographic chemicals, and—crucially—in flavour and fragrance products where ultra-high purity is non-negotiable. The pivot to higher-purity, higher-margin grades was deliberate. Haridas had figured out something the textbooks did not say loudly enough: in bromine chemistry, the difference between 99.0% and 99.9% purity is not a 0.9% difference in selling price. It is often a 2x or 3x difference. Pharma customers and electronics customers will pay enormous premiums for the last decimal of purity, because contamination at the parts-per-million level can ruin an entire downstream batch.

That insight became the cultural pillar of the company: do not chase volume; chase the molecules where purity is the moat. By the time Neogen was inducted into the Indian Chemical Council's lists in the early 2000s and started exporting to Europe, the small Mahape workshop had quietly become one of the most credible high-purity bromine houses in Asia. The journey to becoming the "Bromine Man of India" was, in classic Indian-entrepreneur fashion, slow, unglamorous, and almost entirely unnoticed by Mumbai's financial press.

But sometime around 2008, a young man with a PhD walked into the family office. He had a different idea of what the next decade should look like.

III. The Second Act: Dr. Harin Kanani & the PhD Pivot

If Haridas Kanani was the workshop intuitionist, his son Harin was the laboratory rationalist. Harin Kanani's biography reads almost as if it were designed for the second act of an industrial-chemistry story. Undergraduate engineering at the Institute of Chemical Technology in Mumbai (आईसीटी), one of India's most rigorous chemical-engineering schools. PhD in chemical engineering from the University of Maryland in the United States, focused on process intensification and complex reactor design. Postdoctoral exposure to American specialty chemical practice. And then, in 2008, a quiet return to the family company.[^5]

The cultural transition this triggered inside Neogen is, in retrospect, the single most important event in the company's modern history—more important than the IPO, more important than the BuLi deal, arguably as important as the Mitsubishi license. Because what Harin brought back was not capital, and not contacts. It was epistemology. He believed the old workshop logic—tinker, test, repeat—could be retained as cultural DNA but had to be coupled to a much more formal R&D process, with statistical design of experiments, kinetic modelling, and continuous-flow chemistry where appropriate.

He also brought a different way of looking at chemistry as a portfolio. Instead of thinking only about bromine, Harin started asking: what other hazardous, hard-to-handle chemistries could Neogen master, where similar process alpha could be earned over a decade? Lithium was the obvious answer. Lithium chemistry, like bromine chemistry, is unforgiving—lithium metal reacts explosively with water, lithium salts are hygroscopic, and many lithium intermediates demand inert atmosphere handling. The same discipline that let Neogen handle bromine could, in theory, let it handle lithium. And lithium had two enormous tailwinds: the pharma world was discovering lithium-mediated synthesis (used in everything from antidepressants to organic LEDs), and—visible only on the horizon at that point—lithium-ion batteries were starting to look like the energy storage technology of the century.

Inside the company, the early 2010s were spent quietly building lithium derivatives—lithium bromide for vapour absorption chillers (the kind used in large commercial HVAC), lithium chloride, lithium carbonate, and small but rising volumes of advanced lithium compounds. None of these were huge revenue lines individually. Each was a steppingstone in process know-how.

In leadership style, Harin is the inverse of the Indian promoter stereotype. There is almost no Twitter presence, no airport-book-thought-leadership, no glossy magazine covers. Earnings calls are technical, sometimes painfully so—he will spend ten minutes explaining a yield improvement when the analyst really wants a one-line revenue guide. He treats employees as a long-term compounding asset and is famous internally for paying for his engineers' doctoral coursework. Promoter shareholding sits in the low-fifties as a percentage of equity—reported in regulatory filings at roughly 51%, with Harin's individual stake reported in the low double digits, around the 12–13% range, depending on the quarter and ESOP dilution.3 That alignment matters more than the precise decimal: this is a family that is fundamentally a holder of its company, not a seller of it.

Two specific moments capture the Harin-era pivot. First, the deliberate move from batch chemistry to continuous-flow processes for certain bromination steps, which sharply reduces hazardous inventory at any moment in time—a safety and capital-efficiency win the old guard had not contemplated. Second, the early identification that lithium-ion electrolytes—a thin, almost invisible product line in 2015—were going to become a global strategic chemistry by the late 2020s. Most Indian specialty chemical CEOs in 2015 were still talking about agrochemical custom synthesis. Harin was already asking what an Indian electrolyte plant would look like.

That foresight, far more than any single capex announcement, is what set Neogen up for the public market debut that came next.

IV. The Inflection Point: The 2019 IPO & Scaling

By 2018, Neogen had reached the awkward middle stage of an Indian specialty chemical company. It was big enough to need real growth capital, but too small for the very large private-equity cheques. It had two distinct chemistry platforms—bromine and lithium—each with its own capex hunger. The Dahej (दहेज) industrial cluster in Gujarat and the proposed Karakhadi (कराखाड़ी) site in Vadodara needed funding for new multi-product plants. And the regulatory door to the Indian public markets, after a long cooling-off period following the 2008 crisis, was finally wide open for mid-cap chemical companies.

The IPO came in late April 2019. Neogen priced its issue at a band of ₹212–₹215 per share, with a total issue size of about ₹132 crore, comprising a fresh issue of around ₹70 crore and an offer-for-sale by the promoters of the balance.[^7] The fresh-issue proceeds were earmarked primarily for repayment of debt and for capacity expansion at Dahej and Karakhadi. By Indian specialty-chemical standards, the issue was small. By Neogen's standards, it was transformational.

The market response was telling. The IPO was subscribed many times over, and the stock listed on the NSE (नेशनल स्टॉक एक्सचेंज) and BSE (बीएसई) in early May 2019. Within a year, despite a COVID-induced market shock, the stock had compounded meaningfully above the IPO price, reflecting an emerging consensus that Indian specialty chemicals—propelled by the now-famous "China+1" rebalancing of global supply chains—were a structural growth story. Neogen, with its dual chemistry platforms and its rising export share, was a natural beneficiary.

But the more interesting story sat below the headline numbers. The IPO did three things that were not obvious in the prospectus. First, it forced an upgrade of governance—independent directors, audit committees, formal ESG disclosures—at a moment when global pharma majors were beginning to insist on exactly that level of compliance from their Indian suppliers. The IPO, in effect, qualified Neogen for a different class of customers. Second, it gave the company a public-market currency. Once you have listed shares, ESOPs (एम्प्लॉयी स्टॉक ऑप्शन प्लान) become genuinely attractive to PhD-level chemists, and Neogen quietly built one of the best-paid technical teams in the industry. Third, the IPO converted Neogen from a private family business into a "story stock" that fund managers could anchor to—the rare two-chemistry-platform play with credible promoters.

The two years after listing were spent grinding through capex. The Dahej multi-product facility was built and commissioned in phases. Karakhadi expansions followed. Capacity for bromine derivatives rose, capacity for lithium derivatives rose, and meaningful debottlenecking happened across the Mahape mother plant. Through this period, the company's customer mix shifted in a way that is critical to the later story: away from the dominance of pharma and agro, toward a more diversified base that included flavours and fragrances, electronic chemicals, polymer additives, and—looking forward—energy storage materials.

By FY2022 and FY2023, the company was reporting revenues in the multiple-hundreds of crores, with consolidated revenues climbing toward and through the ₹600 crore mark, supported by a steady gross-margin profile that reflected its high-purity, low-volume product mix.[^8] None of these numbers, on their own, would have justified the multiple the market would later assign Neogen. The justification came from what happened next: two transactions, executed in the space of a few weeks, that changed the trajectory of the company.

The IPO had made Neogen big enough to be taken seriously. It had not yet made it strategic. That was about to change.

V. M&A Strategy: The BuLi Chemicals Heist

In early 2023, somewhere in the bowels of FMC Lithium's American parent—the company you and I now know as Livent (and which subsequently merged with Allkem to form Arcadium Lithium)—a strategic review of non-core assets concluded that a small Indian subsidiary called BuLi Chemicals India Private Limited was, in corporate-portfolio language, "non-strategic". BuLi was a niche operation, sitting on a plot in Gujarat, producing n-butyllithium and other organolithium reagents in modest volumes. For Livent, with its global lithium-mining and lithium-hydroxide ambitions, BuLi was a pebble. For Neogen, it was a missing puzzle piece.

The deal was announced in early 2023 and closed in May 2023, at a consideration of approximately ₹19.4 crore (roughly $2.4 million at then-prevailing rates) on an enterprise-value basis.1 That number, viewed in isolation, looks unremarkable—small Indian companies trade for small sums all the time. But viewed in context, it is one of the most asymmetric trades in recent Indian specialty-chemical history.

Here is why. BuLi Chemicals' product set centred on n-butyllithium and related organolithium compounds—reagents in which a lithium atom is directly bonded to a carbon chain. These are arguably the most useful, and the most violently reactive, reagents in advanced organic chemistry. They are the workhorse of modern drug synthesis. They are also genuinely dangerous: they spontaneously ignite in air, react explosively with water, and demand cryogenic, inert-atmosphere handling. The number of plants worldwide that can produce them at commercial scale is in the low single digits.

To use a sports analogy: most Indian specialty-chemical M&A is the equivalent of signing a useful midfielder. The BuLi acquisition was Neogen quietly signing a player from a league that did not even have an Indian franchise yet. In acquisition-multiple terms, the price worked out to roughly 0.24 times BuLi's annual sales, at a moment when comparable Indian specialty-chemical acquisitions were being priced at 1.0–1.5 times sales or more.4 On a strategic-value basis—what you would pay for the chemistry license alone if you tried to build it from scratch—it was even cheaper.

Why did Livent let it go for so little? Three reasons, none of which involved Neogen being clever, and all of which involved Livent being honest with itself. First, lithium-carbonate and lithium-hydroxide prices were in a violent up-cycle, and Livent's corporate attention was on building out upstream mining, not running a small downstream Indian subsidiary. Second, BuLi was sub-scale: a few hundred tonnes a year of organolithiums was a rounding error in Livent's books and a recurring management headache. Third, Livent was already preparing for the Allkem merger and wanted to declutter the balance sheet. In other words, the seller's clock and the buyer's clock were not aligned, and the spread was Neogen's.

The strategic rationale on Neogen's side was the inverse of Livent's. For Neogen, organolithium chemistry was the perfect adjacency to its existing lithium-salt platform. Lithium salts are intermediates; organolithiums are the reagents that use lithium to do the actual chemistry. Owning both is unusual globally and almost unique in India. It also gave Neogen something subtler: customer access. Global pharma and agro innovators who needed n-butyllithium were now able to source it from an Indian, IP-respecting, ICH-grade supplier rather than rely on a handful of US, Japanese, or German alternatives. The qualification cycles for some of those customers had already begun, and Neogen inherited a partial pipeline along with the assets.

The Acquired playbook lesson here is almost textbook. Buy a strategically critical technology at a moment when the seller is distracted, the commodity cycle is volatile, and the buyer can immediately load that technology onto an adjacent platform to compound returns. Neogen did exactly that. Within months of close, organolithium output was being directed into Neogen's existing pharma intermediate workflow, and the company had quietly become India's only integrated lithium-derivatives house.

The BuLi deal, however, was only the appetiser. The main course was already being plated in a Japanese boardroom.

VI. The Hidden Business: Neogen Ionics & the EV Frontier

In April 2023, a few weeks before the BuLi acquisition formally closed, Neogen Chemicals announced something that, in any other Indian listed company, would have been impossible to believe. It had signed a technology licensing agreement with MU Ionic Solutions Corporation—the joint venture between 三菱ケミカル Mitsubishi Chemical and UBE Corporation that is one of the world's leading suppliers of lithium-ion battery electrolytes—to manufacture electrolytes in India under license.[^1] The agreement made Neogen the first Indian company in history to be granted that kind of global manufacturing tech transfer for EV-grade electrolytes.[^2]

To understand why this is enormous, you have to understand what electrolytes are and what role they play inside a lithium-ion cell. A lithium-ion battery has four critical components: a cathode (the positive material that stores lithium ions), an anode (the negative material that releases them), a separator (a thin film that keeps the two electrodes from touching), and an electrolyte (a liquid that lets lithium ions shuttle back and forth). If you think of a battery as a circulatory system, the electrolyte is the blood. Get the formulation wrong, and you get a cell that either underperforms, dies young, or—in the worst case—catches fire.

Electrolyte chemistry is a strange beast. The base solvent is typically a mixture of organic carbonates—ethylene carbonate, dimethyl carbonate, ethyl methyl carbonate. Into this is dissolved a lithium salt, almost always lithium hexafluorophosphate (LiPF₆), at very precise concentrations. And then, to get cell performance that actually works in a hot Indian summer or a cold Himalayan winter, you add a cocktail of tiny additives—each in single-digit percentage by weight—that stabilise the interface between electrolyte and electrode. Those additives are the secret sauce, and the patent and know-how landscape around them is fiercely protected. This is what MU Ionic Solutions transferred. This is what Neogen Ionics now operates.

Neogen Ionics was incorporated as a separate subsidiary to hold this opportunity, capitalised, and pointed at a site in Gujarat for an electrolyte and lithium-salt manufacturing complex. The scale ambition is enormous. Initial commissioning steps were sized around a few hundred tonnes per annum to qualify samples with global cell makers. The full plan, as articulated in the company's investor presentations and subsequent earnings commentary, targets capacity well into the tens of thousands of tonnes per annum, with management guidance pointing at a multi-thousand-crore revenue contribution from the battery materials business by the end of the decade.[^10]

The backward integration piece is what turns this from a contract-manufacturing exercise into a moat. Most independent electrolyte mixers around the world buy their LiPF₆ salt from a handful of Chinese suppliers. Neogen's plan is to make LiPF₆ in-house. LiPF₆ is one of the hardest chemicals to manufacture commercially. It is extremely hygroscopic, decomposes if you so much as look at it wrong, and demands hydrogen fluoride handling that very few plants in the world have the safety clearance to do. If Neogen can crack LiPF₆ at scale—and it has spent years quietly working on it—then it will own one of the most strategic chemistry stacks in the Indian energy transition.

There is also the matter of the qualification cycle, which is the unfashionable but absolutely critical moat in this business. An EV original-equipment manufacturer or a cell maker does not just buy electrolyte off the shelf. It takes 18 to 24 months of sampling, cell testing, ageing tests, thermal-runaway tests, and safety audits to qualify a new electrolyte supplier into a commercial cell. Once qualified, the supplier becomes part of the bill-of-materials and the customer's regulatory filings. Switching to a new electrolyte supplier means re-qualifying. Almost no one wants to do that. So the qualification cycle, slow and painful as it is, is also one of the most durable customer-lock-in mechanisms in the entire battery-materials value chain.

This is the punchline of Neogen Ionics. The company is not betting on being the cheapest electrolyte producer in the world. It is betting on being the first one inside the qualification cycles of India's emergent battery industry—powered by the central government's PLI (प्रोडक्शन-लिंक्ड इंसेंटिव) scheme for advanced chemistry cells—and using its Mitsubishi-licensed tech to enter those qualification cycles with credibility. Once embedded, the switching costs do the work.

If everything goes to plan, the subsidiary the public market currently treats as an interesting side bet will, by the end of this decade, be larger than the parent business that birthed it. That, in turn, is why Neogen's stock has begun trading at multiples no traditional Indian specialty chemical company would ever earn.

VII. Playbook: Business & Investing Lessons

Step back from the chronological narrative for a moment and look at Neogen through the lens of Hamilton Helmer's 7 Powers framework. The picture that emerges is unusually crisp for an Indian mid-cap.

The first and most underrated power is Cornered Resource. In Helmer's framework, a cornered resource is a preferential access to something valuable that competitors cannot replicate at a reasonable cost. For Neogen, that resource is human: the cumulative thirty-plus years of know-how, embedded in the Kanani family and a small core of long-tenured chemists, in handling bromine and lithium chemistries safely at commercial scale. You cannot buy that knowledge with a chequebook. You can only earn it with two decades of incident-free reactor operation. That is exactly what Neogen has, and what newer Indian entrants—even well-funded ones—lack.

The second power is Switching Costs, which we just discussed in the electrolyte context but which applies even more strongly to the legacy bromine and lithium businesses. Once a global pharma major has qualified a Neogen intermediate into its commercial manufacturing process for, say, an antiepileptic API, switching suppliers requires a regulatory variation filing in dozens of countries. Customers do not switch on price alone. They switch only when they have to.

The third power is Scale Economies. Here, Neogen is mid-game rather than end-game. Its biggest single industrial bet is the proposed integrated complex—built around the broader Dahej/Pakhajan (पाखाजन) industrial belt and the new electrolyte/lithium-salt facility—which, when fully ramped, will be the largest single integrated electrolyte and lithium-salts complex in India. Scale matters in this business because the fixed costs of safety systems, regulatory clearances, and continuous solvent recycling are huge. The first plant in India to cross a credible scale threshold gets a structural cost advantage versus the second, third, and fourth.

The fourth power is Counter-Positioning. This is, in many ways, the most interesting power Neogen wields. Large Indian conglomerates—रिलायंस Reliance Industries, the टाटा Tata Group, अदाणी Adani—have all announced massive battery and energy-transition ambitions. But their public roadmaps focus mostly on cell manufacturing and gigafactories, not on the highly specialised, mid-stream battery chemistry that sits between mining and cell assembly. Neogen, in classic counter-positioning style, has gone after the niche the giants will not pursue with their first wave of investment, because to do so would require them to acquire and operate hazardous chemistry plants that do not yield gigawatt-scale headlines.

The fifth and sixth powers—Network Economies and Branding—do not really apply here in any meaningful way. This is a B2B chemistry business; nobody is buying Neogen on brand power, and there is no network effect among molecules.

The seventh power, Process Power, is arguably what stitches everything else together. Process Power is the embedded organisational capability to do something difficult, reliably and at scale, that competitors cannot replicate quickly. Bromine handling without incidents. Lithium handling without incidents. Continuous flow for hazardous chemistries. Multi-step synthesis with high purity. This is exactly what Neogen has built over three decades, and it is exactly why a new entrant cannot just buy a piece of land and replicate the company.

Now layer Porter's 5 Forces on top.

Barriers to entry are high. New entrants need decade-scale safety records, hazardous-chemistry licenses, customer qualifications, and—now, in the battery materials world—either their own electrolyte tech or a license from someone like MU Ionic Solutions, which is not exactly handing those out freely.

Supplier power is mixed. For bromine, Neogen sources from a small number of large global producers; for lithium, the global supply chain is increasingly dominated by Chinese, Chilean, and Australian players. Neogen mitigates this with long-term arrangements and—on lithium—the planned LiPF₆ backward integration that pulls more of the value chain in-house.

Buyer power is, surprisingly, low for the high-purity end of the product mix. Pharma and electronics customers are price-sensitive at the margin but absolutely not price-sensitive at the qualification threshold; they want the right molecule, on time, every time, and they pay for it.

Threat of substitutes is essentially zero in bromine chemistry (there is no good substitute for a brominated intermediate when a customer's molecule demands one) and low-but-evolving in lithium electrolytes (solid-state battery technology, when commercialised at scale, could eventually disrupt liquid electrolyte demand—but that timeline is well into the 2030s).

Rivalry among existing competitors is intensifying. Indian specialty chemical companies are not asleep. Tatva Chintan (तत्व चिंतन), Aether Industries (एथर), and a handful of others are circling adjacent chemistries. But within the bromine-and-lithium dual platform, Neogen's position remains structurally unique.

The investment playbook lesson is therefore not "buy a specialty chemical company". It is something more specific: when a process-alpha company combines a hazardous-chemistry moat with a credible global technology license and a multi-decade tailwind from an adjacent demand explosion, the resulting compounding can be unusually durable—because none of the inputs reset overnight.

VIII. Management & Governance Analysis

Indian mid-cap promoter-led companies live and die by their governance. The best ones look boring. The worst ones make headlines for the wrong reasons. Neogen, mercifully, sits firmly in the boring camp, and that is meant as the highest possible compliment.

The headline governance story in 2025 was the formal leadership transition, with Haridas Kanani transitioning to a Chairman Emeritus role and Harin Kanani assuming the full operational mantle as Managing Director.5 That language—Chairman Emeritus—matters. It signals a real handover rather than the ceremonial-but-not-actual transitions that bedevil many Indian family businesses. Haridas remains involved in advisory and cultural roles, but day-to-day strategy, capital allocation, and operations sit with Harin and his team.

The board structure has been steadily institutionalised since the IPO. Independent directors with backgrounds in chemicals, finance, and audit have been added, the audit committee is independent-majority, and the related-party transaction policy has tightened in the years since 2019. None of this is exciting reading on its own. But the absence of fireworks—no auditor changes for cause, no related-party transactions large enough to require special shareholder approval, no qualifications on the audit opinion—is itself the signal.

Compensation structure is interesting. Indian companies under the Companies Act 2013 (कंपनी अधिनियम 2013) are bound by limits on managerial remuneration relative to net profits, and Neogen's promoter compensation has been disclosed in annual reports at levels that sit well within the legal caps and, in some recent years, below them. The Employee Stock Option Scheme 2024 was approved to align senior employee incentives with long-term shareholder outcomes, with vesting schedules that stretch out over multiple years.[^12] This matters more than people realise: when your most senior R&D and operations people get paid in equity that vests over four to five years, the time horizon of decision-making inside the company quietly elongates.

The "IIT culture" point is more cultural than measurable. The leadership and senior R&D ranks at Neogen are dominated by graduates of the ICT (formerly UDCT), the IITs (भारतीय प्रौद्योगिकी संस्थान), and a handful of strong American and European chemical engineering programmes. The vocabulary inside Neogen earnings calls is unusually technical—people talk about residence times, selectivity, and reactor configurations the way other companies' management talks about EBITDA bridges. For investors used to growth-by-marketing stories, this can be disorienting. For investors who value engineering depth, it is the single most reassuring signal.

Ownership concentration on the promoter side, in the low fifties as a percentage of equity, leaves enough float for genuine price discovery while ensuring that the family's wealth is overwhelmingly tied to the company's long-term trajectory.3 There has been no aggressive promoter pledging, no large block sales that would suggest the family is hedging its bets. The Kananis are, by every available signal, all-in.

One area worth flagging—because the article would not be honest without doing so—is the working capital intensity of the business and the consequent debt profile during heavy capex phases. Specialty chemicals with multi-step synthesis and high inventory of hazardous raw materials tend to run high working capital cycles, and Neogen's Q1 FY26 commentary made clear that the battery materials ramp was straining short-term financing.6 That is not a governance problem per se. It is a structural feature of the business model that any long-term investor needs to track quarter by quarter.

The leadership transition, the deep R&D culture, and the aligned promoter shareholding together do not eliminate risk. But they do mean that the people steering Neogen through the next decade are betting their own family fortunes on the same outcome the minority shareholders are betting on. In Indian mid-cap land, that alignment is rarer than it should be.

IX. Analysis: The Bull vs Bear Case

Time for the structured argument. As always with Acquired-style analyses, the bull and bear cases are both meant to be taken seriously—if one is laughably stronger than the other, you are not really doing the work.

The bull case begins with the structural setup. India's central government, through the PLI (प्रोडक्शन-लिंक्ड इंसेंटिव) scheme for advanced chemistry cell batteries, has effectively underwritten a domestic cell-manufacturing industry that did not exist five years ago. That industry, when it ramps over the second half of the 2020s, will need electrolytes, lithium salts, separators, cathode materials, and anode materials inside India, both for cost reasons and—increasingly—for strategic reasons under the broader आत्मनिर्भर भारत Atmanirbhar Bharat self-reliance framework. Neogen, with its Mitsubishi license, its planned LiPF₆ integration, and its multi-thousand-tonne electrolyte ambitions, is positioned to be the default first call for any Indian cell maker that does not want to rely entirely on Chinese supply.

The bull case also benefits from a second, quieter tailwind: global bromine supply tightness. Bromine production globally is concentrated in a handful of geographies, including the Dead Sea (Israel and Jordan) and a few US sites, and the geopolitical fragility of those supply chains has begun to push pharma and electronics customers to look for diversified suppliers. Neogen's high-purity bromine derivatives are exactly the kind of capability those customers want to qualify into their bill-of-materials. Bromine margins, in other words, are not just defended—they have an asymmetric upside if global supply tightens further.

Layer on the BuLi-driven organolithium platform, the deepening custom synthesis relationships with global pharma majors, and the option value of Neogen Ionics being able to export electrolytes to the rest of Asia and Europe in the 2030s, and the bull case is genuinely compelling. This is a company whose addressable market expands by a multiple, not a percentage, over the next decade.

Now the bear case, which is just as real.

First, lithium price volatility. Lithium carbonate prices have been a roller coaster over the last several years, swinging by more than an order of magnitude. Neogen's business is hedged at the customer level via formula pricing, but working capital absorbs the volatility, and during sharp price swings the inventory mark-to-market can be brutal. The Q1 FY26 commentary explicitly flagged working capital pressure as a constraint on growth velocity.6

Second, Chinese competition. The single biggest global producer of electrolyte and LiPF₆ is the Chinese specialty chemical industry, which has scale, learning-curve, and cost advantages that no Indian player can erase in the short term. Chinese players are increasingly setting up plants in friendly jurisdictions—South-East Asia, possibly even India in the future—and the price war that would result from a fully cost-competitive Chinese plant in India is a meaningful downside scenario.

Third, execution risk. Neogen's capacity ambitions, particularly on the electrolyte and lithium-salts side, are very large relative to its historical revenue base. Building and ramping a 32,000-tonne-per-annum electrolyte capacity, integrating LiPF₆ backward, qualifying with multiple OEM customers in parallel, and doing it all without a major safety incident in hazardous chemistry is a lot to ask of any management team. The history of Indian mid-cap capex cycles is littered with companies that announced ambitious capacity, delivered it 18 months late, and saw demand slip past them in the meantime.

Fourth, the valuation problem. Through 2024 and into 2026, Neogen has traded at price-to-earnings multiples that look more like a global energy-transition stock than an Indian specialty chemical company. That re-rating reflects the market's belief in the battery materials thesis. It also means that any slippage—in capex timeline, customer qualifications, or working capital—gets punished harshly by the multiple, even before earnings move.

Fifth, and most important from a myth versus reality standpoint: there is a popular narrative that Neogen is "already" an EV company. It is not. As of the most recently reported financials, the overwhelming majority of revenue still comes from organic intermediates, bromine derivatives, and lithium derivatives sold into pharma, agrochemicals, and traditional industrial applications. The battery materials business is in commissioning and ramp-up. The narrative is forward-looking; the cash flows are catching up. Investors who confuse the two are buying a multiple, not a business.

So what does an investor actually track on a quarter-to-quarter basis to know whether the thesis is unfolding? Three KPIs matter more than the rest.

The first is electrolyte and lithium-salts capacity utilisation, in tonnes shipped versus nameplate. This is the single most direct read on whether the Neogen Ionics ramp is on schedule, because revenue per tonne is reasonably stable but tonnes per quarter is what is moving. The second KPI is the gross margin on the battery materials segment, separately disclosed where management provides the segmental detail, because that tells you whether Neogen is being forced to compete on price with Chinese supply or whether the qualification-driven premium is holding. The third is net debt to EBITDA, because the capex cycle and the working capital pressure together make the balance sheet the constraint that decides whether the company can keep funding its ambition or whether it has to raise dilutive equity.

If those three KPIs trend in the right direction over the next eight quarters, the bull thesis is being validated. If they don't, the bear thesis is.

X. Epilogue & Final Reflections

There is a recurring pattern in the history of great industrial companies: they are usually founded by someone who chose to master a chemistry, or a physics, or a manufacturing process that the rest of the industry thought was too hard. DuPont with explosives. Linde with cryogenics. Shin-Etsu with silicones. Asahi Kasei with hydrogen peroxide. The pattern is so consistent that it is almost a screening rule: if a company's founding decision was to do the hard, hazardous, unglamorous thing—and to do it for decades—then the moat that results tends to outlast generations.

Neogen Chemicals' founding decision was bromine, in a country where almost nobody wanted to touch it. Its second decision was lithium, at a moment when lithium meant antidepressants more than electric vehicles. Its third decision—the Mitsubishi license, the BuLi acquisition, and the Neogen Ionics bet, all stacked into a single 2023 calendar year—was to compound those two chemistries into the centre of the Indian energy transition.

The arc of the story is the arc of Indian industry itself. India's specialty chemical sector spent the 1980s and 1990s as a low-cost contract manufacturer for the West. It spent the 2000s and 2010s climbing the value chain into custom synthesis, regulated-market intermediates, and global pharma partnerships. And now, in the 2020s, the best of those companies are climbing one more rung—from "value-added chemistry partner" to "strategic technology provider" in industries like electric vehicles, electronics, and advanced materials. Neogen, with its dual chemistry platforms and its first-mover position on Indian electrolytes, is one of the cleanest expressions of that climb.

What does the next decade look like for the company? On the optimistic path, Neogen Ionics ramps into a multi-thousand-crore revenue line, the LiPF₆ backward integration works, the bromine business compounds steadily, and the company emerges as the default Indian supplier to a domestic gigafactory ecosystem that did not exist when its IPO priced. On the pessimistic path, Chinese supply, lithium price volatility, and execution slippage erode the timeline, and the company's current valuation gets a hard reset. The most likely path, as ever, is somewhere in between—closer to the optimistic case if the qualification cycles inside Indian cell makers progress on schedule, closer to the pessimistic case if they don't.

But here is the deeper thing. Even in the pessimistic scenarios, the underlying chemistry moats—the bromine know-how, the organolithium platform, the lithium salt expertise, the multi-decade safety record—do not evaporate. They sit there, compounding quietly, ready for the next wave of demand, whether that wave is EVs in India, electrolytes in Europe, or some entirely new chemistry that hasn't been imagined yet. That is what process alpha looks like in practice: optionality earned through three decades of doing the hard thing.

The Kanani family started in a Mahape workshop, in 1989, mastering the most corrosive liquid element on the periodic table because nobody else would. Thirty-seven years later, the same family is building India's electrolyte backbone for the energy transition. The compound has changed. The alchemy has not.

That, in the end, is what makes Neogen Chemicals a more interesting business story than its market capitalisation has, until recently, suggested. It is not a chemicals company that happened to find EVs. It is a process company that happened to find bromine, then lithium, then electrolytes—and that will, in all likelihood, happen to find whatever comes next. For a long-term investor trying to underwrite Indian industrial compounding, the alchemist is often the safer bet than the alchemy.

References

References

-

Neogen Chemicals completes acquisition of BuLi Chemicals India — Business Standard, 2023-05-04 ↩↩

-

Neogen Chemicals shareholding pattern and promoter holding — NSE Filings ↩↩

-

Specialty Chemicals: The Lithium-Bromine Powerhouse — Nuvama Wealth Research, 2024-05 ↩

-

Understanding the Bromine Moat in Specialty Chemicals — Chemical Weekly, 2023-09 ↩

-

Neogen Chemicals Q1 FY26 Earnings Call Transcript — Moneycontrol ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube