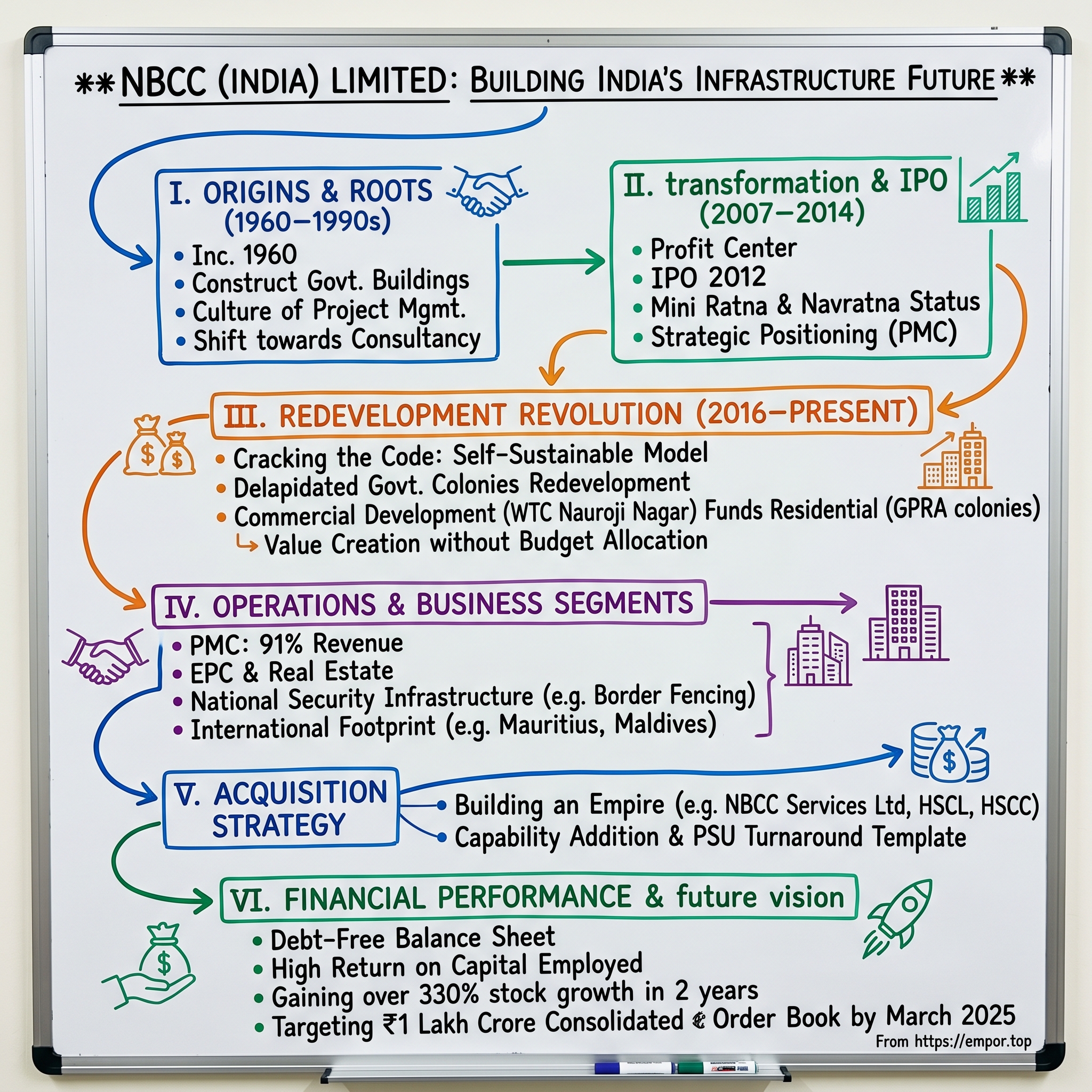

NBCC (India) Limited: Building India's Infrastructure Future

I. Introduction & Episode Roadmap

Picture this: It's 2018, and the Delhi skyline is transforming before your eyes. Where decrepit government housing colonies once stood—buildings from the 1960s with crumbling facades and outdated infrastructure—gleaming modern apartments are rising. But here's the twist: not a single rupee from the government treasury is funding this ₹25,000 crore transformation. Welcome to the world of NBCC India, where a 64-year-old government construction company has cracked the code on self-financing urban renewal. Today, NBCC India stands as one of India's most fascinating corporate transformation stories. With a market capitalization hovering around ₹28,600-29,800 crore and annual revenue of ₹12,300 crore, this isn't just another public sector undertaking—it's the blueprint for how government companies can reinvent themselves for the modern era. As a Navratna Enterprise under the Ministry of Housing and Urban Affairs, the company operates across three major segments: Project Management Consultancy, Engineering Procurement & Construction, and Real Estate.

But here's the real question that drives our story today: How did a sleepy government construction department, established in the bureaucratic maze of 1960s India, transform into the architect of New Delhi's most ambitious urban renewal project? And more intriguingly, how did they figure out a way to rebuild entire government colonies without spending a single rupee of taxpayer money?

This is a tale of patient capital meeting entrepreneurial thinking, of government efficiency defying stereotypes, and of a business model so unique that private developers can only watch from the sidelines. It's the story of NBCC India—a company that has quietly become the backbone of India's infrastructure transformation while generating returns that would make any private equity firm envious. The stock has gained over 330% in two years, and analysts are taking notice. Elara Capital has initiated coverage predicting a potential rise of over 42%.

As we journey through six decades of corporate evolution, we'll explore how NBCC cracked the code on self-financing development, why their asset-light model is virtually impossible to replicate, and what their massive order book tells us about India's infrastructure future. We'll dissect their acquisition strategy, analyze their financial engineering, and understand why 61.8% government ownership might actually be their biggest competitive advantage.

So buckle up as we dive deep into one of India's most underappreciated corporate success stories—a PSU that thinks like a startup, operates like a consultancy, and builds like a nation depends on it. Because in many ways, it does.

II. Origins & Government Roots (1960–1990s)

The year was 1960. Jawaharlal Nehru's India was barely thirteen years old, grappling with the monumental task of building a nation from scratch. In the corridors of power in New Delhi, bureaucrats faced a peculiar problem: who would build the buildings that would house the machinery of this new democracy? Private contractors were few, expertise was scarce, and the scale of construction needed was unprecedented. It was against this backdrop that on November 15, 1960, National Buildings Construction Corporation Limited was incorporated—not as a grand vision, but as a practical necessity.

The early mandate was straightforward yet ambitious: construct government buildings and institutional projects across a rapidly expanding nation. But this wasn't just about pouring concrete and laying bricks. This was nation-building in its most literal sense—creating the physical infrastructure of governance for a country of 400 million people spread across 3.3 million square kilometers.

What made NBCC different from other construction departments was its structure from day one. Unlike typical government departments that operated on budgetary allocations, NBCC was set up as a corporation—expected to generate revenue, manage projects, and eventually, turn a profit. This seemingly small distinction would prove crucial decades later.

The 1960s and early 1970s were marked by what can only be described as institutional learning at scale. NBCC's engineers and project managers cut their teeth on everything from secretariat buildings in state capitals to housing colonies for government employees. Each project was a masterclass in navigating India's complex bureaucracy, managing scarce resources, and dealing with the realities of the License Raj era where even procuring cement required multiple permissions.

Then came 1977—a year that would quietly reshape NBCC's destiny. While the world focused on India's political Emergency ending, NBCC made its first tentative steps into international markets. The Middle East was experiencing an oil boom, African nations were building their post-colonial infrastructure, and they needed expertise. NBCC, armed with two decades of experience building in challenging conditions, found itself uniquely positioned. The company began taking up projects in Iraq, Libya, Yemen, and Nepal—not glamorous work, but solid, profitable contracts that provided precious foreign exchange and, more importantly, exposure to international project management standards.

The international expansion wasn't just about revenue; it was about survival. Back home, the 1980s were tough for public sector undertakings. Many PSUs were bleeding money, becoming symbols of government inefficiency. The joke in Delhi's bureaucratic circles was that PSUs were where careers went to die. But NBCC was different. The international projects provided a cushion, a source of revenue that wasn't dependent on government allocations. The company learned to be lean, to compete, to deliver on time—lessons that would prove invaluable.

By the late 1980s, NBCC had developed something rare in India's public sector: a culture of project management excellence. While other PSUs struggled with cost overruns and delays, NBCC was quietly perfecting the art of delivering projects on time and within budget. They developed systems for everything—from vendor management to quality control, from cost estimation to project scheduling. These weren't Silicon Valley-style innovations; they were grinding, procedural improvements that compound over decades.

The company also made a strategic choice that seemed minor at the time but would prove transformative: instead of just being builders, they began positioning themselves as project management consultants. Why compete with private contractors on laying bricks when you could manage entire projects and earn fees with minimal capital investment? This shift from pure execution to project management consultancy—from EPC to PMC—began in these early years, though it would take decades to fully materialize.

What's remarkable about this period is what NBCC didn't do. They didn't diversify into unrelated businesses like many PSUs. They didn't try to become a conglomerate. They stuck to construction and project management, slowly building expertise, relationships, and most importantly, trust. When government departments needed something built—especially something complex or sensitive—NBCC became the default choice. Not because they were the cheapest, but because they could be trusted to deliver.

The story of NBCC's survival through the License Raj era is really a story about institutional resilience. While private companies could pivot quickly or shut down if things went south, NBCC had to evolve within the constraints of government ownership. Every change required approvals, every innovation needed committees, every decision had to be documented. Yet somehow, they managed to build a culture of competence within these constraints.

By 1990, NBCC had completed over 22,000 projects. From the Prime Minister's Office complex to border outposts in Ladakh, from university campuses to housing for defense personnel—NBCC's fingerprints were everywhere in India's built environment. They had survived when other PSUs had withered, thrived when the smart money said government companies couldn't, and quietly built capabilities that would soon be unleashed in ways no one could have predicted.

The slow-burn years were ending. India was about to liberalize its economy, Delhi was about to transform, and NBCC was about to discover that sometimes, being a government company wasn't a liability—it was the ultimate competitive advantage.

III. The IPO & Transformation (2007–2014)

April 2007. The conference room at NBCC's Lodhi Road headquarters was unusually crowded. For the first time in the company's 47-year history, they were cutting a dividend cheque to the Government of India. ₹7.7 crore—not a massive amount by corporate standards, but symbolic of something much larger. NBCC wasn't just another government department anymore; it was generating profits that could be returned to its shareholder. The transformation from a cost center to a profit center was complete, but this was just the opening act.

The global financial system was about to implode, but in India, something interesting was happening. The government was looking at its portfolio of companies and asking a radical question: what if we took some of these PSUs public? Not privatization—the government would maintain control—but public listing that would bring in private capital, market discipline, and most importantly, transparency.

NBCC's leadership saw an opportunity. Chairman and Managing Director stood before the board with a proposal that would have seemed like fantasy a decade earlier: take NBCC public. The logic was compelling. The company had cleaned up its balance sheet, streamlined operations, and most crucially, had figured out a business model that actually worked—the shift from pure construction to project management consultancy was paying dividends, literally.

April 2012 arrived with the kind of nervous energy that precedes major transformations. NBCC's IPO hit the markets at ₹106 per share, raising ₹126 crore. The response was lukewarm—this wasn't a tech startup or a consumer brand. It was a government construction company. But for those who looked closer, the numbers told a different story. The company was asset-light, had steady government contracts, and operated in a space where competition was limited. The smart money started paying attention.

Five months later, in September 2012, came the first validation: Mini Ratna-I status. In the byzantine hierarchy of Indian PSUs, this meant something. It gave NBCC's board the power to make capital expenditure decisions up to ₹500 crore without running to the ministry for approval. For a company used to seeking permission for everything, this was like being handed the keys to the kingdom.

But the real game-changer came in June 2014. Navratna status—the holy grail of PSU classifications. Now NBCC could invest up to ₹1,000 crore without government approval, enter joint ventures, form subsidiaries, and most importantly, set its own strategic direction. The timing was perfect. Narendra Modi had just been elected Prime Minister with a mandate for development, and infrastructure was at the top of the agenda.

What happened next was a masterclass in strategic positioning. While other construction companies were bidding aggressively for EPC contracts, taking on execution risk and tying up capital, NBCC doubled down on its project management consultancy model. The pitch was simple but powerful: "We'll manage your entire project from concept to completion. You pay us a fee—typically 8-10% of project cost. We handle everything: design, tendering, supervision, quality control, and handover. You get a fixed-price, fixed-time delivery with minimal risk."

For government departments, this was revolutionary. They didn't need to maintain huge engineering departments. They didn't need to worry about cost overruns. They had one throat to choke if something went wrong. And because NBCC was a government company, there was inherent trust—no one could accuse them of favoritism or corruption when they hired another PSU.

The numbers started reflecting this transformation. In FY2008, total income was ₹1,821 crore. By FY2014, it had grown to ₹5,124 crore. But more importantly, the composition of revenue had changed dramatically. PMC fees, which require minimal capital and carry lower risk, were becoming the dominant revenue source. The company was generating returns on equity that would make private developers envious, but with a fraction of the risk.

The market started taking notice. From the IPO price of ₹106, the stock began its steady climb. But this wasn't speculative fervor—this was recognition of a fundamental transformation. NBCC had figured out something that had eluded most PSUs: how to leverage government ownership as a competitive advantage rather than a liability.

The company also began experimenting with what would become its signature move: self-sustainable redevelopment projects. The concept was elegant in its simplicity. Take old, dilapidated government colonies sitting on prime land. Redevelop them with modern apartments for government employees. But here's the twist—develop only part of the land for government housing. Use the rest for commercial development. Sell or lease the commercial space to fund the entire project. The government gets new housing without spending money, NBCC gets development rights and fees, and the city gets modern infrastructure. Everyone wins.

The first major test of this model was the New Moti Bagh redevelopment, completed in 2012. Where 588 quarters once stood in various stages of decay, NBCC built 2,334 modern flats. The commercial component funded everything. The model worked. More importantly, it was replicable.

Between 2007 and 2014, NBCC had transformed from a traditional construction company to something entirely different—a project management and redevelopment specialist with a unique business model that leveraged its government DNA. The company had gone public, achieved operational autonomy, and most importantly, proven that a PSU could innovate and compete.

The foundation was set. The model was proven. The market was paying attention. But what came next would surpass even the most optimistic projections. NBCC was about to embark on the largest urban redevelopment project in India's history—and they were going to do it without spending a rupee of public money.

IV. The Redevelopment Revolution: Cracking the Code

December 2016. Transport Bhawan, New Delhi. The meeting that would reshape Delhi's landscape was about to begin. Around the table sat officials from the Ministry of Housing and Urban Affairs, Delhi Development Authority, and NBCC's senior management. The agenda: redeveloping seven General Pool Residential Accommodation (GPRA) colonies spread across 250 acres of prime Delhi real estate. The challenge: 12,970 government quarters, many dating back to the 1960s, housing nearly 50,000 people, all in various stages of decay. The budget allocated by the government: Zero.

This is where NBCC's decade of experimentation crystallized into revolution. The self-sustainable redevelopment model wasn't just theory anymore—it was about to be deployed at a scale that would make it one of the largest urban renewal projects in Asia.

The genius of the model lay in its financial engineering. Take Sarojini Nagar, one of Delhi's most prime locations. The existing colony had 3,818 quarters sprawled inefficiently across 73 acres. NBCC's plan: build 14,000 modern flats on just 40% of the land through vertical development. The remaining 60%? Commercial development that would fund everything.

But the masterstroke was the World Trade Centre at Nauroji Nagar. Where a sleepy government colony once stood, NBCC envisioned Delhi's new commercial hub. Not just office buildings, but an entire ecosystem—35 towers of premium commercial space, convention centers, retail zones, and service apartments. The 27th e-auction results vindicated this vision spectacularly: NBCC sold 1.81 lakh square feet of commercial space for ₹908.48 crore, with around 1.21 lakh square feet worth ₹596.25 crore sold to PSU/Government entities and 0.60 lakh square feet worth ₹312.23 crore to private entities.

The highest price fetched in this auction was ₹62,261 per square foot against a reserve price of just ₹37,161 per square foot—a 67% premium that demonstrated the market's hunger for quality commercial space in Delhi. This showcases the success of WTC, Nauroji Nagar as a destination desired by many to base their enterprises.

The execution complexity was staggering. This wasn't just construction—it was urban surgery on a living city. Families needed to be relocated temporarily, then moved back into new apartments. Construction had to proceed in phases to minimize disruption. Every tree that could be saved had to be transplanted. Heritage structures needed preservation. All while maintaining the social fabric of communities that had lived there for generations.

NBCC developed a phase-wise approach that was almost surgical in its precision. Phase 1: Identify pockets for initial development. Phase 2: Build temporary transit accommodation. Phase 3: Shift residents from old quarters to transit accommodation. Phase 4: Demolish old structures and begin construction. Phase 5: Complete new towers and shift residents back. Phase 6: Demolish transit accommodation and continue development. Repeat across multiple pockets simultaneously.

The timeline was aggressive—seven years to transform 250 acres. But by 2018, the results were already visible. East Kidwai Nagar's transformation was complete. Where 2,338 quarters once stood, NBCC had built 4,000 modern apartments with parking, green spaces, community centers, and modern amenities. The commercial component was already generating revenue through pre-sales.

What made this model particularly brilliant was its alignment of incentives. The government got new housing without budget allocation. Employees got modern homes with better amenities. NBCC earned project management fees (typically 8% of project cost) plus development profits from commercial sales. The city got efficiently used land with modern infrastructure. Even environmental goals were met—rainwater harvesting, solar panels, and sewage treatment plants were standard. The new buildings were 30% more energy-efficient than the old quarters.

The financial innovation didn't stop there. NBCC structured the commercial sales to maximize value. Instead of bulk sales to single developers, they opted for e-auctions of smaller parcels. This created competition, drove up prices, and more importantly, created a diverse ecosystem of businesses rather than single-owner monopolies. The auction process was transparent, online, and open to all—addressing any concerns about favoritism.

The model also solved a political problem that had plagued redevelopment efforts for decades. Previous attempts at redeveloping government colonies had failed because they required massive budget allocations that became political footballs. Opposition parties would cry waste, media would scrutinize every rupee, and projects would stall. NBCC's self-financing model removed money from the equation. No budget meant no political controversy.

By 2019, the seven GPRA colonies project was valued at over ₹32,000 crore, making it one of the largest redevelopment projects not just in India, but globally. International delegations started visiting to understand the model. The World Bank sent teams to study how public land could be monetized without privatization. Singapore's Housing Development Board, long considered the gold standard in public housing, wanted to learn about the financial structuring.

But perhaps the most telling validation came from an unexpected source: private developers. Several major real estate companies approached NBCC for partnerships, essentially admitting they couldn't replicate this model alone. The reason was simple—the model required patient capital (projects took 7-10 years), government trust (to hand over prime land), and execution capability at scale. Only NBCC had all three.

The redevelopment revolution also changed NBCC's financial profile dramatically. These weren't just construction projects—they were essentially real estate development plays with construction fees attached. The company was sitting on development rights worth tens of thousands of crores, creating a value that traditional accounting metrics couldn't capture. The stock market, however, was beginning to understand.

As NBCC moved into 2020, the redevelopment model was no longer an experiment—it was the playbook. States started approaching them: Can you do this in Mumbai? What about Bangalore's government colonies? Even international governments inquired: Could this work in Colombo? What about African capitals struggling with similar problems?

The code had been cracked. Urban renewal without public expenditure wasn't just possible—it was profitable, scalable, and socially beneficial. NBCC had solved a trillion-dollar problem hiding in plain sight: how to modernize cities without breaking the bank. And they were just getting started.

V. Modern Operations & Business Segments

Walk into NBCC's project control room in Delhi on any given morning, and you'll see something that defies every stereotype about government companies. Multiple screens display real-time updates from construction sites across India—concrete pours in Manipur, steel fabrication status in Chennai, project timelines from Kashmir to Kanyakumari. This isn't your grandfather's PSU. This is a 21st-century project management machine that just happens to be owned by the government.

The numbers tell the story: Project Management Consultancy (PMC) now generates 91% of NBCC's revenue. This isn't by accident—it's by design. Sometimes the best business model is the one that requires the least capital and carries the minimum risk. NBCC figured this out earlier than most.

Here's how the PMC model works in practice. The Ministry of Defense needs a new office complex in Delhi. Instead of maintaining a massive construction department or going through lengthy tender processes with multiple contractors, they call NBCC. One contract, one point of contact, one fee structure—typically 8% of project cost. NBCC handles everything: architectural design, structural engineering, tendering, contractor selection, quality supervision, and final handover. The ministry gets a fixed-price, fixed-time delivery. NBCC gets a steady fee income with minimal capital employed.

The client list reads like a who's who of Indian governance: Ministry of Defense, Ministry of Home Affairs, Ministry of Finance, Central Universities, IITs, IIMs, AIIMS, and state governments including Haryana, Rajasthan, and Maharashtra. When institutions need infrastructure, NBCC has become the default choice—not mandated, but earned through decades of reliable delivery.

But the real evolution is in the type of projects. This isn't just about building government offices anymore. NBCC handles national security infrastructure like border fencing, civil infrastructure including roads and water systems, and executes projects under PMGSY and North Eastern development initiatives. The company is engaged in border fencing alongside the Indo-Bangladesh line in Mizoram, Meghalaya, and Tripura for the Ministry of Home Affairs.

Take the AMRUT (Atal Mission for Rejuvenation and Urban Transformation) projects. NBCC is managing water supply improvements, sewage treatment plants, and urban transport systems across multiple cities. These aren't construction projects in the traditional sense—they're complex urban interventions requiring coordination between multiple agencies, departments, and stakeholders. It's project management at its most complex, and NBCC has become the master orchestrator.

The international portfolio adds another dimension. While domestic projects provide steady income, international work offers higher margins and foreign exchange earnings. NBCC's footprint spans Mauritius (Supreme Court building), Maldives (housing projects), and nine African countries. The Dubai Expo 2020 project was particularly significant—managing construction in one of the world's most competitive construction markets proved NBCC could compete globally.

The three-segment structure seems simple on paper, but the synergies run deep. The PMC segment scouts opportunities and manages relationships. When a redevelopment opportunity emerges from a PMC client, the Real Estate segment takes over. The EPC segment, though smaller now, provides execution capability when needed—particularly for specialized government projects where security clearances and trust matter more than cost.

What's often missed is the intellectual property NBCC has accumulated. Six decades of construction has created India's largest repository of government building standards, specifications, and designs. Need to build a district court that can handle India's climate variations? NBCC has templates. Planning a university campus that needs to accommodate future expansion? They've done dozens. This institutional knowledge is a moat that money can't buy.

The digital transformation, though less visible, is equally important. Building Information Modeling (BIM) is now standard for major projects. Drone surveys track progress in real-time. AI algorithms predict potential delays by analyzing patterns from thousands of past projects. The company that once managed projects with paper files now runs on SAP, with every project milestone tracked digitally.

The sustainability focus isn't just corporate virtue signaling—it's becoming a competitive advantage. NBCC is advancing several Delhi Transport Corporation projects, including facilities at Hari Nagar Colony, Hari Nagar Depot, and Shadipur Colony, with a total value of approximately ₹1,600 crore, with the Vasant Vihar Depot alone representing an investment of Rs. (amount not specified in source). Every major project now includes green building certification as standard. Zero waste construction sites, rainwater harvesting systems, and solar installations aren't add-ons—they're built into the base price. Government clients love this because it helps them meet their sustainability targets without additional budget allocations.

The vendor ecosystem NBCC has built deserves special mention. Over decades, they've developed a network of pre-qualified contractors, suppliers, and consultants. This isn't just a vendor list—it's a carefully curated ecosystem where performance is tracked, ratings are maintained, and relationships are long-term. When NBCC needs to mobilize for a large project, they can tap into this network immediately. Contractors know that NBCC projects mean timely payments and fair dealing—rare in India's construction industry.

Risk management has evolved from a checkbox exercise to a core competency. Every project goes through multiple risk assessments: technical, financial, environmental, and social. The company maintains a risk register that tracks patterns across projects. If steel prices spike in international markets, they know exactly which projects will be affected and by how much. If monsoons are delayed, they can predict impact on project timelines with remarkable accuracy.

The quality control systems are particularly sophisticated. Third-party quality audits are mandatory. Material testing happens at NABL-accredited labs. Every concrete pour is documented. Every steel joint is inspected. This isn't bureaucratic overhead—it's what allows NBCC to offer fixed-price contracts with confidence. When you've built 30,000 projects, you know exactly what can go wrong and how to prevent it.

Looking at NBCC's modern operations, you realize this isn't really a construction company anymore. It's a project management platform that happens to specialize in construction. The asset-light model, technology integration, and focus on fee-based income have transformed a traditional PSU into something that looks more like Accenture than L&T.

But the real competitive advantage isn't the systems or the technology—it's the trust. When a government department hands over a ₹1,000 crore project to NBCC, they're not just buying project management. They're buying peace of mind. In a country where infrastructure projects routinely face delays, cost overruns, and quality issues, NBCC offers something invaluable: predictability.

The modern NBCC is a paradox—a government company that operates like a private firm, a construction company that owns minimal construction equipment, an Indian company that competes globally. But perhaps the biggest paradox is this: in an era where everyone wants to be asset-light and digital-first, NBCC got there by doing something decidedly old-fashioned—building things on time, within budget, and without drama. Sometimes the best innovation is perfect execution of the basics.

VI. The Acquisition Strategy: Building an Empire

January 2014. NBCC's boardroom was buzzing with an energy unusual for a PSU meeting. The agenda wasn't routine—it was transformative. The company was about to embark on an acquisition strategy that would reshape its capabilities and market position. The first move: creating NBCC Services Limited (NSL), a wholly-owned subsidiary focused on post-construction facility management. It seemed like a small step, but it was the beginning of something much larger.

The logic was compelling. NBCC was building thousands of projects, but what happened after handover? Buildings need maintenance, facilities need management, and systems need upkeep. Why let this steady, high-margin business go to others? NSL was born not from grand strategy documents but from a simple observation: the lifecycle value of a building extends far beyond construction.

By 2015, NSL was managing facilities across the country—from ministry buildings in Delhi to AIIMS campuses in remote locations. The subsidiary generated steady cash flows with minimal capital investment. More importantly, it created stickiness with clients. Once NBCC built your project and NSL managed it, switching to another vendor became almost unthinkable.

But the real masterstroke came in 2017. Hindustan Steelworks Construction Limited (HSCL)—a Ranchi-based PSU specializing in industrial construction—was struggling. Years of losses, declining orders, and organizational inertia had pushed it to the brink. The government wanted a solution that didn't involve closure and job losses. NBCC saw opportunity where others saw liability.

The negotiation was complex. HSCL came with baggage—accumulated losses, surplus staff, and outdated systems. But it also came with something valuable: specialized expertise in steel structures and industrial construction, a domain where NBCC had limited presence. The deal structure was creative: NBCC would acquire 51% stake, inject capital, and modernize operations while preserving jobs.

The HSCL turnaround became a template for PSU rehabilitation. NBCC didn't just inject capital; they transformed the culture. Modern project management systems replaced paper-based processes. Performance incentives were introduced. Cross-training programs moved expertise between organizations. Within two years, HSCL was profitable—a turnaround that even private equity firms would admire.

The 2018 acquisition of Hospital Services Consultancy Corporation (HSCC) was different—this was about capability addition rather than turnaround. HSCC, a Mini Ratna PSU under the Ministry of Health, specialized in hospital construction and medical infrastructure. With India's healthcare infrastructure push gaining momentum, this was strategic positioning at its finest.

The HSCC acquisition was structured as a 100% buyout, making it a wholly-owned subsidiary. The price was reasonable, but the strategic value was immense. HSCC brought relationships with the health ministry, expertise in specialized medical construction, and most importantly, a pipeline of hospital projects across the country. Suddenly, NBCC could bid for any healthcare infrastructure project in India with credibility.

The integration wasn't just financial—it was operational. HSCC's hospital design expertise was combined with NBCC's project management capabilities. NSL's facility management was extended to hospital operations. HSCL's steel fabrication capabilities were deployed for pre-fabricated hospital structures. What emerged was an integrated infrastructure platform that could handle any construction challenge the government threw at it.

But the empire-building wasn't just about domestic acquisitions. NBCC established international subsidiaries strategically. The Dubai subsidiary, NBCC DWC-LLC, wasn't just about executing projects—it was about establishing a Middle East hub for the entire region. From Dubai, NBCC could bid for projects across the Gulf, Africa, and Central Asia.

The acquisition strategy also extended to joint ventures, though these were more selective. Real Estate Development & Construction of Rajasthan Ltd. (REDCO-NBCC) was a 50% joint venture focused on affordable housing in Rajasthan. Rather than going alone in unfamiliar territory, NBCC partnered with local expertise while maintaining management control.

What made NBCC's acquisition strategy unique was its purpose. Private companies acquire for market share or capability. NBCC acquired for ecosystem completion. Each acquisition filled a gap in their value chain. Construction (NBCC core) + Industrial (HSCL) + Healthcare (HSCC) + Facility Management (NSL) = Complete infrastructure lifecycle coverage.

The financial engineering behind these acquisitions was equally sophisticated. Instead of large upfront payments, NBCC structured deals with staggered payments linked to performance milestones. Selling shareholders (usually the government) got fair value, NBCC preserved capital, and acquired companies got breathing room for turnaround.

The cultural integration was perhaps the biggest challenge. Merging PSU cultures isn't easy—each comes with its own history, unions, and work practices. NBCC's approach was patient but firm. No forced layoffs, but performance expectations were non-negotiable. Investment in training and systems, but accountability for results. Respect for legacy, but insistence on modernization.

By 2020, the acquisition strategy had transformed NBCC from a single company to a conglomerate. The consolidated order book had swelled, capabilities had multiplied, and market reach had expanded. But more importantly, NBCC had proven something important: PSUs could be effective acquirers and turnaround specialists.

The market noticed. Analysts who had valued NBCC as a construction company started seeing it as an infrastructure platform. The sum of parts was clearly greater than the whole. HSCC alone was worth several thousand crores, HSCL had hidden land assets, and NSL was generating steady cash flows. The stock price started reflecting this value creation.

The acquisition strategy also solved a larger problem for the government. India had hundreds of struggling PSUs—too small to survive independently but politically sensitive to close. NBCC's successful turnarounds created a template. Could strong PSUs absorb weaker ones? Could sectoral consolidation create national champions? The NBCC model suggested yes.

Looking back, the acquisition strategy wasn't just about building a business empire. It was about creating India's first integrated infrastructure PSU—a one-stop shop for any construction need the government might have. From border fencing to hospitals, from steel structures to facility management, NBCC and its subsidiaries could handle it all.

But perhaps the most important outcome was the demonstration effect. NBCC showed that PSUs could be aggressive acquirers, successful turnaround artists, and effective capital allocators. In a country where PSUs were often seen as employment programs rather than businesses, NBCC was writing a different narrative—one acquisition at a time.

The empire was built. The capabilities were in place. The stage was set for the next phase of growth. And as of December 2024, NBCC was targeting to reach ₹1 lakh crore of consolidated order book by March 2025 from the current ₹84,400 crore. The acquisition strategy had worked, but the real test was yet to come: Could this empire deliver?

VII. Financial Performance & Market Position

The analyst from Elara Capital pulled up NBCC's latest numbers on her Bloomberg terminal, paused, and double-checked. Q4 FY25 consolidated net profit had jumped 29.3% year-on-year to ₹176 crore, revenue from operations rose 16.2% to ₹4,643 crore. EBITDA stood at ₹310 crore, up 27.4% YoY, while EBITDA margin improved by 69 basis points to 6.7%. For a PSU in the construction sector, these weren't just good numbers—they were exceptional.

But the headline numbers only told part of the story. Q1 FY26 continued the momentum: net profit rose 26.30% to ₹132.13 crore while sales increased 11.61% to ₹2,391.19 crore. Quarter after quarter, NBCC was delivering consistent growth—not the volatile swings typical of construction companies, but steady, predictable expansion that fund managers love.

The order book position was even more impressive. From ₹84,400 crore in December 2024, NBCC was targeting ₹1 lakh crore by March 2025—a number that would make it one of the largest order books in India's construction sector. But unlike EPC players who took execution risk on every project, NBCC's order book was largely fee-based, providing visibility without the corresponding risk.

The market's recognition of this unique positioning was reflected in valuations. Trading at 11.4 times book value, NBCC commanded a premium that seemed excessive for a construction company but made perfect sense for a fee-based project management firm. The P/E ratio stood at 54.45 with a P/B ratio of 12.21—multiples that suggested the market saw something beyond traditional construction.

The stock performance validated this thesis. Gaining over 330% in two years, NBCC had outperformed not just its PSU peers but most private construction companies. The stock reached its all-time high of ₹139.83 on August 28, 2024, a far cry from its all-time low of ₹3.24 in May 2012.

What made NBCC's financial performance particularly impressive was its consistency across cycles. Construction is inherently cyclical—dependent on government spending, interest rates, and economic growth. But NBCC's model provided buffers. When government capex slowed, redevelopment projects continued. When new projects dried up, the existing order book provided revenue visibility for years.

The working capital management deserved special mention. Construction companies typically struggle with receivables, but NBCC's government clientele meant payments were delayed but never defaulted. The company had mastered the art of managing government payment cycles, maintaining liquidity without excessive borrowing. The company is almost debt free—a rarity in the capital-intensive construction sector.

The dividend policy reflected this financial strength. The Board recommended a final dividend of ₹0.14 per equity share (14%) for FY 2024-25, maintaining NBCC's track record of consistent shareholder returns. Q1 FY26 saw the declaration of first interim dividend of ₹0.21 per share. For a PSU, this balance between growth investment and shareholder returns was exemplary.

The margin profile told an interesting story about business mix evolution. PMC projects typically earned 8-10% fees with minimal capital employed, translating to high return on capital. Redevelopment projects, while requiring more capital, generated both development profits and management fees. The mix was optimized for risk-adjusted returns rather than absolute revenue maximization.

Analyst coverage was expanding, with institutional interest growing. Elara Capital's initiation with a 42% upside prediction reflected growing institutional recognition. The stock's inclusion in multiple indices—BSE 500, Nifty 500, BSE PSU—ensured passive fund flows, providing a stable shareholder base.

The financial strength also enabled strategic flexibility. While private developers struggled with leverage and liquidity, NBCC could be patient. Redevelopment projects with 7-10 year timelines weren't a problem. Land acquisition could be done upfront without financial stress. This patient capital advantage was impossible for private players to replicate.

The subsidiary performance added another layer of value. HSCC was contributing steadily to consolidated numbers. HSCL's turnaround was complete and contributing to profits. NSL's facility management business was generating predictable cash flows. The sum of parts valuation suggested significant hidden value not captured in the consolidated numbers.

International operations, while smaller, offered higher margins. Middle East projects earned fees in foreign currency, providing a natural hedge. African projects, funded by multilateral agencies, came with sovereign guarantees. The international portfolio wasn't just about diversification—it was about accessing higher-quality revenue streams.

The cost structure had been optimized over the years. Fixed costs were controlled through outsourcing of non-core activities. Variable costs were linked to project execution, ensuring margins remained stable regardless of revenue fluctuations. Technology investments had improved productivity, allowing revenue growth without proportional increase in employee costs.

Risk metrics painted a picture of a company that had mastered its domain. Project delays were minimal. Cost overruns were rare. Client disputes were almost non-existent. Quality issues were proactively managed. This operational excellence translated directly to financial predictability—a rare commodity in construction.

The cash flow generation was particularly impressive. Unlike EPC contractors who needed constant capital for equipment and working capital, NBCC's asset-light model generated free cash flow consistently. This cash could be deployed for acquisitions, dividends, or opportunistic investments without stretching the balance sheet.

Looking at peer comparison, NBCC occupied a unique position. It wasn't competing with L&T or other EPC majors on execution. It wasn't competing with DLF or other developers on land banking. It was in a category of its own—a government-backed project management platform with development capabilities. The closest comparables were international firms like AECOM or Jacobs Engineering, but even they didn't have NBCC's unique government relationship advantage.

The forward outlook suggested continued strength. With an order book crossing ₹50,000 crore in FY25 and eyeing newer geographies, actively participating in bids for railway station redevelopment, smart city expansion, and green building projects, analysts believed this robust pipeline would boost growth in upcoming quarters.

The financial performance wasn't just about numbers—it was validation of a business model. NBCC had proven that a PSU could generate private sector returns with public sector stability. They had cracked the code on making construction predictable, profitable, and scalable. For investors seeking exposure to India's infrastructure story without execution risk, NBCC offered a unique proposition.

But perhaps the most important financial metric wasn't on any balance sheet—it was trust. In a sector plagued by delays, disputes, and defaults, NBCC had built something invaluable: a reputation for delivery. That reputation was now translating into financial performance that would make any MBA case study writer jealous. The question wasn't whether NBCC could maintain this performance—it was whether anyone could replicate it.

VIII. Future Vision & Expansion

March 2024. NBCC's strategic planning session in Goa wasn't your typical corporate retreat. The location was deliberate—Goa represented the next frontier. State officials had just committed projects worth ₹10,000 crore, ranging from affordable housing to tourism infrastructure. But this wasn't just about one state. NBCC's leadership was sketching out a vision that would transform the company from a Delhi-centric PSU to India's national infrastructure champion.

The revenue targets were ambitious but grounded in reality. The company projected its value to rise to ₹252.81 in 3 years, ₹371.95 in 5 years, ₹484.82 in 7 years, and ₹661.95 in 10 years. While stock price predictions require caution, the underlying business expansion driving these projections was substantial and tangible.

The ₹25,000 crore revenue target, originally set for 2030, had been advanced to FY29—a statement of confidence that spoke volumes. This wasn't aggressive guidance to please markets; this was based on signed MOUs, confirmed projects, and visible pipeline. The math was straightforward: with an order book approaching ₹1 lakh crore and execution capabilities across subsidiaries, the revenue trajectory was more engineering than aspiration.

The Kochi project marked a strategic inflection point. Worth ₹2,650 crore, it represented NBCC's first major government project in South India—a market historically dominated by regional players. The significance went beyond the project value. South India, with its higher urbanization rates and stronger state finances, offered immense potential for NBCC's redevelopment model.

The state government partnership strategy was particularly clever. Rather than competing with state construction agencies, NBCC positioned itself as a capability partner. The pitch to state governments was compelling: "We'll bring project management expertise, access to central funds, and our self-sustainable model. You provide land and local support." It was a win-win proposition that state governments found hard to refuse.

The Department of Posts MOU signed in July 2025 opened another massive opportunity. Developing postal land parcels across India on NBCC's self-sustainable model meant access to prime urban land in every major city—land that had been lying underutilized for decades. Post offices in city centers could be transformed into mixed-use developments, generating revenue for the postal department while modernizing infrastructure.

The sustainability focus wasn't just compliance—it was becoming a competitive differentiator. Every new project now targeted net-zero emissions. Green building certification was standard. Renewable energy integration was built into design. Waste-to-energy systems were being incorporated. For government clients under pressure to meet climate commitments, NBCC offered a path to sustainable infrastructure without additional cost.

The technology roadmap was equally ambitious. Digital twins for all major projects by 2026. AI-powered project management by 2027. Blockchain for procurement by 2028. These weren't buzzword initiatives—they were fundamental transformations that would further widen NBCC's competitive moat. When you're managing thousands of projects simultaneously, even marginal efficiency improvements translate to massive value creation.

International expansion was taking a new direction. Instead of just executing projects abroad, NBCC was exploring the export of its redevelopment model. Conversations with Sri Lanka, Bangladesh, and Nepal centered on replicating Delhi's transformation in Colombo, Dhaka, and Kathmandu. The model that worked for Indian government colonies could work for government land anywhere in South Asia.

The affordable housing push aligned perfectly with government priorities. NBCC wasn't trying to compete with private developers in luxury segments. They were focused on the segment private developers avoided—affordable housing with thin margins but massive volumes. With government support and their low-cost structure, NBCC could make affordable housing profitable at scale.

The Supertech project takeover demonstrated another growth avenue. NCLAT appointed NBCC as Project Management Consultant for completing 16 stalled projects comprising 49,748 houses across Uttar Pradesh, Uttarakhand, Haryana, and Karnataka. With tentative construction cost of ₹9,445 crore and consultancy fee fixed at 8% (including 1% marketing fee), this opened up the stressed asset resolution space—a market worth tens of thousands of crores.

The railway station redevelopment opportunity was massive. India had 7,000+ railway stations, many sitting on prime urban land. NBCC's redevelopment model was perfect for this—modernize stations using commercial development of railway land. Early pilot projects were showing promise, and if scaled, this could be bigger than the GPRA colonies project.

Smart city projects offered another growth vector. With 100 smart cities planned and many struggling with implementation, NBCC's project management expertise was invaluable. From integrated command centers to smart utilities, from digital infrastructure to green transport—NBCC could handle the complexity that overwhelmed traditional contractors.

The healthcare infrastructure push post-COVID created unprecedented opportunity. India needed thousands of new hospitals, health centers, and medical colleges. HSCC's acquisition positioned NBCC perfectly for this boom. The company wasn't just building hospitals—they were creating integrated healthcare infrastructure including medical colleges, nursing schools, and research facilities.

Education infrastructure represented another underserved market. With new IITs, IIMs, and central universities being established, plus thousands of Kendriya Vidyalayas and Navodaya Vidyalayas needed, NBCC's expertise in institutional construction was in high demand. These projects offered steady work for decades.

Border infrastructure, always sensitive and specialized, was becoming a priority area. From roads in Ladakh to bridges in the Northeast, from border outposts to strategic installations—NBCC's security clearances and trust factor made them the natural choice. These projects carried national importance beyond their commercial value.

The organizational transformation to support this growth was already underway. New regional offices were being established. Talent from private sector was being hired for specialized roles. Training programs were preparing the next generation of project managers. The company that once moved at PSU pace was developing private sector agility.

Risk management for this expanded footprint was sophisticated. Geographic diversification reduced concentration risk. Sector diversification—from housing to healthcare to education—provided stability. The fee-based model limited execution risk. Government backing provided payment security. It was growth without proportional risk increase.

The capital allocation strategy was clear. Organic growth would be funded through internal accruals. Acquisitions would be selective and strategic. Dividends would be maintained to reward shareholders. The balance between growth, returns, and stability was carefully calibrated.

Looking at the vision unfolding, NBCC wasn't just planning growth—they were architecting transformation. From a construction company to an infrastructure platform. From a Delhi-focused PSU to a pan-India presence. From a government contractor to a development partner. The ambition was massive, but unlike many corporate visions, this one was backed by signed contracts, confirmed projects, and proven execution capability.

The future NBCC would be unrecognizable from its past—except for one thing. The core DNA of reliable execution, patient capital, and public purpose would remain. Everything else was being reimagined for a new India that needed infrastructure at unprecedented scale. And NBCC intended to build it.

IX. Playbook: The NBCC Method

If you had to distill NBCC's success into a formula that business schools could teach, where would you start? Not with the financial engineering or the government relationships, but with a fundamental insight that took decades to crystallize: in infrastructure, the real value isn't in laying bricks—it's in managing complexity. Everything else flows from this understanding.

The asset-light model that NBCC pioneered wasn't born from strategic brilliance—it emerged from constraint. As a PSU, NBCC couldn't easily raise capital for equipment and machinery. So they asked a different question: why own excavators when you can manage excavator operators? Why employ thousands of construction workers when you can supervise contractors who employ them? This wasn't just capital efficiency—it was risk transfer at scale.

Consider the mathematics. A typical EPC contractor might earn 15-20% margins but needs massive capital for equipment, faces execution risk, and deals with working capital cycles that can stretch years. NBCC earns 8-10% fees with minimal capital employed, no execution risk, and payment tied to milestones rather than completion. Lower margins, but the return on capital employed tells a different story—often exceeding 40% compared to sub-20% for traditional contractors.

The government relationship advantage goes deeper than most analysts understand. It's not about preferential treatment—private companies can also bid for government projects. The advantage is trust architecture. When a secretary in the Ministry of Defense needs a sensitive project executed, the calculation isn't just about cost. It's about political risk. Choose a private contractor and any delay or cost overrun becomes ammunition for opposition parties and media. Choose NBCC—another government entity—and it's just the system working with itself. This political risk mitigation is worth percentage points of margin.

The self-financing redevelopment model is perhaps the most elegant innovation. Here's the playbook: identify government land in prime urban locations. Current use is inefficient—typically old, low-rise buildings. Propose vertical development that houses the same number of government employees in 40% of the land. Use the remaining 60% for commercial development. Structure it so commercial revenues fund the entire project. The government gets new infrastructure without budget allocation. NBCC gets development rights and fees. The city gets better land utilization. It's value creation without capital.

But here's what competitors miss when they try to replicate this model: it requires patient capital that can wait 7-10 years for returns. Private developers, funded by expensive debt or impatient equity, can't afford this timeline. Their IRR requirements make such projects unviable. NBCC, with government backing and stable funding, can play the long game. Time becomes a competitive advantage.

The procurement and tendering expertise is another underappreciated moat. NBCC has mastered the art of government tendering—creating specifications that ensure quality while enabling competitive bidding, managing the delicate balance between L1 (lowest bidder) requirements and quality outcomes, navigating vigilance and audit requirements without getting paralyzed. They've turned bureaucracy from a burden into a barrier to entry.

Managing political and bureaucratic complexity requires a special skill set. Every project involves multiple stakeholders with different agendas. The minister wants visibility and quick results. The secretary wants compliance and no controversies. The joint secretary wants detailed documentation. The finance department wants cost control. The audit department wants process adherence. Local politicians want employment and contracts for their constituents. NBCC has become the master orchestrator, managing all these stakeholders while keeping projects on track.

The talent model is uniquely hybrid. The core team consists of career PSU employees who understand government culture, process, and requirements. But increasingly, NBCC is hiring from the private sector for specialized roles—bringing in modern project management techniques, technology expertise, and commercial acumen. This blend of government DNA and private sector efficiency is difficult to replicate.

Quality control in the NBCC method isn't just about construction standards—it's about reputation management. Every project carries the company's credibility. One failed project could shut doors across ministries. So quality isn't negotiable. Third-party audits are standard. Documentary evidence is obsessive. When NBCC certifies a building is ready, ministries know they can move in without worry. This reputation for quality becomes a compound advantage over time.

The risk management philosophy is conservative but not paralytic. NBCC takes calculated risks—entering new geographies, trying new models, acquiring struggling companies. But they hedge extensively. Fixed-price contracts with clients but variable-price contracts with vendors. Penalty clauses for delays but also incentives for early completion. Government payment risk mitigated by working with multiple ministries. It's risk-taking with safety nets at every level.

The scalability secret lies in standardization with customization. NBCC has standard operating procedures for everything—from soil testing to project handover. But each project gets customized solutions within this framework. It's mass customization applied to construction. This allows them to handle hundreds of projects simultaneously without losing control.

The technology adoption strategy is pragmatic rather than cutting-edge. NBCC doesn't chase the latest construction tech fads. They adopt proven technologies that enhance efficiency—BIM for design, ERP for project management, drones for monitoring. The focus is on technology that works in Indian conditions with Indian contractors, not what wins innovation awards.

Why can't private developers replicate this model? Beyond patient capital and government trust, there's a deeper reason: mission alignment. Private developers optimize for maximum extraction of value. NBCC optimizes for sustainable value creation that serves public purpose. This philosophical difference shapes every decision—from project selection to pricing to execution. It's not better or worse—just fundamentally different.

The competitive moat is multilayered and reinforcing. Government trust leads to more projects. More projects build expertise. Expertise enhances reputation. Reputation attracts talent. Talent improves execution. Better execution strengthens government trust. It's a virtuous cycle that took decades to build and would take decades to replicate.

Looking at the NBCC method, you realize it's not one breakthrough innovation but hundreds of small optimizations compounded over time. It's the Toyota Production System applied to construction—continuous improvement, waste elimination, and respect for people. Unsexy but incredibly effective.

The lesson for entrepreneurs and investors is counterintuitive: sometimes the best business model isn't the highest margin or fastest growing. Sometimes it's the one that solves a real problem sustainably, builds trust consistently, and compounds advantages patiently. NBCC didn't disrupt construction—they perfected it within their niche.

For other PSUs, the NBCC method offers a template: leverage your inherent advantages rather than lamenting your constraints. Use patient capital as a weapon. Turn government relationships into a moat. Make public purpose profitable. It's possible to be commercial without being extractive.

The NBCC method ultimately isn't about construction or even infrastructure. It's about finding inefficiencies in large systems and creating value by solving them. In NBCC's case, the inefficiency was government infrastructure development—slow, expensive, and politically fraught. They created a solution that was faster, self-financing, and politically neutral. That's not just a business model—it's almost alchemy.

X. Analysis & Investment Case

The research analyst at a Mumbai fund house pulled up NBCC's chart, overlaid it with Nifty Infrastructure, and paused. The outperformance was stark, but was it sustainable? This wasn't a momentum trade or a turnaround story anymore. At current valuations, NBCC was pricing in excellence. The question for investors was whether excellence was enough.

Let's start with the bear case, because in investing, understanding what can go wrong is more important than dreaming about what can go right.

The Bear Thesis:

Execution delays remain NBCC's Achilles' heel. Not from incompetence, but from the nature of their projects. When you're redeveloping colonies with thousands of residents, delays are almost inevitable. Environmental clearances get stuck in the National Green Tribunal. Public Interest Litigations emerge from nowhere. Archaeological discoveries halt construction. Each delay doesn't just push timelines—it affects the entire financial model of self-sustaining projects where commercial development funds residential construction.

The government dependency is both shield and sword. With 61.8% government ownership, NBCC is insulated from hostile takeovers but vulnerable to policy shifts. A new government could change infrastructure priorities. A fiscal crisis could freeze government spending. A policy decision to open up government projects to wider competition could erode NBCC's privileged position. The company that lives by government relations can die by them too.

Valuations have run ahead of fundamentals. At 54.45 times earnings and 12.21 times book value, NBCC is priced for perfection. Any disappointment—a project delay, a cost overrun, a canceled contract—could trigger a sharp correction. The stock has priced in not just current performance but future potential. That's a dangerous place for a PSU operating in the cyclical construction sector.

The redevelopment model, while brilliant, has limits. There are only so many government colonies in prime urban land. Once Delhi's redevelopment is complete, replication in other cities may not be as lucrative. Mumbai's government land is more fragmented. Bangalore's is tied up in litigation. Chennai's doesn't have Delhi's commercial appetite. The model that transformed NBCC might not be infinitely scalable.

Competition is emerging from unexpected quarters. State construction agencies are upgrading capabilities. Private developers are forming consortiums to bid for large government projects. International firms are eyeing India's infrastructure opportunity. NBCC's moat, while formidable, isn't impregnable. The 8-10% fees that seem reasonable today might face pressure tomorrow.

The Bull Thesis:

But for every bear argument, bulls have a compelling counter.

The monopolistic position in government construction is structural, not temporary. It's not just about relationships—it's about trust architecture built over decades. When ministries like Defense, Home Affairs, and Finance repeatedly choose NBCC, they're buying peace of mind that no private player can offer. This isn't a preference—it's institutional risk management.

The massive order book approaching ₹1 lakh crore provides multi-year revenue visibility that few companies enjoy. This isn't speculative pipeline—these are signed contracts with government entities that will be executed regardless of economic cycles. In a world of uncertainty, NBCC offers predictability.

Urbanization tailwinds are just beginning. India needs to build the equivalent of a Chicago every year for the next decade to house its urban population. The infrastructure deficit is measured in trillions of dollars. NBCC isn't just riding this wave—they're one of the few entities capable of executing at the scale required. The opportunity is generational.

The debt-free balance sheet in a capital-intensive sector is a massive advantage. While competitors struggle with leverage, NBCC can be opportunistic. They can take on large projects without financial stress. They can acquire distressed assets. They can invest in technology. Financial flexibility in construction is like water in a desert—invaluable.

The hidden value in subsidiaries and land banks isn't reflected in current valuations. HSCC alone could be worth several thousand crores if listed separately. The development rights from ongoing redevelopment projects represent massive unrealized value. The standard accounting doesn't capture the economic value of multi-year development rights on prime urban land.

The Comparison Framework:

Against L&T, NBCC looks expensive on traditional metrics but cheap on risk-adjusted returns. L&T takes execution risk, uses massive capital, and faces working capital challenges. NBCC's fee-based model with minimal capital employed generates superior return on equity with lower risk. It's like comparing a manufacturing company with a software firm—different models requiring different valuation frameworks.

Versus private developers like DLF or Oberoi, NBCC operates in a different universe. Private developers chase luxury margins but face demand volatility. NBCC accepts lower margins but enjoys guaranteed demand from government. In risk-adjusted terms, NBCC's steady 8-10% fees might be worth more than volatile 30% development margins.

Compared to other PSUs, NBCC is in a league of its own. While NTPC or ONGC are capital-intensive with regulatory challenges, NBCC is asset-light with operational flexibility. While other PSUs struggle with relevance, NBCC is central to India's infrastructure story. It's the rare PSU that combines government backing with entrepreneurial execution.

ESG Considerations:

The environmental, social, and governance story is surprisingly strong. Every NBCC project now incorporates green building norms, renewable energy, and waste management. The social impact of providing modern housing to millions of government employees is immeasurable. Governance, despite being a PSU, is transparent with regular disclosures and professional management.

The nation-building narrative resonates beyond financial returns. NBCC isn't just constructing buildings—they're building the infrastructure for India's emergence as a developed nation. For ESG-focused funds, this is a way to participate in India's development story while maintaining environmental and social standards.

The Investment Decision Framework:

For long-term fundamental investors, NBCC presents a unique proposition: exposure to India's infrastructure story without execution risk. The question isn't whether India needs massive infrastructure development—it does. The question is who can execute at scale, and NBCC has proven they can.

For value investors, the hidden assets and subsidiary value provide margin of safety. Even if the redevelopment model slows, the core PMC business and subsidiaries justify significant value. The downside seems limited given the asset base and order book.

For growth investors, the runway is long. From smart cities to affordable housing, from healthcare infrastructure to education facilities—the opportunities are massive and multi-decade. The current business is just the platform for much larger opportunity ahead.

For risk-averse investors, the government backing, debt-free balance sheet, and fee-based model provide comfort. This isn't a high-risk construction bet—it's a play on India's infrastructure spending with government guarantee.

The Verdict:

NBCC is neither obviously cheap nor obviously expensive. It's fairly valued for what it is today but potentially undervalued for what it could become. The bear case is real—execution risks, government dependency, and valuation concerns are valid. But the bull case is compelling—monopolistic positioning, massive opportunity, and proven execution create a powerful combination.

The investment decision ultimately comes down to time horizon and conviction. For traders, the stock might be ahead of itself. For long-term investors who believe in India's infrastructure story and NBCC's ability to execute it, current valuations might prove reasonable in hindsight.

What's clear is that NBCC has transcended its PSU origins to become something unique—a government company that operates with private efficiency, a construction company that doesn't construct, an infrastructure play without infrastructure risk. It's a paradox that has delivered exceptional returns and might continue to do so.

The smart money isn't asking whether NBCC is a good company—it clearly is. They're asking whether it's a good stock at current prices. That's a harder question, but for investors with patience and conviction in India's infrastructure story, NBCC offers something rare: a way to bet on India's development without betting on execution risk. In a world of uncertainty, that might be worth the premium.

XI. Epilogue & Reflections

Standing at the construction site of what will become South Delhi's newest commercial hub, you can't help but marvel at the transformation. Where decrepit government quarters once stood—buildings that had housed independence-era bureaucrats—gleaming towers now rise. The old residents haven't been displaced; they've been relocated to modern apartments with better amenities. The construction is being funded not by taxpayers but by the commercial development next door. It's urban renewal that seems almost too good to be true, yet here it is, concrete and steel testament to an idea that worked.

NBCC's story is ultimately about institutional evolution—how a sleepy government department transformed into India's infrastructure champion. But it's also about something larger: proving that public sector enterprises, often written off as relics of socialist planning, can innovate, compete, and create value at scale.

The lessons for other countries are profound. Across the developing world, governments struggle with the same challenge: massive infrastructure needs but limited fiscal resources. The NBCC model offers a template—use government land as equity, create self-financing structures, and leverage public sector credibility for execution. It's not privatization, which often faces political resistance. It's not pure government spending, which strains budgets. It's a third way that aligns public purpose with commercial viability.

For entrepreneurs, NBCC demonstrates that innovation doesn't always mean disruption. Sometimes the biggest opportunities lie in perfecting existing systems rather than destroying them. NBCC didn't disrupt construction—they optimized it for a specific niche and scaled relentlessly. They found inefficiencies in government infrastructure development and built a business around solving them.

The investor lessons are equally valuable. NBCC shows that sustainable competitive advantages can come from unexpected sources. Not technology or intellectual property, but trust and relationships. Not disruption or first-mover advantage, but patient execution and compound improvements. In a world obsessed with unicorns and exponential growth, NBCC achieved extraordinary returns through steady execution of an unglamorous business model.

For India's PSU ecosystem, NBCC has rewritten the playbook. They've shown that government ownership doesn't have to mean inefficiency. That public purpose and profitability can coexist. That PSUs can be acquirers, innovators, and value creators. In a country where PSUs employ millions and control vast resources, NBCC's transformation offers hope that others can follow.

The future implications are intriguing. As India pushes toward becoming a $10 trillion economy, infrastructure will be the binding constraint. NBCC has positioned itself at the center of this transformation. But more importantly, they've created a model that can be replicated—by other PSUs, in other sectors, in other countries. The idea that government assets can be leveraged for development without privatization is powerful and politically palatable.

Critics might argue that NBCC's success is unique—dependent on specific circumstances like Delhi's land values and government relationships that can't be replicated. There's truth to this. But every successful business model is somewhat circumstantial. The genius lies in recognizing and exploiting those circumstances. NBCC didn't create Delhi's land scarcity or India's infrastructure needs—they just figured out how to solve them profitably.

The governance implications deserve consideration. NBCC operates in a space where the lines between public and private blur. They're a government company operating with commercial principles, serving public purpose while generating private returns. This hybrid model challenges traditional categorizations and might represent the future of public enterprise—not pure government control or complete privatization, but something in between.

Looking back, NBCC's journey from a government construction department to a ₹28,000 crore enterprise is remarkable not for its speed but for its steadiness. This wasn't a rocket ship trajectory but a compound curve—slow at first, then accelerating as advantages accumulated. It's a reminder that in business, as in life, patient execution often beats brilliant strategy.

The human element shouldn't be forgotten. Behind NBCC's transformation are thousands of engineers, project managers, and workers who evolved from government employees to commercial operators. They learned to think like entrepreneurs while serving like public servants. This cultural transformation, perhaps more than any strategic initiative, explains NBCC's success.

As India enters what many consider its infrastructure decade, NBCC stands as both beneficiary and enabler. They'll build the airports, hospitals, universities, and homes that India needs. But more importantly, they've proven that this can be done efficiently, sustainably, and profitably. In a country where government execution is often criticized, NBCC offers a counter-narrative.

The global implications are worth considering. As developed countries face infrastructure decay and developing countries face infrastructure deficits, the NBCC model offers lessons. Public-private partnerships don't have to be complex financial structures that often fail. They can be simple models where government provides land and credibility while commercial development provides funding. It's a model that could work from Detroit to Dhaka.

For students of business history, NBCC represents a unique case study—a company that succeeded not despite government ownership but because of it. They turned every supposed disadvantage into an advantage. Slow decision-making became patient capital. Bureaucratic processes became trust architecture. Government relationships became competitive moats. It's strategic jujitsu at its finest.

The philosophical implications run deeper. NBCC challenges the binary thinking that dominates economic discourse—that enterprises must be either public or private, either commercial or social, either efficient or equitable. They've shown that with the right model and execution, these aren't trade-offs but synergies. It's a nuanced view that deserves more attention in our polarized times.

As we close this exploration of NBCC's journey, perhaps the most important reflection is this: transformation is possible at any age, in any sector, under any ownership. NBCC was 52 years old when it went public, operating in construction—one of the world's oldest industries—as a government company in a democracy known for bureaucracy. If they could transform, anyone can.

The NBCC story isn't finished. As India builds its infrastructure for the next century, NBCC will be central to that story. They'll face new challenges—technology disruption, climate change, political shifts. But if history is any guide, they'll adapt, evolve, and continue building. Not just buildings, but a model for how public enterprises can serve public purpose while creating private value.

In the end, NBCC's greatest achievement might not be the buildings they've constructed or the returns they've generated. It might be proving that in the right circumstances, with the right model, patient execution beats brilliant strategy, trust beats technology, and purpose-driven capitalism isn't an oxymoron. In a world searching for sustainable business models that serve all stakeholders, NBCC offers not just hope but proof that it's possible.

The cranes at the construction site continue their ballet, lifting steel and concrete into Delhi's sky. Each beam placed is part of a larger story—of a company that refused to accept limitations, of a model that challenged conventions, and of a transformation that continues to unfold. NBCC isn't just building India's infrastructure future—they're showing the world a different way to build it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube